Embed Size (px)

Citation preview

Vo

lum

e- 8

Octo

ber

-20

16

P

ag

es 1

-35

SBS

Digest

By

Fo

r Priv

ate

circ

ula

tion

on

ly

Interns’

An attempt to share knowledge

Interns ofSBS and Company LLP

CONTENTS

INCOME TAX ACT, 1961

INCOME DECLARATION SCHEME, 2016

SECTION 269SS & 269T ................................................................................................................................9

TAXABILITY OF PROVIDENT FUND...................................................................................................................12

AUDIT..............................................................................................................................................14

VOUCHING OF CASH AND BANK TRANSACTIONS...................................................................................................14

SA 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS.........................................................................................17

INDIRECT TAX..................................................................................................................................20

APPLICABILITY OF LIMITATION PERIOD VIS-À-VIS REFUND CLAIM UNDER RULE 5 OF CENVAT CREDIT RULES 2004..............................20

FEMA..............................................................................................................................................23

COMPOUNDING OF CONTRAVENTIONS UNDER FEMA.............................................................................................23

......................................................................................................................1

................................................................................................................1

SBS Interns' Digest www.sbsandco.com/digest

INCOME TAX

UPDATES IN INCOME TAX

FEMA..............................................................................................................................................30

FEMA UPDATES.......................................................................................................................................30

COMPANIES ACT, 2013.....................................................................................................................31

RULES, CIRCULARS AND NOTIFICATIONS ISSUED DURING THE MONTH OF SEPTEMBER, 2016...................................................31

INDIRECT TAX..................................................................................................................................34

IDT UPDATES.........................................................................................................................................34

....................................................................................................................................27

............................................................................................................................27

UPDATES

INCOME DECLARATION SCHEME, 2016

Contributed by Disha Maheshwari & Vetted by CA Ram Prasad

1 | P a g e

INCOME TAX ACT, 1961

SBS Interns' Digest www.sbsandco.com/digest

Income Declaration

Scheme, 2016

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

2 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Introduction

In order to provide an opportunity to all persons, a new scheme, i.e., Income Declaration Scheme, 2016 (“Scheme”) has been introduced by the Finance Ministry which allows all persons who have not paid full taxes in the past to come forward and declare the undisclosed income and pay tax, surcharge and penalty. The amount of such tax, surcharge and penalty works out to 45 percent of such undisclosed income declared.

Chapter IX has been introduced in the Income-tax Act, 961 (“Act”) for the Scheme and is named as ‘The Income Declaration Scheme, 2016’ consisting of sections 181 to section 199. The scheme has been

stintroduced with effect from June 1 2016 and will remain open up to the date to be notified by the Central Government in the Official Gazette which is September 30, 2016 (notified by the Central Government).

The scheme is applicable in respect of undisclosed income for any Financial Year (“FY”) prior to FY 2016-17 (i.e., AY 2017-18). The Income Declaration Rules, 2016 has also been notified by the Central Board of Direct Taxes (“CBDT”) (on May 19, 2016) and has issued various explanatory notes and clarifications in the form of ‘Frequently asked questions’ (“FAQ”) for better compliance with the Scheme.

Detailed Analysis of the Scheme

I. Applicability of the Scheme:

As mentioned above, the Scheme is open for all persons who wish to disclose their undisclosed income and for which full taxes have not been paid in the past.

Section 183 of the Act lays down that in respect of any income chargeable to tax under the Act for any AY(prior to AY 2017-18) for which:

- No return has been under section 139 of the Act- he has failed to disclose such income in the return of income filed (before the commencement

of this Scheme)- has escaped assessment by reason of omission or failure on the part of such person to furnish a

return of income or to disclose fully and truly all material facts necessary for the assessment or otherwise

A person can make a declaration of undisclosed income in Form-1 (to the Principal Commissioner of Income Tax (“CIT”) or the CIT). The declaration can be made in the following manner:

a) electronically under digital signature; orb) through transmission of data in the form electronically under

electronic verification code; or c) in print form, to the concerned Principal Commissioner or the

Commissioner who has the jurisdiction over the declarant.

Co

mp

anie

s Act

3 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Post such declaration, the jurisdictional Principal CIT / CIT will issue an acknowledgement in Form-2 within 15 days from the end of the month in which the declaration in Form-1 has been made. The time limit has been increased to 30 days from the end of the month in which the declaration is made only for all declarations made in the month of July, 2016 due to the changes in Form-2.

Post payment of tax, surcharge and penalty, the declarant has to file Form-3 for the proof of the payment to the Jurisdictional Principal CIT / CIT after which the said authority will issue a certification in Form-4 of the acceptance of declaration within 15 days of submission of proof. However, no time limits have been provided for filing of Form-3.

This income can be in the form of investment in assets in India or otherwise.In case the income is in the form of investment, the Fair Market Value (“FMV”) as on June 1, 2016 (date of commencement of the Scheme) shall be deemed to be undisclosed income. The determination of FMV shall be done in accordance with Rule 3 of the Income Declaration Scheme Rules, 2016 (“Rules”).

No deduction of any expense or any allowance relating to such undisclosed income shall be allowed to the declarant.

II. Non-applicability of Scheme

No declaration can be made in respect of any undisclosed income chargeable to tax under the Act for which:

- A notice under section 142, section 143(2), section 148, section 153A or section 153C of the Act has been issued and served upon the person on or before May 31, 2016 in respect of such AY for which the proceeding is pending before the Assessing Officer; or

- A search has been conducted under section 132 or requisition has been made under section 132A or a survey has been carried out under section 133A in a previous year and the time limit for issuance of notice under section 143(2), section 153A or under section 153C for the relevant AY has not expired;

However, in case the assessment has been completed and certain income has not been disclosed neither been assessed, then for such income a declaration can be made under this Scheme.

- Information is received under an agreement with foreign countries in respect of such undisclosed assets

- Cases covered under the Black Money(Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015

- Persons notified under the Special Courts Act, 1992

- Cases covered under The Indian Penal Code, Narcotic Drugs and Psychotropic Substances Act, 1985, the Unlawful Activities (Prevention) Act, 1967, the Prevention of Corruption Act, 1988

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

4 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

III. Amount of tax to be paid:

Section 184 and 185 deals with the amount of tax, surcharge and penalty to be paid which totals out to 45%.This comprises of the following:

- tax at 30% of such undisclosed income- surcharge / Krishi Kalyan Cess at 25% of

amount of tax (i.e., 7.5% of the amount of undisclosed income)

- penalty at 25% of amount of tax (i.e., 7.5% of the amount of undisclosed income)

IV. Time limit for making the declaration:

The time limit for making the declaration has been limited to 4 months, i.e., from June 1, 2016 to September 30, 2016. However, taxes, surcharge and penalty relating to such undisclosed income can be deposited in the following manner:

?Minimum 25% by Nov 30, 2016.?Minimum 50% by March 31, 2017 (-) amount paid by

Nov 30, 2016?100% of the amount to be paid by Sep 30, 2017

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

5 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

a) Individual himself; b) where individual is absent from India, person

authorized by him; c) where the individual is mentally incapacitated,

his guardian or other person competent to act on his behalf.

a) Karta; b) where the Karta is absent from India, by any

other adult member of the HUF;c) where the Karta is mentally incapacitated from

attending to his affairs, by any other adult member of the HUF

a) Managing Director; b) where for any unavoidable reason the

Managing Director is not able to sign, by any Director

c) where there is no Managing Director, by any Director.

a) Managing Partner; b) where for any unavoidable reason the

Managing Partner is not able to sign, by any Partner, not being a Minor

c) where there is no Managing Partner, by any Partner, not being a Minor

a) Any member of the association or b) The principal officer.

a) That person or b) by some other person competent to act on his

behalf

S. No Status of the declarant Declaration to be signed by

Individual

HUF

Company

Firm

Any other association

Any other person

1.

2.

3.

4.

5.

6.

V. Authorized person to sign the declaration:

It is important to note that the if a declaration (under this Scheme) is made by one person with respect of (“w.r.t“) his income or as a representative assessee in respect of the income of any other person, any other declaration made by the same person, either w.r.t his income or the income of such other person will be considered as void. This implies that a person can make only one declaration under this Scheme, either for his income or such other person on whose behalf he is the representative assessee.

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

6 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

VI. Impact of declaration of undisclosed income under this Scheme:

The following points are noteworthy w.r.t the income declared by a declarant:

- The income declared will not form a part of the total income of the declarant if the respective dues (tax, surcharge and penalty) has been paid within the due date specified.

- Such income will not impact the completed assessments under the Income-Tax Act, 1961 or the Wealth-tax Act, 1957 (27 of 1957)

- No set off or relief can be claimed in any appeal, reference or other proceedings in relation to any assessments or reassessments and the same cannot be reopened as well.

- If the undisclosed income is in the form of investment in asset, which is in the name of a benamidar is transferred to the declarant (who provides the consideration for such asset) or to his legal representative, within the period notified by the Central Government, i.e., within September 30, 2017, such income would not be treated as benami transactions and the provisions of the Benami Transactions (Prohibition) Act, 1988 (45 of 1988) shall not apply to the declarant.

- The amount of tax, surcharge and penalty paid under section 184 and 185 is non-refundable- No further penalties can be levied to the declarant relating to the income declared if the

declaration is not considered void.

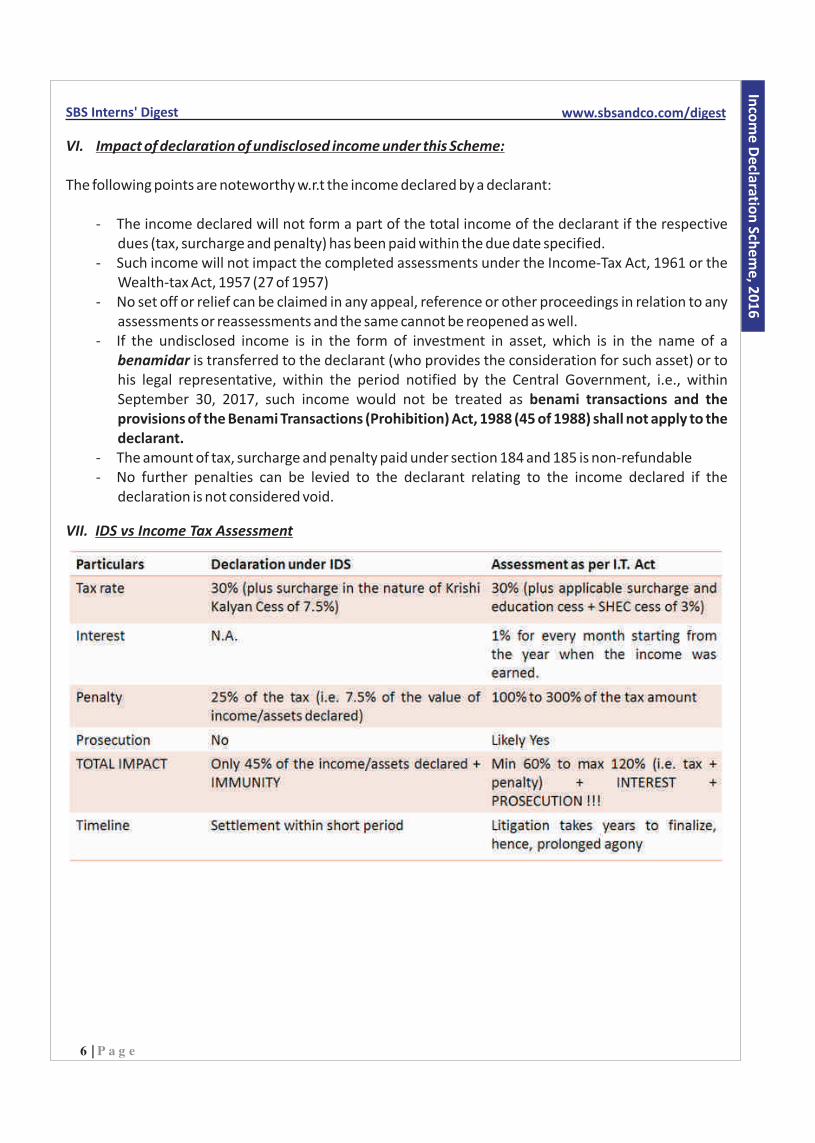

VII. IDS vs Income Tax Assessment

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

7 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

VIII. Cases where declaration will be considered void:

In the below mentioned cases the declaration will be considered as void and the Income-tax Authorities can use the information furnished under such Scheme for assessment under the normal provisions of the Act (including penalties and prosecution):

- In case where declaration has been furnished in circumstances to which the Scheme does not apply (section 196 of the Act)

- In case where a declaration has been furnished within the time limit prescribed but the amount of tax, surcharge and penalty has not been paid within the time limit prescribed

- In case a person has already filed a declaration under this Scheme, the second declaration being filed will be considered as void

- Where the declaration has been made by misrepresentation or suppression of facts or information

Further, as mentioned above, any amount paid under this Scheme shall not be refundable even if the declaration is considered void.

IX. Certain important clarifications issued by CBDT

1) In case of undisclosed income which is in the form of investment in the form of an asset, if the tax, surcharge and penalty has been paid under this Scheme by considering the FMV as on June 1, 2016, in case of capital gains arising (where the asset is sold in future):

- Period of holding will be considered from June 1, 2016- Cost of such asset will be taken as the FMV as on June 1, 2016.

2) In case of undisclosed income which is in the form of investment in the form of an asset and such asset is partly from income that has been assessed to tax earlier, the sub-rule (2) of Rule 3 of the Rules shall apply, wherein it has been mentioned that where investment in any asset is partly from an income which has been assessed to tax, proportionate amount will be disclosed under this Scheme.

3) If a person declares only part of his undisclosed income under the Scheme, no immunity will be granted for the part undisclosed.

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

8 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

4) A person cannot disclose income which has been acquired from money earned through corruption.

5) The declarations made under this Scheme will be kept confidential .There would be no further enquiry post declaration apart from whether any proceedings are pending under the sections mentioned above.

6) The declaration shall be invalid in case only part payment of the amount of tax, surcharge and penalty has been made.

7) In case of change in entities, where the earlier entity is no more in existence, the declaration is to be filed in the name of the existing entity (eg. Amalgamated company in case of amalgamating company as the same is no more in existence)

8) PAN has to mandatorily be disclosed

9) Credit for taxes deducted shall be allowed against such undisclosed income which is related, declared under the Scheme and where credit of such tax has not been claimed in any AY.

The Scheme introduced by the Finance Ministry is akin to a place of worship wherein everyone can wash their sins without having to explain anything to anyone. The declarants are not only protected from prosecution but also huge penalties that might even wash away such income. As rightly mentioned by the IT Department “Your undisclosed income is a time bomb……”

10) Various clarifications and rules have been framed for the method of computation of FMV of certain assets

11) A revised declaration can be filed provided that:

- The undisclosed income in the revised declaration is not less than the undisclosed income declared in the declaration already filed.

"The world breaks everyone, and afterward, some are strong at the broken places" - Ernest Hemingway

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

Disha Maheshwari,

Co

mp

anie

s Act

Inco

me

De

claration

Sche

me

, 20

16

SECTION 269SS & 269T

Contributed by Md. Sameer Hussain & Vetted by CA Ram Prasad

9 | P a g e

INCOME TAX ACT, 1961

SBS Interns' Digest www.sbsandco.com/digest

Section 269SS - Mode of taking or accepting certain loans, deposits and specified sum:

Applicability:

This section applies to all the persons i.e. individual, HUF, Company, Partnership firm, AOP/BOI, Local authority, Co-operative society, Trust, AJP.

Provision:

1 No person shall take or accept from any other person, any loan or deposit or any specified sum , otherwise than by an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account, if

2(a) the amount of such loan or deposit or specified sum or the aggregate of the loan or deposit or specified sum is twenty thousand rupees or more or

(b) On the date of taking or accepting such loan or deposit or specified sum, any loan or deposit or specified sum accepted earlier by such person from the depositor is remaining unpaid (whether repayment has fallen due or not) is Rs.20,000/- or more or

(c) The aggregate amount of loan or deposit or sum specified along with the amount loan or deposit or sum specified taken earlier which is outstanding on the date on which loan or deposit is to be taken is Rs. 20,000/- or more.

Exemption from Sec 269SS: Provisions of this section are not applicable if loan or deposit or sum specified is taken from or taken by:

- Government- any banking company, post office savings bank or cooperative bank;- any corporation established by a Central, State or Provincial Act;- any Government company as defined in clause (45) of section 2 of the Companies Act, 2013 (18 of

2013)- such other institution, association or body or class of institutions, associations or bodies which the

Central Government may, for reasons to be recorded in writing, notify in this behalf in the Official Gazette:

Also, provisions of this section are not applicable in case if both the parties i.e. acceptor and depositor are having agricultural income and neither of them has any income chargeable to tax under Income tax act, 1961.

1 "specified sum" means any sum of money receivable, whether as advance or otherwise, in relation to transfer of 2an immovable property, whether or not the transfer takes place

"loan or deposit" means loan or deposit of money

Co

mp

anie

s Act

Sectio

n 2

69

SS & 2

69

T

10 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Penalty for failure to comply with section 269SS:

As per Section 271D of the Income tax act, 1961 if a person fails to comply with Section 269SS then the Joint Commissioner shall charge a sum by way of penalty equal to the amount of the loan or deposit or specified sumso taken or accepted. Examples:

1. Let Mr. X had borrowed a loan of Rs. 12,000 from Mr. A and Rs. 18,000 from Mr. B in cash as on 20/09/2016 for the first time. Whether there is any contravention to section 269SS?

Ans: There is no contravention for Sec 269SS as both Mr. A and Mr. B are different and aggregate amount need to be checked in individual capacity.

2. Let Mr. X had borrowed a loan of Rs. 12,000 from Mr. A and Rs. 18,000 as Deposit in cash as on 20/09/2016 for the first time. Whether there is any contravention to section 269SS?

Ans: As per Section 269SS (a), no person should accept loan or deposit or any other specified sum in cash if such amount in exceeds Rs 20,000/- As in the instant case, amount is exceeding Rs 20,000/- (i.e. 18,000 + 12,000 = 30,000/-) there is a contravention.

3. Let Mr. X had borrowed a loan of Rs. 12,000 from Mr. A as on 01/07/2014 in form of account payee cheque and the same is still payable as on 20/09/2016 amounting to Rs 15,000 (Including interest). Also he has borrowed Rs. 6,000 as Deposit in cash as on 20/09/2016, whether there is any contravention to section 269SS?

Ans: As per Section 269SS (b), as on the date of taking or accepting loan or deposit or specified sum, if there is any loan or deposit or specified sum accepted earlier is remaining unpaid then the same should be considered for Rs 20,000/- limit. In the instant case, as the amount exceeds 20,000/- (12,000 + 15,000 = 27,000/-) there is a contravention.

Section 269T - Mode of repayment of certain loans or deposits:

Applicability:This section applies to all the persons i.e. individual, HUF, Company (including branch of the banking company), Partnership firm, AOP/BOI, Local authority, Co-operative society, Trust, AJP.

Provision:

3 4The repayment, by any person, of any loan or deposit or specified advance , made with it, should not be done in any mode apart from account payee cheque or account payee bank draft drawn in the name of the person or by use of electronic clearing system through a bank account who has made the loan or deposit, if:

a) The amount of loan or deposit or specified advance along with any interest, if any payable on such loans or deposit is Rs. 20,000 or more or

3 "loan or deposit" means any loan or deposit of money which is repayable after notice or repayable after a period and, in the case of a person other than a company, includes loan or deposit of any nature

4 “specified advance" means any sum of money in the nature of advance, by whatever name called, in relation to transfer of an immovable property, whether or not the transfer takes place

11 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

b) As on the date of repayment, if there exists any other loan or deposits held by the person either in his own name or jointly with any other person, the aggregate amount of such loans or deposit together with interest, if any payable on such loans or depositis Rs. 20,000 or more or

c) In case of specified advances received by such person either in his own name or jointly with any other person, the aggregate of such specified advances along with any interest payable on such specified advances is Rs. 20,000 or more

The repayment made by a branch of a banking company or co-operative bank, of such loan / deposit, can also be made by crediting the amount to the savings bank account or to the current bank account held with the branch.

Cases where the above provisions do not apply:

The provisions of this section does not apply to in case the loan / deposit has been taken / made by the following persons:

- Government;- any banking company, post office savings bank or cooperative bank;- any corporation established by a Central, State or Provincial Act;- any Government company as defined in section 617 of the Companies Act, 1956 (1 of 1956) ;- such other institution, association or body or class of institutions, associations or bodies which the

Central Government may, for reasons to be recorded in writing, notify in this behalf in the Official Gazette.

Penalty for failure to comply with section 269T:

As per Section 271E of the Income tax act, 1961 if a person fails to comply with Section 269T then the Joint Commissioner shall charge a sum by way of penalty equal to the amount of the loan or deposit or specified sum so repaid.

Example:

Mr. A holds the following accounts with ABC Ltd, a banking company:

Account 1: FD of Rs. 10,000; interest payable Rs. 1,250Account 2: FD of Rs. 8,750 interest payable Rs. 1,120

ABC Ltd repays the amount of FD along with the applicable interest payable on such FD to Mr. A, in a mode other than account payee cheque or account payee bank draft. Will there be any contravention of the provisions of section 269T?

On a plain understanding of the section, one would assume that since only Rs. 11,250 is being paid to Mr. A,

Co

mp

anie

s Act

Sectio

n 2

69

SS & 2

69

T

"What we think, we become" - Buddha

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

Md. Sameer Hussain,

TAXABILITY OF PROVIDENT FUND

Contributed byA. Sai Krishna Reddy & Vetted by CA Ram Prasad

12 | P a g e

INCOME TAX ACT, 1961

SBS Interns' Digest www.sbsandco.com/digest

Types of Provident Fund:

• Recognised Provident Fund;• Unrecognised Provident Fund;• Statutory Provident Fund; and• Public Provident fund.

Provident Fund:

The Act that governs Provident fund in India is the Employees Provident Fund and Miscellaneous Provisions Act, 1952. Provident fund is a scheme where by employer and / or employee will contribute to an investment fund. The amount invested in the fund can be withdrawn after a specified time or after attaining specific age.

Employee ContributionFund Details Employer Contribution

For salaried individuals (approved by commissioner of Income Tax)

For salaried individuals (Not recognised by commissioner of Income Tax)

For government employees, university employees

For general public

Yes

Yes

Yes

Yes

Yes

Yes

Optional

Not applicable (as there will be no employer)

RPF

URPF

SPF

PPF

Note: The major difference between URPF and PPF is that, URPF is not recognised by the government. Whereas PPF is recognised by the government.

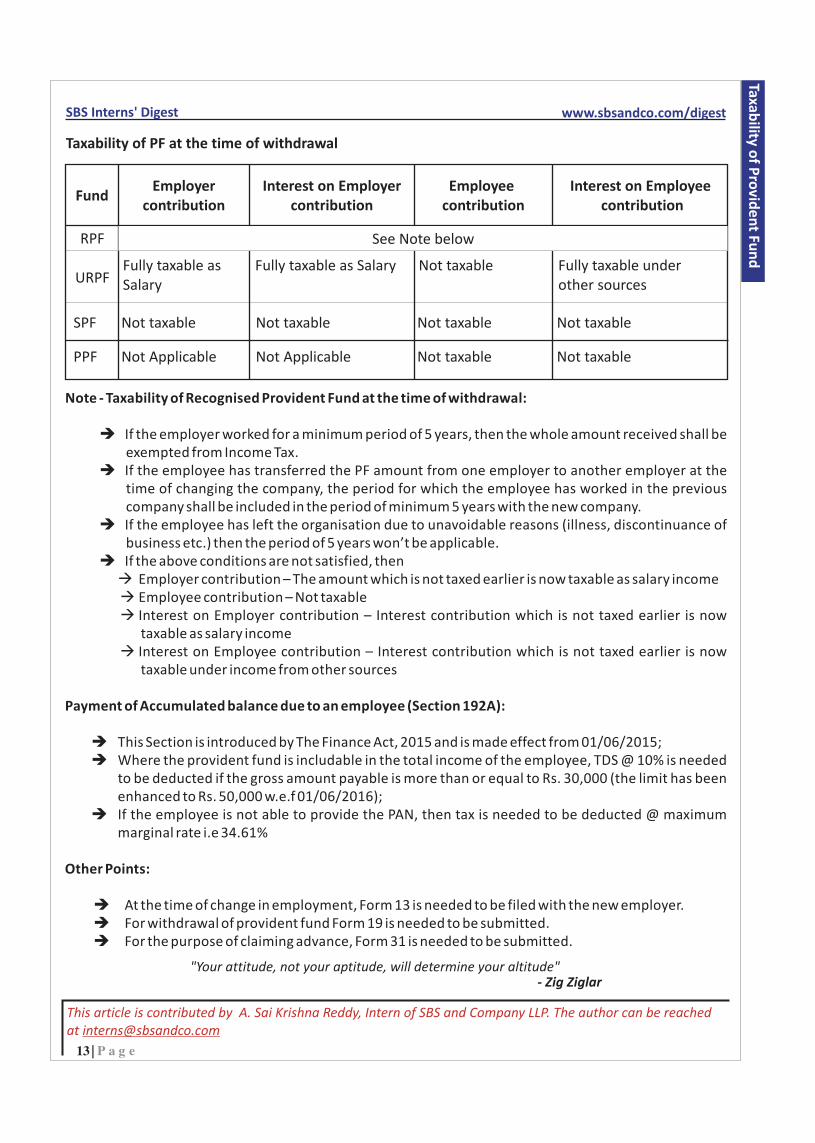

Taxability of PF at the time of contribution

Interest on contributionFund Employer contribution Employee contribution

1RPF Exempt upto 12% of Salary Deduction u/s 80C is available Exempt upto 9.5% pa

URPF Not taxable No deduction is available Not taxable

SPF Not taxable Deduction u/s 80C is available Not taxable

PPF Not Applicable Deduction u/s 80C is available Exempt upto 9.5% pa

1Salary = Basic Salary + Dearness Allowance

Co

mp

anie

s Act

Taxability o

f Pro

vide

nt Fu

nd

13 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Interest on Employee contribution

FundEmployer

contributionInterest on Employer

contributionEmployee

contribution

See Note belowRPF

Fully taxable as Salary

Fully taxable as Salary Not taxable Fully taxable under other sources

SPF Not taxable Not taxable Not taxable Not taxable

PPF Not Applicable Not Applicable Not taxable Not taxable

URPF

Taxability of PF at the time of withdrawal

Note - Taxability of Recognised Provident Fund at the time of withdrawal:

èIf the employer worked for a minimum period of 5 years, then the whole amount received shall be exempted from Income Tax.

èIf the employee has transferred the PF amount from one employer to another employer at the time of changing the company, the period for which the employee has worked in the previous company shall be included in the period of minimum 5 years with the new company.

èIf the employee has left the organisation due to unavoidable reasons (illness, discontinuance of business etc.) then the period of 5 years won’t be applicable.

èIf the above conditions are not satisfied, thenàEmployer contribution – The amount which is not taxed earlier is now taxable as salary incomeàEmployee contribution – Not taxableàInterest on Employer contribution – Interest contribution which is not taxed earlier is now

taxable as salary incomeàInterest on Employee contribution – Interest contribution which is not taxed earlier is now

taxable under income from other sources

Payment of Accumulated balance due to an employee (Section 192A):

èThis Section is introduced by The Finance Act, 2015 and is made effect from 01/06/2015;èWhere the provident fund is includable in the total income of the employee, TDS @ 10% is needed

to be deducted if the gross amount payable is more than or equal to Rs. 30,000 (the limit has been enhanced to Rs. 50,000 w.e.f 01/06/2016);

èIf the employee is not able to provide the PAN, then tax is needed to be deducted @ maximum marginal rate i.e 34.61%

Other Points:

èAt the time of change in employment, Form 13 is needed to be filed with the new employer.èFor withdrawal of provident fund Form 19 is needed to be submitted.èFor the purpose of claiming advance, Form 31 is needed to be submitted.

"Your attitude, not your aptitude, will determine your altitude" - Zig Ziglar

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

A. Sai Krishna Reddy,

VOUCHING OF CASH AND BANK TRANSACTIONS

Contributed by P. Ashok Reddy & Vetted by CA Sandeep Das

14 | P a g e

AUDIT

SBS Interns' Digest www.sbsandco.com/digest

1. What is meant by Vouching

ØVouching is a process of checking the vouchers related to the transactions recorded in the books of accounts.

ØVouching is the essence of the Auditing. The object of vouching is to Gain assurance regarding the existence assertion.

ØVouching tracks a result backward to the originating event, ensuring that a recorded amount is properly supported.

2. Points to should be considered while Vouching

ØArranged Voucher: All the voucher should be consecutively arranged and Pre-numbered cash vouchers should be used.

ØChecking of Date:The date of the voucher falls within the accounting period.

ØChecking of authority: Voucher should be authorized as per internal policy framed by the organisation.

ØCutting and Change: There should be no changes in the voucher. Any person for making the fraud can change the time, amount, date and name concern. So, this changes can't be acceptable till the approval authority has made the signature for that changes.

ØCompare the Words and Figures: The auditor should satisfy himself amount written on the voucher, it figures and words are same or not.

ØTransaction must relate to Business: The transaction should relate only to the business aspects of the organization and transactions of personal nature should not be recorded.

ØChecking of Head of Account: Auditor must be satisfied about the head of account in which cash received or paid. The transactions should be clearly classified into revenue or capital transactions and accordingly entered in the books of accounts.

ØCancelled Voucher’s: The auditor should not accept the cancelled vouchers. In this cases there will be a chances of double payments.

Check list for vouching of Cash & Bank Transactions

1. Internal check System : Steps should involve in the verification of Internal Control System,

ØReview the Segregation of DutiesØExamine the financial power vested in the different persons and conditions under which they

exercise them.ØSegregation Duties: Segregation of duties is a key internal control in any organisation. The

purpose of this segregation of duties is to minimize the opportunity for an employee to misappropriate funds and avoid detection.

Co

mp

anie

s Act

Vo

uch

ing o

f Cash

and

Ban

k Transactio

ns

15 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Cash handling duties can be divided into four stages:

o Custody. O Recordingo Authorization O Reconcilingo Depositing

2. Documentary Evidence of Transactions: Examine all the vouchers with the appropriate documentary evidence. Documentary Evidence is of two types,

ØInternal Evidence : Created and used and retained within the organization ØExternal Evidence:Originate outside the client’s organization. Examples: Bank Statement,

Supplier Invoice, Insurance policies, etc.

Points should be considered while verifying the evidence:

vDatevName and Address vAmountvPeriodvEntry in the books of accounts

3. Examine the Method of Depositing Cash Receipts Daily: Examine the method adopted for depositing daily cash receipts in bank. The pay in slip should invariably be used for this purpose.

4. Verification of Cash in Hand: Verify the cash in hand by actually counting it and see whether it agrees with cash book balance.

5. Revenue Stamps: The stamps are required according to the valuation of the amount and cash memo. For the stamps, The stamps Act, 1899 is applicable while fixing the revenue stamps. Ensure that cash payments exceeding Rs.5000/- should be supported by a revenue stamp.

6. Petty Cash Transactions:

ØUnderstanding Imprest petty cash fund system in existence to control petty cash.ØVerify the Pre-numbered petty cash vouchers should be used for withdrawing cash from the

fund and same should be supported by appropriate bills.ØEnsure that limit should be placed on the size of reimbursements.

7. Opening Balance Verification: Match the opening balance of the Cash & Bank Balances as reflected in the Cash Book with the closing balance as per the audited financials of the previous year. In case of any discrepancy in the amounts, the same is to be noted and clarification is required from the Management.

8. Balance Confirmations from Banks: Cross check bank balances as per books with confirmations received from banks.

16 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

9. Verification of Bank Reconciliation statements:

ØCheck that Bank reconciliation statements in respect of all the bank accounts are prepared on a monthly basis.

ØCheck that the entries appearing in the Bank reconciliation statements are cleared in the subsequent month.

ØCheck that entries relating to cheques issued but not presented for payment for more than 6 months are reversed

10. During verification, the following points are also to be taken care of:

ØEnsure that there is no unrecorded cash.ØAuthorization of cheques is made as per the delegation.ØCheck that payments are made only against original supporting.ØCheck that cheque books / counter foils are kept in safe custody.

Generally the below frauds are identified while vouching of cash & bank transactions,

ØTeaming and Lading ØTheft of cashØCash received is not brought to accountØPayments are illegally transferred or diverted by making duplicate payments, paying the wrong

person, or by increasing the value of one payment at the expense of another.ØInvoices are falsified or duplicated in order to generate a false payment

"Don't go through life, grow through life"

- Eric Butterworth

Co

mp

anie

s Act

Vo

uch

ing o

f Cash

and

Ban

k Transactio

ns

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

P. Ashok Reddy,

SA 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS

Contributed by G. Chandrashekar & Vetted by CA Sandeep Das

17 | P a g e

AUDIT

SBS Interns' Digest www.sbsandco.com/digest

Scope:

a. This Standard on Auditing(SA) deals with auditor’s responsibility to plan an audit of financial statements

b. It is framed in the context of recurring auditsc. Additional considerations in initial audit engagements are separately identified

Objective: The objective of the auditor is to plan the audit so that it will be performed in an effective manner.

stEffective Date: This SA is effective for audits of financial statements for periods beginning on or after 1 April 2008.

Requirements:

1. Involvement of Key Engagement Team Members,2. Preliminary Engagement Activities,3. Planning Activities,4. Documentation, and5. Additional Considerations in Initial Audit Engagements.

1. Involvement of Key Engagement Team Members: The involvement of engagement member and other key members of the engagement team in planning the audit

To be involved in planning

üParticipate in discussion with audit teamüBenefit of their experience and insightüIncreases effectiveness and efficiency of planning

SA315 also contains a requirement for discussion with the audit team as to the susceptibility of the financial statements of the entity to material misstatements.

Revised SA240 also contains a requirement for discussion among audit team as to susceptibility of the financial statements to fraud

2. Preliminary Engagement Activities:

üPerform procedures required under SA 220, “Quality Control for an Audit of Financial Statements” regarding the continuance of the client relationship and the specific audit engagement

Co

mp

anie

s Act

SA 3

00

Plan

nin

g an A

ud

it of Fin

ancial State

me

nts

18 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

üEvaluate compliance with ethical requirements, including independence, as required by SA 220 and

üEstablish an understanding of the terms of the engagement as per SA 210, “Agreeing the Terms of Audit Engagement”

3. Planning Activities: Nature and extent of planning activitiesvary according to

üSize and complexity of the entityüKey engagement team member’s previous experienceüChanges in circumstances

Planning Activities include:

üEstablish an overall audit strategyüDeveloping audit plan

Considerations in developing an audit strategy

üDetermine the characteristics of the engagementüKnowledge of the businessüUnderstanding of the accounting and internal control systemsüRisk and materialityüNature, timing and extent of proceduresüCoordination, direction, supervision and review

Contents of audit plan

Audit plan is more detailed than the overall strategy which includes :

üNature, timing & extent of risk assessment proceduresüNature, timing & extent of planned further audit procedures at assertion levelüOther procedures required to comply with Sas

Need to update audit plan

üUnexpected events,üChanges in circumstances,üAudit evidence obtained from the results of audit procedures, and üInformation comes to the auditor’s attention that differs significantly from the information

available when the auditor planned the audit procedures

19 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

4. Documentation: The auditor shall document

üThe overall audit strategy,üThe audit plan, andüAny significant changes made during the audit engagement to the overall audit strategy or the

audit plan, and the reasons for such changes.

5. Additional Considerations in Initial Audit Engagements: Before starting initial audit engagement:

üPerform procedures required under revised SA220–client acceptanceüCommunicating with predecessor auditor.

Benefits:

üAttention is devoted to major areasüAssists in selection of engagement teamüAssists in proper assignment of work to assistantsüPotential problems are identified and resolvedüWork is performed in an efficient, effective and timely manner

Direction, Supervision and Review:

The nature, timing and extent of the direction and supervision of engagement team members and review of their work vary depending on many factors, including:

vThe size and complexity of the entityvThe area of the audit.vThe assessed risks of material misstatementvThe capabilities and competence of the individual team members performing the audit work.

Considerations Specific to Smaller Entities:

When an audit is carried out entirely by the engagement partner, questions of direction and supervision of engagement team members and review of their work do not arise. In such cases, the engagement partner, having personally conducted all aspects of the work, will be aware of all material issues.

Forming an objective view on the appropriateness of the judgments made in the course of the audit can present practical problems when the same individual also performs the entire audit. When particularly complex or unusual issues are involved, and the audit is performed by a sole practitioner, it may be desirable to consult with other suitably-experienced auditors or the auditor’s professional body.

The toughest thing about success is that you've got to keep on being success

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

G. Chandrashekar,

Co

mp

anie

s Act

SA 3

00

Plan

nin

g an A

ud

it of Fin

ancial State

me

nts

20 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Rule 5 of CENVAT Credit Rules, 2004 (for brevity ‘Rule 5 of CCR’) provides for refund of accumulated CENVAT credit of inputs and input services used in relation to the goods/services exported, to a manufacturer/service provider subject to certain safeguards and conditions as prescribed in Notification No.27/2012 – CE (N.T.) as amended. The notification provides for time limit for filing of refund claims.

This article aims to through light on the confusion/misinterpretation by certain authorities surrounding the time limit issue that was put to end through recent amendment in the notification.

Position prior to 1st March 2016 (i.e. before amendment of Notification 27/2012-CE(NT)):

Notification no 27/2012—CE (NT) specifies that the refund claims under rule 5 should be made before period of expiry specified in section 11B of the Central Excise Act, 1944(for brevity ‘Sec 11B’ of CX).

Sec 11B deals with period of limitation with respect to refund claim of excise duty and interest. It states that the refund claim should be made before the expiry of one year from the relevant date. The relevant date has been defined in the explanation to the rule which is as follows:

"relevant date" means, -

(a) in the case of goods exported out of India where a refund of excise duty paid is available in respect of the goods themselves or, as the case may be, the excisable materials used in the manufacture of such goods, -

(i) if the goods are exported by sea or air, the date on which the ship or the aircraft in which such goods are loaded, leaves India, or

(ii) if the goods are exported by land, the date on which such goods pass the frontier, or (iii) if the goods are exported by post, the date of despatch of goods by the Post Office concerned to a

place outside India; . . . (f) in any other case, the date of payment of duty

Thus, there is no relevant clause in the definition of relevant date which provides for relevant date in case of accumulated CENVAT credit.

This lead to various doubts in the trade and department resulting in the following standpoints:

st1 School of thought:

Sec 11B deals with time limit for filing refund claim of excise duty (and service tax by virtue of Sec 83 of Finance Act 1994) and interest thereof. Accumulated CENVAT Credit due to exports loses the character of tax. It is a cash amount due by Government to exporter.

Contributed by P.Uday Kumar & Vetted by CA Manindar K

APPLICABILITY OF LIMITATION PERIOD VIS-À-VIS REFUND CLAIM UNDER RULE 5 OF CENVAT CREDIT RULES 2004

INDIRECT TAX

Co

mp

anie

s Act

Refu

nd

claim u

nd

er R

ule

5 o

f CEN

VA

T Cre

dit R

ule

s 20

04

SBS Interns' Digest www.sbsandco.com/digest

Sec 11B does not provide for the relevant date from which the one year time limit is to be counted, for refund claim of accumulated CENVAT credit. Thus, time limit specified in Sec 11B does not apply to refund claim under rule 5.

Allahabad High Court opined that said time limit is not applicable (Elcomponics Sales Pvt Ltd case)

nd2 School of Thought:

Since the notification 27/2012 specifically provides for applicability of time limit as per Sec 11B, it cannot be said that time limit as per Sec 11B does not apply to refund claims under rule 5.

Upon harmonious reading of the notification and the section, it can be said that the relevant date in case of refund under rule 5 is date of export. This view has been taken by the Madras High Court in the case of Commissioner of Central Excise, Coimbatore v. GTN Engineering (I) Ltd.

Now, coming to what exactly is date of export in case of export of service has been interpreted differently. They are:

Viewpoint 1: Services to be considered as exported, the proceeds need to be realised in foreign currency as per rule 6A of Service Tax Rules, 1994. Also, Notification 27/2012 requires the claim to be filed with relevant BRCs so as to establish the realisation of proceeds in foreign currency. Thus, the export of services is complete only on realisation of proceeds and hence, is the date of export from which the one year time period applies.

Viewpoint 2: Services are exported as soon as the invoice is raised and condition of receipt of proceeds is only a condition to ensure realisation of foreign currency. Thus, date of export invoice is the date of export from which the time limit applies.

These diverged viewpoints lead to confusion with respect of time limit for refund claim under rule 5Amendment of Notification 27/2012-CE(NT) w.e.f. 1.03.2016:

To clear up the confusion and to speed up the processing of claims, the notification has been amended vide notification no. 14/2016-CE (NT) which can be summarised as follows:

The refund claim has to be filed:

• In case of manufacturer-before expiry of period as specified in Sec 11B of Central Excise.• In case of Service provider, before the expiry of one year from the date of –

üReceipt of payment in convertible foreign exchange, where service has been provided prior to such receipt of payment;

üIssue of invoice, where payment has been received in advance prior to issue of invoice.

Thus, the misinterpretation by authorities of the above provision of time limit has been put to an end.

21 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

Remarks:

ØComing to the point that whether time limit as per Sec 11B is actually applicable to refund claim, before the amendment to the notification, Section 11B is applicable for claim of duty/tax. But refund filed on account of balance accumulated CENVAT Credit due to exports is a cash incentive extended by Central Government losses the character of tax. It is a cash amount due by Government to exporter.

Thus, Sec 11B has no relevance with respect to refund claim of accumulated CENVAT credit. As Rule 5 is intended to achieve zero rating of exports, one may explore the possible application of general limitation under Limitation Act if not the limitation specified under section 11B.

ØEven if time limitation is applicable prior to amendment, it can be said that there was no ambiguity with respect to the export point of time from which the limitation period is to be calculated i.e. whether date of invoice or date of realisation of proceeds constitute the date of export. It can be only mis- interpretation by authorities but not ambiguity in the law.

A service is said to be exported only when the proceeds are realised in foreign currency, non-receipt of the same would make the services being treated as unexported. This can also be established through the method specified for calculation of export turnover as per rule 5 of CCR, whereby turnover is nothing but the payments received pertaining to the relevant period of refund claim.

Also, in the case of foreign currency being received in advance and invoices are raised setting off the against advance received, there could not be any confusion as – Export cannot be materialised just because foreign exchange is received, but only when the actual service is provided and the export invoice being raised.

Concluding words:

It is the policy of the country that exports should be zero rated. No taxes should be exported. This is for the larger interest of the country for boosting the economy. Compared to this time limit should be of less importance. Many practical constraints have led to belated filing of refund claims like FIRCs/BRCs/STPI certifications etc.

Further to add; an exporter who is having domestic and export turnover, may use his accumulated CENVAT Credit at any point of time for set-off against his output liability. When there is no time restriction on utilization of credit relating to exports, how far it is prudent to impose such restriction for claiming refund of such credit in case of exporters who do not have domestic turnover and are forced to file refund claim in order to get their exports zero-rated.

Thus, in order to protect the greater objective of not to export taxes, the technical issues like time limit should be given less/no consideration in genuine cases where eligibility of refund claim is established beyond doubt.

"If everyone is moving forward together, then success takes care of itself” - Heny Ford

Co

mp

anie

s Act

Refu

nd

claim u

nd

er R

ule

5 o

f CEN

VA

T Cre

dit R

ule

s 20

04

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

P.Uday Kumar,

22 | P a g e

Contributed by P. Visweshwar Rao & Vetted by CA Murali Krishna G

SBS Interns' Digest www.sbsandco.com/digest

Introduction about Compounding

Contravention is a breach of the provisions of the Foreign Exchange Management Act (FEMA), 1999 and rules/ regulations/ notification/ orders/ directions/ circulars issued there under. Compounding refers to the process of voluntarily admitting the contravention, pleading guilty and seeking for remedy. The Reserve Bank is empowered to compound any contraventions as defined under section 13of FEMA, 1999 except the contravention under section 3(a), for a specified sum after offering an opportunity of personal hearing to the contravener. It is a voluntary process in which an individual or a corporate seeks compounding of an admitted contravention.

Persons eligible for compounding

Any person who contravenes any provision of the FEMA, 1999 [except section 3(a)] or contravenes any rule, regulation, notification, direction or order issued in exercise of the powers under this Act or contravenes any condition subject to which an authorization is issued by the Reserve Bank, can apply for compounding to the RBI.

Time limit to apply for compounding

Any contravention under section 13 may, on an application made by the person committing such contravention, be compounded within one hundred and eighty days from the date of receipt of application by the Director of Enforcement or such other officers of the Directorate of Enforcement and officers of the Reserve Bank.One can also make an application for compounding, voluntarily, on becoming aware of the contravention.

I. The guidance structure for calculating the amount to be imposed on compounding is as given below:

23 | P a g e

FEMA

COMPOUNDING OF CONTRAVENTIONS UNDER FEMA

Co

mp

anie

s Act

Co

mp

ou

nd

ing o

f Co

ntrave

ntio

ns u

nd

er FEM

A

SBS Interns' Digest www.sbsandco.com/digest

FormulaType of contravention

1) Reporting ContraventionsA) FEMA 20i. Para 9(1)(A) (Delay in reporting inward remittance for issue of shares)ii. Paragraph 9(1)(B) (Delay in filing form FC(GPR) after issue of shares)iii. Regulation 4(Taking on record transfer of shares by investee company, in the absence of certified from FC-TRS).iv. FCTRS (Reg. 10)(Delay in submission of form FC-TRS on transfer of shares from Resident to Non-Resident or Non-resident to resident).v. Part B of FC(GPR)B) FEMA 3Non submission of ECB statementsC) FEMA 120N o n r e p o r t i n g / d e l a y i n r e p o r t i n g o f acquisition/setup of subsidiaries/step down subsidiaries /changes in the shareholding patternD) Any other reporting contraventions (except those in Row 2 below)

E) Reporting contraventions by LO/BO/PO

Fixed amount: Rs10,000/- (applied once for each contravention in a compounding application) +

Variable amount as under:

Upto 10 lakhs: 1,000 per yearRs.10-40 lakhs: 2,500 per yearRs.40-100 lakhs: 7,000 per yearRs.1-10 crore: 50,000 per yearRs.10-100 Crore: 1,00,000 per yearAbove Rs.100 Crore: 2,00,000 per year

As above, subject to ceiling of Rs.2 lakhs. In case of Project Office, the amount of contravention shall be @10% of total project cost.

2) AAC/ APR/ Share certificate delaysIn case of non-submission/ delayed submission of APR/ share certificates (FEMA 120) or AAC (FEMA 22) or FCGPR (B) Returns (FEMA 20)

Rs.10000/- per AAC/APR/FCGPR (B) Return delayed.

Delayed receipt of share certificate – Rs.10000/- per year, the total amount being subject to ceiling of 300% of the amount invested.

3) A) Allotment/RefundsPara 8 of FEMA 20/2000-RB (non-allotment of shares or allotment/ refund after the stipulated 180 days)

B) LO/BO/PO (Other than reporting contraventions)

Rs.30000/- + given percentage: 1styear : 0.30%1-2 years : 0.35%2-3 years : 0.40%3-4 years : 0.45%4-5 years : 0.50%>5 years : 0.75%(For project offices the amount of contravention shall be deemed to be 10% of the cost of project).

24 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

FormulaType of contravention

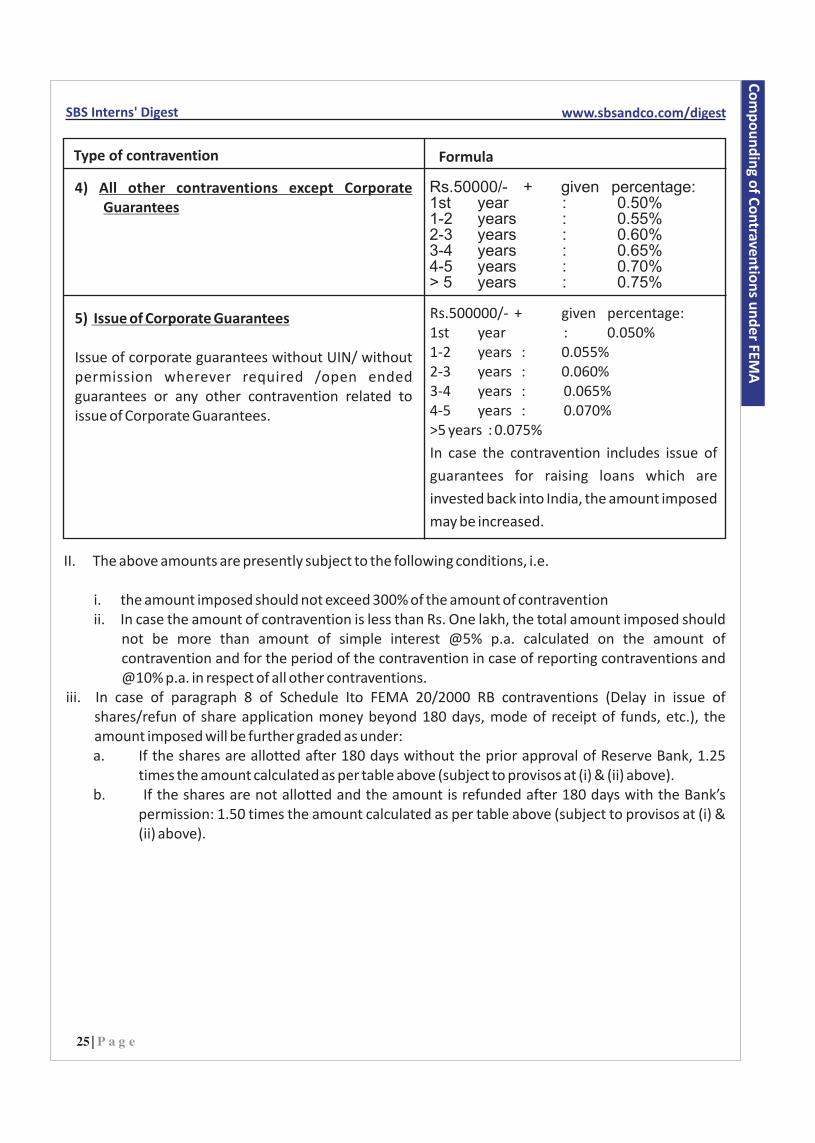

4) All other contraventions except Corporate Guarantees

Rs.50000/- + given percentage:1st year : 0.50%1-2 years : 0.55%2-3 years : 0.60%3-4 years : 0.65%4-5 years : 0.70%> 5 years : 0.75%

5) Issue of Corporate Guarantees

Issue of corporate guarantees without UIN/ without permission wherever required /open ended guarantees or any other contravention related to issue of Corporate Guarantees.

Rs.500000/- + given percentage:1st year : 0.050%1-2 years : 0.055%2-3 years : 0.060%3-4 years : 0.065%4-5 years : 0.070%>5 years : 0.075%

In case the contravention includes issue of

guarantees for raising loans which are

invested back into India, the amount imposed

may be increased.

II. The above amounts are presently subject to the following conditions, i.e.

i. the amount imposed should not exceed 300% of the amount of contraventionii. In case the amount of contravention is less than Rs. One lakh, the total amount imposed should

not be more than amount of simple interest @5% p.a. calculated on the amount of contravention and for the period of the contravention in case of reporting contraventions and @10% p.a. in respect of all other contraventions.

iii. In case of paragraph 8 of Schedule Ito FEMA 20/2000 RB contraventions (Delay in issue of shares/refun of share application money beyond 180 days, mode of receipt of funds, etc.), the amount imposed will be further graded as under:a. If the shares are allotted after 180 days without the prior approval of Reserve Bank, 1.25

times the amount calculated as per table above (subject to provisos at (i) & (ii) above).b. If the shares are not allotted and the amount is refunded after 180 days with the Bank’s

permission: 1.50 times the amount calculated as per table above (subject to provisos at (i) & (ii) above).

Co

mp

anie

s Act

Co

mp

ou

nd

ing o

f Co

ntrave

ntio

ns u

nd

er FEM

A

25 | P a g e

SBS Interns' Digest www.sbsandco.com/digest

c. If the shares are not allotted and the amount is refunded after 180 days without the Bank’s permission: 1.75 times the amount calculated as per table above (subject to provisos at (i) & (ii) above).

iv. In cases where it is established that the contravenor has made undue gains, the amount thereof may be neutralized to a reasonable extent by adding the same to the compounding amount calculated as per chart.

v. If a party who has been compounded earlier applies for compounding again for similar contravention, the amount calculated as above may be enhanced by 50%.

III. For calculating amount in respect of reporting contraventions under para I.1 above, the period of contravention may be considered proportionately {(approx. rounded off to next higher month ÷ 12) X amount for 1 year}. The total no. of days includes Sundays/holidays.

Co

mp

anie

s Act

Co

mp

ou

nd

ing o

f Co

ntrave

ntio

ns u

nd

er FEM

A

This article is contributed by Intern of SBS and Company LLP. The author can be reached at [email protected]

P. Visweshwar Rao,

"A person with a new idea is a crank until the idea succeeds”

- Mark Twain

26 | P a g e

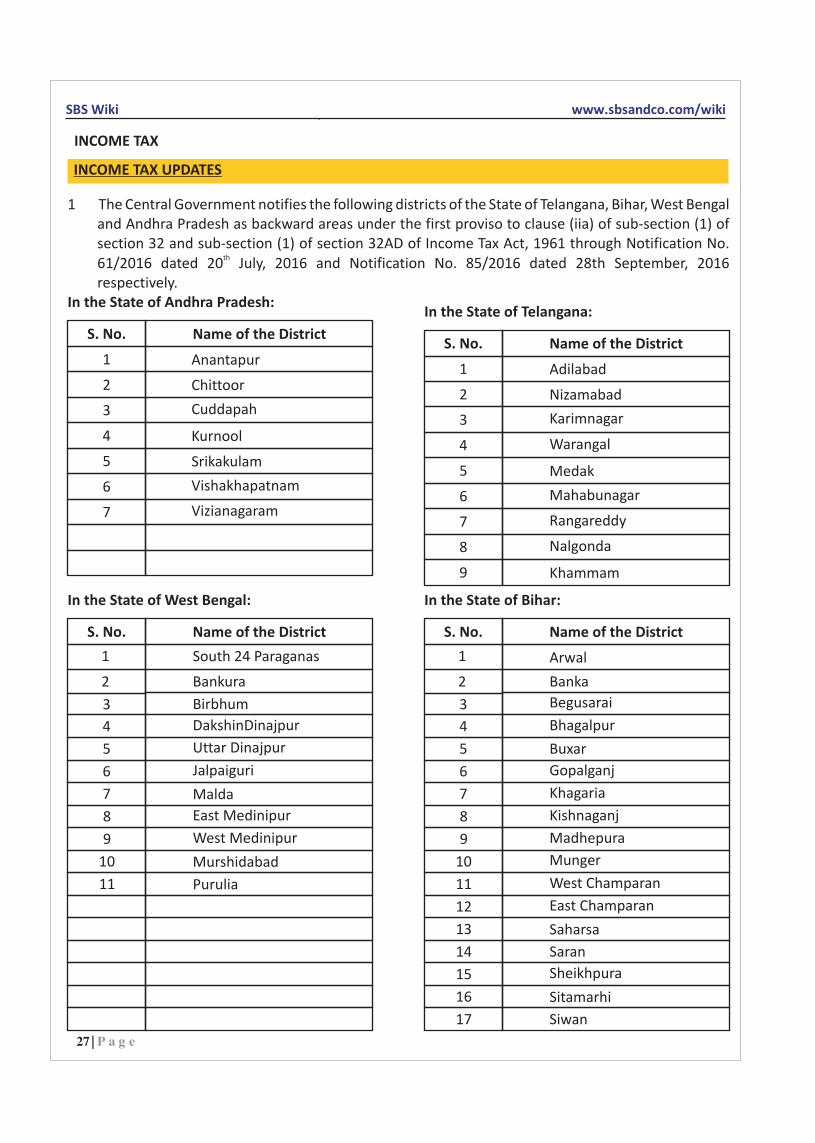

1 The Central Government notifies the following districts of the State of Telangana, Bihar, West Bengal and Andhra Pradesh as backward areas under the first proviso to clause (iia) of sub-section (1) of section 32 and sub-section (1) of section 32AD of Income Tax Act, 1961 through Notification No.

th61/2016 dated 20 July, 2016 and Notification No. 85/2016 dated 28th September, 2016 respectively.

INCOME TAX UPDATES

S. No.

1

2

3

4

5

6

7

Name of the District

Anantapur

Chittoor

Cuddapah

Kurnool

Srikakulam

Vishakhapatnam

Vizianagaram

In the State of Andhra Pradesh:

S. No.

1

2

3

4

5

6

7

8

9

Name of the District

In the State of Telangana:

Adilabad

Nizamabad

Karimnagar

Warangal

Medak

Mahabunagar

Rangareddy

Nalgonda

Khammam

In the State of West Bengal:

S. No. Name of the District

1

2

3

4

5

6

7

8

11

10

9

South 24 Paraganas

Bankura

Birbhum

DakshinDinajpur

Uttar Dinajpur

Jalpaiguri

Malda

East Medinipur

West Medinipur

Murshidabad

Purulia

In the State of Bihar:

S. No. Name of the District

1

2

3

4

5

6

7

8

11

14

16

15

17

13

12

10

9

Arwal

Banka

Begusarai

Bhagalpur

Buxar

Gopalganj

Khagaria

Kishnaganj

Madhepura

Munger

West Champaran

East Champaran

Saharsa

Saran

Sheikhpura

Sitamarhi

Siwan

SBS Wiki www.sbsandco.com/wiki

27 | P a g e

INCOME TAX

28 | P a g e

Co

mp

anie

s Act

Inco

me

Tax Up

date

s

SBS Wiki www.sbsandco.com/wiki

S. No. Scenarios Original Due Date Extended Due Date

Form 15G/H received during the period from 01.10.2015 to 31.03.2016

Form 15G/H received during the period from 01.04.2016 to 30.06.2016

Form 15G/H received during the period from 01.07.2016 to 30.09.2016

Form 15G/H received during the period from 01.10.2016 to 31.12.2016

Form 15G/H received during the period from 01.01.2016 to 31.03.2016

30.06.2016

15.07.2016

15.10.2016

15.01.2016

30.04.2016

31.10.2016

31.10.2016

31.12.2016

15.01.2016

30.04.2016

1

2

3

4

5

2. If monthly maintenance charges are stipulated in the rent agreement to be paid by lessor / licencee /tenant, the same shall form part of rent for the purposes of computing annual value of the property. Where, however, the rent agreement stipulates that these charges shall be paid by the owner, it is obvious and reasonable to presume that the same is factored into the rent, fee or compensation payable by the lessee or the licencee. In that event the same cannot be added to the rent agreed to be paid. [Sunil Kumar Gupta Vs. Assistant Commissioner of Income-tax at High Court of Punjab & Haryana on September 27, 2016]

3. In exercise of the powers conferred by sub-section (2) of section 145 of the Income-tax Act, 1961, the Central Government rescinds the notification of the Government of India in the Ministry of Finance, Department of Revenue, published in the Gazette of India, Part-II, Section 3, Sub-section (ii), vide notification number S.O. 892(E) dated the 31st March, 2015, except as respects things done or omitted to be done before such rescission. And notifies the income computation and disclosure standards (ICDS) to be followed by all the Assessees (other than an individual or a Hindu undivided family who are not required to get their accounts of the previous year audited in accordance with the provisions of section 44AB of the said Act) following the mercantile system of accounting, for the purposes of computation of income chargeable to income-tax under the head “Profits and gains of business or profession” or “Income from other sources” from assessment year 2017-18 and subsequent assessment years. Accordingly, CBDT makes the Income Tax (23rd Amendment) Rules, for changes in Appendix II of Income-tax rules, 1962 [i.e., sub-clause (d) of clause (13) in Part-B of Form No. 3CD].

4. No deduction of Tax shall be made from payments of the nature specified in section 193 or 194A or 194-I of Income Tax Act, 1961 to TirumalaTirupatiDevasthanams, Tirupati, Andhra Pradesh as per Notification No. 81/2016 dated 9th September, 2016.

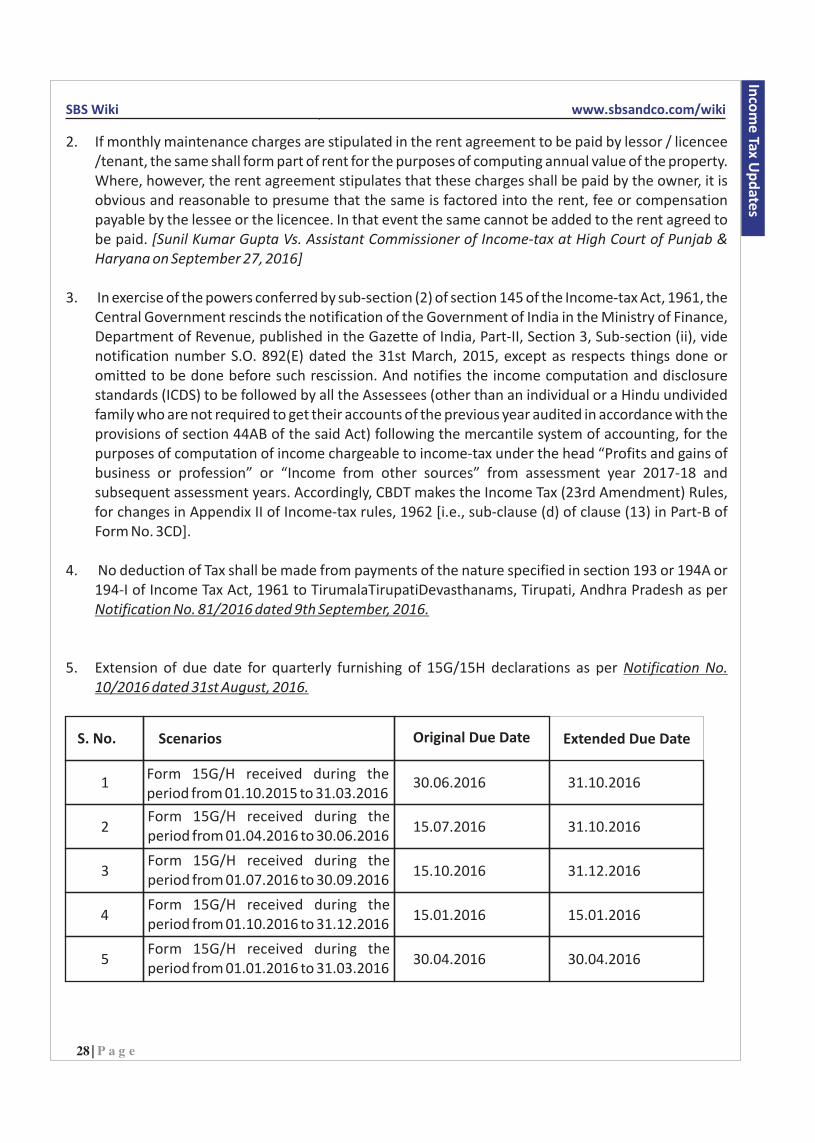

5. Extension of due date for quarterly furnishing of 15G/15H declarations as per Notification No. 10/2016 dated 31st August, 2016.

29 | P a g e

Co

mp

anie

s Act

Inco

me

Tax Up

date

s

SBS Wiki www.sbsandco.com/wiki

6. CBDT has issued an Order under Section 119 of the Income Tax Act, 1961 dated 9th September, 2016, whereby the due date of filing the IT return & Tax Audit report is extended to 17th October, 2016 for all Assessees who are liable to file the IT return on or before 30th September, 2016.

7. Generation of Electronic Verification Code (EVC) through ATM is now available which will be helpful for the assesses who have not availed facility of Internet banking. At present this option is enabled by SBI.

8. Generation of Electronic Verification Code (EVC) is enabled for online filing of appeal in Form 35 for taxpayers not required to file using DSC.

9. Online facility for filing Return of Income u/s 119(2)(b)/92CD has been enabled in e-filing portal (www.incometaxindiaefiling.gov.in).

These updates are contributed by B.Venkata Krishna and vetted by CA Ram prasad of SBS and Company LLP, Chartered Accountants. For any queries reach at [email protected]

1. Thirteenth Amendment to the Notification No. 20/2000 RB- Transfer of Issue of Security by a Person Resident Outside India

Prior to the amendment, Foreign Investment in the Other Financial Services require prior Approval of Government. In accordance with the amendment FDI is permitted as below with the conditions attached:

Sector % of FDI permitted Automatic/Approval

Automatic

Approval

Other Financial Services* 100%

Other Financial Services** 100%

*Financial services activities regulated by financial sector regulators**Financial Services not regulated or where only part is regulated or where there is doubt regarding the regulatory oversight

Other Conditions:

1. Subject to conditionalities including the minimum capitalization norms, as specified by the concerned Regulator/ Government Agency.

2. Any activity which is specifically regulated by an Act, the FDI will be restricted to the limits mentioned in the Act, if any

3. Downstream investments by any of the entities engaged in "Other Financial Services" will be subject to the extant sectoral regulations and provisions of Foreign Exchange Management (Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000, as amended from time to time.”

2. Revision to the Notification No. FEMA 5/2000-RB i.e., Foreign Exchange Management (Deposit) Regulations, 2000

In the exercise of the powers of the 6(3(f)) & 47(2) of Foreign Exchange Management Act, 1999, RBI has made Foreign Exchange Management (Deposit) Regulations, 2016 vide Notification No. FEMA 5(R)/2016-RBrelating to deposits between a person resident in India and a person resident outside India in supersession to the FEM (Deposit) Regulations, 2000. FEM (Deposit) Regulations, 2016 has come into force with effect from April 01, 2016 except the provisions of Regulation 7(2) (Para 6 (iii) above), which have come into effect from January 21, 2016.

With effect from April 01, 2016 FEM (Deposit) Regulations, 2000 has been replaced by FEM (Deposit) Regulations, 2016.

thGeneral Update: Mr. Urjit Patel has taken charge as Governor of RBI with effect from 4 September, 2016.

FEMA UPDATES

FEMA

SBS Interns' Digest www.sbsandco.com/digest

These updates are contributed by N. Supriya and vetted by CA Murali Krishna G of SBS and Company LLP, Chartered Accountants. For any queries reach at [email protected]

30 | P a g e

RULES, CIRCULARS AND NOTIFICATIONS ISSUED DURING THE MONTH OF SEPTEMBER, 2016

COMPANIES ACT, 2013

SBS Interns' Digest www.sbsandco.com/digest

RULES

vInvestor Education and Protection Fund Authority (Appointment of Chairperson and Members, holding of meetings and provision for offices and officers) Amendment Rules, 2016, Dt:05-09-2016.

Vide the above amendment rules, a new Rule 3-A, has been inserted, designating the nature of the Authority as prescribed in Rule-3 of the Principal rules. As per the amendment rules, the Authority under Rule-3, shall be a Body Corporate. Click the following link for the complete rules. Click here for the complete Rule

vInvestor Education and Protection Fund Authority (Accounting, Audit, Transfer and Refund) Rules, 2016,Dt:05-09-2016.

Vide the above rules, the Ministry has come with a set of rules/procedural aspects, relating to Accounting, Audit and Transfer and refund of the Investor Education and Protection Fund. Click the following link for the complete rules. Click here for the Complete Rule

vCompanies (Mediation and Conciliation) Rules, 2016, Dt:09.09.2016.

Pursuant to the provisions of Section 442 of Companies Act, 2013, rules have been notified. The rules provide forvarious procedural aspects relating to mediators or conciliators, their qualifications/disqualifications, procedure for the appointment disposal of the matters and related provisions. Click here for the Complete Rule

vThe Companies (Management and Administration) Amendment Rules, 2016, Dt:23.09.2016.

Vide the above amendment rules, certain provisions in the Companies (Management and Administration) Rules, 2014, have been further amended, relating to (a)Transfer of data from old register of members;(b)Omission of the requirement of submission of declarations under 89(1) & 89 (2) in duplicate;(c) Filing of MGT-10, in case of listed companies, where the change of shareholding position of the Promoters and top 10 shareholders, of the Company, amounts to 2% or more in entire paid-up share capital of company, within 15 days of such change;(d) conducting of EGM by requisitionists, on any day (including Sunday) but not on National holiday; (e) Listed companies and other companies having shareholders not less than 1000 members, to provide facility of e-voting to its members, and Nidhi Companies, satisfying the explanation given in the amendment rules, are not required to provide e-voting facility to its members even though it has more than 1000 members; (f)Omission of the Sub-rule (7) & (14) of Rule 22 of the Principal Rules, with reference to procedure for conducting business through Postal Ballot(g)Minutes of the General Meeting to be kept at the Registered office only; and (h)Notification of a new form MGT-6.Click here for the Complete Rule

31 | P a g e

Co

mp

anie

s Act

Tax Co

nse

qu

en

ces o

n Tran

sfer o

f Re

side

ntial H

ou

se P

rop

erty

SBS Interns' Digest www.sbsandco.com/digest

vThe Companies (Incorporation) Amendment Rules, 2016, Dt:01.10.2016.

Vide the above amendment rules, certain provisions in the Companies (Incorporation) Rules, 2014, have been further amended, relating to (a) Providing of a new Form No.INC-27, for filing the Order of the Tribunal along with a printed copy of the Articles of Association, within 15 days from the date of receipt of the Order from Tribunal, for effecting conversion of the Public Company into a Private Company(b) Introduction of a new Integrated form INC-32, for incorporation of a Company, along with e-MOA & e-AOA in form INC-33 & INC-34, to be effective from 02.10.2016; (c) Prescribing the procedure for conversion of a Company limited by Guarantee into a Company limited by Shares, with effect from 01.11.2016.Click here for theComplete Rule.

CIRCULARS

vGeneral Circular No.10/2016, Dt:07.09.2016:

Vide General Circular No.5, Ministry has given clarification with regard to relaxation for the additional fees for filing the Form IEPF-1Click here for the Circular

NOTIFICATIONS

vDesignation of Special Courts under section 435 of the Companies Act, 2013:

Ministry vide Notification Dt:01.09.2016, has designated the following courts as Special Courts, pursuant to Section 435 of the Companies Act, 2013, for the purpose of trial of offences punishable with imprisonment of 2 years or more. Extract of the notification is as below. Click here for the complete notification

JURISDICTION AS SPECIAL COURTEXISTING COURT

Sessions Judge, Bilaspur State of Chhattisgarh

Court of Special Judge, (Sati Niwaran), Jaipur State of Rajasthan

Court of Sessions Judge and 2nd Additional Sessions Judge,

Court of Sessions Judge and 2nd Additional Sessions Judge, Gurgaon

Court of Sessions Judge and 2nd Additional Sessions Judge, Chandigarh

I Additional District and Sessions Court, Coimbatore

II Additional District and Sessions Court, Puducherry

Sessions Judge, Imphal East

S.A.S. Nagar State of Punjab

State of Haryana

Union Territory of Chandigarh

Union Territory of Puducherry

State of Manipur

Districts of Coimbatore, Dharmapuri, Dindigul, Erode, Krishnagiri, Namakkal, Nilgiris, Salem and Tiruppur.

32 | P a g e

Co

mp

anie

s Act

Tax Co

nse

qu

en

ces o

n Tran

sfer o

f Re

side

ntial H

ou

se P

rop

erty

SBS Interns' Digest www.sbsandco.com/digest

vCommencement of various provisions relating to Investor Education and Protection Fund:

Vide above notification, the Ministry has notified that the provisions of Section 124 (1) to (4) & (6) and Section 125 (8) to (11), shall come in to effect from 07.09.2016.Click here for the notification

vCommencement of various provisions:

Vide above notification, the Ministry has notified that the provisions of section 227, clause (b) of sub-section (1) of section 242, clauses (c) and (g) of sub-section (2) of section 242, section 246 and sections 337 to 341 (to the extent of their applicability for section 246), of the said Act shall come into force with effect from 09.09.2016. Click here for the notification

vAmendment to the Schedule V of the Companies Act 2013

Vide Notification Dt: 12.09.2016, the Ministry has made the amendments to the Schedule V of the Act, with reference to Section-II of Part-II The amendment doubles the remuneration to the original Section-II of the Schedule-V. Click here for the notification.

vConstitution of National Advisory Committee on Accounting Standards:

Vide Notification Dt: 03.10.2016, the Ministry has notified the National Advisory Committee on Accounting Standards, to advise the Central Government on the formulation and laying down of accounting policies and accounting standards for the adoption by the Companies. Click here for the notification.

These updates are contributed by K. Bhavani and vetted by CS D V K Phanindra of SBS and Company LLP, Chartered Accountants. For any queries, please reach at [email protected]

33 | P a g e

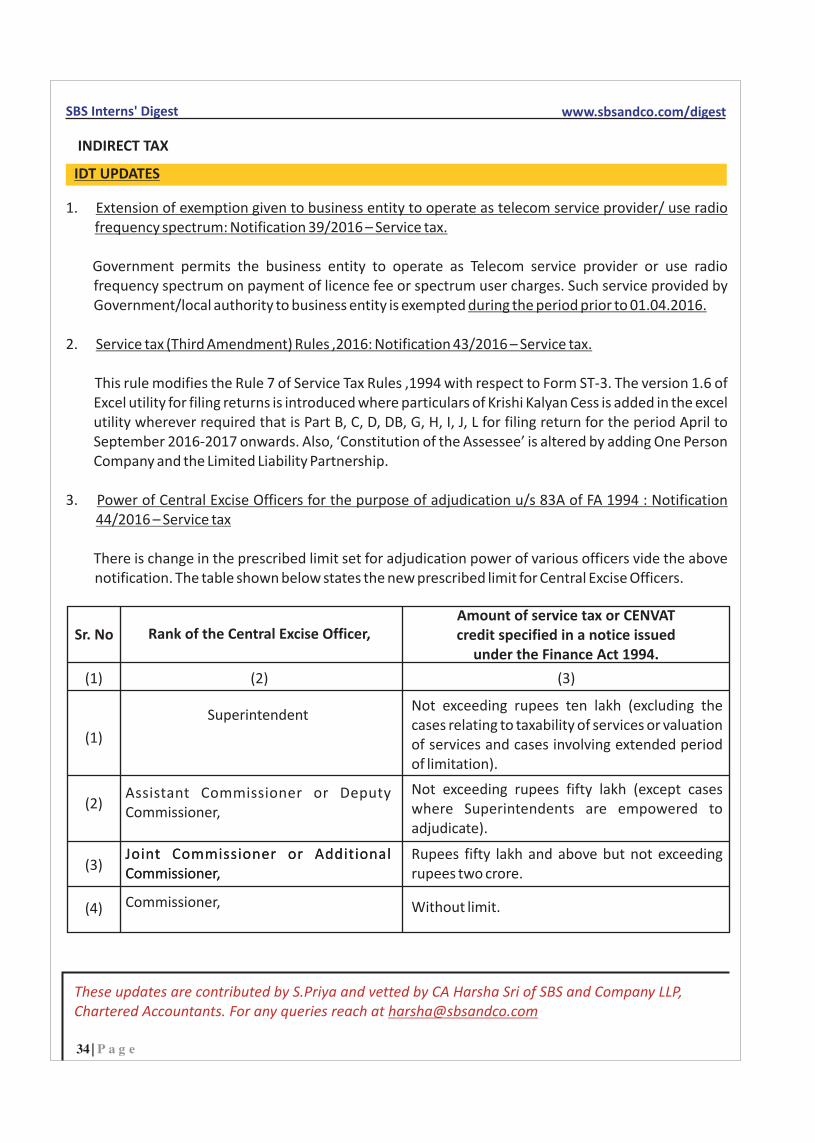

IDT UPDATES

INDIRECT TAX

SBS Interns' Digest www.sbsandco.com/digest

1. Extension of exemption given to business entity to operate as telecom service provider/ use radio frequency spectrum: Notification 39/2016 – Service tax.

Government permits the business entity to operate as Telecom service provider or use radio frequency spectrum on payment of licence fee or spectrum user charges. Such service provided by Government/local authority to business entity is exempted during the period prior to 01.04.2016.

2. Service tax (Third Amendment) Rules ,2016: Notification 43/2016 – Service tax.

This rule modifies the Rule 7 of Service Tax Rules ,1994 with respect to Form ST-3. The version 1.6 of Excel utility for filing returns is introduced where particulars of Krishi Kalyan Cess is added in the excel utility wherever required that is Part B, C, D, DB, G, H, I, J, L for filing return for the period April to September 2016-2017 onwards. Also, ‘Constitution of the Assessee’ is altered by adding One Person Company and the Limited Liability Partnership.

3. Power of Central Excise Officers for the purpose of adjudication u/s 83A of FA 1994 : Notification 44/2016 – Service tax

There is change in the prescribed limit set for adjudication power of various officers vide the above notification. The table shown below states the new prescribed limit for Central Excise Officers.

Amount of service tax or CENVAT credit specified in a notice issued

under the Finance Act 1994.Sr. No Rank of the Central Excise Officer,

(1)

(1)

(2)

(3)

(4)

(2) (3)

Not exceeding rupees ten lakh (excluding the cases relating to taxability of services or valuation of services and cases involving extended period of limitation).

Not exceeding rupees fifty lakh (except cases where Superintendents are empowered to adjudicate).

Rupees fifty lakh and above but not exceeding rupees two crore.

Without limit.

Superintendent

Assistant Commissioner or Deputy Commissioner,

Joint Commissioner or Additional Commissioner,Joint Commissioner or Additional Commissioner,

Commissioner,

These updates are contributed by S.Priya and vetted by CA Harsha Sri of SBS and Company LLP, Chartered Accountants. For any queries reach at [email protected]

34 | P a g e

Controls to be followed in Purchase, Property, Plant and Equipment processes

A. Sai Krishna Reddy

G. Prudhvi

S. Priya

K.Bhavani

N.Supriya

G. Chandrashekar

A. Vaishnavi

SBS - Hyd

SBS - Hyd

SBS - Hyd

VenueSpeakerDateEventS.No.

1

2

3

SATURDAY SESSIONS

Audit of Purchases

Sec 56(2) - Receipts without Consideration

SBS - Hyd

SBS - Hyd

SBS - Hyd

SBS - Hyd

Taxability of service of Nodal agency to Govt. Department- Case study

4

Points to be verified in TDS from Audit Perspective

ODI

Audit of Fixed Assets

5

6

7

SBS Interns' Digest www.sbsandco.com/digest

Audit of Bonus - G. Samatha 5 W's and 1H under CENVAT Credit rules, 2004 (Part 2)- P.Uday Kumar

35 | P a g e

08/10/2016

08/10/2016

15/10/2016

15/10/2016

22/10/2016

22/10/2016

29/10/2016

SBS Interns' Digest www.sbsandco.com/digest

Disclaimer:

© All Rights Reserved with SBS and Company LLP

Hyderabad: 6-3-900/6-9, #103 & 104, Veeru Castle, Durganagar Colony, Panjagutta, Hyderabad, Telangana

Kurnool: No. 302, 3rd Floor, V V Complex, 40/838, R.S. Road, Near SBI Main Branch, Kurnool, Andhra Pradesh

Nellore: 16-6-259, 1st Floor, Near Santi Sweets Opp: SBI ATM, Vijayamahal Centre, SPSR Nellore, Andhra Pradesh

Tada: 8-3-425/2, Flat No. 202, 2nd Floor, Bigsun Avenue, Near SRICITY, TADA, SPSR Nellore Dist, Andhra Pradesh Visakhapatnam: # 39-20-40/6, Flat No.7, Sai Yasoda Apartments, Madhavadhara,Visakhapatnam (Urban),Vizag, Andhra Pradesh

Bengaluru: B104,RIRCO, Santosh Apartments, Wind Tunnel Road, Murugeshpalya, Old Airport Road, Bangalore – 560017, Karnataka.