Embed Size (px)

Citation preview

SANASA Development Bank PLC

REQUEST FOR PROPOSAL (RFP) For implementation of

Loan Origination System and Collections System

Contents

Invitation for Bids ................................................................................................................................................. 3

Introduction ......................................................................................................................................................... 4

Scope of Work .................................................................................................................................................... 5

Functional Requirements ...................................................................................................................................... 6

Technical Requirements ..................................................................................................................................... 16

Hardware Requirements ..................................................................................................................................... 18

Eligibility Criteria ................................................................................................................................................ 18

Service Level Agreement (SLA) ................................................................................................................................ 19

Project Time Schedule ....................................................................................................................................... 20

Payment Terms ................................................................................................................................................. 21

Warranty & Annual Maintenance ......................................................................................................................... 21

Terms and Conditions during Warranty and AMC Period ....................................................................................... 22

Selection Strategy ............................................................................................................................................. 23

Delay in adhering to the project timelines/Liquidated damages ............................................................................... 23

General Terms and Conditions ............................................................................................................................ 24

Order Cancellation ............................................................................................................................................. 24

Termination ....................................................................................................................................................... 24

Governing Law .................................................................................................................................................. 24

Force Majeure ................................................................................................................................................... 25

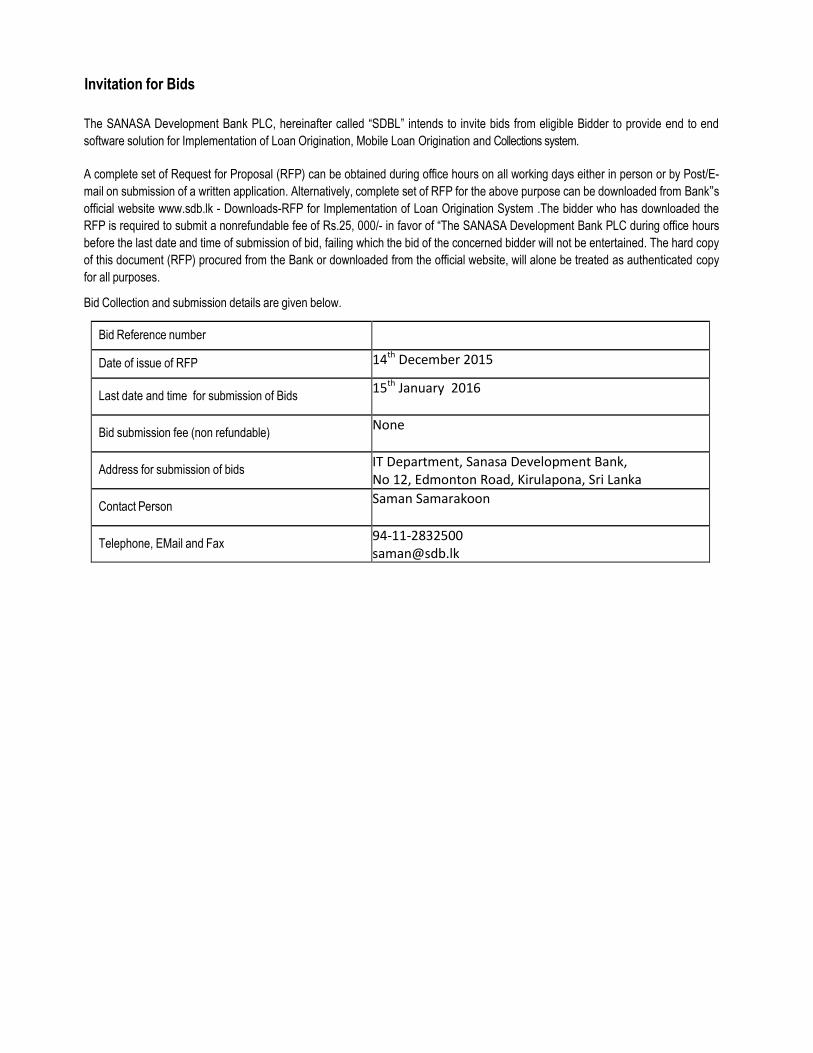

Invitation for Bids

The SANASA Development Bank PLC, hereinafter called “SDBL” intends to invite bids from eligible Bidder to provide end to end

software solution for Implementation of Loan Origination, Mobile Loan Origination and Collections system.

A complete set of Request for Proposal (RFP) can be obtained during office hours on all working days either in person or by Post/E-

mail on submission of a written application. Alternatively, complete set of RFP for the above purpose can be downloaded from Bank‟s

official website www.sdb.lk - Downloads-RFP for Implementation of Loan Origination System .The bidder who has downloaded the

RFP is required to submit a nonrefundable fee of Rs.25, 000/- in favor of “The SANASA Development Bank PLC during office hours

before the last date and time of submission of bid, failing which the bid of the concerned bidder will not be entertained. The hard copy

of this document (RFP) procured from the Bank or downloaded from the official website, will alone be treated as authenticated copy

for all purposes.

Bid Collection and submission details are given below.

Bid Reference number

Date of issue of RFP 14th December 2015

Last date and time for submission of Bids 15th January 2016

Bid submission fee (non refundable) None

Address for submission of bids IT Department, Sanasa Development Bank, No 12, Edmonton Road, Kirulapona, Sri Lanka

Contact Person Saman Samarakoon

Telephone, EMail and Fax 94-11-2832500 [email protected]

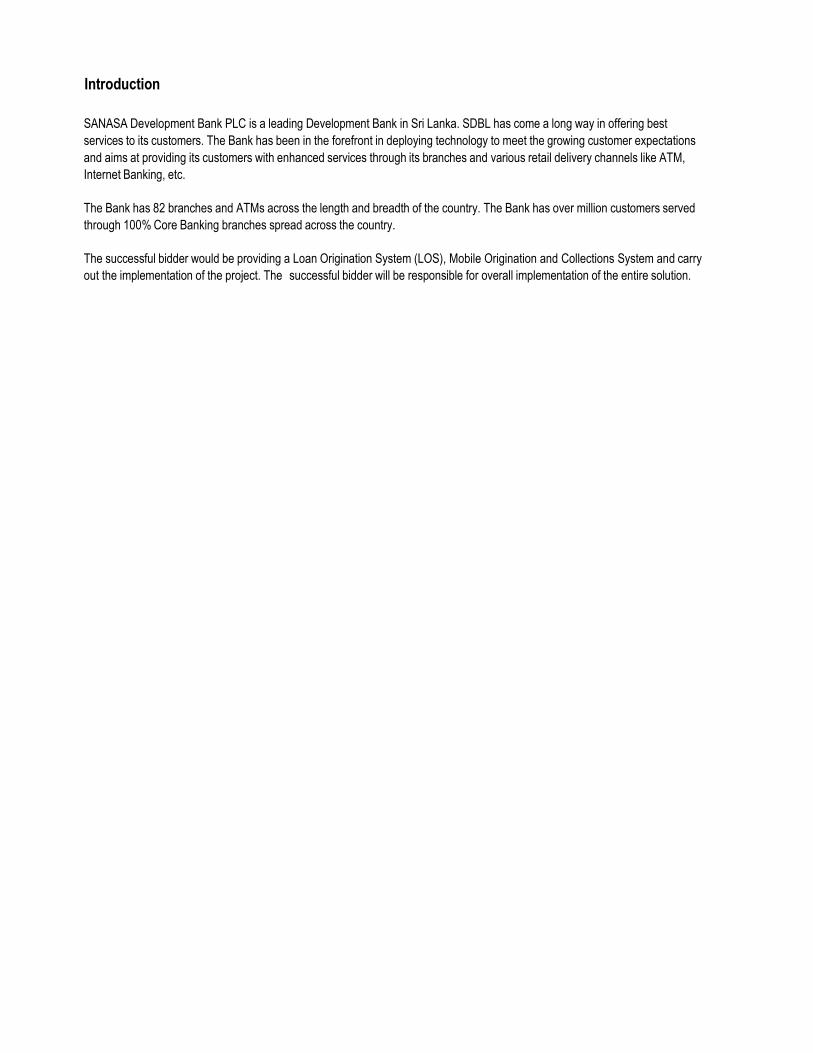

Introduction

SANASA Development Bank PLC is a leading Development Bank in Sri Lanka. SDBL has come a long way in offering best

services to its customers. The Bank has been in the forefront in deploying technology to meet the growing customer expectations

and aims at providing its customers with enhanced services through its branches and various retail delivery channels like ATM,

Internet Banking, etc.

The Bank has 82 branches and ATMs across the length and breadth of the country. The Bank has over million customers served

through 100% Core Banking branches spread across the country.

The successful bidder would be providing a Loan Origination System (LOS), Mobile Origination and Collections System and carry

out the implementation of the project. The successful bidder will be responsible for overall implementation of the entire solution.

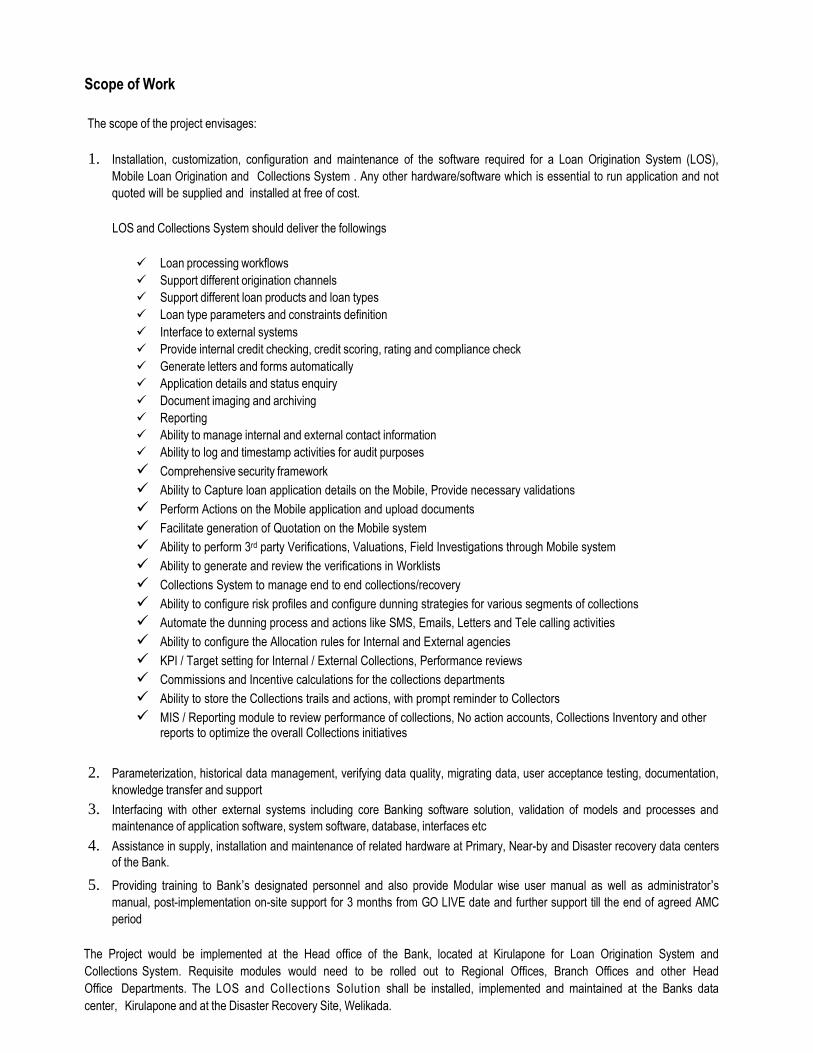

Scope of Work

The scope of the project envisages:

1. Installation, customization, configuration and maintenance of the software required for a Loan Origination System (LOS),

Mobile Loan Origination and Collections System . Any other hardware/software which is essential to run application and not

quoted will be supplied and installed at free of cost.

LOS and Collections System should deliver the followings

Loan processing workflows

Support different origination channels

Support different loan products and loan types

Loan type parameters and constraints definition

Interface to external systems

Provide internal credit checking, credit scoring, rating and compliance check

Generate letters and forms automatically

Application details and status enquiry

Document imaging and archiving

Reporting

Ability to manage internal and external contact information

Ability to log and timestamp activities for audit purposes

Comprehensive security framework

Ability to Capture loan application details on the Mobile, Provide necessary validations

Perform Actions on the Mobile application and upload documents

Facilitate generation of Quotation on the Mobile system

Ability to perform 3rd party Verifications, Valuations, Field Investigations through Mobile system

Ability to generate and review the verifications in Worklists

Collections System to manage end to end collections/recovery

Ability to configure risk profiles and configure dunning strategies for various segments of collections

Automate the dunning process and actions like SMS, Emails, Letters and Tele calling activities

Ability to configure the Allocation rules for Internal and External agencies

KPI / Target setting for Internal / External Collections, Performance reviews

Commissions and Incentive calculations for the collections departments

Ability to store the Collections trails and actions, with prompt reminder to Collectors

MIS / Reporting module to review performance of collections, No action accounts, Collections Inventory and other reports to optimize the overall Collections initiatives

2. Parameterization, historical data management, verifying data quality, migrating data, user acceptance testing, documentation,

knowledge transfer and support

3. Interfacing with other external systems including core Banking software solution, validation of models and processes and

maintenance of application software, system software, database, interfaces etc

4. Assistance in supply, installation and maintenance of related hardware at Primary, Near-by and Disaster recovery data centers

of the Bank.

5. Providing training to Bank’s designated personnel and also provide Modular wise user manual as well as administrator’s

manual, post-implementation on-site support for 3 months from GO LIVE date and further support till the end of agreed AMC

period

The Project would be implemented at the Head office of the Bank, located at Kirulapone for Loan Origination System and

Collections System. Requisite modules would need to be rolled out to Regional Offices, Branch Offices and other Head

Office Departments. The LOS and Collections Solution shall be installed, implemented and maintained at the Banks data

center, Kirulapone and at the Disaster Recovery Site, Welikada.

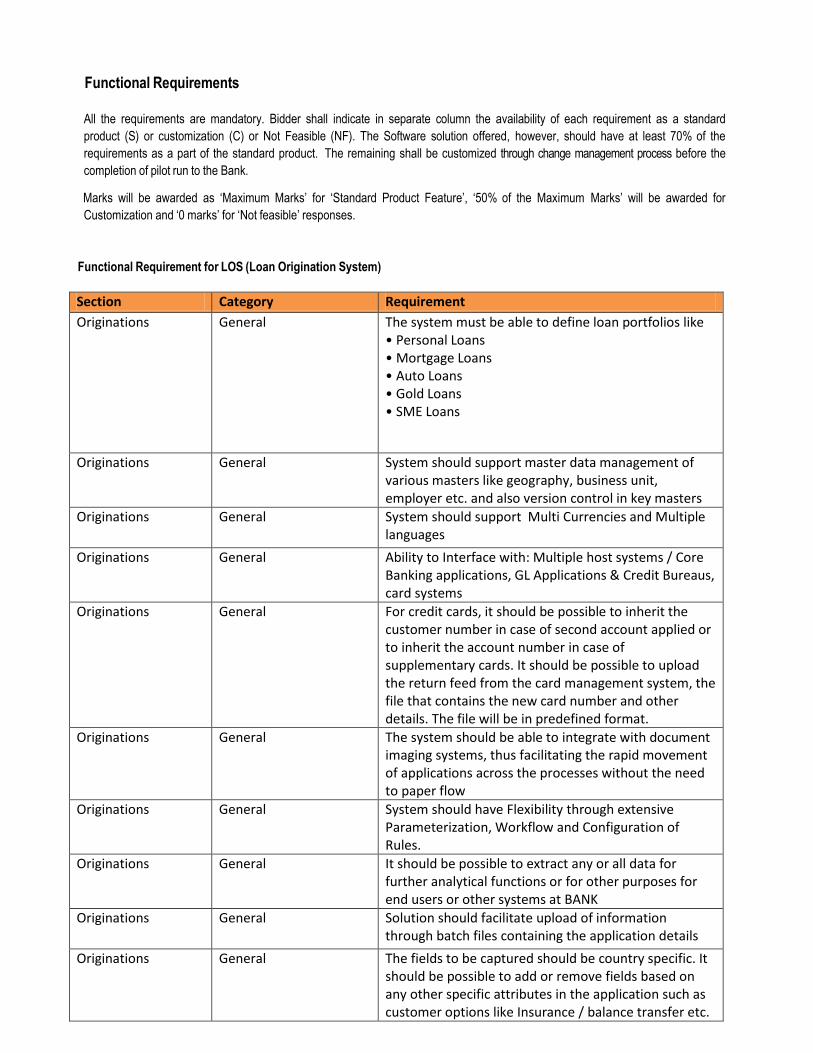

Functional Requirements

All the requirements are mandatory. Bidder shall indicate in separate column the availability of each requirement as a standard

product (S) or customization (C) or Not Feasible (NF). The Software solution offered, however, should have at least 70% of the

requirements as a part of the standard product. The remaining shall be customized through change management process before the

completion of pilot run to the Bank.

Marks will be awarded as „Maximum Marks‟ for „Standard Product Feature‟, „50% of the Maximum Marks‟ will be awarded for

Customization and „0 marks‟ for „Not feasible‟ responses.

Functional Requirement for LOS (Loan Origination System)

Section Category Requirement

Originations General The system must be able to define loan portfolios like • Personal Loans • Mortgage Loans • Auto Loans • Gold Loans • SME Loans

Originations General System should support master data management of various masters like geography, business unit, employer etc. and also version control in key masters

Originations General System should support Multi Currencies and Multiple languages

Originations General Ability to Interface with: Multiple host systems / Core Banking applications, GL Applications & Credit Bureaus, card systems

Originations General For credit cards, it should be possible to inherit the customer number in case of second account applied or to inherit the account number in case of supplementary cards. It should be possible to upload the return feed from the card management system, the file that contains the new card number and other details. The file will be in predefined format.

Originations General The system should be able to integrate with document imaging systems, thus facilitating the rapid movement of applications across the processes without the need to paper flow

Originations General System should have Flexibility through extensive Parameterization, Workflow and Configuration of Rules.

Originations General It should be possible to extract any or all data for further analytical functions or for other purposes for end users or other systems at BANK

Originations General Solution should facilitate upload of information through batch files containing the application details

Originations General The fields to be captured should be country specific. It should be possible to add or remove fields based on any other specific attributes in the application such as customer options like Insurance / balance transfer etc.

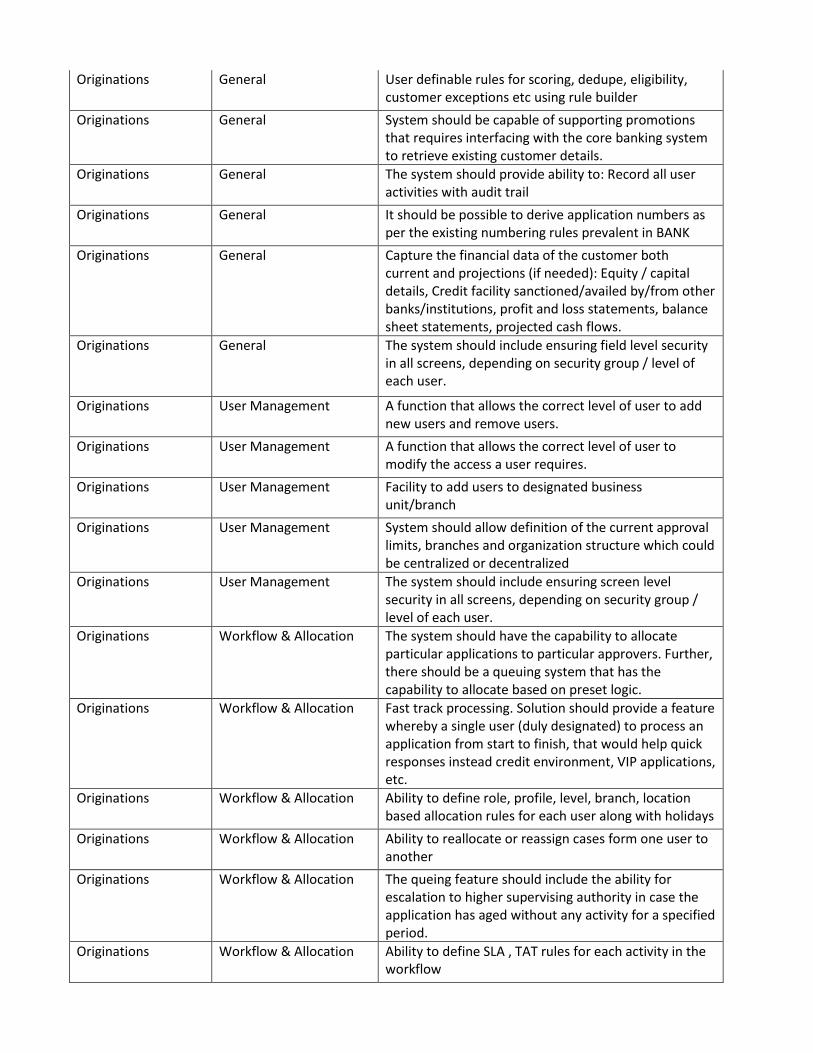

Originations General User definable rules for scoring, dedupe, eligibility, customer exceptions etc using rule builder

Originations General System should be capable of supporting promotions that requires interfacing with the core banking system to retrieve existing customer details.

Originations General The system should provide ability to: Record all user activities with audit trail

Originations General It should be possible to derive application numbers as per the existing numbering rules prevalent in BANK

Originations General Capture the financial data of the customer both current and projections (if needed): Equity / capital details, Credit facility sanctioned/availed by/from other banks/institutions, profit and loss statements, balance sheet statements, projected cash flows.

Originations General The system should include ensuring field level security in all screens, depending on security group / level of each user.

Originations User Management A function that allows the correct level of user to add new users and remove users.

Originations User Management A function that allows the correct level of user to modify the access a user requires.

Originations User Management Facility to add users to designated business unit/branch

Originations User Management System should allow definition of the current approval limits, branches and organization structure which could be centralized or decentralized

Originations User Management The system should include ensuring screen level security in all screens, depending on security group / level of each user.

Originations Workflow & Allocation The system should have the capability to allocate particular applications to particular approvers. Further, there should be a queuing system that has the capability to allocate based on preset logic.

Originations Workflow & Allocation Fast track processing. Solution should provide a feature whereby a single user (duly designated) to process an application from start to finish, that would help quick responses instead credit environment, VIP applications, etc.

Originations Workflow & Allocation Ability to define role, profile, level, branch, location based allocation rules for each user along with holidays

Originations Workflow & Allocation Ability to reallocate or reassign cases form one user to another

Originations Workflow & Allocation The queing feature should include the ability for escalation to higher supervising authority in case the application has aged without any activity for a specified period.

Originations Workflow & Allocation Ability to define SLA , TAT rules for each activity in the workflow

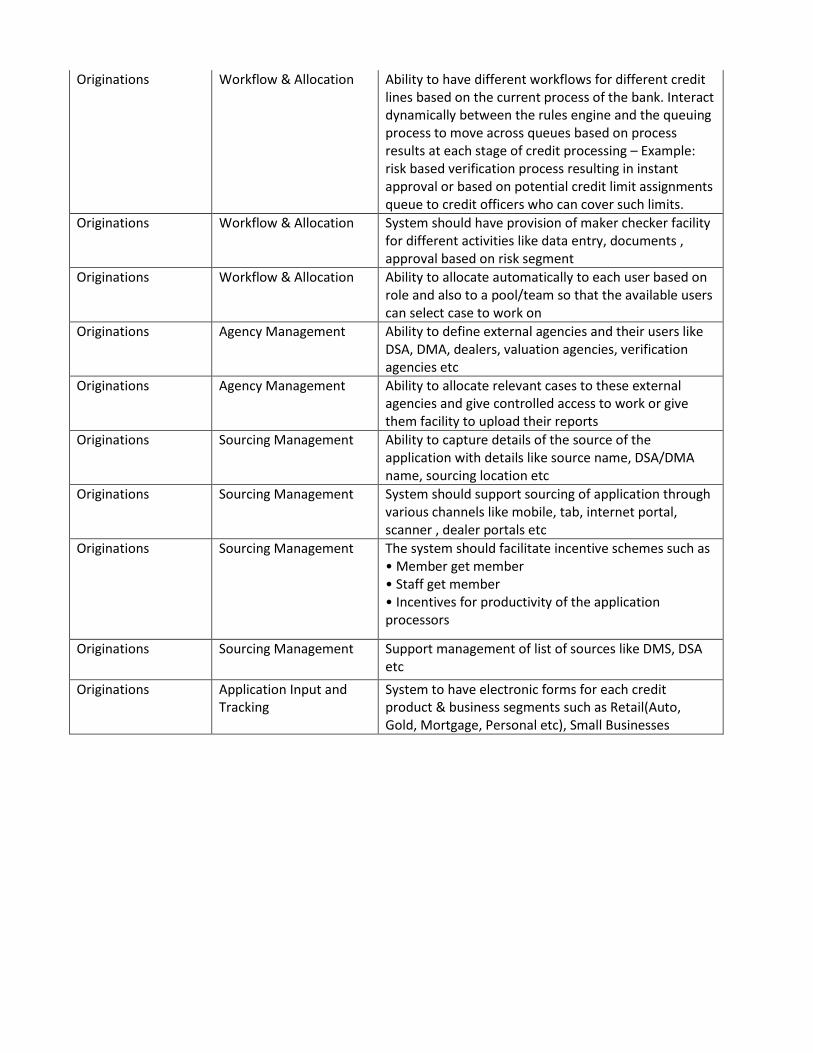

Originations Workflow & Allocation Ability to have different workflows for different credit lines based on the current process of the bank. Interact dynamically between the rules engine and the queuing process to move across queues based on process results at each stage of credit processing – Example: risk based verification process resulting in instant approval or based on potential credit limit assignments queue to credit officers who can cover such limits.

Originations Workflow & Allocation System should have provision of maker checker facility for different activities like data entry, documents , approval based on risk segment

Originations Workflow & Allocation Ability to allocate automatically to each user based on role and also to a pool/team so that the available users can select case to work on

Originations Agency Management Ability to define external agencies and their users like DSA, DMA, dealers, valuation agencies, verification agencies etc

Originations Agency Management Ability to allocate relevant cases to these external agencies and give controlled access to work or give them facility to upload their reports

Originations Sourcing Management Ability to capture details of the source of the application with details like source name, DSA/DMA name, sourcing location etc

Originations Sourcing Management System should support sourcing of application through various channels like mobile, tab, internet portal, scanner , dealer portals etc

Originations Sourcing Management The system should facilitate incentive schemes such as • Member get member • Staff get member • Incentives for productivity of the application processors

Originations Sourcing Management Support management of list of sources like DMS, DSA etc

Originations Application Input and Tracking

System to have electronic forms for each credit product & business segments such as Retail(Auto, Gold, Mortgage, Personal etc), Small Businesses

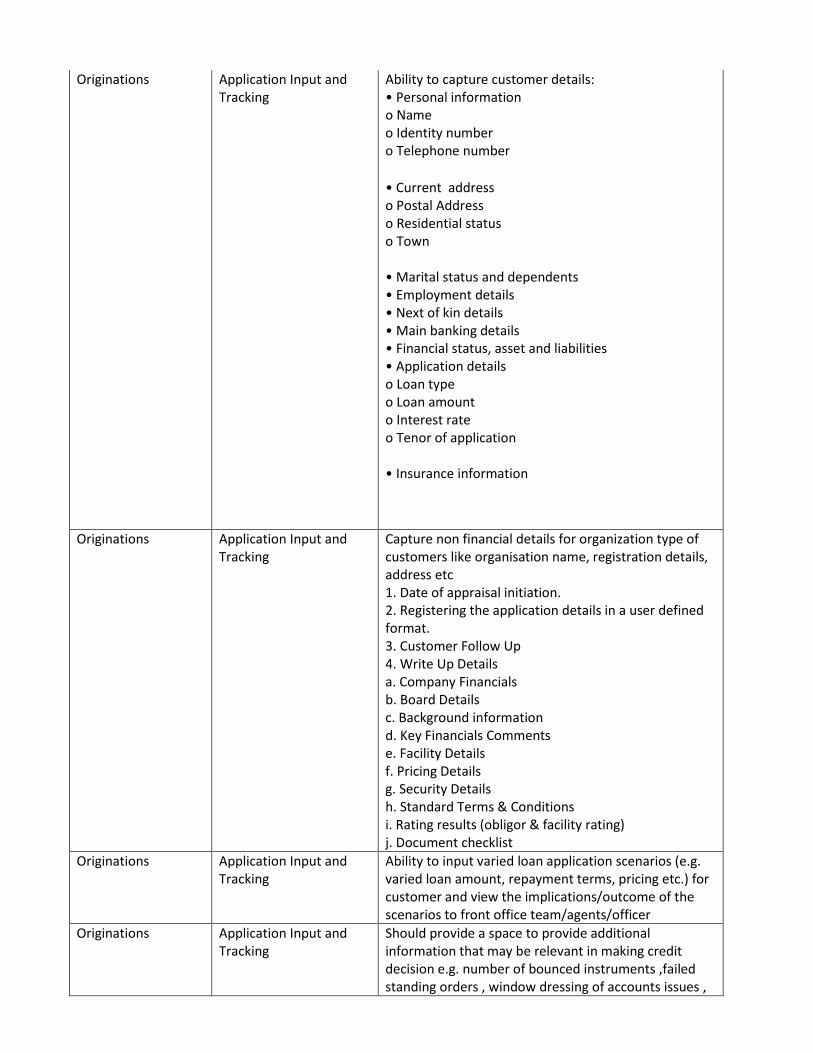

Originations Application Input and Tracking

Ability to capture customer details: • Personal information o Name o Identity number o Telephone number

• Current address o Postal Address o Residential status o Town • Marital status and dependents • Employment details • Next of kin details • Main banking details • Financial status, asset and liabilities • Application details o Loan type o Loan amount o Interest rate o Tenor of application • Insurance information

Originations Application Input and Tracking

Capture non financial details for organization type of customers like organisation name, registration details, address etc 1. Date of appraisal initiation. 2. Registering the application details in a user defined format. 3. Customer Follow Up 4. Write Up Details a. Company Financials b. Board Details c. Background information d. Key Financials Comments e. Facility Details f. Pricing Details g. Security Details h. Standard Terms & Conditions i. Rating results (obligor & facility rating) j. Document checklist

Originations Application Input and Tracking

Ability to input varied loan application scenarios (e.g. varied loan amount, repayment terms, pricing etc.) for customer and view the implications/outcome of the scenarios to front office team/agents/officer

Originations Application Input and Tracking

Should provide a space to provide additional information that may be relevant in making credit decision e.g. number of bounced instruments ,failed standing orders , window dressing of accounts issues ,

Originations Application Input and Tracking

It should be possible to generate quotations and use the same in further processing of the application

Originations Application Input and Tracking

System should support QDE, DDE and checking of the data for any corrections extensively so as to ensure integrity of data.

Originations Application Input and Tracking

System should have facility to validate the data being entered with validations like mandatory/non mandatory, format validations etc

Originations Application Input and Tracking

Must generate a unique loan number for every loan application and The application enquiry should be possible on specific keys such as ID number, account number, product reference number, name etc….

Originations Application Input and Tracking

The unique loan number generate should be easy to trace by the various users who may wish to track the application eg can be queried by inputing customer's id no, name or business registration number

Originations Application Input and Tracking

Allow syndication with other banks

Originations Customer Management System must generate a unique customer number

Originations Customer Management System should allow searching based on the unique customer number

Originations Customer Management System should allow automatic fetch of the customer data for an existing customer 1. Customer Profile 2. Exposure Details 3. Group Exposure if any 4. Existing Facility Details 5. Securities Pledged

Originations Dedupe & Fraud Check Ability to find if an customer is an existing customer and also check for a fraud customer

Originations Dedupe & Fraud Check The system should have the ability to de-dup with the current application details like Id numbers, names or parts thereof , telephone numbers , post box numbers against similar lists in other product data bases such as credit card (issued) master, personal finance (funded) master, Sanction lists, negative lists, branch banking, negative list of employers etc

Originations Dedupe & Fraud Check Option to reject the application for customer based on the fraud check results

Originations Dedupe & Fraud Check Ability to view the match details and compare the matched parameters to be sure that the customer match is exact and then map them against same customer id

Originations Dedupe & Fraud Check Ability to view the existing history, relationship of the customer with bank

Originations Dedupe & Fraud Check Ability to do the dedupe against multiple sources like CBS, CRM etc

Originations Credit Evaluation and Scoring

Customised Internal credit rating system for retail borrowers and counterparties . The solution should provide flexibility in defining credit scoring rules / policies with different multiple combinations and base criteria, provide on-line credit scoring processing with auto approvals / auto rejections for each product line / type. Each scoring matrix must be accompanied by failure reason codes

Originations Credit Evaluation and Scoring

The product should have a scoring engine that is capable of credit scoring across demographic and bureau variables with ability to handle multiple score cards across products and segments. Amendment of credit scoring parameters to suit particular purposes

Originations Credit Evaluation and Scoring

Ability to calculate the total credit score for particular customer as per bank’s set criterions. There must be no restriction on the number of scoring rules for each type.

Originations Credit Evaluation and Scoring

Ability to key in financial data and use the same for scoring

Originations Credit Evaluation and Scoring

Developing customized risk scoring cards for the various customer segments/asset classes in the bank.

Originations Credit Evaluation and Scoring

Ability to interface with third party credit rating systems and use the same for defining different paths of the workflow or in internal scoring engine real time or in batches

Originations Credit Evaluation and Scoring

Ability to interface with multiple credit bureaus and use the results of same in scoring. The system should be able to generate a file on periodic intervals during a day that contains details to be sent to credit bureau for credit inquiry. Upon receipt of response file, it should be possible to upload the bureau details onto the system.

Originations Credit Evaluation and Scoring

The system should have the infrastructure to support rule based decisions with embedded architecture enabling such rules to be written by users using customer level elemental data.

Originations Eligibility Ability to define the customer eligibility rules based on different parameters

Originations Eligibility Ability to arrive at eligible loan amount for a customer based on these rules and data entered for application

System should support financial analysis base don parameters like :- Turnover Liquidity Profitability Leverage Debt Service ratios Balance sheet and Profit and Loss analysis Cash flow and fund-flow analysis

Originations Financial Analysis System should support definition of standard formats for financial data and statements like Balance sheet, Cash Flow statement, P&L account, Funds flow statements. Definition of financial structures based key parameters like Industry segment, customer type etc. Structures can be defined for various financial statements like Balance sheet, Cash Flow statement, P&L account, Funds flow statements etc.

Originations Financial Analysis System should allow defining ratios like operating profit, margin, etc base don formulae and data obtained in financial statements System should support details like Average and benchmark ratios

Originations Financial Analysis Financial data for the customer can be uploaded using excel downloaded based on the structures defined above

Originations Financial Analysis System should capture Number of years for which the data can be uploaded

Originations Financial Analysis The system should capture remarks (with replies) of latest internal/ external auditors (concurrent, statutory, stock audit, etc.), first site inspections. It should also support capturing of text comments along with capturing of remarks and irregularities pertaining to the account in the bank’s monthly / quarterly monitoring reports

Originations Financial Analysis Data should be uploaded for “Audited” as well as “Projected” years

Originations Financial Analysis Based on the data uploaded, system should compute the financial ratios as per the configuration in the masters. The system should be able to perform comparison of selected key ratios, financial parameters across borrowers within the industry and against bench marks. Ratios like debt ratio, current ratio etc • Paid up capital • Reserves and Surplus • Intangible assets • Revaluation reserve • Tangible net worth • Long-term liabilities • Capital employed • Net block • Investments • Non-current assets • Net working capital • Current assets • Current liabilities • Net sales • Other income • Net profit after tax • Depreciation • Intangible assets • Cash accruals • ROCE (Return on capital employed)

Originations Financial Analysis The system should support sensitivity analysis where the User can modify the financial data to find out how the change will affect certain key financial ratios/indicators.

Originations Eligibility Ability to compute ratios like NPV, IRR, FOIR for eligibility evaluation

Originations Document Management Ability to define the documents checklist for an application, applicant, asset

Originations Document Management Ability to track the receipt of Documents for an application

Originations Document Management Ability to upload documents against checklist in different formats like jpg, jpeg, png, gif etc

Originations Document Management Ability to Update, inquire and archive the documents

Originations Document Management Ability to defer, waive the documents based on customer request

Originations Document Management Ability to define mandatory , non mandatory documents

Originations Document Management Ability to track documents stage wise

Originations Document Management Ability to mark the no of pages, date of receipt, location of the document while receiving it

Originations Document Management Ability to have a verification of the documents by a different user

Originations Fees & Charges System should have a facility to define different fees, charges and taxes which are to be collected for a credit product type and customer type

Originations Fees & Charges Ability to collect fees and charges based on the checklist of generated charges partially or fully

Originations Fees & Charges Ability to waive or defer a charge

Originations Deviation Management Ability to define deviation based on rules for pricing, demographics and other parameters

Originations Deviation Management Generation of deviations automatically by the system and allocation to designated authority for approval

Originations Deviation Management Maker Checker process for deviation approval

Originations Deviation Management Facility to add certain user deviations based on the discretion of the user/RM in authority

Originations User Workspace User must be able to see all application he has to work on in a single view

Originations User Workspace User should be able to prioritize his work by being able to filter cases based on certain parameters like application id, first name, last name, product etc

Originations User Workspace User should also be able to view cases in a pool and claim the case to start working on same

Originations User Workspace Supervisor user should be able to view records of his subordinates and be able to take actions on same

Originations Collateral Management Ability to define different collaterals and attributes in the system which have to captured for a collateral

Originations Collateral Management Ability to capture collaterals for an application

Originations Collateral Management Ability to generate a collateral id for each collateral

Originations Collateral Management Ability to generate technical and legal valuation for a collateral and allocate it to a user or agency and capture the valuation details

Originations Collateral Management Ability to calculate eligibility based on collateral value and NPV

Originations Collateral Management Ability to upload valuation documents into the system

Originations Verification Management

Ability to generate different verifications for customer based on his application and evaluation process

Originations Verification Management

Allocate verifications like phone, income, personal, address etc to user/agencies

Originations Verification Management

Ability to initiate and do field investigations

Originations Verification Management

Ability to capture details and documents related to each verification

Originations Credit Approval Ability to define the sanctioning authority based loan size, product etc. Ability to have a multi level sanctioning matrix and automatic routing of the case based on that

Originations Credit Approval The system should aid credit decision making based on the proposal evaluation analysis and credit risk rating. It should facilitate users/reviewers in understanding assessments through electronic case files

Originations Credit Approval Ability to allow authorized personnel to override system credit approval or rejection recommendations but with an audit trail that can be tracked.

Originations Credit Approval Ability to route the case for committee approval in case of higher loan amounts

Originations Credit Approval Ability to generate Credit Appraisal report

Originations Credit Approval System should provide for definition of the minimum requirements for one to qualify for a credit facility generally and within each stage.

Originations Credit Approval Ability to allow reviewing personnel to view defined sets of information/comments on each credit request.

Originations Covenants Ability to view covenants and adhere to them

Originations Credit Approval Ability to view the application data in a summarized form to take credit action

Originations Review Allow annual review of application

Originations Exception Handling Ability to add certain actions/conditions if the application is not fully up to the mark for approval like addition of co-borrower, collateral etc

Originations Exception Handling Ability re-routing the case to an appropriate officer in case of any changes or amendments to be made

Originations Exception Handling Ability to automatically reroute the case in case of any data change based on which the approval was done

Originations Exception Handling Ability to reject the application with reasons. The system should allow review of rejected applications through a screen that includes the reason for rejection.

Originations Exception Handling Ability to review rejected applications for reopening in special cases

Originations Exception Handling Facility to recommend an application if it is not in users approving authority

Originations Exception Handling The system should facilitate archival of rejected applications for de-dup purposes.

Originations Exception Handling Once an application for credit is closed, it should not be possible to change the data, except for certain non critical fields.

Originations Exception Handling The system should have a mechanism that cancels an application if it is pending for more than a specified number of days after follow-up for missing documents / information.

Originations Exception Handling The system should have override options whereby an earlier rejection or cancellation can be revoked and the application be brought back into the mainstream for positive closure.

Originations Offer Letter Generate offer letter for customer

Originations Offer Letter Allow acceptance by the customer via a compliance call

Originations Offer Letter Allow printing of approval/rejection letter in desired format

Originations Offer Letter Ability to view the status of applications under process Stage wise, branch wise and user wise

Originations Offer Letter The system should support creation of sanction advice with the following details at a minimum: Customer details Product details Classification of loan / sector code Purpose of the sanctioned loan Terms and conditions of the sanction amount (rate of interest including any additional charges applicable) Period of sanction or tenure of loan Payment terms of interest, margin etc. Credit rating Repayment schedules Moratorium period Renewal details (where applicable) Charges to be created with appropriate authorities Guarantees Insurance details Documentation and legal formalities to be executed

Originations Offer Letter Is customer correspondence, including reminder letters, notice of default etc, automatically generated by the system in accordance with defined parameters?

Originations Appraisal Note System to have the capability to show a snap shot view of the entire appraisal

Originations Disbursement Ability to generate a disbursement request based on customer need

Originations Disbursement Ability to enter disbursement details like beneficiary, mode of disbursement etc

Originations Disbursement Have maker checker process for disbursement approval

Originations Disbursement Facility to update disbursement details like cheque no etc once the disbursement has been done

Originations Disbursement Facility to update details of asset details if any like engine , chassis no in auto loans or property details on mortgage

Originations Disbursement Facility to do multi tranche disbursement for home loans and under construction properties

Originations Notification Management

Facility to provide real time notification of customers on credit application status through SMS, Email or letter as per configuration of the bank

Originations Notification Management

Ability to automatically send notifications of rejections/approvals to appropriate personnel as well as to customers with predefined data and conditions

Originations Notification Management

When an application is approved by a review and forwarded to the next person on the workflow, ability to send auto-notification via outlook to the receiving personnel to inform on applications awaiting actions.

Originations Notification Management

Ability to automatically notify or alert applicable credit officer when the loan is disbursed to the customer

Originations Notification Management

Ability to define templates for sms, email, letters for notifications based on existing templates of the bank

Originations Notification Management

The system should handle and generate documents like but not limited to: Loan Sanction Letter Loan Rejection Letter Loan Related Agreements Mortgage Contract

Originations Notification Management

Support to insert images, signatures, table and format the template as per bank standard formats

Originations Product Management Ability to define new portfolios, products, schemes based on the current offering of the bank along with their validity

Originations Product Management Ability to define pricing(fixed, floating) with different frequencies like yearly monthly etc along with ability to set up rules for risk based pricing

Originations Product Management Ability to define different amort calculation methods, repayments methods, repayment variations like step up, step down, bullet, balloon etc

Originations Product Management Ability to restrict the availability of the product location wise

Originations Product Management Ability to copy and configure new product on the fly easily

Originations Product Management Tier Based Loans The system must have capability for pricing to be based on the tenor of the loan. The system should give capability for longer tenors to have higher pricing.

Originations Product Management Capability for Top Up loans In the event that a customer already has an existing loan, the system must have automated capability to settle the existing loan and generate a new loan application, with a consolidated balance of the new and old loan.

Originations Product Management Capability for balance transfers In the event that a customer has an existing loan with another institution, the system must allow for input of this information at origination. This will allow for this information to be reviewed at verification.

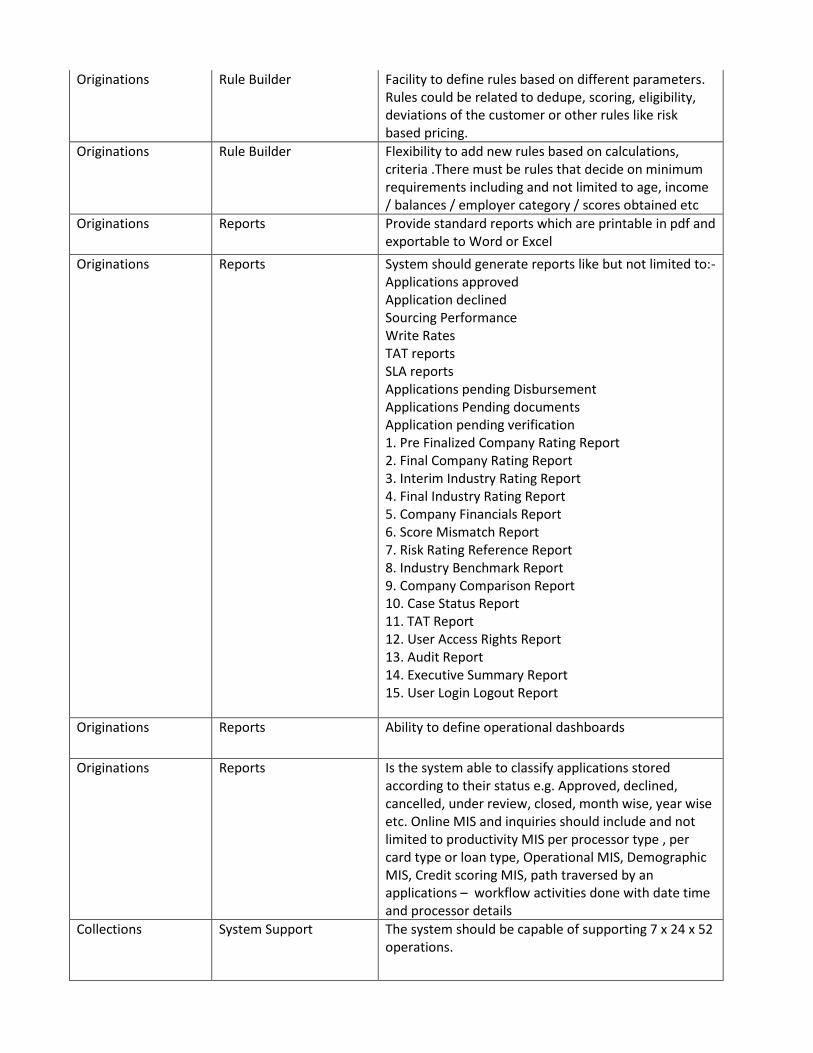

Originations Rule Builder Facility to define rules based on different parameters. Rules could be related to dedupe, scoring, eligibility, deviations of the customer or other rules like risk based pricing.

Originations Rule Builder Flexibility to add new rules based on calculations, criteria .There must be rules that decide on minimum requirements including and not limited to age, income / balances / employer category / scores obtained etc

Originations Reports Provide standard reports which are printable in pdf and exportable to Word or Excel

Originations Reports System should generate reports like but not limited to:- Applications approved Application declined Sourcing Performance Write Rates TAT reports SLA reports Applications pending Disbursement Applications Pending documents Application pending verification 1. Pre Finalized Company Rating Report 2. Final Company Rating Report 3. Interim Industry Rating Report 4. Final Industry Rating Report 5. Company Financials Report 6. Score Mismatch Report 7. Risk Rating Reference Report 8. Industry Benchmark Report 9. Company Comparison Report 10. Case Status Report 11. TAT Report 12. User Access Rights Report 13. Audit Report 14. Executive Summary Report 15. User Login Logout Report

Originations Reports Ability to define operational dashboards

Originations Reports Is the system able to classify applications stored according to their status e.g. Approved, declined, cancelled, under review, closed, month wise, year wise etc. Online MIS and inquiries should include and not limited to productivity MIS per processor type , per card type or loan type, Operational MIS, Demographic MIS, Credit scoring MIS, path traversed by an applications – workflow activities done with date time and processor details

Collections System Support The system should be capable of supporting 7 x 24 x 52 operations.

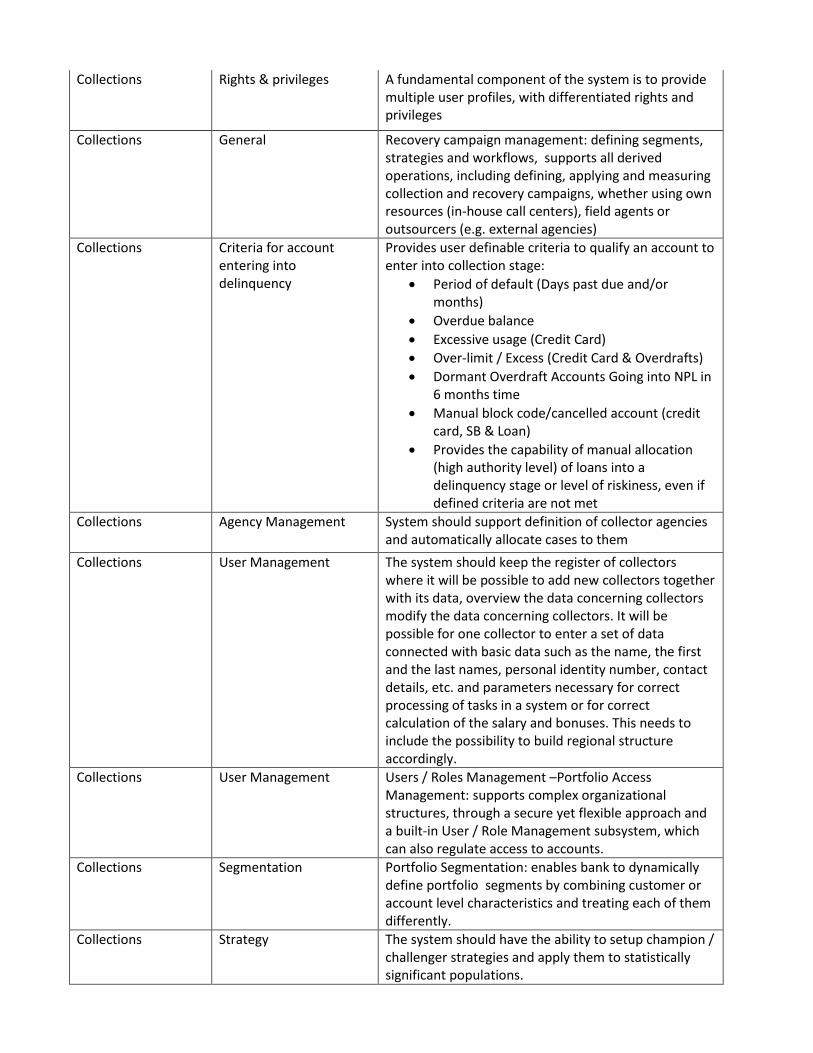

Collections Rights & privileges A fundamental component of the system is to provide multiple user profiles, with differentiated rights and privileges

Collections General Recovery campaign management: defining segments, strategies and workflows, supports all derived operations, including defining, applying and measuring collection and recovery campaigns, whether using own resources (in-house call centers), field agents or outsourcers (e.g. external agencies)

Collections Criteria for account entering into delinquency

Provides user definable criteria to qualify an account to enter into collection stage:

Period of default (Days past due and/or months)

Overdue balance

Excessive usage (Credit Card)

Over-limit / Excess (Credit Card & Overdrafts)

Dormant Overdraft Accounts Going into NPL in 6 months time

Manual block code/cancelled account (credit card, SB & Loan)

Provides the capability of manual allocation (high authority level) of loans into a delinquency stage or level of riskiness, even if defined criteria are not met

Collections Agency Management System should support definition of collector agencies and automatically allocate cases to them

Collections User Management The system should keep the register of collectors where it will be possible to add new collectors together with its data, overview the data concerning collectors modify the data concerning collectors. It will be possible for one collector to enter a set of data connected with basic data such as the name, the first and the last names, personal identity number, contact details, etc. and parameters necessary for correct processing of tasks in a system or for correct calculation of the salary and bonuses. This needs to include the possibility to build regional structure accordingly.

Collections User Management Users / Roles Management –Portfolio Access Management: supports complex organizational structures, through a secure yet flexible approach and a built-in User / Role Management subsystem, which can also regulate access to accounts.

Collections Segmentation Portfolio Segmentation: enables bank to dynamically define portfolio segments by combining customer or account level characteristics and treating each of them differently.

Collections Strategy The system should have the ability to setup champion / challenger strategies and apply them to statistically significant populations.

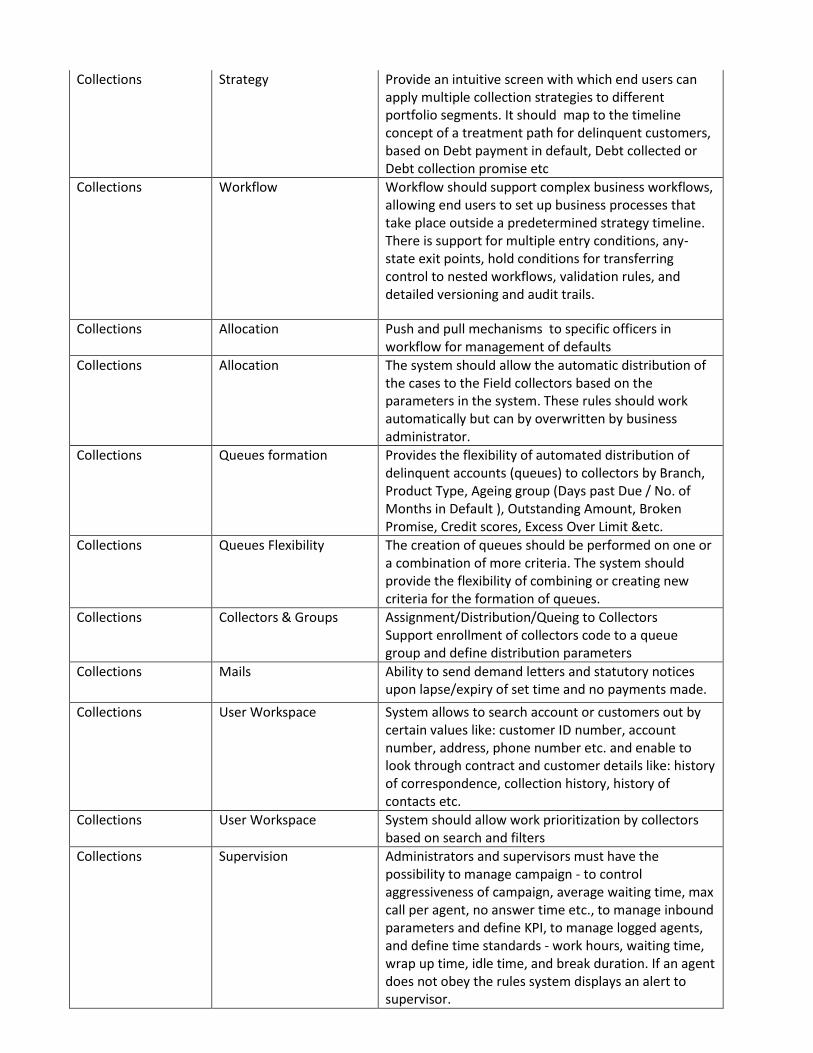

Collections Strategy Provide an intuitive screen with which end users can apply multiple collection strategies to different portfolio segments. It should map to the timeline concept of a treatment path for delinquent customers, based on Debt payment in default, Debt collected or Debt collection promise etc

Collections Workflow Workflow should support complex business workflows, allowing end users to set up business processes that take place outside a predetermined strategy timeline. There is support for multiple entry conditions, any-state exit points, hold conditions for transferring control to nested workflows, validation rules, and detailed versioning and audit trails.

Collections Allocation Push and pull mechanisms to specific officers in workflow for management of defaults

Collections Allocation The system should allow the automatic distribution of the cases to the Field collectors based on the parameters in the system. These rules should work automatically but can by overwritten by business administrator.

Collections Queues formation Provides the flexibility of automated distribution of delinquent accounts (queues) to collectors by Branch, Product Type, Ageing group (Days past Due / No. of Months in Default ), Outstanding Amount, Broken Promise, Credit scores, Excess Over Limit &etc.

Collections Queues Flexibility The creation of queues should be performed on one or a combination of more criteria. The system should provide the flexibility of combining or creating new criteria for the formation of queues.

Collections Collectors & Groups Assignment/Distribution/Queing to Collectors Support enrollment of collectors code to a queue group and define distribution parameters

Collections Mails Ability to send demand letters and statutory notices upon lapse/expiry of set time and no payments made.

Collections User Workspace System allows to search account or customers out by certain values like: customer ID number, account number, address, phone number etc. and enable to look through contract and customer details like: history of correspondence, collection history, history of contacts etc.

Collections User Workspace System should allow work prioritization by collectors based on search and filters

Collections Supervision Administrators and supervisors must have the possibility to manage campaign - to control aggressiveness of campaign, average waiting time, max call per agent, no answer time etc., to manage inbound parameters and define KPI, to manage logged agents, and define time standards - work hours, waiting time, wrap up time, idle time, and break duration. If an agent does not obey the rules system displays an alert to supervisor.

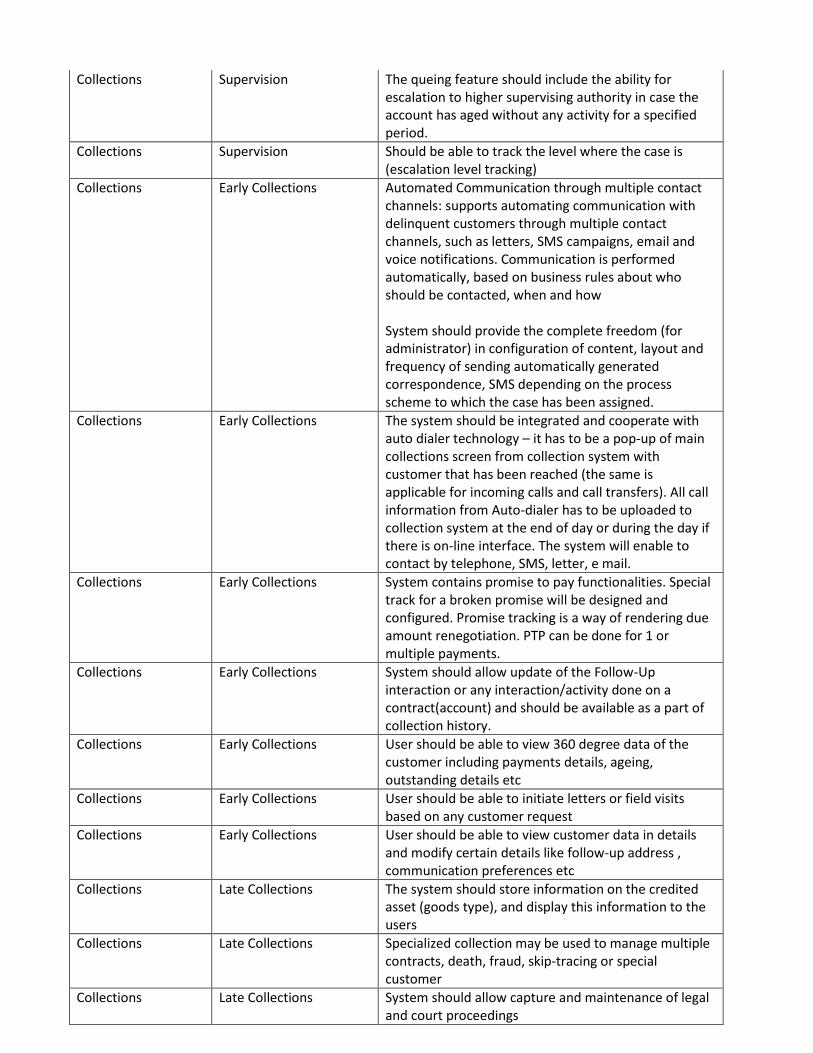

Collections Supervision The queing feature should include the ability for escalation to higher supervising authority in case the account has aged without any activity for a specified period.

Collections Supervision Should be able to track the level where the case is (escalation level tracking)

Collections Early Collections Automated Communication through multiple contact channels: supports automating communication with delinquent customers through multiple contact channels, such as letters, SMS campaigns, email and voice notifications. Communication is performed automatically, based on business rules about who should be contacted, when and how System should provide the complete freedom (for administrator) in configuration of content, layout and frequency of sending automatically generated correspondence, SMS depending on the process scheme to which the case has been assigned.

Collections Early Collections The system should be integrated and cooperate with auto dialer technology – it has to be a pop-up of main collections screen from collection system with customer that has been reached (the same is applicable for incoming calls and call transfers). All call information from Auto-dialer has to be uploaded to collection system at the end of day or during the day if there is on-line interface. The system will enable to contact by telephone, SMS, letter, e mail.

Collections Early Collections System contains promise to pay functionalities. Special track for a broken promise will be designed and configured. Promise tracking is a way of rendering due amount renegotiation. PTP can be done for 1 or multiple payments.

Collections Early Collections System should allow update of the Follow-Up interaction or any interaction/activity done on a contract(account) and should be available as a part of collection history.

Collections Early Collections User should be able to view 360 degree data of the customer including payments details, ageing, outstanding details etc

Collections Early Collections User should be able to initiate letters or field visits based on any customer request

Collections Early Collections User should be able to view customer data in details and modify certain details like follow-up address , communication preferences etc

Collections Late Collections The system should store information on the credited asset (goods type), and display this information to the users

Collections Late Collections Specialized collection may be used to manage multiple contracts, death, fraud, skip-tracing or special customer

Collections Late Collections System should allow capture and maintenance of legal and court proceedings

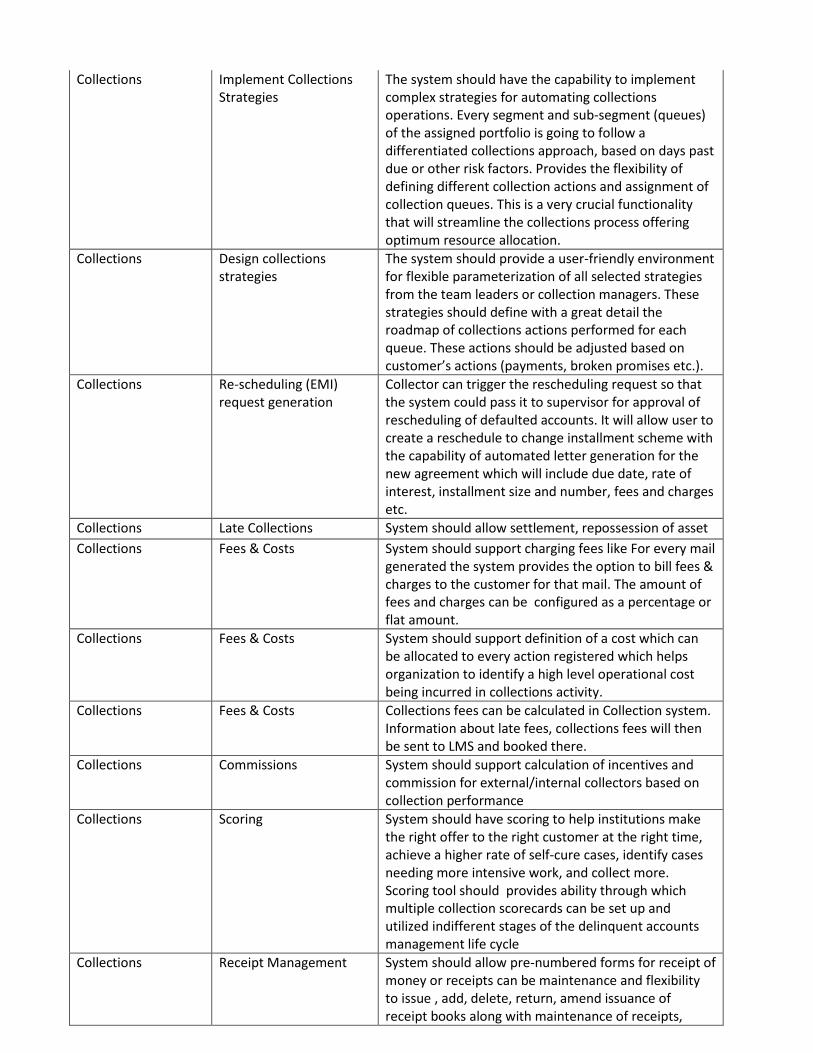

Collections Implement Collections Strategies

The system should have the capability to implement complex strategies for automating collections operations. Every segment and sub-segment (queues) of the assigned portfolio is going to follow a differentiated collections approach, based on days past due or other risk factors. Provides the flexibility of defining different collection actions and assignment of collection queues. This is a very crucial functionality that will streamline the collections process offering optimum resource allocation.

Collections Design collections strategies

The system should provide a user-friendly environment for flexible parameterization of all selected strategies from the team leaders or collection managers. These strategies should define with a great detail the roadmap of collections actions performed for each queue. These actions should be adjusted based on customer’s actions (payments, broken promises etc.).

Collections Re-scheduling (EMI) request generation

Collector can trigger the rescheduling request so that the system could pass it to supervisor for approval of rescheduling of defaulted accounts. It will allow user to create a reschedule to change installment scheme with the capability of automated letter generation for the new agreement which will include due date, rate of interest, installment size and number, fees and charges etc.

Collections Late Collections System should allow settlement, repossession of asset

Collections Fees & Costs System should support charging fees like For every mail generated the system provides the option to bill fees & charges to the customer for that mail. The amount of fees and charges can be configured as a percentage or flat amount.

Collections Fees & Costs System should support definition of a cost which can be allocated to every action registered which helps organization to identify a high level operational cost being incurred in collections activity.

Collections Fees & Costs Collections fees can be calculated in Collection system. Information about late fees, collections fees will then be sent to LMS and booked there.

Collections Commissions System should support calculation of incentives and commission for external/internal collectors based on collection performance

Collections Scoring System should have scoring to help institutions make the right offer to the right customer at the right time, achieve a higher rate of self-cure cases, identify cases needing more intensive work, and collect more. Scoring tool should provides ability through which multiple collection scorecards can be set up and utilized indifferent stages of the delinquent accounts management life cycle

Collections Receipt Management System should allow pre-numbered forms for receipt of money or receipts can be maintenance and flexibility to issue , add, delete, return, amend issuance of receipt books along with maintenance of receipts,

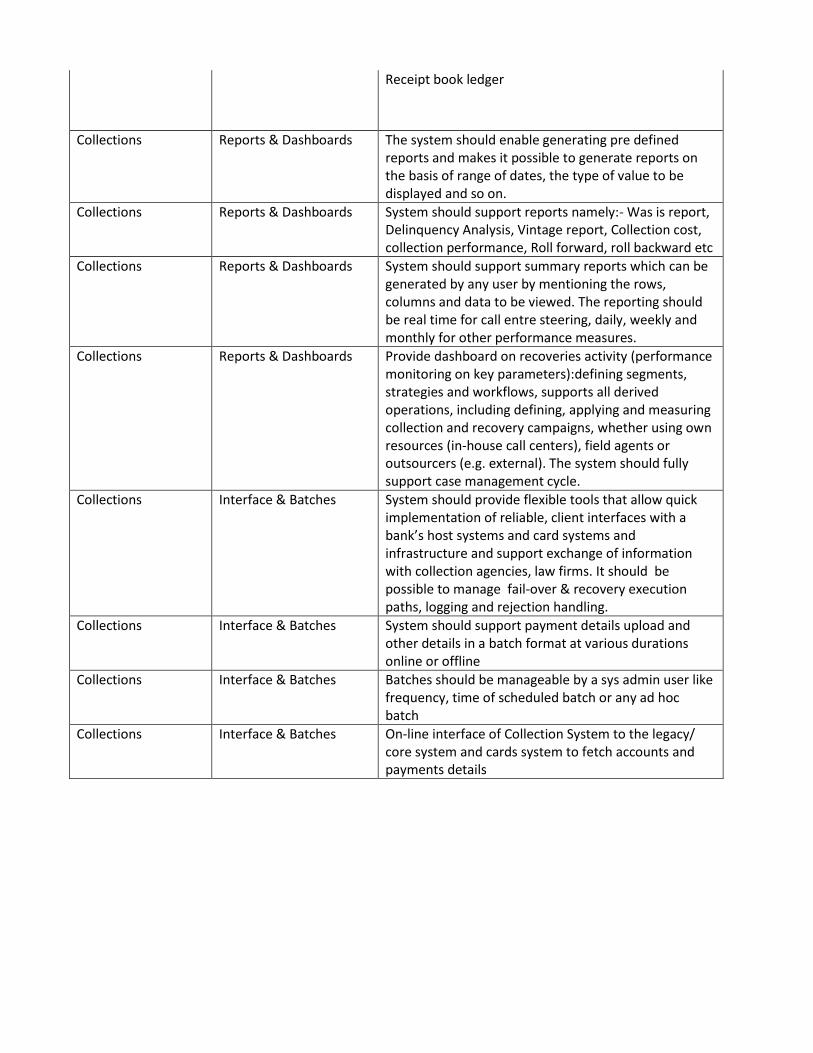

Receipt book ledger

Collections Reports & Dashboards The system should enable generating pre defined reports and makes it possible to generate reports on the basis of range of dates, the type of value to be displayed and so on.

Collections Reports & Dashboards System should support reports namely:- Was is report, Delinquency Analysis, Vintage report, Collection cost, collection performance, Roll forward, roll backward etc

Collections Reports & Dashboards System should support summary reports which can be generated by any user by mentioning the rows, columns and data to be viewed. The reporting should be real time for call entre steering, daily, weekly and monthly for other performance measures.

Collections Reports & Dashboards Provide dashboard on recoveries activity (performance monitoring on key parameters):defining segments, strategies and workflows, supports all derived operations, including defining, applying and measuring collection and recovery campaigns, whether using own resources (in-house call centers), field agents or outsourcers (e.g. external). The system should fully support case management cycle.

Collections Interface & Batches System should provide flexible tools that allow quick implementation of reliable, client interfaces with a bank’s host systems and card systems and infrastructure and support exchange of information with collection agencies, law firms. It should be possible to manage fail-over & recovery execution paths, logging and rejection handling.

Collections Interface & Batches System should support payment details upload and other details in a batch format at various durations online or offline

Collections Interface & Batches Batches should be manageable by a sys admin user like frequency, time of scheduled batch or any ad hoc batch

Collections Interface & Batches On-line interface of Collection System to the legacy/ core system and cards system to fetch accounts and payments details

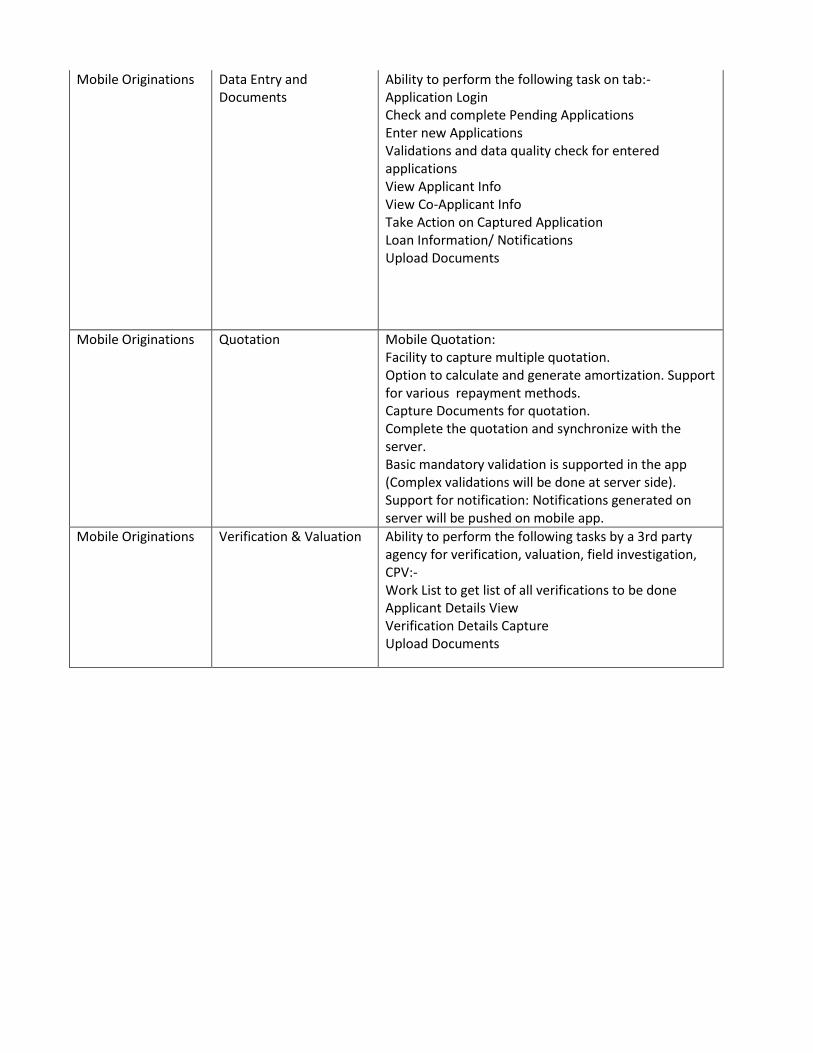

Mobile Originations Data Entry and Documents

Ability to perform the following task on tab:- Application Login Check and complete Pending Applications Enter new Applications Validations and data quality check for entered applications View Applicant Info View Co-Applicant Info Take Action on Captured Application Loan Information/ Notifications Upload Documents

Mobile Originations Quotation Mobile Quotation: Facility to capture multiple quotation. Option to calculate and generate amortization. Support for various repayment methods. Capture Documents for quotation. Complete the quotation and synchronize with the server. Basic mandatory validation is supported in the app (Complex validations will be done at server side). Support for notification: Notifications generated on server will be pushed on mobile app.

Mobile Originations Verification & Valuation Ability to perform the following tasks by a 3rd party agency for verification, valuation, field investigation, CPV:- Work List to get list of all verifications to be done Applicant Details View Verification Details Capture Upload Documents

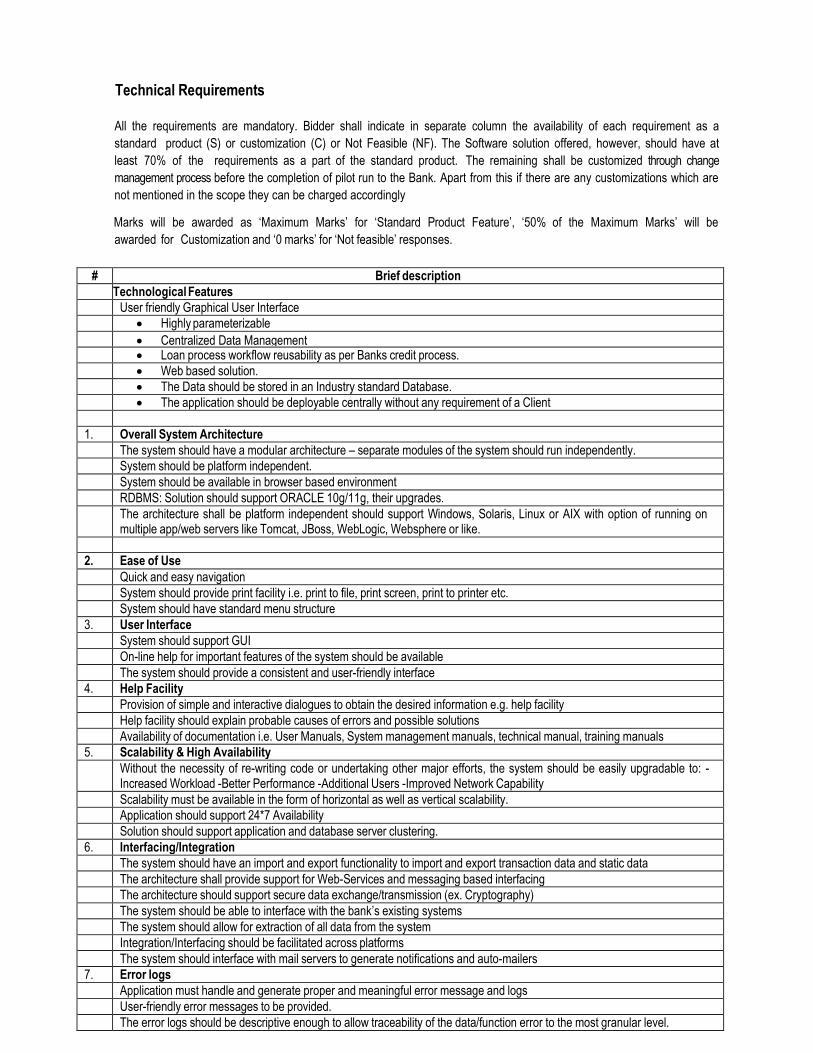

Technical Requirements

All the requirements are mandatory. Bidder shall indicate in separate column the availability of each requirement as a

standard product (S) or customization (C) or Not Feasible (NF). The Software solution offered, however, should have at

least 70% of the requirements as a part of the standard product. The remaining shall be customized through change

management process before the completion of pilot run to the Bank. Apart from this if there are any customizations which are

not mentioned in the scope they can be charged accordingly

Marks will be awarded as „Maximum Marks‟ for „Standard Product Feature‟, „50% of the Maximum Marks‟ will be

awarded for Customization and „0 marks‟ for „Not feasible‟ responses.

# Brief description

Technological Features User friendly Graphical User Interface

Highly parameterizable

Centralized Data Management

Loan process workflow reusability as per Banks credit process.

Web based solution.

The Data should be stored in an Industry standard Database.

The application should be deployable centrally without any requirement of a Client

1. Overall System Architecture

The system should have a modular architecture – separate modules of the system should run independently.

System should be platform independent.

System should be available in browser based environment

RDBMS: Solution should support ORACLE 10g/11g, their upgrades.

The architecture shall be platform independent should support Windows, Solaris, Linux or AIX with option of running on multiple app/web servers like Tomcat, JBoss, WebLogic, Websphere or like.

2. Ease of Use

Quick and easy navigation

System should provide print facility i.e. print to file, print screen, print to printer etc.

System should have standard menu structure

3. User Interface

System should support GUI

On-line help for important features of the system should be available

The system should provide a consistent and user-friendly interface

4. Help Facility

Provision of simple and interactive dialogues to obtain the desired information e.g. help facility

Help facility should explain probable causes of errors and possible solutions

Availability of documentation i.e. User Manuals, System management manuals, technical manual, training manuals

5. Scalability & High Availability

Without the necessity of re-writing code or undertaking other major efforts, the system should be easily upgradable to: - Increased Workload -Better Performance -Additional Users -Improved Network Capability

Scalability must be available in the form of horizontal as well as vertical scalability.

Application should support 24*7 Availability

Solution should support application and database server clustering.

6. Interfacing/Integration

The system should have an import and export functionality to import and export transaction data and static data

The architecture shall provide support for Web-Services and messaging based interfacing

The architecture should support secure data exchange/transmission (ex. Cryptography)

The system should be able to interface with the bank‟s existing systems

The system should allow for extraction of all data from the system

Integration/Interfacing should be facilitated across platforms

The system should interface with mail servers to generate notifications and auto-mailers

7. Error logs

Application must handle and generate proper and meaningful error message and logs

User-friendly error messages to be provided.

The error logs should be descriptive enough to allow traceability of the data/function error to the most granular level.

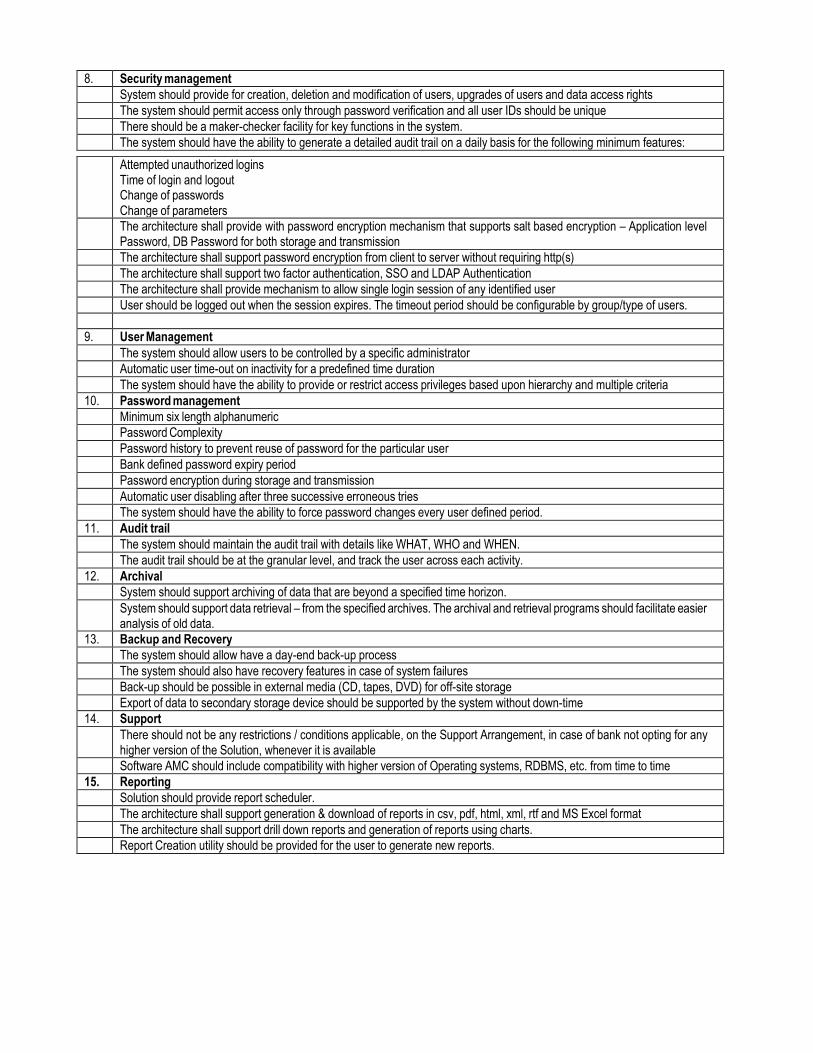

8. Security management

System should provide for creation, deletion and modification of users, upgrades of users and data access rights

The system should permit access only through password verification and all user IDs should be unique

There should be a maker-checker facility for key functions in the system.

The system should have the ability to generate a detailed audit trail on a daily basis for the following minimum features:

Attempted unauthorized logins Time of login and logout Change of passwords Change of parameters

The architecture shall provide with password encryption mechanism that supports salt based encryption – Application level Password, DB Password for both storage and transmission

The architecture shall support password encryption from client to server without requiring http(s)

The architecture shall support two factor authentication, SSO and LDAP Authentication

The architecture shall provide mechanism to allow single login session of any identified user

User should be logged out when the session expires. The timeout period should be configurable by group/type of users.

9. User Management

The system should allow users to be controlled by a specific administrator

Automatic user time-out on inactivity for a predefined time duration

The system should have the ability to provide or restrict access privileges based upon hierarchy and multiple criteria

10. Password management

Minimum six length alphanumeric

Password Complexity

Password history to prevent reuse of password for the particular user

Bank defined password expiry period

Password encryption during storage and transmission

Automatic user disabling after three successive erroneous tries

The system should have the ability to force password changes every user defined period.

11. Audit trail

The system should maintain the audit trail with details like WHAT, WHO and WHEN.

The audit trail should be at the granular level, and track the user across each activity.

12. Archival

System should support archiving of data that are beyond a specified time horizon.

System should support data retrieval – from the specified archives. The archival and retrieval programs should facilitate easier analysis of old data.

13. Backup and Recovery

The system should allow have a day-end back-up process

The system should also have recovery features in case of system failures

Back-up should be possible in external media (CD, tapes, DVD) for off-site storage

Export of data to secondary storage device should be supported by the system without down-time

14. Support

There should not be any restrictions / conditions applicable, on the Support Arrangement, in case of bank not opting for any higher version of the Solution, whenever it is available

Software AMC should include compatibility with higher version of Operating systems, RDBMS, etc. from time to time

15. Reporting

Solution should provide report scheduler.

The architecture shall support generation & download of reports in csv, pdf, html, xml, rtf and MS Excel format

The architecture shall support drill down reports and generation of reports using charts.

Report Creation utility should be provided for the user to generate new reports.

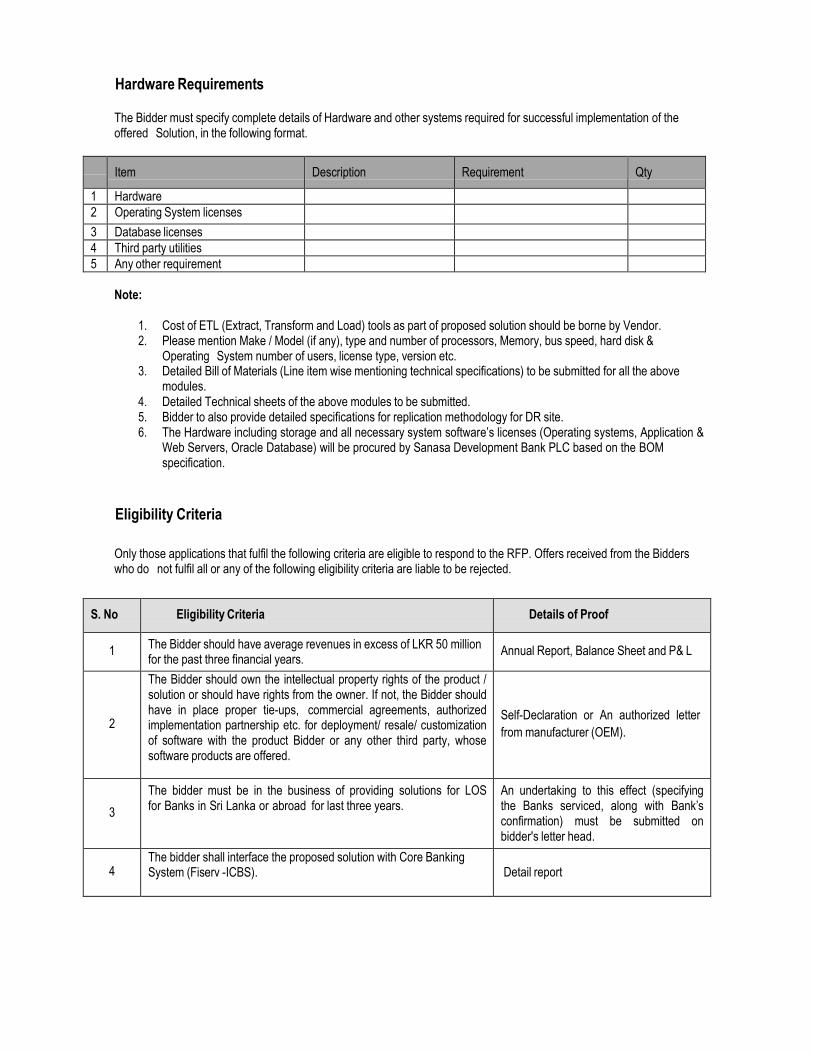

Hardware Requirements

The Bidder must specify complete details of Hardware and other systems required for successful implementation of the offered Solution, in the following format.

Item Description Requirement Qty

1 Hardware 2 Operating System licenses 3 Database licenses 4 Third party utilities 5 Any other requirement

Note:

1. Cost of ETL (Extract, Transform and Load) tools as part of proposed solution should be borne by Vendor. 2. Please mention Make / Model (if any), type and number of processors, Memory, bus speed, hard disk &

Operating System number of users, license type, version etc. 3. Detailed Bill of Materials (Line item wise mentioning technical specifications) to be submitted for all the above

modules. 4. Detailed Technical sheets of the above modules to be submitted. 5. Bidder to also provide detailed specifications for replication methodology for DR site. 6. The Hardware including storage and all necessary system software‟s licenses (Operating systems, Application &

Web Servers, Oracle Database) will be procured by Sanasa Development Bank PLC based on the BOM specification.

Eligibility Criteria

Only those applications that fulfil the following criteria are eligible to respond to the RFP. Offers received from the Bidders who do not fulfil all or any of the following eligibility criteria are liable to be rejected.

S. No Eligibility Criteria Details of Proof

1 The Bidder should have average revenues in excess of LKR 50 million for the past three financial years.

Annual Report, Balance Sheet and P& L

2

The Bidder should own the intellectual property rights of the product / solution or should have rights from the owner. If not, the Bidder should have in place proper tie-ups, commercial agreements, authorized implementation partnership etc. for deployment/ resale/ customization of software with the product Bidder or any other third party, whose software products are offered.

Self-Declaration or An authorized letter

from manufacturer (OEM).

3

The bidder must be in the business of providing solutions for LOS for Banks in Sri Lanka or abroad for last three years.

An undertaking to this effect (specifying the Banks serviced, along with Bank‟s confirmation) must be submitted on bidder's letter head.

4 The bidder shall interface the proposed solution with Core Banking System (Fiserv -ICBS).

Detail report

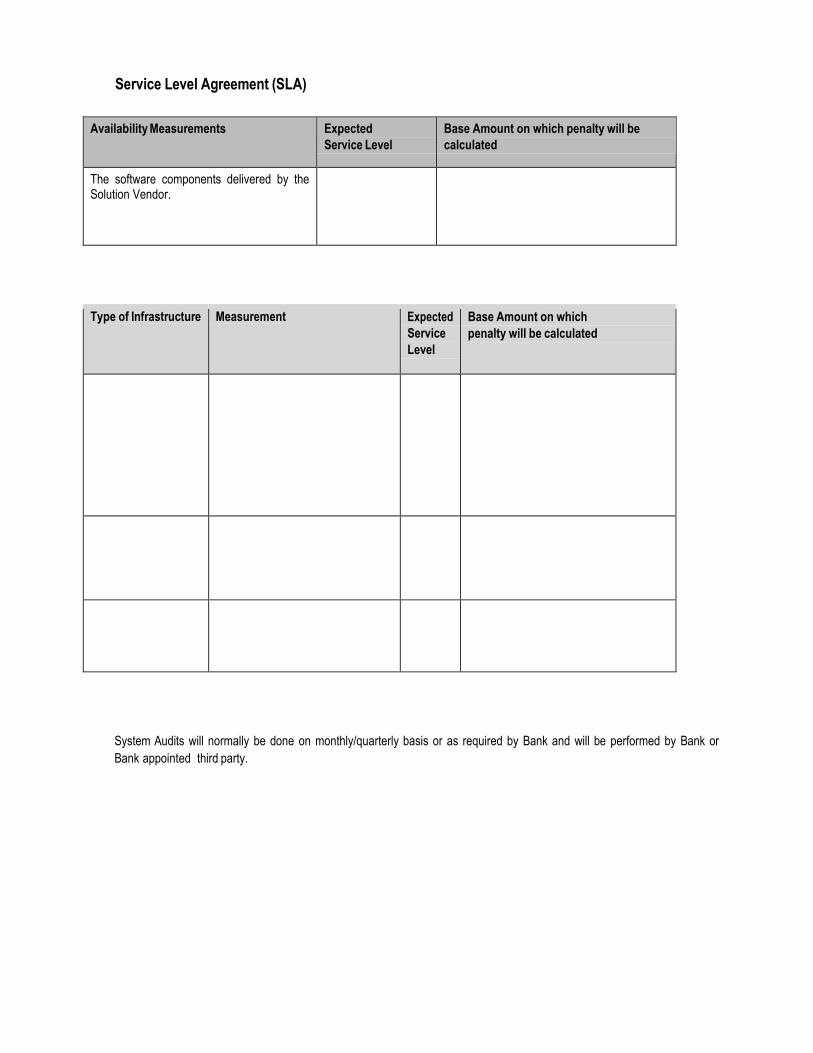

Service Level Agreement (SLA)

Availability Measurements Expected

Service Level

Base Amount on which penalty will be

calculated

The software components delivered by the Solution Vendor.

Type of Infrastructure Measurement Expected

Service

Level

Base Amount on which

penalty will be calculated

System Audits will normally be done on monthly/quarterly basis or as required by Bank and will be performed by Bank or

Bank appointed third party.

Project Time Schedule

The following time schedules should be adhered to for completion of the activities from the date of the Purchase Order:

Business requirement study – 20 working days

Limited Customization, if required for Go Live (80 days)

Product Installation – 10working days (Assuming Infrastructure and other System software‟s are fully installed)

Interface development, integration, customization, UAT, Training and operationalization - 60 working days

Please note that maximum expected time frame of the project to GO LIVE is 6 months from the date of issuing

Purchase Order*. Accordingly vendors have to deploy the resources.

Post-implementation on-site support should be provided for 3 months from Go Live date.

All works related to the assignment handled are to be well documented and will form the part of deliverables. They

should be delivered both in hard copy and soft copy at the end of the each stage.

*Appropriate decision of extending the implementation period will be taken by bank, if required.

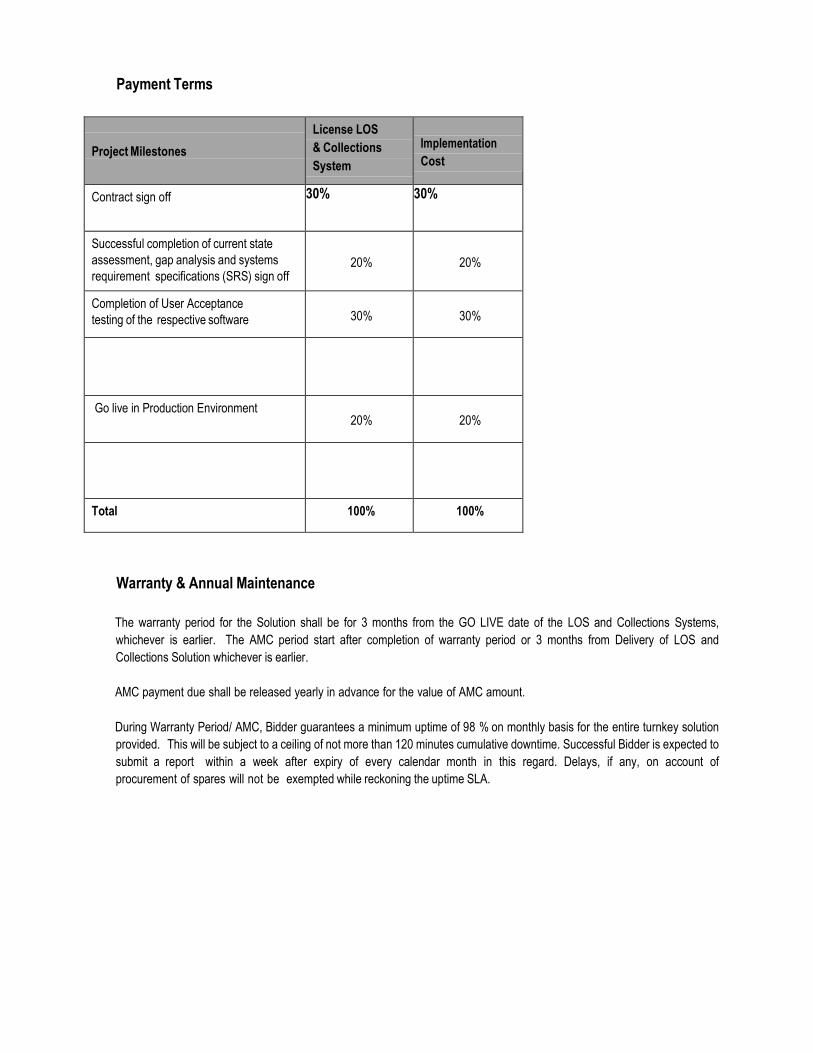

Payment Terms

Project Milestones

License LOS

& Collections

System

Implementation

Cost

Contract sign off 30% 30%

Successful completion of current state

assessment, gap analysis and systems

requirement specifications (SRS) sign off

20%

20%

Completion of User Acceptance

testing of the respective software

30%

30%

Go live in Production Environment 20%

20%

Total 100% 100%

Warranty & Annual Maintenance

The warranty period for the Solution shall be for 3 months from the GO LIVE date of the LOS and Collections Systems,

whichever is earlier. The AMC period start after completion of warranty period or 3 months from Delivery of LOS and

Collections Solution whichever is earlier.

AMC payment due shall be released yearly in advance for the value of AMC amount.

During Warranty Period/ AMC, Bidder guarantees a minimum uptime of 98 % on monthly basis for the entire turnkey solution

provided. This will be subject to a ceiling of not more than 120 minutes cumulative downtime. Successful Bidder is expected to

submit a report within a week after expiry of every calendar month in this regard. Delays, if any, on account of

procurement of spares will not be exempted while reckoning the uptime SLA.

During the period of AMC, if the service provided by the Bidder is not satisfactory, the Bank reserves the right to terminate the

AMC contract and appoint any other agency at the risk and cost of the Bidder.

Terms and Conditions during Warranty and AMC Period

During the period of contract up to completion of Warranty and also during annual maintenance, the selected bidder shall

do the following:

1. Service Support is defined specifically as helpdesk, technical guidance problem solving and troubleshooting,

rectification of bugs,

2. The support shall be given in person or through telephone, FAX, letter and E-mail within a reasonable time as the

case may be.

3. In future, if any configuration changes are required, it should be done by the bidder during warranty and AMC

period through change management process. However Bank will intimate the bidder well in advance for doing such

configuration changes. Configuration changes may be done either centrally or remotely as decided by the bank

when need arises. However in case the bidder has any concerns, it should be informed to the Bank in writing with

reason for taking appropriate/ amicable/ mutually agreed decision in the matter.

4. The Solution offered should have all components which are bug free, no known vulnerabilities reported and of

latest stable version, which are having a 3 years clean track record.

5. The Bidder shall be bound to provide technical consultancy and guidance for successful operation of the Risk

Solutions and its expansion in future by the Bank during the warranty and AMC period The consultancy can be

provided at T & M basis through change management process.

6. Level of support required for Support of LOS and Collections solution as a part of AMC:

Level-3 support for application bug-fixes (if any) and email query resolution.

All defects reported during this period will be corrected by the vendor free-of-charge as per the following timelines for mutually agreed severity levels: Severity 1 System unavailable for use – business has come to a halt Cannot use critical functionality of the system Turnaround time: Work around / Resolution within 4 hours Severity 2 Cannot perform certain functions – but there are workarounds. In some cases, a Priority 1 problem may reduce in severity to a Priority 2 problem because of a workaround provided by vendor Turnaround time: 48 hours Severity 3 Minor issue / look & feel irritant Turnaround time: Next planned release, not later than one month

Selection Strategy

1. The objective of the evaluation process is to evaluate the bids to select an effective and best fit solution at a competitive

price. The evaluation will be undertaken by an Internal Selection Committee formed by the Bank. The Bank may consider

recommendations made by External Experts/Consultants on the evaluation. The committee or authorised official shall

recommend the successful bidder to be engaged for this assignment before Board and the decision of our Board shall be

final, conclusive and binding on the bidders.

2. Through this Request for Proposal, Bank aims to select a Bidder/ application provider who would undertake the designing

and implementation of the required solution. The Bidder shall be entrusted with end to end responsibility for the execution

of the project under the scope of this RFP

3. The Bank will scrutinize the offers to determine whether they are complete, whether any errors have been made in the

offer, whether required technical documentation has been furnished, whether the documents have been properly signed,

and whether items are quoted as per the schedule. The Bank may, at its discretion, waive any minor non- conformity or

any minor deficiency in an offer. This shall be binding on all Bidders and the Bank reserves the right for such waivers and

the Bank‟s decision in the matter will be final.

4. Bank may call for any clarifications/additional particulars required, if any, on the bids submitted. The bidder has to submit

the clarifications/ additional particulars in writing within the specified date and time. The bidder‟s offer may be disqualified,

if the clarifications/ additional particulars sought are not submitted within the specified date and time. Bank reserves the

right to call for presentation/s, product walkthroughs, on the features of the solution offered etc., from the bidders based on

the technical bids submitted by them. Bank also reserves the right to conduct Reference Site Visits at the bidder‟s client

sites. Based upon the final technical scoring, short listing would be made of the eligible bidders for final selection.

Delay in adhering to the project timelines/Liquidated damages

The Successful Bidder must strictly adhere to the time schedule, as specified in the Contract, executed between the Bank and the

bidder, pursuant hereto, for performance of the obligations arising out of the contract and any delay will enable the Bank to resort to

any or all of the following at sole discretion of the Bank.

1. Penalty

2. Termination of the agreement fully or partly

If there is any delay in the implementation of the project due to bidder /partner’s fault in complying with time schedule furnished by

the bidder and accepted by the Bank, it will charge 1% on the total project implementation cost to the bidder for each week of delay

as penalty. Project Implementation cost in this context refers to total expenditure expected to be incurred by the bank for procurement,

design and implementation of software solutions required to lay down LOS & Credit Rating. The cost does not include Cost of

Hardware procured for the implementation. This penalty will be subject to an upper limit of 10% on the total project implementation

cost. Thereafter the order/contract may be cancelled and amount paid if any, may be recovered with 2% interest per month. Any

deviations from the norms would be treated as breach of the contract by the bidder and will be dealt with accordingly. The delay will

be measured with reference to time schedule to be specified in the contract to be entered with the successful bidder.

The Bank also reserves its right to claim damages for improper or incomplete execution of the assignment.

General Terms and Conditions

1. Bidder should compulsorily respond to any clarification (technical, functional, commercial) letter/E-mail sent by the Bank.

2. SDBL reserves the right to open the quotations soon after their receipt from all the Bidders without waiting till the last date

specified.

3. Continuity of project team members to be ensured during the period of project.

4. Presence of any incomplete or ambiguous terms/ conditions/ quotes will disqualify the offer.

5. SDBL is not responsible for non-receipt of quotations within the specified date and time due to any reason including postal

holidays, or other types of delays.

6. SDBL is not bound to place the order from the lowest price bidder or the most competent bidder.

7. The bidder shall share its technology strategies and research & development efforts, conducted in the course of this

assignment with SDBL.

8. All inquiries, communications and requests for clarification shall be submitted in Hard copies/e-mail to SDBL and response

for the same shall be obtained in writing. Only such documents shall be considered as authoritative.

9. The bidders should ensure that all points in the RFP document are taken into account before submitting the Bid Documents.

10. The bidder should have implemented similar assignment and necessary verifiable references in this effect should be

submitted with the proposal.

11. Bidders are bound to make full disclosure of information required to judge them on the basis of selection criteria specified

in RFP.

Order Cancellation

The Bank reserves its right to cancel the Purchase Order at any time by assigning appropriate reasons in the event of one or more of the following conditions:

1. Delay in delivery beyond the specified period for delivery. 2. Serious discrepancy noticed during the pre-dispatch inspection. 3. Serious discrepancies noted in the items delivered. 4. Breaches in the terms and conditions of the Order.

In addition to the cancellation of purchase order, the Bank reserves the right to foreclose the Security Deposit given by the supplier against the order to appropriate the damages.

Termination

Bank may, without prejudice to any other remedy for breach of agreement, by written notice of default sent to the selected bidder, terminate the agreement in whole or in part:

1. If the Bidder fails to deliver any or all of the Goods and Services within the time period(s) specified in the agreement, or within any extension thereof granted by SDBL or

2. If the Bidder fails to perform any other obligation(s) under the agreement. 3. If the Bidder, in the judgment of SDBL has engaged in corrupt or fraudulent practices in competing for or in executing the

agreement.

In the event SDBL terminates the agreement in whole or in part, SDBL may procure, upon such terms and in such manner, as it deems appropriate, Goods and services similar to those delivered and the selected bidder shall be liable to SDBL for any excess costs for such similar Goods and/or Services. However, the selected bidder shall continue performance of the agreement to the extent not terminated.

Governing Law

This document shall be governed by and construed in accordance with the laws of Sri Lanka and the courts of Sri Lanka shall have exclusive jurisdiction to hear and determine any matters or disputes arising herefrom or hereunder.

Force Majeure

The vendor shall not be liable for default or non -performance of the obligations under the contract, if such default or non -performance of the obligations under this contract is caused by any reason or circumstances or occurrences beyond the control of the vendor, i.e. Force Majeure . For the purpose of this clause, “Force Majeure” shall mean an event beyond the control of the vendor, due to or as a result of or caused by acts of God, wars, insurrections, riots, earth quake and fire, events not foreseeable but does not include any fault or negligence or carelessness on the part of the vendor, resulting in such a situation.

In the event of any such intervening Force Majeure, the Vendor shall notify the Bank in writing of such circumstances and the cause thereof immediately within five calendar days. Unless otherwise directed by the Bank, the Vendor shall continue to perform / render / discharge other obligations as far as they can reasonably be attended / fulfilled and shall seek all reasonable alternative means for performance affected by the Event of Force Majeure.

In such a case, the time for performance shall be extended by a period (s) not less than the duration of such delay. If the duration of delay continues beyond a period of three months, the Bank and the Vendor shall hold consultations with each other in an endeavor to find a solution to the problem. Notwithstanding above, the decision of the Bank shall be final and binding on the Vendor