Embed Size (px)

Citation preview

COMPANY LAWFINANCE

Saturday 11th August 2012

Lecturer: Rowin Gurusami

SHARES Transferable form of property, carrying rights and obligations, by which the interest of a member of a company limited by shares is measured (in accordance with s33 of Companies Act 2006)

A share is the interest of a shareholder in the company measured by a sum of money, for the purposes of liability in the first place, and of interest in the second, but also consisting of a series of mutual covenants entered into by all the shareholders inter se– Borland’s Trustee v Steel Bros & Co Ltd (1901)

Shares are personal property but do not comprise of any proprietary interest in company’s assets

Lecturer: Rowin Gurusami

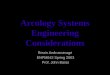

SHARES Share must be paid for (‘liability’)Nominal value of share fixes liabilityNo share can be issued below the nominal value

Share gives proportionate entitlement to dividends, votes and any return of capital (‘interest’)

Since share is a form of personal property, it is by nature transferrable

Sale price of shares do not need to reflect nominal value of share (so may be greater or less)

Lecturer: Rowin Gurusami

TYPE OF SHARES Class rights: rights attached to particular types of shares by company’s constitution (e.g. Dividends, return of capital, voting, right to appoint/remove director, etc...) Shares which have different rights from others are grouped together to form a class

Ordinary shares: if no differences between shares are expressed in constitution of company, then all shares are equity shares with same rights

Ordinary shares entitle holders to remaining divisible profits after any fixed level of dividend to preference shareholders

Lecturer: Rowin Gurusami

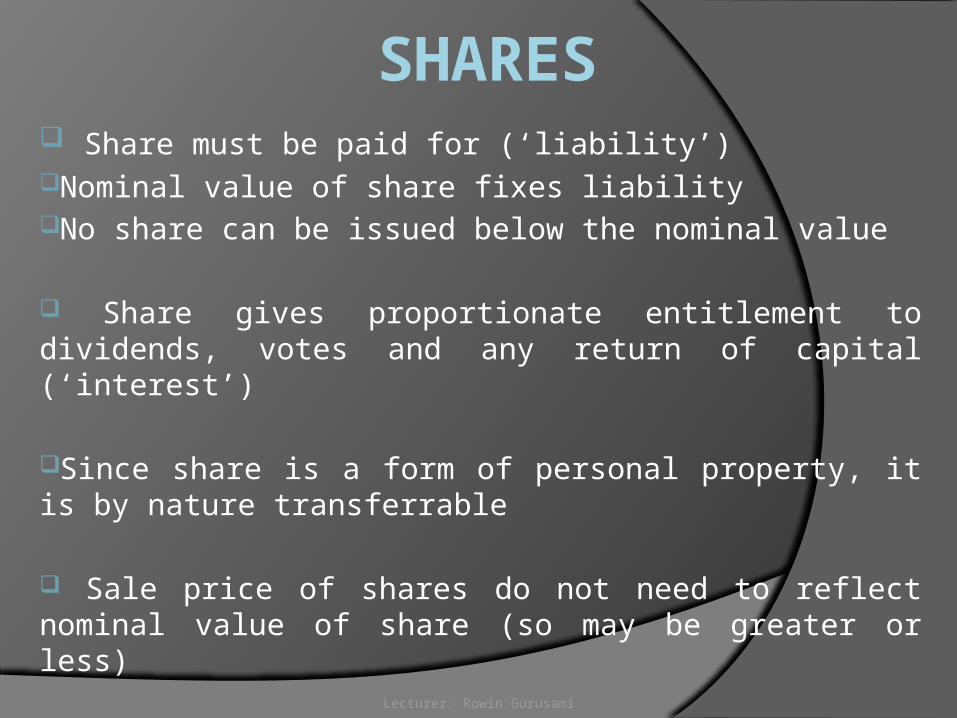

TYPE OF SHARES Preference shares: Attaching preferential rights

Fixed preferential cumulative dividend paid to holders in any year company has distributable profits Cumulative element means arrears become payable in respect of years no dividend is declared (All preferential shares are deemed to be cumulative – Webb v Earle [1875])

Also entitled to return of capital on winding-up in priority to ordinary shareholders Usually have restricted voting rights Not entitled to participate in any additional dividend over and above specified rate

Lecturer: Rowin Gurusami

VARIATION OF CLASS RIGHTS

Vested rights can only be varied by special resolution passed by at least three quarters of votes cast at separate class meeting or by written consent (s630 of CA 2006)

The following rules apply to variation:1. If class rights are set by articles and provide for

variation procedure, that procedure must be followed for any variation (even if it is less onerous than statutory procedure)

2. If class rights are defined otherwise than by article and there is no variation of procedure, statutory procedure applies

Lecturer: Rowin Gurusami

MINORITY PROTECTION In situations where class rights have been varied, a dissenting minority can apply to the court to have the variation cancelled as ‘unfairly prejudicial.

The following conditions have to be satisfied by the dissenting minority:-Hold not less than 15% of issued shares of class in question

-Not having consented to or voted in favour of variation

-Apply to the court within 21 days of consent being given by the class

Lecturer: Rowin Gurusami

ALLOTMENT OF SHARES The issue and allocation to a person of a certain number of shares under a contract of allotment

Allotment of shares is a form of contract (intending shareholder applies to company for shares, and company accepts)

Share allotted when person to whom it is allotted acquires unconditional right to be entered in register of members as holder of that share. Takes place when board of director considers application and formally resolves to allot the shares

Issue of shares takes place at later stage when letter of allotment or share certificate issued by company

Lecturer: Rowin Gurusami

ALLOTMENT OF SHARES Various methods of selling shares to public:1. Public offer2. Offer for sale3. Placing

Private companies cannot sell shares to public- Application for allotment must be made to directors

directly- After that, shares are allotted and issued and return

of allotment made to Registrar (similarly to a public company)

Lecturer: Rowin Gurusami

ALLOTMENT - DIRECTOR’S POWERS

Directors of private companies with one class of share have authority to allot shares (unless restricted by articles)

Directors of public companies or private companies with more than one class of share may not allot shares without authority from members

Authority may be given by articles or by ordinary resolution passed in general meeting

Authority to allot must be given until a specific date or for a specified period

Lecturer: Rowin Gurusami

PRE-EMPTION RIGHTS Rights of existing ordinary shareholders to be offered new shares issued by the company pro rata to their existing holding of that class of shares

If a company proposes to allot ordinary shares (i.e. Equity securities) wholly for cash, it has a statutory obligation to offer those shares first to holders of similar shares in proportion to their holdings

Must be on same or more favourable terms than what would have been offered to non-members

Lecturer: Rowin Gurusami

ISSUE OF SHARES Every share has a nominal value and may not be allotted at a discount to that (s580)

When shares allotted, company required to obtain in money or money’s worth, consideration of a value at least equal to nominal value of shares plus the whole of any premium

Issuing shares ‘at par’ means obtaining equal value

Although shares paid under nominal value, at time of insolvency, holders required to pay the remainder of nominal value (the ‘no-discount’ rule)

Lecturer: Rowin Gurusami

SHARE PREMIUM Share premium is excess received (either cash or other consideration) over nominal value of shares issued

Excess must be credited to a share premium account

Use of share premium account usually limited for bonus issues

Can be use to pay for fully paid shares under a bonus issue

Also used to pay issue expenses and commission in respect of new share issue

Lecturer: Rowin Gurusami

ISSUE OF SHARES Consideration for shares:1. Partly-paid shares2. Underwriting fees3. Bonus issue4. Money’s worth

Private companies may issue shares for inadequate consideration (usually by acceptance of goods or services at an over-value) provided directors are behaving reasonably and honestly (Re Wragg 1897)

Blatant and unjustified overvaluation will be declared invalid by the courts

Lecturer: Rowin Gurusami

ISSUE OF SHARES Public companies have to respect certain stringent rules:1. Must receive at least one quarter of nominal value

of shares and whole of premium (s586)2. Non-cash consideration must be independently

valued3. Non-cash consideration not accepted if undertaking

in consideration is to be performed more than 5 years after allotment

4. Undertaking to do work or perform services not accepted as consideration

5. Within 2 years of receiving trading certificate, company may not receive transfer of non-cash assets from subscriber to memorandum

Lecturer: Rowin Gurusami

SHARE CAPITAL Authorised share capital – removed by CA 2006

Issued and allotted share capital – type, class, number and amount of shares issued and allotted to specific shareholders Company need not issue all its share capital at once. Anything retained is unissued share capital

Called up share capital: amount company has required shareholders to pay now ore in the future on shares issued Paid up share capital: amount shareholders have actually paid on shares issued and called up

Loan capital: Debentures and other long-term loans to company

Lecturer: Rowin Gurusami

Lecturer: Rowin Gurusami

REDUCTION OF SHARE CAPITAL

Why?- Company suffered loss in value of assets and

reduce capital to reflect that fact- Company wishes to extinguish interests of some

members entirely (i.e. reduce nominal value of shares)

- Part of complicated arrangement capital, e.g. Replacing share capital with loan capital

Limited company can reduce issued share capital if it:- Has power to do so in articles- Passes a special resolution- Obtains confirmation of reduction from the court

Lecturer: Rowin Gurusami

REDUCTION OF SHARE CAPITAL Private company need not apply to court if special

resolution is supported with a solvency statement

Solvency statement is a declaration by directors (provided 15 days in advance of meeting where special resolution is to be voted on) stating that there is no ground to suspect the company is currently unable (or will unlikely to be able) to pay its debts for the next 12 months

For court application, main concern is the interests of the creditors and different classes of shareholders

Courts will usually ask company to advertise for creditors to state their objections (if any) to reduction of share capital

Lecturer: Rowin Gurusami

REDUCTION OF SHARE CAPITAL

This can be dispensed with if:- Pay off all creditors before application is made to

court, or- Produce to the court a guarantee (e.g. From the

company’s bank) that its existing debts will be paid in full

Another concern is how reduction affects different classes of shareholders

If reduction is (in the circumstances) a variation of class rights, consent of the class is required

Lecturer: Rowin Gurusami

REDEMPTION OF SHARES Issue shares that are to be redeemed at the option

of the company or the shareholder

Company may only redeem shares if there are still shares which cannot be redeemed

Only fully paid shares can be redeemed and they must be paid for on redemption

Only private companies may redeem shares out of capital

Otherwise redeemed from profits or proceeds of any fresh issue of shares made for purpose of redemption

Lecturer: Rowin Gurusami

PURCHASE OF OWN SHARES A limited company may purchase its own shares

subject to any restriction or prohibition in the company’s articles

Company may not purchase its own shares if, as a result, there would no longer be any issued shares other than redeemable ones (s690(2))

Only fully paid shares can be purchased and they must be paid for on purchase (s691)

Purchased shares must be cancelled unless they are held ‘in treasury’ from where they can be sold/transferred (e.g. to employee share scheme)

Also return to the Registrar to be made within 1 month

Lecturer: Rowin Gurusami

PURCHASE OF OWN SHARES To finance purchase of its own shares, company

has to use:- distributable profits (s692(2))- proceeds of a fresh share issue made (s692(2))

Private companies may (under the Companies Act 1985) purchase its own shares out of capital (s692(1) and s709)

Under Companies Act 2006, for private company, power to purchase no longer need to be contained in articles (although articles can restrict or prohibit this exercise)

Lecturer: Rowin Gurusami

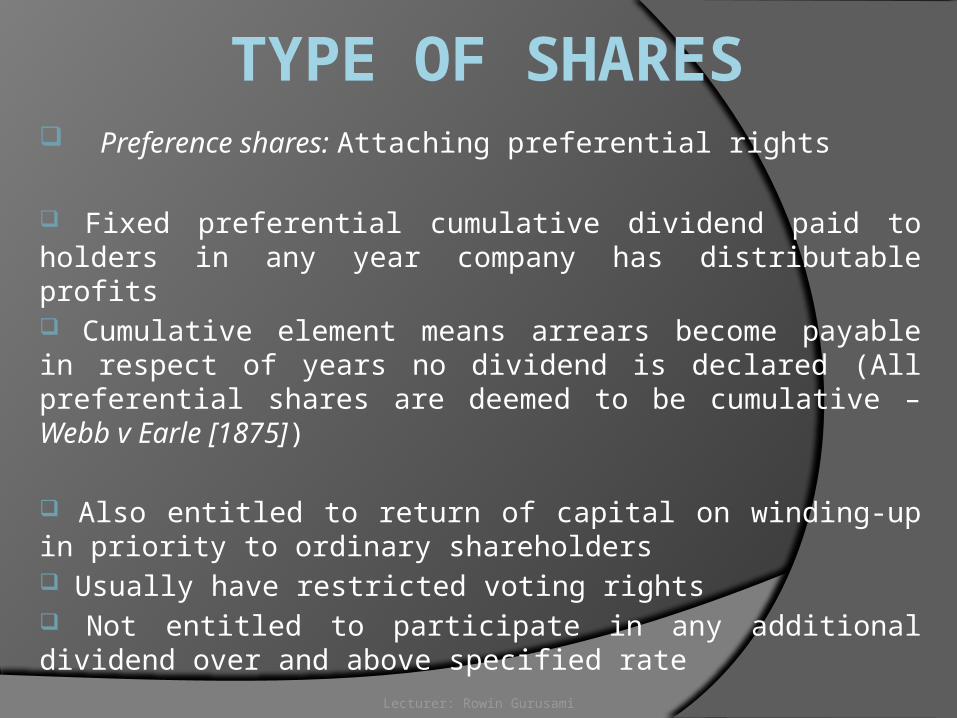

FINANCIAL ASSISTANCE Companies can give financial assistance for the

acquisition of their shares (restrictions for public co.)

- By way of gift / gift of money to buy the shares- Guaranteeing or providing security for a loan given

by a third party

Public companies can only give financial assistance if:

- Purpose of assistance is something other than proposed acquisition

- Assistance is only incidental part of a larger purpose- Assistance is given in good faith in best interests of

company

Lecturer: Rowin Gurusami

DISTRIBUTING DIVIDENDS Dividend is an amount payable to shareholders

from profits or other distributable reserves

Company may only pay dividend out of ‘distributable profits’ (s830(1))

Distributable profits means accumulated, realised profits less accumulated realised losses

Public company may only make a distribution if its net assets are, at the time, not less than the aggregate of its called-up share capital and undistributable reserves (s831)

Lecturer: Rowin Gurusami

INFRINGEMENTS OF DIVIDEND RULES

If dividend paid otherwise than out of distributable profits, directors and shareholders may have to make good to the company the unlawful distribution

1. Directors liable if they recommend or declare dividend which they know is paid out of capital

2. Directors liable if, without preparing accounts, they declare/recommend dividend paid out of capital

3. Directors liable if they make mistake of law or interpretation of constitution, leading to them declaring/recommending unlawful dividend

Lecturer: Rowin Gurusami

INFRINGEMENTS OF DIVIDEND RULES

Position of member is as follows:1. Member may obtain injunction to restrain company

from paying unlawful dividend2. Members voting in GM cannot authorise payment of

unlawful dividend nor release liability of directors to pay it back

3. Company can recover from members an unlawful dividend if members knew or had reasonable grounds to believe it was unlawful (s847)

4. If directors have to make good unlawful dividend to company, they may claim indemnity from members who, at time, knew of irregularity

5. Members knowingly receiving unlawful dividend may not bring action against directors

Lecturer: Rowin Gurusami

LOAN CAPITAL Comprises all amounts borrowed for long-term, such as:-Permanent overdrafts from bank-Unsecured loans from bank or other party-Loans secured on assets from bank or other party

At some point, borrowing must be repaid while share capital is only returned to shareholders when company is wound up

Companies often issue long-term loans as capital in the form of debentures

Lecturer: Rowin Gurusami

DEBENTURES Formal legal document, i.e. written acknowledgement of a debt by company, normally containing provisions as to payment of interest and terms of repayment of principal

Debenture usually creates a charge over the company’s assets as security for the loan

Three main types of debentures:-Single debenture-Debentures issued as a series and usually registered-Debenture stock subscribed by large number of lenders

Lecturer: Rowin Gurusami

REGISTER OF DEBENTUREHOLDERS

No statutory obligation to maintain a register of debentureholders

However, company usually required to maintain a register by the debenture of debenture trust deed when debentures are issued as a series or with debenture stock

- Register must be kept at registered office (s743)- Register open to inspection by any person (unless constitution or trust deed provide otherwise) and holder of denture may require a copy of deed (s749)- Register properly kept in accordance with requirements of Companies Act 2006

Lecturer: Rowin Gurusami

RIGHTS OF DEBENTUREHOLDERS

Rights are very similar to those of shareholders-Own transferable company securities-Issue procedure is the same-Similar procedure of transfer

However there are differences:-Debentureholder is creditor of the company-Deventureholder may not vote at general meetings-Debentures may be offered at discount to nominal value-Interest paid over debentures while shares only received dividends when there is distributable profits declared by directors-Debenture paid back before shareholder paid in insolvency

Lecturer: Rowin Gurusami

ADVANTAGES/DISADVANTAGES Advantages (for company):-Easily traded-Terms clear and specific-Assets subject to floating charge may be traded-Guaranteed income-Interest tax-deductible

Disadvantages (for company):-May have to pay higher rate of interest to attract-Interest payments mandatory-Remedy of liquidators by debentureholders-Crystallisation of floating charge not good for business

Lecturer: Rowin Gurusami

CHARGES Encumbrance upon real or personal property granting holder certain rights over that property. No title in property is passed

Often used as security for debt owed to charge holder

Principal purpose is to enable lender to recover from company in event of its default (usually in situations of impending insolvency)

Charge secured over company’s assets gives creditor (the ‘chargee’) a prior claim over other creditors to payment of that debt out of the specified assets

Lecturer: Rowin Gurusami

FIXED CHARGE Form of protection given to secured creditors relating to specific assets of a company

The chargee’s rights attach immediately to the property in question

Restricts the company’s power to deal with the charged asset without first obtaining creditor’s permission

Fixed charge can also be over future property to be acquired. The charge is deemed to come into existence as soon as the property is acquired by chargor (Holroyd v Marshall (1862))

Lecturer: Rowin Gurusami

FLOATING CHARGE Also requires identifiable property but it contemplates that chargor is free to deal with charged property in ordinary course of business without reference to chargor

Characteristics of floating charge defined in Re Yorkshire Woolcombers Association (1903):1. A charge on a class of assets of a company, present

& future2. Which class is, in ordinary course of company’s

business, changing from time to time3. Until holders enforce the charge, the company may

carry on business and deal with assets charged Does not attach to relevant assets until charge

crystallises

Lecturer: Rowin Gurusami

CRYSTALLISATION Crystallisation converts floating charge into an equitable fixed charge over the assets of company owned by it at the time (thus can include future acquired assets within scope of the charge – NW Robbie & Co Ltd v Witney Warehouse Co Ltd (1963))

Floating charges crystallise or harden (convert into a fixed charge) on certain relevant events:-Liquidation of company-Cessation of company’s business-Active intervention by chargee (usually through receiver)-When the charge contract so provides (specified events)-Crystallisation of another floating charge causing cessation of business

Lecturer: Rowin Gurusami

COMPARISON - FIXED/FLOATING Fixed charge more satisfactory form of security as it confers immediate rights over identified assets

Floating charge applicable to current assets (usually easier to realise than long term assets)

Holder of floating charge cannot be certain which assets form his security until charge crystallises

Preferential debts such as wages may be paid out first out of assets subject to floating charge

Holder of fixed charge over same property have priority

Floating charge automatically invalid if company goes insolvent within a year of creating charge (s245 Insolvency Act 1986). Period of six months only for fixed charge

Lecturer: Rowin Gurusami

PRIORITY OF CHARGES Fixed charges rank according to order of creation Floating charges also rank according to time of creation

Normally any fixed charge has priority over floating charge

Floating charge created before fixed charge only take priority when latter created, the fixed chargee had notice of clause in floating charge preventing later prior charge

If charged assets sold to 3rd party, chargee with fixed charge will have recourse in property (charge automatically transfers with property) while chargee with floating charge will only have recourse if 3rd party had notice of the charge

Lecturer: Rowin Gurusami

REGISTRATION OF CHARGES To be valid and enforceable, charges must be registered within 21 days of creation with the Registrar by either company or chargee

Registrar needs to be sent details of charge, such as date of creation, amount of debt secured, particulars of property, person entitled to it, etc.

Failure to deliver particulars will result in the company and its officers being liable to a fine

Non-delivery in time period results in charge being void against liquidator or any creditor of company Non-delivery also means money secured is payable forthwith on demand