Embed Size (px)

Citation preview

S.3855 Actuarial Challenges

Igor Afanassiev

Prepared by Lesley Thomson

2

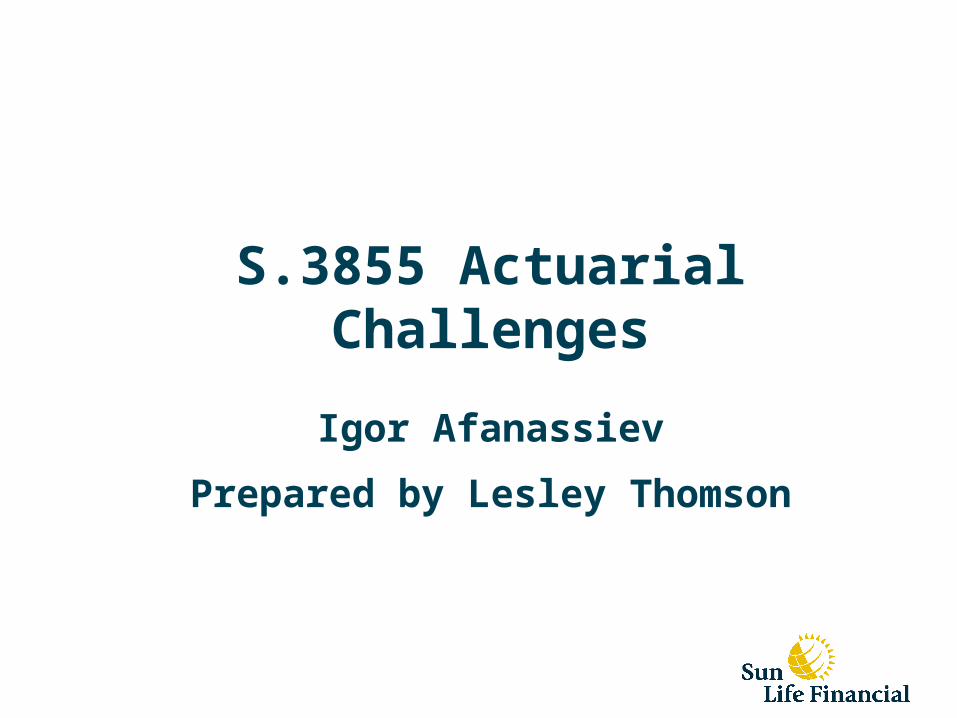

Changes to Asset Reporting

New reporting depends on asset designation

No more deferral of realized gains “Fair value option” (FVO) with OSFI restrictions

Asset Class Balance Sheet Unrealized Gains

HTM Amortized cost NI

HFT Fair value NI

AFS Fair value OCI

Loans Amortized cost NI

3

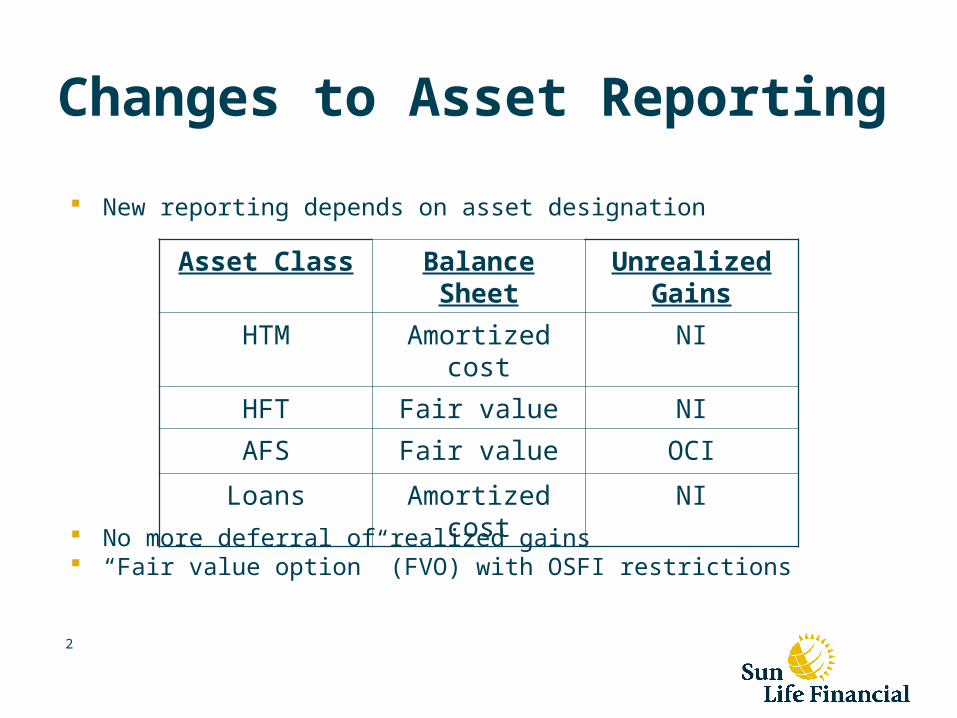

Other Comprehensive Income

“Other Comprehensive Income” is new to Canadian GAAP (US GAAP has it)

OCI is a below-the-line item of income

– Income that hasn’t been recognized yet

Unrealized gains/losses on AFS assets go to OCI, creating a disconnect between balance sheet and income statement

– Never before in Canadian GAAP

Realized gains/losses on AFS assets are transferred from OCI to “real” income

4

CALM Valuation

Policy Liabilities = Statement value of assets needed to discharge the obligations

– Based on analysis of asset and liability cash flows

If statement value of assets changes (all else being equal), the liabilities change by exactly the same amount

– CALM gets the balance sheet right

So why is 3855 a problem?

5

CALM Valuation

The disconnect between the balance sheet and income statement for AFS assets is the problem

The liability valuation gets the balance sheet right, but income will be wrong

– Income + OCI will be OK, but nobody will care

If we changed to get the income right, then the balance sheet would be wrong

6

Illustrative Example

AFS asset (MV=$1000) whose cash flows perfectly match liability cash flows. Liability value = $1000

Nothing changes except asset MV rises to $1100. Still a perfect match, so liability value = $1100

Income statement:

– Increase in asset value goes to OCI (not income)

– Increase in liability value goes to income

– $100 loss shown on income statement!

7

Solutions?

Discussed a number of possible solutions with CICA, but all were rejected

Problem is unique to insurance industry, and CICA will not create “special” rules for one industry

End result is that life insurance companies won’t use AFS assets to back liabilities

Creates a minor annoyance – different asset designations for Canadian and US GAAP

8

Issue – Valuation Timing

CALM valuation usually done a quarter in arrears

Increased volatility of asset values means using the Q3 information to set Q4 liabilities is more difficult

Different approaches for different blocks

9

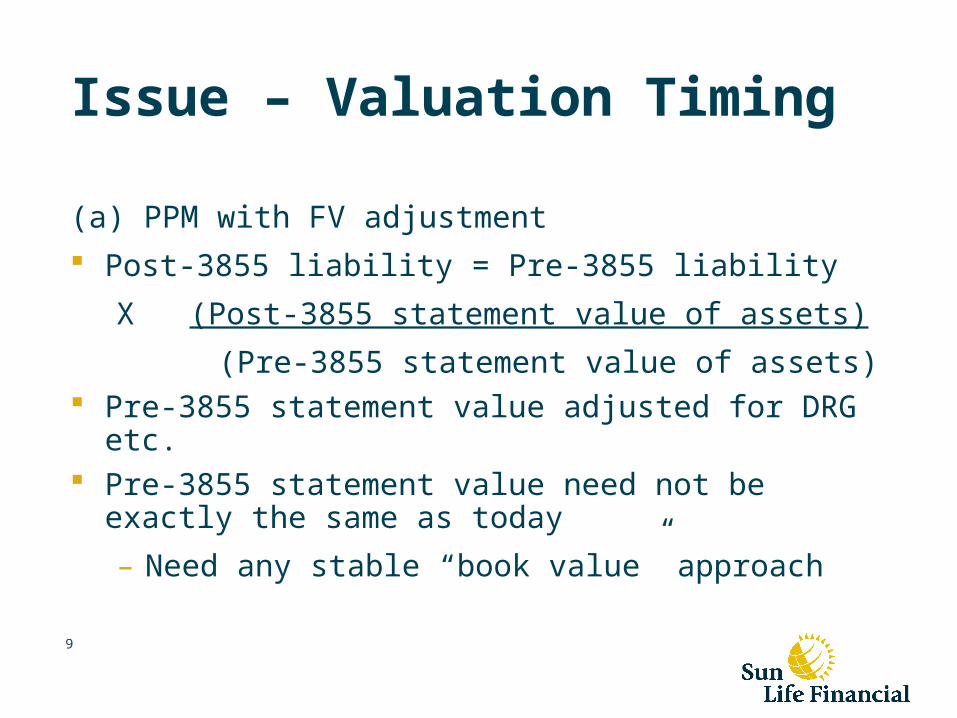

Issue – Valuation Timing

(a) PPM with FV adjustment

Post-3855 liability = Pre-3855 liability

X (Post-3855 statement value of assets)

(Pre-3855 statement value of assets) Pre-3855 statement value adjusted for DRG etc. Pre-3855 statement value need not be exactly the same as

today

– Need any stable “book value” approach

10

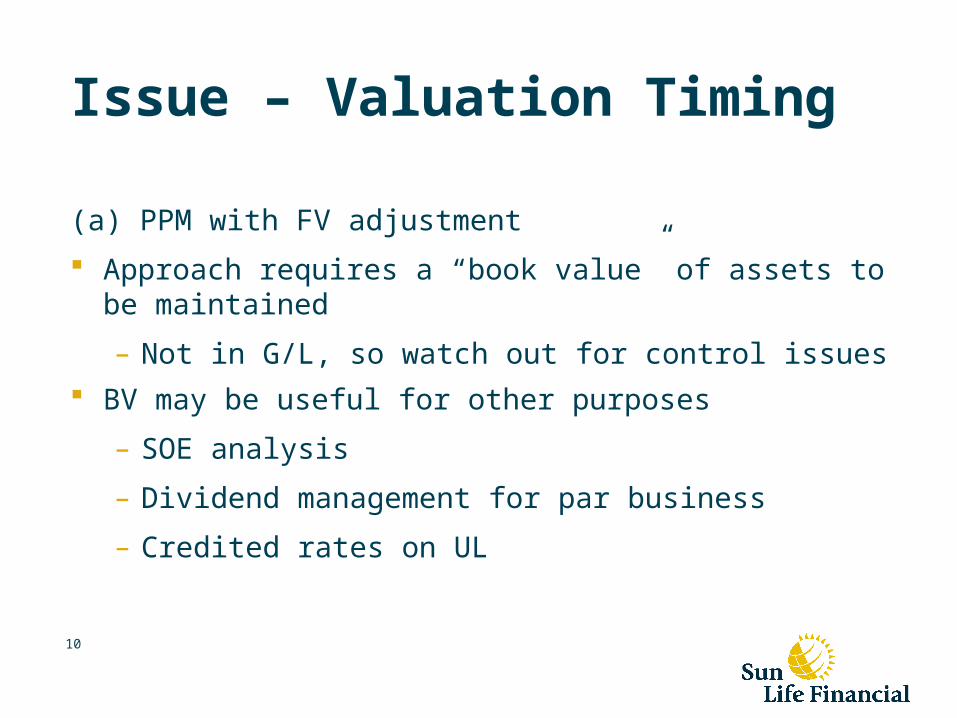

Issue – Valuation Timing

(a) PPM with FV adjustment

Approach requires a “book value” of assets to be maintained

– Not in G/L, so watch out for control issues

BV may be useful for other purposes

– SOE analysis

– Dividend management for par business

– Credited rates on UL

11

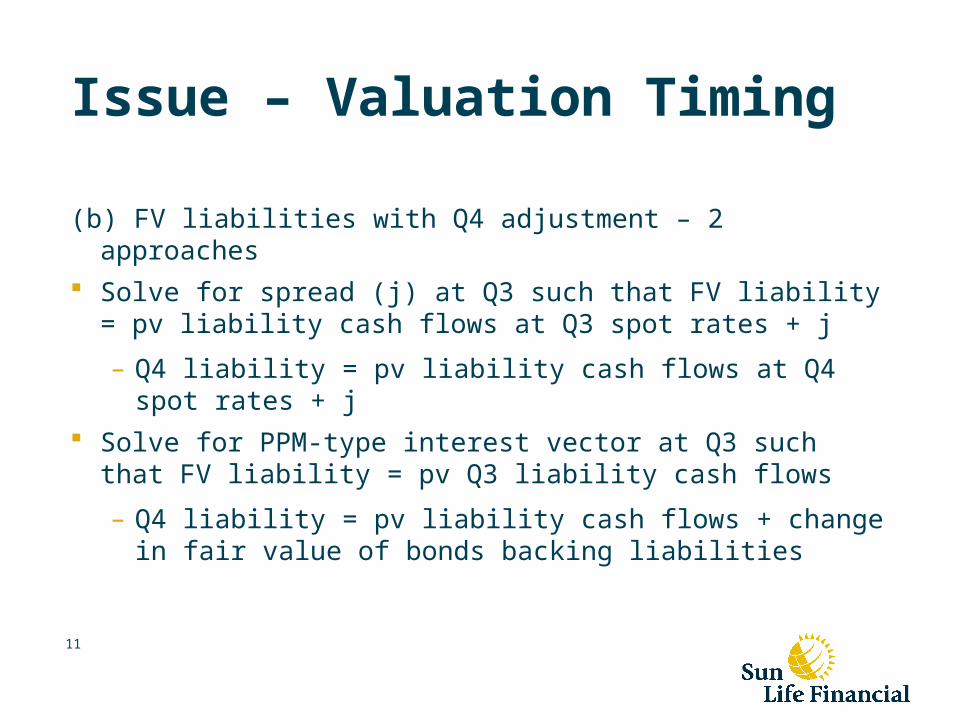

Issue – Valuation Timing

(b) FV liabilities with Q4 adjustment – 2 approaches

Solve for spread (j) at Q3 such that FV liability = pv liability cash flows at Q3 spot rates + j

– Q4 liability = pv liability cash flows at Q4 spot rates + j

Solve for PPM-type interest vector at Q3 such that FV liability = pv Q3 liability cash flows

– Q4 liability = pv liability cash flows + change in fair value of bonds backing liabilities

12

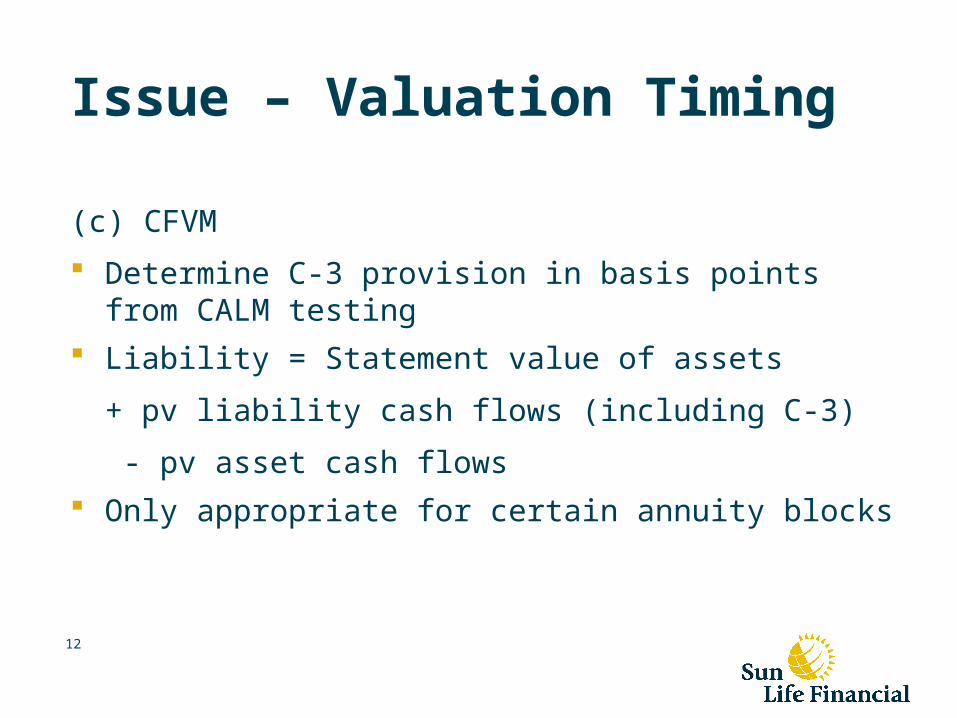

Issue – Valuation Timing

(c) CFVM

Determine C-3 provision in basis points from CALM testing

Liability = Statement value of assets

+ pv liability cash flows (including C-3)

- pv asset cash flows

Only appropriate for certain annuity blocks

13

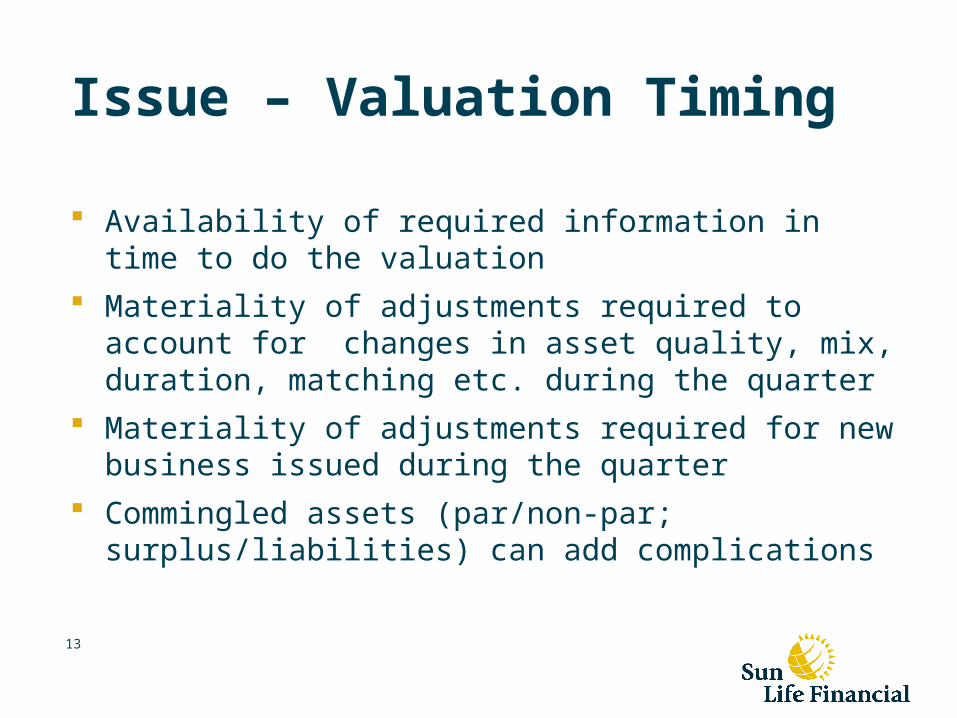

Issue – Valuation Timing

Availability of required information in time to do the valuation

Materiality of adjustments required to account for changes in asset quality, mix, duration, matching etc. during the quarter

Materiality of adjustments required for new business issued during the quarter

Commingled assets (par/non-par; surplus/liabilities) can add complications

14

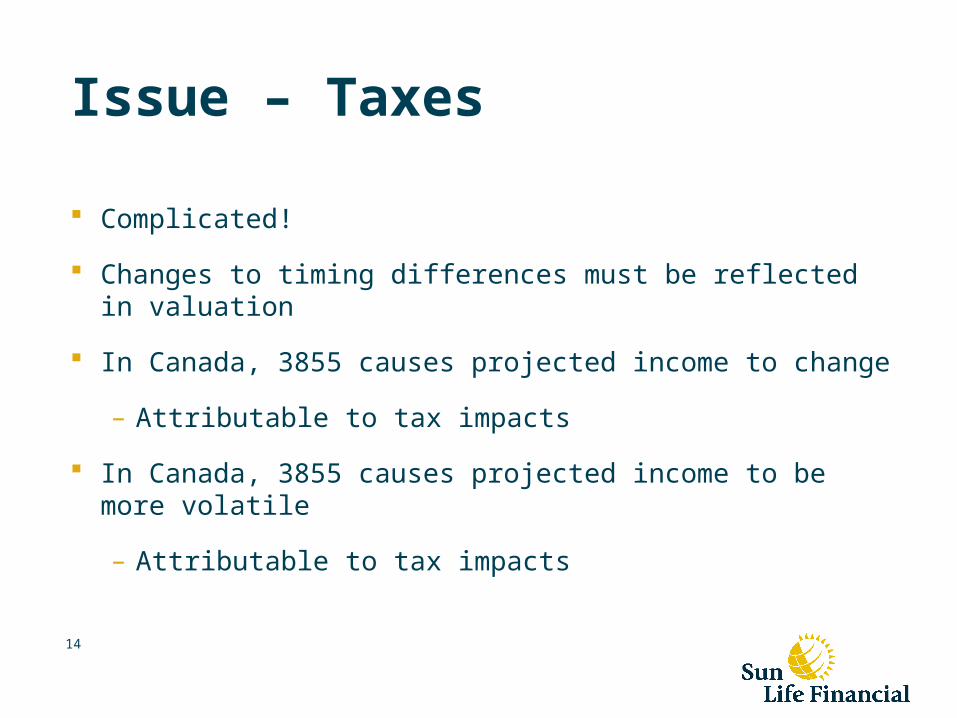

Issue – Taxes

Complicated!

Changes to timing differences must be reflected in valuation

In Canada, 3855 causes projected income to change

– Attributable to tax impacts

In Canada, 3855 causes projected income to be more volatile

– Attributable to tax impacts

15

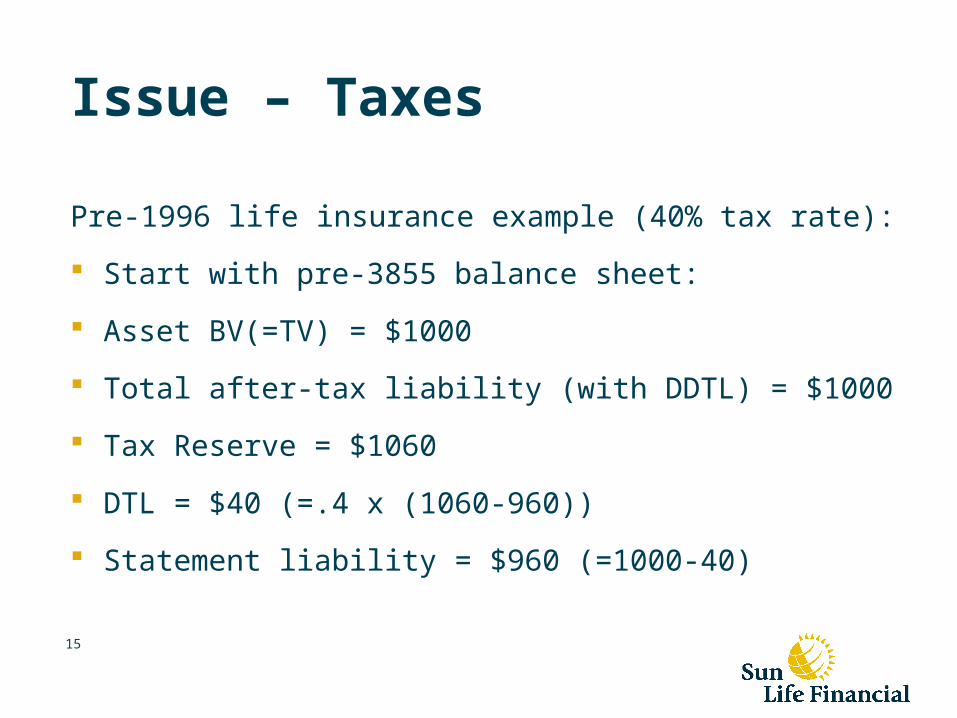

Issue – Taxes

Pre-1996 life insurance example (40% tax rate):

Start with pre-3855 balance sheet:

Asset BV(=TV) = $1000

Total after-tax liability (with DDTL) = $1000

Tax Reserve = $1060

DTL = $40 (=.4 x (1060-960))

Statement liability = $960 (=1000-40)

16

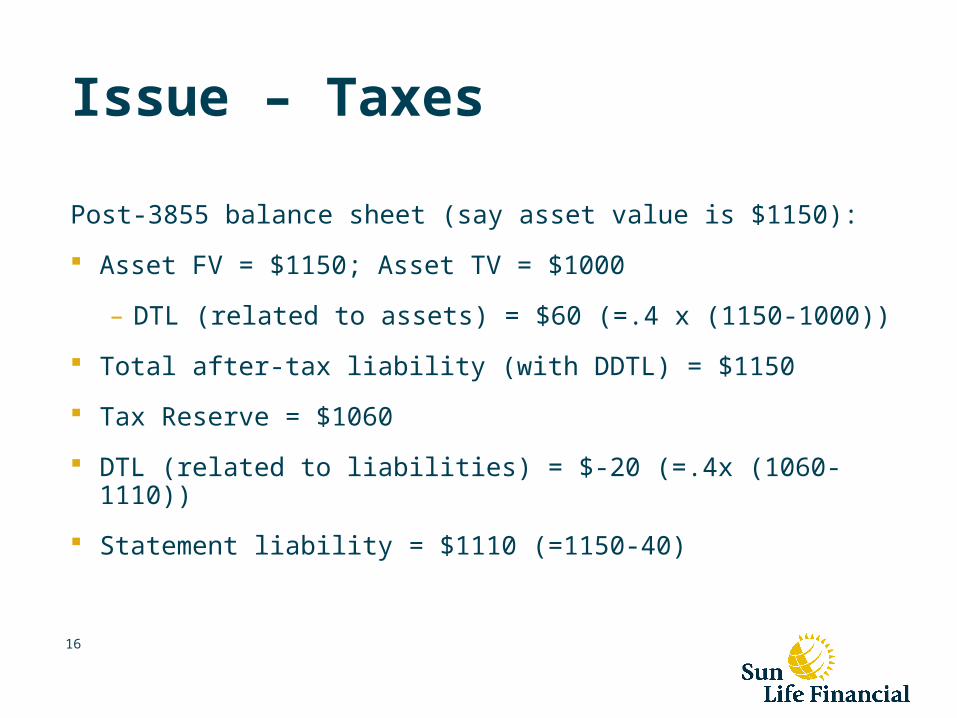

Issue – Taxes

Post-3855 balance sheet (say asset value is $1150):

Asset FV = $1150; Asset TV = $1000

– DTL (related to assets) = $60 (=.4 x (1150-1000))

Total after-tax liability (with DDTL) = $1150

Tax Reserve = $1060

DTL (related to liabilities) = $-20 (=.4x (1060-1110))

Statement liability = $1110 (=1150-40)

17

Issue – Taxes

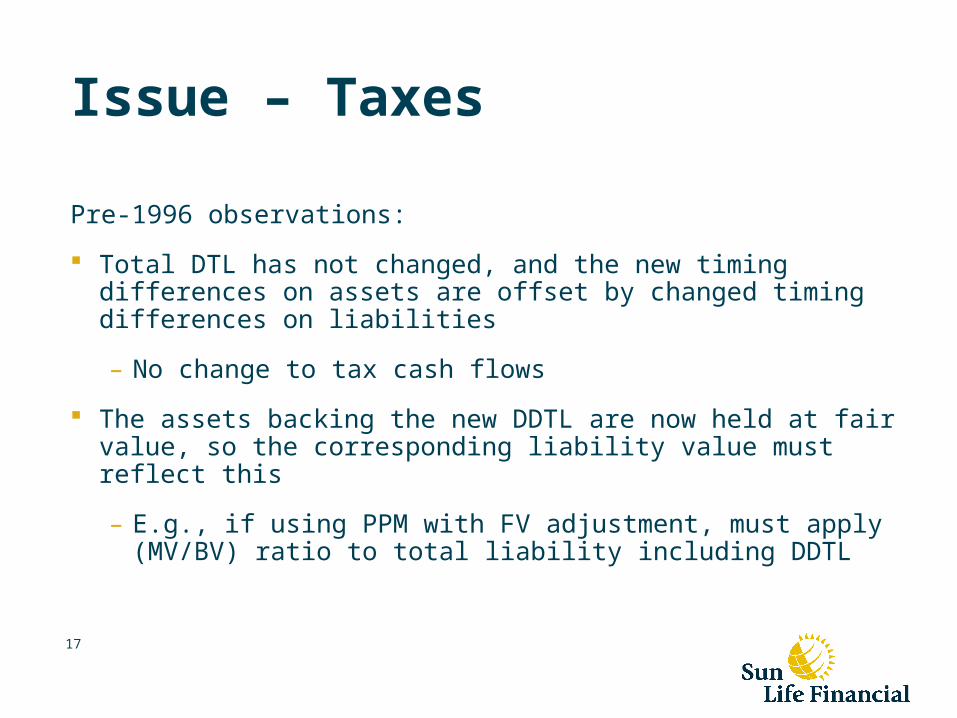

Pre-1996 observations:

Total DTL has not changed, and the new timing differences on assets are offset by changed timing differences on liabilities

– No change to tax cash flows

The assets backing the new DDTL are now held at fair value, so the corresponding liability value must reflect this

– E.g., if using PPM with FV adjustment, must apply (MV/BV) ratio to total liability including DDTL

18

Issue – Taxes

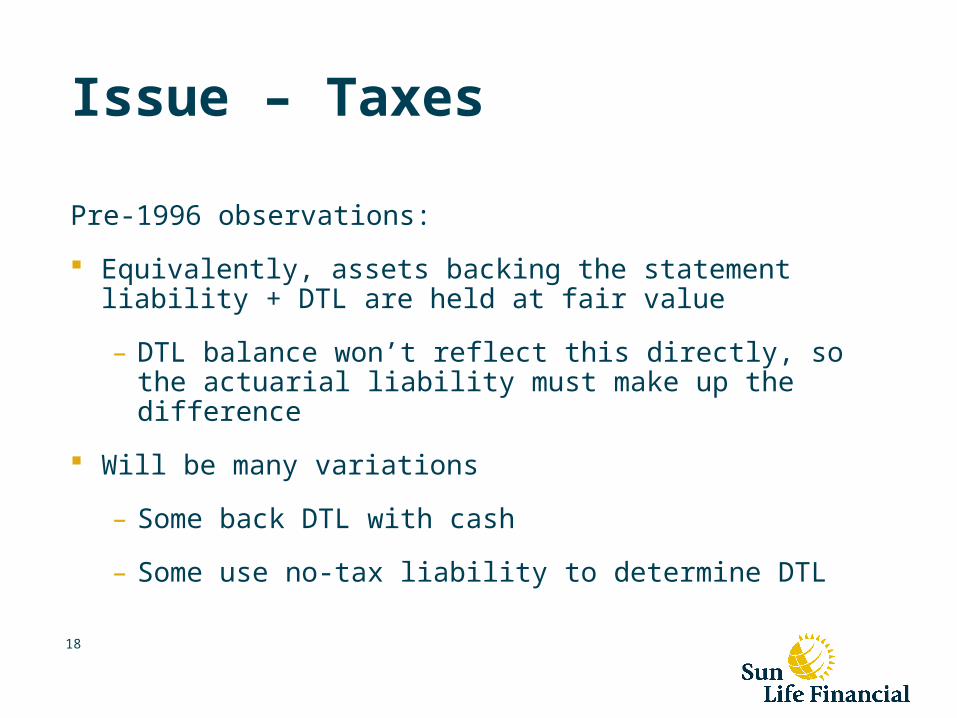

Pre-1996 observations:

Equivalently, assets backing the statement liability + DTL are held at fair value

– DTL balance won’t reflect this directly, so the actuarial liability must make up the difference

Will be many variations

– Some back DTL with cash

– Some use no-tax liability to determine DTL

19

Issue – Taxes

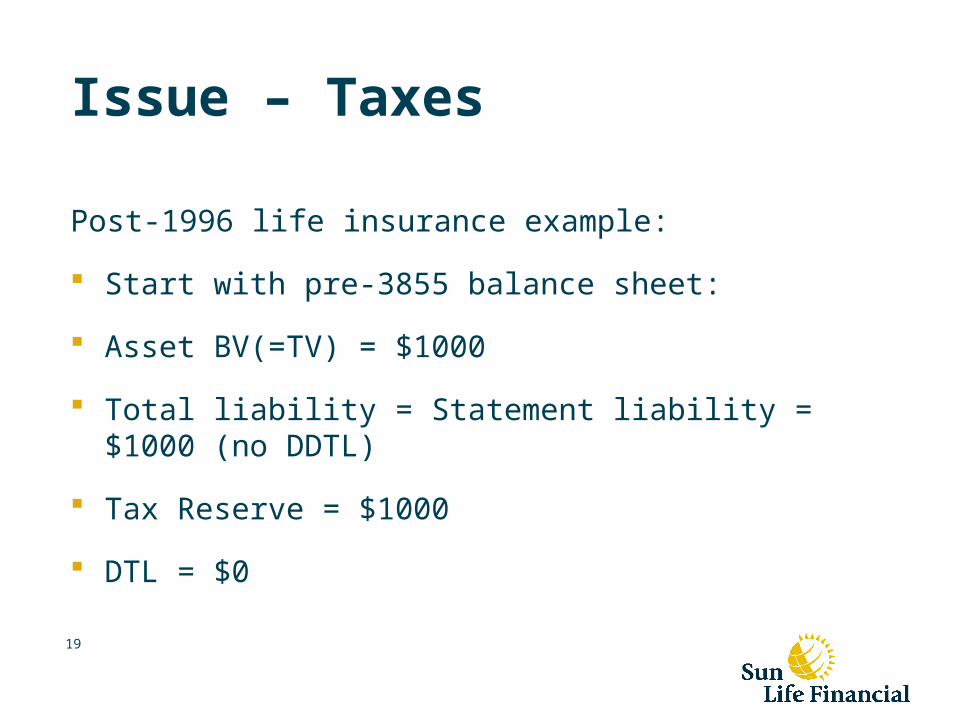

Post-1996 life insurance example:

Start with pre-3855 balance sheet:

Asset BV(=TV) = $1000

Total liability = Statement liability = $1000 (no DDTL)

Tax Reserve = $1000

DTL = $0

20

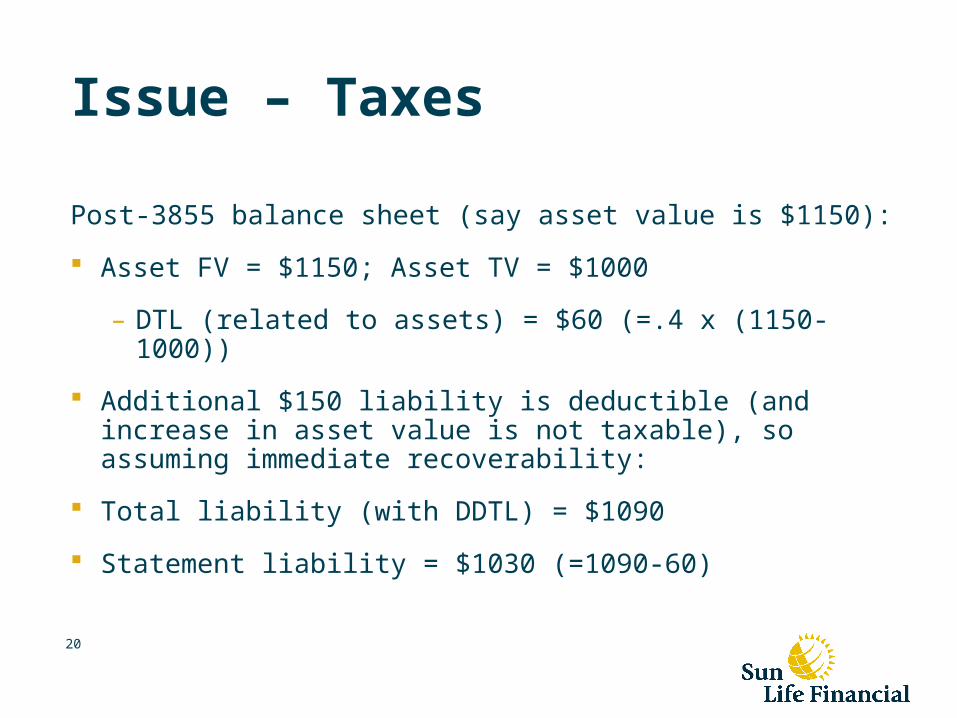

Issue – Taxes

Post-3855 balance sheet (say asset value is $1150):

Asset FV = $1150; Asset TV = $1000

– DTL (related to assets) = $60 (=.4 x (1150-1000))

Additional $150 liability is deductible (and increase in asset value is not taxable), so assuming immediate recoverability:

Total liability (with DDTL) = $1090

Statement liability = $1030 (=1090-60)

21

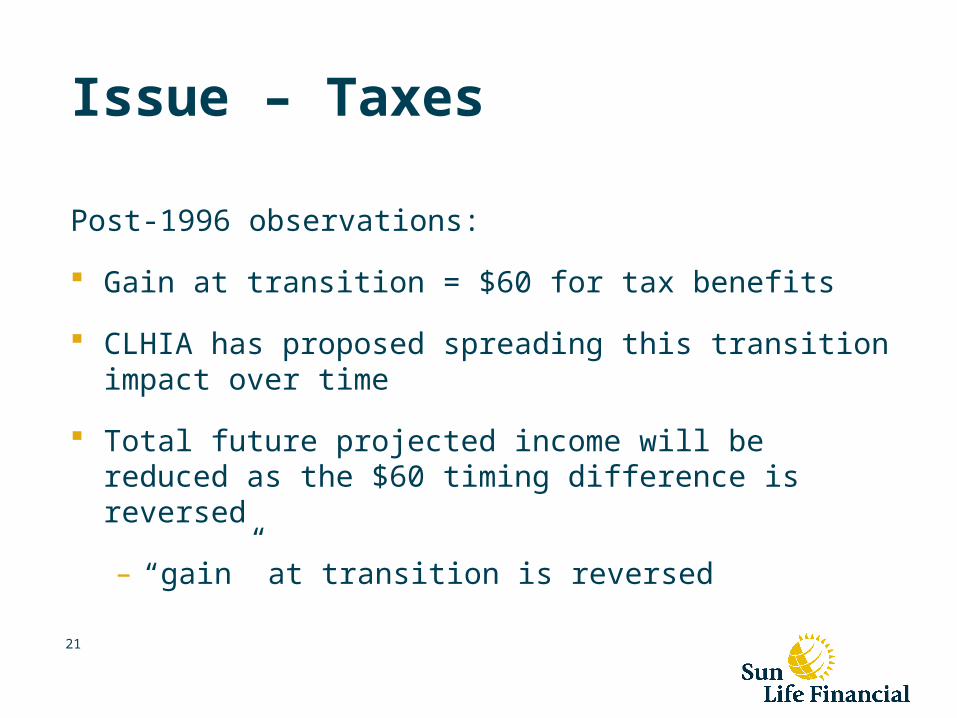

Issue – Taxes

Post-1996 observations:

Gain at transition = $60 for tax benefits

CLHIA has proposed spreading this transition impact over time

Total future projected income will be reduced as the $60 timing difference is reversed

– “gain” at transition is reversed

22

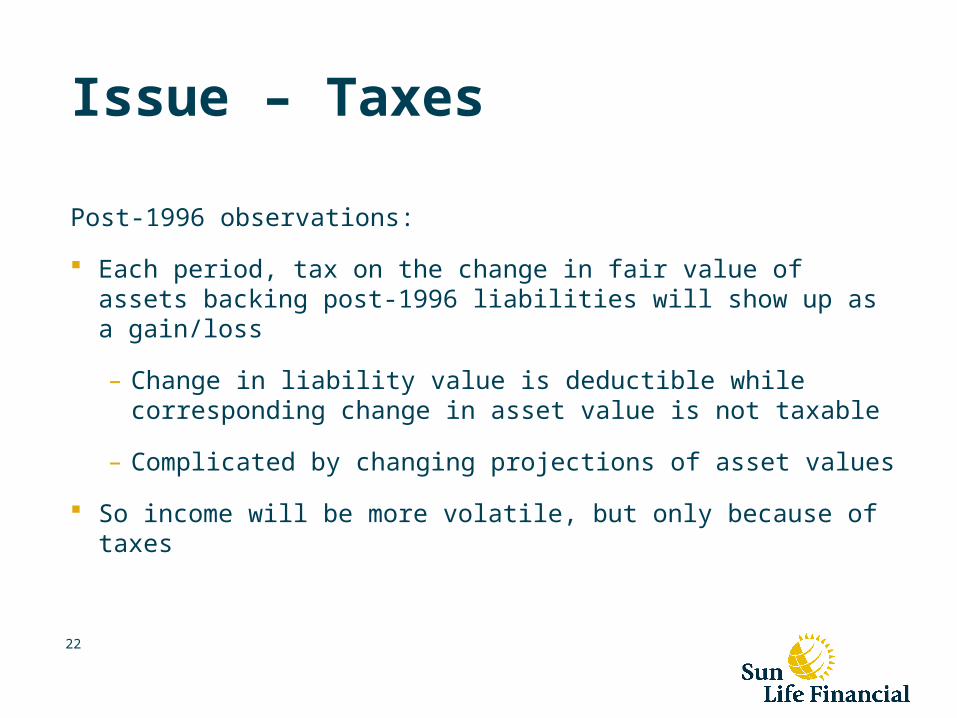

Issue – Taxes

Post-1996 observations:

Each period, tax on the change in fair value of assets backing post-1996 liabilities will show up as a gain/loss

– Change in liability value is deductible while corresponding change in asset value is not taxable

– Complicated by changing projections of asset values

So income will be more volatile, but only because of taxes

23

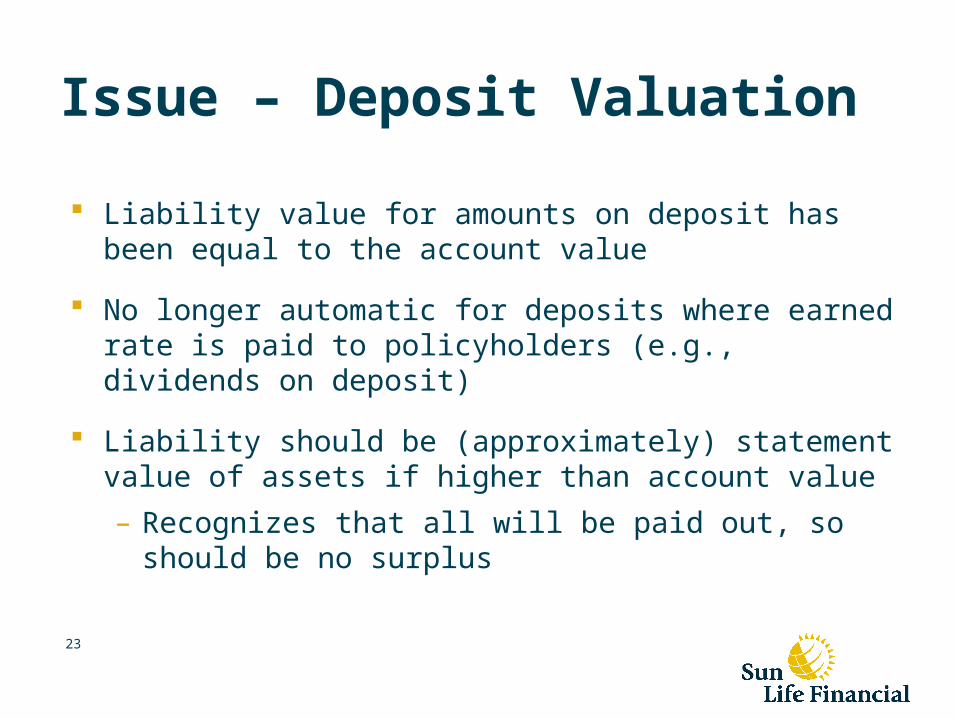

Issue – Deposit Valuation

Liability value for amounts on deposit has been equal to the account value

No longer automatic for deposits where earned rate is paid to policyholders (e.g., dividends on deposit)

Liability should be (approximately) statement value of assets if higher than account value

– Recognizes that all will be paid out, so should be no surplus

24

Issue – MCCSR

MCCSR required capital will increase

Asset values increasing and liability values increasing

Some required capital factors are a simple percentage of assets or liabilities

Some OCI will be Tier 2 instead of Tier 1 capital

25

Issue – Dividends

Policyholder dividends in many countries are set based on book rates of return

Book rates of return will no longer be easily available

Same problem for setting credited rates of interest on UL-type business

26

Issue – Sources of Earnings

SOE analysis is more complex when using market values

One solution is to continue SOE analysis on “book value” basis and add a line for impacts due to MV fluctuations

Analysts are beginning to react, and may want additional disclosures

27

Issue – Intersegment Trading

Intersegment trading of assets is done at market value

– Creates a “notional” realization of gains/losses for internal reporting

– Adjustments net to zero for external reporting

Too difficult to do this for AFS assets (notional accounting is far more complex with OCI)

Sun Life solution is to prohibit intersegment trading of AFS assets

28

Issue – Hybrid Segments

“Hybrid” segments containing both AFS and HFT assets will generally be prohibited at Sun Life

Accounting is too complex

So no mixing of liabilities and surplus, except for immaterial amounts

29

Issue – SOX Compliance

SOX processes will need to be reviewed for 3855 changes

Additional disclosures at transition (e.g., statement of balance sheet changes) may require special SOX controls

30

Issue – AuG43

Additional AuG43 audit requirements coming at the same time

Approach to valuation will need to be well documented

31

Issue – Disclosure

Disclosure requirements likely to increase

Both to OSFI (e.g., to satisfy FVO) and externally

Recent analyst report indicated they wanted disclosure of change in policy liabilities caused by changes in interest rates

– “Investment income” line of won’t be as meaningful as before

32

Issue – Reporting Changes

DCAT

SOE

EV, VNB

Business Plans

AAR

Notes, MD&A Disclosures

33

Issue - Transition

Tax, capital transition rules not yet finalized

DNRG balances written off, so never get to report the income on the balance sheet (only for surplus assets)

Treatment of deferred unrealized gains on equities still unresolved

Change from book to market value booked to retained earnings, not income

– Except AFS goes to OCI, and later to NI

34