Embed Size (px)

Citation preview

Saving and InvestingSaving and Investing

Your Money at Work

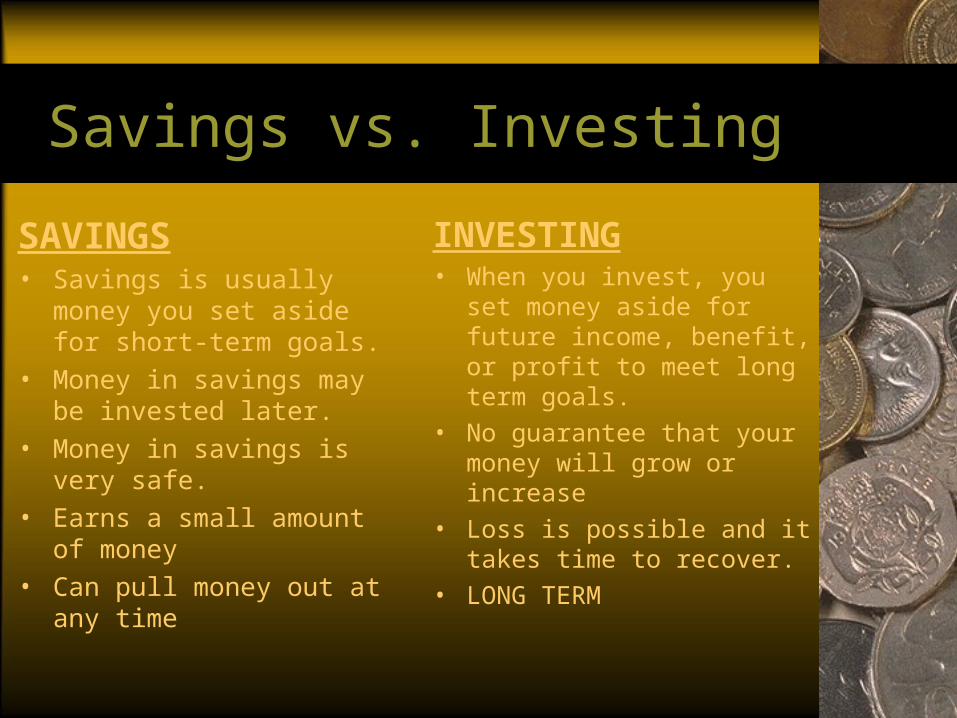

Savings vs. Investing

SAVINGS• Savings is usually money you

set aside for short-term goals.

• Money in savings may be invested later.

• Money in savings is very safe.

• Earns a small amount of money

• Can pull money out at any time

INVESTING• When you invest, you set

money aside for future income, benefit, or profit to meet long term goals.

• No guarantee that your money will grow or increase

• Loss is possible and it takes time to recover.

• LONG TERM

Compounding

• The idea of earning interest on interest.

Savings

• Savings is money put aside for future use.

• Most common reasons to save are:

–Major purchases

–Emergencies•Saving money for a “rainy day”

–Retirement

•Putting your money to use in order to make money on it

•Simple Interest vs. Compound Interest•Simple – interest that is computed only on the amount saved•Compound – interest that is computed on the amount saved plus interest previously earned

•Securities refers to bonds, stocks, and other documents sold by corporations and governments to raise large sums of money.

Investing

Investing Through Banks

•Savings Account –Simplest form of saving

–Offered by all institutions (banks, credit unions, etc.)

–Generally, a low minimum deposit is required.

–Interest is low and varies from institution to institution.

•Certificate of Deposit–Requires a minimum deposit for a minimum amount of time

–Interest rates are higher than a savings account

• Money Market Fund

Investing Through Banks

–Kind of mutual fund, or pool of money, put into a variety of short-term debt by business and government

Bonds

• Bonds– Promise to pay a definite amount of money at a

stated interest rate on a specified maturity date

• Bondholder – Individual who lends money to a corporation

Bond Terms

• Face Value– Amount being borrowed by the seller of the

bond

• Coupon Rate– Rate of interest on the bond

Types of Bonds

• Corporate Bonds– Issued by corporations– Used to finance buildings and equipment

• Municipal Bonds– Issued by local and state governments– Used to finance schools, roads, airports, etc.

Types of Bonds• Treasury Bonds

– Issued by federal government– Known as Savings or Federal Bonds– Types:

• Series EE Bonds– Cost half the face value– After a specified number of years the bond becomes worth the face value.

• Treasury Bills– Issued for three months to one year

• Treasury Notes– Issued for two to ten years

• Treasury Bonds– Issued for ten or more years

Stocks

• Stock– Share of ownership in a business

• Stock Certificate– Proof of ownership in a corporation

• Market Value– Price at which a stock can be bought or sold

• Dividends– Part of profits shared with stockholders

Types of Stocks

• Preferred– Priority over common stockholders in the payment of

dividends– No voting rights

• Common– General ownership in a corporation and a right to share

in the corporation’s profits– Right to vote at shareholder meetings

• One vote per share

Understanding Stock Quote Tables

• 52 Week Hi – Highest price during previous 52 weeks

• 52 Week Lo – Lowest price during previous 52 weeks

• Stock – Company name abbreviated• Stock Symbol – Ticker symbol• Dividend – Current dividend in dollars per share

based on the last dividend paid• Yield – Dividend yield based on the current selling

prices per share

Understanding Stock Quote Tables

• PE – Price/Earnings ratio, comparing the price of the stock with earnings per share

• Volume – Number of shares traded• High – Highest price during the day• Low – Lowest price during the day• Close – Closing price for the day• Net Change – Change in the closing price today

compared with closing price on the previous day

2. Floor broker (buyer) goes to the trading post at which time this specific stock is traded. It is traded with the floor broker (seller) who has an order to buy.

Typical transactions follow these steps:

1. Account executive receives your order to sell stock and relays to the brokerage firm’s representative at the stock exchange.

3. A clerk signals the transaction to a floor broker on the stock exchange floor.

Buying and Selling on the NYSE

4. Floor broker (buyer) signals the transaction back to the clerk. Then a floor reporter – an employee of the exchange – collects the information about the transaction and inputs it into the ticker system.

5. The sale appears on the price board, and a confirmation is relayed back to your account executive, who then notifies you of the completed transaction.

Buying and Selling on the NYSE

Brokerage Firm

Sells stocks for consumers

• Broker– Person who acts as a go-between for buyers and

sellers of securities.

• Commission – Fee charged by a brokerage firm for the buying

and/or selling of a security

Stock Exchange

• Marketplace where brokers who represent investors meet to buy and sell securities.

• Examples:– NYSE– NASDAQ– AMEX– Exchanges in San Francisco, Boston, Chicago

Types of Markets

• Bull Market– Occurs when investors are optimistic about the

economy

• Bear Market– Occurs when investors are pessimistic about the

economy

Selling a Stock

• Total Return– Calculation that includes the annual dividend as well as

any increase or decrease in the original purchase price of the investment

• Capital Gains– Profit from the sale of an asset such as stocks, bonds, or

real estate. Taxed as income

• Capital Loss– Sale of an investment for less than its purchase price.

Subtract up to $3,000 in losses from your income.

Investing in Insurance

• Life Insurance– Cash-value insurance that provides both

savings and death benefits

Investing in Your Future

• Pension– Series of regular payments made to a retired worker under an

organized plan

• Individual Retirement Account (IRA)– Tax sheltered retirement plan in which people can annually invest

earnings– Types:

• 401k or 403b contributions are tax deductible and funds are taxed as regular income when they are withdrawn after age 59 ½.

• Roth IRA contributions are not tax deductible, but investment gains and all funds on which taxes are prepaid are tax free when they are withdrawn after age 59 ½.

Investing in Your Future

• Annuity– Amount of money that an insurance company

will pay at definite intervals to a person who has previously deposited money with the company

Other Investment Options

• Real Estate– Land and anything that is attached to it

– Mortgage

• Legal document giving the lender a claim against the property

– Home Equity

• Difference between the price at which you could currently sell your house and the amount owed on the mortgage

• Appreciation – general increase in value of a property

• Depreciation – general decrease in value of a property

Other Investment Options

• Types of Property– Undeveloped Property (Land)

• Unused land intended only for investment purposes

– Commercial Property• Land and buildings that produce lease or rental

income

– Real Estate Investment Trusts (REITs)• Works like a mutual fund

• Combines funds to invest in real estate

Other Investment Options

• Collectibles– Items of personal interest to collectors– Rare coins, works of art, antiques, stamps, rare

books, comic books, sports memorabilia, rugs, ceramics, paintings, and other items that appeal to collector and investors

Other Investment Options

• Commodities– Includes grain, livestock, precious metals,

currency, and financial instruments– Futures

• Commodity contract-purchased in anticipation of higher market prices for the commodity in the near future

Other Investment Options

• Investing with Others– Investment Clubs

• Small group of people who organize to study stocks and to invest their money

– Mutual Funds• Created by an investment company that raises

money from many shareholders and invests it in a variety of stocks

– Limit risk by diversifying investment

Savings Plan

• Putting money aside in a systematic order

• Ways to put money aside:– Regular deposit– Automatic deposit– Electronic funds transfer

• Factors determining a program– Safety

• Assurance that the money you have invested will be returned to you

– Liquidity• Ease with which an investment can be changed into cash

without losing any of its value

– Yield• Rate of return (percentage of interest that will be added to

your savings over a period of time)

– Diversification• Process of spreading your assets among several different

types of investments to lessen risk

Starting Program

Factors That Affect the Rate of Return on an Investment• Risk - Chance of loss• Rate of Return (yield)

– Amount of money the investment earns– Compounding frequency is the interest computed on

the amount saved plus the interest previously earned.

• Liquidity– Ease with which an investment can be changed into

cash

• Resistance to inflation– Will rate of return keep up with inflation?

• Tax considerations

Factors that Affect the Selection of Financial Institutions

• Services offered

• Business hours

• Location

• On line services

Financial Security Investments (low risk)

• Cash

• Savings Accounts

• Money Market Accounts

• Certificate of Deposit

• US Government Bonds

• Retirement Accounts

Safety and Income Investments

• US Treasury Securities

• Conservative Corporate Bonds

• State and Municipal Bonds

• Income and Utility Stocks

Growth Investments

• Income and Growth Stocks

• Mutual Funds

• Real Estate

• Convertible Bonds

Speculation Investments (high risk)

• Options

• Commodities

• Precious Metals and Gems

• Speculative Stocks

• Junk Bonds

• Collectibles

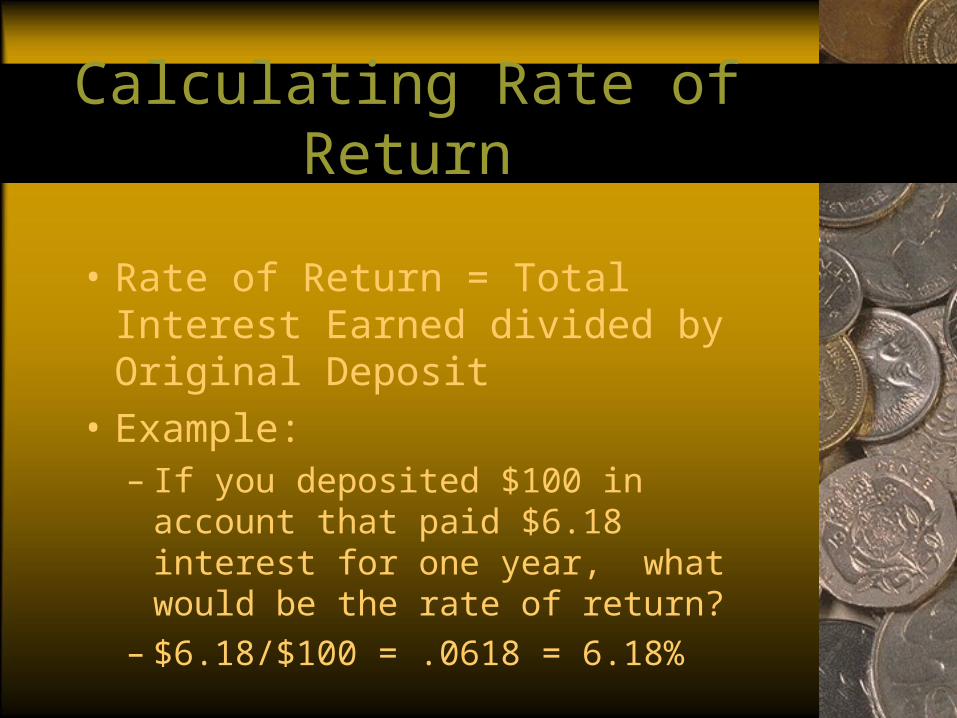

Calculating Rate of Return

• Rate of Return = Total Interest Earned divided by Original Deposit

• Example:– If you deposited $100 in account that paid

$6.18 interest for one year, what would be the rate of return?

– $6.18/$100 = .0618 = 6.18%

Earned Interest

• The payment you receive for allowing a financial institution or corporation to use your money

Rule of 72

• Tells you how long it takes your money to double in value

• Divide 72 by interest rate to determine number of years to double.

• Divide 72 by years to determine rate needed to double your money in a given time period.

Try It!Apply the Rule of 72 to find the time or rate.

• Assume you can earn 6% on your money. How long will it take $100 to grow to $200?

• 72 ÷ 6% interest =

12 years

Try It!Apply the Rule of 72 to find the time or rate.

• If you have $200 today and need $400 in eight years, what interest rate do you need to earn?

• 72 ÷ 8 years = 9% Interest

Regulators

• Securities and Exchange Commission (www.sec.gov)– Protects investors and maintains the integrity of

the securities markets

Regulators

• Department of the Secretary of State (www.secretary.state.nc.us /sec )

• State Securities Laws– Known as “blue sky” laws– Intent of laws is to protect the investing public by requiring

a satisfactory investigation of both the people who offer securities as investments and of the securities themselves.

– The securities division addresses investor complaints concerning securities brokers and dealers , investment advisers and commodity dealers as well as complaints about offerings of particular investment vehicles.

Regulators

• NASD (www.nasd.com)– Registers member firms, writes rules to govern

their behavior, examines them for compliance and disciplines those that fail to comply

– Largest private sector provider of financial regulatory services

– Has helped bring integrity to the markets and confidence in investors