Embed Size (px)

Citation preview

In February, we republished three ar-ticles from 1996 about AIG’s rela-tionship with Coral Re, a nebulousBarbados reinsurer to which AIG

ceded about $1.6 billion in reserves.Although Coral Re looked and smelledlike an AIG affiliate, AIG denied that itwas. On the following pages we are re-publishing nine articles about AIG thatwere written between 1998 and 2004. (Forall of our articles about AIG, please referto the index in the March 15 issue.)

Although AIG has long been extremelyprofitable, it has also been a “black box”that appeared to have a predilection for in-novative bookkeeping. If you mentionedthat AIG may have engaged in some sortof legerdemain, it tended to elicit a strongreaction from 70 Pine Street, the com-pany’s headquarters. “AIG has always pro-vided complete and accurate financial in-formation,” was a standard response.(Yelling, threatening, and bullying werealso standard responses.)

On March 30, AIG issued a press re-lease in which it admitted the ugly truth:it did not provide complete and accurate fi-nancial information. The press release

stated that AIG entered into transactionsthat “appear to have to have been struc-tured for the sole or primary purpose ofaccomplishing a desired accounting re-sult.” Translated into English, that meansthat AIG screwed around with its num-bers, thereby misleading everyone whorelied on them.

What follows are some examples ofAIG’s mischief.

AIG entered into $500 million of“reinsurance” transactions with GeneralRe. Because no risk was transferred, thetransactions weren’t really reinsurance.This phony “reinsurance” made AIG’sloss reserves appear greater than theywould have been otherwise, giving themisleading impression that the company’sreserving practices were more conserva-tive than they really were.

Between 1991 and 2004, AIG ceded alot of reinsurance business to a littleBarbados company called Union ExcessReinsurance. These “reinsurance” trans-actions accounted for $1.1 billion of AIG’snet income. Upon closer inspection, AIGdiscovered that these transactions weresomething of a sham. AIG doesn’t knowwhat the hell happened, but it says that it“now believes” that Union Excess’sshareholders have a financial arrangementwith Starr International Company(SICO)—a private holding company thatowns twelve percent of AIG and is con-trolled by Hank Greenberg and other AIGhonchos. The bottom line: it appears thatthere was no economic substance to the$1.1 billion of net income that AIG re-ported from these transactions.

The Union Excess transactions also

SCHIFF’S

SCHIFF’S INSURANCE OBSERVER • 300 CENTRAL PARK WEST, NEW YORK, NY 10024 • (212) 724-2000 • DAV I D@IN S U R A N C EOB S E RV E R.C O M

April 4, 2005Volume 17 • Number 9 I N S U R A N C E O B S E R V E R

The world’s most dangerous insurance publicationSM

Say it Ain’t So, Hank

TA B L E O F C O N T E N T SOctober 1998: Darkness on the Edge of Town—AIGand SunAmerica . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

September 2000: An Extreme Price for Growth . . . .7

April 5, 2001: Hostile Takeover Attempt for AmericanGeneral—Is AIG’s Stock Too High? . . . . . . . . . . . . .9

May 2, 2002: The Greatest Risk is Taking Too MuchRisk—AIG’s Audit-Committee Report . . . . . . . . . .12

July 25, 2002: Audit Committees, Legends, and P/ERatios, Part 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

August 16, 2002: AIG to Change Audit CommitteeReport . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

April 7, 2003: Inside AIG’s Proxy Statement . . . . . .23

June 23, 2003: AIG’s Secret Connection with Director . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

February 26, 2004: The Art of Manipulation? . . . . .30

AIG and the Art of Financial Prestidigitation

SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000 APRIL 4, 2005 2

raise questions that AIG has not ad-dressed. How could AIG have failed todisclose such large “related-party” trans-actions to its shareholders? Did AIG’sboard of directors know about these trans-actions? If not, why didn’t AIG’s senior ex-ecutives—who are officers, directors,shareholders, or beneficiaries of SICO—tell the board about the transactions?AIG’s “Code of Business Conduct andEthics” states that “situations whichcould result in conflicts of interest or theappearance of a conflict of interest shouldbe avoided whenever possible.” If an AIGofficer or director is aware of anything thatcould reasonably be expected to create aconflict of interest, he’s supposed to dis-cuss it with the company’s general coun-sel. Ernest Patrikis has been AIG’s gen-eral counsel since 1998. His predecessor,Florence Davis, now runs the StarrFoundation, which owns 2.05% of AIG.What do they know? Or, what don’t theyknow?

AIG ceded a significant amount of“reinsurance” to Richmond InsuranceCompany in Bermuda. Or did it just shiftassets from one of its pockets to anotherand call it reinsurance? AIG’s recent “re-view of operations” turned up “previouslyundisclosed evidence” that AIG controlsRichmond. As a result, there was no transfer of risk, which means that AIG’sfinancials didn’t accurately portray thereal income statement or balance sheet—or maybe both.

Between 2000 and 2003, AIG engagedin some nifty transactions with CapcoReinsurance Company, located in lovelyBarbados. Somewhere between NewYork and the Caribbean these transac-tions magically turned $200 million ofAIG’s underwriting losses into $200 mil-lion of capital losses (losses from invest-ments). That means that AIG’s operatingincome appeared $200 million greaterthan it really was. (Operating income isof great importance, because, as HankGreenberg pointed out in AIG’s 2000 let-ter to shareholders, it’s “the way we andthe investment community look at our re-sults.” Considering that AIG’s stock hasoften traded at thirty times earnings, itseems reasonable to say that the Capcodeals inflated AIG’s market cap by about$1.5 billion.

AIG had other ways to make its oper-ating income appear larger than it reallywas. Between 2001 and 2003, it sold call

REGISTER NOW

David Schiff, editor of Schiff’s Insurance Observer, will tell you whathe’s riled up about these days. Throughout the conference he will, as always,interrogate the speakers and force them to answer brazen questions.

In June 1994, Schiff ’s wrote an admiring profile of Christopher Davis, portfoliomanager of the Davis Funds, which had $300 million under management. (Chrisis the only money manager we’ve ever profiled.) We picked a winner. The DavisFunds now manage $40 billion, and the firm’s primary fund has outperformed theS&P 500 during every meaningful period since its inception in 1969. Chris will tellus about the Davis’s sixty-year history of investing in the insurance business, andshare his thoughts on the mutual-fund industry, shareholder activism, and more.

Two years after receiving his Ph.D. in economics from Harvard, 27-year-oldJames Stone became the youngest insurance commissioner ( Massachusetts)in history. Four years later, in 1979, Jimmy Carter appointed him as chairmanof the Commodity Futures Trading Commission. When his term ended in 1983,he moved back to Boston and founded The Plymouth Rock Company, aprivately-held insurance holding company that now writes well over $1 billionin premiums—quite profitably. Jim will share his perspective on auto insurance,regulation, public policy, and being an entrepreneur in the insurance business.

William Koenig is Senior Vice President and Chief Actuary of “the quietcompany,” Northwestern Mutual. Bill will give us his perspective aboutreserving—especially when it involves universal-life products with secondaryguarantees. His comments, which will not be quiet, should leave some membersof the insurance industry feeling worried.

Lunch: Decent food, fine conversation.

Andrew Kaufman, a founding partner of Kaufman Borgeest & RyanLLP, is one of the leading attorneys specializing in the defense of health-careproviders and hospitals. He’s tried more than sixty cases to verdict, and is thepast president of the New York State Medical Malpractice Defense Bar and pastvice chairman of the American Bar Association Section on Law and Medicine.Andy will give you a view from the battlefield, tell you his thoughts on tortreform, and explain why he’s not for caps on pain and suffering.

continued on next page

9:00 a.m.

9:30 a.m.

10:40 a.m.

11:20 a.m.

Noon

1:00 p.m.

‘A Vast Wasteland’PRESENTING THE ANNUAL

SCHIFF’SINSURANCE CONFERENCE

Tuesday, April 12, 20058:30 am - 5:30 pm

New York City

Registration fee: $695 for subscribers

$745 for non-subscribersCall (434) 977-5877 for more

information, or reserve a place [email protected]

http://www.snlcenter.com/schiff/spring2005/intro.asp

options on some of its bonds that had un-realized gains. It then entered into a seriesof forward transactions and swaps that,somehow, transformed $300 million ofcapital gains into $300 million of “invest-ment income.” (Since investment incomeis a component of “operating income” andcapitals gains aren’t, this had the effect ofoverstating AIG’s earnings power.)

Finally, it turns out that AIG misclassi-fied “certain items,” and, as a result, its re-ported net investment income was over-stated by four percent between 2000 to2004. That doesn’t sound so bad, does it?After all, what’s four percent in the grandscheme of things? Well, it turns out to bea lot—$3 billion. In 2003, for example,this “misclassification” caused AIG’s op-

erating income (the key figure everyonelooks at), to be overstated by about fourpercent—$660 million.

It’s likely that there will be more rev-elations about the unsavory inner work-ings of AIG. Perhaps that’s why AIG putout another press release last night. It wasa letter from CEO Martin Sullivan that,we suppose, was meant to reassure share-holders that AIG wasn’t a house of cardsrun by a gang of con men overseen by di-rectors who are deaf, dumb, and blind.“We are committed to improving trans-parency and corporate governance,” wroteSullivan.

We’re certain that AIG’s governanceand transparency will improve. The ques-tion, however, is this: “Exactly how badare they right now?”

Sullivan also said that it was “unfortu-nate that current circumstances have ob-

scured the reality that AIG’s unique globalfranchise is sound.” Alas, he got it back-wards. It’s unfortunate that AIG’s uniqueglobal franchise obscured the reality of thecompany’s financial condition.

Please continue to the following pages toread articles about AIG from 1998 to 2004.

SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000 APRIL 4, 2005 3

Property insurers’ combined ratios are five to eight points higher than theyshould be, says Robert Dowdell, CEO of Marshall & Swift/Boeckh(M&S/B), which is doing something to remedy that. M&S/B, long known as abuilding-cost provider in claims and underwriting, has become a corporateSherlock Holmes that uses logic and statistical analysis on the massive amountsof data it processes to improve carriers’ underwriting results. “The data has animportant story to tell,” says Bob, who will tell us an important story about riskdifferentiation, pricing, database analytics, and much more.

Warren Buffett talked to just one securities analyst: Alice Schroeder ofMorgan Stanley. In 2003, Alice, then Institutional Investor’s top-ranked P/Canalyst, made an unusual career move—she left the day-to-day world of WallStreet to write a book about Buffett’s life and philosophies. Alice, who is toBuffett what Boswell was to Johnson, won’t be finished with her tome (which wepredict will be a best seller) for a couple of years. In the meantime, she’ll tell youwhat’s on her mind.

David Schiff will have his say on the great insurance issues of the day, and discusswhere he sees value and solvency (or the lack thereof).

Attendees will socialize with their fellow insurance mavens and observers, dis-cussing the day’s events and making deals over cocktails while taking in the viewfrom the top of the New York Athletic Club.

There will be an additional reception and dinner for those who want more of agood thing. The venue is the Coffee House, a convivial, somewhat worn-at-the-edges private club devoted to “agreeable, civilized conversation.” Attendance islimited to 36 people.

1:45 p.m.

2:45 p.m.

3:45 p.m.

4:45 p.m.

6:00 p.m.

‘A Vast Wasteland’PRESENTING THE ANNUAL

SCHIFF’SINSURANCE CONFERENCE

Tuesday, April 12, 20058:30 am - 5:30 pm

New York City

Editor and Writer . . . . . . . . David SchiffProduction Editor . . . . . . . . . Bill LauckForeign Correspondent . . Isaac SchwartzEditorial Associate. . . Yonathan DessalegnCopy Editor . . . . . . . . . . . . John CaumanPublisher . . . . . . . . . . . Alan ZimmermanSubscription Manager . . . . . . Pat LaBua

Editorial OfficeSchiff’s Insurance Observer300 Central Park West, Suite 4HNew York, NY 10024Phone: (212) 724-2000Fax: (434) 244-4615E-mail: [email protected] Website: InsuranceObserver.com

Publishing HeadquartersSchiff’s Insurance ObserverSNL c/o Insurance Communications Co.One SNL Plaza, P.O. Box 2056Charlottesville, VA 22902Phone: (434) 977-5877Fax: (434) 984-8020E-mail: [email protected]

Annual subscriptions are $189. For questions regarding subscriptions pleasecall (434) 977-5877.

© 2005, Insurance Communications Co., LLC.All rights reserved.

Reprints and additional issues are avail-able from our publishing headquarters.

Copyright Notice and WarningIt is a violation of federal copyright law toreproduce all or part of this publication. You arenot allowed to e-mail, photocopy, fax, scan, dis-tribute, or duplicate by any other means thecontents of this publication. Violations of copy-right law can lead to damages of up to $150,000per infringement.

Insurance Communications Co. (ICC) is controlled bySchiff Publishing. SNL Financial LC is a research and pub-lishing company that focuses on banks, thrifts, real estateinvestment companies, insurance companies, energy andspecialized financial-services companies. SNL is a nonvot-ing stockholder in ICC and provides publishing services to it.

SCHIFF’SThe world’s most dangerous insurance publicationSM

I N S U R A N C E O B S E R V E R

It is said that markets are efficient.We won’t bother to debate that. Buteven if they’re efficient, that doesn’tmean they’re always rational.

Markets are made by people, who aregiven to feelings such as optimism, fear, exuberance, and depression. Theirbehavior will now and then drive pricesto extreme highs or lows. (Even Schiff’sInsurance Observer’s subscribers aren’talways rational; several hundred havefailed to sign up for our Evening TelegraphEdition, which is delivered by e-mail orfax and included with subscriptions at noadditional charge.)

When markets become too irrational—when pricing, supply, or demand gets wayout of whack—something usually hap-pens. If, for example, gold were selling for$275 in London and $273 in New York,arbitrageurs would short London gold andbuy New York gold. These actions wouldeventually result in a convergence of theLondon and New York prices.

Insurance can work in a similar fashion.If writing non-standard auto insurance inNorth Carolina is unusually profitable, thesmell of money will cause numerous insur-ers to flock to that market. The increased

competition will then drive profit marginsdown, or eliminate them entirely. Theabsence of profits will cause some insurersto exit the market, which will, in turn,reduce competition and, eventually, createan environment in which profits can bemade—at least for a while.

In a brief examination, we shall turnour attention to AIG, an example of agreat company whose stock trades at anextreme, optimistic, exuberant valuationthat leaves little margin for safety.

There is, of course, a certain logicbehind AIG’s rich valuation. It has a$200-billion market cap and its stock isextremely liquid (which means that insti-tutions can easily buy and sell in size).More importantly, AIG has a long historyof steady growth. (Because AIG hasnever disappointed in the past, many

take it on faith that it will never disap-point in the future.) AIG is a core holdingof institutions and mutual funds, and,according to Zacks, is rated a “buy” by 21of the 24 securities analysts that follow it.

Because of its virtues, AIG’s shareschange hands at 37.4 times earnings and5.8 times book value—levels that arestratospheric, at least as measured byboth basic math and financial history. (Ata 37.4 p/e multiple, investors are earninga 2.7% yield on their investment in AIG.)To justify its current valuation, AIG mustcompound its earnings at a breathtakingrate for a long period—a feat thatbecomes increasingly difficult with size.

The definitive study of AIG, AmericanInternational Group: Cultivating GlobalGrowth, was published in May, when AIG’sstock was at 74. (The report’s authors,

SCHIFF’S

SCHIFF’S INSURANCE OBSERVER • 300 CENTRAL PARK WEST, NEW YORK, NY 10024 • (212) 724-2000 • DAV I D@IN S U R A N C EOB S E RV E R.C O M

September 2000Volume 12 • Number 1 I N S U R A N C E O B S E R V E R

The world’s most dangerous insurance publicationSM

“You suffer from the delusion that your casualty reserves are adequate.”

Walk Softly and Carry a Big Multiple

TA B L E O F C O N T E N T S

An Extreme Price for Growth: There’s no roomfor error in AIG’s stock price . . . . . . . . . . . . . . . . .1

The Catcher in the Rye Reliance: Saul Steinberg’sstory, as you’ve never read it before . . . . . . . . . . . .3

Comparing the Rating Agencies: Best, Moody’s,and S&P on Reliance . . . . . . . . . . . . . . . . . . . . . .4

Steal This Insurance Company: MONY,MetLife, and John Hancock • Demutualization andIts Discontents . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Insurance Companies’ Secret ‘Public’ Data:What’s the Insurance Industry Afraid Of? • TraipsingThrough the Regulatory Morass . . . . . . . . . . . . . .9

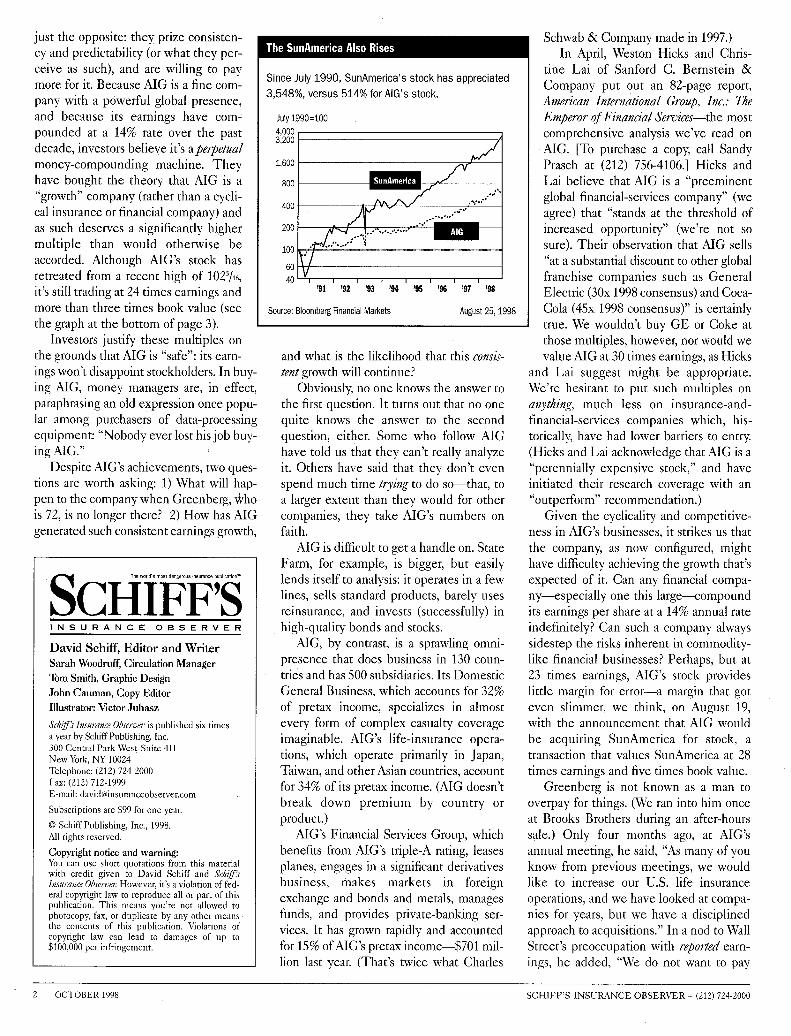

An Extreme Price for Growth

Alice Schroeder, Gregory Lapin, and ChrisWinans, were then at PaineWebber; theyare now at Morgan Stanley Dean Witter.)Their 286-page tome projects that AIG’searnings will grow at a 16% rate through2005. If AIG does indeed do that, its cur-rent stock price, 86, will be 16 times thatyear’s earnings. Viewed another way, if allgoes as planned, in 2005 an investor will“earn” a 6.25% return, based upon AIG’scurrent stock price.

Rather than dispute the detailedanalysis of Schroeder, et al. (Schroeder,after all, is a friend, subscriber, and fea-tured speaker at our spring conference),we’ll stick to the risks of investing inAIG at its current, extreme valuation.

For starters, AIG will not be a big ben-eficiary of any upturn in the domesticproperty-casualty market, since its domes-tic property-casualty income is only 25% ofits operating earnings. (Domestic property-casualty is projected to grow at an 8% clip.)

Although long viewed as a property-

casualty company, AIG has changed itsstripes, and a disproportionate amount ofits future growth is expected to comefrom life insurance, financial services, andasset management. Domestic and foreignlife insurance are projected to grow atmore than a 17% pace, and earnings fromasset management are projected toquadruple by 2005, and comprise 10% ofAIG’s earnings then (up from 5% now).

Way back in our October 1998 issue,when AIG’s stock was 49, we observedthat it was selling at a lofty 24 times earn-ings. The stock is now 86—an even lofti-er 37.4 times earnings.

Although AIG’s earnings haveexpanded at a 17% annual pace over thelast two years, its price-earnings ratio hasexpanded 60%. If AIG’s p/e multiple hadremained constant, its stock price wouldbe 66 rather than 86. (If its multiple hadshrunk to 20 times earnings, its stockwould still be at 49.)

The bottom line: 54% of the gain inAIG’s share price over the last two yearshas been due to the expansion of its p/emultiple, rather than to earnings growth.

Price-earnings multiples cannotexpand indefinitely. Indeed, they havebeen known to contract. This happenedto AIG (and many others) during the1970s (see chart). During the 1990s,however, AIG’s p/e multiple regained itslost ground, and then some, as AIGbecame the insurance stock.

According to Value Line, AIG’s earn-ings have grown at a 13.5% rate over thepast ten years. During that same periodits p/e multiple has expanded from 10.9times earnings to 37.4 times earnings.

An advantage of having a high p/e mul-tiple is that a company’s stock becomes afine acquisition currency. (BerkshireHathaway’s acquisition of General Re forstock is a case in point.) Interestingly, AIGhas not benefited much from its high mul-tiple. Although it acquired SunAmerica forstock, SunAmerica had an even higher p/ethan AIG; thus the acquisition was notimmediately accretive to earnings.

AIG should earn about $5.8 billion in2000. If it is to grow at the projected16% next year, it must come up with anadditional $900 million in earnings. (Byway of comparison, Chubb’s total earn-ings for next year are projected to beabout $825 million.) One way AIG cangrow is by using its high-p/e currency tobuy earnings. AIG is acquiring HSB (for-

merly Hartford Steam Boiler) for $1.2billion in stock—a price equal to 20times earnings. Because AIG’s p/e ratiois almost double that of HSB, the acqui-sition will be accretive to AIG’s earningper share, and, in fact, should representabout 3% of AIG’s earnings-per-sharegrowth next year.

But AIG is so large that it’s difficultfor it to make acquisitions that, by them-selves, materially alter its growth rate. Atthe margin, however, if it can use itsstock to buy lower-multiple companies,then it can eke out incremental growthvia an arbitrage of earnings’ multiples.

Absent an expansion in its multiple, ifAIG grows at a 14% rate forever, aninvestor could expect no more than a14% annual return. If AIG’s growth ratefails to achieve this difficult hurdle, it’sslower growth would likely lead to amuch lower multiple. (A much lowermultiple could also occur if investors’exuberance subsides.)

From our vantage point, the risk ofbuying AIG outweighs the reward. �

2 SEPTEMBER 2000 SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000

Editor and Writer . . . . . . . David SchiffCopy Editor . . . . . . . . . . . . . John CaumanEditorial Associate . . . . . . Isaac SchwartzProduction Editor . . . . . . . . . . Bill Lauck

Publisher. . . . . . . . . . . . . . . . . . Reid NagleSubscription Manager . . . . . . . Pat LaBuaAdvertising Manager . . . . . Mark Outlaw

Editorial OfficeSchiff’s Insurance Observer300 Central Park West, Suite 4HNew York, NY 10024Phone: (212) 724-2000Fax: (212) 712-1999E-mail: [email protected]

Publishing HeadquartersSchiff’s Insurance ObserverSNL c/o Insurance Communications Co.321 East Main Street, P.O. Box 2056Charlottesville, VA 22902Phone: (804) 977-5877Fax: (804) 984-8020E-mail: [email protected]

Subscriptions are $149 for one year, whichincludes a subscription to our EveningTelegraph Edition. For questions regardingsubscriptions please call (804) 977-5877.

© 2000, Insurance Communications Co., LLCAll rights reserved.

Copyright Notice and WarningIt is a violation of federal copyright law toreproduce all or part of this publication. Youare not allowed to photocopy, fax, scan, orduplicate by any other means the contentsof this publication. Violations of copyrightlaw can lead to damages of up to $100,000per infringement.

SCHIFF’SThe world’s most dangerous insurance publicationSM

I N S U R A N C E O B S E R V E R

0

100

200

300

400

500

600

700

-10

-5

0

5

10

15

20

25

30

35

40

AIG: Does Anyone Remember 1972?

P/E ratio

American International Group

Price to Book Value

In 1972, AIG’s shares traded at 518% of bookvalue and 32.6 times earnings. Between 1972and 1974, AIG’s stock fell 66%, as these inflat-ed multiples shrank, even though AIG’s earn-ings grew. During the last two years, AIG’sprice-to-book-value ratio and p/e ratio haveentered uncharted territory.

Source: Value Line

Price to Book Value P/E ratio

0

100%

200%

300%

400%

500%

600%

700%

’72 ’76 ’80 ’84 ’88 ’92 ’96 ’00

40

35

30

25

20

15

10

5

On Tuesday, after the markethad closed, AIG announced anunsolicited $46-per share offerto acquire American General

in a $23-billion stock transaction—a 25%premium over the closing price.

One wouldn’t go so far as to call HankGreenberg a corporate raider, but the factremains: American General had previ-ously agreed to be acquired by Britain’sPrudential Plc. The value of that transac-tion—$26 billion when announced—hadfallen due to the decline in Prudential’sshares. Hank Greenberg, seizing themoment, made a big move at a timewhen his actions were likely to be metwith acceptance from Wall Street, andscant resistance from American General.(Since the company was already in play,management could not easily rebuff asignificantly higher offer.)

That AIG would attempt to use itsrichly valued stock to make acquisitionsisn’t surprising. On February 16 wewrote that we expected insurance com-panies to issue equity to take advantageof the favorable market for insurancestocks. We didn’t expect AIG, “whichsells for 548% of book value, to issuestock in a secondary offering. AIG is solarge ($200-billion market cap) that itcouldn’t do an offering large enough tobe meaningful. Hank Greenberg hassaid, however, that AIG is looking atacquisitions, and given his company’sstupendous price-earnings (p/e) multi-ple, we’d be surprised if his currency ofchoice was not AIG stock.”

Last September, in an article dis-cussing the optimistic valuation accorded

AIG’s shares, we noted that becauseAIG’s stock had an extremely high p/eratio (37.4), it made a fine acquisitioncurrency. We also noted that AIG hadn’tbeen able to put that currency to gooduse. (Given AIG’s multiple, almost anyacquisition would be accretive to earn-ings the first year—although not neces-sarily in later years.)

In order for AIG to maintain its sky-high p/e ratio, at the very least it mustcontinue to achieve the rapid and steadygrowth in earnings per share for which itis known and loved. Given AIG’s sizeand its cyclical businesses—includingproperty-casualty insurance, life insur-ance, investment, finance, financial ser-vices, and aircraft leasing—we’ve beenskeptical (for several years) of AIG’s abil-ity to accomplish that. Consequently,we’ve felt that the risk in owning AIG’sstock was greater than the reward.

Price-earnings ratios and cyclicityaside, acquisitions are one way for AIG togoose its earnings, at least for a while. But,as we observed, “AIG is so large that it’sdifficult for it to make acquisitions that, bythemselves, materially alter its growthrate. At the margin, however, if it can useits stock to buy lower-multiple companies,then it can eke out incremental growth viaan arbitrage of earnings multiples.”

AIG’s proposed takeover of AmericanGeneral would be an example of such anarbitrage.

Hostile?Although AIG’s offer for American

General was unsolicited, there’s somequestion as to whether it’s “hostile,” andwhether AIG engages in hostiletakeovers. The New York Times reported

that Greenberg said his offer was “nothostile.” The Wall Street Journal statedthat “AIG has never pursued a hostiletakeover.”

One could get into a long discussionof what “hostile” means, which we aren’tinclined to do. However, a deal is gener-ally considered hostile if the CEO of thetarget doesn’t want to be taken over—regardless of whether the deal is good forshareholders. We don’t care if a deal ishostile or not, and neither do sharehold-

SCHIFF’S

SCHIFF’S INSURANCE OBSERVER • 300 CENTRAL PARK WEST, NEW YORK, NY 10024 • (212) 724-2000 • DAV I D@IN S U R A N C EOB S E RV E R.C O M

April 5, 2001Volume 13 • Number 8 I N S U R A N C E O B S E R V E R

The world’s most dangerous insurance publicationSM

AIG’s ‘Hostile’ TakeoverAttempt for American GeneralIs AIG’s Stock Too High?

Average Year annual p/e ratio1972 32.61973 28.21974 17.51975 161976 12.41977 9.21978 8.91979 8.81980 8.71981 9.61982 9.71983 11.61984 15.51985 17.11986 15.61987 13.71988 9.21989 11.21990 10.91991 12.11992 12.61993 14.41994 13.21995 14.51996 161997 19.81998 26.71999 28.88/18/00 38.44/5/01 31.9

The rise and fall and rise of AIG’s p/e ratio.

AIG’s Price-Earnings Ratio

2 APRIL 5, 2001 SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000

ers. They generally care about whichdeal gives them the best value.

Whether AIG engages in “hos-tile” deals, however, is a subjectworth a few paragraphs. For exam-ple, AIG has been gradually increas-ing its ownership in 21st CenturyInsurance, and now has 63% of thecompany. Shareholders might right-ly view AIG’s accumulation as a“creeping takeover”—one in whichit gains control without paying thecontrol premium that a tender offerfor the entire company would neces-sitate.

AIG has also struck fear in thehearts of insurance companies in thepast. In 1974, American Reinsurancefiled suit to prevent AIG from buyingmore than 9.9% of American Re’sstock. In 1979, Mission InsuranceGroup rejected an unsolicited mergeroffer from AIG (which then owned4.5% of Mission), stating that thedeal was “not in the best interest ofMission and its stockholders.”(Mission was wrong.)

In 1981, AIG disclosed that it hadacquired 8.53% of USLife, promptingthat company’s chairman, GordonCrosby, to state that USLife’s board wasopposed to any attempt to take over thecompany, and that it was in USLife’s bestinterest to remain independent. In 1982,AIG sold its USLife shares back toUSLife. (In 1997, USLife was acquiredby American General in an all-stocktransaction.)

In 1983, AIG bought 8% ofProgressive and was planning to pur-chase a 12.3% stake held by AmericanFinancial. This threat prompted a groupof Progressive shareholders who held a39% interest in the company to form abloc opposing AIG’s accumulation ofProgressive shares. As a result, AIG can-celled its agreement to buy AmericanFinancial’s 12.3% stake, and AmericanFinancial subsequently sold these sharesback to Progressive.

The American Re, Mission, USLife,and Progressive situations differed fromthat of American General in at least onerespect: none of those companies wasalready “in play,” and AIG would havehad considerable difficulty accomplish-ing a takeover that was unwanted bythose companies. (In order to acquire aninsurance company—especially one with

licenses in many states—the approval ofeach state’s regulator is generallyrequired. A hostile insurance takeover istime consuming, and the regulatory road-blocks can make a deal impossible.Allegheny, for example, was unable totake over St. Paul.)

A final thought: Greenberg hadbreakfast with American General’s CEO,Robert Devlin, six months ago and,according to Greenberg, there was sup-posed to be some follow-up, but it neveroccurred. One presumes that if Devlinhad wanted AIG to acquire AmericanGeneral, then he’d have picked up thephone and asked Greenberg to make abid.

Anyway, Hank Greenberg is a genius,and if he says that his unsolicited offer tobuy American General isn’t “hostile,”then who are we to disagree?

Thoughts on SpeculationBefore discussing this deal further, we

want to step back and examine the cur-rent stock-market environment, specula-tion, and p/e multiples, because theseaffect AIG’s ability to complete a deal,and because they’re driving forces in theindustry.

We conducted a Dow Jones NewsRetrieval search to see how many timesthe words “stock,” “market,” and “bub-

ble” appeared in articles duringMarch. The number—1,710—wassizable, apparently demonstratingthat reporters are good at identifyinga stock-market bubble after it hasburst. (In March 1999, for instance,these words appeared one-third asoften as they did this past March.)

Although we labeled “Internet-stock mania” a “speculative bubble”in our March 1999 issue, we didn’tprofess to know when it would end,even though we had thoughts abouthow it would end. As we wrote,“Whether one chooses to call thecurrent U.S. economic environmenta boom, bubble, bull market, or newera, it will, in all likelihood, be fol-lowed by what will be known as abust, bear market, recession, ordepression.”

While our call was accurate, itwasn’t necessarily something onecould profit from. Indeed, the priceof Internet and tech stocks contin-ued to rise sharply for the next 12

months. In December 1999 we noted that

Yahoo’s market cap—then $93 billion—was equal to those of Marsh & McLennan,Allstate, Cigna, Hartford, Chubb, St. Paul,and Progressive combined.

Things have changed. Yahoo is nowvalued at $7 billion, while the insurancecompanies are worth $25 billion, $30 bil-lion, $16 billion, $14 billion, $12 billion,$9 billion, and $7 billion, respectively, ora total of $113 billion.

How could Yahoo, which had $1.1 bil-lion in revenues in 2000, ever carry a $93billion valuation? (Indeed, one must makevery optimistic assumptions to justify thecompany’s current valuation.) The answeris that Yahoo’s valuation was wildly specu-lative, and represented investors’ frenziedand unwarranted optimism about thecompany’s long-term prospects. Yahoo waspriced for permanent perfection, andwhen that didn’t materialize, its absurd p/eratio gave the company a long way to fallbefore it would be priced rationally. AsJames Grant, editor of the marvelousGrant’s Interest Rate Observer recentlywrote, “Booms don’t last forever: they arecut short by their own excesses…However, busts, too, generate excessesthat tend to hasten cyclical reversals, or atleast to exaggerate their magnitude oncethey start.” continued

Internet 12/10/99 01/14/00 10/13/00 04/04/01America Online $205 $141 $123 $155*Yahoo 93 93 33 7Amazon 36 22 10 3CMGI 23 30 5 0.65

eBay 21 17 15 8.2E*Trade 9 7 4 1.8InsWeb 1 0.7 0.06 0.04Quotesmith 0.2 0.2 0.03 0.006

Insurance 12/10/99 01/14/00 10/13/00 04/04/01AIG $172 $177 $214 $179Marsh & McLennan 24 28 32 25Allstate 22 19 24 30Cigna 15 15 18 16

Hartford 10 10 16 14Chubb 9 10 13 12Progressive 6 5 5 7W. R. Berkley 0.6 0.5 0.8 1.3

*Valuation is after stock merger with Time Warner

Market caps of various companies, in billions of dollars.

E-Madness: Internet vs. Insurance—An Update

SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000 APRIL 5, 2001 3

We bring up Yahoo not just becausewe’ve written about it in the past, butbecause it’s a good example of anextreme. Financial history is filled withcompanies that sported wildly high valu-ations during periods of mass euphoria,and depressed valuations (or no valua-tion) during the ensuing busts.

The boom-and-bust cycle isn’t limit-ed to technology stocks—over the yearsit has embraced virtually every industry,from automobiles, oil & gas, telephones,utilities, and conglomerates, to electron-ics, specialty retail, entertainment,restaurants, finance, and, yes, insurance.

All of which brings us back to AIG.We first expressed concern about thecompany’s p/e and price-to-book ratioback in October 1998 when its stockprice was $49—$27 lower than it is now.We revisited the subject in ourSeptember 2000 issue, when AIG’s stockwas $86. Although AIG’s excellentrecord of earnings growth is one of thefactors in its stock’s superior returns, itisn’t the only factor. AIG’s p/e ratio hasbeen in a long-term bull market of itsown; more than quadrupling since itsbottom in 1979.

A recent Merrill Lynch studyshowed that since 1980, AIG’s averagep/e ratio based on forward consensus esti-mates has been 13.8. The lowest p/eratio—6.8—was recorded in June 1982,and the highest—35.1—occurred inDecember 2000. Perhaps coincidental-ly, AIG’s average p/e, according to theMerrill study, is not very different fromthe S&P 500’s average p/e over the last129 years—14.5.

If one can infer anything about valua-tions from the past it is this: they fluctu-ate considerably. In 1929, for example,the Dow Jones Industrial Average(DJIA) was priced at 4.5 times book

value. Three years later, when the DJIAhit its all-time low, it was valued at one-half of book. (The p/e ratio wasn’t mean-ingful in 1932, as the companies in theDJIA lost money.)

Although the S&P 500’s p/e ratio hasaveraged 14.5 over the long term, stockshave often traded way above, or waybelow, that figure. Valuations, however,have historically reverted to the mean,and then some. Every period in whichstocks have traded in excess of a 14.5multiple has been followed by a periodin which valuations fell well below thatfigure. History, of course is just a guide,not a blueprint for the future. The pastdoes not have to repeat itself.

Thus, the history of AIG’s valuationdoesn’t foretell how AIG’s stock will bevalued in the future. Nonetheless, thepast is still worth considering. In 1972,AIG’s p/e ratio was 32.6—about what it istoday. Despite the fact that AIG’s earn-ings continued to rise steadily, AIG’sshares lost two-thirds of their value overthe next two years, and AIG’s stock pricedidn’t get back to its 1972 high until1978—even though earnings hadquadrupled and book value had tripledduring that period.

AIG is a great company, but there’sconsiderable risk in owning a finan-cial-services company selling for 32times earnings. AIG’s high valuationleaves little room for error or disap-pointment.

In order for AIG’s shares to appreci-ate, two things must happen: earningsper share must grow, and the p/e ratiomust remain the same or go higher.Steadily rising earnings per share areessential because investors, in anticipa-tion of such, have bid up AIG’s stock toan extreme p/e ratio, which, of course,facilitates AIG’s use of its stock to

acquire lower-multiple companies, thusproviding a boost to earnings per share.As AIG gets larger—and it is alreadyhuge—greater than average growthbecomes more difficult.

While it’s wise for AIG to use its high-multiple stock to make acquisitions, oneconcerned with security analysis mustask a basic question: if AIG, which tradesat 32 times earnings, buys AmericanGeneral for 18 times earnings, shouldAIG’s 32 multiple be applied toAmerican General’s supposedly lower-growth business once that businessbecomes part of AIG? According toGreenberg, the answer is yes. At yester-day’s conference call he spoke of cross-marketing and cost savings, and said,“I’m comfortable that two and two herewill make five, if not seven.”

In the 1960s, under the guise of “syn-ergy”—a 2+2=5 equation—conglomer-ates, which had staggeringly high p/eratios, acquired diverse, lower-multiplebusinesses including bakeries, foundries,machine shops, and insurance compa-nies. For a while, the market was willingto apply the conglomerates’ high p/emultiples to the earnings acquired fromthe acquisition of slower-growth busi-nesses. Eventually, however, the merry-go-round came to a halt.

In theory, AIG—or any business witha high p/e ratio—can be a perpetualgrowth machine by endlessly performingthe arbitrage of using its high p/e stock toacquire earnings that are selling at alower p/e. In practice, this is difficult todo, and, of course, is dependant upon,among other things, always having a highp/e multiple.

Investors in AIG would do well toremember that AIG, which traded at 32.6times earnings in 1972, traded at 8.7times earnings in 1980, 9.2 times earn-ings in 1988, and 13.2 times earnings in1994.

Although Yahoo traded at 100 timesrevenues last year, we doubt that AIG’sp/e ratio has much room for expansion.Absent any change in the p/e,investors’ returns will mirror AIG’sgrowth, which many analysts peg atabout 15% annually.

If that growth fails to materialize forsome reason—or if earnings actuallydecline, as they did in 1984—it’s a safebet that AIG will trade at a much lowermultiple. �

Editor and Writer . . . . . . . . . . . David SchiffCopy Editor . . . . . . . . . . . . . . . . . John CaumanEditorial Associate . . . . . . . . . . Isaac SchwartzProduction Editor . . . . . . . . . . . . . . Bill Lauck

Publisher . . . . . . . . . . . . . . . . Alan ZimmermanCustomer Service Director . . . . . . Pat LaBuaAdvertising Manager . . . . . . . . . Mark Outlaw© 2001, Insurance Communications Co., LLC.All rights reserved.

Editorial OfficeSchiff’s Insurance Observer300 Central Park West, Suite 4HNew York, NY 10024Phone: (212) 724-2000Fax: (212) 712-1999E-mail: [email protected]

Publishing HeadquartersSchiff’s Insurance ObserverSNL c/o Insurance Communications Co.321 East Main StreetP.O. Box 2056Charlottesville, VA 22902Phone: (804) 977-5877Fax: (804) 984-8020E-mail: [email protected]

SCHIFF’SThe world’s most dangerous insurance publicationSM

I N S U R A N C E O B S E R V E R

In its reports for the years ending2001 and 2000, AIG’s audit commit-tee disclaims virtually all responsi-bility for AIG’s accounting, internal

controls, and financial statements. It alsosays that it cannot assure that AIG’s inde-pendent accountants are actually “inde-pendent.” (The most recent audit-com-mittee report is on page 17 of AIG’sproxy statement.)

If AIG’s audit committee can’texpress an unqualified opinion aboutAIG’s accounting, doesn’t it makesense that the public’s faith in AIG’saccounting should be somewhat dimin-ished? And, if the public’s faith isdiminished, isn’t it reasonable toexpect AIG’s stock to trade at a lowermultiple of earnings than it would oth-erwise trade?

Before discussing these issues, we’llnote that AIG has been the greatest suc-cess story in the insurance business. It’sthe largest, most important insuranceorganization in the world. The story of itssuccess, however, is not readily available.Although Hank Greenberg is a legend, hisachievements have not received wide-spread attention. Jack: Straight from the Gutis on the best-seller list; Hank: Straightfrom 70 Pine Street, will probably not bewritten.

We have great admiration forGreenberg (given his record, it’s hard notto), and are planning to write a lot aboutAIG in the coming months. Althoughwe’d prefer to write chronologically, pub-lishing constraints make this difficult.Thus, this article focuses on currentissues rather than on AIG’s 1969 exchangeoffers or Greenberg’s letters to sharehold-ers in the 1970s, even though all of thesesubjects are of equal interest to us.

In the post-Enron Era, the minutia ofaccounting principles have becomeof greater concern to many. Investors,

having recently seen several trillion dol-lars of stock-market value melt like but-ter on a hot skillet, are more skeptical ofcompanies whose finances are complexor opaque—even those companies withfine long-term records. This wariness islogical; if you can’t understand a businessand analyze its financials, how can youplace a value on the company?

This was not a question asked oftenenough during the great bull market,when the “extrapolation method” ofanalysis was sufficient for many“investors.” (They would take recentyears’ reported earnings and project thesame growth rate for many years into

the future.) This method had its advan-tages: it was really simple and saved alot of time that would have otherwisebeen spent reading balance sheets,cash-flow statements, and footnotes.

The extrapolation method has adrawback, however—it doesn’t work.The footnotes, fine print, and SEC-man-dated disclosures are there becausethey’re important. Words really meansomething, and when a company sayssomething unusual—or doesn’t saysomething usual—one should take thatinto consideration.

AIG has a long record of growth, butthe market’s opinion of its growth hasvaried. In 1988, AIG’s stock traded at anaverage of 9.2 times earnings. ByDecember 8, 2000, when the stock hit an

SCHIFF’S

SCHIFF’S INSURANCE OBSERVER • 300 CENTRAL PARK WEST, NEW YORK, NY 10024 • (212) 724-2000 • DAV I D@IN S U R A N C EOB S E RV E R.C O M

May 2, 2002Volume 14 • Number 7 I N S U R A N C E O B S E R V E R

The world’s most dangerous insurance publicationSM

The Greatest Risk is Taking Too Much Risk

Hank Greenberg stays ahead of his competitors.

AIG’s Audit-Committee Report

2 MAY 2, 2002 SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000

all-time high of $103.75 (it is now$71.51), the p/e ratio had quadrupled to42. Such a multiple is difficult to justifyin any company, much less one so largethat its future growth rate cannot possi-bly match its past.

What is the proper multiple for ahighly complex, international financial-services conglomerate whose businessesare cyclical? We don’t know—nor doesanyone else—but the lower the multiple,the more appealing we find the stock.

In 2001, AIG’s earnings did some-thing that not one of the dozens of ana-lysts following the company expected—they declined. The decline, the firstsince 1984, was a reminder that even thegreatest companies are not immune tothe vicissitudes of business. Investors,

however, don’t like being reminded thatthe earnings of “growth” companies donot always grow. (While a growthcompany’s failure to grow may be irk-some to growth-stock investors, it is notnearly so irksome as the failure of agrowth company to maintain solvency—the condition that afflicted Enron.)

According to the SEC, “Audit com-mittees play a critical role in thefinancial reporting system by over-

seeing and monitoring management’sand the independent auditors’ participa-tion in the financial reporting process.”Financial statements are prepared bymanagement and audited by independentaccountants.

PricewaterhouseCoopers, AIG’s inde-pendent accountants, says that it con-ducted its audit of AIG in accordancewith generally accepted standards, andthat the audit provides a reasonable basisfor its opinion that AIG’s financial state-ments present the company’s financialcondition fairly, in all material respects.This is standard lingo found in virtuallyevery financial statement.

AIG’s audit-committee report, how-ever, provides an opinion that’s ambigu-ous, elusive, equivocal, hedged, andoblique—qualities that aren’t particular-ly comforting to investors or creditors.(Perhaps the only outside parties thatwould like the wording in the audit-com-mittee report are the company’s D&Oinsurers.) The report does not containthe same language found in many otheraudit-committee reports. In fact, AIG’saudit committee’s disclaimers are soextensive that they render the report vir-tually meaningless.

The key paragraph in AIG’s audit-committee report follows. We’ve addeditalics for emphasis:

The members of the [Audit] Committee arenot professionally engaged in the practice ofauditing or accounting and are not experts inthe fields of accounting or auditing, including inrespect of auditor independence. Members ofthe Committee rely without independent veri-fication on the information provided to themand on the representations made by manage-ment and the independent accountants.Accordingly, the Committee’s oversight does not pro-vide an independent basis to determine that manage-ment has maintained appropriate accounting andfinancial reporting principles or appropriate inter-nal controls and procedures designed to assurecompliance with accounting standards andapplicable laws and regulations. Furthermore,

the Committee’s considerations and discussionsreferred to above do not assure that the audit of AIG’sfinancial statements has been carried out in accor-dance with generally accepted auditing standards,that the financial statements are presented in accor-dance with generally accepted accounting principlesor that AIG’s auditors are in fact “independent.”

The disclaimers in AIG’s audit-com-mittee report aren’t common. PerhapsAIG is on the cutting edge, however, andin years to come more audit committeeswill adopt similar verbiage.

Viewed by itself, AIG’s audit-com-mittee report is not such a big deal. Butviewed in the context of AIG’s inherentcomplexity and the inherent imprecisionof insurance-company “earnings,” ittakes on greater meaning and is worththinking about.

AIG’ stock has declined more than30% from its all-time high, and isnow trading at the price it was

three years ago—despite the fact that thecompany is expected to produce recordearnings this year. On many occasions,AIG has benefited from having a highp/e ratio; it has been able to use its stockto make acquisitions on attractive terms.Its current p/e ratio (about 20 times pro-jected earnings) reduces the possibilityof most stock acquisitions because theeffect of issuing stock at this level (rela-tive to what AIG would receive inreturn) would probably be dilutive toearnings rather than accretive.

None of this is lost on HankGreenberg, who seemingly knows every-thing. He is acutely aware of the impor-tance of financial strength as well as theimportance of perception. If, for example,people perceive—correctly or incorrect-ly—that AIG does not pay claims, it will, atthe margin, hurt AIG’s business. If AIG’sfinancial strength is perceived as beingweaker than it is, that can become a self-fulfilling prophecy as lenders demandslightly higher spreads, causing the compa-ny’s cost of capital to rise, thereby reducingprofitability. Finally, if AIG’s stock price istainted by Enronesque issues such as com-plexity, lack of transparency, or sheerincomprehensibility, then it stands to rea-son that the stock will trade at a lower mul-tiple of earnings than it would otherwise.

While no one knows with certaintythe reasons why a stock goes down (otherthan the obvious—that sellers were morepersistent than buyers), it appears that

Editor and Writer . . . . . . . David SchiffProduction Editor . . . . . . . . . . Bill Lauck

Publisher . . . . . . . . . . . . Alan ZimmermanSubscription Manager . . . . . . . Pat LaBuaAdvertising Manager . . . . . Mark Outlaw

Editorial OfficeSchiff’s Insurance Observer300 Central Park West, Suite 4HNew York, NY 10024Phone: (212) 724-2000Fax: (212) 712-1999E-mail: [email protected]

Publishing HeadquartersSchiff’s Insurance ObserverSNL c/o Insurance Communications Co.321 East Main StreetP.O. Box 2056Charlottesville, VA 22902Phone: (434) 977-5877Fax: (434) 984-8020E-mail: [email protected]

For questions regarding subscriptions pleasecall (434) 977-5877.

© 2002, Insurance Communications Co., LLC.All rights reserved.

Copyright Notice and WarningIt is a violation of federal copyright law toreproduce all or part of this publication. You arenot allowed to e-mail, photocopy, fax, scan, dis-tribute, or duplicate by any other means thecontents of this publication. Violations of copy-right law can lead to damages of up to $100,000per infringement.Reprints and additional issues are availablefrom our publishing headquarters.

Insurance Communications Co. (ICC) is controlled bySchiff Publishing. SNL Financial LC is a research and pub-lishing company that focuses on banks, thrifts, real estateinvestment companies, insurance companies, energy andspecialized financial-services companies. SNL is a nonvot-ing stockholder in ICC and provides publishing services to it.

SCHIFF’SThe world’s most dangerous insurance publicationSM

I N S U R A N C E O B S E R V E R

SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000 MAY 2, 2002 3

AIG’s stock has been under pressure forseveral reasons: 1) it had been selling atan unusually high multiple; 2) the com-pany reported a decline in earnings lastyear, 3) investors are more concernedabout accounting and complexity thanthey have been in the past; 4) AIG is dif-ficult to understand, and investors are

less willing to accord high multiples tothings they don’t understand; and 5) AIGis a diversified financial company ratherthan a pure play on property-casualty, andtherefore is not benefiting as much assome companies from the turn in cycle.

AIG’s stock price appears to be of consid-erable concern to AIG, and the company has

been attempting to respond to various crit-icisms. For example, it has been faulted forhaving too few “independent” directors. Itsresponse: Bernard Aidinoff, a director since1984, is now “senior counsel” at Sullivan &Cromwell (which represents AIG) ratherthan a “partner.” And Carla Hills, a directorsince 1993, terminated her consultingagreement with AIG in early 2002. Wedoubt that these cosmetic changes willmake Aidinoff and Hills better or worsedirectors than they were before. (Most cor-porate directors aren’t too independent,anyway. If they were, they wouldn’t be puton a board in the first place.)

AIG has now instituted quarterly con-ference calls—the first was held lastweek—and has provided additional dis-closure in its annual report and 10-K. Ithas also attempted to deal with the “suc-cession” issue by creating an Office ofthe Chairman, naming co-chief operatingofficers, and announcing several promo-tions. (The actuaries at Schiff’s think thatGreenberg is in better shape than mostinsurance-company CEOs, and won’tneed a successor for many years.)

It’s impossible to say whether any ofthe changes made by AIG will have anyeffect on the company’s stock price. AsBenjamin Graham famously wrote, in theshort term the market is a voting machine;in the long term it is a weighing machine.

Which brings us to the morning ofApril 22. AIG’s stock was down severalpoints amidst rumors that the companywould miss its second-quarter earnings(it didn’t), and that it was being investi-gated. In the early afternoon, AIG putout the following press release: “AIG’sstock is trading down significantly. Wehave observed considerable short sellingin the stock and have requested the NewYork Stock Exchange and the Securitiesand Exchange Commission to investi-gate this activity.”

Blaming shortsellers for a decline in acompany’s stock is a tactic often used byhighly promotional companies whoseshares are overvalued, and is unusual fora company of AIG’s stature, for many rea-sons. First of all, shortselling is not illegal orunethical. (At year end, AIG was short $8.3billion of securities and commodities.) Sowhy did AIG ask the authorities to inves-tigate? (“No comment,” said AIG.)

If AIG is so concerned about the trad-ing activity in its stock, why didn’t it askthe SEC and NYSE to investigate the

Do someone a favor. Send them a free gift subscription.

Give us the names of one or more people you think would enjoy reading Schiff’s Insurance Observer and we’ll send them

a free gift subscription (four issues) from you. Please send an e-mail to [email protected] and include the name, company, and e-mail address of the people you would like to give

a free gift subscription to. We’ll take care of the rest.

David Schiff looks for new subscribers.

SCHIFF’SThe world’s most dangerous insurance publicationSM

I N S U R A N C E O B S E R V E R

Gift subscriptions will not be sent to current subscribers.

4 MAY 2, 2002 SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000

considerable buying (and all the broker-age “buy” recommendations) when itsshares were 50% higher and, apparently,trading under the influence of irrationalexuberance?

Also, how did AIG “observe” shortselling on April 22? (“No comment,” saidAIG.)

AIG’s request that the NYSE investi-gate carries extra weight. HankGreenberg is on the NYSE’s board, andAIG director, Frank Zarb, is the formerchairman of the NYSE’s nominating com-mittee. Section 202.03 of the NYSE’s“Listed Company Manual” provides thefollowing recommendations for dealingwith rumors or unusual market activity:

220022..0033 DDeeaalliinngg wwiitthh RRuummoorrss oorr UUnnuussuuaallMMaarrkkeett AAccttiivviittyy

If rumors or unusual market activity indi-cate that information on impending develop-ments has leaked out, a frank and explicitannouncement is clearly required. If rumors arein fact false or inaccurate, they should be promptlydenied or clarified. A statement to the effect that thecompany knows of no corporate developments toaccount for the unusual market activity can have asalutary effect…[Emphasis added.]

The Exchange recommends that its listedcompanies contact their Exchange represen-tative if they become aware of rumors circu-lating about their company...Information pro-vided concerning rumors will be promptlyinvestigated.

Why didn’t AIG use the standardNYSE comment—that it knows of nocorporate developments to account forthe unusual market activity—in its pressrelease? (“No comment,” said AIG.)

After all the “no comments” we didn’tbother asking AIG if it “observed” any ofthe alleged shortsellers reading a copy ofthe company’s audit-committee report. E

Coming soon in a future issue of Schiff’sInsurance Observer: “The Great Greenbergand the Rise of AIG.”

On May 2 we published an arti-cle about AIG’s audit-com-mittee report. Specifically,we noted that the report’s

elusive, equivocal verbiage made it lit-tle more than an extensive disclaimer—exactly the opposite of what an audit-committee report should be.

Audit-committees reports are a dullsubject. So dull, in fact, that to the bestof our knowledge, no one else in theworld had written about the disclaimersin AIG’s report. (In fairness to AIG, anumber of other large companies usedthe same evasive language.)

Our article caused a stir among insur-ance cognoscenti, and then createdsomething of a commotion when TheEconomist had the good judgment to pickup our story. Although we received posi-tive feedback from many subscribers, wewere amazed that some subscribers—including respected analysts and insur-ance-company presidents—told us thatour observations were out of line. Auditcommittees are not worthy of so muchattention, they said, and it reflectedpoorly on us to be making a big dealabout them.

It seems remarkable that less thanthree months ago learned folks stillbelieved that the numbers in companies’financial statements were sanctified justbecause CEOs and the accountants theyhired set those numbers in type.

Of course, any belief in the inviolabil-ity of corporate accounting disappearedon June 25, when WorldCom’s numericalinnovations became known. That audit-ed financial statements can be manipulat-ed so that losses become profits is noth-ing new. Nor is it new that many compa-nies are run by rapacious scoundrels.

During bull markets investors happi-ly ignore blatant warnings. In our August1999 issue, for example, we commentedon InsWeb, the Internet insurance mar-ketplace that had just gone public andcommanded a $1.5 billion market cap,even though it had virtually no revenuesand expected to “incur substantial oper-ating losses for the foreseeable future.”

Thanks to the Securities Act of 1933,there was no reason for any investor tolose a penny investing in InsWeb. TheSecurities Act—also known as the “truthin securities” law—requires issuers toprovide investors with meaningful dis-closure. InsWeb dutifully carried out itsresponsibility, and warned investorsabout the toxicity of its common stock.The “risk factors” section of its prospec-tus came in at 8,477 words, which maybe a record. (InsWeb’s stock is nowdown 99%.)

In our May 2 article, we questionedwhether the failure of AIG’s audit com-mittee to express an unqualified opinionabout the company’s accounting wouldcause AIG’s stock to trade at a lower mul-

tiple of earnings. (AIG stock was then$71.51; it is now $53.38.)

Before we delve further into AIG’saccounting and audit-committee report,the SEC, and related subjects, we wantto make sure that readers put ourthoughts in perspective. Over the yearswe’ve written about a dozen articles onAIG. We’ve commented on its success,complexity, mergers and acquisitions,and p/e ratio. In late 1994 we wrote thatAIG’s stock was cheap and that we’dbought it. (We sold it several years later.)In 1998 and 2000, we noted that AIG’sp/e ratio was so high that the stock pricehad scant margin of safety. We’ve alsowritten about companies that AIG hassubsequently acquired (SunAmerica),and about AIG’s mysterious offshorereinsurance transactions (Coral Re).

There are many reasons to writeabout AIG, not the least being that it isthe largest, most important, and greatestworldwide insurance organization. AIG,by virtue of its size, scope, “AAA” rating,and nature is a fabulous (and fabulouslycomplex) company. It is not, however,

SCHIFF’S

SCHIFF’S INSURANCE OBSERVER • 300 CENTRAL PARK WEST, NEW YORK, NY 10024 • (212) 724-2000 • DAV I D@IN S U R A N C EOB S E RV E R.C O M

July 25, 2002Volume 14 • Number 10 I N S U R A N C E O B S E R V E R

The world’s most dangerous insurance publicationSM

AIG, Audit Committees, Legends, and P/E RatiosThe Tao of Hank, Part 1

AIG’s Audit Committee Report: Caveat Emptor

The key paragraph in AIG’s audit-committee report follows. Italics have been added for emphasis.

The members of the [Audit]Committee are not professionally engagedin the practice of auditing or accountingand are not experts in the fields ofaccounting or auditing, including inrespect of auditor independence.Members of the Committee rely withoutindependent verification on the informa-tion provided to them and on the repre-sentations made by management and theindependent accountants. Accordingly, theCommittee’s oversight does not provide an inde-pendent basis to determine that management

has maintained appropriate accounting andfinancial reporting principles or appropriateinternal controls and procedures designedto assure compliance with accounting stan-dards and applicable laws and regulations.Furthermore, the Committee’s considerationsand discussions referred to above do not assurethat the audit of AIG’s financial statements hasbeen carried out in accordance with generallyaccepted auditing standards, that the financialstatements are presented in accordance withgenerally accepted accounting principles or thatAIG’s auditors are in fact “independent.”

2 JULY 25, 2002 SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000

easy to understand, and cannot be fullyunderstood by an outsider. (Actually, itcannot be fully understood by an insider,either, but that’s probably true of everygiant multinational.) AIG’s history—which we’ve been researching for sometime—is a story of entrepreneurship, dar-ing, audacity, internationalism, and capi-talism. It is a remarkable feat that in 40years or so, AIG, which was a loosely-knit group of foreign underwriting agen-cies, life insurers, and second-ratedomestic insurers—managed to eclipse,by a wide margin, the titans of yesteryear:Aetna, CNA, Connecticut General,Continental, The Hartford, The Home,INA, Metropolitan, Prudential, Travelers,and USF+G. Today, AIG is worth muchmore than all these combined.

Hank Greenberg, who has led AIGfor the last 33 years, is admired,respected, and feared. Greenberg,despite his 77 years, is not mellow; he’sintense and competitive. He’s alsocharming, charismatic, funny, anddeeply concerned about every aspect ofhis business. He’s filled with energyand enthusiasm, and, despite hisinvolvement with big issues around theglobe, seems easily aggravated bydetails so small you wouldn’t expect theCEO of one of the world’s largest com-panies to pay attention to them.Greenberg’s attention to minutia doesnot seem to have hurt his company’sresults. Perhaps it has even contributedto his success.

If there’s anyone in the industry whocan be considered a living legend, it isGreenberg. This status was dramatizedat Schiff’s Insurance Conference in April, atwhich he was the first speaker. AfterGreenberg had talked for almost anhour without notes, he was asked a goodquestion: “How do you spend yourday?” He gave an answer that interestedour hardboiled, skeptical audience. (Wewon’t repeat it; you just had to bethere.) It is unimaginable that the sameaudience would exhibit much curiosityabout how other insurance CEOs spendtheir days.

Why do insurance mavens care whatGreenberg does all day? We carebecause, in an industry where it’s so easyto go awry and so hard to excel, AIG hasaccomplished what no other companyhas. Watching Greenberg’s performanceis akin to watching a sleight-of-hand

artist who makes cards appear and disap-pear. Although you know the legerde-main isn’t magic—it’s the result of prac-tice and hard work—it seems like magic.

“When the legend becomes fact,print the legend,” says the newspapereditor at the end of John Ford’s elegiacWestern, The Man Who Shot LibertyValance. But separating legends fromfacts is often impossible. “Once a news-paper touches a story, the facts are lostforever,” Norman Mailer wrote, “even tothe protagonists.” So we all read about theGreenberg of legend: the World War IIand Korean War veteran who’s tough,hard-driving, combative, and intolerantof failure. There is, of course, much moreto him.

Greenberg is a disciplined man. He islean and fit, and his posture is perfect.He is careful about what he eats andexercises regularly. He appears to havelittle interest in the trappings of extremewealth. He doesn’t have the fanciesthomes or the biggest art collection, andhis name doesn’t appear in societycolumns. He wears conservative suits,button-down shirts, and an inexpensivewatch. He loves to ski and play tennis.He can recall names and details from 50years ago.

Schiff ’s has gotten to know manyinsurance CEOs reasonably well over theyears. One could say that they all have areason to talk to us: to attempt to influ-ence us or to get on our good side (thepresumption being that we actually havea good side). Out of all those CEOs, wehave never met anyone who has been asopen as Greenberg.

And yet, there are many Wall Streetanalysts who are terrified of him becausethey believe that if he wanted to, he couldcause them to be fired. This may or may notbe true, but if it is widely believed, thenisn’t the effect the same as if it weretrue?

Many of Greenberg’s competitors—sane, successful men—are also afraid ofpissing him off because—mind you, thisis just one example—he controls the NewYork Department of Insurance and could getthem tied up in a regulatory morass.Whether he really controls the depart-ment is irrelevant to the perception thathe does. The effect on his competitorsis the same. (When we discussed thiswith him, Greenberg scoffed at thenotion that he controls the insurance

department, and grumbled somethingabout how long it takes AIG to get fil-ings through.)

The foregoing brings us back toour May 2 article about AIG’saudit-committee report, and our

musings about the effects that issues ofcomplexity and transparency have onAIG’s stock price and p/e ratio.

The gist of our article was that AIG’saudit committee, in its reports for theyears ending 2001 and 2000, used atypi-cal—and in our view, inappropriate—lan-guage: “The [audit] committee’s over-sight does not provide an independentbasis to determine that AIG’s manage-ment has maintained appropriate inter-nal controls and procedures,” statedAIG’s audit-committee report. “Thecommittee’s considerations…do notassure that the audit of AIG’s financialstatements has been carried out in accor-dance with generally accepted auditingstandards…or that AIG’s auditors are infact ‘independent.’” [Emphasis added.]

The audit-committee’s verbiageprompted us to pose two questions: 1) IfAIG’s audit committee (which, like allaudit committees, is comprised of “inde-pendent” directors), can’t express anunqualified opinion about AIG’saccounting, doesn’t it make sense thatthe public’s faith in AIG’s accountingshould be somewhat diminished, and 2)if the public’s faith is diminished, isn’t itreasonable to expect AIG’s stock to tradeat a lower multiple of earnings than itwould otherwise?

The first question is more important,because if the answer to it is “No,” thesecond question becomes moot. Since itis a fact that AIG’s audit-committeereport contains caveats that render it vir-tually meaningless, we are faced with theinevitable question: Will these caveatsdiminish the public’s faith in AIG’saccounting?

There are reasons why one couldanswer “No”: 1) Some other large com-panies use identical language, and, per-haps, hundreds use similar language; 2)The caveats are there for legal reasons; 3)The financial statements are prepared bymanagement and audited by outsideaccountants; 4) The audit committeemerely plays an “oversight” role.Assurance about the financial state-ments comes from the outside accoun-

SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000 JULY 25, 2002 3

tants in the “Report of IndependentAccountants” and from AIG’s manage-ment in the “Report of Management’sResponsibilities;” 5) The audit commit-tee can’t be expected to provide assur-ance that the financial statements con-form to GAAP or that the accountants areactually independent; 6) The audit com-mittee is comprised of respectable peo-ple; and, 7) One would have to be out ofhis mind to think that anyone gives adamn about audit-committee reports.

These responses are reasonableenough, but we continue to doubt they’llsatisfy every thoughtful, intelligentinvestor. If that is correct, then it’s rea-sonable to assume that the caveats inAIG’s audit-committee report have someeffect on AIG’s p/e multiple, even if thateffect is slight. We don’t know of any way

to estimate what the effect will be or howto measure it.

As we mentioned in our previous arti-cle, in the post-Enron (and now, post-WorldCom) era, accounting minutia areof greater concern to many. By itself,AIG’s audit-committee report is not asmoking gun. However, no one viewsanything by itself. The audit-committeereport is one piece of a large puzzle. Onone hand there’s AIG’s great history andstrong businesses; on the other handthere’s the company’s inherent “black-box” complexities. Investors, for goodreasons, are now more wary of complexi-ty—and of things they don’t understand.

AIG’s caveat-filled audit-committeereport is a farce, and AIG’s board made amistake when it accepted it. Perhaps itdidn’t understand that the times werechanging and AIG’s stock, which hadtraded at an unusually high p/e multiplefor many years, was vulnerable. We wrotenumerous times over the last four yearsthat the risk of buying AIG’s shares at astratospheric p/e multiple outweighedthe reward.

AIG’s p/e multiple, which had been asingle-digit figure for much of the 1970sand 1980s, rose sharply after 1988, whichboosted the increase in AIG’s stock priceover the years. (The p/e multiple even-tually peaked at about 42—a figure thatleft virtually no margin of safety.) AIG’sstock has been declining for a year and ahalf. Viewed another way, the company’sp/e multiple has been contracting.

Beginning next month, HankGreenberg will file a sworn written state-ment with the SEC personally attestingthat AIG’s financials are materially truth-ful. (Officers at 945 large companies mustfile the same statement for their compa-nies.)

Beginning next year, we expect AIG’saudit committee to drop the caveats anddisclaimers in its report. While that won’tmake AIG easier to analyze, it will makethe audit committee more responsiblefor its work. That can only be a goodthing. E

To be continued. Part 2 of this article willprobably appear early next week.

A couple of months ago, when discussingAIG with Greenberg, we said that when valu-ing the company we put a lower multiple onearnings from GICs than on other earnings.Greenberg’s response: “I don’t think youshould value the company based on the com-

ponents of its earnings. It’s the diversificationof earnings that’s important. That’s whatmakes AIG. It’s the totality...not the pieces.AIG is a great company with an unparalleledfranchise. You couldn’t put it together today ifyou wanted to.”

We don’t use the same method to valueAIG that Hank does, but we do agree with hissentiments. Although we don’t think AIG’sstock is a bargain, in the interest of full dis-closure we must admit that we became ashareholder yesterday. We paid $49 pershare—14 times this year’s projected earn-ings. That’s higher than we like to pay, and itgives our investment a more speculative char-acteristic than we ordinarily prefer.

Unlike stockbrokers, who rate a stock a“buy” and then list a much higher targetprice, we tend to think about how much lowera stock must go before we buy more. Rightnow we’re planning to double our investmentwhen AIG hits 39. Of course, we may changeour opinion. If we do, it is highly unlikely thatwe will notify you at that moment.

Editor and Writer . . . . . . . David SchiffProduction Editor . . . . . . . . . . Bill Lauck

Publisher . . . . . . . . . . . . Alan ZimmermanSubscription Manager . . . . . . . Pat LaBuaAdvertising Manager . . . . . Mark Outlaw

Editorial OfficeSchiff’s Insurance Observer300 Central Park West, Suite 4HNew York, NY 10024Phone: (212) 724-2000Fax: (212) 712-1999E-mail: [email protected]

Publishing HeadquartersSchiff’s Insurance ObserverSNL c/o Insurance Communications Co.321 East Main StreetP.O. Box 2056Charlottesville, VA 22902Phone: (434) 977-5877Fax: (434) 984-8020E-mail: [email protected]

For questions regarding subscriptions pleasecall (434) 977-5877.

© 2002, Insurance Communications Co., LLC.All rights reserved.

Copyright Notice and WarningIt is a violation of federal copyright law toreproduce all or part of this publication. You arenot allowed to e-mail, photocopy, fax, scan, dis-tribute, or duplicate by any other means thecontents of this publication. Violations of copy-right law can lead to damages of up to $150,000per infringement.Reprints and additional issues are availablefrom our publishing headquarters.

Insurance Communications Co. (ICC) is controlled bySchiff Publishing. SNL Financial LC is a research and pub-lishing company that focuses on banks, thrifts, real estateinvestment companies, insurance companies, energy andspecialized financial-services companies. SNL is a nonvot-ing stockholder in ICC and provides publishing services to it.

SCHIFF’SThe world’s most dangerous insurance publicationSM

I N S U R A N C E O B S E R V E R

American International Groupcan run but it can’t hide, andHank Greenberg knows that.Times have changed, and AIG

is trying to change with them. Thus, inthe new corporate spirit of opennessand transparency, AIG has held its firstquarterly conference call to discuss itsearnings, created an office of the chair-man, made two of its so-called “inde-pendent” directors more “indepen-dent,” ran an all-day meeting forinvestors, provided new disclosures inits annual report and 10-K, andannounced that it will expense stockoptions beginning next year.

Most of these changes are cosmetic—form over substance—but they’re posi-tive and make good sense for AIG which,due in part to its complexity and inher-ent impenetrability, is now viewed withconsiderably more skepticism than it hasbeen for many years.

For our money, however, the mostsignificant change that AIG will make isone that hasn’t been reported: it will alterits audit-committee report in next year’sproxy statement.

For the past two years AIG’s board ofdirectors has accepted—and fobbed off onshareholders—audit-committee reportsthat were evasive, equivocal, and not inkeeping with the spirit of last year’s SECrequirement that an audit-committeereport be included in public companies’proxy statement.

Beginning next year, AIG’s audit-committee report will, apparently, con-tain a positive opinion about AIG’s finan-cial reporting rather than a disclaimerdesigned to insulate AIG’s directors fromresponsibility. Greenberg, who is con-cerned with transparency and appear-

ances for many reasons (not the leastbeing that the perception that there’ssomething to hide affects the company’sstock price and access to capital), told ushe will “insist” upon a better audit-com-mittee report. “I don’t think anyone paidmuch attention to it,” he said, referringto the myriad qualifications in AIG’saudit-committee report. “We relied onoutside counsel. In retrospect, that was amistake.” Greenberg, who’s been in theinsurance business for 50 years, didn’tbecome The Great Greenberg by lettingmistakes go uncorrected.

For those who don’t recall the May 2and July 25 issues of Schiff’s, we’ll pro-vide a brief reminder: AIG’s audit-com-mittee report, as it is now written, is notan endorsement of the company’saccounting; rather, it’s a legal disclaimerfor the audit committee. “The [audit]

committee’s oversight does not providean independent basis to determine thatAIG’s management has maintainedappropriate internal controls and proce-dures,” states the audit-committeereport of the world’s most valuable insur-ance organization. “The committee’sconsiderations…do not assure that theaudit of AIG’s financial statements hasbeen carried out in accordance with gen-erally accepted auditing standards…orthat AIG’s auditors are in fact indepen-dent.”

If the audit-committee of the compa-ny that believes that the greatest risk isnot taking one can’t state that AIG’sfinancial statements conform withGAAP, then who needs the audit com-mittee? If the audit-committee can’tdetermine whether or not AIG’s auditorsare “independent,” then the members of

SCHIFF’S

SCHIFF’S INSURANCE OBSERVER • 300 CENTRAL PARK WEST, NEW YORK, NY 10024 • (212) 724-2000 • DAV I D@IN S U R A N C EOB S E RV E R.C O M

August 16, 2002Volume 14 • Number 11 I N S U R A N C E O B S E R V E R

The world’s most dangerous insurance publicationSM

AIG to Change Audit-Committee ReportDon’t Look Back

“Your mother is responsible for your fear of Generally Accepted Accounting Principles.”

2 AUGUST 16, 2002 SCHIFF’S INSURANCE OBSERVER ~ (212) 724-2000

the audit committee should be replacedby people who can make such a determi-nation.

That AIG, which is worth approxi-mately $175 billion, will change its audit-committee report is a testament to thechanging times. If the stock-marketboom at the end of the last millenniumqualified as a “new era,” then thepresent climate of skepticism andcorporate accountability is anothernew era. (The future, of course, iscomprised of nothing but “neweras.” They come and go all thetime.)

After our May 2 article, wereceived complaints from some sub-scribers, including securities analystswho were recommending AIG’sstock. (According to First Call, 22 of23 analysts covering AIG rate it a“buy.”) Schiff’s was destroying publicconfidence, we were told, by writingabout AIG’s audit-committee report,especially during a time when themarket was so volatile. We were alsotold that the audit committee is onlyan overseer: it hires the accountantsbut doesn’t really have access to finan-cial information.