Embed Size (px)

Citation preview

Sampling Concepts in Sales and Use Tax Audits

Revised February 23, 2008

Dr. Will Yancey, CPAIndependent Consultant

Dallas, [email protected]

972.387.8558

2

Objective

Objective is NOT: To stress you To make you a statistician in one hour

Objective IS: To stimulate your thinking To impart practical knowledge for managing audits

of sales and use tax, unclaimed property, etc.

Encourage discussion at any time

3

Copyright

You are welcome to use these concepts and repeat anecdotes.

Before you reproduce or distribute these materials, please let me know.

Dr. Will Yancey retains the copyright on all materials he creates.

©

4

Know Your Data!

Availability of supporting documents is your best defense in any audit of sales and use tax, unclaimed property, or other transactions.

Do a preliminary investigation before the auditors arrive. Conduct a “walk-through” to discover and document what

supporting documents are available and retrievable. Include electronic and paper files

Identify potential exposure areas

Data mining software links at http://willyancey.com/data-mining.htm IDEA from www.audimation.com in Houston

5

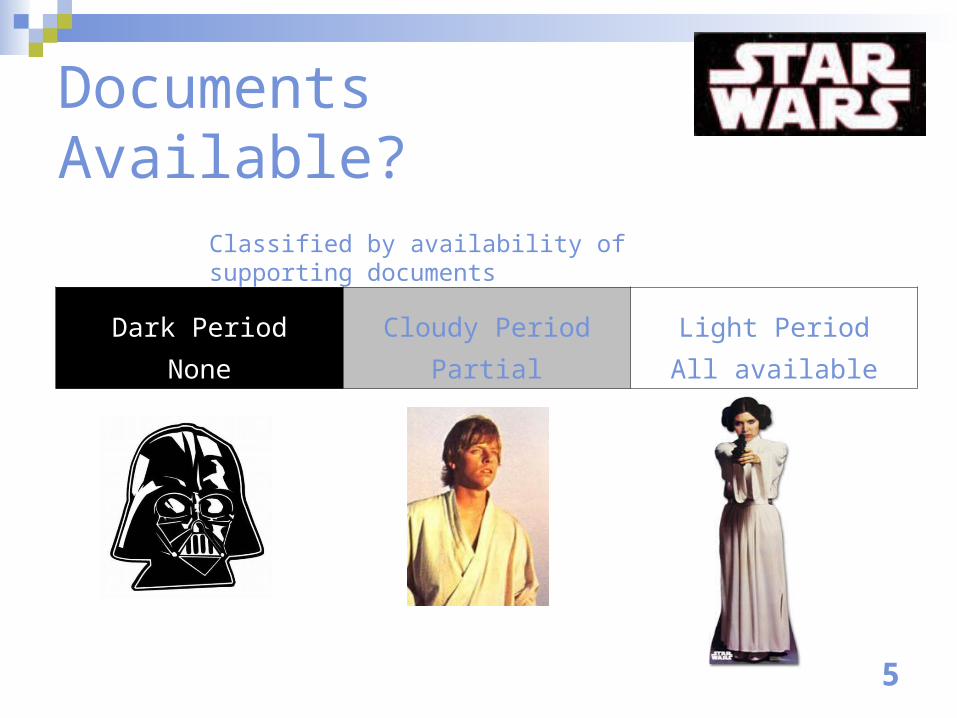

Documents Available?

Classified by availability of supporting documents

Dark Period Cloudy Period Light Period

None Partial All available

6

Dark Period

The Dark Period includes the older years where no supporting documentation can be located.

All that may be known about the Dark Period is total revenue by year, total purchases, or some other total $.

7

Light Period

The Light Period covers the more recent years where we have access to all data:

Total revenue Supporting documents Name and address information

The Light Period is the basis for estimation to the Dark Period

Depending on the number of items we can: Sample, or Review the actual detail (also known as 100% sample, census,

actual basis).

8

Cloudy Period

Facts and data are unclear in the Cloudy Period.

Control totals may exist.

Some supporting documents are missing. BUT, we must make a decision on where to separate

the Dark Period from the Light Period. Know your records before the auditor selects the sample!

9

Dark Period Estimation

Estimate liability for the Dark Period. Generally involves an estimated ratio of Liability-to-

Revenue or Liability-to-Total-Payables from the Light Period.

Project that ratio onto Dark Period.

Justification All states do estimates for bars, restaurants, and small

businesses where records are unavailable. If there is less than 100% error rate in the Light Period, it

is reasonable to assume less than 100% error rate in the Dark Period.

10

Sales Data

Billing system versus Accounts Receivable (A/R) system

Customer master file Sales tax exemption certificates

http://willyancey.com/tax_sales.htm#exempt-certs Sales product description codes Sales tax billed but not paid (“short pay”) Bad debts: billed but no payment On consignment but sale not consummated

11

Location Data

Bill-to versus ship-to address Origin vs. Destination sourcing for taxing

jurisdiction Local city and county situsing errors

Increasing attention from local government Goods received documentation Services delivered documentation Modification at central facility before deployment

to field locations

12

Purchases Data General Ledger (G/L) versus Accounts Payable (A/P)

Detail versus aggregate Documenting where and how used

Purchase orders (PO) Requisitions to vendor or company stores Authorization for expenditure (AFE) Contracts Receiving reports Affidavits from operations people

Clearing accounts Work in progress (WIP) Construction in progress (CIP) Prepaid expenses Installment payments and deposits paid

13

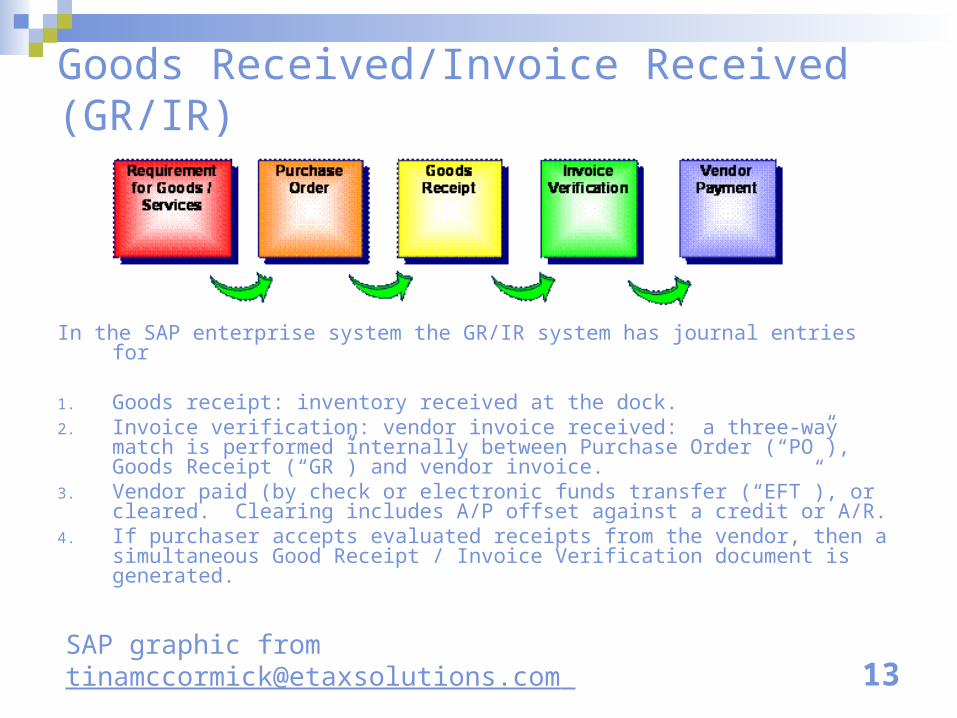

Goods Received/Invoice Received (GR/IR)

In the SAP enterprise system the GR/IR system has journal entries for

1. Goods receipt: inventory received at the dock.2. Invoice verification: vendor invoice received: a three-way match is

performed internally between Purchase Order (“PO”), Goods Receipt (“GR”) and vendor invoice.

3. Vendor paid (by check or electronic funds transfer (“EFT”), or cleared. Clearing includes A/P offset against a credit or A/R.

4. If purchaser accepts evaluated receipts from the vendor, then a simultaneous Good Receipt / Invoice Verification document is generated.

SAP graphic from [email protected]

14

Fruit Salad Parable

Task is to estimate the amount of different fruits by sampling a single spoonful.

1. Fruit in four large chunks.

2. Fruit cut in many small pieces

3. Fruit crushed in a smoothie

4. Fruit floating in liquid

15

Triage

Different strategies for

different sub-populations Exclude: No likelihood of error Detail: Actual base exam of every item Sample: Likely to be some errors; and

cost of sampling is less than cost of detail.

16

Exclude

Possible exclusions in a sales and use tax audit (but not all situations):

Always pay sales tax to vendor and always taxable: telecom, utilities, etc.

Never pay sales or use tax and always exempt: charitable contributions, government taxes and fees, inventory for resale, employee benefits

No tax consequence: some journal entries, reversals, and reclasses, etc.

17

Detail

Possible detail in a sales and use tax audit (but not all situations):

High dollar items. High threshold somewhere between $5,000 and $500,000,

depending on population. Select vendors or customers where always in

error. Construction in progress (CIP) Information Technology (IT) purchases that

include taxable and nontaxable components

18

Reversals

Reversals (“negative amounts”) occur because of reclassifications, error corrections, returns, voids, etc.

The negative amounts are offset to the positive amounts.Matched pair = one positive $ offset one

negative $ to the exact amountMultiple rows or partial offsets

19

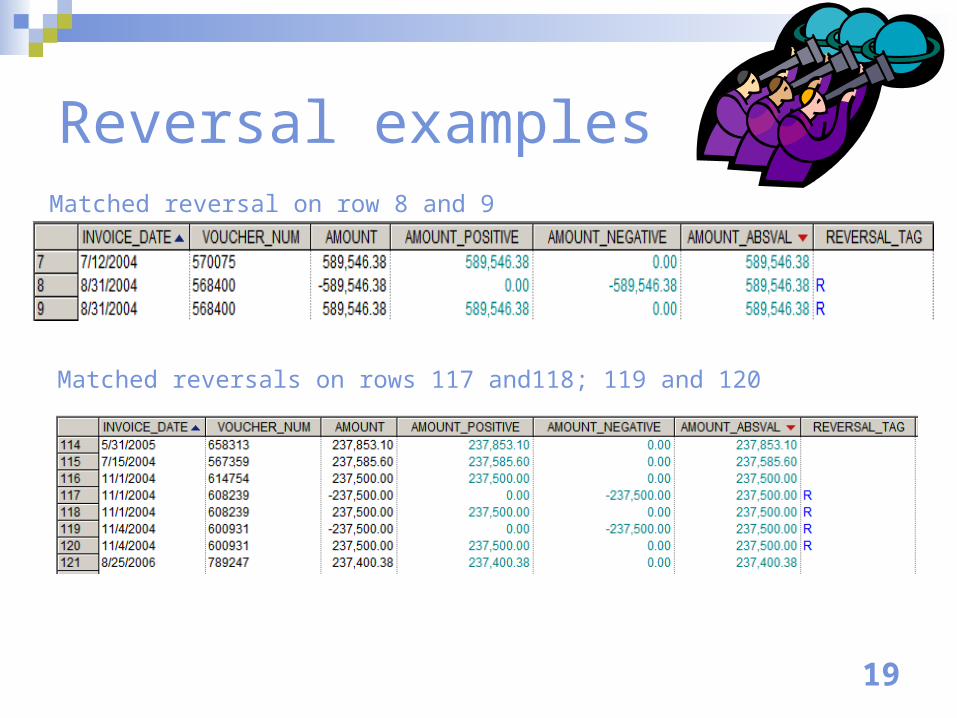

Reversal examplesMatched reversal on row 8 and 9

Matched reversals on rows 117 and118; 119 and 120

20

Strategies for Reversals

Chose a combination of these: Match and extract

Sort by descending absolute value $ Detail the largest negative items Sample some negative items Apply error rate from positive $ onto negative $ Ignore the negatives if very small % of total

positive population base $Does the auditor need to see supporting

documentation for every reversal?

21

Sampling

Sampling in a sales and use tax audit (but not all situations):

Likely to be some error Cost of sampling is less than detail exam. Mix of many different vendors. Taxpayer and auditor can agree on

sampling plan.

22

What Pie to Sample?The sample error rate is projected on to what pie?

23

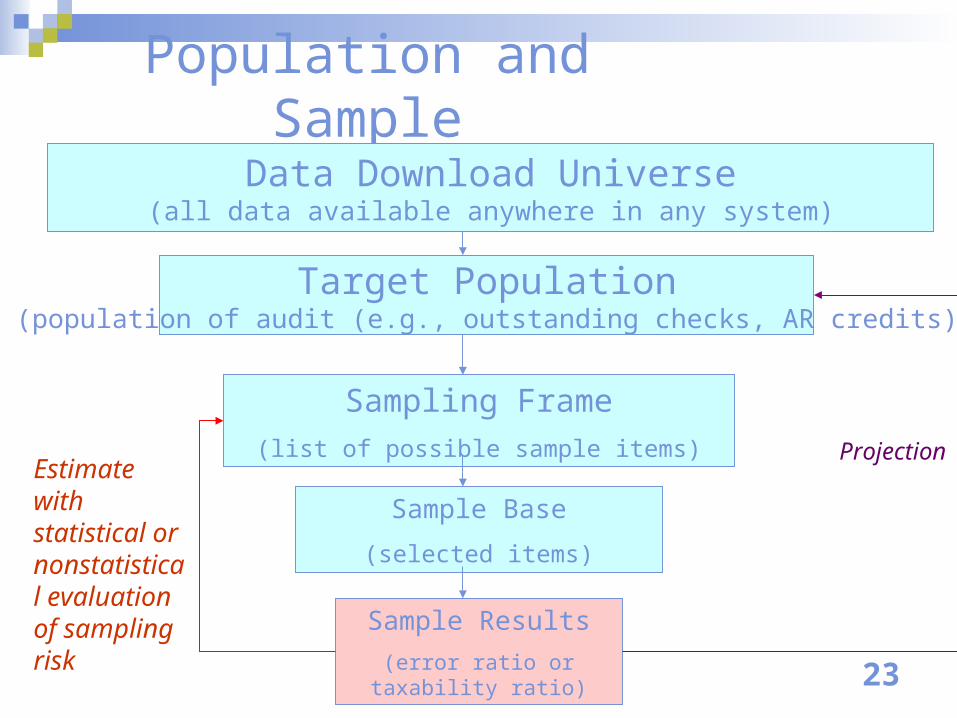

Population and Sample

Data Download Universe(all data available anywhere in any system)

Target Population(population of audit (e.g., outstanding checks, AR credits)

Sampling Frame

(list of possible sample items)

Sample Base

(selected items)

Sample Results

(error ratio or taxability ratio)

Estimate with statistical or nonstatistical evaluation of sampling risk

Projection

24

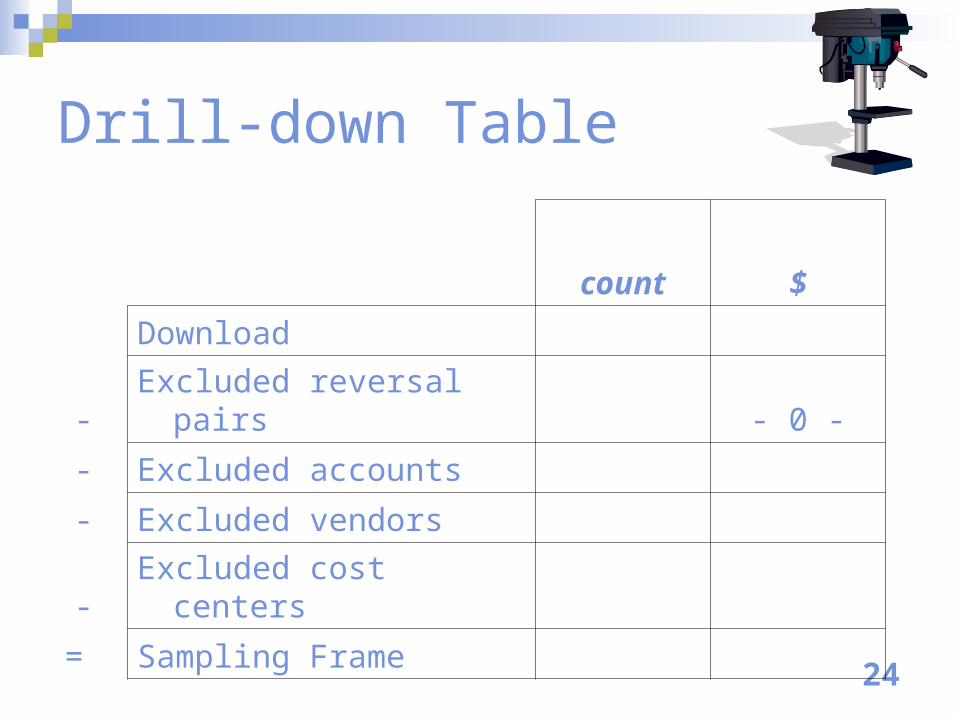

Drill-down Table

count $

Download

- Excluded reversal pairs - 0 -

- Excluded accounts

- Excluded vendors

- Excluded cost centers

= Sampling Frame

25

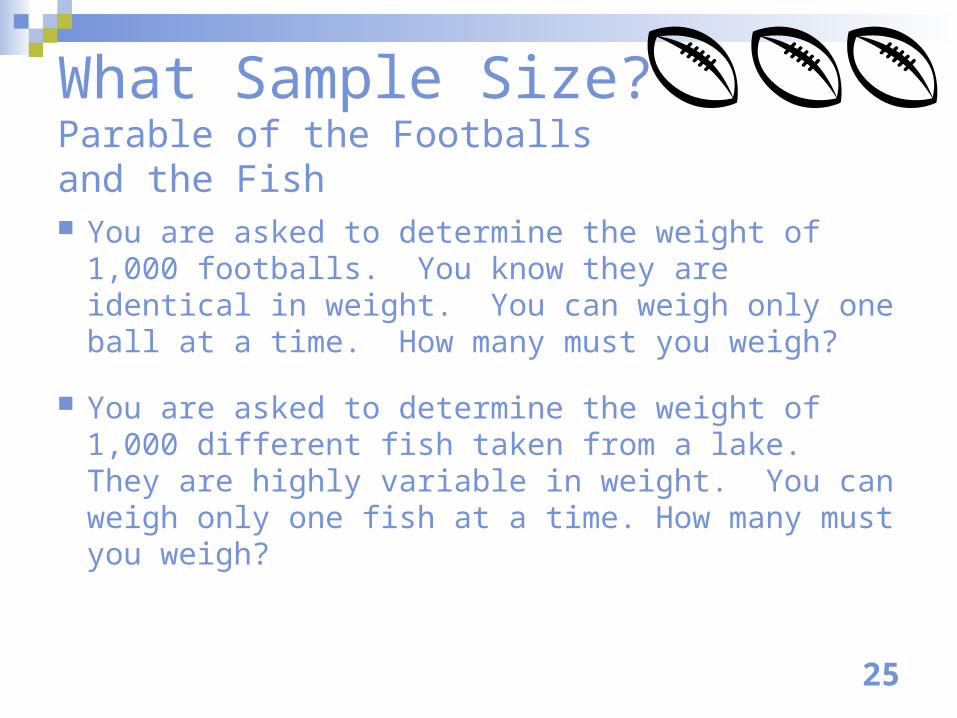

What Sample Size?Parable of the Footballs and the Fish

You are asked to determine the weight of 1,000 footballs. You know they are identical in weight. You can weigh only one ball at a time. How many must you weigh?

You are asked to determine the weight of 1,000 different fish taken from a lake. They are highly variable in weight. You can weigh only one fish at a time. How many must you weigh?

26

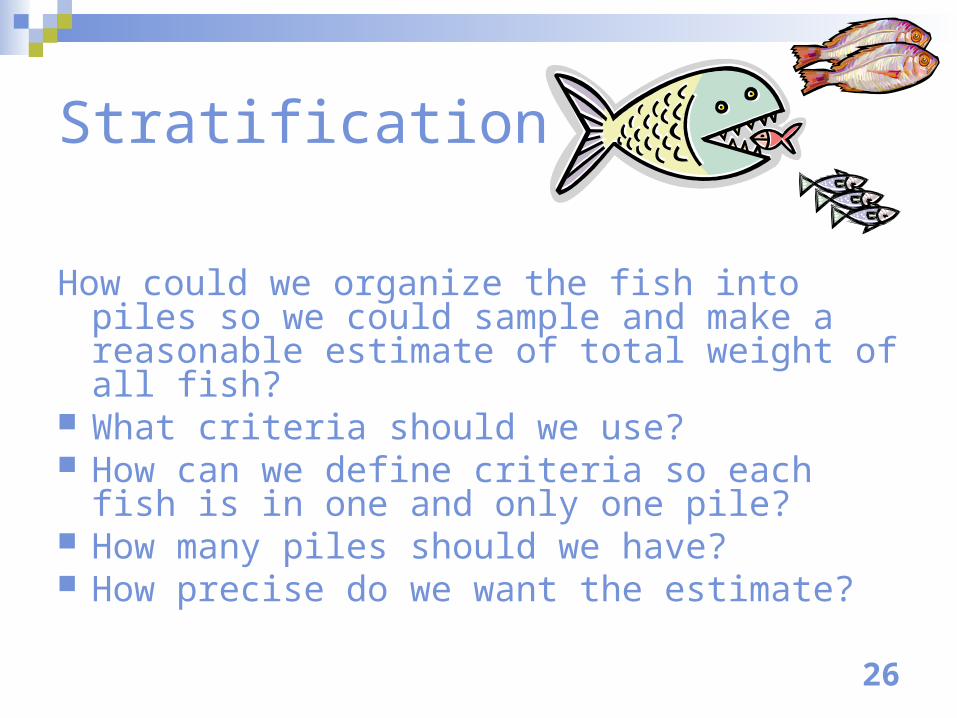

Stratification

How could we organize the fish into piles so we could sample and make a reasonable estimate of total weight of all fish?

What criteria should we use? How can we define criteria so each fish is in one

and only one pile? How many piles should we have? How precise do we want the estimate?

27

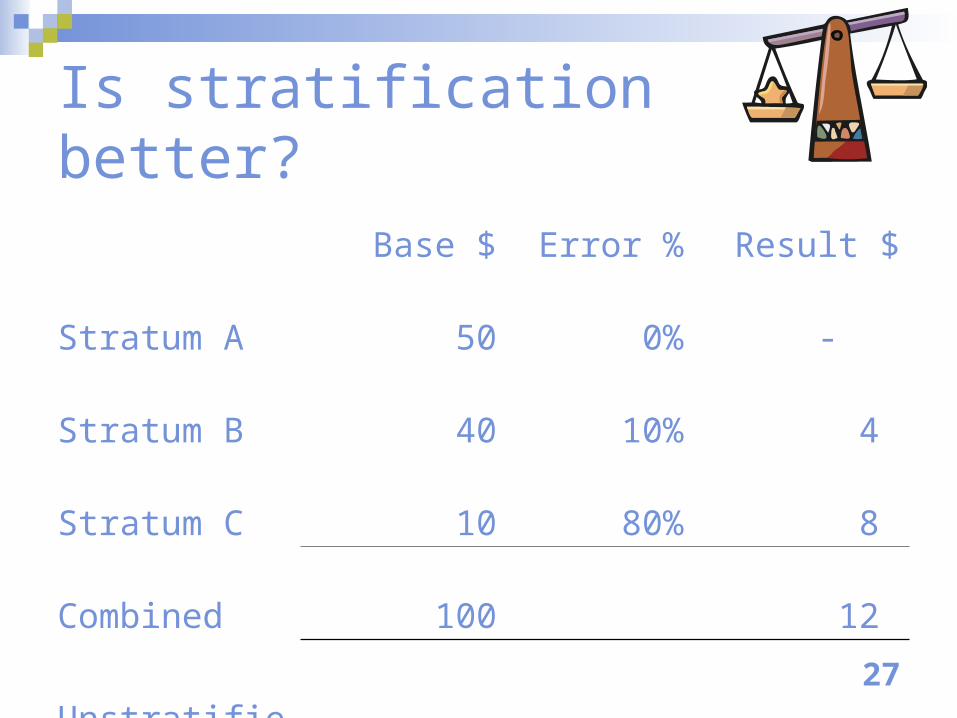

Is stratification better?

Base $ Error % Result $

Stratum A 50 0% -

Stratum B 40 10% 4

Stratum C 10 80% 8

Combined 100 12

Unstratified 100 12% 12

28

Texas Sample Size

CAMS (Computer Audit Menu System)

Policy for stratified random samples

http://www.cpa.state.tx.us/taxinfo/audit/sampling/samplin3.htm Minimum 100 per stratum if taxed and nontaxed

are not in the same stratum

Minimum 125 per stratum if taxed and nontaxed are mixed within that stratum

29

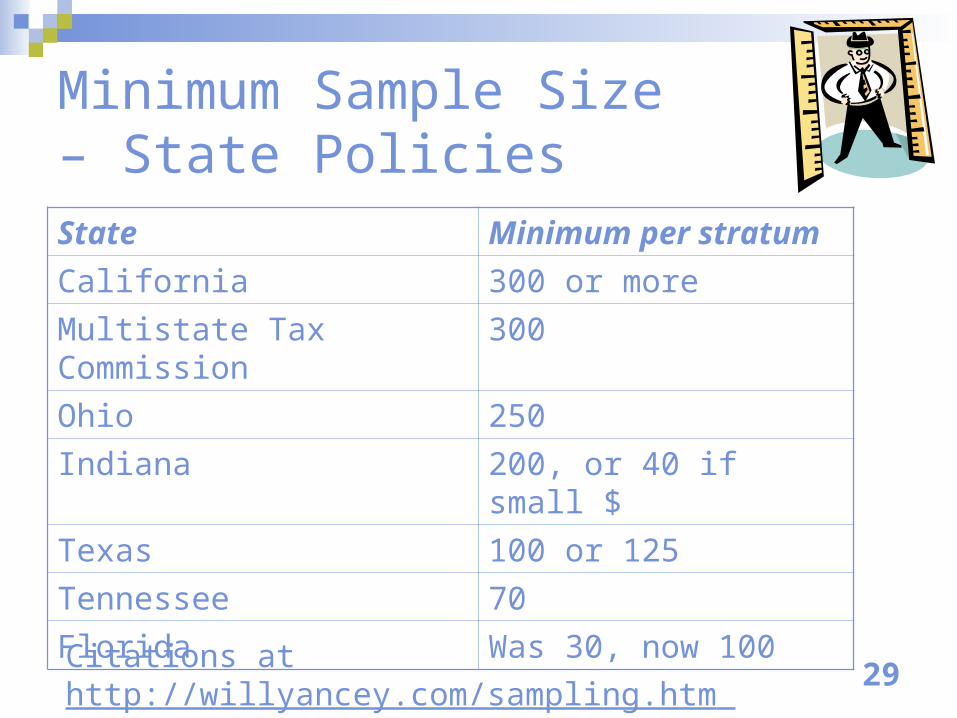

Minimum Sample Size – State PoliciesState Minimum per stratum

California 300 or more

Multistate Tax Commission 300

Ohio 250

Indiana 200, or 40 if small $

Texas 100 or 125

Tennessee 70

Florida Was 30, now 100

Citations at http://willyancey.com/sampling.htm

30

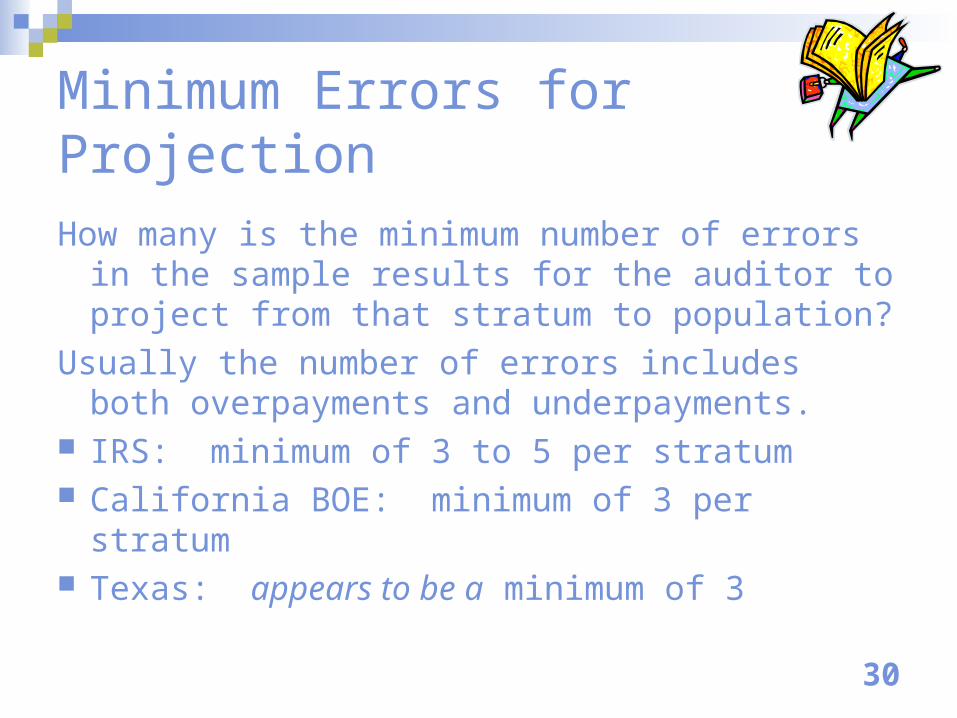

Minimum Errors for Projection

How many is the minimum number of errors in the sample results for the auditor to project from that stratum to population?

Usually the number of errors includes both overpayments and underpayments.

IRS: minimum of 3 to 5 per stratum California BOE: minimum of 3 per stratum Texas: appears to be a minimum of 3

31

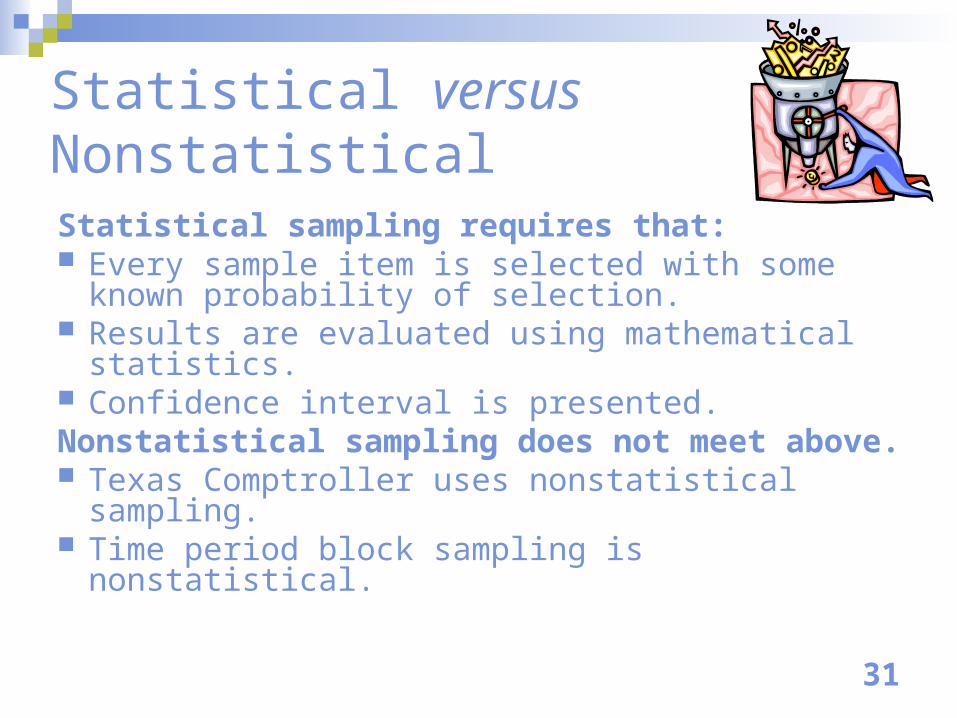

Statistical versus NonstatisticalStatistical sampling requires that: Every sample item is selected with some known

probability of selection. Results are evaluated using mathematical

statistics. Confidence interval is presented.Nonstatistical sampling does not meet above. Texas Comptroller uses nonstatistical sampling. Time period block sampling is nonstatistical.

32

References

Statistical Education and Software http://willyancey.com/statistics.htm

Sampling in Sales and Use Tax Audits http://willyancey.com/sampling.htm

Sampling SUT Audit Review Articles http://willyancey.com/sampling-sut-review.html

May the Force be with you!