Embed Size (px)

Citation preview

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 1

Planning , Budgeting and Forecasting 20%

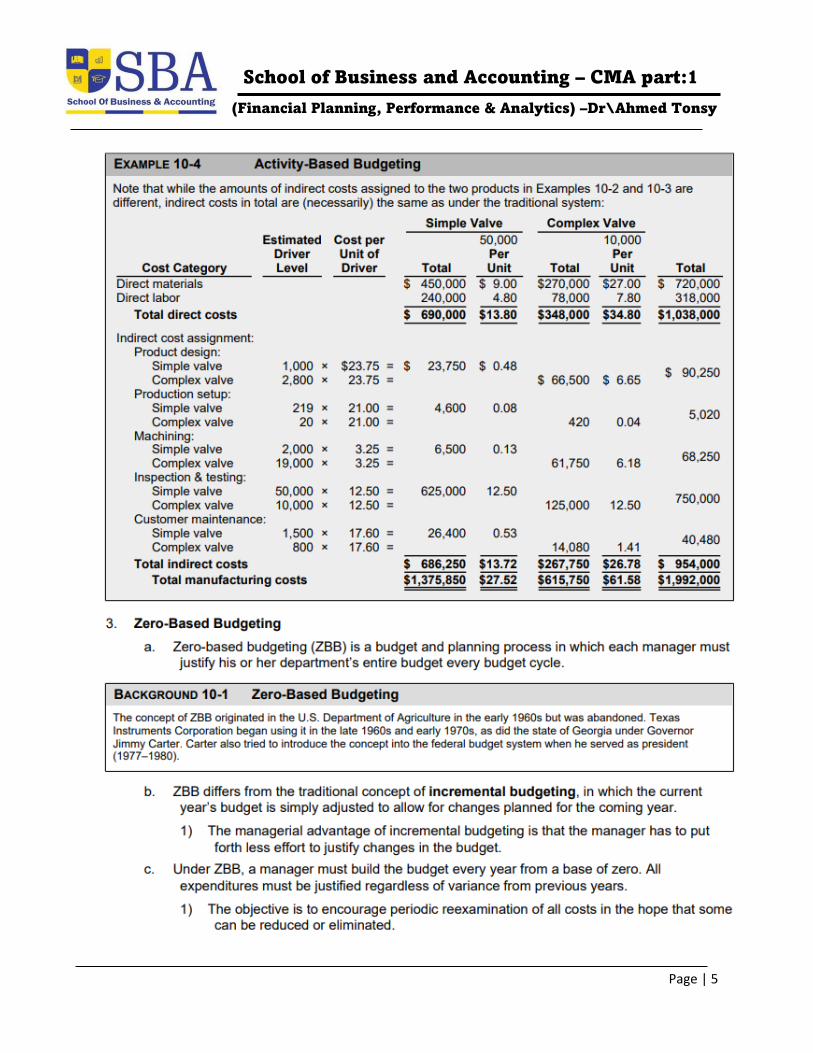

Class (2) : Standard cost , Budget Methodologies & Master Budget Note: Test bank for class 2 include 3 file at telegram group 10.2 standard Cost. 20.3 the master Budget 10.4 Budget methodologies

First : Cost Standards

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 2

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 3

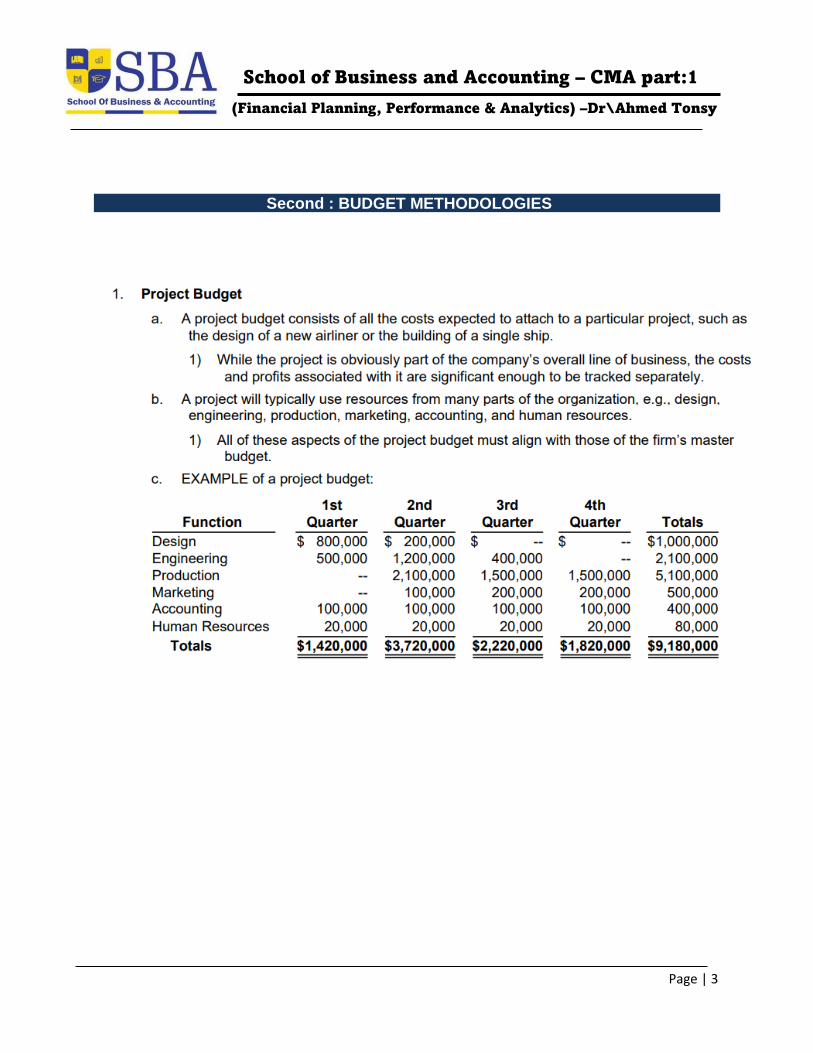

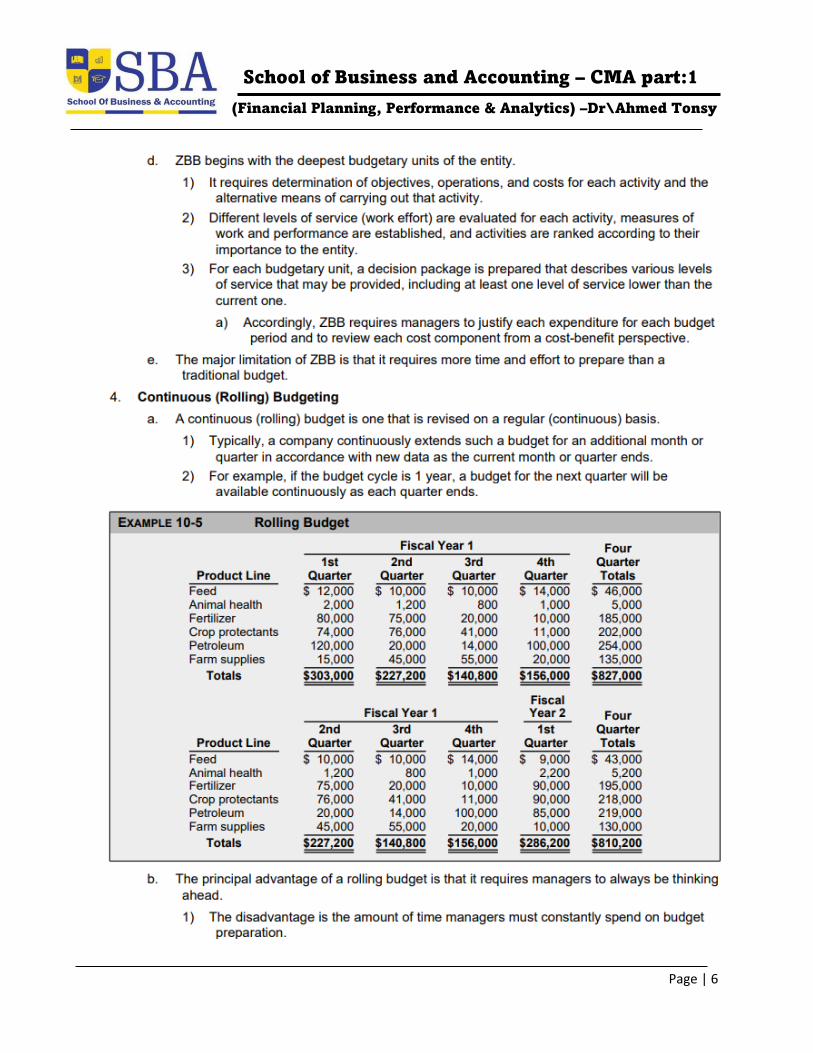

Second : BUDGET METHODOLOGIES

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 4

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 5

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 6

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 7

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 8

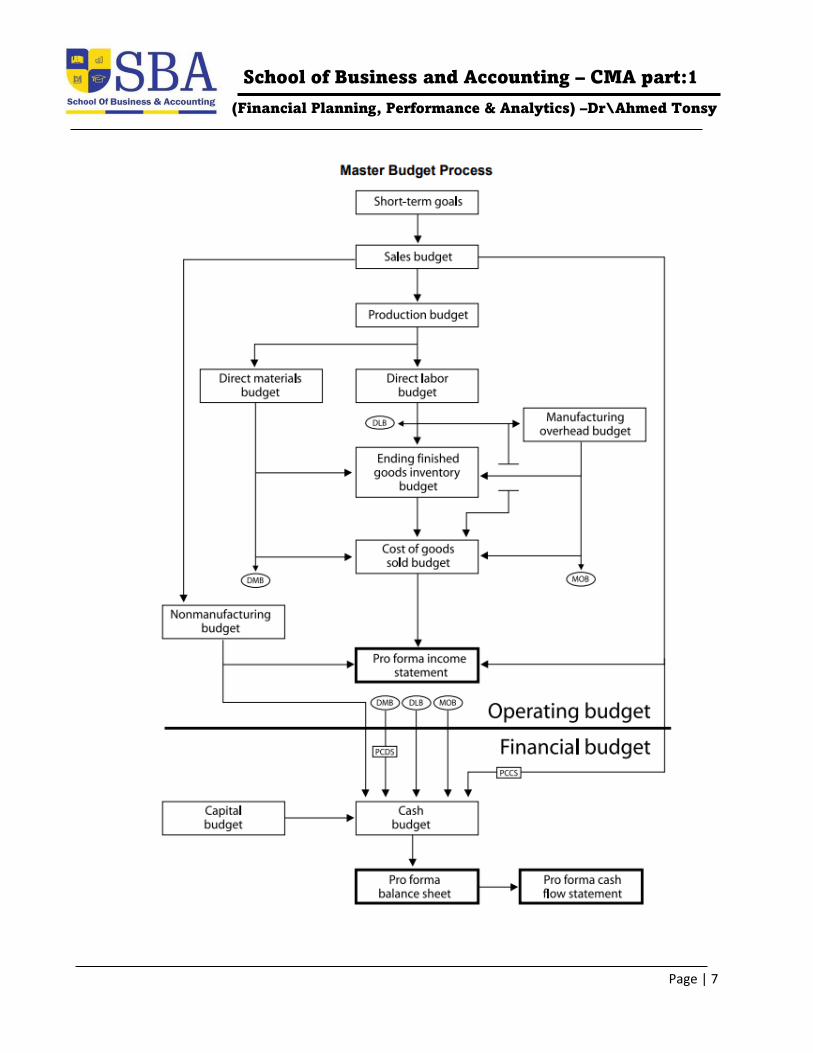

Master Budget

LEARNING OBJECTIVE

1

Describe the master budget and explain its benefits

1.1 A budget is (a) the quantitative expression of a management’s proposed plan for

a specified period, and (b) an aid to coordinate what needs to be done to implement the plan.

1.2 The master budget expresses management’s operating and financial plans for a

specified period (usually a fiscal year). The master budget is actually a series of budgets including a set of budgeted financial statements (sometimes called pro forma statements).

A. Operating budget 1. Sales budget 2. Production budget—Based on desired inventory levels 3. Direct materials purchases budget—Based on desired inventory levels 4. Direct labor budget 5. Manufacturing overhead budget 6. Cost of goods manufactured budget 7. Cost of goods sold budget 8. Pro forma income statement B. Financial Budget 1. Capital assets budget 2. Financing needs schedule 3. Cash budget 4. Pro forma balance sheet 5. Pro forma statement of cash flows

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 9

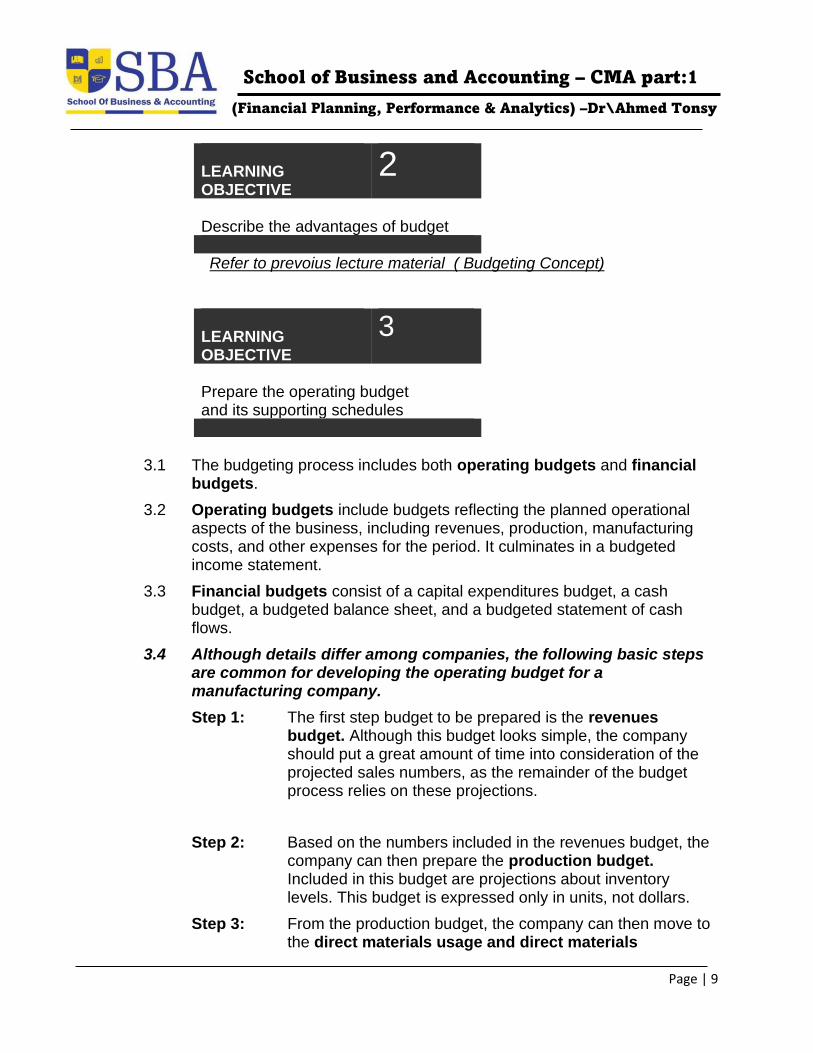

LEARNING OBJECTIVE

2

Describe the advantages of budget Refer to prevoius lecture material ( Budgeting Concept)

LEARNING OBJECTIVE

3

Prepare the operating budget and its supporting schedules

3.1 The budgeting process includes both operating budgets and financial budgets.

3.2 Operating budgets include budgets reflecting the planned operational aspects of the business, including revenues, production, manufacturing costs, and other expenses for the period. It culminates in a budgeted income statement.

3.3 Financial budgets consist of a capital expenditures budget, a cash budget, a budgeted balance sheet, and a budgeted statement of cash flows.

3.4 Although details differ among companies, the following basic steps are common for developing the operating budget for a manufacturing company.

Step 1: The first step budget to be prepared is the revenues budget. Although this budget looks simple, the company should put a great amount of time into consideration of the projected sales numbers, as the remainder of the budget process relies on these projections.

Step 2: Based on the numbers included in the revenues budget, the company can then prepare the production budget. Included in this budget are projections about inventory levels. This budget is expressed only in units, not dollars.

Step 3: From the production budget, the company can then move to the direct materials usage and direct materials

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 10

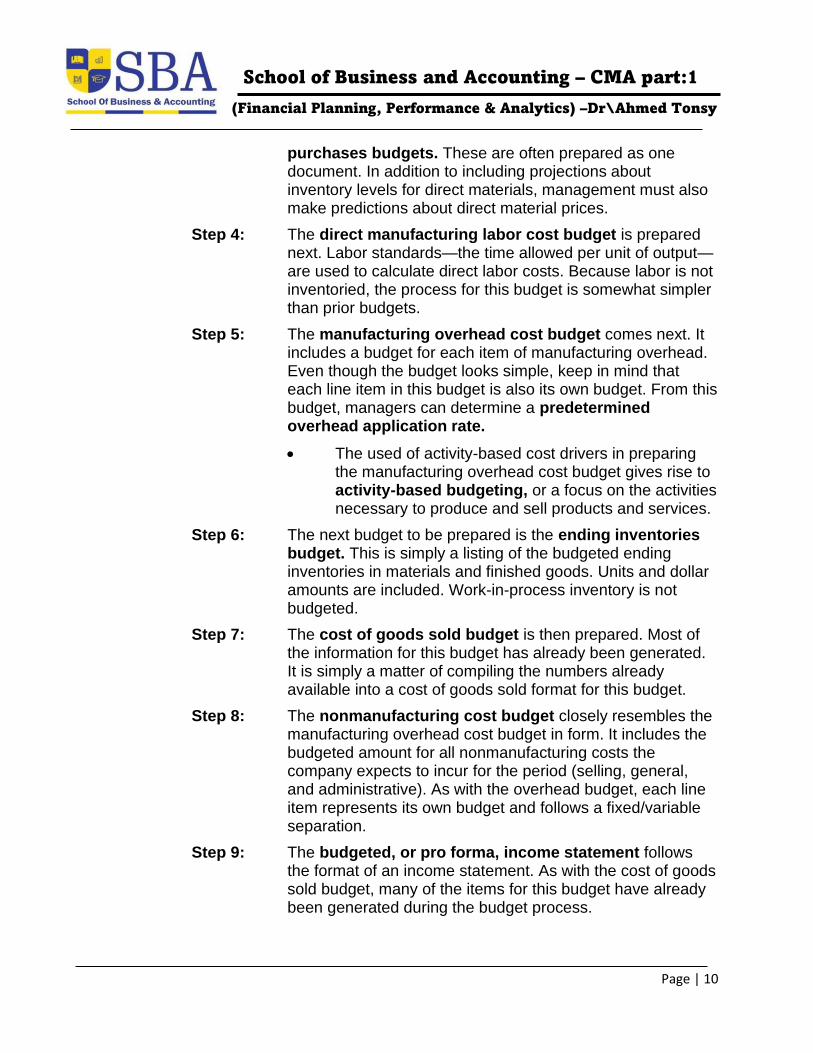

purchases budgets. These are often prepared as one document. In addition to including projections about inventory levels for direct materials, management must also make predictions about direct material prices.

Step 4: The direct manufacturing labor cost budget is prepared next. Labor standards—the time allowed per unit of output—are used to calculate direct labor costs. Because labor is not inventoried, the process for this budget is somewhat simpler than prior budgets.

Step 5: The manufacturing overhead cost budget comes next. It includes a budget for each item of manufacturing overhead. Even though the budget looks simple, keep in mind that each line item in this budget is also its own budget. From this budget, managers can determine a predetermined overhead application rate.

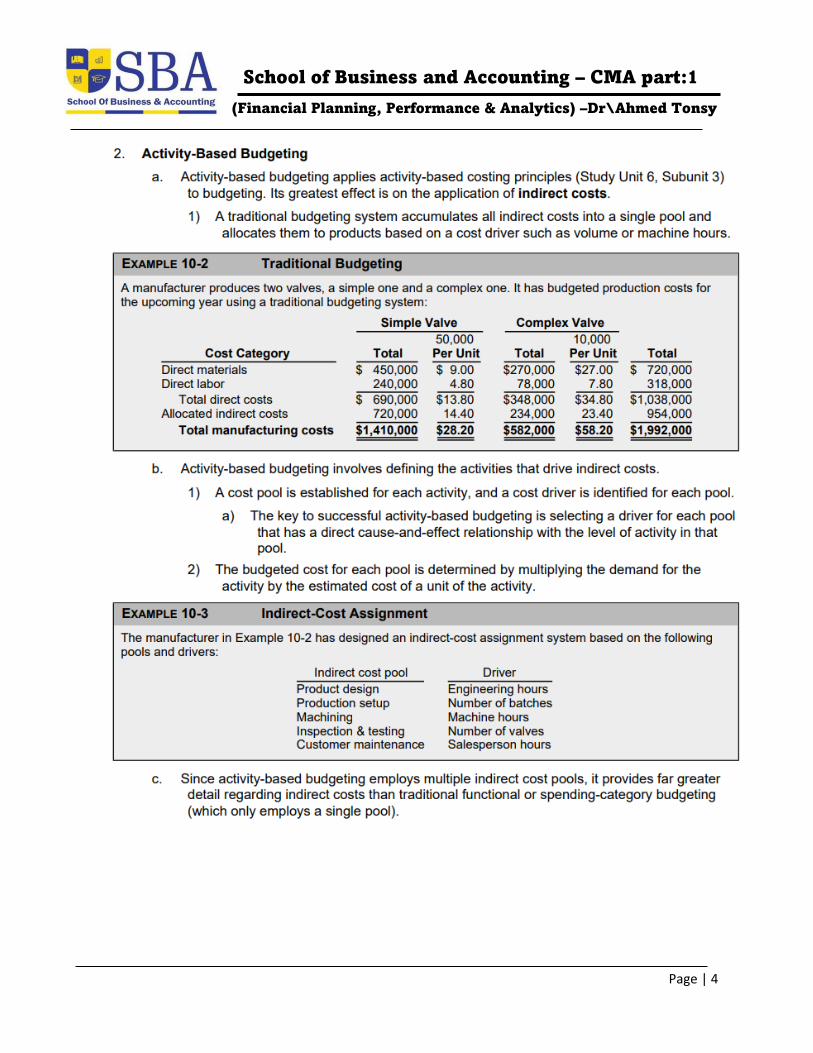

• The used of activity-based cost drivers in preparing the manufacturing overhead cost budget gives rise to activity-based budgeting, or a focus on the activities necessary to produce and sell products and services.

Step 6: The next budget to be prepared is the ending inventories budget. This is simply a listing of the budgeted ending inventories in materials and finished goods. Units and dollar amounts are included. Work-in-process inventory is not budgeted.

Step 7: The cost of goods sold budget is then prepared. Most of the information for this budget has already been generated. It is simply a matter of compiling the numbers already available into a cost of goods sold format for this budget.

Step 8: The nonmanufacturing cost budget closely resembles the manufacturing overhead cost budget in form. It includes the budgeted amount for all nonmanufacturing costs the company expects to incur for the period (selling, general, and administrative). As with the overhead budget, each line item represents its own budget and follows a fixed/variable separation.

Step 9: The budgeted, or pro forma, income statement follows the format of an income statement. As with the cost of goods sold budget, many of the items for this budget have already been generated during the budget process.

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 11

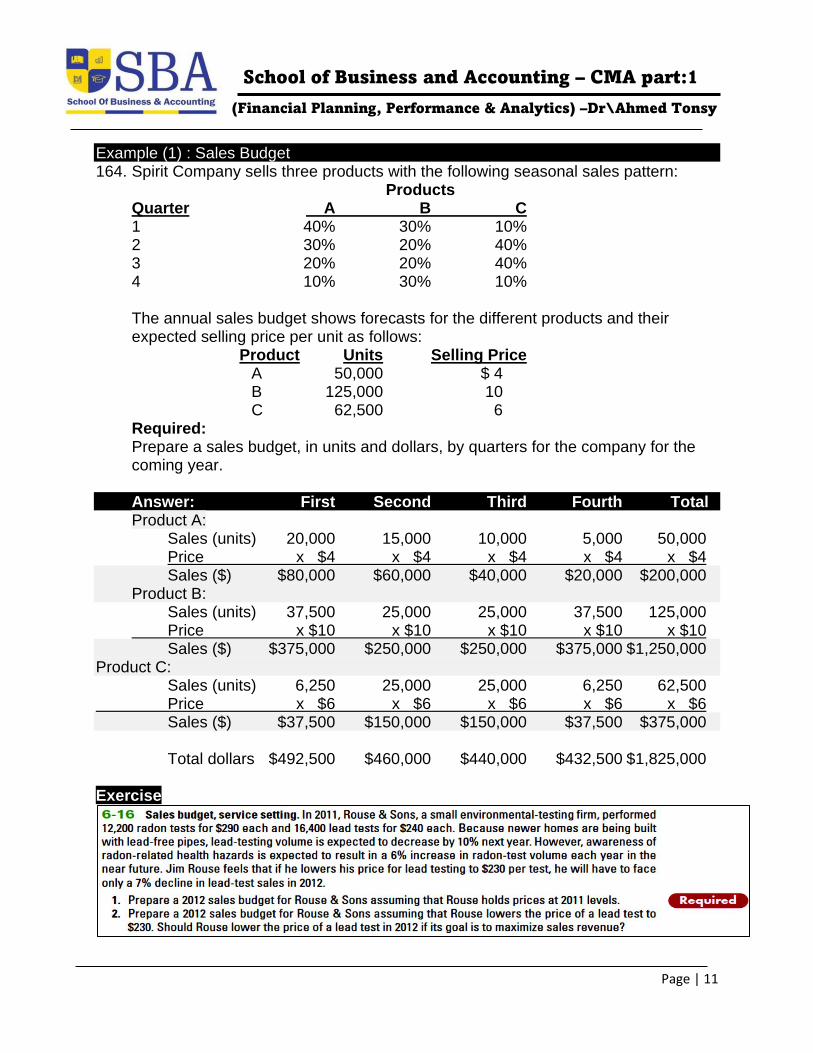

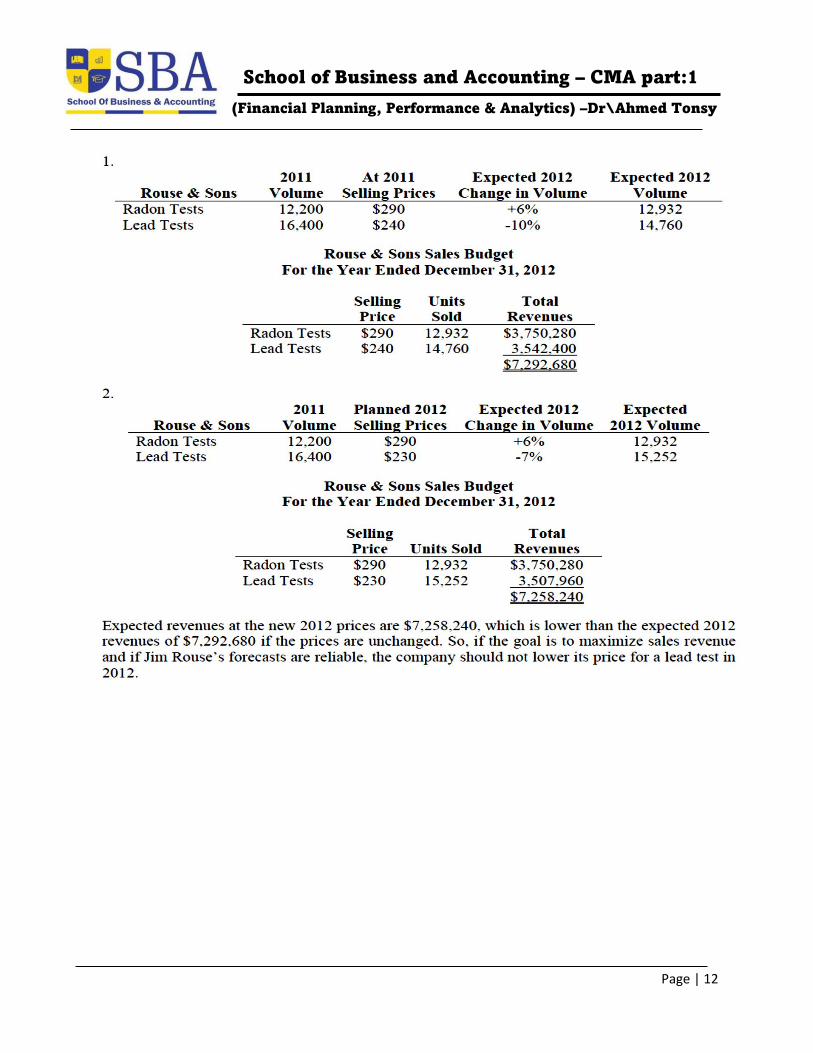

Example (1) : Sales Budget 164. Spirit Company sells three products with the following seasonal sales pattern: Products Quarter A B C 1 40% 30% 10% 2 30% 20% 40% 3 20% 20% 40% 4 10% 30% 10% The annual sales budget shows forecasts for the different products and their

expected selling price per unit as follows: Product Units Selling Price A 50,000 $ 4 B 125,000 10 C 62,500 6 Required: Prepare a sales budget, in units and dollars, by quarters for the company for the

coming year. Answer: First Second Third Fourth Total Product A: Sales (units) 20,000 15,000 10,000 5,000 50,000 Price x $4 x $4 x $4 x $4 x $4 Sales ($) $80,000 $60,000 $40,000 $20,000 $200,000 Product B: Sales (units) 37,500 25,000 25,000 37,500 125,000 Price x $10 x $10 x $10 x $10 x $10 Sales ($) $375,000 $250,000 $250,000 $375,000 $1,250,000 Product C: Sales (units) 6,250 25,000 25,000 6,250 62,500 Price x $6 x $6 x $6 x $6 x $6 Sales ($) $37,500 $150,000 $150,000 $37,500 $375,000 Total dollars $492,500 $460,000 $440,000 $432,500 $1,825,000 Exercise

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 12

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 13

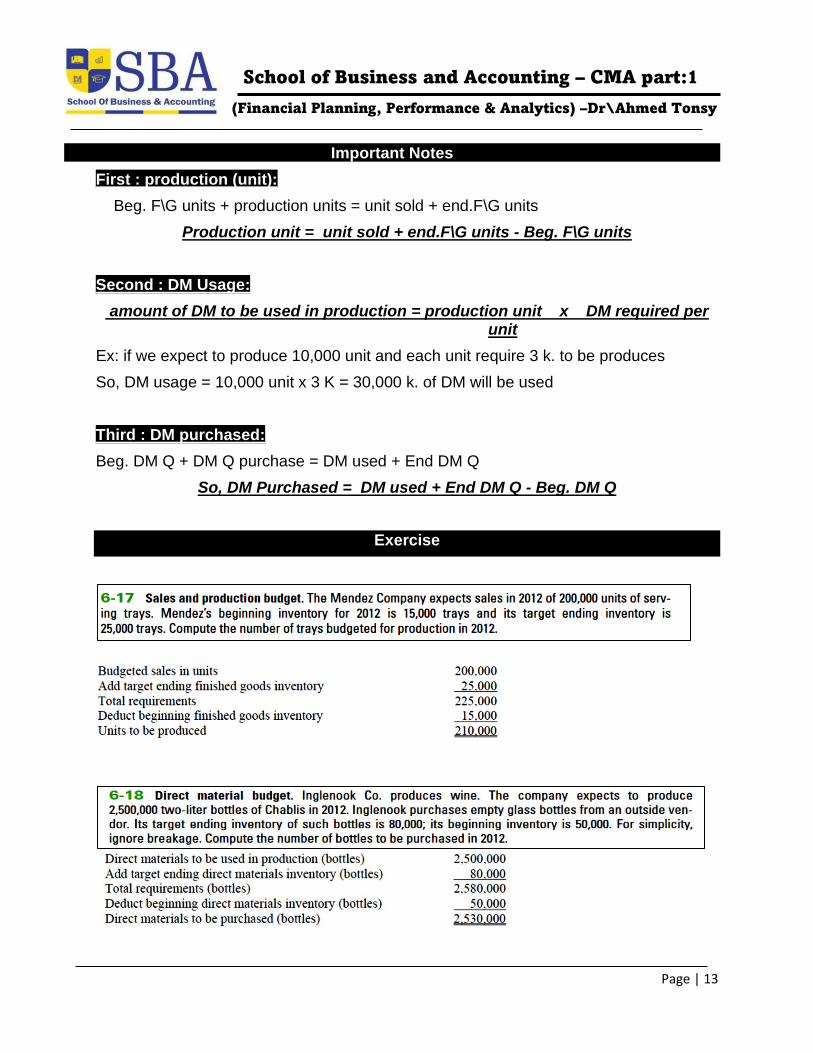

Important Notes

First : production (unit):

Beg. F\G units + production units = unit sold + end.F\G units

Production unit = unit sold + end.F\G units - Beg. F\G units

Second : DM Usage:

amount of DM to be used in production = production unit x DM required per unit

Ex: if we expect to produce 10,000 unit and each unit require 3 k. to be produces

So, DM usage = 10,000 unit x 3 K = 30,000 k. of DM will be used

Third : DM purchased:

Beg. DM Q + DM Q purchase = DM used + End DM Q

So, DM Purchased = DM used + End DM Q - Beg. DM Q

Exercise

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 14

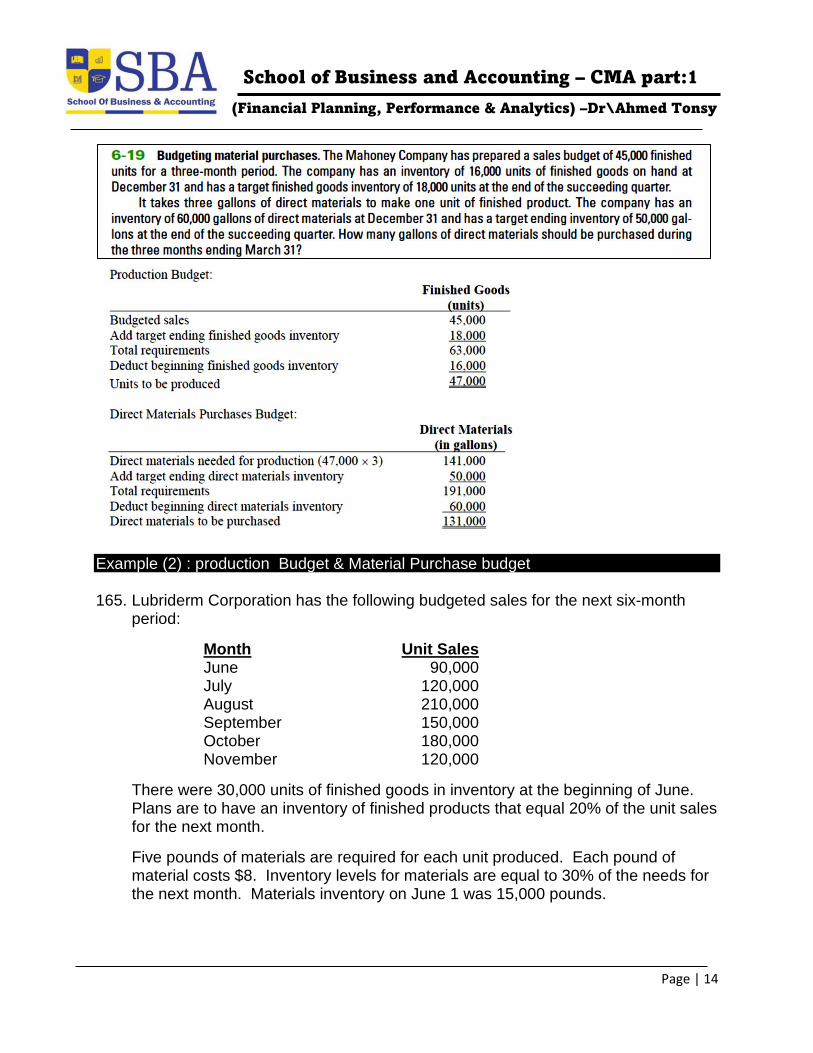

Example (2) : production Budget & Material Purchase budget 165. Lubriderm Corporation has the following budgeted sales for the next six-month

period:

Month Unit Sales June 90,000 July 120,000 August 210,000 September 150,000 October 180,000 November 120,000

There were 30,000 units of finished goods in inventory at the beginning of June. Plans are to have an inventory of finished products that equal 20% of the unit sales for the next month.

Five pounds of materials are required for each unit produced. Each pound of material costs $8. Inventory levels for materials are equal to 30% of the needs for the next month. Materials inventory on June 1 was 15,000 pounds.

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 15

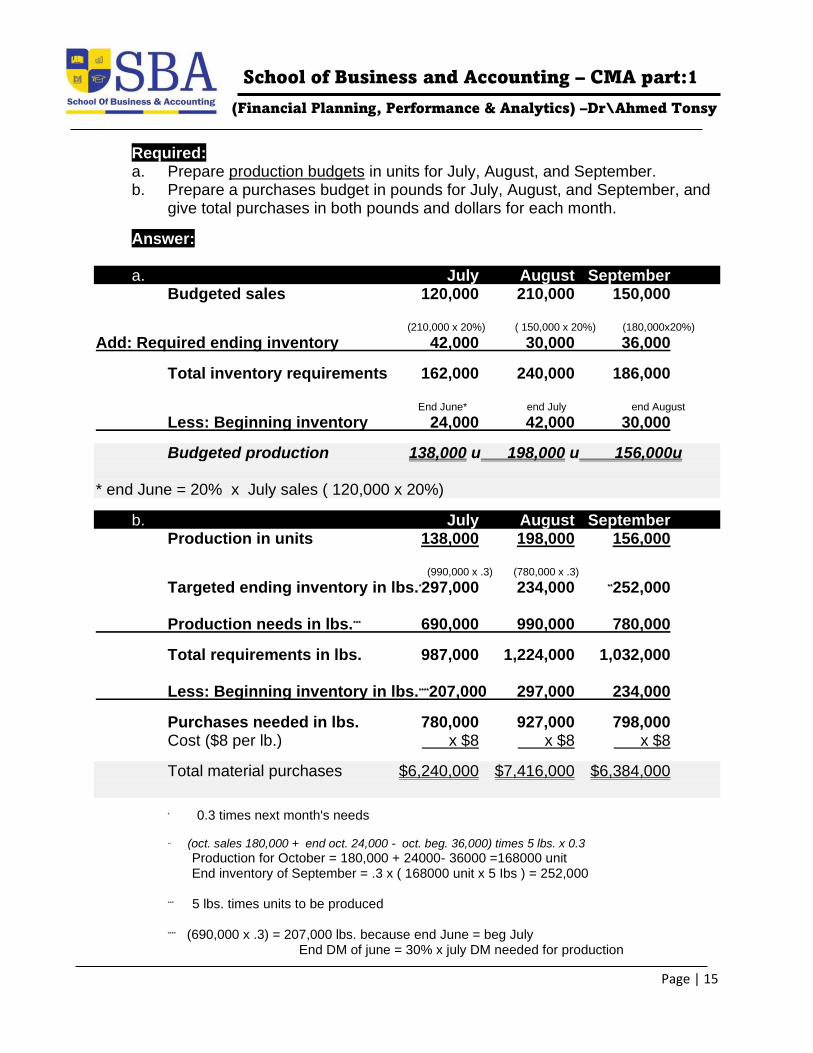

Required: a. Prepare production budgets in units for July, August, and September. b. Prepare a purchases budget in pounds for July, August, and September, and

give total purchases in both pounds and dollars for each month.

Answer: a. July August September Budgeted sales 120,000 210,000 150,000 (210,000 x 20%) ( 150,000 x 20%) (180,000x20%)

Add: Required ending inventory 42,000 30,000 36,000

Total inventory requirements 162,000 240,000 186,000 End June* end July end August

Less: Beginning inventory 24,000 42,000 30,000

Budgeted production 138,000 u 198,000 u 156,000u * end June = 20% x July sales ( 120,000 x 20%)

b. July August September Production in units 138,000 198,000 156,000

(990,000 x .3) (780,000 x .3)

Targeted ending inventory in lbs.*297,000 234,000 **252,000 Production needs in lbs.*** 690,000 990,000 780,000

Total requirements in lbs. 987,000 1,224,000 1,032,000 Less: Beginning inventory in lbs.****207,000 297,000 234,000

Purchases needed in lbs. 780,000 927,000 798,000 Cost ($8 per lb.) x $8 x $8 x $8

Total material purchases $6,240,000 $7,416,000 $6,384,000

* 0.3 times next month's needs ** (oct. sales 180,000 + end oct. 24,000 - oct. beg. 36,000) times 5 lbs. x 0.3

Production for October = 180,000 + 24000- 36000 =168000 unit End inventory of September = .3 x ( 168000 unit x 5 Ibs ) = 252,000 *** 5 lbs. times units to be produced **** (690,000 x .3) = 207,000 lbs. because end June = beg July End DM of june = 30% x july DM needed for production

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 16

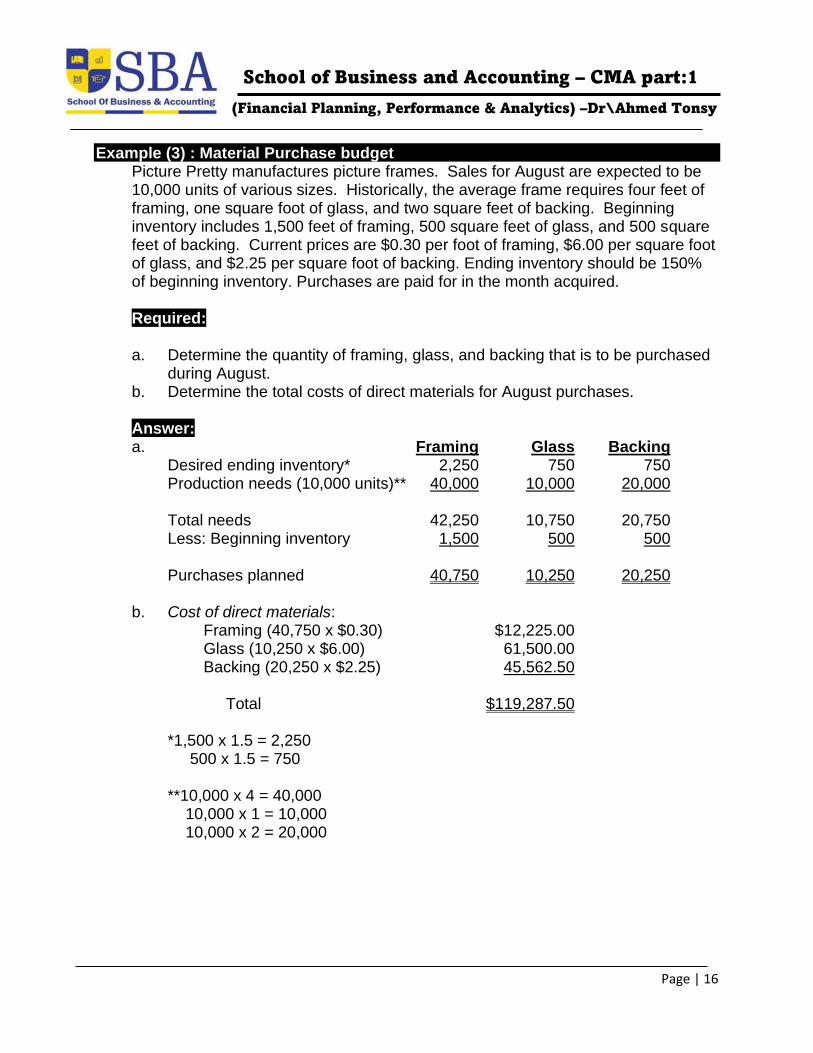

Example (3) : Material Purchase budget Picture Pretty manufactures picture frames. Sales for August are expected to be

10,000 units of various sizes. Historically, the average frame requires four feet of framing, one square foot of glass, and two square feet of backing. Beginning inventory includes 1,500 feet of framing, 500 square feet of glass, and 500 square feet of backing. Current prices are $0.30 per foot of framing, $6.00 per square foot of glass, and $2.25 per square foot of backing. Ending inventory should be 150% of beginning inventory. Purchases are paid for in the month acquired.

Required: a. Determine the quantity of framing, glass, and backing that is to be purchased

during August. b. Determine the total costs of direct materials for August purchases. Answer: a. Framing Glass Backing Desired ending inventory* 2,250 750 750 Production needs (10,000 units)** 40,000 10,000 20,000 Total needs 42,250 10,750 20,750 Less: Beginning inventory 1,500 500 500 Purchases planned 40,750 10,250 20,250 b. Cost of direct materials: Framing (40,750 x $0.30) $12,225.00 Glass (10,250 x $6.00) 61,500.00 Backing (20,250 x $2.25) 45,562.50 Total $119,287.50 *1,500 x 1.5 = 2,250 500 x 1.5 = 750 **10,000 x 4 = 40,000 10,000 x 1 = 10,000 10,000 x 2 = 20,000

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 17

School of Business and Accounting – CMA part:1

(Financial Planning, Performance & Analytics) –Dr\Ahmed Tonsy

Page | 18