Embed Size (px)

DESCRIPTION

ICQ with specific details and procedures that the auditor needs to consider in finding how the question can be answer

Citation preview

REVENUE CYCLE

Internal Control Questions IssuesProcessTransactionsVC No one person should have complete control over the cash handling process

In Ithaca College proper segregation of duties is exercised to safeguard assets

Degree Of Risk

1) Does adequate segregation of duties exist within your department between staff members responsible for receiving depositing and reconciling cash and checks

1 All persons accepting cash (ie currency checks money orders) must be authorized to do so by the Cashiering Services Office

2 Departmental receipt logs must be maintained for the purpose of documenting a permanent record of incoming cash checks or money orders The departmental supervisor is responsible for reviewing the cash log on a regular basis and ensuring all cash receipts have been deposited to the proper account

VC

4 All deposits should be personally handed to the cashier

1) Does adequate segregation of duties exist within your department between staff members responsible for receiving depositing and reconciling cash and checks

3 At the end of each business day a physical count of all cash and checks received must be completed and those amounts must be reconciled to the receipt log The receipt log must be signed and dated by a departmental designee other than the individual who performed the physical count and reconciliation to the receipt log

The management must ensure that the cash‐handling and record‐keeping functions be kept separate For smaller departments where separation of duties is impossible or impractical the supervisory personnel who do not handle cash should perform specific verification for reasonable and sound internal controls

MC

the Buyers

2) What is the minimum information required to review the creditworthiness of

An entity needs to do a background check on its buyers to know whether or not they have the capacity to meet payments on time Entities need to set up standards on the kind and amount of transactions that potential clients with different financial capacities can enter into

In universities however a different kind of background check is conducted Donors and rich parents aside admissions to large universities are largely based on academic performance and potential

In Yale University for example an applicantrsquos academic strength is the first consideration The school review grades standardized test scores and evaluations by a counselor and two teachers to determine academic strength The admissions committee then factors in student qualities such as motivation curiosity energy leadership ability and distinctive talents

MC In universities threats in this area include

(2) tuition bills may have occurred but may

not have been billed andor recorded and

(3) Intentional errors or misappropriation of information could occur

VC

3) Are billings reviewed and approved prior to billing andor recording

(1) tuition bills incorrectly prepared andor billings and other terms may be misstated

In University of Arizona accountability for tuition bills are the responsibility of the RegistrarStudentBusiness Services (SBS) and may not be delegated to any other functional area

Where invoices are computer generated SBS should ensure adequate controls exist over invoice preparation

4) Do changes to the prescribed billing amount require the approval of an authorized individual

All credit transactions should be included in the accounting records and should be approved by the proper individuals

VC

vC

4) Do changes to the prescribed billing amount require the approval of an authorized individual

In University of Arizona all credit memos issued to students should be supported by documentation and approved by Financial Services prior to issuance

Also credit memo transactions should be numerically controlled and accounted for periodically Credit memos should be pre-numbered where the integrity of sequencing is not computer controlled

5) If cash is accepted are pre-numbered receipts used to track payment

Unless documented there is no way to trace the movement of money A proper internal control entails the documentation of every sale of goods or services with a cash register entry a pre-numbered receipt form an invoice etc Customers are issued a duplicate

In institutions like Ithaca College whenever cashcheck is received in person an acceptable form of receipt must be used

vC

2 Dated cash log

4 Cash register tapes

5 Other documentation

Date received Name of the payee Amount received What the payment was for

Unique receipt number

5) If cash is accepted are pre-numbered receipts used to track payment

1 Uniquely and consecutively pre‐numbered receipts with a duplicate copy maintained as a cash receipts log

3 Pre‐numbered tickets

In the University of Glasgow a receipt must be issued for all cash received and a copy retained The receipt should be processed through the Cash Register or issued manually and shall show

Type of payment received ie cash cheque postal order credit card debit card

VC6) Do tellers have their own vault cubicle or controlled cash drawer in which to store their cash supply

As much as possible each cashier should start hisher shift with a new beginning cash balance and hisher own cash drawer If a register must be shared it must have

sufficient controls to allow collections to be attributed to individual cashiers (egseparate user IDs and passwords to access the register)

In University of Wellington the following guidelines in the storage of cash is implemented

(a) During business hours all cash should be securely stored in a locked cash register cash drawer or similar with access restricted to authorised cash handling staff

(b) For staff security during business hours the amount of cash securely stored in a locked cash register cash drawer or similar should be monitored Where necessary cash should be transferred into a safe or similar for secure storage

VC

VC

6) Do tellers have their own vault cubicle or controlled cash drawer in which to store their cash supply

(c) Outside of business hours all cash should be securely stored in a safe or similar away from where cash is typically handled Cash should not be stored in an obvious place such as in a locked cash tin on the cashier counter

7) Is each tellerrsquos cash checked daily to an independent control from the proof or accounting control department

Reconciliations should be completed by a specified individual who does not collect funds If this is not feasible within a department someone outside of the collections process should review the reconciliation

Daily reconciliations should be performed by a specified individual comparing the following

middot the cash receipt records (eg cash register balancing records prenumbered receipts and bank deposit slip if applicable)

middot the completed Collections Report

Monthly reconciliation should be performed by a specified individual comparing deposit information to the Organization Detail Activity Report from Banner

VC

The daily balance must contain information on the following

(i) the total physical cash received

(ii) the total physical cash distributed

(iii) a breakdown of the modes of cash received

(iv) a breakdown of the modes of cash distributed

7) Is each tellerrsquos cash checked daily to an independent control from the proof or accounting control department

In University of Wellington a ldquodaily cash balancerdquo is created The cash collection point should create a formal record of cash handling transactions at the close of each business day

(v) a reconciliation of physical cash received and distributed against the receipting system regardless of whether that system is manual or automated

(vi) a breakdown of any difference between the physical cash balance against the cashier system cash balance (referred to as a ldquocash surplusrdquo or ldquocash shortagerdquo) and

an explanation of any difference between the physical cash balance against the system cash balance

VC

VC

In University of Houston the following guidelines are followed

7) Is each tellerrsquos cash checked daily to an independent control from the proof or accounting control department

The supervisor of the cashier department together with someone from the accounting department counts the cash and reconciles it with the daily cash balance at the end of the day

8) Is an individual cumulative over and short record maintained for all persons handling cash and does management review the record

It is important that a record for overage and shortages be kept for cashiers to identify differences in records and actual cash count This would also identify patterns that will determine fraud perpetrators in the cash receiving department

A Overages and Shortages of less than $20 on cash receipts are recorded to the departmental cost center on the deposit journal using account 50015

B Departments must maintain a log of all overagesshortages which is recorded on OverageShortage Report Form

VC

MC

Cash Deposits Control

8) Is an individual cumulative over and short record maintained for all persons handling cash and does management review the record

C Individual overagesshortages of $20 or more or annual cumulative overagesshortages of $40 or more must be immediately reported to General Accounting and the Treasurerrsquos Office Departments with large cash handling operations may be permitted larger overageshortage allowances with permission from the Treasurer The Treasurer will provide the names of these unitsdepartments to Internal Auditing

9) Are checks photocopied or is a cash receipt log maintained to create supporting documentation to which you can reconcile deposits

To ensure proper documentation and transfer of accountability records of transfer of assets is a must

Ithaca College has the following rules regarding the deposit of cash by the cashier to the Cashiering Services Office

1 All deposits should be accompanied by a deposit slip These forms can be found on the Cashiering Services website and are also available at the Cashiering Services Office

MC

2 Deposits are to be made at the Cashiering Services Office window

1 All deposits should be personally handed to the cashier

3 Deposits should always be in a sealed envelope or locked bag

6 Do not group more than 100 checks together in a single deposit

Cash Reconciliation Control

9) Are checks photocopied or is a cash receipt log maintained to create supporting documentation to which you can reconcile deposits

2 Do not leave a deposit at an un‐attended window or on the counter if the cashier is busy with another customer

3 All cash deposits must be processed and a receipt generated while the depositor is present

4 A calculator tape listing the cash total for each denomination and each check along with a grand total for each must accompany deposits

5 Each check must include the Parnassus account number to be deposited into

MC

VC

9) Are checks photocopied or is a cash receipt log maintained to create supporting documentation to which you can reconcile deposits

1 Upon completion of a deposit made at the Cashiering Services Office a receipt would have been given to the depositor

2 It is the responsibility of each department to reconcile all deposit receipts against their own departmental receipt log and Parnassus account(s)

3 This reconciliation process should be done no less than once a month and approved by the departmental supervisor

When proper internal controls are existing and effective regarding the deposit or transfer of money from the cashier to the bank or to another department proper trail of the asset will be created Thus creating a small if not non-existent window for theft or fraud

10) Are deposits of funds made on the next business day

Deposits are to be made in a timely manner to insure proper posting of accounts and to insure the safety of funds

VC

A chart is provided to guide department on the deposit of their income

CUMULATIVE RECEIPTS

UP TO $49999

$50000 TO $499999

10) Are deposits of funds made on the next business day

In Northwestern University all bank deposits are to be made at the Bursars Office on the Evanston or Chicago campuses unless alternate arrangements have been made in conjunction with the Bursar Office for armored car service Deposits may be made at the Chicago Bursars Office Monday - Friday between 9 am and 4 pm and at the Evanston Bursars Office Monday - Friday between 830 am and 4 pm

Deposits must be routed directly from the department to the University Bursar University funds for deposit must never be taken off campus

VC

$500000 TO $4999999

$5000000 OR MORE

CONVERSION CYCLE

Internal Control Questions IssuesProcessTransactionsVC

10) Are deposits of funds made on the next business day

ANY SINGLE ITEM $25000000 OR MORE

Degree Of Risk

1 Are production scheduled prepared by the production planning team

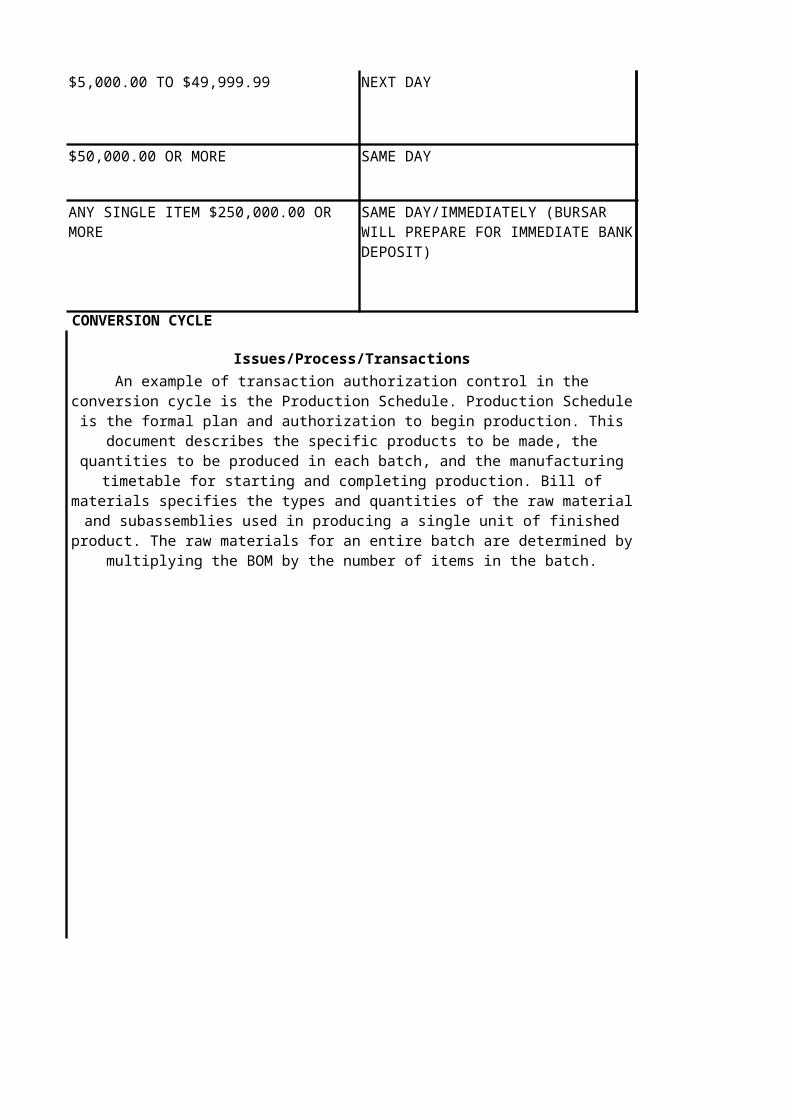

An example of transaction authorization control in the conversion cycle is the Production Schedule Production Schedule is the formal plan and authorization to begin production This document describes the specific products to be made the quantities to be produced in each batch and the manufacturing timetable for

starting and completing production Bill of materials specifies the types and quantities of the raw material and subassemblies used in producing a single unit

of finished product The raw materials for an entire batch are determined by multiplying the BOM by the number of items in the batch

2 Are bill of materials (BOM) prepared by the production planning team

MC

VC

3 Are route sheet prepared Route sheet shows the production path that a particular batch of product follows during manufacturing It is similar conceptually to a BOM Whereas the BOM

specifies material requirements the route sheet specifies the sequence of operations (machining or assembly) and the standard time allocated to each task

4 Are work orders or production order drawn from BOMs and route sheets

In the traditional manufacturing environment production planning and control authorize the production activity via a formal work order This document

reflects production requirements

The work order or production order draws from BOMs and Route sheet to specify the material and production (machining assembly and so on) for each batch These together with move tickets initiate the manufacturing process in

the production departments

VC

VC

5 Does the company use move tickets Another example of Transaction Authorization control is Move Tickets Move tickets record work done in each work center Move tickets signed by the

supervisor in each authorize activities for each batch and for the movement of products through the various work centers

6 Does the company use material requisition

Material requisition authorizes the storekeeper to release materials (and subassemblies) to individuals or work centers in the production process This

document usually specifies only standard quantities Materials needed in excess of standards amounts require separate requisitions that may be identified

explicitly as excess materials requisition This allows for closer control over the production process by highlighting excess materials usage In some cases Less than the standard amount of material is used in production When this happens the work centers return the unused materials to the storeroom accompanied by a

materials return ticket

VC

VC

VC

7 Are materials as well as the machining and the labor required to manufacture the product applied in compliance with the work order

Materials as well as the machining and the labor required to manufacture the product are applied in compliance with the work order When the task is

complete at a particular work center the supervisor or other authorized person signs the move ticket which authorizes the batch to proceed to the next work

center

8 Is there a way to confirm stage of production has been completed

To evidence that a stage of production has been completed a copy of the move ticket is sent back to production planning and control to update the open work

order file Upon receipt of the last move ticket the open work order file is closed The finished product along with a copy if the work order is sent to the finished goods warehouse Also a work order is sent to inventory control to

update the FG inventory records

9 Do work center supervisors records and sends labor time cost information

Work centers also fulfill in an important role in recording labor time costs This task is handled by work center supervisors who at the end of each workweek send employee time cards and job tickets to the payroll and cost accounting

departments respectively

VC

VC

10 Are inventory controls present Inventory control function consists of three main activities First it provides production planning and control with status reports on finished goods and raw

materials inventory Second the inventory control function is continually involved in updating the raw material inventory records form the materials

requisitions and materials return tickets Finally upon receipt of the work order form the last work center inventory control records the completed production by

updating the finished goods inventory records

11 Are raw materials updated by matching materials requisitions and material return tickets

12 Are finished goods updated using information from work order from the last work center

13 Is there an inventory model used An objective of inventory control is to minimize total inventory cost while ensuring that adequate inventories exist to meet current demand Inventory

models used to achieve this objective help answer two fundamental question

1 When should inventory be purchase

2 How much inventory should be purchased

VC14 Are materials requisitions excess materials requisitions and materials return matched in the cost accounting department

The cost accounting process for a given production run begins when the production planning and control department sends a copy of the original work

order to the cost accounting department This marks the beginning of the production event by causing a new record to be added to the WIP file which is

the subsidiary ledger for the WIP control account in the general ledger

15 Are job tickets and completed move tickets sent to cost accounting department

As material and labor are added throughout the production process documents reflecting these events flow to the cost accounting department Inventory control

sends copies of materials requisitions excess materials requisitions and materials returns The various work centers send job tickers and completed

move tickets These documents along with standards provided by the standards cost file enable cost accounting to update the affected WIP accounts with the

standard charges for direct labor material and manufacturing overhead (MOH) Deviations from standard usage are recorded to produce material usage direct

labor and manufacturing overhead variances Calculated variances are an important source of data for the management reporting system

VC

VC

VC The following separations apply

16 Are deviations from standard usage accounted

The receipt of the last move ticket for a particular batch signals the completion of the production process and the transfer of products from WIP to the FG

inventory At this point cost accounting closes the WIP account Periodically summary information regarding charges (debits) to WIP reductions (credits) to

WIP and variances are recorded on journal vouchers and sent to the GL department for posting to the control account

17 Is WIP account closed when goods are finished

18 Is segregation of transaction authorization and transaction processing observed

The production planning and control department is organizationally segregated from the work centers because there should be separation in transaction

authorization and transaction processing

19 Is there separation in record keeping from asset custody

1 Inventory control maintains accounting records for RM and FG inventories This activity is kept separate from the materials storeroom and from the FG

warehouse functions which have custody of these assets

VC

VC The following supervision procedures apply to conversion cycle

VC

19 Is there separation in record keeping from asset custody

2 Similarly cost accounting functions should be separate from the work centers in the production process

20 Is there a supervisor assigned to oversee activities

1 The supervisors in the work centers oversee the usage of RM in the production process This helps to ensure that all materials released form stores are used in production and that waste is minimized Employee time cards and

job tickets must also be checked for accuracy

2 Supervisors also observe and review timekeeping activities This promotes accurate employee time cards and job tickets

21 Are access controls to physical product and production process implemented

1 Firms often limit access to sensitive areas such as storerooms production work centers and FG warehouses Control methods used include identification badges security guards observation devices and various electronic sensors and

alarms

VC

PURCHASESInternal Control Question Issues Process Transactions

VC Segregation of Duties

21 Are access controls to physical product and production process implemented

2 The use of standard costs provides a type of access control By specifying the quantities of material and labor authorized for each product the firm limits

unauthorized access to those resources To obtain excess quantities requires special authorization and formal documentation

Degree of Risk

1 Is the purchasing function separate from accounting receiving and payment processing No one employee should have complete control over the entire purchasing

function The responsibilities for requisitioning goods and services purchasing receiving goods and approving payments for goods and services preparing payment vouchers approving payment vouchers should be assigned among different employees This is primarily to prevent or make it less easy for employees to collude for fraudulent

purposes Assigning one employee with the combined responsibilities of preparing and approving purchase requisitions receiving the goods

recording the transaction etc could be an opportunity to perpetrate fraud against the company For instance he could make personal purchases and

record them as the companyrsquos purchases thus the company will have to pay for purchases not really incurred in relation to the business

VC

a Less than $5000 - no bid required

2 Does the organization obtain competitive bids for items to be purchased over specified amounts

Purchases should be made by a competitive process even when not expressly required to ensure a prudent and efficient use of funds This entails a process of selecting valid vendors offering cost-effective and

quality items in the most reasonable price for the company to minimize cost

The company can establish purchase policies setting thresholds on when will the need for bids arise For example

3 Are there procedures to obtain the best possible price for items not subject to competitive bidding requirements such as approved vendor lists and supply item catalogs

b $5000 to $25000- buyer discretion and must be from small business unless impractical

VC

c $25000 to $50000 - informal bids required

d Greater than $50000 - request for proposal formal bids

For purchases not subject to competitive bidding requirements the company should assess the adequacy of their pricing by cross-referencing to a lsquoprice bookrsquo ndash a document that contains policies on the point or price at which the products can be negotiated and will help determine whether

the prices are appropriate by referring to the threshold on at what level can the prices be inflated The company can also refer the current industry

market prices in comparing the vendorrsquos prices

VC

c Pre-numbered and controlled

4 Is the inventory level continually monitored to assess when purchases are needed

The inventory control function should continually monitor inventory levels When the inventory levels drop to the predetermined reorder points inventory control formally prepares a purchase requisition for replenishment This document will have to be authorized by the inventory control manager Formal authorization process promotes efficient inventory management and ensures the legitimacy of purchases transactions Without this step purchasing agents could purchase inventories at their own discretion if they both have the task of authorizing and processing the transactions Unauthorized purchasing can also result to over or under stocking of inventory which will be potentially damaging to the company as excessive inventory will increase storage or handling costs while stock-outs will lead to lost sales and manufacturing delays

5 Are purchase requisitions

a Required for all purchases of goods and services

b Approved by officials designated to authorize requisitions

VC

a Pre-numbered and controlled

6 Are purchase orders Purchase orders (PO) are prepared based on valid approved purchase requisitions and are properly executed as to price quantity and vendor

The potential risks of not preparing POs as to the appropriate price quantity and vendor are as follows

middot Payment in excess of optimum price

b Required for all non-exempt purchases (exempt small items purchased from petty cash)

middot Quantities not adequate or in excess of need

c Prepared only on the basis of purchase requisitions approved by authorized persons

middot Quality of materials or services received or substandard

VC

d Compared to unencumbered balances to avoid budget over expenditure

All purchases should be for necessary goods and services to support the departmentrsquos mission and programs and in accordance with established

budgetary guidelines In cases where purchases are exceeding the standard quantity and amount additional approval with sufficient explanation as to the excess arise are necessary to justify that the purchases are still in line

to support the companyrsquos operations and programs

e Approved by an authorized individual

A purchase order is prepared by vendor and a copy is sent to each vendor In addition a copy is sent to the accounts payable function for temporary

filing in the AP pending file and a blind copy is sent to the receiving goods function The last copy is for filing in the purchase order file

VC

VC

7 Is the purchasing agent required to obtain additional approval on purchase orders above a stated amount

8 Does the purchasing agent prepare sufficient copies of PO to be used and distributed to the respective departments

9 Are received goods inspected and verified as to purchase order terms

Verify goods and services received agree with contractpurchase order terms

10 Does the receiving clerk use a blind copy upon receipt of goods

1048729 Received goods are secured in a safe location and inspected for quality and condition

VC

11 Does the receiving clerk prepare sufficient copies of receiving report

Goods arriving from the vendor are reconciled with the blind copy of the PO The blind copy contains no quantity or price information about the products being received The purpose of the blind copy is to force the

receiving clerk to count and inspect the inventories prior to completing the receiving report

Upon completion of the physical count and inspection the receiving clerk prepares a receiving report stating the quantity and condition of the

inventories in which one copy accompanies the physical inventories to the warehouse and another copy is filed in the PO file The other copies are

sent to the AP and inventory control functions The final copy is placed in the receiving report file

MC12 Does the company set up liability upon receipt of vendor invoices

The company will have to defer recording of liability until the vendorrsquos invoice arrives

13 Are invoices reviewed or reconciled with other source documents before liability is set up

When invoices arrives invoices are matched with purchase orders and receiving reports before approval for payment The AP clerk performs a

three-way match by reconciling the financial information with the receiving report and PO in the pending file This will also be a means to review invoices for accuracy by comparing charges (eg quantity price etc) to amounts indicated in purchase orders contracts or other source

documents

MC14 Is there a policy statement with regard to conflicts of interest including employee-vendor relationships

Employees involved in the purchasing function should not use their position to receive any type of personal benefit from any vendor or

contractor and any potential conflict of interest should be disclosed to an appropriate supervisor or manager

For example vendors might bribe or give gifts to the purchasing clerk to win the bids or to misstate the prices Another conflict of interest might be

when the vendor is a relative eg sister of the purchasing clerk If no policy prohibiting the transaction the clerk might be biased in choosing

the vendor even if the quality and other requirements by the company for the purchase are not met

REVENUE CYCLE

IssuesProcessTransactionsNo one person should have complete control over the cash handling process

In Ithaca College proper segregation of duties is exercised to safeguard assets

1 All persons accepting cash (ie currency checks money orders) must be authorized to do so by the Cashiering Services Office

2 Departmental receipt logs must be maintained for the purpose of documenting a permanent record of incoming cash checks or money orders The departmental supervisor is responsible for reviewing the cash log on a regular basis and ensuring all cash receipts have been deposited to the

4 All deposits should be personally handed to the cashier

3 At the end of each business day a physical count of all cash and checks received must be completed and those amounts must be reconciled to the receipt

receipt log must be signed and dated by a departmental designee other than the individual who performed the physical count and

to the receipt log

The management must ensure that the cash‐handling and record‐keeping functions be kept separate For smaller departments where separation of duties is impossible or impractical the supervisory personnel who do not handle cash should perform specific verification for reasonable and sound internal controls

An entity needs to do a background check on its buyers to know whether or not they have the capacity to meet payments on time Entities need to set up standards on the kind and amount of transactions that potential clients with different financial capacities can enter into

In universities however a different kind of background check is conducted Donors and rich parents aside admissions to large universities are largely based on academic performance and potential

In Yale University for example an applicantrsquos academic strength is the first consideration The school review grades standardized test scores and evaluations by a counselor and two teachers to determine academic strength The admissions committee then factors in student qualities such as motivation curiosity energy leadership ability and distinctive talents

In universities threats in this area include

(2) tuition bills may have occurred but may

not have been billed andor recorded and

(3) Intentional errors or misappropriation of information could occur

(1) tuition bills incorrectly prepared andor billings and other terms may be

accountability for tuition bills are the responsibility of the RegistrarStudentBusiness Services (SBS) and may not be delegated

Where invoices are computer generated SBS should ensure adequate controls exist over invoice preparation

All credit transactions should be included in the accounting records and should be approved by the proper individuals

In University of Arizona all credit memos issued to students should be supported by documentation and approved by Financial Services prior to

Also credit memo transactions should be numerically controlled and accounted for periodically Credit memos should be pre-numbered where the integrity of sequencing is not computer controlled

Unless documented there is no way to trace the movement of money A proper internal control entails the documentation of every sale of goods or services with a cash register entry a pre-numbered receipt form an invoice etc Customers

In institutions like Ithaca College whenever cashcheck is received in person an acceptable form of receipt must be used

2 Dated cash log

4 Cash register tapes

5 Other documentation

Date received Name of the payee Amount received What the payment was for

Unique receipt number

1 Uniquely and consecutively pre‐numbered receipts with a duplicate copy maintained as a cash receipts log

In the University of Glasgow a receipt must be issued for all cash received and a copy retained The receipt should be processed through the Cash Register or issued manually and shall show

Type of payment received ie cash cheque postal order credit card debit

As much as possible each cashier should start hisher shift with a new beginning cash balance and hisher own cash drawer If a register must be shared it must

sufficient controls to allow collections to be attributed to individual cashiers (egseparate user IDs and passwords to access the register)

In University of Wellington the following guidelines in the storage of cash is

(a) During business hours all cash should be securely stored in a locked cash register cash drawer or similar with access restricted to authorised cash

(b) For staff security during business hours the amount of cash securely stored in a locked cash register cash drawer or similar should be monitored Where necessary cash should be transferred into a safe or similar for secure

(c) Outside of business hours all cash should be securely stored in a safe or similar away from where cash is typically handled Cash should not be stored

such as in a locked cash tin on the cashier counter

Reconciliations should be completed by a specified individual who does not collect funds If this is not feasible within a department someone outside of the collections process should review the reconciliation

Daily reconciliations should be performed by a specified individual comparing

the cash receipt records (eg cash register balancing records prenumbered receipts and bank deposit slip if applicable)

the completed Collections Report

Monthly reconciliation should be performed by a specified individual comparing deposit information to the Organization Detail Activity Report from

The daily balance must contain information on the following

(i) the total physical cash received

(ii) the total physical cash distributed

(iii) a breakdown of the modes of cash received

(iv) a breakdown of the modes of cash distributed

In University of Wellington a ldquodaily cash balancerdquo is created The cash collection point should create a formal record of cash handling transactions at the close of each business day

(v) a reconciliation of physical cash received and distributed against the receipting system regardless of whether that system is manual or automated

(vi) a breakdown of any difference between the physical cash balance against the cashier system cash balance (referred to as a ldquocash surplusrdquo or ldquocash

an explanation of any difference between the physical cash balance against the

In University of Houston the following guidelines are followed

supervisor of the cashier department together with someone from the accounting department counts the cash and reconciles it with the daily cash

at the end of the day

It is important that a record for overage and shortages be kept for cashiers to identify differences in records and actual cash count This would also identify patterns that will determine fraud perpetrators in the cash receiving department

A Overages and Shortages of less than $20 on cash receipts are recorded to the departmental cost center on the deposit journal using account 50015

B Departments must maintain a log of all overagesshortages which is recorded on OverageShortage Report Form

Cash Deposits Control

C Individual overagesshortages of $20 or more or annual cumulative overagesshortages of $40 or more must be immediately reported to General Accounting and the Treasurerrsquos Office Departments with large cash handling operations may be permitted larger overageshortage allowances with permission from the Treasurer The Treasurer will provide the names of these unitsdepartments to Internal Auditing

To ensure proper documentation and transfer of accountability records of

Ithaca College has the following rules regarding the deposit of cash by the cashier to the Cashiering Services Office

1 All deposits should be accompanied by a deposit slip These forms can be found on the Cashiering Services website and are also available at the Cashiering Services Office

2 Deposits are to be made at the Cashiering Services Office window

1 All deposits should be personally handed to the cashier

3 Deposits should always be in a sealed envelope or locked bag

6 Do not group more than 100 checks together in a single deposit

Cash Reconciliation Control

2 Do not leave a deposit at an un‐attended window or on the counter if the cashier is busy with another customer

3 All cash deposits must be processed and a receipt generated while the

4 A calculator tape listing the cash total for each denomination and each check along with a grand total for each must accompany deposits

5 Each check must include the Parnassus account number to be deposited

1 Upon completion of a deposit made at the Cashiering Services Office a receipt would have been given to the depositor

2 It is the responsibility of each department to reconcile all deposit receipts against their own departmental receipt log and Parnassus account(s)

3 This reconciliation process should be done no less than once a month and approved by the departmental supervisor

When proper internal controls are existing and effective regarding the deposit or transfer of money from the cashier to the bank or to another department proper trail of the asset will be created Thus creating a small if not non-existent

Deposits are to be made in a timely manner to insure proper posting of accounts and to insure the safety of funds

A chart is provided to guide department on the deposit of their income

FREQUENCY OF DEPOSIT

WITHIN 5 BUSINESS DAYS

WITHIN 2 BUSINESS DAYS

In Northwestern University all bank deposits are to be made at the Bursars Office on the Evanston or Chicago campuses unless alternate arrangements have been made in conjunction with the Bursar Office for armored car service Deposits may be made at the Chicago Bursars Office Monday - Friday between 9 am and 4 pm and at the Evanston Bursars Office Monday - Friday between

Deposits must be routed directly from the department to the University Bursar University funds for deposit must never be taken off campus

NEXT DAY

SAME DAY

CONVERSION CYCLE

IssuesProcessTransactions

SAME DAYIMMEDIATELY (BURSAR WILL PREPARE FOR IMMEDIATE BANK DEPOSIT)

An example of transaction authorization control in the conversion cycle is the Production Schedule Production Schedule is the formal plan and authorization to begin production This document describes the specific products to be made the quantities to be produced in each batch and the manufacturing timetable for

starting and completing production Bill of materials specifies the types and quantities of the raw material and subassemblies used in producing a single unit

of finished product The raw materials for an entire batch are determined by multiplying the BOM by the number of items in the batch

Route sheet shows the production path that a particular batch of product follows during manufacturing It is similar conceptually to a BOM Whereas the BOM

specifies material requirements the route sheet specifies the sequence of operations (machining or assembly) and the standard time allocated to each task

In the traditional manufacturing environment production planning and control authorize the production activity via a formal work order This document

reflects production requirements

The work order or production order draws from BOMs and Route sheet to specify the material and production (machining assembly and so on) for each batch These together with move tickets initiate the manufacturing process in

the production departments

Another example of Transaction Authorization control is Move Tickets Move tickets record work done in each work center Move tickets signed by the

supervisor in each authorize activities for each batch and for the movement of products through the various work centers

Material requisition authorizes the storekeeper to release materials (and subassemblies) to individuals or work centers in the production process This

document usually specifies only standard quantities Materials needed in excess of standards amounts require separate requisitions that may be identified

explicitly as excess materials requisition This allows for closer control over the production process by highlighting excess materials usage In some cases Less than the standard amount of material is used in production When this happens the work centers return the unused materials to the storeroom accompanied by a

materials return ticket

Materials as well as the machining and the labor required to manufacture the product are applied in compliance with the work order When the task is

complete at a particular work center the supervisor or other authorized person signs the move ticket which authorizes the batch to proceed to the next work

center

To evidence that a stage of production has been completed a copy of the move ticket is sent back to production planning and control to update the open work

order file Upon receipt of the last move ticket the open work order file is closed The finished product along with a copy if the work order is sent to the finished goods warehouse Also a work order is sent to inventory control to

update the FG inventory records

Work centers also fulfill in an important role in recording labor time costs This task is handled by work center supervisors who at the end of each workweek send employee time cards and job tickets to the payroll and cost accounting

departments respectively

Inventory control function consists of three main activities First it provides production planning and control with status reports on finished goods and raw

materials inventory Second the inventory control function is continually involved in updating the raw material inventory records form the materials

requisitions and materials return tickets Finally upon receipt of the work order form the last work center inventory control records the completed production by

updating the finished goods inventory records

An objective of inventory control is to minimize total inventory cost while ensuring that adequate inventories exist to meet current demand Inventory

models used to achieve this objective help answer two fundamental question

When should inventory be purchase

How much inventory should be purchased

The cost accounting process for a given production run begins when the production planning and control department sends a copy of the original work

order to the cost accounting department This marks the beginning of the production event by causing a new record to be added to the WIP file which is

the subsidiary ledger for the WIP control account in the general ledger

As material and labor are added throughout the production process documents reflecting these events flow to the cost accounting department Inventory control

sends copies of materials requisitions excess materials requisitions and materials returns The various work centers send job tickers and completed

move tickets These documents along with standards provided by the standards cost file enable cost accounting to update the affected WIP accounts with the

standard charges for direct labor material and manufacturing overhead (MOH) Deviations from standard usage are recorded to produce material usage direct

labor and manufacturing overhead variances Calculated variances are an important source of data for the management reporting system

The following separations apply

The receipt of the last move ticket for a particular batch signals the completion of the production process and the transfer of products from WIP to the FG

inventory At this point cost accounting closes the WIP account Periodically summary information regarding charges (debits) to WIP reductions (credits) to

WIP and variances are recorded on journal vouchers and sent to the GL department for posting to the control account

The production planning and control department is organizationally segregated from the work centers because there should be separation in transaction

authorization and transaction processing

Inventory control maintains accounting records for RM and FG inventories This activity is kept separate from the materials storeroom and from the FG

warehouse functions which have custody of these assets

The following supervision procedures apply to conversion cycle

Similarly cost accounting functions should be separate from the work centers in the production process

The supervisors in the work centers oversee the usage of RM in the production process This helps to ensure that all materials released form stores are used in production and that waste is minimized Employee time cards and

job tickets must also be checked for accuracy

Supervisors also observe and review timekeeping activities This promotes accurate employee time cards and job tickets

Firms often limit access to sensitive areas such as storerooms production work centers and FG warehouses Control methods used include identification badges security guards observation devices and various electronic sensors and

alarms

PURCHASESIssues Process Transactions

Segregation of Duties

The use of standard costs provides a type of access control By specifying the quantities of material and labor authorized for each product the firm limits

unauthorized access to those resources To obtain excess quantities requires special authorization and formal documentation

No one employee should have complete control over the entire purchasing function The responsibilities for requisitioning goods and services purchasing receiving goods and approving payments for goods and services preparing payment vouchers approving payment vouchers should be assigned among different employees This is primarily to prevent or make it less easy for employees to collude for fraudulent

purposes Assigning one employee with the combined responsibilities of preparing and approving purchase requisitions receiving the goods

recording the transaction etc could be an opportunity to perpetrate fraud against the company For instance he could make personal purchases and

record them as the companyrsquos purchases thus the company will have to pay for purchases not really incurred in relation to the business

a Less than $5000 - no bid required

Purchases should be made by a competitive process even when not expressly required to ensure a prudent and efficient use of funds This entails a process of selecting valid vendors offering cost-effective and

quality items in the most reasonable price for the company to minimize cost

The company can establish purchase policies setting thresholds on when will the need for bids arise For example

b $5000 to $25000- buyer discretion and must be from small business unless impractical

c $25000 to $50000 - informal bids required

d Greater than $50000 - request for proposal formal bids

For purchases not subject to competitive bidding requirements the company should assess the adequacy of their pricing by cross-referencing to a lsquoprice bookrsquo ndash a document that contains policies on the point or price at which the products can be negotiated and will help determine whether

the prices are appropriate by referring to the threshold on at what level can the prices be inflated The company can also refer the current industry

market prices in comparing the vendorrsquos prices

Purchase orders (PO) are prepared based on valid approved purchase requisitions and are properly executed as to price quantity and vendor

The potential risks of not preparing POs as to the appropriate price quantity and vendor are as follows

Payment in excess of optimum price

Quantities not adequate or in excess of need

Quality of materials or services received or substandard

All purchases should be for necessary goods and services to support the departmentrsquos mission and programs and in accordance with established

budgetary guidelines In cases where purchases are exceeding the standard quantity and amount additional approval with sufficient explanation as to the excess arise are necessary to justify that the purchases are still in line

to support the companyrsquos operations and programs

A purchase order is prepared by vendor and a copy is sent to each vendor In addition a copy is sent to the accounts payable function for temporary

filing in the AP pending file and a blind copy is sent to the receiving goods function The last copy is for filing in the purchase order file

Verify goods and services received agree with contractpurchase order terms

Received goods are secured in a safe location and inspected for quality and condition

Goods arriving from the vendor are reconciled with the blind copy of the contains no quantity or price information about the

products being received The purpose of the blind copy is to force the receiving clerk to count and inspect the inventories prior to completing the

receiving report

Upon completion of the physical count and inspection the receiving clerk prepares a receiving report stating the quantity and condition of the

inventories in which one copy accompanies the physical inventories to the warehouse and another copy is filed in the PO file The other copies are

sent to the AP and inventory control functions The final copy is placed in the receiving report file

The company will have to defer recording of liability until the vendorrsquos invoice arrives

When invoices arrives invoices are matched with purchase orders and receiving reports before approval for payment The AP clerk performs a

three-way match by reconciling the financial information with the receiving report and PO in the pending file This will also be a means to review invoices for accuracy by comparing charges (eg quantity price etc) to amounts indicated in purchase orders contracts or other source

documents

Employees involved in the purchasing function should not use their position to receive any type of personal benefit from any vendor or

contractor and any potential conflict of interest should be disclosed to an appropriate supervisor or manager

For example vendors might bribe or give gifts to the purchasing clerk to win the bids or to misstate the prices Another conflict of interest might be

when the vendor is a relative eg sister of the purchasing clerk If no policy prohibiting the transaction the clerk might be biased in choosing

the vendor even if the quality and other requirements by the company for the purchase are not met

Internal Control Questions IssuesProcessTransactionsVC

Degree Of Risk

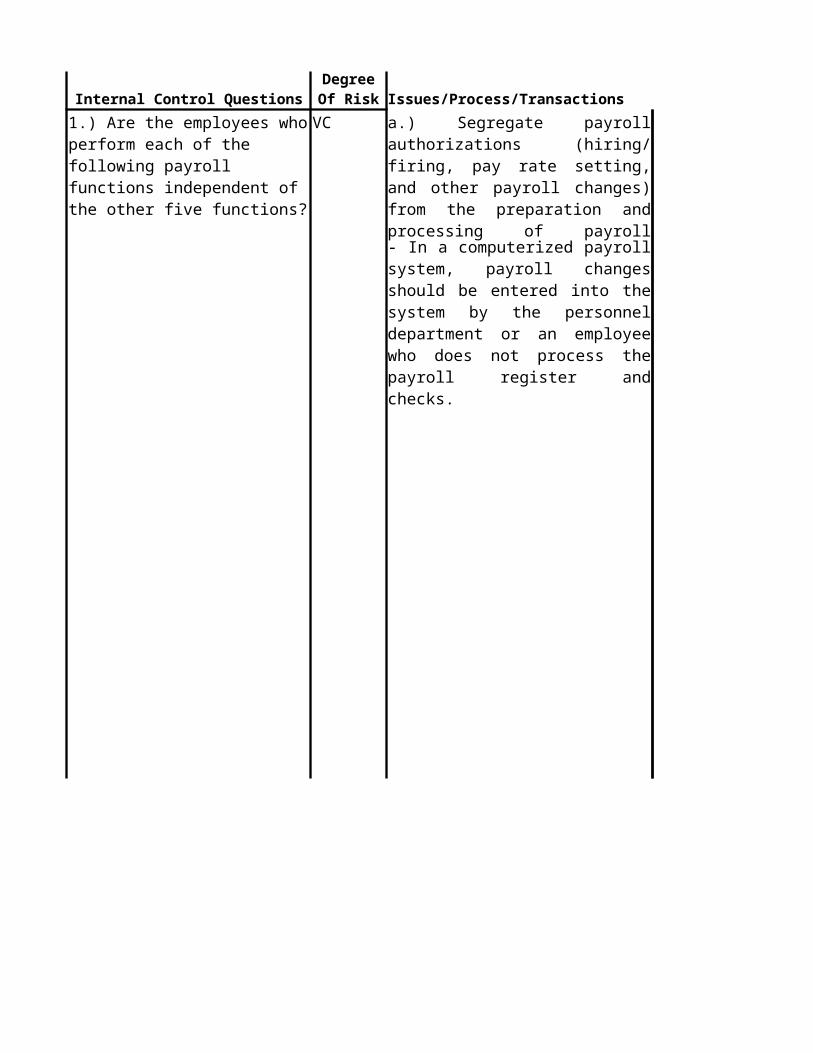

1) Are the employees who perform each of the following payroll functions independent of the other five functions

a) Segregate payroll authorizations (hiring firing pay rate setting and other payroll changes) from the preparation and processing of payroll records and checks

middot personnel and approval of payroll changes

- In a computerized payroll system payroll changes should be entered into the system by the personnel department or an employee who does not process the payroll register and checks

VC

middot preparation of payroll data

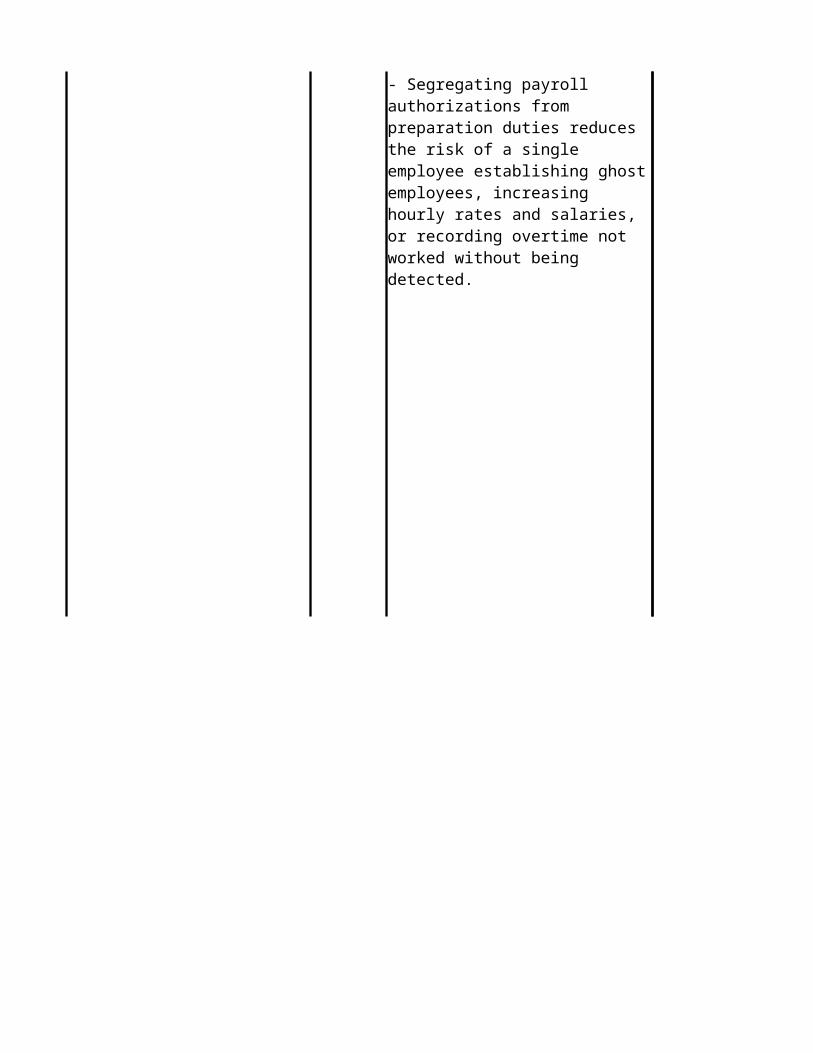

- Segregating payroll authorizations from preparation duties reduces the risk of a single employee establishing ghost employees increasing hourly rates and salaries or recording overtime not worked without being detected

VC

middot approval of payroll

Example Scenario In the City and County of San Francisco the Controllerrsquos Payroll and Personnel Services Division disburses salaries and wages for approximately City 27000 employees through biweekly paychecks and direct deposits To make this possible the following City organizations and department payrollpersonnel staff work together to execute payroll duties

VC

middot signing of paychecks

Payroll amp Personnel Services Division (PPSD) processes payroll data for employees of city departments and ensures compliance with city state and federal tax wage and hour regulations

VC

middot distribution of paychecks

Department Payroll Staff are responsible for administering the departmentrsquos payroll and ensuring that employeesrsquo time information is submitted accurately to PPSD

VC

middot reconciliation of payroll account

eMerge is a unit within the Controllerrsquos Office that manages and operates PeopleSoft an integrated system that provides human resources benefits administration and payroll services to the Citys active retired and future workforce

VC

Department of Human Resources (DHR) administers City-wide personnel policies and procedures negotiates and administers collective bargaining agreements with labor unions and advises the Cityrsquos other departments in these areas

VC

Civil Service Commission (CSC) oversees the merit system for the City by establishing rules and policy related to the merit system hearing appeals on examinations eligibility lists minimum qualifications classification discrimination complaints and future employment and interpreting rules and policies

VC

San Francisco Employeesrsquo Retirement System (SFERS) secures protects and invests pension trust assets administers the mandated benefits programs and provides promised benefits to active and retired members of the system And lastly

VC

Health Service System (HSS) creates contracts based on negotiations with health providers which offer eligible employees the opportunity to enroll themselves and eligible family members in medical dental vision and flexible spending account benefits

Threat if control is missing Fraud theft of paychecks

VC

VC

We will use the payroll procedures of City and County of San Francisco as the example scenario in each internal control questions

2) Are payroll changes (hires separations salary changes overtime bonuses promotions etc) properly authorized and approved

a) All changes in employment status (eg additions and terminations) salary and wage rates should be properly authorized approved and documented to support employment status changes

VC2) Are payroll changes (hires separations salary changes overtime bonuses promotions etc) properly authorized and approved

- When a formal process exists to document authorized changes to salaries and wages the opportunity for fraudulent or erroneous payroll changes to occur without detection decreases

VC2) Are payroll changes (hires separations salary changes overtime bonuses promotions etc) properly authorized and approved

b) When appropriate payroll change forms should be used to document and authorize wage and salary changes authorized by the governing board

Example Scenario The Controllerrsquos Payroll and Personnel Services Division had established a policy where

VC2) Are payroll changes (hires separations salary changes overtime bonuses promotions etc) properly authorized and approved

- Any changes to employee pay must be documented and approved by proper authorities

- Before any modifications to employee pay is entered into PeopleSoft department payrollpersonnel staff must have documentation that describes the specifics of the pay change (such as the pay change amount the effective date(s) classification(s) affected etc) and copies of approving documentation must be retained in filed for future auditing review

VC2) Are payroll changes (hires separations salary changes overtime bonuses promotions etc) properly authorized and approved

- And lastly any adjustment requests for pay rate changes must be submitted to PPSD with the following documentation Problem Description Form (PDF) Payroll Register Multiple Pay Period Adjustment Worksheet (form 1004A) For a promotion at a higher step a letter from DHR or department head and Relevant page(s) from the MOU

Threat if control is missing Unauthorized pay raises and fictitious employees

MC3) Is change in payroll recording periodically reviewed by supervisors or internal audit personnel

a) Management or the internal auditor should periodically review payroll change reports When unusual changes are identified those items should be traced to authorization documents (ie board minutes payroll change forms or collective bargaining agreements)

MC3) Is change in payroll recording periodically reviewed by supervisors or internal audit personnel

- Managerial review of this type of report provides assurance that payroll changes are being properly authorized and input correctly

Example Scenario The Controllerrsquos Payroll and Personnel Services Division had established a policy where

MC3) Is change in payroll recording periodically reviewed by supervisors or internal audit personnel

- Department payrollpersonnel staff must closely review and analyze PeopleSoft payroll reports each pay period to identify whether any employee payroll errors occurred Numerous reports and queries are available in PeopleSoft to aid in review activities

MC3) Is change in payroll recording periodically reviewed by supervisors or internal audit personnel

-Further management should periodically review payroll change reports to ensure that any payroll changes are being properly authorized and input correctly into PeopleSoft

Threat if control is missing Errors not detected and corrected

MC4) Are payrolls disbursed through a direct deposit

a) Requests for direct deposit should be made in writing and kept on file for audit purposes

- Direct deposits can be used to disguise payments to nonexistent employees

MC4) Are payrolls disbursed through a direct deposit

In large units of local government such as San Francisco a once-a-year verification of the legitimacy of all direct deposits may detect unauthorized or fictitious employees It may also detect the continuation of terminated or retired employees on the payroll

Example Scenario City and County of San Francisco (CCSF) employees may access their pay information through direct deposit

MC4) Are payrolls disbursed through a direct deposit

Although All employees are strongly encouraged to enroll in direct deposit for their pay and electronically access their employee pay information Departments only allow exceptions in limited circumstances at the written request of the employee

Threat if control is missing payment to unauthorized or fictitious employees

VC5) Is reconciliation of the payroll fund or bank account done regularly by employees independent of all other payroll transaction processing activities

a) The payroll bank reconciliation should be performed by an employee who is not connected with the authorization of payroll changes or with payroll preparation

VC5) Is reconciliation of the payroll fund or bank account done regularly by employees independent of all other payroll transaction processing activities

- Segregating reconciliation duties from authorization and preparation duties provides for an independent review of transactions that have been processed by the bank and of outstanding checks

b) Reconcile the payroll account monthly

VC5) Is reconciliation of the payroll fund or bank account done regularly by employees independent of all other payroll transaction processing activities

- Payroll is often one of the last bank accounts to be reconciled because it is generally a zero balance account It is important to reconcile this account monthly so that uncashed payroll checks can be promptly identified and rectified

VC5) Is reconciliation of the payroll fund or bank account done regularly by employees independent of all other payroll transaction processing activities

Example Scenario In continuation to the previous illustration monthly payroll reconciliations in the Controllerrsquos Payroll and Personnel Services Division is reviewed and signed by the supervisor and recorded appropriately In addition reconciliations is performed by an employee who does not have modification rights to the payroll system or processes payroll

VC5) Is reconciliation of the payroll fund or bank account done regularly by employees independent of all other payroll transaction processing activities

Threat if control is missing Failure to detect and correct problems Further without regular systematic reconciliation activities and report cross-checks undetected payroll errors can result in over- or under-payments

VC6) Is access to personnel and payroll records checks forms signature plates etc limited

a) Limit access to payroll applications and data files containing potentially confidential information such as social security numbers and deductions to prevent fraudulent payroll

VC6) Is access to personnel and payroll records checks forms signature plates etc limited

b) The payroll process involves a range of confidential and personal information Hence access to computerized applications and paper files (such as personnel files) should be restricted to the fewest number of officers and employees possible

c) If payroll change forms are used control access to these forms by keeping them in a locked cabinet or drawer

VC6) Is access to personnel and payroll records checks forms signature plates etc limited

- Limiting access to payroll change forms reduces the risk that fraudulent authorization could be made by forging authorized signatures and other information

Example Scenario The payroll department of City and County of San Francisco had established a policy where

VC6) Is access to personnel and payroll records checks forms signature plates etc limited

- Access to payrollpersonnel data files containing sensitive or confidential information (eg Social Security numbers deductions) should be restricted to the fewest number of offices and employees possible

VC6) Is access to personnel and payroll records checks forms signature plates etc limited

- Department managers shall provide written instructions for the specific actions required to submit and approve the weekly timesheets for their units including appropriate levels of review and approval (including supervisorsrsquo signatures) documentation and instructions to prohibit access and distribution of confidential information contained in time records

Threat if control is missing Fraudulent payroll authorization

MC7) Is payroll distribution handled by employees who are not involved in the hiring or firing of employees the approval of time and attendance or payroll preparation and data entry

a) Pay checks should be distributed by a responsible employee who is not otherwise connected with any of the steps of payroll preparation

- This will segregate the responsibility for processing payroll information from the distribution of payroll checks

MC7) Is payroll distribution handled by employees who are not involved in the hiring or firing of employees the approval of time and attendance or payroll preparation and data entry

Example scenario In small local governments employees can be required to call for their checks at a central location In other governments like in San Francisco where a large number of employees and physical spread of work locations precludes central distribution checks should be given out at the work station by someone who is not responsible for time and attendance reporting

Threat if control is missing Unauthorized pay to fictitious employees

VC8) Do supervisiontime-keeping procedures and controls include the following

a) Using time clocks to record arrival and departure times will provide additional control over days and hours worked by employees Electronic time clocks can also reduce manual processing of payroll data if the time clock and payroll application are compatible

VC

a) Procedures for time keeping and attendance records

b) Time clocks should be placed in an area where their use can be observed by supervisors This will discourage employees from clocking in or out for co-workers who are not actually present

VC

b) Review and approval by the employees supervisor of hours worked overtime hours and other special benefits

- With large numbers of employees or where shift work is involved an electronic time clock system will help ensure that employees are paid accurately for hours and days worked An electronic time clock can also reduce data entry work if time clock entries can be downloaded directly into the payroll application

VC

c) Placing the time clock in a position where it can be observed by a supervisor

d) Require the use of leave request forms to document advance requests to use accrued leave credits and to document absences covered by the use of leave credits

VC

d) Review for completeness and for the employees supervisors approval of time cards or other time reports

- Leave request forms provide an audit trail on the use of accrued leave credits and assist with the preparation of accurate gross payroll amounts for individual employees

VC

c) Require employees to document days and hours worked and leave credits used on either time sheets or time cards Time sheets and time cards should be reviewed and approved by supervisory personnel who have direct contact with the employee

VC

Example Scenario In the local government of San Francisco the following procedures are being followed with respect to recording of time and attendance

VC

- The department management assign time entry responsibilities to ldquotimekeepersrdquo for payroll data collection timesheet signature and appropriate documentation of all time reporting A back-up timekeeper is also appointed and trained

VC

- Completed timesheets is reviewed and certified by the person having direct supervision over employees to indicate that services were actually performed by the persons listed and that dayshours worked are accurate and justified Only after timesheets have been reviewed and approved by such supervisory personnel should timesheets be transmitted to department payrollpersonnel staff

VC

- Leave request documentation is used to document advance requests to use accrued leave and to document absences covered by the use of such leave

VC

Internal Control Questionnaire ndash Payroll Cycle

Threat if control is missing Lack of appropriate time and attendance records increases the likelihood that an employee could be paid for time not worked or for unauthorized absences

VC1) Are the employees who perform each of the following payroll functions independent of the other five functions

middot personnel and approval of payroll changes

middot preparation of payroll data

middot approval of payroll

middot signing of paychecks

middot distribution of paychecks

middot reconciliation of payroll account

VC

a) Segregate payroll authorizations (hiring firing pay rate setting and other payroll changes) from the preparation and processing of payroll records and checks

- In a computerized payroll system payroll changes should be entered into the system by the personnel department or an employee who does not process the payroll register and checks

- Segregating payroll authorizations from preparation duties reduces the risk of a single employee establishing ghost employees increasing hourly rates and salaries or recording overtime not worked without being detected

Example Scenario In the City and County of San Francisco the Controllerrsquos Payroll and Personnel Services Division disburses salaries and wages for approximately City 27000 employees through biweekly paychecks and direct deposits To make this possible the following City organizations and department payrollpersonnel staff work together to execute payroll duties

Payroll amp Personnel Services Division (PPSD) processes payroll data for employees of city departments and ensures compliance with city state and federal tax wage and hour regulations

Department Payroll Staff are responsible for administering the departmentrsquos payroll and ensuring that employeesrsquo time information is submitted accurately to PPSD

eMerge is a unit within the Controllerrsquos Office that manages and operates PeopleSoft an integrated system that provides human resources benefits administration and payroll services to the Citys active retired and future workforce

Department of Human Resources (DHR) administers City-wide personnel policies and procedures negotiates and administers collective bargaining agreements with labor unions and advises the Cityrsquos other departments in these areas

Civil Service Commission (CSC) oversees the merit system for the City by establishing rules and policy related to the merit system hearing appeals on examinations eligibility lists minimum qualifications classification discrimination complaints and future employment and interpreting rules and policies

San Francisco Employeesrsquo Retirement System (SFERS) secures protects and invests pension trust assets administers the mandated benefits programs and provides promised benefits to active and retired members of the system And lastly

Health Service System (HSS) creates contracts based on negotiations with health providers which offer eligible employees the opportunity to enroll themselves and eligible family members in medical dental vision and flexible spending account benefits

Threat if control is missing Fraud theft of paychecks

We will use the payroll procedures of City and County of San Francisco as the example scenario in each internal control questions

VC

4 All deposits should be personally handed to the cashier

1) Does adequate segregation of duties exist within your department between staff members responsible for receiving depositing and reconciling cash and checks

3 At the end of each business day a physical count of all cash and checks received must be completed and those amounts must be reconciled to the receipt log The receipt log must be signed and dated by a departmental designee other than the individual who performed the physical count and reconciliation to the receipt log

The management must ensure that the cash‐handling and record‐keeping functions be kept separate For smaller departments where separation of duties is impossible or impractical the supervisory personnel who do not handle cash should perform specific verification for reasonable and sound internal controls

MC

the Buyers

2) What is the minimum information required to review the creditworthiness of

An entity needs to do a background check on its buyers to know whether or not they have the capacity to meet payments on time Entities need to set up standards on the kind and amount of transactions that potential clients with different financial capacities can enter into

In universities however a different kind of background check is conducted Donors and rich parents aside admissions to large universities are largely based on academic performance and potential

In Yale University for example an applicantrsquos academic strength is the first consideration The school review grades standardized test scores and evaluations by a counselor and two teachers to determine academic strength The admissions committee then factors in student qualities such as motivation curiosity energy leadership ability and distinctive talents

MC In universities threats in this area include

(2) tuition bills may have occurred but may

not have been billed andor recorded and

(3) Intentional errors or misappropriation of information could occur

VC

3) Are billings reviewed and approved prior to billing andor recording

(1) tuition bills incorrectly prepared andor billings and other terms may be misstated

In University of Arizona accountability for tuition bills are the responsibility of the RegistrarStudentBusiness Services (SBS) and may not be delegated to any other functional area

Where invoices are computer generated SBS should ensure adequate controls exist over invoice preparation

4) Do changes to the prescribed billing amount require the approval of an authorized individual

All credit transactions should be included in the accounting records and should be approved by the proper individuals

VC

vC

4) Do changes to the prescribed billing amount require the approval of an authorized individual

In University of Arizona all credit memos issued to students should be supported by documentation and approved by Financial Services prior to issuance

Also credit memo transactions should be numerically controlled and accounted for periodically Credit memos should be pre-numbered where the integrity of sequencing is not computer controlled

5) If cash is accepted are pre-numbered receipts used to track payment

Unless documented there is no way to trace the movement of money A proper internal control entails the documentation of every sale of goods or services with a cash register entry a pre-numbered receipt form an invoice etc Customers are issued a duplicate

In institutions like Ithaca College whenever cashcheck is received in person an acceptable form of receipt must be used

vC

2 Dated cash log

4 Cash register tapes

5 Other documentation

Date received Name of the payee Amount received What the payment was for

Unique receipt number

5) If cash is accepted are pre-numbered receipts used to track payment

1 Uniquely and consecutively pre‐numbered receipts with a duplicate copy maintained as a cash receipts log

3 Pre‐numbered tickets

In the University of Glasgow a receipt must be issued for all cash received and a copy retained The receipt should be processed through the Cash Register or issued manually and shall show

Type of payment received ie cash cheque postal order credit card debit card

VC6) Do tellers have their own vault cubicle or controlled cash drawer in which to store their cash supply

As much as possible each cashier should start hisher shift with a new beginning cash balance and hisher own cash drawer If a register must be shared it must have

sufficient controls to allow collections to be attributed to individual cashiers (egseparate user IDs and passwords to access the register)

In University of Wellington the following guidelines in the storage of cash is implemented

(a) During business hours all cash should be securely stored in a locked cash register cash drawer or similar with access restricted to authorised cash handling staff

(b) For staff security during business hours the amount of cash securely stored in a locked cash register cash drawer or similar should be monitored Where necessary cash should be transferred into a safe or similar for secure storage

VC

VC

6) Do tellers have their own vault cubicle or controlled cash drawer in which to store their cash supply

(c) Outside of business hours all cash should be securely stored in a safe or similar away from where cash is typically handled Cash should not be stored in an obvious place such as in a locked cash tin on the cashier counter

7) Is each tellerrsquos cash checked daily to an independent control from the proof or accounting control department

Reconciliations should be completed by a specified individual who does not collect funds If this is not feasible within a department someone outside of the collections process should review the reconciliation

Daily reconciliations should be performed by a specified individual comparing the following

middot the cash receipt records (eg cash register balancing records prenumbered receipts and bank deposit slip if applicable)

middot the completed Collections Report