Embed Size (px)

Citation preview

Safety & Risk Script

Client concerns: Diversify and Safety. Not putting all our eggs in one basket. Please REASSURE us.

These are very valid concerns for our clients. The prudent thing to do historically is to diversify diversify diversify. Because you want to be sure your money is going to be there and safe.

What’s important is that you understand how this works so you can make your decision. I will give you my professional recommendation.

I’m going to give two different answers on diversification. The reason why is because I were two hats.

One hat is what I specialize in which is Income Planning for baby boomers.

The other hat is called a Registered Investment Advisor hat in which I act as fiduciary on behalf of our clients. There are 1.3 million licensed people that offer financial products nationwide. There is only less than a couple hundred thousand that are required acting as a fiduciary.

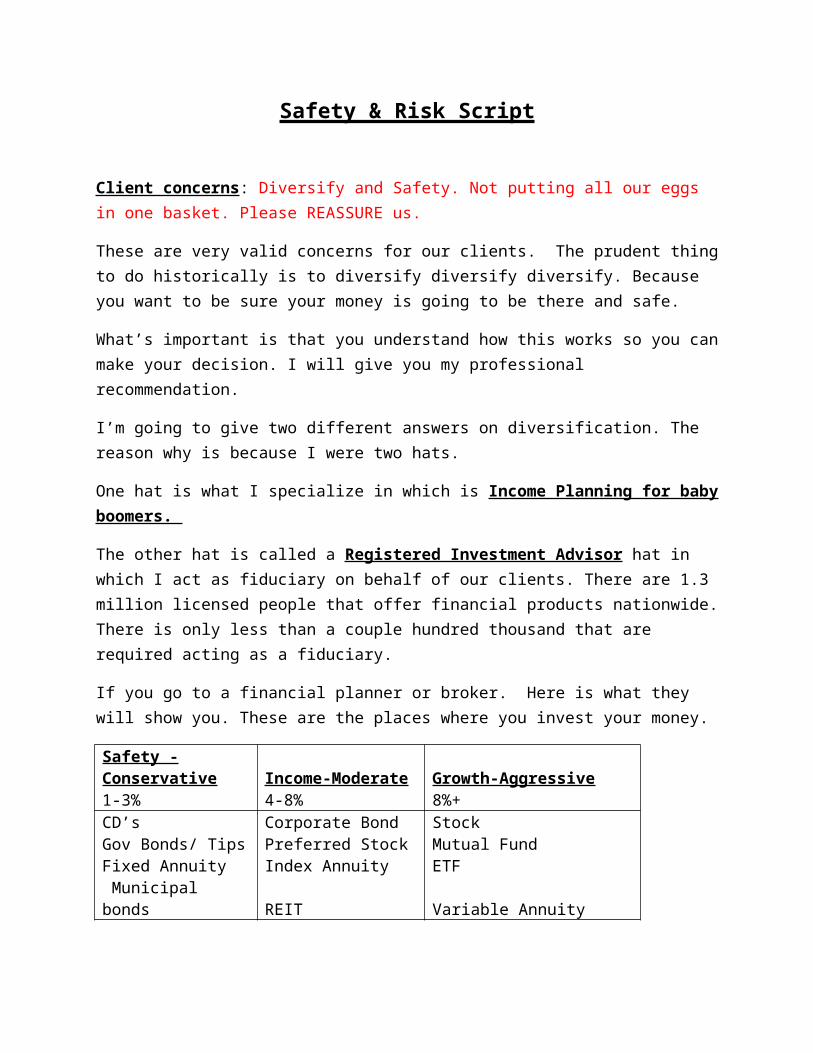

If you go to a financial planner or broker. Here is what they will show you. These are the places where you invest your money.

Safety -Conservative Income-Moderate Growth-Aggressive1-3% 4-8% 8%+CD’s Corporate Bond StockGov Bonds/ Tips Preferred Stock Mutual FundFixed Annuity Index Annuity ETF Municipal bonds REIT Variable Annuity

Most people look at investments as these and say where I can get the Highest return on my money first. Then How safe is it. Finally- What are the dividends or income? This is how most advisors look at investments. They want to diversify and used stocks, bonds and different types of plans in your portfolio.

Return on Your money-Return on Investments

Growth of Money/Investments

Definition of an investment is it can grow or lose principle.

When most people look at investments they look at where they can get the highest return on your investments

-This is how brokers/financial advisors look at most investments.

-They look at how do I get the highest return on investments.

Priority view for an Investment/return on investments.

1. Return-Highest return on investment.2. Safety-How safe is it3. Income-What are the dividends or income.

This is how most advisors work. They focus on the return. That’s why they tell you to diversify.

Return of Your Money-Income on Money

Income PlanningIncome/Savings

Definition of a savings plan means save to use as income and not lose principle.

This is how an income planner views your plan. We look at return on your money with Contractual Guarantees. Meaning how can maximize the income on my money.

Priority View for Income1. Safety- Always a need for safety2. Income – Always a need for lifetime income.3. Return- Growth

-There is always the need for safety and there’s always the need for lifetime income.

-Seeing how most people live in a Pension less Society today.

Example- If you had the opportunity today to take 1 million dollars today and put into the Social Security Administration system today and turn on income for $80,000 a year it goes up with inflation for the rest of you and your wife life’s. I would tell you to sign up today. Social Security grows with inflation and government’s version CPI. Income planning is when I look for the plan that gives you the highest income guarantee for rest of both lives’s. I’m looking the best plan that gives you safety and income with Contractual Guarantees.

Default Risk

3 Safest Places to Put your Money-Legal Reserve System

1. Government Bonds: Government Bonds are the safest investment. If the government defaults we have much bigger problems than our investments. Nothing is safe. The only thing safe is Gold and Guns.-Corporate Bonds: When we look at corporate bonds it is true that your money is only as safe as the guarantee of the corporation. The ability of the corporation to pay its liabilities.

2. Banks are FDIC insured: -Monies are insured up to $250,000 per person.-Banks leverage monies 9x. $100K can be lent up to 9 times. -This is how the banks make so much money. - But this also why they went out of business when borrowers defaulted on these loans.

3. Insurance Companies: Legal Reserve system.- $1 for $1 in reserves - Surplus Capital 3%-5%- Must have Reinsures. Usually there are 4-14 reinsures.- State Guarantee fund

Example: For Stocks and Bonds.

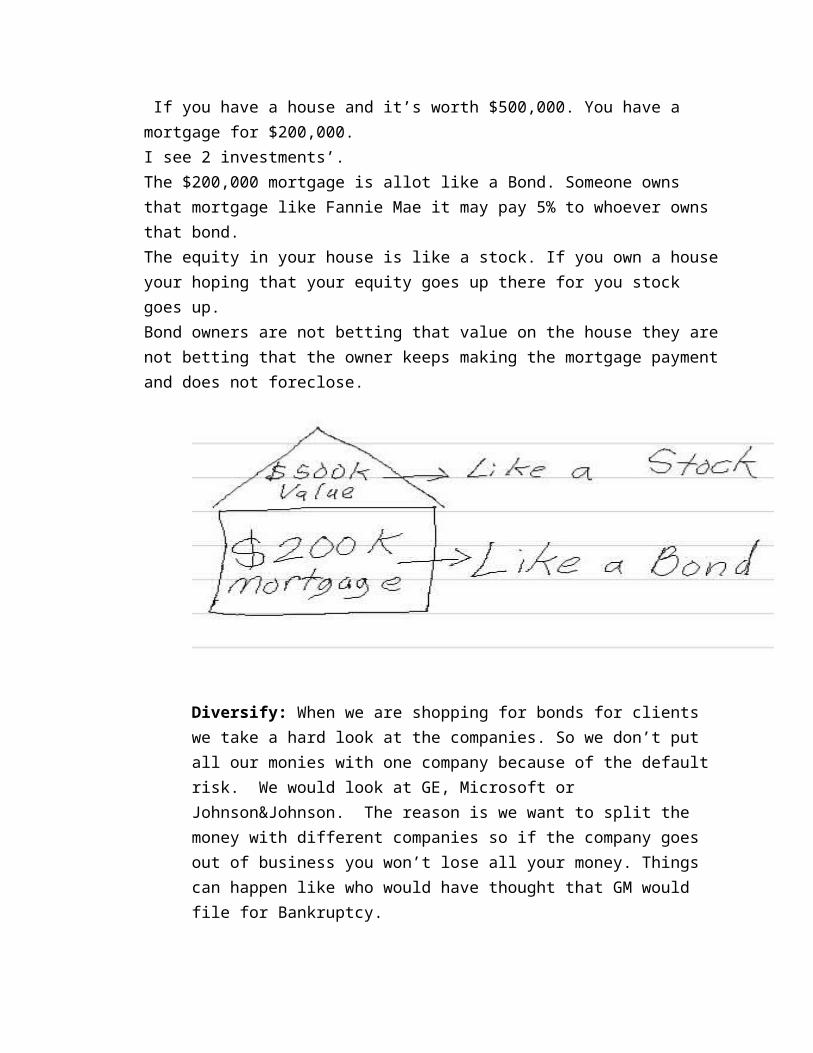

Stocks are base on a company’s profitability. Stock price goes up.Bonds are based on survivability/ liability. Betting the company does not go Bankrupt so they can pay the bond. If you have a house and it’s worth $500,000. You have a mortgage for $200,000.I see 2 investments’.The $200,000 mortgage is allot like a Bond. Someone owns that mortgage like Fannie Mae it may pay 5% to whoever owns that bond.The equity in your house is like a stock. If you own a house your hoping that your equity goes up there for you stock goes up.Bond owners are not betting that value on the house they are not betting that the owner keeps making the mortgage payment and does not foreclose.

Diversify: When we are shopping for bonds for clients we take a hard look at the companies. So we don’t put all our monies with one company because of the default risk. We would look at GE, Microsoft or Johnson&Johnson. The reason is we want to split the money with different companies so if the company goes out of business you won’t lose all your money. Things can happen like who would have thought that GM would file for Bankruptcy. That’s why we would want to use the diversification strategy with corporate bonds and stocks I agree. This probably doesn’t matter when your buying bank CD’s as long as the bank is not on the FDIC watch list. You can just split it up at different banks at $250K each. If you could get 10% on bank CD’s I would tell to put all your money in CD’s game over. Or US Government Treasuries. Our T-bill just keeps getting worse today it is under 3%.

Legal Reserve System

What would need to happen for you to lose your money?

Banks: FDIC Insured

Banks are able to leverage money 9 times. So if you take $100,000 CD at 2% for 5 years. The bank can lend that 9 times at 5% or higher. They pay you $2000 and make $45,000.This is how banks make huge amount of money. FDIC backs up these deposits. But FDIC has less than 1% in reserves. If one the big banks goes under like Chase or BofA it will wipe out the reserves in one day. FDIC also has the ability to borrow from the Federal Reserve. Government backs the FDIC. This would cause a great depression.

Investment Banks like Goldman Sachs can go 30 to 1.

Insurance Companies: Legal reserve system

This does not include all insurance products.

Life Insurance Products

Fixed Annuities

Indexed Annuities

Hybrid Annuities

Insurance companies investment the money into investment grade bonds and T-bills. Most insurance companies range from 20%-75% of monies in US Government Treasury Bonds.

-All these insurance companies must have to have $1for $1 in reserves.

-Most insurance have 3%-5% in surplus capital. What this means they have there own money backing up the bond.

-This is also why companies buy very low percentage with each company and a very high percentage with US Government Bonds.

-Insurance companies also have reinsures. What that means is that each insurance company has 4-14 insurance companies reinsuring them. So in case something goes wrong and have use all surplus capital and reserves they can pay out there claims.

-The last level of security is the State Guarantee fund. This is fund that the state controls for insurance companies. The rules are every time there’s a contract open small percent like1% or less will into the state guarantee fund.

So this is how it works.

If bonds default it could be that a couple of companies not all companies would default at once. All reserves were used up all the surplus capital was used up then that State Guarantee fund would come in and take over. It would pay out whatever is needed guarantee all the principle. In the history of the US there has been 3 times that this has happened and no one has lost there principle. It could take some time to get paid out but you would receive your principle. Money could have been frozen for a year.

Going into AIG all the accounts that were in the investment side of AIG were are risk at one point. But Insurance companies have 2 sides the insurance side and the investment side that has separate accounts. Every insurance policy, immediate annuity,fixed annuity and fixed index annuity was still covered.

So let’s take a look at American Equity’s Portfolio.

See Below