Embed Size (px)

Citation preview

Sabana Shari’ah Compliant Industrial REIT3Q FY2011

Financial Results Presentation

19 October 2011

Disclaimers

This presentation shall be read in conjunction with Sabana REIT’s financial statements for the financial

period ended 30 September 2011.

This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future

performance, outcomes and results may differ materially from those expressed in forward-looking

statements as a result of a number of risks, uncertainties and assumptions.

Representative examples of these factors include (without limitation) general industry and economic

conditions, interest rate trends, cost of capital and capital availability, competition from similar

developments, shifts in expected levels of property rental income, changes in operating expenses, including

employee wages, benefits and training, property expenses and governmental and public policy changes and

the continued availability of financing in the amounts and the terms necessary to support future business.

You are cautioned not to place undue reliance on these forward looking statements, which are based on

current view of management on future events.

Any discrepancies in the tables included in this presentation between the listed amounts and total thereof

are due to rounding.

2

3

III. Financial performance

I. About Sabana REIT

IV. Portfolio update

II. Key financial highlights

V. Market outlook

VI. Summary

4

About Sabana REIT

Sabana Shari'ah Compliant Industrial REIT ("Sabana REIT")(1) was listed on the

Singapore Exchange on 26 November 2010. It aims to create value for its unit holders by

investing in income-generating industrial real estate across Asia, in line with Shari’ah

investment principles. Sabana REIT is:

� the world’s largest listed Shari’ah compliant REIT

� the first listed REIT globally to adopt stricter GCC-standard Shari’ah compliance

� the first Shari’ah compliant certified REIT in Singapore

� the largest IPO free float for Singapore industrial REITs

� included in major indices such as the MSCI Global Small-cap Indices and in the Dow Jones

Singapore Index, the Dow Jones World Index and several regional Dow Jones indexes.

� Assigned a ‘BBB-’ long term corporate credit rating and ‘aXA-’ ASEAN scale rating with a stable

outlook from Standard & Poor’s Rating Services

(1) Sabana REIT was a dormant private trust from the date of constitution on 29 October 2010 until the Properties were acquired on 26 November 2010. Sabana Shari’ah Compliant REIT was officially listed on the same day (“Listing Date”) on the Singapore Exchange Securities Trading Limited (“SGX-ST”). Consequently the operations of Sabana Shari’ah Compliant REIT commenced from 26 November 2010.

In July 2011, Sabana REIT’s efforts to raise investor familiarity with Shari’ah

compliant products during its IPO were recognised by the International Public

Relations Association (IPRA), which gave Sabana REIT a Golden World Award.

Widening international recognition

Since it was listed on 26 November 2010, Sabana REIT has received six international awards

In February 2011, Sabana REIT was awarded “IPO Deal of the Year (2010)” and

“Real Estate Deal of the Year (2010)” by Islamic Finance News, one of the most

prestigious awards that honors the best in the Islamic finance industry.

In September 2011, Sabana REIT was awarded the Triple A Award for ‘Best

Islamic Deal in Singapore’ and ‘Most Innovative Islamic Deal” by The Asset,

Asia’s leading issuer and investor-focused financial monthly publication.

On 4 October 2011, Sabana REIT received “The Most Outstanding Islamic REIT”

at the KLIFF Islamic Finance Awards Ceremony, which was organised in

conjunction with the 8th Kuala Lumpur Islamic Finance Forum (KLIFF 2011).

5

6

III. Financial performance

I. About Sabana REIT

IV. Portfolio update

II. Key financial highlights

V. Market outlook

VI. Summary

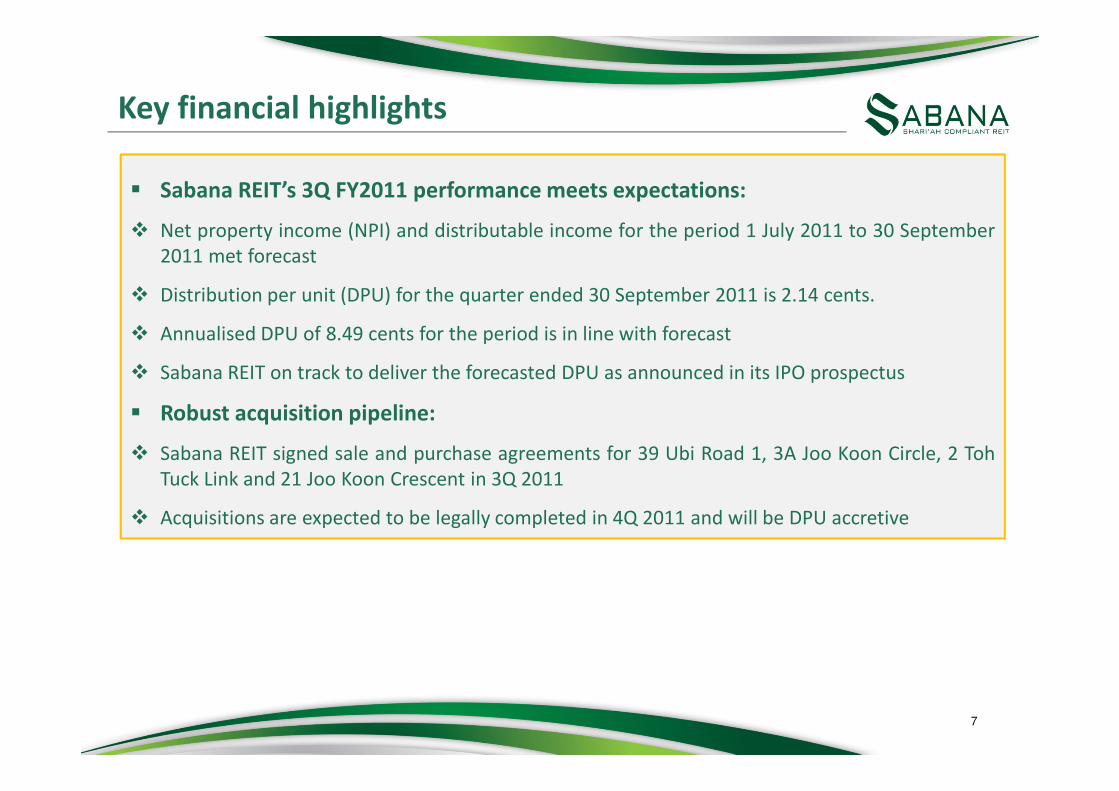

Key financial highlights

� Sabana REIT’s 3Q FY2011 performance meets expectations:

� Net property income (NPI) and distributable income for the period 1 July 2011 to 30 September

2011 met forecast

� Distribution per unit (DPU) for the quarter ended 30 September 2011 is 2.14 cents.

� Annualised DPU of 8.49 cents for the period is in line with forecast

� Sabana REIT on track to deliver the forecasted DPU as announced in its IPO prospectus

� Robust acquisition pipeline:

� Sabana REIT signed sale and purchase agreements for 39 Ubi Road 1, 3A Joo Koon Circle, 2 Toh

Tuck Link and 21 Joo Koon Crescent in 3Q 2011

� Acquisitions are expected to be legally completed in 4Q 2011 and will be DPU accretive

7

8

III. Financial performance

I. About Sabana REIT

IV. Portfolio update

II. Key financial highlights

V. Market outlook

VI. Summary

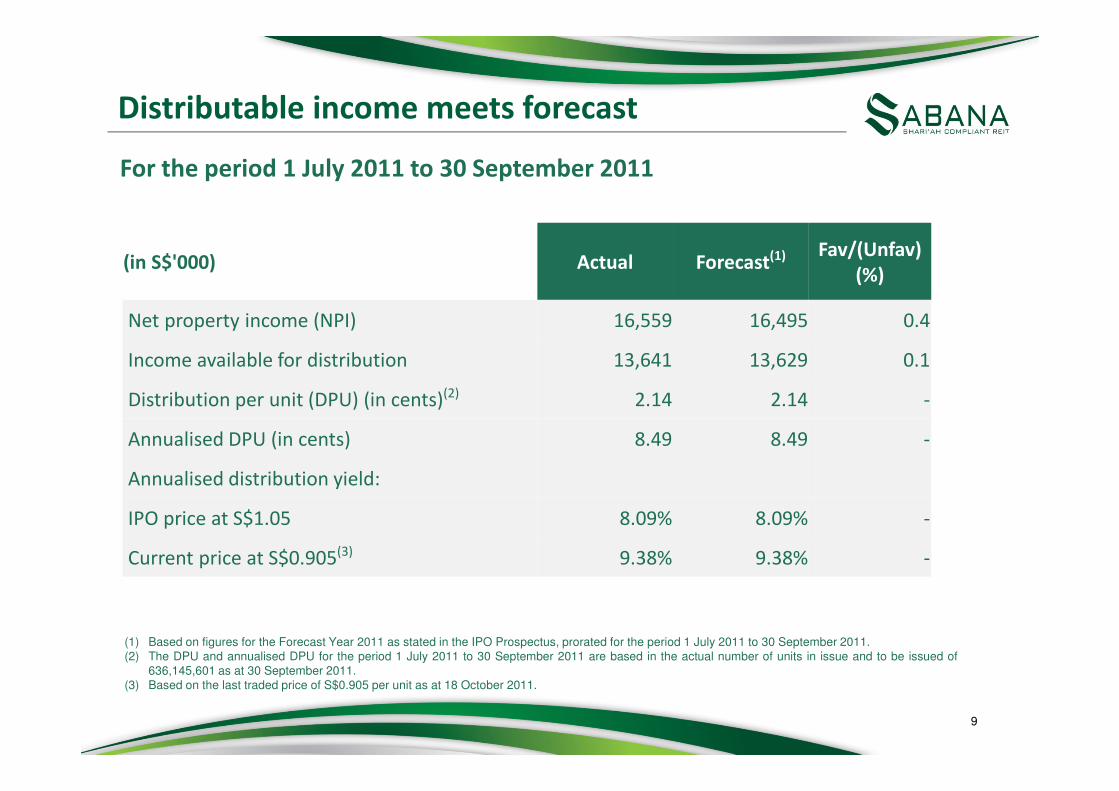

Distributable income meets forecast

For the period 1 July 2011 to 30 September 2011

(1) Based on figures for the Forecast Year 2011 as stated in the IPO Prospectus, prorated for the period 1 July 2011 to 30 September 2011.(2) The DPU and annualised DPU for the period 1 July 2011 to 30 September 2011 are based in the actual number of units in issue and to be issued of

636,145,601 as at 30 September 2011.(3) Based on the last traded price of S$0.905 per unit as at 18 October 2011.

9

(in S$'000) Actual Forecast(1) Fav/(Unfav)

(%)

Net property income (NPI) 16,559 16,495 0.4

Income available for distribution 13,641 13,629 0.1

Distribution per unit (DPU) (in cents)(2) 2.14 2.14 -

Annualised DPU (in cents) 8.49 8.49 -

Annualised distribution yield:

IPO price at S$1.05 8.09% 8.09% -

Current price at S$0.905(3) 9.38% 9.38% -

Financial performance

• Gross revenue exceeded

forecast by 1.1% and NPI is in

line with forecast

• Property expenses are

16.2% above forecast mainly

due to higher actual utilities

costs and higher JTC land rent

• Amortisation of intangible

asset is 22.1% higher than

forecast due to higher

drawdown of rental support

for 9 Tai Seng Drive

• Distributable Income is 0.1%

higher than forecast mainly

due to higher gross revenue

and savings from lower trust

expenses

(1) Based on figures for the Forecast Year 2011 as stated in the IPO Prospectus, prorated for the period 1 July 2011 to 30 September 2011.

10

For the period 1 July 2011 to 30 September 2011

(in S$'000) Actual Forecast(1) Fav/

(Unfav)(%)

Gross revenue 17,398 17,217 1.1

Property expenses (839) (722) (16.2)

NPI 16,559 16,495 0.4

Net financing costs (2,611) (2,543) (2.6)

Amortisation of intangible asset (348) (285) (22.1)

Manager's fees (1,177) (1,099) (7.0)

Trustee's fees (90) (88) (2.3)

Donation of non-Shari'ah compliant income (40) (34) (17.6)

Other trust expenses (264) (324) 18.5

Net income 12,029 12,122 (0.8)

Net change in fair value of financial

deriviatives(1,194) - N.M.

Net change in fair value of investment

properties 51,279 - N.M.

Distribution adjustments (48,473) 1,507 N.M.

Distributable income 13,641 13,629 0.1

Balance sheet

(1) Comprises 635,069,362 units in issue as at 30 September 2011 and 1,076,239 units to be issued to the Manager by 31 October 2011 as partialconsideration of Manager’s fees incurred for the period 1 July 2011 to 30 September 2011.

(2) Excludes distributable income of SGD13.6 million available for distribution for the period ended 30 September 2011.

11

As at 30 September 2011 S$'000

Investment properties 897,329

Intangible asset 3,971

Other assets 32,889

Total assets 934,189

Debt, at amortised cost 216,719

Other liabilities 33,486

Total liabilities 250,205

Net assets attributable to unitholders 683,984

Units in issue(1) 636,145,601

NAV per unit (SGD) 1.08

Adjusted NAV per unit(2) (SGD) 1.05

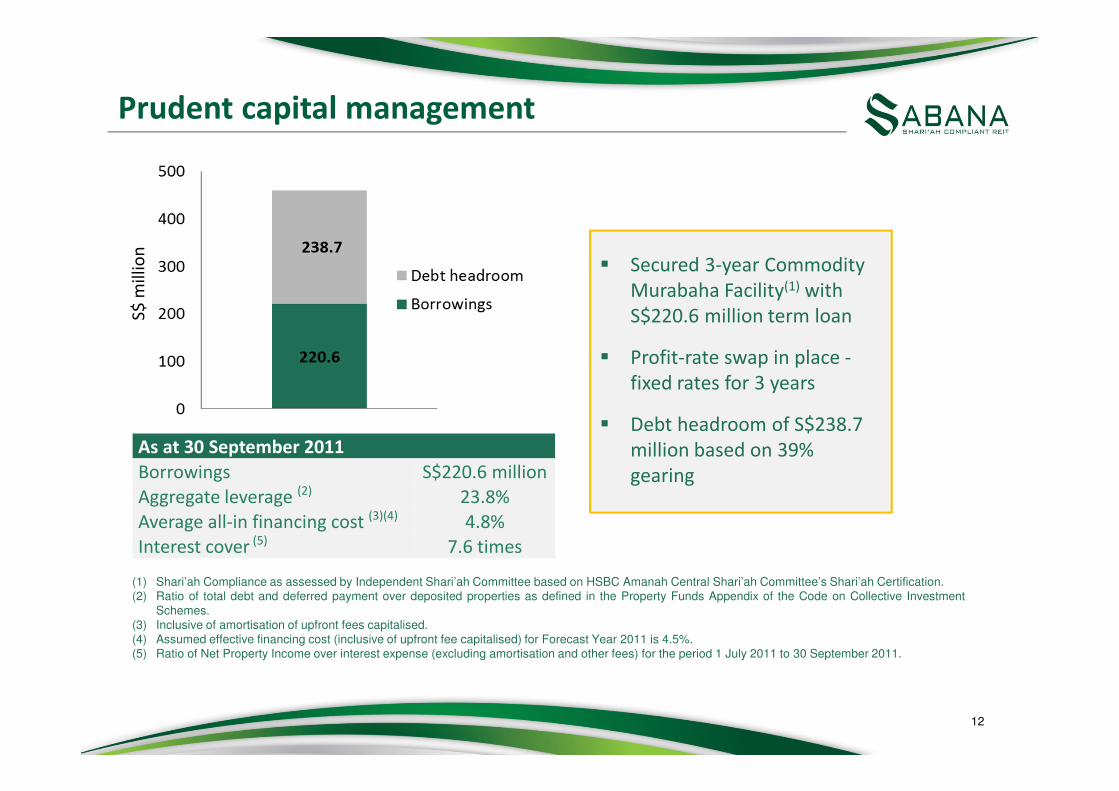

Prudent capital management

� Secured 3-year Commodity

Murabaha Facility(1) with

S$220.6 million term loan

� Profit-rate swap in place -

fixed rates for 3 years

� Debt headroom of S$238.7

million based on 39%

gearing

(1) Shari’ah Compliance as assessed by Independent Shari’ah Committee based on HSBC Amanah Central Shari’ah Committee’s Shari’ah Certification.(2) Ratio of total debt and deferred payment over deposited properties as defined in the Property Funds Appendix of the Code on Collective Investment

Schemes.(3) Inclusive of amortisation of upfront fees capitalised.(4) Assumed effective financing cost (inclusive of upfront fee capitalised) for Forecast Year 2011 is 4.5%.(5) Ratio of Net Property Income over interest expense (excluding amortisation and other fees) for the period 1 July 2011 to 30 September 2011.

12

S$

mil

lio

n

As at 30 September 2011

Borrowings S$220.6 million

Aggregate leverage (2) 23.8%

Average all-in financing cost (3)(4) 4.8%

Interest cover (5) 7.6 times

13

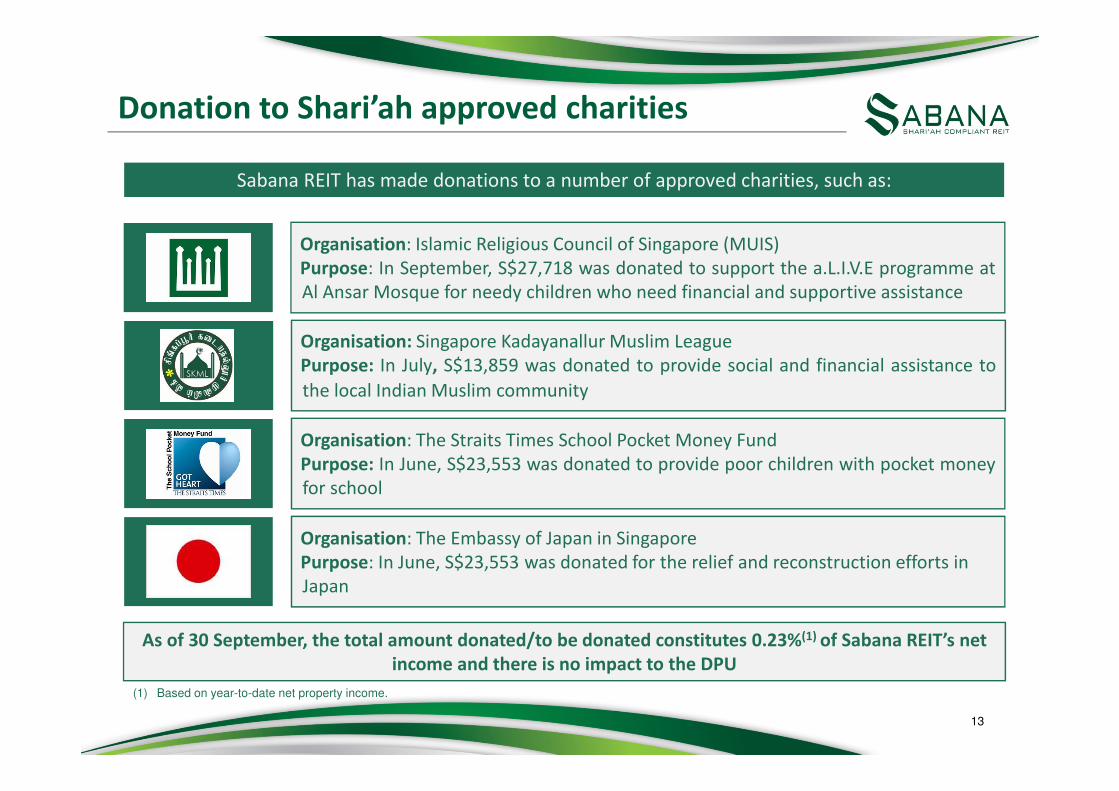

Donation to Shari’ah approved charities

Sabana REIT has made donations to a number of approved charities, such as:

As of 30 September, the total amount donated/to be donated constitutes 0.23%(1) of Sabana REIT’s net

income and there is no impact to the DPU

Organisation: Islamic Religious Council of Singapore (MUIS)

Purpose: In September, S$27,718 was donated to support the a.L.I.V.E programme at

Al Ansar Mosque for needy children who need financial and supportive assistance

Organisation: Singapore Kadayanallur Muslim League

Purpose: In July, S$13,859 was donated to provide social and financial assistance to

the local Indian Muslim community

Organisation: The Straits Times School Pocket Money Fund

Purpose: In June, S$23,553 was donated to provide poor children with pocket money

for school

Organisation: The Embassy of Japan in Singapore

Purpose: In June, S$23,553 was donated for the relief and reconstruction efforts in

Japan

(1) Based on year-to-date net property income.

14

III. Financial performance

I. About Sabana REIT

IV. Portfolio update

II. Key financial highlights

V. Market outlook

VI. Summary

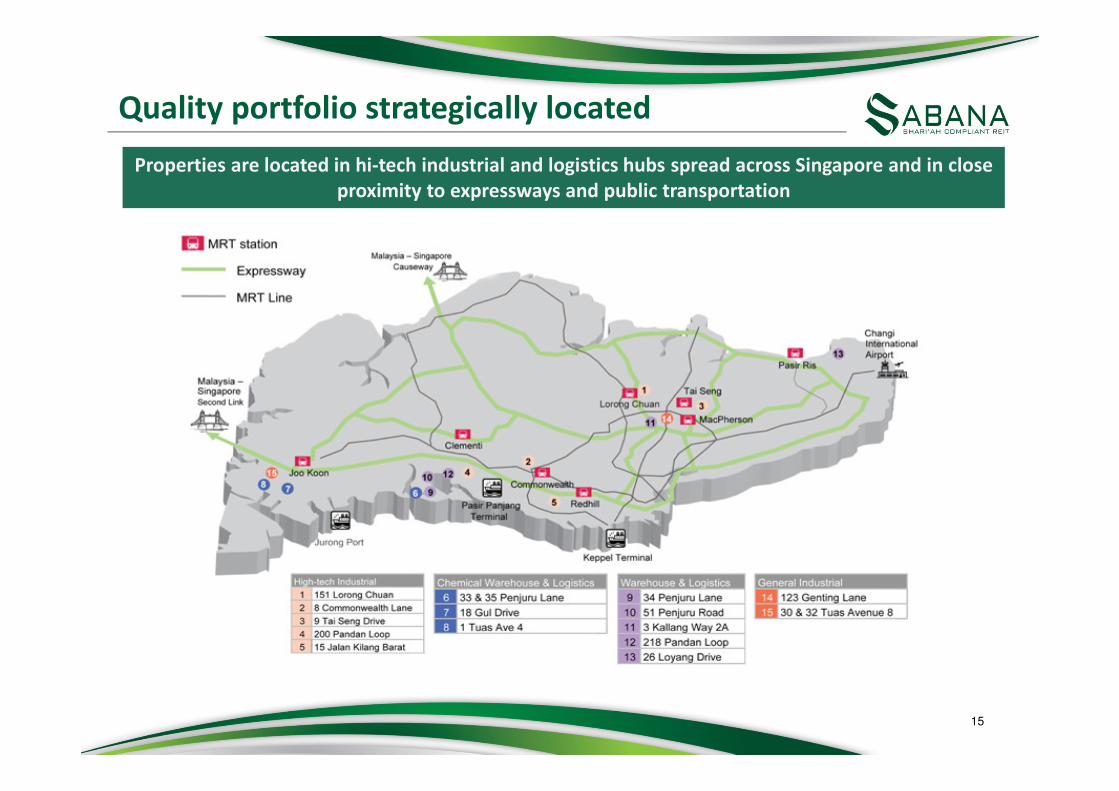

Quality portfolio strategically located

Properties are located in hi-tech industrial and logistics hubs spread across Singapore and in close

proximity to expressways and public transportation

15

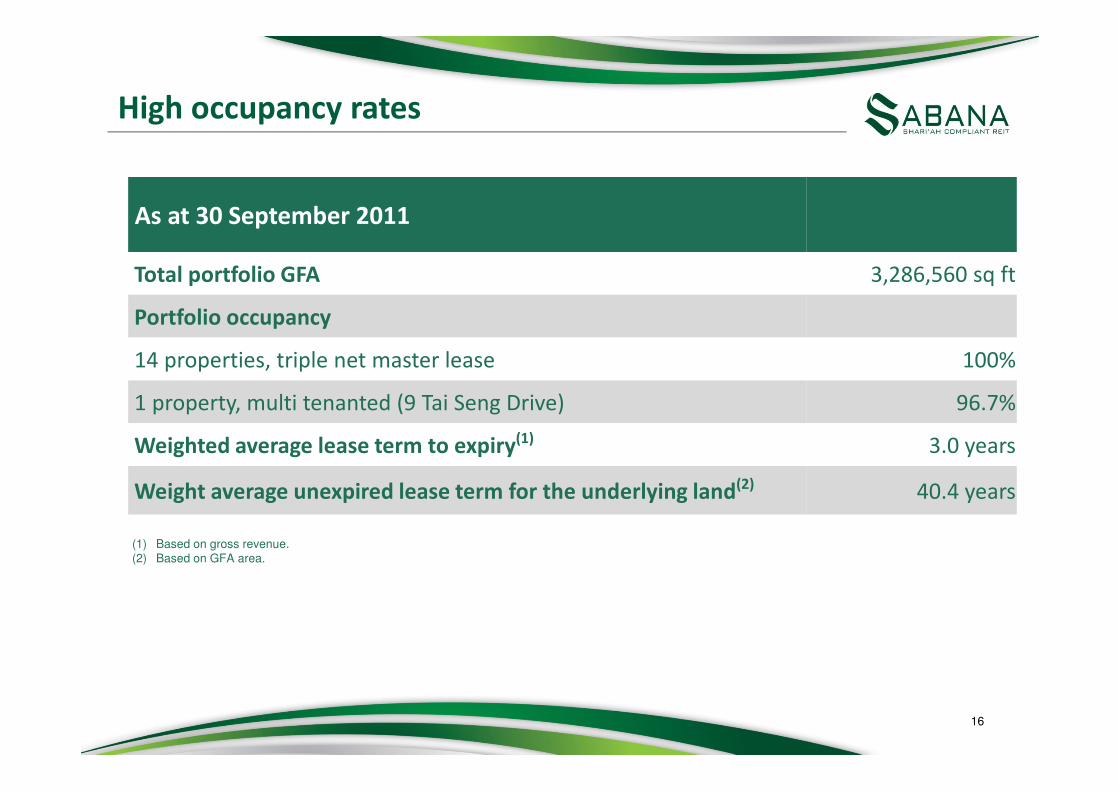

High occupancy rates

(1) Based on gross revenue.(2) Based on GFA area.

16

As at 30 September 2011

Total portfolio GFA 3,286,560 sq ft

Portfolio occupancy

14 properties, triple net master lease 100%

1 property, multi tenanted (9 Tai Seng Drive) 96.7%

Weighted average lease term to expiry(1) 3.0 years

Weight average unexpired lease term for the underlying land(2) 40.4 years

• High-tech Industrial

• Chemical Warehouse & Logistics

Asset Breakdown by GFA for 3QFY2011 Gross Revenue by Asset Type for 3QFY2011

Diverse asset types

• Warehouse & Logistics

• General Industrial

Sabana REIT’s portfolio is diversified in the following asset types:

17

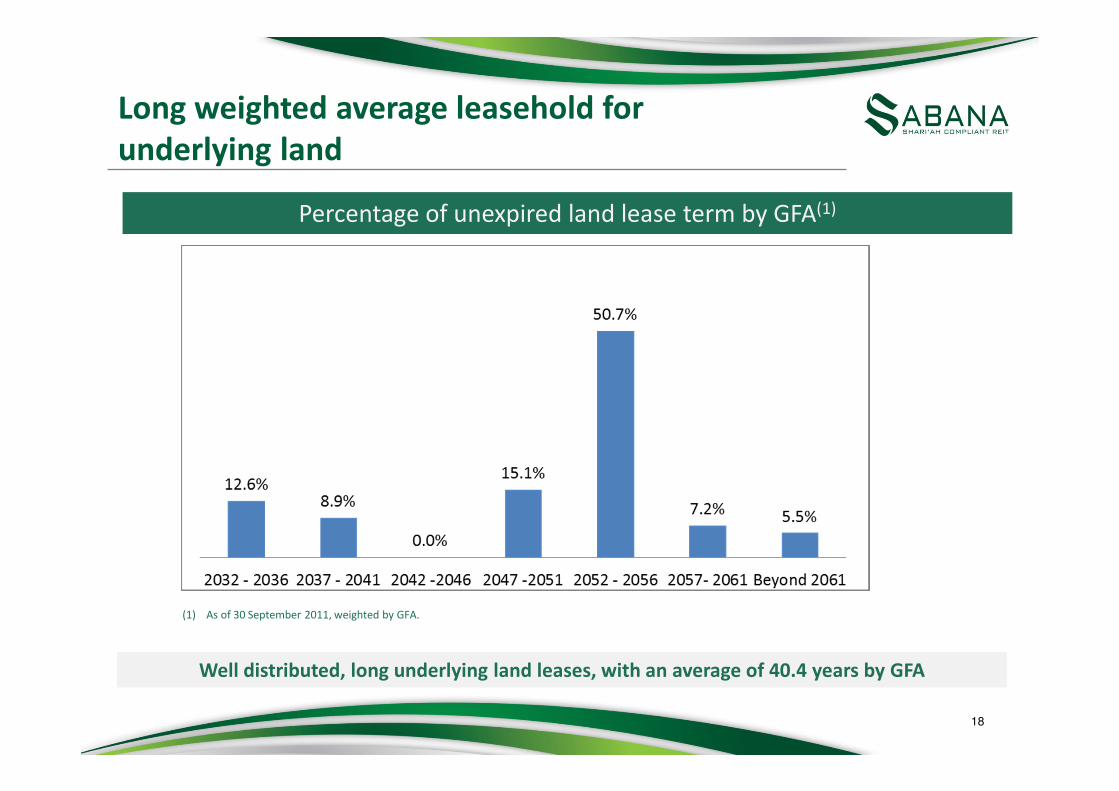

Long weighted average leasehold for

underlying land

(1) As of 30 September 2011, weighted by GFA.

Well distributed, long underlying land leases, with an average of 40.4 years by GFA

Percentage of unexpired land lease term by GFA(1)

18

Long weighted average master lease duration

Lease Expiry Profile by Gross Revenue(1)

(1) Excludes 9 Tai Seng Drive property which is not on a triple net master lease (as at 30 September 2011).

Weighted average lease term to expiry of 3.0 years provides income stability

19

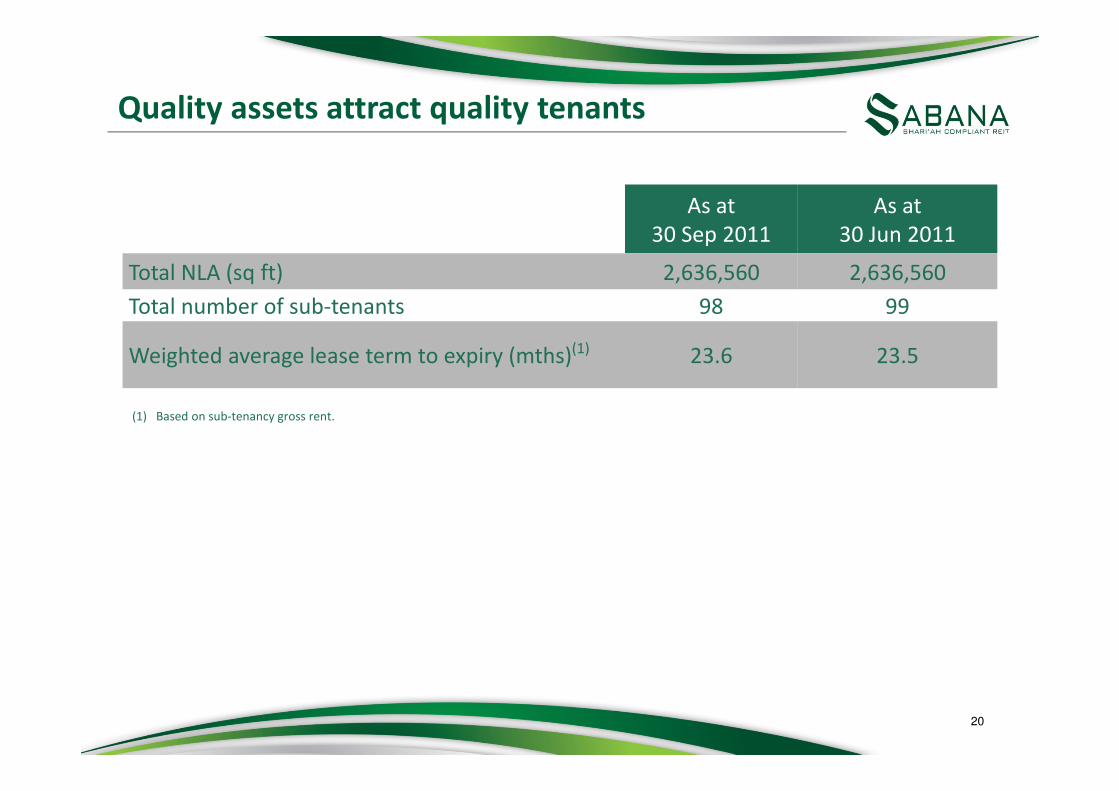

Quality assets attract quality tenants

(1) Based on sub-tenancy gross rent.

20

As at

30 Sep 2011

As at

30 Jun 2011

Total NLA (sq ft) 2,636,560 2,636,560

Total number of sub-tenants 98 99

Weighted average lease term to expiry (mths)(1) 23.6 23.5

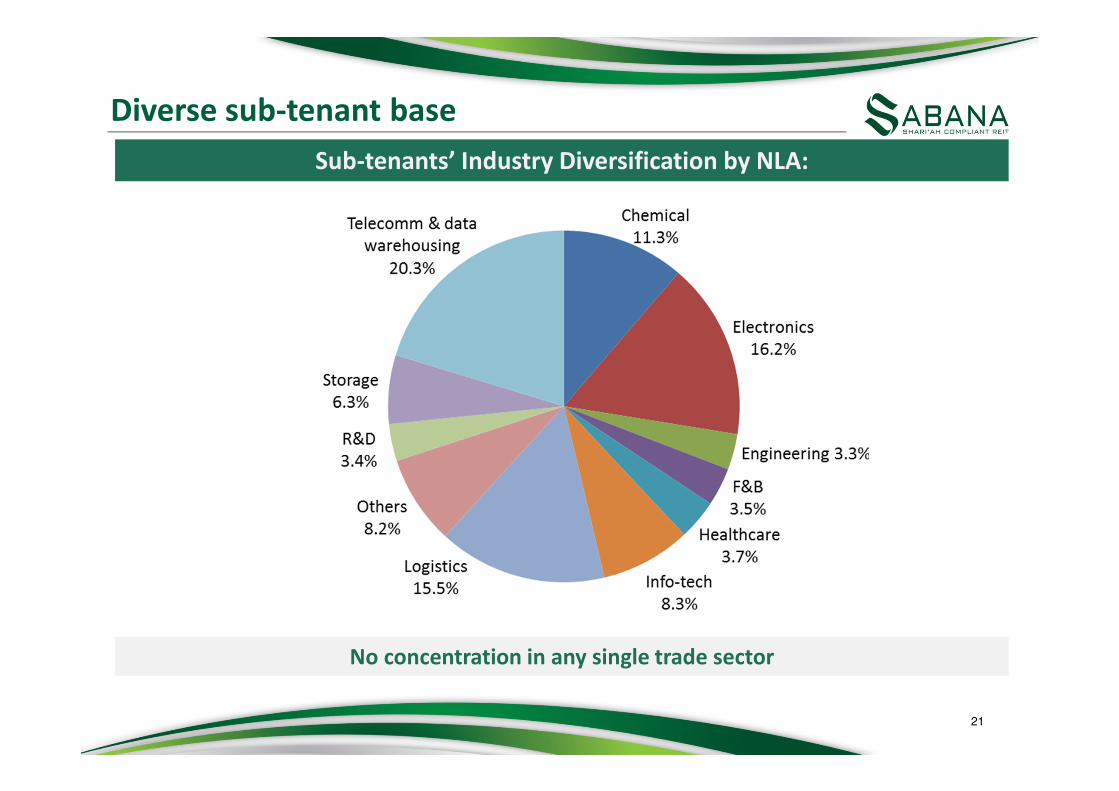

Sub-tenants’ Industry Diversification by NLA:

Diverse sub-tenant base

No concentration in any single trade sector

21

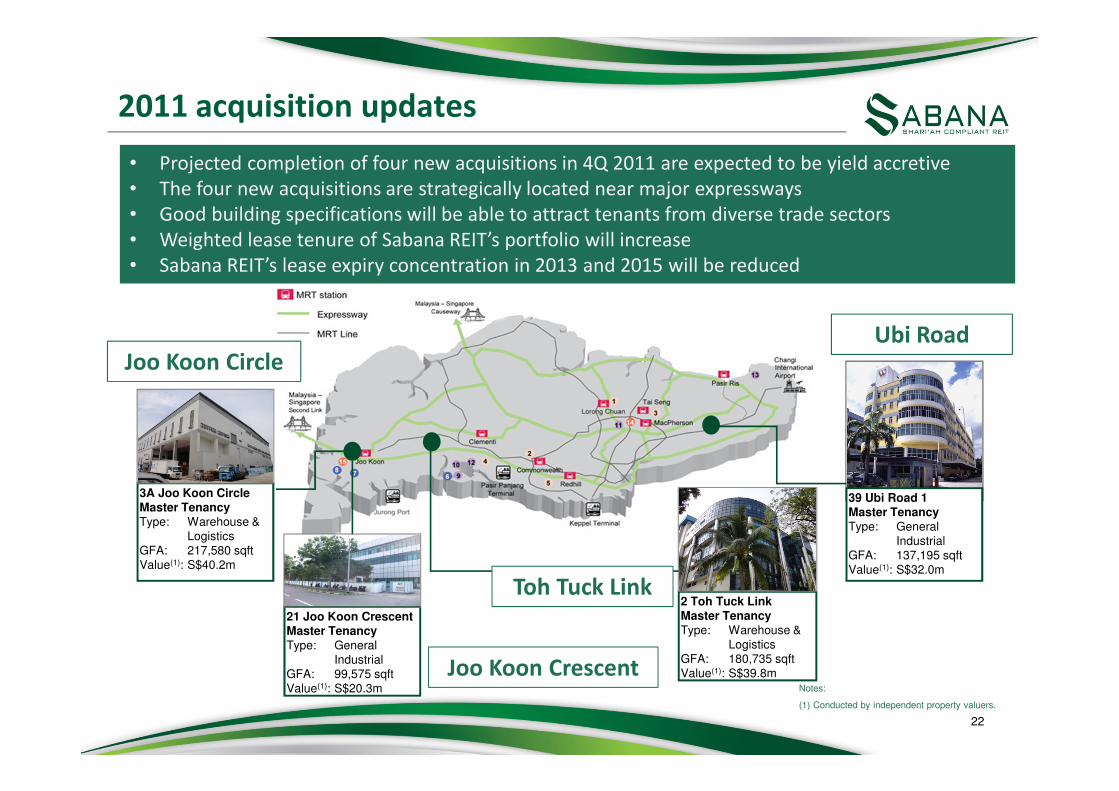

2011 acquisition updates

Notes:

(1) Conducted by independent property valuers.

22

39 Ubi Road 1Master TenancyType: General

IndustrialGFA: 137,195 sqftValue(1): S$32.0m

3A Joo Koon CircleMaster TenancyType: Warehouse &

Logistics GFA: 217,580 sqftValue(1): S$40.2m

2 Toh Tuck LinkMaster TenancyType: Warehouse &

LogisticsGFA: 180,735 sqftValue(1): S$39.8m

• Projected completion of four new acquisitions in 4Q 2011 are expected to be yield accretive

• The four new acquisitions are strategically located near major expressways

• Good building specifications will be able to attract tenants from diverse trade sectors

• Weighted lease tenure of Sabana REIT’s portfolio will increase

• Sabana REIT’s lease expiry concentration in 2013 and 2015 will be reduced

Joo Koon Circle

Toh Tuck Link

Ubi Road

21 Joo Koon CrescentMaster TenancyType: General

IndustrialGFA: 99,575 sqftValue(1): S$20.3m

Joo Koon Crescent

23

III. Financial performance

I. About Sabana REIT

IV. Portfolio update

II. Key financial highlights

V. Market outlook

VI. Summary

� According to a report by DTZ Research, average capital value of industrial space continued

to rise but at a slower rate in 3Q 2011, while average rents for industrial space remained

unchanged in 3Q 2011 compared to 2Q 2011(1).

� Colliers International is of the view that the rate of increase in industrial capital values to

be around 10% in the second half of 2011.

� On the outlook for 2012, Colliers International is opined that any gains in rents and capital

values are to moderate further from second half of 2011, level in light of the fragile

economic situation and ample supply of some 10.6 million square feet of industrial space

completing in 2012(2).

� The Singapore economy grew by 5.9% on year-on-year basis in the 3Q 2011. For the year as

a whole, the Ministry of Trade and Industry (MTI) expects GDP growth to be around 5.0%(3),

down from the earlier forecast range of 5.0% to 6.0%.

S’pore industrial property sector becomes cautious

(1) DTZ Research: Property Times, 11 October 2011, “Singapore Q3 2011 Caution sets in”.

(2) The Business Times, 15 September 2011, “What lies ahead for industrial space?”.

(3) Ministry of Trade and Industry Singapore, 14 October 2011, Press Release.

24

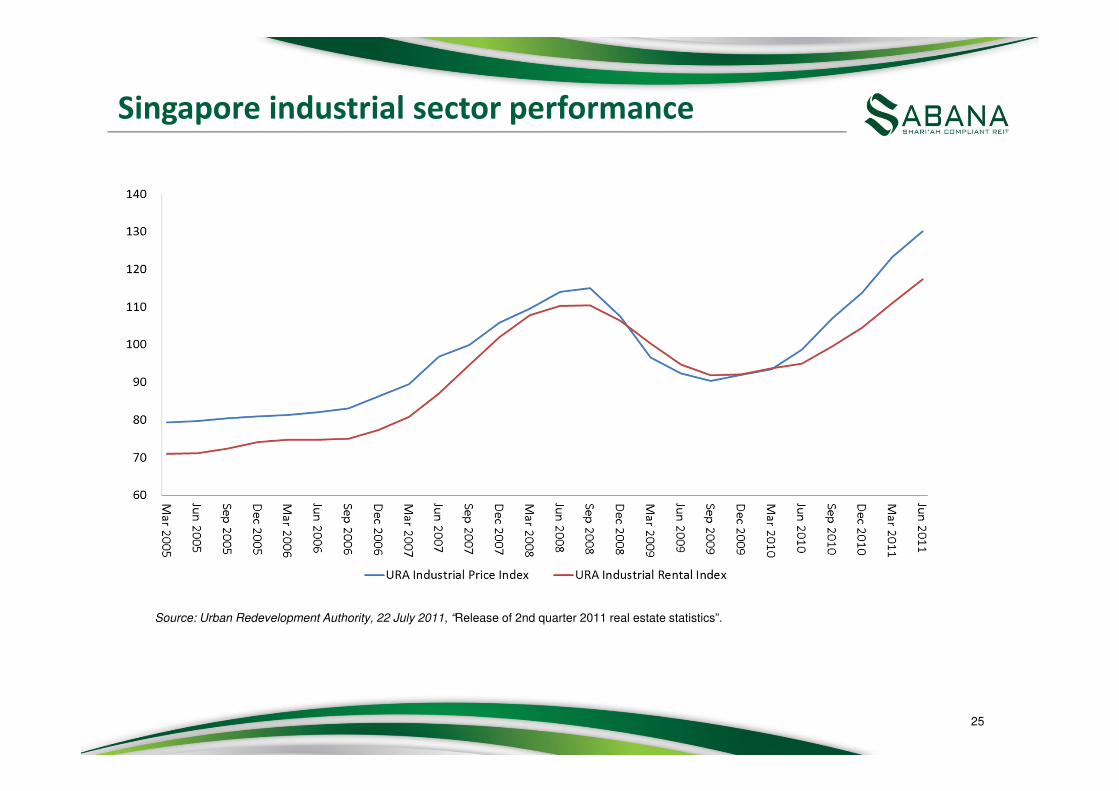

Singapore industrial sector performance

Source: Urban Redevelopment Authority, 22 July 2011, “Release of 2nd quarter 2011 real estate statistics”.

25

26

III. Financial performance

I. About Sabana REIT

IV. Portfolio update

II. Key financial highlights

V. Market outlook

VI. Summary

Summary

27

Sabana REIT will continue to drive stable and growing returns for unitholders by:

Actively sourcing

for yield accretive

acquisitions to

drive DPU growth

Substantially debt

funded

acquisitions with

the goal of

crossing S$1

billion portfolio

Focus on the

Singapore market

in the near to

medium term

Actively manage

existing portfolio

to optimize asset

performance

Distribution details

28

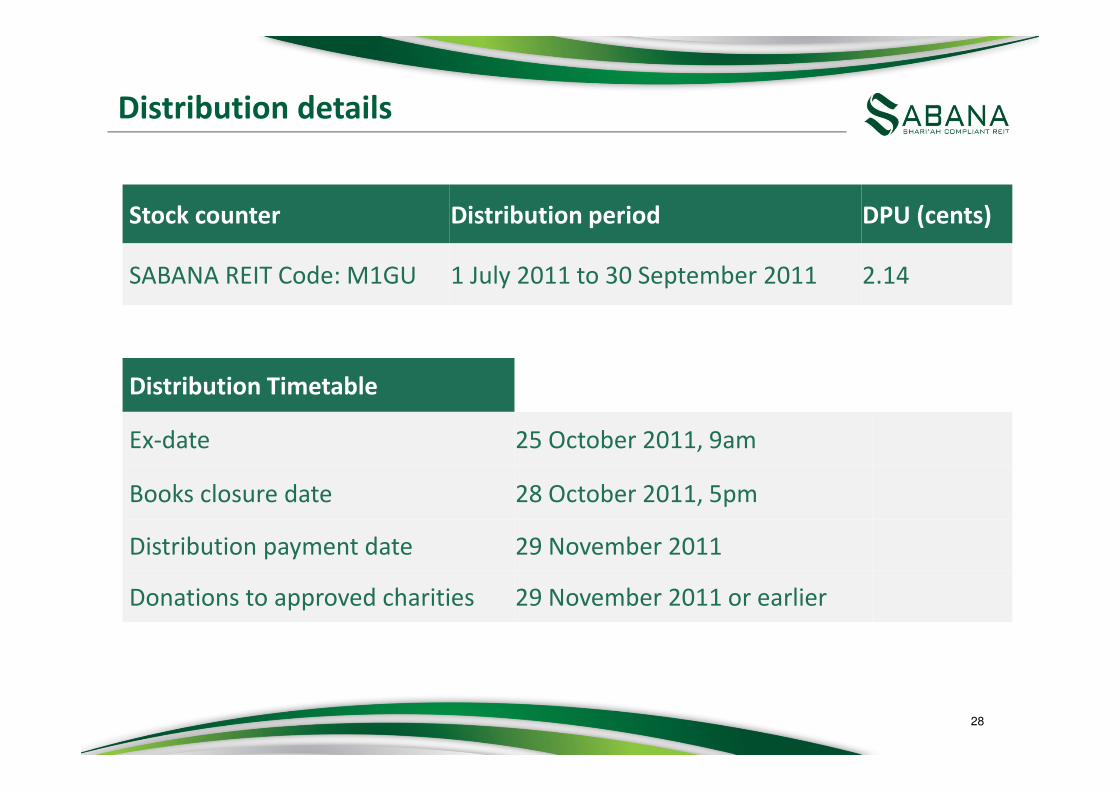

Stock counter Distribution period DPU (cents)

SABANA REIT Code: M1GU 1 July 2011 to 30 September 2011 2.14

Distribution Timetable

Ex-date 25 October 2011, 9am

Books closure date 28 October 2011, 5pm

Distribution payment date 29 November 2011

Donations to approved charities 29 November 2011 or earlier

Sabana Real Estate Investment Management Pte Ltd151 Lorong Chuan#02-03 New Tech ParkSingapore 556741

www.sabana-reit.com

Tel: +65 6580 7750Fax: +65 6280 4700

For enquires, please contact:

Mr Bobby TayChief Strategy Officer & Head of Investor RelationsTel: +65 6580 7750Email: [email protected]

Thank you!

29

Important Notice

This presentation is for information only and does not constitute an offer, invitation or solicitation of securities in Singapore orany other jurisdiction nor should it or any part of it form the basis of, or be relied upon in connection with, any contract orcommitment whatsoever.

The value of the Units and the income derived from them may fall as well as rise. Units are not obligations of, deposits in, orguaranteed by, the Manager, HSBC Institutional Trust Services (Singapore) Limited, as trustee of Sabana Shari’ah CompliantIndustrial Real Estate Investment Trust, Freight Links Express Holdings Limited, the Joint Bookrunners or any of theirrespective affiliates.

An investment in the Units is subject to investment risks, including the possible loss of the principal amount invested. Investorshave no right to request that the Manager redeem or purchase their Units while the Units are listed. It is intended thatUnitholders may only deal in their Units through trading on the SGX-ST. Listing of the Units on the SGX-ST does not guaranteea liquid market for the Units.

This presentation is not an offer or sale of the Units in the United States. The Units have not been and will not be registeredunder the United States Securities Act of 1933, as amended (the "Securities Act") and may not be offered or sold in the UnitedStates absent registration except pursuant to an exemption from, or in a transaction not subject to, registration under theSecurities Act. Any public offering of the Units to be made in the United States will be made by means of a prospectus that maybe obtained from the Manager or Sabana Shari’ah Compliant Industrial Real Estate Investment Trust and that will containdetailed information about Sabana Shari’ah Compliant Industrial Real Estate Investment Trust, the Manager and itsmanagement, as well as financial statements. Sabana Shari’ah Compliant Industrial Real Estate Investment Trust does notintend to register any portion of the offering in the United States or to conduct a public offering of securities in the United States.Accordingly, the Units are being offered and sold outside the United States (including to institutional and other investors inSingapore) in reliance on Regulation S under the Securities Act.

This presentation is not to be distributed or circulated outside of Singapore. Any failure to comply with this restriction mayconstitute a violation of United States securities laws or the laws of any other jurisdiction.

30