Embed Size (px)

DESCRIPTION

Schemes and Programmes Central Bank Nigeria ENG

Citation preview

Central Bank of Nigeria

BRIEFS ON SCHEMES AND PROGRAMMES

OF

THE DEVELOPMENT FINANCE DEPARTMENT OF THE CENTRAL

BANK OF NIGERIA

Central Bank of Nigeria

Introduction� The CBN’s involvement in development financing dates back to the early sixties. The Bank collaborates with the government, development partners, companies and other private institutions to: � Improve banks’ lending to the real sector;

� Empower small scale entrepreneurs;

� Create employment opportunities;

� Alleviate poverty; and

� Ensure food security

� Responsibility for development financing activities of the CBN lies with the Development Finance Department.

Central Bank of Nigeria

Current Focus Of Development Finance Activities Of The CBN

� Agricultural financing

� Promotion of Small and medium Enterprises

�Micro finance

� Agricultural Credit Support Scheme (ACSS)

Central Bank of Nigeria

Schemes & Programmes of DFD� Agricultural Credit Guarantee Scheme (ACGS)

� Small and Medium Enterprises Equity Investment Scheme (SMEEIS)

�Microfinance policy

Central Bank of Nigeria

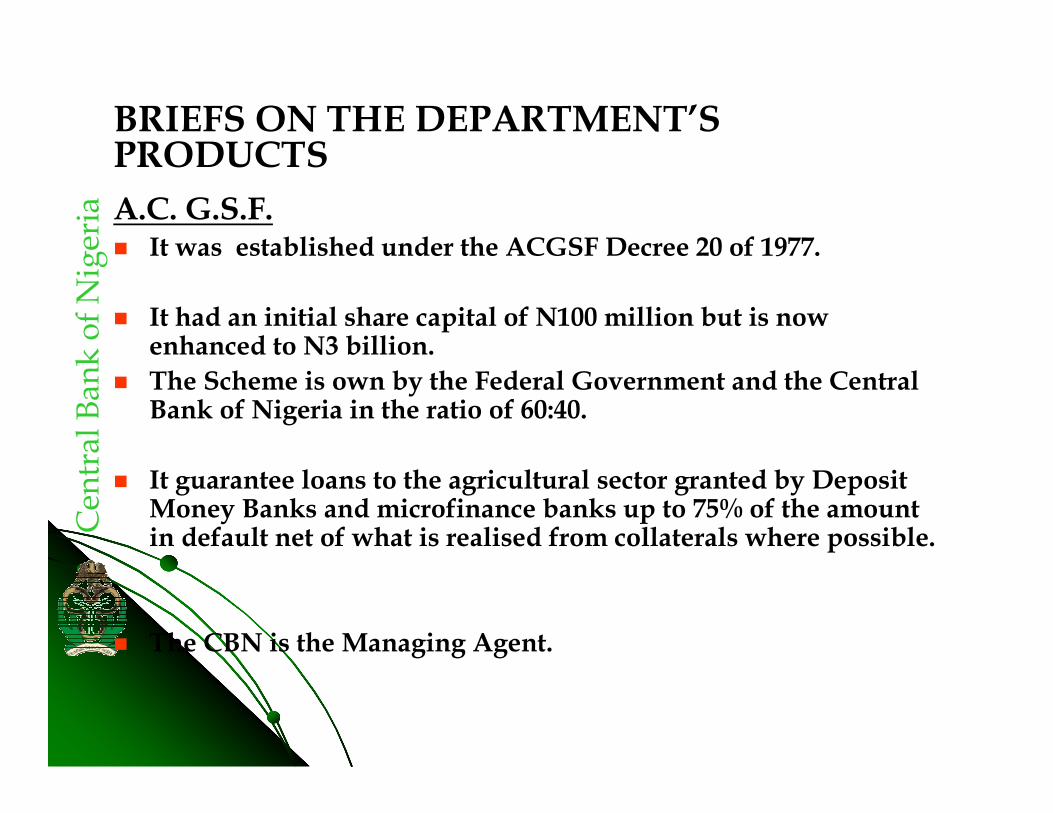

BRIEFS ON THE DEPARTMENT’S PRODUCTS

A.C. G.S.F.� It was established under the ACGSF Decree 20 of 1977.

� It had an initial share capital of N100 million but is now enhanced to N3 billion.

� The Scheme is own by the Federal Government and the Central Bank of Nigeria in the ratio of 60:40.

� It guarantee loans to the agricultural sector granted by DepositMoney Banks and microfinance banks up to 75% of the amount in default net of what is realised from collaterals where possible.

� The CBN is the Managing Agent.

Central Bank of Nigeria

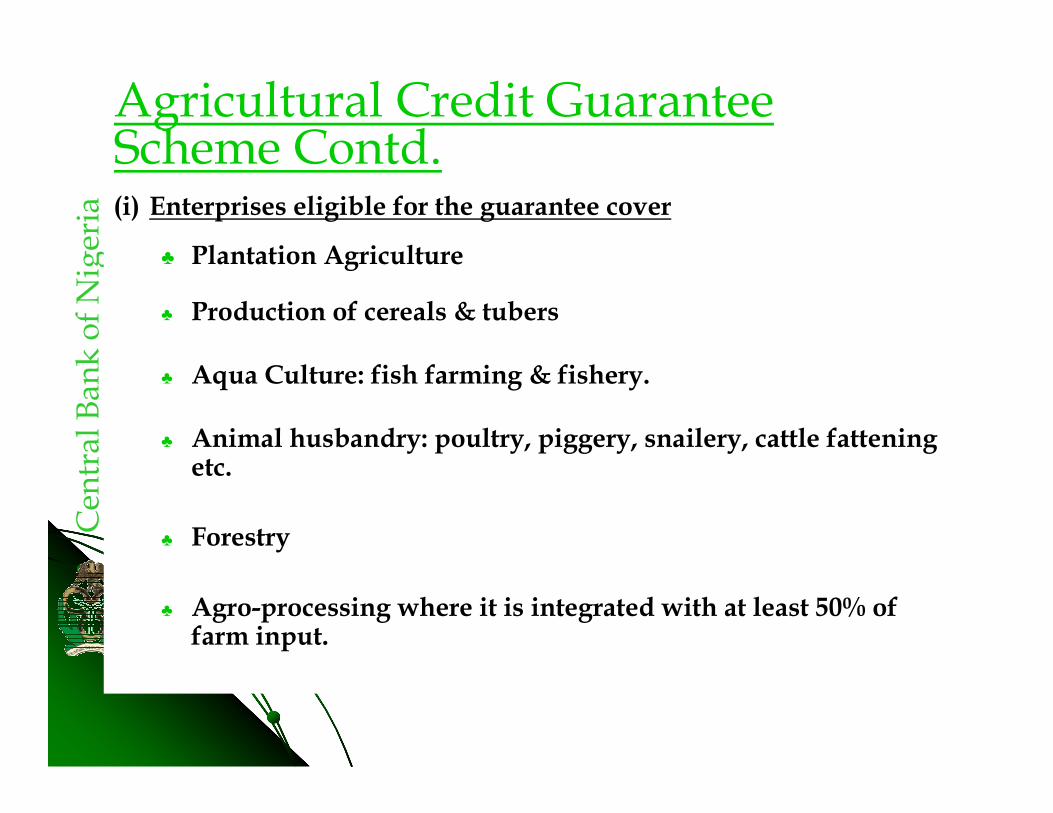

Agricultural Credit Guarantee Scheme Contd.(i) Enterprises eligible for the guarantee cover

♣ Plantation Agriculture

♣ Production of cereals & tubers

♣ Aqua Culture: fish farming & fishery.

♣ Animal husbandry: poultry, piggery, snailery, cattle fattening etc.

♣ Forestry

♣ Agro-processing where it is integrated with at least 50% of farm input.

Central Bank of Nigeria

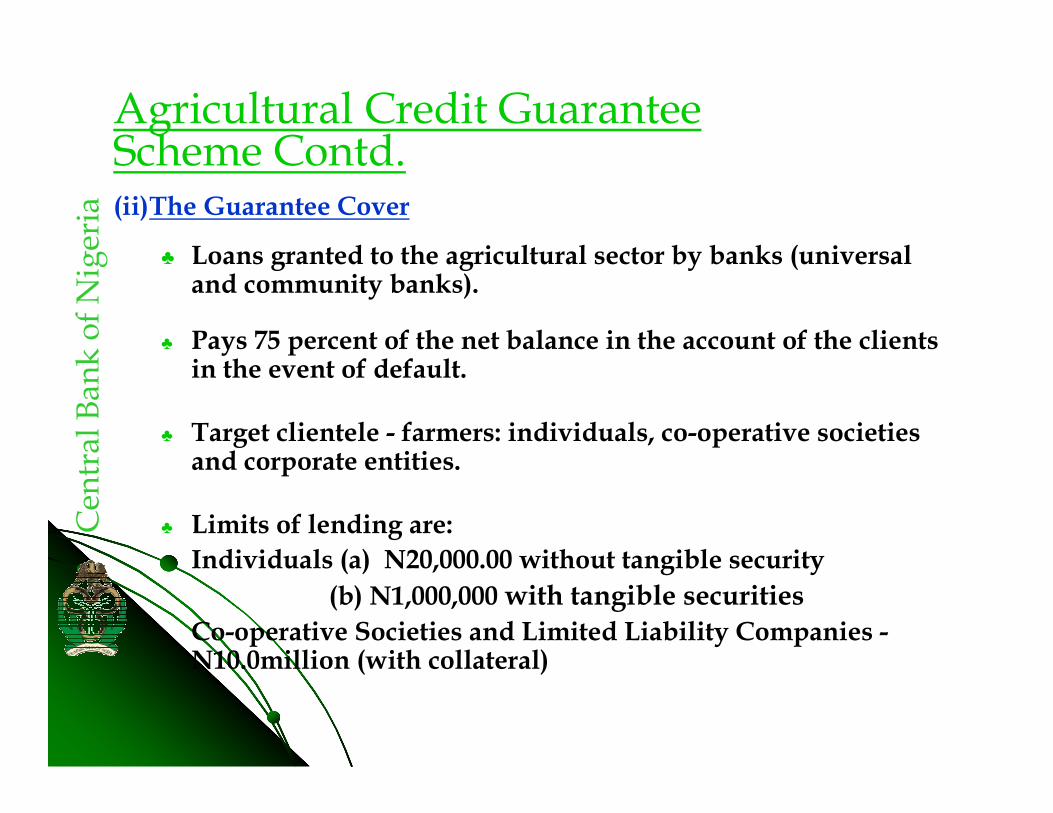

Agricultural Credit Guarantee Scheme Contd.(ii)The Guarantee Cover

♣ Loans granted to the agricultural sector by banks (universal and community banks).

♣ Pays 75 percent of the net balance in the account of the clientsin the event of default.

♣ Target clientele - farmers: individuals, co-operative societies and corporate entities.

♣ Limits of lending are:

Individuals (a) N20,000.00 without tangible security

(b) N1,000,000 with tangible securities

Co-operative Societies and Limited Liability Companies -N10.0million (with collateral)

Central Bank of Nigeria

BREIFS ON THE DEPARTMENT’S PRODUCTS

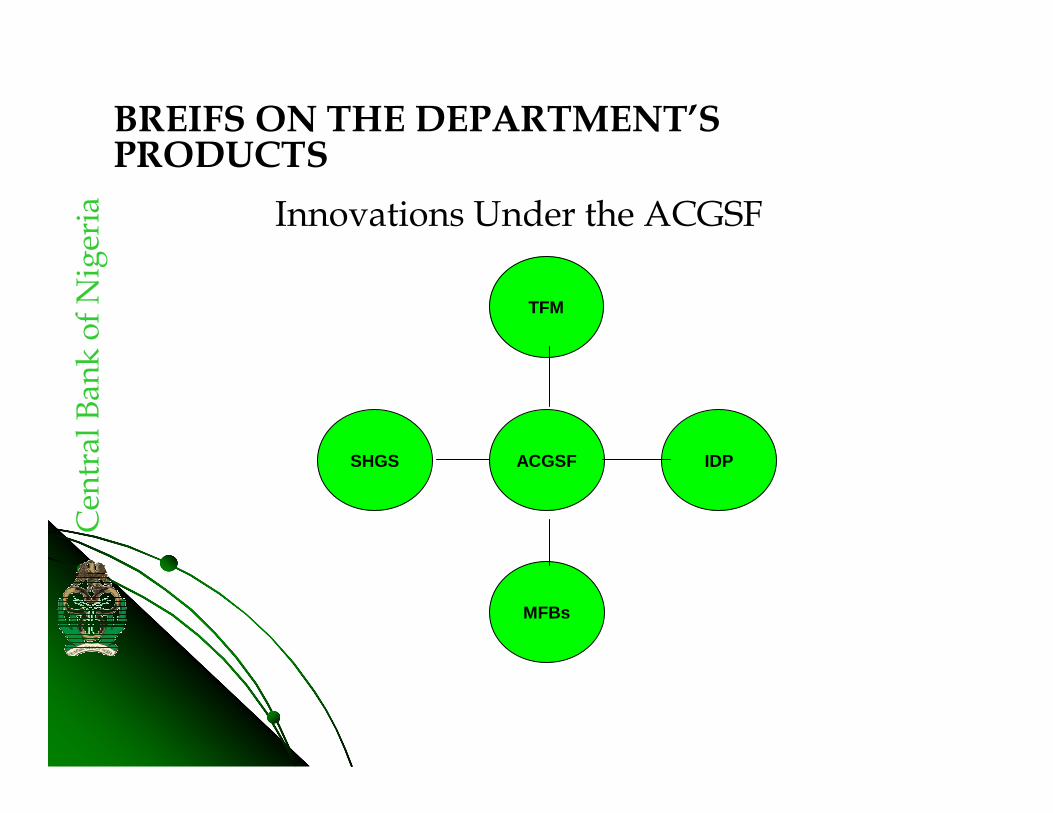

Innovations Under the ACGSF

TFM

IDP

MFBs

SHGS ACGSF

Central Bank of Nigeria

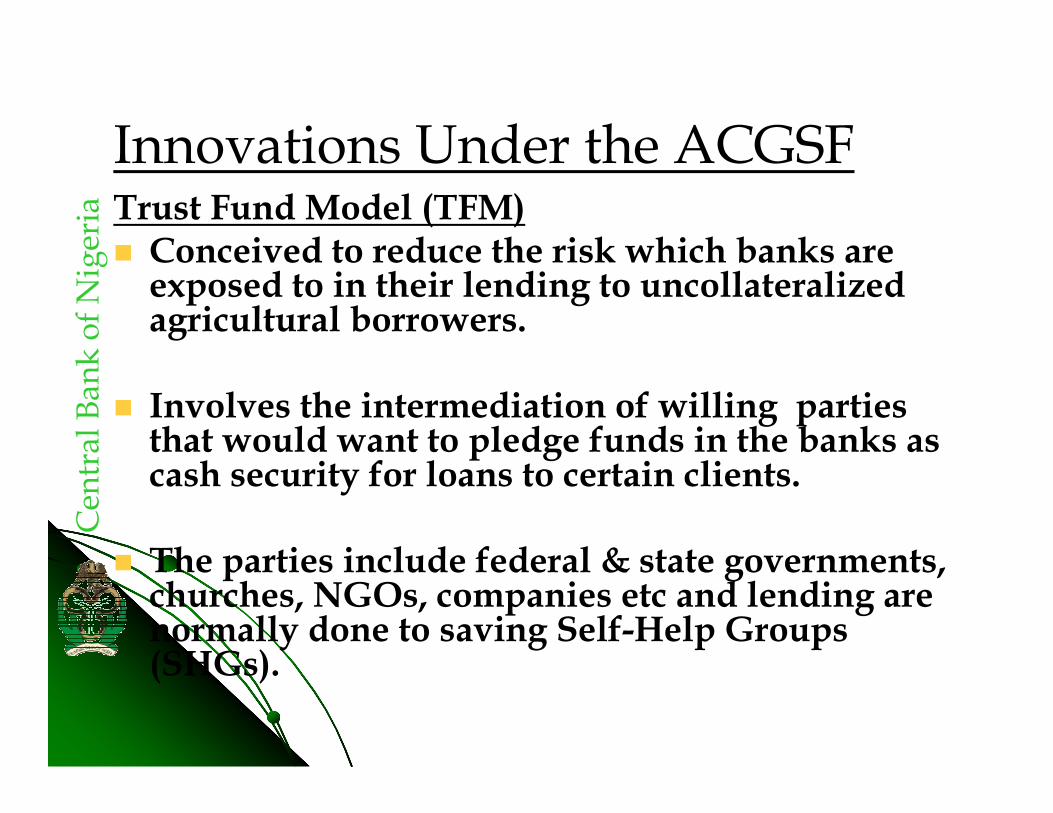

Innovations Under the ACGSFTrust Fund Model (TFM)� Conceived to reduce the risk which banks are exposed to in their lending to uncollateralized agricultural borrowers.

� Involves the intermediation of willing parties that would want to pledge funds in the banks as cash security for loans to certain clients.

� The parties include federal & state governments, churches, NGOs, companies etc and lending are normally done to saving Self-Help Groups (SHGs).

Central Bank of Nigeria

Trust Fund Model (TFM) Cont’dModalities of the TFM.� Provision of evidence that the state government/any other organization

have deposited 25 percent of the proposed client loan exposure in the intermediary bank and that the prospective clients have been formed into non-politicized small holder groups, linked to the bank and saved additional 25 percent of the intended loan amount.

� Application for loan to the intermediary bank by the groups.

� Inspection of the projects, approval of the loan (usually two times the sum of the government deposit and farmers savings) and application to the ACGSF for guarantee.

� Guarantees of 75% of the 50 percent unsecured part of the loan package by the ACGSF.

� Disbursement of loan to farmers

Central Bank of Nigeria

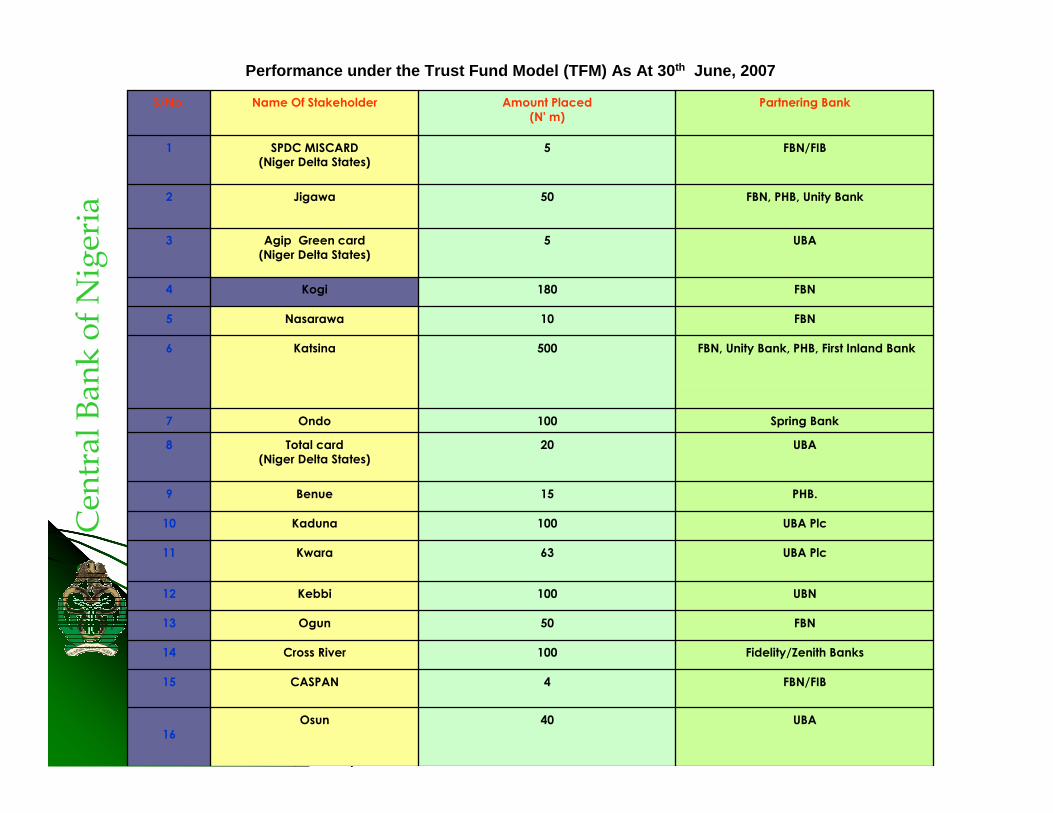

Fidelity/Zenith Banks100Cross River14

FBN/FIB4CASPAN15

UBA40Osun

16

FBN50Ogun13

UBN100Kebbi12

UBA Plc63Kwara11

UBA Plc100Kaduna 10

PHB.15Benue 9

UBA20Total card

(Niger Delta States)

8

Spring Bank100Ondo7

FBN, Unity Bank, PHB, First Inland Bank500Katsina6

FBN10Nasarawa5

FBN180Kogi4

UBA5Agip Green card

(Niger Delta States)

3

FBN, PHB, Unity Bank50Jigawa2

FBN/FIB5SPDC MISCARD(Niger Delta States)

1

Partnering BankAmount Placed

(N' m)

Name Of StakeholderS/No.

Performance under the Trust Fund Model (TFM) As At 30th June, 2007

Central Bank of Nigeria

Innovations Under the ACGSF (Cont’d)Interest Drawback Programme (IDP)

� Introduced with effect from 2003 lending season.

� Capital of N2.0 billion, separate from the ACGSF.

� Funded jointly by the Federal Government of Nigeria and the Central Bank of Nigeria in 60:40 shareholding ratio.

� Assist borrowers under the ACGSF reduce their effective borrowing rates.

� Farmers borrow from lending banks at market-determined rates but are given interest rebate of 40% if they repay their loans as and at when due.

Central Bank of Nigeria

BREIFS ON THE DEPARTMENT’S PRODUCTS (Cont’d)S.M.E.E.I.S.

� Initiated by the Bankers’ Committee in 2001.

� In it, banks set aside 10% of their profit after tax (PAT) for equity investment in projects (except commerce & trading).

� Definition of SME: For the purpose of the scheme, a Small & Medium Enterprise is defined as any business activity with a maximum asset base of N1.5billion excluding land and working capital; and employing any number of staff.

� The Scheme has created a window for small and micro enterprises by setting aside 10% of the 10% for them to access.

Central Bank of Nigeria

BREIFS ON THE DEPARTMENT’S PRODUCTS (Cont’d)

� Objectives of the Scheme: To stimulate economic growth, develop local resources/technologies and generate employment through the facilitation of the flow of funds for the establishment of new SME projects, reactivation of moribund ventures, expansion and modernization of on-going projects.

� Activities Covered: Agric. agro-allied enterprises, information technology/ telecommunication, manufacturing, educational establishments, services and service-related, tourism and leisure, solid minerals exploration and exploitations, construction, etc. Except commerce

� Guidelines have been reviewed to the effect that 10 percent of the SMEEIS Funds would be apportioned to micro entrepreneurs.

Central Bank of Nigeria

BREIFS ON THE DEPARTMENT’S PRODUCTS (Cont’d)

Microfinance Policy

� The Bank launched ‘’the Microfinance Policy, Regulatory and Supervisory Framework for Nigeria’’ on the 15th of December, 2005.

� Presently the Department has the mandate to monitor and ensure full implementation of the policy framework.

Central Bank of Nigeria

The Microfinance Policy

� Main objectives:

� To make financial services accessible to a large segment of the potentially productive Nigerian population which otherwise wouldhave little or no access to financial services;

� Promote synergy and mainstreaming of the informal sub-sector into the national financial system;

� Enhance service delivery by microfinance institutions to micro, small and medium entrepreneurs;

� Contribute to rural transformation; and

� Promote linkage programs between universal/development banks, specialized institutions and microfinance banks.

Central Bank of Nigeria

FRAMEWORK FOR MICROFINANCE BANKS

Provides for the setting up of private sector driven microfinance

banks to provide financial services for poor and low income

groups

Two categories of MFBs are recognized:

1. MFBS licensed to operate as a unit bank with a minimum capital requirement of N20 million; and

2. MFBs licensed to operate in a state with a minimum capital requirement of N1 billion.

- the two categories can aspire to have national coverage provided they grow organically.

Central Bank of Nigeria

CONCLUSION� The Development Finance Department is actively promoting development financing in Nigeria.

� It has been achieving this objective through the management of ACGSF, implementation of SMEEIS and the design of complementary products that enhance sustainability.

� It looks to the future with optimism for enhance performance.

Central Bank of Nigeria

THANK YOU

FOR LISTENING