Embed Size (px)

Citation preview

Sam

sung Life Insurance Annual R

eport

Samsung Life InsuranceAnnual Report FY2010 ( April 1, 2010 - March 31, 2011)

This brochure is printed on paper promoting sustainable forest management.

www.samsunglife.comSAMSUNG LIFE INSURANCE Co., Ltd 150, Taepyeongno 2-ga, Jung-gu,Seoul, KoreaTel. 1588-3114

2

Samsung Life values people first.

For over 50 years, as a trusted partner to our customers we strive to provide

the best products and services. Through continuous innovation, we are

a market leader in Korea and have set a higher goal of becoming a global

recognized insurance company going forward. We’ll spread a message

of caring as we believe insurance is founded on a deep desire to care and

protect your loved one.

People & Love

We spread a message of‘caring’ because people protect their loved ones fromtheir deep caring and love.

V i s i o n

C E O ’ s M e s s a g e

K e y E x e c u t i v e s

F i n a n c i a l H i g h l i g h t s

People & Love

02 Vision

04 CEO’s Message

06 Key Executives

08 Financial

Highlights

Innovation & Value

12 Love

Management

14 Virtuous

Management

16 Communicative

Management

Passion & Life

20 Research & Business

Operations

22 Global Operations

24 Asset

Management

26 Products

28 Customer Services30 Brands

Love & Love

34 Social

Contributions36 Sports

Sponsorship and

Arts & Cultures

Financial Report

39 Management’s

Discussion and

Analysis

43 Financial

Statements

51 Business Overview 54 Operations

Overview59 Corporate

Governance61 Audit Reports

0 2 0 3

Samsung Life has endeavored to emerge as

a global leader in providing customers

with secure and advanced financial insurance

solutions. In consideration of the rapidly

changing market environment, we are

redefining business domains and intensifying

core competencies that meet global standards.

Simultaneously, we are doing our best to

enhance business fundamentals for more

efficient business management.

Samsung Life has set targets on the retirement,

wealthy and overseas financial markets as

the main driving areas of future growth as well as

practicing creative change and innovation.

We will continue to make efforts to establish

our status as a globally competitive insurer

based on utmost products and services.

To be Respected as the World’s Premier

Provider of Financial Freedom

Enhance Core Competencies

We are laying the foundation

to take a leap toward being

one of the world’s premier

financial service providers by

intensifying differentiated core

competencies, while at the

same time creating greater

customers and shareholder

values.

Reform the Management System

We continue innovation to

promote swift decision-

making and practice rational

management.

We ensure stable corporate

growth through the

establishment of efficient

management systems.

Redefine Business Domain

We are redefining business

domains to offer more

stable and advanced

financial insurance solutions

in this rapidly evolving

financial environment as

well as to secure

sustainable growth.

V i s i o n

0 4 0 5

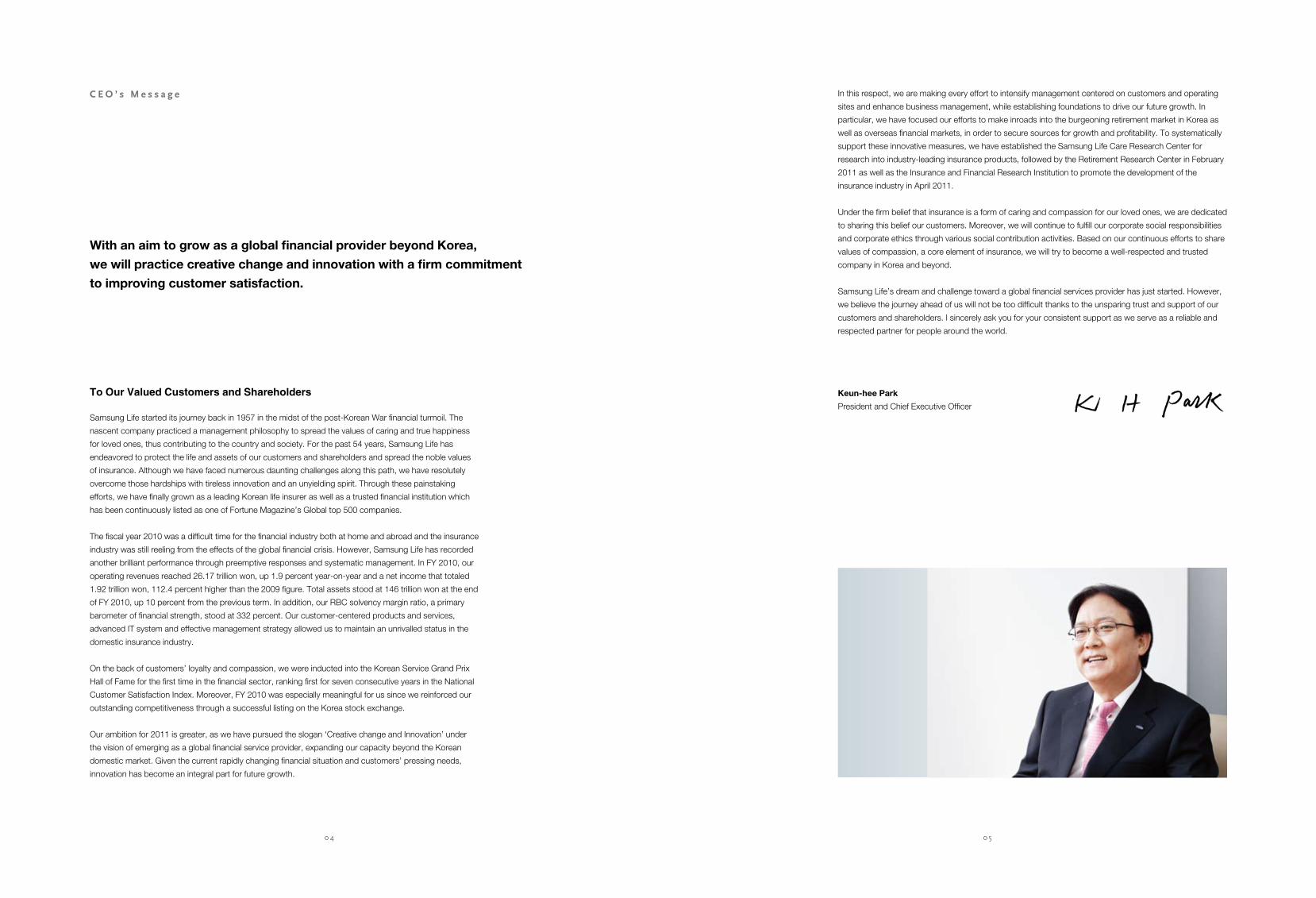

To Our Valued Customers and Shareholders

Samsung Life started its journey back in 1957 in the midst of the post-Korean War financial turmoil. The

nascent company practiced a management philosophy to spread the values of caring and true happiness

for loved ones, thus contributing to the country and society. For the past 54 years, Samsung Life has

endeavored to protect the life and assets of our customers and shareholders and spread the noble values

of insurance. Although we have faced numerous daunting challenges along this path, we have resolutely

overcome those hardships with tireless innovation and an unyielding spirit. Through these painstaking

efforts, we have finally grown as a leading Korean life insurer as well as a trusted financial institution which

has been continuously listed as one of Fortune Magazine’s Global top 500 companies.

The fiscal year 2010 was a difficult time for the financial industry both at home and abroad and the insurance

industry was still reeling from the effects of the global financial crisis. However, Samsung Life has recorded

another brilliant performance through preemptive responses and systematic management. In FY 2010, our

operating revenues reached 26.17 trillion won, up 1.9 percent year-on-year and a net income that totaled

1.92 trillion won, 112.4 percent higher than the 2009 figure. Total assets stood at 146 trillion won at the end

of FY 2010, up 10 percent from the previous term. In addition, our RBC solvency margin ratio, a primary

barometer of financial strength, stood at 332 percent. Our customer-centered products and services,

advanced IT system and effective management strategy allowed us to maintain an unrivalled status in the

domestic insurance industry.

On the back of customers’ loyalty and compassion, we were inducted into the Korean Service Grand Prix

Hall of Fame for the first time in the financial sector, ranking first for seven consecutive years in the National

Customer Satisfaction Index. Moreover, FY 2010 was especially meaningful for us since we reinforced our

outstanding competitiveness through a successful listing on the Korea stock exchange.

Our ambition for 2011 is greater, as we have pursued the slogan ‘Creative change and Innovation’ under

the vision of emerging as a global financial service provider, expanding our capacity beyond the Korean

domestic market. Given the current rapidly changing financial situation and customers’ pressing needs,

innovation has become an integral part for future growth.

With an aim to grow as a global financial provider beyond Korea,

we will practice creative change and innovation with a firm commitment

to improving customer satisfaction.

C E O ’ s M e s s a g e

Keun-hee Park

President and Chief Executive Officer

In this respect, we are making every effort to intensify management centered on customers and operating

sites and enhance business management, while establishing foundations to drive our future growth. In

particular, we have focused our efforts to make inroads into the burgeoning retirement market in Korea as

well as overseas financial markets, in order to secure sources for growth and profitability. To systematically

support these innovative measures, we have established the Samsung Life Care Research Center for

research into industry-leading insurance products, followed by the Retirement Research Center in February

2011 as well as the Insurance and Financial Research Institution to promote the development of the

insurance industry in April 2011.

Under the firm belief that insurance is a form of caring and compassion for our loved ones, we are dedicated

to sharing this belief our customers. Moreover, we will continue to fulfill our corporate social responsibilities

and corporate ethics through various social contribution activities. Based on our continuous efforts to share

values of compassion, a core element of insurance, we will try to become a well-respected and trusted

company in Korea and beyond.

Samsung Life’s dream and challenge toward a global financial services provider has just started. However,

we believe the journey ahead of us will not be too difficult thanks to the unsparing trust and support of our

customers and shareholders. I sincerely ask you for your consistent support as we serve as a reliable and

respected partner for people around the world.

0 6 0 7

Jong-yun Han Executive vice presidentCorporate insurance business division head

Stephan Rajotte Executive vice presidentInternational business division head

Woo-jung Suh Executive vice presidentCorporate governance division head

Sang-yong Kwak Executive vice presidentCorporate planning division head

Sang-hang Kim PresidentAsset Management business

Tae-gon Moon Standing member of audit committee Audit committee

Jae-ho Shim Senior vice presidentOverseas business division head

Young-soo Cha Senior vice presidentAsset management division head

Sang-yong Lee Senior vice presidentIndividual insurance business division head

See-hoon Cho Senior vice president Product strategy division head

Gwang-il ChoiSenior vice president Corporate business department 1 head

Sang-mook LeeSenior vice president Research institute of insurance & finance

Young-jae KangSenior vice president Gangbuk regional headquarters head

Je-hoon Yeon Senior vice presidentHuman resources division head

Young-june Park Senior vice presidentManagement innovation division head

Young-bin Lim Senior vice president Corporate business support division head

Sang-chul Lee Senior vice president Real estate investments department head

Jong-jung Youn Senior vice presidentBusan regional headquarters head

Chang-woo ByunSenior vice president Marketing division head

Jeong-soo HanSenior vice president Overseas business planning

Byung-soo ChoiSenior vice president IT Strategy division head

Donald CardenSenior vice president The president of siam samsung

Hong-joo KwakSenior vice president Internal audit division head

We will grow as a global financial institution based on

an effective and responsible management system that

incorporates creative change and innovation.

K e y E x e c u t i v e s

0 8 0 9

2008

121,000,000

2009

25,695,200

2008205%

2010

26,177,800 1.9%

2010

146,000,000 10%

2010 332%

52%

Net Income

Operating revenues

2008 113,000

Total assets

2009 133,000,000

2009

280%

2009

906,100

F i n a n c i a l H i g h l i g h t s

RBC ratio (Risk-based Capital Ratio)

2010

1,924,900 112.4%

2008

25,288,600

Unit : million won

Unit : million won

Unit : million won

Innovation & Value

Samsung Life offers custom management Through Innovative management philosophy and customers values.

L o v e M a n a g e m e n t

V i r t u o u s M a n a g e m e n t

C o m m u n i c a t i v e M a n a g e m e n t

1 2 1 3

Samsung Life values customers as it has strived

to satisfy customers’ needs through high quality

products and services. Through these efforts, it

has been ranked first in the Life Insurance seg-

ment on Korea’s National Customer Satisfaction

Index for seven consecutive years. Moreover,

the company has provided customers with

more systematic and advanced services includ-

ing our program ‘With Partner Service’ that

offers our business know-how of customer ser-

vice and the online consulting service ‘Web &

Call’ service.

Throughout 2011, Samsung Life will more ac-

tively pursue management centered on caring

and compassion. We will serve as a reliable and

life-long partner for our customers by offering

a wide range of valuable products and heartfelt

services. In addition, we will continue our efforts

to make the world a better place for everyone.

We are committed to providing a helping hand

for neglected neighbors through various volun-

teer activities as well as creating a welcoming

and pleasant living environment via our support

for sports, culture and the arts. Samsung Life

will spread true happiness and caring for all in

the world.

Love Management

Customers are the very

reason for our corporate

existence Through ‘Love

Management’ Samsung

Life will serve as a trusted

and life-long partner that

provides customers with

valuable products and

heartfelt services.

1 4 1 5

feedback

using various

feedback channels

Fevaluation

offering fair evalu-

ation and compen-

sation

Elistening

listening to various

opinions

Lidentification

identifying sound standards for

judgment

I

Samsung Life pursues management practices

that are pursuant to its core principles. We try

to secure management stability and growth by

sticking to fundamental values such as integrity,

sincerity and observance of laws.

Under our firm belief that we should be faithful

to the company’s fundamentals and principles,

even in the midst of the global financial crisis

that started in 2009, we proclaimed virtuous

management and established an ethics com-

mittee based on core action plans. Along with

an intensified monitoring system and fair trade

compliance program, we provide education on

virtuous management to our executives and

employees on a regular basis. In addition, we

allow our executives and employees to sponta-

neously participate in our ethical management

through an internal whistle blowing system and

campaigns on customer information protection

and incomplete sales prevention to expand vir-

tuous management to the corporate level.

Samsung Life has adopted strict rules and

regulations in order to enhance its overall level

of corporate transparency and reliability as a

publically listed company. We will continuously

pursue right-path management without being

swayed by the rapidly changing insurance mar-

ket environment.

Companies faithful to

undamental principles of

doing business deserve

to be respected by

ustomers. Samsung Life

has maintained its status

as a reliable and valuable

corporation through its

‘Virtuous anagement’ for

customers and society.

Virtuous Management

1 6 1 7

We can understand each

other and develop through

effective communications.

Samsung Life grows through

listening to various opinions

of customers, society and

employees and reflecting

them to management.

Samsung Life practices ‘Communicative Man-

agement‘ for understanding and development

of its customers and services. We have promot-

ed reasonable development based on commu-

nications with our employees, customers and

society.

To promote communications between head-

quarters and field sites sites, our executives

regularly visit operating sites to reflect on

changing customers’ needs and management

issues. Also, we listen to various opinions of

our employees by regularly posting the CEO’s

message on the corporate intranet to facilitate

more effective communications between our

executives and employees. We introduced and

operate a customer panel system for commu-

nications with our customers for the first time in

the industry, thus maintaining diverse commu-

nications channels with society through various

and systematic social contribution activities.

Samsung Life will continue to diversify commu-

nications channels for more effective commu-

nications and reflect these valuable opinions to

management.

Communicative Management

Passion & Life

Passion for customers and their life, Samsung Life endeavors to secure customers’ happiness.

R e s e a r c h & B u s i n e s s

O p e r a t i o n s

G l o b a l O p e r a t i o n s

A s s e t M a n a g e m e n t

P r o d u c t s

C u s t o m e r S e r v i c e s

B r a n d s

2 0 2 1

R e s e a r c h & B u s i n e s s O p e r a t i o n s

R&D to drive insurance advancement

Samsung Life established a scientific and systematic R&D

system to promote advancements in insurance services in an

effort to provide world-class insurance products and services.

The Retirement Research Center, established in February in

2011, was designed to enhance greater public awareness

on retirement and offer systematic retirement plans to

customers through a variety of comprehensive retirement

and financial planning schemes which are assisted by

the largest force of specialized agents. As a think tank to

support advanced retirement planning models, Samsung Life

offers customized retirement solutions and is taking the lead

creating a healthy retirement culture.

The Insurance & Financial Research Institute, founded in April

2011, consists of a financial industrial team, policy research

team and global strategy team. Moreover, the entire research

manpower is comprised of researchers with Master’s or

Doctoral degrees concentrating on future-oriented research.

Based on preemptive forecasts on changes in the insurance

and financial environment, it will secure mid to long-term

competitive edges of the company and advance the

development of insurance industry.

The Life Care Research Center, established in October

2010, contributes to the overall improvement of public health

and quality of life through its research into the health and

diseases of the public. This singular focus helps to create

trends in applicable insurance products. In collaboration with

various related institutions, it shares valuable information

including life-cycle health enhancement programs.

Samsung Life will continue its differentiated research and

development efforts and take a leading role in the insurance

and financial industry based on its specialized research

centers. These centers include the Retirement Research

Center, Insurance & Financial Research Institute and the Life

Care Research Center.

Samsung Life consultants, experts in financial planning

Samsung Life consultants, consisting of the largest force

of agents in Korea (over 40,000), is made up of a group

of comprehensive financial planning experts who offer

consulting services for protection-type and retirement

assets of customers through the state-of-the-art financial

planning tools and various financial products. These agents

are divided into various categories by target customer and

sales channels, thus ensuring the most professional and

efficient financial consulting services available. The categories

include: Financial Consultants (FCs) who provide financial

planning to individual customers; Samsunglife Advisors

(SAs), who offer integrated financial consulting services;

Group Financial Consultants (GFCs) who serve corporate

customers; Financial Advisors (FAs) who mainly sell variable

universal insurance policies and beneficiary certificates;

Special Financial Planners (SFPs) who are young university

graduates in their 20s and 30s; and Total Consultants (TCs)

who provide financial service telemarketing tools.

Samsung Life developed and operates its own consultant

education program and for the first time in Korea, obtained

the much-vaunted ISO 9001 certification related to education

program development and operating systems. In addition,

it continuously enhances its specialty in consulting services

through operating academy-industry and MBA programs.

About 75 percent of the 40,000 consultants are authorized

f inancia l consul tants, wi th 1,562 hav ing obta ined

membership in the Million Dollar Round Table, a renowned

international association of life insurance professionals.

Scientific and systematic Financial Planning Center

Samsung Life Financial Planning Center is a Wealth

Management group that offers wide-ranging scientific and

systematic financial planning services including investment,

taxation and real estate advice as well as consulting on

relevant laws, inheritance, donations and risk management to

VIP customers based on long-term perspectives. Samsung

Life has operated its FP center since 2002 and provides

effective comprehensive financial planning services through

asset management experts and financial analysis system

(SAPS), according to various customers’ financial situations.

Samsung Life FP Center has been selected as the ‘Best

PB’ in the life insurance category by Hankyung Business

magazine in 2010 for its differentiated competence and

brilliant performance.

Leveraging our methodical

R&D system, we take a leading role in

the insurance and financial industry.

We offer best-in-class financial

planning services to our customers

through experienced 40,000 of

financial consultant channel.

Our FP center delivers scientific

and comprehensive asset

management services based on

long-term perspectives.

2 2

G l o b a l O p e r a t i o n s

Samsung Life’s Current Overseas Business

12 overseas branches in 8 countries

(Insurance 2, Asset management 3, offices 7)

Insurance

China (2005)

Title : Samsung Air China Life Insurance Co., Ltd.

Local partner : Air China (5 : 5 joint venture)

Sales : 63.6 billion won (2010)

Thailand (1997)

Local partner

Saha Pathanapibul Group (37.5 percent)

Siam City Bank (25 percent)

Sales : 44.0 billion won (2010)

Investment

UK (1991) · US (1993) · Hong Kong (1996)

Investment scale : 3.5 trillion won

Third party consignment : 0.2 trillion won

Representative offices

U.S.(2), UK, Japan, China, India, Vietnam

Steady growth through localization strategy

Samsung Life has realized aggressive global management

through consistently exploring overseas financial markets

while diversifying our revenue resources by pursuing new

growth opportunities.

Siam Samsung Life Insurance Company, a joint venture in

Thailand (established in 1997), has maintained sound and

stable management practices through realistic localization

strategies by expanding the recruitments of local employees

as well as developing products suitable to local situations.

Samsung Air-China Life Insurance, a joint venture in China,

has also diversified its sales channels and enhanced its

overall product competitiveness to increase sales while

expanding its sales scope by opening branches in Tianjin in

March 2009 and Qingdao in July 2010.

We have opened branch offices in Mumbai in India and

Hanoi in Vietnam, attempting to make inroads into new

overseas financial markets. Additionally, Samsung Life

operates representative offices in New York, London, Tokyo

and Beijing to research advanced insurance markets and

systems. Through the aggressive expansion of our overseas

business divisions, we will reinforce our status as a global

financial service provider.

Stable overseas asset management

Samsung Life has been expanding its overseas investment

portfolio as part of its strategy to sustain continuous growth.

We have established subsidiaries in London in 1991 and

New York in 1993 to stay tuned to local financial markets.

We have accumulated investment experience in various

areas including overseas bonds, equities and funds, by

exchanging information with internationally renowned

financial institutions. We have partially reduced our overseas

investment in the aftermath of the global financial crisis,

but plan to gradually expand our overseas investment in

consideration of the current domestic investment market

conditions and increases in our invested assets in the

future. We are enhancing our risk management capacity for

overseas investment including intensifying self-screening

capacity and promoting the diversification of investment

areas and products.

We realize stable overseas asset management

based on our strong risk management capacity.

Through a successful implementation of localization strategy,

we solidify our presence in the global market.

2 3

2 5

Effective asset management philosophy

and investment strategy

Samsung Life has taken a stable and value-oriented asset

management approach that guarantees long-term results.

We are fully aware that stable asset management is the

foremost concern among our customers. To that end, we

have established a clearly defined management philosophy,

investment principles and guidelines. Our strategic asset

allocation (SAA) method allows us to build a portfolio from a

long-term perspective. Meanwhile we follow a tactical asset

allocation (TAA) strategy to respond flexibly to short-term

market fluctuations.

Efficient asset management portfolio

Samsung Life, with an AUM of approximately 146 trillion

won (General account 125 trillion won, Separate account

21 trillion won), is one of the largest asset managers in

Korea. We have invested these assets mainly in equities and

bonds, along with various additional investment products

including alternative investments and properties. In Korea,

our portfolio extends to various loan products for retail and

corporate borrowers. In the process, we have served as a

source of capital for various industries, contributing to the

nation’s economic development. We began investing in other

countries starting in 1996 and our overseas investments

today are worth a total of 12.7 trillion won. As such, our asset

management capabilities are recognized as being one of the

best in Korea.

Systematic scientific risk management

Samsung Life employs a phased approach to managing all

potential risks throughout the asset management process.

Risk management policy is first decided; risk is then managed

and measures are taken to stem any potential loss. We begin

by managing assets in consideration of their individual liability

characteristics, managing risks preemptively and balancing

risks and returns. Our approaches are both qualitative and

quantitative. We have proprietary VaR measuring and stress

testing instruments along with early warning and response

tools through risk monitoring.

In addition, our highly experienced underwriters and

advanced credit risk management system allow us to filter

out toxic assets while strengthening our capabilities to

analyze the quality of new financial instruments. We will

reinforce our risk management skills to ensure a stable return

on our customers’ valued assets.

Topnotch experts and system in asset management

Samsung Life ensures effective asset management by

employing the largest team (more than 480) of specialists in

the domestic industry. They include PhD holders in financial

engineering, graduates from the top MBA programs,

Certified Public Accountants, Chartered Financial Analysts,

Certified Commercial Investment Members, Financial Risk

Managers and employees with experience at some of

the world's top financial institutions. They are our valued,

unique assets. Moreover, we have established a unified

investment management system that systematically

handles the transaction, status and evaluation data for

all assets, providing customers with an effective range of

comprehensive services.

A s s e t M a n a g e m e n t Our efficient strategic asset management

portfolio in consideration of the market conditions

ensures sable profits for our customers

Our top-class asset management specialists

offer scientific and systematic risk management

2 4

2 6

Advanced insurance products

Our product lines include combination life insurance, variable

life insurance, whole-life insurance, health/critical illness (CI)

insurance, accident insurance and annuity products. The

combination life insurance product, which was developed

for the first time in the insurance industry, offers various

protection benefits under the umbrella of a single insurance

policy, while the variable life insurance increases or reduces

contractors’ contributions according to the overall fund

management performance. The whole-life insurance offers

various selective items and benefits in accordance with

customers’ specific needs and the health/critical illness (CI)

insurance guarantees benefits in the event of critical illness

or death. Additionally, annuity products promise financial

stability after retirement. In particular, “Perfect Combination

Life Insurance,” which we first introduced in September

2008, is a new product that combines whole-life, CI and

medical indemnity into a single insurance policy. So far, more

than 1.27 million of these plans have been sold to date as of

the end of April 2011.

Differentiated pension services for security in old age

Samsung Life leads Korea’s retirement insurance market

with 30 years’ experience in the business and offers the

best corporate pension specialists in the country. In 2009,

we launched the Total Solution service brand to even

further strengthen our position. Total Solution is Korea's first

corporate pension-related service available both online and

offline. With the introduction of the Total Solution service

brand, we continue to provide a wide range of services

that cover individual living benefits, annuity products,

management consulting and lifestyle design.

Convenient and quick Loan services

We offer effective loan products to suit customers’ financial

convenience.

All policyholders can borrow money against their policy

without actually having to visit us in person. Our credit loans

are available over the phone or online, eliminating the need

to visit our branch offices. In addition, borrowers do not

have to provide any collateral. Finally, our mortgage loans

offer various options with regard to specific interest rates

and terms. These include long term rates for customers who

need money to purchase or lease a house through consulting

services via the call center or loan consultants.

Funds and investment trusts for asset augmentation

Samsung Life fund products stand clearly apart from those

offered by brokerage houses or banks. We take advantage

of our strengths as an insurer, applying our extensive

expertise in managing a massive volume of long-term assets

to our fund management business for maximum customer

satisfaction. In addition, our investment trusts provide

customers with the best opportunities to augment their asset

portfolios. We individually design optimal asset portfolio for

our customers and recommend ideal trust instruments (non-

discretionary, discretionary and money markets) to suit each

individual’s long-term investment goals.

P r o d u c t s We satisfy our customers’ diverse needs

with outstanding insurance plans.

Our differentiated retirement products and

corporate pensions, loans, funds and investment

trusts contribute to creating a convenient and

abundant life for customers.

2 7

2 9

With partner service sharing CS know-how

Samsung Life has set its priority on management centered on

caring and compassion and tried to share customer services

know-how with both customers and local communities. As

part of this outreach effort, we began offering ‘With Partner

Service,’ a free customer service consulting program in

2008. As of 2010, the program has been conducted 1,822

times for 1,438 companies. The ‘With Partner Service’ is a

free training customer service program for volunteer groups,

government offices and small businesses that find it hard to

perform an objective evaluation for their customer service as

well as systematic CS education of their employees.

Ongoing efforts to raise customer satisfaction

We carefully listen to customer feedback at all times. Our

Call Center and service windows are standing by to answer

customers’ questions and to check on their policy status

and other financial matters. Our new Customer Complaint

Management System (CCMS) allows our staff to take the

initiative in resolving problems and is part of our efforts

to provide preventative responses that are up to global

standards. Our Voice-of-the-Customer (VoC) program is

another channel for customers allowing them to convey their

dissatisfaction, give advice or make demands. We take their

comments and feedback seriously and adapt them as much

as possible into the details of our operations. We also run an

online/offline customer panel as a way to collect customer

suggestions and requests for improving our overall service

quality. In addition, our relentless efforts to improve customer

satisfaction have been recognized by our top position on

Korea’s leading indices for customer service.

Business continuity plan to secure seamless

operation in crisis

Samsung Life has established a Business Continuity Plan

that guarantees smooth business management in the event

of a crisis. Based on core business areas that should be

immediately restored in emergency situations including

natural disasters, terrorism, fire or occupational hazards, we

established an extensive backup system, alternative areas

of business as well as an emergency manpower system.

By maintaining thorough preparations against emergencies,

we have obtained an international certificate from the

British Standards Institution for the first time in the domestic

financial industry in 2008. With our unyielding belief that

customer service should be seamlessly provided under any

circumstances, we will continue to develop our Business

Continuity Plan.

From one-stop to insurance consulting services

Samsung Life continues to develop various services to

ensure customer convenience. ‘Web & Call System,’ which

allows consultants to provide customers with a full range

of consulting services via the Internet, suggested a new

paradigm of insurance sales. We were first to adopt mobile

system in the domestic insurance industry to provide

customers with optimal financial consulting services and

introduced an Internet-based Insurance Service to allow

customers to browse account or produce information and

buy insurance policies through a one-stop process on the

Internet.

In addition, we ensure customer convenience by offering

a specialized consulting service program in which our

consultants make visits to customers in person to provide

information on specific benefits and insurance policies that

customers have purchased.

C u s t o m e r S e r v i c e s

2010 ~2011

Ranked 1st on the National Customer Satisfaction Index (NCSI) for seven consecutive years (’04~’10)

Ranked 1st on the Korean Customer Satisfaction Index (KCSI) for six years in a row (’05~’10)

Ranked 1st on the Korea Standard Service Quality Index (KS-SQI) for the past eight years straight (’03~’10)

Ranked 1st on Korea’s Most Admired Companies for eight consecutive years (’04~’11) : ranked 10th among

the 30 Most Admired All Star Companies (ranked 1st among financial institutions)

Ranked 1st on the Korea Service Grand Prix for the past six years in a row (’04~’09) : Inducted in the Hall

of Fame in 2010 (first in the financial sector)

We make customer convenience as a top priority, and

listen carefully to our customers’ feedback as we continue

innovation for quality and rewarding services.

2 8

3 0

A new advertising campaign

stressing values of insurance

The new ‘People, Compassion’ campaign, launched in

2011, has been well received by the public. The advertising

campaign is based on the fundamental values of insurance

that Samsung Life believes in, namely ‘Insurance is Love.’

Thus, the key message promotes the basic values that life

insurance provides to customers such as people, love, family

and life. We have partnered up with swimming gold medalist

Park Tae-hwan to appeal to a wide demographic range.

Through this campaign, we try to deliver our wil l to

establish new standards in the insurance business by

actively expressing our promise to secure ‘compassion’ for

‘loved ones’ along with values of compassion and caring

as the nature of the insurance industry. We maintain the

fundamental values of insurance, keeping it in mind and

acting as a trusted partner for our customers to return the

caring and support we received.

B r a n d s

Human beings are

made to love each

other including family

and themselves.

Samsung Life helps

customers to protect

their loved ones.

3 1

S o c i a l C o n t r i b u t i o n s

S p o r t s S p o n s o r s h i p a n d

A r t s & C u l t u r e s

Love & Love

Through sharing for tomorrow and increasing compassion for others, Samsung Life contributes to making the world a better place for all.

3 4 3 5

Project to fund trips back home for immigrant women married to Korean men

CSR programs for women

Samsung Life has continued to support women as an

integral part of its corporate social contribution programs.

Since 2002, we have offered seed money and business

consulting services to help low-income single mothers,

either divorced or widowed, start their own businesses. Our

employees have even started to donate funds to a Mothers’

Hope Camp, giving children plagued by poverty or illness the

necessary opportunities to realize their dreams. In addition,

Samsung Life promotes various activities including providing

funds to trips back for immigrant women married to Korean

men and establishing a multi-culture community.

Volunteer work in local communities

Samsung Life remains committed to helping Korea’s rural

areas across the country, thus alleviating regional disparities.

We established partnerships with 110 rural areas to promote

exchanges between urban and rural areas through offering

a helping hand during farming seasons, the purchase of

farming products as well as cultural exchanges. In addition,

we established a working dog training center in 2001. These

dogs have played a pivotal role in emergency rescues, drug

and explosives detection, infectious disease prevention and

cultural property preservation. Moreover, we have continued

to buy sporting equipment and other gears for the national

Paralympics team since 2000.

Environmental protection as a global citizen

Samsung Life has endeavored to fulfill its responsibility and

roles as a responsible global citizen. In an effort to preserve

the environment for succeeding generations, we continue

to be involved in tree planting campaigns across many

regions including the World Peace Forest in Incheon. These

efforts are conducted in conjunction with a planting project

of mangrove trees in Thailand in 2010 to reduce greenhouse

gas emissions.

S o c i a l C o n t r i b u t i o n s

Continuous and systematic CSR programs

help to make a better world for all.

We try to fulfill our responsibilities and

roles as a global citizen.

Various CSR programs

Samsung Life is engaged in various CSR activities as a good

global corporate citizen. To fulfill our responsibilities toward

society, we established the Samsung Life Public Service

Foundation in May 1982 and later on, the Samsung Life

Volunteer Corps in March 1995. Also, we have contributed

to raising public awareness on life insurance and spreading

insurance culture through the establishment of the Life

Insurance Social Contribution Fund in 2007. Our systematic

CSR programs for women, the environment and individuals

as well as local communities will continue to help make a

better world.

CSR programs as a partner for life

The various CSR programs at Samsung Life reflect elements

that characterize the life of the insurance business. Currently,

23 childcare centers are operating nationwide under the

Samsung Life Public Welfare Foundation, helping to support

working mothers and finding solutions for issues related to

early childhood development. The Samsung Medical Center

offers state-of-the-art medical systems that are used to

elevate the quality of medical care facilities and equipment

available in Korea. In an effort to address Korea’s rapidly

aging society, we operate Noble County, an advanced

retirement community with residential accommodations

and medical care facilities, along with cultural, sports and

recreational programs that ensure a comfortable life for the

elderly.

CSR programs for children and youth

We have continued to help children and youth to grow up

healthy and happy. In order to resolve the recent low-birth

rate issue, we implemented the ‘Three-Year Old Village

Project’ which provides for total care from childbirth to

nurture, along with various programs to encourage childbirth

and early childhood education programs. In addition, we

offer opportunities for youth to express their emotions

and improve their social skills through the ‘Samsung Life

Serotonin Drum Club Program.’

Planting program of mangrove trees in Thailand

The opening ceremony of store No.192 in the entrepreneurship support program for low-income single mothers

Farming volunteer work for local communities

3 6 3 7

Ji-hyeon Jeong, Samsung Life Wrestling Team

Jeong-eun Park, Samsung Life Women’s Basket Ball Team

Plateau, a cultural and resting space for the public

Art contest for youths

We have been organizing an annual art contest for children

and teenagers since 1981. Now in its 31st year in 2011, this

is the largest contest of its kind in Korea. The aggregate

number of participants exceeds 5.15 million and many

up and coming artistic talents have been identified and

nurtured though this inspiring event. We will ensure that the

competition continues to serve as a leading promoter of art

education in Korea.

HOAM Art Hall

HOAM Art Hall, which marks its 26th anniversary in 2010,

has helped to develop culture and nurture the arts in

Korea by showcasing both domestic and foreign quality

performances. In 2002, Korea’s cultural service specialist

Credia was entrusted with managing the center. The Hall has

re-established itself as an arts center specialized in classical

music and dance performances, becoming one of the most

successful cultural venues in the country.

The HOAM Art Hall remains committed to leading Korea’s

performing arts segment by taking on creative challenges

while preserving its unique tradition and dignified character.

Plateau

The Rodin Gallery, which opened in 1999 and remains

increasingly popular as a place where the public can

appreciate the quintessence of modern art, reopened under

the new title of “Plateau” in May 2011. Plateau will become

a cherished artistic venue for the public through various

cultural and artistic events and performances.

Bichumi Women’s Awards

The Bichumi Women’s Awards, established in 2001,

recognize those who have contributed to expanding

women’s social roles and to building women-friendly

practices in Korean society. They seek out next-generation

female leaders and work toward empowering them. Awards

are given to women in the workforce in the following four

categories: “Sun Awards,” for contributions in improving

the social status of women and in expanding women’s

rights; “Moon Awards,” for outstanding achievements in the

cultural, journalistic and social service fields; “Star Awards,”

for outcomes in the educational and R&D sectors; and

Special Awards.

S p o r t s S p o n s o r s h i p a n d A r t s & C u l t u r e s

Samsung Life Wrestling Team

Samsung Life established a wrestling team back in 1983

as one of several programs for supporting amateur sports

in Korea. Through hard work, the wrestling team has

significantly contributed to strengthening Korea’s stature

in international wrestling competitions. We have continued

with our sponsorship of this lesser-known sport and

many members of our team have represented Korea in

international competitions. Team members have earned

a total of 11 medals (4 Gold, 6 Silver and 1 Bronze) in the

Olympics since the 1988 Seoul Summer Olympics Games.

Samsung Life Women’s Basketball Team

Bichumi, the women’s basketball team sponsored by

Samsung Life, was established in 1977 and remained a

dominant force in the game, winning eight championships

at the Korea Basketball Festival (Amateur League) and five

more in the Professional Women’s Basketball League. Their

superb playing skills have earned them great popularity

among local basketball fans. Many team members have

also played on the Korea National Women’s Basketball

Team, which earned a silver medal during the 1984 LA

Summer Olympics, reached the semifinals at the 2000

Sydney Summer Olympics and the semifinals at the 2002

International Women’s Basketball Championship Games.

Samsung Life Table Tennis Team

The Men’s and Women’s Table Tennis Teams sponsored

by Samsung Life have helped to make Korea internationally

known in this sport. The teams were created in 1978 and

Samsung Life began managing them in 1999. They have

produced many world-class players, winning a Gold in the

Men’s Singles event and a Silver in the Women’s Doubles

event at the 2004 Athens Summer Olympics. Going

forward, we remain committed to developing Korean table

tennis and cultivating excellent players at the professional

level.

Various cultures and elegant arts create

a pleasant atmosphere and enrich our lives.

We share the spirit of hope through

sports participation.

Se-hyeok Ju, Samsung Life Table Tennis Team

The annual art competition for youth

3 8 3 9

M a n a g e m e n t ’ s D i s c u s s i o n a n d A n a l y s i s

39 Overview of Financial Results

F i n a n c i a l S t a t e m e n t s

43 Balance Sheet

47 Income Statement

50 Statements of Appropriations of Retained Earnings

B u s i n e s s O v e r v i e w

51 Business Developments

52 Corporate Developments

O p e r a t i o n s O v e r v i e w

54 Operating Performance Review

57 Operation Results and Financial Condition of the Recent Three Years

58 Mergers and Acquisitions

58 Challenges

Co r p o r a t e G o v e r n a n c e

59 Major Shareholders

59 Board of Directors and Audit Committee

A u d i t R e p o r t s

60 Audit Committee’s Audit Report

61 Report of Independent Auditors

M a n a g e m e n t ’ s D i s c u s s i o n a n d A n a l y s i s

Overview of Financial Results

Ⅰ. Largest Net Profit, Strong Growth in Assets, Capital, and EV

Unit : KRW billions

FY2010 FY2009 YoY

I/S Summary

Premium Income (excluding Corporate Pension)

18,787 17,913 4.9%

APE 3,526 3,659 – 3.6%

Net Profit 1,925 906 112.4%

B/S Summary

Total Assets 146,354 133,045 10.0%

Invested Assets * 118,656 107,229 10.7%

Shareholders' Equity 15,390 12,133 26.8%

RBC Ratio 332% 280% 52%p

EV Summary

Embedded Value 21,325 17,599 21.2%

Value of New Business 1,021 1,074 – 5.0%

New Business Margin 29.0% 29.2% – 0.2%p

* General Account Assets only. Excludes Separate Account Assets (21.5 trn) and Unamortized Deferred Acquisition Expense (3.8 trn).

Samsung Life’s total premium income for 2010, excluding corporate pension and retirement insurance, reached 18 trillion and 787

billion Won, which is a 4.9% increase from 2009. Including corporate pension and retirement insurance, the figure is 21 trillion 573

billion won.

Our net income grew 112% this year to a record 1 trillion 925 billion won. Our total assets increased 10% and our shareholders’

equity by 27% to end the year at 146 trillion 354 billion and 15 trillion 390 billion won respectively. Our RBC ratio, which gauges the

insurer’s financial strength, also jumped by 52 percentage points to end the year at 332%.

Meanwhile our embedded value at the end of 2010 increased by 21% over the year to record 21 trillion 325 billion won.

Financial Report

4 0 4 1

Annual Persistency Rate

77.8%

60.8%

81.8%

62.5%

FY2010FY2009

81.3%

60.8%

81.4%

61.2%

81.9%

63.4%

82.4%

64.8%

2Q10 3Q10 4Q101Q10

FY10 Persistency Rate by Quarter

Our persistency rate for the fiscal year was 81.8% and 62.5% for the 13th month and 25th month respectively. That translates to a 4

percentage point and 1.7 percentage point improvement year on year.

Breaking down those improvements quarterly, you can see there was a steady upward trend over the quarters. The standalone 4th

quarter persistency is the highest at 82.4% and 64.8% respectively.

Such improvements in persistencies is a direct result of the company’s efforts to instill sales practices focused on achieving efficiency

while pursuing new business growth. Because of such efforts, we expect further persistency improvement going forward.

Operating Expense Ratio

15.3

%

15.2

%

FY2010FY2009

Loss Ratio

85.3

%

84.3

%

FY2010FY2009

The improving profitability of the company is also visible in our expense and loss ratios.

Our operating expense ratio decreased by 0.1 percentage point to 15.2% this year, when excluding one-off organizational

restructuring expenses.

Our loss ratio is also stable, having decreased by 1 percentage point to record 84.3% for the entire year.

Both of those figures reflect the company’s tight cost discipline and claims management efforts. We will continue to improve the

company’s profitability in both areas going forward.

ROE

9.3%

15.3

%

14.0

%

23.2

%

FY2010FY2009

Net Profit

906

1,92

5

FY2010FY2009

Unit : KRW billions

Our net profit more than doubled this year to 1 trillion 925 billion won.

The main contributing factors are number one, the recovery of our Seoul Guarantee ABS loan loss provisions, and number two, the

gain on disposal of beneficiary certificates realized ahead of the introduction of IFRS Phase I, which add up to approximately 900

billion won in one-off profits for the year.

However, I would also like to note that even without these one-off items, our net profit for the year is 13% higher than last year. This

fulfills the promise we made at our IPO to deliver 10% earnings growth every year.

As a result of this performance, our stated ROE jumped from 9% to 14% this year, and our operating ROE, which adjusts for our

unrealized gains on affiliate holdings, jumped 8 percentage points to record 23%.

APE

3,65

9

3,52

6

FY2010FY2009

Unit : KRW billions

Our 2010 APE was 3.6% lower than our 2009 APE at 3 trillion 526 billion won.

This drop is largely due to a high base effect, stemming from an exceptional boost to our 2009 APE booked just before the October

2009 regulatory standardization of indemnity health insurance products, and the January 2010 change to the experience life table.

In addition, our companywide campaigns to improve policy persistency and eradicate mis-selling practices during the 2nd and 3rd

quarters also temporarily affected our new business sales.

That said, as you can see on the right side, our 4th quarter APE of 1 trillion 27 billion won is 23% higher than the average APE for the

first three quarters of this year.

Breaking down the quarterly APEs by product, you can see that our growth was well-balanced and achieved growth across all our

product lines, namely Protection, Annuity and Savings.

Such a rebound in our APE from January is a result of our new growth strategy and a new field oriented management focus. We are

confident that our sales force’s strong rebound in generating new business will continue going forward.

4Q APE Over 1~3Q Average

Annuity

Savings

Protection

Ⅱ. 4Q APE, Up 23% Over 1~3Q Average Ⅳ. Continued Improvement in Expense and Claims Management

Ⅲ. Net Profit Up 112% due to Stable Insurance Profit and One-offs Ⅴ. Continued Persistency Improvement through Emphasis on Sales Efficiency

ROE

Operating ROE

13th

25th

13th

25th

833

1,02

7

FY10 4Q(Avg.)FY10 1Q~3Q(Avg.)

Unit : KRW billions

4 2 4 3

F i n a n c i a l S t a t e m e n t

Balance Sheets

Samsung Life Insurance Unit : KRW

Account FY2010 FY2009

Assets

Ⅰ. Cash and deposits 4,466,756,254,342 3,544,742,015,942

1. Cash and deposits 933,996,509,519 1,499,389,185,167

Cash 226,295,200 272,810,319

Checking accounts 5,351,887,421 4,330,041,065

Savings accounts 193,094,726,668 216,620,561,413

Overseas savings accounts 7,863,110,940 8,936,410,325

Term deposits 257,979,000,000 825,670,505,056

Other bank deposits 469,481,489,290 443,558,856,989

Other deposits - -

2. Deposits 3,532,759,744,823 2,045,352,830,775

Term deposits 3,511,809,600,000 1,618,780,338,301

Other bank deposits 20,045,555,371 421,729,919,208

Deposits in future margin accounts 904,589,452 4,842,573,266

Other deposits - -

Ⅱ. Securities 84,790,273,347,545 74,086,845,239,422

1. Trading Securities 706,611,367,813 379,014,500,423

Government and public bonds 101,252,155,600 92,949,595,800

Special bonds 209,595,993,900 51,622,642,800

Financial bonds 50,314,012,100 -

Corporate bonds 94,395,111,080 -

Income securities 11,939,027,433 203,554,459,823

International securities - 30,887,802,000

Other securities 239,115,067,700 -

2. Available-for-sale securities 80,909,444,533,295 69,930,601,740,977

Equities 13,453,414,164,505 11,482,278,079,732

Investment in other companies - -

Government and public bonds 27,041,575,364,745 21,341,331,061,257

Special bonds 20,284,043,356,496 15,644,356,211,606

Financial bonds 1,883,952,935,338 1,922,394,553,288

Corporate bonds 3,016,643,847,358 2,735,266,572,494

Income securities 2,698,512,937,851 3,407,862,661,460

Investment Yield

5.5% 6.

2% 6.4%

7.4%

FY2010FY2009

As with other years, we continued our steadfast adherence to our asset liability matching investment strategy. In doing this, we saw

the proportion of bonds growing by 3 percentage points to make up 56% of our investment assets. Together with our loan book, the

total share of interest bearing assets as a percentage of total investment assets is over 80%.

Meanwhile, our investment yield increased by 90 basis points to 6.4%, due to the sale of our privately placed beneficiary certificates

ahead of the implementation of IFRS Phase I from April 1st, 2011.

The sale also helped our adjusted investment yield, which adjusts for unrealized valuation gains on our AFS securities, to increase by

120 basis points to 7.4%.

Total Assets & Invested Assets RBC ratio

280%

332%

FY2010FY2009

Total assets grew 10% to 146 trillion won at the year end while our investment assets grew 11% to 119 trillion won.

In particular, our total asset growth rate grew 8.2% per year, not including gains on equity valuation. At this rate, our total assets will

reach 200 trillion won by the year 2015.

As for our RBC ratio, which completely replaces the Solvency I regime starting from FY2011, we recorded 332% at the year end,

jumping 52% percentage points year on year.

This is because our risk amount or required capital increased by only 3% to 6 trillion 663 billion won while our available capital grew

by 22% to 22 trillion 116 billion won due to increase in net profit which flowed into our retained earnings.

Ⅵ. Continued Growth in Invested Assets & Capital Position

Investment Portfolio Composition

Total Assets

Invested Assets

Bonds 56%

Loans 20%

Stocks 13%

Investment Properties 4%

Beneficiary Certificates 3%

Cash and Deposits 4%

Investment Yield

Adjusted Investment Yield

Ⅶ. Continued Asset Liability Matching Strategy; Improved Investment Yield

FY 2010 : The year ended March 31, 2011

FY 2009 : The year ended March 31, 2010133

107

146

119

FY2010FY2009

Unit : KRW billion

4 4 4 5

Account FY2010 FY2009

International securities 12,296,012,129,916 12,512,666,001,950

Other securities 235,289,797,086 884,446,599,190

3. Held-to-maturity securities 1,228,480,500,374 2,261,192,703,611

Government and public bonds 1,088,482,675,928 2,061,113,484,633

Special bonds 139,997,824,446 200,079,218,978

4. Equity-method investment securities 1,945,736,946,063 1,516,036,294,411

Equities 1,762,340,470,056 1,350,458,811,800

Investment in affiliates 57,925,034,490 39,626,364,901

Non-listed international equities 102,849,396,576 98,655,664,516

Other securities 22,622,044,941 27,295,453,194

Ⅲ. Loans 24,200,854,920,562 24,530,227,455,000

(Reserves for doubtful accounts) (256,034,593,619) (708,116,775,655)

(Additional income in deferred loans) 5,816,364,090 1,629,536,732

1. Call loans 13,720,000,000 26,604,000,000

2. Policy loans 12,503,049,249,880 12,020,428,123,888

3. Loans secured by securities 20,179,000,000 20,000,000,000

4. Loans secured by real estate 7,371,377,965,506 7,941,726,462,354

5. Unsecured loans 3,803,474,861,567 3,981,700,728,234

6. Loans secured by third party guarantee 88,243,716,292 84,520,189,725

7. Other loans 651,028,356,846 1,161,735,189,722

Ⅳ. Investment Properties 719,899,664,658 725,924,183,331

1. Land 431,155,437,638 435,501,737,015

2. Buildings 322,442,636,687 285,283,144,228 319,535,204,683 289,598,246,752

(Accumulated depreciation) (37,159,492,459) (29,936,957,931)

3. Other structures 940,924,690 136,374,766 1,236,494,590 99,968,213

(Accumulated depreciation) (804,549,924) (1,136,526,377)

4. Assets under construction 3,324,708,026 724,231,351

Ⅴ. Tangible assets 4,541,708,645,641 4,397,673,296,098

1. Land 1,625,148,146,963 1,556,302,717,769

2. Buildings 3,533,741,213,557 2,705,419,822,210 3,396,363,180,451 2,633,937,356,171

(Accumulated depreciation) (828,321,391,347) (762,425,824,280)

3. Structures 47,167,077,222 7,910,100,972 48,156,503,054 9,157,641,492

(Accumulated depreciation) (39,256,976,250) (38,998,861,562)

4. Assets under construction 139,670,931,409 141,391,162,412

5. Vehicles and transportation equipment 6,596,135,770 3,331,661,028 5,130,966,264 3,183,311,776

(Accumulated depreciation) (3,264,474,742) (1,947,654,488)

6. Tools and equipment 386,289,301,157 51,364,801,162 393,431,884,577 45,144,595,981

Account FY2010 FY2009

(Accumulated depreciation) (334,924,499,995) (348,287,288,596)

7. Other tangible assets 8,863,181,897 8,556,510,497

Ⅵ. Other assets 6,167,174,691,027 6,223,279,874,714

1. Insurance receivables 53,208,013,263 53,123,211,661 57,463,748,152 57,411,731,995

Reserves for doubtful accounts (84,801,602) (52,016,157)

2. Other receivables 130,882,608,729 84,367,182,007 65,555,918,249 57,943,704,758

Reserves for doubtful accounts (46,515,426,722) (7,612,213,491)

3. Leasehold and other deposits 179,755,827,986 170,918,730,205

4. Accrued income 1,435,310,160,556 1,433,814,727,254 1,548,142,290,756 1,507,833,541,202

Reserves for doubtful accounts (1,495,433,302) (40,308,749,554)

5. Prepaid expenses 13,584,699,011 16,684,697,129

6. Prepaid income taxes 17,858,445,588

7. Advanced payments 1,521,483,061 1,870,973,592

8. Deferred acquisition cost 3,849,666,862,579 3,907,108,534,897

9. Financial derivatives assets 420,347,977,044 373,724,628,807

10. Intangible assets 105,542,720,424 86,415,886,541

Development cost 75,860,071,637 60,647,266,222

Software 27,754,564,843 23,447,429,326

Other intangible assets 1,928,083,944 2,321,190,993

11. Other assets 25,450,000,000 25,509,000,000

Ⅶ. Special account assets 21,466,951,335,493 19,536,380,885,879

Total assets 146,353,618,859,268 133,045,072,950,386

Liabilities and shareholders’ equity

Ⅰ. Policy reserves 99,133,436,390,357 92,024,917,919,895

(Reserve adjustment account for reinsurance ceded) (13,412,945,946) (14,434,527,253)

1. Premium reserves 94,794,270,031,756 88,118,767,795,089

2. Unearned premium reserves 17,300,821,105 21,598,158,216

3. Reserves for outstanding claims 572,473,506,573 331,243,803,437

Guaranteed minimum accumulation benefits 137,011,136,061 92,172,414,126

Guaranteed minimum death benefits 103,421,169,740 17,096,226,303

Others 332,041,200,772 221,975,163,008

4. Reserves for benefit payments 2,190,318,714,782 2,186,938,476,677

5. Reserves for participating policyholder dividends 1,419,567,568,775 1,335,451,108,499

Interest rate difference guarantee reserves 215,917,680,811 230,914,121,097

Mortality gains reserve 480,689,954,270 484,045,430,875

Interest gains reserve 440,512,447,059 329,369,723,114

Unit : KRW Unit : KRW

4 6 4 7

Income Statements

Samsung Life Insurance Unit : KRW

Account FY2010 FY2009

Ⅰ. Operating revenue 26,177,817,021,593 25,695,232,613,808

1. Premium income 14,589,412,645,073 14,514,661,423,051

Individual premium 14,119,956,851,444 14,024,401,808,069

Group premium 469,455,793,629 490,259,614,982

2. Reinsurance income 261,260,142,890 259,984,545,528

Assumed reinsurance premium 13,938,157,498 16,385,821,362

Ceded reinsurance claims recovered 201,237,135,689 198,826,267,499

Ceded Reinsurance Experience Refund 46,084,849,703 44,772,456,667

3. Interest income 5,069,741,032,484 4,929,102,366,246

Interest on bank deposits 138,367,580,265 161,894,927,761

Interest on trading securities 13,357,563,583 9,366,126,805

Interest on available-for-sale securities 2,978,159,697,875 2,677,061,941,202

Interest on held-to-maturity securities 109,274,487,896 156,916,633,191

Interest on loans 1,811,354,683,741 1,903,369,103,714

Interest on other deposits 286,398,257 799,826,871

Other interest income 18,940,620,867 19,693,806,702

Account FY2010 FY2009

Expense gains reserve 273,419,679,491 280,626,753,361

Long-term duration dividend reserves 8,737,801,405 10,169,626,067

Reserves for asset revaluation 290,005,739 325,453,985

6. Excess participating policyholder dividend reserves 146,559,763,161 38,501,692,780

7. Reserves for assumed reinsurance premium 6,358,930,151 6,851,412,450

Ⅱ. Policyholders’ equity adjustment 5,213,858,993,823 4,739,854,792,927

1. Reserves for policyholder dividend stabilization 113,824,607,586 113,824,607,586

2. Fund for public projects 44,000,060,898 44,000,060,898

3. Gains (losses) on valuation of available-for-sale securities 4,973,127,015,504 4,533,084,906,397

4. Gains (losses) on valuation of held-to-maturity securities 1,731,988,326 2,304,858,186

5. Gains (losses) on valuation of equity-method investment 81,175,321,509 46,640,359,860

Ⅲ. Other liabilities 4,972,055,704,410 4,510,073,140,217

1. Unpaid claims 9,561,617,396 12,717,271,985

2. Other accounts payable 55,820,255,663 97,014,254,436

3. Accrued expenses 468,932,467,216 379,097,935,906

4. Accrued income taxes 146,709,613,670

5. Advance receipt 61,880,800 596,984,100

6. Unearned revenue 1,403,201,152 431,286,484

7. Withholdings 32,631,031,484 31,798,891,779

8. Accrued VAT

9. Unearned insurance premium 172,735,531,403 93,275,155,168

10. Leasehold deposits received 456,715,909,323 443,256,912,991

11. Reserves for severance benefits 250,222,339,000 56,210,754,322 230,206,920,310 45,377,390,848

(National Pension Fund Payment) (1,409,089,238) (1,663,537,538)

(Corporate pension plan asset) (192,602,495,440) (183,165,991,924)

12. Deferred income tax credits 2,337,803,839,333 1,768,382,853,584

13. Financial derivatives liabilities 1,140,828,843,314 1,539,917,967,556

14. Other trust accounts payable 3,336,856,853 607,522,433

15. Other liabilities 89,303,902,481 97,598,712,947

Ⅳ. Separate account liabilities 21,644,287,347,190 19,637,406,624,404

Total liabilities 130,963,638,435,780 120,912,252,477,443

Ⅰ. Capital stock 100,000,000,000 100,000,000,000

1. Common stocks 100,000,000,000 100,000,000,000

Ⅱ. Capital surplus 6,131,429,078 6,131,429,078

1. Asset revaluation reserves 6,131,429,078 6,131,429,078

Ⅲ. Capital adjustment 13,493,452,365 0

Account FY2010 FY2009

1. Other capital adjustment 13,493,452,365 0

Ⅳ. Accumulated other comprehensive income 7,461,164,091,242 5,948,767,137,032

1. Gains (losses) on valuation of available-for-sale securities 8,203,393,094,668 7,041,126,770,664

2. Gains (losses) on valuation of held-to-maturity securities 2,861,814,883 3,599,114,252

3. Gains (losses) on valuation of equity-method investment 135,884,217,436 74,648,216,540

4. Gains (losses) on valuation of derivatives (908,290,985,249) (1,193,949,259,896)

5. Separate account capital adjustment 27,315,949,504 23,342,295,472

Ⅴ. Retained earnings 7,809,191,450,803 6,077,921,906,833

1. Legal reserves 50,000,000,000 50,000,000,000

2. Other legal reserves 2,327,741,074 2,327,741,074

Reserves for business improvement 2,327,741,074 2,327,741,074

3. Unappropriated retained earnings 7,756,863,709,729 6,025,594,165,759

(Net income) (1,924,853,105,490) (906,095,135,663)

Total shareholders’ equity 15,389,980,423,488 12,132,820,472,943

Total liabilities and shareholders’ equity 146,353,618,859,268 133,045,072,950,386

FY 2010 April 1 – March 31, 2011

FY 2009 April 1 – March 31, 2010

Unit : KRW Unit : KRW

4 8 4 9

Account FY2010 FY2009

8. Gains (losses) in securities trading 51,069,550,502 209,579,406,821

Losses on valuation of trading securities 853,487,987 240,762,856

Losses on disposition of trading securities 2,550,529,961 953,306,869

Losses on disposition of available-for-sale securities 34,670,502,956 166,565,207,532

Impairment loss on available-for-sale securities 12,995,029,598 41,820,129,564

9. Losses on valuation and disposition of loans 520,749,528

Bad debt expenses

Losses on sale of loans 520,749,528

10. Losses on foreign currency trading 54,736,484,581 373,058,921,042

Losses on foreign currency translation 11,336,969,928 118,821,473,393

Losses on foreign currency transaction 43,399,514,653 254,237,447,649

11. Amortization expenses of intangible assets 33,474,953,071 18,855,064,605

12. Discount expenses 3,100,980,644 1,151,422,124

13. Separate account expense 3,179,885,849,390 3,759,799,223,706

14. Amortization expenses of real estate 52,572,138,197 54,951,763,398

15. Other operating expenses 260,235,687,795 443,802,757,305

Losses on disposition of derivatives 193,870,709,934 346,455,911,992

Losses on valuation of derivatives 12,586,364,503 38,821,412,044

Other bad debt expenses 555,054,749 718,841,461

Other operating expenses 53,223,558,609 57,806,591,808

Ⅲ. Operating income 1,947,198,409,240 848,748,759,940

Ⅳ. Non-operating income 775,557,702,084 430,576,583,336

1. Gains on valuation of equity method 322,270,249,946 236,264,225,515

2. Gains on disposition of equity-method investments 340,273,570 -

3. Gains on disposition of investment properties 1,324,597,568 82,334,903,270

4. Gains on disposition of tangible assets 8,390,790,304 67,084,575,325

5. Miscellaneous non-operating income 443,231,790,696 44,892,879,226

Ⅴ. Non-operating expenses 113,115,130,005 110,407,375,895

1. Losses on valuation of equity method 9,216,930,672 6,542,736,467

2. Losses on disposition of equity-method investments 4,969,617,183

3. Losses on disposition of investment properties 13,947,940,572

4. Losses on disposition of tangible assets 4,265,704,634 19,492,398,471

5. Donations 76,604,985,083 32,379,417,038

6. Miscellaneous losses 23,027,509,616 33,075,266,164

Ⅵ. Net income before income taxes 2,609,640,981,319 1,168,917,967,381

Ⅶ. Income taxes expenses 684,787,875,829 262,822,831,718

Ⅷ. Net income 1,924,853,105,490 906,095,135,663

Account FY2010 FY2009

4. Gains on securities trading 1,092,471,480,326 353,266,981,149

Gains on valuation of trading securities 435,468,980 5,385,352,659

Gains on disposition of trading securities 15,196,658,953 9,875,528,123

Gains on disposition of available-for-sale securities 1,076,839,352,393 293,168,174,740

Restoration of available-for-sale securities 44,837,925,627

5. Gains on valuation and disposition of loans 464,358,781,054 9,279,468,842

Transfer from allowance for credit losses 464,358,781,054 9,279,468,842

6. Gains on foreign currency trading 154,125,352,053 238,226,524,186

Gains on foreign currency translation 2,524,365,894 97,697

Gains on foreign currency transaction 151,600,986,159 238,226,426,489

7. Commission income 50,451,892,676 47,608,594,860

8. Dividend income 191,680,695,533 160,560,916,989

9. Rental income 255,064,717,746 211,273,492,446

10. Separate account commission received 633,214,740,452 541,597,967,544

11. Separate account income 3,179,885,849,390 3,759,799,223,706

12. Trust account income 1,191,169,675 426,875,187

13. Other operating income 234,958,522,241 669,444,234,074

Gains on disposition of derivatives 95,245,897,537 414,662,122,979

Gains on valuation of derivatives 79,486,617,805 225,124,804,197

Other operating income 60,226,006,899 29,657,306,898

Ⅱ. Operating expenses 24,230,618,612,353 24,846,483,853,868

1. Increase in policy reserves 7,009,440,905,400 4,485,012,224,692

2. Claim paid 9,505,249,576,570 11,585,814,898,277

Benefit payments 1,655,022,315,195 1,319,641,431,025

Refund 7,736,204,826,349 10,136,392,659,835

Dividend expenses 114,022,435,026 129,780,807,417

3. Reinsurance expenses 283,057,288,015 280,713,238,080

Ceded reinsurance premium 269,763,561,556 269,084,278,753

Assumed reinsurance claims 10,675,320,568 7,775,758,318

Assumed reinsurance experience refund 2,618,405,891 3,853,201,009

4. Operating expenses 1,531,797,214,422 1,339,510,086,007

(Deferred acquisition expenses) (1,799,029,735,360) (1,890,722,523,388)

Acquisition expenses 1,807,685,076,565 1,930,792,004,656

Administration expenses 1,523,141,873,217 1,299,440,604,739

5. Amortization of deferred acquisition cost 1,856,471,407,678 1,903,278,320,419

6. Property administrative expenses 394,682,406,775 377,481,447,572

7. Interest expenses 14,323,419,785 13,475,079,820

Unit : KRW Unit : KRW

5 0 5 1

B u s i n e s s O v e r v i e w

Business Developments

Throughout FY 2010, Samsung Life has aggressively pursued three main corporate strategies such as securing solid sources for

profitability over the mid-to long-term, building leadership in the market and reinforcing intangible competitiveness through corporate

culture innovation. These three goals have been pursued under management’s direction to secure profitability and growth for

maximum corporate values.

To that end, we have established a next-generation system to support a ubiquitous computing-based operating environment to

secure differentiated operating competitiveness and introduced an advanced management system for customers and products.

In addition, we have endeavored to make qualitative improvements through enhancing persistency ratio as well as simultaneously

improving our corporate competencies through optimizing work process. Moreover, we have secured an unrivalled competitive edge

in human resources by recruiting outstanding new workers as the basis of our growth engine while reinforcing our core manpower

resources.

As a result, we achieved operating revenues of 26.17 trillion won and a net income of 1.92 trillion won. Our total assets amounted to

146.35 trillion won at the end of FY 2010. Moreover, we still held the highest market share in terms of overall protection, annuity and

retirement pension insurance plans.

Based on accumulated risk management skills and profitability, we are making full-fledged efforts to secure the innovation of our

business structure, improve sound profitability as well as new growth engines in order to sustain continuous growth and secure

additional sources of profits.

We have made efforts to develop various new products to offer customers a wide range of choices and diversified insurance

channels by actively using our advantageous exclusive sales channels as well as general agents and bancassurance schemes. We

will establish the largest retirement research center in order to fully prepare for the retirement market which is expected to lead to

steady growth stemming from Korea’s rapidly aging society. In addition, we will maintain our solid and sound growth momentum by

strengthening our efforts to make inroads into wealthier markets. In addition, the establishment of a ‘comprehensive marketing team’

under the direct control of the CEO will allow us to realize the utmost in customer satisfaction management.

Our efforts to diversify revenue sources are also accelerating to secure a long-term growth engine. As part of this attempt, we have

expanded our existing overseas business department to the overseas business division. Other changes include more aggressively

expanding our overseas business through thorough localization efforts in China and Thailand.

Samsung Life has reinforced its status as the largest domestic life insurer as it successfully went public on the Korean exchange on

May 12, 2010. Without being satisfied with the success that we have achieved, we will make every effort to practice the values of life

insurance, enhancing our corporate values as our top management priority which will help us emerge as a global insurance services

provider that is trusted and loved by our customers and shareholders throughout the world.

Statements of Appropriations of Retained Earnings

Samsung Life Insurance Unit : KRW

Account FY2010 FY2009

Ⅰ. Retained earnings before appropriations 7,756,863,709,729 6,025,594,165,759

1. Unappropriated retained earnings carried forward from prior years

5,800,594,165,759 5,119,499,030,096

2. Cumulative Effect of the Equity Method 31,416,438,480 0

3. Net income 1,924,853,105,490 906,095,135,663

Ⅱ. Appropriations of retained earnings 400,000,000,000 225,000,000,000

1. Dividends

Cash dividends 400,000,000,000 225,000,000,000

(Dividend rate as of Par Value) (400%) (225%)

Ⅲ. Unappropriated retained earnings carried over to subsequent year

7,356,863,709,729 5,800,594,165,759

Expected date of appropriation in FY 2010 June 3

Settlement date of appropriation in FY 2009 June 1

5 2 5 3

Ⅴ. Shares 1. Types and Numbers of Shares Issued Unit: KRW

Type The volume of stocks Amount Proportion (percent) Remark

Registered common shares 200,000,000 100,000,000,000 100% -

2. Changes in Capital Stock Unit: KRW

Date Type The volume

of stocksChange in the

Shareholders’ Equity Total Shareholders’

EquityDetail

’63. 1. 28 Registered common shares 50,000 25,000,000 50,000,000 Capitalization of revaluation reserves

’71. 4. 26 Registered common shares 300,000 150,000,000 200,000,000 Capital increase with consideration

’77. 9. 23 Registered common shares 600,000 300,000,000 500,000,000 Capital increase with consideration