Embed Size (px)

Citation preview

Oxford

Saudi Arabia Employment ReportInsights for 2016

AuthorsDr. Najat Benchiba-SaveniusRobert MogielnickiScott OwensProfessor William Scott-Jackson

ii

Saudi Arabia Employment Report: Insights for 2016 – Contents

www.oxfordstrategicconsulting.com

1 www.oxfordstrategicconsulting.com

ContentsIntroduction 2

Methodology 4

Sample Breakdown 6

Results 8

Analysis 24

2

Saudi Employment Report: Insights for 2016 – Introduction

www.oxfordstrategicconsulting.com

Introduction

3 www.oxfordstrategicconsulting.com

In December 2015, Oxford Strategic Consulting conducted a survey of Saudi nationals on their opinions pertaining to employment in the Kingdom. This report provides a summary of the results and offers new insights underpinning the current and future aspirations of Saudis which will serve as a useful tool to both the private and public sectors as well as governments and organisations. It is clear that there are significant and dynamic shifts in the labour market in terms of motivation, ideal careers and approaches to employment for the under 30s.

www.oxfordstrategicconsulting.com4

Saudi Arabia Employment Report: Insights for 2016 – Results

Methodology

5 www.oxfordstrategicconsulting.com

We asked 300 Saudi nationals aged under 30 about their views and attitudes towards employment in the Kingdom.

▪ Interviews were conducted over the phone by a third party fieldwork provider.

▪ The survey covered their motivations, perceptions of the best employers, their ideal job role, the best way for employers to attract nationals, the most and least attractive employment sectors, the importance of the private sector and difficulties faced when searching for jobs.

▪ The results have been presented at an overall level and also split by gender, age, region, working status and employment sector. Chi square and correlation tests have been carried out where appropriate.

6

Saudi Arabia Employment Report: Insights for 2016 – Sample Breakdown

www.oxfordstrategicconsulting.com

Sample Breakdown

7 www.oxfordstrategicconsulting.com

50%50% 41%

40%

40%

19%

60%50%

50%Male Female

Agedbetween

22-29

Dammam

Agedbetween

16-21

Riyadh

Jeddah

Working in government and semi-government

Working in private sector orfamily businesses

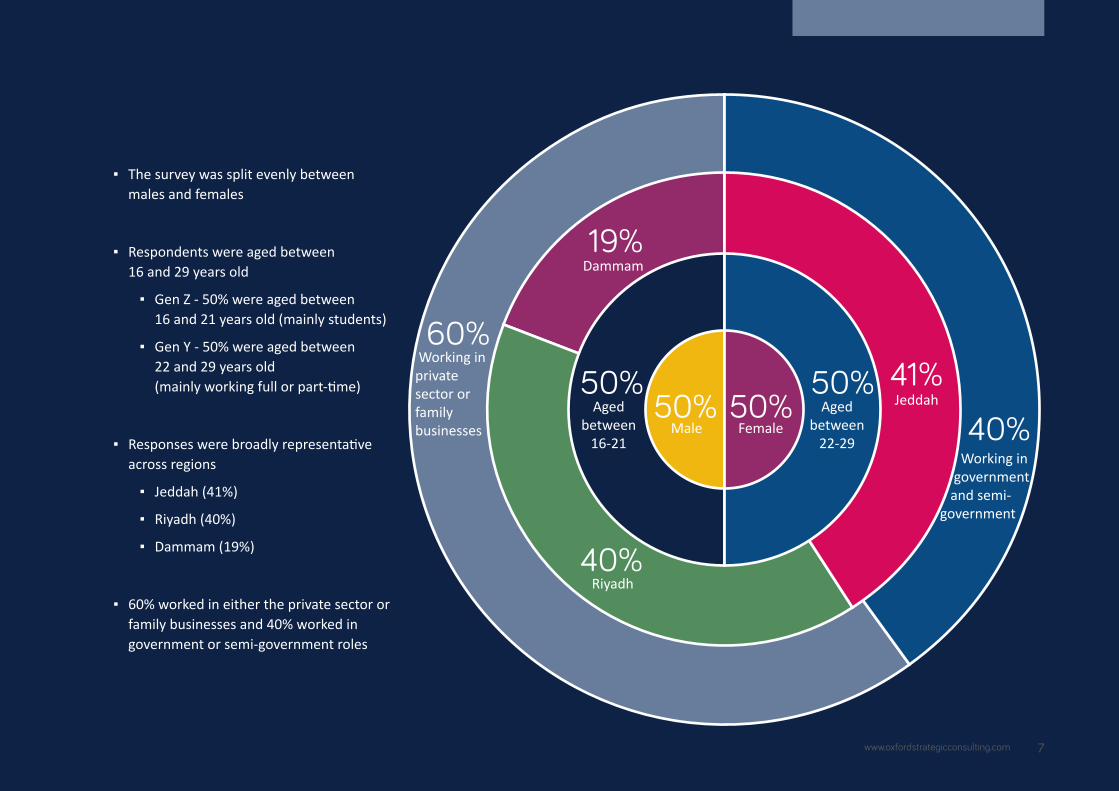

▪ The survey was split evenly between males and females

▪ Respondents were aged between 16 and 29 years old

▪ Gen Z - 50% were aged between 16 and 21 years old (mainly students)

▪ Gen Y - 50% were aged between 22 and 29 years old (mainly working full or part-time)

▪ Responses were broadly representative across regions

▪ Jeddah (41%)

▪ Riyadh (40%)

▪ Dammam (19%)

▪ 60% worked in either the private sector or family businesses and 40% worked in government or semi-government roles

www.oxfordstrategicconsulting.com8

Saudi Arabia Employment Report: Insights for 2016 – Results

Results

www.oxfordstrategicconsulting.com 9

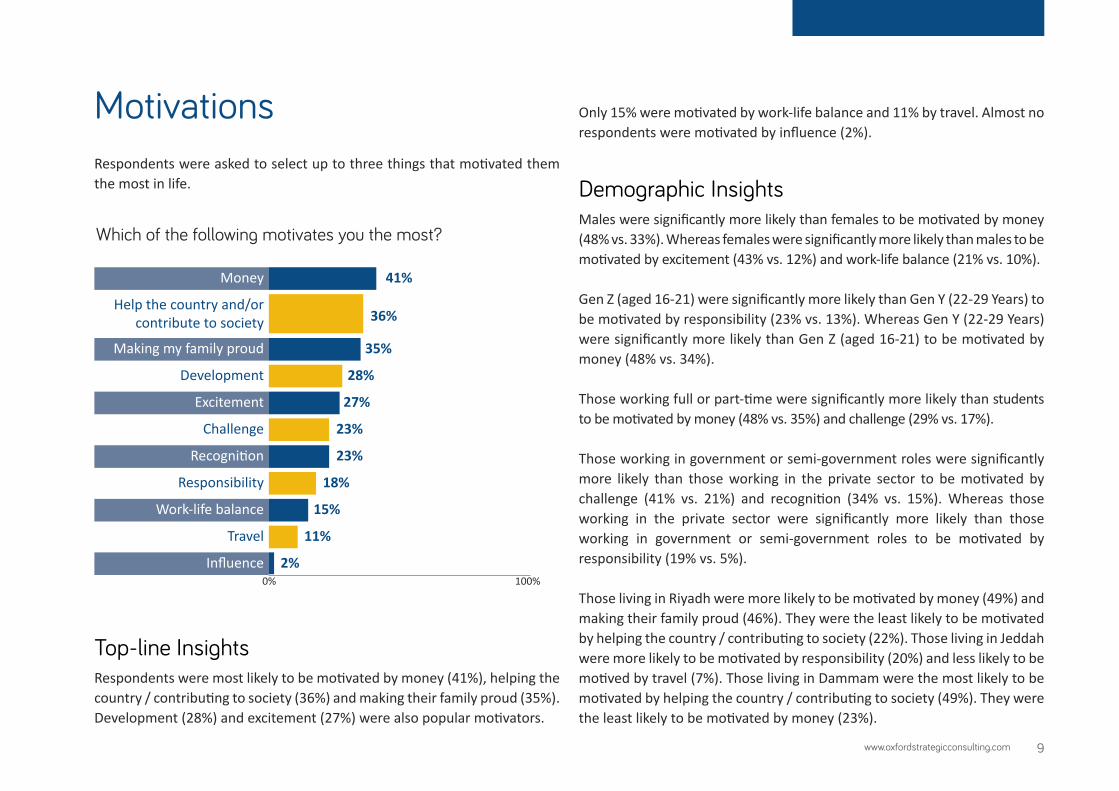

MotivationsRespondents were asked to select up to three things that motivated them the most in life.

Top-line InsightsRespondents were most likely to be motivated by money (41%), helping the country / contributing to society (36%) and making their family proud (35%). Development (28%) and excitement (27%) were also popular motivators.

Only 15% were motivated by work-life balance and 11% by travel. Almost no respondents were motivated by influence (2%).

Demographic InsightsMales were significantly more likely than females to be motivated by money (48% vs. 33%). Whereas females were significantly more likely than males to be motivated by excitement (43% vs. 12%) and work-life balance (21% vs. 10%).

Gen Z (aged 16-21) were significantly more likely than Gen Y (22-29 Years) to be motivated by responsibility (23% vs. 13%). Whereas Gen Y (22-29 Years) were significantly more likely than Gen Z (aged 16-21) to be motivated by money (48% vs. 34%).

Those working full or part-time were significantly more likely than students to be motivated by money (48% vs. 35%) and challenge (29% vs. 17%).

Those working in government or semi-government roles were significantly more likely than those working in the private sector to be motivated by challenge (41% vs. 21%) and recognition (34% vs. 15%). Whereas those working in the private sector were significantly more likely than those working in government or semi-government roles to be motivated by responsibility (19% vs. 5%).

Those living in Riyadh were more likely to be motivated by money (49%) and making their family proud (46%). They were the least likely to be motivated by helping the country / contributing to society (22%). Those living in Jeddah were more likely to be motivated by responsibility (20%) and less likely to be motived by travel (7%). Those living in Dammam were the most likely to be motivated by helping the country / contributing to society (49%). They were the least likely to be motivated by money (23%).

Which of the following motivates you the most?

Money

0% 100%

41%

Help the country and/orcontribute to society 36%

Making my family proud 35%

Development 28%

Excitement 27%

Challenge 23%

Recognition 23%

Responsibility 18%

Work-life balance 15%

Travel 11%

Influence 2%

www.oxfordstrategicconsulting.com10

Saudi Arabia Employment Report: Insights for 2016 – Results

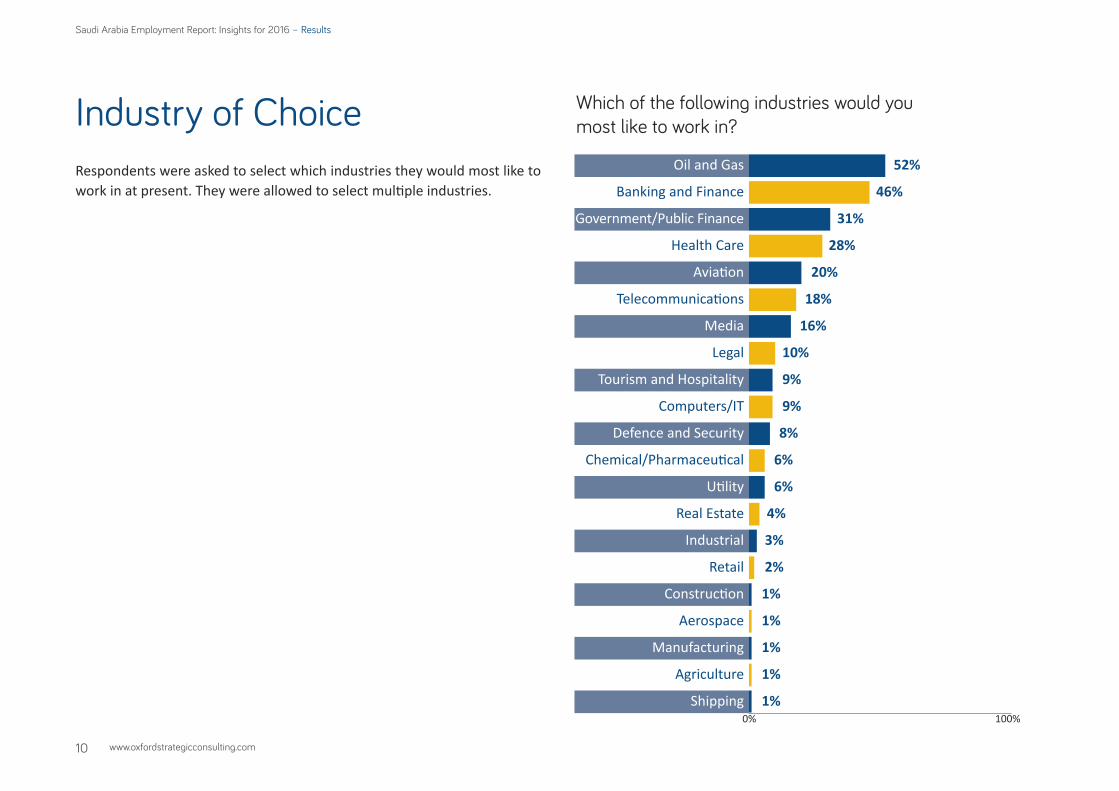

Industry of ChoiceRespondents were asked to select which industries they would most like to work in at present. They were allowed to select multiple industries.

Which of the following industries would you most like to work in?

Oil and Gas

0% 100%

52%

Banking and Finance 46%

Government/Public Finance 31%

Health Care 28%

Aviation 20%

Telecommunications 18%

Media 16%

Legal 10%

Tourism and Hospitality 9%

Computers/IT 9%

Defence and Security 8%

Chemical/Pharmaceutical 6%

Utility 6%

Real Estate 4%

Industrial 3%

Retail 2%

Construction 1%

Aerospace 1%

Manufacturing 1%

Agriculture 1%

Shipping 1%

www.oxfordstrategicconsulting.com 11

Top-line InsightsOver half of respondents felt their ideal career was in Oil and Gas (52%) and 46% wanted to work in Banking and Finance. A third (31%) felt their ideal career was working for the Government / Public Sector and 28% wanted to work in Health Care.

Demographic InsightsMales were significantly more likely to desire a career in Oil and Gas (58% vs. 45%), Aviation (30% vs. 9%) or Defence and Security (15% vs. 1%). Females were significantly more likely to desire a career in Banking and Finance (57% vs. 35%), Government / Public Sector (38% vs. 24%), Health Care (37% vs. 20%) or Media (21% vs. 10%).

Gen Z (aged 16-21) were significantly more likely to desire a career in Government / Public Sector (38% vs. 24%). Gen Y (22-29 Years) were significantly more likely to desire a career in Tourism and Hospitality (13% vs. 5%).

Students were significantly more likely to desire a career in Government / Public Sector (36% vs. 25%) or Health Care (35% vs. 21%).

There were no significant differences between employment sectors.

Those working in Riyadh were the most likely to desire a career in Telecommunications (25%). Those working in Jeddah were the most likely to desire a career in Oil and Gas (57%). Those working in Dammam were the most likely to desire a career in Media (21%).

www.oxfordstrategicconsulting.com12

Saudi Arabia Employment Report: Insights for 2016 – Results

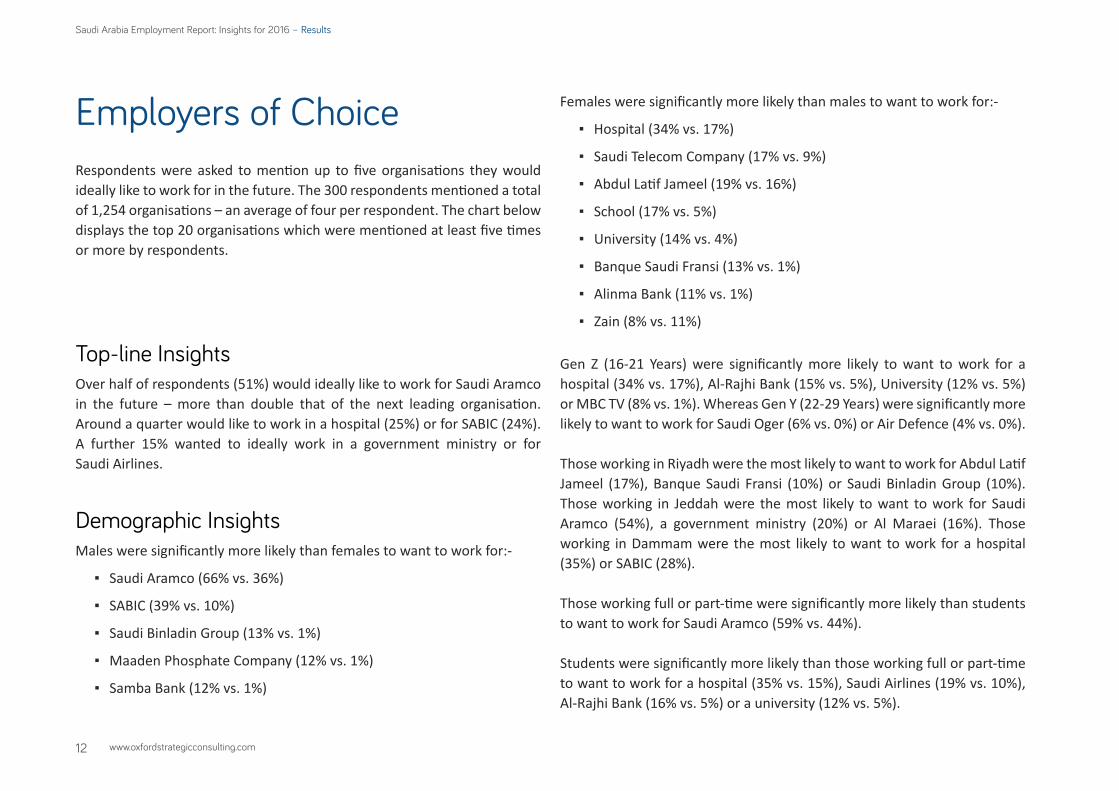

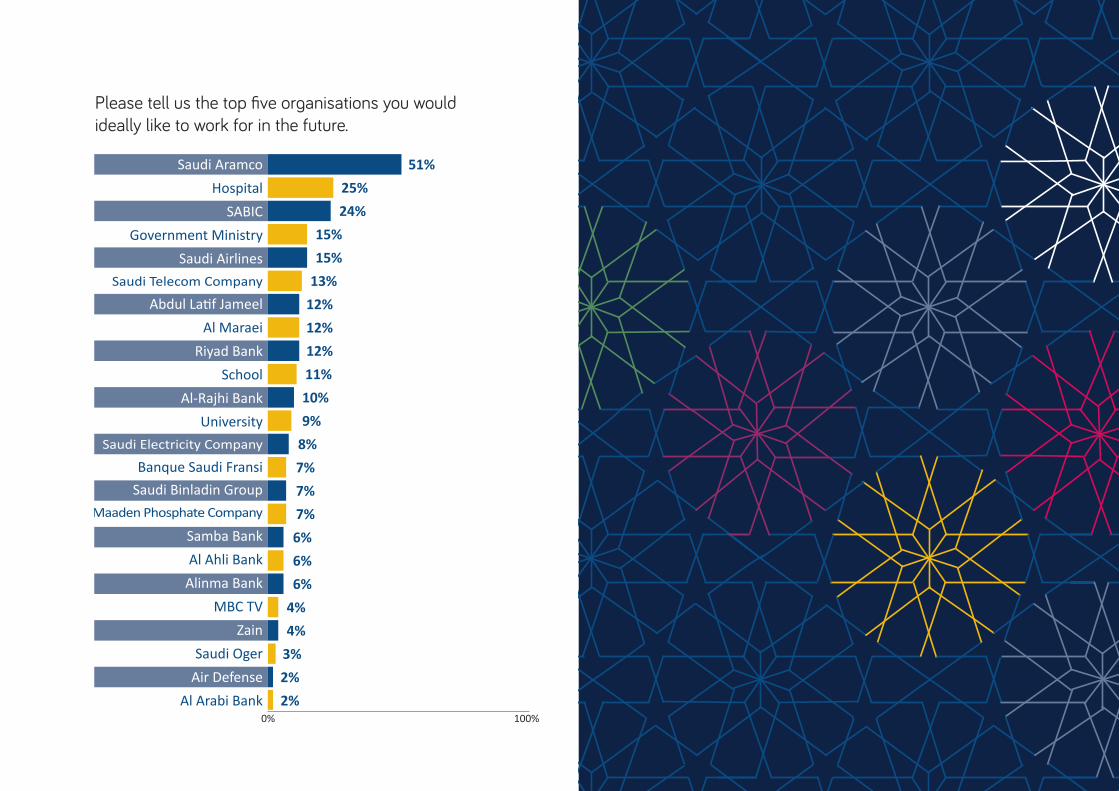

Employers of ChoiceRespondents were asked to mention up to five organisations they would ideally like to work for in the future. The 300 respondents mentioned a total of 1,254 organisations – an average of four per respondent. The chart below displays the top 20 organisations which were mentioned at least five times or more by respondents.

Top-line InsightsOver half of respondents (51%) would ideally like to work for Saudi Aramco in the future – more than double that of the next leading organisation. Around a quarter would like to work in a hospital (25%) or for SABIC (24%). A further 15% wanted to ideally work in a government ministry or for Saudi Airlines.

Demographic InsightsMales were significantly more likely than females to want to work for:-

▪ Saudi Aramco (66% vs. 36%)

▪ SABIC (39% vs. 10%)

▪ Saudi Binladin Group (13% vs. 1%)

▪ Maaden Phosphate Company (12% vs. 1%)

▪ Samba Bank (12% vs. 1%)

Females were significantly more likely than males to want to work for:-

▪ Hospital (34% vs. 17%)

▪ Saudi Telecom Company (17% vs. 9%)

▪ Abdul Latif Jameel (19% vs. 16%)

▪ School (17% vs. 5%)

▪ University (14% vs. 4%)

▪ Banque Saudi Fransi (13% vs. 1%)

▪ Alinma Bank (11% vs. 1%)

▪ Zain (8% vs. 11%)

Gen Z (16-21 Years) were significantly more likely to want to work for a hospital (34% vs. 17%), Al-Rajhi Bank (15% vs. 5%), University (12% vs. 5%) or MBC TV (8% vs. 1%). Whereas Gen Y (22-29 Years) were significantly more likely to want to work for Saudi Oger (6% vs. 0%) or Air Defence (4% vs. 0%).

Those working in Riyadh were the most likely to want to work for Abdul Latif Jameel (17%), Banque Saudi Fransi (10%) or Saudi Binladin Group (10%). Those working in Jeddah were the most likely to want to work for Saudi Aramco (54%), a government ministry (20%) or Al Maraei (16%). Those working in Dammam were the most likely to want to work for a hospital (35%) or SABIC (28%).

Those working full or part-time were significantly more likely than students to want to work for Saudi Aramco (59% vs. 44%).

Students were significantly more likely than those working full or part-time to want to work for a hospital (35% vs. 15%), Saudi Airlines (19% vs. 10%), Al-Rajhi Bank (16% vs. 5%) or a university (12% vs. 5%).

www.oxfordstrategicconsulting.com 13

Please tell us the top five organisations you would ideally like to work for in the future.

0% 100%

51%Hospital 25%

24%Government Ministry 15%

15%Saudi Telecom Company 13%

12%Al Maraei 12%

12%School 11%

10%University 9%

8%Banque Saudi Fransi 7%

7%Maaden Phosphate Company 7%

6%Al Ahli Bank 6%

6%4%4%Zain

Saudi OgerAir Defense

MBC TV

3%2%2%

Saudi Aramco

SABIC

Saudi Airlines

Abdul Latif Jameel

Riyad Bank

Al-Rajhi Bank

Saudi Electricity Company

Saudi Binladin Group

Samba Bank

Alinma Bank

Al Arabi Bank

www.oxfordstrategicconsulting.com14

Saudi Arabia Employment Report: Insights for 2016 – Results

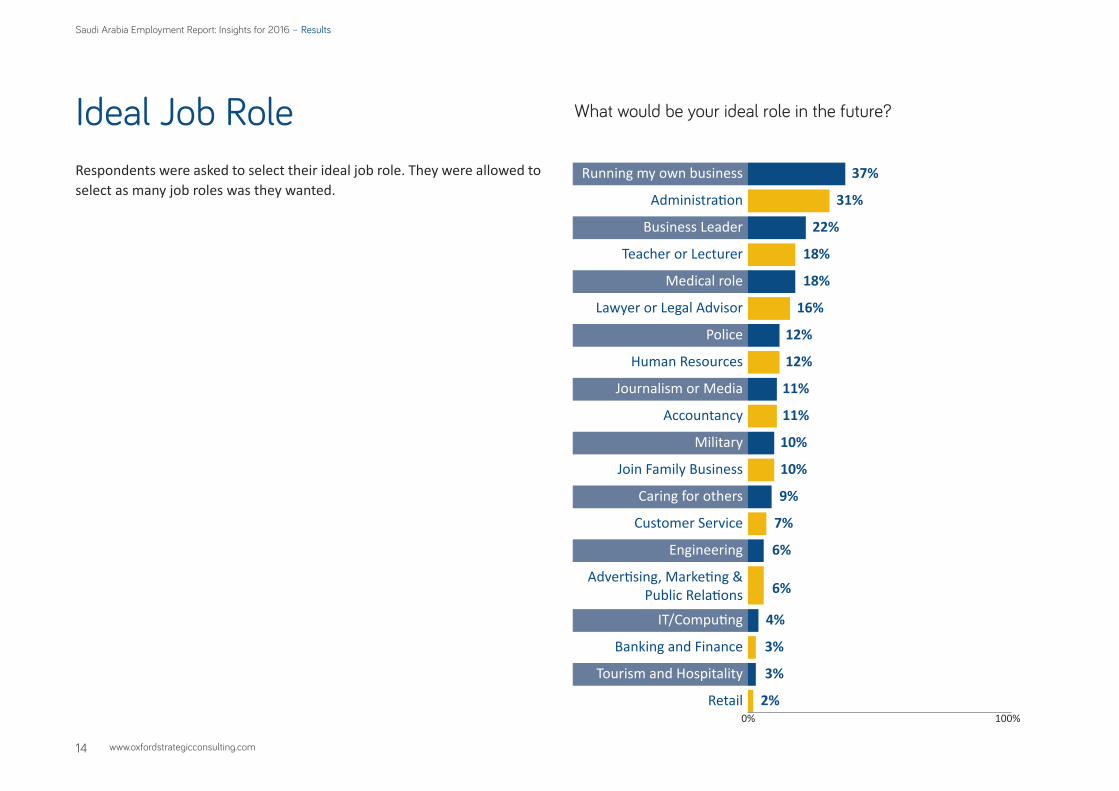

Ideal Job RoleRespondents were asked to select their ideal job role. They were allowed to select as many job roles was they wanted.

What would be your ideal role in the future?

Running my own business

0% 100%

37%

Administration 31%

Business Leader 22%

Teacher or Lecturer 18%

Medical role 18%

Lawyer or Legal Advisor 16%

Police 12%

Human Resources 12%

Journalism or Media 11%

Accountancy 11%

Military 10%

Join Family Business 10%

Caring for others 9%

Customer Service 7%

Engineering 6%

Advertising, Marketing &Public Relations 6%

IT/Computing 4%

Banking and Finance 3%

Tourism and Hospitality 3%

Retail 2%

www.oxfordstrategicconsulting.com 15

Top-line InsightsAlmost six out of ten respondents wanted to either run their own business (37%) or be a business leader in the future (22%). A further third felt their ideal role was in administration (31%).

Teacher / lecturer (18%), medical role (18%) and lawyer / legal advisor (16%) were also frequently selected as ideal careers.

Demographic InsightsMales were significantly more likely to consider their ideal role as a business leader (28% vs. 16%), in the police (17% vs. 7%), military (19% vs. 1%) or as an engineer (9% vs. 3%). Females were significantly more likely to consider their ideal role to be in administration (41% vs. 22%) or journalism / media (16% vs. 7%).

Gen Z (16-21 Years) were significantly more likely to consider their ideal role as a teacher / lecturer (26% vs. 10%) or a medical role (23% vs. 13%). Whereas Gen Y (22-29 Years) were significantly more likely to join the family business (14% vs. 5%).

Those working in Riyadh were the most likely to consider their ideal role as a lawyer or legal advisor (18%). Those working in Jeddah were the most likely to consider their ideal role as administration (41%) or human resources (21%). Those working in Dammam were the most likely to consider their ideal role as running their own business (46%) or IT/computing (11%).

Those working full or part-time were significantly more likely to consider their ideal role as a business leader (29% vs. 15%). Whereas students were significantly more likely to consider their ideal role as a teacher or lecturer (24% vs. 12%).

www.oxfordstrategicconsulting.com16

Saudi Arabia Employment Report: Insights for 2016 – Results

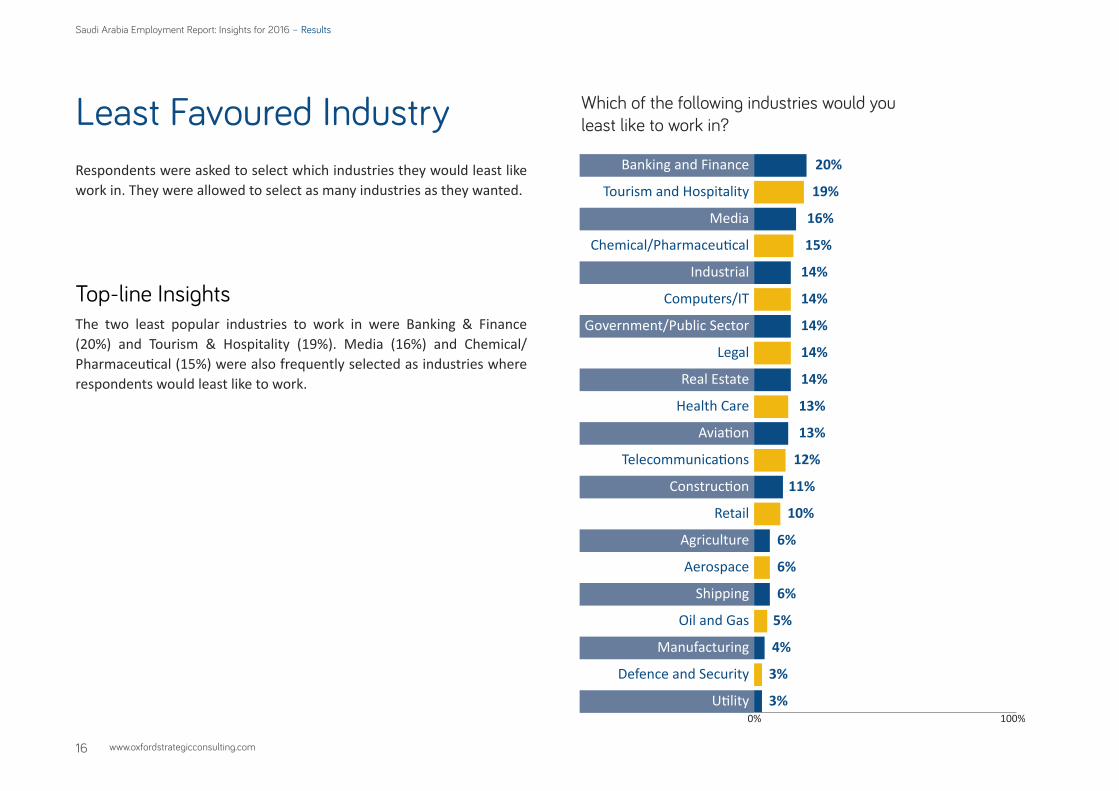

Least Favoured IndustryRespondents were asked to select which industries they would least like work in. They were allowed to select as many industries as they wanted.

Top-line InsightsThe two least popular industries to work in were Banking & Finance (20%) and Tourism & Hospitality (19%). Media (16%) and Chemical/Pharmaceutical (15%) were also frequently selected as industries where respondents would least like to work.

Which of the following industries would you least like to work in?

Banking and Finance

0% 100%

20%

Tourism and Hospitality 19%

Media 16%

Chemical/Pharmaceutical 15%

Industrial 14%

Computers/IT 14%

Government/Public Sector 14%

Legal 14%

Real Estate 14%

Health Care 13%

Aviation 13%

Telecommunications 12%

Construction 11%

Retail 10%

Agriculture 6%

Aerospace 6%

Shipping 6%

Oil and Gas 5%

Manufacturing 4%

Defence and Security 3%

Utility 3%

www.oxfordstrategicconsulting.com 17

Demographic InsightsMales were significantly more likely to select Real Estate (19% vs. 8%) and Retail (14% vs. 6%) as industries they would least like to work. Whereas females were significantly more likely to select Media (19% vs. 12%), Computers/IT (18% vs. 10%) and Construction (18% vs. 5%).

Gen Z (aged 16-21) were significantly more likely than Gen Y (22-29 Years) to select Tourism & Hospitality (26% vs. 11%) and Health Care (17% vs. 9%) as industries they would least like to work.

Those already working full or part-time were significantly more likely to select Construction (15% vs. 8%) and Defence and Security (6% vs. 1%) as industries they would least like to work. Whereas students were significantly more likely to select Media (20% vs. 11%) and Health Care (15% vs. 11%) as industries they would least like to work.

Those working in government or semi-government roles were significantly more likely to select Industrial (26% vs. 12%) and Health Care (21% vs. 4%) as industries where they would least like to work. Whereas those working in the private sector were significantly more likely to select Government / Public Sector (21% vs. 7%) as the industry where they would least like to work.

Those living in Riyadh were the most likely to select Banking and Finance (26%), Health Care (20%) and Retail (14%) as industries they would least like to work. Those living in Jeddah were the most likely to select Legal (16%) and Real Estate (16%) as industries they would least like to work. Those living in Dammam were the most likely to select Computers/IT (26%) and Telecommunications (21%) as industries they would least like to work.

www.oxfordstrategicconsulting.com18

Saudi Arabia Employment Report: Insights for 2016 – Results

www.oxfordstrategicconsulting.com 19

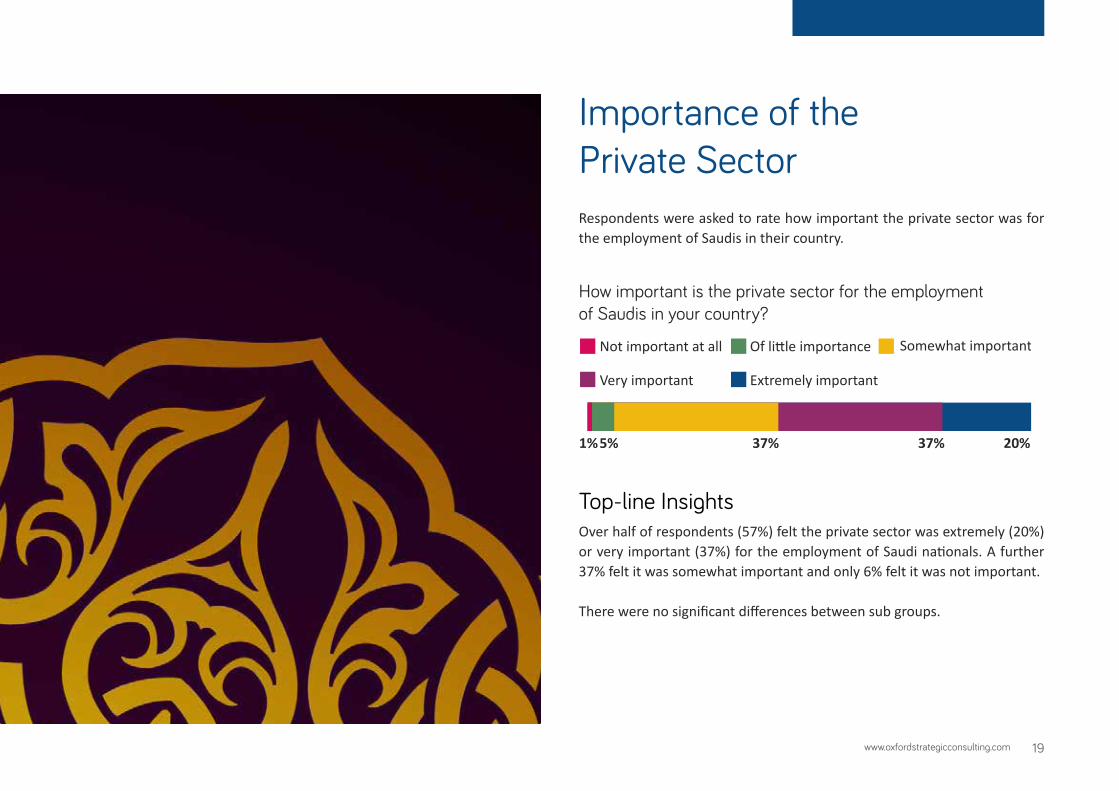

Importance of the Private SectorRespondents were asked to rate how important the private sector was for the employment of Saudis in their country.

1%5% 37% 37% 20%

How important is the private sector for the employment of Saudis in your country?

Not important at all Of little importance Somewhat important

Very important Extremely important

Top-line InsightsOver half of respondents (57%) felt the private sector was extremely (20%) or very important (37%) for the employment of Saudi nationals. A further 37% felt it was somewhat important and only 6% felt it was not important.

There were no significant differences between sub groups.

www.oxfordstrategicconsulting.com20

Saudi Arabia Employment Report: Insights for 2016 – Results

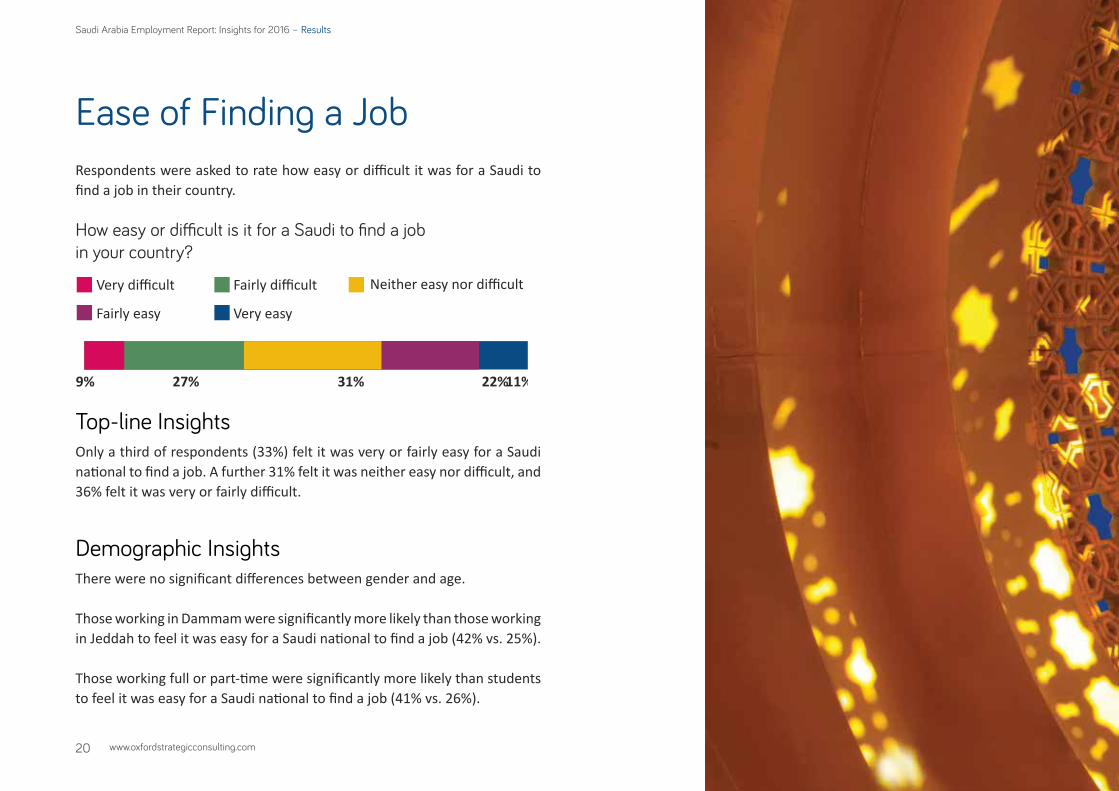

Ease of Finding a JobRespondents were asked to rate how easy or difficult it was for a Saudi to find a job in their country.

9% 27% 31% 22%11%

How easy or di�cult is it for a Saudi to find a job in your country?

Very difficult Fairly difficult Neither easy nor difficult

Fairly easy Very easy

Top-line InsightsOnly a third of respondents (33%) felt it was very or fairly easy for a Saudi national to find a job. A further 31% felt it was neither easy nor difficult, and 36% felt it was very or fairly difficult.

Demographic InsightsThere were no significant differences between gender and age.

Those working in Dammam were significantly more likely than those working in Jeddah to feel it was easy for a Saudi national to find a job (42% vs. 25%).

Those working full or part-time were significantly more likely than students to feel it was easy for a Saudi national to find a job (41% vs. 26%).

www.oxfordstrategicconsulting.com 21

www.oxfordstrategicconsulting.com22

Saudi Arabia Employment Report: Insights for 2016 – Results

www.oxfordstrategicconsulting.com 23

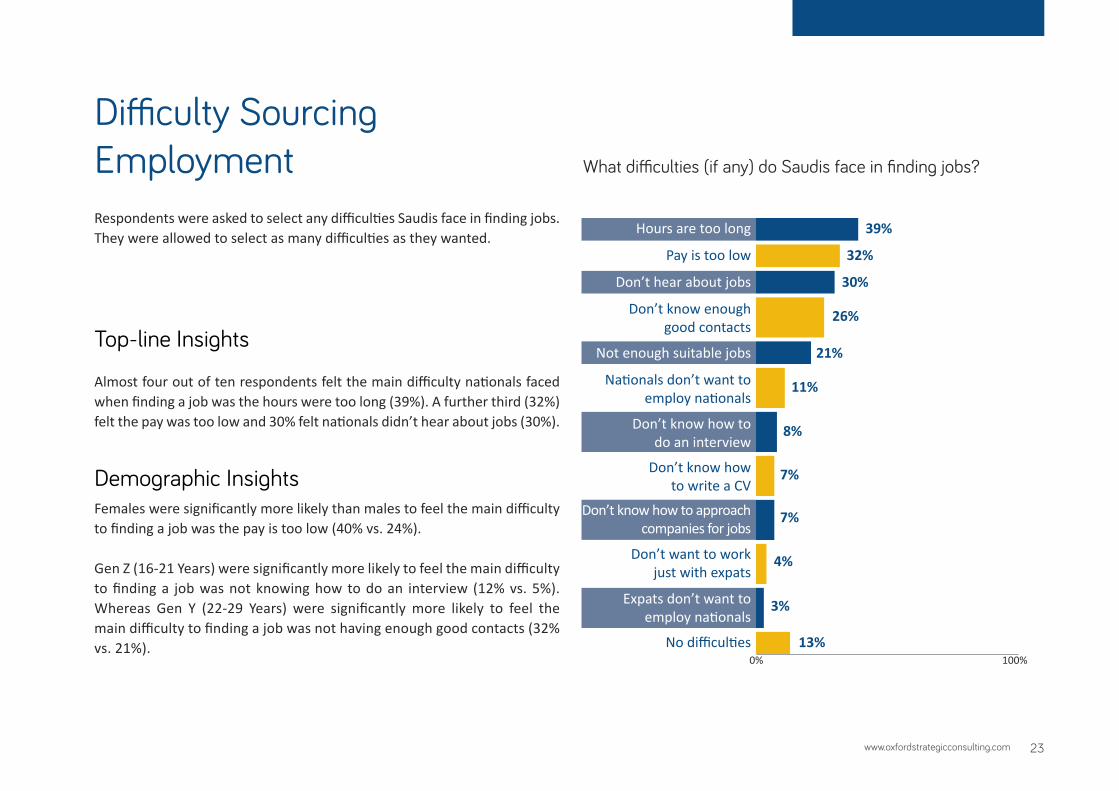

What di�culties (if any) do Saudis face in finding jobs?

Hours are too long

0% 100%

39%

Pay is too low 32%

Don’t hear about jobs 30%

Don’t know enough good contacts

26%

Not enough suitable jobs 21%

Nationals don’t want toemploy nationals

11%

Don’t know how todo an interview

8%

Don’t know howto write a CV

7%

Don’t know how to approachcompanies for jobs

7%

Don’t want to workjust with expats

4%

Expats don’t want toemploy nationals

3%

No difficulties 13%

Difficulty Sourcing EmploymentRespondents were asked to select any difficulties Saudis face in finding jobs. They were allowed to select as many difficulties as they wanted.

Top-line Insights

Almost four out of ten respondents felt the main difficulty nationals faced when finding a job was the hours were too long (39%). A further third (32%) felt the pay was too low and 30% felt nationals didn’t hear about jobs (30%).

Demographic InsightsFemales were significantly more likely than males to feel the main difficulty to finding a job was the pay is too low (40% vs. 24%).

Gen Z (16-21 Years) were significantly more likely to feel the main difficulty to finding a job was not knowing how to do an interview (12% vs. 5%). Whereas Gen Y (22-29 Years) were significantly more likely to feel the main difficulty to finding a job was not having enough good contacts (32% vs. 21%).

24

Saudi Arabia Employment Report: Insights for 2016 – Analysis

www.oxfordstrategicconsulting.com

Analysis

25 www.oxfordstrategicconsulting.com

Tapping into Male and Female TalentSaudi men were found to be more than twice as likely to consider working in defence and security when compared to women.1 These results show that the defence and security sector could tailor their employment programs to bolster female recruitment practices and engage more women in the sector. The sector could also think about improving scholarships to tap into this potential recruitment pool of both male and females.

Conversely, the survey found that women are six times less likely than men to entertain the notion of working in tourism and hospitality.2 The tourism industry across the GCC has struggled to overcome negative perceptions that the industry is unfit for local employment. However, these negative perceptions can be changed by implementing flexible hours, remote work and women-only environments. Jumeirah, for example, has done an excellent job transforming Emirati perceptions of the industry and building a critical mass of Emirati managers within the organisation. The tourism industry in Saudi Arabia would do well to learn from Jumeirah’s success in the UAE.

The survey also found that female Saudis were more than twice as likely as men to aspire to a job in aerospace.3 This is a statistically significant finding, and employers in the aerospace industry should tailor their recruitment drives to women and young female undergraduates as this could be a leading trend in the future. Moreover, Saudi women appear to be shunning ‘traditional’ office roles in lieu of other careers, and this employment trend should be met by bolstering non-stereotypical roles in lieu of traditional roles.

1 Test: Chi Square (1) = 4.252, p < .05, Odds Ratio = 2.19.2 Test: Chi Square (1) = 13.238, p < .001, Odds Ratio = 6.3.3 Test: Chi Square (1) = 5.526, p < .05, Odds Ratio = 2.00.

26

Saudi Arabia Employment Report: Insights for 2016 – Analysis

www.oxfordstrategicconsulting.com

Age is RelevantSaudis are cognisant of the need to find suitable employment that is relevant to their educational background, needs and status. The survey found that the younger a participant, the more likely they are to feel that there are not enough suitable jobs.4 This finding could prove very useful to careers services and employers across the Kingdom, as maximising employability and matching skills early on can lead to greater job satisfaction amongst young Saudis.

The results also found that the older an individual, the less they want to work with expats.5 This has clear implications for the Saudi Ministry of Labour, which manages the national Saudisation programme. The older generation is more traditional in its approach to nationalisation in the Kingdom. However, the younger generation of Saudis seem less concerned with traditional notions of nationalisation. Younger Saudis are more inclined to work with expats; however, this employment preference likely exists on the supposition that adequate employment opportunities remain available for the national population.

Generally speaking, the findings provide valuable insights on Saudisation for Human Resource Management practices in both public and private sectors. Moreover, these insights can help bolster the Saudisation policy by allowing local and global firms to better recruit, retain and effectively manage their labour force.

4 Test: correlation: r = -.137, p < .05.5 Test: correlation: r = 206, p < .01.

27 www.oxfordstrategicconsulting.com

Saudis Prefer Local Employment Saudis are significantly more inclined to work for Saudi Aramco – more than double that of the next leading organisation. Indeed, over half of the respondents (51%) cited the national oil and gas conglomerate as the ideal company to work for in the future. Respondents were likely swayed by the prestige and stability of this large organisation. Yet it is clear that this organisation alone cannot absorb half of the Kingdom’s job-seeking Saudis. Instead, other local organisations will have to help shoulder the national responsibility of employing Saudis.

On this note, many Saudis listed jobs outside of Saudi Aramco and the government as their ideal roles. Around a quarter of respondents considered working in a hospital (25%) as their ideal role, while approximately another quarter (24%) listed SABIC. A further 15% wanted to work for Saudi Airlines. These findings are encouraging signs for the healthcare, banking & finance and aviation industries. Private and semi-government organisations within these three industries should help to boost employment during this period of unstable commodity prices.

28

Saudi Arabia Employment Report: Insights for 2016 – Analysis

www.oxfordstrategicconsulting.com

29 www.oxfordstrategicconsulting.com

Entrepreneurial SpiritDeveloping an entrepreneurial ecosystem for Saudi youth could provide unparalleled opportunities in the Kingdom. Oxford Strategic Consulting found that almost six out of ten respondents wanted to either run their own business (37%) or be a business leader in the future (22%). This bodes well for increasing employment opportunities in the Kingdom through SME development. Both private and public sectors should provide entrepreneurial training, youth enterprise schemes and funding to promote risk-taking and encourage young Saudis to indulge their appetite for business.

Yet support for entrepreneurs must be targeted to those most likely to contribute to employment growth. Most start-ups fail, and those SMEs that survive tend not to make significant contributions to employment. In order to maximise the investment in entrepreneurism, high-potential entrepreneurs who actually contribute to employment growth, known as ‘gazelles’ should be identified and supported by the private and public sectors. Providing seed funding and early support for high-potential Saudi entrepreneurs is much more cost-effective than employing the equivalent public sector employees for an entire career in the government.

30

Saudi Arabia Employment Report: Insights for 2016 – Analysis

www.oxfordstrategicconsulting.com

31 www.oxfordstrategicconsulting.com

Private Sector Gains MomentumThere is a major push at the moment to encourage more Saudis to join the private sector, and it appears that Saudi nationals are aligned with the government on this strategic country goal. Approximately 57% of Saudi nationals thought the private sector was ‘extremely important’ for employment within the Kingdom, with only 6% considering the sector as ‘not important’ at all. Moreover, those working in the private sector were significantly more likely than public sector employees to select the government or public sector (21% vs. 7%) as the industry they would least like to work in at present. These findings suggest that those Saudis currently working in the private sector are less likely to seek public sector roles.

The role and purpose of the private sector has risen dramatically in the last decade. It is now clear that private sector organisations within the Kingdom have a social responsibility to increase employment opportunities for Saudis and support healthy HR policies. At the same time, the private sector has a responsibility to increase the quality of education, training and vocational skills development within the Kingdom. On the bright side, there exist plenty of eager, job-seeking Saudis within the local population. It’s time for the private sector to transform this momentum into sustainable development.

32

Saudi Arabia Employment Report: Insights for 2016 – Contact

www.oxfordstrategicconsulting.com

Contact & inquiriesFor additional information about the survey findings and analyses in this report, or to learn more about Oxford Strategic Consulting’s other research on Nationalisation in Saudi Arabia, please contact Robert Mogielnicki at [email protected].

For more insights, publications and services related to HR in the GCC, please visit www.oxfordstrategicconsulting.com.

33 www.oxfordstrategicconsulting.com

www: www.oxfordstrategicconsulting.com

Email: [email protected]

UK office Head Office 30 St Giles’ Oxford OX1 3LE, UK

Tel: +44 208 720 6440

UAE office Emirates Towers Level 41 Sheikh Zayed Road Dubai

Tel: +971 4 319 9378

Qatar office Tornado Tower Level 22, West Bay Doha Qatar

Tel: +974 4429 2463

Saudi Arabia officeFaisaliah Tower, Level 18 King Fahed Highway P.O. Box 54995, Riyadh 11524 Kingdom of Saudi Arabia

Tel: +966 11 490 3706