Embed Size (px)

Citation preview

Saudi Arabia - A Promising

Proposition for Private Equity

November 2014

Tel: +966 12 658 8888

Fax: +966 12 658 6663

CMA License : 07074-37

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 2

Saudi Arabia, the largest GCC economy, is poised to grow strongly in the coming years led

by the government’s diversification efforts. The government is also pushing for economic and

regulatory reforms to actively promote foreign as well as domestic investment and create a

conducive environment for private sector growth. Domestic businesses in the country are

eager to ride on long term favorable demand trends driven by the growing youth population.

To take advantage of these underlying trends, companies, especially the small and medium

enterprises (SMEs), will not only need financial infusion, but also expert guidance in scaling

up their business models. Currently, mega projects and infrastructure investments dominate

banking sector balance sheets, leaving the SME sector constrained for funds. These SMEs

face financing challenges due to the over-cautious approach of most banks in the nation.

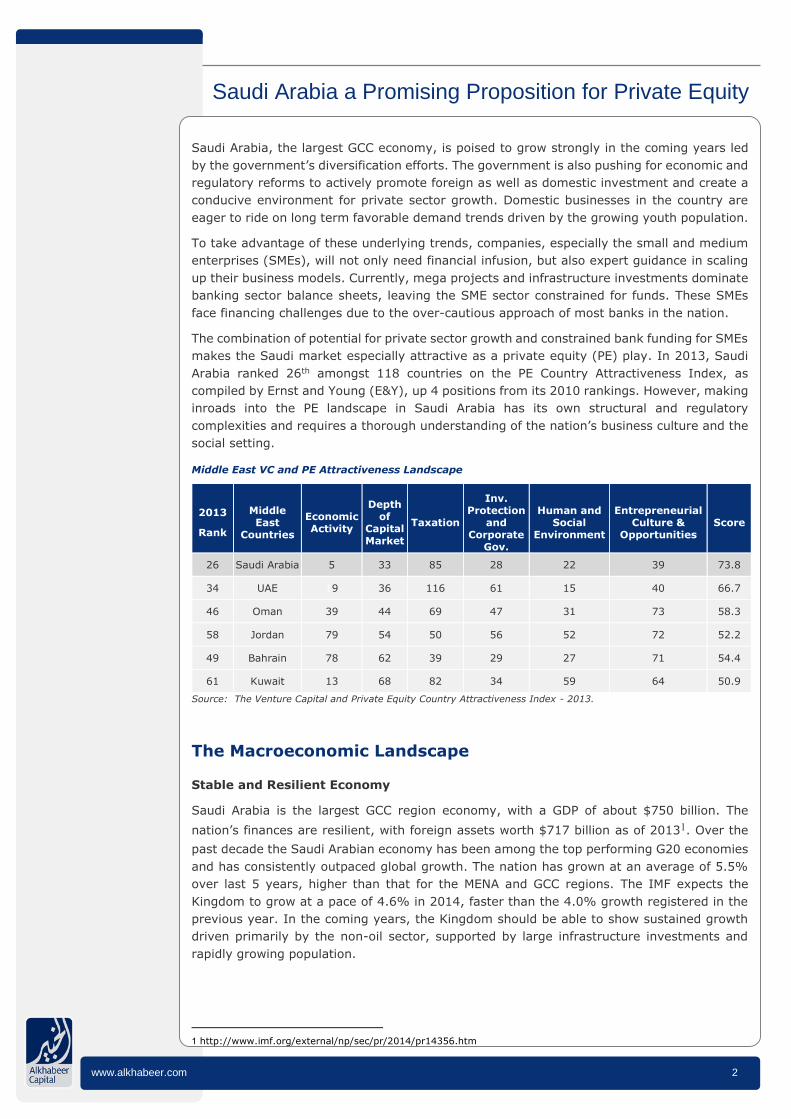

The combination of potential for private sector growth and constrained bank funding for SMEs

makes the Saudi market especially attractive as a private equity (PE) play. In 2013, Saudi

Arabia ranked 26th amongst 118 countries on the PE Country Attractiveness Index, as

compiled by Ernst and Young (E&Y), up 4 positions from its 2010 rankings. However, making

inroads into the PE landscape in Saudi Arabia has its own structural and regulatory

complexities and requires a thorough understanding of the nation’s business culture and the

social setting.

Middle East VC and PE Attractiveness Landscape

2013

Rank

Middle East

Countries

Economic Activity

Depth of

Capital Market

Taxation

Inv. Protection

and Corporate

Gov.

Human and Social

Environment

Entrepreneurial Culture &

Opportunities Score

26 Saudi Arabia 5 33 85 28 22 39 73.8

34 UAE 19 36 116 61 15 40 66.7

46 Oman 39 44 69 47 31 73 58.3

58 Jordan 79 54 50 56 52 72 52.2

49 Bahrain 78 62 39 29 27 71 54.4

61 Kuwait 13 68 82 34 59 64 50.9

Source: The Venture Capital and Private Equity Country Attractiveness Index - 2013.

The Macroeconomic Landscape

Stable and Resilient Economy

Saudi Arabia is the largest GCC region economy, with a GDP of about $750 billion. The

nation’s finances are resilient, with foreign assets worth $717 billion as of 20131. Over the

past decade the Saudi Arabian economy has been among the top performing G20 economies

and has consistently outpaced global growth. The nation has grown at an average of 5.5%

over last 5 years, higher than that for the MENA and GCC regions. The IMF expects the

Kingdom to grow at a pace of 4.6% in 2014, faster than the 4.0% growth registered in the

previous year. In the coming years, the Kingdom should be able to show sustained growth

driven primarily by the non-oil sector, supported by large infrastructure investments and

rapidly growing population.

1 http://www.imf.org/external/np/sec/pr/2014/pr14356.htm

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 3

KSA Outpacing MENA and GCC Growth (% YoY)

Source: SAMA and IMF

Saudi Economy – Consistent Growth in the Non-oil Sector (% YoY)

Source: SAMA, *At Constant Prices

Political stability inspires confidence in investors

It is a well-researched2 fact that political stability directly correlates to foreign investment

inflows in a country. Saudi Arabia is perceived to be a safe haven in terms of political stability

in the MENA region. Largely unscathed from the Arab spring, the country has also not

witnessed any political turmoil faced by its neighboring countries such as Egypt, Syria, and

Iraq. The Kingdom has made inroads in establishing cordial relations with its neighbours.

Moreover, the recent appointment of Prince Muqrin, as second in line to the throne, has eased

fears of the Kingdom's long-term succession plans. The stable political environment inspires

confidence amongst fund managers.

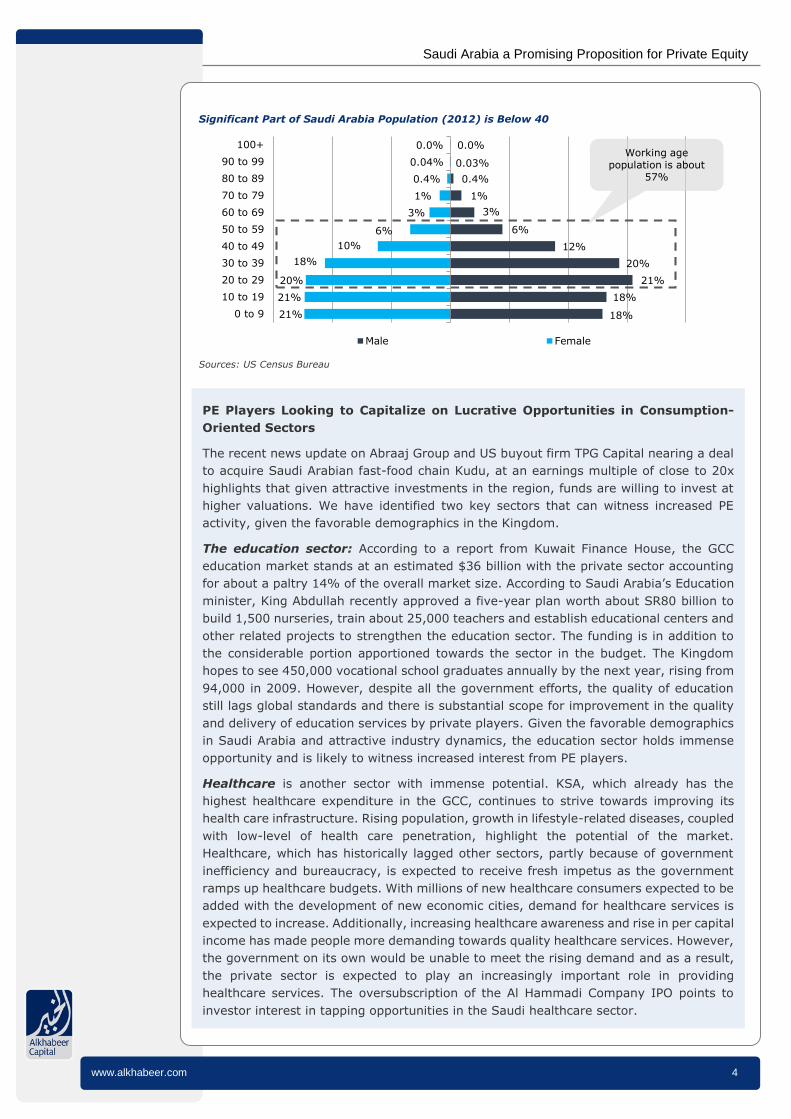

The demographic profile opens significant avenues for PE investments

The Saudi population grew by an average annual pace of 3.2%3 between 2004 and 2013,

sharply higher than the global rate of 1.2% seen during the same period. Moreover, 50% of

the Saudi population is below 25 years, representing the immense potential for consumption

oriented sectors. Notable players in the PE universe remain optimistic of the consumption-

led growth in Saudi Arabia and have displayed marked interest in the consumer, education

and healthcare space. Rapid urbanization, increase in per capita income and increasing

participation of women in workforce would be key drivers for growth in the consumer sectors.

Saudi Population Growth Continues to Outpace Global Population Growth

Sources: United Nation

2 http://www.cefir.org/papers/WP190.pdf 3 http://www.sama.gov.sa/sites/samaen/ReportsStatistics/statistics/Pages/YearlyStatistics.aspx

0.0%

2.5%

5.0%

7.5%

10.0%

Average 2000–08

2010 2012 2014E

Saudi GDP Growth MENA GDP Growth

GCC GDP Growth

-10%

-5%

0%

5%

10%

15%

20%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

GDP Growth*

Oil Sector Growth

Non-oil Sector growth

1.5%1.3% 1.2% 1.2% 1.2%

2.7%

1.6%

4.1%

2.0% 1.9%

0.0%

1.2%

2.4%

3.6%

4.8%

1990-1995 1995-2000 2000-2005 2005-2010 2010-2015 E

World Population Growth Rate (%) Saudi Population Growth Rate (%)

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 4

Significant Part of Saudi Arabia Population (2012) is Below 40

Sources: US Census Bureau

18%

18%

21%

20%

12%

6%

3%

1%

0.4%

0.03%

0.0%

21%

21%

20%

18%

10%

6%

3%

1%

0.4%

0.04%

0.0%

0 to 9

10 to 19

20 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70 to 79

80 to 89

90 to 99

100+

Male Female

Working age population is about

57%

PE Players Looking to Capitalize on Lucrative Opportunities in Consumption-

Oriented Sectors

The recent news update on Abraaj Group and US buyout firm TPG Capital nearing a deal

to acquire Saudi Arabian fast-food chain Kudu, at an earnings multiple of close to 20x

highlights that given attractive investments in the region, funds are willing to invest at

higher valuations. We have identified two key sectors that can witness increased PE

activity, given the favorable demographics in the Kingdom.

The education sector: According to a report from Kuwait Finance House, the GCC

education market stands at an estimated $36 billion with the private sector accounting

for about a paltry 14% of the overall market size. According to Saudi Arabia’s Education

minister, King Abdullah recently approved a five-year plan worth about SR80 billion to

build 1,500 nurseries, train about 25,000 teachers and establish educational centers and

other related projects to strengthen the education sector. The funding is in addition to

the considerable portion apportioned towards the sector in the budget. The Kingdom

hopes to see 450,000 vocational school graduates annually by the next year, rising from

94,000 in 2009. However, despite all the government efforts, the quality of education

still lags global standards and there is substantial scope for improvement in the quality

and delivery of education services by private players. Given the favorable demographics

in Saudi Arabia and attractive industry dynamics, the education sector holds immense

opportunity and is likely to witness increased interest from PE players.

Healthcare is another sector with immense potential. KSA, which already has the

highest healthcare expenditure in the GCC, continues to strive towards improving its

health care infrastructure. Rising population, growth in lifestyle-related diseases, coupled

with low-level of health care penetration, highlight the potential of the market.

Healthcare, which has historically lagged other sectors, partly because of government

inefficiency and bureaucracy, is expected to receive fresh impetus as the government

ramps up healthcare budgets. With millions of new healthcare consumers expected to be

added with the development of new economic cities, demand for healthcare services is

expected to increase. Additionally, increasing healthcare awareness and rise in per capital

income has made people more demanding towards quality healthcare services. However,

the government on its own would be unable to meet the rising demand and as a result,

the private sector is expected to play an increasingly important role in providing

healthcare services. The oversubscription of the Al Hammadi Company IPO points to

investor interest in tapping opportunities in the Saudi healthcare sector.

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 5

Government’s commitment to infrastructure build up

The recent infrastructure initiatives in urban centres, setting up of five economic cites,

measures to expand Saudi’s footprint in downstream refining and fast tracking key railway

projects, displays the government’s commitment to sustained economic growth. Capital

expenditure, which accounted for about 19% of total government expenditure during the

previous decade, has increased to 32% in 20134, the highest share in the GCC region after

Qatar. It is estimated that investments worth SR500 billion5 would be made in building

economic cities as domestic manufacturing bases for various industries. Large scale

investments done in the nation’s rail network will assist growth in infrastructure, trade and

tourism sectors. The Haramain high-speed link connecting Mecca with Medina is scheduled

to be completed by the end of next year. Moreover, the North South Railway has been given

priority on account of its economic and strategic importance, as this will assist mining activity

in the Northern areas. Completion of key infrastructure projects in important business centres

is also in full swing. All these initiatives will help the Kingdom to meet the crucial goal of

diversifying its overall economy and could attract a considerable amount of foreign capital.

Fostering the development of these industrial cities will ensure migration of the productive

youth workforce to these areas and thereby funnel the benefits of economic development in

the key sections of the society. There is now more openness to public-private partnerships

in infrastructure projects and this could underpin Private Equity’s role in contributing to

infrastructure development in the nation.

Increased Spending on Socially Relevant Sectors

Sources: Ministry of Finance *Budgeted Allocation

Rising Share of Capital Expenditure

Sources: Ministry of Finance

Saudi Arabia Infrastructure Projects: Value

and Number of Projects

Source: Zawya, KFHR

4 http://www.sama.gov.sa/sites/samaen/ReportsStatistics/statistics/Pages/YearlyStatistics.aspx 5 http://www.arabnews.com/news/492731

0

60

120

180

240

2005 2006 2007 2008 2009 2010 2011 2012 2013* 2014 F

SR B

illion

Education & Manpower Developments Health & Social Affairs

Municipality Services Transportation & Telecommunication

Water, Agriculture & Infrastructure

390 413 439579 589 648 607

120 138188

225 264278

248

0

250

500

750

1,000

2008 2010 2012 2014F

SR B

illion

Current Expenditure Capital Expenditure

0

75

150

225

300

$0

$25

$50

$75

$100

Roads

Metr

o

Port

s

Airport

s

Bridges

Railw

ay

Oth

ers

Billion

Value (LHS) No.of Project (RHS)

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 6

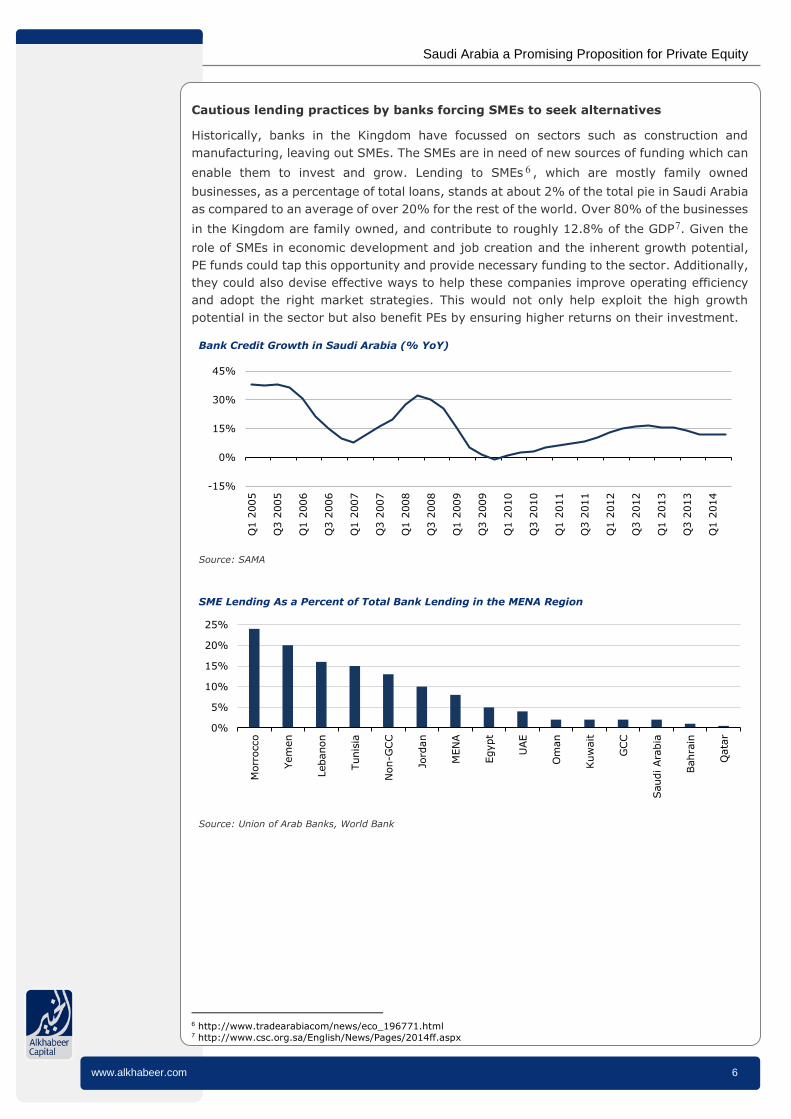

Cautious lending practices by banks forcing SMEs to seek alternatives

Historically, banks in the Kingdom have focussed on sectors such as construction and

manufacturing, leaving out SMEs. The SMEs are in need of new sources of funding which can

enable them to invest and grow. Lending to SMEs 6 , which are mostly family owned

businesses, as a percentage of total loans, stands at about 2% of the total pie in Saudi Arabia

as compared to an average of over 20% for the rest of the world. Over 80% of the businesses

in the Kingdom are family owned, and contribute to roughly 12.8% of the GDP7. Given the

role of SMEs in economic development and job creation and the inherent growth potential,

PE funds could tap this opportunity and provide necessary funding to the sector. Additionally,

they could also devise effective ways to help these companies improve operating efficiency

and adopt the right market strategies. This would not only help exploit the high growth

potential in the sector but also benefit PEs by ensuring higher returns on their investment.

Bank Credit Growth in Saudi Arabia (% YoY)

Source: SAMA

SME Lending As a Percent of Total Bank Lending in the MENA Region

Source: Union of Arab Banks, World Bank

6 http://www.tradearabiacom/news/eco_196771.html 7 http://www.csc.org.sa/English/News/Pages/2014ff.aspx

-15%

0%

15%

30%

45%

Q1 2

005

Q3 2

005

Q1 2

006

Q3 2

006

Q1 2

007

Q3 2

007

Q1 2

008

Q3 2

008

Q1 2

009

Q3 2

009

Q1 2

010

Q3 2

010

Q1 2

011

Q3 2

011

Q1 2

012

Q3 2

012

Q1 2

013

Q3 2

013

Q1 2

014

0%

5%

10%

15%

20%

25%

Morr

occo

Yem

en

Lebanon

Tunis

ia

Non-G

CC

Jord

an

MEN

A

Egypt

UAE

Om

an

Kuw

ait

GCC

Saudi Ara

bia

Bahra

in

Qata

r

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 7

The PE industry in Saudi Arabia remains under penetrated

The PE industry in Saudi Arabia is under penetrated and in a nascent stage of development,

largely hampered by regional geo-political concerns, and business and cultural challenges.

The global financial crisis had also increased risk-aversion amongst investors making it harder

for PEs to raise funds and exit previously entered deals. Many fund managers were forced to

downsize, raising doubts about the sustainability of PE funds in the region. However, much

of these concerns have subsided following the dramatic change in the financial and macro-

economic landscape in recent years. The investment cycle appears on the upturn and many

funds seem to be witnessing good traction in fund raising. Saudi Arabia’s progress is evident

from the recent World Bank study, which has ranked the Kingdom above all the GCC

countries, except the UAE, in the “Doing Business” index for the current year.

Increasing Number of Recent Deals Shows Rising Confidence Of PE Players

Improvement in risk appetite and receding global macro-economic concerns have resulted

in both regional and international private equity firms showing significant interest in Saudi

companies. On the other hand, the rise in Saudi equity markets has provided invested PE

funds with an opportunity to exit some investments.

According to Bloomberg, Saudi Arabian companies raised $760 million through share sales

in the six months through June 2014, the most active first half since 2009. The recent rally

in markets has resulted in many IPOs, which have witnessed good investor interest. The

recent IPO by Abdul Mohsen Al Hokair Group for Tourism and Development Company (Al

Hokair Group) was oversubscribed 11.9 times. Private equity player, Jadwa Investments

utilized the market opportunity to offload part of its investment in the company via the

IPO route.

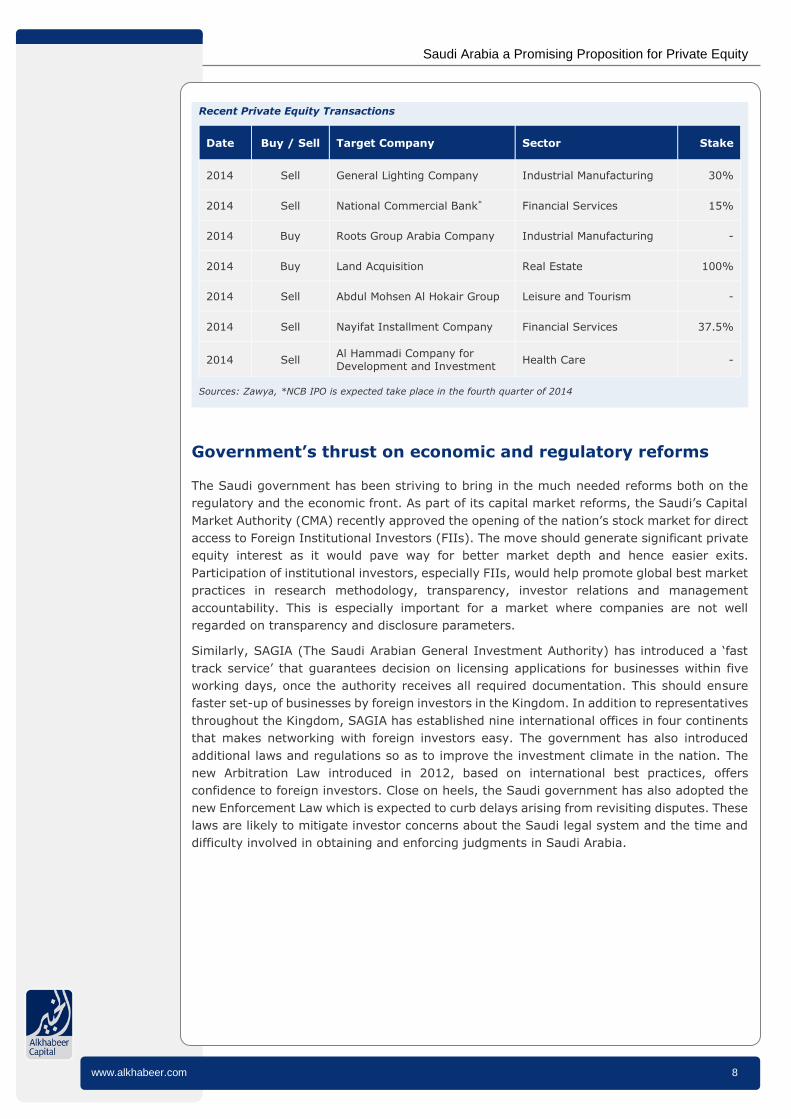

Private Equity Transactions in Saudi Arabia

Source: Zawya

The oversubscription of the IPO of Al Hammadi Company for Development and Investment

can be ascribed to high investor confidence in the growth potential of the Saudi healthcare

sector.

Some notable PE exits have also been witnessed recently. Carlyle Group successfully sold

its 30% stake in General Lighting Company, selling it to Royal Philips. Similarly, NBK

Capital sold its 38% stake in Nayifat Instalment Company to Falcom Financial Services,

after transforming the latter into an efficient financing company with an extensive

countrywide network catering to the needs of underserved consumers and SME businesses.

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Buy Sell

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 8

Recent Private Equity Transactions

Date Buy / Sell Target Company Sector Stake

2014 Sell General Lighting Company Industrial Manufacturing 30%

2014 Sell National Commercial Bank* Financial Services 15%

2014 Buy Roots Group Arabia Company Industrial Manufacturing -

2014 Buy Land Acquisition Real Estate 100%

2014 Sell Abdul Mohsen Al Hokair Group Leisure and Tourism -

2014 Sell Nayifat Installment Company Financial Services 37.5%

2014 Sell Al Hammadi Company for Development and Investment

Health Care -

Sources: Zawya, *NCB IPO is expected take place in the fourth quarter of 2014

Government’s thrust on economic and regulatory reforms

The Saudi government has been striving to bring in the much needed reforms both on the

regulatory and the economic front. As part of its capital market reforms, the Saudi’s Capital

Market Authority (CMA) recently approved the opening of the nation’s stock market for direct

access to Foreign Institutional Investors (FIIs). The move should generate significant private

equity interest as it would pave way for better market depth and hence easier exits.

Participation of institutional investors, especially FIIs, would help promote global best market

practices in research methodology, transparency, investor relations and management

accountability. This is especially important for a market where companies are not well

regarded on transparency and disclosure parameters.

Similarly, SAGIA (The Saudi Arabian General Investment Authority) has introduced a ‘fast

track service’ that guarantees decision on licensing applications for businesses within five

working days, once the authority receives all required documentation. This should ensure

faster set-up of businesses by foreign investors in the Kingdom. In addition to representatives

throughout the Kingdom, SAGIA has established nine international offices in four continents

that makes networking with foreign investors easy. The government has also introduced

additional laws and regulations so as to improve the investment climate in the nation. The

new Arbitration Law introduced in 2012, based on international best practices, offers

confidence to foreign investors. Close on heels, the Saudi government has also adopted the

new Enforcement Law which is expected to curb delays arising from revisiting disputes. These

laws are likely to mitigate investor concerns about the Saudi legal system and the time and

difficulty involved in obtaining and enforcing judgments in Saudi Arabia.

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 9

Challenges Remain

Although Saudi Arabia is emerging as the regional favourite in terms of the PE opportunities,

there are underlying challenges facing PE players that have or are in the process of

establishing a presence in the market.

Bureaucratic delays

Although Saudi Arabia has simplified some laws and procedures, the bureaucracy is slow-

moving, especially the length of time required for the various regulators. For example, the

change of ownership of a SAGIA licensed company requires an approval from SAGIA which

can be a lengthy and unpredictable process. Acquiring a stake in listed companies comes

under the purview of the capital market regulator which might result in additional delays for

approval. Moreover, acquiring controlling stakes in companies is marred with regulatory and

legal limitations. On the other hand, structuring an exit can be difficult as there is a

mandatory two-year lock-up period for the founding shareholders of a closed joint stock

company (CJSC) from the date of its incorporation or conversion. The restriction also applies

to new investors who joined the CJSC through a share subscription.

Legal, corporate governance & disclosure issues

Lack of a transparent and reliable legal framework remains an obstacle to the development

of the private equity market. Firstly, finding a deal in Saudi Arabia is a difficult task in itself

given the poor track record of firms in matters relating to corporate governance. Difficulty in

obtaining accurate financial information of companies has often been cited as a key problem

faced by potential buyers in the region. Moreover, the influence of family-owned businesses

usually hinders the process of corporate disclosures, limiting transparency.

Dispute resolution norms absent

Absence of appropriate bankruptcy laws also presents significant uncertainty to PE investors,

should any of the portfolio companies fail. Saudi Arabia practises Shariah law which primarily

governs contractual arrangements between parties in general. The broad and general nature

of the Shariah means that KSA courts are subject to interpretation of individual clerics. This

flexibility and the absence of judicial precedent results in ambiguity in the scope,

interpretation and enforceability of transaction documents. This could lead to problems in

case of disputes that require arbitration or contract enforcement.

Laws in KSA prevent the use of put options which is generally used as a mechanism that can

provide an alternative exit for the PE investor. According to the World Bank’s International

Finance Corporation, Saudi Arabia ranks 140th out of 183 countries for enforcing contracts.

Added to that, the legal delays put PE investors at a significant disadvantage. The potential

for PE deals is also limited by the lack of a liquid secondary market and the high capital gains

tax imposed by the Saudi Capital Market authority on non-Gulf investors. Compare this with

Egypt, where the PE market is more mature and corporate legal system is based on the

English law and assisted by more developed courts. Banks in Egypt have been very supportive

of PEs in terms of financing deals and are familiar with the working model of PEs. Domestic

firms are also more liberal and understand the benefits of bringing a PE investor on board.

Laws do not provide adequate protection to minority shareholders

Minority investors are at a significant disadvantage as regulations governing preferred

shares, takeovers and squeeze-out provisions are either unclear or absent altogether.

Therefore, Saudi Arabia has failed to enthuse much PE interest despite ranking as the 22nd

most business-friendly country out of 185 economies worldwide in the World Bank’s “Doing

Business 2013” report.

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 10

Resistance to non-family ownership control

As highlighted earlier, a large number of the businesses in Saudi Arabia are family owned.

Some have enough funds for expansion, while there are others which lack access to finance.

These family businesses have grown over the years and have the potential and need to move

on to the next level. A PE player can bring in the much needed capital as well as expertise to

help these businesses take the next leap. However, most family businesses are reluctant to

part sell stakes, perceiving it to be a loss of family wealth.

Even those firms that are cash-starved generally first approach close family members and

friends for assistance rather than outsiders, including private equity. Therefore, making in-

roads into family businesses and convincing them of the strategic benefits that a private

equity can bring to their business is a big challenge. The problem is compounded when there

are multiple families involved, as wading through different voices requires certain skills and

understanding of the dynamics of each of those families.

Unrealistic valuation expectations

As discussed above, most businesses in Saudi Arabia are family-owned, going back a number

of generations. Therefore the owner attaches a high value to their business on account of the

emotional attachment. Frenzy of investment activity in the region during the pre-crisis period

led to over estimation of the market opportunity and demanding of high market valuations

by business owners. However, PEs have now turned cautious as some of them are being

forced to hold on to their portfolio companies longer than expected, particularly those which

belong to sectors that have been impacted more severely by the economic downturn of 2008.

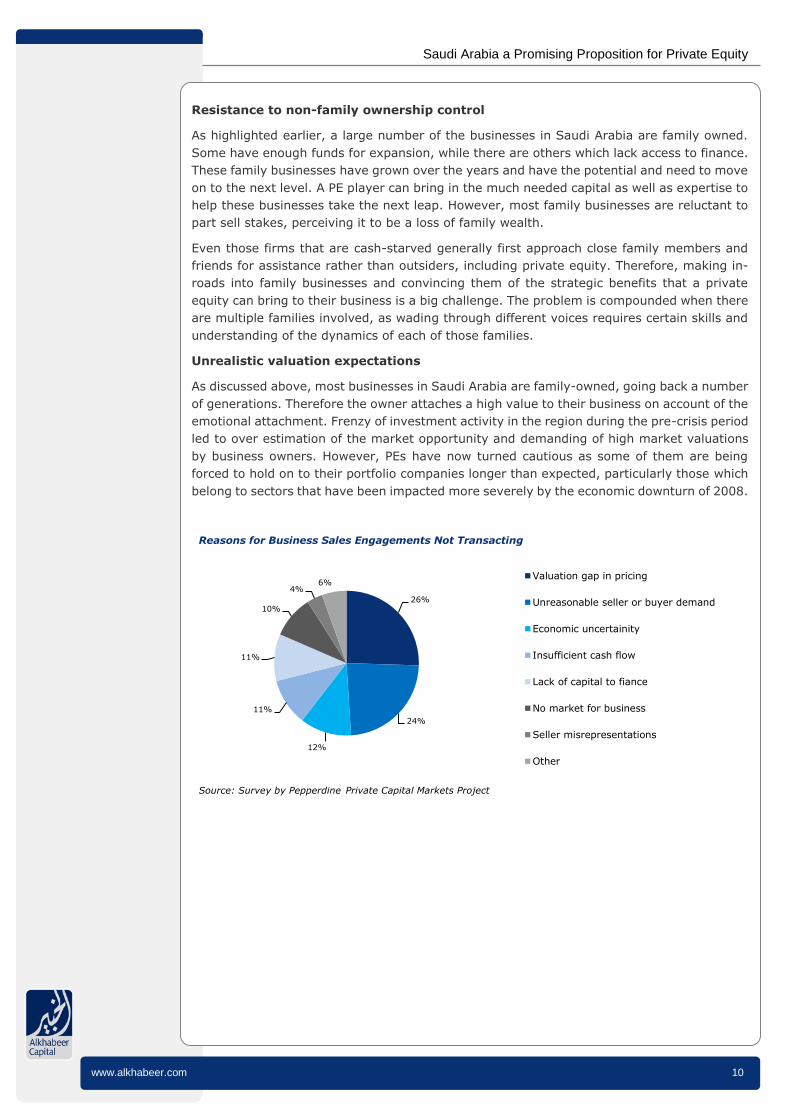

Reasons for Business Sales Engagements Not Transacting

Source: Survey by Pepperdine Private Capital Markets Project

26%

24%

12%

11%

11%

10%

4%6%

Valuation gap in pricing

Unreasonable seller or buyer demand

Economic uncertainity

Insufficient cash flow

Lack of capital to fiance

No market for business

Seller misrepresentations

Other

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 11

Win-Win Strategies to Ensure Healthy Deal Flow

As discussed above, PE investments in Saudi Arabia are innately complex, and it is imperative

that both the investor and the investee realize the importance of win-win strategies for a

successful deal in this niche and inherently complex market.

Understanding the social setting and business culture

Saudi Arabia is unique as its businesses are culturally based on longstanding relationships

and trust rather than rigid schedules and legalities. PE team would gain vastly by

understanding this cultural aspect. The fund manager needs to understand family concerns

and form relationships to gain trust amongst the owners. PE firms that have a local team for

conducting business in addition to market knowledge and strong business networks will have

an added advantage. “Who you know is more important than what you know” and family

businesses will only consent to an external board member if they have confidence in the PE

and foresee strong value addition in the relationship.

Appropriate due diligence

Every partnership has its unique set of challenges and concerns, but win-win deals based on

mutual trust and good legal framework are imperative. Businesses need to disclose true state

of finances for inspection, accompanied by appropriate due diligence by PEs for assessing

target companies. The PE fund managers can seek assistance from local law firms, industry

experts and auditors, to gauge any possible risks in acquiring the company.

Assure owners that PE partnership is not limited to financing, but will aid in value

creation

With Saudi government’s active liberalisation policy, smaller family owned businesses are ill

prepared to face the challenges of globalization and stiff competition from international

companies. PE firms can step in to address these challenges to bring in the necessary

technical expertise and provide strategic vision and professionalism.

a) Assist in value creation

PE firms bring in value addition, beyond financial planning, by way of operational

improvements, arising from deep industry and functional expertise. Businesses should

acknowledge that PE firms will position the company for future growth and profitability, to

achieve their targeted return on exit, making it a win-win proposition.

A case in point, the Carlyle Group acquired a 30% stake in Saudi Arabia’s largest lighting

fixture manufacturer, General Lighting Company (GLC) in 2010. In the four years through

exit, the PE firm helped GLC to expand its business focus into an international lighting player.

GLC became active in more than thirty markets, set up a distributor network in twelve African

countries and also acquired a large lighting company in Malaysia, Davex. Production

increased two-fold to 15 million units a year with the addition of a third factory in Riyadh.

b) Help to promote professionalism and corporate governance

Family businesses in Saudi Arabia are considered unprofessional, with opaqueness in financial

disclosures, absence of corporate governance policies and succession plans to name a few.

A PE partner can complement the local businesses by lending support to set up sound

business practices and policies. PE firms can assist in setting up processes for financial

reporting, risk management and compliance measures.

c) To ensure orderly succession plans

International studies have shown that only about 33% of the family businesses continue to

exist through the second generation, while the number drops to 10% when they move on to

the third generation, and merely 4% survive to the fourth generation. Saudi businesses are

often exposed to internal family disputes, especially after the death of the founder of the

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 12

company. About SR15 billion worth frozen assets in the Kingdom are mainly due to internal

squabbles. A PE being a third party to the business can help to formulate a succession plan

and address issues relating to ownership rights that is in harmony with the business vision.

Create flexible investment models to avoid conflicts

a) Stake holding pattern

Unlike the Western model, private equity stake in the GCC region companies is limited to a

minority, mainly due to government restriction on foreign ownerships and reluctance of the

investee company to part with ownership. This model however is also likely to benefit the PE

investor, as the owners have well established business connections, market access and are

well adept to the local know how. A PE firm vying for a greater share could risk losing the

existing management’s commitment and focus. A PE investor could look to acquiring a stake

of about 20% to 35%, and this trend is likely to continue for some time to come.

b) Pre-deciding the exit strategies

Predetermined and well-defined exit strategies are crucial for a successful PE deal. A mutual

agreement on an exit schedule prior to investing would result in more commitment from both

the parties. It is very important that the PE fund manager is aware of the seller’s business

intent since few businesses intend to go the IPO route to tap large flotation by public

subscription and provide a market exit to the PE.

Exit Strategies for Saudi Arabia

Of the three broadly prevalent exit strategies globally, namely IPOs, trade sales and

secondary buyouts, the latter (a PE firm selling of one of its portfolio companies to another

sponsor) is not very prevalent in the country.

Trade sales (stake sale to another corporate entity) is the most common type of exit

in the region. Trade sale exits usually offer better terms and higher valuations, translating

into greater returns. Owners can get a premium valuation, arising from synergetic

opportunities to the final acquirer. Regional as well as international buyers looking to

expand in the region, business customers and suppliers can compete for acquiring the

stake for sale.

In March 2014, Netherlands's Philips entered into an agreement to acquire 51% of General

Lighting Company (GLC) discussed earlier. The joint venture named ‘Philips Lighting Saudi

Arabia’, will help Philips expand its footprint in the Kingdom augmented with GLC’s deep

local market knowledge. This acquisition comes at a time, when the lighting market in the

country is expected to post robust growth, thanks to increased construction spending and

energy efficient lighting initiatives. GLC will benefit from Philips expertise in LED technology

and its global supply base.

The IPO route: Very few PE-backed IPOs have been listed on the Saudi exchange in the

past few years. Near absence of institutional investors, CMA regulations for disclosures,

administrative delays, and six-month lock-up period for original shareholders have been

deterrents for selecting the IPO route. Nevertheless, exits via the IPO route are expected

to increase, with fund managers assisting the company with IPO listing and corporate

governance practices. Companies in Saudi Arabia typically offer 30% of their share capital

in an IPO, (unlike the UAE where the minimum floatation needed is about 50%) while

retaining managerial control of the business. The IPO route can help companies generate

funds for business expansion.

Saudi Arabia a Promising Proposition for Private Equity

www.alkhabeer.com 13

c) Stipulating a lock in period

Not allowing to redeem or sell shares can bring in more commitment. Generally a lock up

period of 2-3 years can limit a fund’s ability to realize its investment during such a period.

On the other hand, a lock in period for the promoters would ensure that the current

management does not lose interest in the venture.

d) Clauses that allow promoters to buy back the PE investor’s stake:

To mitigate the risk of losing the controlling stake, family businesses could incorporate an

exit clause that allows them to buy back the external investor’s stake in the company since

exit options to funds are limited.

Win-Win valuations

Many a times a well-structured deal, which makes a lot of strategic sense, may not be

economically viable for the PE at a certain valuation. Therefore the entire deal needs to be

structured in such a way that it is a win-win situation for both the business owner as well as

the PE. Comparing international multiples for the purpose of valuations may not be the best

option for a country that has a different economic landscape compared to western peers.

Moreover, limited information on transaction and dearth of listed companies in the domestic

space make peer comparisons difficult. A PE firm evaluating a business can look at multiple

methods to arrive at an accurate and acceptable value. An important aspect of deal

negotiation is for the PE to convince the family business owner to shift his focus from the

current valuation to the prospective improvements that the PE could bring into the company,

post the acquisition.

About Us

www.alkhabeer.com 14

About Alkhabeer:

Alkhabeer Capital is a leading investment & asset management firm that provides world-class financial

products and services which help institutions, family groups and qualified investors.

It is licensed by Saudi Arabia’s Capital Market Authority (CMA) under license No. 07074-37. The Asset

Management area provides investment opportunities through a large and growing portfolio of public and

private funds in the areas of real estate, private equity and capital markets while the advisory area helps

clients improve their capital structures with a wide range of innovative investment and corporate finance

services and solutions.

Alkhabeer Capital has offices in Jeddah and Riyadh.

Disclaimer:

This document is issued by Alkhabeer Capital and it is intended for general information purposes only,

and does not constitute an offer to buy or subscribe or participate in any security, nor shall it (or any part

of it) form the basis of or be relied on in connection with or act as inducement to enter into any contract

whatsoever. This document is confidential in nature and is only intended for selected sophisticated

investors. If you have mistakenly received this document, you are hereby requested to disregard its

contents and return it to Alkhabeer Capital or destroy it. Alkhabeer Capital shall not be liable for any loss

that may arise from the use of this document or its contents or otherwise arising in connection therewith.

Alkhabeer Capital, its affiliates or funds managed by Alkhabeer Capital or its affiliates may own securities

or may be involved in advisory mandates in one or more of the aforementioned companies. Any

projections, opinion, and statements regarding future prospects contained in this document may not be

realized. All projections, opinions and statements included in this document constitute opinions of

Alkhabeer Capital as of the date of this document, and are subject to change without notice. Any type of

past performance cannot be construed as a guarantee of future results. The value, price and income from

securities can go down as well as up. Investors may get back less than what they originally invested.

Changes in currency rates may have an adverse effect on the value, price or income of the securities.

For an illiquid security, it may be difficult for the investor to sell or realize the security and to obtain

reliable information about its value or the extent of the risks to which it is exposed.

The Capital Market Authority does not take any responsibility for the contents of this document, does not

make any representation as to its accuracy or completeness and expressly disclaims any liability

whatsoever for any loss arising from, or incurred in reliance upon, any part of this document.