Embed Size (px)

Citation preview

Page | 1

UNIVERSITY OF HARGEISA

SCHOOL OF ECONIOMICS AND POLITICAL SCIENSE

Title

IMPACT OF WORKING CAPITAL MANAGEMENT ON BUSINESS

OPERATIONAL PERFORMANCE

By ID

MAHAD ISMACIL AKULE 127054

AHMED HUSEIN MAHAMED 126997

Advisor: SEED ABDILAHI SEED

A Research Proposal/Thesis Submitted to the School of Economics and

Political Sciences, Fulfillment of the Requirements for the Award of

Bachelor Degree in Economics

August, 2016

Page | 2

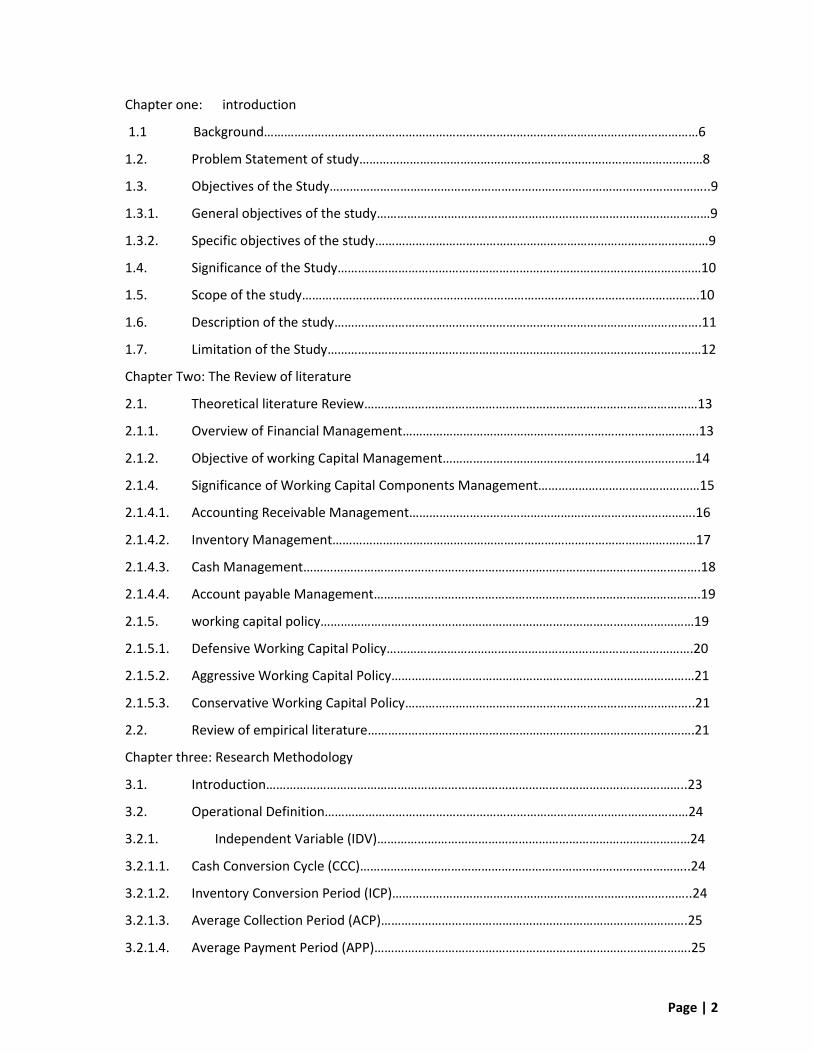

Chapter one: introduction

1.1 Background…………………………………………………………………………………………………………………6

1.2. Problem Statement of study…………………………………………………………………………………………8

1.3. Objectives of the Study…………………………………………………………………………………………………..9

1.3.1. General objectives of the study………………………………………………………………………………………9

1.3.2. Specific objectives of the study………………………………………………………………………………………9

1.4. Significance of the Study………………………………………………………………………………………………10

1.5. Scope of the study……………………………………………………………………………………………………….10

1.6. Description of the study……………………………………………………………………………………………….11

1.7. Limitation of the Study…………………………………………………………………………………………………12

Chapter Two: The Review of literature

2.1. Theoretical literature Review………………………………………………………………………………………13

2.1.1. Overview of Financial Management…………………………………………………………………………….13

2.1.2. Objective of working Capital Management…………………………………………………………………14

2.1.4. Significance of Working Capital Components Management…………………………………………15

2.1.4.1. Accounting Receivable Management………………………………………………………………………….16

2.1.4.2. Inventory Management………………………………………………………………………………………………17

2.1.4.3. Cash Management……………………………………………………………………………………………………….18

2.1.4.4. Account payable Management…………………………………………………………………………………….19

2.1.5. working capital policy…………………………………………………………………………………………………19

2.1.5.1. Defensive Working Capital Policy……………………………………………………………………………….20

2.1.5.2. Aggressive Working Capital Policy………………………………………………………………………………21

2.1.5.3. Conservative Working Capital Policy…………………………………………………………………………..21

2.2. Review of empirical literature…………………………………………………………………………………….21

Chapter three: Research Methodology

3.1. Introduction……………………………………………………………………………………………………………..23

3.2. Operational Definition………………………………………………………………………………………………24

3.2.1. Independent Variable (IDV)…………………………………………………………………………………24

3.2.1.1. Cash Conversion Cycle (CCC)……………………………………………………………………………………..24

3.2.1.2. Inventory Conversion Period (ICP)……………………………………………………………………………..24

3.2.1.3. Average Collection Period (ACP)……………………………………………………………………………….25

3.2.1.4. Average Payment Period (APP)………………………………………………………………………………….25

Page | 3

3.2.2. Dependent Variable (DV)………………………………………………………………………………..25

3.3. Research design……………………………………………………………………………………………………..26

3.4. Research Approaches………………………………………………………………………………………………26

3.5. Sample Design………………………………………………………………………………………………………..26

3.5.1. Population……………………………………………………………………………………………………………….27

3.5.2. Sample Frame………………………………………………………………………………………………………….27

3.5.3. Sample Size……………………………………………………………………………………………………………..28

3.5.4. Sampling Techniques………………………………………………………………………………………………29

3.6. Source of Data………………………………………………………………………………………………………..29

3.6.1. Primary Data……………………………………………………………………………………………………………29

3.6.2. Secondary Data……………………………………………………………………………………………………….29

3.7. Data Collection Techniques………………………………………………………………………………………30

3.8. Data Analysis and presentation…………………………………………………………………………………30

3.9. Ethical Consideration…………………………………………………………………………………………………30

Chapter Four: RESULTS AND DISCUSSION AND INTERPRETATION

4.1. Introduction………………………………………………………………………………………………………………..31

4.2. Descriptive Statistics……………………………………………………………………………………………………31

4.2.1. Demographic statistics of Respondents……………………………………………………………………..31

4.2.1. Manager’s Knowledge in Working Capital Management………………………………………………34

4.2.1. Cash Convention Cycle…………………………………………………………………………………………………34

4.2.1.2. Inventory Management……………………………………………………………………………………………….36

4.2.1.3. Account Receivable management……………………………………………………………………………….37

4.2.1.4. Account Payable management…………………………………………………………………………………….38

4.2.2. Analysis for measurement indicators………………………………………………………………………………….39

4.2.3. Correlations…………………………………………………………………………………………………………………42

4.2.3.1. Relationship between CCC and Profitability…………………………………………………………………42

4.2.3.2. Account receivable and Firm’s Profitability………………………………………………………………….43

4.2.3.3. Account Payable and Inventory against Profit Margin Ratio………………………………………44

4.2.3.4. Relationship between CCC and Liquidity…………………………………………………………………….44

Chapter Five: Conclusion and Recommendations

5.1. Introduction………………………………………………………………………………………………………………45

5.2. Conclusion………………………………………………………………………………………………………………….45

Page | 4

5.2.1. Correlation of Cash convention Cycle with Profitability and Liquidity…………………………46

5.2.2. Components in Cash Convention Cycle against Liquidity and Profitability……………….…46.

5.2.3. Manager’s Knowledge and competence level in Working Capital Management…………47

5.3. Recommendations……………………………………………………………………………………………………47

5.3.1. Working Capital Balancing Acct……………………………………………………………………………….48

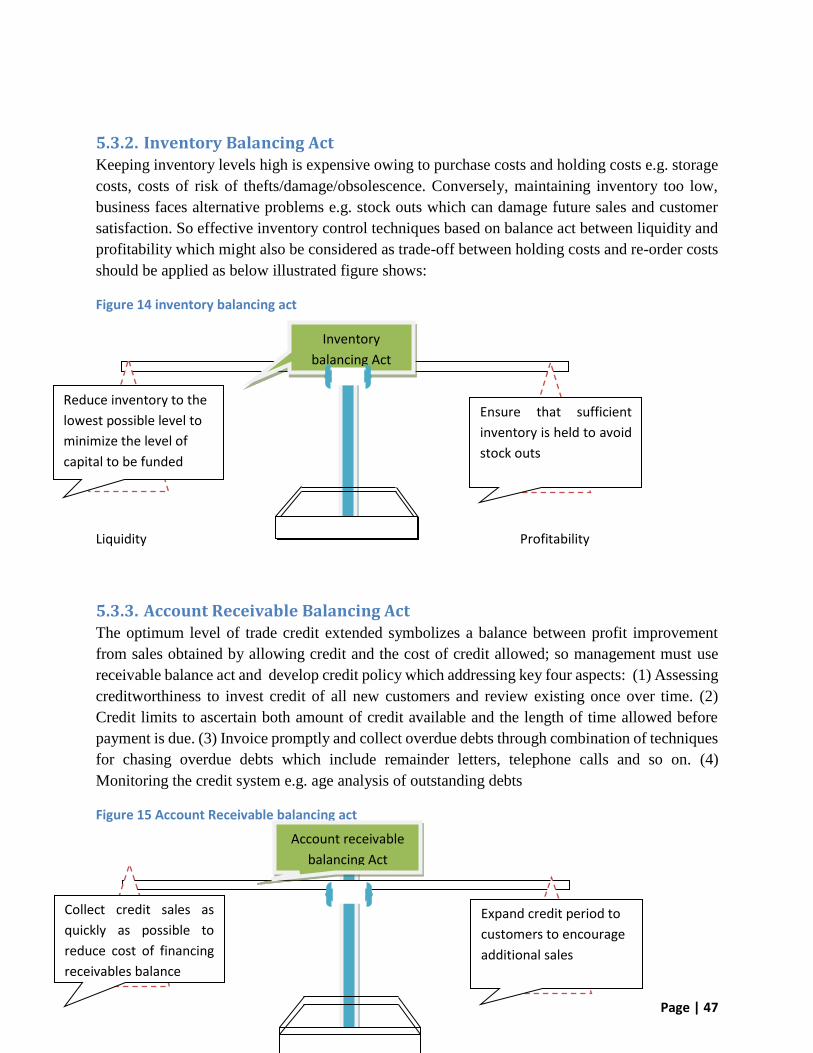

5.3.2. Inventory Balancing Act……………………………………………………………………………………………48

5.3.3. Account Receivable Balancing Act………………………………………………………………………………49

5.3.4. Account Payable Balancing Act………………………………………………………………………………….49

6.0. Reference…………………………………………………………………………………………………………………………….50.

List of figures:

Figure 1 Conceptual framework for Working Capital Management Components of the Study ................. 14

Figure 2 Typology of working capital policy ............................................................................................. 19

Figure 3 Age categories of respondents ................................................................................................ 32

Figure 4 of respondent’s level Educational ........................................................................................... 33

Figure 5 Impact of CCC on Liquidity and Profitability against manager’s perceptions ....................... 33

Figure 6 impact of inventory management on liquidity and profitability against manager’s insights .. 35

Figure 7 impact of Account receivable on liquidity and profitability against manager’s perceptions . 36

Figure 8 impact of Account payable management on liquidity and profitability against manager’s

perceptions ............................................................................................................................................ 37

Figure 9 correlation between CCC and Profitability............................................................................. 40

Figure 10 correlation of average collection period with profit margin ratio ......................................... 42

Figure 11 correlation of CCC and liquidity (measured current ratio) ................................................... 43

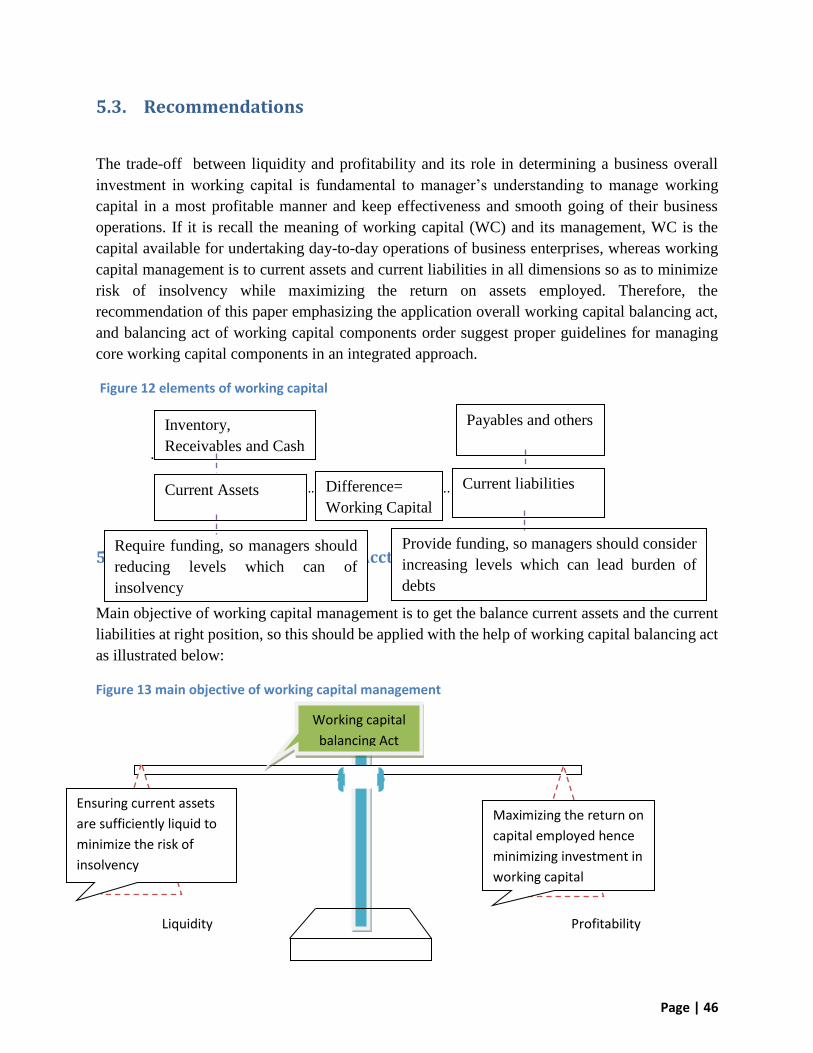

Figure 12 elements of working capital .................................................................................................. 46

Figure 13 main objective of working capital management ................................................................... 46

Figure 14 inventory balancing act ........................................................................................................ 47

Figure 15 Account Receivable balancing act ........................................................................................ 47

Figure 16 Account Payable balancing act ............................................................................................. 48

Page | 5

List of Tables Table 1 Sample frame………………………………………………………………………………………………………………………..27

Table 2 Respondent's Gender ............................................................................................................... 31

Table 3Marital Status of respondents................................................................................................... 31

Table 4 the position of respondents in their firms (What is your current position in your firm?) ....... 32

Table 5 Summary of all Variables of paper ........................................................................................... 38

Table 6 Descriptive Statistics for all Samples ........................................................................................ 39

List of Appendixes: Appendix 1 Questionnaires ............................................................................ Error! Bookmark not defined.

Page | 6

Chapter one: Introduction

1.1. Background

Generally, financial management is essential part of the economic and non economic activities

at the global perspective, which leads to decide the efficient procurement and utilization of finance

with profitable manner. Earlier, the subject of financial management was part of accountancy with

traditional approaches. No a days it has been enlarged with innovative and multi dimensional

functions in the field of the business (Subramanian, 2009). The term financial management has

been given many definitions by many authors. The most popular and acceptable definition of

financial management as given by S.C Kuchal is that “the financial management deals with

procurement of funds and their effective utilization in the business”. Basically, the objectives of

financial management may be broadly divided into two parts which are (1) Profit maximization:

The profit maximization is considered as parameter of measuring business operational efficiency

and helps to reduce business risk, (Subramanian, 2009) (2) Wealth Maximization: the wealth

maximization is one of the modern approaches, which involves the latest innovation and

improvement in the field of the business concern (Subramanian, 2009).

So, Business concern then needs Finance to meet their requirements in the economic world. Any

kind of business activities depends on finance regardless size (small or large) of business to fulfill

operational activities in a highly profitable manner (Subramanian, 2009). In the modern world, all

the activities are concerned with the economic movements very particular to earning profit and

avoid risk of insolvency through combination of various strategies, hence the entire normal

business course of actions directly relate with making profit. According to economics concept of

factors of production; rent given to landlord, wage given to labour, return given to capital and

profit given to shareholders, a business concern needs finance to meet all the requirements.

Therefore, the finance is often called as lifeblood of organization. The finance can be classified

into two board categories which are private finance and public finance each of them can be further

sub-divided. The private finance includes individuals, firms, business or corporation financial

resources to meet the requirement, whereas public finance concerns the revenue and disbursement

of Government such as central Government, State Government, and semi-Government financial

matters (Subramanian, 2009).

Page | 7

However, it is also profoundly indispensable to understand the basic definitions of current assets

and current liability in order to clearly insight the meaning of working capital, and its relevant

management in the normal business course of actions.

(Fitzgerald 2006) defined current assets as, “cash and other assets which are expected to be

converted into cash in the ordinary course of business within one year or within such longer period

as constitutes the normal operating cycle of a business.” The claims or obligations which are

normally expected to mature for payment within an accounting cycle are known as current

liabilities. Then, Working capital is the capital available for conducting the day-to-day operations

of an organization, normally the excess of current assets over current liabilities, whereas working

capital management is the management of all aspects of both current assets and current liabilities

to minimize the risk of insolvency while maximizing the return on assets. So, it’s clear without

doubt that inefficient financial management including working capital management may damage

business enterprise’s profitability (Gebrehiwot & Wolday, 2006). On the contrary, the efficient

management of working capital is a fundamental part of the overall corporate strategy to create

shareholders value (Nazir and Afza, 2008).

In addition to, “The working capital plays the same role in the business as the role of heart in

human body. Working capital funds are generated and these funds are circulated in the business.

As and when this circulation stops, the business becomes lifeless. It is because of this reason that

the working capital is known as the circulating capital as it circulates in the business just like blood

in the human body.” (Agarwal, 2000:171-172). Nevertheless, excessive levels of current assets

may have a negative effect on the firm’s profitability, whereas a low level of current assets may

lead to lower level of liquidity and stock outs leading to difficulties in maintaining smooth

operations (Van Horne and Wachowicz, 2004). Accordingly, working capital management is an

attempt to manage and control the current assets and the current liabilities in order to maximize

profitability and proper level of liquidity in business.

Though a number of research works have discovered the impact of working capital management

on the performance of organizations, there is no investigation has been carried out regarding to

impact of working capital management on the business operations in the context of Somaliland.

This limited evidence and information gaps related to the research topic in Somaliland perspective

invite for research to be undertaken so as to identify the impact of existing real practice, and

Page | 8

techniques of working capital management currently applied, underline problems, evaluate its

magnitude to some extent and propose relevant recommendations. In view of that, the focus of this

paper will be to assess working capital management in-depth and how proper management on

working capital components fundamentally effect on business operational performance through

the liquidity and profitability balance act.

1.2. Problem Statement of study

Working Capital Management and its Impact on Firms’ Performance has been studied significantly

by different researchers (Padachi, K. (2006); F. Finau, (2011); Anand and Gupta (2002); Mohamad

and Noriza (2010); Deloof (2003); Luo et al. (2009); Vishmani at el., (2007) Koperunthevi (2010);

Fathi and Tavakkoli (2009); V. Ganesan, (2007)). Most of these and other researchers identified

significant association between working capital management and firms’ operational performance.

It has however been discovered that some methods that managers use in practice to make working

capital decisions do not rely on the principles of finance, rather they use vague rules of thumb or

poorly constructed models (Emery, Finnerty and Stowe 2004). This practice of poorly constructed

models makes managers not capable to successfully manage the various mixes of available

working capital components. Thus, the organization may either be overcapitalized or

undercapitalized. Egbide (2009) found that large number of business failures in the past has been

blamed on the inability of the financial manager to plan and control the working capital of their

respective firms.

However, while searching on internet, browsing the books and journals no study directly related

to research topic which has been conducted in Hargeisa as well as in Somaliland. Thus, lack of

proper research which has been locally conducted in relation to this question, and with light of

underlined problems by above referenced intercontinental studies, this problem seems uncovered

potential bottleneck in Somaliland business environment in which may give chance local

company’s managers to have limited wakefulness in working capital management decisions, and

encourage them to apply traditional approaches of working capital management, rather they should

Page | 9

apply financial management principles. As a result, this may hinder the entire local business

operational performance.

Therefore, the aim of this study is to assess significance and impact of proper working capital

management decisions on business operational performance. The paper will emphasize the

liquidity and profitability balance act in order to ensure how to maintain overall working capital

investment levels in a rational and reasonable position focusing on the key components of current

assets and current liabilities namely: cash, accounts receivable, inventory and accounts payable.

1.3. Objectives of the Study

1.3.1. General objectives of the study

The general objective of this paper will be to examine balance of current assets and current

liabilities where currents assets are sufficiently liquid to minimize the risk of insolvency and return

on capital employed is the highest as possible with least possible working capital investment level.

1.3.2. Specific objectives of the study

1. To examine the impact of cash management on firm’s operational performance.

2. To evaluate the effect of inventory management on firm’s operational performance

3. To analyze the effect of receivable management on firm’s operational performance

4. To address the importance of trade payable management on firm’s operational performance

1.4. Significance of the Study

The findings of this paper will provide implications for managers of companies located and operate

in Somaliland whose are attempting to make decisions regarding to working capital management

Page | 10

reform models. It will also assist managers to understand and develop financial policies, practices

and techniques for managing working capital components in a most productive way. The findings

will reveal the significance of working capital management for companies in Hargeisa Somaliland

in terms of performance and the practice of liquidity and profitability balance act to some extent.

Moreover, the study will help me as a researcher not only for academic requirement, but also to

have solid experience, expert insight and grounded intuition from this question or issue under the

investigation. Also it will provide basic guidelines and relevance benchmark for potential

researchers as well as other fundamental stakeholders of this environment such as accountants,

financial managers, and financial policy makers.

1.5. Scope of the study

The paper will be delimited to investigate impact of working capital management on business

operational performance emphasizing the management of core working capital components ( cash,

account receivable, inventory, and account payable) with relative measurement indicators

including CCC (cash conversion cycle), which are used for WCM measurement. The study will

also use liquidity and profitability ratios particularly current ratio (CR), quick ratio (QR), profit

margin ratio (PMR), and return on asset ratio (ROAR) for performance measurement. Moreover,

the coverage of the paper will not cover all categories of privately owned businesses, rather it will

confine on carefully selected representative sample of wholesale businesses specifically

merchandising companies exist and run in Hargeisa. The wholesale businesses are those buy goods

in bulk and then resell them, generally for a higher price than they were purchased to retailers or

other wholesalers not directly to the end users/ consumers.

Considering the geographical scope, the research will take place in Hargeisa, the city of Somaliland

situated in a mountainous area, 1,334 meters (4,377 feet) above sea level in an enclosed valley of

the northwestern Galgodon highlands (Ogo Mountains). According to Demography, Hargeisa has

a population of around 750,000 residents as of 2015. The urban area occupies 65 square kilometers

(25 sq mi), with a population density of 11,600 inhabitants per square kilometer (30,000/sq mi).

In addition to, Hargeisa is the financial hub to many entrepreneurial industries ranging from

Page | 11

gemstone cutters, to construction, food processing, retail, and import and export firms. Regarding

to climate, Hargeisa has a semi-arid climate (Köppen: BSh). The city generally features warm

winters and hot summers. However, despite its location in the tropics, due to the high altitude

Hargeisa seldom experiences either very hot or very cold weather. This is a trait rarely seen in

regions with semi-arid climates. The city receives the bulk of its precipitation between the months

of April and September, averaging just less than 400 mm of rainfall annually. Average monthly

temperatures in Hargeisa range from 18 C in the months of December and January to 24 C in the

month of June.

1.6. Description of the study

Large merchandising companies along with retailers which exist and operate in Somaliland are

large in number than other manufacturing and service industries. So they have tremendous

influence on effectiveness and smooth going of country’s economic conditions as long as they are

one of the major private sector sources of job opportunities, take incredible part the aggregate price

level in the economy and revitalize or refresh entire economic cycle. They also increase demand

of foreign currency particularly U.S dollar for buying goods from foreign markets due to lack of

international recognition of Somaliland local currency which only works and circulates within the

Somaliland territory. The large merchandising companies which are under consideration of this

study are those buy goods in bulk and then resell them, generally for a higher price than they were

purchased to retailers or other wholesalers not directly to the end users/ consumers. These large

merchandising companies are comparatively systemized in terms managerial skills including

financial management, accounting and reporting, documentation and record keeping then lower

tiers of business.

1.7. Limitation of the Study

The major drawbacks of this paper can be lack of commitment, inappropriate information

disclosure, and treatment which may hinder to clearly understand existing situation and actual

Page | 12

happenings in the right of reality. The research paper might also face lack of relevance, reliable,

and complete data. In addition to, there may be lack of sophisticated accounting system practice

and correct record keeping in sampled companies which will be under investigation. However, this

drawback will limit the findings of the study.

Chapter Two: The Review of literature

This chapter calls attention to on present literatures involving to the working capital management

components, and its effect on business operational performance. The literature review section

comprises two sections. The first section concerns the theoretical review of working capital

management while the second section examines the empirical evidence pertinent to working

capital management

Page | 13

2.1. Theoretical literature Review

2.1.1. Overview of Financial Management

The traditional definition of Finance is the study of funds management and the directing of these

funds in order to achieve its particular objectives. The unique objective of a good financial

management is to maximize returns that associate with minimizing of financial risks

simultaneously. In Financial management it is critical to understand the business objectives and

financial functions before recognizing the major component that is the short-term financial

management or the Working Capital Management relative to the day-to-day operations (Brigham

and Ehrhardt, 2010; Chandra, 2008; Keown, Martin, Petty, and Scott, 2002; D. Sharma, 2009).

Financial management is also concerned with the creation of economic wealth, maximizing the

share price for shareholders’ equity, planning and controlling of the business’s financial resources,

increasing its profitability and maximizing the rate of returns on Equity.

2.1.2. Objective of working Capital Management

According to Gitman (2009) the objective of Working Capital Management (WCM) is to minimize

the Cash Conversion Cycle (CCC) the amount of capital tied up in the firm’s current assets. It

focuses on controlling account receivables and their collection process, and managing the

investment in inventory. Working capital management is vital for all business survival,

sustainability and its direct impact on performance (Mengesha, 2014). Moreover, the primary

cause of an enterprise’s failure is the poor control management of Working Capital internally

amongst its components. Thus, the finance manager of an enterprise must be alert to the level of

working capital (Finau, 2011).

Page | 14

However, the primary emphasis of this paper is to examine the four critical components of working

capital management namely Cash, Accounting receivable, Inventory and Accounts payable. Even

though the operation cycle of these components relative to operational performance should be

considered, it will not be given a great consideration as the below illustrated conceptual

Framework (Figure 2.1.2-1) demonstrates the critical portion of the financial management

components for this study.

Figure 1 Conceptual framework for Working Capital Management Components of the Study

Financial Management

Working Capital

Management

Cash management

Impact on Performance

Accounts Receivable

Management

Impact on Performance

Inventory Management

Impact on Performance

Accounts Payable

Management

Impact on Performance

Ensure Liquidity and Profitability Balance Liquidity

Profit Margin and Return on

Assets Ration

Profitability

Page | 15

2.1.3.

2.1.4. Significance of Working Capital Components Managemen

Working capital is so important for business day-to-day operations. A decision made on one of the

Working Capital components has an impact on the other components. In order to maximize the

performance of a business, the Working Capital Management should be integrated into the short

term financial decision making process (Crum, Klingman, and Tavis, 1983). Working Capital or

Net Working Capital is “the difference between current assets less current liabilities” (Arnold,

2008). In financial annual reports, working capital is defined in an algebraic expression as follows:

The investment in NWC is so vital and helps the capital budgeting analysis of a given firm.

Working Capital (WC) can be invested in short-term sources of finance, such as cash, inventories,

account receivables, and notes receivables. WC is minimised in terms of payments made to

account payables (creditors), account notes payable and other accrued liabilities. In order to

balance out the optimal levels of costs and benefits, then the liquidity components of working

capital must be managed with appropriate techniques through raising or lowering the stocks, cash,

account receivables and account payables (Arnold, 2008; Gitman, 2009).

2.1.4.1. Accounting Receivable Management

Account receivables are assets representing amounts owed to the firm as a result of the sale of

goods or services in the ordinary course of business. Kelly and McGowen (2010) suggest that

credit customers who pay late or don’t pay at all only aggravate the problem. Thus, it is important

for the financial manager or account receivables manager to establish a good policy that controls

the advantages of offering credit with the associated costs.

Current Ratio and Quick

Ratio

Net Working Capital (NWC) = Current Assets (CA) – Current Liabilities (CL).

Page | 16

The firm should establish its receivables policies after carefully considering both the benefits and

costs of different policies. (Hampton 2004). Three factors should be analyzed:

Profits. The firm should investigate different possibilities and forecasts the effect of each

on its future profits. The cost of funds tied up in receivables, collection costs, bad debt

losses, and money lost discounts for early payment should be compared with additional

sales or losses of sales as a result of each proposed policy

Growth in sales. Sometimes firms are willing to accept short term setbacks with respect

to profits if a new policy enables the firm to increase its sales significantly. A firm may

adopt a certain policy to gain a foothold in previously closed market. Because growth is so

important aside from profits, it should be viewed as a separate factor in determining

receivables policies.

Possible problems. In spite of increase sales and profits, some policies may be

accompanied by obvious and annoying problems.

2.1.4.2. Inventory Management

The composition of an inventory differs depending on what kind of production or business

companies are involved in. The five different assets an inventory can consist of are; raw materials,

work in progress materials, finished goods, extra material and consumption materials. Most

companies have an inventory that they more or less depend on in their operation (Lantz, 2008, p.

306).

Raw Materials Raw materials are concerned with the goods that have been delivered by the

supplier to purchaser’s warehouse but have not yet been taken into the production area for

conversion process (Cinnamon et al., 2010).Work In Progress (WIP) Work in progress concerns

are when the product has left the raw material storage area, until it is declared for sale and delivery

to customers (Birt et al., 2011; Cinnamon et al., 2010). Finished Goods refer to the stock sitting

in the warehouse waiting for sale and delivery to customers.

The management of inventory is one of the more challenging tasks for working capital managers

who, if they could decide, would like to minimize the inventory as much as possible in order to

shorten the cash conversion cycle and reduce costs. The risk of minimizing an inventory down to

Page | 17

a level close to zero is that it increases the possibility of running out of materials needed in the

production or running short of finished goods during a high demand. Such situation would be

costly for any company due to the revenues they would lose (Maness and Zietlow, 2005, p. 99).

Each manager has their own interests they first and foremost would like to satisfy which

complicate the task to reach a joint decision. Each company should find the balance that they will

benefit most from (Pass & Pike, 2007).

The just-in-time approach is a strategy for effective inventory management and help keeping

inventory levels on a lower level. The strategy aims to make the orders of material, produce and

deliver just in time when it is required and not before (Brealey, Myers and Allen, p. 820).

2.1.4.3. Cash Management

In a financial sense, the term cash refers to all money items and sources that are immediately

available to help pay firms bills (Hampton, 2004). Managing cash is becoming ever more

sophisticated in the global and electronic age of the 1990s as financial managers try to squeeze the

last dollar of profit out of their cash management strategies (Block and Hirt, 1992).

The management with account payables and receivables that has been described above and below

goes under the term of cash management. Following paragraphs summarizes what cash

management engage in order to shorten the cash conversion cycle (Lantz, 2008, p. 119);

Extend the credit time for account payables

Shorten the credit time for account receivables

Incorporate more efficient methods for the management of account payables and

receivables

Improve the procurement of capital surplus and deficits (Lantz, 2008, p. 119)

Despite the ambition to minimize the cash conversion time and therefore the costs in the

conversion cycle, the companies cannot escape all costs since they have their own obligations to

Page | 18

consider. Taking into the account these responsibilities companies must keep some cash for

expected as well as unexpected expenditures that occur in their everyday business. Lantz have

mentioned about these three motives why companies should hold cash (Lantz, 2008, p. 119);

The transaction motive: the company must be able to manage their own obligations like

payments to suppliers. They should not be dependable on customers paying in time since

they can be late and pay after due date which will involve extra costs.

The speculative motive: the market is unpredictable and opportunities could turn up at any

time and when they do, companies should see to that they have money available if they

would like to invest.

The precautionary motive: as well as the market is unpredictable so are the activities in the

business. Unexpected events like; machines breaking down, a suddenly increase or

decrease of the demand and more, can occur and could have a very negative influence for

the whole company if not taken care of (Lantz, 2008, p. 120).

2.1.4.4. Account payable Management

The general guidelines for optimizing the managing of account payables involve the timing of

payments. Companies should try prolonging the time of payment as long as possible as they can

use the advantage of their suppliers financing their investments until payment has been made.

Another argument for prolonging the time for payment is that the producing companies, for

example, need some time to convert their purchased raw material into products they can get sold

and get cash in return (Maness and Zietlow, 2005, . 235-238).

Some suppliers offer their customers discount rates as an attempt to get them to pay their

receivables before maturity date which may sound tempting but this is not always the most

profitable option. To avoid being misled by theses discounts offers, companies should carefully

consider every discount offer they get to see that it is beneficial in terms of their conditions Maness

and Zietlow, 2005, p. 235-238). If there is no discount offer given companies should use the whole

credit period and pay their payables on due date. Paying after due date should always be avoided

unless the company has fallen in financial difficulties and there is no other choice. The reason for

Page | 19

this is that delayed payments can result in unnecessary costs as late fees (Dolfe and Koritz, 2000,

p. 49).

2.1.5. Working Capital Policy

Working capital policy can be best described as a strategy which provides the guideline to manage

the current assets and current liabilities in such a way that it reduces the risk of default (Afza and

Nazir, 2007). Working capital policy is mainly focusing on the liquidity of current assets to meet

current liabilities. Liquidity is very important because, if the level of liquidity is too high then a

company has lot of idle resources and it has to bear the cost of these idle resources. However, if

liquidity is too low then it will face lack of resources to meet its current financial liabilities (Arnold,

2008). Current assets are key component of working capital and the WCP also depends on the

level of current assets against the level of current liabilities (Afza and Nazir, 2007). On this base

the literature of finance classifies working capital policy into three categories as defensive or

hedging, aggressive and conservative working capital policy (Arnold, 2008 pp.535-36) and

discussed as follows:

Figure 2 Typology of working capital policy

2.1.5.1. Defensive Working Capital Policy

Defensive policy: Company follows defensive policy by using long term debt and equity to finance

its fixed assets and major portion of current assets. Under this approach, the business concern can

adopt a financial plan which matches the expected life of assets with the expected life of the

sources of funds raised to finance assets (Paramasivan and Subramanian, 2009). Inventory

expected to be sold in 30 days could be financed with a 30- day bank loan; a machine expected to

last for 5 years could be financed with a 5-year loan; a 20-year building could be financed with a

Working Capital Policy

Defensive Policy Aggresesive Policy Concervative Policy

Page | 20

20 year mortgage bond; and so forth (Weston and Brigham, 1977, P. 716). Inventory expected to

be sold in 30 days could be financed with a 30- day bank loan; a machine expected to last for 5

years could be financed with a 5-year loan; a 20-year building could be financed with a 20 year

mortgage bond; and so forth (Weston and Brigham, 1977, P. 716).

Defensive policy reduces the risk by reducing the current liabilities but it also affects profitability

because long term debt offers high interest rate which will increase the cost of financing (Arnold,

2008 p.530)

2.1.5.2. Aggressive Working Capital Policy

Aggressive policy: Paramasivan and Subramanian (2009) pinpointed that in aggressive policy the

entire estimated requirement of current assets should be financed from short-term sources and even

a part of fixed assets financing be financed from short- term sources. This approach makes the

finance mix more risky, less costly and more profitable. This policy increases the risk of default

because a company might face a lack of resources to meet the short term liabilities but it also gives

a high return as the high return is associated with high risk (Arnold, 2008, p.536).

2.1.5.3. Conservative Working Capital Policy

Conservative policy: It is also a mixture of defensive WCP and aggressive WCP. So Conservative

Working Capital Policy refers to minimize risk by maintaining a higher level of Working Capital.

This type of Working Capital Policy is suitable to meet the seasonal fluctuation of the

manufacturing operation (T.Subramanian, 2009).

2.2. Review of empirical literature

Several researchers have conducted researches in relation to working capital management from

dissimilar standpoint and in different atmospheres. Below are some of them which might be

incredibly fascinating and valuable for the research:

Page | 21

Moyer et al. (2003) found that Working Capital consists of a large portion of a firm’s total

investment in assets, 40% in manufacturing and 50-60% in retailing and wholesale industries

respectively. The firms could reduce its financing cost and increase the funds available for

expansion if they minimize the funds tied up in current assets. They found that cash helps to keep

the firm liquid. It enables the firm to pay its obligations and also protects the firm from becoming

bankrupt.

Alipour (2011) researched about working capital management and corporate profitability while

taking sample of 1063 companies from Tehran stock exchange. To test the hypothesis, multiple

regressions and Pearson’s correlation was used. He analyzed that sale and profit of a company is

greatly influenced by the working capital management. Due to inefficient working capital

management, a company may be incapable to pay its debts on time. The results show a significant

relationship between working capital management and profitability of a company. There is a

negative relationship between cash conversion cycle, average collection period, inventory turnover

in days and profitability.

The study on Kenyan firms suggest that more profitable firms takes the shortest time to collect

cash from their customers and high inventory levels reduce costs of possible interruptions in the

production process and loss of business due to scarcity of products. The study also reveals that the

longer a firm takes to pay its creditors, the more profitable it is M. Mathuva, (2010).

Usama (2012) extended the work of Rehman and Nasar regarding working capital management

while taking the sample of 18 companies from other food sector listed on Karachi Stock Exchange

for the period of 2006-2010. The researcher used different variables to measure working capital

management such as average collection period, inventory turnover in days, cash conversion cycle,

average payment period, debt ratio, firm size, current ratio, and financial asset to total asset. Using

common effect model and pooled least square regression, the results indicated that working capital

management has significant positive association with firm’s profitability and liquidity. He also

concluded that firm size and minimum inventory turnover in days has positive influence on firm’s

profitability.

In Malaysia, Mohamad and Noriza (2010) did their study by taking secondary data from

Bloomberg’s 72 listed companies for 5 years from 2003-2007 to derive the relationship empirically

Page | 22

between Working capital management and profitability. Study was done to check effects of

working capital components (such as CCC, CATA (Current Asset over Total Assets Ratio) ratio,

debt to asset ratio, CR and current liabilities over total asset ratio) on firm’s performance and

profitability measured by Tobin’s Q ratio, return on invested capital and ROA (Return on Assets).

Correlation and Multiple Regression results showed a significant negative relation between

working capital components and company’s performance.

Bhunia, Khan and Mukhuti (2011) provided the evidence with respect to the relationship between

liquidity and profitability of a firm. They took steel companies of private sector in India to assess

the management of liquidity as a factor of performance. They studied important liquidity indicators

and analyzed that optimal working capital management can be achieved by controlling the trade-

off between profitability and liquidity of a firm. Firm value is positively affected by optimal

working capital management so the investment in working capital must be satisfactory. They

concluded that liquidity and profitability are significantly positively associated.

Regarding to profitability, the empirical result suggests there is a significant positive relation

between the cash conversion cycle and profitability which is opposed to results found in the prior

studies (Deloof, 2003; Hyun-Han & Soenen, 1998; Lazaridis & Tryfonidis, 2006; Jose, et al.,1996;

Eljelly, 2004). But it is consistent with the study of Jeng-Ren, et al. (2006). Considering the

component of the cash conversion cycle, the regression result point out a significant positive

relation between number of days inventory and profitability which is opposed to the previous

studies (Deloof, 2003; Raheman & Nasr, 2007; Samiloglu & Demirgunes, 2008; Lazaridis &

Tryfonidis, 2006). The positive result with the cash conversion cycle points out that an increase in

profitability is associated with a rise in the cash conversion cycle. It shows that the profitable

companies tend to have the longer cash conversion cycle which indicates to inefficient working

capital management. The result contrasts with our expectation. This might be affected by either

inventory period, accounts receivable period or accounts payable period.

Chapter three: Research Methodology

3.1. Introduction

Page | 23

The preceding chapter opened a way to identify the literary work of people in relation to working

capital management and its impact on firm’s operational performance. On the contrary, this chapter

takes a step forward to demonstrate the research methodology by explaining the operational

definition, type of research to be employed along with the research approach and determining

sample design of the paper. It also addresses the data sources and ways of getting relevant data, its

collection instrument, and the mode of data analysis and synthesize. Hence, this chapter also deals

with ethical issues that the researcher must give a great attention in course of conducting the

research.

3.2. Operational Definition

The ultimate goal of working capital management is to get balances of current assets and current

liabilities right. So this section profoundly identifies an independent variable (IV) and dependent

variable (DV) of the paper as mentioned below:

3.2.1. Independent Variable (IDV)

The independent variable (IV) refers to the status of the presumed 'cause,' changes in which lead

to changes in the status of the dependent variable (Rosenthal & Rosnow, 1991, p. 71). However,

the independent variables of the paper will be working capital management through WCM

measurement indicators namely: Average Collection Period (ACP), Inventory Conversion Period

(ICP), Average Payment Period (APP), and Cash Conversion Cycle (CCC as detailed below in

brief with formula to calculate them:

3.2.1.1. Cash Conversion Cycle (CCC):

Business enterprises purchase inventories from suppliers on credit basis and then sell inventory on

credit as well to the customers. The CCC simply means the length of time (in days) that company

uses to sell inventory, collect receivables and pays its accounts payable. CCC is the difference

between sum of inventory period and receivable period (operating cycle) and payment period

(Cash conversion cycle = Average number of days accounts receivable+ Average number of days

inventory –Average number of days accounts payable).

Page | 24

3.2.1.2. Inventory Conversion Period (ICP):

The ICP also called days inventory outstanding and it gives a measure of days it takes for

company’s inventory to turn over, i.e., to be converted to sales, either as cash or accounts

receivable. Inventory period is calculated by dividing average inventory by cost of sales per day.

Formula:

Average number of days inventory = Average inventory /Cost of goods sold x 365

3.2.1.3. Average Collection Period (ACP)

This variable is defined as the number of the days which is needed to collect the receivables. In

other words, it is the average period for which receivables are outstanding. The information about

the net annual sales of the firm and the average beginning and ending receivables are used

(Mohammadi, 2007):

Formula:

Average number of days accounts receivable = Average accounts receivable/Annual credit Sales

x 365

3.2.1.4. Average Payment Period (APP)

This is the number of days a company takes to pay off the accounts payable. In other words, it

gives measure of how long it takes the company to pay its obligations to suppliers as they come

due. The average beginning and ending accounts payable are used to measure the average payment

period (Deloof, 2003)

Formula:

Average number of days accounts payable = Average accounts payable/Credit purchase x 365

3.2.2. Dependent Variable (DV)

Page | 25

Dependent Variables or outcome variables will be the variables used to measure the performance

of the firm. Although profitability ratios measure a firm’s overall efficiency and effectiveness in

generating profit, the liquidity will be considered as a factor of performance. However, the

dependent variable (DV)) will be operational performance in particular liquidity and profitability

of selected business firms through the measurement of liquidity and profitability ratios namely:

current ratio and quick ratio for liquidity measurement, as well as profit margin and return on

assets ratios for profitability measurement. In order to understand clearly the DVs, let us have

closer look at liquidity and profitability. Liquidity in the context of working capital management

means having enough cash or ready access to cash to meet all payment obligations when these fall

due, whereas profitability is calculated by establishing relationships between profit figures on the

one hand, and sales or assets on the other hand.

3.3. Research design

Research designs are plans or proposals and procedures for research that span the decisions from

broad assumptions to detailed methods of data collection and analysis (Creswell, 2009).

Regarding to this paper, the descriptive research design will be utilized in order to gather data

relevant to research topic, analysis the data and organize the information so as to reach proper

conclusion; and provide collective picture about the impact of working capital management

techniques on business operational performance. Furthermore, Seyom and Ayalew (1987) agreed

that descriptive survey method of research is more appropriate to gather several kinds of data on a

broad size to achieve the objective of the study. Based on that, the descriptive research design

will be used to describe the nature of the existing circumstances of the research problem.

3.4. Research Approaches

Page | 26

The type of investigation brings to light to determine the research approach in which to follow.

Therefore, the approach of the study will be quantitative particularly inferential quantitative

approach with the probabilistic systematic sampling technique.

3.5. Sample Design

Population sampling is the process of taking a subset of subjects that is representative of the entire

population. The sample must have sufficient size to warrant statistical analysis.

3.5.1. Population

The population is theoretically specified aggregation of research elements; while target population

is the complete group of particular population elements relevant to the research project.

Considering this study, the research population of the paper will be the privately owned businesses,

whereas target population shall be 41 merchandising wholesale companies which exist and operate

in Hargeisa.

3.5.2. Sample Frame

The list which holds the target population under the investigation in which sample size can drawn

is called Sample frame as shown below:

Table 1 Sample Frame

ID Name of the Company Location Type Of License

Sample Size (n), Population (N), K and Random

Start #

Selected Sample Units

46 Mohamed Ibrahim Guled( Daus Company) Hargeisa Wholesale N = 41

79 International Center Compnay Haregisa Whole Sale n = 12

85 Hussein Ahmed Jama(Tayosan Fuel Station)

Hargeisa Whole sale K= 3

100 Star Fuel Station Hargeisa Wholesale RSN(1,41) = 5

135 Ahmed Sulub Warsame Hargeisa Wholesale 1

149 Abdi Ibrahim Ismail( Solar Plane Company)

Hargeisa Whalesale

164 Hawa Sheikh Muse Gabilay Whole sale

Page | 27

200 Abdi Karim Nuur Hassan Hargeisa Whole Sale 2

221 Mohamed Hassan Kaahin(Kaahin F.Station)

Hargeisa Whole sale

231 Awl Ahmed Hussien(Africa Fuel Station) Hargeisa Wholesale

232 Maxamed Xirsi Yousuf(Hamze interprise) Hargeisa Wholesale A 3

239 Mohamed Awnur Mohamed Hargeisa Wholesale

240 Mohamoud Mohamed Kahin(Nasteex0 F.ST)

Hargeisa Wholesale

243 Ubah Mohamed Duale (Degaan Trading &Hotel)

Hargeisa Wholesale 4

253 Mohamed Hussein Ahmed Hargeisa Wholesale

268 Kaiseh Omer Hassan Hargeisa Wholesale

293 Mohamed Ahmed Mohamed (Som.F.st) Hargeisa Wholesale 6

296 Zayid Ali Mohamed Jama(Zayid Style) Hargeisa Wholesale C

306 Kosar Shabel Ali (Xaraf Gas Station) Hargeisa Wholesale

322 Ahmed Saed Farah ( Jabali General Trading Co.)

Hargeisa Wholesale 7

325 Idiris Mohamed Abdallah ( Brothers) Hargeisa Wholesale

328 Faisal Mohamed Ali Samale (Germany Pharmeceuical

Hargeisa Wholesale

340 Abdirashid Dahir Habane Hargeisa Wholesale 8

353 Abdil Karim Aw Adan Hargeisa Wholesale

358 Muhumed Sulub (Tayo Maal Workshop Co.)

Hargeisa Wholesale

370 Faizal H Yousuf Aden ( Liban Petrolium&F.Station)

Hargeisa Wholesale 9

373 Ahmed Nur Mohamed (Barwaqo Fuel Station)

Hargeisa Wholesale

388 Abdikarim Mohamed Adan (Gacanle Fuel Station)

Hargeisa Wholesale

389 Adan Ilmi Abdallah(Mabruk Vegitables) Hargeisa Wholesale 10

390 Ahmed Omer Ali (Googaa Cigale ) Hargeisa Wholesale

391 Mohamed Matan Jama(Commercial Honey Trading)

Hargeisa Wholesale

560 Sacaada General Trading Company Hargeisa Wholesale 11

580 Mohamed Muse Shiraqle (Shiraqleh Fuel Station)

Hargeisa Wholesale

679 Abdirahman Nour Egal( Home of Educational Material and Accessories )

Hargeisa Wholesale

728 Ahmed Sulub Warsame (Sulub Fuel Station)

Hargeisa Wholesale 12

751 Soma Yaman Hargeisa Wholesale

762 Qani Abdi Alin ( Dheeman Tailor and Supermarket)

Hargeisa Wholesale

771 Surad Electric Connection Hargeisa Wholesale

Page | 28

794 Mohamed Hussein Ahmed (National Fuel Station)

Hargeisa Wholesale

818 Star Group of Companies Hargeisa Wholesale

3.5.3. Sample Size

The sample size simply means number of research elements in which the researcher should

communicate in the course of gathering the primary data; the sample size should also possess the

characteristics of efficiency, representativeness, relevance, reliability and flexibility in order to

provide comprehensive snapshot which actually can reflect the real characteristics of entire

population under the question. So it must be selected in a scientific way. However, the rule of

thumb says if the population under given study is less than 1000 take 30% as a sample. In this

context, the target population will be 41 companies which is less than 1000. Therefore, the sample

size of this study has been determined using rule of thumb and it becomes 41*.3= 12 wholesale

businesses exist and operate in Hargeisa city.

3.5.4. Sampling Techniques

After determining sample size from the target population, it is rational to identify sample units

using sampling techniques. Consequently, the sampling technique of the study will be probability

sampling particularly systematic random sampling so as to choose actual, final sampling units to

be contacted in the course of conducting the research especially the primary data collection phase.

3.6. Source of Data

3.6.1. Primary Data

The primary data will be generated from the selected final units or respondents of the sample size

under the examination, which are sampled 12 wholesale companies.

3.6.2. Secondary Data

According to level ten designs (2006) describes secondary research as information gathered

through literature, publication and other reasonable sources. Hence, the secondary data is often

Page | 29

comparatively quite simple and easier to collect than in primary research. In this study; secondary

research draws attention to the collection of information relevant to the topic through literature

review of publication, Books, Journal articles, academic researches and other sensible sources.

3.7. Data Collection Techniques

In this context; the data collection methods are techniques and tools used for gathering primary

data from given issue under study. However, the questionnaire will be data collection method used

as a primary data collection mechanism.

3.8. Data Analysis and presentation

Globally, it is a consensus or widely accepted opinion that the data are not valuable themselves

and fruitful for making transparent and evidence based decisions across each particular situations

under the issue unless the data converted into information in the course of technical analysis.

Therefore, the quantitative data will be synthesized and analyzed by using descriptive type

analysis with the help and utilization of statistical package for social science (SPSS) and excel

spreadsheet. Furthermore, the analytical will be presented in a tabular and chart form along with

interpretation.

3.9. Ethical Consideration

Ethical issue is profoundly critical in doing research and special consideration should be given.

Based on this, many authors had addressed it and proposed several ethical issues to be

concentrated on. For instant, Creswel (2003) states that the researcher has an obligation to respect

Page | 30

the rights, needs, values and desires of the informants. However, the researcher must avoid

disclosure of confidential information, involvement without consent, any form of

misrepresentation and deceiving research participants e.g. concealing the purpose of the research.

The researcher also should respect religion, culture, norms, values and individual behavior and

attitude as well.

Chapter Four: RESULTS AND DISCUSSION AND INTERPRETATION

4.1. Introduction

In this chapter, presents empirical results from quantitative data analysis using

combination of SPSS and excel spread sheet. The chapter covers analysis of

variables of paper and investigates associations between and among them using

selected key working capital ratios including cash convention cycle, accounts

receivable days, inventory days, account payable days to measure independent

variables. Likewise, current ratio and profit margin ratio for measurement

dependent variables, the liquidity and profitability. Total the valid response of

respondents is 16 which corresponding to 84.2% while 3

4.2. Descriptive Statistics

Descriptive analysis shows the mean, and standard deviation of the different

variables of interest in the study. It also presents the minimum and maximum

values of the variables which help in getting a picture about the maximum and

minimum values a variable has achieved. Moreover, the descriptive analysis can

be categorized into three sections; the first section involves general knowledge

and competence of managers in working capital management relative to the

business liquidity and profitability, the section deals with indicators used to

measure variables of the research and the last section emphasizes correlation

between independent and dependent variables.

Page | 31

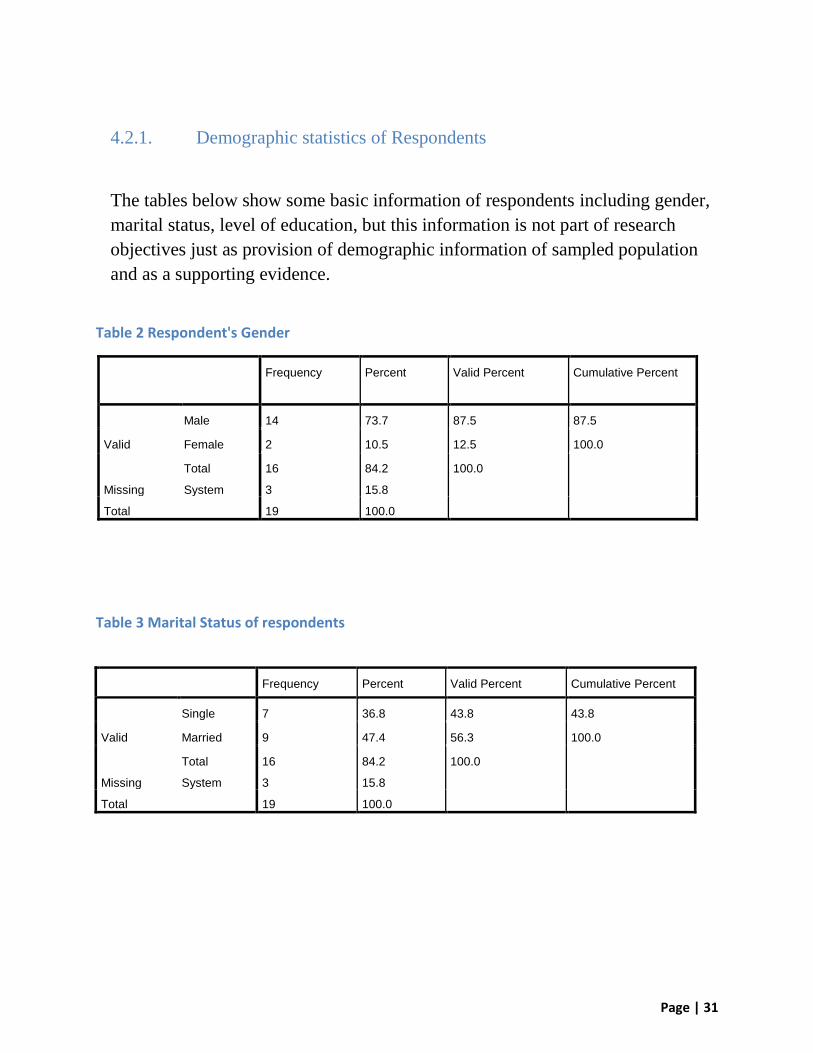

4.2.1. Demographic statistics of Respondents

The tables below show some basic information of respondents including gender,

marital status, level of education, but this information is not part of research

objectives just as provision of demographic information of sampled population

and as a supporting evidence.

Table 2 Respondent's Gender

Frequency Percent Valid Percent Cumulative Percent

Valid

Male 14 73.7 87.5 87.5

Female 2 10.5 12.5 100.0

Total 16 84.2 100.0

Missing System 3 15.8

Total 19 100.0

Table 3 Marital Status of respondents

Frequency Percent Valid Percent Cumulative Percent

Valid

Single 7 36.8 43.8 43.8

Married 9 47.4 56.3 100.0

Total 16 84.2 100.0

Missing System 3 15.8

Total 19 100.0

Page | 32

Figure 3 Age categories of respondents

Table 4 the position of respondents in their firms (What is your current position in your firm?)

Frequency Percent Valid Percent C.Percent

Valid

Accountant 8 42.1 50.0 50.0

Financial Manager 1 5.3 6.3 56.3

Sales Manager 2 10.5 12.5 68.8

Owner and Manager 5 26.3 31.3 100.0

Total 16 84.2 100.0

Missing System 3 15.8

Total 19 100.0

Page | 33

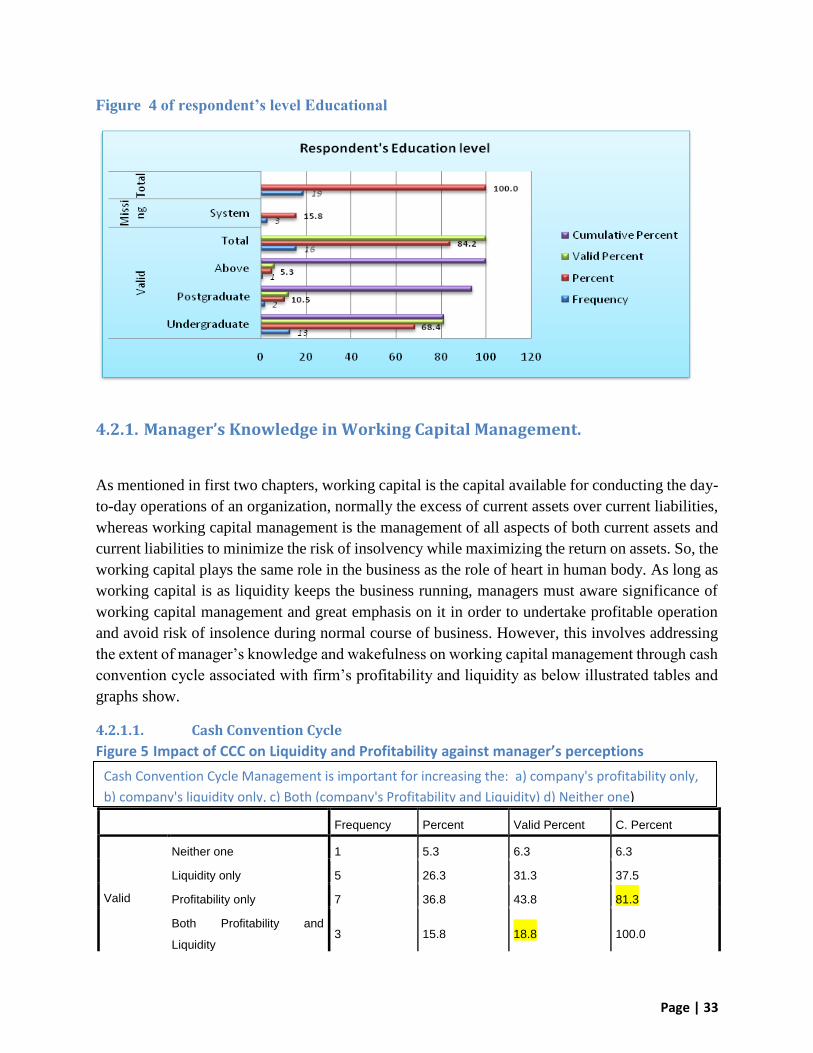

Figure 4 of respondent’s level Educational

4.2.1. Manager’s Knowledge in Working Capital Management.

As mentioned in first two chapters, working capital is the capital available for conducting the day-

to-day operations of an organization, normally the excess of current assets over current liabilities,

whereas working capital management is the management of all aspects of both current assets and

current liabilities to minimize the risk of insolvency while maximizing the return on assets. So, the

working capital plays the same role in the business as the role of heart in human body. As long as

working capital is as liquidity keeps the business running, managers must aware significance of

working capital management and great emphasis on it in order to undertake profitable operation

and avoid risk of insolence during normal course of business. However, this involves addressing

the extent of manager’s knowledge and wakefulness on working capital management through cash

convention cycle associated with firm’s profitability and liquidity as below illustrated tables and

graphs show.

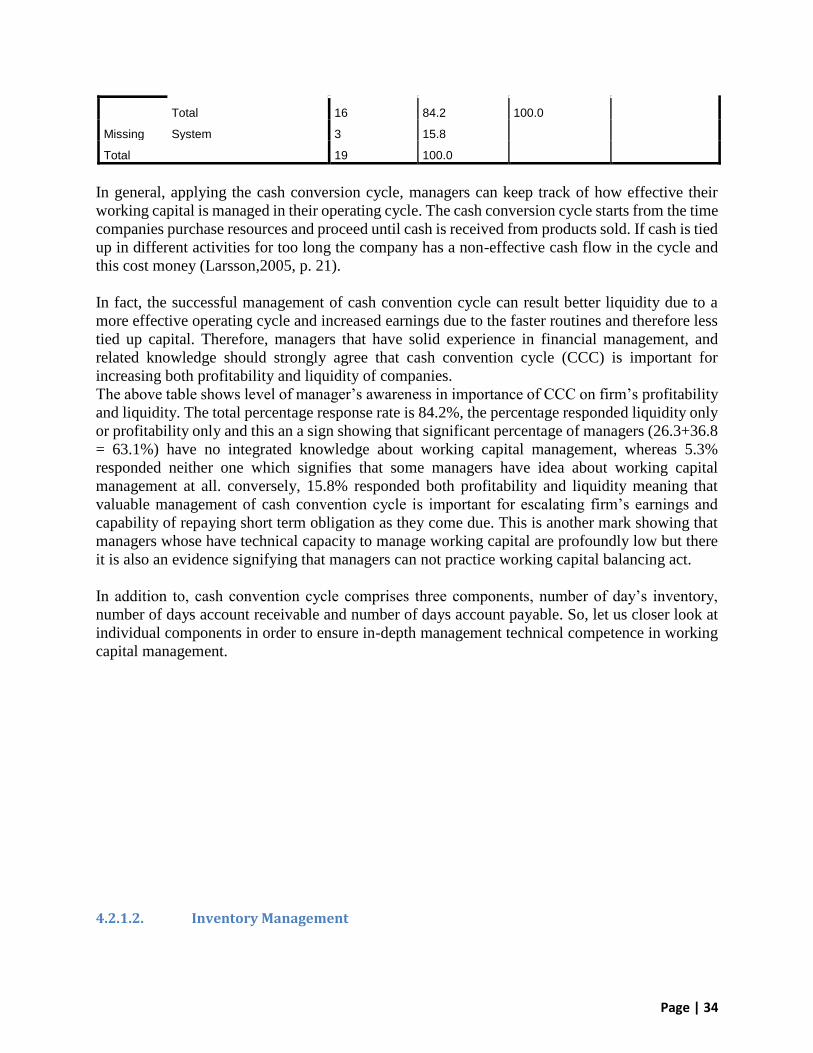

4.2.1.1. Cash Convention Cycle

Figure 5 Impact of CCC on Liquidity and Profitability against manager’s perceptions

Frequency Percent Valid Percent C. Percent

Valid

Neither one 1 5.3 6.3 6.3

Liquidity only 5 26.3 31.3 37.5

Profitability only 7 36.8 43.8 81.3

Both Profitability and

Liquidity 3 15.8 18.8 100.0

Cash Convention Cycle Management is important for increasing the: a) company's profitability only,

b) company's liquidity only, c) Both (company's Profitability and Liquidity) d) Neither one)

Page | 34

Total 16 84.2 100.0

Missing System 3 15.8

Total 19 100.0

In general, applying the cash conversion cycle, managers can keep track of how effective their

working capital is managed in their operating cycle. The cash conversion cycle starts from the time

companies purchase resources and proceed until cash is received from products sold. If cash is tied

up in different activities for too long the company has a non-effective cash flow in the cycle and

this cost money (Larsson,2005, p. 21).

In fact, the successful management of cash convention cycle can result better liquidity due to a

more effective operating cycle and increased earnings due to the faster routines and therefore less

tied up capital. Therefore, managers that have solid experience in financial management, and

related knowledge should strongly agree that cash convention cycle (CCC) is important for

increasing both profitability and liquidity of companies.

The above table shows level of manager’s awareness in importance of CCC on firm’s profitability

and liquidity. The total percentage response rate is 84.2%, the percentage responded liquidity only

or profitability only and this an a sign showing that significant percentage of managers (26.3+36.8

= 63.1%) have no integrated knowledge about working capital management, whereas 5.3%

responded neither one which signifies that some managers have idea about working capital

management at all. conversely, 15.8% responded both profitability and liquidity meaning that

valuable management of cash convention cycle is important for escalating firm’s earnings and

capability of repaying short term obligation as they come due. This is another mark showing that

managers whose have technical capacity to manage working capital are profoundly low but there

it is also an evidence signifying that managers can not practice working capital balancing act.

In addition to, cash convention cycle comprises three components, number of day’s inventory,

number of days account receivable and number of days account payable. So, let us closer look at

individual components in order to ensure in-depth management technical competence in working

capital management.

4.2.1.2. Inventory Management

Page | 35

Figure 6 impact of inventory management on liquidity and profitability against manager’s insights

The management of inventory is one of the more challenging tasks compared to

all other components in the cycle. So managers pay attention to minimize the

inventory as much as possible in order to shorten the cash conversion cycle and

reduce costs. Regarding above graph, 31.6% answered neither one and they have

no idea concerning with importance of inventory management on company’s

liquidity and profitability, while 36.9% have no integrated knowledge and only

15.8% (those responded both) have technical capacity to deal with this issue.

Nevertheless, inventory involves major working capital investment and therefore

levels need to be very tightly controlled, but this evidence indicates managers not

capable to employ inventory balancing act which is significant to reduce

inventory to the lowest possible level and to ensure sufficient inventory at the

same time.

Page | 36

4.2.1.3. Account Receivable management

Figure 7 impact of Account receivable on liquidity and profitability against manager’s perceptions

Companies depend more or less on their account receivables to finance some if not all of their

payables and they should therefore attempt to reduce their credit time to customers as much as

possible. The credit time runs from the invoice date until the due date of the invoice. The reason

for shortening the credit period is due to the fact that longer credit time to customers includes the

unfavorable effect that it keeps companies from benefiting the capital inflow that they are

expecting from sales. Observing the above graph, the percentage of valid response is 84.2% where

63.1% (26.3% liquidity only +36.8% profitability only =63.1%) have no integrated financial

management knowledge. moreover, this is also signal showing that managers not able to apply

account receivable balancing act which is useful to undertake two opposite tasks (collecting

receivables very quickly as possible and expanding the credit period to customers) at same time.

Besides, only 21.1% (those responded both) have technical capacity. This is low rate indicating

that the most companies are exposing themselves to a higher risk of ending up in an unstable

financial situation and less profitable operations. Further, no one has responded ‘neither one’ that

is way not visible in the graph. More optimistically, if it is boiled down, this can be interpreted

growing accounting receivable management knowledge compared to other components in the

cycle.

Page | 37

4.2.1.4. Account Payable management

Figure 8 impact of Account payable management on liquidity and profitability against manager’s perceptions

Regarding to previous study, the general guidelines for optimizing the managing of account

payables involve the timing of payments. Companies should try prolonging the time of payment

as long as possible as they can use the advantage of their suppliers financing their investments

until payment has been made. Another argument for prolonging the time for payment is that the

producing companies, for example, need some time to convert their purchased raw material into

products they can get sold and get cash in return (Maness and Zietlow, 2005, . 235-238). Based on

that, Account payable management has a great influence to both liquidity and profitability.

Considering the graph above, 42.1% (neither one) of respondents answered that account payable

management has no consequence to entire working capital management; so this can restrict

companies to utilize their supplier’s cheap finance through prolonging the time of payment as

possible until the maturity date on the basis of account payable balancing act, rather they might

pay it very quickly prior to due date which may lead another unfavorable financial situation like

prolonging cash convention cycle, risk of insolvency and bad reputation cash crises manner. in

contrast, 25.5% (15.8% liquidity only +10.5% profitability only = 25.5%) have no integrated

financial management knowledge. on the other hand, only 15.8% (those responded both) have

Page | 38

technical competence and this indicates that the most companies are exposing themselves to a

higher risk of ending up in an unstable financial situation and less profitable operations.

4.2.2. Analysis for measurement indicators

This section involves to measure cash convention cycle and its components so as to be able to

evaluate impact of working capital management on business operational performance. The table

shows variables those have been directly calculated from raw data gathered from sampled

wholesale companies during data collection using the following formulas detailed in chapter three:

Category1: Independent Variables

Cash conversion cycle = Average number of days accounts receivable+ Average number of days

inventory –Average number of days accounts payable

Average number of days inventory = Average inventory /Cost of goods sold x 365

Average number of days accounts receivable = Average accounts receivable/Annual credit Sales

x 365

Average number of days accounts payable = Average accounts payable/Credit purchase x 365

Category2: dependent Variables

Current Ratio = Current Assets/ Current Liabilities and Profit Margin Ratio = Net Profit/ Sales

Table 5 Summary of all Variables of paper

Independent Variables Dependent Variables

Company Names

ACP ICP APP CCC C R P MR ROA

Company001 87 109.6 181 15.6 4.95 0.4405 N/A

Company002 97 69.55 141 25.55 1.63 0.40 N/A

Company003 67 69.3 87 49.3 1.09 0.39 N/A

Company004 121 97 165 53 4.02 0.41 N/A

Company005 150 85 179 56 0.92 0.39 N/A

Company006 75 77.3 94 58.3 1.98 0.35 N/A

Company007 82 84.3 103 63.3 1.05 0.29 N/A

Company008 102 204.3 256 50.3 1.33 0.31 N/A

Company009 216 93 152 157 0.994 0.28 N/A

Company010 105 107.3 53 159.3 0.15 0.25 N/A

Page | 39

Company011 143 105 72 176 0.13 0.23 N/A

Company012 171 107 50 228 0.21 0.20 N/A

Company013 98 150 60 188 0.26 0.31 N/A

Company014 127 75 39 163 0.22 0.38 N/A

Company015 154 142.3 65 231.3 0.19 -0.09 N/A

Company016 93 191 234.61 49.39 1.02 0.41 N/A

Company017 Rejected Rejected Rejected Rejected Rejected Rejected Rejected

Company018 Rejected Rejected Rejected Rejected Rejected Rejected Rejected

Company019 Rejected Rejected Rejected Rejected Rejected Rejected Rejected

Table 1 shows the descriptive statistic of independent and dependent variables for the entire sample

of 19 wholesale companies in which exist and operate in Hargeisa. The first four variables are

measured in the unit of days.

The cash conversion cycle as we use as our independent variable has a mean of 107.71 days. This

explains that it takes in average 107.71 days to convert capital tied up in working capital into cash.

Hence, the mean of all three variables of in the CCC are compatible as the lay between 110.43

days and 120.73. The minimum amount of days it takes for the capital in the cash conversion cycle

to convert into cash is 16 days and the maximum amount of days is 231.

The components of the cash conversion cycle are the following three variables; the number of days

inventory, the number of days accounts receivable and the number of days of accounts payable.

The table shows that minimum number of days account receivable and minimum number of days

inventory are 67 days and 69 days respectively. Even though the minimum number of days it takes

to convert inventories into sales and collects relative account receivable from customers is very

close to each other, the minimum number of days account payable is 39 days and this indicates

that some companies have limited time to repay short term obligations to their suppliers.

Table 6 Descriptive Statistics for all Samples

Cash Convention

Cycle

Average

Collection Period

Inventory

Convention

Period

Average

Payment Period

Current Ratio Profit Margin

Ratio = Net

N Valid 16 16 16 16 16 16

Missing 3 3 3 3 3 3

Mean 107.71 118.00 110.43 120.73 1.25900 .30941

Std. Deviation 75.023 40.038 41.203 67.945 1.391614 .128537

Minimum 16 67 69 39 .130 -.090

Maximum 231 216 204 256 4.950 .441

Page | 40

Studying the maximum number of days, these are not as compatible for the three variables as the

minimum number of days. The number of day’s accounts payable has the highest maximum with

256 days followed by the number of days account receivable that has a maximum of 116 days. The

number of day’s inventory has the lowest maximum with 104 days. Observing the mean in the

table, the number of day’s accounts receivable has a mean of 118 days and the number of days

accounts payable has a mean on 120.73 days. That fact that these variables have values close to

each other is remarkable as their maximum number of days differs greatly between them as one of

them has the second lowest maximum and the other one the highest. The mean for the number of

day’s inventory is 110.43 days.

The profitability, given by net profit/ sales is measured in the unit of percent and for our sample

the maximum profitability is 44.1%, a minimum of -9 % and a mean of 30.9%. This shows that

the sampled companies conduct printable operations on average, but some of them are running

with los instead of generating profit.

Regarding to current ratio, order to manage current liabilities with enough current assets the level

of the ratio should stay above 1 which both the mean and the maximum are for this sample. The

mean stays on a level above one which is 1.259, while the maximum comes up around 4.950 which

signifies that the current assets are approximately five times greater than the current liabilities.

However, the current ratio has a minimum of 0.130 in which designates that some companies not

capable to pay current liabilities as they come due which can result risk of insolvent.

4.2.3. Correlations

4.2.3.1. Relationship between CCC and Profitability

Figure 9 correlation between CCC and Profitability

Page | 41

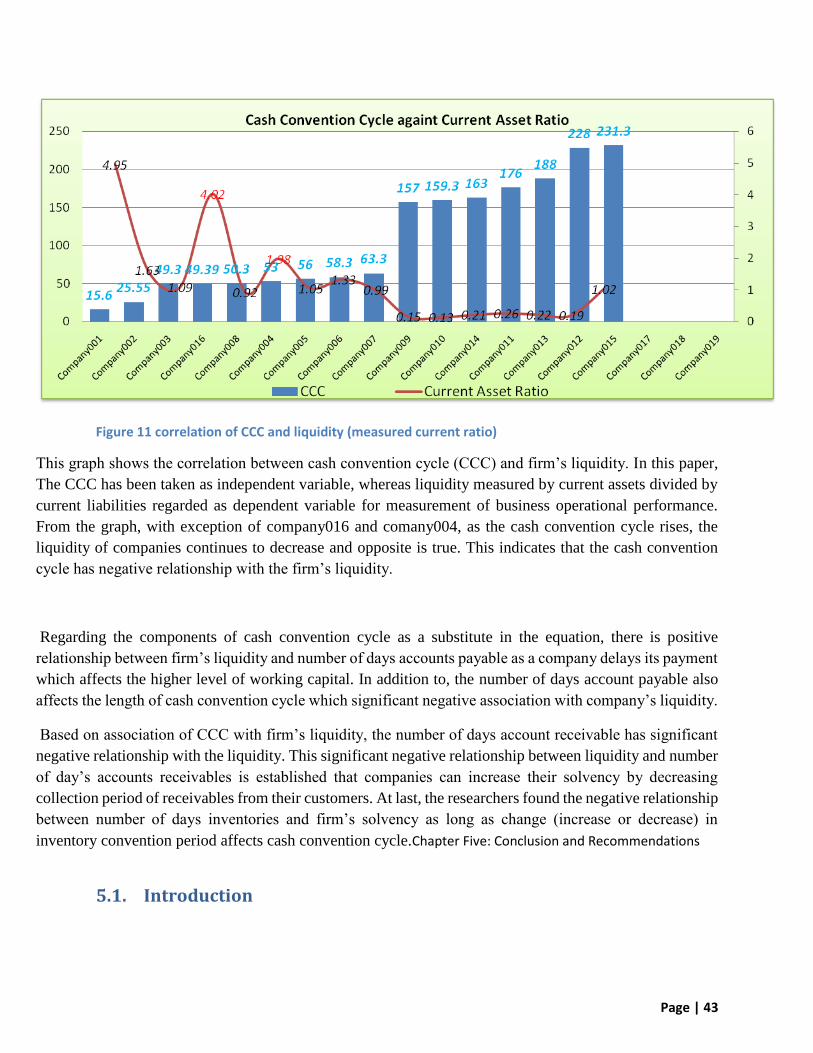

This graph shows the correlation between cash convention cycle (CCC) and profitability. In this paper,

The CCC has been taken as independent variable, whereas profitability measured by Profit margin ratio

has been considered as dependent variable. From the graph, the company001 and company002 have

lowest cash conventions cycles which are 15.6 days and 25.55 days correspondingly with the highest

profitability of 44% and 40% in that order. On the contrary, company012 and company015 have CCC of

228 days 231 days respectively with lowest profitability of 20% and -9% respectively.

Thus, as the cash convention cycle rises, the profitability of companies continues to decrease and

opposite is true. The exception of company014 and company013 showed slightly opposite pattern and

this can be caused by the effect of other variables assumed as consistent. Therefore, the cash convention

cycle and profitability have negative relationship which supporting the work of Lazaridis and Tryfonidis

(2006) investigate the relationship between working capital management and company’s profitability

measured by gross operating profit on 131companies listed in the Athens Stock Exchange for the period

from 2001 to 2004. Regression result shows the negative relationship between cash conversion cycle and

profitability.

4.2.3.2. Account receivable and Firm’s Profitability

Regarding the components of cash convention cycle as a substitute in the equation, the number of day’s

accounts payables, number of days accounts receivable and number of day’s inventories for cash conversion

cycle. Observing the below illustrated graph, although there is considerable variation in trends of the two

variables, the most companies that have lower average collection period are the most profitable. Based this

trends and with the light of association of CCC with firm’s profitability, the number of days account

receivable has significant negative relationship with the gross operation profit. This significant negative

relationship between gross operating profit and number of day’s accounts receivables is demonstrated that

companies can increase their profitability by decreasing credit term giving to their customers.

Page | 42

Figure 10 correlation of average collection period with profit margin ratio

4.2.3.3. Account Payable and Inventory against Profit Margin Ratio

There is positive relationship between gross operating profit and number of days accounts payable as a