Embed Size (px)

Citation preview

Sales Forecasting with Financial Indicators and Experts’ Input

Vishal Gaur∗, Nikolay Osadchiy†, Sridhar Seshadri‡

October 23, 2008

Abstract

The volume of retail sales is commonly understood to be correlated with the state of the

economy. This information can potentially be employed in demand forecasting, operations

decisions, and risk management. We propose a model in which the total sales of a retailer

is a function of sales forecasts generated by equity analysts, the term of the forecast, and

the return on an aggregate financial market index over the term of the forecast. We test

this model on a panel of 4,698 observations of annual firm-level sales forecasts for 97 retailers

over 10 years, each year containing multiple forecasts of varying terms. We show that the

correlation coefficient of sales forecast error with the financial market return is significant, and

varies across firms depending on the retail segment, the gross margin, and the term of the

forecast. Our model provides results on other parameters for forecasting as well, and a method

for forecast updating. We show that forecast updates from our model provide new information

not contained in the forecast updates by equity analysts, so that a combined forecast leads

to improved forecast accuracy. These results have applications in forecast updating, decision

postponement, production planning, and risk management.

∗Johnson Graduate School of Management, Cornell University, 321 Sage Hall, Ithaca NY 14853-6201; email:

[email protected].†Leonard N. Stern School of Business, New York University, 44 West 4th St, Suite 8-160, New York NY 10012;

email: [email protected].‡Department of Information, Risk, and Operations Management, McCombs School of Business, University of

Texas at Austin, 3.440, 1 University Station, Austin, TX 78712. E-mail: [email protected].

Sales Forecasting with Financial Indicators and Experts’ Input

Abstract

The volume of retail sales is commonly understood to be correlated with the state of the

economy. This information can potentially be employed in demand forecasting, operations

decisions, and risk management. We propose a model in which the total sales of a retailer

is a function of sales forecasts generated by equity analysts, the term of the forecast, and

the return on an aggregate financial market index over the term of the forecast. We test

this model on a panel of 4,698 observations of annual firm-level sales forecasts for 97 retailers

over 10 years, each year containing multiple forecasts of varying terms. We show that the

correlation coefficient of sales forecast error with the financial market return is significant, and

varies across firms depending on the retail segment, the gross margin, and the term of the

forecast. Our model provides results on other parameters for forecasting as well, and a method

for forecast updating. We show that forecast updates from our model provide new information

not contained in the forecast updates by equity analysts, so that a combined forecast leads

to improved forecast accuracy. These results have applications in forecast updating, decision

postponement, production planning, and risk management.

1. Introduction

There is ample evidence in the business press that end-consumer demand is correlated with broad

financial market indicators. For example, in the period 2000-2002, when the NASDAQ composite

index lost more than 60% of its value and the S&P 500 index lost about 40%, retail sales were

documented to be lower than predicted by analysts (Business Week (2001)). A number of retailers,

such as J. C. Penney, Sears, ShopKo, and OfficeMax announced store closings. Bonds of Saks Inc.

and ShopKo Stores were downgraded from investment quality to junk (Kaufman (2001)). Several

retailers, including Kmart, filed for bankruptcy.

More recent examples relate to the 2007-08 crisis of the mortgage-backed securities market. In

September 2007, the CFO of Office Depot announced: “Our small-business customers have changed

their buying habits as a result of this environment, and traffic remains slower than normal in our

retail stores” (Reuters (2007)). Several retailers, such as furniture store Levitz, electronics seller

Sharper Image, and home furnishings retailer Linens ‘n Things have filed for bankruptcy. While

high-end retailers such as Saks Inc. have suffered unexpected declines in sales, Wal-Mart and select

other discount retailers have benefited through stronger-than-expected sales. On the other hand,

during 1998-99 as well as during 2004-05, US financial markets and retail sales were both rising

(BBC (1999)).

These facts suggest that retail sales are correlated with financial market returns. This corre-

lation would not be surprising because financial market returns affect income and wealth, which

further affect household consumption. For example, one mechanism for this relationship is the per-

manent income hypothesis of Friedman (1957). In the recent operations literature, many academic

papers have studied models of optimal inventory decisions and hedging demand risk predicated

on this correlation, see for example, Caldentey and Haugh (2006), Gaur and Seshadri (2005), and

Van Mieghem (2003). However, the extent of this correlation is not known. It is also not known how

the correlation coefficient varies across firms and why. In this paper, we develop and test a model

to examine statistical evidence for this phenomenon and examine its usefulness for forecasting,

operational decision-making, and risk management.

Our study is concerned with the firm-level, dollar-denominated annual sales realized by retailers.

Forecasts of annual sales of firms are generated by equity analysts up to three years in advance of

their fiscal year-end dates, and are updated frequently. We model the joint evolution of the forecast

1

and the financial market using a continuous time stochastic process. We represent the financial

market by one broad market indicator, such as the value weighted market index. Besides financial

market indicators, retail sales can also be correlated with non-financial metrics of the state of the

economy, such as the GDP growth rate. In this paper, we focus on financial market indicators

because they are traded. We further focus on contemporaneous returns rather than lagged returns.

These two features of our model are key because they enable us to apply it for not only forecasting

but also risk assessment and hedging. Our model can easily be generalized to allow a vector of

multiple market indicators, non-financial metrics, or lagged variables.

One output of this model is an analytical expression for the forecast error as a function of the

term of the forecast, financial market return over the term of the forecast, and various volatility

parameters. We use this expression to test various hypotheses about the correlation coefficient

between sales forecast error and financial market return over the term of the forecast. Our data

set is a panel of 4,698 observations across 97 US public retailers and fiscal years 1997-2007, each

year containing multiple forecasts made at different times for each firm. The time period for these

data is useful since it covers a wide range of variation: two periods of high market returns, 1998-

2000 and 2003-2005, and two periods of low or negative market returns, 2001-2002 and 2006-07.

Another output of our model is a method to revise sales forecasts using up-to-date information

on financial market prices. We evaluate the accuracy of these forecasts and compare them to the

forecast revisions issued by equity analysts at the same time epochs. Thus, we determine if analysts

incorporate publicly available historical financial return information in their forecast updates, and

if our model adds new information augmenting their forecasts.

Our results show that the correlation between the sales forecast error and market return is

significant. With an average value of 0.17 across our entire data set, it varies across retail segments

from a high of 0.83 for office supplies stores to not significant or negative for shoe stores and

auto parts and accessories stores. We classify retail segments into two categories, discretionary

purchase and everyday use, analogous to a ‘needs versus wants’ distinction in economics. We

find that retail segments in the discretionary purchase group, such as jewelry, home improvement,

consumer electronics and apparel, have higher correlation coefficient estimates on average than

retail segments in the everyday purchase group, such as discounters and wholesale clubs. We

further classify retailers in each segment into high- and low-gross margin groups, and find that the

2

average correlation coefficient for high-margin retailers is significantly higher than that for low-

margin retailers. Our results not only fit our expectations of retailers, but also show a wide range

of variation across firms. For example, in the jewelry stores segment, Tiffany’s, a high-margin

retailer, has an estimated correlation coefficient of 0.87, whereas Zale Corp., a lower margin retailer

has 0.29. In the discounters and wholesale clubs segment, BJ’s Wholesale Club, a warehouse

club selling durable discretionary purchase items has an estimated correlation coefficient of 0.91,

whereas Wal-mart Stores, a discounter has 0.01, and Dollar General has -0.81. We further test the

hypothesis whether the correlation coefficient increases with the term of the forecast. We find that

its average value across the data set almost doubles as the term of the forecast increases from 12-15

months to 20-24 months.

The main application of our model is to forecast updating. Firm-level sales forecasts are issued

by retailers for planning and by equity analysts for estimating earnings. In both cases, substantial

effort is required to generate and update forecasts. In contrast, financial data are readily available

and highly reliable. Thus, our model, together with financial data, can be used to update sales

forecasts in a cost-efficient way. We test the accuracy of the model for forecast updating by

comparing errors of the forecasts generated by the model vis-a-vis forecasts issued by equity analysts

at the same times. We find that, on average, analysts have lower forecast root mean squared error

than our model. This is not surprising because analysts have access to many types of information

for their forecast updates, whereas our model-based updates are based on only one variable. More

importantly, we find only a weak evidence that analysts take financial market returns into account

in their forecast updates. We conduct a regression of analyst forecast updates on financial returns

over the period of update as per our model, and find that the financial returns are weakly significant

even though they were public information at the times when analysts updated their forecasts. To

further examine the usefulness of our model, we construct a combined model based on analysts’

forecast updates as well as our model’s forecast updates, and find that both variables are statistically

significant in improving forecast accuracy. Thus, a combined forecast obtained from both sources

performs better than the equity analysts. Furthermore, as expected, the improvement is higher for

firms with high correlation coefficients and for longer term forecasts.

Our paper contributes to the operations management literature by investigating empirical sup-

port for recent studies in financial and operational hedging, decision postponement, and forecast

3

evolution. Gaur and Seshadri (2005) examine optimal inventory and financial hedging decisions for

a firm when its demand is correlated with contemporaneous returns on financial market indices.

They present evidence for the existence of such correlations using retail industry-level data for same

store sales growth rates. Caldentey and Haugh (2006) use a continuous time model to study the

optimal operating policy and trading strategy when their payoffs are correlated. Chod et al. (2007)

study the optimal combination of operational flexibility and financial hedging for a two-product

firm whose demand is correlated with financial market indicators, and show when the risk mitiga-

tion strategies are complements or substitutes. Van Mieghem (2008)(Chapter 9) discusses various

types of risk and their mitigation through operational and financial means. Chen et al. (2007) study

inventory and financial hedging decisions in a multi-period model in which demand is correlated

with the prices of traded assets. Besides these research papers, a correlation between operational

payoffs and financial market returns is also often assumed in the real options literature, see for

example, Dixit and Pindyck (1994). In comparison to this research, our paper presents a method

to estimate the correlation between operational payoffs and financial market returns, examines its

drivers, and shows when knowledge of this correlation is most advantageous.

The theoretical framework of our model is similar to the martingale model of the forecast

evolution (MMFE) developed independently by Graves et al. (1986), Graves et al. (1998) and

Heath and Jackson (1994). A continuous time version of MMFE was studied by Sapra and Jackson

(2005). Our model can be viewed as a particular case of the MMFE. The difference is that rather

than using past observations for forecast updates, we find explanatory variables which drive the

update.

This paper uses data for the retailing sector, but our model can also be applied to the manu-

facturing and wholesale trade sectors because changes in consumer demand will eventually affect

demand at the upstream layers of the supply chain. In this respect, our paper complements the

literature on stock returns of industry portfolios along the supply chain. For example, Hong et al.

(2007) study if stock returns of industry portfolios predict future stock market movements, and

Menzly and Ozbas (2006) study cross-industry momentum. While these studies seek to predict fu-

ture industry-specific or aggregate stock market returns using current industry portfolios, we seek

to predict sales using aggregate stock market returns. Hence, our hypotheses rely on consumption

being dependent on financial market returns, and can be extended to examine lead and lag effects

4

among industries.

The paper is organized as follows: we set up our hypotheses in §2; in §3, we formulate a model

of the joint evolution of the forecast and financial indicators and discuss an econometric setup

for its estimation; §4 and §5 contain the description of the data set and the estimation results,

respectively; in §6, we evaluate the forecast accuracy of our model compared to equity analysts; in

§7, we conclude the paper with a discussion of applications, limitations, and further research. The

online appendix to the paper gives detailed firm-by-firm estimates of the correlation coefficient and

results on the forecast accuracy of our model.

2. Hypotheses

Consider the forecast of total dollar denominated annual sales of a retailer and the actual sales

realization for a particular fiscal year. Suppose that the forecast is a consensus estimate given

by several experts or financial analysts incorporating all the information available to them on the

forecast date, and the sales realization is announced by the retailer after the fiscal year-end date. We

denote the difference between the sales realization and the forecast as the sales forecast error, and

the time interval from the forecast date to the fiscal year-end date as the term of the forecast. We

use the terms experts and analysts interchangeably throughout the paper since our mathematical

model is generic and could be applied to situations other than firm-level sales.

We want to capture the causal relationship between the state of economy and spending behavior

of consumers, and the resulting effect on retail sales. We use broad aggregate financial indices as

proxies for the state of the economy because they are correlated with increase in wealth and income

of consumers. For our model, they are preferred to other proxies, such as growth rate of GDP,

since they are traded on a market and offer opportunities for continuous updating of forecasts as

well as hedging against uncertainty. We refer to the return on a broad market index generically

as financial market return. Alternatively to a broad index, one might consider using a return on

a portfolio of retail stocks. Most likely, the return on such a portfolio will be correlated with the

sales forecast error of a retailer since the stock value would tend to go up (down) in response to

higher (lower) sales. However, limiting the choice to sector specific indicators limits their ability

to proxy for the state of the economy and customers’ propensity to consume. A broad indicator

is also preferred if it suffices to explain the forecast error for a wide range of retailers. We might

5

also consider using vector valued processes to capture the evolution of financial information. The

model presented in this paper can easily be modified to accommodate this change.

A large stream of economics literature studies the effect of income and wealth on household

consumption. In the late fifties, Friedman formulated his permanent income hypothesis according

to which consumption does not depend on short term changes in disposable income but rather on

long-term income expectations. This idea was refined by several researchers. For example, Ando

and Modigliani (1963) formulated the income lifecycle hypothesis in which consumption depends

on the future returns on capital. Subsequently, a number of papers attempted to link marginal

propensity to consume to the stock market wealth of households and measure the magnitude of

the effect for different types of households, see Poterba (2000) for a review. These papers find that

rising stock market leads to increase in consumption among equity holding households, and even

non-stockholding households may experience spending increase due to buoyed confidence in their

future income. Poterba (2000) also acknowledges that stock market decline can prompt a sharp

and asymmetric decrease in consumption, admitting limited empirical evidence of this effect. More

recent papers such as Dynan and Maki (2001) use quarterly survey data of households with equity

investments and study how consumption depends on current and lagged stock returns. Dynan and

Maki (2001) find that the consumption amounts to 3.5 cents per dollar of stock wealth and the

effect of lagged stock returns is insignificant after 18 months. Thus, this literature implies that total

consumption, and hence, demand, increases with returns on equity investments of households. We

proxy returns on equity investments of households between the forecast date and the fiscal year-end

date by the return on the financial market index over the term of the forecast. Thus, motivated by

this literature, we set up the following hypothesis:

Hypothesis 1 Sales forecast error of retail firms is positively correlated with the return on a fi-

nancial market index over the term of the forecast.

Another stream of economics literature deals with the problem of determining how a consump-

tion structure changes with income. The fact that the proportion of income spent on everyday

purchase goods, such as food, basic medications, etc., decreases with income and that spent on

discretionary purchase goods, such as luxury goods, increases with income was first observed by

Engel in the 19th century. A substantial body of literature has been developed since then. Modern

econometric techniques have been used to estimate Engel curves for different segments, see for

6

example, Banks et al. (1997). This literature suggests that demand for everyday purchase prod-

ucts is negatively correlated with income, whereas demand for discretionary purchase products is

positively correlated with income. Therefore, we classify retailers into discretionary purchase and

everyday purchase retail segments based on the types of products that they sell. We expect to see

different values of the correlation of sales forecast error with market return across firms depending

on their classification. For example, we expect supermarket stores and pharmacies to have a steady

demand that is relatively insensitive to the financial market. On the other hand, we expect the

demand for luxury goods to be higher in periods of booming economy when consumer have more

disposable income. Our second hypothesis is based on this reasoning:

Hypothesis 2 (a) Retailers in discretionary purchase retail segments have positive correlation

between sales forecast error and financial market return over the term of the forecast. (b) Retailers

in everyday purchase retail segments have negative or insignificant correlation between sales forecast

error and financial market return over the term of the forecast.

Further motivated by the above reasoning, we expect that, within each retail segment, retailers

with higher gross margin would have higher correlation with financial market return because such

retailers would be selling high-ticket items targeting the upper and premium market segments. The

demand for products in these segments would have a greater discretionary or luxury component.

Such demand could be high in periods of high economic growth. In periods of low economic growth,

demand could be depressed due to consumers putting off their purchases or substituting to lower

priced products carried by the same or other firms. Prices could also be depressed due to greater

markdowns of merchandize. Both these reasons would lead to a reduction in dollar denominated

sales. On the contrary, retailers with lower gross margin would benefit due to increase in demand

from consumers who would otherwise have bought products from higher-priced retailers. In this

reasoning, we use gross margin as a proxy for price. This assumption is justifiable in retailing

because this industry is very competitive. Competition implies that cost changes would be passed

on to consumers because abnormally high or low margins cannot be sustained for too long. Thus,

we test the following hypothesis:

Hypothesis 3 In each retail segment, retailers with higher gross margin have a higher correlation

between sales forecast error and financial market return over the term of the forecast.

7

The term of the forecast is a key variable in our model since uncertainty around the forecast

would increase with the term of the forecast. Hence, we look at how the term of the forecast affects

the correlation of sales forecast error with the return on the financial indicator. We expect that

when the forecast horizon is longer, the sales forecast error is more influenced by changes in the

economy. As the forecast horizon gets shorter, the economic uncertainty gradually gets resolved

but the idiosyncratic uncertainty associate with the firm doesn’t get resolved. Therefore, we expect

that the correlation coefficient should be high for long term forecasts and should decrease as the

forecast horizon gets shorter. Thus, we have:

Hypothesis 4 The correlation of sales forecast error with the financial market return increases

with the term of the forecast.

Hypotheses 2-4 focus on three potential predictors of the correlation coefficient between sales

forecast error and financial market return. The predictors are the type of product, the gross margin,

and the term of the forecast. Thus, the results of these hypotheses will be useful in determining

situations in which the correlation coefficient is high. In such situations, the correlation with the

financial market return will have greater impact on forecasting and decision-making in a firm.

The next section sets up the model to estimate the correlation of sales forecast error with

financial market return and thereby test the above hypotheses.

3. Estimation Methodology

3.1 Model

We develop a model of joint evolution of the financial market and the future sales for each company

for each year. Through this analysis, we construct two equations, one for estimating the parameters

of our model and testing the hypotheses, and another for updating forecasts using financial market

information. We omit the firm and year indices for convenience. We shall introduce these indices

later when we specify the estimation procedure and data. Suppose we are in time t = 0, we are

interested in the sales for the next fiscal year, that will start at time T1 and end at time T . Such

sales forecasts are issued by the experts ahead of the selling season. Let Dt, 0 ≤ t ≤ T , be the time

t value of information variable representing the sales realized over the next financial year. At time

8

Figure 1: Forecasting and demand realization timeline

T , DT equals to the actual realized sales D (see Figure 1). We assume that lnDt is a martingale,

that is,

E[ln(Dt)|Fs] = ln(Ds), 0 ≤ s ≤ t ≤ T,

where Ft represents the time t information. We assume that the martingale process is square

integrable. By the martingale representation theorem (Karatzas and Shreve 1991, Thm. 4.15 p.

182),

lnDt = ln D0 +∫ t

0σD(u)dBD(u),

which implies that

d(lnDt) = σD(t)dBD. (1)

Solving (1) gives us

Dt = D0 exp(σDBDt). (2)

The experts forecast the value of DT , which is a random variable. At time t, their forecast is

given by

Ft = E[DT |Ft],

where the length of the period T − t is the term of the forecast. Under this definition, Ft is also a

martingale. Indeed, when t > s, Ft ⊃ Fs and

E[Ft|Fs] = E [E[DT |Ft]|Fs] = E[DT |Fs] = Fs.

The martingale evolution of the forecast is widely assumed in the literature (e.g., Graves et al.

(1986), Heath and Jackson (1994)) and directly corresponds to the unbiasedness of the forecast.

9

Let the stochastic process {Mt} represent the evolution of the financial indicator. We assume

that Mt ∈ Ft. The evolution of Mt is given by

dMt

Mt= µMdt + σMdBM . (3)

The financial indicator can be the price of shares of a company or the value of a portfolio or a

composite market index. We discuss choices of the indicator in §3.2. For simplicity we consider an

one dimensional process {Mt}, but our derivation can be extended to allow {Mt} to be a vector

process.

We assume that {Dt} and {Mt} are correlated processes, that is,

dBDdBM = ρdt.

The coefficients ρ, µD and σD may vary across firms. The coefficients µM and σM relate to the

financial market and are common for all firms. We assume that the values of all these coefficients are

time-invariant. This assumption is made in order to derive a regression equation that is separable

in the term of the forecast. We test this assumption in Hypothesis 4 by estimating our model

independently for different time buckets for the term of the forecast.

Equation (3) has the following solution at time T :

MT = M0 exp(

µMT − 12σ2

MT + σMBM T

). (4)

Given that the financial index at time T has the value MT , we can find the conditional expec-

tation for the future sales. From (2), lnDT = ln D0 + σDBDT. We can derive the value of lnD0

from the experts’ forecast at time zero, F0 = D0 exp(σ2DT/2). Therefore,

E[lnDT |F0,MT ] = lnF0 −12σ2

DT + σDE[BDT|F0,MT ]. (5)

Also, from (4),

BM T =1

σM

(ln

MT

M0− (µM − 1

2σ2

M )T)

M= a.

From the joint normality of (BDT , BM T ),

(BDT , BM T ) ∼ N

µ1

µ2

,

σ11 σ12

σ21 σ22

= N

0

0

, T

1 ρ

ρ 1

.

10

Thus, the conditional distribution of BDT given BM T can be written as (BDT |BM T = a) ∼ N(µ̄, Σ̄),

where

µ̄ = µ1 + σ12σ−122 (a− µ2) = ρa, Σ̄ = σ11 − σ12σ

−122 σ21 = T − Tρ2.

Redefining MTM0

= 1 + r0T , we have the following expression for the conditional expectation in (5):

E[BDT|F0,MT ] =

ρ

σM

(ln(1 + r0T )−

(µM − 1

2σ2

M

)T

).

Finally,

E[lnDT |F0, ST ] = lnF0 +ρσD

σMln(1 + r0T ) + T

ρσD

σM

(−µM +

σ2M

2− σDσM

2ρ

). (6)

Equation (6) is the conditional expectation of the logarithm of sales. The second term in (6)

reflects how the return on the financial index affects the conditional expectation. The last term

reflects the dependency on the term of the forecast T and the volatility correction. The common

effect of the financial market on both these terms is proportional to ρσD/σM . If ρ = 0 the effect of

the financial market vanishes.

The conditional variance of the logarithm of sales is given by:

Var[lnDT |F0,MT ] = σ2DVar[BDT |F0,MT ] = σ2

DT (1− ρ2). (7)

Market information is valuable unless ρ = 0. If |ρ| = 1, we get a perfect forecast of sales once we

know the value of MT . For other values of ρ, the forecast error is partially explained by the return

on the financial indicator. We shall use equations (6) and (7) to estimate the parameters of our

model and test Hypotheses 1-4 regarding the value of ρ.

In reality, we would not know the financial market information all the way up to time T .

Suppose that we know the experts’ forecast F0 and the value of the financial index Mt at some

moment t > 0. Let 1 + r0t = Mt/M0. Then,

E[lnDT |F0,Mt] = lnF0 −12σ2

DT + σDE[BDT |F0, BM t].

Since BD is a martingale, E[BDT |F0, BM t] = E[BDt|F0, BM t] = ρσS

(ln(1 + r0t)− (µM − 1

2σ2M )t

).

Therefore,

E[lnDT |F0,Mt] = lnF0 +ρσD

σM

(ln(1 + r0t)−

(µM − 1

2σ2

M

)t

)− 1

2σ2

DT, (8)

11

and

Var[lnDT |F0,Mt] = σ2D(T − tρ2). (9)

This equation will be useful to update forecasts as we discuss in §6. It will also be useful for

evaluating the benefits of our model and testing whether forecast updates by experts incorporate

observed financial market returns. Note that the effect of volatility in (8) is proportional to the

term of the original forecast T since only partial information has been revealed through the price

of the financial indicator.

3.2 Estimation

We use two ways to estimate (6)-(7). First, we estimate model parameters directly from the ex-

pressions for the conditional mean (6) and variance (7) using the maximum likelihood estimation

(MLE) method. Then, we estimate (6)-(7) using a random coefficients regression model incorpo-

rating parameter heterogeneity and a general covariance structure for errors.

Each observation in our data set is a combination of a forecast by experts, corresponding actual

sales realization, term of the forecast, and corresponding financial market return. Let Fijy denote

the j-th sales forecast by experts for firm i for year y, Diy denote the actual sales realization for firm

i for year y, Tijy denote the term of the forecast corresponding to Fijy, and rijy denote the financial

market return over the time period represented by Tijy. Note that there are several forecasts each

year and Diy is constant for all forecasts j for a given firm-year. In this notation, we write (6)-(7)

as

lnDiy = a + b1 lnFijy +ρσD

σMln(1 + rijy) + Tijy(−

ρσD

σMµM +

12ρσDσM − 1

2σ2

D) + εijy,

where εijy ∼ N(0, σ2

DTijy(1− ρ2)), and intercept a and coefficient b1 are added as controls.

Let zijy(a, b1, ρ, σD) = lnDiy−a−b1 lnFijy− ρσDσM

ln(1+rijy)−Tijy(−ρσDσM

µM + 12ρσDσM− 1

2σ2D).

The likelihood of the observation is

f(εijy|Diy, Fijy, rijy, Tijy) =1√

2πσ2DTijy(1− ρ2)

exp(−zijy(a, b1, ρ, σD)2

2σ2DTijy(1− ρ2)

).

Suppose for now that the observations are independent. We maximize the log-likelihood function

12

with respect to model parameters ρ and σD and controls a and b1 subject to the constraint σD ≥ 0:

lnL(ρ, σD, a, b1|D,F, r,T) =∑i,j,y

ln f(εijy|Dijy, Fijy, rijy, Tijy)

= −12

∑i,j,y

[ln(σ2

DTijy(1− ρ2)) + ln 2π +zijy(a, b1, ρ, σD)2

σ2DTijy(1− ρ2)

]. (10)

We apply the MLE method to estimate firm-specific values of the parameters a, b1, ρ and σD. We

also apply it to various groups of firms to obtain pooled estimators of the parameters.

Our data set contains many experts’ forecasts of sales in each year for each firm, so that the

estimation errors across these forecast would be correlated with each other. We use a subsampling

and bootstrap method to solve the problem of such correlations affecting our parameter estimates.

Specifically, we draw one observation per firm per year without replacement, then estimate the

model and repeat the procedure. The asymptotic variance of the estimators is the variance of

the sample of estimates. Since the number of forecasts for a firm may vary across years, some

observations may be drawn more often then others. To address this issue, we conduct a weighted

MLE by assigning a weight to each observation proportional to the size of the firm-year subsample

from which the observation is drawn.

We use MLE as the primary method because it is asymptotically efficient, allows for direct

estimation of the parameters of the model, allows subsampling and bootstrap, and is fully parame-

terized by the conditional mean and variance. Alternatively to MLE, we can set up a regression

model from equation (6) as follows:

lnDiy = a + b1 lnFijy + b2 ln(1 + rijy) + b3Tijy + εijy. (11)

The advantage of this approach compared to MLE is that it allows us to estimate general covariance

structures for the error term. Its disadvantage is that it does not recognize the common parameters

in the coefficients b1 and b2 and in the variance of the error term.

Coefficients b2 and b3 can vary among firms due to differences in ρ and σD. Thus, we adopt the

random coefficients (RC) method for estimation of (11) by letting b2 = b̄2+δi and b3 = b̄3+γi, where

δi ∼ N(0, σ22), γi ∼ N(0, σ2

3). By this assumption, coefficients b2 and b3 are normally distributed

with means b̄2, b̄3 and standard deviations σ2, σ3. We allow for the random disturbances δi and γi to

be correlated, since coefficients for the same firm have common factors. The correlation structure

is estimated from the data.

13

Model (11) provides a parsimonious way to capture the heterogeneity in slope parameters when

the estimation is done on pooled samples (Greene (2003), Chapter 13). Model (11) can also be

augmented by including extra variables such as the forecast update from one forecast to the next

and lagged returns on the financial index. Thus, we use this model to compare our forecasting

method with forecast updates provided by equity analysts. We also use it to cross-check the MLE

estimates with the results of model (11), where the coefficients ρ and σD are derived from the

estimates of b̄2 and b̄3 and best linear unbiased predictors of δi and γi.

4. Data Description

We use data for US retailers listed on NYSE/NASDAQ/AMEX stock exchanges. We focus on the

retailing sector because retailing is immediate to the consumer demand so that the effect of the state

of economy on the consumer demand will be first observed through retail sales. The US Department

of Commerce assigns NAICS codes 44 and 45 to retailers. We obtained data for all firms with the

NAICS codes shown in Table 1. We excluded the NAICS codes for gas stations, used merchandise

stores, art dealers, manufactured (mobile) home dealers, tobacco stores, nonstore retailers, vending

machine operators, direct selling establishments, and fuel dealers. We included data for firms in the

electronic shopping segment (NAICS = 45411), mail order houses (NAICS = 454113), and florists

(NAICS = 45311) in the firm-wise estimation of parameters, but excluded them from segment-wise

and overall pooled estimation; the first two segments were excluded because they contain dissimilar

firms selling a wide spectrum of products, the third segment was excluded since florists are primarily

service firms that collect orders and network with local stores for execution.

We obtained sales forecast data from the Institutional Brokers Estimate System (I/B/E/S)

summary history file, actual sales revenue and other financial information from Compustat, and

prices of financial indicators from CRSP. I/B/E/S contains analysts’ forecasts of firm-level sales

for fiscal years 1997 onwards. Thus, this is the start date of our data set. Our data span the

fiscal years 1997-2007. For each fiscal year, there are multiple sales forecasts of varying terms made

by analysts. We consider all forecasts made 24 to 12 months before the fiscal year-end date. All

databases were accessed through Wharton Research Data Services (WRDS).

For the firms and time-periods defined above, we obtained data on three variables from the

I/B/E/S summary history file, MEANEST, the mean forecast of sales made by equity analysts,

14

STATPERS, the corresponding forecast date, and NUMEST, the number of analysts included in

the mean. From the Compustat annual files, we obtain yearly sales revenue, cost of goods sold, and

inventory data. Using CRSP, we obtain prices of three composite indices: S&P 500 Index, Equal

Weighted Market Index, and Value Weighted Market Index. The returns on the three indices

are correlated, with the highest correlation of 0.981 between the S&P 500 and the Value Weighted

Market Index. Estimation results are consistent for each choice of the index. The results we present

in the paper are based on the Value Weighted Market Index. This index is a composite of the value

weighted prices and dividends of all stocks traded at the NYSE, the AMEX, and the NASDAQ.

To estimate µM and σM , we use the mean and standard deviation of historical daily returns from

the period 1996-2007, which yields annualized estimates of µM = 0.078 and σM = 0.193 (see Hull

(1993), Chapter 10).

Our initial data set retrieved from I/B/E/S contained 13,798 observations for 265 different firms,

as identified by their unique CUSIP codes. We applied several filters to clean these data. First,

firms with more than 40% deviation of actual sales from the first forecasted value were excluded

as they represented potential mergers or acquisitions. Second, we excluded companies with fewer

than three years of data in Compustat since we use subsampling. There were 209 firms left after

these two filters. We then excluded firms that were covered by fewer than three analysts, firms with

inventory less than 2% of the sales revenue, firms with sales revenue less than 5M$, and overseas

firms traded on US stock exchanges via American Depositary Shares (ADS).

After applying all the above filters, our final data set contains 97 firms. The total number of

observations is 4,698, and since there are multiple forecasts per firm-year, the unique number of

firm-year pairs is 570. The average number of forecasts per firm-year is 8.24. Observations in the

data set represent 36.4% of the total annual U.S. retail sales excluding motor vehicles and parts

dealers in the year 2005 according to the U.S. Census Bureau’s Annual Retail Trade Survey. Table

1 shows descriptive statistics of our data set.

5. Results

Hypotheses tests. We first discuss tests of Hypotheses 1-4 using the estimates of ρ from pooled,

segment-wise and firm-wise MLE. Table 2 presents the results for testing Hypotheses 1-2. The first

four columns present various pooled and segment-wise estimates of the parameters of (10). The

15

final three columns present summary statistics of firm-wise MLE estimates for ρ. Detailed MLE

results for all firms are included in the online appendix.

Hypothesis 1 is based on the reasoning that total consumption is positively correlated with the

contemporaneous financial market return. Since the hypothesis is based on total consumption, we

test it using a pooled estimate of the correlation coefficient ρ for all firms in our data set. The

pooled estimates can be interpreted as the means of ρ and σD across the various firms in our

data set. Since we use subsampling and bootstrap in MLE, these are weighted means, with the

weight of each firm-year being equal to the number of forecasts available for that firm-year. The

estimation results, shown in the first row of Table 2, are that ρ̂ = 0.170 (standard error = 0.020)

and σ̂D = 0.075 (standard error = 0.001). Both estimates are statistically significant at p=0.01.

Thus, Hypothesis 1 cannot be rejected based on this evidence. This inference is also consistent

with the median of the firm-wise estimates of ρ. The median is 0.1960, the minimum is -0.9934

(Great Atlantic and Pacific Tea Co.) and the maximum is 0.9550 (Officemax Inc.). The range of

variation between the minimum and the maximum is striking. We characterize this variation by

showing how it is explained by segment classification, gross margins, and presence of outliers.

To test Hypothesis 2, we classify the thirteen retail segments into two groups, discretionary

purchase and everyday purchase. The discretionary purchase group is composed of the six segments,

home furnishings stores, consumer electronics stores, home improvement stores, apparel stores,

jewelry stores, and department stores; and the everyday purchase group consists of the seven

remaining segments. We base this classification on the median gross margin of each segment shown

in Table 1 and on our subjective assessment of the types of products sold by retailers in each

segment. For example, jewelry, home furnishings, and home improvement stores can be expected

to have a higher component of sales from discretionary purchase items, and discount stores to have

a lower component of sales from discretionary purchase items.

Table 2 shows the estimation results for Hypothesis 2. First, note that the pooled estimates of

ρ for the discretionary purchase and everyday purchase groups are 0.1938 and 0.1153, respectively.

Using a paired t-test, the difference between them is statistically significant at p = .05, supporting

Hypothesis 2. Thus, the discretionary purchase retailers have a higher value of ρ than the everyday

purchase retailers.

Now consider the segment-wise estimates. The highest estimate of ρ is 0.8264 for the office

16

supplies stores. While we classified this segment in the everyday purchase group, the outcome is

intuitive since the customers of office supplies stores tend to be small businesses, whose needs will

be closely linked to the financial market return. The large magnitude of this estimate shows the

usefulness of incorporating financial market returns in sales forecasting for this segment. The second

highest value of ρ is 0.6075 for jewelry retailers. The other segments with high estimates of ρ are

home improvement, supermarkets, pharmacies, and apparel. All these estimates are statistically

significant at p = .01.

Home furnishings, consumer electronics, and department stores were classified in the discre-

tionary purchase group, but have estimates of ρ insignificant or lower than everyday purchase

segments. This is due to the presence of outliers as we discuss in the next paragraph. The remain-

ing segments with low estimates of ρ are everyday purchase segments: auto parts and accessories,

shoe stores, sports and hobby stores, and discounters and wholesale clubs.

The firm-wise estimates of ρ are useful since they show segments for which firm-wise estimates

are consistent with segment-wise estimates, and those in which we have outliers. In the office

supplies segment, there are three firms with ρ̂ = 0.85, 0.95, and 0.96, and median = 0.95. Thus,

the segment-wise estimate is consistent with the firm-wise estimates. In jewelry retailers, there are

four firms, with estimates of ρ as 0.87, 0.29,−0.69, and −0.93. The last two firms were assigned to

the jewelry segment by us due to the nature of their products. They are internet-based retailers

of customized luxury gifts. Thus, the firm-wise median of ρ differs from the segment-wise estimate

for jewelry retailers due to the presence of outliers.1 In home furnishings, one firm is an outlier,

Pier 1 Imports Inc., with ρ̂ = −0.68, while all other firms have positive estimates of ρ. Likewise,

in consumer electronics, Tweeter Home Entertainment Group is an outlier with ρ̂ = −0.64, while

all other firms have ρ̂ > 0.41. In discounters and wholesale clubs, we see that the segment can be

divided into two parts. Wholesale clubs such as BJ’s and Costco have large positive estimates of ρ,

whereas discounters such as Wal-Mart and Target have ρ close to zero. One can argue that these1This difference occurs because the firm-wise median treats each firm as having equal weight, whereas the segment-

wise pooled estimate gives higher weight to firms with more annual observations. For jewelry segment, our data set

has many more observations for Tiffany & Co. (ρ̂ = 0.87) and Zale Corp. (ρ̂ = 0.29) than the remaining two,

internet-based, retailers. Our methodology can be easily replicated to compute pooled estimates that assign equal

weights to all firms. Which weighting is more accurate depends on the outlier firms in a sample. Alternatively, one

may use firm-wise estimates shown in the online appendix.

17

retailers sell different kinds of products, with the wholesale clubs selling much more of durable

goods, which are discretionary purchase items, and discounters selling a larger fraction of everyday

purchase items, whose demand would be less correlated with the financial market return.

We find that a possible explanation for outlier firms is sales coming below analysts’ forecast

consistently year after year. For example, Tweeter Home Entertainment Group, experienced un-

expected sales declines over several years which resulted in March 2007 closing of 49 stores. Pier 1

Imports has similarly shown sales below expectations from 2005 through 2007 due to competitive

pressure, unfavorable exchange rate movements, and change in customer tastes. Therefore, when a

retailer has unexpected sales declines, we may see negative sales forecast errors, and thus, negative

values of ρ even when the economy is doing well. A possible use of our model is to detect such

outliers, since the model can be used to construct confidence intervals for parameters as well as

forecasts.

To test Hypothesis 3, we further classify firms in each segment into high and low gross margin

subgroups. Since we have panel data, we classify firms in two ways, static and dynamic. In the

static classification, we compute the median gross margin of each firm across its annual observations

and the median gross margin of each segment across all the firm-year observations in that segment.

We classify firms into high- and low- gross margin groups by comparing their medians with their

segment medians. For example, if the median gross margin for Best Buy Co. falls below the median

for the consumer electronics segment, then Best Buy would be classified in the low gross margin

group for each observation. In the dynamic classification, we classify firm-years into high- and low-

gross margin groups by comparing the gross margin of each firm in each year with the segment

median for that year. We classify observations for a firm in year y by comparing its gross margin

in year y − 1 with the median gross margin of its segment for year y − 1. For example, in this

method, Best Buy could be classified as a high margin retailer in one year and a low margin retailer

in another year. The static classification has the advantage of being less susceptible to noise in

the estimation of gross margin, whereas the dynamic classification has the advantage of capturing

relative changes in gross margin over time. Results for the static classification are shown in Table

3. Results for the dynamic classification are similar and are shown in the online appendix.

In Table 3, first consider the pooled estimates of ρ for high- and low- gross margin firms

across all segments as shown in the first row. The estimates are 0.192 and 0.133, respectively,

18

and the difference between them supports Hypothesis 3 at p=0.01 according to a paired t-test.

The estimates for different segments show that 8/13 segments have estimates of ρ consistent with

Hypothesis 3, 4/13 are significant in the reverse order, and 1/13, office supplies stores, has no

statistical difference between high and low margin groups. Thus, the result of the hypothesis test

is statistically significant at the aggregate level, but varies across segments. This variation may

possibly be due to the presence of outliers or small sample sizes in some segments. There may also

be classification errors for firms whose gross margin values are close to the median. In the case of

office supplies stores, both high- and low-gross margin groups have large estimates of ρ, 0.95 and

0.91, respectively.

Hypothesis 4 states that the magnitude of the correlation coefficient can depend on the term

of the forecast. To test this hypothesis, we split the observations into three time-buckets according

to the term of the forecast, namely, short (12-15 months), medium (16-19 months) or long (20-24

months) term forecasts. The time buckets have different number of observations because there

are fewer long-term forecasts than short-term forecasts available in the data set. However, the

industry composition within each bucket is approximately the same, allowing us to compare the

results fairly.

Table 4 presents the estimation results. As the term of the forecast increases, estimates of

the correlation coefficient ρ increase from 0.10 for short term to 0.30 for long term forecasts.

Monotonically increasing correlation coefficient ρ suggests that as the term of the forecast increases,

a larger percent of forecast error can be predicted by financial market returns. This result supports

Hypothesis 4. It implies that forecast updating based on our model is more suitable for longer term

forecasts.

Volatility estimates. Our model predicts not only the mean forecast, but also the volatility of

the forecast. This feature is useful for building confidence intervals and planning against uncertainty.

Table 2 reports the pooled and segment-wise estimates of σD. The pooled estimate is 0.075,

significant at p = .01. Retailers in the discretionary purchase group have higher volatility of sales

(σ̂D = 0.085) compared to those in the everyday purchase group (σ̂D = 0.057). From (6), the effect

of financial market return on mean sales is proportional to the product ρσD, thus, the higher the

volatility of sales the higher is the exposure of sales to the financial market return. Among retail

segments, apparel stores have the highest estimate of sales volatility (σ̂D = 0.097) followed by office

19

supplies (σ̂D = 0.092) and consumer electronics (σ̂D = 0.086). Pharmacies have the lowest estimate

of sales volatility (σ̂D = 0.035), followed by home improvement stores (σ̂D = 0.041) and discounters

and wholesale clubs (σ̂D = 0.047). Table 3 reports the variation in σ̂D with gross margin. The

pooled estimates of σD are 0.084 and 0.063 for high and low margin firms, respectively. These

estimates as well as segment-wise estimates for 10/13 segments show that high gross margin firms

have higher volatility than low margin firms. Table 4 reports the variation in σ̂D with the term

of the forecast. The estimates remain around 0.075 for all three time buckets. Constant volatility

across time buckets implies that the variance of the forecast error is linear in time, which supports

the assumption used in deriving our model. In summary, the instantaneous volatility of the forecast

is more for discretionary purchase than everyday purchase retailers. It is also more for high gross

margin retailers than low gross margin retailers. However, it is the same for forecasts of different

terms, ceteris paribus.

Comparison of MLE and RC models. Finally, we present a comparison of estimates obtained

by MLE and RC models. The RC model, (11), gives best linear unbiased predictions (BLUPs) of

the coefficients on financial market return (b2) and the term of the forecast (b3) for each firm. We

also compute these coefficients from firm-by-firm MLE estimates for ρ and σD using (6). Figure 2

plots the estimates obtained by these two models against each other. We observe that the results

for b2 are consistent across the two models. It is, however, difficult to draw a conclusion for the

estimates of b3. Computed by the RC model, they exhibit higher variation than the MLE estimates.

This is not surprising since the confidence interval for b3 is wider in relative terms than that for b2,

suggesting a larger variation in the results for b3.

We also used the RC model to test Hypotheses 1-4 using the estimate for the coefficient of

ln(1 + rijy) in (11). All these results were consistent with those obtained using MLE. In a previous

version of this paper, we tested the hypotheses on a larger data set containing 214 firms, since we

did not apply all the data filters reported in §4. The results on this larger set were also consistent

with those reported in this paper, and the estimates of ρ and σD were similar.

20

6. Comparison with Analysts’ Forecasts

Equations (8)-(9) can be used to update a previous sales forecast and its variance as the price

information for the financial indicator is revealed with the passage of time. Likewise, equity analysts

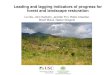

also update their forecasts over time. Figure 3 presents an example of these forecast updates for

an apparel retailer, Limited Brands, for fiscal year 2006. It shows the initial analysts’ forecast,

made 23 months before the fiscal year-end date, the periodic updates to this forecast, the forecasts

computed by our model using as input the initial analysts’ forecast and the financial market return,

and the actual sales realization. Notice that, in this example, our model forecast progressively grew

more accurate with time, whereas the experts’ forecast diverged.

In this section, we compare our forecast updates with those of equity analysts to address three

questions: Do equity analysts incorporate financial market returns in their forecast updates? Does

our model provide new information that augments the forecast updates by equity analysts? Do

the updates by equity analysts contain new information not contained in our model? We answer

these questions in the affirmative, thus showing that both financial market returns and updates by

equity analysts contain unique information useful for sales forecasting. Finally, we show that using

our model to augment the forecasts by equity analysts improves forecast accuracy.

The regression models used in this section are modifications of equations (8) and (11). All

models are estimated using ordinary least squares as well as the RC method summarized in §4.2.

We use all the observations in our data set for estimation except the first observation in each firm-

year, since the first forecast by equity analysts is used as input in our model. In other words, the

regression models in this section deal with forecast updates represented by observations (i, j, y) for

all j 6= 1.

To address the first question, we use (8) to set up a new regression model as follows:

lnFijy − lnFi1y = a + b1 ln(1 + r̂ijy) + b2tijy + b3Ti1y + εijy, j 6= 1. (12)

Here, Fijy and Fi1y are the j-th and first forecasts for firm-year (i, y), tijy is the time interval

between Fijy and Fi1y, r̂ijy is the return on the financial indicator for this time interval, εijy is the

error term, and a, b1, . . . , b3 are added as controls. Thus, the dependent variable in this model is

the consensus forecast update made by equity analysts, and the explanatory terms are the financial

market return and term of forecast variables from our model. Whereas in (8), we specified forecast

21

updating at the intermediate time instant t according to our model, in (12), we determine if the

forecast updates by equity analysis at the same time instant incorporate historical financial market

returns. Therefore, we are interested in testing the hypothesis whether b1 in (12) is positive.

For the second question, we regress actual sales on the forecast provided by equity analysts and

the update provided by our model. The regression model for this test is an extension of (11) as

follows:

lnDiy = a + b1 lnFijy + b2 ln(1 + rijy) + b3Tijy + b4 ln(1 + r̂ijy) + b5tijy + εijy, j 6= 1. (13)

Here, the dependent variable is the sales realization for firm i in year y, and the explanatory

variables are the experts’ updated forecast, Fijy, the financial market return over the term of

the forecast, rijy, lagged financial market return over the time period from the first forecast to

the updated forecast, r̂ijy, the time elapsed since the first forecast, tijy, and the term of the first

forecast, Ti1y. Note the similarity between this equation and (11); this equation augments (11) with

lagged financial market return and time elapsed since the first forecast because these two variables

are used by our model to update forecasts. The equity analysts know the lagged financial return,

r̂ijy, at the time of making their updated forecast, Fijy. Hence, by putting both variables together

in the regression equation, we test if our model provides information that augments the forecast

updates by equity analysts, i.e., if the coefficient b4 is positive.

To answer the third question, we modify (11) differently from above.

lnDiy = a+b1 lnFmijy+b2 ln(1+rijy)+b3Tijy+b4(lnFijy−lnFi1y)+b5tijy+εijy, j 6= 1. (14)

Here, Fmijy is our model forecast obtained from (8) using as inputs forecast Fi1y, the return on

the market index r̂ijy over the time-period from the first to the updated forecast, and firm-wise

estimates of parameters ρ and σD. We are interested in testing whether coefficient b4 is positive,

i.e., whether the forecast update provided by equity analysts has value beyond the forecast provided

by our model.

Table 5 shows the results of the above three models. From columns (1-2) corresponding to

(12), we find that the estimate for the coefficient of ln(1 + r̂ijy), b1, is 0.0321 using OLS estimation

and 0.0181 using the RC method. While both estimates are positive and the OLS estimate is

statistically significant at p=.01, the RC estimate is not. Thus, we obtain only a weak evidence

that equity analysts incorporate financial returns in their forecast updates. From columns (3-4)

22

corresponding to (13), we find that the coefficient of ln(1 + r̂ijy), b4, is statistically significant at

p=0.01 under both OLS and RC methods. Its estimates are 0.0872 and 0.0891, respectively. This

shows that our model provides information not incorporated by equity analysts in their updated

forecasts. The remaining coefficients in this model are as expected: the experts’ updated forecast,

lnFijy, is significant at p=0.01 with a value close to 1, and the financial market return over the

term of the forecast, ln(1+ rijy), is also significant at p=0.01. Finally, columns (5-6) corresponding

to (14) show that the model forecast lnFmijy, the experts’ forecast update, lnFijy − lnFi1y, and the

financial market return over the term of the forecast, ln(1 + rijy), are all positive and significant at

p=0.01.

In summary, we see that the financial market return and the forecast updates by equity analysts

both contain unique information useful for forecasting. The result about financial market returns

particularly is surprising since they are public information at the time when equity analysts update

their forecasts. Among other things, this result implies that these two information sources can be

used together to construct a combined forecast that should be more accurate than either of them.

We can compute the combined forecast by using (15) and replacing the initial experts’ forecast

with the updated experts’ forecast. We denote the combined forecast as F cijy and define it as

lnF cijy ≡ lnFijy +

ρσD

σM

(ln(1 + r̂ijy)−

(µM − 1

2σ2

M

)tijy

)− 1

2σ2

DTi1y, j 6= 1.

Note that the experts’ updated forecast Fijy replaces the initial forecast Fi1y in this equation. The

rest of the parameters are as in (8). Similarly to (14), we use the firm-wise MLE estimates of

parameters to compute the forecast.

Table 6 compares the forecast accuracy of the experts’ initial forecast Fi1y, the experts’ updated

forecast Fijy, the model’s updated forecast Fmijy, and the combined forecast F c

ijy for each segment.

As noted before, we compare predictions for each observation in the data set except the first one for

each firm-year since the first one is used an input in our model. For each forecast series, we use root

mean squared error (RMSE) as the performance measure. To account for heteroscedasticity, we

first compute percentage forecast errors for all observations, then segment-wise or firm-wise RMSE.

Table 6 shows the segment-wise RMSE. From the column (M/E), we observe that the RMSE values

are larger on average for our model than for the updated forecasts by equity analysts. Thus, the

equity analysts are on average more accurate than our model. This is to be expected since our

model uses information on only one financial indicator whereas equity analysts have access to a

23

much larger information set.

We also observe from the column (M/E0) that the RMSE of model forecast errors are on

average smaller than RMSE of errors of the initial analysts’ forecasts. This is consistent with

previous regressions, and shows that the updates computed by our model are useful in improving

forecast accuracy. Likewise, column (C/E0) shows that the combined forecast is on average better

than the experts’ initial forecast for each segment. The magnitude of improvement here is larger

than seen in (M/E0) since the combined forecast uses updated inputs from both the equity analysts

and the model. Finally, column (C/E) shows that the ratio of RMSE of the combined forecasts

to the RMSE of updated analysts’ forecasts is 0.9969 across all observations. Thus, the combined

forecast is more accurate than the experts’ updated forecast on average. We also observe from the

segment-wise values that the combined forecasts are more accurate on average than the analysts’

updated forecasts for 10/13 segments.

We investigate the reasons for performance differences between the forecasting methods, and

find that there are two possible reasons: the magnitude of ρ, and whether experts incorporate

historical financial returns in their forecasts. First, in comparing the ratio (M/E) across firms and

segments, we see that the model forecasts are closer to the experts’ forecasts for segments with

large magnitudes of ρ, such as electronics stores, jewelry stores, department stores, discounters and

warehouse clubs, and office supplies stores, with the exception of some outlier firms. Second, note

that the (C/E) ratio was greater than one for three segments, jewelry stores, sports and hobby

stores, and office supplies stores. This result is as expected for sports and hobby stores, since they

have a small and insignificant value of ρ in Table 2, but not for jewelry stores and office supplies

stores which have the highest values of ρ across all segments. To investigate this result, we regressed

model (13) individually for each segment. We found that past return was not significant for all

three segments where the combined forecast could not improve over experts. On the contrary, the

coefficient on past return was statistically significant for the remaining ten segments. This might be

an indication that for jewelry stores and office supplies stores, experts do incorporate the financial

information in their updates.

In the online appendix, we present forecast accuracy comparisons between the model and the

experts for each firm. The M/E ratio varies across firms from 0.68 to 1.98, with a median of 1.17.

Thus, for half the firms, the model’s RMSE is at most 17% worse than the analysts’ RMSE. The

24

M/E0 ratio ranges from 0.68 to 1.34, with a median of 0.99. The combined forecast has C/E ratio

ranging from 0.86 to 1.54 with a median of 1.0, and C/E0 ratio ranging from 0.47 to 1.21 with a

median of 0.88. Finally, we note that the performance of our model and combined forecasts could

be improved further based on the results of our hypotheses tests. For example, one could modify

the estimate of ρ based on the term of the forecast and the gross margin of a firm. One could also

remove outlier firms that consistently had sales below forecasts and yielded large negative estimates

of ρ.

7. Discussion

We presented a model in which sales forecast error is a function of the state of the economy

characterized by the return on a financial index. We tested this model using firm-level total annual

sales forecasts and financial data for public US retailers in several NAICS groups for the period

1997-2007. The pooled estimate for the correlation coefficient is positive and statistically significant.

Firms in different retail segments have different correlation coefficients, varying from 0.95 for office

supplies stores to insignificant or negative for some other segments. Within a retail segment, the

correlation coefficient increases with gross margin on average. It also increases with the term of

the forecast. Our model provides results on other parameters for forecasting as well, such as the

volatility of sales forecast error and the adjustment for drift rates. Together, these results can

be applied for forecast updating. We showed that forecast updates from our model provide new

information not contained in the forecast updates by equity analysts. Hence, a combination of

these two inputs has higher average forecast accuracy than equity analysts. This result is most

useful for firms with high correlation coefficients.

Beyond forecast updating, our model can be applied for risk management, calculating the value

of decision postponement, and planning other operational decisions. Several recent research papers

have discussed financial hedging based on demand being correlated with the price of a traded asset.

The correlation information obtained from our model can be used to inform such hedging decisions,

and shows that its value varies depending on the retail segment, the gross margin of a firm, and

the time horizon.

Alternatively, retailers may use operational hedging strategies of at least four types: multiple

25

store formats, flexibility in product assortments, price markdowns, and risk sharing with suppliers.2

Multiple store formats are used by many retailers and provide natural hedging. For example,

Nordstrom Stores and Saks Inc., both high-end retailers, have outlet store chains targeted at a

lower end of the market. High values of ρ for their premium stores will be moderated by low

values of ρ for their outlet stores. Wal-Mart Stores has a discount store chain, with small ρ,

and a warehouse club, with large ρ. Other examples include Gap Stores Inc., Brooks Brothers,

etc. An example of flexibility in product assortment is presented by Tiffany’s, which sells both

high priced and low priced jewelry, and manages changes in demand by customers substituting

downwards or upwards under different market conditions. Some retailers may be unable to utilize

natural hedges if their product market is too focused, for example, office supplies stores or other

category killers. Such retailers may benefit more from price markdowns and risk sharing with

suppliers, both of which have been widely studied in the operations management literature. Thus,

operational hedging methods enable retailers to manage the risk caused by demand for different

products being variously correlated with financial market indicators.

Our model can be used to quantify the value of decision postponement. Long term company-

wide decisions will have greater benefit from our model because they are based on aggregate fore-

casts and because financial information carries more value for updating long term forecasts. Exam-

ples of such decisions include production of retailer’s private brand products, procurement of raw

materials (e.g., fabric procurement for a fashion retailer), and reservation of logistics capacity; see

Swaminathan and Lee (2003) for a comprehensive discussion. The value of postponement generally

comes from two sources: an increase in expected profit, and a decrease in the variance of profit.

It can easily be shown for our model that increase in expected profit through decision postpone-

ment is more for firms with higher correlation and greater demand volatility. The reduction in

profit variance depends mostly on the extent of correlation between the sales forecast error and the

financial market return, and is less sensitive to the magnitude of demand volatility.

Besides the above applications, our model shows that retailers face a spectrum of different

degrees of market risk as quantified by ρ. During a period of growth, a firm may be tempted to

make long-term investments in expanding or changing its product portfolio or market position, only

to find this investment become risky later on. By quantifying the value of ρ for different markets2Van Mieghem (2008: p.333) presents a generic classification of four types of operational hedging strategies. Our

discussion focuses on specific examples of these four types for retailers.

26

and types of firms, our model helps identify the risks faced by firms in such decisions. Our results

are particularly useful here since they are based on a data set that includes two periods of high

growth, 1997-99 and 2002-05, and two periods of low growth, 2000-01 and 2006-07.

Our paper has some limitations that can be addressed in future research. One limitation is that

we assume sales forecast to evolve as a martingale. In practice, forecast updates by analysts may not

conform to this assumption. This does not affect our model since we use the analysts’ forecast as an

initial input and do updates only using financial market indicators. However, this assumption might

become important if updates are based on both financial and firm-specific data. Second, after the

issuance of a forecast, a firm may take decisions regarding prices, product assortment, and supply

chain that can change the correlation coefficient with financial market returns. For example, we

found the correlation coefficient to depend on the term of the forecast. This finding presents an

opportunity for future research incorporating firms’ decisions in the forecasting model. In this

respect, our model could be extended to a multi-period formulation and estimated on within-firm

product-level data. Third, we believe that results similar to ours can be found in upstream layers

of the supply chain, e.g., in manufacturing or wholesale distribution. The empirical investigation

of this phenomenon and the study of its applications to supply chain models would be valuable.

References

Ando, A., F. Modigliani. 1963. The” Life Cycle” hypothesis of saving: aggregate implications and tests. The

American Economic Review 53(1) 55–84.

Banks, J., R. Blundell, A. Lewbel. 1997. Quadratic engel curves and consumer demand. The Review of

Economics and Statistics 79(4) 527–539.

BBC. 1999. Business: The economy us retail sales boom. BBC, 03/11/1999, retrieved on 11/29/2007 .

Business Week. 2001. September retail sales drop stuns street. Business Week, Standard & Poor’s Global

Markets , 10/12/2001 retrieved on 11/29/2007.

Caldentey, R., M. Haugh. 2006. Optimal control and hedging of operations in the presence of financial

markets. Mathematics of Operations Research 31(2) 285.

Chen, X., M. Sim, D. Simchi-Levi, P. Sun. 2007. Risk aversion in inventory management. Operations

Research 55(5) 828.

27

Chod, J., N. Rudi, J. Van Mieghem. 2007. Operational flexibility and financial hedging: complements or

substitutes? Working paper .

Dixit, A.K., R.S. Pindyck. 1994. Investment under uncertainty . Princeton University Press Princeton, NJ.

Dynan, K.E., D.M. Maki. 2001. Does stock market wealth matter for consumption? FEDS Discussion Paper

No. 2001-23 .

Friedman, M. 1957. A theory of the consumption function. Princeton University Press.

Gaur, V., S. Seshadri. 2005. Hedging inventory risk through market instruments. Manufacturing & Service

Operations Management 7(2) 103–120.

Graves, S.C., D.B. Kletter, W.B. Hetzel. 1998. A dynamic model for requirements planning with application

to supply chain optimization. Operations Research 46 S35–S49.

Graves, S.C., H.C. Meal, S. Dasu, Y. Qiu. 1986. Two-stage production planning in a dynamic environment. in

Multi-stage Production Planning and Control, Axsater, S., Schneeweiss, C., Silver, E. (eds). Springer

Verlag, Berlin.

Greene, W.H. 2003. Econometric analysis. Prentice Hall, Upper Saddle River, NJ.

Heath, D. C., P. L. Jackson. 1994. Modeling the evolution of demand forecasts with application to safety

stock analysis in production/distribution systems. IIE Trans. 26(3) 17–30.

Hong, H., W. Torous, R. Valkanov. 2007. Do industries lead stock markets? Journal of Financial Economics

83(2) 367–396.

Hull, J. 1993. Options, futures, and other derivative securities. Prentice Hall, Upper Saddle River, NJ.

Karatzas, I., S. Shreve. 1991. Brownian motion and stochastic calculus. Springer, New York, NY.

Kaufman, L. 2001. Empty aisles and empty stores; what happens when anchor stores weigh anchor? The

New York Times, 02/06/2001, retrieved on 11/29/2007 .

Menzly, Lior, Oguzhan Ozbas. 2006. Cross-industry momentum. SSRN eLibrary .

Poterba, J.M. 2000. ” Stock Market Wealth and Consumption”. Journal of Economic Perspectives 14(2)

99–118.

Reuters. 2007. Office depot falls on gloomy forecast. Reuters, 09/07/2007, retrieved on 11/29/2007 .

Sapra, A., P.L. Jackson. 2005. The martingale evolution of price forecasts in a supply chain market for

capacity. Tech. rep., Working paper, Cornell University.

Swaminathan, J.M., H.L. Lee. 2003. Design for postponement , Handbooks in Operations Research and

Management Science, vol. 11. Elsevier Publishers.

Van Mieghem, J.A. 2003. Commissioned paper: capacity management, investment, and hedging: review and

recent developments. Manufacturing & Service Operations Management 5(4) 269–302.

28

Van Mieghem, J.A. 2008. Operations Strategy: Principles and Practice. Dinesystems.

29

30

Figure 2. Scatter plots of the coefficients b2 and b3 computed using MLE estimates and best linear unbiased predictors of the RC model.

Figure 3. Comparison of the initial forecast, the forecast updates generated by analysts and by the model, and the actual sales for Limited Brands, Inc., for fiscal year 2006.

b 2, (ln(1+r))

-1

-0.5

0

0.5

1

-1 -0.5 0 0.5 1

WMLE

RC

_BL

UP

b 3, (T)

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2

-0.2 -0.15 -0.1 -0.05 0 0.05 0.1 0.15 0.2

WMLE

RC

_BL

UP

Limited Brands (rho=0.80), FY 2006

9800

9900

10000

10100

10200

10300

10400

10500