Embed Size (px)

Citation preview

1

SAGCOT Center LtdTanzania Investment Opportunities

May, 2016

2SAGCOT Centre Ltd. 2

Overview of the Tanzania Investment Landscape

Introduction to SAGCOT

Overview of Ihemi cluster and key value chain opportunities

3

Overview of the Tanzania Investment Landscape

Opportunities in Agribusiness

Agricultural processing

Tanzania is the third largest country by area inthe region and there is ample arable land.Significant opportunity exists in:

Post-harvest marketing

Infrastructure (warehousing, cold storage, transport)

Tanzania has become an attractive investment destination, due to it’s political stability and steady economic growth. Agribusiness holds much investment potential.

Tanzania as an investment destination1

• Politically stable

• Steady economic growth in recent years(average 8% GDP rise)

• Less competitive investment markets thanUganda and Kenya

Investor profile to be well positioned for theTanzanian market

• Flexible investment criteria

• Local presence

• Technical assistance facilities for pipelinebuilding.

1. GIIN/ Open Capital https://thegiin.org/assets/documents/pub/East%20Africa%20Landscape%20Study/07Tanzania_GIIN_eastafrica_DIGITAL.pdf

Inputs production

4SAGCOT Centre Ltd. 4

Overview of the Tanzania Investment Landscape

Introduction to SAGCOT

Overview of Ihemi cluster and key value chain opportunities

5

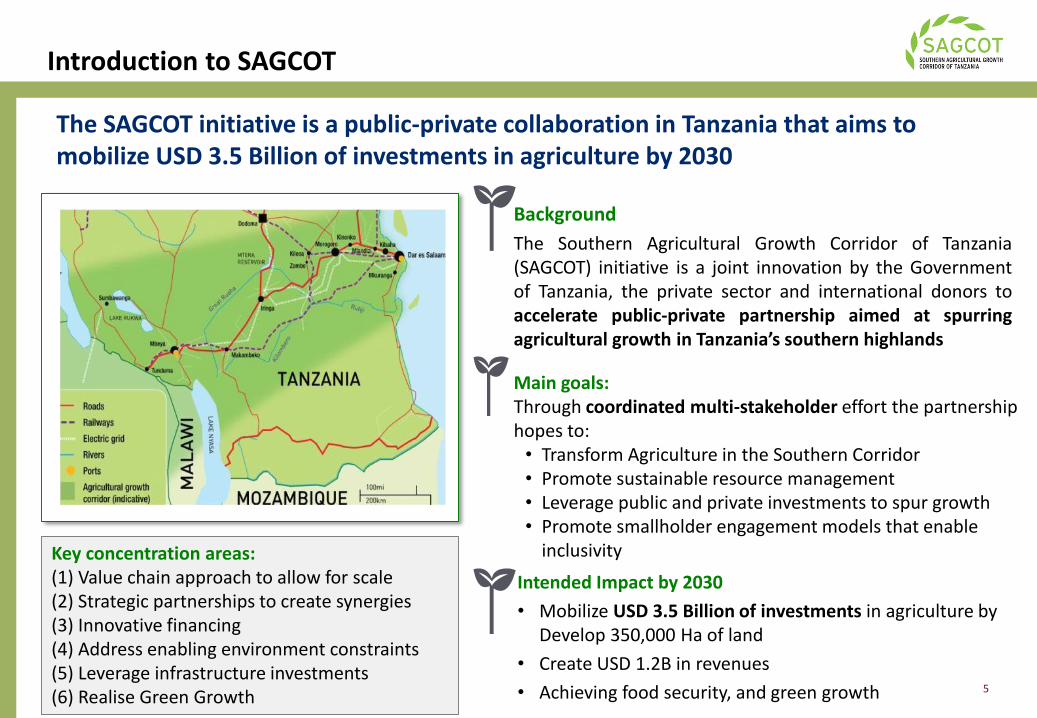

The SAGCOT initiative is a public-private collaboration in Tanzania that aims to mobilize USD 3.5 Billion of investments in agriculture by 2030

Background

The Southern Agricultural Growth Corridor of Tanzania(SAGCOT) initiative is a joint innovation by the Governmentof Tanzania, the private sector and international donors toaccelerate public-private partnership aimed at spurringagricultural growth in Tanzania’s southern highlands

Main goals:Through coordinated multi-stakeholder effort the partnership hopes to:• Transform Agriculture in the Southern Corridor• Promote sustainable resource management• Leverage public and private investments to spur growth• Promote smallholder engagement models that enable

inclusivityKey concentration areas:(1) Value chain approach to allow for scale(2) Strategic partnerships to create synergies(3) Innovative financing (4) Address enabling environment constraints(5) Leverage infrastructure investments(6) Realise Green Growth

Introduction to SAGCOT

Intended Impact by 2030

• Mobilize USD 3.5 Billion of investments in agriculture by Develop 350,000 Ha of land

• Create USD 1.2B in revenues

• Achieving food security, and green growth

6

23 Southern Agricultural Growth Corridor of T anzania

Figure 3.1 Agricultural potential and backbone infrastructure

SAGCOT’s backbone infrastructure provides a

reasonable but incomplete platform upon which

to develop commercial agriculture in the southern

corridor. The majority of infrastructure was built after

Tanzanian independence as an alternative to the South

African and M ozambican transport links to Zambia,

and includes:

• the Port of Dar es Salaam, which currently handles

approximately eight million tonnes per year,

• the Tanzania-Zambia Railway Authority (TAZARA)

network of 1,870km of rail, commissioned in 1976

to link Dar es Salaam Port to Kapiri M poshi and

then to the Zambian Railways (and the DRC and

Southern African rail networks),

• The Tanzania-Zambia (TANZAM ) Highway, a

paved trunk road system of 1,762km linking Dar es

Salaam Port to Kapiri M poshi,

• the TANESCO electricity grid servicing major towns

along the corridor within Tanzania, and

• total renewable water resources amounting to

93km3 per year, of which 84km3 per year is

produced internally.

If this backbone infrastructure is going to provide

the services that are needed for agricultural

growth, several important improvements are

needed. Firstly, Dar es Salaam Port ’s capacity

needs to be expanded and customs procedures

accelerated. Secondly, the road system requires

rehabil itation and maintenance. Thirdly, even

though rail transport is less expensive than

road haulage, it is currently slow, unsecure

and unreliable. Interchange facil it ies must be

improved and railway wagon and locomotive

stock upgraded to make it more competitive.

Fourthly, the power grid will need upgrading

in places and national shortages in generating

capacity wil l need to be met.

Investments in some of these improvements

are already taking place (see Figure 3.4

Anchor investment map). The government and

development partners, with cooperation from the

private sector, must be committed to see proposed

infrastructure investments completed, including

cooperation from state-owned enterprises.

Source: JICA, SAGCOT technical team estimates

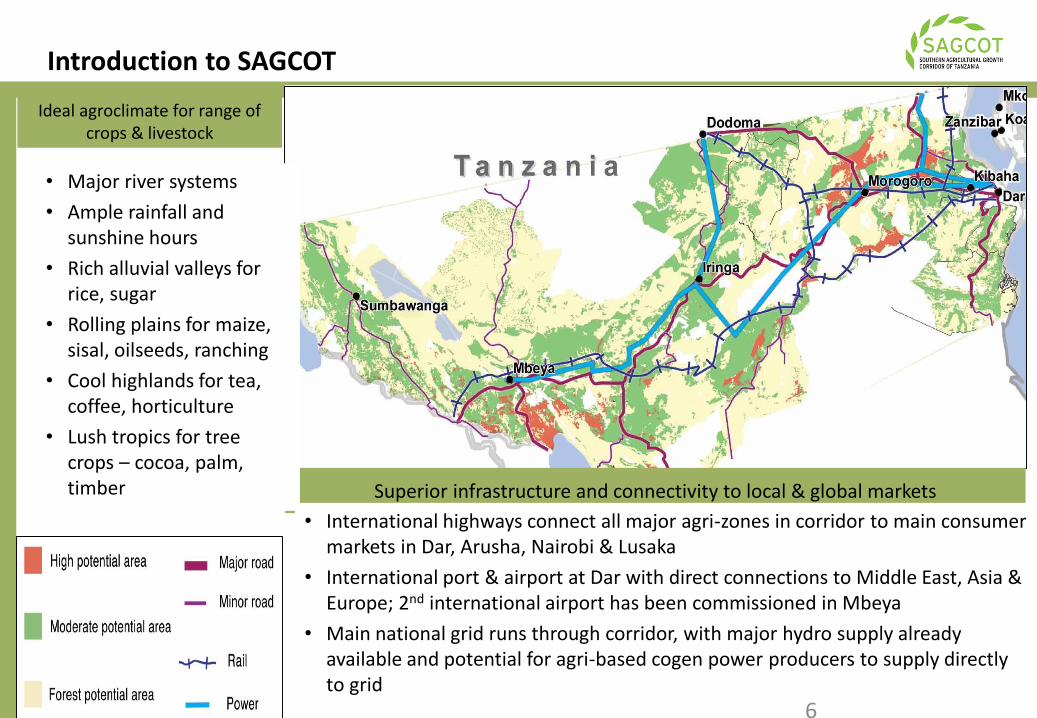

Introduction to SAGCOT

Superior infrastructure and connectivity to local & global markets

Ideal agroclimate for range of crops & livestock

• Major river systems

• Ample rainfall and sunshine hours

• Rich alluvial valleys for rice, sugar

• Rolling plains for maize, sisal, oilseeds, ranching

• Cool highlands for tea, coffee, horticulture

• Lush tropics for tree crops – cocoa, palm, timber

• International highways connect all major agri-zones in corridor to main consumer markets in Dar, Arusha, Nairobi & Lusaka

• International port & airport at Dar with direct connections to Middle East, Asia & Europe; 2nd international airport has been commissioned in Mbeya

• Main national grid runs through corridor, with major hydro supply already available and potential for agri-based cogen power producers to supply directly to grid

6

23 Southern Agricultural Growth Corridor of T anzania

Figure 3.1 Agricultural potential and backbone infrastructure

SAGCOT’s backbone infrastructure provides a

reasonable but incomplete platform upon which

to develop commercial agriculture in the southern

corridor. The majority of infrastructure was built after

Tanzanian independence as an alternative to the South

African and M ozambican transport links to Zambia,

and includes:

• the Port of Dar es Salaam, which currently handles

approximately eight million tonnes per year,

• the Tanzania-Zambia Railway Authority (TAZARA)

network of 1,870km of rail, commissioned in 1976

to link Dar es Salaam Port to Kapiri M poshi and

then to the Zambian Railways (and the DRC and

Southern African rail networks),

• The Tanzania-Zambia (TANZAM ) Highway, a

paved trunk road system of 1,762km linking Dar es

Salaam Port to Kapiri M poshi,

• the TANESCO electricity grid servicing major towns

along the corridor within Tanzania, and

• total renewable water resources amounting to

93km3 per year, of which 84km3 per year is

produced internally.

If this backbone infrastructure is going to provide

the services that are needed for agricultural

growth, several important improvements are

needed. Firstly, Dar es Salaam Port ’s capacity

needs to be expanded and customs procedures

accelerated. Secondly, the road system requires

rehabilitation and maintenance. Thirdly, even

though rail transport is less expensive than

road haulage, it is currently slow, unsecure

and unreliable. Interchange facil it ies must be

improved and railway wagon and locomotive

stock upgraded to make it more competitive.

Fourthly, the power grid will need upgrading

in places and national shortages in generating

capacity will need to be met.

Investments in some of these improvements

are already taking place (see Figure 3.4

Anchor investment map). The government and

development partners, with cooperation from the

private sector, must be committed to see proposed

infrastructure investments completed, including

cooperation from state-owned enterprises.

Source: JICA, SAGCOT technical team estimates

7

Introduction to SAGCOT

Our portfolio of partners represents a balanced mix of local and international institutions across all stages of agri-business value chains

8

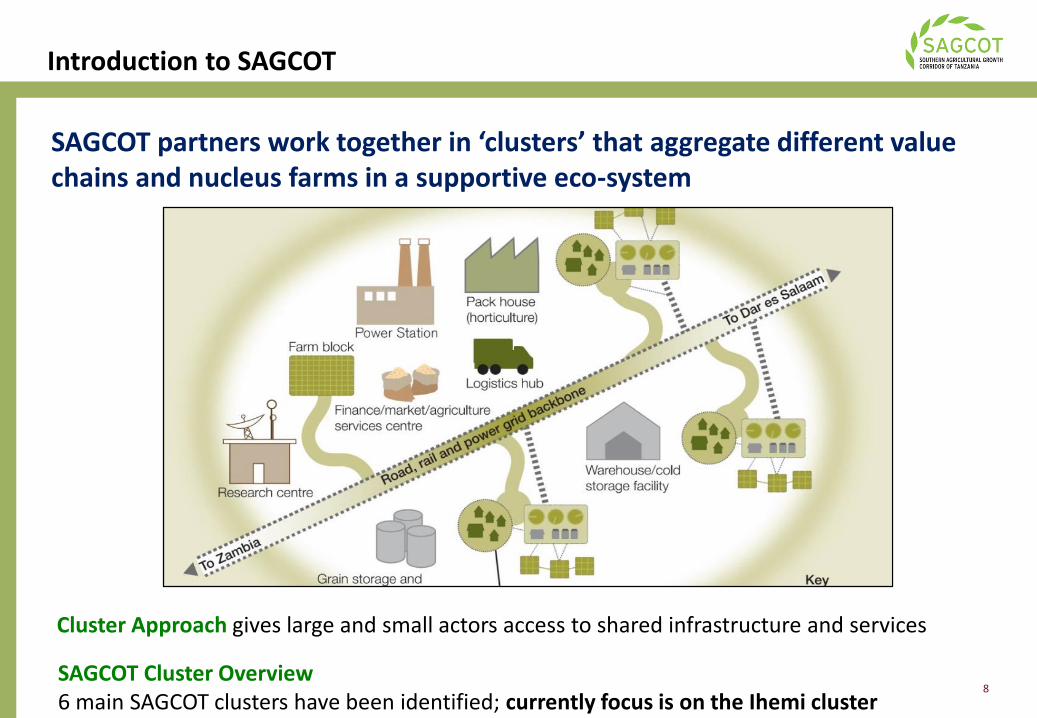

SAGCOT partners work together in ‘clusters’ that aggregate different value chains and nucleus farms in a supportive eco-system

Cluster Approach gives large and small actors access to shared infrastructure and services

SAGCOT Cluster Overview6 main SAGCOT clusters have been identified; currently focus is on the Ihemi cluster

Introduction to SAGCOT

9

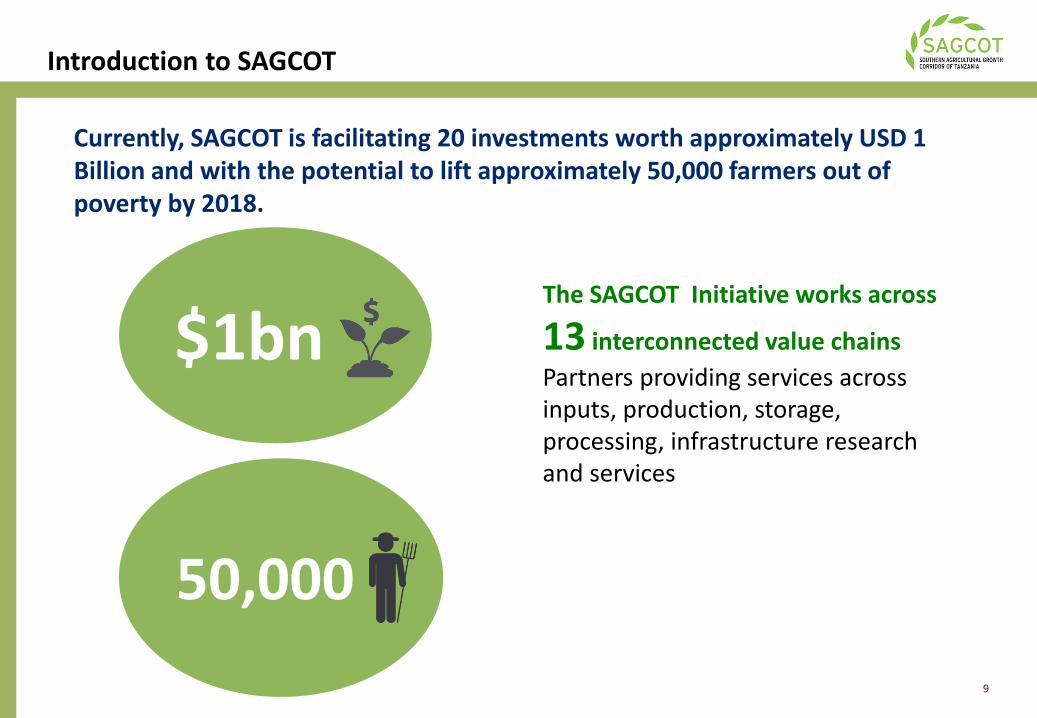

Currently, SAGCOT is facilitating 20 investments worth approximately USD 1 Billion and with the potential to lift approximately 50,000 farmers out of poverty by 2018.

Introduction to SAGCOT

The SAGCOT Initiative works across

13 interconnected value chains

Partners providing services across inputs, production, storage, processing, infrastructure research and services

$1bn

50,000

10SAGCOT Centre Ltd. 10

Overview of the Tanzania Investment Landscape

Introduction to SAGCOT

Overview of Ihemi cluster and key value chain opportunities

11

Ihemi as an Investment Cluster

SOURCE: SAGACOT Center Annual Forum report http://www.sagcot.com/fileadmin/documents/2016/SAGCOT_Annual_Forum_2015_Report.pdf

Ihemi Cluster Overview

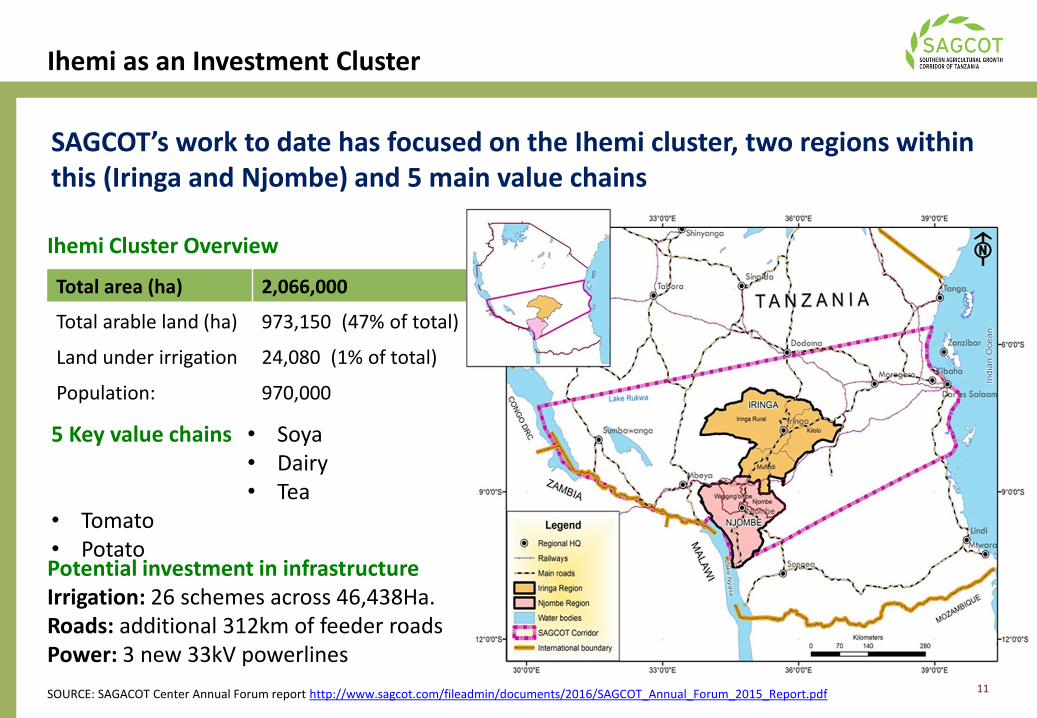

SAGCOT’s work to date has focused on the Ihemi cluster, two regions within this (Iringa and Njombe) and 5 main value chains

5 Key value chains

• Tomato• Potato

• Soya• Dairy• Tea

Potential investment in infrastructureIrrigation: 26 schemes across 46,438Ha.Roads: additional 312km of feeder roadsPower: 3 new 33kV powerlines

Total area (ha) 2,066,000

Total arable land (ha) 973,150 (47% of total)

Land under irrigation 24,080 (1% of total)

Population: 970,000

12

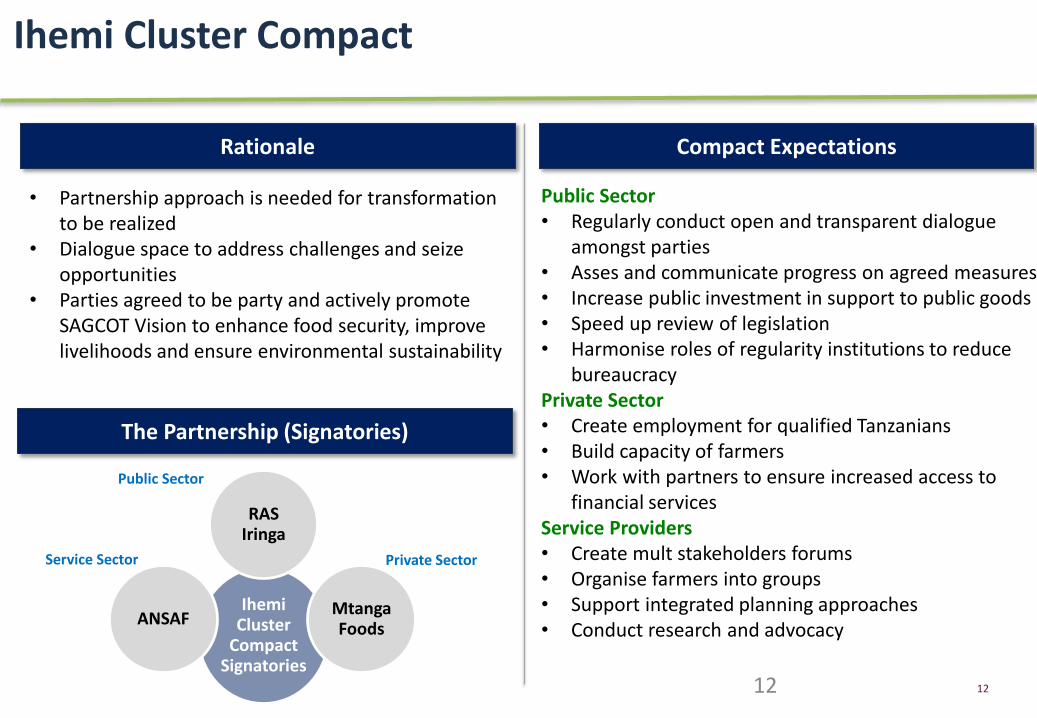

Ihemi Cluster Compact

12

IhemiCluster

Compact Signatories

RAS Iringa

MtangaFoods

ANSAF

Rationale

The Partnership (Signatories)

Compact Expectations

Public Sector

Service Sector Private Sector

• Partnership approach is needed for transformation to be realized

• Dialogue space to address challenges and seize opportunities

• Parties agreed to be party and actively promote SAGCOT Vision to enhance food security, improve livelihoods and ensure environmental sustainability

Public Sector• Regularly conduct open and transparent dialogue

amongst parties• Asses and communicate progress on agreed measures• Increase public investment in support to public goods• Speed up review of legislation• Harmonise roles of regularity institutions to reduce

bureaucracyPrivate Sector• Create employment for qualified Tanzanians• Build capacity of farmers• Work with partners to ensure increased access to

financial services Service Providers• Create mult stakeholders forums • Organise farmers into groups• Support integrated planning approaches• Conduct research and advocacy

13

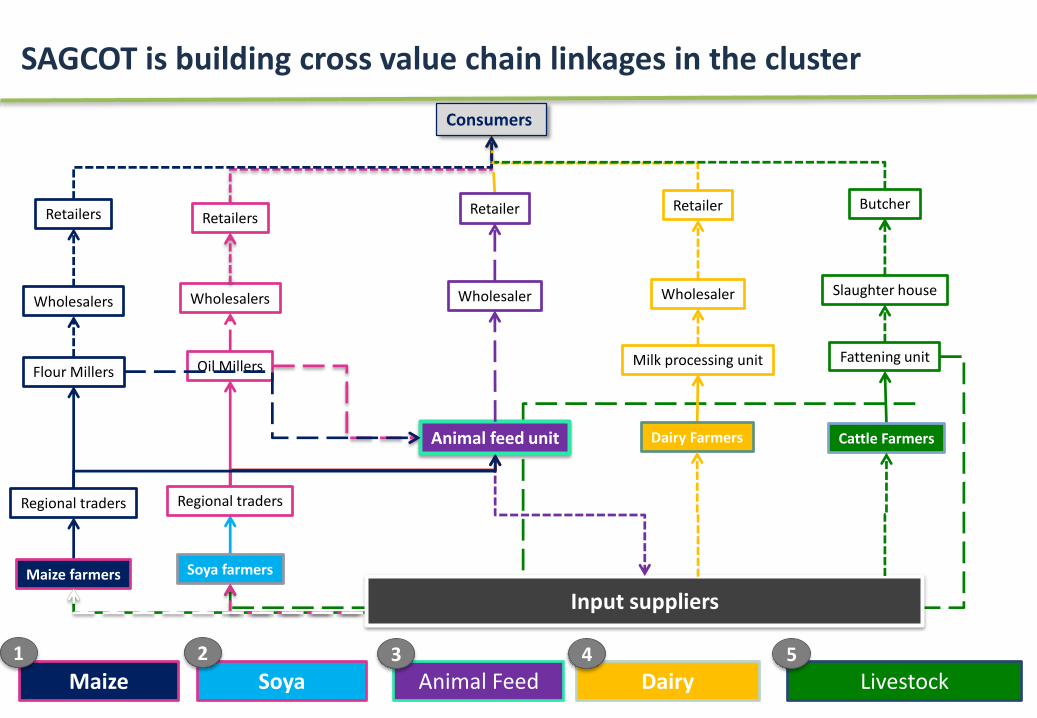

Butcher

Slaughter house

Fattening unit

Retailer

Wholesaler

Milk processing unit

Consumers

Input suppliers

Cattle FarmersDairy Farmers

Retailers

Wholesalers

Oil Millers

Regional traders

Soya farmers

SAGCOT is building cross value chain linkages in the cluster

Soya Dairy LivestockAnimal Feed

Animal feed unit

Retailer

Wholesaler

Maize

Retailers

Wholesalers

Flour Millers

Regional traders

Maize farmers

21 3 4 5

14

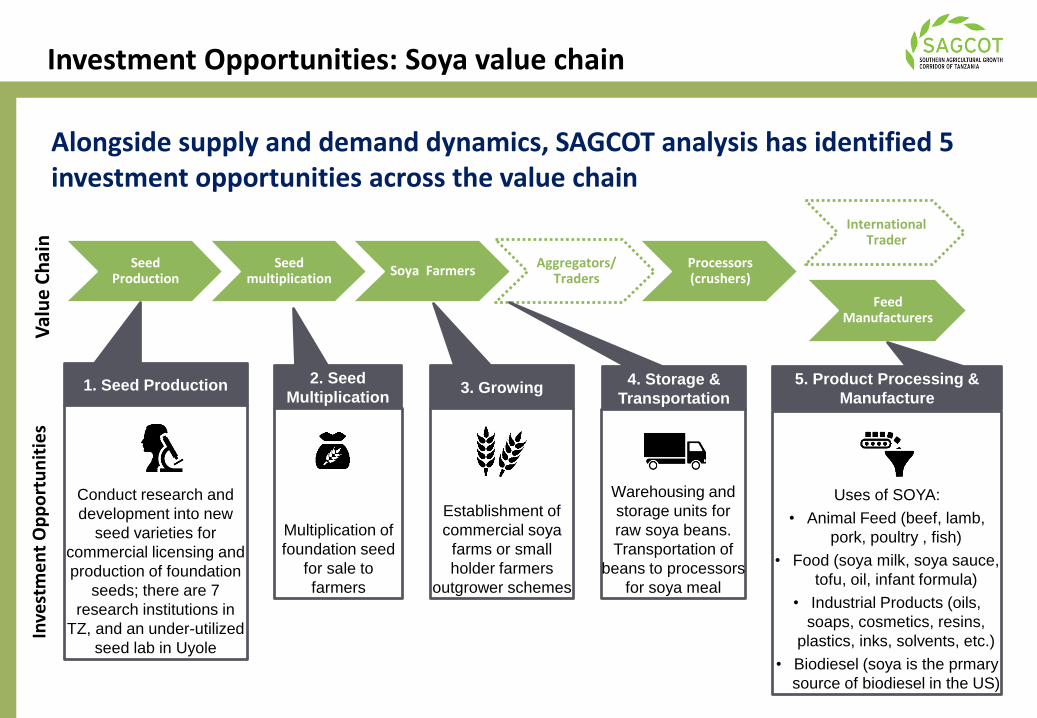

Investment Opportunities: Soya value chain

SOURCE: Evaluation of Market Opportunities for Soybean in Tanzania USDA FAS Soya ni Pesa Project December 2012,

Technoserv Soya Value chain assessment, 2015

There is currently significant unmet demand in the production of soybean, primarily for use in animal feeds. This unmet demand is partly serviced by imports.

Domestic: Production: estimated 5,000 MTCrushing capacity: estimated 26,000 MTCrushing utilization: 19%

Imports: Soya cake: 43,000 MTSoya oil: 3,000 MT

Cost of production: US$125 per MT

Market Price:Farm Gate: US$267- $534 (seasonal variance) Retail market: US$1,334/MTWorld Market price: US$548 – $598 MT

Edible oils: 400,000 MT of edible oil per annum, over 50% is imported

Animal feed: 800,000 MT per annum is purchased, demand is for 2,000,000 MT per annum.

SUPPLY DEMAND

15

Soya experiences global demand from humanconsumption and animal consumption due to highprotein content (40%, versus 20% of other legumes)

An increase in productive capacity would lead to anincrease in extrusion capacity and the usage ofhigher quality seeds.

Short term opportunity: Increased use of soybeans and associated products in animal feeds.

Longer term opportunity: Change in human consumption patterns for increase demand in soya products (oil, milk, etc.)

Investment Opportunities: Soya value chain

Highest Production Lowest Production

Producing regions: Southern highlands

The short-term opportunity is for the increase of productive capacity for production of animal feed, with longer term potential of increasing human consumption

16

Seed Production

Seed multiplication

Soya FarmersAggregators/

TradersProcessors (crushers)

Feed Manufacturers

International Trader

1. Seed Production

Conduct research and

development into new

seed varieties for

commercial licensing and

production of foundation

seeds; there are 7

research institutions in

TZ, and an under-utilized

seed lab in Uyole

Inve

stm

en

t O

pp

ort

un

itie

s

2. Seed

Multiplication

Multiplication of

foundation seed

for sale to

farmers

5. Product Processing &

Manufacture

Uses of SOYA:

• Animal Feed (beef, lamb,

pork, poultry , fish)

• Food (soya milk, soya sauce,

tofu, oil, infant formula)

• Industrial Products (oils,

soaps, cosmetics, resins,

plastics, inks, solvents, etc.)

• Biodiesel (soya is the prmary

source of biodiesel in the US)

3. Growing

Establishment of

commercial soya

farms or small

holder farmers

outgrower schemes

4. Storage &

Transportation

Warehousing and

storage units for

raw soya beans.

Transportation of

beans to processors

for soya meal

Investment Opportunities: Soya value chain

Alongside supply and demand dynamics, SAGCOT analysis has identified 5 investment opportunities across the value chain

Val

ue

Ch

ain

17SOURCE: CGIAR World Potato Atlas

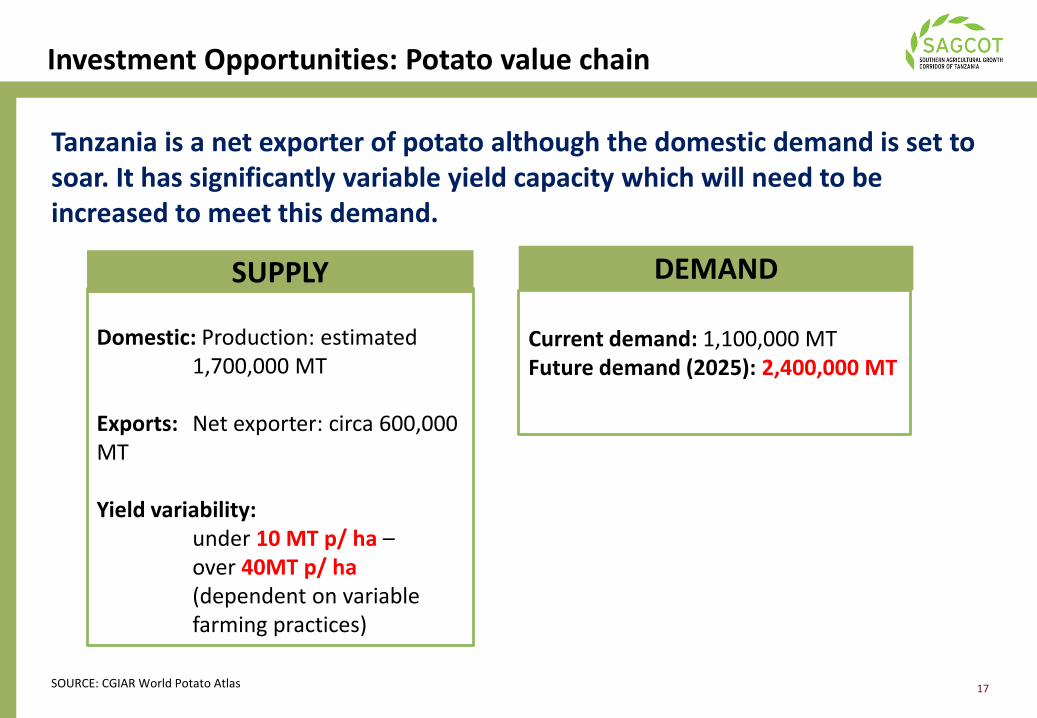

Tanzania is a net exporter of potato although the domestic demand is set to soar. It has significantly variable yield capacity which will need to be increased to meet this demand.

Domestic: Production: estimated1,700,000 MT

Exports: Net exporter: circa 600,000 MT

Yield variability: under 10 MT p/ ha –over 40MT p/ ha (dependent on variable farming practices)

Current demand: 1,100,000 MTFuture demand (2025): 2,400,000 MT

SUPPLY DEMAND

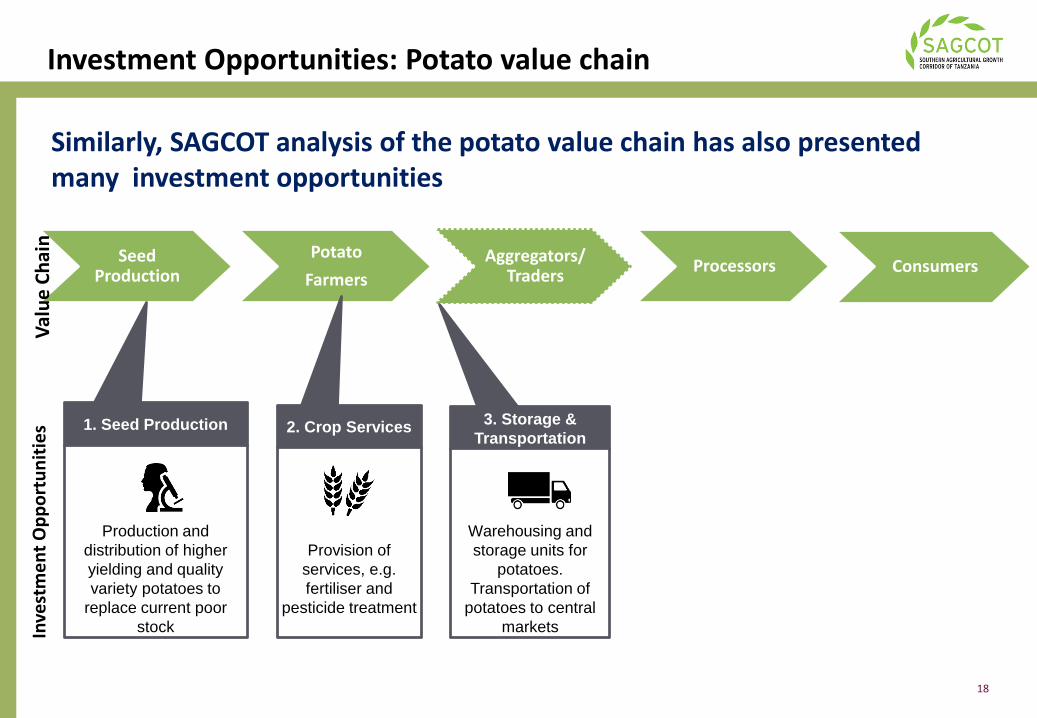

Investment Opportunities: Potato value chain

18

Seed Production

Potato

Farmers

Aggregators/ Traders

Processors Consumers

1. Seed Production

Production and

distribution of higher

yielding and quality

variety potatoes to

replace current poor

stock Inve

stm

en

t O

pp

ort

un

itie

s 2. Crop Services

Provision of

services, e.g.

fertiliser and

pesticide treatment

3. Storage &

Transportation

Warehousing and

storage units for

potatoes.

Transportation of

potatoes to central

markets

Investment Opportunities: Potato value chain

Similarly, SAGCOT analysis of the potato value chain has also presented many investment opportunities

Val

ue

Ch

ain

1919

Geoffrey Kirenga is currently the Chief Executive Officer of theSAGCOT Centre Ltd. He is the former Director of the CropDevelopment Division at the Tanzania Ministry of Agriculture,Food Security and Cooperatives. Prior to this position, Mr.Kirenga specialized in crop promotion services, pest managementand plant protection.

Mr. Kirenga has an extensive network in both the Tanzanian andinternational agriculture and agribusiness communities, and he ishighly committed to driving the SAGCOT Centre Ltd to deliveringon its role as the catalyst dedicated to transforming Tanzania'sagriculture sector.

Geoffrey Kirenga| CEO | SAGCOT Centre [email protected] Building Mwaya street, Masaki P.O. Box 11313 | Dar es Salaam, TanzaniaTel: +255 (0) 22 2 601024| Mobile: +255 (0) 756 480 069www.sagcot.com

2020

Jennifer Baarn is an experienced professional in the developmentand facilitation of international public-private partnerships(PPPs), with a particular focus on the role of partnerships inagriculture as drivers of economic growth. Prior to joining theSAGCOT Centre, Jennifer was an Associate Director at the WorldEconomic Forum (WEF) where she helped develop the WEF’sNew Vision for Agriculture initiative. Jennifer spent a number ofyears in financial services at Rabobank International, identifyinggrowth opportunities in food and agribusiness and developingkey insights into the agricultural sector. A South American whohas lived in Europe and holds a passion for Africa, Jennifer bringsknowledge and experience from around the globe to apply infurthering the objectives of SAGCOT.

Jennifer Baarn | Deputy CEO | SAGCOT Centre [email protected] Building Mwaya street, Masaki P.O. Box 11313 | Dar es Salaam, TanzaniaGeneral phone number: +255 (0) 22 260 1024www.sagcot.com