Embed Size (px)

DESCRIPTION

SC Agent & Broker mag, Fall 2012

Citation preview

Ocean Marine

2

Serving The TransportationIndustry Since 1946

800.432.7715

www.RPSins.comEDWIN M. ROLLINS COMPANY

We specialize in writing all types, sizes and classes of transportation

Speed to market is vital in today’s world. Our “In-house” underwriting and pricing authority through A rated carriers allows us to offer immediate quotes and binders. Whatever road your client is on ... we have you covered.

Call Us Today!

QQ Business AutoQQ ContractorsQQ Courier ServicesQQ Church VansQQ Day Care Vans

QQ Dump TrucksQQ Fleets QQ HotshotsQQ LimousinesQQ Logging

QQ Owner OperatorsQQ Social ServicesQQ Truckers (Local / Intermediate / Long Haul)

QQ Wreckers

A Subsidiary of Risk Placement Services, Inc.

RPS Rollins - Big I Virginia 7-2012.indd 1 6/15/2012 2:16:36 PM

Fall 2012 • South Carolina Agent & Broker 3

South Carolina Agent & Broker is the official magazine of the Independent Insurance Agents and Brokers of South Carolina and is published four times annually. IIABSC does not necessarily endorse any of the companies advertising in this publication or the views of its writers.

Articles and information published in this magazine may not be reproduced without written consent of the IIABSC. South Caroli-na Agent & Broker is not responsible for unsolicited manuscripts, art or photography. The publisher cannot assume responsibility for claims made by advertisers and is not responsible for the opinions expressed by contributing authors.

For more information on advertising,Contact Jim Aitkins

Blue Water Publishers22727 - 161st Avenue SE

Monroe, WA 98272360-805-6474 fax: [email protected]

IIABSC Staff

G. Frank Sheppard, AAI, CAEPresidentext. 23, [email protected]

Rebecca H. McCormack, CPCU, CIC, AAI,CPIWVice Presidentext. 14, [email protected]

Anita J. TrevinoDirector of Communicationsext. 29, [email protected]

Beth ChastieDirector of Administration & Financeext. 17, [email protected]

Laura CornellDirector of Insurance Programsext. 22, [email protected]

Megan HuebnerMeetings & Membership Coordinatorext. 16, [email protected]

Mary A. EllisProfessional Development Administratorext. 12, [email protected]

Jeanette BlossEducation Coordinatorext. 11, [email protected]

Pat FetnerReceptionistext. 10, [email protected]

Lee RuefDirector of State Government [email protected]

Independent Insurance Agents & Brokers of South Carolina

PO Box 210008, Columbia, SC 29221800 Gracern Road, Columbia, SC 29210

803-731-9460 803-772-6425 (fax)e-mail: [email protected]

Advertiser Index

Message from the Chairman of the Board 6

Message from the National Director 8

SC Big “I” Member Elected SC Senate President Pro Tempore 10

2012 Big “I” SC Education Awards Luncheon 14

2012 Outstanding CSR of the Year - Kelly Frontroth, API, AAI, CPIW 16

2012 Young Agents Conference Photo Recap 18

ACT: Agency Strategies to Send and Receive Personal Data Securely 22

ACT: A Millennial’s Take on Social Media 25

Don’t Let Texting Create an E&O Wreck 28

New Residential Numbering Program Launches Thanks to $5000 Grant 30

“Choppers for Charity” Results in $150K Donation to Make-A-Wish 32

Regional Trusted Choice Contacts 33

Palmetto Partners Program 34

IIABSC Member News 35

IIABSC Education & Events Calendar 36

2012 Board of Directors and Executive Committee 38

Allstar Financial 38Assure Alliance 11Astonish Results 7Bankers Insurance Group 24Builders Mutual Insurance 35Burns & Wilcox 5FCCI Insurance Group 37Genesee General 26GUARD Insurance Group 37JM Wilson 31Jackson Sumner & Associates 2Johnson & Johnson 20, 21

M. J. Kelly of South Carolina 36Montgomery Insurance 29NetComp 11Preferred Specialty 39Prime Rate Premium Finance 17RPS Rollins 3Summit Marketing Services 29TAPCO Underwriters 31The National Security Group 27UPC Insurance 40Universal North America 15Utica National Insurance Group 9

FALL 2012

Contents

4 South Carolina Agent & Broker • Fall 2012

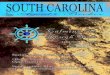

Cover Image: ©Sam Holland Photography. Senator John Courson smiles at the remarks of his colleagues during the hearing where he was elected President Pro Tempore of the Senate. Sen. Courson is also Senior Vice President at member agency Keenan & Suggs Insurance, Risk Management and Employee Benefits in Columbia.

PROFESSIONAL LIABILITYCOVERAGE IS IN THE DETAILS

&

&

31332_Burns_NC1,NC2,NC3,SC1_sc-A&B, Data Privacy_APPROVED.indd 1 8/15/12 4:04 PM

Fall 2012 • South Carolina Agent & Broker 5

T

IIABSC Chairman of the BoardAshley Brady, CIC

6 South Carolina Agent & Broker • Fall 2012

he leaves changing means the year is winding down, and as I prepare to attend our annual convention in Savannah to accept the opportunity to serve as chairman for another year I can’t help but wonder what happened to this one!

Change happens all the time and not just with the seasons, but it really seems like its pace has really picked up the past couple of years. We all must learn how to adapt to the pace of change more quickly and efficiently. It is important not only in how we run our agencies, but how we respond to our customers.

Your association has been working hard on your behalf all year long. One, on a national level we started the first phase of the much anticipated Consumer Agent Portal (CAP) project, which made available supplemental tools for evolving your agency’s website into a massive, multi-tiered and integrated platform to reach and relate to today’s internet personal-lines consumer. Your state association supplemented the investments of member agencies that made the jump to be early adopters of those tools. Next year we look forward to the launch of the consumer-facing portal that will include comparative rating for multiple carriers, agency directories and other consumer resources. It will be available only to Big “I” member agencies.

Two, we built a diamond-award winning online education program this year with a special webcast system that includes live, full-motion video of the presenter with high-quality audio and coordinated presentation slides. It allows users to email questions to presenters in real time and email themselves notes they’ve made in the system during the broadcast. Topics include ethics, building codes, bonds, business auto, certificates of insurance, workers comp and even some L&H hours with estate planning, retirement planning and the top five life insurance uses. Next year we’re adding even more industry-relevant and engaging topics to meet your CE needs.

Three, and another area of which I am particularly proud is our continued promotion and support of Trusted Choice®, the brand for independent insurance agents. The consumer recognition and understanding of our brand continues to grow,

which drives customers and business to your agency. This year was our first as a major sponsor for the SC Make-

A-Wish Foundation. Teaming up with such a well-known charitable organization is a great way to promote our brand while supporting a worthy cause. Through the partnership, local Trusted Choice® agency representatives make appearances at schools that have sponsored the wishes for children with life-threatening medical conditions. During the presentation ceremonies, they announce a contribution to their collective efforts, oftentimes matching dollar-for-dollar. This surprise is intended to boost the intrinsic rewards of community service and working together in the hopes of inspiring our state’s future leaders. We expect this partnership to grow in 2013.

And finally, with all this talk of change and growth, no matter how our business world evolves, our association will always have a hand in advocacy with our state regulators and encouraging our members’ involvement in the political process both locally and nationally. As heavily regulated as our industry is, we just can’t afford not to.

In 2012 there was a lot of publicity, especially in Charleston, about property insurance rates. We kept a close watch on the situation and are anticipating some legislative discussions in January. As always we will work diligently with companies and the DOI to maintain the competitive environment that has helped add numerous insurance companies in South Carolina for the past few years.

Please, let us know what issues are important to you. Contact your association President Frank Sheppard by calling 803.731.9460 or emailing [email protected] or emailing me, your association Chairman of the Board, at [email protected].

Challenges will continue, opportunities will arise, and that is why we have our association. I look forward to leading you through another year of overcoming those challenges and seeking new opportunities. Happy Holidays to you and yours.

7

have two major updates from your national association, and while on the surface they may seem unrelated, they are two great examples of some of the most important benefits provided to you with your membership to the state and national Big “I.”

Important benefit No. 1: Advocacy. Even those who actively avoid politics (as big of a mistake as that is) have not been able to completely shut it out this election season. In my last column, I told you about the national convention and legislative conference held each spring along with a brief update on current national legislative issues. There has been progress on one of those issues, the NFIP finally has a long-term extension; it won’t expire until September 2017. Several issues are being held until after the election, but one important issue to our industry is charging ahead and looks like it will continue to be a major national issue in 2013.

On Sept. 11, I testified before Congress during the first House Subcommittee hearing on the Terrorism Risk Insurance Program since its reauthorization in 2007. The Terrorism Risk Insurance Act (TRIA) was enacted by Congress in response to severe disruptions in the entire insurance market in the wake of the Sept. 11 attacks. It was designed as a government reinsurance program for commercial property and casualty insurers in the form of a federal backstop.

The initial law authorizing the program was passed in November 2002 and was reauthorized in 2005 and 2007. The reauthorizations included many additional private market cost sharing measures such as a program trigger, deductibles, copays and recoupment mechanisms.

TRIA expires Dec. 31, 2014. The hearing made clear that passing another reauthorization of TRIA in its current form is expected to be a “heavy lift,” which is why the Insurance, Housing and Community Opportunity subcommittee has started seemingly early.

On the 11th anniversary of the Sept. 11 attacks in New York and attempts in Washington, D.C., I testified that TRIP has done its job so far to preserve and stabilize a viable market for terrorism insurance, and that continuing that stability and maintaining this limited public-private partnership is vitally important. I reminded Committee Members of the severe disruption that the Sept. 11 attacks caused in the marketplace and how difficult it became for businesses to secure adequate coverage and its effect on industries outside of insurance. I reminded them that TRIA has operated at

virtually no cost to taxpayers, and what level losses would have to occur before any federal dollars are spent. I also reminded them that the private sector still lacks the ability and capacity to assess risk and perform proper underwriting as we do not have access to much of the information that is kept internal to federal agencies for security and law enforcement reasons. We cannot fill the void that would be created were TRIP to cease operations.

Our national association expects the TRIA extension to be a major issue in 2013. More updates to come as they develop.

Important benefit No. 2: Collective Branding. Trusted Choice® is the national marketing brand of independent insurance agents, developed almost ten years ago in response to extensive research in order to help agents capture a greater share of the consumer market. The name itself highlights the benefits of working with an independent agent, who is a “trusted” advisor that offers consumers a “choice” of products and services. Ten years later and consumer research still reflects these two aspects are incredibly important to consumers looking for insurance.

This summer, our national brand launched a social-media campaign that encouraged members and consumers to “share” content from its Facebook page (www.facebook.com/trustedchoice) and promised to contribute $10 to the well-known charitable organization Make-A-Wish each time someone did. While much of the content shared came straight from the Trusted Choice® consumer website (www.trustedchoice.com), in order to boost the “fun” content required for a successful social media experience our brand also commissioned a custom motorcycle built by the stars of the incredibly popular Discovery Channel reality show American Choppers. Make-A-Wish happened to be cause dear to the heart of one of its stars, and they were pleased for the opportunity to help bring in the $150,000 that ended up being contributed when it was all over.

The now-dubbed Chopper for Charity is on tour throughout the nation, stopping at our annual convention in Savannah, and afterwards will provide at least one more fundraising opportunity for Make-A-Wish, possibly next summer. See photos of the chopper on page 32 or on the Trusted Choice® Facebook webpage (www.facebook.com/trustedchoice).

INational Director

Jon A. Jensen, AAI, AIP

8 South Carolina Agent & Broker • Fall 2012

Fall 2012 • South Carolina Agent & Broker 9

Let’s face it. As an independent agent, you’re looking for a company that’s in it for the long haul, not a “here-today-and-on-to-something-else-tomorrow” carrier. We’ve been writing through the independent agency system almost back to our founding in 1914. We consider the agent a customer of our company.

We’ve got a tremendous selection of “niche” commercial lines products, and we’re a great market for general commercial business as well. Along with custom coverages, your clients get specialized risk management services to help preserve life and property and keep insurance affordable, along with claims service that’s fast, fair and friendly from claims people who know these classes of business.

We offer our agent-customers competitive commissions and a great contingency commission program as well – all with the goal of helping you build sales and build revenue.

Carve your niche – Get to Know Utica! Call me today to find out what Utica can add to your agency!

...WITH PRODUCTS AND SERVICETHAT WILL STAND THE TEST OF TIME.

Matt Lupino — Resident Senior Vice President Utica National Insurance Group

1100 Boulders Parkway, Suite 300, Richmond, VA 23225 Phone: 804-560-6620 • [email protected]

10 South Carolina Agent & Broker • Fall 2012

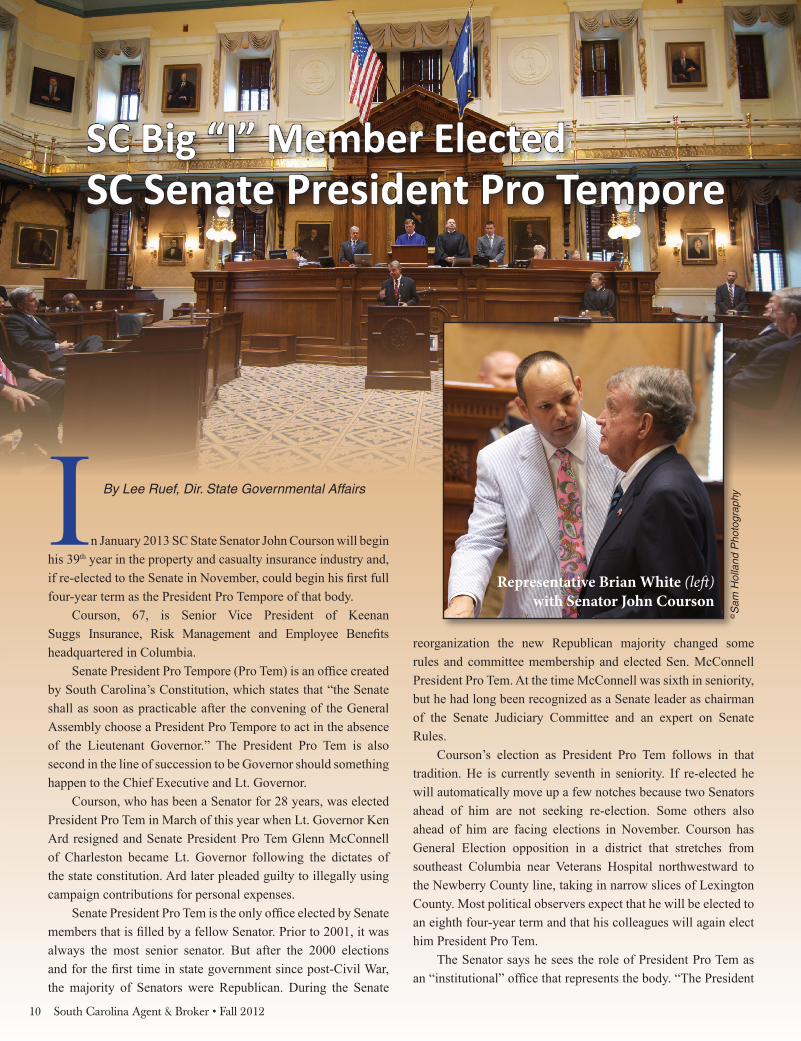

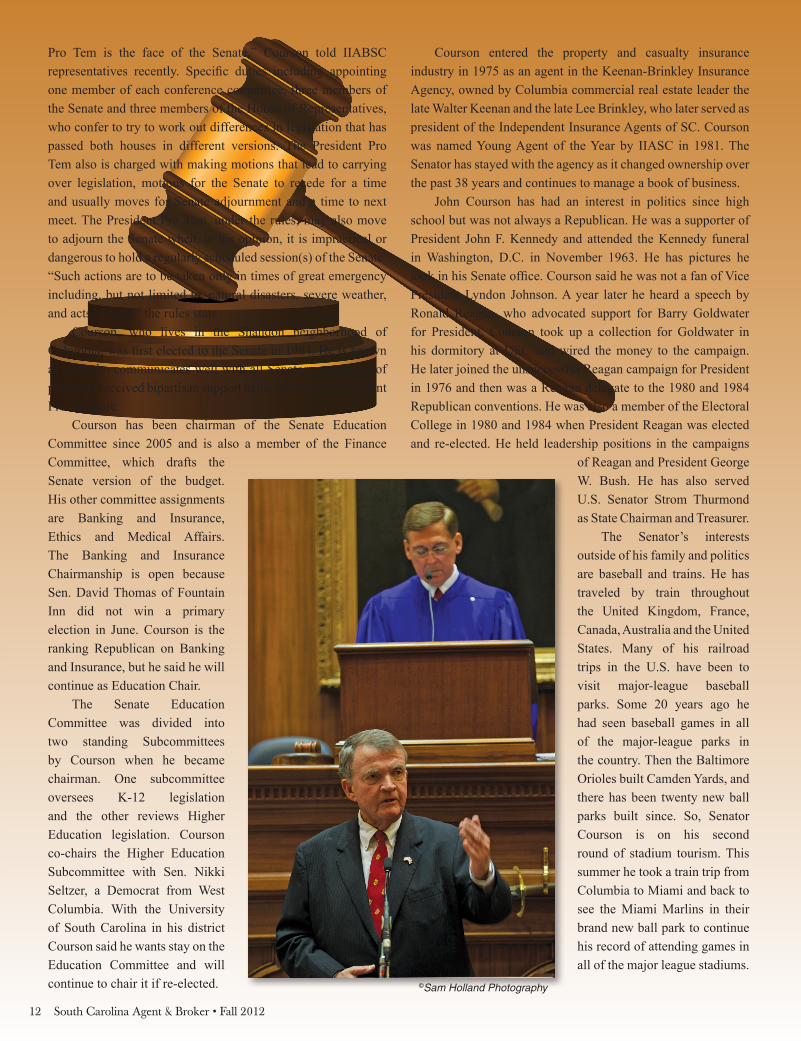

n January 2013 SC State Senator John Courson will begin his 39th year in the property and casualty insurance industry and, if re-elected to the Senate in November, could begin his first full four-year term as the President Pro Tempore of that body.

Courson, 67, is Senior Vice President of Keenan Suggs Insurance, Risk Management and Employee Benefits headquartered in Columbia.

Senate President Pro Tempore (Pro Tem) is an office created by South Carolina’s Constitution, which states that “the Senate shall as soon as practicable after the convening of the General Assembly choose a President Pro Tempore to act in the absence of the Lieutenant Governor.” The President Pro Tem is also second in the line of succession to be Governor should something happen to the Chief Executive and Lt. Governor.

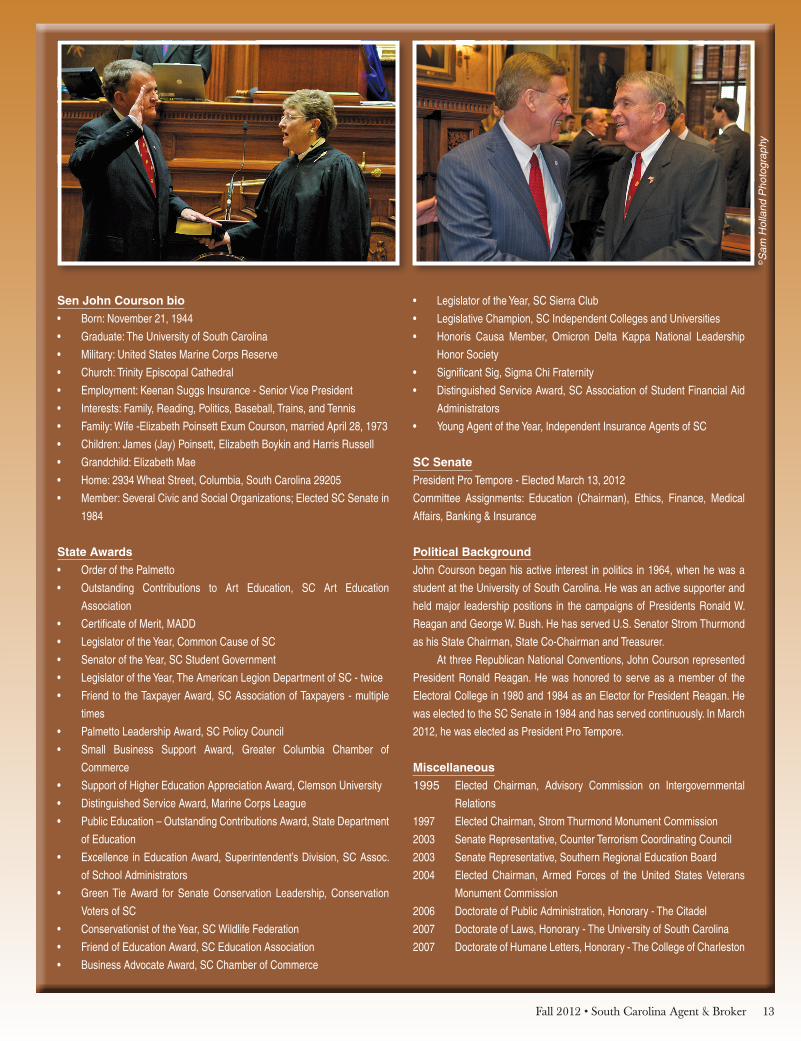

Courson, who has been a Senator for 28 years, was elected President Pro Tem in March of this year when Lt. Governor Ken Ard resigned and Senate President Pro Tem Glenn McConnell of Charleston became Lt. Governor following the dictates of the state constitution. Ard later pleaded guilty to illegally using campaign contributions for personal expenses.

Senate President Pro Tem is the only office elected by Senate members that is filled by a fellow Senator. Prior to 2001, it was always the most senior senator. But after the 2000 elections and for the first time in state government since post-Civil War, the majority of Senators were Republican. During the Senate

reorganization the new Republican majority changed some rules and committee membership and elected Sen. McConnell President Pro Tem. At the time McConnell was sixth in seniority, but he had long been recognized as a Senate leader as chairman of the Senate Judiciary Committee and an expert on Senate Rules.

Courson’s election as President Pro Tem follows in that tradition. He is currently seventh in seniority. If re-elected he will automatically move up a few notches because two Senators ahead of him are not seeking re-election. Some others also ahead of him are facing elections in November. Courson has General Election opposition in a district that stretches from southeast Columbia near Veterans Hospital northwestward to the Newberry County line, taking in narrow slices of Lexington County. Most political observers expect that he will be elected to an eighth four-year term and that his colleagues will again elect him President Pro Tem.

The Senator says he sees the role of President Pro Tem as an “institutional” office that represents the body. “The President

SC Big “I” Member ElectedSC Senate President Pro Tempore

By Lee Ruef, Dir. State Governmental AffairsIRepresentative Brian White (left)

with Senator John Courson

©S

am H

olla

nd P

hoto

grap

hy

Fall 2012 • South Carolina Agent & Broker 11

*Insurance Journal’s “Top 100 of 2011”

www.assurealliance.com

1-864-541-0168

12 South Carolina Agent & Broker • Fall 2012

Pro Tem is the face of the Senate,” Courson told IIABSC representatives recently. Specific duties including appointing one member of each conference committee, three members of the Senate and three members of the House of Representatives, who confer to try to work out differences in legislation that has passed both houses in different versions. The President Pro Tem also is charged with making motions that lead to carrying over legislation, motions for the Senate to recede for a time and usually moves for Senate adjournment and a time to next meet. The President Pro Tem, under the rules, may also move to adjourn the Senate when, in his opinion, it is impractical or dangerous to hold a regularly scheduled session(s) of the Senate. “Such actions are to be taken only in times of great emergency including, but not limited to, natural disasters, severe weather, and acts of God,” the rules state.

Courson, who lives in the Shandon neighborhood of Columbia, was first elected to the Senate in 1984. He is known as one who communicates well with all Senators regardless of party and received bipartisan support in his election for President Pro Tempore.

Courson has been chairman of the Senate Education Committee since 2005 and is also a member of the Finance Committee, which drafts the Senate version of the budget. His other committee assignments are Banking and Insurance, Ethics and Medical Affairs. The Banking and Insurance Chairmanship is open because Sen. David Thomas of Fountain Inn did not win a primary election in June. Courson is the ranking Republican on Banking and Insurance, but he said he will continue as Education Chair.

The Senate Education Committee was divided into two standing Subcommittees by Courson when he became chairman. One subcommittee oversees K-12 legislation and the other reviews Higher Education legislation. Courson co-chairs the Higher Education Subcommittee with Sen. Nikki Seltzer, a Democrat from West Columbia. With the University of South Carolina in his district Courson said he wants stay on the Education Committee and will continue to chair it if re-elected.

Courson entered the property and casualty insurance industry in 1975 as an agent in the Keenan-Brinkley Insurance Agency, owned by Columbia commercial real estate leader the late Walter Keenan and the late Lee Brinkley, who later served as president of the Independent Insurance Agents of SC. Courson was named Young Agent of the Year by IIASC in 1981. The Senator has stayed with the agency as it changed ownership over the past 38 years and continues to manage a book of business.

John Courson has had an interest in politics since high school but was not always a Republican. He was a supporter of President John F. Kennedy and attended the Kennedy funeral in Washington, D.C. in November 1963. He has pictures he took in his Senate office. Courson said he was not a fan of Vice President Lyndon Johnson. A year later he heard a speech by Ronald Reagan, who advocated support for Barry Goldwater for President. Courson took up a collection for Goldwater in his dormitory at USC and wired the money to the campaign. He later joined the unsuccessful Reagan campaign for President in 1976 and then was a Reagan delegate to the 1980 and 1984 Republican conventions. He was also a member of the Electoral College in 1980 and 1984 when President Reagan was elected and re-elected. He held leadership positions in the campaigns

of Reagan and President George W. Bush. He has also served U.S. Senator Strom Thurmond as State Chairman and Treasurer.

The Senator’s interests outside of his family and politics are baseball and trains. He has traveled by train throughout the United Kingdom, France, Canada, Australia and the United States. Many of his railroad trips in the U.S. have been to visit major-league baseball parks. Some 20 years ago he had seen baseball games in all of the major-league parks in the country. Then the Baltimore Orioles built Camden Yards, and there has been twenty new ball parks built since. So, Senator Courson is on his second round of stadium tourism. This summer he took a train trip from Columbia to Miami and back to see the Miami Marlins in their brand new ball park to continue his record of attending games in all of the major league stadiums.

©Sam Holland Photography

Fall 2012 • South Carolina Agent & Broker 13

Sen John Courson bio

• Born: November 21, 1944

• Graduate: The University of South Carolina

• Military: United States Marine Corps Reserve

• Church: Trinity Episcopal Cathedral

• Employment: Keenan Suggs Insurance - Senior Vice President

• Interests: Family, Reading, Politics, Baseball, Trains, and Tennis

• Family: Wife -Elizabeth Poinsett Exum Courson, married April 28, 1973

• Children: James (Jay) Poinsett, Elizabeth Boykin and Harris Russell

• Grandchild: Elizabeth Mae

• Home: 2934 Wheat Street, Columbia, South Carolina 29205

• Member: Several Civic and Social Organizations; Elected SC Senate in

1984

State Awards

• Order of the Palmetto

• Outstanding Contributions to Art Education, SC Art Education

Association

• Certificate of Merit, MADD

• Legislator of the Year, Common Cause of SC

• Senator of the Year, SC Student Government

• Legislator of the Year, The American Legion Department of SC - twice

• Friend to the Taxpayer Award, SC Association of Taxpayers - multiple

times

• Palmetto Leadership Award, SC Policy Council

• Small Business Support Award, Greater Columbia Chamber of

Commerce

• Support of Higher Education Appreciation Award, Clemson University

• Distinguished Service Award, Marine Corps League

• Public Education – Outstanding Contributions Award, State Department

of Education

• Excellence in Education Award, Superintendent’s Division, SC Assoc.

of School Administrators

• Green Tie Award for Senate Conservation Leadership, Conservation

Voters of SC

• Conservationist of the Year, SC Wildlife Federation

• Friend of Education Award, SC Education Association

• Business Advocate Award, SC Chamber of Commerce

• Legislator of the Year, SC Sierra Club

• Legislative Champion, SC Independent Colleges and Universities

• Honoris Causa Member, Omicron Delta Kappa National Leadership

Honor Society

• Significant Sig, Sigma Chi Fraternity

• Distinguished Service Award, SC Association of Student Financial Aid

Administrators

• Young Agent of the Year, Independent Insurance Agents of SC

SC Senate

President Pro Tempore - Elected March 13, 2012

Committee Assignments: Education (Chairman), Ethics, Finance, Medical

Affairs, Banking & Insurance

Political Background

John Courson began his active interest in politics in 1964, when he was a

student at the University of South Carolina. He was an active supporter and

held major leadership positions in the campaigns of Presidents Ronald W.

Reagan and George W. Bush. He has served U.S. Senator Strom Thurmond

as his State Chairman, State Co-Chairman and Treasurer.

At three Republican National Conventions, John Courson represented

President Ronald Reagan. He was honored to serve as a member of the

Electoral College in 1980 and 1984 as an Elector for President Reagan. He

was elected to the SC Senate in 1984 and has served continuously. In March

2012, he was elected as President Pro Tempore.

Miscellaneous

1995 Elected Chairman, Advisory Commission on Intergovernmental

Relations

1997 Elected Chairman, Strom Thurmond Monument Commission

2003 Senate Representative, Counter Terrorism Coordinating Council

2003 Senate Representative, Southern Regional Education Board

2004 Elected Chairman, Armed Forces of the United States Veterans

Monument Commission

2006 Doctorate of Public Administration, Honorary - The Citadel

2007 Doctorate of Laws, Honorary - The University of South Carolina

2007 Doctorate of Humane Letters, Honorary - The College of Charleston

©S

am H

olla

nd P

hoto

grap

hy

AAIChristine H. Baker, CISR, AAIAnn H. Givens, CIC, AAI, AIAM

AIAMChristine L. Allen, AIAMMichelle L. Banks, AAI, AIAMJanice M. Barr, AIAMCheryl F. Blevins, AIAMBarbara A. Bradham, AIP, CISR, AIAMCamille C. Buster, AIAMSusan C. Carter, ACSR, AIAMBarbara K. Causey, AAI, CISR, AIAMRobin Easterlin, AIAMJennifer S. Fisher, CISR, AIAMDonna Franklin, CIC, AAI, ACSR, AIAMAnn H. Givens, CIC, AAI, AIAMGail Graham, CISR, AAI, ACSR, AIAMHeather Hagadorn, AIAMCharlene S.Hartley, CPCU, CIC, AAI, AIAMKaren G. Hawkins, AIAMStacey Herndon, CISR, AIAMJulie A. Hollaway, AIAMHelen Howard, CISR, ACSR,AIAMAltonia L. Howell, CISR, CPIA, AIAM, CPIWJennifer Jastromski, AIAMPixie H. Melfi, CISR, AIAMPaula J. Moss, CISR, AIAMDeborah O’Kimosh, CISR, CRIS, AIAMTeri L. Robinson, CISR, AIAMDonna Michele Rye, CISR, AIAMWillard A. Silcox, III, AIAMMelissa Sills, API, AIAMSarah Smith, CISR, ACSR, AAI, AIAMJanice l. Starnes, CISR, ACSR, AIAMLisa M. Thompkins, AIAMSharon Warren, CISR, ACSR, AIAMElaena Whitman, CISR, AIAM

CICFrank S. Barksdale, Jr., CICPamela C. Bass, CIC, CISRSusan Miley Blackwood, CIC, AICKeisha J. Brooks, CIC, CISRTammy J. Brookshire, CIC, CISRHilary L. Brown, CIC, AIC, AIS, APILori L. Carrozza, CIC, CPIA,CLCS,CPIWCarrie L. Cox, CIC, CISRLevi D. Crawford, CIC, AAI

2012 Big “I” SC

August 21, Doubletree Hotel, Columbia, SCEducation Awards Luncheon

Timothy M. Faulhaber, Sr., CICSusan M. Finley, CICJennifer C. Gentry, CICKaren P. Gwinn, CICRobin E. Hawkins, CIC, CISRJulie S. Head, CIC, CISR, CPIA, CWCAH. Michael Herlong, III, CICDeborah J. Holbrook, CIC, CISREmily Renee Johnson, CIC, CISRChristine N. Kareis, CICBonnie N. Knox, CIC, CISRJamie I. Leach, CIC, AISJackie G. Marsh, CIC, CISRArmour Kyle Milner, III, CIC, AAIJill Nicholson-Houston, CICAmy M. Owings, CICJames Robert Peed, CIC, CPCULeigh Petty, CIC, CISRRaymond M. Scruggs, CICAlice R. Seel, CICJaime Lee Tatara, CIC, CPCU, AISJanna M. Taylor, CIC, CISRHattie M. Tracey, CIC, CISRPamela C. Williams, CIC

CISRCarol Beth Akins, CISRCharlotte Maxine Altman, CISRAmanda Baker, CISRKim D. Boggs, CISRPhyllis D. Brockington, CISR, LUTCFFrankie S. Burden, CISR, CPIWDianne W. Butler, CISR, ACSRMileidys Chappelear, CISR

Charles T. Cole, III, CISRCasey Marie Cummings, CISRLisa Marie Earnhardt, CISRGail K. Ferri, CISR, AAIJulianna V.C. Hassell, CISRStacey E. Herlong, CISRBarbara J. James, CISRSusan T. Jones, CISRKerri W. Kitchens, CISRElizabeth W. Laster, CISRSidney Thomas Layden, CISRBrandy Lynn Maxey, CISRKristi Anne Mize, CISRElliott H. Phillips, CISRMaria Gema Rains, CISRJennifer Marie Ridgill, CISRDonna Michele Rye, CISRCatherine Ann Schultz, CISRWendy J. Seguine, CISRLauren Jean Shangraw, CISRKaren S. Smith, CISRBrenda S. Snyder, CISR, AISDebbie C. Tompkins, CISRTina M. Torlina, CISRMatthew Thomas Trainor, CISRDara Hart Williams, CISR

CSRM/CRMJeffrey Blake Lindsey, CSRMJeffrey B. Barnard, CIC, CRMJames B. Carlton, CIC, CRM, CSPRichard Brooks Jones, CRM, CSRM, AAIMatthew Quinton, CIC, CRM

Congratulations to new designees:

14 South Carolina Agent & Broker • Fall 2012

Listen.

* Written through National Flood Insurance Program.

Universal North America Insurance Company’s Financial Strength Rating of A- (Excellent) has been reaffi rmed by A.M. Best. The company’s Outlook is Stable. Insurance products are issued and underwritten by one of Universal North America’s insurance companies: Universal North America Insurance Company or Universal Insurance Company of North America. Issuance of coverage is subject to underwriting review and approval. Products may not be available in all states. © 2012 Universal North America.

At Universal North America®�, you have our ear 24/7.

Caring, professional help is always standing by – delivering best-in-class

service to our agents and policyholders.

Available. Attentive. There when you need us. It’s one of the Universal

values we do business by.

(866) 338-4262 UniversalNorthAmerica.com

Insurance with values.

HomeownersFlood*

BUSINESSOWNERSHOME FLOOD

Fall 2012 • South Carolina Agent & Broker 15

16 South Carolina Agent & Broker • Fall 2012

he answer to clients who place emphasis on price is easy: offer competitive rates. But wait. What would I be asking my clients to give up? Insurance is a business, and by both business and regulatory standards companies must remain profitable and be able to fulfill their obligations to pay claims. So how can a company remain profitable, fulfill clients’ needs and help my agency to become more competitive?

The first action for a company to take is to make sure they find stability in the market. It negates the point of having competitive rates if those rates are developed just to get the customer in the door. Competitive rates must remain competitive. Clients understand rate increases, but they will not tolerate rate explosions.

A company must develop products with competitive pricing. After stability, this is the second-most important action a company can take in helping an agency become more competitive. Different clients have different needs. Times have definitely changed from “one product fits all.” There are clients who want to be covered for whatever may occur. Many personal lines companies have implemented an accident forgiveness or minor-violation forgiveness program. This coverage may be built in or added as an endorsement. The charge is made on the front end, and clients do not experience a large rate increase when an accident or violation occurs. Other clients are willing to retain more exposure for better premiums. Credits are a great way for premium to be reduced for a client

Kelly Frontroth, API, AAI, CPIW of Hutson Etherredge Companies in Aiken has been named the 2012 SC Outstanding Customer Service Representative of the Year. This award is the highest honor in our state for insurance customer service reps who have distinguished themselves through contributions to their industry and profession. She will be recognized at this year’s annual convention awards banquet.

Once nominated, Kelly was required to write an essay from the following prompt: Given the emphasis that many of your clients place on price, identify and explain four important actions your companies have taken, or could take, to help you and your agency become more competitive.

(Winning Essay)

Kelly Frontroth, API, AAI, CPIW2012 SC Outstanding CSR of the Year Award

T

Fall 2012 • South Carolina Agent & Broker 17

taking on more exposure. This is an advantage for the company and the client as it reduces both the company’s exposure and the client’s rates. Companies have implemented this action with a choice of higher deductibles. It is the job of the agent to know their clients’ needs and how to meet those needs. A company that has a variety of coverage and credits to offer can help the agent become more competitive in the product market.

Providing educational opportunities for the agent and the public is a third action that companies can take to help an agent become more competitive. Many clients look at the dollar amount of coverage shown on the declaration page, and it is all they see. Unfortunately many clients have not been educated on “perils.” The best way for a company to educate a client is through the agent. Companies need to develop programs to let agents know what is available for their clients, not just in the products and the pricing area, but also in loss-control programs, printed information and co-op advertising opportunities to name a few. The better educated a client becomes, the agent establishes a more competitive marketing position establishing that trusted-choice bond. Companies also need to open the door for an active interchange of information between the company representatives and agents. Agency panels or committees are the best way for this exchange of information to take place. This exchange educates the agent about the company and what projects are in development and positions the company is taking as well as

educating the company about the needs and desires of the agent and client.

Companies must have proper staffing to support the agent. This is the fourth action to give an agency a competitive position in the market place. Marketing representatives are a very vital link between the relationship between an agent and a company. Many times they are the eyes and ears of the company. Underwriters must also be knowledgeable and help an agent find the proper coverage and pricing for those unique customers. Without the ability to properly place the business, not only will the agent lose the business, it may also damage his reputation as an agent. Finally the company adjuster is the person to whom the client is most exposed at the time of a loss. The adjuster should be able to explain the pay out or denial of a client’s claim in a professional and courteous manner. Without proper staffing, any other action a company takes will not make an agent more competitive in the market place.

Even though the clients place emphasis on price, it is the job of the agent to have an open conversation with the client about all elements of the insurance industry as a whole. The actions a company must take to make this agent more competitive are stability, product and pricing, educational opportunities and proper staffing. Without these actions and the proper support from the company, an agent could lose the competitive advantage in the marketplace.

Young Agents Conference

Aug. 2-5 Marriott Resort & SpaHilton Head

Walking the Tightrope

IIABSC

Sponsors:Access Insurance CompanyAFCO/Prime Rate Prem. Fin. Corp.American Strategic InsuranceAmTrust North AmericaAuto-Owners Insurance CompanyBankers Insurance GroupBerkley Mid-Atlantic Group, LLCBuilders Mutual Ins. CompanyBurns & Wilcox, Ltd.Capitol Preferred Ins.Capitol Special RisksCompanion Property & Casualty Insurance CompanyFirstCompFrontline Homeowners InsuranceGenesee General/ GSBGMACHanover Excess & Surplus, Inc.The HartfordIIABSC Agency, Inc.Insurance HouseJackson Sumner & AssociatesJohnson & JohnsonMain Street America GroupMid-Continent GroupMontgomery Ins./Safeco Ins.Phenix Mutual Fire Ins. Co.Preferred Specialty, LLCProgressive InsuranceQBERPS ContinentalSouthern Cross UnderwritersState Auto Insurance CompaniesSt. Johns Insurance Co.Tapco UnderwritersTravelersUnited Property & Casualty Ins. Co. Zurich Small Business

18 South Carolina Agent & Broker • Fall 2012

Sponsors:Access Insurance CompanyAFCO/Prime Rate Prem. Fin. Corp.American Strategic InsuranceAmTrust North AmericaAuto-Owners Insurance CompanyBankers Insurance GroupBerkley Mid-Atlantic Group, LLCBuilders Mutual Ins. CompanyBurns & Wilcox, Ltd.Capitol Preferred Ins.Capitol Special RisksCompanion Property & Casualty Insurance CompanyFirstCompFrontline Homeowners InsuranceGenesee General/ GSBGMACHanover Excess & Surplus, Inc.The HartfordIIABSC Agency, Inc.Insurance HouseJackson Sumner & AssociatesJohnson & JohnsonMain Street America GroupMid-Continent GroupMontgomery Ins./Safeco Ins.Phenix Mutual Fire Ins. Co.Preferred Specialty, LLCProgressive InsuranceQBERPS ContinentalSouthern Cross UnderwritersState Auto Insurance CompaniesSt. Johns Insurance Co.Tapco UnderwritersTravelersUnited Property & Casualty Ins. Co. Zurich Small Business

Fall 2012 • South Carolina Agent & Broker 19

Johnson & Johnson Preferred Financing

Serv

ing

Inde

pendent Agents &Com

pan ies

Since 1930

J J

Johnson & Johnson Preferred Financing

Serv

ing

Inde

pendent Agents &Com

pan ies

Since 1930

J J

t is no wonder then that E&O underwriters extending coverage for data breach to agencies increasingly are asking applicants whether they encrypt (or use other protective measures) to safeguard this client personal data when it is being transmitted.

Encryption A common question agents ask is: “what is encryption?” When you think of encryption, consider those codes the military employs to keep conversations unintelligible to the enemy. There are many definitions, but I like this simple one from Microsoft:

Encryption is a way to enhance the security of a message or file by scrambling the contents so that it can be read only by someone who has the right encryption key to unscramble it. For example, if you purchase something from a website, the information for the transaction (such as your address, phone number, and credit card number) is usually encrypted to help keep it safe. Use encryption when you want a strong level of protection for your information.

Requiring a strong password to gain access to your system is an important security procedure, but it is not the same as encrypting the data within the system.

Personal DataWhat are the types of “personal data” that are most sensitive and need to be encrypted when transmitted? The definition of “personal data” can vary by state and is contained in state data breach notification and privacy laws (South Carolina Section 39.01-90 found at: www.scstatehouse.gov/code/t39c001.php) as well as in various federal laws, such as Protected Health Information, under HIPAA. Insurers too might employ various definitions of “personal data” in their policies, so it is important that the agency be familiar with not only specific laws but also the coverage definitions that apply. Note also that the applicable state law is based upon the residency of the individual whose personal data needs protecting, not the location of the agency. Residency is an important consideration for both agencies writing business in multiple states and those writing policies that cover individuals residing in multiple states.

With all of the above caveats, the most commonly mentioned types of non-public, individually identifiable

22 South Carolina Agent & Broker • Fall 2012

Agents are being increasingly asked by their E&O underwriters whether they encrypt their clients’ personal data when it is being transmitted. This article provides recommendations with regard to two major areas agen-cies need to address – securing email and securing their websites when personal data is requested. It also discusses “encryption” and major types of “personal data” that are the subject of the various laws. Finally, the article outlines the type of resources that are available on the ACT website to help agencies address the those issues, as well as to develop and implement a comprehensive agency information security policy and program for their agency.

Agency Strategies to Send & Receive Personal Data Securely

By Jeff Yates, ACT Executive Director

I

“personal data” covered in the laws are those such as: social security numbers, driver’s license numbers and other government issued ids, debit and credit card numbers and pins, bank and financial account numbers and Protected Health Information. While often not mentioned in state laws, other personal data that should be protected includes information commonly used for security verification (mother’s maiden name, date/place of birth, etc.) or sensitive insurance information (such as jewelry schedules).

It is important for agencies to know what types of personal information they collect, where it is retained and who has access to it. Then they need to decide whether they really need to keep it. For example, many agencies stopped retaining copies of bank checks and are careful to pass along credit card numbers to carriers, but not to retain them, so that they do not become subject to the comprehensive PCI (Payment Card Industry) compliance requirements. These agencies are also extremely careful to shred this personal data as soon as it is no longer needed.

Further, if the agency decides it must keep particular sensitive personal data, it should limit access as much as possible to only those who need it. This precaution is particularly necessary for Protected Health Information. Finally, the agency should be careful to make sure that personal data is kept off of PCs, mobile devices, thumb drives or anywhere there is a significant risk of loss or theft.

PCs and Mobile DevicesUsers should be trained to remove any emails received with personal data from all PCs or mobile devices as soon as they are read. In addition, the agency should audit to make sure all PCs and mobile devices that access agency applications are password protected. Further, they should implement software that can remotely wipe all data off of these devices if they are lost or stolen.

Secure EmailEmail is the first major area agencies need to focus on when they begin encrypting communications to carriers and clients when personal data is included. Some prominent examples of emails likely to include personal data include: sending insurance applications to carriers for a quote or to clients to complete and sending insurance policies to clients.

With respect to emails between agencies and carriers (and general agents), ACT recommends that TLS secure email be implemented wherever possible. TLS (Transport Layer Security) is an open standard that once implemented between an agency and a carrier (both parties must have TLS implemented), all of the emails between the partners go securely in a manner that is transparent to the end users. In other words, the agent or carrier underwriter does not have to go to a proprietary website to pick up each email (which many underwriters will not do and is inefficient

for agency employees to do). TLS is a great solution for business partners where there are frequent email communications going back and forth.

Many agencies can implement TLS if they have email servers or hosted solutions that offer it. We recommend that the initial set up be handled by the agency’s technology expert, who should also verify it is working properly with each carrier and general agent. You can find a number of resources that explain TLS secure email more thoroughly on the ACT website (see “ACT Resources” on page 24), including a list of carriers that have advised us that they have TLS available.

Unfortunately, most agency clients will not have TLS capability and therefore, TLS is not a solution for communications with them. Those solutions require the agency to implement a proprietary email solution as well. When the agent sends a secure email to the client using one of these proprietary solutions, the client accesses it on the email vendor’s secure website. The tool also enables the client to send a secure reply back to the agent, which is very helpful when the client is being asked to complete a D&O application, for example. There are a number of vendors who can help agencies with both TLS-hosted emails and proprietary emails, as well as providing many other useful tools. (Two examples of such vendors are AppRiver and RPost.)

Real TimeToday email is used heavily to convey applications and other information between agencies and carriers and general agents, particularly in commercial lines. It is important to note, however, that Real Time offers a more efficient and secure method to handle these communications, where they are automatically encrypted and kept within the agency’s and carrier’s management systems.

Agencies are heavily using Real Time for personal lines, and we need to increase the usage in commercial lines. Many agencies and carriers are already using Real Time to submit commercial-lines applications and make quote requests for small commercial business, and some have started using real-time functionality to make mid-commercial submissions.

In addition, there is great potential for the industry to use Activity Notifications to communicate other types of messages directly between systems (such as the need for more underwriting information), without having to manage a morass of emails in employees’ mailboxes.

We urge agencies and carriers to continue to push the use of Real Time within their organizations and with their business partners, particularly for commercial-lines transactions and communications. Real Time is the workflow of the future for commercial lines, as well as personal lines. Email is not.

Agency WebsitesIt is also critical that agencies provide secure website connections when they ask the consumer to provide personal data through the

Fall 2012 • South Carolina Agent & Broker 23

24 South Carolina Agent & Broker • Fall 2012

agency website – to receive a quote, for example. The website should create a secure “https” tunnel before the consumer can fill out any form asking for personal data, just as you would experience when purchasing something or banking online.

In addition, if the agency provides a “non-https” -protected free-form text field for the consumer to contact the agency and make requests there is some risk the consumer will enter private, personal data. Therefore, it is a best practice to take one of the following steps with regard to this free-form text field: (1) to secure it, (2) change it to specified fields that ask only for basic contact information, such as name, phone number, email, address, or (3) conspicuously state that it is not secure and should not be used to provide any private personal data.

If the agency provides clients with the capability to access their insurance information or documents online, the website should create an “https” connection before any information can be accessed. Once again, agents should work with their website provider to help them with the technical aspects of creating this secure website capability.

Some agency E&O providers also require agencies to post a privacy statement if there is an option for the consumer to submit personal data through the website. It is important that the agency customize its privacy statement to track the agency’s particular data collection, usage, sharing and protection practices with regard to data collected through its website(s). Honda’s financial services website privacy statement (www.hondafinancialservices.com/help/privacy-policy) provides a good example.

ACT ResourcesThis article has covered only a few of the areas agencies must manage when protecting the security of their clients’ and employees’ personal data. ACT has developed several resources for agencies to review as they establish and implement their agency’s comprehensive information security program. All of these resources are included on the “Security & Privacy” page of the ACT website (www.iiaba

.net/act). These resources include a prototype agency information security policy, which agencies can use as a template to build their own customized policy or as a checklist of security issues they should address.

For more on TLS secure email, the ACT “Security & Privacy” webpage

includes articles, FAQs, a recorded webinar and a list of carriers that have implemented TLS. For more on securing your website and managing potential E&O exposures arising from the website, see the article Don’t Get Caught in the Web (also found in our magazine archives, Vol. 4, Fall 2010, p. 10)

ACT’s Security & Privacy page also includes sample website disclaimers, a recorded briefing on HIPAA-HITECH requirements for “Business Associates,” and additional articles focusing on the E&O and security risks arising from the use of social media, precautions to take when using public Wi-Fi sites and how to manage the “Bring Your Own Device” trend, where employees are using their personal devices to access business applications.

Jeff Yates is Executive Director of the Agents Council for Technology (ACT) which is part of the Independent Insurance Agents & Brokers of America. Jeff can be reached at [email protected]. ACT’s website is www.iiaba.net/act. This article reflects the views of the author and should not be construed as an official statement by ACT.

The OriginalFlood Experts

Agents love us, floods fear us.Get to know us.

Tim KillianFlood Underwriter & Monster Mitigator

Deborah BrckaVice President & Risk Wrangler

800.627.0000 x4900 | BankersInsurance.com

“I’ll be making a splash at the IIABSC Convention in Savannah, October 28-30. See you there!”Felix Flood Risk Monster & Star of MeetTheRisks.com

A MillenniAl’s TAke on

Marketing to Millennials” by Michael Fleischner (IA Magazine, Dec. 2011: www.iamagazine.com/Magazine/2011/December/Insurance-Views.aspx) is a good article for the way my generation would look at media and commercials. As I discuss below, I think most of the article’s points are on target. Some, however, are less important than others.

Have a Social Media presence, make it genuine I think one of the better points the author makes is: “Make sure your company has a space among social media outlets. Keep in mind though not to be overly commercial. Millennials can see right through it. Rather, be genuine and let your prospective market understand what you’re really about and what you stand for.”

While I am not sure how you can be insincere regarding matters of insurance, I think that the author

makes a good point to be sure your target really understands what you are marketing. One example would be to not make a company look like a friendly personal environment when chances are a customer would have to get through many automated messages or new employees each time they try to contact the company. This disconnect just makes people angry. This advice is common sense, but I do think it has become more relevant in the age of the Internet. Finding a company on the Internet is a lot more of a guessing game than getting personal recommendations or knowing the right people. If you are trying to attract people through this medium, it is much easier to do so when the message and the reality are matching.

Engage on a personal levelAnother point the author made was to “communicate on a personal level,” which is an easy thing to do with blogs or Facebook, etc. I have “liked” a few companies that I never see

again. I have done so to others that now seem to haunt my Facebook feeds. I think a medium

level of posts is good. If you are on someone’s Facebook feeds with a lot of uninteresting comments, you are more likely to get hidden. However, I can think of two companies that I see on my Facebook a lot, and I am more likely to consider them when I

am in the market. The way they achieve this is

by posting r e l e v a n t

By Lauren Foy, Student

sociAl MediAIndependent Agent Mike Foy asked his daughter Lauren, currently in college, to comment on a recent Independent Agent article, “Marketing to Millennials,” by Michael Fleischner. Lauren provided a very interesting perspective as a future insurance consumer on how she views and uses social media, commercials and the Internet to shop. She also comments on the continuing importance of personal relationships.

“

Fall 2012 • South Carolina Agent & Broker 25

information and doing it on a consistent, reasonable basis. One company usually posts a fact, story or comment relevant

to their product and ends with a question. This gets a lot of feedback and then is likely to show up on more people’s home screens. Don’t ask me how to take this skill from a sales company and make it relevant to insurance, but this is just one idea. My generation feeds on being “heard” and finds it so appealing that we give more attention to the social media sites that try to engage us.

I learned in my persuasive writing class that the best way to be effective in a blog setting is to use a question at the end so readers will feel like they have a say in your opinion and the topics covered. A good way to use this technique is by making a point with your question or crafting one that will get a lot of response from both sides. This will help to get positive feedback as well as some insight into the opposing side.

Be consistent and creative Two additional points made in the article are also good ones: be consistent and creative. These qualities help capture the attention of an otherwise preoccupied generation. While we are always multitasking, it is hard to pay complete attention to the radio (online or live) or the TV while trying to do homework or whatever we might be doing. So consistency and repetition are good tools to use. Creativity will always help a website when dealing with my generation.

Also, I am always drawn to the website that looks more professional and attractive. For a generation that has grown up dealing with the Internet, a functional and appealing website shows that the business is viable.

Info, contacts must be easy to findOne point missing from the article, which is very important when dealing with my generation, is that for the most part we expect instant gratification. Everyone grew up with the Internet getting faster and faster, providing answers to everything at our fingertips. With the invention of online radio, DVR/TiVo, the iPod and the prevalence of smart phones, we grew up having everything we wanted whenever we wanted it. I think this is a very important (but sometimes negative) aspect of my generation.

Since we are so technologically literate, we have access to hundreds of websites selling the same thing. We have the knowledge to navigate our way through, but I doubt most of us have the time or patience. We gravitate toward information, forms and products that we can find now. I

think this trait is an important aspect to marketing, because you can draw all the attention you want to your website, but if it is not easy to navigate or to find a way to contact someone, I think a good many prospective customers will drift to their second choice.

How I use the Internet to shopI use the Internet for almost all of my shopping. If I am at a shopping center and I need something, I will buy it there, but most other times, I will just rely on the Internet. I have always found it more convenient to go to a website for what I might need than to find a store. Websites usually are easier to navigate, have more options and are faster than traveling to a store. Generally I will start with a website that I have used before and have had a good experience with. If I have a longstanding relationship with a company, I usually will just trust that they have the best price and not look any further. However, if it is a new website or one I have not used a lot, I will tend to look around the Internet for a better deal, and if I can’t find one, I will come back to the first one.

I think that my generation would rather not take a day to travel around and price shop when they could just get the same amount accomplished in a much smaller period of time through the Internet. Many would rather do something on the Internet than pick up the phone and call. As a generation, we seem to be more comfortable with the Internet than with the phone.

For the most part, I have found the Internet to be a reliable buying outlet, so there has been no reason to use another means

26 South Carolina Agent & Broker • Fall 2012

of shopping. A few unappealing encounters can teach an Internet buyer to look into the company before buying from them. It is easier for a company to lie about their product when it is being presented on a webpage. This “threat” is where the relationship with a company comes into play. If you have bought a product with them that wasn’t what it said it was, then a bad relationship is created.

Personal relationships are still importantPersonal relationships are still important for some things. I look at these relationships in a similar way to a website, in the sense that if I had a positive relationship with a store or service, then I am more likely to return. If the experience was negative, I won’t. There are a few things that I will never buy online, one of them being a cell phone. I got my first cell phone from a sales representative, Stan, and I have returned every time I needed a new phone or anything else cellular. On the other hand, there are companies I will never return to based on bad experiences. I am currently in the process of cancelling one of my debit-card accounts because of bad customer service.

Customer service is where people establish relationships, and if the goal is to attract Internet users to come into an office or even pick up the phone to speak with a person, relationships play a huge role. Going back to the example of Stan, I have many opportunities and online resources to buy a cell phone or accessories on a website, but due to the strong relationship with

the store personnel, I always return rather than go to the Internet. These personal relationships give the customer a respect for the opinions and suggestions of the service representative that one cannot get from online ratings or a customer service representative in a call center.

In a perfect situation, there would be a strong relationship with the personnel of the business, coupled with the support of a functional website and/or mobile app. Providing a personal relationship enhanced by these online tools is the best way to get my generation off the Internet and into the office.

Editor’s Note: Trusted Choice® has invested significant resources to provide member agents with the tools to provide exactly what the author is suggesting: online/mobile tools to enhance the personal relationships and expertise independent agencies already provide. Basic packages are free with Big ”I” membership. Learn more at www.projectcapmarketing.com.

Lauren Foy is a sophomore at University of Rhode Island and can be reached at [email protected]. Lauren wrote this article for ACT and based it on an email she wrote to her dad, an independent agent, to assist him with the millennials’ perspective with regard to social media and marketing. The Agents Council for Technology (ACT) is part of the Independent Insurance Agents & Brokers of America, Inc. Their website is www.independentagent.com/act. This article reflects the views of the author and should not be construed as an official statement by ACT.

Fall 2012 • South Carolina Agent & Broker 27

Our cOmprehensivemOBiLe hOmeOWners insurance

reWarDs Our agents.

•15%NewBusinessCommission

•PartnershipProfitSharing

•100,000MaximumPolicyLimits

•50+AgeOfInsuredDiscounts

•NewerHomeDiscounts

•FastOnlineQuotes,Policies AndEndorsements

National Security strives to provide competitive, affordable insurance for policyholders, but we also reward our agents with some of the highest commissions in the industry, a partnership profit sharing program and an award-winning web site that provides fast online quotes, policies, and endorsements. Find out more by calling 1-800-239-2358 x213 or visit us on the web at www.nationalsecuritygroup.com. Elba, Alabama • 800-239-2358

28 South Carolina Agent & Broker • Fall 2012

Don’t Let Texting Create

Distracted driving continues to be a serious issue at both the state and national lev-els. Text messaging while driving is a primary distraction and can have the same effect as driving while intoxicated when it comes to increasing the chances of an accident while behind the wheel. Your agency may be thinking about texting and its ef-fects on the risk exposure of your commercial and personal auto policyholders, but have you ever stopped to think about how text messaging may be affecting your agency’s E&O exposure? Think about it now, before you wind up with an E&O wreck on your hands.

The ways agencies communicate with their customers and carriers in today’s fast-paced world continue to change. Phone, fax, e-mail, websites, blogs, social media websites, Twitter ac-counts and texting are all vehicles of communication. Is your agency staff texting customers or carriers? If so, what informa-tion and for what purposes? Text messaging could be used by agency staff to maintain customer relationships, communicate and gather relevant information or bind or modify coverage. In fact, it may even be your customers’ preference to communicate with the agency via text message because of the convenience. But does your agency have existing procedures to address texting and have a consistent policy for how agency personnel should handle both incoming and outgoing texts? Here are some things to think about when it comes to utilizing texting in the agency:

1. Create an agency policy on texting. Does your agen-cy have a written procedure for how texts should be handled? The procedure should be thorough with clear standards for all agency staff. It should cover how tex-ting can be used with both customers and carriers. If you don’t have any procedural guidelines in place, sit

down with agency staff and talk about who is texting and how it’s being used for business purposes. Also, consider any nuances with agency staff texting from personal phones versus agency-provided phones.

2. File documentation of texts. Should an E&O claim arise against the agency, the No. 1 tool for a defense is going to be documentation in the customer file. E&O claims are often the customer’s word against the agent’s, and well-documented files can be the differ-ence between winning and losing. Text messages to and from both customers and carriers can serve as vital documentation. That’s right, carriers!

KEEP IT PROFESSIONAL

OMG, BRT, OOTO, CYE and LMK (Oh My God, Be Right There, Out Of The Office, Check Your E-mail and Let Me Know) are all commonly used texting abbrevia-tions. To say that texting is a more relaxed form of com-munication is an understatement.

Don’t let employees fall into this trap if the agency is using texts to communicate with customers. Communi-cation should stay professional and clear to both parties. Ambiguity is not the agency’s friend in defending an E&O claim. When it comes to customer file documentation in the agency management system, just like all documentation, it should adhere to the agency’s standard input procedures so that all employees can reconstruct the conversation, the ac-tion taken and any additional follow-up required.

OMG!By David Hulcher

AVP Agency Risk ManagementBig “I” Professional Liability

an E&O Wreck

Fall 2012 • South Carolina Agent & Broker 29

E&O claims from carriers against agents continue to rise. Important file documentation includes offers and declinations of coverage, information for the application, changes to the policy or limits, carriers’ permission to bind, declinations to offer terms and midterm change requests. The author of the text, along with date, time and summary of the text should be in the customer’s file in the agency management system. Remember, the ability to provide optimal customer service relies on all agency staff knowing what has been discussed with the customer. A disciplined approach to documentation is extremely important.

With so many ways to communicate with customers and carriers, it is important to understand what agency staff is do-ing. Valuable customer documentation that could help defend the agency should an E&O claim occur could be getting lost in the form of text messages. If your agency has never thought about texting or doesn’t have written guidelines for using it, take the time to discuss the issue with agency staff and come up with a plan.

David Hulcher ([email protected]) is AVP of agency profes-sional liability risk management for the Big “I” Professional Liabil-ity program, the largest national insurance agents E&O program in the country, insuring approximately two-thirds of all Big “I” mem-bers. He is focused on developing risk management information and tools to assist agents not only in avoiding E&O claims but also in improving general agency business practices and procedures.

usyou

Montgomery Insurance™ is committed to the success of its independent agents. We meet the needs of your small to mid-sized commercial lines customers by providing the Montgomery Advantage™: stability and consistency, profitable growth, ease of doing business, local decision making, service you need and expect, competitive products and services, and people you know and trust. Doing more to help independent agents conquer the fast turbulent currents of business today.

No one keeps independent agents on course to succeed like we do.

www.montgomery-ins.com

© 2010 Montgomery Mutual Insurance Company. All rights reserved.

MIC_AgentBroker_Kayaker_Ad.indd 1 11/9/10 3:35 PM

30 South Carolina Agent & Broker • Fall 2012

New Residential Numbering Program Launches Thanks to $5,000 Grant

Program Enables Firefighters to Locate Residences Faster

©20

12 F

irem

an’s

Fund

Insu

ranc

e Co

mpa

ny, N

ovat

o, C

A. A

ll ri

ghts

rese

rved

. 1

0256

-IIAB

SC-7

-12

More than 40 percent of the St. John’s Fire District service area is rural and many homes are poorly marked, making emergency response times – even under ideal conditions – challenging. Now, thanks to a $5,000 grant from Independent Insurance Agents and Brokers of South Carolina (IIABSC) and Fireman’s Fund Insurance Company, St. John’s Fire District is installing reflective or adhesive numbers that would be placed on residents’ homes, mailbox posts, fence posts, or other locations that meet the intent of the Charleston County Code.

Many of the homes in this community are located on unpaved and unmaintained roads in excess of a mile. The only indication of the amount of homes located on these roads is a cluster of mailboxes at the beginning of the road. The numbering on the mailboxes may not exist, and the home may also lack proper numbering making it difficult to find. This may help explain why the National Fire Protection Association reports that the fire death rate of rural communities is roughly twice the rate as compared to suburban communities in the U.S.

“We are grateful for this grant. This program increases the safety of the citizens. By having homes with proper and quick identification, we can locate the residence more quickly when responding to an emergency call”, said St. John’s Fire District Captain James Ghi.

The grant is part of a nationwide philanthropic program funded by Fireman’s Fund Insurance Company. The program is designed to provide needed equipment, training and educational tools to local fire departments and burn prevention organizations. Since 2004, Fireman’s Fund has issued grants to 1,900 different organizations totaling more than $29 million. Through the program, independent insurance agencies and brokers that sell Fireman’s Fund products, like Independent Insurance Agents and Brokers of South Carolina, are able to direct these grants to support the fire service.

“Firefighters have incredibly demanding jobs, and it’s important they can identify where they need to respond to an emergency,” said Laura Cornell, of IIABSC. “We are also pleased to be able to show our gratitude for all the department does for the community.”

To learn more about the grant program and other grants awarded in South Carolina, visit: www.facebook.com/SupportingFirefighters or www.twitter.com/ffundheritage

For more information, visit: www.iiabsc.com

Fall 2012 • South Carolina Agent & Broker 31

“As an artist, the quiet confidence I receive from painting helps me guide my team of underwriters to be creative with a keen eye for detail so that our customers receive competitive quotes they can sell.”

Roxanne Barry, CISR, CIC Property & Casualty Manager —and the “Warhol” of J.M. Wilson

Connect with Roxanne on LinkedIn!

800.666.5692 jmwilson.com

PIA National 2011 MGA of the Year

Property/Casualty • Professional Liability • Surety Commercial Transportation • Personal Lines • Premium Finance

KNOWLEDGECOMES FROM EXPERIENCE Alarm Installation coverage

in a five-minute phone call.

Call. Quote. Bind. Using TAPCO’s courteous and prompt call center, Alarm Installation coverage can be

quoted, bound and delivered to your e-mail inbox quickly and accurately during one five-minute phone call.

CGL Coverage Available:• Primary limits up to $3 million Occurrence/Aggregate• Electronic Data Liability• Errors & Omissions Coverage Part—Policy Limits• Excess or Umbrella limits up to $5 million• Blanket Additional Insured Endorsement• Medical Payments—$5,000 limit• Lost Key Coverage—$25,000 limit• Property Damage Extension (Care, Custody, and Control)—Policy limits up to a maximum of $200,000 per occurrence/$300,000 aggregate

Property Coverage Available:• Building• Contents• Business Income• Basic, Broad or Special Form• Replacement Cost or Actual Cash Value• Equipment Breakdown

* Available coverages and markets may varydependent upon risk characteristics.

1,000 Strong More than 1,000 classes of P&C businesswritten under binding authority.

• “A”-rated non-admitted carrier

• Competitive pricing

• Fast policy turnaround

• In-house financing available

• Quick claims handling

• $10 credit to your personalized TAPCO EZ Bucks Visa debit card with each policy

• Visa, MasterCard and ACH payments accepted

The TAPCO Service Pledge

800-334-5579www.gotapco.com

View campaign photos now on the Trusted Choice® Facebook page

This summer, Trusted Choice® wrapped a successful social media campaign documenting the progress of the Chopper for Charity build with Orange County Choppers (featured on reality TV show American Choppers on Discovery Channel) that ended with a $150,000 donation to Make-A-Wish.

This fall, the SC Trusted Choice team will launch its own chari-table activities with Make-A-Wish South Carolina that includes sponsorship of its Kids For Wish Kids® and Wishmakers On Campus® programs.

In both programs, elementary- to college-age students sponsor the wishes of children with life-threatening medical conditions, and Trusted Choice® makes a contribution oftentimes matching dollar for dollar.

To help bring the program to a community near you, contact a committee representative listed on the following page.

32 South Carolina Agent & Broker • Fall 2012

Regional Contacts

PeeDee/ Grandstrand – Chesterfield, Darlington, Dillon, Florence, Georgetown, Horry, Marion, Marlboro, Williamsburg counties

Gardiner MarekGardiner Marek AgencyNorth Myrtle Beach, [email protected]

Kim GoreHUB International SoutheastMyrtle Beach, [email protected]

Piedmont – Chester, Lancaster, York counties

Chase WarringtonJohnson & JohnsonCharlotte, [email protected]

Charleston Lowcountry Berkeley, Charleston, Colleton, Dorchester counties

Kathy McKayMcKay InsuranceMt. Pleasant, [email protected]

Buck InabinetTaylor AgencySummerville, [email protected]

Lisa VlietThe HartfordMt. Pleasant, [email protected]

Midlands – Aiken, Allendale, Bamberg, Barnwell, Calhoun, Clarendon, Edgefield, Fairfield, Kershaw, Lee, Lexington, McCormick, Newberry, Orangeburg, Rich-land, Saluda, Sumter counties

Gus BrabhamFrank B. Norris & Co.Columbia, [email protected]

Frank SheppardIIABSCColumbia, [email protected]

Upstate – Abbeville, Anderson, Cherokee, Greenville, Greenwood, Pickens, Spartanburg, Oconee counties

Tom BatesHerlong Bates Burnett InsuranceGreenville, [email protected]

Jeff D. PhillipsCountybanc InsuranceGreenwood, [email protected]

Curtis TaylorHerlong Bates Burnett InsuranceGreenville, [email protected]

Hilton Head /BeaufortBeaufort, Hampton, Jasper counties

Jay TaylorKinghorn Ins Agency of BeaufortBeaufort, [email protected]

“I wish to be a pilot for a day.”

View campaign photos now on the Trusted Choice® Facebook page

This summer, Trusted Choice® wrapped a successful social media campaign documenting the progress of the Chopper for Charity build with Orange County Choppers (featured on reality TV show American Choppers on Discovery Channel) that ended with a $150,000 donation to Make-A-Wish.

This fall, the SC Trusted Choice team will launch its own chari-table activities with Make-A-Wish South Carolina that includes sponsorship of its Kids For Wish Kids® and Wishmakers On Campus® programs.

In both programs, elementary- to college-age students sponsor the wishes of children with life-threatening medical conditions, and Trusted Choice® makes a contribution oftentimes matching dollar for dollar.

To help bring the program to a community near you, contact a committee representative listed on the following page.

Fall 2012 • South Carolina Agent & Broker 33

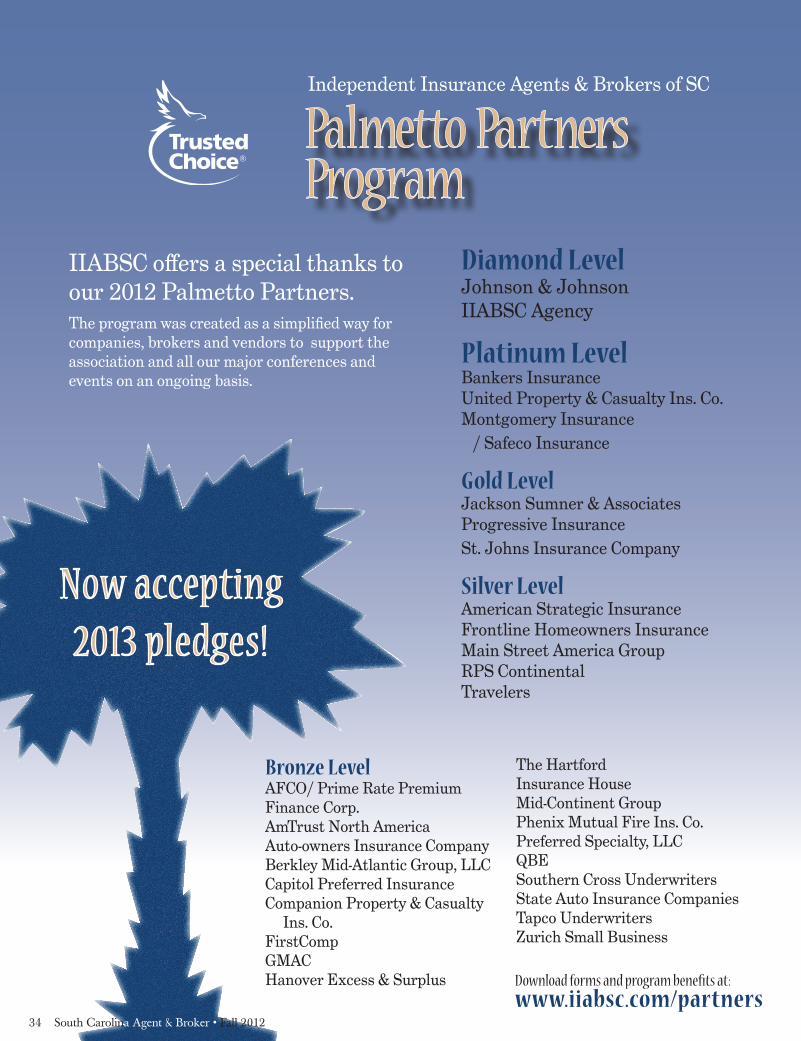

IIABSC offers a special thanks to our 2012 Palmetto Partners. The program was created as a simplified way for companies, brokers and vendors to support the association and all our major conferences and events on an ongoing basis.

Silver LevelAmerican Strategic InsuranceFrontline Homeowners InsuranceMain Street America GroupRPS ContinentalTravelers

Diamond LevelJohnson & JohnsonIIABSC Agency

Platinum LevelBankers InsuranceUnited Property & Casualty Ins. Co.Montgomery Insurance / Safeco Insurance

Gold LevelJackson Sumner & AssociatesProgressive InsuranceSt. Johns Insurance Company

Download forms and program benefits at: www.iiabsc.com/partners

Independent Insurance Agents & Brokers of SC

Bronze LevelAFCO/ Prime Rate Premium Finance Corp. AmTrust North AmericaAuto-owners Insurance CompanyBerkley Mid-Atlantic Group, LLC Capitol Preferred InsuranceCompanion Property & Casualty Ins. Co.FirstCompGMACHanover Excess & Surplus

The HartfordInsurance HouseMid-Continent GroupPhenix Mutual Fire Ins. Co.Preferred Specialty, LLCQBE Southern Cross UnderwritersState Auto Insurance CompaniesTapco UnderwritersZurich Small Business

34 South Carolina Agent & Broker • Fall 2012

Fall 2012 • South Carolina Agent & Broker 35

Member News

NEW AGENCY MEMBERS:Cypress Risk Management, Ltd.Ridgeville

James Strickland Insurance Agency, LLCRock Hill

Lamplighter Insurance, LLCColumbia

Rose & Kiernan, Inc.Charleston

Sturgis Beaty Insurance GroupRock Hill

Upstate Insurance Consultants, LLCClinton

NEW ASSOCIATE MEMBERS:Municipal Association of SCColumbia

Private Client Insurance GroupPalm Beach Gardens, Fl.

Welcome New Members(April - August 2012)

The Seneca Rotary Club recently honored C. Lane Morgan, owner of Morgan Insurance Agency, as the recipient of the 2012 Ballenger Award, given to a local businesses or businessperson to recognize their vocational service to the community.

To be considered for the award, a business must have operated in the Seneca area for 10 years or more, demonstrate and promote loyalty and dedication to the local

community and exemplify the ideals of Rotary: truth, fairness, goodwill and friendship.

Morgan has been serving people in Oconee County since 1969 from his office on North First Street. The Seneca Rotary Club is made up of Seneca Area business people and community members who are working together to make Seneca a better place to live. Club projects and fundraisers benefit area schools and children.

Brigadier General Glenn A. Bramhall SCARNG ‘79 has been confirmed by the Senate for promotion to the rank of Major General. He is currently serving as Deputy Commanding General, 263d Air and Missile Defense Command. When not on active military duty, Glenn works with PC&L Agency in Spartaburg.

LANE MORGAN, INDEPENDENT INSURANCE AGENT HONORED BY SENECA ROTARY CLUB

For nearly 30 years, Builders Mutual® has been exclusively dedicated to the construction industry. Risk management consultants and Builders University® courses are available to help your customers protect their bottom line. When you combine our industry expertise with time saving tools like BOB 2.0, the insurance choice is simple.

EXPERTISE YOU CAN

LEVERAGE. IT,S THAT

SIMPLE.

Login today at buildersmutual.com.And connect with us on Facebook.

36 South Carolina Agent & Broker • Fall 2012

December5 Estate Planning Techniques, 2 hrs. L&H5 Agency Management Based Ethics, 3 hrs. Ethics6 Basic Flood, 3 hrs. P&C10 Retirement Planning & Annuities, 2 hrs. L&H11 Liability Issues to Worry About, 2 hrs. P&C13 Top 5 Life Insurance Needs, 2 hrs. L&H13 Advanced Flood, 2 hrs. P&C 18 COPE Property Underwriting, 2 hrs. P&C18 Ethics and Business, 3 hrs. Ethics19 Building Codes are Bad for Insureds, 2 hrs. P&C