Embed Size (px)

Citation preview

School of Accounting Seminar Series Semester 2, 2012

Imagining accounting governance as indexical through Michel Serres’

“Theory of Relations”

Gillian Vesty RMIT University

Date: Friday, 31st August 2012 Time: 3.00pm – 4.30pm Venue: Tyree Energy Technologies Building LGO5

(Refer to campus map reference H6 here)

Australian School of Business School of Accounting

Imagining Accounting Governance as Indexical through

Michel Serres’ “Theory of Relations”

Gillian Vesty School of Accounting

RMIT University Melbourne, Australia

Abstract

Engaging Michel Serres ‘theory of relations’ this paper provides the means to theoretically explore the connections between high-‐level accounting conceptualisations and the multiplicity of expertise and low-‐level practices. A typology has been developed from stories of clinical governance and practices directed at linking ‘good care’ with rational marketplace concerns of efficiency and efficacy. In this study, a relational form of accounting emerges, offering a practical, and political, means for accounting intervention.

Introduction

A decade ago, Brown (2002) lamented that the work of Michel Serres, an influential precursor to actor-‐network theory (ANT) and prolific poststructuralist author, had failed to find an audience in the British and North American social science literature. Greater access to Serres work has been made possible through English translations. However, his work and influence on ANT is still not widely known, even within the growing body of accounting literature applying ANT1. Serres use of rich metaphors challenges us to rethink traditional boundaries between individual and collective as well as science, politics, society and nature. He invites us to see the connections between seemingly disparate worlds through simple stories that build to powerful models, which he then rigorously tests and extends. In this paper, Serres “theory of relations” provides an empirical basis on which to explore the dynamics of accounting in healthcare settings, one that is complicated by heterogeneous expertise and requisite knowledge translation between the accounting and clinical domains (Miller, Kurunmäki & O’Leary, 2008; Oborn, Barrett & Rancko, 2010). The governance of public healthcare provision is rigorously contested along the lines that there

1 Acknowledgements of Serres influence is found in seminal works such as Latour (Pasteurization of France), Deleuze and Guttari (A Thousand Plateaus) as well as in work by ANT founders (Callon, 1980; Latour, 1983; Law, 1999). Callon’s (1986) Sociology of Translation was inspired by Serres Hermes series. See Brown (2002) for further discussion on the influences of Serres philosophy. My aim with this paper is to introduce Serres to the accounting academy, demonstrating how works such as Serres’ “The Parasite” (1982); “The Natural Contract” (1995); “The Five Senses: A Philosophy of Mingled Bodies” (2009); and, Serres and Latour’s Conversations on Science, Culture, and Time (1995) can continue to contribute to our theoretical developments. 2 Serres (1982) would define this as the creation of “quasi-‐objects” as a passage from thing (commerce) to object (money, goods) and thence to quasi-‐object (accounting information), which is a marker of a relation. 3 Pierce’s notion of semiotic is adopted in this paper to explain parasitic exchange as three different modes of

2 Vesty

2

is best practice ‘out there’ and ‘ideal’ governance structures that can be achieved (Braithwaite & Tavaglia, 2008). While much of the mainstream accounting governance literature is aligned with this view, Roberts (2009) points out that there is nothing wrong with the efforts to achieve transparent governance, as long as it is recognised that perfect transparency is not possible. In adopting this view, this paper seeks to define new ways to explore the interdisciplinary efforts to achieve accounting governance. Empirical research from a public hospital setting is used to develop the analytic typology. It has been argued that governance from a conformance (to legislative accounting standards) perspective only creates a “hyper-‐surveillance and control machine” (Ezzamel & Reed, 2008: 598). Similarly, in public health care provision clinicians argue that accounting efficiency must necessarily be balanced with performance from a clinician’s practice viewpoint (Braithwaite & Travaglia, 2008). A conformance-‐only approach to governance undermines the important connections to the internal control structure and the practices and processes associated with social arrangements that necessarily flow beyond organisational bounds (Power, 2009; Chapman, Cooper & Miller, 2009). There is an acknowledgement that broader business responsibilities, risk management and strategic control procedures must be better represented in governance system designs (IFAC, 2004; OECD, 2004; ICGN, 2008; see also Miller & O’Leary, 2000; Bhimani & Soonawalla, 2005; Stevens, 2010). Yet there is minimal research focusing on the processes that make this happen (Ahrens & Chapman, 2007). This research thereby addresses Ahrens and Chapman (2007) call for a focus on situated practices. It aims to bring to life, through Serres, the contingent connecting activities between organisational experts. In seeking to extend the view that accounting knowledge translation is a hybridising globality (Kurrunmäki, 2004; Miller, Kurunmäki & O’Leary, 2008; Power, 2009; Chapman, Cooper & Miller, 2009) this paper does not focus on governance as transparent disclosure of conformance to accounting ideals, or consider hybridisation of expertise from an accounting-‐ or clinical-‐only perspective. Instead, a typology is developed to help focus on the connecting activities between the legislated public health care funding model and the situated clinical accounting practices. Using Serres, I contend that we can make a difference with research techniques that examine the “correspondence work” or the conflation activities of multiple experts that sanction a form of reality as constitutional procedure (Latour, 2004: 248). The aims of this paper is to contribute to the emerging accounting literature that views accounting as a trail of connections and separations with practices that make it a viable technique (Briers and Chua, 2001; Ahrens & Chapman, 2007; Mouritsen Hansen & Hansen, 2009; Power, 2009; Quattrone, 2009)2. ANT theorists suggest mainstream approaches tend to fold, simplify and summarise complexity; while performative approaches are perpetually unfolding and seeking out new complexities (Quattrone, 2009; Boedker, 2010). These researchers follow economic technologies as they come into being, are rearranged, transformed or become momentary conventions (Preston, Cooper & Coombes, 1992; Chua, 1996; Mouritsen, 1999; MacKenzie, Muniesa & Siu, 2007; Mouritsen, Hansen & Hansen,

2 Serres (1982) would define this as the creation of “quasi-‐objects” as a passage from thing (commerce) to object (money, goods) and thence to quasi-‐object (accounting information), which is a marker of a relation.

| P a g e

Gillian Vesty

3

2009; Quattrone, 2009). In this growing body of literature, research gaps continue to draw attention. If we situate our studies entirely in the accounting domain, minimal attention is paid to theorising the accounting correspondence work or framing of relations that emerge between momentary connections of otherwise heterogeneous parties. Brown, points out that: “In an age where the rhetoric of interdisciplinarity is commonplace, it still shocks to encounter work [such as Serres] where the deliberate crossing (and re-‐crossing) of disciplinary boundaries is seriously put into practice” (2002:1). The broader challenge for accounting researchers is to make sense of the social setting, ignore the disciplinary boundaries and embrace the multiplicity of behaviours, contexts and expert accounts. This research thereby takes up the challenge to develop research techniques that help to look beyond the efficacy of theorised conceptual frameworks or the capacity of the individual accounting parts, standards and measurement models that represent accounting’s foundational ideals. Where a financial accountant may view ‘earnings management’ as an upset to accounting order (and recognise a disconnect between practice and the conceptual accounting framework) the management accountant’s story might be a valuation problem, finding with fault in the performance measurement model’s ability to adequately represent organisational strategy. In a public hospital, a clinician may decide to treat a patient for reasons that appear to be at odds with the accountant’s system that directs government funded care. Researchers, trapped in domain specific framings frequently ignore the everyday connections between actors as they work consciously and unconsciously to reconcile individual difference and achieve enterprise-‐wide governance goals. Accounting research, while focused on calculation, fails to recognise the representational properties of numbers and accounts and they ways they articulate, not only systems of value, but map pathways to achieving social order. This paper attempts to move the research focus beyond the traditional domain specific and relativist framing devices. A relational typology is developed to enable researchers to deliver relevant research on gaps that currently exist between theoretically derived accounting conceptualisations and the growing multiplicity recognised in practice (Parker, 2012). In the following sections I begin by discussing Serres theory of relations in terms of theorising the ‘space’ between high level governance procedures and the connecting activities that occur between heterogeneous organisational experts. Drawing on Serres, I recognise the ‘space’ as an interference (a parasite) that must be attended to but is frequently ignored in the academic literature. I follow with the clinical governance setting and present four stories that offer the connections between the otherwise disparate accounting and clinical practices. These stories become my analytic typology defined as three representational forms. I discuss each of the representational forms in turn and explain my adapted model of relations through grounding in the clinical governance setting. I conclude this paper with discussion on how this typology of accounting practices can be applied in other emerging governance structures, in particular, those that challenge the links between commerce, society and nature. Theorising the ‘space’: accounting representation

Accounting depictions of corporate activities typically contain vocabularies of efficiency and effectiveness and management structures focused on strategy achievement and healthy risk

4 Vesty

4

management ideals. Accounting is commonly seen as a system of communication; a means to picture a governable entity, a stable linguistic model of observable objects, underpinned by a fixed ontology (see arguments posed by Thompson (1991) and Bloomfield & Verdubakis, (1997)). In this form of picturing accounting governance is achieved through formalised procedures and protocols to sanction corporate activities in a way that links accounting representation with the ideals of “moral order” (Woolgar, 1991). Accounting can thus be understood as a high order connecting device, or representational form that engenders governance: “The basic function of representation can be summarized as presenting (making present) one thing in terms of another, a representation is what can “stand in for” an absence and thus make it present …” (Bloomfield & Vurdabakis, 1997: 644-‐645). In examining the detailed processes of making accounting present, two aspects become apparent: the moral order itself, and the associated representational activities performed by the lower levels to achieve this order. In the accounting literature, this representational activity is regarded as situated practice (Ahrens & Chapman, 2007) .

In drawing on sociology literature engaging with semiotics, I consider three different representational modes of accounting: iconic, symbolic and indexical representations.3 In the first, iconic representation is recognised in the macro-‐economic models that help express a constitutionally accepted, societal order (Woolgar, 1991). Examples of iconic accounting models might include the Conceptual Framework (even in its re-‐development to meet international standards), well-‐respected models such as the Capital Asset Pricing Model (CAPM) or possibly even emerging environmental models, such as The FullCam Carbon Accounting Model. Each has emerged from rigorous research and recognised for the solid theoretical foundations that interpret and manage, through accounting, the state of society or nature. Following the introduction of New Public Management (Hood, 1991), the internationally adopted public hospital-‐funding model, Casemix, is also included in this broad repertoire of iconic accounting representations. Based on Diagnosis-‐Related Group (DRG) methodology this macroeconomic model of governance has likewise attempted to engender social order, this time through public healthcare provision. The second form of generalising is recognised by its symbolic valuing properties. Chua (1995) described how the Casemix funding model was first theorised in its entirety, and then separated into activity-‐based cost categories of patient care. Calculable values derived for each of the diagnoses, provide acceptable standard costs that can then be managed and audited. The individual component values are given voice by key practitioners and other stakeholders (accountants, clinicians, health economists, system engineers, government administrators, patients, families and community) who all play a role in the cost and delivery of patient care. If there is any disagreement, the derived standard or individual DRG, can be taken out of the model, modified and re-‐valued. All the while the overarching health economic theory is undisputed, the iconic status of the high-‐order conceptual model remains intact, even when component parts are re-‐worked. The funding models arguably create order by generalising standard values for the average clinical inliers that meet clinical domain specific practices (Llewellyn and Nothcott, 2001). Nevertheless, if outliers generate

3 Pierce’s notion of semiotic is adopted in this paper to explain parasitic exchange as three different modes of representation: iconic, symbolic and indexical. See Hoopes’ (1991) interpretation of C.S Pierce’s seminal work on the typology of signs in literature and Verran who uses Pierce’s typology of signs to explain economic models as the signatory of numbers (2011, p.7).

| P a g e

Gillian Vesty

5

too much [theoretical] noise and the model no longer meets collective needs, its iconic status is brought into question (Kuhn, 1962). In a recent example, MacKenzie’s (2010) demonstrated the failure of the Black-‐Scholes model during the global financial crisis. The ability for the situated practices to come together and represent the whole is a function of the capacity to which accounting’s framing device engages stakeholders (Briers & Chua, 2001). All stakeholders are engaged in ongoing valuing processes so they are not only represented in the model but are given value in healthcare audits. The value of healthcare provision can be expressed numerically (for example, as a % GDP) and provides globally comparitive means to demonstrate the value of each of the stakeholders in the funding model. Both valuing and ordering are routine activities performed by accountants and others. Sometimes they think of the accounting models as symbols representing value for the processes of healthcare audit or alternatively as systematic processes effecting a fair way to allocate scarce government resources among its public hospitals. Yet, as we generalise back and forth between order and value -‐ the activities of the multiple situated experts disappear in the processes of commensuration, their practices become part of the background, taken for granted in the model (Latour, 1983). This everyday commonplace conflation of value and order is recognised as the third indexical form of representation but, to date, remains largely unrecognised by the research academy (Verran, 2011). Accounting research is largely centred on iconic modelling and finding imperfections in the ‘theory’ argued for. Alternatively, there are the relativists who are concerned with missing values (or denied variables) that must be included in a re-‐worked model. What accounting research does not do well is acknowledge the power of indexical generalisation that proceeds simultaneously as both value and order. Indexical moments are recognised in the simultaneous relations of ordering and re-‐ordering responses to values that become calculable. With attention on indexical generalisation, sociologists like Verran suggest we can improve our understanding of accounting by following the connecting activities of the actors. As Serres explains, if we only focus on the accounting governance message, we only see betrayal (or conformance) to the expected moral order, or governance reality. However, if we recognise the accounting space as a third representational form researchers are offered new opportunities. In the following section I propose Serres’ theory of relations as a typology to test indexical generalisation in the public healthcare domain. This provides an interesting setting, given the now well-‐established iconic and symbolic representational practices and frequently juxtaposed clinical and accounting views. I introduce the indexical space as Serres’ parasite, or interference – “one living off another when the other does not even suspect it” (Serres & Latour, 1995:134). When theorising accounting’s connecting activities, Serres’ work suggests we must study the performative space as if it were a marker of a relation, a quasi object (Serres, 1982). In this way we can see the potential for change and innovation.

Theorising the ‘space’: Serres’ theory of relations

Recognised by its Deleuzean rhizomatic-‐style connectivity and “inhabiting the heart or the middle of the world” the parasite finds his host and feverishly seeks out the truth (Deleuze & Guttari, 1987; Deleuze, 1988). The ultimate position “sojourning at the summit, the

6 Vesty

6

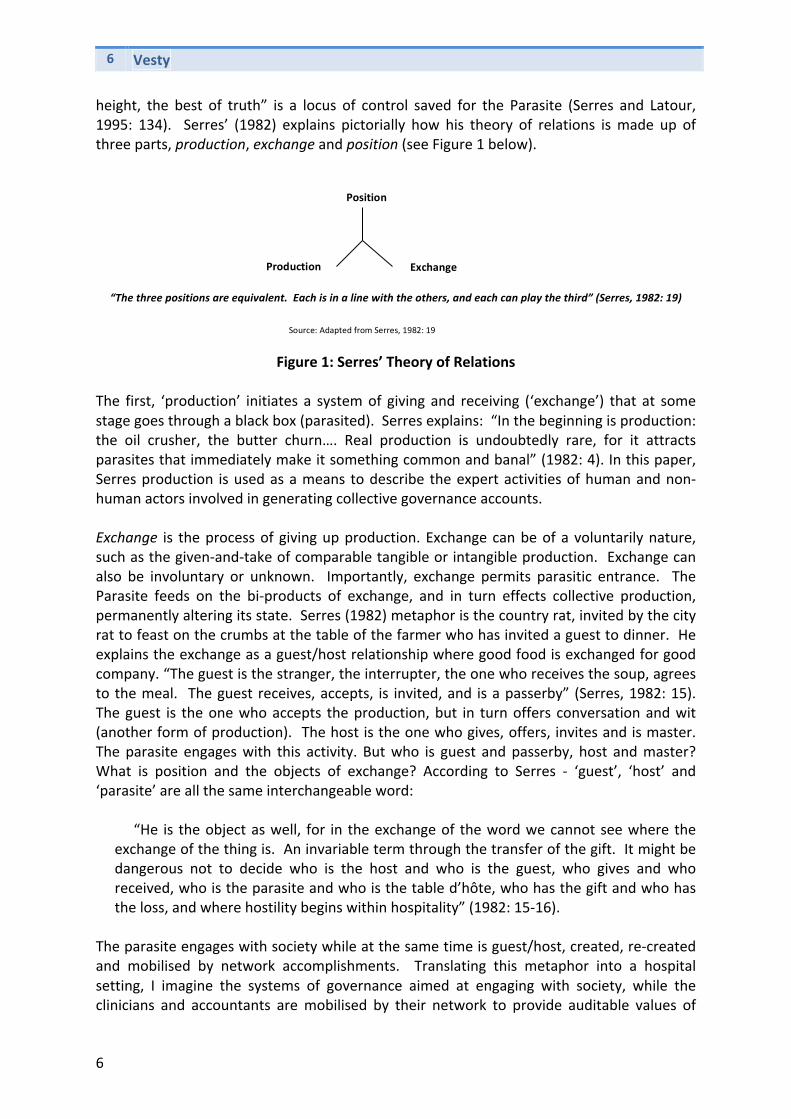

height, the best of truth” is a locus of control saved for the Parasite (Serres and Latour, 1995: 134). Serres’ (1982) explains pictorially how his theory of relations is made up of three parts, production, exchange and position (see Figure 1 below).

“The three positions are equivalent. Each is in a line with the others, and each can play the third” (Serres, 1982: 19)

Figure 1: Serres’ Theory of Relations The first, ‘production’ initiates a system of giving and receiving (‘exchange’) that at some stage goes through a black box (parasited). Serres explains: “In the beginning is production: the oil crusher, the butter churn…. Real production is undoubtedly rare, for it attracts parasites that immediately make it something common and banal” (1982: 4). In this paper, Serres production is used as a means to describe the expert activities of human and non-‐human actors involved in generating collective governance accounts. Exchange is the process of giving up production. Exchange can be of a voluntarily nature, such as the given-‐and-‐take of comparable tangible or intangible production. Exchange can also be involuntary or unknown. Importantly, exchange permits parasitic entrance. The Parasite feeds on the bi-‐products of exchange, and in turn effects collective production, permanently altering its state. Serres (1982) metaphor is the country rat, invited by the city rat to feast on the crumbs at the table of the farmer who has invited a guest to dinner. He explains the exchange as a guest/host relationship where good food is exchanged for good company. “The guest is the stranger, the interrupter, the one who receives the soup, agrees to the meal. The guest receives, accepts, is invited, and is a passerby” (Serres, 1982: 15). The guest is the one who accepts the production, but in turn offers conversation and wit (another form of production). The host is the one who gives, offers, invites and is master. The parasite engages with this activity. But who is guest and passerby, host and master? What is position and the objects of exchange? According to Serres -‐ ‘guest’, ‘host’ and ‘parasite’ are all the same interchangeable word:

“He is the object as well, for in the exchange of the word we cannot see where the exchange of the thing is. An invariable term through the transfer of the gift. It might be dangerous not to decide who is the host and who is the guest, who gives and who received, who is the parasite and who is the table d’hôte, who has the gift and who has the loss, and where hostility begins within hospitality” (1982: 15-‐16).

The parasite engages with society while at the same time is guest/host, created, re-‐created and mobilised by network accomplishments. Translating this metaphor into a hospital setting, I imagine the systems of governance aimed at engaging with society, while the clinicians and accountants are mobilised by their network to provide auditable values of

Position

Production Exchange

Source: Adapted from Serres, 1982: 19

| P a g e

Gillian Vesty

7

clinical care. Emerging from Serres parasitic logic the ‘theory of relations’ is the negotiation of a collective from heterogeneous parts. Through this negotiation, position is achieved. In my reading of Serres, I recognise parasitism as not necessarily threatening, rather a metaphor for the creation of a system – a common world where position is informed meaning making. The first step in the construction of a common world is the production. Production follows with an attachment to a collective (for example, in the all-‐encompassing systems that enable the corporate regulatory and strategic business, or clinical environments to communicate). Accounting captures production and converts it to a common language enabling exchange. The conformance or performance activities are negotiated as a single language and the parasite is the offer to negotiate towards a ‘better’ governance world. There is a to and fro negotiation between the parts. Accounting facilitates and channels but at the same time hybridises existing processes and activities and becomes hybridised in the process (see Lépinay, 2007; Lépinay & Callon, 2009). Exchange is the space where the complex parts/whole relations work to momentarily bind the conformance and performance technologies as collective enterprise governance. Accounting for clinical governance might be examined as participating in order or likewise engaged in representing order in a specific way—as value. Networks “sometimes work in ordering and at other times in valuing—it depends. And because it depends and because often those who love numbers are unaware of what they depend on, we find dissembling in numbering: ends disporting themselves as means; ordering in the guise of mere valuing” (Verran, 2011: 3). While high-‐level accounting conceptualisations are recognised for their desired iconic accounting governance status and accounting practices recognised as the symbolic generalisations of individual experts working their clinical governance practices –an important indexical space is revealed where the reiterative exchange can be examined to make sense of the complexities associated with representation. This reiterative indexical process of generalisation acknowledges the constitutive categories in the production of new forms of collective governance. Importantly this space, the parasite, or position, is recognisable as “informed” indexicality. In other words, rather than not knowing whether the representational activity is ordering or valuing, the position achieved in the processes of production and exchange is the creation of a third representational governance object (Serres, 1982: 38). In this knowing exchange, the space between high-‐level structures and low-‐level action is revealed, thereby allowing political intervention. I now put this typology of representation to practice in the clinical governance setting theorising through stories of clinical and accounting approaches to governance. In the discussion that follows, I first describe the contemporary clinical governance setting and the emergence of clinical governance frameworks. I present four carefully selected stories from this setting to show accounting performativity as the indexical manoeuvre operating in the space between the symbolic and iconic forms of generalising. I conclude this paper with discussion on the development and potential use of this typology to theorise the space and cohesive moments of governance in other accounting settings.

8 Vesty

8

The Clinical Setting

New Public Management paved the way for the corporatisation of public healthcare around the Western world (Hood, 1991; 1995). Government oversight was achieved through decentralised output-‐based performance management control mechanisms, the most important being the patient diagnosis-‐related group (DRG)-‐based funding model called Casemix (Lowe, 2001; Balnave & Reid, 2007; Duckett, 1995; 2000; Palmer, 1996)4. The success of the New Public Management project was entirely dependent on the engagement of clinicians, and the ability for the accounting system to overcome the conflict between caring and financial constraints (Abernethy & Stoelwinder, 1995; Chua, 1996; Comerford & Abernethy, 1999; DHS, 2000). As an overarching constitutional commitment to clinical governance, Casemix was designed to bring social order to public healthcare provision (Chua, 1996). Early accounting experimentation made clinical activities visible before they became standardised as performance measures (Chua, 1996; Star & Strauss, 1999). The professional work environment was reorganised with new zones for inter-‐disciplinary accounting practices with multidimensional performance measurement to communicate the desired performance (Grafton and Lillis, 2005; Chan & Ho, 2000; Aidemark, 2001; Abernethy, Horne, Lillis & Malina, 2005; Miller et al., 2008; Northcott & France 2008). Through accounting changes, both costing and caring governance practice were more visible to the hospital executive and communicated as a legislated hybrid to the wider public hospital constituencies (Kurunmäki, 2004; Miller et al., 2008; Northcott & France 2008). Casemix accounting and standardised balanced scorecard performance indicators became tightly linked to legislated external disclosures and output-‐based performance funds (DHS, 2008; Miller et al., 2008; Scobie, Thompson, McNeil, & Phillips, 2006; DHA, 2010). With the Casemix function of ‘sorting’ patients according to their clinically meaningful categories of care, “best clinical practice” standards were thought to emerge at the same time operating as a strict monitoring device for medical treatment cost variances (DHS, 2000). Acting as governance mechanisms Casemix and multidimensional performance measures offered a contemporary discourse to address concerns about quality and safety in health-‐care provision and to further the working relationship between medicine and management (Scally & Donaldson, 1998; Braithwaite & Travaglia, 2008). The transition from central control and input funding to output activity-‐based Casemix was not, however, without debate (Chua, 1996). The ‘system’ was argued to recognise clinician work through performance measures (Star & Strauss, 1999), patients as inliers or outliers, with the ‘average’ patient or hospital taking precedence in accounting costing designs (Llewellyn & Northcott, 2005).

4 Since the late 1980s there are modified version of the United States – diagnosis related group (DRG) method of categorisation adopted throughout the world. Referred to as Casemix, this form of funding has been adopted by governments in Australia, parts of Europe, The Middle East and Asia (see http://www.casemix.com.au; Balnave & Reid, 2007: 59–67). It is an activity-‐based costing approach, predetermined around each DRG classification (every surgical and medical procedure carefully costed) with standard costs providing a consistent pricing/funding model for each patient treated. Hospitals are reimbursed for the pre-‐determined/contracted number of services and types of patient treatments provided (as an example, see http://www.health.vic.gov.au). Casemix could be argued as generating politico-‐socio-‐technical lock-‐in (Callon and Muniesa, 2005) with hospital administrators relatively comfortable with the methodology and continue to make investments (Balnave & Reid, 2007; Palmer, 1996).

| P a g e

Gillian Vesty

9

Concerned clinicians continue to argue that an overtly rigid “conformance” focus has dominated governance designs, to the detriment of their clinical practices (Degeling et al., 2004; see also Degeling et al., 2006: p. 758). Lost in the accomplishment of Casemix and multidimensional performance tools is the flexible, evidence-‐based governance arrangements, underpinned by a framework of ethics and trust (Braithwaite & Travaglia, 2008). Clinicians are calling for more evidence-‐based clinical practice guidelines and integrated care pathways, developed through decades of world standard medical developments in clinical care, to be the forefront of hospital funding mechanisms (Gabbay & le May, 2004; Marshall, 2008). Clinical pathways place clinicians in the centre of a peer supported team approach to patient management and governance and as a best-‐practice model provides a way to guide improved clinical governance practices (Gabbay & le May, 2004; Degeling et al., 2004; Marshall, 2008; Maliapen & Dangerfield, 2010). In maximising collaborative clinical arrangements, expertise is considered in terms of patient care activities; timelines of care; intermediate and long-‐term outcomes as well as any documented deviations from expected results. The aim is to focus on both quality and co-‐ordinated patient care. The pathways identify the step-‐by-‐step course of events for the standard patient that fits within a diagnosis-‐related group (DRG) 5. Not disconnected from Casemix funding models, clinical pathways or DRG-‐processes of patient care aim to reduce medical errors and prevent widespread deviations in clinical practice; at the same time provide an efficiency benefit, through the economies of scale generated in streamlining resource use and capacity management by a reduction in length of patient stay (Maliapen & Dangerfield, 2010: 259). Developed by the multidisciplinary, global network-‐based teams in charge of patient care, the clinical pathways model of care is dynamic in that there is a continual systematic review of treatment outcomes for each clinical condition (Marshall, 2008). This system accepts that there must be exceptions to the general rule, in one way respecting clinician expertise and preserving their autonomy in providing them with an ability to individually assess and categorise every individual patient case. It is up to the clinician to decide whether or not it is in the patient’s best interests to follow the prescribed clinical pathway. Informed clinician expertise is built into the system offering them a process that permits them to manage the unexpected or exceptions to the pathway if or when they occur. Clinical pathways for the top DRGs are widely consolidated in evidence-‐based best practice standards but not fully embedded in accounting governance designs. 6 However, if integrated care pathways remain closely tied with the DRG-‐Casemix management and clinical goals, and are central to the proposed big picture of clinical governance; there is the

5 The top ten clinical pathways include cardiac pathways, maternity pathways, diabetic foot pathways, surgical pathways, orthopaedic pathways, transient ischaemic attack (TIA)/stroke pathways. For example, a patient arriving to emergency department with chest pain and suspected heart attach is treated according to the clinical pathways approach – requiring certain drugs and specified medical tests within timeframes designed for optimal outcomes. For further information, see the clinical practice improvement centre website, accessed August 2010 http://www.health.qld.gov.au/cpic/service_improve/current_sw_clin_path.asp. 6 Clinical pathways and Casemix connect according to DRG cost efficiencies. They are currently being used in the US for bonus performance funds and more recently investigated for similar use in Australia (DHA, 2011).

10 Vesty

10

potential for the multidisciplinary clinician teams and administrators to balance the interconnections and power-‐sharing implications between the clinical activities and the resource accountability dimensions of care (Degeling et al., 2004). The links between Casemix and the balanced scorecard input and output measures (such as “hospital clinician caseload”, “patient satisfaction”, “clinician satisfaction”, “repeat episodes”, “admissions”, “DRG weekly frequency”, “cash flows”, “fees relative to Medicare”) might be given greater visibility when clinical pathways become central in clinical governance regimes (DHA, 2010; Maliapen & Dangerfield, 2010). While the “patient” might not necessarily benefit if treated as a “client” with the rights of treatment choice, it is argued that a “logic of care” approach with flexible accounting arrangements that, recognise the clinical expertise alongside others in the patient care network, will optimise patient care (Mol, 2008). In ways not widely explored in accounting literature, the health care setting has slowly begun to embrace the need for clinical governance while at the same time fostering a flexible clinical pathways culture where clinical practice and patient care is enhanced. In the following section I use stories to show the heterogeneity of accounting for clinical governance. Each of the carefully selected stories plays an important part in explaining the way clinical pathways as connecting devices between the imagined big picture accounts of clinical governance and the detailed activities associated with clinical and administrative practices of governance. The stories, guided by Serres’ theory of relations, have informed my typology development. I contribute this novel research analytic for use in varying contemporary accounting settings; particularly those where integrated governance designs and multiple heterogeneous expert connections are fighting to achieve their own diverse modus operandi. Four clinical governance stories

The following stories have been gathered from research in four public hospitals – two are regionally based and the other two are large metropolitan teaching hospitals. Interviews were conducted with clinicians, accountants and other administrators over a two-‐year period. When the balanced scorecard reporting format was introduced to public hospitals, I was invited to sit in on management reporting meetings as senior managers considered the impact of the top-‐down reporting model on practices. Observation and archival data, together with the interviews, enabled me to develop this typology of practices.

The stories that follow are designed to elicit the three modes of representation, iconic, symbolic and indexical representation. Serres’ theory of relations is used to explain the indexical representation by revealing the parasite in the processes of production, exchange and position. This first story offered is a nurse’s recollection from the past. Set back in time before New Public Management this story is used to demonstrate real production that will later be parasitised by accounting designs and rendered as average, a normal inlier cost. The aim of this story is to introduce the multiple individuals and how they might play a part in accounting and clinical governance model designs. Some might argue the value of the governance model is contingent on all views being represented. Others would expect the model to sanction societal expectations of the administration of public hospital governance. This first story aims to familiarise readers with difficulties associated with representing practices in public health care provision as both order and value.

| P a g e

Gillian Vesty

11

1. Nursing Production. Caring for a dying patient (as explained by a junior nurse) A young high school boy, I will call Jack, too shy and embarrassed to tell anyone about his

testicular lump, finally sought help when the pain was too much to bear. By then, it was too late. He became one of my oncology patients. I was a junior nurse, not really that much older than Jack, working at a large teaching hospital in Melbourne, in the oncology ward. Jack was reserved and always extremely polite, not at all demanding, even though you could see he was in constant pain. He tried to be brave. He suffered by himself and so did his parents as they sat there with him, not really coming to terms with it all. He had a younger sister – they tried to maintain as “normal” as possible a life for her – I could not help but see how hard, and helpless or hopeless, it was for everyone. Including me. I popped in and out, checking on him as I did my other patients in my eight-‐hour shift.

We were generally allocated around five or six patients to care for during the day, and I always felt bad that he did not demand my time as much as my other patients. I would try to make conversation, always try to make him as comfortable as he could be – offer him food and fluids, check his pulse and blood pressure and scribble them down on his daily record chart, which was located at the end of his bed. I tried to be the best nurse I could, spend time with him when I could, but felt pretty useless. He just lay there in his bed, locked up in a shell, politely and quietly resigned to his destiny. This one particular morning – it still remains vivid in my mind – I arrived at 7am for my eight-‐hour day shift. We were given the usual handover from the night staff and the senior nurse in charge of the day shift allocated our patients. I was given Jack, who was in a single room, along with four other patients who were in an adjacent four-‐bed room. I usually popped my head in to say hello to my patients before I began the round of helping them with breakfast, bathing & dressing as well as looking after their intravenous drips, medications or wound dressings, and anything else, if required.

I looked in on Jack. He did not look good. I fluffed his pillows, tried to sit him up for breakfast and felt a sudden knot in my stomach as I realised that there was no way I would be able get food, let alone drink, into him this morning. His colour was terrible. He was struggling to be Jack. More pain than usual, and not so good with his breathing. I went to the nurse in charge and suggested we call his parents, right now, even though I knew they would be in sometime that day. I wanted them to hurry and I also wanted to warn them. I called; spoke with his mum, telling her that Jack was not so good this morning. They should come in as soon as they can. Jack’s mum said, they would drop their daughter at school and come straight in. I stayed with Jack, saying silently under my breath – “hurry mum and dad, please hurry” – but Jack faded so quickly. He died as quietly as he lived. As I walked out of his room, his parents raced into the ward – at the other end of the corridor, looking down the hallway to Jack’s room they saw me come out; saw the look on my face. Jack’s mum collapsed on the floor in the hallway.

The following two stories demonstrate the process of exchange. The first component is iconic representation while the second explores the process of symbolic representation. These two stories consider the ordering/valuing practices by clinicians and administrators as they negotiate the individual components of the iconic funding model. 2. The process of exchange: Recognising Casemix as a constitutionally-‐derived icon? Hospital CEO managing ‘Casemix’ funding in a small public hospital.

The CEO of one small public hospital I visited has an accounting background. He explained the ins-‐and-‐outs of Casemix funding to me, on a white board in his office. He discussed the terminology – the average “length of stay” for every DRG; the “inliers” and “outliers” of patient classifications – WIES or “Weighted Inlier Equivalent Separations” where “separations” loosely meant patient discharge (i.e.,

12 Vesty

12

that they left the hospital to go home, to another health-‐care facility, or because they had died). One WIES was given a dollar value and at budget time “x” WIES were allocated to individual hospitals as part of their Agreements to the determined patient Casemix.7 He explained how important it was to get Casemix right. “If we do not deliver service performance according to the Casemix agreement, then future funding is cut. This happened to us one year.” His governance role was outlined to me on his whiteboard. Checking targets presented to him as spreadsheets against those in the large bound book that is developed annually by the Department is about making sure the reported Casemix activity matched the allocated, capped level of WIES funding. Patients were classified as a diagnosis group and may be inliers or outliers. Although outliers might indicate excess costs for the hospital, he explained how occasionally this was not necessarily so. Sometimes extended care patients required minimal hospital resources while they were waiting for placement in another care facility. A large bound book outlining the Annual Casemix targets for Victorian public hospitals was the tool that directed his accounting production; the methods of classifying types of patients, their treatments, associated costs and the total annual revenue the hospital would receive.

For this hospital administrator, governance was about demonstrating corporate responsibility by following and reporting on the Casemix systems of compliance – by making sure that: there is equity of “access” for different patient classifications; that the correct number of Category 1, 2 and 3 patients have been treated according to the right timeframes; “effectiveness” can be demonstrated (in Casemix and associated funding parameters such as costs per Casemix-‐adjusted separation and length of patient stay); acceptable levels of effectiveness in terms of waiting times for surgery; quality and safety in the service provided. Developing these accounts was about accounting production – for the CEO on the whiteboard it was factual, rational and accepted as a thoroughly worked through macroeconomic policy or extension of clinical governance. It ordered his way of managing clinical conformance to government policy; in general, but not always. Sometimes the outliers created a nice revenue stream for the hospital. Sometimes a particular Casemix episode created a financial risk for the hospital. The CEO would recognise and need to manage the differences between clinical conformance and clinical performance. Sometimes when activity did not match funding, serious decisions needed to be made about bed closures, patient waiting lists, clinician rosters and engagements.

In conversation with clinicians from the operating theatre it was later explained that many surgeons seemed to be operating under their physical capacity. Some were frustrated that their technical prowess was not recognised in the funding models. Highly skilled surgeons could potentially operate on a lot more patients than budgeted for by the Casemix funds. However, when the operating theatre list was constructed (a list of surgical patients to be treated by surgeons) the number of patients must exactly meet the allocated Casemix fund weights. “We can only do ‘x’ number of tonsillectomies, even though the surgeon, is an excellent operator and could safely get through more of the waiting list in the time allocated in theatre.” This Casemix amount is all that is funded for, even though surgeons try to add more to their lists and nursing staff were rostered (and costs fixed) to allocated shifts. Sometimes, even though it is possible, one surgeon was not allowed to

7 More specifically, WIES is a DRG cost weight, part of the inpatient coding and classification system, that provides the basis for payments to public hospitals in Australia. Under the Casemix system, hospitals are paid based upon the numbers and types of patients they treat, not upon the resources they use. The patient’s WIES value depends upon the amount of time they stay in hospital compared to other patients with similar conditions (inlier equivalence) and the relative cost of treating their condition compared to the cost of other illnesses (cost weight or relativity). For example, 0.19 WIES is allocated to a same day chemotherapy patient; 30.02 WIES is allocated to a liver transplant patient staying 40 days; 7.51 WIES is allocated to a liver transplant patient dying after 3 days. In 2008 metropolitan hospitals received $3,279 per WIES while country hospitals received slightly more in recognition of the higher fixed costs of running small hospitals (http://casemix.health.vic.gov.au). It was pointed out that “WIES activity” is the most measured activity in Victorian Hospitals and “must withstand careful scrutiny by public hospital managers and officials in funding organisations” (Duckett, 2000: p. 120).

| P a g e

Gillian Vesty

13

perform two procedures under the one anaesthetic (i.e., a colonoscopy and gastroscopy together) because they are different procedures that are accounted for separately.

The flaws were regarded as challenges that could be sorted by the system. The Casemix targets were there at the outset and they were accepted (sometimes grudgingly) but worked towards. As for changes, it was a matter for continual tweaking and adjustment. If dissention occurs, the system can be disembedded or sectioned into its respective conformance and performance parts to be fine-‐tuned and managed. But the general policy remained as one with the technological zone of clinical governance. In the context of social ordering the Casemix system was viewed as a high level accounting model that held iconic status. Kept at a distance, it could be judged and labelled by both accounting administrators and clinicians as user-‐friendly or at times difficult and behaviour controlling. In this context it provided a way of ordering public hospital practices.

3. The process of exchange: representing categories that matter – symbolically. Balanced Scorecard implementation -‐ disappearing measures

Sitting in the back offices of a large public hospital, the Senior Management Accountant explained to me how they wanted to do more with “balanced scorecards” at lower organisational levels. While the hospital’s performance itself was measured in dollars (the ability to balance funding mechanisms like Casemix with costs) other non-‐financial performance measures (based on hospital-‐running and patient access to care issues) were also implicated in funding mechanisms. He was concerned that many of these indicators in their former generic balanced scorecard model (categorised as “patient”; “resource use”; “patient care processes”; and, “people, learning & innovation”) did not necessarily match with the actual activities and processes going on in the hospital. He explained how the balanced scorecard tool was removed from the website when it was pointed out that only the legislated 7 Casemix-‐funding related measures were up-‐to-‐date (5 in the “resource use” and 2 in “patient care processes”). Later, one surgeon told me that he only ever occasionally viewed the WIES activity in the “resource use” quadrant and totally ignored the others. He did not even realise the balanced scorecard had been removed from the intranet.

The reason for the meeting – how to better cascade the balanced scorecard from a high-‐level board reporting tool – certainly provided the opportunity to initiate conversations, to rank and order important measures and to look at ways the accountant and clinician worlds would come together and be represented.

The clinicians began by arguing that they did not always understand how the numbers were derived. They pointed out that overhead allocations and shared costs were problematic. They tried to manage the allocations between themselves, often just accepting another costs centre’s costs. But was this always appropriate? They required assistance to better see the links between the Casemix dollar accounts and the patient care they provide. A manager of the critical care unit (CCU) explained how a team was following one DRG patient’s care throughout their entire stay in the CCU. The project involved counting every step of care provided, everything from bandages to drugs to nursing hours. They wanted to determine how closely the government DRG funding amount matched their own activity costs for a typical CCU patient. This was an interesting project and everyone was keen to find how closely the funding derivation and hospital costs matched. This would provide them with a better understanding of their cost objects – the patients.

A document presented by one clinician highlighted ‘patient separations’ as the significant driver of costs and activity in the hospital (also an important driver of the Casemix funding system and one of the “resource use” measures of the balanced scorecard). She explained how patient departures meant that beds needed to be cleaned, new patients admitted and allocated to nursing staff on that shift. Patient admissions required preliminaries such as detailing a paperwork trail of patient health history and current temperature, pulse, blood pressure readings and medications. This was followed by doctor visits and other paperwork associated with the medical admission which made official the

14 Vesty

14

patient treatments, medications and other tests or procedures to be performed. The changeover of patients needed to be streamlined. They needed to quickly link the patient into the appropriate clinical-‐care pathways, particularly if important time-‐related tests, medical or operative procedures were required by that pathway of care.

Another clinician explained their localised budgeting activities in relation to allocating nursing staff. She explained how some clinical units managed their staff really well while other clinical units found it really difficult to keep their staff. They constantly were recruiting casual agency staff for some reason or another. The major reason given was related to the workload on certain wards being really heavy. The clinical wards were generally structured around specific patient diagnosis groups and the wards that had challenging DRG patients were often harder to recruit staff to (i.e., wards where patients required continual care – drainage bags emptied, chronic lung disease patients that required frequent chest physiotherapy or suctioning of their lung secretions, heavy lifting orthopaedic cases, and medical wards with stroke patients, and the like). Having to employ agency staff increased hospital costs. Her spreadsheet tried to find relationships between heavy patient loads, sick leave, nurse turnover and long-‐standing nursing employment. It connected nursing staff with ward and patient DRG requirements. Although she developed this model for her own use, she wanted to see it more widely used. She later spoke to me about how she was working with the accountants to develop this model further.

In the meeting, the accountants and clinicians were both contemplating how they might better work together; and a new reporting system would encourage alignment of clinical governance goals. Conversations went like this: “We hope that … we will start the amalgamation … start devising the relationships between activity data and the financials … and the payroll.” Interestingly the categories of concern were those that matched the clinical cost categories underlying the DRGs (underlying Casemix). The accountants became increasingly comfortable with the individual activities the clinicians were talking about because they recognised and linked them with the Casemix funding measures and summary WIES budget results they delivered every month. For example, patient “separations” as high-‐level measures for Casemix funding purposes and the underlying clinical activities associated with patient costs categories and nursing staff movements unfolded as important measures for both accounts and clinicians.

Unexpected funding for an enterprise-‐wide resource planning (ERP) and financial management system gave accountants and clinicians further opportunity to see the big financial picture and drill down on the individual department details they desired. The management reports to the Board would benefit from this ERP system detail and individual needs could be worked out between accountant and clinician. Everyone was happy.

What emerged in discussions, however, were the efforts to create a common language and manage business responsibilities; the representational activities that defined the balanced scorecard categories, shifted, to more closely align the clinical pathways and best practice guidelines with the high-‐level Casemix funding model. The two previous stories provide moments of ordering and valuing. The Casemix, health economics funding model provided the tool for accountants and clinicians to generate calculable values that could then become audited through systems such as balanced scorecards. The symbolic effectiveness of the balanced scorecard was debateable. Nevertheless, it provided a system of exchange and highlighted the moments of hybridising clinical and accounting production. In the following, final story, a moment of indexical generalisation is offered. In this story, the moments of exchange can be recognised as on-‐going responses of ordering, re-‐ordering as a response to Casemix values that must be included. The parasitic position is achieved by the surgeon in his demonstration of working both versions of representation, in a way that value and order emerge simultaneously as informed indexicality.

| P a g e

Gillian Vesty

15

4. Casemix as generative simultaneous negotiating: working position. What to do with unexpected Casemix funds?

In a general surgeon’s office, adjacent to the hospital, the surgeon and his secretary were looking at his public patient waiting list. He explained to me that the government had released some extra Casemix funds enabling additional procedures to be performed. As well as his patient waiting list, he was searching through his diary with his secretary to see when he could fit in two more theatre sessions before the end of financial year. It was only weeks away. The procedures had to be performed in this financial year. I watched him work through his diary to find two free mornings in which he could operate. He regularly operated at three hospitals (two public hospitals and one private hospital) and needed to fit this extra operating time around his set operating hours and patient consultation clinic hours at each of these hospitals and his own rooms. Once his diary was sorted he began to work through the waiting lists with his secretary to determine the best mix of general surgical procedures. What varicose veins, hernias and carpal tunnels would he fit in at the last minute? Running his finger down the list, he said – “not Mrs Smith. We can’t do her. She needs bilateral varicose veins. They are too messy. Not a straight forward ligation and stripping. I can’t fit her in, given the time and funding allotted”. While he started at the top of the list and worked his way down, he could not always operate on every patient according to their position on the waiting list. Some procedures were too complex, too time consuming and too costly for the few hours of additional theatre time/funding allocated. For some procedures certain equipment was required and assistant doctors needed to be coordinated. These additional costs were included in the DRG which made the procedure costly. As he ran down the list, it was a balancing act of his availability, Casemix payment versus surgery time, DRG complexity, equipment, assistance; he aimed to maximise the number of patient treatments for the allocated funds. This was a moment of coordinated clinical governance production. He was consciously and confidently negotiating between the high-‐level ordering system and the clinical pathways. Analytic typology: explaining the three representational forms

The three parts of Serres’ theory of relations, production, exchange and position provides a language to begin to talk, in a general way, about the mid-‐level practices that operate between the high-‐level conceptualisations and the individual low-‐level clinical governance practices. A costing/caring relationship is made possible through prodution and exchange, giving birth to new forms of collective governance. Exchange is enabled by the third, the parasite —bringing power to the governance synthesis. As highlighted earlier, this alternative way of seeing is a much ignored strategy that can prevent us overlooking the relational form of generalising. The theory of relations offers us the possibility of revealing a ‘mid-‐level’ set of descriptors. Not the specific intuitive commonsense lower-‐level symbolic descriptions that participants might offer for what they are doing, nor the large, iconic final conceptual accounts ―but a mid-‐level form of categories that often remain silent in analysis. These mid-‐level descriptors are the focus of this proposed representational analytic typology. Iconic representation

The opening stories show the CEO and the nurse as a producers. The nurse’s attention is on nursing care, not really aware that she was doing “clinical governance”; the nurse was doing her best to follow well-‐ordered rules taught by the clinical profession about best-‐practice pathways of patient care in an oncology unit. She followed routine directions to assist her

16 Vesty

16

patients with meals and bathing; taking blood; administering drugs as ordered; deciding whether additional pain relief is necessary (panadeine or morphine?); deciding whether to inform senior clinicians that further intervention might be required; performing additional or routine four-‐hourly observations (blood pressure, pulse, respirations and oxygen levels); completing the patient chart at the foot of the bed; recording activities of note in the patient records. Her activities might be viewed as factual, value-‐free and rational in following the clinical and Casemix constitution. The nurse begins her day with a list of caring duties and works towards her pre-‐defined goals to deliver high quality care while minimising patient risk. A linear, means-‐end, production of care according to the implicit care pathways as universally accepted and taught by the clinical profession. The list of tasks can be converted to accounting and accountability measures, linked to the Casemix or clinical pathways models to both measure (provide a value for) and demonstrate responsibility in meeting expected governance ideals.

The CEOs attention is on the budgeting details, ensuring governance is achieved in matching the hospital’s Casemix funds with planned clinical activity. Working the nitty gritty details of the accounts in his daily activities, his accounts present as if an image of the Casemix accounting icon. Iconic systems are designed to effect coherence by maintaining trust between the competing parties and can only be possible when all opposing interests (i.e. economic, social, political and clinical powers) are included as stakeholders. In meeting Casemix budgets, the CEO realises desired regulatory order and stabilises future funding for the hospital. The success of this clinical governance system de-‐politicises and rules out dissention between other public sector facilities as well as the internal clinical and costing environments. The two members of this clinical governance system – the accountant’s corporate governance technologies and the clinician’s operational governance practices – are recognised as constituted conformance-‐performance categories. The whole of clinical governance is made up of its clinical and corporate governance parts. In this form of iconic generalising, clinical business governance and accounting corporate governance, two equal categories, participate as one to effect the collective sustainability governance.

The stories have helped to show, that in a similar way, Casemix defines the abstract quality that public healthcare provision holds. It provides a moral (clinical governance) prescription of “how we should live”, and thereby creates social order. For Casemix (or the balanced scorecard) to be celebrated as iconic, rigorous collective development processes with opportunities for stakeholder investment must be provided. With this form of representation it is necessary that order is first imagined as an extension of the wider public healthcare provision problem at hand, followed by deductive reasoning and related research that tests the hypothesised cause and effect relations. For example, a general reduction/increase in the costs/patient throughput components would be viewed as a positive contribution to the efforts to negate spiralling healthcare costs and at the same time improve patient access issues and contribute to maintaining order. The accountant carefully selects and determines all accounts that make up the collective governance (i.e., WIES targets, patient access, patient separations, and others that align with the required conformance ideals). The nurse is given ‘x’ number of category ‘x’ patients to care for; follows the nursing care plan that prescribes her routine activities. Similarly, the balanced scorecard reporting group’s methodical preparatory work of interviewing and engaging all clinical stakeholders demonstrates the activities to rule out any potential future dissent. If

| P a g e

Gillian Vesty

17

there was dissent, this would be attributed to the underlying theory and the balanced scorecard model’s ability to represent collectively agreed clinical governance. Failure would require more theoretical consultation.

Accounting icons, such as Casemix, are designed to effect a practical equivalence between societal care and the monetary economy (Verran, 2009b). The two conformance-‐performance realms of the clinical governance system are recognised as two distinct members that collectively make up the icon. Any failure in clinical governance suggests a need for further consultation and re-‐evaluation of the understood state of flow of clinical economic activities. The result is a reworked icon that maintains accounting order.

Symbolic representation

In the second context, working symbolically is about participating in valuing, not ordering. In comparison with Casemix accounting as an extension of clinical governance, this second form of representational foundational logic is contingent upon multiplicity as constitutive of clinical governance. This inductive form of reasoning is more open-‐ended and exploratory in nature. It involves qualitative reasoning about the value of health care provision. The clinical and accounting categories are sectioned into a plurality of units and then calculated/added to the collective whole. That is, imagined as a nested whole with a single value (Verran, 2011: 8).8 The valuing of the multiple categories (financial and non-‐financial) is aimed at representing clinical governance. For example, we could take the individual perspective of the nurse, Jack, Jack’s family, the accountant, the hospital administrators, the government, other patients with similar diagnoses etc. The values they place on a functioning public healthcare system add together to represent the collective clinical governance. The context generated in the second story, the balanced scorecard meeting, is about developing an accounting system that brings all these interests together as one system. It would be a “theoretically justified context that can be ratified, possibly by a vote, at a meeting of constituent interests or interested parties” (Verran, 2009a: 14). Each of the individual perspectives is considered as separate values, loosely held together. Including myself as group participant and observer, we were all important parts of representing the collective.

The balanced scorecard was originally designed from qualitative reasoning to represent the multiplicity of stakeholder values. Added together the values were designed to symbolise the public hospital context. In the multiple headings and boxes, individual parties (patients, clinicians, accountants, resource providers) can see where they are positioned in the performance management model. Concerned individuals with varying voices and interests are presented with the theoretical guide – a modelled set of scenarios, defined in the balanced scorecard – that can be debated according to their varying individual background expertise. Any ambiguity leaves “those with interests unable to choose and/or unable to point clearly to what they are giving up in the event of a move to compromise” (Verran, 2009a: 14). In the context presented here the scorecard carried the flavour of a segregated

8 The difference can be explained with numbers. For example, “14” can be seen as having one member (1 x 14) only or it could have 14 members (14 x 1) each with individual values (Verran, 2009b: 146–147). That is, numbers either mark or commensurate (Eseland & Stevens, 2008). Icons mark while symbols commensurate. Indexes work both simultaneously.

18 Vesty

18

collective. In trying to develop a symbolic representation of governance, the scorecard was vague and misunderstood and the parties that it was trying to account for were left without choice or a place in the system. They were unable to see what was required of them in the call to achieve collective governance. A single language or passage to clinical governance was unable to be negotiated and the balanced scorecard could not generate categories that connected the multiplicity of views. It required too much interpretation thus undermining its ability to be a symbolic representation of clinical governance.

Collectively the DRG-‐ related clinical pathways stood as an extension or embodiment of the iconic Casemix system. At the same time the pathway activities served to represent the individual needs of the accountant, clinician, patient, relative, hospital management team and government. The balanced scorecard and clinical pathways were parallel technologies, and through the hospital meetings, brought to life only glimpses of momentary connections. Indexical representation

In the third part of the typology the connections and separations between the two (value/order) processes are brought to the foreground. In efforts to better manage the boundary between the ideal and the political, a performative space, or knowing exchange, is evidenced. Latour refers to this indexical activity as “compositionism”:

Compositionism takes up the task of searching for universality but without believing that this universality is already there, waiting to be unveiled and discovered.… From universalism it takes up the task of building a common world; from relativism, the certainty that this common world has to be built from utterly heterogeneous parts that will never make a whole, but at best a fragile, revisable and diverse composite material. (Latour, 2010: 3–4)

While Latour explains this as a knowing activity, Verran points out that the simultaneous value/ordering generalising is largely unrecognised in moving from the individual to the collective. A range of healthcare services, which can be valued, somehow becomes a whole: “a general class”. In clinical and costing activities we move seamlessly from value to order. Several “services” that can be represented and valued become, in the next sentence, the order of the world itself (Verran, 2009b: 9). In the stories, the nurse and the accountant do not recognise they are working indexically. Like most of us, we are doing it all the time; we do not consciously treat accounting and clinical practices as icons or use them as symbols. Working to suitable targets (blood levels; pain levels; time frames) are not necessarily pre-‐conditions for the nurse’s activities. The targets are there; they are understood, but are not at once recognised by the nurse or accountant before they commence their daily activities: “instead of establishing [targets] before you engage in action, you keep on searching for [them] while you act” (Mol, 2008: 46). The CFO accountant is working value, adding services and costs together while at the same time relieved when budgeted targets are met and uncertainty discharged. The nurse in the first story is deciding at every encounter, with each of her patients, the type of care she will give. The nurse observes, chats, makes judgments about patients, families and treatments:

| P a g e

Gillian Vesty

19

“In the process of care it is not possible to put the facts on the table first, to then add the values, so as to finally decide what to do. This is not to say that facts mould themselves to our wishes. Instead, the point is that practices informed by the logic of care do not proceed in a linear manner. Instead, a “sensible course of action” and the “normative facts” relevant to it, co-‐constitute each other. Care practices are resilient as well as adaptable” (Mol, 2008: 45–46).

In working indexically we unconsciously attend to the mess of the real and through this co-‐constituting activity. In this way our representational generalizing proceeds simultaneously (as order and value). We might ask does it matter that this practice is unrecognised, and that sometimes we might work in ordering and at other times we are engaged in representing order in a specific way – as value? I suggest this dual-‐generalising property does matter. If we make efforts to recognise and highlight this unconscious, but very important generative practice, we have the opportunity to better intervene in clinical governance world making. Informed good faith in using accounting systems is in part being familiar with the difference in using them as icons and using them as symbols and also in recognising opportunities for governance improvements (Verran, 2009a: 9).

The surgeon in the third story was working knowing exchange. He was showing a certain familiarity in using the Casemix system as both an icon and symbol. It is an ordered way of producing care; not ordered in a linear fashion and not a producer of disorder, but an ordered co-‐constitution of working the differences between the two. He knowingly managed the connections between the two generalising logics that saw clinical governance as either providing order in the health-‐care community or to symbolise order through accounting for the multiple values associated with health-‐care provision. That is, he managed the value-‐order space where Casemix operates as both iconic, generated from deductive economic logic, and symbolically, generated from inductive valuing. In working Casemix accounting as indexical, he is addressing the governance that is overlooked in iconic numbers and denied in symbolic numbers. The logic of care is a logic which emerges as an outcome of collective participation in everyday patient care9.

When we use accounting governance frameworks as icons we overlook the symbolic-‐valuing potential. We develop enterprise-‐wide models that manage “nothing” when we ignore the performative space (Power, 2009). Qualitative reasoning is overlooked as individual expertise and contributions are cleansed from view. This is because the big picture accounts are believed to capture the needs of all stakeholders. In working symbolically we equally deny the iconic-‐valuing representations of political reality. The way to represent order is only understood through the processes of valuing the individual contributions to the collective. Contingent on multiplicity we also deny the experience of what is happening in 9 This approach to theorising is one that is open to multiplicity (Mol, 2002; 2008). For example, Mol (2002) shows atherosclerosis (a medical condition) enacted as a multiplicity. Multiple values. For the pathologist – as calcified and narrow veins “under the microscope”, for the patient – pain in legs on walking; for the doctor – a weak pulse in the legs; a cloud on the x-‐rays after radioactive dye injection; for the surgeon – blocked vessels to be unblocked; for the exercise therapist – a disease that can be treated with exercise. There is a certain “cohesion” of these enactments when there is enough correspondence among the stories that everyone can be said to be talking of the same disease. It is not the same thing i.e. enterprise governance from different perspectives (perspectivalism) – we cannot really add them up to provide a single value. Each story enacts its own reality. The indexicality is caught in the moments of correspondence among the stories.

20 Vesty

20

the here and now of corporate reality, we deny the need to “wrestle with the real”(Verran, 2009a: 9).

For indexical exchange to come to life and to stay alive there must be an elaborate network of smoothly functioning institutions with trained and willing workers, complex technical procedures and material arrangements and routines, and multiple texts of differing genres to be interpolated. As always in indexical exchange there are surprises. Surprise can occur when the surgeon manages to exceed his own definitions of working capacity, given the system constraints. In iconic representation there would be no surprise. The surgeon’s work would be overlooked, or cleansed from view, as it would be assumed in the Casemix model. In symbolic representation the surprise would be hidden in the specific ways the surgeon goes about valuing the additional Casemix dollars. When we acknowledge the capacities that accounting framework partiality can provide and that the governance excess can be fulfilled through varying business rituals; this is where we find exemplars of calculative technologies intervening in the happening of the real – and vice-‐versa (Verran, 2009a: 11). Through applying this typology to our research, we are more equipped to deal with the unexpected threat to enterprise governance, and better deal with the perverse effects of policy choice. Conclusion

“Understanding the system and the rules of parasitism is thus more important than giving a still picture of reified markets” (Lépinay, 2007: 280-‐281).

In this paper I have developed and applied a typology of practices in order to explore the nature of collective connected governance in emergent accounting framings. The clinical setting provides a useful setting to show heterogeneous individuals constructing the collective ideal while at the same time seeking to represent this world. Following from Ahrens and Chapman (2007), I contend that we should not base our analysis on a universal rule that indicates a priori what should be produced. Instead we should follow the big picture conceptual icons and their low-‐level detailed representations as they emerge together and multiply as performative practice. I have attempted to extend the notion of performative practice by showing accounting practice is not only performed by situated expects, such as the surgeon, but can be further identified as performed “informed indexicality”. The typology of production, exchange and position helps to identify the accounting parts, the situations of governance, and the kinds of technical, regulatory and property-‐right practices that shape a connected enterprise governance reality (Barry, 2001). The Peircian notions of semiotic and the conflation of the iconic and symbolic numbering in exchange draw our attention to the frequently ignored space between value and order. The generative, indexical form of generalising is the everyday performative practice of contemporary society, made visible in clinical governance practices. But this is the riskier context. It involves mess, confusion and noise. Being able to intervene in this space requires value and order generalisations to be pushed to the background, so the indexical context can be brought to the fore. In the space between the two-‐way conversation Serres’ parasitic

| P a g e

Gillian Vesty

21

logic exists as the simultaneous negotiation. Importantly the parasite it is not just about creating a system of relations, through production and exchange, but the politics and mastery of that system. These are the relations of domination and these are the relations that must be understood, not after the fact (when governance fails or invention is exalted), but while they are happening. This is the point when practices can best be recognised and designated good/bad governance.