Embed Size (px)

Citation preview

Strategic Management JournalStrat. Mgmt. J., 26: 887–911 (2005)

Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/smj.492

SCHUMPETER’S GHOST: IS HYPERCOMPETITIONMAKING THE BEST OF TIMES SHORTER?

ROBERT R. WIGGINS1* and TIMOTHY W. RUEFLI2

1 Fogelman College of Business and Economics, University of Memphis, Memphis,Tennessee, U.S.A.2 McCombs School of Business and IC2 Institute, University of Texas at Austin, Austin,Texas, U.S.A.

At the center of Schumpeter’s theory of competitive behavior is the assertion that competitiveadvantage will become increasingly more difficult to sustain in a wide range of industries. Morerecently, this assertion has resurfaced in the notion of hypercompetition. This research examinestwo large longitudinal samples of firms to discover which industries, if any, exhibit performancethat is consonant with Schumpeterian theory and the assertions of hypercompetition. We findsupport for the argument that over time competitive advantage has become significantly harderto sustain and, further, that the phenomenon is limited neither to high-technology industriesnor to manufacturing industries but is seen across a broad range of industries. We also findevidence that sustained competitive advantage is increasingly a matter not of a single advantagemaintained over time but more a matter of concatenating over time a sequence of advantages.Copyright 2005 John Wiley & Sons, Ltd.

INTRODUCTION

While Schumpeter’s (1942: 84) notion of a ‘gale ofcreative destruction’ has garnered the most atten-tion in the research and practitioner literatures, itis the role profit plays in motivating innovation asa precursor to creative destruction that is the keyto his theories. Schumpeter (1939: 105) said thatprofit is ‘the premium put upon successful inno-vation in capitalist society and is temporary bynature: it will vanish in the subsequent processof competition and adaptation.’ Drucker (1983)observed:

Schumpeter’s Economic Development does whatneither the classical economists nor Marx norKeynes was able to do: It makes profit fulfill an

Keywords: Schumpeter; hypercompetition; performance;persistence; sustainability*Correspondence to: Robert R. Wiggins, Fogelman College ofBusiness and Economics, University of Memphis, Memphis, TN38152, U.S.A. E-mail: [email protected]

economic function. In the economy of change andinnovation, profit, in contrast to Marx and his the-ory, is not a Mehrwert, a ‘surplus value’ stolenfrom the workers. On the contrary, it is the onlysource of jobs for workers and of labor income. Thetheory of economic development shows that no oneexcept the innovator makes a genuine ‘profit’; andthe innovator’s profit is always quite short-lived.But innovation in Schumpeter’s famous phrase isalso ‘creative destruction.’ It makes obsolete yes-terday’s capital equipment and capital investment.The more an economy progresses, the more cap-ital formation will it therefore need. Thus whatthe classical economists—or the accountant or thestock exchange—considers ‘profit’ is a genuinecost, the cost of staying in business, the cost ofa future in which nothing is predictable except thattoday’s profitable business will become tomorrow’swhite elephant.

Schumpeter’s gale of creative destruction wouldcreate a disequilibrium in which ‘practically everyenterprise [is] threatened and put on the defensiveas soon as it comes into existence (Schumpeter,1939: 107).’ For decades Schumpeter’s theory was

Copyright 2005 John Wiley & Sons, Ltd. Received 16 May 2003Final revision received 12 May 2005

888 R. R. Wiggins and T. W. Ruefli

occasionally mentioned but did not figure promi-nently in many analyses of business behavior.

Over the past decade, however, there has beenincreasing attention given to Schumpeterian the-ory and to hypercompetition in the academic lit-erature. Primary, of course, is D’Aveni’s seminalbook (1994), where he defines hypercompetitionas ‘an environment characterized by intense andrapid competitive moves, in which competitorsmust move quickly to build advantage and erodethe advantage of their rivals’ (D’Aveni, 1994:217–218), as well as Christensen’s (1997) book onthe problems of industry-leading companies facingcompetition from upstarts. Beyond that there havebeen two special issues of Organization Science(July and August 1996) devoted to hypercompeti-tion, an edited book (Ilinitch, Lewin, and D’Aveni,1998) that overlaps with the special issues, andsome articles in academic journals. Few of theseresearch studies have been empirically based, butthose that were will be reviewed below. In par-ticular, the current research and its findings willbe compared to McNamara, Vaaler, and Devers(2003) since it is the most comprehensive and com-parable study to date.

The purpose of our study is to add substan-tially to the base of empirical evidence concerningSchumpeter’s theory in terms of the nature andmagnitude of the claimed shift in the US economy.Given Schumpeter’s emphasis on the role of prof-its, the underlying subject of our study will be arecognized hallmark of traditional firm and indus-try behavior: sustained competitive advantage. Thereason for this is as D’Aveni (1994: 7) has noted:‘The pursuit of sustainable advantage has longbeen the focus of strategy.’ The key predictionsof Schumpeterian theory for strategy researchersare: (1) that firms are increasingly less able to sus-tain a strategic advantage over their competition;(2) that such behavior is characteristic of a widerange of industries; and (3) that sustained compet-itive advantage has become less a matter of findingand sustaining a single competitive advantage andmore a case of finding a series of competitiveadvantages over time and concatenating them intoa sustained competitive advantage. Thus all of thethree key Schumpeterian outcomes cited relate tosustained competitive advantage.

Our approach will be to develop a theoreticalframework and hypotheses that relate Schumpete-rian theory to sustained competitive advantage. Wethen examine not only 6,772 firms in 40 industries

over a 25-year period but also all 13,899 businessunits in 8,806 firms over a 17-year period (a super-set of the sample employed by the most recent andcomparable study of hypercompetition; McNamaraet al., 2003) and identify in a rigorous way thosefirms and business units that have been able tomaintain, for a sustained period of time, a com-petitive advantage in a fashion that yielded supe-rior economic performance. We will examine theseperiods of superior performance to determine if, inconsonance with hypercompetition, those periodshave become significantly shorter over time—and,if so, for which groups of industries. Then we willexamine these same firms for evidence that sus-tained competitive advantage is increasingly notsingular, but is instead composed more and moreoften of multiple short advantages over time.

THEORETICAL FRAMEWORKAND ANTECEDENT LITERATURE

Historically, traditional theories of strategic man-agement eschewed the Schumpeterian theory ofdisequilibrium as a base framework and choseinstead the equilibrium-oriented approach of indus-trial organization. In so doing they placed empha-sis on what Schumpeter (1947: 153) called the‘adaptive response’ of managers and on creat-ing a sustained competitive advantage for a firm.Thus for decades sustained competitive advan-tage has been a dominant concept in strategicmanagement research. Emerging from the struc-ture–conduct–performance paradigm of industrialorganization economics (Bain, 1959; Mason, 1939,1949) and popularized by the Harvard BusinessSchool and the work of Michael Porter (1985), sus-tained competitive advantage is the most influentialmechanism for explaining the persistence of supe-rior economic performance.1 The increasingly pop-ular resource-based view of the firm extends theinfluence of sustained competitive advantage andits result, above-normal returns, by making achiev-ing sustained competitive advantage the very rea-son for firms’ existence (Conner, 1991: 132).

1 Coff (1999) {, 1999 #718} points out that there may be casesin which firms have a competitive advantage in the marketfor outputs, but not for inputs—and thus may not realizesuperior economic performance. We shall explicitly assume thatcompetitive advantage obtains overall for a firm.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 889

A firm’s ability to maintain superior economicperformance has a long and varied history in eco-nomic and strategic management research. Neo-classical economics argues that persistent superioreconomic performance is an anomaly, a tempo-rary condition that will vanish when equilibriumis reached (Debreu, 1959). Industrial organizationeconomics argues that any persistence is the resultof industry structure, with mechanisms such asentry barriers preventing the equilibrium of neo-classical economics from being achieved (Bain,1959). Evolutionary economics (Nelson and Win-ter, 1982) as well as the related Austrian schoolof economics (Jacobson, 1992; Schumpeter, 1939)both argued that persistent superior economic per-formance is the result of cycles of entrepreneurialinnovation and imitation that create a continuingdisequilibrium where some firms can achieve per-sistence of performance although it will be even-tually eroded. Organizational and strategic man-agement theories have incorporated most of theseideas and added the concept of sustained competi-tive advantage (Porter, 1985) that can lead directlyto persistent superior economic performance.

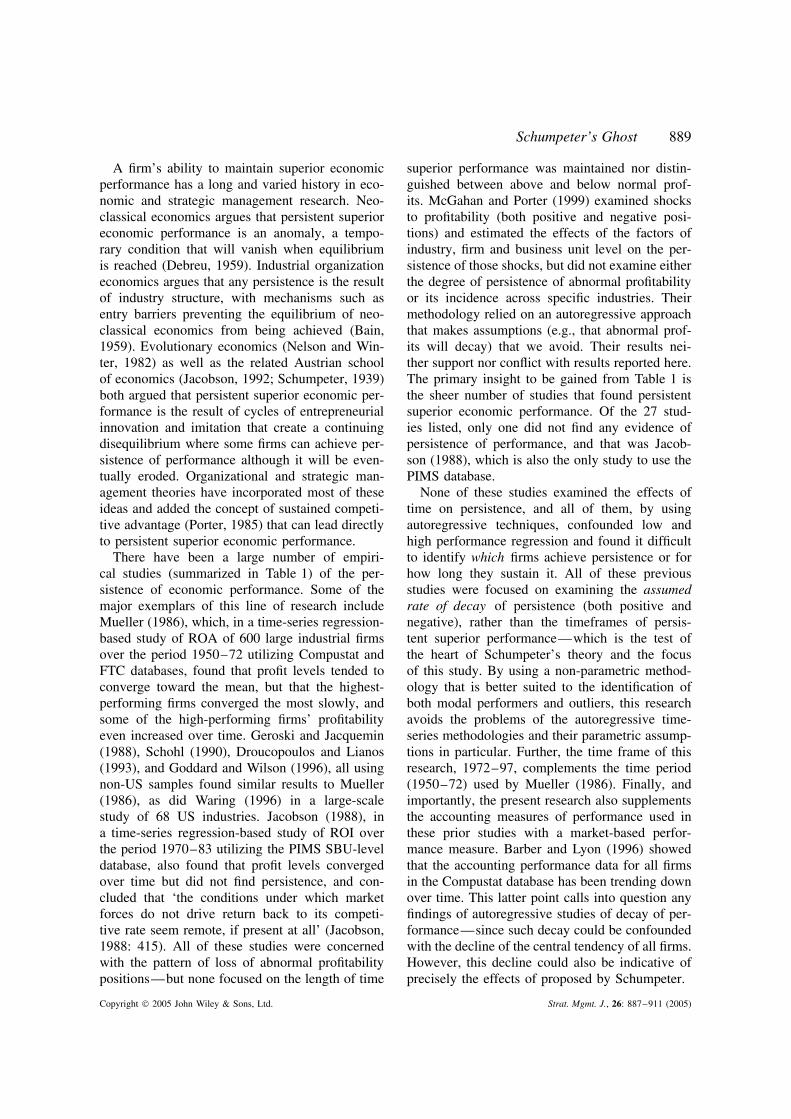

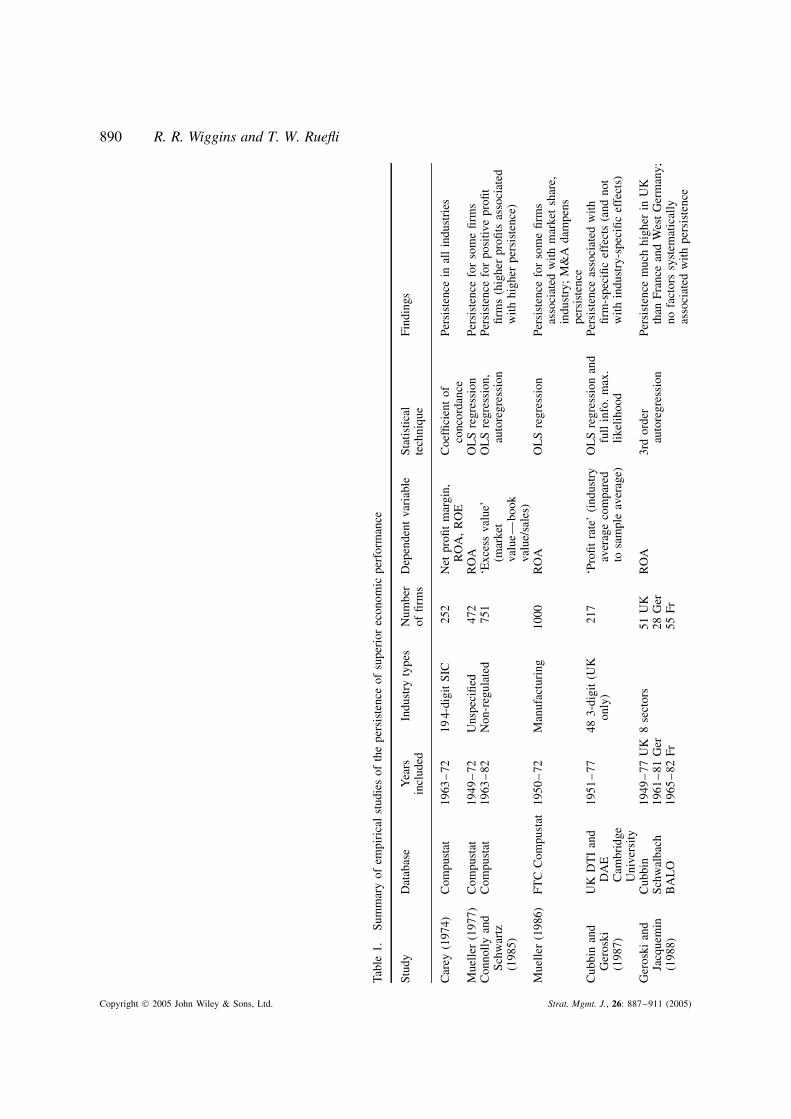

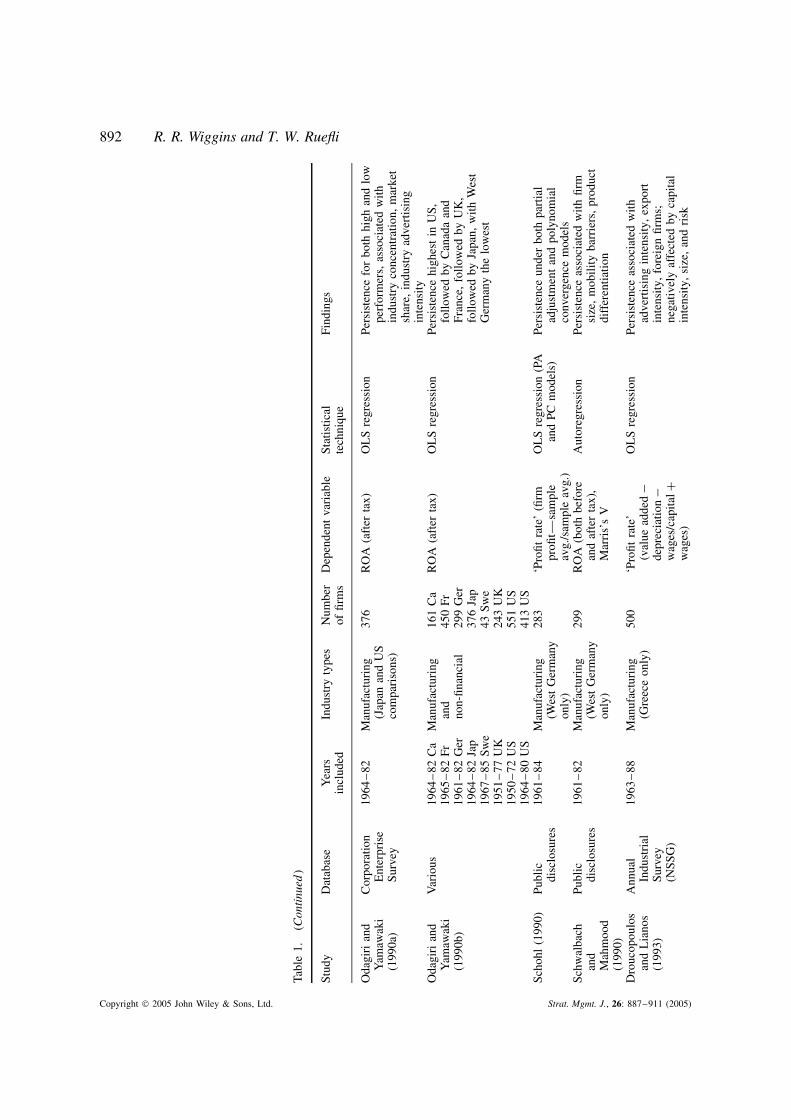

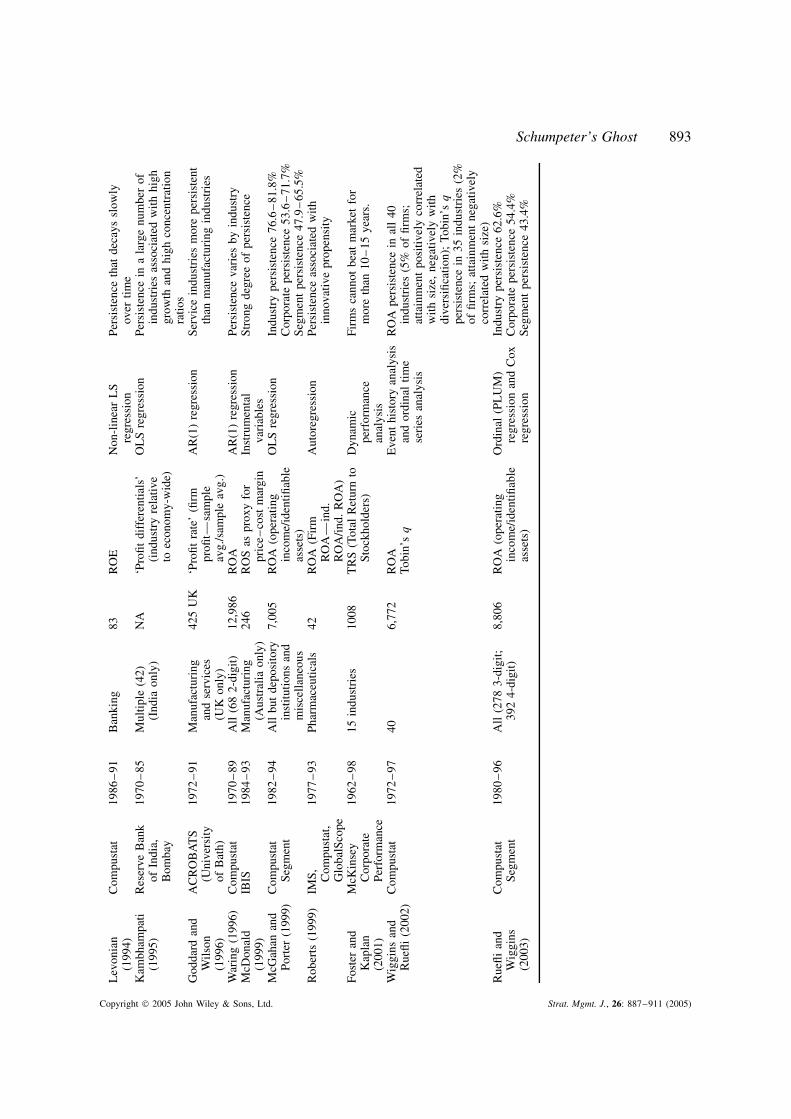

There have been a large number of empiri-cal studies (summarized in Table 1) of the per-sistence of economic performance. Some of themajor exemplars of this line of research includeMueller (1986), which, in a time-series regression-based study of ROA of 600 large industrial firmsover the period 1950–72 utilizing Compustat andFTC databases, found that profit levels tended toconverge toward the mean, but that the highest-performing firms converged the most slowly, andsome of the high-performing firms’ profitabilityeven increased over time. Geroski and Jacquemin(1988), Schohl (1990), Droucopoulos and Lianos(1993), and Goddard and Wilson (1996), all usingnon-US samples found similar results to Mueller(1986), as did Waring (1996) in a large-scalestudy of 68 US industries. Jacobson (1988), ina time-series regression-based study of ROI overthe period 1970–83 utilizing the PIMS SBU-leveldatabase, also found that profit levels convergedover time but did not find persistence, and con-cluded that ‘the conditions under which marketforces do not drive return back to its competi-tive rate seem remote, if present at all’ (Jacobson,1988: 415). All of these studies were concernedwith the pattern of loss of abnormal profitabilitypositions—but none focused on the length of time

superior performance was maintained nor distin-guished between above and below normal prof-its. McGahan and Porter (1999) examined shocksto profitability (both positive and negative posi-tions) and estimated the effects of the factors ofindustry, firm and business unit level on the per-sistence of those shocks, but did not examine eitherthe degree of persistence of abnormal profitabilityor its incidence across specific industries. Theirmethodology relied on an autoregressive approachthat makes assumptions (e.g., that abnormal prof-its will decay) that we avoid. Their results nei-ther support nor conflict with results reported here.The primary insight to be gained from Table 1 isthe sheer number of studies that found persistentsuperior economic performance. Of the 27 stud-ies listed, only one did not find any evidence ofpersistence of performance, and that was Jacob-son (1988), which is also the only study to use thePIMS database.

None of these studies examined the effects oftime on persistence, and all of them, by usingautoregressive techniques, confounded low andhigh performance regression and found it difficultto identify which firms achieve persistence or forhow long they sustain it. All of these previousstudies were focused on examining the assumedrate of decay of persistence (both positive andnegative), rather than the timeframes of persis-tent superior performance—which is the test ofthe heart of Schumpeter’s theory and the focusof this study. By using a non-parametric method-ology that is better suited to the identification ofboth modal performers and outliers, this researchavoids the problems of the autoregressive time-series methodologies and their parametric assump-tions in particular. Further, the time frame of thisresearch, 1972–97, complements the time period(1950–72) used by Mueller (1986). Finally, andimportantly, the present research also supplementsthe accounting measures of performance used inthese prior studies with a market-based perfor-mance measure. Barber and Lyon (1996) showedthat the accounting performance data for all firmsin the Compustat database has been trending downover time. This latter point calls into question anyfindings of autoregressive studies of decay of per-formance—since such decay could be confoundedwith the decline of the central tendency of all firms.However, this decline could also be indicative ofprecisely the effects of proposed by Schumpeter.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

890 R. R. Wiggins and T. W. Ruefli

Tabl

e1.

Sum

mar

yof

empi

rica

lst

udie

sof

the

pers

iste

nce

ofsu

peri

orec

onom

icpe

rfor

man

ce

Stud

yD

atab

ase

Yea

rsin

clud

edIn

dust

ryty

pes

Num

ber

offir

ms

Dep

ende

ntva

riab

leSt

atis

tical

tech

niqu

eFi

ndin

gs

Car

ey(1

974)

Com

pust

at19

63–

7219

4-di

git

SIC

252

Net

profi

tm

argi

n,R

OA

,R

OE

Coe

ffici

ent

ofco

ncor

danc

ePe

rsis

tenc

ein

all

indu

stri

es

Mue

ller

(197

7)C

ompu

stat

1949

–72

Uns

peci

fied

472

RO

AO

LS

regr

essi

onPe

rsis

tenc

efo

rso

me

firm

sC

onno

llyan

dSc

hwar

tz(1

985)

Com

pust

at19

63–

82N

on-r

egul

ated

751

‘Exc

ess

valu

e’(m

arke

tva

lue—

book

valu

e/sa

les)

OL

Sre

gres

sion

,au

tore

gres

sion

Pers

iste

nce

for

posi

tive

profi

tfir

ms

(hig

her

profi

tsas

soci

ated

with

high

erpe

rsis

tenc

e)

Mue

ller

(198

6)FT

CC

ompu

stat

1950

–72

Man

ufac

turi

ng10

00R

OA

OL

Sre

gres

sion

Pers

iste

nce

for

som

efir

ms

asso

ciat

edw

ithm

arke

tsh

are,

indu

stry

;M

&A

dam

pens

pers

iste

nce

Cub

bin

and

Ger

oski

(198

7)

UK

DT

Ian

dD

AE

Cam

brid

geU

nive

rsit

y

1951

–77

483-

digi

t(U

Kon

ly)

217

‘Pro

fitra

te’

(ind

ustr

yav

erag

eco

mpa

red

tosa

mpl

eav

erag

e)

OL

Sre

gres

sion

and

full

info

.m

ax.

like

liho

od

Pers

iste

nce

asso

ciat

edw

ithfir

m-s

peci

ficef

fect

s(a

ndno

tw

ithin

dust

ry-s

peci

ficef

fect

s)

Ger

oski

and

Jacq

uem

in(1

988)

Cub

bin

Schw

alba

chB

AL

O

1949

–77

UK

1961

–81

Ger

1965

–82

Fr

8se

ctor

s51

UK

28G

er55

Fr

RO

A3r

dor

der

auto

regr

essi

onPe

rsis

tenc

em

uch

high

erin

UK

than

Fran

cean

dW

est

Ger

man

y;no

fact

ors

syst

emat

ical

lyas

soci

ated

with

pers

iste

nce

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 891Ja

cobs

on(1

988)

PIM

SC

RSP

and

Com

pust

at

1970

–83

1963

–82

Uns

peci

fied

2000

sbu

241

RO

IA

R(1

)re

gres

sion

Litt

lepe

rsis

tenc

eN

oef

fect

ofin

dust

ryco

ncen

trat

ion

Som

eef

fect

ofm

arke

tsh

are

Con

tini

(198

9)IS

TAT

Ann

ual

Surv

eyof

Mfr

s

1973

,19

77,

and

1981

Man

ufac

turi

ng(I

taly

only

)N

AG

ross

profi

tra

tioC

ontin

genc

yta

bles

Pers

iste

nce

inal

lin

dust

ries

Cub

bin

and

Ger

oski

(199

0)

UK

DT

Ian

dD

AE

Cam

brid

geU

nive

rsit

y

1948

–77

483-

digi

t(U

Kon

ly)

243

‘Pro

fitra

te’

(ind

ustr

yav

erag

eco

mpa

red

tosa

mpl

eav

erag

e)

1st

orde

rau

tore

gres

sion

Pers

iste

nce

asso

ciat

edw

ithfir

m-s

peci

ficef

fect

s(a

ndno

tw

ithin

dust

ry-s

peci

ficef

fect

s)

Jenn

yan

dW

eber

(199

0)

Publ

icdi

sclo

sure

s19

65–

82M

anuf

actu

ring

(Fra

nce

only

)45

0R

OA

(bef

ore

tax)

OL

Sre

gres

sion

Pers

iste

nce

for

both

high

perf

orm

ers

and

low

perf

orm

ers

Kes

side

s(1

990)

Com

pust

at19

67–

8234

44-

digi

tN

AR

OS

GL

Sre

gres

sion

Indu

stry

pers

iste

nce

asso

ciat

edw

ithsm

all

num

bers

offir

ms,

conc

entr

atio

n,gr

owth

,sc

ale,

high

capi

tal

requ

irem

ents

Khe

man

ian

dSh

apir

o(1

990)

Com

pust

at19

64–

8219

68–

82M

anuf

actu

ring

and

min

ing

(Can

ada

only

)

129

161

RO

A(b

oth

befo

rean

daf

ter

tax)

OL

Sre

gres

sion

Pers

iste

nce

(gre

ater

than

inU

S)as

soci

ated

with

prod

uct

diff

eren

tiatio

nM

uelle

r(1

990)

FTC

Com

pust

at19

50–

72M

anuf

actu

ring

(63

3-di

git

and

4-di

git)

551

RO

AO

LS

regr

essi

onPe

rsis

tenc

eas

soci

ated

with

mar

ket

shar

e,pr

oduc

tdi

ffer

entia

tion,

grow

th;

nega

tivel

yas

soci

ated

with

conc

entr

atio

n,M

&A

(con

tinu

edov

erle

af)

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

892 R. R. Wiggins and T. W. Ruefli

Tabl

e1.

(Con

tinu

ed)

Stud

yD

atab

ase

Yea

rsin

clud

edIn

dust

ryty

pes

Num

ber

offir

ms

Dep

ende

ntva

riab

leSt

atis

tical

tech

niqu

eFi

ndin

gs

Oda

giri

and

Yam

awak

i(1

990a

)

Cor

pora

tion

Ent

erpr

ise

Surv

ey

1964

–82

Man

ufac

turi

ng(J

apan

and

US

com

pari

sons

)

376

RO

A(a

fter

tax)

OL

Sre

gres

sion

Pers

iste

nce

for

both

high

and

low

perf

orm

ers,

asso

ciat

edw

ithin

dust

ryco

ncen

trat

ion,

mar

ket

shar

e,in

dust

ryad

vert

isin

gin

tens

ity

Oda

giri

and

Yam

awak

i(1

990b

)

Var

ious

1964

–82

Ca

1965

–82

Fr19

61–

82G

er19

64–

82Ja

p19

67–

85Sw

e19

51–

77U

K19

50–

72U

S

Man

ufac

turi

ngan

dno

n-fin

anci

al

161

Ca

450

Fr29

9G

er37

6Ja

p43

Swe

243

UK

551

US

RO

A(a

fter

tax)

OL

Sre

gres

sion

Pers

iste

nce

high

est

inU

S,fo

llow

edby

Can

ada

and

Fran

ce,

follo

wed

byU

K,

follo

wed

byJa

pan,

with

Wes

tG

erm

any

the

low

est

1964

–80

US

413

US

Scho

hl(1

990)

Publ

icdi

sclo

sure

s19

61–

84M

anuf

actu

ring

(Wes

tG

erm

any

only

)

283

‘Pro

fitra

te’

(firm

profi

t—sa

mpl

eav

g./s

ampl

eav

g.)

OL

Sre

gres

sion

(PA

and

PCm

odel

s)Pe

rsis

tenc

eun

der

both

part

ial

adju

stm

ent

and

poly

nom

ial

conv

erge

nce

mod

els

Schw

alba

chan

dM

ahm

ood

(199

0)

Publ

icdi

sclo

sure

s19

61–

82M

anuf

actu

ring

(Wes

tG

erm

any

only

)

299

RO

A(b

oth

befo

rean

daf

ter

tax)

,M

arri

s’s

V

Aut

oreg

ress

ion

Pers

iste

nce

asso

ciat

edw

ithfir

msi

ze,

mob

ility

barr

iers

,pr

oduc

tdi

ffer

entia

tion

Dro

ucop

oulo

san

dL

iano

s(1

993)

Ann

ual

Indu

stri

alSu

rvey

(NSS

G)

1963

–88

Man

ufac

turi

ng(G

reec

eon

ly)

500

‘Pro

fitra

te’

(val

uead

ded

−de

prec

iatio

n−

wag

es/c

apita

l+w

ages

)

OL

Sre

gres

sion

Pers

iste

nce

asso

ciat

edw

ithad

vert

isin

gin

tens

ity,

expo

rtin

tens

ity,

fore

ign

firm

s;ne

gativ

ely

affe

cted

byca

pita

lin

tens

ity,

size

,an

dri

sk

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 893

Lev

onia

n(1

994)

Com

pust

at19

86–

91B

anki

ng83

RO

EN

on-l

inea

rL

Sre

gres

sion

Pers

iste

nce

that

deca

yssl

owly

over

time

Kam

bham

pati

(199

5)R

eser

veB

ank

ofIn

dia,

Bom

bay

1970

–85

Mul

tipl

e(4

2)(I

ndia

only

)N

A‘P

rofit

diff

eren

tials

’(i

ndus

try

rela

tive

toec

onom

y-w

ide)

OL

Sre

gres

sion

Pers

iste

nce

ina

larg

enu

mbe

rof

indu

stri

esas

soci

ated

with

high

grow

than

dhi

ghco

ncen

trat

ion

ratio

sG

odda

rdan

dW

ilso

n(1

996)

AC

RO

BA

TS

(Uni

vers

ityof

Bat

h)

1972

–91

Man

ufac

turi

ngan

dse

rvic

es(U

Kon

ly)

425

UK

‘Pro

fitra

te’

(firm

profi

t—sa

mpl

eav

g./s

ampl

eav

g.)

AR

(1)

regr

essi

onSe

rvic

ein

dust

ries

mor

epe

rsis

tent

than

man

ufac

turi

ngin

dust

ries

War

ing

(199

6)C

ompu

stat

1970

–89

All

(68

2-di

git)

12,9

86R

OA

AR

(1)

regr

essi

onPe

rsis

tenc

eva

ries

byin

dust

ryM

cDon

ald

(199

9)IB

IS19

84–

93M

anuf

actu

ring

(Aus

tral

iaon

ly)

246

RO

Sas

prox

yfo

rpr

ice–

cost

mar

gin

Inst

rum

enta

lva

riab

les

Stro

ngde

gree

ofpe

rsis

tenc

e

McG

ahan

and

Port

er(1

999)

Com

pust

atSe

gmen

t19

82–

94A

llbu

tde

posi

tory

inst

itut

ions

and

mis

cella

neou

s

7,00

5R

OA

(ope

ratin

gin

com

e/id

entifi

able

asse

ts)

OL

Sre

gres

sion

Indu

stry

pers

iste

nce

76.6

–81

.8%

Cor

pora

tepe

rsis

tenc

e53

.6–

71.7

%Se

gmen

tpe

rsis

tenc

e47

.9–

65.5

%R

ober

ts(1

999)

IMS, Com

pust

at,

Glo

balS

cope

1977

–93

Phar

mac

eutic

als

42R

OA

(Fir

mR

OA

—in

d.R

OA

/ind.

RO

A)

Aut

oreg

ress

ion

Pers

iste

nce

asso

ciat

edw

ithin

nova

tive

prop

ensi

ty

Fost

eran

dK

apla

n(2

001)

McK

inse

yC

orpo

rate

Perf

orm

ance

1962

–98

15in

dust

ries

1008

TR

S(T

otal

Ret

urn

toSt

ockh

olde

rs)

Dyn

amic

perf

orm

ance

anal

ysis

Firm

sca

nnot

beat

mar

ket

for

mor

eth

an10

–15

year

s.

Wig

gins

and

Rue

fli(2

002)

Com

pust

at19

72–

9740

6,77

2R

OA

Tobi

n’s

qE

vent

hist

ory

anal

ysis

and

ordi

nal

time

seri

esan

alys

is

RO

Ape

rsis

tenc

ein

all

40in

dust

ries

(5%

offir

ms;

atta

inm

ent

posi

tivel

yco

rrel

ated

with

size

,ne

gativ

ely

with

dive

rsifi

catio

n);

Tobi

n’s

qpe

rsis

tenc

ein

35in

dust

ries

(2%

offir

ms;

atta

inm

ent

nega

tivel

yco

rrel

ated

with

size

)R

uefli

and

Wig

gins

(200

3)

Com

pust

atSe

gmen

t19

80–

96A

ll(2

783-

digi

t;39

24-

digi

t)8,

806

RO

A(o

pera

ting

inco

me/

iden

tifiab

leas

sets

)

Ord

inal

(PL

UM

)re

gres

sion

and

Cox

regr

essi

on

Indu

stry

pers

iste

nce

62.6

%C

orpo

rate

pers

iste

nce

54.4

%Se

gmen

tpe

rsis

tenc

e43

.4%

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

894 R. R. Wiggins and T. W. Ruefli

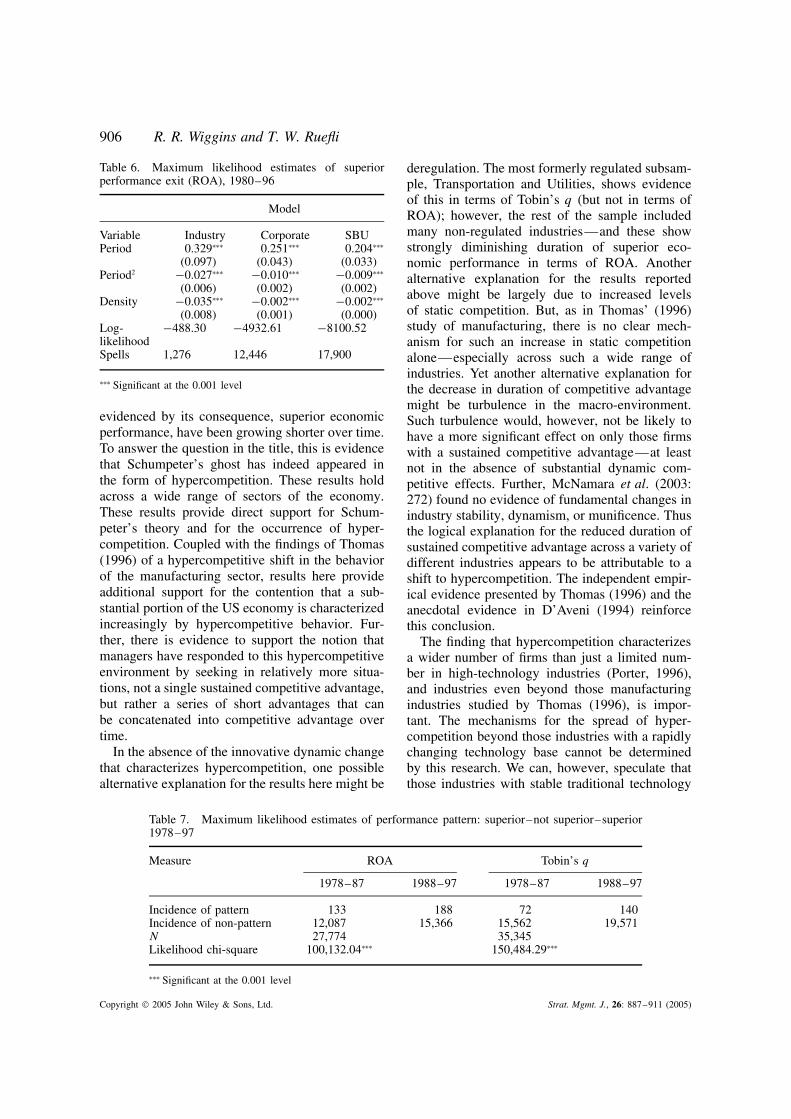

Some have argued that hypercompetition is sopervasive that ‘all competitive advantage is tem-porary’ (Fine, 1998: 30). But not everyone agrees.Michael Porter stated ‘in many industries, how-ever, what some call hypercompetition is a self-inflicted wound, not the inevitable outcome of achanging paradigm of competition’ (Porter, 1996:61) and that it is most likely to be limited to asubset of firms in high-technology industries. Thequestion of which of these arguments should pre-vail is ultimately an empirical one, and that is thepurpose of this research, to examine this questionby a longitudinal examination of the nature of thetiming of the loss of sustained competitive advan-tage, the scope across industries, and the unitary ormultiple nature of competitive advantage. In short,we seek to test whether there is a basis on whichthe call for ‘advocates of the hypercompetitiveparadigm to back up their sweeping generalizationsabout the ubiquity of hypercompetition with rigor-ous large-sample empirical evidence’ (Makadok,1998) can be answered.

While the above focuses on the state of empir-ical research on persistent superior performance,there have also been some investigations specif-ically into hypercompetition. In the first notableantecedent empirical test of some of the aspectsof hypercompetition, Thomas (1996) performed alarge-scale study, examining over 200 manufac-turing industries during the period from 1958 to1991 and found that a ‘hypercompetitive shift’ hasindeed occurred in this sector of the US economy.These models used growth rates in stock marketvalue as the dependent variable, the results camefrom pooled cross-section time-series data ana-lyzed using regression-based methodologies, andthe sample was restricted to manufacturing firms.Our study will build on Thomas’s approach, butwill use alternate measures and methods to directlyfocus on the signature aspects of hypercompetition.Both accounting and market measures of perfor-mance will be employed to provide immediatecomparisons with antecedent research. Longitudi-nal data will be employed to better enable theexamination of possible effects of hypercompeti-tion over time. We also use a unique stratifica-tion methodology applied industry by industry toidentify superior performers and to control for thecommon effects of general economic and industryconditions and then employ event history analysisto better discern over time which firms and whichindustries are involved in the possible effects of

Schumpeterian dynamics. Further, we include notonly manufacturing firms but also mining, naturalresource, transportation, utility, financial, and ser-vice firms, thus providing evidence about the scopeof possible hypercompetitive effects.

Another empirical study that bears on hyper-competition is that of Young, Smith, and Grimm(1996), who, in an examination of single-businessfirms in the software industry, obtained resultsthat indicated that competitive moves, unless theywere extreme, contributed more to increased per-formance than to industry rivalry. These resultswere extended and greatly expanded upon by Fer-rier, Smith, and Grimm (1999) who, in a pairedsample empirical study of single or dominant busi-ness firms, examined the possible market shareerosion and dethronement of market leaders whenconfronted by challengers. Their findings indicatethat across a wide range of industries market lead-ers which are faced with relatively more aggres-sive challengers are likely to be subject to marketshare erosion and dethronement as market leader.This finding is confirmed by Foster and Kaplan(2001) who, working with a McKinsey sampleof 1008 firms over 36 years, found that even themost admired firms could not maintain their above-market performance for more than 10–15 years.

The most recent large-scale empirical examina-tion of hypercompetition was assayed by McNa-mara et al. (2003) and is the study most com-parable to the one reported here. Their study ofa subset of the firms in this study, covering theperiod 1977–97, included an autoregressive modelsimilar to that used by Mueller (1986) and Jacob-son (1988), but included an interaction term toexamine changes in the rate of decay of perfor-mance (both superior and inferior). This interac-tion term was not significantly different from zero,indicating no significant change in the decay rateover time. These studies also reported no increasein mortality rates, no increasing trend in indus-try dynamism, and no decreasing trend in industrymunificence. Based on these findings, they arguethat the tendency for researchers to believe inhypercompetition may be a result of researcherhindsight. While we do not dispute their find-ings on mortality, dynamism, and munificence, andwe applaud their focus on changes in the rate ofdecay in their autoregressive models, we reiter-ate our arguments about the use of autoregressivemodels that admix superior, average, and inferiorperformers, do not compensate for overall trends in

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 895

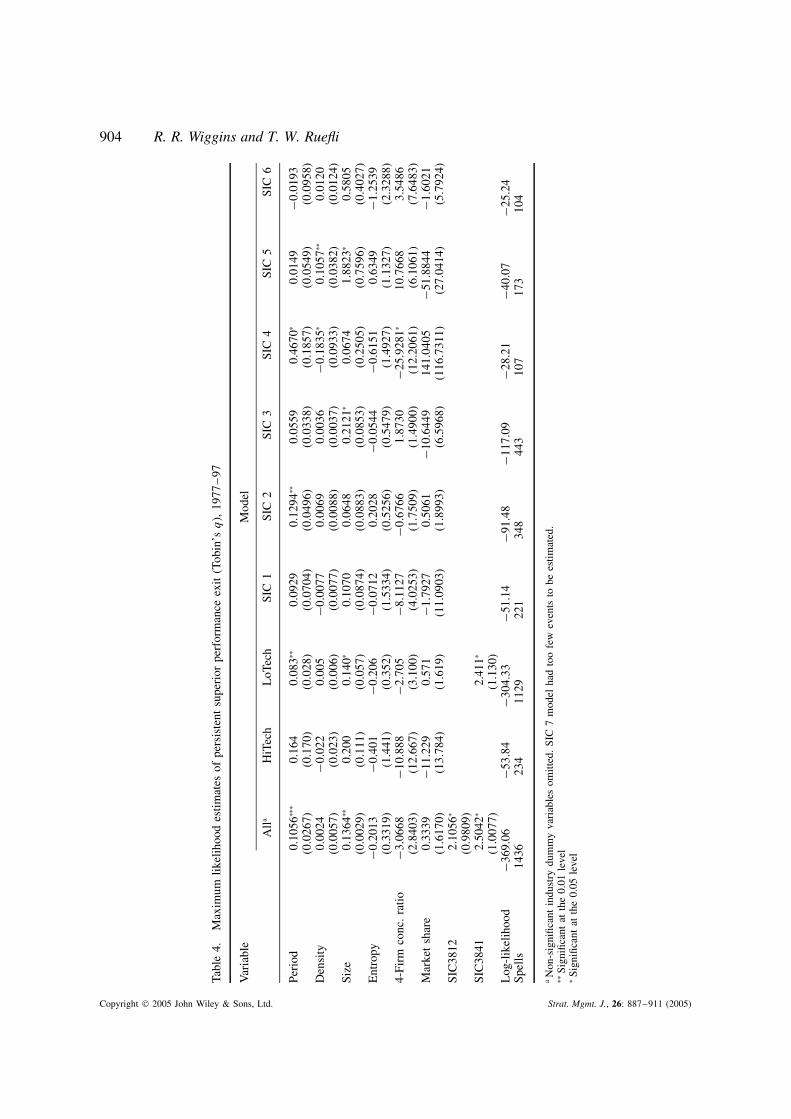

performance, require parametric assumptions, andthat are sensitive to outliers. Our approach willbe to focus only on the persistent superior per-formers and any effects on their rate of loss ofperformance. After all, the primary effect men-tioned in Schumpeterian theory and argued byD’Aveni (1994) is increased difficulty in sustaininga competitive advantage. To enhance direct com-parability with McNamara et al. (2003), we willinclude analyses utilizing the same Compustat seg-ment dataset that they (as well as McGahan andPorter, (1999) used.

THE RESEARCH QUESTIONS

Has persistent superior economic performancebecome more difficult to maintain over time, as theSchumpeterian theories would suggest? In whichindustries? Have firms increasingly sought sus-tained competitive advantage through concatena-tion of a set of shorter-term competitive advan-tages? These are the chief research questionsthat will be addressed through the formulation ofhypotheses and via a novel empirical study.

HYPOTHESIS DEVELOPMENT

Hypercompetition and loss of persistentsuperior economic performance

Conventional strategic management theory doesnot give a prominent role to either Schumpeteriantheory or hypercompetition. Porter (1980, 1985,1996) has long argued that classic industrial orga-nization solutions such as ‘increasing barriers toentry and gaining market power over rivals, sup-pliers and buyers will reduce rivalry within anindustry’ (Ilinitch et al., 1998: xxvi). Indeed, suchreasoning argues that we should see over timean increase in the length of time that competi-tive advantage can be maintained. McNamara et al.(2003) indicate there has been no change. On theother hand, D’Aveni (1994) clearly argues thathypercompetition is making it more and more dif-ficult for firms to maintain a competitive advan-tage. Therefore, we should see the average periodfor which firms sustain a competitive advantagedecrease over time. Following Schumpeterian the-ory and D’Aveni’s line of reasoning, the hypothesisis proposed:

Hypothesis 1: Periods of persistent superioreconomic performance have decreased in dura-tion over time.

Hypercompetition across multiple industries

Schumpeter (1939), followed by D’Aveni (1994:4), originally argued for the near-ubiquity of hyper-competition: ‘There are few industries and com-panies that have escaped this shift in compet-itiveness.’ Porter (1996) argued that hypercom-petitive effects are likely to be limited to high-technology industries. D’Aveni, in a more recentpublication (1999), proposed that there are fourenvironments of varying turbulence ranging from‘equilibrium’ to ‘disequilibrium.’ The latter envi-ronment he identifies with hypercompetition, buthe does not in this work specify the degree ofprevalence of any of his environments in the econ-omy. To formulate our next hypothesis we revertto Schumpeter and to D’Aveni’s original position,which leads directly to this formulation:

Hypothesis 2: Hypercompetition is not limited tohigh-technology industries, but occurs through-out most industries.

Hypercompetition and series of temporarycompetitive advantages

D’Aveni specifically stated, ‘Instead of seeking asustainable advantage, strategy in hypercompeti-tive environments now focuses on developing aset of temporary advantages’ (D’Aveni, 1994: 7).He reiterated this when he said, ‘If companiesare not seeking a sustainable competitive advan-tage, what is the goal of strategy in hypercom-petitive environments? The primary goal of thisnew approach to strategy is disruption of the sta-tus quo, to seize the initiative through creating aseries of temporary advantages’ (D’Aveni, 1994:10). Brown and Eisenhardt (1998) also argued thatsuccess can only come from a continuous streamof temporary advantages when the environmentis ‘relentlessly shifting’ (Brown and Eisenhardt,1997). These arguments lead directly to the fol-lowing hypothesis:

Hypothesis 3: Over time firms increasingly havesought to sustain competitive advantage by con-catenating a series of short-term competitiveadvantages.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

896 R. R. Wiggins and T. W. Ruefli

METHODS

Data

Data were collected from three primary sources:the Compustat PC-Plus database (both active andresearch files) for the 20 years from 1978 to 1997inclusive, the Compustat Back History databasefor the 5-year period from 1972 to 1977, andthe Compustat Segment Tapes for 1978–97. Weincluded data from the Compustat Back Historydatabase to provide 20 overlapping 5-year peri-ods (1974–97), as well as two additional years(1972–73) to alleviate some of the left-censoringproblem. SIC codes for firms that exited thedatabase prior to 1978 are not included in theBack History database; these firms were classi-fied employing the CRSP/Compustat Cross Refer-ence database maintained by the Johnson GraduateSchool of Management at Cornell University, andalso the Moody’s Industrial, OTC, Transportation,Financial, and Utilities Manuals. Two samples (afirm-level and a business-unit-level sample) werederived from the primary source data.

Dependent variables

While the theories used to develop the hypothe-ses relate to sustained competitive advantage, weare unable to directly operationalize the concept.Barney (1991: 102), for example, defines a sus-tained competitive advantage as a competitiveadvantage that ‘continues to exist after efforts toduplicate that advantage have ceased.’ What wecan operationalize is the consequence of sustainedcompetitive advantage, persistent economic per-formance. While some may find this less desir-able, it is consistent with the work of Porter, whorefers to ‘long-term profitability’ (Porter, 1985: 1)and ‘above-average performance in the long run’(Porter, 1985: 11) when discussing the outcomesof sustained competitive advantage.

Two measures were used to operationalize eco-nomic performance: return on assets (ROA), anaccounting measure, and Tobin’s q (the ratio offirm market value to the replacement cost of itsassets), a market measure, because some studieshave shown results that vary between accountingand market measures (Hoskisson, Hitt and John-son, 1993). ROA (net income divided by totalassets for firms, segment net income divided byidentifiable assets for business units) was selected

primarily for comparability with earlier economicand strategic management research in this area (seeTable 1, where most of the studies use ROA astheir primary or only measure of performance).Tobin’s q was selected because, although he didnot use it in his study, Mueller (1990: 8–14) sug-gested its potential, and because Tobin’s q was uti-lized by McGahan and Porter (1999) and Wigginsand Ruefli (2002), and so its inclusion enhancescomparability with their results. Tobin’s q wasoperationalized as the ratio of market value to thebook value of assets. This ratio has been shownto be not only empirically equivalent (Perfect andWiles, 1994) but also theoretically equivalent toTobin’s q (Varaiya, Kerin, and Weeks, 1987).

Superior economic performance was operation-alized as statistically significant above averageeconomic performance (relative to other firms inthe same industry for the firm-level analyses, andrelative to all business units, or all industries, or allfirms for the segment-level analyses) over a 5-yearperiod. Note that this is consistent with Besanko,Dranove, and Shanley (1996), who define compet-itive advantage as a firm outperforming its indus-try. This was determined using the Iterative Kol-mogorov–Smirnov (IKS) technique, which strati-fies time-series data into statistically significantlydifferent levels of performance using iterativecomparisons described in detail in Ruefli and Wig-gins (2000). A rolling 5-year window (Cool andSchendel, 1988; Fiegenbaum and Thomas, 1988)was used for all measures. Since this techniqueyields ordinal categorical data (Argresti, 1984),factors such as the common effects of general eco-nomic conditions, industry cycles, and product lifecycles are controlled in the stratification process.

However, IKS analysis can generate varyingnumbers of performance strata over time, whichmakes longitudinal comparisons difficult. We areinterested only in the firms with performanceabove the industry or reference set modal stratum.Therefore, as a form of a fortiori analysis (becauseit is conservative in regard to the hypotheses beingtested), the number of performance strata was com-pressed in each time period to three by creating twosupersets of strata: those above the modal stratumand those below the modal stratum. To validate thestratification supersets, discriminant function anal-ysis was employed in a confirmatory mode on theindustries studied. For these industries, all of thediscriminant functions were significant (p < 0.05)

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 897

for all variables, demonstrating the validity of thesuperset performance strata.

Persistent superior economic performance at thecorporate level was operationalized as superioreconomic performance lasting for six or more win-dows (i.e., a 10-year period), inasmuch as therewere two non-overlapping 5-year windows in sucha period, which eliminated potential bias owing tothe effect of a single year of outstanding perfor-mance. This establishes a very stringent test for theperformance effects of hypercompetition and onethat is tied directly to Schumpeterian theory, in thatit is only the significant shortening of the periodsduring which only those firms with significant sus-tained competitive advantage (i.e., over periods of10 years or more) that will be accepted as evi-dence. The first 5-year window in the firm-levelmodels is 1977–81 since that is the first windowin which an exit from the persistent superior eco-nomic performance stratum could occur. For thebusiness unit-level data, 5 years (one window) wasused to enhance comparability with McNamaraet al. (2003).

Independent and control variables

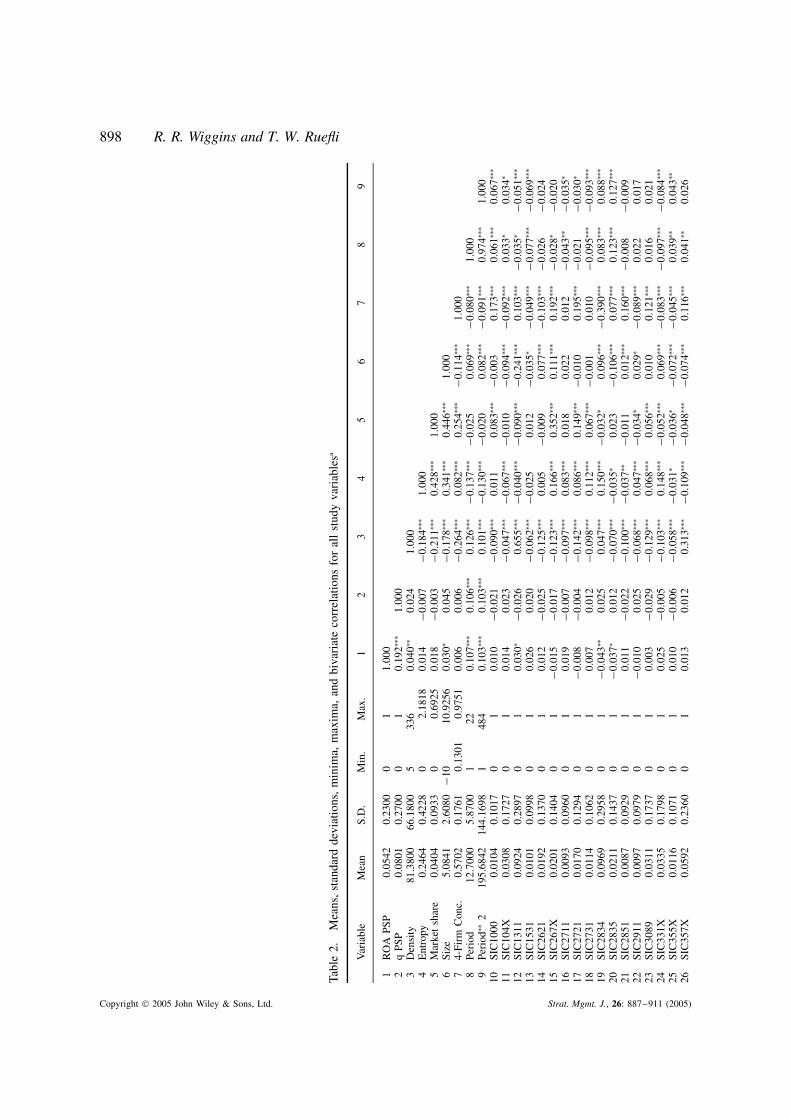

Because the primary question we are investigat-ing is the change over time of the rate at whichfirms lose superior profitability positions, the onlyindependent variable is time period. The strat-ification methodology controls for the commoneffects of general economic conditions, thus othercontrol variables included market share, industryconcentration, firm size, diversification, industrydensity, and dummy variables for each industry.These variables were operationalized as follows.For market share we used the ratio of each firm’stotal revenues to the total revenues of all firmsin the industry. Table 2 shows that market shareranged from 0 to 0.69 with a mean across allfirms of 0.04. Industry concentration was oper-ationalized by calculating the four-firm concen-tration ratio by dividing the combined total rev-enues of the four largest firms in each industryby the total revenues of all firms in the industry.As seen in Table 2, the industry four-firm con-centration ratio ranged from 0.13 to 0.98, with amean across all 40 industries of 0.57. For firm sizethe natural logarithm of total sales was employed.Table 2 shows the range of firm size as −10 to10.93 with a mean of 5.08. For diversificationwe used the Jacquemin–Berry entropy measure

of diversification (Jacquemin and Berry, 1979;Palepu, 1985), which is defined as

E =n∑

i=1

Pi ln(1/Pi)

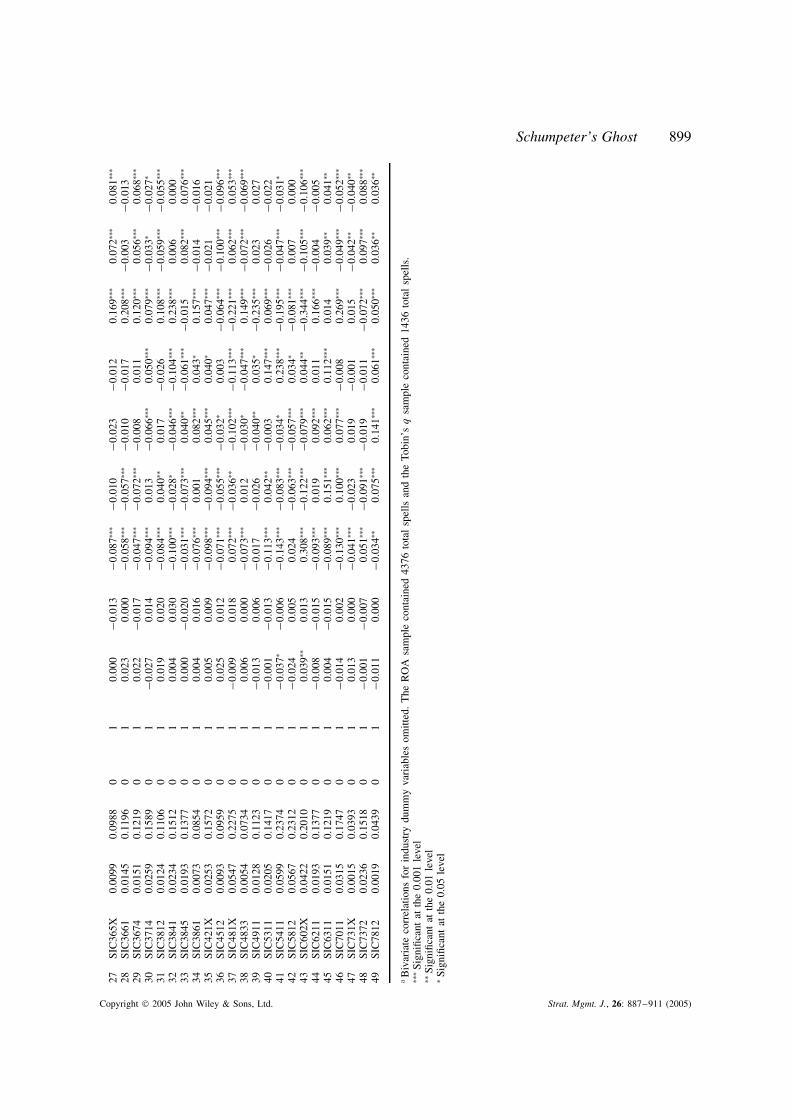

where Pi is the ith segment’s share of the firm’stotal sales, which operates in n segments. As seenin Table 2, entropy ranged from 0 to 2.18 with amean of 0.25. For density we used the total num-ber of firms in each industry in each period, whichas Table 2 shows ranged from 5 to 336 with amean of 81.38. Because the dependent variablesrepresent 5-year windows, all of the control vari-ables were 5-year moving averages matched to thedependent variables’ 5-year windows. Finally, theindustry dummy variables were coded using thedeviation method, which compares the effect ofeach dummy variable to the overall effect. Thedescriptive statistics and correlations of the studyvariables are shown in Table 2.

Samples

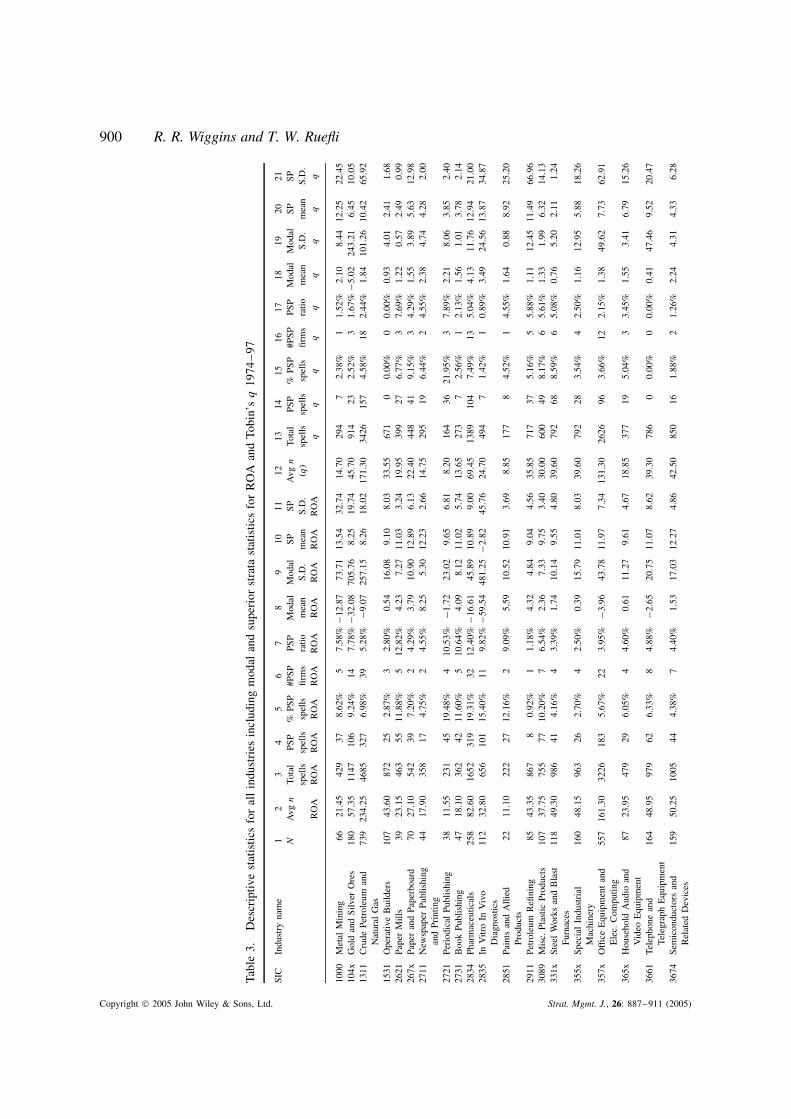

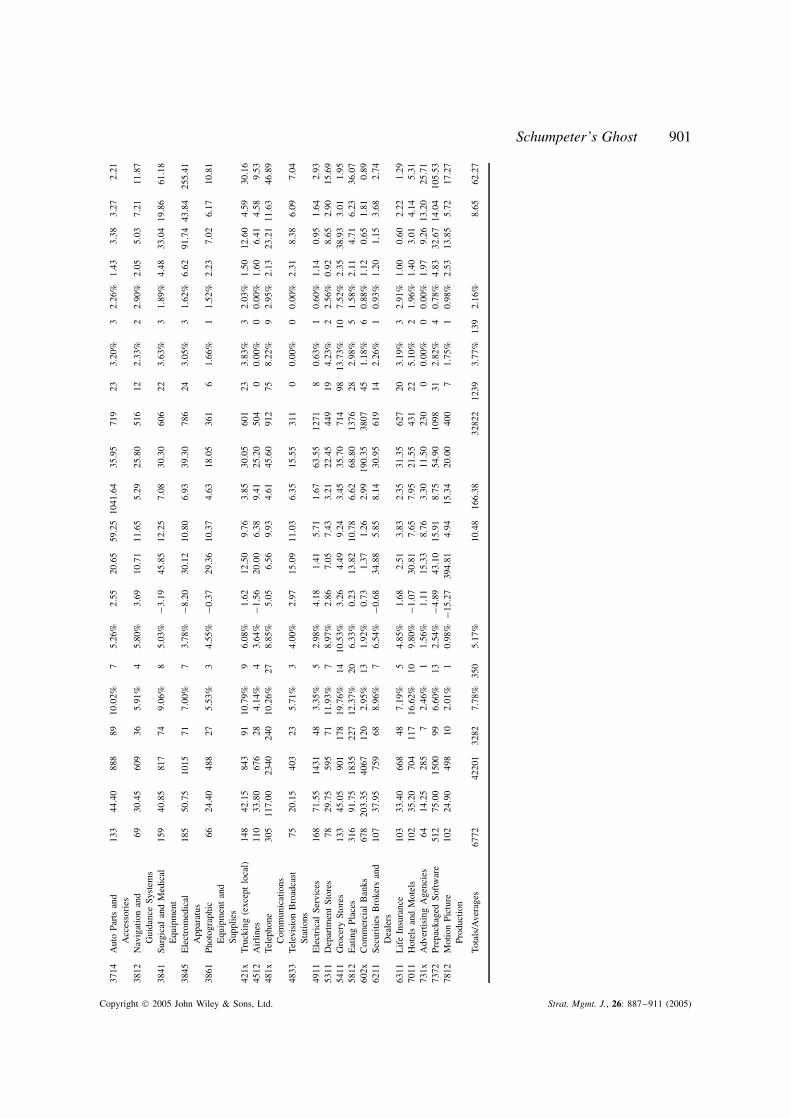

For the firm-level sample we selected the same 40industries (listed in Table 3) used by Wiggins andRuefli (2002). The industries in this sample repre-sent 7 out of 10 1-digit SIC level categories. Thissample thus includes an overlap with Thomas’s(1996) sample, although most of the industriesconsidered are outside the manufacturing sectorand is a superset of the sample used by McNamaraet al. (2003). Table 3 shows the complete firm-level sample, along with some descriptive statis-tics. For the segment-level sample we used all ofthe available Compustat segment data, since wewere not utilizing regression and therefore did notface the same methodological issues as McGahanand Porter (1999) and McNamara et al. (2003), andtherefore did not have to screen the data and loseobservations.

Identification of superior performance

In essence, our research concentrates on an outlieror frontier phenomenon (Starbuck, 1993), i.e., theloss of superior economic performance. In orderto identify firms that have lost superior economicperformance, we first identified firms that obtainedsuperior economic performance. Most statisticaltechniques, however, are based on measures ofcentral tendency, and consequently their focus is

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

898 R. R. Wiggins and T. W. Ruefli

Tabl

e2.

Mea

ns,

stan

dard

devi

atio

ns,

min

ima,

max

ima,

and

biva

riat

eco

rrel

atio

nsfo

ral

lst

udy

vari

able

sa

Var

iabl

eM

ean

S.D

.M

in.

Max

.1

23

45

67

89

1R

OA

PSP

0.05

420.

2300

01

1.00

02

qPS

P0.

0801

0.27

000

10.

192∗∗

∗1.

000

3D

ensi

ty81

.380

066

.180

05

336

0.04

0∗∗0.

024

1.00

04

Ent

ropy

0.24

640.

4228

02.

1818

0.01

4−0

.007

−0.1

84∗∗

∗1.

000

5M

arke

tsh

are

0.04

040.

0933

00.

6925

0.01

8−0

.003

−0.2

11∗∗

∗0.

428∗∗

∗1.

000

6Si

ze5.

0841

2.60

80−1

010

.925

60.

030∗

0.04

5−0

.178

∗∗∗

0.34

1∗∗∗

0.44

6∗∗∗

1.00

07

4-Fi

rmC

onc.

0.57

020.

1761

0.13

010.

9751

0.00

60.

006

−0.2

64∗∗

∗0.

082∗∗

∗0.

254∗∗

∗−0

.114

∗∗∗

1.00

08

Peri

od12

.700

05.

8700

122

0.10

7∗∗∗

0.10

6∗∗∗

0.12

6∗∗∗

−0.1

37∗∗

∗−0

.025

0.06

9∗∗∗

−0.0

80∗∗

∗1.

000

9Pe

riod

∗∗2

195.

6842

144.

1698

148

40.

103∗∗

∗0.

103∗∗

∗0.

101∗∗

∗−0

.130

∗∗∗

−0.0

200.

082∗∗

∗−0

.091

∗∗∗

0.97

4∗∗∗

1.00

010

SIC

1000

0.01

040.

1017

01

0.01

0−0

.021

−0.0

90∗∗

∗0.

011

0.08

3∗∗∗

−0.0

030.

173∗∗

∗0.

061∗∗

∗0.

067∗∗

∗

11SI

C10

4X0.

0308

0.17

270

10.

014

0.02

3−0

.047

∗∗∗

−0.0

67∗∗

∗−0

.010

−0.0

94∗∗

∗−0

.092

∗∗∗

0.03

3∗0.

034∗

12SI

C13

110.

0924

0.28

970

10.

030∗

−0.0

260.

655∗∗

∗−0

.040

∗∗∗

−0.0

90∗∗

∗−0

.241

∗∗∗

0.10

3∗∗∗

−0.0

35∗

−0.0

51∗∗

∗

13SI

C15

310.

0101

0.09

980

10.

026

0.02

0−0

.062

∗∗∗

−0.0

250.

012

−0.0

35∗

−0.0

49∗∗

∗−0

.077

∗∗∗

−0.0

69∗∗

∗

14SI

C26

210.

0192

0.13

700

10.

012

−0.0

25−0

.125

∗∗∗

0.00

5−0

.009

0.07

7∗∗∗

−0.1

03∗∗

∗−0

.026

−0.0

2415

SIC

267X

0.02

010.

1404

01

−0.0

15−0

.017

−0.1

23∗∗

∗0.

166∗∗

∗0.

352∗∗

∗0.

111∗∗

∗0.

192∗∗

∗−0

.028

∗−0

.020

16SI

C27

110.

0093

0.09

600

10.

019

−0.0

07−0

.097

∗∗∗

0.08

3∗∗∗

0.01

80.

022

0.01

2−0

.043

∗∗−0

.035

∗

17SI

C27

210.

0170

0.12

940

1−0

.008

−0.0

04−0

.142

∗∗∗

0.08

6∗∗∗

0.14

9∗∗∗

−0.0

100.

195∗∗

∗−0

.021

−0.0

30∗

18SI

C27

310.

0114

0.10

620

10.

007

0.01

2−0

.098

∗∗∗

0.11

2∗∗∗

0.06

7∗∗∗

−0.0

010.

010

−0.0

95∗∗

∗−0

.093

∗∗∗

19SI

C28

340.

0969

0.29

580

1−0

.043

∗∗0.

025

0.04

7∗∗∗

0.15

0∗∗∗

−0.0

32∗

0.09

6∗∗∗

−0.3

90∗∗

∗0.

083∗∗

∗0.

088∗∗

∗

20SI

C28

350.

0211

0.14

370

1−0

.037

∗0.

012

−0.0

70∗∗

∗−0

.035

∗0.

023

−0.1

06∗∗

∗0.

077∗∗

∗0.

123∗∗

∗0.

127∗∗

∗

21SI

C28

510.

0087

0.09

290

10.

011

−0.0

22−0

.100

∗∗∗

−0.0

37∗∗

−0.0

110.

012∗∗

∗0.

160∗∗

∗−0

.008

−0.0

0922

SIC

2911

0.00

970.

0979

01

−0.0

100.

025

−0.0

68∗∗

∗0.

047∗∗

∗−0

.034

∗0.

029∗

−0.0

89∗∗

∗0.

022

0.01

723

SIC

3089

0.03

110.

1737

01

0.00

3−0

.029

−0.1

29∗∗

∗0.

068∗∗

∗0.

056∗∗

∗0.

010

0.12

1∗∗∗

0.01

60.

021

24SI

C33

1X0.

0335

0.17

980

10.

025

−0.0

05−0

.103

∗∗∗

0.14

8∗∗∗

−0.0

52∗∗

∗0.

069∗∗

∗−0

.083

∗∗∗

−0.0

97∗∗

∗−0

.084

∗∗∗

25SI

C35

5X0.

0116

0.10

710

10.

010

−0.0

06−0

.058

∗∗∗

−0.0

31∗

−0.0

36∗

−0.0

72∗∗

∗−0

.045

∗∗∗

0.03

9∗∗0.

043∗∗

26SI

C35

7X0.

0592

0.23

600

10.

013

0.01

20.

313∗∗

∗−0

.109

∗∗∗

−0.0

48∗∗

∗−0

.074

∗∗∗

0.11

6∗∗∗

0.04

1∗∗0.

026

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 899

27SI

C36

5X0.

0099

0.09

880

10.

000

−0.0

13−0

.087

∗∗∗

−0.0

10−0

.023

−0.0

120.

169∗∗

∗0.

072∗∗

∗0.

081∗∗

∗

28SI

C36

610.

0145

0.11

960

10.

023

0.00

0−0

.058

∗∗∗

−0.0

57∗∗

∗−0

.010

−0.0

170.

208∗∗

∗−0

.003

−0.0

1329

SIC

3674

0.01

510.

1219

01

0.02

2−0

.017

−0.0

47∗∗

∗−0

.072

∗∗∗

−0.0

080.

011

0.12

0∗∗∗

0.05

6∗∗∗

0.06

8∗∗∗

30SI

C37

140.

0259

0.15

890

1−0

.027

0.01

4−0

.094

∗∗∗

0.01

3−0

.066

∗∗∗

0.05

0∗∗∗

0.07

9∗∗∗

−0.0

33∗

−0.0

27∗

31SI

C38

120.

0124

0.11

060

10.

019

0.02

0−0

.084

∗∗∗

0.04

0∗∗0.

017

−0.0

260.

108∗∗

∗−0

.059

∗∗∗

−0.0

55∗∗

∗

32SI

C38

410.

0234

0.15

120

10.

004

0.03

0−0

.100

∗∗∗

−0.0

28∗

−0.0

46∗∗

∗−0

.104

∗∗∗

0.23

8∗∗∗

0.00

60.

000

33SI

C38

450.

0193

0.13

770

10.

000

−0.0

20−0

.031

∗∗∗

−0.0

73∗∗

∗0.

040∗∗

−0.0

61∗∗

∗−0

.015

0.08

2∗∗∗

0.07

6∗∗∗

34SI

C38

610.

0073

0.08

540

10.

004

0.01

6−0

.076

∗∗∗

0.00

10.

082∗∗

∗0.

043∗

0.15

7∗∗∗

−0.0

14−0

.016

35SI

C42

1X0.

0253

0.15

720

10.

005

0.00

9−0

.098

∗∗∗

−0.0

94∗∗

∗0.

045∗∗

∗0.

040∗

0.04

7∗∗∗

−0.0

21−0

.021

36SI

C45

120.

0093

0.09

590

10.

025

0.01

2−0

.071

∗∗∗

−0.0

55∗∗

∗−0

.032

∗0.

003

−0.0

64∗∗

∗−0

.100

∗∗∗

−0.0

96∗∗

∗

37SI

C48

1X0.

0547

0.22

750

1−0

.009

0.01

80.

072∗∗

∗−0

.036

∗∗−0

.102

∗∗∗

−0.1

13∗∗

∗−0

.221

∗∗∗

0.06

2∗∗∗

0.05

3∗∗∗

38SI

C48

330.

0054

0.07

340

10.

006

0.00

0−0

.073

∗∗∗

0.01

2−0

.030

∗−0

.047

∗∗∗

0.14

9∗∗∗

−0.0

72∗∗

∗−0

.069

∗∗∗

39SI

C49

110.

0128

0.11

230

1−0

.013

0.00

6−0

.017

−0.0

26−0

.040

∗∗0.

035∗

−0.2

35∗∗

∗0.

023

0.02

740

SIC

5311

0.02

050.

1417

01

−0.0

01−0

.013

−0.1

13∗∗

∗0.

042∗∗

−0.0

030.

147∗∗

∗0.

069∗∗

∗−0

.026

−0.0

2241

SIC

5411

0.05

990.

2374

01

−0.0

37∗

−0.0

06−0

.143

∗∗∗

−0.0

83∗∗

∗−0

.034

∗0.

238∗∗

∗−0

.195

∗∗∗

−0.0

47∗∗

∗−0

.031

∗

42SI

C58

120.

0567

0.23

120

1−0

.024

0.00

50.

024

−0.0

63∗∗

∗−0

.057

∗∗∗

0.03

4∗−0

.081

∗∗∗

0.00

70.

000

43SI

C60

2X0.

0422

0.20

100

10.

039∗∗

0.01

30.

308∗∗

∗−0

.122

∗∗∗

−0.0

79∗∗

∗0.

044∗∗

−0.3

44∗∗

∗−0

.105

∗∗∗

−0.1

06∗∗

∗

44SI

C62

110.

0193

0.13

770

1−0

.008

−0.0

15−0

.093

∗∗∗

0.01

90.

092∗∗

∗0.

011

0.16

6∗∗∗

−0.0

04−0

.005

45SI

C63

110.

0151

0.12

190

10.

004

−0.0

15−0

.089

∗∗∗

0.15

1∗∗∗

0.06

2∗∗∗

0.11

2∗∗∗

0.01

40.

039∗∗

0.04

1∗∗

46SI

C70

110.

0315

0.17

470

1−0

.014

0.00

2−0

.130

∗∗∗

0.10

0∗∗∗

0.07

7∗∗∗

−0.0

080.

269∗∗

∗−0

.049

∗∗∗

−0.0

52∗∗

∗

47SI

C73

1X0.

0015

0.03

930

10.

013

0.00

0−0

.041

∗∗∗

−0.0

230.

019

−0.0

010.

015

−0.0

42∗∗

−0.0

40∗∗

48SI

C73

720.

0236

0.15

180

1−0

.001

−0.0

070.

051∗∗

∗−0

.091

∗∗∗

−0.0

19−0

.011

−0.0

72∗∗

∗0.

097∗∗

∗0.

088∗∗

∗

49SI

C78

120.

0019

0.04

390

1−0

.011

0.00

0−0

.034

∗∗0.

075∗∗

∗0.

141∗∗

∗0.

061∗∗

∗0.

050∗∗

∗0.

036∗∗

0.03

6∗∗

aB

ivar

iate

corr

elat

ions

for

indu

stry

dum

my

vari

able

som

itted

.T

heR

OA

sam

ple

cont

aine

d43

76to

tal

spel

lsan

dth

eTo

bin’

sq

sam

ple

cont

aine

d14

36to

tal

spel

ls.

∗∗∗

Sign

ifica

ntat

the

0.00

1le

vel

∗∗Si

gnifi

cant

atth

e0.

01le

vel

∗Si

gnifi

cant

atth

e0.

05le

vel

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

900 R. R. Wiggins and T. W. Ruefli

Tabl

e3.

Des

crip

tive

stat

istic

sfo

ral

lin

dust

ries

incl

udin

gm

odal

and

supe

rior

stra

tast

atis

tics

for

RO

Aan

dTo

bin’

sq

1974

–97

SIC

Indu

stry

nam

e1 N

2A

vgn

RO

A

3To

tal

spel

lsR

OA

4PS

Psp

ells

RO

A

5%

PSP

spel

lsR

OA

6#P

SPfir

ms

RO

A

7PS

Pra

tioR

OA

8M

odal

mea

nR

OA

9M

odal

S.D

.R

OA

10 SP mea

nR

OA

11 SP S.D

.R

OA

12A

vgn

(q)

13 Tota

lsp

ells

q

14 PSP

spel

lsq

15%

PSP

spel

lsq

16#P

SPfir

ms

q

17 PSP

ratio q

18M

odal

mea

nq

19M

odal

S.D

.q

20 SP mea

nq

21 SP S.D

.q

1000

Met

alM

inin

g66

21.4

542

937

8.62

%5

7.58

%−1

2.87

73.7

113

.54

32.7

414

.70

294

72.

38%

11.

52%

2.10

8.44

12.2

522

.45

104x

Gol

dan

dSi

lver

Ore

s18

057

.35

1147

106

9.24

%14

7.78

%−3

2.08

705.

768.

2519

.74

45.7

091

423

2.52

%3

1.67

%−5

.02

243.

216.

4510

.05

1311

Cru

dePe

trol

eum

and

Nat

ural

Gas

739

234.

2546

8532

76.

98%

395.

28%

−9.0

725

7.15

8.26

18.0

217

1.30

3426

157

4.58

%18

2.44

%1.

8410

1.26

10.4

265

.92

1531

Ope

rativ

eB

uild

ers

107

43.6

087

225

2.87

%3

2.80

%0.

5416

.08

9.10

8.03

33.5

567

10

0.00

%0

0.00

%0.

934.

012.

411.

6826

21Pa

per

Mill

s39

23.1

546

355

11.8

8%5

12.8

2%4.

237.

2711

.03

3.24

19.9

539

927

6.77

%3

7.69

%1.

220.

572.

490.

9926

7xPa

per

and

Pape

rboa

rd70

27.1

054

239

7.20

%2

4.29

%3.

7910

.90

12.8

96.

1322

.40

448

419.

15%

34.

29%

1.55

3.89

5.63

12.9

827

11N

ewsp

aper

Publ

ishi

ngan

dPr

intin

g44

17.9

035

817

4.75

%2

4.55

%8.

255.

3012

.23

2.66

14.7

529

519

6.44

%2

4.55

%2.

384.

744.

282.

00

2721

Peri

odic

alPu

blis

hing

3811

.55

231

4519

.48%

410

.53%

−1.7

223

.02

9.65

6.81

8.20

164

3621

.95%

37.

89%

2.21

8.06

3.85

2.40

2731

Boo

kPu

blis

hing

4718

.10

362

4211

.60%

510

.64%

4.09

8.12

11.0

25.

7413

.65

273

72.

56%

12.

13%

1.56

1.01

3.78

2.14

2834

Phar

mac

eutic

als

258

82.6

016

5231

919

.31%

3212

.40%

−16.

6145

.89

10.8

99.

0069

.45

1389

104

7.49

%13

5.04

%4.

1311

.76

12.9

421

.00

2835

InV

itro

InV

ivo

Dia

gnos

tics

112

32.8

065

610

115

.40%

119.

82%

−59.

5448

1.25

−2.8

245

.76

24.7

049

47

1.42

%1

0.89

%3.

4924

.56

13.8

734

.87

2851

Pain

tsan

dA

llied

Prod

ucts

2211

.10

222

2712

.16%

29.

09%

5.59

10.5

210

.91

3.69

8.85

177

84.

52%

14.

55%

1.64

0.88

8.92

25.2

0

2911

Petr

oleu

mR

efini

ng85

43.3

586

78

0.92

%1

1.18

%4.

324.

849.

044.

5635

.85

717

375.

16%

55.

88%

1.11

12.4

511

.49

66.9

630

89M

isc.

Plas

ticPr

oduc

ts10

737

.75

755

7710

.20%

76.

54%

2.36

7.33

9.75

3.40

30.0

060

049

8.17

%6

5.61

%1.

331.

996.

3214

.13

331x

Stee

lW

orks

and

Bla

stFu

rnac

es11

849

.30

986

414.

16%

43.

39%

1.74

10.1

49.

554.

8039

.60

792

688.

59%

65.

08%

0.76

5.20

2.11

1.24

355x

Spec

ial

Indu

stri

alM

achi

nery

160

48.1

596

326

2.70

%4

2.50

%0.

3915

.79

11.0

18.

0339

.60

792

283.

54%

42.

50%

1.16

12.9

55.

8818

.26

357x

Offi

ceE

quip

men

tan

dE

lec.

Com

putin

g55

716

1.30

3226

183

5.67

%22

3.95

%−3

.96

43.7

811

.97

7.34

131.

3026

2696

3.66

%12

2.15

%1.

3849

.62

7.73

62.9

1

365x

Hou

seho

ldA

udio

and

Vid

eoE

quip

men

t87

23.9

547

929

6.05

%4

4.60

%0.

6111

.27

9.61

4.67

18.8

537

719

5.04

%3

3.45

%1.

553.

416.

7915

.26

3661

Tele

phon

ean

dTe

legr

aph

Equ

ipm

ent

164

48.9

597

962

6.33

%8

4.88

%−2

.65

20.7

511

.07

8.62

39.3

078

60

0.00

%0

0.00

%0.

4147

.46

9.52

20.4

7

3674

Sem

icon

duct

ors

and

Rel

ated

Dev

ices

159

50.2

510

0544

4.38

%7

4.40

%1.

5317

.03

12.2

74.

8642

.50

850

161.

88%

21.

26%

2.24

4.31

4.33

6.28

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 887–911 (2005)

Schumpeter’s Ghost 901

3714

Aut

oPa

rts

and

Acc

esso

ries

133

44.4

088

889

10.0

2%7

5.26

%2.

5520

.65

59.2

510

41.6

435

.95

719

233.

20%

32.

26%

1.43

3.38

3.27

2.21

3812

Nav

igat

ion

and

Gui

danc

eSy

stem

s69

30.4

560

936

5.91

%4

5.80

%3.

6910

.71

11.6

55.

2925

.80

516

122.

33%

22.

90%

2.05

5.03

7.21

11.8

7

3841

Surg

ical

and

Med

ical

Equ

ipm

ent

159

40.8

581

774

9.06

%8

5.03

%−3

.19

45.8

512

.25

7.08

30.3

060

622

3.63

%3

1.89

%4.

4833

.04

19.8

661

.18

3845

Ele

ctro

med

ical

App

arat

us18

550

.75

1015

717.

00%

73.

78%

−8.2

030

.12

10.8

06.

9339

.30

786

243.

05%

31.

62%

6.62

91.7

443

.84

255.

41

3861

Phot

ogra

phic

Equ

ipm

ent

and

Supp

lies

6624

.40

488

275.

53%

34.

55%

−0.3

729

.36

10.3

74.

6318

.05

361

61.

66%

11.

52%

2.23

7.02

6.17

10.8

1

421x

Tru

ckin

g(e

xcep

tlo

cal)

148

42.1

584

391

10.7

9%9

6.08

%1.

6212

.50

9.76

3.85

30.0

560

123

3.83

%3

2.03

%1.

5012

.60

4.59

30.1

645

12A

irlin

es11

033

.80

676

284.

14%

43.

64%

−1.5

620

.00

6.38

9.41

25.2

050

40

0.00

%0

0.00

%1.

606.

414.

589.

5348

1xTe

leph

one

Com

mun

icat

ions

305

117.

0023

4024

010

.26%

278.

85%

5.05

6.56

9.93

4.61

45.6

091

275

8.22

%9

2.95

%2.

1323

.21

11.6

346

.89

4833

Tele

visi

onB

road

cast

Stat

ions

7520

.15

403

235.

71%

34.

00%

2.97

15.0

911

.03

6.35

15.5

531

10

0.00

%0

0.00

%2.

318.

386.

097.

04

4911

Ele

ctri

cal

Serv

ices

168

71.5

514

3148

3.35

%5

2.98

%4.

181.

415.

711.

6763

.55

1271

80.

63%

10.

60%

1.14

0.95

1.64

2.93

5311

Dep

artm

ent

Stor

es78

29.7

559

571

11.9

3%7

8.97

%2.

867.

057.

433.

2122

.45

449

194.

23%

22.

56%

0.92

8.65

2.90

15.6

954

11G

roce

rySt

ores

133

45.0

590

117

819

.76%

1410

.53%

3.26

4.49

9.24

3.45

35.7

071

498

13.7

3%10

7.52

%2.

3538

.93

3.01

1.95

5812

Eat

ing

Plac

es31

691

.75

1835

227

12.3

7%20

6.33

%0.

2313

.82

10.7

86.

6268

.80

1376

282.

98%

51.

58%

2.11

4.71

6.23

36.0

760

2xC

omm

erci

alB

anks

678

203.

3540

6712

02.

95%

131.

92%

0.73

1.37

1.26

2.99

190.

3538

0745

1.18

%6

0.88

%1.

120.

651.

810.

8962

11Se

curi

ties

Bro

kers

and

Dea

lers

107

37.9

575

968

8.96

%7

6.54

%−0

.68

34.8

85.

858.

1430

.95

619

142.

26%

10.

93%

1.20

1.15

3.68

2.74

6311

Lif

eIn

sura

nce

103

33.4

066

848

7.19

%5

4.85

%1.

682.

513.

832.

3531

.35

627

203.

19%

32.

91%

1.00

0.60

2.22

1.29

7011

Hot

els

and

Mot

els

102

35.2

070

411

716

.62%

109.

80%

−1.0

730

.81

7.65

7.95

21.5

543

122

5.10

%2

1.96

%1.

403.

014.

145.

3173

1xA

dver

tisin

gA

genc

ies

6414

.25

285

72.

46%

11.

56%

1.11

15.3

38.

763.

3011

.50

230

00.

00%

00.

00%

1.97

9.26

13.2

025

.71

7372

Prep

acka

ged

Soft

war

e51

275

.00

1500

996.

60%

132.

54%

−4.8

943

.10

15.9

18.

7554

.90

1098

312.

82%

40.

78%

4.83

32.6

714

.04

105.

5378

12M

otio

nPi

ctur

ePr

oduc

tion

102

24.9

049

810

2.01

%1

0.98

%−1

5.27

394.

814.

9415

.34

20.0

040

07

1.75

%1

0.98

%2.

5313