Embed Size (px)

Citation preview

“Many landlords in Midtown are escalating their

tenant retention efforts. Some are boosting the

value of build-out packages, others are showing

flexibility on rent."

Daniel Horowitz, Executive Vice President

"Best-in-class new product and premiere

Midtown buildings are maintaining steady

demand. However, a significant amount of

commodity space is available, with more coming.

This is the soft spot in today’s market where the

best deals can be found.

Bill Montana, Senior Managing Director

Savills Studley Report New York City office sector Q3 2016

Savills Studley Research New York City

SUMMARYMarket Highlights

AVAILABILITY RATES NUDGE HIGHER

Manhattan’s overall availability rate inched up by 0.2 pp from 10.4% to 10.6%. Midtown’s Class A availability rate jumped by 120 basis points from 11.1% to 12.3%, its highest mark in three years. In contrast Downtown's Class A rate fell by 1.0 pp to 14.3%. Additionally, Class B and C availability in Manhattan dropped to 8.9%, with declines in most submarkets.

RENTS FLAT IN MIDTOWN

Class A asking rent in Midtown was essentially flat in the third quarter, falling from $88.89 to $88.85. Of note, Class A asking rent in the Plaza District fell by 3.9%.

Class A rent Downtown decreased by 0.9% to $64.64.

LEASING ACTIVITY DECREASES

Leasing activity fell slightly from 8.0 msf in the second quarter to 7.6 msf in the third quarter. Midtown captured all of the top 10 leases in the quarter, except for one. Additionally, Coach's 694,000-sf sales leaseback accounted for nearly 10% of activity. Bloomberg and WeWork - two of the most active tenants in recent years - both signed major expansions.

02

Savills Studley Report | New York City

Tenant Retention Efforts Intensify

Following the lull of July and August, September often ushers in some excitement as the market anticipates a rush of activity in the last few months of the year. Heading into this fall, though, some Manhattan landlords appear to be placing a vote of no confidence in the outlook for leasing activity in Class A properties. More owners have shifted from trying to prod demand, to doing their best to preserve the status quo and keeping a firm grip on the tenants already in place in their buildings.

This escalation in the leasing campaign is taking several different forms: a wider cross-section of owners are adjusting lease terms, some are raising concessions even on renewals and shorter term deals, and others are increasing the value of turnkey/build-out packages. Additionally, some landlords are retreating on their asking rent.

REITS and funds with a shorter holding period for their property were often the first to adopt these tactics. More recently, some longer-term holders of assets are being compelled to boost concessions and build-outs. Other owners are taking on the expense and risk of building out space with high-end glass and wood installations that many law firms and some professional/business services still prefer – not just for smaller and mid-sized firms, but for larger ones as well. The expense associated with these projects is mounting due to labor shortages and a moderate increase in the cost of materials. Owners are going to greater lengths to keep important tenants within their portfolio, sometimes restacking space or providing swing space while they build out a renewing tenant’s space.

The big shift though, is the move off of asking rents. A few quarters ago concessions were being dangled almost exclusively as the lure to drive leasing. Tenants have been pushing back against pricing for the last few quarters. Companies willing to move to commodity space on a lower floor, or those able to secure sublet space found lower-cost alternatives. Several months ago many owners did little to keep tenants from relocating. Of late though, landlords are stretching to keep tenants from jumping ship. Some landlords are working with key tenants that extend their lease commitment by reducing rent on the back end of their existing lease.

Source: Bureau of Labor Statistics

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-9.0%

-7.0%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40Millions

NYC Off. Emp. NYC (% Annual Change) U.S.(% Annual Change)

Office-Using Employment Trends

$81.41$78.31

$70.64$72.01

$61.00$60.39

$0

$20

$40

$60

$80

3Q162Q161Q164Q153Q15

Overall Rental Rate Trends

Midtown Midtown South Downtown

($/sf)

Asking Rent Trends (All Classes)

11.2%9.8%

8.7%8.9%10.5%

12.4%

0%

5%

10%

15%

3Q162Q161Q164Q153Q15

(%) Overall Availability Rate Trends

Midtown Midtown South Downtown

Availability Rate Trends (All Classes)

savills-studley.com/research 03

Q3 2016

Tenant Sq Feet Address Market AreaCoach, Inc.^ 694,000 501 W 30th St Hudson YardsRandom House** 631,025 1745 Broadway Columbus CircleMilbank, Tweed, Hadley & McCloy 250,000 55 Hudson Yards Hudson YardsWeWork 238,121 12 E 49th St Plaza IIBloomberg^^ 204,442 919 Third Ave Plaza IDentons* 190,576 1221 Avenue of the Americas Times SquareZurich American Insurance Company 131,856 4 World Trade Center WTC / Brookfield Place W. W. Norton & Company, Inc.* 109,735 500 Fifth Ave Grand CentralMorgan Stanley* 108,394 399 Park Ave Plaza IIThe Michael J Fox Foundation 86,492 111 W 33rd St Penn Plaza/Times Square SouthSum of Top Leases 2,644,641 Sum of 3rd Quarter Leasing Activity 7.6 MSF

Keep the Bird in HandTenant retention has always been critical to landlords but of late has become increasingly paramount. The cost of replacing a tenant is too high in this market. Landlords with run-of-the-mill space face the risk of an extended lease-up period. In turn, more landlords are accommodating shorter-term leases. More owners are plugging any holes in their roster, accepting that “a bird in hand” is better in light of the likelihood that demand will remain tepid for the foreseeable future.

Leasing activity has not fallen off a cliff, but it remains choppy, and few market participants anticipate a big turnaround in the short term. Manhattan’s Class A market has been dealing with anemic demand for the last two years. Tenants have leased 51.8 msf since the start of 2015, an 18.4% decrease from the prior seven quarters. If leasing continues on the same pace set in the first three quarters of the year leasing will barely exceed 30.0 msf – an increase from the 28.1 msf in 2015, but a far cry from the 35.0 msf averaged in 2013 and 2014. It is not as though tenants have a lack of different options to choose from; Class A available space has increased by 3.0 msf to 26.7 msf from the third quarter of 2015.

Pullback Apparent in the Plaza District

Class A asking rent across all of Midtown was nearly flat in the third quarter, inching lower from $88.89 to $88.85. The Plaza District registered a 3.9% quarter-on-quarter decrease in its Class A rent. Asking rent is budging a bit even though the amount of available sublet space has only very recently started to rise. Total Class A sublet space available for occupancy in the next 12 months in the Plaza District was down by nearly 10.0% year-on-year as of early September. Tenants are taking quality built sublet space when they can find it. Across all of Manhattan, though, total available sublet space has increased three consecutive quarters, rising from 7.2 msf to 8.1 msf as of late September.

The dropoff in demand, and associated increase in available space, is particularly apparent in Manhattan’s most expensive submarket, the Plaza District. Class A availability in the Plaza District ballooned to 12.9%, an increase of more than 370 basis points from a year ago. Of note, the Class A availability rate increased in every single Midtown submarket with the exception of Penn Plaza/Times Square South, where it dropped by 100 basis points to 8.5%. Penn Plaza/Times Square South continues to

benefit from tenants being pushed out of Midtown South due either to a lack of space options or elevated rents.

Shorting the Market

The willingness of landlords to sign short-term leases aligns with the needs of some, but not all tenants. Expanding firms focused on talent recruitment and retention, for example, will not extend their lease in outdated buildings. On the other hand, short term leases suit the needs of a growing number of companies facing uncertainty about their headcount and outlook in the next several years. Additionally, anticipation of rental rate declines in the next few years may be leading a few tenants to hold back on a long-term lease commitment. Although rent is likely to decrease within the next four to eight quarters, there is no reason to believe that the 30.0% correction in the post-Lehman shock of 2008 will be repeated.

Looking Forward

The increase in those firms opting for a short-term lease also reflects growing caution among Manhattan businesses. There is no one specific threat looming over the market but many businesses question whether conditions are about as good as they can get. Anyone thinking that uncertainty will evaporate if voters pick one candidate over the other in November’s election is kidding themselves. There are ample causes for concern beyond November. Next year could bring new banking regulations, changes to the tax code or a big infrastructure spending package. Or, Washington could remain mired in gridlock. Regardless of the election’s outcome, and the first 100 days of the new administration, savvy landlords with upcoming vacancies are going to greater lengths to put their houses in order.

Availability Rate Comparison Rental Rate Comparison

Major Transactions

*Renewal ** Renewal&Expansion ^^ Expansion ^Sale-Leaseback

$108.93$92.44$91.83$90.30

$81.41$80.70

$77.70$75.65$75.59$75.54$74.92$74.81$73.59

$70.64$68.45

$66.60$64.90$64.82$63.41$63.16

$61.00$57.59$57.40$56.39

$33.82

$0 $15 $30 $45 $60 $75 $90 $105 $120

Plaza IGreenwich Village

Hudson YardsPlaza II

MidtownTimes Square

SohoHudson Square

Grand CentralTribeca

ManhattanUnion Square

Columbus CircleMidtown South

Park Ave S./Madison SquarePenn Plaza/TSQ South

ChelseaFlatiron

WTC/Brookfield PlaceEast Side/UN

DowntownEast Side/UN

City HallFinancial District

U.S. Index

($/sf)

2.2%4.2%

6.5%6.6%6.8%

7.8%7.8%7.9%

8.7%9.2%9.2%9.5%9.5%9.9%10.5%10.6%

11.2%11.3%

12.7%13.1%

14.1%16.1%

17.8%17.9%

0% 5% 10% 15% 20%

East Side/UNCity Hall

TibecaGreenwich Village

ChelseaFlatiron

Park Ave S./Madison SquareSoho

Midtown SouthTimes SquareUnion Square

Columbus CirclePenn Plaza/TSQ South

Financial DistrictDowntownManhattan

MidtownPlaza II

Grand CentralWTC/Brookfield Place

Plaza IHudson Square

Hudson YardsU.S. Index

(%)

Savills Studley Report | New York City

04

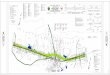

Map Submarket Total

SF(1000's)

ThisQuarter

ThisQuarter

%Change

fromLast Qtr.

YearAgo

ThisQuarter

ppChange

fromLast Qtr. (1)

YearAgo

ThisQuarter

%Change

fromLast Qtr.

YearAgo

Columbus Circle 28,877 857 2,734 2.1% 3,192 9.5% 0.2% 11.1% $73.59 -8.8% $86.92Columbus Circle - Class A 19,972 791 2,110 0.7% 2,271 10.6% 0.1% 11.4% $76.09 -8.8% $95.90Times Square 35,647 446 3,275 10.7% 3,368 9.2% 0.9% 9.4% $80.70 3.2% $76.24Times Square - Class A 30,932 416 2,568 16.7% 2,501 8.3% 1.2% 8.1% $85.74 2.1% $83.62Hudson Yards 5,297 1,027 941 44.3% 455 17.8% 5.1% 13.3% $91.83 -8.2% $86.21Hudson Yards - Class A 3,875 1,027 787 29.0% 383 20.3% 4.6% 17.8% $96.76 -3.3% $90.00Penn Plaza/Times Square South 55,205 899 5,269 -2.3% 5,330 9.5% -0.2% 9.7% $66.60 0.3% $64.25Penn Plaza/Times Square South - Class A 8,401 144 713 -10.3% 674 8.5% -1.0% 8.0% $93.96 -7.6% $85.32Plaza I 29,819 455 4,202 30.4% 2,440 14.1% 3.3% 8.2% $108.93 -9.0% $91.10Plaza I - Class A 22,960 380 3,578 28.3% 2,055 15.6% 3.4% 8.9% $113.61 -9.8% $94.47Plaza II 43,995 900 4,991 10.0% 4,174 11.3% 1.0% 9.5% $90.30 -0.1% $89.85Plaza II - Class A 38,909 786 4,425 9.0% 3,640 11.4% 0.9% 9.4% $92.38 0.1% $94.54Grand Central 72,399 1,150 9,201 -4.0% 7,415 12.7% -0.5% 10.3% $75.59 3.9% $73.73Grand Central - Class A 40,461 391 6,260 5.4% 4,717 15.5% 0.8% 11.7% $81.96 4.5% $79.17East Side/UN 3,266 1.5 71 5.5% 193 2.2% 0.1% 5.9% $63.16 9.7% $55.39East Side/UN - Class A 783 1.5 0 0.0% 143 0.0% 0.0% 18.3% N/A N/A N/A

9 Chelsea 16,116 170 1,098 -3.5% 843 6.8% -0.2% 5.3% $64.90 1.0% $57.85Chelsea - Class A 330 0 92 2143.8% 0 27.8% 26.6% 0.0% $97.80 N/A NS

10 Flatiron 13,063 191 1,021 -0.8% 1,036 7.8% -0.1% 8.0% $64.82 3.2% $68.22Flatiron - Class A 858 0 0 0.0% 58 0.0% 0.0% 6.7% N/A N/A N/A

11 Park Ave South/Madison Square 23,641 200 1,850 -0.3% 1,707 7.8% 0.0% 7.2% $68.45 5.4% $69.16Park Ave South/Madison Sq. - Class A 3,462 6.9 40 -14.9% 38 1.1% -0.2% 1.1% $95.00 0.0% $102.00Union Square 7,419 143 685 -15.2% 993 9.2% -1.7% 13.5% $74.81 2.0% $78.68Union Square - Class A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/AGreenwich Village 6,931 113 455 -17.7% 464 6.6% -1.4% 7.0% $92.44 N/A $80.11Greenwich Village - Class A 835 22 94 40.8% 96 11.2% 3.2% 11.5% $160.00 N/A $154.20

14 Hudson Square 10,134 117 1,634 1.7% 1,658 16.1% 0.3% 16.5% $75.65 0.0% $75.49Hudson Square - Class A 1,439 0 0 0.0% 13 0.0% 0.0% 0.9% N/A N/A N/A

15 Soho 3,972 74 316 5.3% 464 7.9% 0.4% 12.1% $77.70 -4.1% $76.67Soho - Class A 154 0 0 0.0% 0 0.0% 0.0% 0.0% N/A N/A N/A

16 Tribeca 5,966 0 387 -7.2% 438 6.5% -0.5% 7.6% $75.54 3.5% $78.85Tribeca - Class A 765 0 0 0.0% 0 0.0% 0.0% 0.0% N/A N/A N/A

17 City Hall 4,061 65 169 71.7% 69 4.2% 1.7% 1.7% $57.40 22.8% $44.50City Hall - Class A N/A 0 NA NA N/A N/A N/A N/A N/A N/A N/A

18 WTC/Brookfield Place 31,523 385 4,142 -3.5% 4,991 13.1% -0.5% 15.8% $63.41 -2.2% $65.36WTC/Brookfield Place - Class A 18,911 362 2,783 -7.2% 3,537 14.7% -1.1% 18.7% $68.75 -1.4% $72.17

19 Financial District 50,381 413 4,993 -9.8% 5,831 9.9% -1.1% 11.7% $56.39 0.7% $52.88Financial District- Class A 22,285 118 3,231 -5.9% 3,510 0.0% -0.9% 6.7% $60.93 0.2% $58.04

1-8 Midtown 274,505 5,736 30,682 5.5% 26,566 11.2% 0.6% 9.8% $81.41 2.1% $78.31Midtown - Class A 166,294 3,937 20,440 10.6% 16,385 12.3% 1.2% 10.0% $88.85 0.0% $86.27Midtown South Total 81,276 1,008 7,059 -3.2% 7,164 8.7% -0.3% 8.9% $70.64 1.1% $72.01Midtown South - Class A 7,078 29 225 92.2% 301 3.2% 1.5% 4.3% $113.78 -14.6% $114.56Downtown Total 91,931 863 9,692 -6.3% 11,329 10.5% -0.7% 12.4% $61.00 -1.2% $60.39Downtown Total - Class A 41,960 480 6,014 -6.5% 7,046 14.3% -1.0% 17.0% $64.64 -0.9% $65.51Manhattan Total 447,712 7,606 47,433 1.5% 45,059 10.6% 0.2% 10.1% $74.92 3.3% $72.62Manhattan Total - Class A 215,332 4,444 26,679 6.6% 23,733 12.4% 0.8% 11.1% $82.38 3.1% $80.25

LeasingActivity

AvailableSF

AvailabilityRate

Asking RentsPer SF

1

2

3

4

5

9-15

7

8

16-19

6

12

13

@SavillsStudleywww.savills-studley.com

Please contact us for further information

(1) Percentage point change for availability rates. Unless otherwise noted, all rents quoted throughout this report are average asking gross (full service) rents psf. Statistics are calculated using both direct and sublease information. Short-term sublet spaces (terms under two years) were excluded.

The information in this report is obtained from sources deemed reliable, but no representation is made as to the accuracy thereof. Statistics compiled with the support of The CoStar Group. Copyright © 2016 Savills Studley

Savills Studley399 Park Avenue11th FloorNew York, NY 10022(212) 326-1000

Chairman & CEOMitchell S. Steir [email protected](212) 326-1000

3

17

19

18

9

10

2

1213

1516

14

1

4

20

11

7

5

6 8

50th St

42nd St54th St

30th St

14th St

Houston St

34th St

23rd St

Canal St

Frankfort St

Lexi

ngto

n

2nd

Ave

6th

Ave

3rd

Ave

5th

Ave

9th

Ave

Corporate Research ContactKeith DeCoster - Director, U.S. Real Estate Analytics