Embed Size (px)

Citation preview

Schroder US Small & Smid Cap Product Review

Representing Schroders:

Jenny B. Jones, Head of U.S. Small and Mid Cap Equities

Frederick Schaefer, Product Manager

May 8, 2013

| For professional investors only. This material is not suitable for retail clients

Supported by: 3 traders; 1 product executive; 1 portfolio management assistant, and 1 additional support staff

Jenny Jones Portfolio Manager

33 years of experience Insurance, Capital Goods

Robert Starbuck Research Director 35 years of experience Energy, Materials

John Helfst 18 yrs experience Banks, Brokers,

Specialty Finance

Steve Kirson, CFA 29 yrs experience

Technology

Cezary Nadecki, CFA 14 yrs experience Utilities, Telecom

Fred Schaefer 25 yrs experience

Product Mgr.

Peter Wen 18 yrs experience

Health Care

Average analyst experience: 21 years

Team

1

Robert Kaynor 19 yrs experience

Consumer

Joanna Wald 12 yrs experience

Consumer

Photo Not Available

Source: Schroders, as at 6 May 2013

David Speyer, CFA 8 yrs experience

Consumer

People – portfolio manager supported by an experienced team

Schroder US Small & Smid Cap Equity

2

Leading our Consumer work; January joiner

Robert Kaynor, CFA Type of Experience

2013 Schroders, Equity Analyst Long-only US equity

2010 Ballast Capital Group, Chief Investment Officer,

Managing Member

Long/short US equity

2003 Ramius Capital Group, Managing Director/Portfolio

Manager, Analyst

Long/short equity; portion of

multi-strategy fund

2000 Barbary Coast Capital Management, Partner/Analyst Long/short US equity

1994 RCM Capital Management, Analyst/Assistant Portfolio

Manager

Long-only US equity

Education: Southern Methodist University, BS

Has held a series of progressively more senior investment roles

Experience with both long-only and long/short investing

19 years of fundamental research and investment experience

Joined US Schroders US Small and Mid Cap in January 2013

Schroder ISF US Small & Mid Cap Equity Portfolio Positioning and Performance Attribution

Performance Pattern

We tend to outperform in flat to modestly rising markets and negative markets

We are less likely to outperform in strongly rising markets, given our emphasis on quality and our tendency to

avoid momentum oriented stocks.

Smid – Clear performance pattern Why diversification of alpha sources is important

Source: Schroders; Monthly observations for the composite, gross of fees, between 31 December 2004 and 31 March 2013.

Market environment: Number of months

Number of months Schroders

outperformed

Percentage of months

outperforming

Strongly rising (index >3% in a month) 35 5 14%

Moderately rising (index between 0 and 3%) 27 14 52%

Falling (Less than 0%) 37 30 80%

4

0

10

20

30

40

50

60

70

Dec-

05

Mar-

06

Jun

-06

Sep-0

6

Dec-

06

Mar-

07

Jun

-07

Sep-0

7

Dec-

07

Mar-

08

Jun

-08

Sep-0

8

Dec-

08

Mar-

09

Jun

-09

Sep-0

9

Dec-

09

Mar-

10

Jun

-10

Sep-1

0

Dec-

10

Mar-

11

Jun

-11

Sep-1

1

Dec-

11

Mar-

12

Jun

-12

Sep-1

2

Dec-

12

Mar-

13

Mispriced Growth Steady Eddie Turnaround

Schroder ISF US Small & Mid Cap Equity Diversified alpha sources – historical allocations (weighted)

36%

58%

6%

Source: Schroders, FactSet as at 30 April 2013.

5

Portfolio vs. index

Schroder US ISF Small & Mid Cap Equity Sector weights – April 30, 2013

6

Source: FactSet as of April 30, 2013. Sector weights for the account and the Benchmark Index are subject to change and should not be viewed as an investment recommendation.

13.311.9

14.8

16.6

10.8

14.2

15.9

25.7

1.5

3.2

9.7

5.3

17.6

10.4

3.0

6.37.7

5.9

0

5

10

15

20

25

30

Te

chn

olo

gy

He

alth

Ca

re

Ma

teri

als

&

Pro

cess

ing

Util

itie

s

En

erg

y

Co

nsu

me

r

Sta

ple

s

Pro

du

cer

Du

rab

les

Co

nsu

me

r

Dis

cre

tion

ary

Fin

an

cia

l

Se

rvic

es

Schroder US SMID Cap Russell 2500

% REITs are 9.2% of the

index

Performance Attribution LUX-SISF SMID vs. Russell 2500

12/31/2012 to 3/28/2013

U.S. Dollar

LUX-SISF SMID Russell 2500 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

Russell Sectors Extended Weight Return To Return Weight Return To Return Effect Interaction Effect

Health Care 11.89 19.68 2.24 10.18 15.51 1.56 0.03 0.43 0.47

Energy 6.38 14.92 0.95 6.20 11.41 0.71 0.02 0.20 0.22

Producer Durables 12.99 16.76 2.17 14.45 14.98 2.13 -0.02 0.21 0.19

Financial Services 16.90 15.57 2.61 25.18 14.16 3.53 -0.10 0.22 0.12

Utilities 3.01 11.84 0.35 5.97 11.66 0.69 0.04 0.01 0.05

Technology 14.27 9.93 1.46 11.29 8.89 1.03 -0.11 0.13 0.02

E T Fs & Futures 1.07 7.06 0.12 -- -- -- -0.00 -- -0.00

Consumer Staples 1.18 12.25 0.13 2.94 17.29 0.50 -0.08 -0.08 -0.16

Materials & Processing 10.10 7.14 0.75 8.12 7.76 0.66 -0.10 -0.09 -0.18

Consumer Discretionary 14.73 10.21 1.55 15.65 12.94 2.03 -0.01 -0.29 -0.31

[Cash] 7.46 0.03 0.00 -- -- -- -0.93 -- -0.93

Total 100.00 12.33 12.33 100.00 12.85 12.85 -1.26 0.74 -0.52

Schroder US ISF Small & Mid Cap Equity Performance attribution - 1Q 2013

Source: Schroders, FactSet., Gross of fees in USD

+ Stock selection adds most value in health care, producer durables and financial services

+ Value added from underweight utilities and overweight health care

– Poor stock selection detracts in materials & processing and consumer discretionary

– Overweight cash and technology detract

7

Schroder US ISF Small & Mid Cap Equity Top and bottom performers - 1Q 2013

8 Source: FactSet, gross of fees in USD. Stock examples are for illustrative purposes only and are not a recommendation to buy or sell

Performance Attribution

LUX-SISF SMID vs. Russell 2500

12/31/2012 to 3/28/2013

U.S. Dollar

LUX-SISF SMID Russell 2500 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

High/Low - Total Effect Weight Return To Return Weight Return To Return Effect Interaction Effect

10 Highest 11.25 31.26 3.19 0.61 32.74 0.18 1.82 -0.13 1.69

Life Technologies Corp. 1.41 31.82 0.46 -- -- -- 0.27 -- 0.27

Alaska Air Group Inc. 0.82 48.43 0.36 0.12 48.43 0.05 0.23 -- 0.23

Spirit Airlines Inc. 0.87 43.03 0.32 0.03 43.03 0.01 0.20 -- 0.20

PAREXEL International Corp. 1.12 33.63 0.34 0.07 33.63 0.02 0.19 -- 0.19

Universal Health Services Inc. Cl B 1.28 32.21 0.38 0.17 32.21 0.05 0.18 -- 0.18

CareFusion Corp. 1.70 22.43 0.36 -- -- -- 0.14 -- 0.14

VeriSign Inc. 1.60 21.77 0.36 -- -- -- 0.14 -- 0.14

Brinker International Inc. 0.74 11.50 0.19 0.08 22.18 0.02 0.12 -- 0.12

Questar Corp. 1.21 24.03 0.27 0.14 24.03 0.03 0.11 -- 0.11

Kansas City Southern 0.50 33.12 0.15 -- -- -- 0.08 -- 0.08

Other 72.26 13.31 9.65 98.54 12.71 12.53 0.04 0.40 0.44

[Cash] 8.49 0.03 0.00 -- -- -- -1.04 -- -1.04

10 Lowest 8.00 -5.88 -0.50 0.85 16.81 0.14 0.45 -2.06 -1.61

Waste Connections Inc. 1.67 6.78 0.15 0.14 6.78 0.01 -0.09 -- -0.09

Amdocs Ltd. 1.64 7.04 0.12 -- -- -- -0.09 -- -0.09

Elizabeth Arden Inc. 0.54 -10.58 -0.06 0.04 -10.58 -0.00 -0.12 -- -0.12

Children's Place Retail Stores Inc. 0.80 1.20 -0.04 0.04 1.20 0.00 -0.13 -- -0.13

Netflix Inc. -- -- -- 0.29 104.43 0.19 -0.16 -- -0.16

Cabot Corp. 0.64 -13.58 -0.10 0.08 -13.58 -0.01 -0.17 -- -0.17

NII Holdings Inc. 0.27 -35.76 -0.16 0.03 -39.34 -0.02 -0.18 -- -0.18

Royal Gold Inc. 0.49 -18.77 -0.15 0.16 -12.49 -0.02 -0.18 -- -0.18

Yamana Gold Inc. 0.88 -10.42 -0.12 -- -- -- -0.24 -- -0.24

Life Time Fitness Inc. 1.07 -13.07 -0.13 0.07 -13.07 -0.01 -0.25 -- -0.25

Total 100.00 12.33 12.33 100.00 12.85 12.85 1.27 -1.79 -0.52

Performance Attribution LUX-SISF SMID vs. Russell 2500

12/31/2012 to 4/30/2013

U.S. Dollar

LUX-SISF SMID Russell 2500 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

Russell Sectors Extended Weight Return To Return Weight Return To Return Effect Interaction Effect

Health Care 11.86 22.33 2.50 10.24 16.68 1.68 0.04 0.56 0.60

Producer Durables 14.15 15.83 2.21 14.52 11.78 1.73 -0.01 0.52 0.50

Consumer Discretionary 14.33 16.37 2.34 15.54 16.89 2.57 -0.00 0.03 0.02

Energy 6.24 8.05 0.51 6.14 7.82 0.51 0.01 -0.00 0.01

E T Fs & Futures 0.79 7.06 0.12 -- -- -- -0.00 -- -0.00

Utilities 3.02 17.49 0.51 6.04 17.46 1.02 -0.11 0.01 -0.10

Technology 14.04 7.21 1.05 11.17 6.73 0.80 -0.19 0.06 -0.13

Consumer Staples 1.22 14.07 0.16 2.97 19.79 0.57 -0.11 -0.08 -0.19

Financial Services 17.09 14.64 2.47 25.34 15.58 3.87 -0.17 -0.15 -0.32

Materials & Processing 9.97 3.14 0.41 8.04 4.92 0.45 -0.14 -0.20 -0.34

[Cash] 7.29 0.03 0.00 -- -- -- -0.95 -- -0.95

Total 100.00 12.29 12.29 100.00 13.20 13.20 -1.65 0.74 -0.91

Schroder US ISF Small & Mid Cap Equity Performance attribution – YTD to 30 April 2013

Source: Schroders, FactSet., Gross of fees in USD

+ Stock selection adds most value in health care and producer durables

+ Value added from overweight health care and energy

– Poor stock selection detracts in materials & processing and financial services

– Overweight cash and technology detract

9

Schroder US ISF Small & Mid Cap Equity Top and bottom performers - YTD to 30 April 2013

10

Source: FactSet, gross of fees in USD. Stock examples are for illustrative purposes only and are not a recommendation to buy or sell

Performance Attribution

LUX-SISF SMID vs. Russell 2500

12/31/2012 to 4/30/2013

U.S. Dollar

LUX-SISF SMID Russell 2500 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

High/Low - Total Effect Weight Return To Return Weight Return To Return Effect Interaction Effect

10 Highest 11.91 35.84 3.78 0.76 36.69 0.25 2.20 -0.11 2.10

Life Technologies Corp. 1.36 50.30 0.61 -- -- -- 0.40 -- 0.40

Spirit Airlines Inc. 0.85 50.59 0.36 0.03 50.59 0.01 0.24 -- 0.24

Universal Health Services Inc. Cl B 1.29 37.84 0.44 0.17 37.84 0.06 0.23 -- 0.23

PAREXEL International Corp. 1.17 38.39 0.39 0.07 38.39 0.02 0.23 -- 0.23

Ross Stores Inc. 1.91 22.50 0.47 -- -- -- 0.20 -- 0.20

Alaska Air Group Inc. 0.88 43.05 0.32 0.13 43.05 0.05 0.20 -- 0.20

Brinker International Inc. 0.95 15.20 0.24 0.08 26.24 0.02 0.16 -- 0.16

Questar Corp. 1.25 29.43 0.33 0.14 29.43 0.04 0.15 -- 0.15

Hanesbrands Inc. 0.80 40.03 0.29 0.13 40.03 0.05 0.15 -- 0.15

VeriSign Inc. 1.46 18.68 0.32 -- -- -- 0.12 -- 0.12

Other 72.50 12.59 9.10 98.30 12.97 12.77 0.06 -0.29 -0.23

[Cash] 8.05 0.03 0.00 -- -- -- -1.06 -- -1.06

10 Lowest 7.54 -6.24 -0.59 0.95 20.39 0.19 0.48 -2.20 -1.72

Elizabeth Arden Inc. 0.54 -9.02 -0.05 0.03 -9.02 -0.00 -0.12 -- -0.12

Arrow Electronics Inc. 1.21 3.02 0.04 0.14 3.02 0.00 -0.12 -- -0.12

Amdocs Ltd. 1.58 5.41 0.09 -- -- -- -0.12 -- -0.12

Dresser-Rand Group Inc. 1.17 -2.19 -0.01 0.15 -0.94 -0.00 -0.13 -- -0.13

Cabot Corp. 0.60 -5.09 -0.05 0.08 -5.09 -0.00 -0.13 -- -0.13

Royal Gold Inc. 0.36 -18.77 -0.15 0.15 -31.31 -0.06 -0.15 -- -0.15

Life Time Fitness Inc. 1.09 -6.16 -0.04 0.06 -6.16 -0.00 -0.17 -- -0.17

NII Holdings Inc. 0.20 -35.76 -0.16 0.03 22.02 0.01 -0.20 -- -0.20

Netflix Inc. -- -- -- 0.30 133.36 0.24 -0.21 -- -0.21

Yamana Gold Inc. 0.81 -28.22 -0.26 -- -- -- -0.38 -- -0.38

Total 100.00 12.29 12.29 100.00 13.20 13.20 1.68 -2.59 -0.91

Schroder ISF US Small & Mid Cap Equity Performance – Net of fees

11

Periods ending 31 March 2013 (%) (Periods greater than one year are annualized)

Source: Schroders. ‘C‘ Class shares, net of fees in USD; index lagged.

Source: Schroders. ‘C’ Class shares, net of fees in USD; index lagged

Calendar year performance (%)

2012 2011 2010 2009 2008 2007 2006

SISF US Small & Mid Cap 9.1 -2.4 17.0 36.7 -34.4 12.0 16.3

Russell 2500 15.2 -2.6 25.9 40.0 -38.9 1.2 16.2

Outperformance -6.2 +0.2 -8.9 -3.3 +4.5 +10.8 +0.1

1Q13 1 Year 3 Years 5 Years Since incept.

SISF US Small & Mid Cap 12.2 10.7 10.3 6.9 8.1

Russell 2500 14.5 17.2 14.2 9.1 7.6

Outperformance -2.3 -6.5 -3.9 -2.2 +0.5

Source: Schroders. Performance shown is past performance. Past performance is not necessarily a guide to future performance. The value of investments can go down as well as up and is not guaranteed. Please see the important composite disclosures at end of presentation.

Schroder ISF US Small Cap Equity Portfolio Positioning and Performance Attribution

Performance pattern

We tend to outperform in flat to modestly rising markets and negative markets

We are less likely to outperform in strongly rising markets, given our emphasis on quality and our tendency to

avoid momentum oriented stocks.

Small – Clear performance pattern Why diversification of alpha sources is important

Source: Schroders; Monthly observations for the composite between 31 January 2003 and 31 March 2013.

Market environment: Number of months

Number of months Schroders

outperformed

Percentage of months

outperforming

Strongly rising (index >3% in a month) 47 8 17%

Moderately rising (index between 0 and 3%) 31 17 55%

Falling (less than 0%) 45 40 89%

13

Schroder ISF US Smaller Companies Fund Diversified alpha sources – historical allocations

Source: Schroders, FactSet as at 30 April 2013

64%

30%

6%

14

0

10

20

30

40

50

60

70

80

Ja

n-0

9

Apr-0

9

Ju

l-09

Oct-0

9

Ja

n-1

0

Apr-1

0

Ju

l-10

Oct-1

0

Ja

n-1

1

Apr-1

1

Ju

l-11

Oct-1

1

Ja

n-1

2

Apr-1

2

Ju

l-12

Oct-1

2

Ja

n-1

3

Apr-1

3

Mispriced Growth Steady Eddies Turnarounds

Portfolio vs. index

Schroder ISF US Smaller Companies Sector weights – April 30, 2013

15

Source: FactSet as of April 30, 2013. Sector weights are based on a Schroder ISF US Smaller Companies Fund

Sector weights for the account and the Benchmark Index are subject to change and should not be viewed as an investment recommendation.

10.8 11.3

18.5

15.4

13.1 13.4

15.3

25.0

3.54.9

8.7

4.4

16.4

12.8

3.24.3

7.25.8

0

5

10

15

20

25

30

Te

chn

olo

gy

He

alth

Ca

re

Ma

teri

als

&

Pro

cess

ing

Util

itie

s

En

erg

y

Co

nsu

me

r

Sta

ple

s

Pro

du

cer

Du

rab

les

Co

nsu

me

r

Dis

cre

tion

ary

Fin

an

cia

l

Se

rvic

es

Schroder ISF US Smaller Companies Russell 2000

% REITs are 8.8% of the

index

Performance Attribution LUX-SISF Small vs. Russell 2000

12/31/2012 to 3/28/2013

U.S. Dollar

LUX-SISF Small Russell 2000 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

Russell Sectors Extended Weight Return To Return Weight Return To Return Effect Interaction Effect

Producer Durables 17.70 15.76 2.70 13.85 14.35 1.95 0.08 0.21 0.29

Financial Services 15.04 15.61 2.25 24.36 13.35 3.23 -0.07 0.30 0.24

Utilities 4.54 15.39 0.68 4.12 9.59 0.40 -0.01 0.24 0.23

Consumer Discretionary 14.64 12.91 1.87 14.91 12.62 1.88 0.01 0.04 0.05

Consumer Staples 2.56 12.98 0.33 3.08 12.25 0.37 0.01 0.02 0.02

Energy 4.92 11.82 0.58 5.91 11.60 0.69 0.02 -0.01 0.01

E T Fs & Futures 1.46 11.69 0.22 -- -- -- 0.00 -- 0.00

Health Care 11.51 14.85 1.68 12.51 14.74 1.83 -0.02 0.00 -0.02

Materials & Processing 9.11 6.41 0.61 7.54 8.47 0.66 -0.06 -0.20 -0.26

Technology 11.47 5.78 0.68 13.72 9.84 1.38 0.05 -0.46 -0.41

[Cash] 7.05 0.02 0.00 -- -- -- -0.95 -- -0.95

Total 100.00 11.60 11.60 100.00 12.39 12.39 -0.95 0.15 -0.80

Schroder ISF US Smaller Companies Performance attribution - 1Q 2013

Source: Schroders, FactSet., Gross of fees in USD

+ Stock selection adds most value in producer durables, financial services and utilities

+ Value added from underweight technology and overweight producer durables

– Poor stock selection detracts in technology and materials & processing

– Overweight cash and underweight financial services detract

16

Schroder ISF US Smaller Companies Top and bottom performers - 1Q 2013

Source: FactSet, gross of fees in USD.

17

Performance Attribution

LUX-SISF Small vs. Russell 2000

12/31/2012 to 3/28/2013

U.S. Dollar

LUX-SISF Small Russell 2000 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

High/Low - Total Effect Weight Return To Return Weight Return To Return Effect Interaction Effect

10 Highest 7.39 41.11 2.57 0.66 38.76 0.22 1.45 0.13 1.58

PAREXEL International Corp. 1.56 33.63 0.47 0.16 33.63 0.05 0.25 -- 0.25

Fifth & Pacific Companies Inc 0.74 51.65 0.35 0.14 51.65 0.06 0.21 -- 0.21

Spirit Airlines Inc. 0.83 43.03 0.32 0.07 43.03 0.03 0.20 -- 0.20

Redwood Trust Inc. 0.90 38.92 0.31 0.12 38.92 0.04 0.17 -- 0.17

Brown & Brown Inc. 1.24 26.26 0.29 -- -- -- 0.15 -- 0.15

Primoris Services Corp. 0.56 47.21 0.22 0.04 47.21 0.02 0.14 -- 0.14

HFF Inc. Cl A 0.66 33.76 0.20 0.04 33.76 0.01 0.12 -- 0.12

EnPro Industries Inc. 1.06 25.11 0.25 0.07 25.11 0.02 0.11 -- 0.11

Brinker International Inc. 0.61 11.50 0.16 -- -- -- 0.11 -- 0.11

NYF-ICE RUSSELL 2000 MINI -0.78 -- -- -- -- -- 0.11 -- 0.11

Other 79.23 12.27 9.65 98.76 12.20 12.07 0.04 0.02 0.05

[Cash] 7.95 0.02 0.00 -- -- -- -1.07 -- -1.07

10 Lowest 5.42 -10.78 -0.63 0.58 17.93 0.10 0.20 -1.56 -1.36

Alaska Air Group Inc. -- -- -- 0.28 48.43 0.12 -0.08 -- -0.08

Group 1 Automotive Inc. 0.70 -2.84 -0.02 0.11 -2.84 -0.00 -0.09 -- -0.09

ScanSource Inc. 0.46 -11.17 -0.05 0.07 -11.17 -0.01 -0.09 -- -0.09

Fairchild Semiconductor

International Inc. 0.70 -1.81 -0.01 -- -- -- -0.10 -- -0.10

NetScout Systems Inc. 0.63 -5.46 -0.04 0.07 -5.46 -0.00 -0.10 -- -0.10

Laredo Petroleum Holdings Inc. 0.77 0.72 -0.00 -- -- -- -0.10 -- -0.10

PetroQuest Energy Inc. 0.32 -14.95 -0.08 0.02 -10.30 -0.00 -0.12 -- -0.12

Cabot Corp. 0.49 -13.58 -0.07 -- -- -- -0.14 -- -0.14

Standard Parking Corp. 0.78 -5.87 -0.05 0.03 -5.87 -0.00 -0.15 -- -0.15

Pretium Resources Inc 0.57 -40.05 -0.30 -- -- -- -0.38 -- -0.38

Total 100.00 11.60 11.60 100.00 12.39 12.39 0.61 -1.41 -0.80

Performance Attribution LUX-SISF Small vs. Russell 2000

12/31/2012 to 4/30/2013

U.S. Dollar

LUX-SISF Small Russell 2000 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

Russell Sectors Extended Weight Return To Return Weight Return To Return Effect Interaction Effect

Producer Durables 17.79 14.93 2.56 13.74 10.66 1.48 -0.05 0.68 0.63

Utilities 4.60 20.90 0.91 4.15 14.87 0.60 0.01 0.24 0.26

Consumer Discretionary 14.83 16.77 2.37 14.94 15.46 2.25 0.02 0.16 0.19

Financial Services 15.32 15.77 2.28 24.55 13.76 3.32 -0.13 0.26 0.13

Consumer Staples 2.76 15.55 0.41 3.10 15.36 0.47 0.02 -0.00 0.01

E T Fs & Futures 1.07 11.69 0.22 -- -- -- 0.01 -- 0.01

Energy 4.84 8.15 0.42 5.88 9.13 0.55 0.04 -0.06 -0.02

Materials & Processing 9.05 4.78 0.51 7.46 4.13 0.36 -0.10 0.03 -0.07

Health Care 11.49 14.99 1.68 12.60 16.01 1.98 -0.03 -0.11 -0.15

Technology 11.33 1.24 0.15 13.57 6.73 0.97 0.11 -0.62 -0.51

[Cash] 6.91 0.02 0.00 -- -- -- -0.93 -- -0.93

Total 100.00 11.53 11.53 100.00 11.98 11.98 -1.04 0.58 -0.45

Schroder ISF US Smaller Companies Performance attribution – YTD to 30 April 2013

Source: Schroders, FactSet., Gross of fees in USD

+ Stock selection adds most value in producer durables, financial services and utilities

+ Value added from underweight technology and energy

– Poor stock selection detracts in technology and health care

– Overweight cash and underweight financial services detract

18

Schroder ISF US Smaller Companies Top and bottom performers – YTD to 30 April 2013

Source: FactSet, gross of fees in USD.

19

Performance Attribution

LUX-SISF Small vs. Russell 2000

12/31/2012 to 3/28/2013

U.S. Dollar

LUX-SISF Small Russell 2000 Attribution Analysis

Average Total Contribution Average Total Contribution Allocation Selection + Total

High/Low - Total Effect Weight Return To Return Weight Return To Return Effect Interaction Effect

10 Highest 7.39 41.11 2.57 0.66 38.76 0.22 1.45 0.13 1.58

PAREXEL International Corp. 1.56 33.63 0.47 0.16 33.63 0.05 0.25 -- 0.25

Fifth & Pacific Companies Inc 0.74 51.65 0.35 0.14 51.65 0.06 0.21 -- 0.21

Spirit Airlines Inc. 0.83 43.03 0.32 0.07 43.03 0.03 0.20 -- 0.20

Redwood Trust Inc. 0.90 38.92 0.31 0.12 38.92 0.04 0.17 -- 0.17

Brown & Brown Inc. 1.24 26.26 0.29 -- -- -- 0.15 -- 0.15

Primoris Services Corp. 0.56 47.21 0.22 0.04 47.21 0.02 0.14 -- 0.14

HFF Inc. Cl A 0.66 33.76 0.20 0.04 33.76 0.01 0.12 -- 0.12

EnPro Industries Inc. 1.06 25.11 0.25 0.07 25.11 0.02 0.11 -- 0.11

Brinker International Inc. 0.61 11.50 0.16 -- -- -- 0.11 -- 0.11

NYF-ICE RUSSELL 2000 MINI -0.78 -- -- -- -- -- 0.11 -- 0.11

Other 79.23 12.27 9.65 98.76 12.20 12.07 0.04 0.02 0.05

[Cash] 7.95 0.02 0.00 -- -- -- -1.07 -- -1.07

10 Lowest 5.42 -10.78 -0.63 0.58 17.93 0.10 0.20 -1.56 -1.36

Alaska Air Group Inc. -- -- -- 0.28 48.43 0.12 -0.08 -- -0.08

Group 1 Automotive Inc. 0.70 -2.84 -0.02 0.11 -2.84 -0.00 -0.09 -- -0.09

ScanSource Inc. 0.46 -11.17 -0.05 0.07 -11.17 -0.01 -0.09 -- -0.09

Fairchild Semiconductor

International Inc. 0.70 -1.81 -0.01 -- -- -- -0.10 -- -0.10

NetScout Systems Inc. 0.63 -5.46 -0.04 0.07 -5.46 -0.00 -0.10 -- -0.10

Laredo Petroleum Holdings Inc. 0.77 0.72 -0.00 -- -- -- -0.10 -- -0.10

PetroQuest Energy Inc. 0.32 -14.95 -0.08 0.02 -10.30 -0.00 -0.12 -- -0.12

Cabot Corp. 0.49 -13.58 -0.07 -- -- -- -0.14 -- -0.14

Standard Parking Corp. 0.78 -5.87 -0.05 0.03 -5.87 -0.00 -0.15 -- -0.15

Pretium Resources Inc 0.57 -40.05 -0.30 -- -- -- -0.38 -- -0.38

Total 100.00 11.60 11.60 100.00 12.39 12.39 0.61 -1.41 -0.80

Schroder ISF US Smaller Companies Performance

Periods ending 31 March 2013 (%) (Periods greater than one year are annualized)

Source: Schroders. ‘C’ Class shares, net of fees in USD.

Annual periods (%) Calendar years

2012 2011 2010 2009 2008 2007 2006

Schroder ISF US Smaller

Companies 11.2 -4.8 20.0 36.6 -35.0 10.3 21.3

Russell 2000 13.4 -4.4 26.2 33.3 -36.5 -1.7 18.6

Outperformance -2.2 -0.4 -6.2 +3.3 +1.5 +12.0 +2.7

1Q 2013 1 Year 3 Years 5 Years Since incept.

Schroder ISF US Smaller Companies 12.0 14.0 10.8 6.9 13.6

Russell 2000 14.6 15.9 13.1 8.4 9.0

Outperformance -2.6 -1.9 -2.3 -1.5 +4.6

Source: Schroders. ‘C’ Class shares, net of fees in USD; index lagged.

20

Schroder US Small & Smid Cap Equity Berry Plastics – a recent addition

Key elements:

• History as private company

• Recent IPO; private equity

firm (Apollo) retains a stake

• Strong management team

• Solid experience and record

• Recurring revenue stream

• Growth potential

misunderstood by market

• Rising margins and ROIC

• Management of input costs

• Exciting new products

• Value added packaging, at

lower costs to end market

21

Berry Plastics Corporation is a leading global producer of “value

added” consumer packaging and engineered materials, with a

broad range of products for food & beverage, health care,

household, retail, personal care and industrial end markets

Consumer Ideas

Schroder US Small & Smid Cap Equity Consumer Framework

• General principle: Invest in stocks with multiple ways to win

• Understand opportunities for margin improvement, operational leverage

• Unsustainable value (catalysts)

• Current approach: Who are beneficiaries of the US recovery?

• Asset relation favors homeowners, 401k holders et al.

• Housing recovery related stocks

• Auto industry beneficiaries of inflection points

23

Company Business

Brinker Casual dining restaurant company; owns, operates

and franchises Chili’s Bar and Grill and Maggiano’s

Little Italy restaurant brands

Fortune Brands &

Home Security

Manufactures home and security products.

Plumbing accessories, windows, doors, cabinets

and security devices and systems.

Dean Foods Full line of dairy and dairy related products. Fresh

Dairy unit distributes branded and private label dairy

products to retailers. WhiteWave manufactures and

sells plant based foods and beverages

KAR Auction Services Vehicle auction services in North America. It offers

auction services for sellers of used or whole car

vehicles and salvage vehicles.

Consumer Example holdings

Source: FactSet; company annual reports

24

Health Care Change is in the Air

25

Health Care – impact of “Obamacare” ACA creates a significant increase in the insured population

Source: Kaiser Family Foundation, “The Uninsured, A Primer” October 2012

• 30 million people (estimated) will be added to the pool of insured

• This represents an enormous opportunity for health care companies

26

56%

17%

18%

9%

58%

10%

12%

20%

0% 10% 20% 30% 40% 50% 60% 70%

Employer sponsored insurance

Private non-group insurance

Medicaid

Uninsured

Health Insurance Coverage: pre- and post-ACA implementation Percentage of non-elderly population

2011 2016 (est)

Schroder US Small & Smid Cap Equity Health Care Ideas

• Opportunities created by the Affordable Care Act (ACA or “Obamacare”)

• Beneficiaries of new demand/volume generated by an increase in the

insured population

• Value creation through reducing health care cost

• Reduction of waste and error; detection of fraud/abuse

• Impact of Moore’s law (exponential increases in computing power)

• Ability to innovate product at lower cost with better performance

• Recurring revenue models with economies of scale

• Consumable products with high frequency of usage

27

Health Care Example holdings

Source: FactSet; company annual reports

28

Company Business

CareFusion Hospital supply company, focusing on medical drug

dispensing, IV pumps, respiratory equipment and

infection control.

• Benefits from increased healthcare usage (ACA)

• Also helps clients (hospitals) to be more efficient

and save money

Life Technologies Global life sciences and biotechnology company. A

leader in genome sequencing devices.

• Genome sequencing has become faster and

cheaper (Moore’s law)

• Company has been object of a bidding war;

Thermo Fisher Scientific

United Health

Services

Owner and operator of hospitals and behavioral health

centers.

• Beneficiary of ACA – expansion of insured

population and behavioral health services

Market Environment

Schroder US Small & Smid Cap Equity Market environment: summary

• Strong quarter for US equities

• Global concerns (Cyprus, Italy) have no impact

• Valuations rising

• Highest beta stocks lagged

• Strongest sectors:

• Consumer staples: +17.3%

• Health Care: +15.5%

30

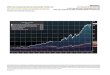

Schroder US Small & Smid Cap Equity Market environment: US Equity markets surge

Source: Schroders, FactSet as at 31 March 2013.

31

• Strength in the US Equity markets

• Russell 2500 and S&P 500 reach all time highs during Q1

• Large advance from mid-November until end of March

Russell 2500 S&P 500

1Q 2013 2Q 2012 2Q 2012 3Q 2012 3Q 2012 4Q 2012 4Q 2012 1Q 2013

Schroder US Small & Smid Cap Equity Market environment: Low rates, falling gold price, strong dollar

Source: Schroders, FactSet as at 31 March 2013.

32

• Interest rates have remained quite low

• Gold declining since October

• Strengthening USD (not shown)

10-year US Treasury yield Gold – spot price

5.0

10.0

15.0

20.0

25.0

1Q79 1Q83 1Q87 1Q91 1Q95 1Q99 1Q03 1Q07 1Q11

Absolute Trailing P/E*

.

33

Russell 2500 valuations ticking up Still near long-term average on forecast earnings

Source: Bank of America Merrill Lynch. Data to 31 March 2013. *P/E excludes negative earnings

Lehman Crash of ‘87

Internet Bubble

5.0

10.0

15.0

20.0

25.0

30.0

1Q79 1Q83 1Q87 1Q91 1Q95 1Q99 1Q03 1Q07 1Q11

Absolute Forecast P/E

0.5

0.7

0.9

1.1

1.3

1.5

1Q79 1Q83 1Q87 1Q91 1Q95 1Q99 1Q03 1Q07 1Q11

Relative Forecast P/E

0.5

0.8

1.1

1.4

1.7

1Q79 1Q83 1Q87 1Q91 1Q95 1Q99 1Q03 1Q07 1Q11

Relative Trailing P/E*

34

Relative valuations modestly favor Large Cap On trailing and forecast earnings

Source: Bank of America Merrill Lynch. Data to 31 March 2013. *P/E excludes negative earnings

Russell 2500 vs. Russell 1000 Valuations

Smid Caps Expensive

Smid Caps Cheap

Smid Caps Cheap

Smid Caps Expensive

Appendix

35

Market Liquidity Volume has decreased by 47% in 5 years

Source: FactSet, NYSE

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

Jan-0

7

Apr-

07

Jul-

07

Oct-

07

Jan-0

8

Apr-

08

Ju

l-0

8

Oct-

08

Jan-0

9

Apr-

09

Jul-

09

Oct-

09

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

NYSE Volume has declined by 47% between 2007 and 2012

Average monthly volume Linear (Average monthly volume)

Team biographies

37

Jenny B. Jones – Portfolio Manager

2002 Schroders, Head of US Small & SMID Cap Equity

1996 Morgan Stanley Investment Management, Portfolio Manager

1990 Oppenheimer Capital LP, Head of Small Cap Value Department

1983 Mutual of America Life Insurance Co., Portfolio Manager, Investment Department

1982 Shearson/American Express, Institutional Options Sales, Financial Consultant

1980 Drexel Burnham, Sales Liaison/Assistant Options Strategist

New York University, MBA

Yale University, BA (honors)

33 years of investment experience

10 years with Schroders

Experienced portfolio manager

Team biographies

38

US Small & Mid Cap Equity Analysts

Robert Kaynor, CFA – Analyst

2013 Schroders, Equity Analyst

2010 Ballast Capital Management, Managing Member, Chief Investment Officer

2003 Ramius Capital Group, Managing Director/Portfolio Manager, Analyst

2000 Barbary Coast Capital Management, Partner/Analyst

1994 RCM Capital Management, Analyst/Assistant Portfolio Manager

Southern Methodist University, BS

19 years of fundamental equity research and investment experience

<1 year with Schroders

Robert F. Starbuck – Head of US Small and SMID Cap Research

2003 Schroders, Director of US Small & SMID Cap Research

2000 Bramwell Capital Management, Senior Vice President, Investment Research

1997 Equinox Capital Management, Senior Vice President, Investment Research

1992 The Bank of New York, Vice President, Investment Research

1984 Axe Houghton Management, Research Analyst and Portfolio Manager

1978 General American Investors, Research Analyst

1977 The Bank of New York, Assistant Vice President, Investment Research

1974 General Foods Corporation, Senior Financial Analyst and Accounting Supervisor

Columbia University, MBA, BA

35 years of investment experience

10 years with Schroders

Team biographies

39

US Small & Mid Cap Equity Analysts

John Helfst – Analyst

2005 Schroders, Equity Analyst

2003 Endeavour Capital Advisers, Hedge Fund, Equity Analyst

1999 SalomonSmithBarney, Equity Research Associate

1998 PaineWebber & Co., CMBS Underwriter

1994 PNC Bank, Credit Analyst and Real Estate Lender

New York University, MBA

Colgate University, BA

18 years of fundamental equity research and credit analysis experience

8 years with Schroders

Steven Kirson, CFA – Analyst

2005 Schroders, Equity Analyst

2002 Astral Securities Research, LLC, Founder/ Research Analyst

1989 Putnam Investments, Analyst/Portfolio Manager

1984 Equitable Bank, N.A., Credit Analyst

University of Pennsylvania, MBA

University of Miami, FL, BA

29 years of investment experience

8 years with Schroders

Team biographies US Small & Mid Cap Equity Analysts

40

Cezary Nadecki, CFA – Analyst

2004 Schroders, Equity Analyst

2002 FactSet Research Inc, Senior Consultant

2001 General Re, Statutory Filing Coordinator

1999 Eli Lilly, Financial Business Manager, Warsaw, Poland

1997 Charles Schwab, Registered Trading Representative

Thunderbird, American Graduate School of International Management, MIM

Arizona State University, MBA

University of Arizona, BS

15 years of investment experience

9 years with Schroders

Peter Wen, CFA – Analyst

2010 Schroders, Equity Analyst

2004 Director and Health Care Sector Analyst, Angelo Gordon Asset Management

1999 Warburg Pincus Global Health Sciences Fund, Analyst/Portfolio Manager

1994 Lynch & Mayer, Health Care Research Analyst

University of Pennsylvania, MBA

Harvard University, BA

18 years of investment experience

3 years with Schroders

Team biographies US Small & Mid Cap Equity Analysts

41

David Speyer, CFA – Analyst 2013 Schroders, Junior Equity Analyst

2009 Schroders, Fund Management Assistant – U.S. Small & Mid Cap Equities

2007 J.P. Morgan Asset Management, Analyst - Client Portfolio Management

2005 Merrill Lynch, Registered Client Associate – Global Private Client

Indiana University, BS

8 years of investment experience

4 years with Schroders

Joanna Wald – Analyst 2013 Schroders, Equity Analyst

2010 Ballast Capital Management, Equity Analyst

2008 Ramius Capital Group – Equity Analyst

2006 Trivium Capital Management – Senior Analyst

2001 Century Capital Analyst – Equity Analyst

1999 Liberty Mutual Insurance Company, Financial Analyst

1998 Ernst & Young LLP, Actuarial Analyst

University of Pennsylvania, MBA

Boston University, BA

12 years of investment experience

<1 year with Schroders

Photo Not

Available

Team biographies Product Management

Frederick Schaefer – Client Portfolio Manager

2007 Schroders, Client Portfolio Manager

1987 Evaluation Associates, Senior Consultant and Principal

1979 Greenwich Associates, Research Manager

BA, University of Notre Dame

26 years of investment experience

6 years with Schroders

Sarah Bratton – Product Executive

2011 Schroders, Product Executive

2010 JP Morgan Asset Management , Senior Analyst Investment Performance

2007 JP Morgan Chase, Associate – Client Service

BA, BS, St. Francis College

6 years of investment experience

2 year with Schroders

42

Philosophically, we believe in:

Schroder US Small & Mid Cap Equity Philosophy

43

Bottom-up, fundamental research – creates an

information edge

Flexibility across sources of alpha -

creates an attractive

risk/return profile

Entry price/valuation

matters – overpaying

detracts from return potential

Understanding your risks –

what you don’t know can hurt

you

Understand the business model

Is it sustainable?

What is the size of the addressable market?

Barriers to entry? Competitive advantages?

Scrutinise the financials

Special attention paid to cash flows and balance sheets

Analyse valuations; calculate target price

Must use two separate methodologies to derive target price

Business model

Financials Valuations

Ideas

Approach

44

Information sources:

Meetings with management

What are their plans?

Good steward of capital?

What does it take to succeed in the industry?

Financial statements

Cash flow and balance sheet analysis important

Discussion with competitors, customers

Talk to sell side analysts:

Understand the industry

Find the negative case

Schroder US Small & Smid Cap Equity Building the mosaic

45

Leveragability of Business

Model

Barriers to Entry

Sales/Earnings Growth Patterns

Management Quality

Competitive Advantage

Cash Flow

Dynamics

Goal: Understand company

and the business model

Initial

research

Portfolio

holding

In-depth

research

Ongoing

inquiry

Schroder US Small & Smid Cap Equity Research-driven process

Idea generation Deep fundamental research Final stock selection

Sources of new ideas:

― Analyst generates new idea

― Brief write-up with supporting materials

― Reviewed by Fund Manager or Research

Director

― Key question: does this stock have a

reasonable chance of getting into the portfolio?

― If yes, proceed with full analysis

Thorough fundamental analysis of:

― Business model

― Cash flows and financials

― Management track record

― Competitors

― Other relevant factors

― Valuation and Target price

Portfolio manager decides:

— Buy, don’t buy or defer

— Position sizing

Source: Schroders,*Represents general market cap but is subject to change

46

Viable Candidate?

No

Yes

Buy?

No

Ideas Bin

Discard

Yes

Distinguishing characteristics

Mispriced growth (50-60% of portfolio)

Companies experiencing a period of growth due to industry or company factors

Resulting in solid growth in top and bottom lines

Price understates: sales growth OR incremental margin growth OR rising cash flow return on investment

Tend to lead our portfolio in rising markets as investors seek growth opportunities

Steady eddies (20-50% of portfolio)

Companies with stable growth characteristics

Low variability in revenue/earnings; consistency in meeting earnings expectations

Strong free cash flow, good balance sheet

Provide the ‘ballast’ for difficult markets as investors seek consistency

Turnarounds (0-20% of portfolio)

Companies whose growth engine has broken. This can be due to an accounting, management or product issue

Catalysts in place with evidence that growth is returning

Riskiest category, outperformance is driven by specific risk

Diversified sources of alpha

47

Single period correlations: January 2006 – March 2013

Competitive advantage

Mispriced growth Steady eddie Turnaround

Mispriced growth 1.00

Steady eddie -0.12 1.00

Turnaround -0.04 -0.39 1.00

Source: FactSet, Schroders

Correlations are based on historical performance. Past performance is not necessarily a guide to future performance. The value of investments can go down as well as up and is not

guaranteed. Based on the US Smid Composite

Proof statement: our alpha sources deliver returns at different times

48

Performance pattern: truncating the return distribution Diversification of alpha sources creates a lower risk portfolio

49

We truncate the left (negative) tail

By giving up a portion of the right tail

This trade-off is valuable - consider the nature of compounding:

In an extreme case if your portfolio declines 50% you need a 100% return to be made whole

Managing the downside is important for the long-run compounding of wealth

Schroder ISF US Small & Mid Cap Equity Top ten holdings– 30 April 2013

Source: FactSet. Securities mentioned are for illustrative purposes only and should not be viewed as a recommendation to buy/sell. Please note that portfolio holdings can change at any time. Holdings may vary between accounts with in the same strategy.

Company Description % of Fund

Ross Stores Inc. Off-price retail apparel and home fashion stores 2.0

Gardner Denver Inc. Designs, manufactures, and markets engineered industrial machinery and related parts 1.7

Apartment Investment &

Management Co. A REIT concentrated on multi-family housing 1.7

Sealed Air Corp. Engaged in food safety and security, facility hygiene and product protection business 1.7

CareFusion Corp. Global medical technology company 1.6

Denbury Resources Inc. An independent oil and natural gas company 1.6

Vantiv Inc Provider of electronic payment processing services 1.6

Brinker International Inc. Owns, develops, operates, and franchises the Chili’s Grill & bar and Maggiano’s restaurant

brands 1.6

PartnerRe Ltd. International reinsurance holding company 1.6

Crown Holdings, Inc. Manufacturer of packaging products for consumer goods 1.5

Total 16.6

50

Schroder ISF US Small Cap Equity Top ten holdings– 30 April 2013

Source: FactSet. Securities mentioned are for illustrative purposes only and should not be viewed as a recommendation to buy/sell. Please note that portfolio holdings can change at any time. Holdings may vary between accounts with in the same strategy.

Company Description % of Fund

NorthWestern Corp. Electricity and natural gas distributor 1.9

Finish Line Inc. Cl A Retailer of athletic shoes, apparel and accessories 1.5

Brinker International Inc. Owns, develops, operates, and franchises the Chili’s Grill & bar and Maggiano’s restaurant

brands 1.5

PTC Inc. Develops and sells product lifecycle management software 1.4

PAREXEL International Corp. Biopharmaceutical services company 1.4

Alterra Capital Holdings Ltd. Insurance holding company 1.4

Applied Industrial

Technologies Inc. North American industrial distributor 1.3

Brown & Brown Inc. Diversified insurance agency 1.3

Cleco Corp. Public utility holding company 1.2

EnerSys Inc. Manufacturer, marketer, and distributor of industrial batteries 1.2

Total 14.1

51

Schroder ISF US Small & Mid Cap Equity Characteristics

Source: Schroders, Bank of New York Mellon as of March 31, 2013..

*Based on composite data.

Portfolio holdings characteristics, except where otherwise indicated, are based on Representative account or the Benchmark Index, and are shown as of March 31, 2013. Tracking error,

Information ratio and Sharpe ratio are based on the composite. Performance shown is past performance. Past performance is not necessarily a guide to future performance. The value of

investments can go down as well as up and is not guaranteed. Please see the important composite disclosures at end of presentation.

Schroders US SMID Cap Equity Russell 2500

Market cap – Weighted median ($bn) 5.1 3.4

Market cap range $819 million – 17.6 billion $24 million – 11.1 billion

P/E (excluding neg. earnings) 16.8x 18.7x

P/B 2.3x 2.1x

Dividend Yield 1.1% 1.4%

1 Year Forecast Growth (I/B/E/S Medians) 9.6% 10.9%

% in top 10 stocks 16.5% 3.0%

Beta* 0.81 1.00

Tracking error (actual, 5yrs)* 5.72 --

Information ratio (5yrs)* -0.13 --

Sharpe ratio (5yrs)* 0.41 --

52

Schroder ISF US Smaller Companies Characteristics

Source: Schroders, Bank of New York Mellon as of March 31, 2013.

*Based on composite data.

Portfolio holdings characteristics, except where otherwise indicated, are based on Representative account or the Benchmark Index, and are shown as of March 31, 2013. Tracking error,

Information ratio and Sharpe ratio are based on the composite. Performance shown is past performance. Past performance is not necessarily a guide to future performance. The value of

investments can go down as well as up and is not guaranteed. Please see the important composite disclosures at end of presentation.

Schroders US Small Cap Equity Russell 2000

Market cap – Weighted median ($bn) 2.3 1.5

Market cap range $196 million – 17.6 billion $24 million – 5.6 billion

P/E (excluding neg. earnings) 19.7x 19.2x

P/B 2.3x 2.0x

Dividend Yield 1.1% 1.4%

1 Year Forecast Growth (I/B/E/S Medians) 16.7% 16.4%

% in top 10 stocks 14.0% 2.6%

Beta* 0.84 1.00

Tracking error (actual, 5yrs)* 5.4% --

Information ratio (5yrs)* 0.01 --

Sharpe ratio (5yrs)* 0.38 --

53

Important information

Risk Warnings:

Investments in equities are subject to market risk and, potentially, to currency exchange rate risk. This fund may use financial derivative instruments as a part

of the investment process. This may increase the fund’s price volatility by amplifying market events

Important Information:

This document does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder International Selection Fund (the

“Company”). Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares

Subscriptions for shares of the Company can only be made on the basis of its latest prospectus together with the latest audited annual report (and

subsequent unaudited semi-annual report, if published), copies of which can be obtained, free of charge, from Schroder Investment Management

(Luxembourg) S.A.

An investment in the Company entails risks, which are fully described in the prospectus

Past performance is not a reliable indicator of future results, prices of shares and the income from them may fall as well as rise and investors may not get the

amount originally invested

Schroders has expressed its own views and opinions in this document and these may change

This document is issued by

Schroder Investment Management Limited, 31 Gresham Street, London, EC2V 7QA.

54