Embed Size (px)

Citation preview

Georgia Department of Revenue

ACCG Annual Conference 2013

Sales Tax Update

This presentation is the property of the Commissioner, Georgia Department of Revenue. All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any

means, electronic, mechanical photocopying, recording, or otherwise, without the prior written permission of

the Commissioner, Georgia Department of Revenue

1

Georgia Department of Revenue

2

Presented By:

Amy Oneacre Sales & Use Tax Policy Manager

Georgia Department of Revenue

3

Discussion Topics

•Tax Reform – Georgia HB 386 (2012)

•GATE Program

•Manufacturing Exemptions

•E-Fairness and CPRS

•TSPLOST

•2013 Legislative Update

Georgia Department of Revenue

HB 386 Sales Tax Related Impact

• Film Industry

• Motor Vehicles

• Manufacturing

• Agriculture

• Sales Tax Holidays

• E-Fairness

• Jet Fuel

• Convention and Trade Shows

• Competitive Projects of Regional Significance

4

Georgia Department of Revenue

Manufacturing Exemptions § 48-8-3.2

• Effective January 1, 2013, the sale, use, or storage of

machinery, equipment, industrial materials, and

manufacturing packaging supplies shall be exempt

from all sales and use taxation.

• Effective January 1, 2013, Energy used in

manufacturing will be partially exempt from sales and

use taxation.

5

Georgia Department of Revenue

New For Manufacturing 2013

• Returnable, reusable, single use packaging;

• Industrial materials of all kinds;

• Manufacturing for promotional use;

• Energy Phase-In;

• No Exemption application process for new

manufacturing plants.

6

Georgia Department of Revenue

Exemption for Energy Used in Manufacturing

§ 48-8-3.2

• Effective January 1, 2013, the sale, use, storage, or

consumption of energy, which is necessary and integral to the

manufacture of tangible personal property at a manufacturing

plant in this state, will be partially exempt from sales tax.

• This exemption applies to energy used for administrative

purposes, transport of raw or finished goods, heating and

cooling, and “any other purpose” at a manufacturing plant.

7

Georgia Department of Revenue

Energy Used in Manufacturing (Cont.)

• "Energy" means natural or artificial gas, oil, gasoline,

electricity, solid fuel, wood, waste, ice, steam, water, and other

materials essential for heat, light, power, refrigeration, climate

control, processing, or any other use in any phase of the

manufacture of tangible personal property.

• This energy exemption does not apply to energy purchased by

a manufacturer primarily engaged in producing electricity for

resale.

8

Georgia Department of Revenue

Energy Used in Manufacturing (Cont.)

• This energy exemption will be phased in a four year period,

2013 through 2016.

• Transactions occurring during the 2013 calendar year qualify

for a 25% exemption.

• 50% in 2014.

• 75% in 2015.

• 100% in 2016.

Note: Energy will still be subject to ELOST.

9

Georgia Department of Revenue

Energy Used in Manufacturing (Cont.)

• Counties and municipalities have the option to levy a local

excise tax on energy. This would be subject to sales and use

tax except for exemptions.

• The obligation of a local excise tax is phased-in the same

manner as exemptions.

• The rate of the tax will vary depending on the locality or

district. Other local taxes are imposed, but in no event can the

rate exceed 2%.

10

Georgia Department of Revenue

Agriculture Related Exemptions

§ 48-8-3.3

• Effective January 1, 2013, sales and use by a “Qualified Agriculture Producer” of agricultural production inputs, energy used in agriculture, agricultural machinery and equipment, shall be exempt from sales and use tax.

• A taxpayer that meets the statutory criteria for designation as a “Qualified Agriculture Producer” may apply to the Commissioner of Agriculture requesting an agricultural sales and use tax exemption certificate (GATE) that contains an exemption number – 27,000+ GATE cards issued.

11

Georgia Department of Revenue

Agriculture Related Exemptions (Cont.)

Machinery and equipment, including repair and replacement

parts, will be exempt from sales and use tax. If at the time of

sale or lease, the components, when assembled, will have the

character of agricultural machinery or equipment.

Note: ATV’s and UTV’s sold to qualified agriculture producers are exempt. 12

Georgia Department of Revenue

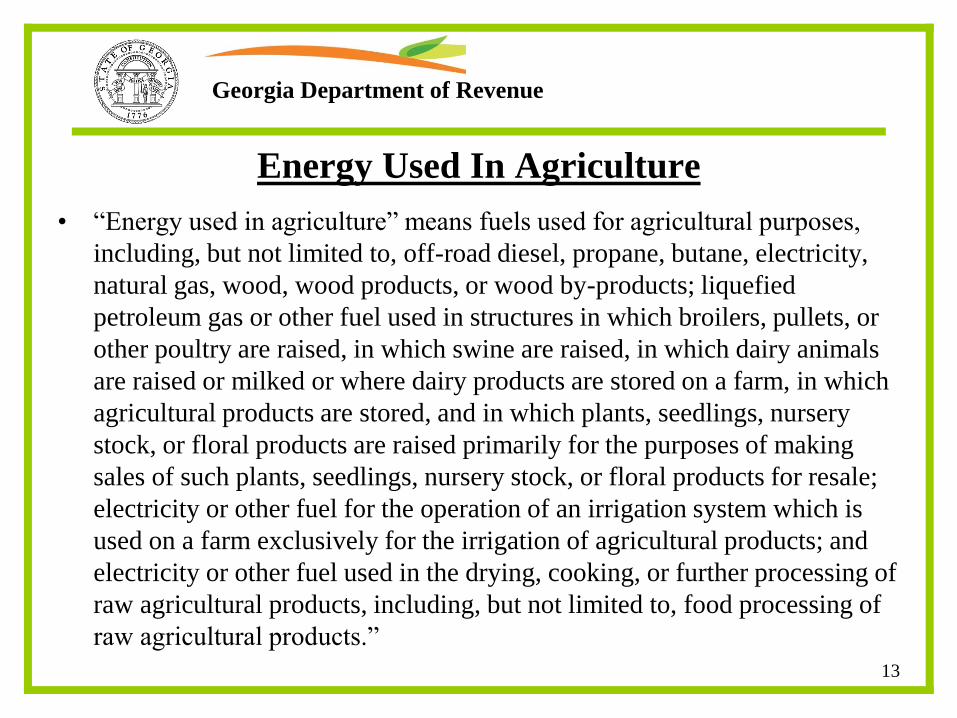

Energy Used In Agriculture

• “Energy used in agriculture” means fuels used for agricultural purposes,

including, but not limited to, off-road diesel, propane, butane, electricity,

natural gas, wood, wood products, or wood by-products; liquefied

petroleum gas or other fuel used in structures in which broilers, pullets, or

other poultry are raised, in which swine are raised, in which dairy animals

are raised or milked or where dairy products are stored on a farm, in which

agricultural products are stored, and in which plants, seedlings, nursery

stock, or floral products are raised primarily for the purposes of making

sales of such plants, seedlings, nursery stock, or floral products for resale;

electricity or other fuel for the operation of an irrigation system which is

used on a farm exclusively for the irrigation of agricultural products; and

electricity or other fuel used in the drying, cooking, or further processing of

raw agricultural products, including, but not limited to, food processing of

raw agricultural products.”

13

Georgia Department of Revenue

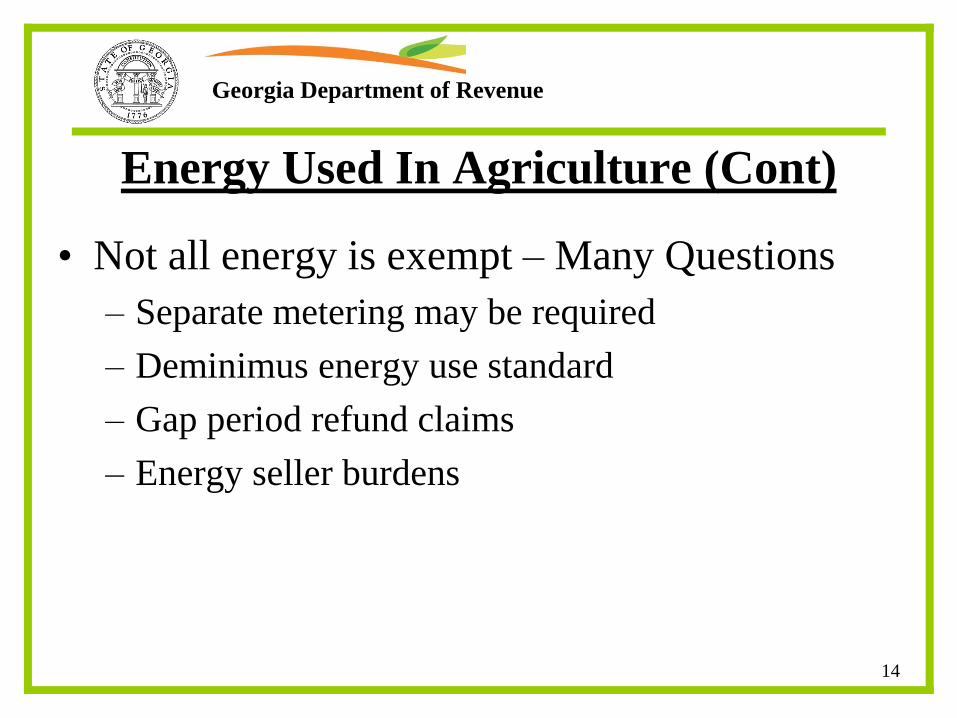

Energy Used In Agriculture (Cont)

• Not all energy is exempt – Many Questions

– Separate metering may be required

– Deminimus energy use standard

– Gap period refund claims

– Energy seller burdens

14

Georgia Department of Revenue

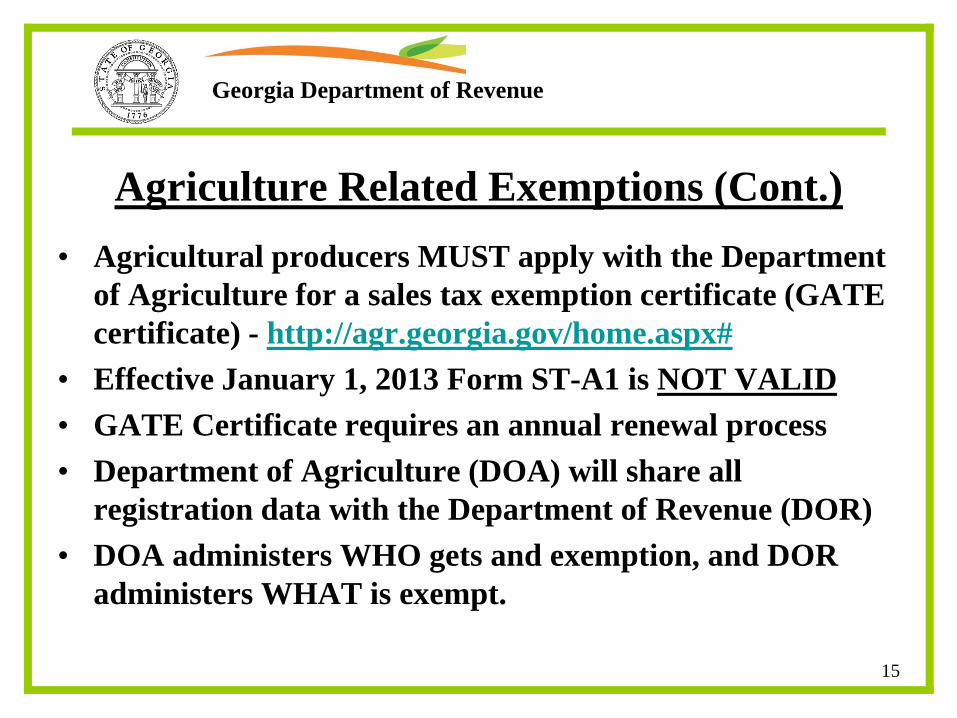

Agriculture Related Exemptions (Cont.)

• Agricultural producers MUST apply with the Department

of Agriculture for a sales tax exemption certificate (GATE

certificate) - http://agr.georgia.gov/home.aspx#

• Effective January 1, 2013 Form ST-A1 is NOT VALID

• GATE Certificate requires an annual renewal process

• Department of Agriculture (DOA) will share all

registration data with the Department of Revenue (DOR)

• DOA administers WHO gets and exemption, and DOR

administers WHAT is exempt.

15

Georgia Department of Revenue

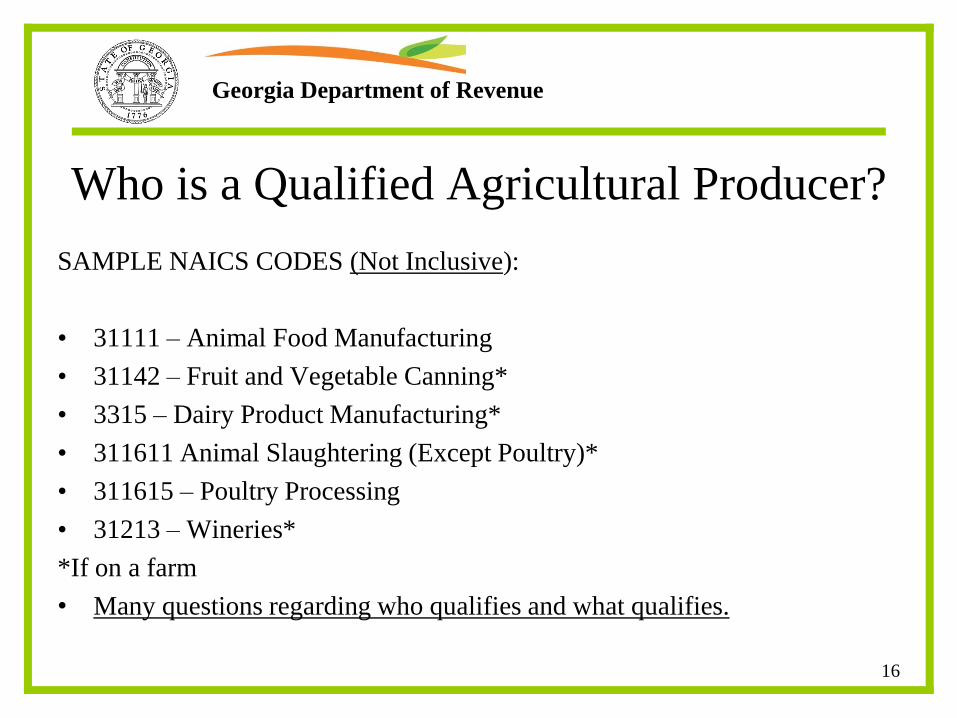

Who is a Qualified Agricultural Producer?

SAMPLE NAICS CODES (Not Inclusive):

• 31111 – Animal Food Manufacturing

• 31142 – Fruit and Vegetable Canning*

• 3315 – Dairy Product Manufacturing*

• 311611 Animal Slaughtering (Except Poultry)*

• 311615 – Poultry Processing

• 31213 – Wineries*

*If on a farm

• Many questions regarding who qualifies and what qualifies.

16

Georgia Department of Revenue

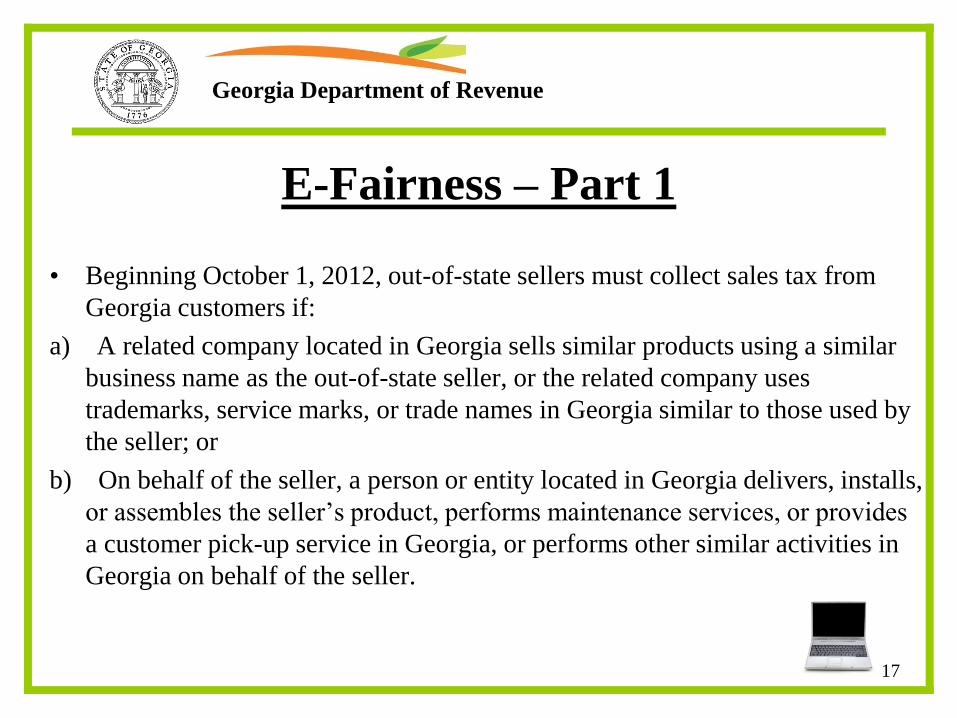

E-Fairness – Part 1

• Beginning October 1, 2012, out-of-state sellers must collect sales tax from

Georgia customers if:

a) A related company located in Georgia sells similar products using a similar

business name as the out-of-state seller, or the related company uses

trademarks, service marks, or trade names in Georgia similar to those used by

the seller; or

b) On behalf of the seller, a person or entity located in Georgia delivers, installs,

or assembles the seller‟s product, performs maintenance services, or provides

a customer pick-up service in Georgia, or performs other similar activities in

Georgia on behalf of the seller.

17

Georgia Department of Revenue

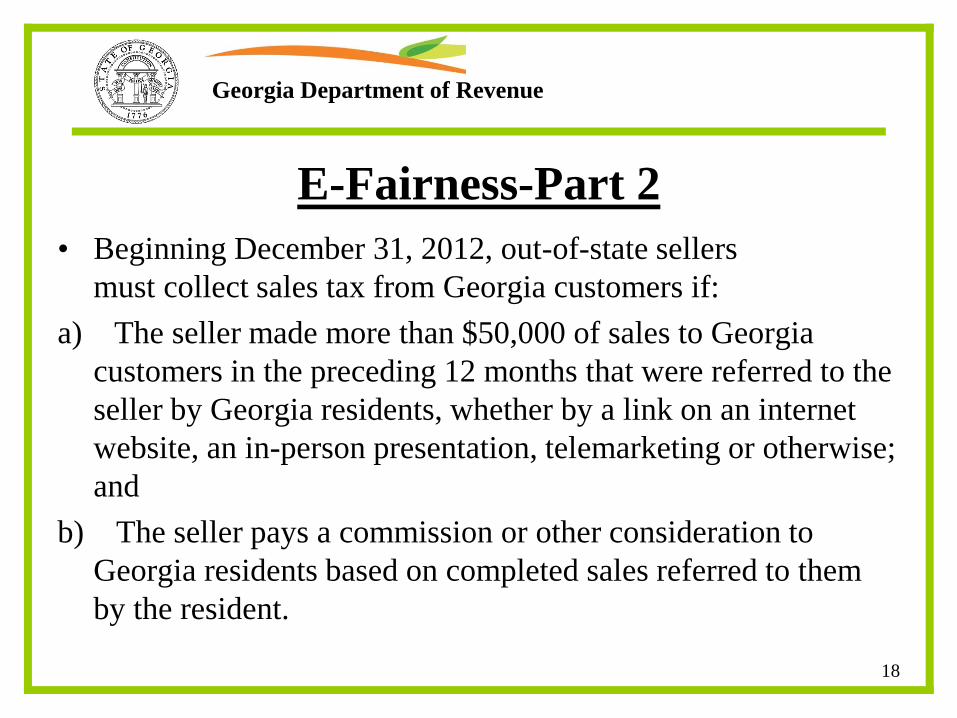

E-Fairness-Part 2

• Beginning December 31, 2012, out-of-state sellers

must collect sales tax from Georgia customers if:

a) The seller made more than $50,000 of sales to Georgia

customers in the preceding 12 months that were referred to the

seller by Georgia residents, whether by a link on an internet

website, an in-person presentation, telemarketing or otherwise;

and

b) The seller pays a commission or other consideration to

Georgia residents based on completed sales referred to them

by the resident.

18

Georgia Department of Revenue

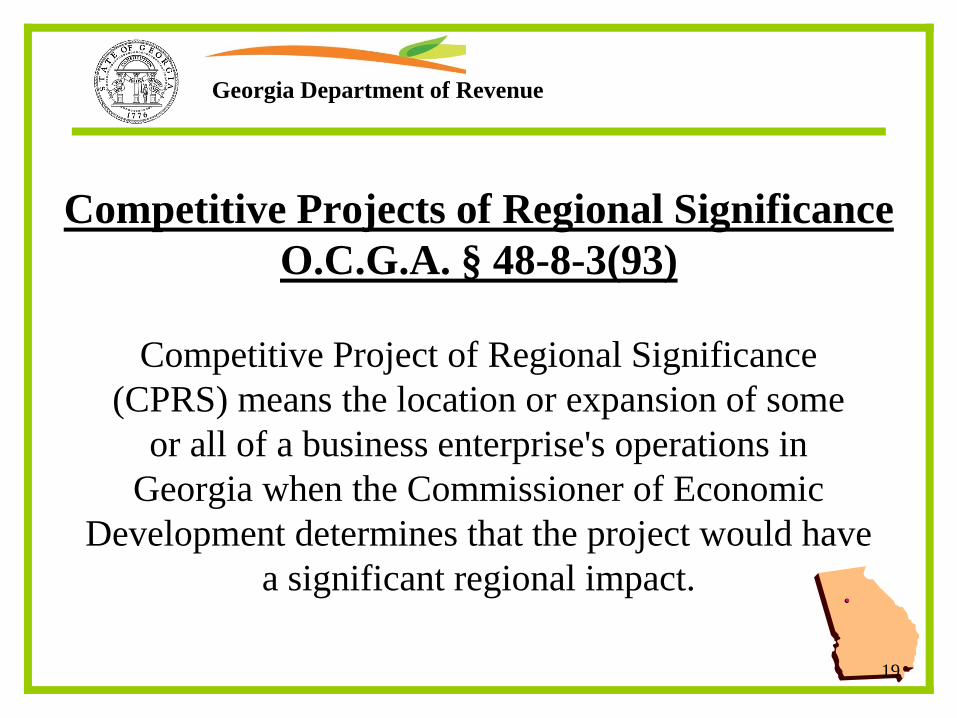

Competitive Projects of Regional Significance

O.C.G.A. § 48-8-3(93)

Competitive Project of Regional Significance

(CPRS) means the location or expansion of some

or all of a business enterprise's operations in

Georgia when the Commissioner of Economic

Development determines that the project would have

a significant regional impact.

19

Georgia Department of Revenue

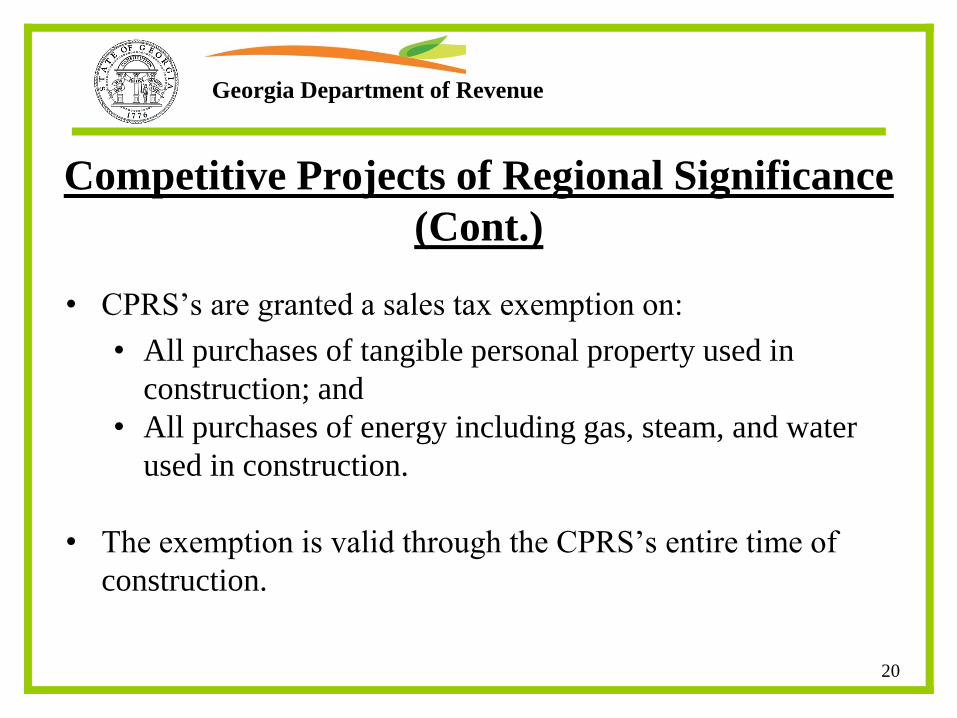

Competitive Projects of Regional Significance

(Cont.)

• CPRS‟s are granted a sales tax exemption on:

• All purchases of tangible personal property used in

construction; and

• All purchases of energy including gas, steam, and water

used in construction.

• The exemption is valid through the CPRS‟s entire time of

construction.

20

Georgia Department of Revenue

TSPLOST

• 3 Regional Transportation Districts passed the

TSPLOST – Central Savannah, River Valley,

and Heart of Georgia;

• 1% additional sales tax – Some exemptions

apply;

• TSPLOST requires separate reporting,

accounting, and distribution;

• Form ST-3 changed significantly!!

21

Georgia Department of Revenue

FORM ST-3 Form Changes

• Separate county by county line item reporting

for energy sold to manufacturers.

• TSPLOST Schedule – Separate reporting

required.

• Multiple sales tax rate charts.

22

Georgia Department of Revenue

2013 Legislative Update – HB 164

• Extends sunset for exemption on aircraft

engine, parts and equipment and other tangible

personal property used in maintenance for

aircraft not registered in Georgia.

• Continues support for Georgia‟s aircraft

maintenance and repair industries.

23

Georgia Department of Revenue

2013 Legislative Update – HB 193

• Reinstates Several Sales Tax Exemptions

– Nonprofit or volunteer health centers and clinics

– Sales of food to food banks and hunger relief

– Prepared food donated for disaster relief

– Job training organizations

• Modifies dates for sales tax holiday 2013

• Excludes direct mail postage from “delivery charges”

• Tourism Act Correction

• NOT signed by Governor – 4/15/13

24

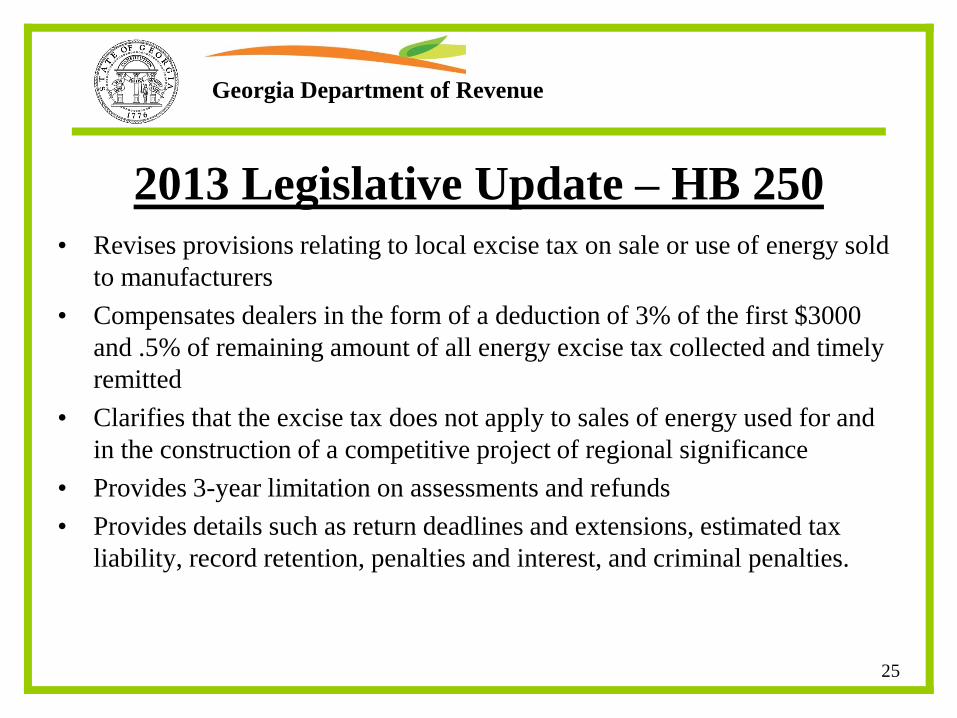

Georgia Department of Revenue

2013 Legislative Update – HB 250

• Revises provisions relating to local excise tax on sale or use of energy sold

to manufacturers

• Compensates dealers in the form of a deduction of 3% of the first $3000

and .5% of remaining amount of all energy excise tax collected and timely

remitted

• Clarifies that the excise tax does not apply to sales of energy used for and

in the construction of a competitive project of regional significance

• Provides 3-year limitation on assessments and refunds

• Provides details such as return deadlines and extensions, estimated tax

liability, record retention, penalties and interest, and criminal penalties.

25

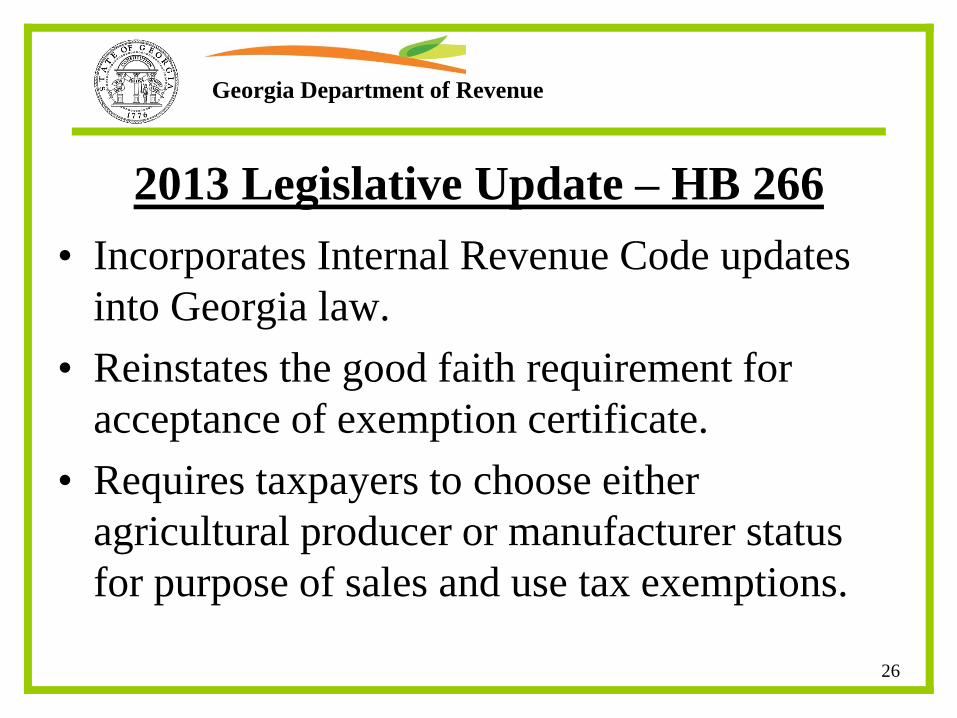

Georgia Department of Revenue

2013 Legislative Update – HB 266

• Incorporates Internal Revenue Code updates

into Georgia law.

• Reinstates the good faith requirement for

acceptance of exemption certificate.

• Requires taxpayers to choose either

agricultural producer or manufacturer status

for purpose of sales and use tax exemptions.

26

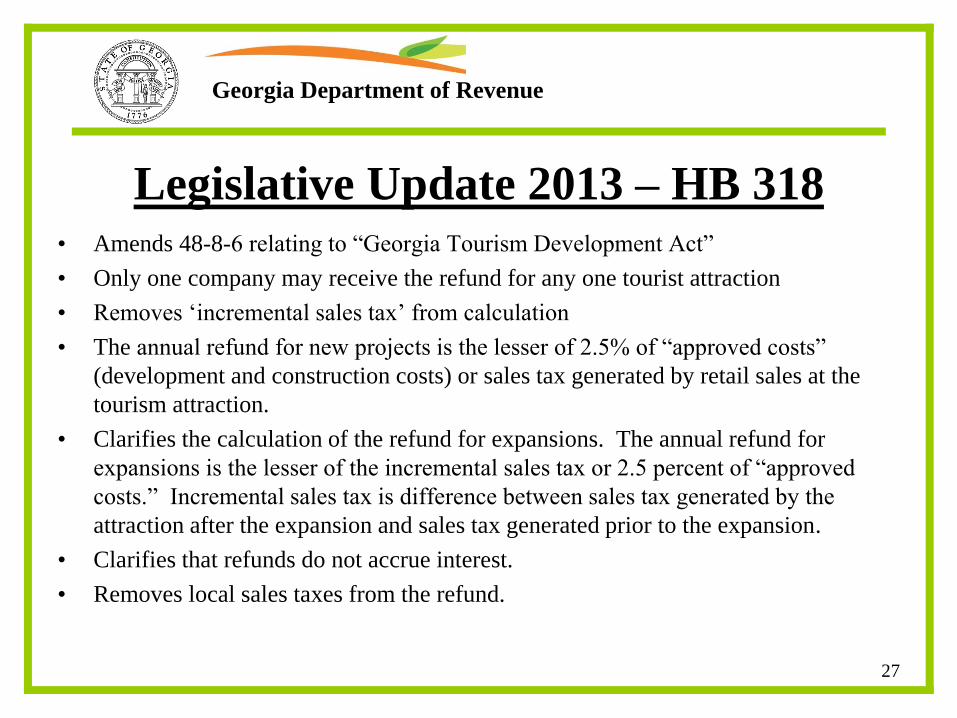

Georgia Department of Revenue

Legislative Update 2013 – HB 318 • Amends 48-8-6 relating to “Georgia Tourism Development Act”

• Only one company may receive the refund for any one tourist attraction

• Removes „incremental sales tax‟ from calculation

• The annual refund for new projects is the lesser of 2.5% of “approved costs”

(development and construction costs) or sales tax generated by retail sales at the

tourism attraction.

• Clarifies the calculation of the refund for expansions. The annual refund for

expansions is the lesser of the incremental sales tax or 2.5 percent of “approved

costs.” Incremental sales tax is difference between sales tax generated by the

attraction after the expansion and sales tax generated prior to the expansion.

• Clarifies that refunds do not accrue interest.

• Removes local sales taxes from the refund.

27