Embed Size (px)

Citation preview

September 2016 | For professional investors or advisers only. *Schroder International Selection Fund is referred to as Schroder ISF throughout the presentation

Schroder ISF*

European Equity

Absolute Return

October 2016

James Freeman | Product Manager

Fund Manager

Steve Cordell – Fund Manager

Moved across to Schroders as part of the takeover of Cazenove Capital

in July 2013

Originally joined Cazenove Capital in 2002

A senior member of the Pan-European equity team and manager of the

Schroder European Opportunities Fund, Schroder ISF European Equity

Absolute Return, Schroder ISF European Opportunities, Schroder ISF

European Equity (ex. UK) and Schroder European Absolute

Target fund

Previously at HSBC Asset Management (Europe) Ltd where he was

responsible for several retail and institutional Pan-European portfolios

Has 22 years of investment experience, including over 12 years

managing absolute return funds

1

Source: Schroders

19/10/2016 17:54:28

UK and European Equities Well resourced team of over 50 professionals

2

Source: Schroders, as at 30 September 2016 1 Includes two Global Analysts with full global sector coverage that make a significant contribution to UK and European equity portfolios

Head of UK and European Equities

Rory Bateman

Specialist / Quality

12 Pan European Sector Analysts1

Business Cycle Blend

Global Head of Equities

Nicky Richards

Value Small & Mid Cap Dynamic Small

5

Fund Managers /

Analysts

8

Fund Managers /

Analysts

9

Fund Managers /

Analysts

6

Fund Managers /

Analysts

6

Fund Managers /

Analysts

3

Fund Managers /

Analysts

8 Pan European Equity Product Team, 6 Equity traders, 5 Fund Management Assistants

Business cycle team

3

Source: Schroders, as at 31 July 2016

Pan European team with shared research responsibilities

Matt Hudson

Head of Pan-European Business Cycle

Investment team and product responsibilities

Matt Hudson Michael Zorko (UK Equity & Income)

Steve Cordell Nitin Bhalotia (Pan Europe)

Lionel Rayon Thibault Levacher (Pan Europe, High Alpha)

James Sym James Rutland (Pan Europe & Income)

Schroder ISF European Equity Absolute Return

HFRI Equity Long/Short

HFRI Equity Market Neutral

HFRI Fund of Funds

MSCI World

FTSE World Europe

JPM World Gov Bonds

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0% 2% 4% 6% 8% 10% 12% 14% 16%

Annual return

Annual Volatility

Why consider alternatives? Risk return reward – Schroder ISF European Equity Absolute Return

4

Source: Schroders, Datastream and HFRI. As at 31 August 2016. Schroder ISF European Equity Absolute Return was launched in February 2014 to accommodate a transfer of

shareholders from the Cazenove fund to the Schroder ISF SICAV. Prior to 11 February 2014 the fund uses the track record of Cazenove European Equity Absolute Return Fund

(launched on 30/10/2003) as a performance track record.

Targeting positive

returns, net of fees,

independent of market

conditions

A portfolio diversifier

Low market correlation

Broadly market neutral

Daily priced UCITS

SICAV structure

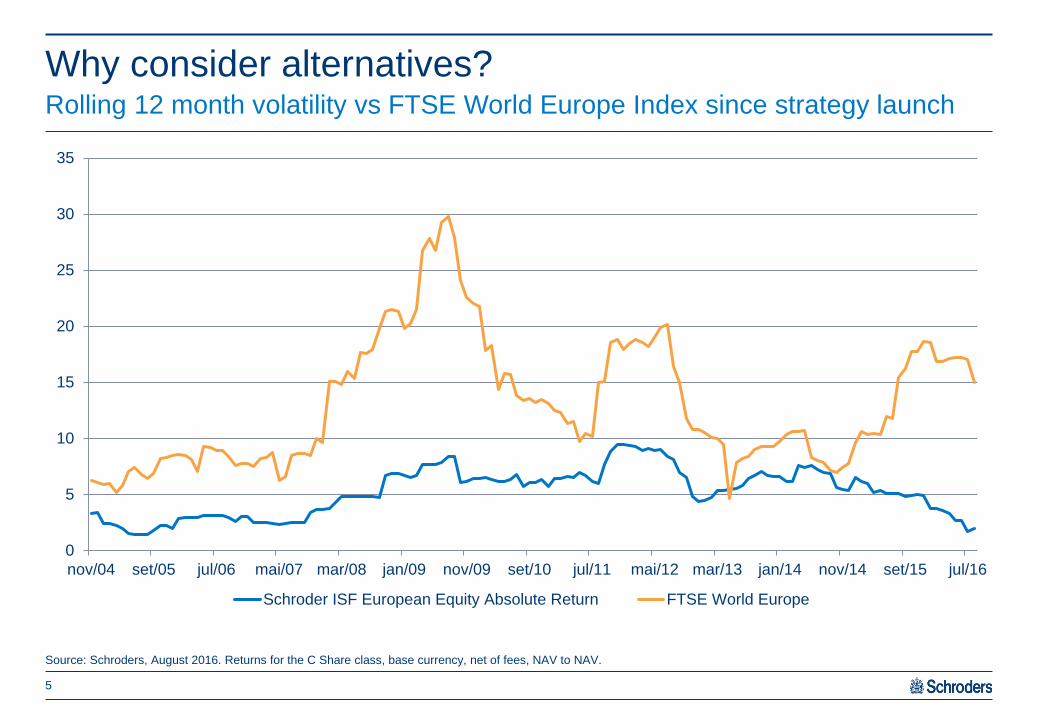

Why consider alternatives? Rolling 12 month volatility vs FTSE World Europe Index since strategy launch

Source: Schroders, August 2016. Returns for the C Share class, base currency, net of fees, NAV to NAV.

5

0

5

10

15

20

25

30

35

nov/04 set/05 jul/06 mai/07 mar/08 jan/09 nov/09 set/10 jul/11 mai/12 mar/13 jan/14 nov/14 set/15 jul/16

Schroder ISF European Equity Absolute Return FTSE World Europe

Worst market monthly drawdowns vs. fund

Protecting capital in market drawdowns Schroder ISF European Equity Absolute Return

Source: Schroders, August 2016. Returns for the C Share class, base currency, net of fees, NAV to NAV.

-11,6

-10,1 -10,8

-13,2

-6,7

-9,4

-4,8

-10,4

-4,8

-6,0

-5,2 -4,5

-8,3

-5,2 -6,2

2,2 1,5 0,9

6,0

-1,1 -0,6 -0,7 -1,3

4,7

-0,1

0,1

-0,1

0,0 1,0

-0,6

-16,0

-12,0

-8,0

-4,0

0,0

4,0

8,0

jan 08 jun 08 set 08 out 08 nov 08 fev 09 mai 10 ago 11 set 11 mai 12 jun 13 jun 15 ago 15 dez 15 jan 16

FTSE World Europe Schroder ISF European Equity Absolute Return

6

Investment process

Business cycle – a pragmatic approach

Analyse sensitivity of companies’ earning streams to business cycle

Use leading indicators to assess where we are in the business cycle

This will determine how much risk we want in the portfolio

The beta of the portfolio should therefore change through the different phases of the cycle

Stock selection will usually be the key driver of return except at turning points in the cycle

8

Source: BofAML European Quantitative Strategy

19/10/2016 17:54:28

‘Designed to deliver consistent performance’

Business cycle

Sector market divides are not homogenous. They do not necessarily help us determine the behaviour of these

stocks within the cycle

Define the beta of stocks and allocate them to seven style groupings:

Pragmatic approach combining top-down macro view with earnings based security selection

Avoid permanent style/size bias

Demand for products and services changes throughout the business cycle

Operational gearing of companies impacts profitability of companies

9

Source: Schroders

19/10/2016 17:54:28

Commodity cyclicals Growth Financials Growth defensives

Consumer cyclicals Value defensives

Industrial cyclicals

HIGH BETA LOW BETA

Stock selection…variability is predictable

Long

Market

Short

Growth defensive

Growth

Value defensives

Commodity cyclicals

Interest rate sensitive

Consumer cyclicals

Industrial cyclicals

Value defensive

Growth defensive

Growth

Consumer cyclicals

Commodity cyclicals

Interest rate sensitive

Industrial cyclicals

Consumer cyclicals

Industrial cyclicals

Interest rate sensitive

Commodity cyclicals

Growth

Value defensives

Growth defensives

Commodity cyclicals

Industrial cyclicals

Growth

Consumer cyclicals

Interest rate sensitive

Growth defensives

Value defensive

Typical longs

Typical shorts

Slowdown Recession Recovery Expansion

Source: Schroders

10

IFO business cycle indicator

EZ Composite PMI vs. Money Supply

How we determine turning points in the business cycle

11

Source: Top & Bottom RHS: JP Morgan and Datastream as at September 2016. Bottom LHS: Bloomberg as at September 2016.

US Corporate High Yield Bond yields also key

-10,0

-5,0

0,0

5,0

10,0

15,0

35

40

45

50

55

60

65

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Eurozone Composite PMIM1, deflated using HICP, %y/y (brought forward by 9m)

-50%-40%-30%-20%-10%0%10%20%30%40%50%

-25%

-15%

-5%

5%

15%

25%

07 08 09 10 11 12 13 14 15 16

European Cyclicals rel to Defensives (%3mom)

US 10y Bdy %3mom (rhs)

-0,2

-0,15

-0,1

-0,05

0

0,05

0,1

0,15

0,2

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Europe Cyclicals rel to Defensives (%6mom) IFO (%6mom, rhs)

Portfolio construction

12

Pan-European Equity

strategy meeting

Portfolio

Position sizing

Stock selection process

7 style tilts

Strength of view

Potential returns

Stock volatility

Quantitative screening

Qualitative screening

Stock opportunities analysed more in depth

Where are we?

Where are we going?

Tilts weighting to reflect our business

cycle view

Avoid permanent style/size bias

Diversified portfolio

Beta changes through cycle

Emphasis

50%

50%

Source: Schroders

EPS momentum

Price momentum

Valuation

Leverage

Analyst revisions

Databases: Bloomberg, Reuters, Datastream,

FactSet, Mirabaud Securities

Qualitative and quantitative screening of the

stock universe is undertaken in order to detect

potential opportunities

Looking for turning points in relative revisions Quantitative analysis

Stock selection process

13

Source: Mirabaud Securities, Schroders, as at September 2016

19/10/2016 17:54:28

AP Moeller - Maersk

Three types of trades 1. Business cycle

Source: Schroders, JP Morgan, as at September 2016

Business cycle factors

Long: A cyclical

Short: A defensive

Business cycle trades

50 – 90%

Trade

range

Example:

IFO business cycle indicator

14

Three types of trades 2. Relative value

Source: Schroders, Bloomberg, 9 September 2016. This is for illustrative purposes only.

Security analysis

Long: Boliden

Short: Antofagasta

Relative value trades

0 – 10%

15

Three types of trades 3. Directional – earnings revisions

Source: Schroders, Bloomberg, September 2016. This is for illustrative purposes only.

Security analysis

Long: Micro Focus International

Short: Ingenico

Directional trades

20 – 50%

16

Performance and

positioning

Schroder ISF European Equity Absolute Return

Source: Schroders, as at 31 August 2016. Returns from 2003 to 11 February 2014, quoted are for Cazenove European Equity Absolute Return Fund C Class, net of fees. Returns

from 11 February 2014 onwards, are for Schroder ISF European Equity Absolute Return C Class, base currency, net of fees, NAV to NAV. *FTSE World Europe TR Index

Fund Jan Feb Mar April May June July Aug Sep Oct Nov Dec Annual Index*

2016 -0.64 -0.27 -0.12 -0.21 -0.84 0.05 0.03 -1.33 -3.30% -2.64%

2015 3.75 1.04 0.98 -1.38 2.05 -0.13 1.90 0.05 -0.52 -0.47 -0.44 1.05 +8.04% +8.84%

2014 0.45 2.45 -1.24 -3.01 0.00 -0.93 -0.40 0.30 2.82 -0.31 0.61 -0.21 +0.43% +7.53%

2013 2.25 -1.13 -1.38 1.49 2.94 0.09 2.90 -1.47 3.00 4.25 1.71 1.08 +16.68% +19.99%

2012 1.65 -0.49 0.28 1.82 -0.08 1.92 1.11 0.56 1.15 3.41 3.39 0.32 +16.00% +18.77%

2011 2.07 -1.17 -2.31 0.86 1.78 -1.21 -2.45 -1.25 4.75 4.29 -4.06 -1.03 -0.14% -8.50%

2010 0.03 -1.19 -0.75 -2.67 -0.71 1.51 -3.64 0.88 -3.06 0.49 -2.56 -0.60 -11.72% +11.70%

2009 0.70 -0.60 -1.62 -2.93 0.71 -0.93 2.40 3.23 0.56 -1.75 -1.37 1.76 -0.04% +33.18%

2008 2.18 -1.37 -1.15 0.96 0.47 1.55 1.74 0.90 0.89 6.04 -1.09 0.11 +11.58% -43.24%

2007 2.06 -0.22 0.99 0.83 0.45 1.33 -0.01 0.88 -0.04 2.84 2.89 0.38 +13.05% +3.63%

2006 2.77 1.59 0.94 0.95 -0.25 0.46 0.82 0.38 1.09 0.22 -0.55 0.50 +9.26% +20.67%

2005 1.04 1.04 0.31 0.61 0.57 0.62 1.12 1.02 -0.25 -0.57 1.09 1.02 +7.89% +23.87%

2004 2.87 0.01 -0.40 -0.18 -0.52 1.17 0.52 0.63 0.57 0.37 1.20 1.79 +8.28% +12.57%

2003 1.41 +1.41% +2.77%

Performance

18

Schroder ISF European Equity Absolute Return Gross and Net exposure

Source: Schroders as at 31 August 2016. Performance shown for C Acc share class, net of fees, NAV to NAV. *Strategy launched 30 October 2003.

Since Launch*

Volatility (% p.a.) 5.6 Net performance 103.8%

Correlation with FTSE World Europe Index 0.09 Net annualised return 5.7%

Sharpe ratio 0.7 Fund size €479.1m

Average gross exposure (%) Average net exposure [Beta Adjusted] (%)

0

25

50

75

100

125

150

175

200

-30

-20

-10

0

10

20

30

40

50

60

70

de

z/0

3m

ar/

04

jun/0

4set/04

de

z/0

4m

ar/

05

jun/0

5set/05

de

z/0

5m

ar/

06

jun/0

6set/06

de

z/0

6m

ar/

07

jun/0

7set/07

de

z/0

7m

ar/

08

jun/0

8set/08

de

z/0

8m

ar/

09

jun/0

9set/09

de

z/0

9m

ar/

10

jun/1

0set/10

de

z/1

0m

ar/

11

jun/1

1set/11

de

z/1

1m

ar/

12

jun/1

2set/12

de

z/1

2m

ar/

13

jun/1

3set/13

de

z/1

3m

ar/

14

jun/1

4set/14

de

z/1

4m

ar/

15

jun/1

5set/15

de

z/1

5m

ar/

16

jun/1

6set/16

Average net exposure [Beta Adjusted] (%)(lhs) Average gross exposure (%)(rhs)

Schroder ISF European Equity Absolute Return characteristics

Top 10 long positions and business cycle positioning

Stock name % of NAV

Micro Focus 3.6

Nexity 3.5

Imerys 3.5

Rentokil Initial 3.4

Sage Group 3.2

Ahold Delhaize 2.6

Imperial Brands 2.5

Com Hem 2.2

Orange 2.1

Thyssen Krupp 2.1

Source: Schroders 30 September 2016. The securities shown are for illustrative purposes only and not a recommendation to buy or sell shares.

Sector Gross weight (%) Net weight (%)

Commodity cyclical 9.3 3.6

Industrial cyclical 20.2 2.6

Consumer cyclical 8.1 -5.3

Financial 20.0 4.1

Value defensive 18.3 7.7

Growth defensive 18.2 -8.5

Growth 16.8 2.2

20

Schroder ISF European Equity Absolute Return

Source: Schroders 30 September 2016, (ex cash)

21

Country % breakdown by Gross and Net exposure

-6,2

-5,9

-4,6

-2,7

-1,2

-1,2

-1,1

0,1

1,5

3,5

4,2

4,3

5,4

7,6

-10,0 -5,0 0,0 5,0 10,0

Future

Germany

Switzerland

Italy

Belgium

Portugal

Finland

Norway

Denmark

Spain

Sweden

Netherlands

United Kingdom

France

Net wgt %

1,1

1,2

1,6

1,9

4,6

5,1

6,0

6,2

6,9

7,4

9,6

20,5

21,6

30,3

0,0 10,0 20,0 30,0 40,0

Finland

Portugal

Norway

Belgium

Spain

Italy

Denmark

Future

Netherlands

Switzerland

Sweden

France

Germany

United Kingdom

Gross wgt %

Market outlook

The Global Earnings Cycle is turning up… …but will it follow through?

23

Source: Citigroup, September 2016

Global EPS revisions Pro Cyclical Rotation

40

50

60

70

80

90

100

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

12m Fwd EPSCyc/Def

Yes No No No ? Yes

First 10%

-0,8

-0,6

-0,4

-0,2

0

0,2

0,4

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Yes No No No ? Yes

First 10%

Bond yields begin to close the gap… …as deflation fears ease

24

Source: Bloomberg, September 2016

Cyclical vs Defensives and bond yields Citi inflation surprise index

-20

-15

-10

-5

0

5

10

15

20

25

30

92

93

94

95

96

97

98

99

100

101

102

103

104

105

mar 16 abr 16 mai 16 jun 16 jul 16 ago 16 set 16

European Cyclicals vs Defensives

German 10Y bund yields (bp) - rhs

Banks finally start to perform as Value turns up

25

Source: LHS: Bloomberg & J.P. Morgan RHS: Datastream & J.P. Morgan. September 2016

Bond yields are also important for Value/Growth call… European Banks’ performance and German Bunds

0,9%

1,4%

1,9%

2,4%

2,9%

3,4%

3,9%

4,4%

4,9%

65

70

75

80

85

90

95

100

07 08 09 10 11 12 13 14 15 16

MSCI Europe Value vs Growth (TR) US 10Y Bond Yields (rhs)

-0,3%

-0,2%

-0,1%

0,0%

0,1%

0,2%

0,3%

0,4%

0,5%

0,6%

70

75

80

85

90

95

100

jan 16 fev 16 mar 16 abr 16 mai 16 jun 16 jul 16 ago 16 set 16

European banks relative German bund yields (rhs)

Bund yield curve begins to steepen as ECB defers further stimulus…

…more fiscal, less monetary now?

26

Source: Bloomberg, J.P. Morgan, September 2016

Eurozone credit impulse index vs retail sales Bund yield curve steepens

-4%

-3%

-2%

-1%

1%

2%

3%

4%

5%

-11

-9

-7

-5

-3

-1

1

3

5

7

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Eurozone credit impulse Eurozone retail sales %yoy, rhs

Will US fiscal policy move US long bond yields?

27

Source: Goldman Sachs, September 2016

Western leading indicators losing momentum…

28

Source: BAML & Bloomberg, September 2016

Is Long Banks / Short Cyclicals the solution?

29

Source: LHS: Datastream & J.P. Morgan RHS: IBES & J.P. Morgan. September 2016

Cyclicals 12m Fwd P/E relative to Banks Banks vs Cyclicals and bond yields

1,3

1,4

1,5

1,6

1,7

1,8

1,9

2,0

2,1

2,2

2,3

75

80

85

90

95

100

jan 16 fev 16 mar 16 abr 16 mai 16 jun 16 jul 16 ago 16 set 16

Banks relative to Cyclicals US 10Y Bond Yields

0,9

1,0

1,1

1,2

1,3

1,4

1,5

1,6

1,7

1,8

1,9

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Europe Cyclicals 12m Fwd P/E relative to Banks

Median

+1stdev

-1stdev

Risk management

Source: Schroders

Leverage and Stock controls

Max 250% gross exposure

(typical range 100 – 175%)

Max 50% net exposure (typically up to

+/-25%)

Will not invest in unquoted stocks

Normal positions <5% NAV

Typically 30 – 50 holdings on each

side of the balance sheet

Independent monitoring

Daily VaR monitoring and stress

testing done in-house

Fortnightly factor analysis

Monthly analysis of realised

performance

Monthly liquidity analysis

Size, style, hedging

Unconstrained sector positioning

Bias to large and midcap

No automatic stop loss

Will use CFDs

Use of futures and ETFs

Selective investment in European

markets

Can buy options or write calls

30

Schroder ISF European Equity Absolute Return

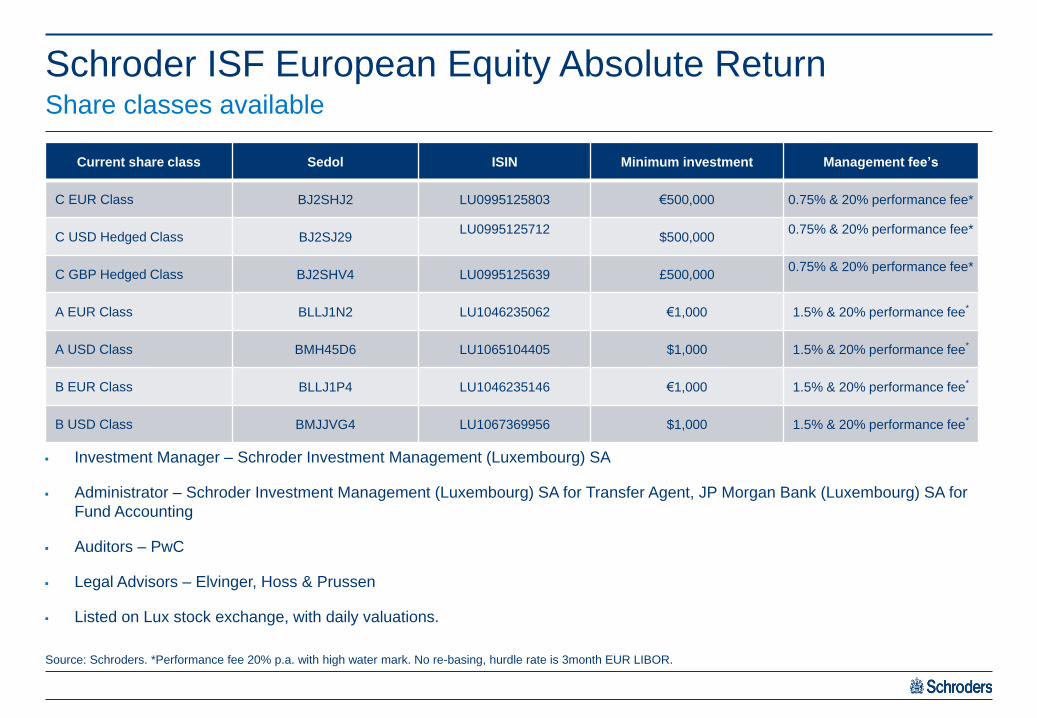

Source: Schroders. *Performance fee 20% p.a. with high water mark. No re-basing, hurdle rate is 3month EUR LIBOR.

Current share class Sedol ISIN Minimum investment Management fee’s

C EUR Class BJ2SHJ2 LU0995125803 €500,000 0.75% & 20% performance fee*

C USD Hedged Class BJ2SJ29 LU0995125712

$500,000

0.75% & 20% performance fee*

C GBP Hedged Class BJ2SHV4 LU0995125639 £500,000 0.75% & 20% performance fee*

A EUR Class BLLJ1N2 LU1046235062 €1,000 1.5% & 20% performance fee*

A USD Class BMH45D6 LU1065104405 $1,000 1.5% & 20% performance fee*

B EUR Class BLLJ1P4 LU1046235146 €1,000 1.5% & 20% performance fee*

B USD Class BMJJVG4 LU1067369956 $1,000 1.5% & 20% performance fee*

Investment Manager – Schroder Investment Management (Luxembourg) SA

Administrator – Schroder Investment Management (Luxembourg) SA for Transfer Agent, JP Morgan Bank (Luxembourg) SA for

Fund Accounting

Auditors – PwC

Legal Advisors – Elvinger, Hoss & Prussen

Listed on Lux stock exchange, with daily valuations.

Share classes available

Why consider alternatives? Conclusion

Returns competitive with equities

Volatility less than half the equity market

Proven ability to protect capital in big market falls

Process designed to be flexible enough to cope with varying business

cycles

32

Source: Schroders

19/10/2016 17:54:33

For professional advisers only. This material is not suitable for retail clients.

This document does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder International Selection Fund (the “Company”). Nothing in this

document should be construed as advice and is therefore not a recommendation to buy or sell shares.

Subscriptions for shares of the Company can only be made on the basis of its latest Key Investor Information Document and prospectus, together with the latest audited annual

report (and subsequent unaudited semi-annual report, if published), copies of which can be obtained, free of charge, from Schroder Investment Management (Luxembourg) S.A.

An investment in the Company entails risks, which are fully described in the prospectus.

Past performance is not a reliable indicator of future results, prices of shares and the income from them may fall as well as rise and investors may not get the amount originally

invested.

Schroders has expressed its own views and opinions in this document and these may change.

Risk considerations: The capital is not guaranteed. All equity forward sales are with a single counterparty. In case of default, the relevant equities will be sold in the market and

this may affect performance. Investments denominated in a currency other than that of the share-class may not be hedged. The market movements between those currencies will

impact the share-class.

The fund may hold indirect short exposure in anticipation of a decline of prices of these exposures or increase of interest rate. There is no guarantee that a financial derivative

contract will achieve its intended outcome, even if the terms of the contract are completely satisfied.

Third Party Data Disclaimer: Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data

provider's consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the third

party data. The Prospectus and/or www.schroders.com contains additional disclaimers which apply to the third party data. FTSE International Limited (“FTSE”) © FTSE (2016).

“FTSE®” is a trade mark of London Stock Exchange Plc and The Financial Times Limited and is used by FTSE International Limited under licence. All rights in the FTSE indices

and / or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and / or FTSE ratings or

underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

Issued in October 2016 by Schroder Investment Management Ltd., 31, Gresham Street, EC2V 7QA, who is authorised and regulated by the Financial Conduct Authority. For your

security, all telephone calls are recorded. PEE00222

Important information

33

This material was prepared by Schroder Investment Management, in response to a request from the client sent to Schroder and should not be understood as an

analysis of any securities, advertising material, offer to purchase or sell, offer or recommendation of any financial assets or investment. The purpose of this

material is exclusively informative and does not include investment objectives, financial conditions or the particular and specific needs of any shareholders or other

investors. The opinions stated in this material pertain to Schroder and may change at any time. The opinions are based on the date of their submission and do not

encompass any fact that may have arisen after this date, hence, Schroder is not compelled to update this material to reflect such provisions after the submission

of the same. This material is for exclusive Financial Intermediary, Institutional and Consultant and should not be used as support material by other individuals.

THIS MATERIAL IS HIGHLY CONFIDENTIAL AND SHOULD NOT BE REPRODUCED OR DISTRIBUTED, ENTIRELY OR PARTIALLY, TO PERSONS

OTHER THAN THE ORIGINAL RECIPIENTS. The Fund and the distribution of the shares of the same are not registered at the Brazilian Securities Commission

"CVM", and therefore do not meet certain requirements and procedures usually observed in public offerings of securities registered with the CVM, with which

investors in Brazilian capital markets may be familiar. For this reason, the access of the investors to certain information regarding the Fund may be restricted.

SCHRODER DOES NOT GUARANTEE PERFORMANCE.

Important information

34

![IN THE COURT OF HON'BLE SHRI JUSTICE P.N ... WP/391/2016 MOHIT S/O SH # MS MEGHA D/O: ANURAG S. BHALOTIA ] # BHAVANA M. KASARE ORDERS ON LETTER I.W.NO. 21085/16. [LETTE /R R RECD](https://img.pdfslide.us/doc/110x75/5adfcf247f8b9a6e5c8c9bb6/in-the-court-of-honble-shri-justice-pn-wp3912016-mohit-so-sh-ms-megha.jpg)