Embed Size (px)

DESCRIPTION

investment banking in Singapore

Citation preview

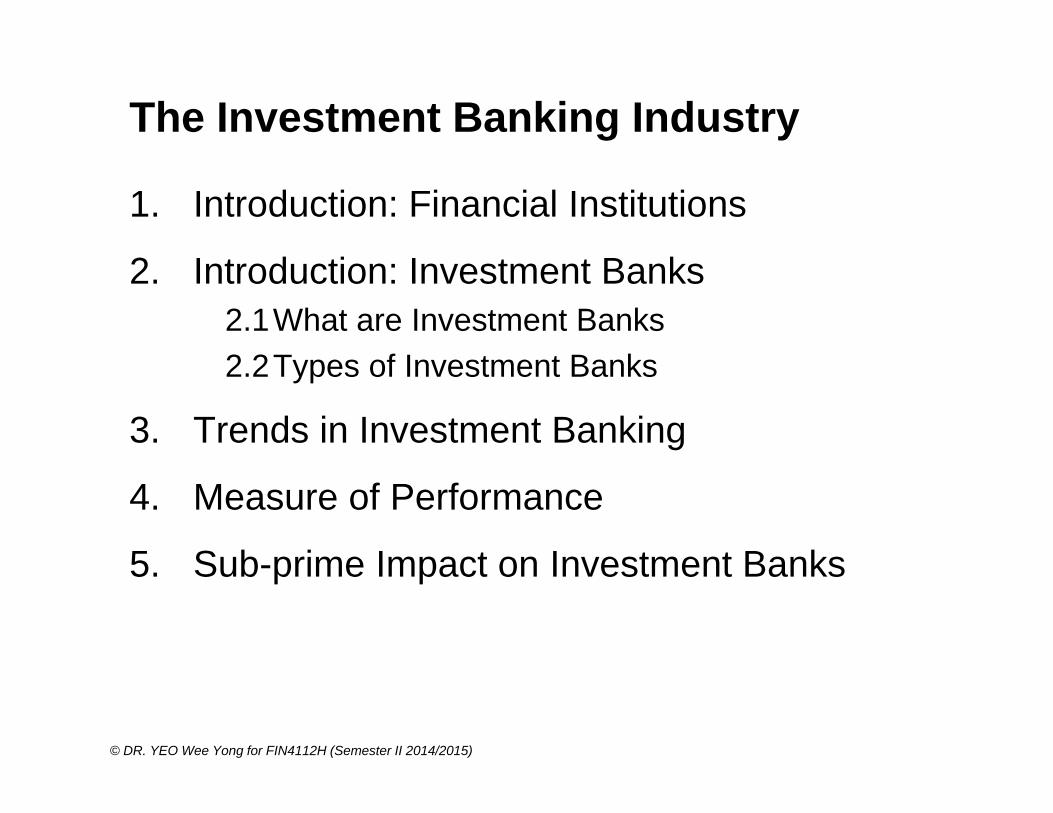

The Investment Banking Industry

1. Introduction: Financial Institutions

2. Introduction: Investment Banks2.1What are Investment Banks2.2Types of Investment Banks

3. Trends in Investment Banking

4. Measure of Performance

5. Sub-prime Impact on Investment Banks

© DR. YEO Wee Yong for FIN4112H (Semester II 2014/2015)

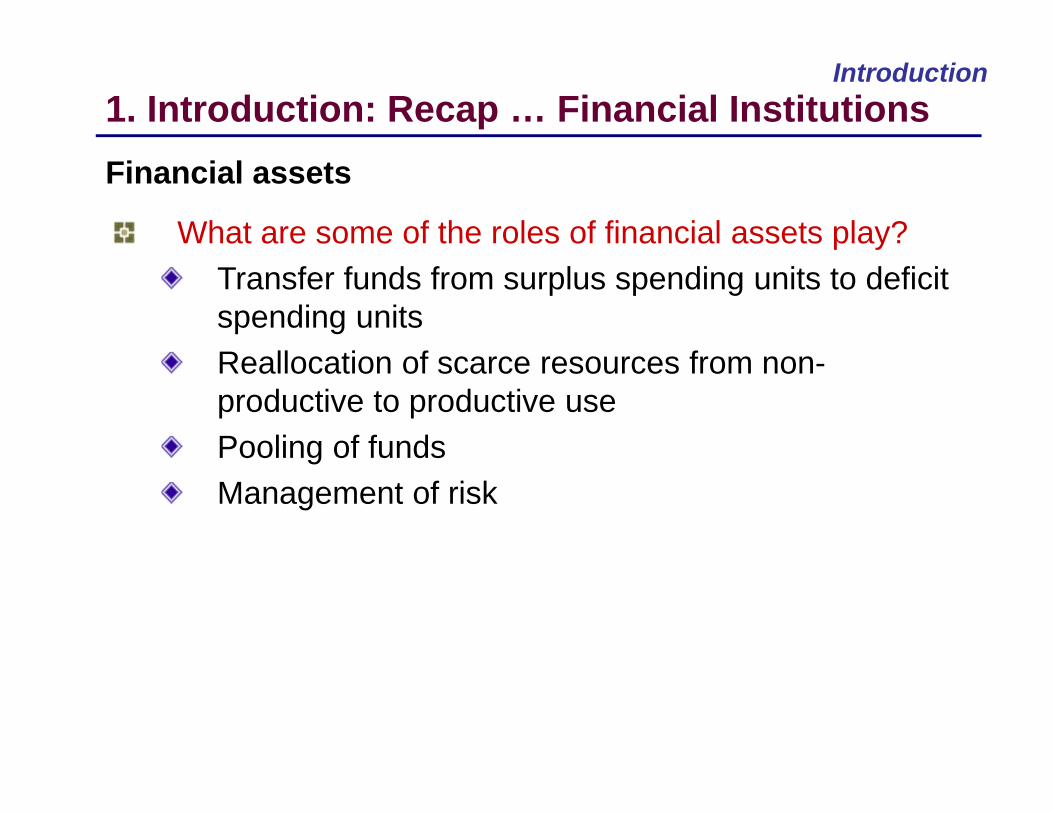

Financial assets

1. Introduction: Recap … Financial InstitutionsIntroduction

What are some of the roles of financial assets play?Transfer funds from surplus spending units to deficit spending unitsReallocation of scarce resources from non-productive to productive usePooling of fundsManagement of risk

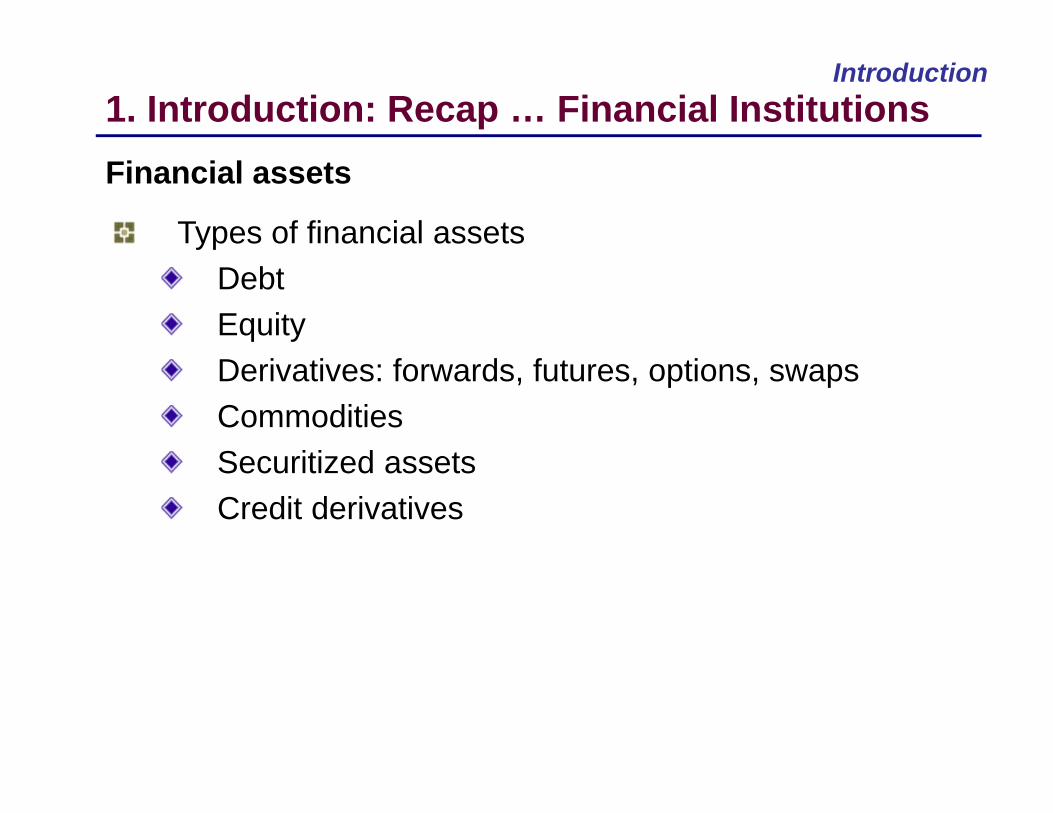

Financial assets

Introduction

Types of financial assetsDebtEquityDerivatives: forwards, futures, options, swapsCommoditiesSecuritized assetsCredit derivatives

1. Introduction: Recap … Financial Institutions

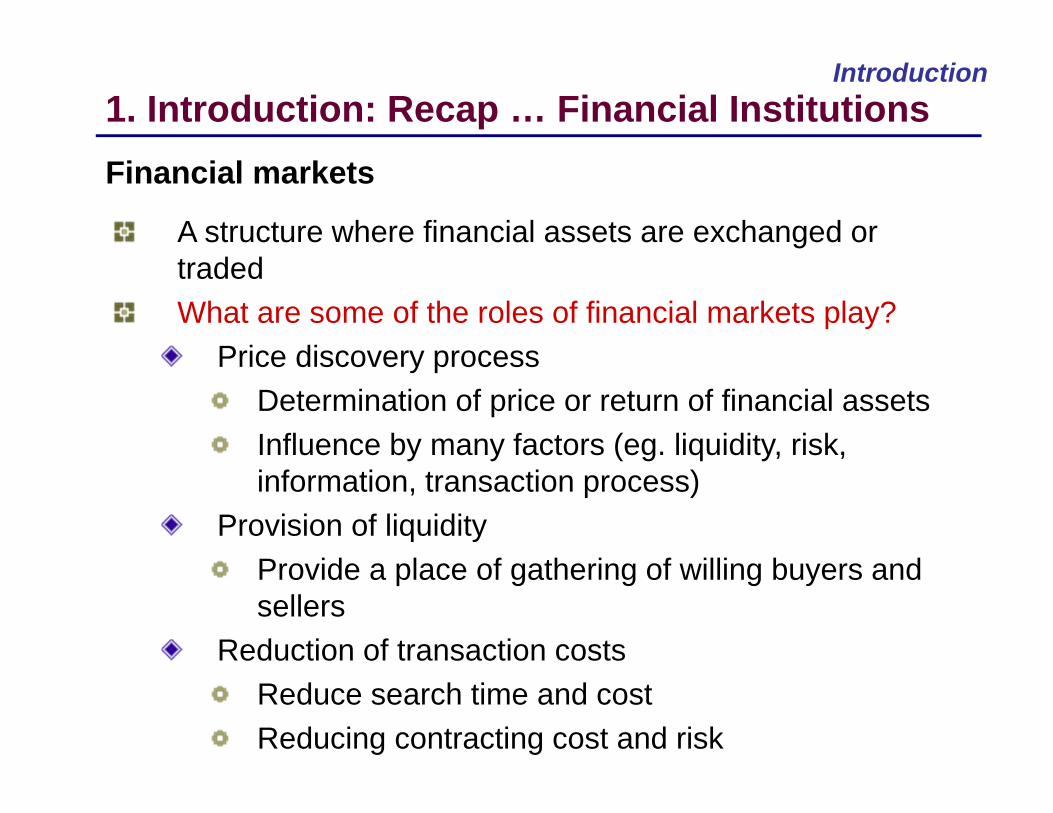

Financial markets

Introduction

A structure where financial assets are exchanged or tradedWhat are some of the roles of financial markets play?

Price discovery processDetermination of price or return of financial assetsInfluence by many factors (eg. liquidity, risk, information, transaction process)

Provision of liquidityProvide a place of gathering of willing buyers and sellers

Reduction of transaction costsReduce search time and costReducing contracting cost and risk

1. Introduction: Recap … Financial Institutions

Financial markets

Introduction

Types of financial marketsThere are many ways to classify

Primary and secondaryPrimary:

New IssuesIPO and SEO

Secondary: Trading of issued assets

Debt, equity, or derivatives

1. Introduction: Recap … Financial Institutions

Financial markets

Introduction

Types of financial marketsThere are many ways to classify

Money and capitalMoney: Short-term: 1 year or less

Federal funds and discount windowsT-billsShort-term municipal securitiesCertificates of deposits (negotiable and nonnegotiable)Repurchase agreementCommercial papers

1. Introduction: Recap … Financial Institutions

Financial markets

Introduction

Types of financial marketsThere are many ways to classify

Money and capitalCapital: More than 1 year

Stocks and bondsExchange or OTCSpot or forward, future

1. Introduction: Recap … Financial Institutions

What are investment banks?

2. Introduction: Investment BanksIntroduction

Investment banks are financial institutions that engage in public and private market transactions for corporations, governments, and investors

Examples of market transactions:Fund sourcing: Issuance of equity and debt securitiesMergers and Acquisition or M & ADivestitures

What are investment banks?

2. Introduction: Investment BanksIntroduction

Other activities: Proprietary trading: trades on its own capitalSecuritization: pooling and repackaging of financial assets into securities: Pros and Cons?Financial engineering: using mathematical and numerical methods and simulations to create financial products, or to make trading, hedging and investment decisions

What are investment banks?

2. Introduction: Investment BanksIntroduction

Other activities: Investment management: helping individual and institutions to invest Prime brokerage

The offering of tools and services to clients to support their operations in trading and portfolio managementExample of services offered: lending of securities and funds, to hedge funds and other professional investors to support their investment strategies

Types of investment banks

2. Introduction: Investment BanksIntroduction

Financial holding companiesLarge financial companies, under universal banking, have always existed in places other than the USGramm-Leach-Bliley Act 1999 created large financial holding companies in the USExamples: HSBC, Deutsche Bank, UBS, Citigroup, JPMorgan Chase, BOA

Types of investment banks

2. Introduction: Investment BanksIntroduction

Financial holding companiesBusinesses includes:

Retail (or consumer) bankingCorporate bankingInvestment bankingAsset managementWealth (private) managementCredit cards

2. Introduction: Investment BanksIntroduction

Full service (bulge bracket) investment banks: Used to be …

Bear Stearns Lehman BrothersMerrill LynchGoldman SachsMorgan Stanley

Then, there were … none!

Types of investment banks

2. Introduction: Investment BanksIntroduction

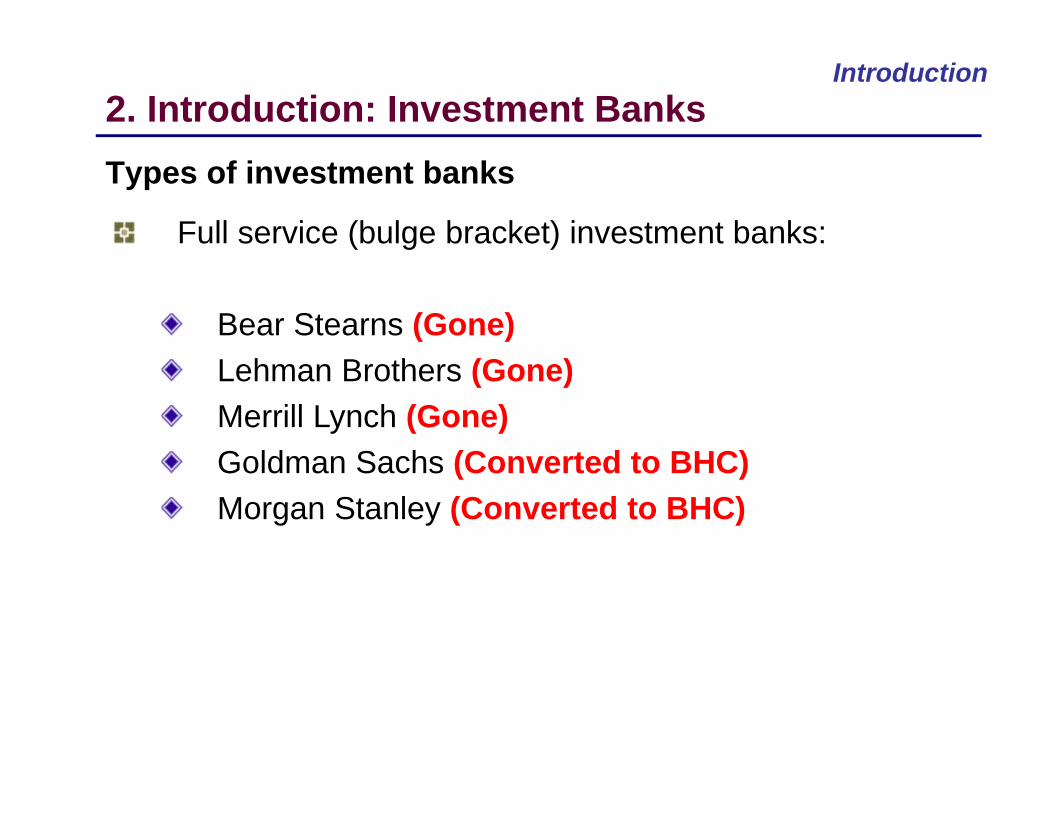

Full service (bulge bracket) investment banks:

Bear Stearns (Gone)Lehman Brothers (Gone)Merrill Lynch (Gone)Goldman Sachs (Converted to BHC)Morgan Stanley (Converted to BHC)

Types of investment banks

2. Introduction: Investment BanksIntroduction

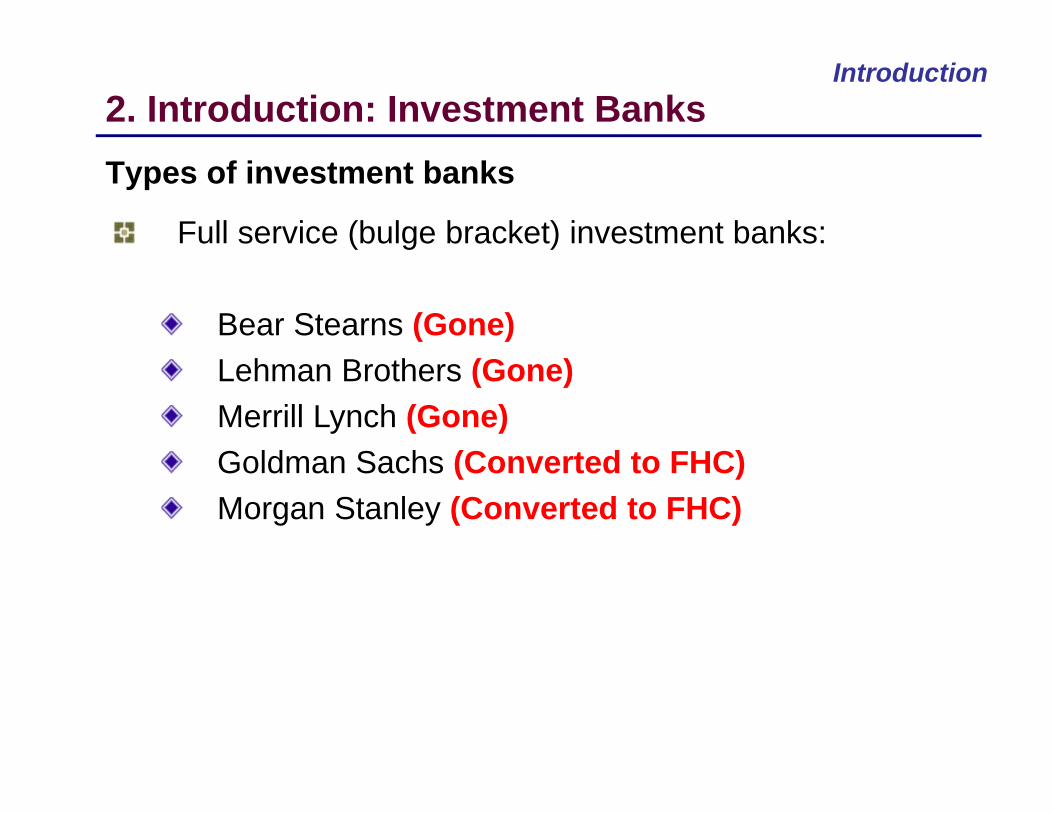

Full service (bulge bracket) investment banks:

Bear Stearns (Gone)Lehman Brothers (Gone)Merrill Lynch (Gone)Goldman Sachs (Converted to FHC)Morgan Stanley (Converted to FHC)

Types of investment banks

2. Introduction: Investment BanksIntroduction

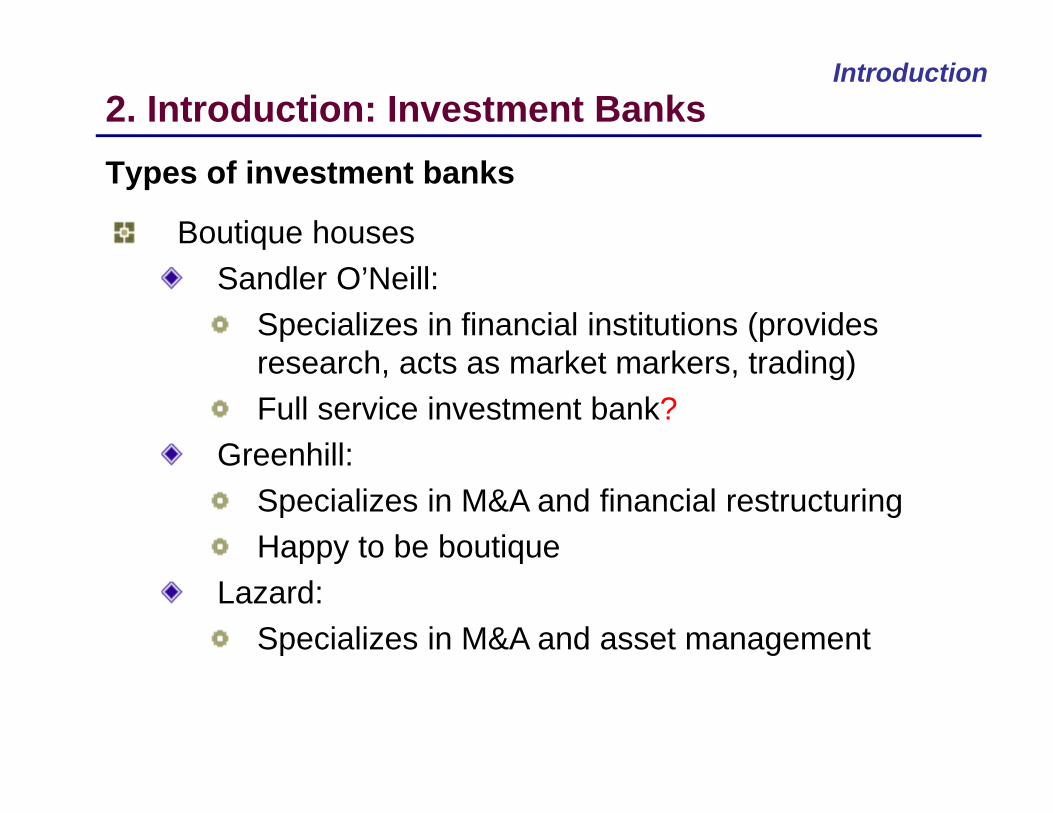

Boutique housesSandler O’Neill:

Specializes in financial institutions (provides research, acts as market markers, trading)Full service investment bank?

Greenhill: Specializes in M&A and financial restructuringHappy to be boutique

Lazard: Specializes in M&A and asset management

Types of investment banks

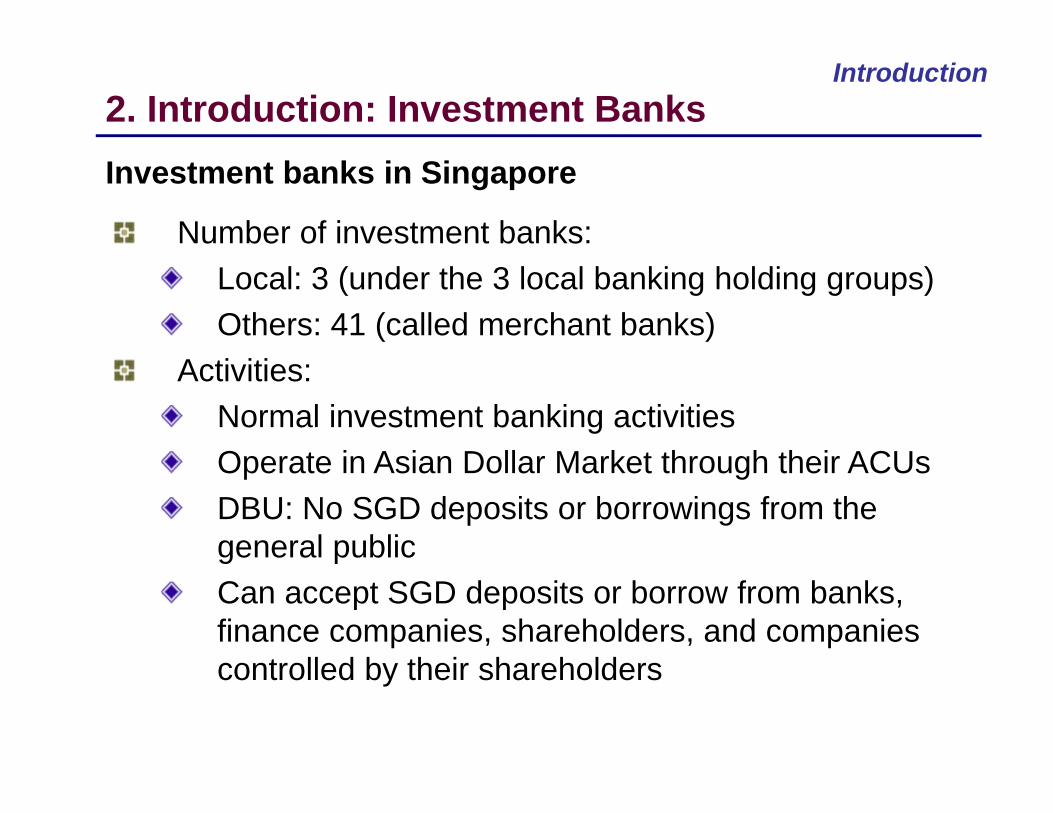

2. Introduction: Investment BanksIntroduction

Number of investment banks: Local: 3 (under the 3 local banking holding groups)Others: 41 (called merchant banks)

Activities:Normal investment banking activitiesOperate in Asian Dollar Market through their ACUsDBU: No SGD deposits or borrowings from the general publicCan accept SGD deposits or borrow from banks, finance companies, shareholders, and companies controlled by their shareholders

Investment banks in Singapore

3. Trends in investment banking Introduction

Regulation to deregulation to re-regulation to …..The financial industry has always been oscillating between regulation and deregulation. Why?Regulation leads to orderly market practices but hamper growth and competitionDeregulation on the other hand promotes growth and competition but give room for abuse and misuseand ultimately cause too much damage to the market

Deregulation

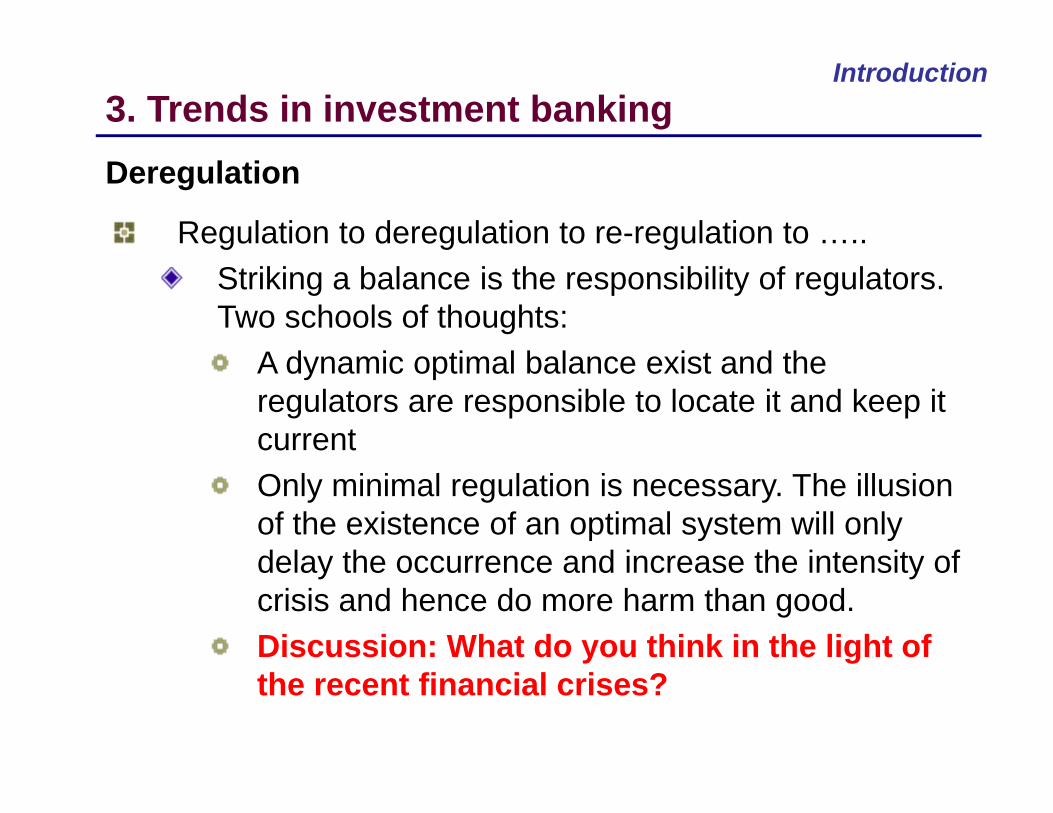

3. Trends in investment banking Introduction

Regulation to deregulation to re-regulation to …..Striking a balance is the responsibility of regulators. Two schools of thoughts:

A dynamic optimal balance exist and the regulators are responsible to locate it and keep it current Only minimal regulation is necessary. The illusion of the existence of an optimal system will only delay the occurrence and increase the intensity of crisis and hence do more harm than good.Discussion: What do you think in the light of the recent financial crises?

Deregulation

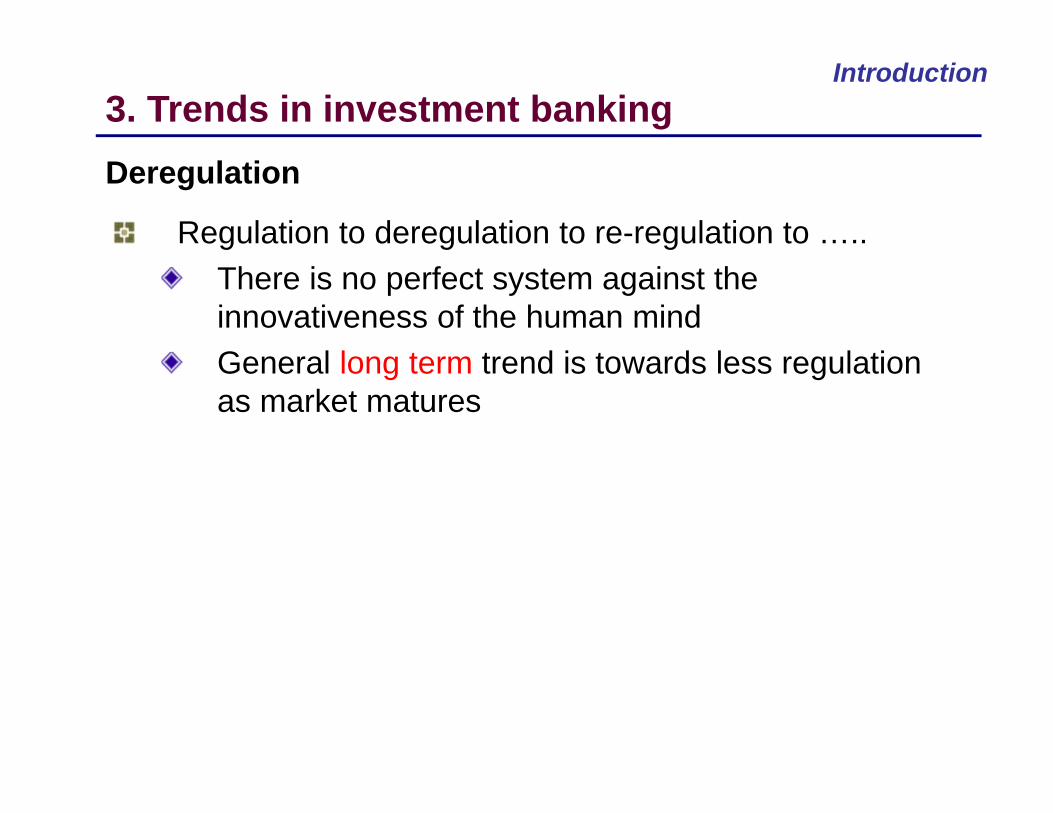

3. Trends in investment banking Introduction

Regulation to deregulation to re-regulation to …..There is no perfect system against the innovativeness of the human mind General long term trend is towards less regulation as market matures

Deregulation

3. Trends in investment banking Introduction

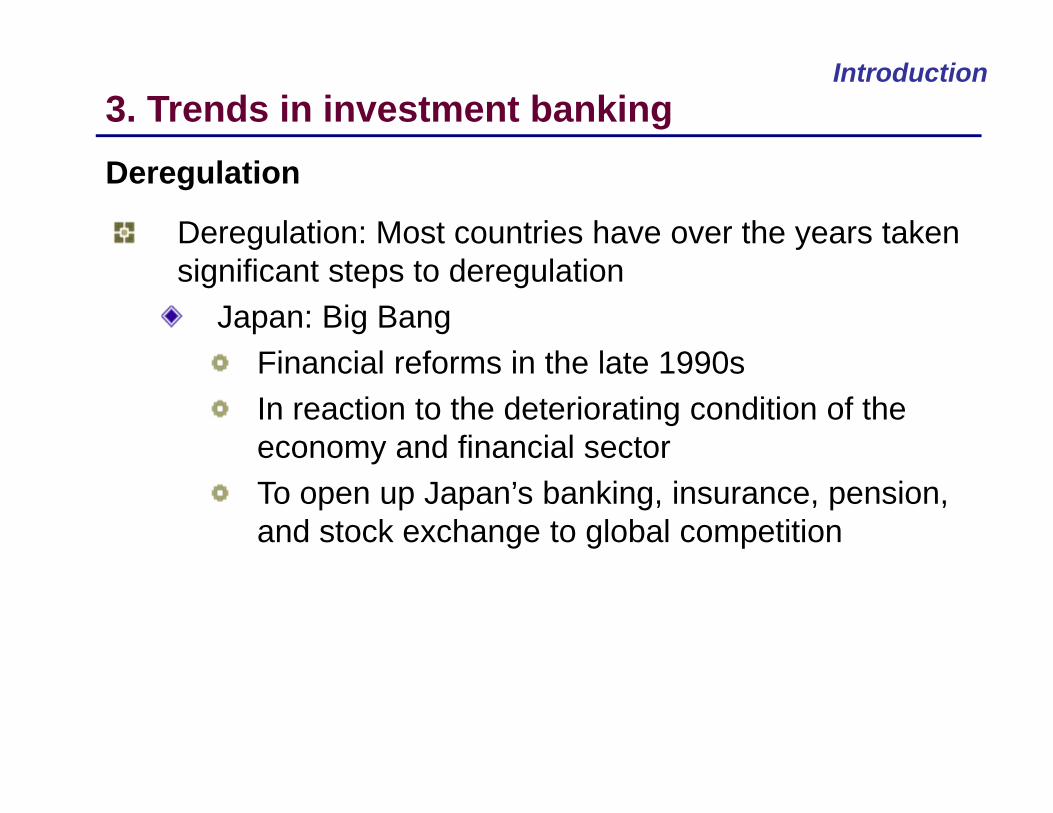

Deregulation: Most countries have over the years taken significant steps to deregulation

UK: Big Bang Margaret Thatcher government's reform program in the 1980s to deregulate the financial market London, once a global financial centre was losing ground to New YorkProblems: overregulation and the dominance of elitist old boys' networksSolution: free market doctrines of unfettered competition and meritocracyResults: London is still one of the most important financial centre in the world

Deregulation

3. Trends in investment banking Introduction

Deregulation: Most countries have over the years taken significant steps to deregulation

Japan: Big Bang Financial reforms in the late 1990sIn reaction to the deteriorating condition of the economy and financial sectorTo open up Japan’s banking, insurance, pension, and stock exchange to global competition

Deregulation

3. Trends in investment banking Introduction

Deregulation: Most countries have over the years taken significant steps to deregulation

Japan Postal system reform Up to 2007, Japan Post offers postal services, banking services, and life insurance.One third of all government employees worked for the PostLargest saving system: US$3.2trPrivatize in 2007: Split into 4 units (Japan Post, Network, Bank, and Insurance)

Deregulation

3. Trends in investment banking Introduction

Deregulation: Most countries have over the years taken significant steps to deregulation

Singapore: Can you name some?“Privatization” of POSBOpening competition for the banking sectorRelaxing control of S$

Deregulation

Deregulation of the investment banking sector

Introduction

Gramm-Leach-Bliley Act vs Glass-Steagall Act Glass-Steagall Act 1933: What and why?

In the light of the great depressionTo curb conflict of interestCommercial banking, investment banking, and insurance activities cannot be under the same roofLead to the break up of big banks. Example JP Morgan and Morgan Stanley

3. Trends in investment banking

Deregulation of the investment banking sector

Introduction

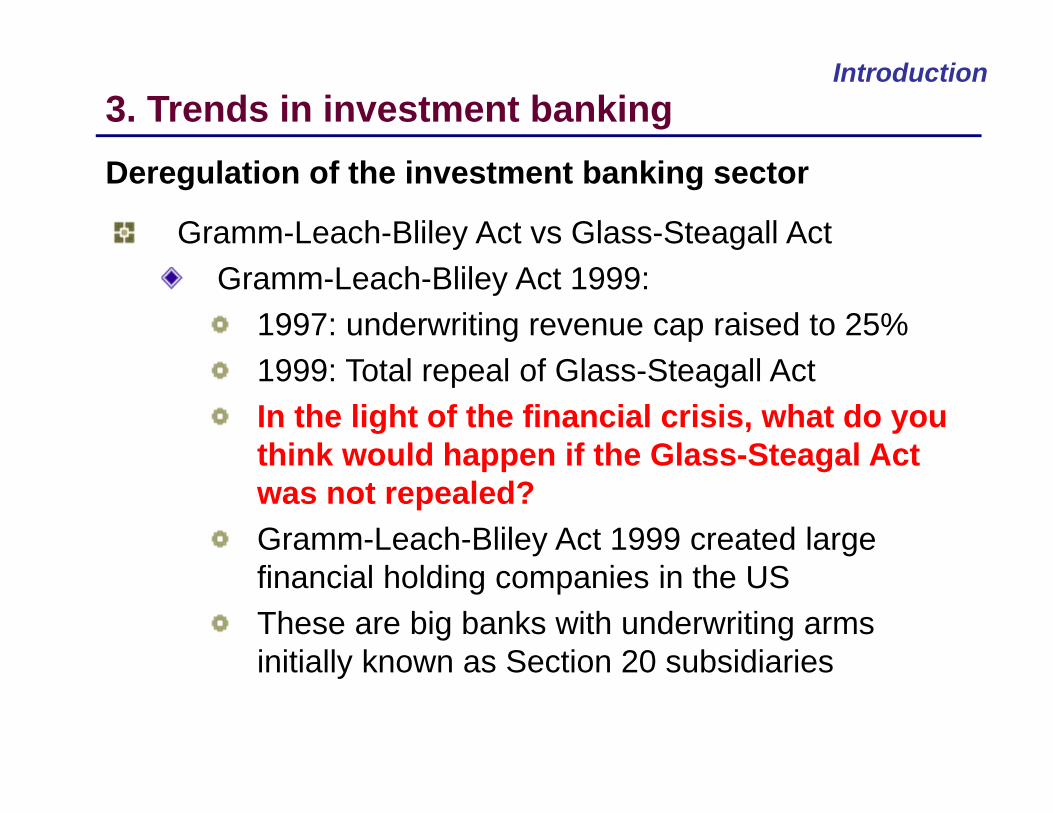

Gramm-Leach-Bliley Act vs Glass-Steagall Act Gramm-Leach-Bliley Act 1999: What and why?

Repeal of the Glass-Steagall Act occurred in steps1987: Fed allowed banks to underwrite and deal in Tier 1 securities: commercial papers, munis, MBS, etc1988: Fed allowed banks to underwrite and deal in Tier 2 securities: all types of debt and equity instruments (Why not allow investment banks to conduct commercial banking activities?)1989: underwriting revenue cap raised from 5% to 10% of total revenue

3. Trends in investment banking

Deregulation of the investment banking sector

Introduction

Gramm-Leach-Bliley Act vs Glass-Steagall Act Gramm-Leach-Bliley Act 1999:

1997: underwriting revenue cap raised to 25%1999: Total repeal of Glass-Steagall ActIn the light of the financial crisis, what do you think would happen if the Glass-Steagal Act was not repealed?Gramm-Leach-Bliley Act 1999 created large financial holding companies in the USThese are big banks with underwriting arms initially known as Section 20 subsidiaries

3. Trends in investment banking

Deregulation of the investment banking sector

Introduction

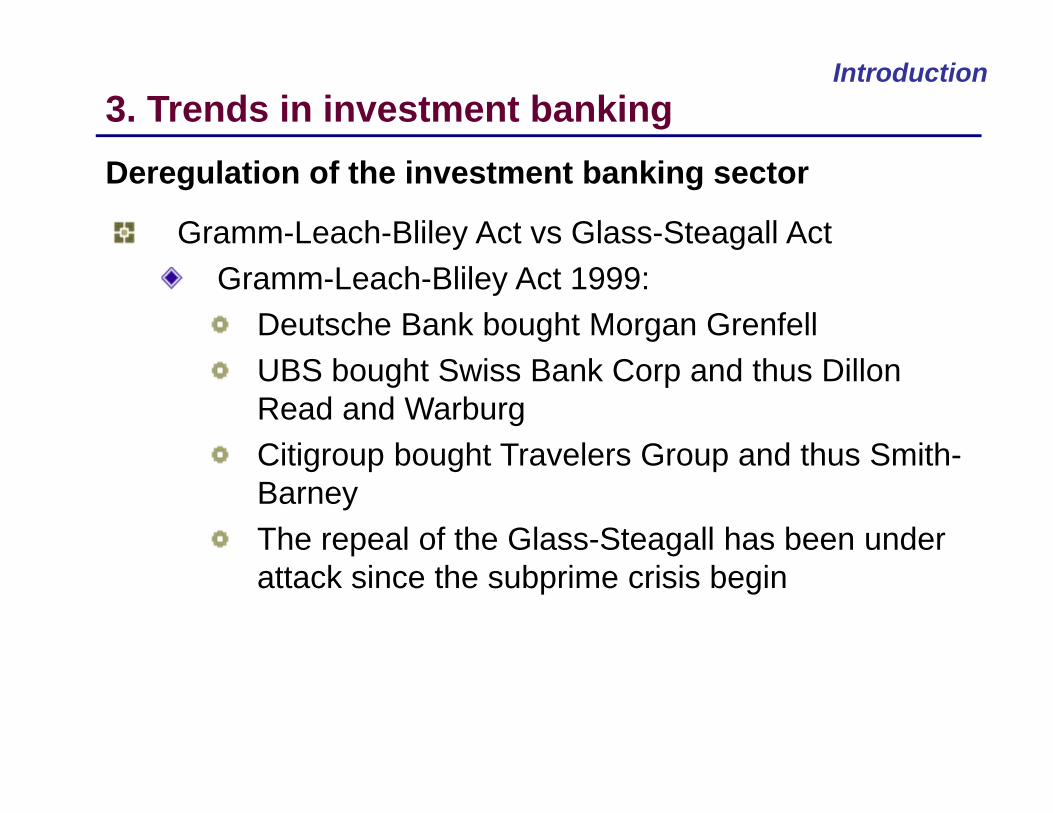

Gramm-Leach-Bliley Act vs Glass-Steagall Act Gramm-Leach-Bliley Act 1999:

Deutsche Bank bought Morgan GrenfellUBS bought Swiss Bank Corp and thus Dillon Read and WarburgCitigroup bought Travelers Group and thus Smith-BarneyThe repeal of the Glass-Steagall has been under attack since the subprime crisis begin

3. Trends in investment banking

Introduction

Sub-prime related In the light of the recent failure of investment banks, who should regulate investment banks? The FED or SEC?

3. Trends in investment banking New regulations in the investment banking sector

Introduction

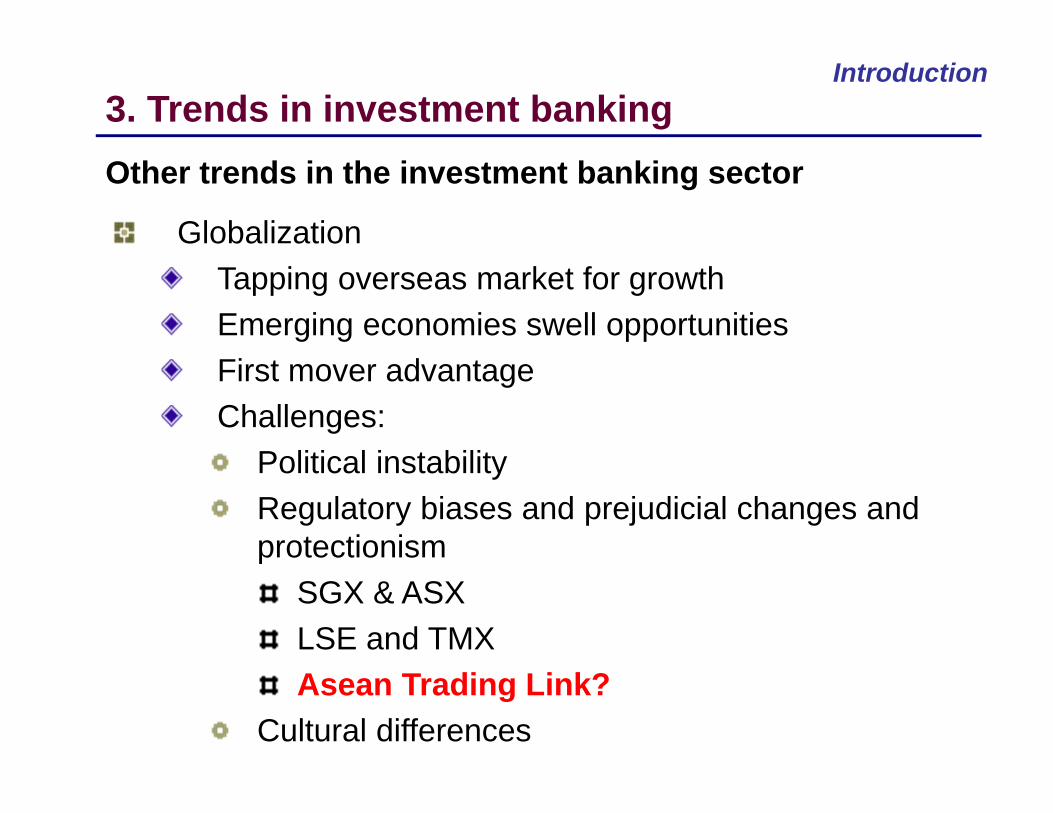

Globalization Tapping overseas market for growthEmerging economies swell opportunitiesFirst mover advantageChallenges:

Political instabilityRegulatory biases and prejudicial changes and protectionism

SGX & ASXLSE and TMXAsean Trading Link?

Cultural differences

3. Trends in investment banking Other trends in the investment banking sector

Introduction

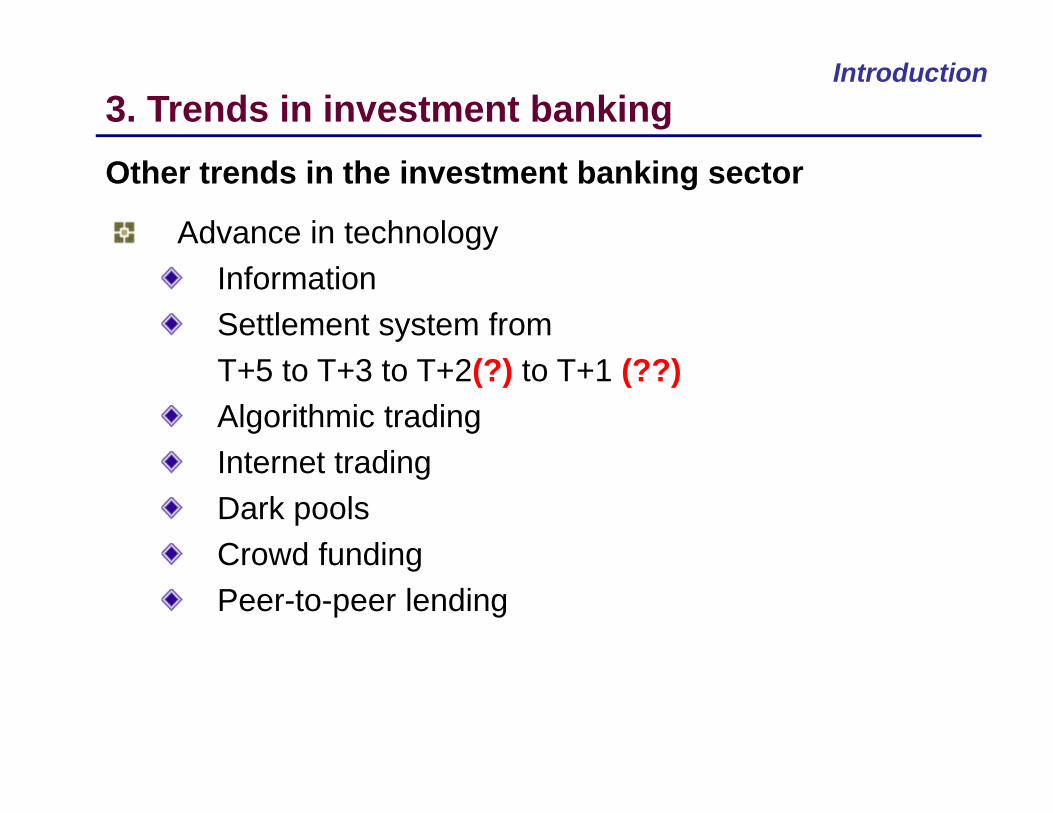

Advance in technologyInformation Settlement system fromT+5 to T+3 to T+2(?) to T+1 (??)Algorithmic tradingInternet tradingDark poolsCrowd fundingPeer-to-peer lending

3. Trends in investment banking Other trends in the investment banking sector

Introduction

Diversification What is diversification?Financial institutions, especially investment banks, have become more diversified Financial holding companies are diversified behemoth (thanks to Gramm-Leach-Bliley)Investment banking represent a smaller and smaller portion of total incomeOther income sources: trading, hedge funds, securitization, asset and wealth management, prime-brokerage, credit cards

3. Trends in investment banking Other trends in the investment banking sector

Introduction

Income sources Underwriting spreadM&A feeTrading profitsPrime-brokerage (interest and fee)Market making (spread)Research

4. Measure of Performance Risk and Returns: Returns

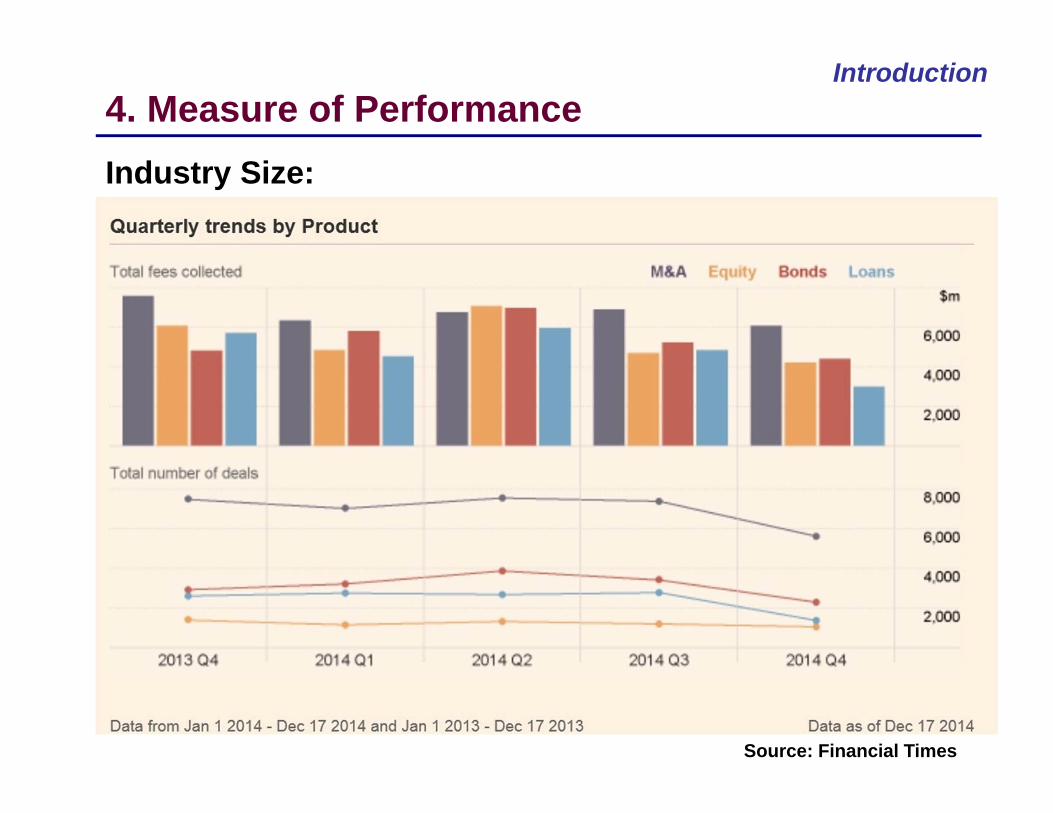

Introduction4. Measure of Performance Industry Size:

Source: Financial Times

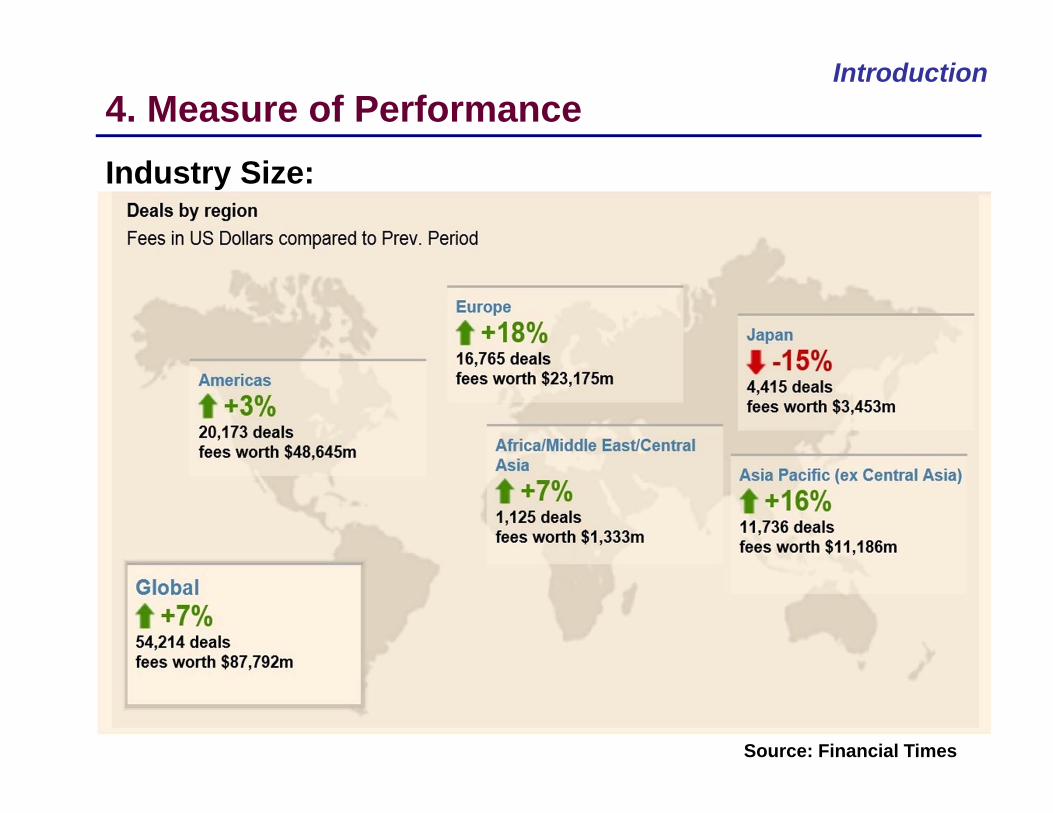

Introduction4. Measure of Performance Industry Size:

Source: Financial Times

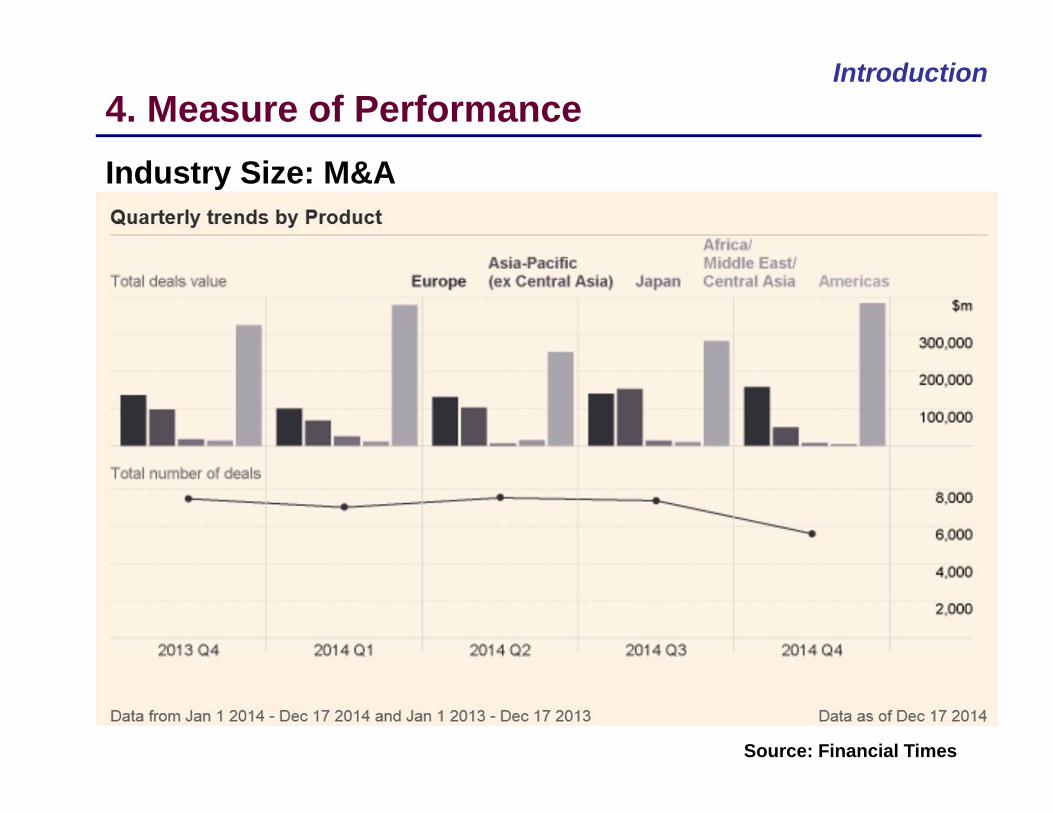

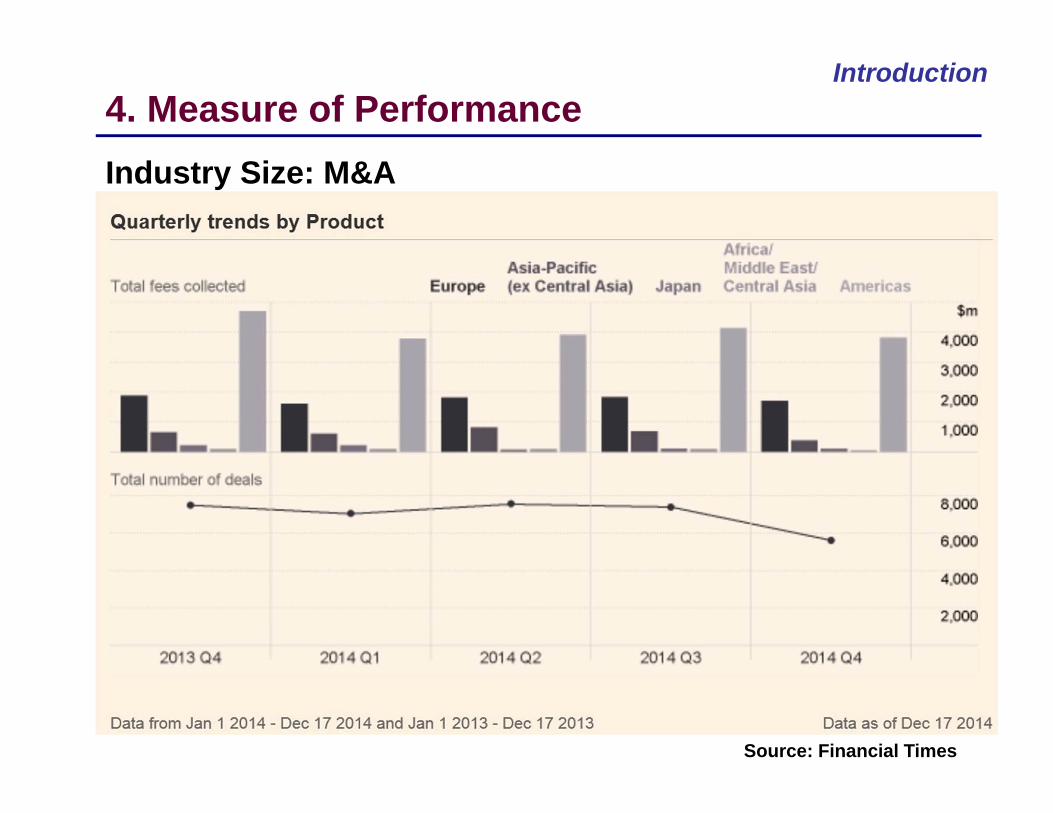

Introduction4. Measure of Performance Industry Size: M&A

Source: Financial Times

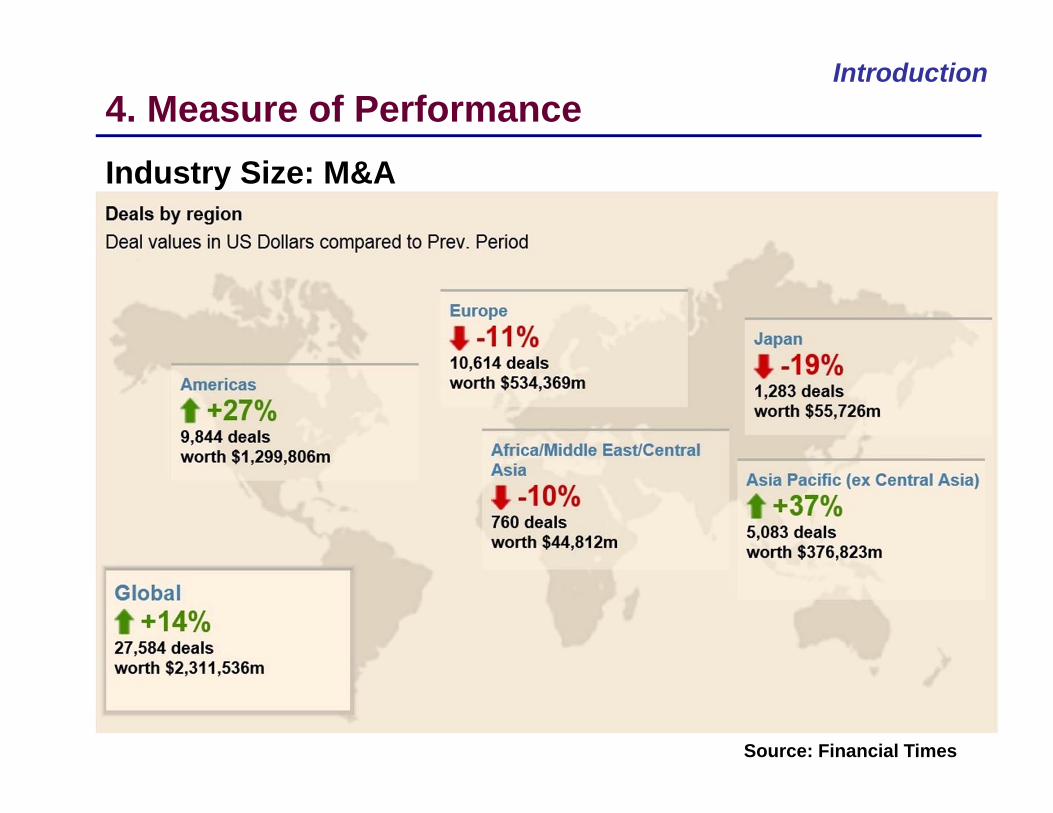

Introduction4. Measure of Performance Industry Size: M&A

Source: Financial Times

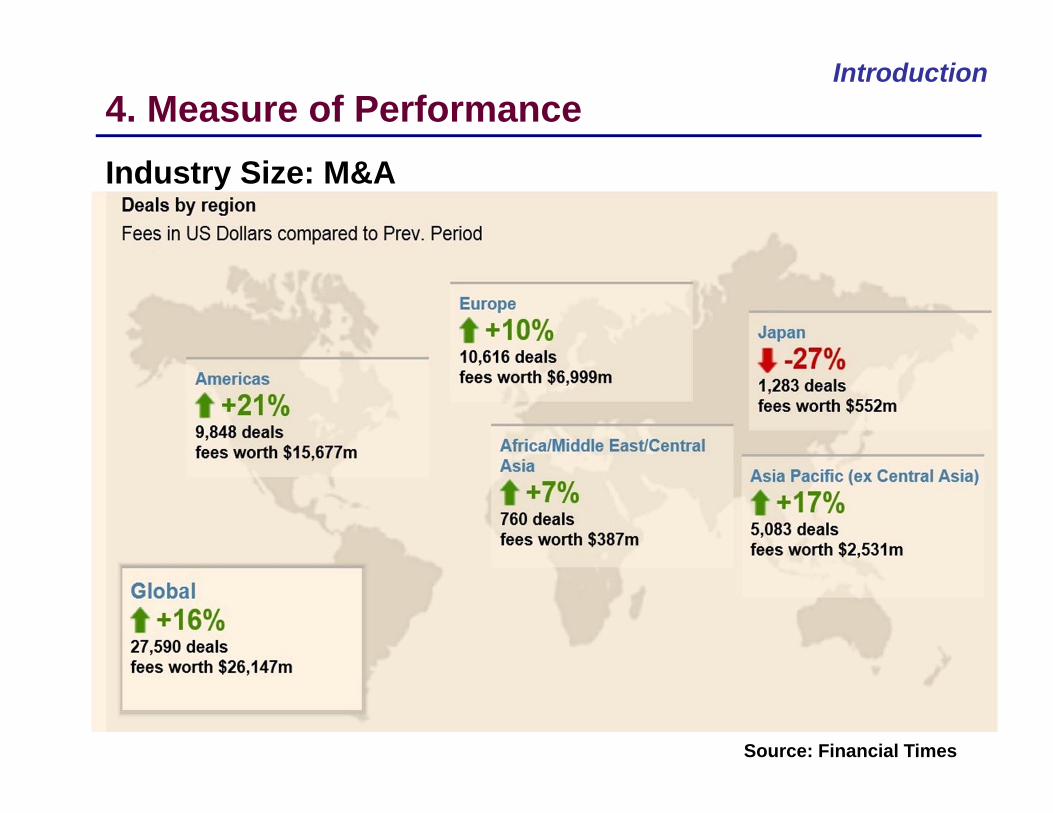

Introduction4. Measure of Performance Industry Size: M&A

Source: Financial Times

Introduction4. Measure of Performance Industry Size: M&A

Source: Financial Times

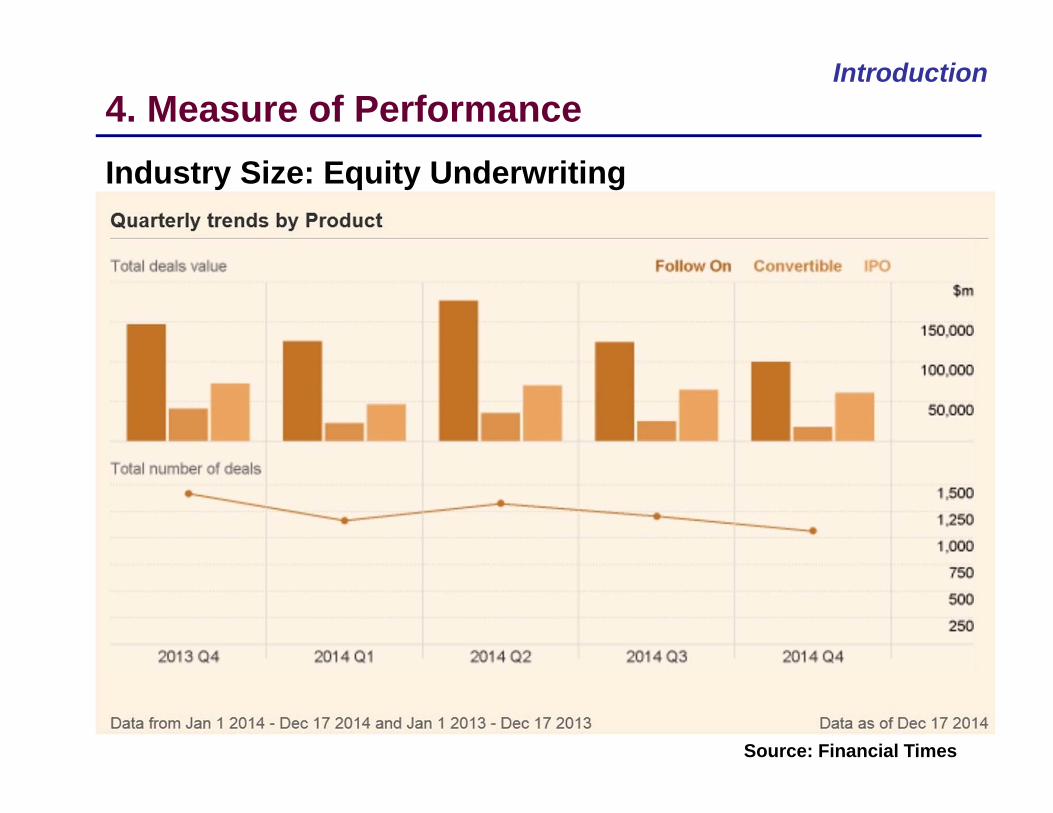

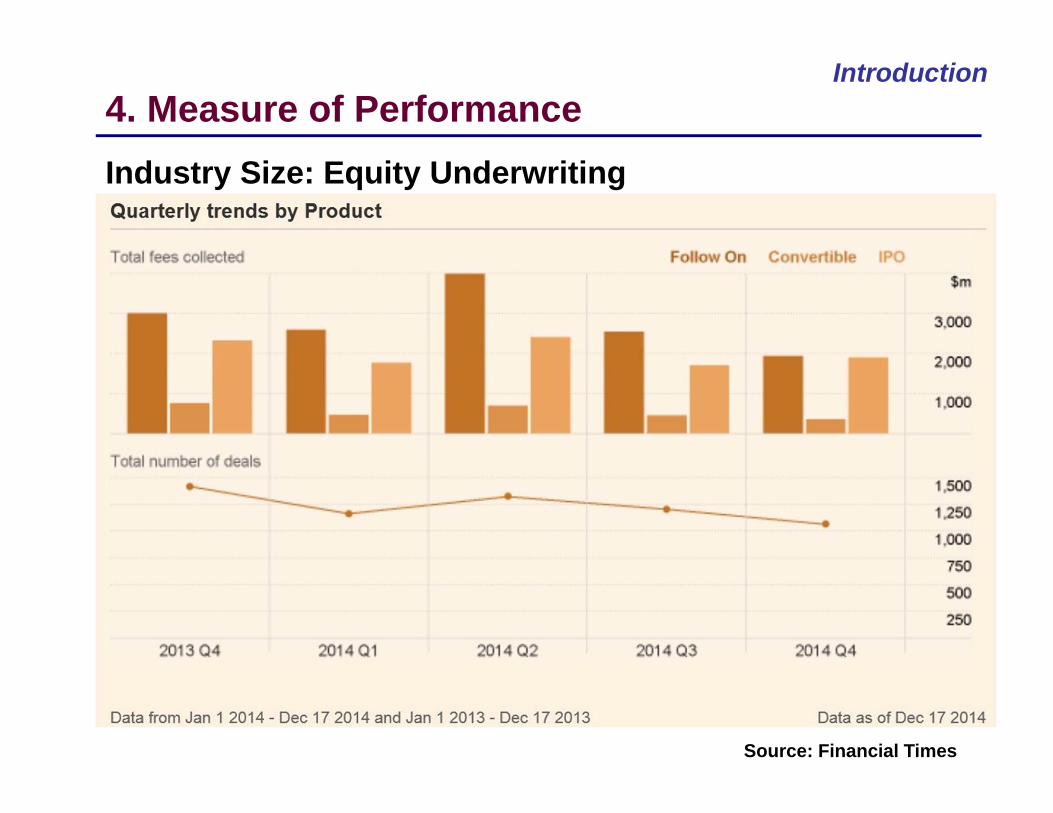

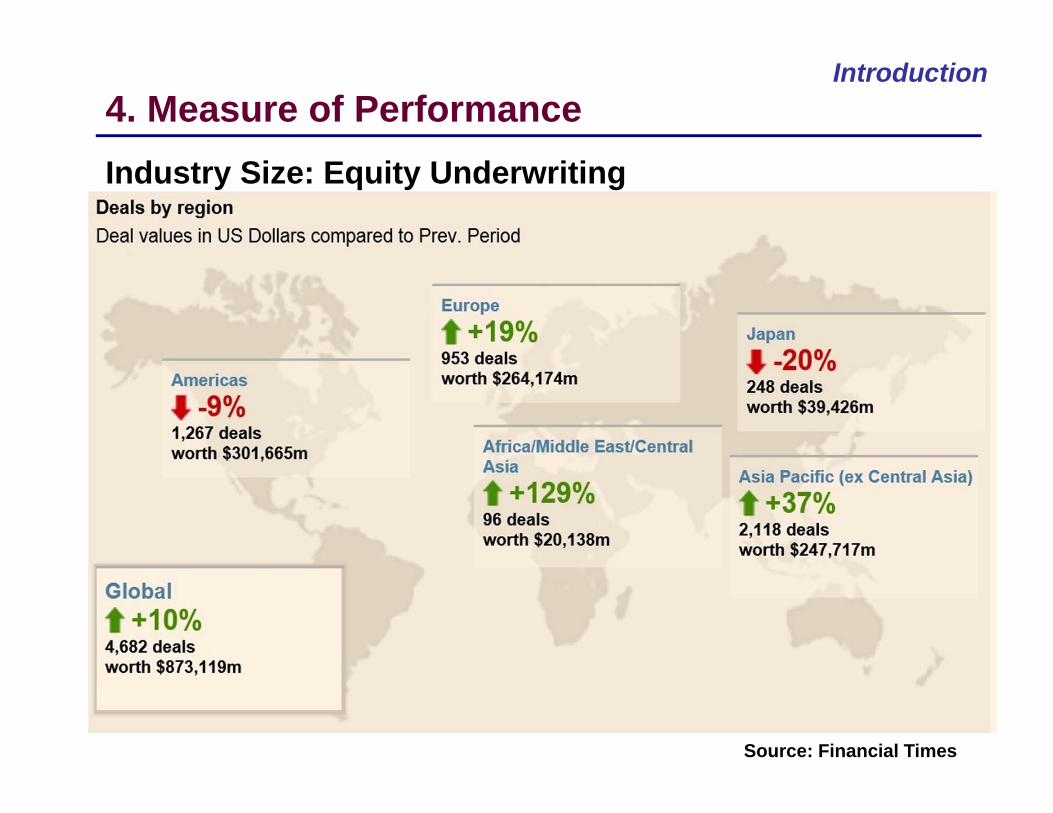

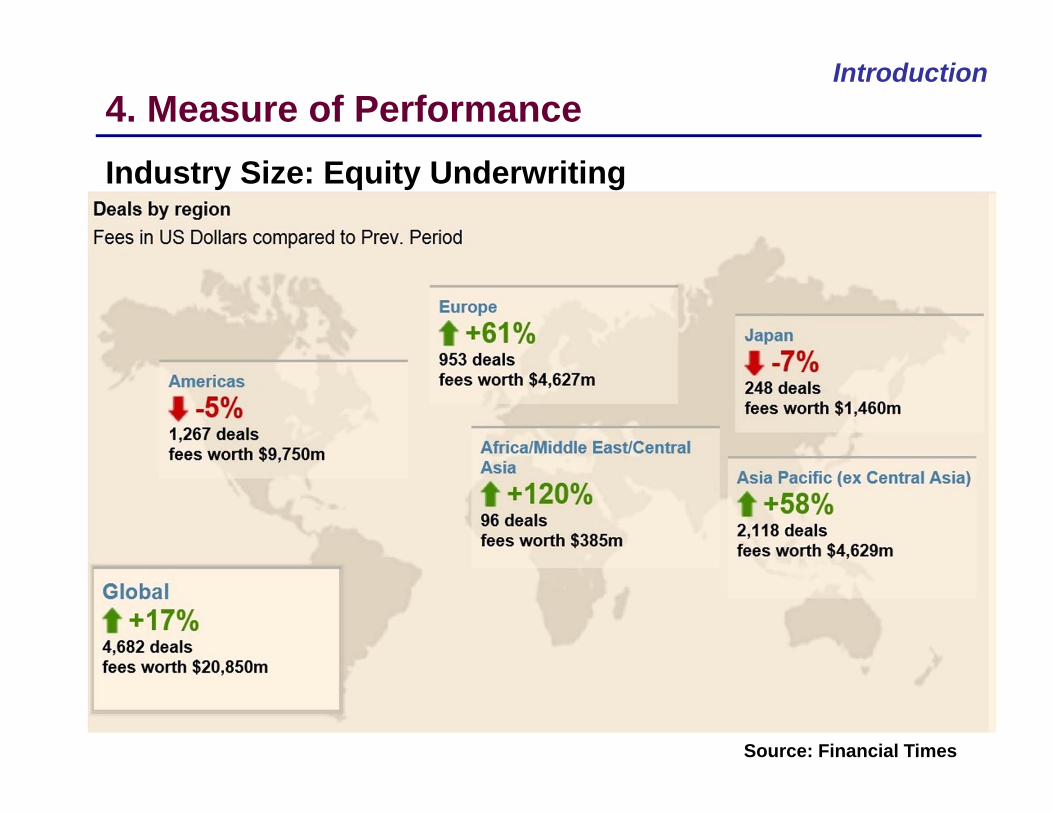

Introduction4. Measure of Performance Industry Size: Equity Underwriting

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Equity Underwriting

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Equity Underwriting

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Equity Underwriting

Source: Financial Times

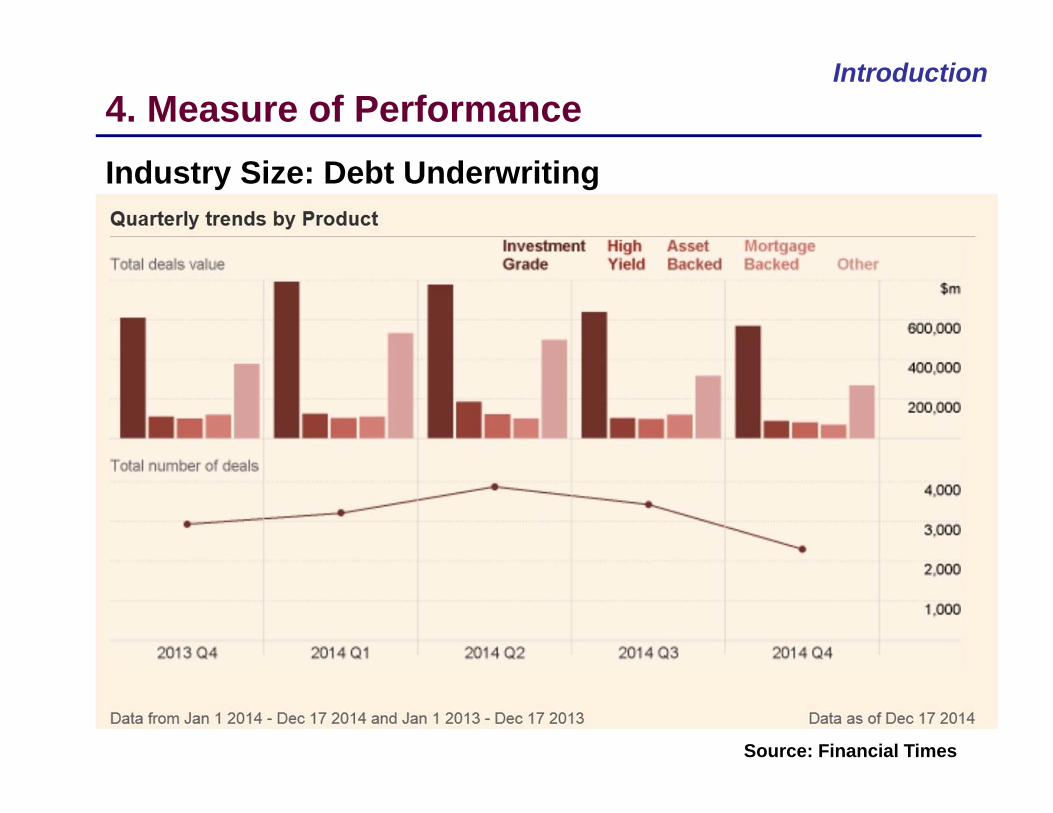

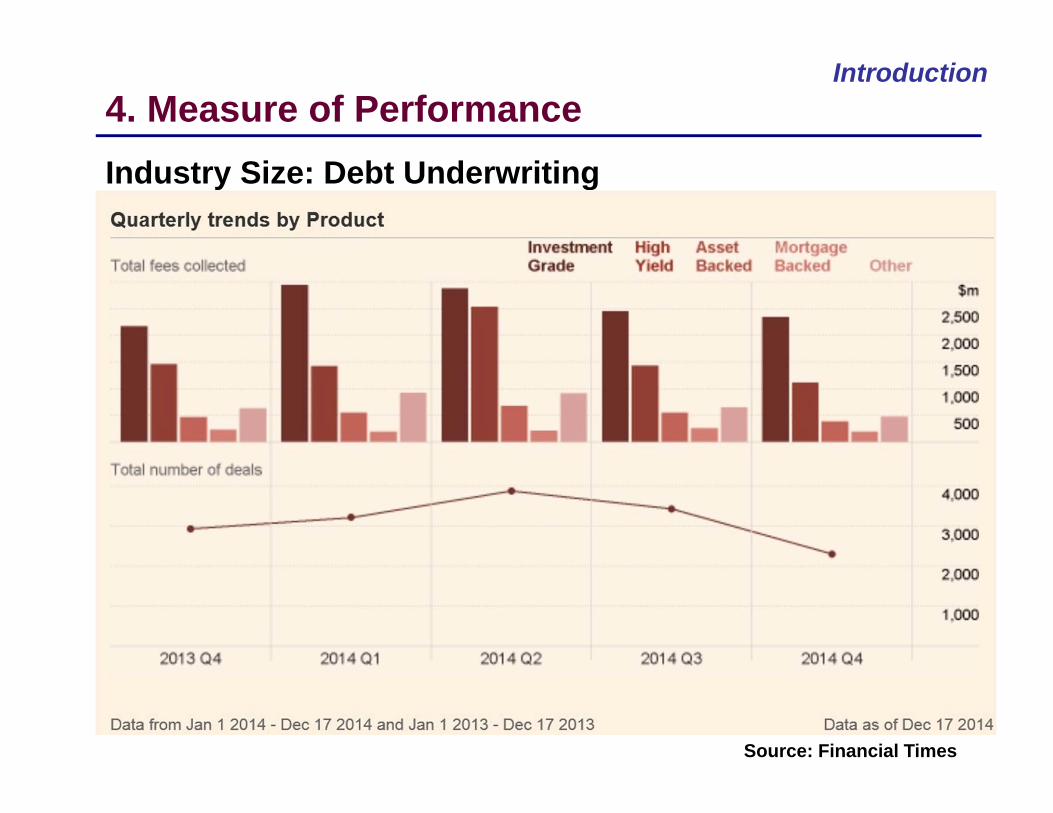

Introduction4. Measure of Performance Industry Size: Debt Underwriting

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Debt Underwriting

Source: Financial Times

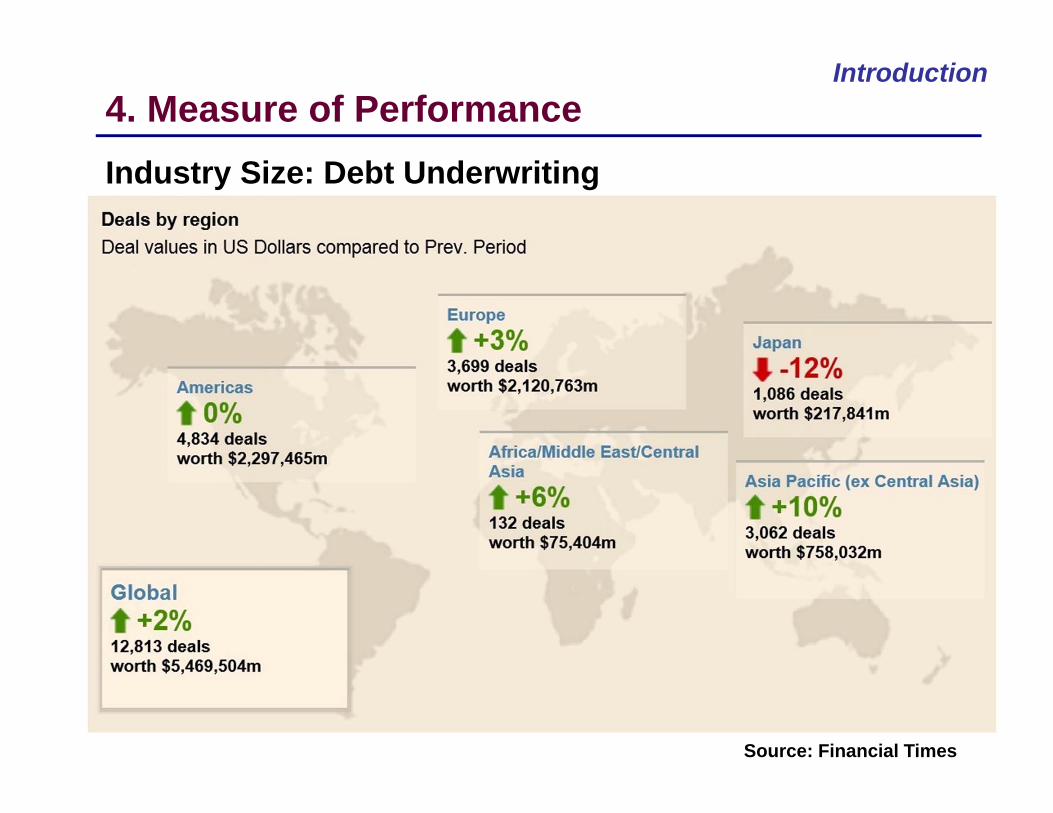

Introduction4. Measure of Performance Industry Size: Debt Underwriting

Source: Financial Times

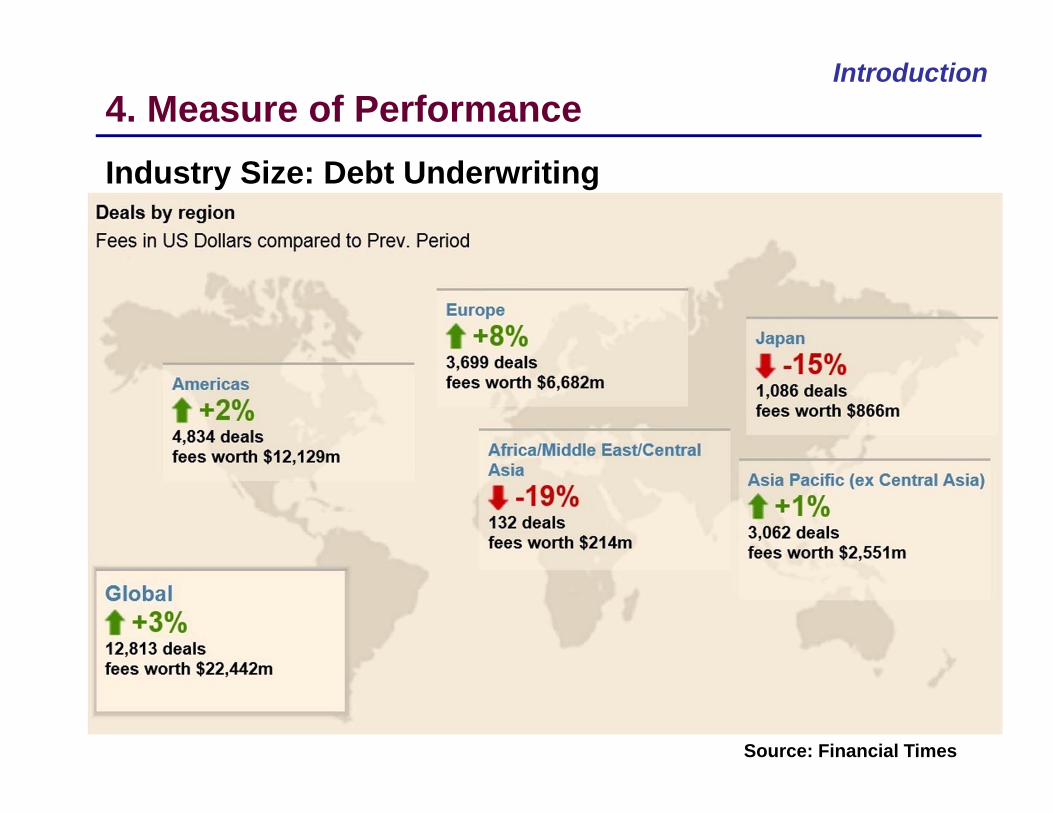

Introduction4. Measure of Performance Industry Size: Debt Underwriting

Source: Financial Times

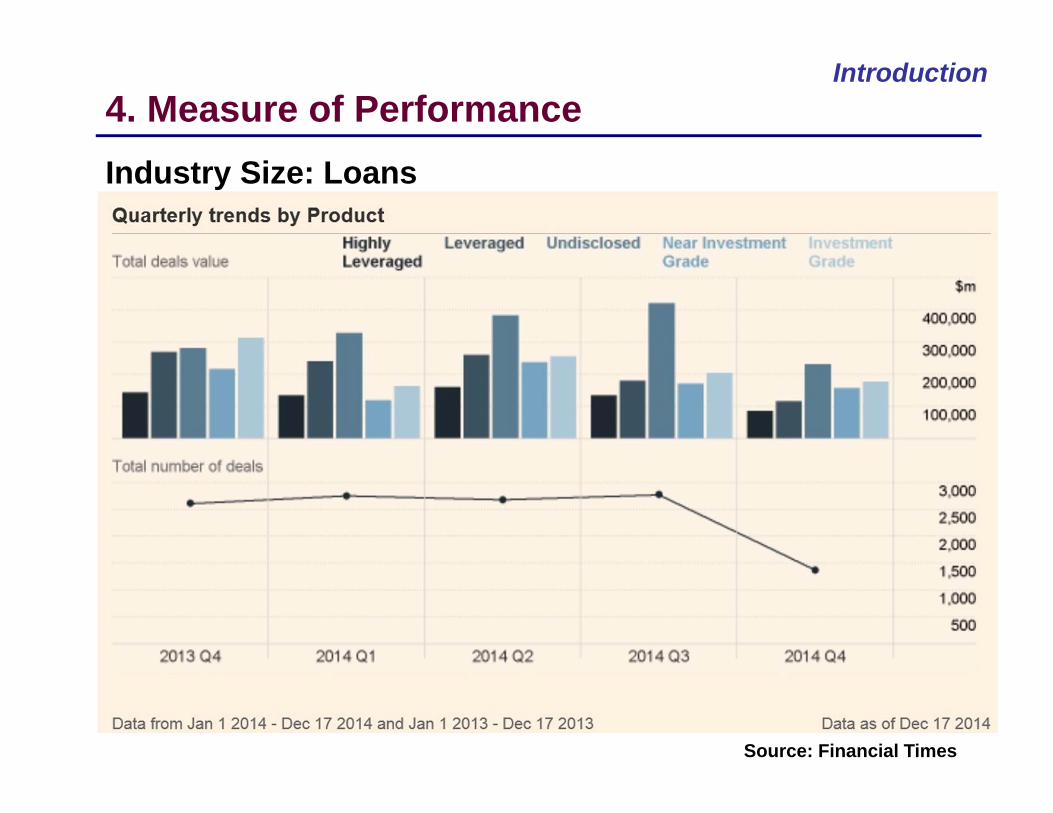

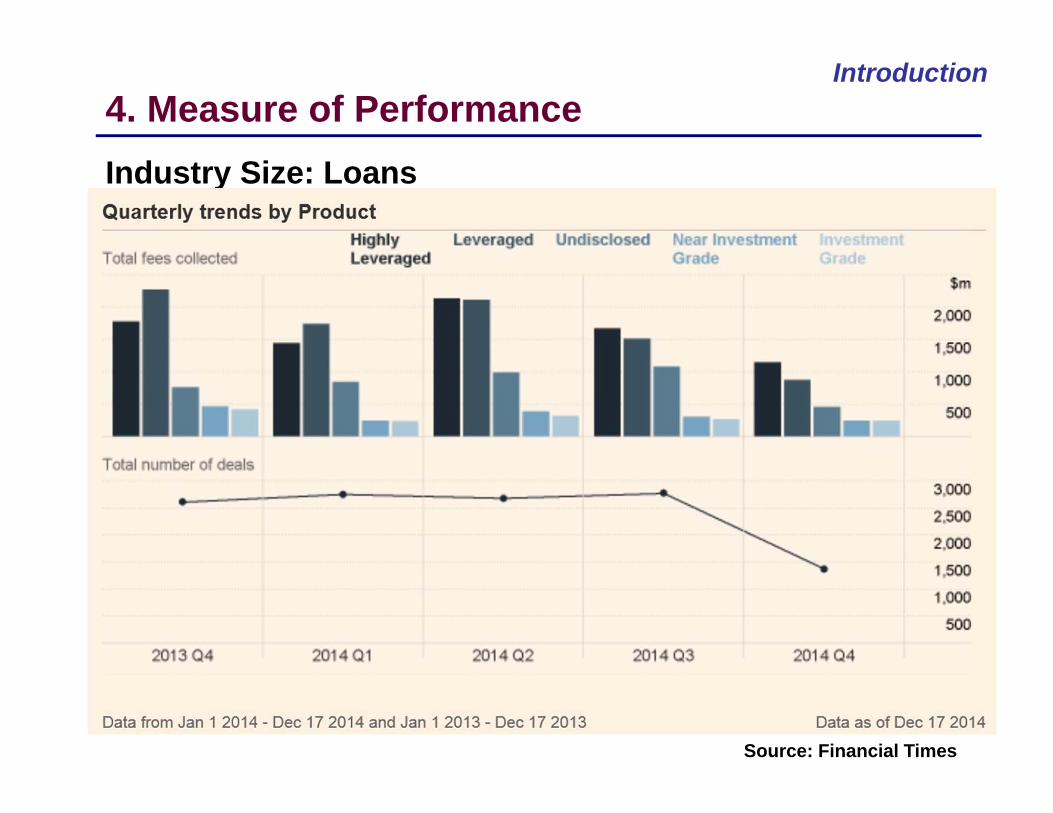

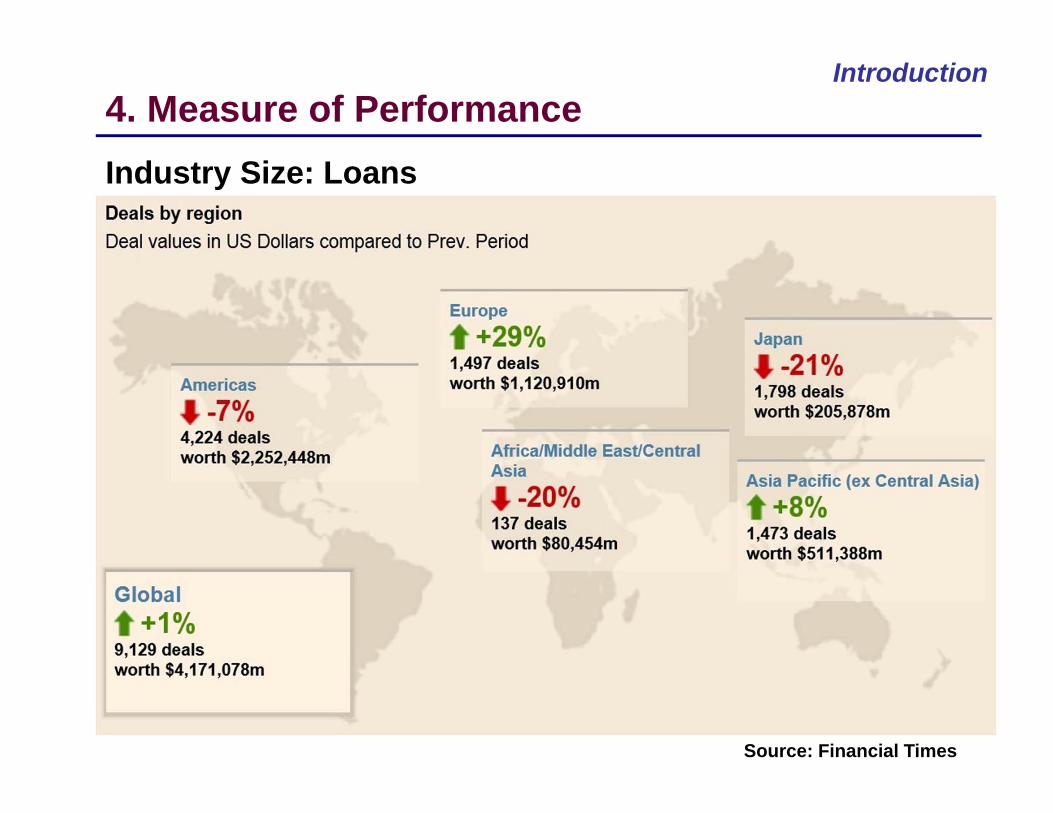

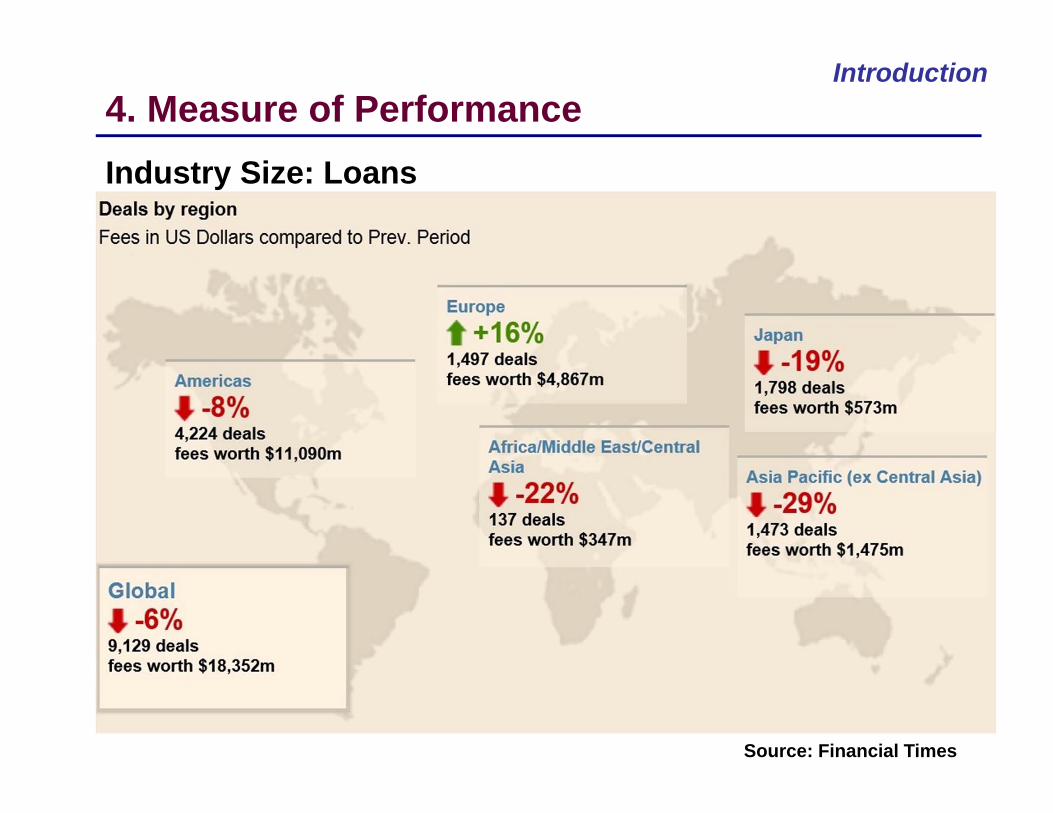

Introduction4. Measure of Performance Industry Size: Loans

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Loans

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Loans

Source: Financial Times

Introduction4. Measure of Performance Industry Size: Loans

Source: Financial Times

Introduction

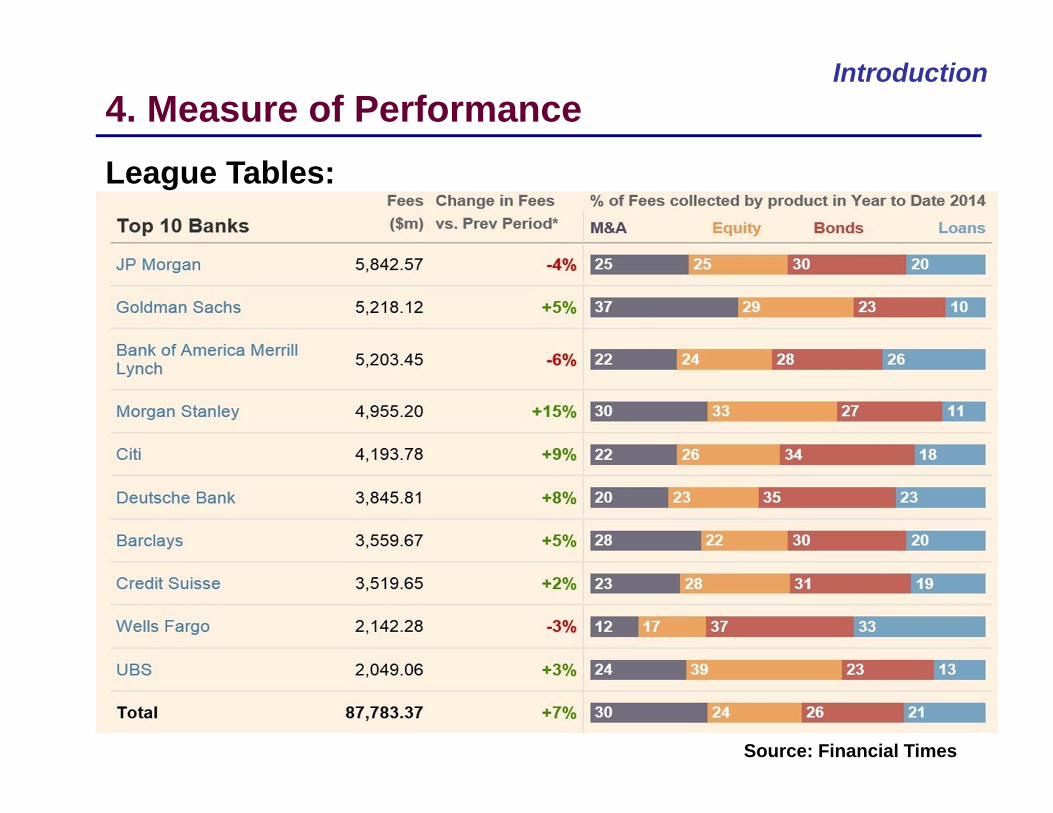

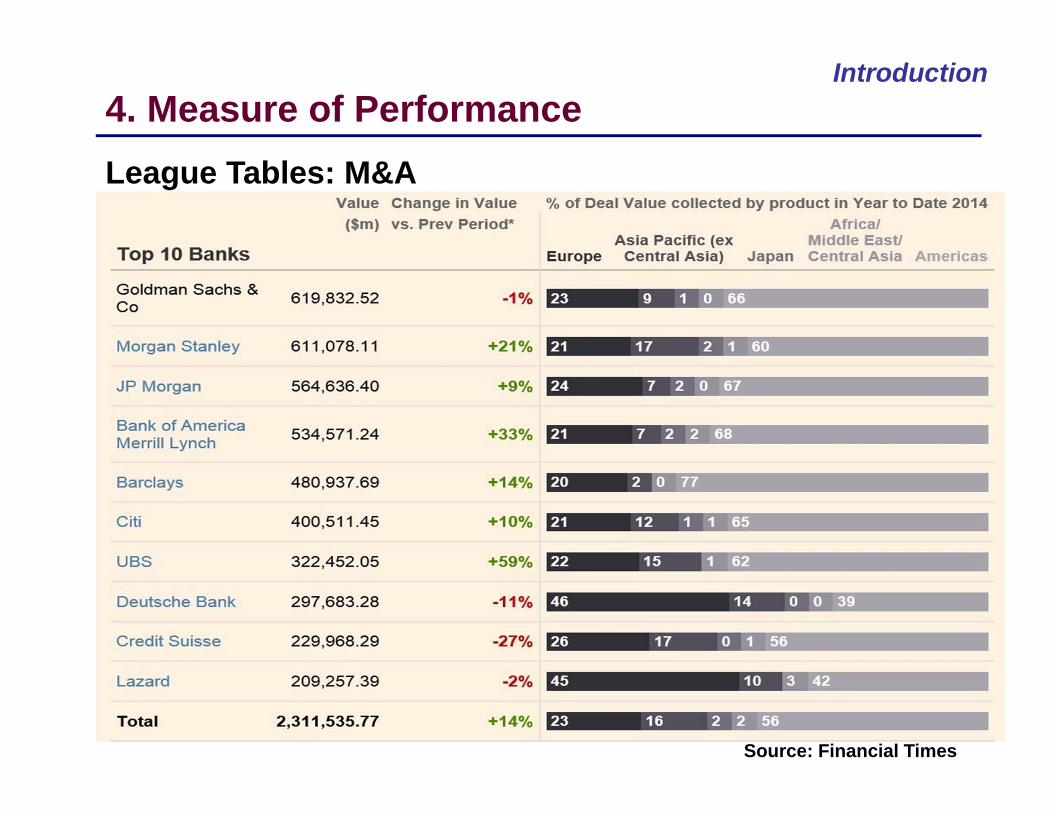

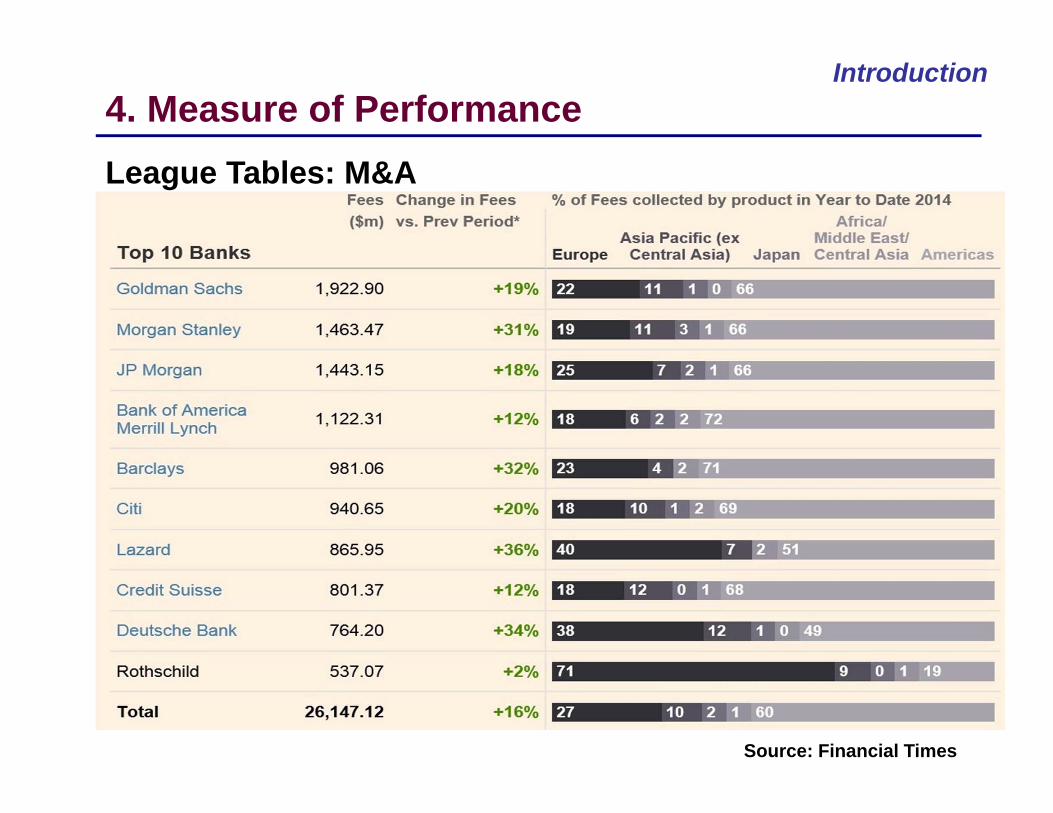

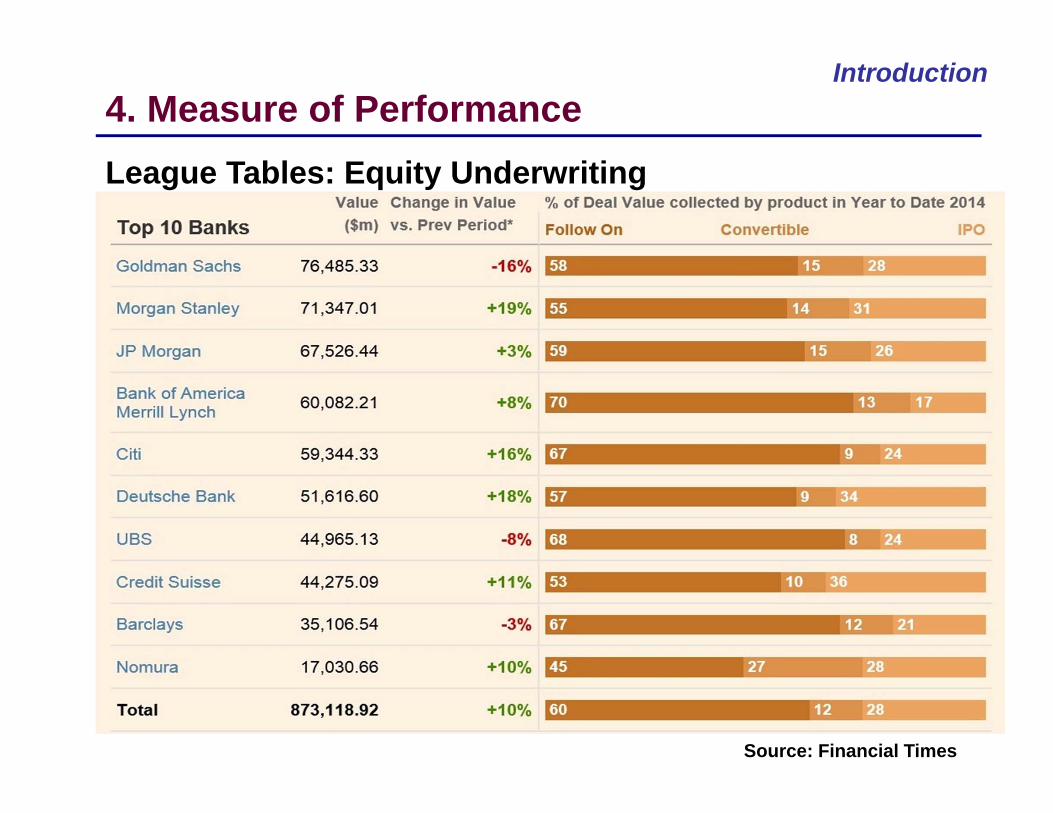

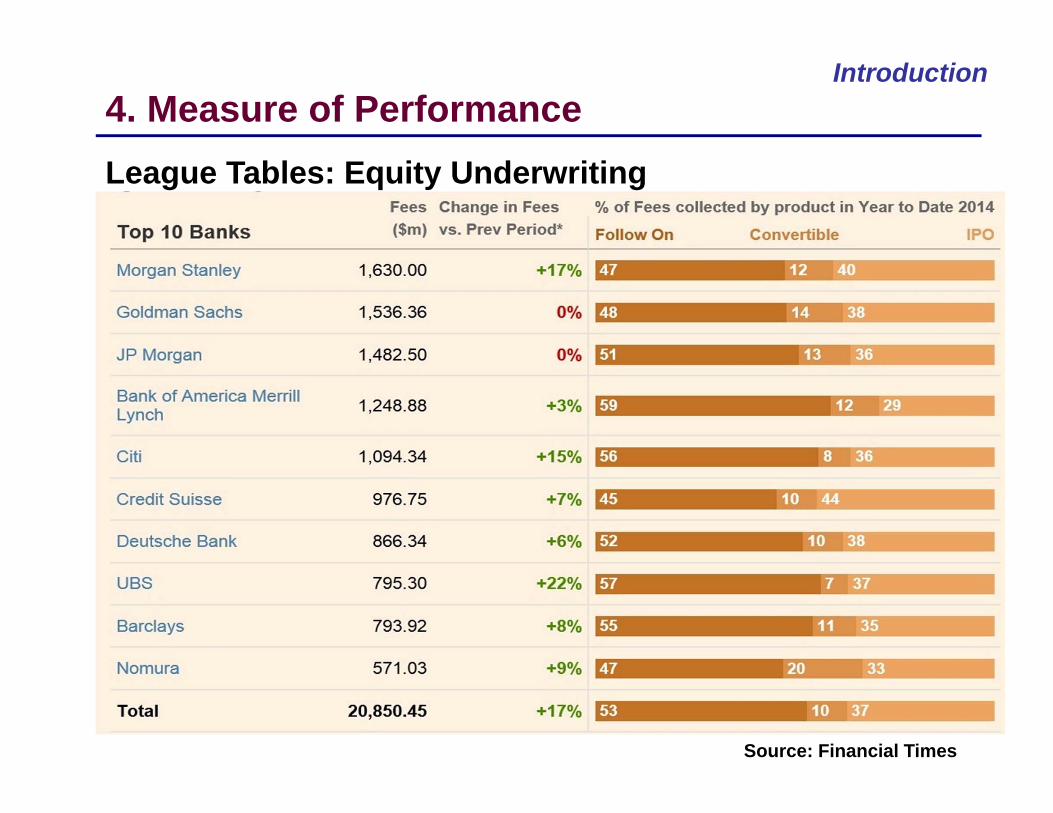

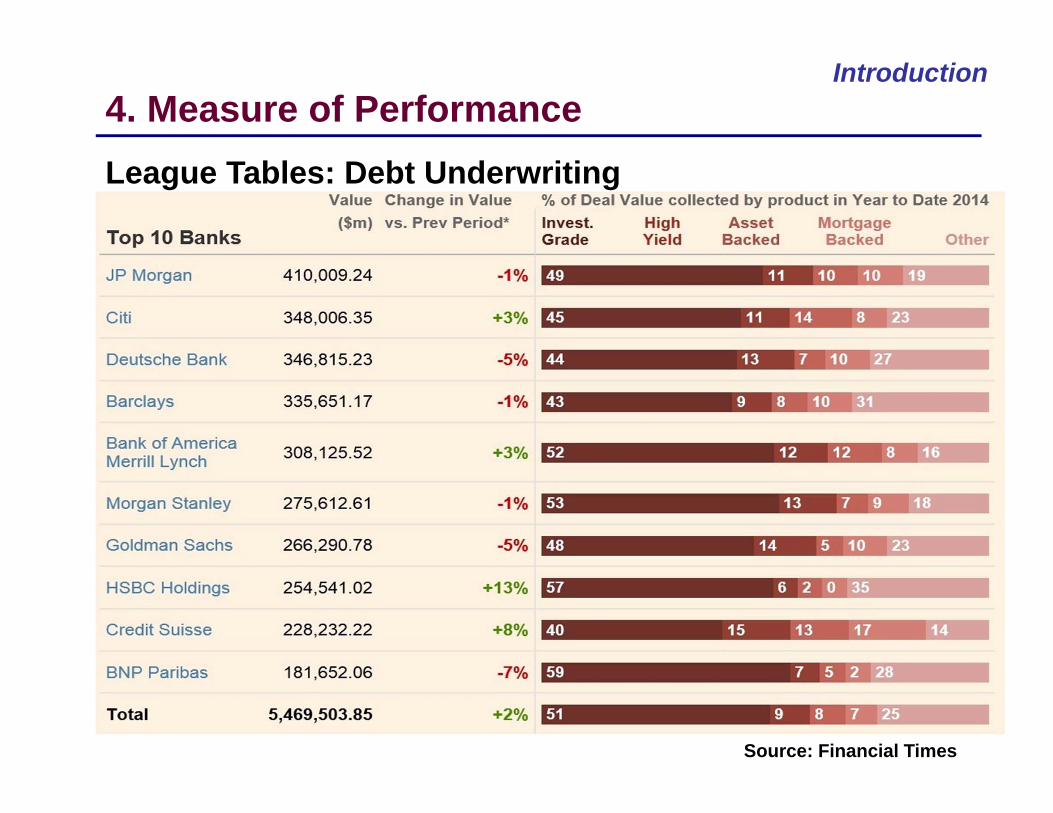

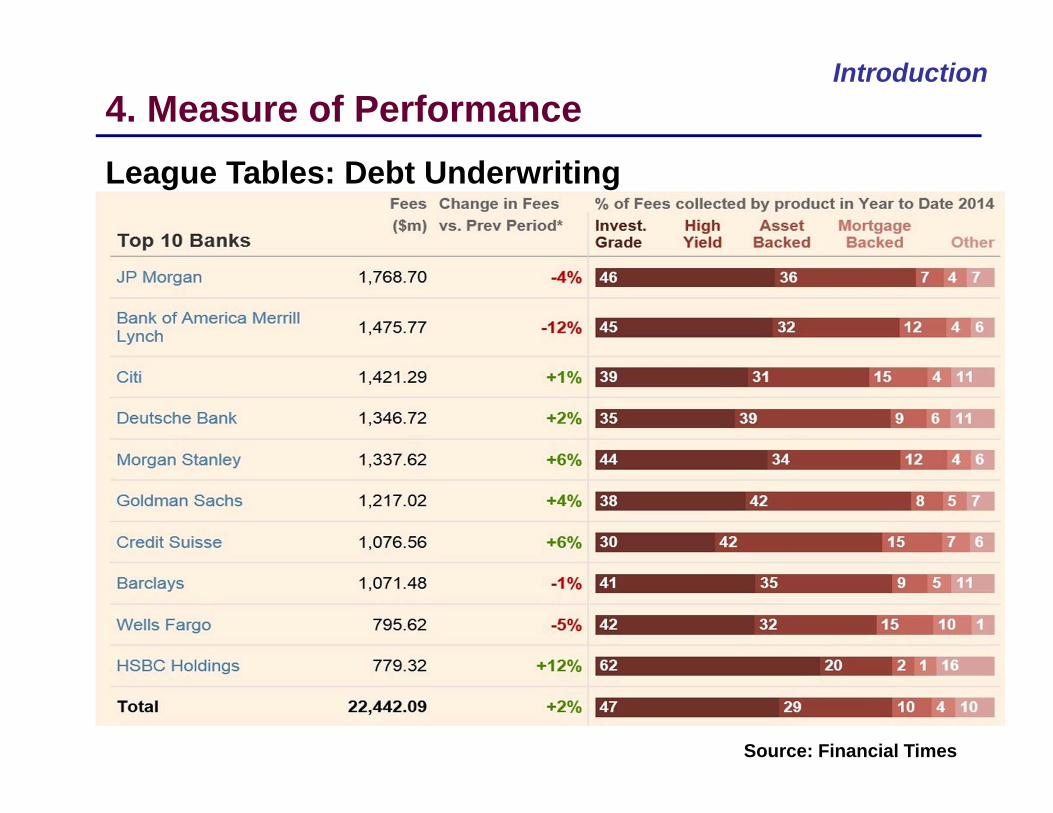

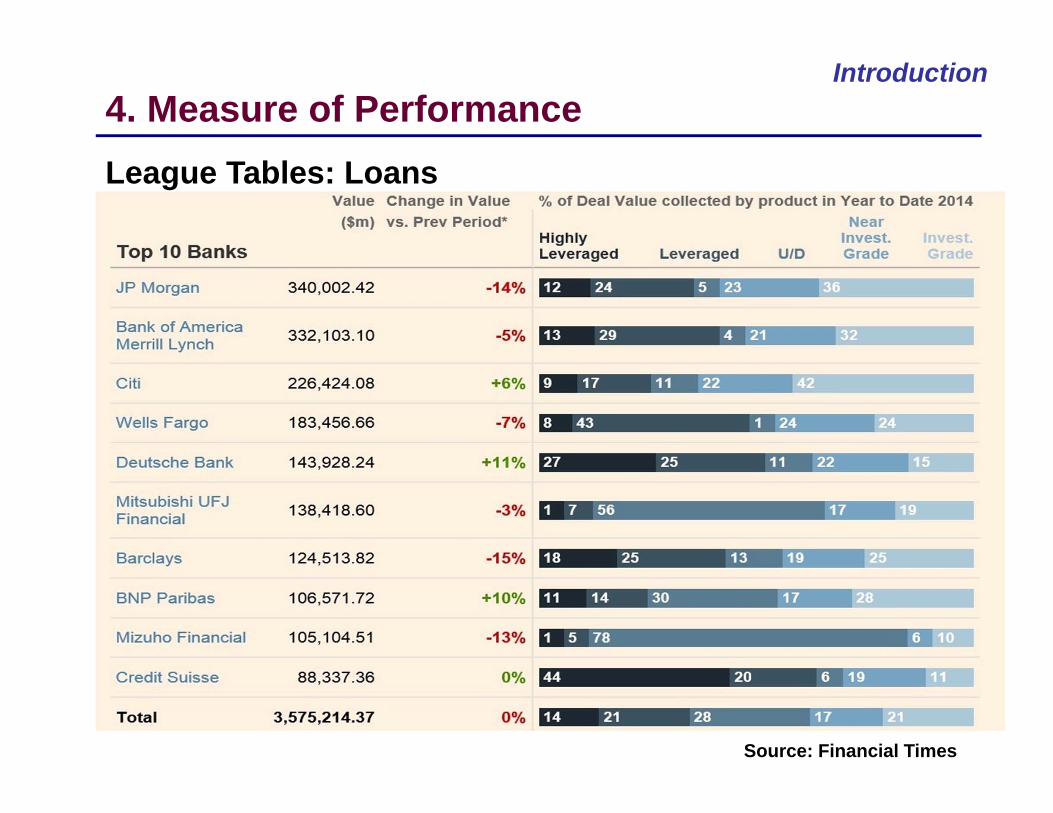

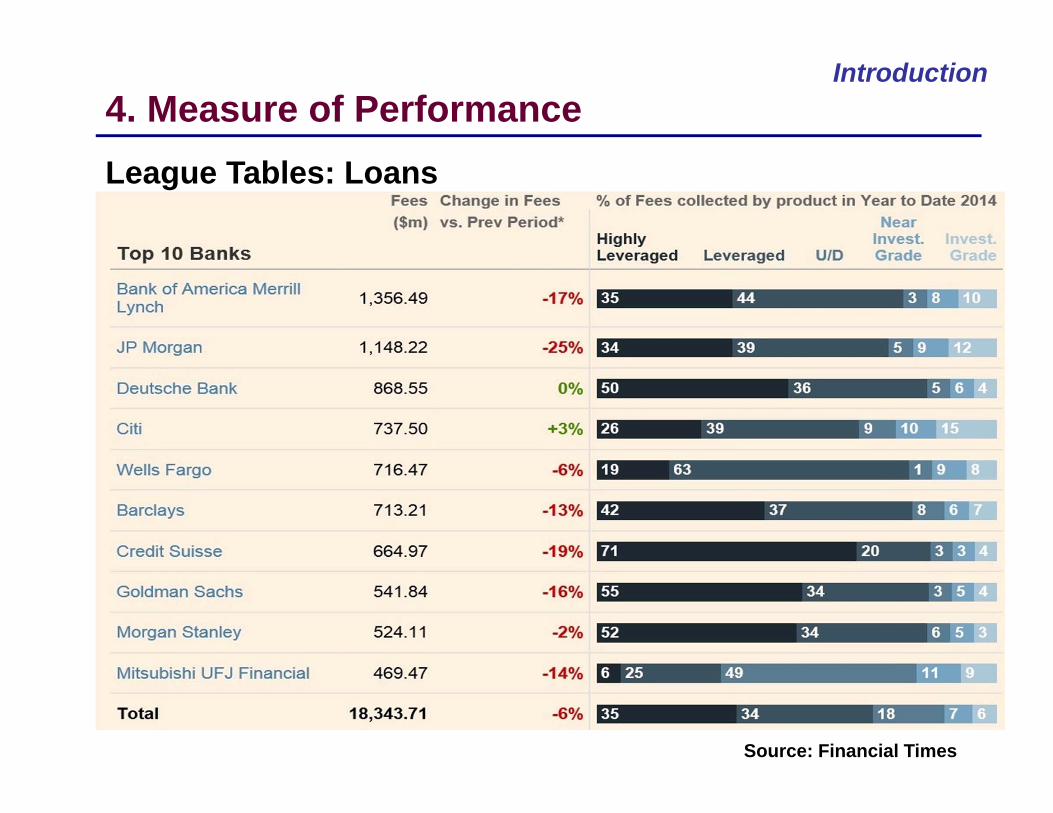

League tables Ranking of investment banks in terms of underwriting, M&A, fee earned, etcInvestment banks treat this very seriouslyMany have specialist teams devoted to supplying data to the firms that compile the rankings, and to challenging the positions of rivalsBlamed in part for the sub-prime crisis

4. Measure of Performance Risk and Returns: Returns

Introduction4. Measure of Performance League Tables:

Source: Financial Times

Introduction4. Measure of Performance League Tables: M&A

Source: Financial Times

Introduction4. Measure of Performance League Tables: M&A

Source: Financial Times

Introduction4. Measure of Performance League Tables: Equity Underwriting

Source: Financial Times

Introduction4. Measure of Performance League Tables: Equity Underwriting

Source: Financial Times

Introduction4. Measure of Performance League Tables: Debt Underwriting

Source: Financial Times

Introduction4. Measure of Performance League Tables: Debt Underwriting

Source: Financial Times

Introduction4. Measure of Performance League Tables: Loans

Source: Financial Times

Introduction4. Measure of Performance League Tables: Loans

Source: Financial Times

Introduction

Market riskInterest rate risk

Trading in fixed income securitiesPrice risk

Assets/securities price volatilityForex risk

Forex exposure

4. Measure of Performance Risk and Returns: Risks

Introduction

Credit riskCounterparty default risk: swap, derivatives, credit derivativesPrime-brokerage: Hedge fund failuresIssuers default: MBS, bonds, commercial papersIn the light of the increasingly complicated securities, who can really understand?

4. Measure of Performance Risk and Returns: Risks

Introduction

Operation risk Settlement and clearingEntry errors

Legal Tons and tons of regulations - other than all the different acts: Dodd-Frank, fair disclosure, money laundering, funding of terrorists, etcLiability law suits: eg Enron, WorldCom

4. Measure of Performance Risk and Returns: Risks

Introduction

Funding risk Borrowing: capital and money marketCredit crunchCredit squeeze

Liquidity risk What is liquidity risk?The inability to liquidate immediately at fair value

4. Measure of Performance Risk and Returns: Risks

Introduction

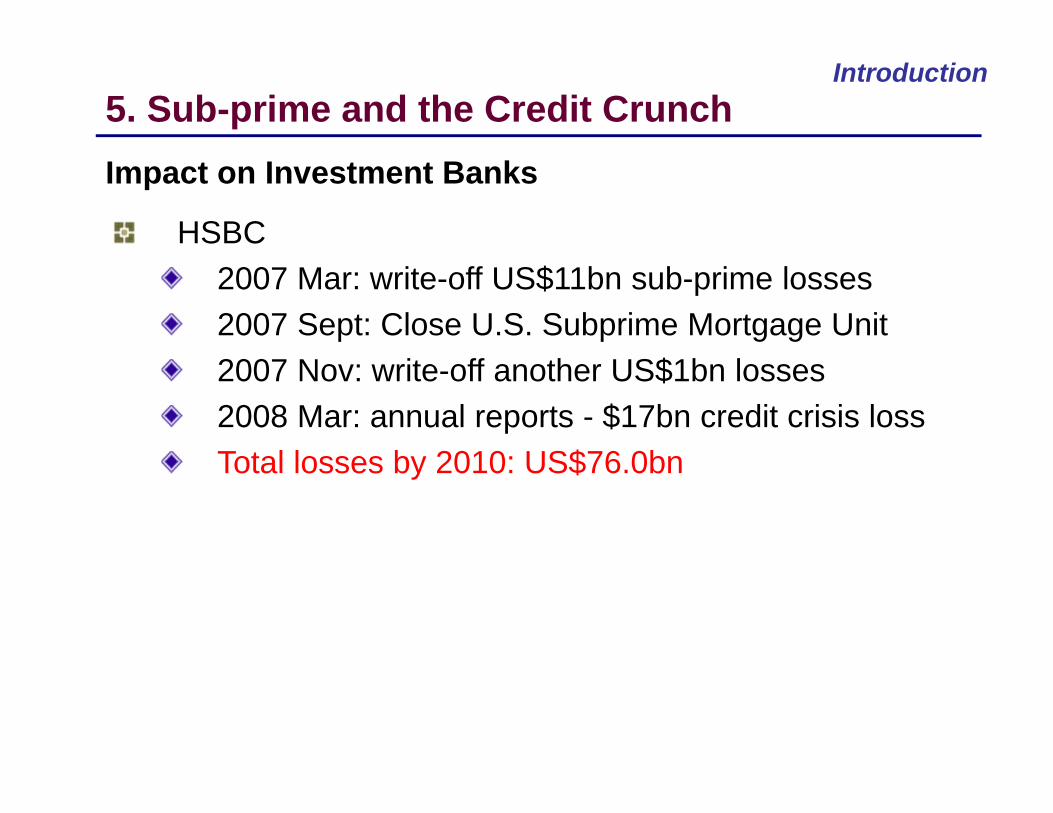

HSBC 2007 Mar: write-off US$11bn sub-prime losses2007 Sept: Close U.S. Subprime Mortgage Unit2007 Nov: write-off another US$1bn losses2008 Mar: annual reports - $17bn credit crisis lossTotal losses by 2010: US$76.0bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

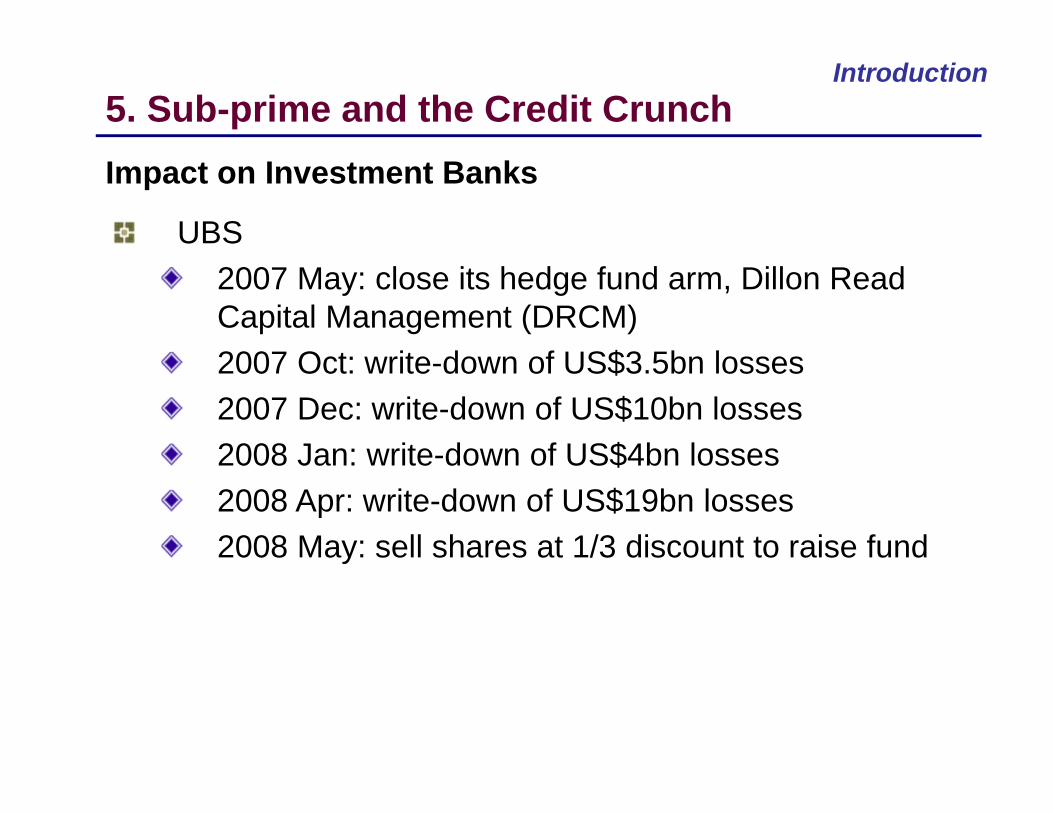

UBS 2007 May: close its hedge fund arm, Dillon Read Capital Management (DRCM)2007 Oct: write-down of US$3.5bn losses2007 Dec: write-down of US$10bn losses2008 Jan: write-down of US$4bn losses2008 Apr: write-down of US$19bn losses2008 May: sell shares at 1/3 discount to raise fund

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

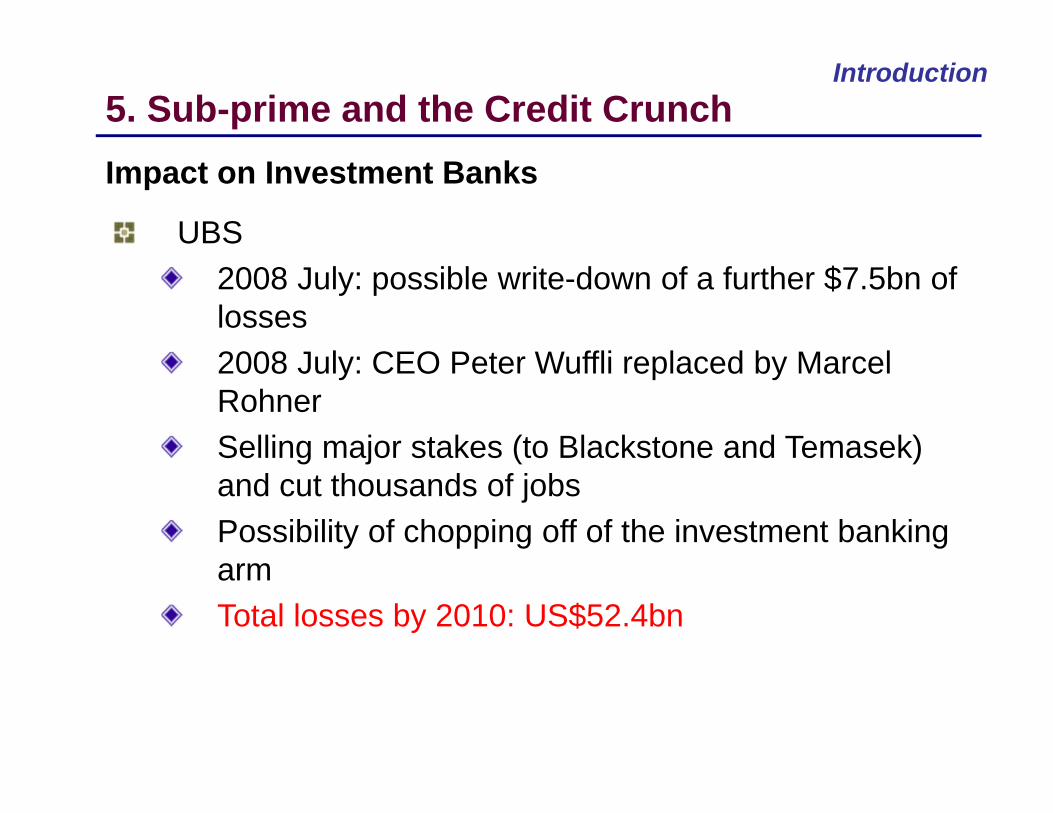

UBS 2008 July: possible write-down of a further $7.5bn of losses2008 July: CEO Peter Wuffli replaced by Marcel RohnerSelling major stakes (to Blackstone and Temasek) and cut thousands of jobsPossibility of chopping off of the investment banking arm Total losses by 2010: US$52.4bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

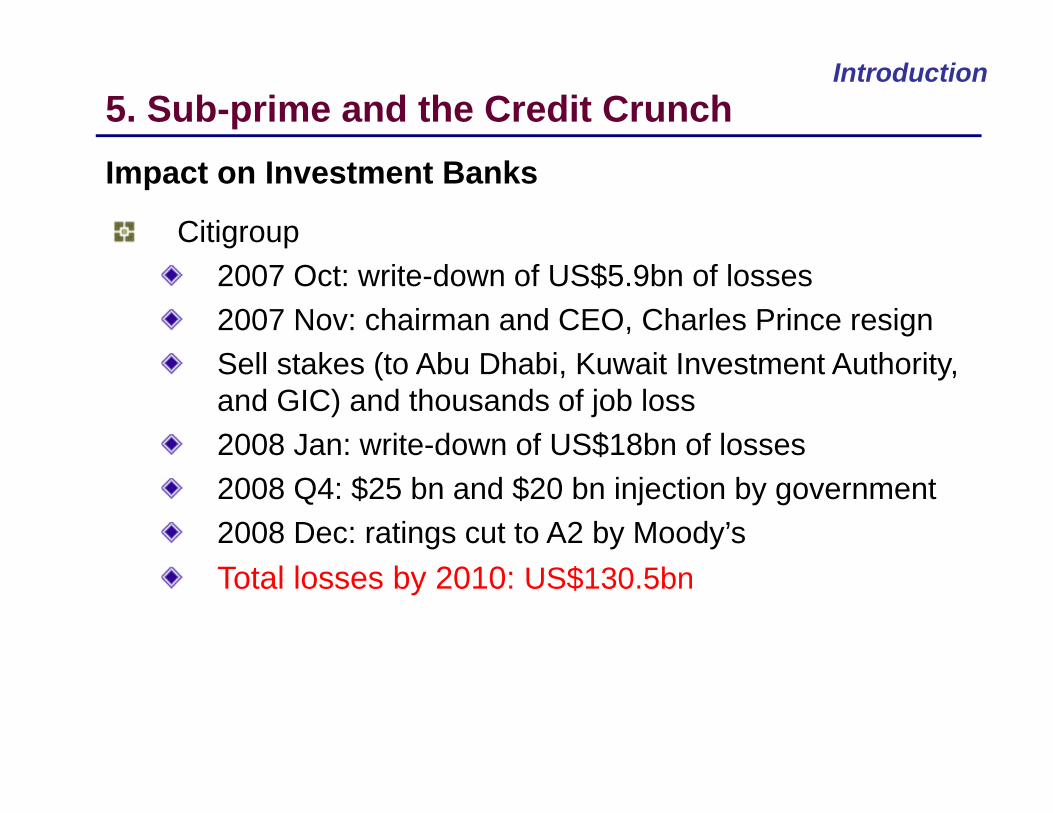

Citigroup 2007 Oct: write-down of US$5.9bn of losses2007 Nov: chairman and CEO, Charles Prince resignSell stakes (to Abu Dhabi, Kuwait Investment Authority, and GIC) and thousands of job loss2008 Jan: write-down of US$18bn of losses2008 Q4: $25 bn and $20 bn injection by government2008 Dec: ratings cut to A2 by Moody’sTotal losses by 2010: US$130.5bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

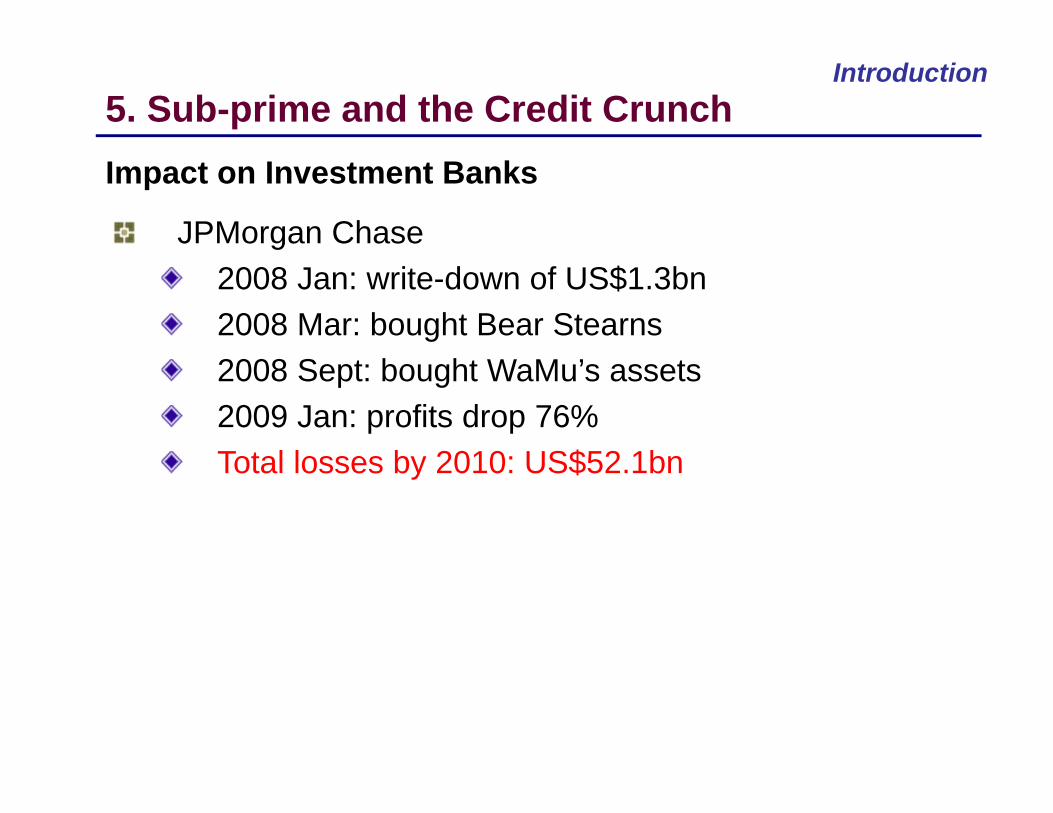

JPMorgan Chase 2008 Jan: write-down of US$1.3bn2008 Mar: bought Bear Stearns2008 Sept: bought WaMu’s assets2009 Jan: profits drop 76%Total losses by 2010: US$52.1bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

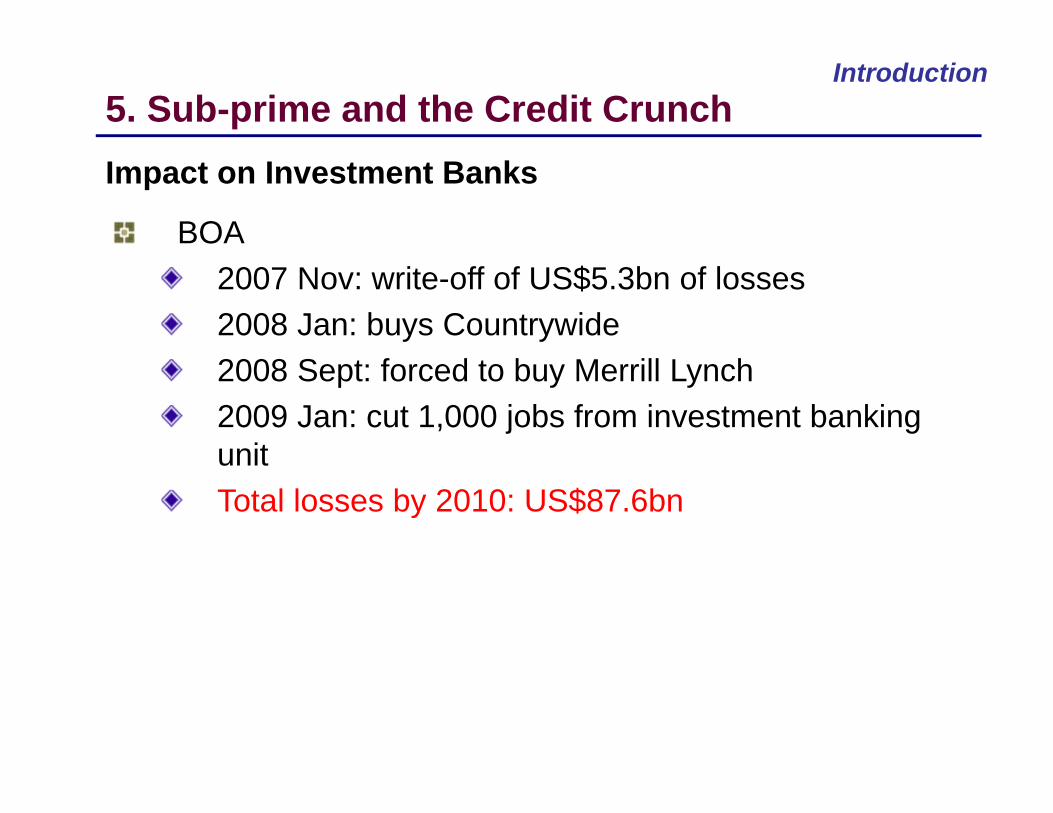

BOA2007 Nov: write-off of US$5.3bn of losses2008 Jan: buys Countrywide2008 Sept: forced to buy Merrill Lynch2009 Jan: cut 1,000 jobs from investment banking unitTotal losses by 2010: US$87.6bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

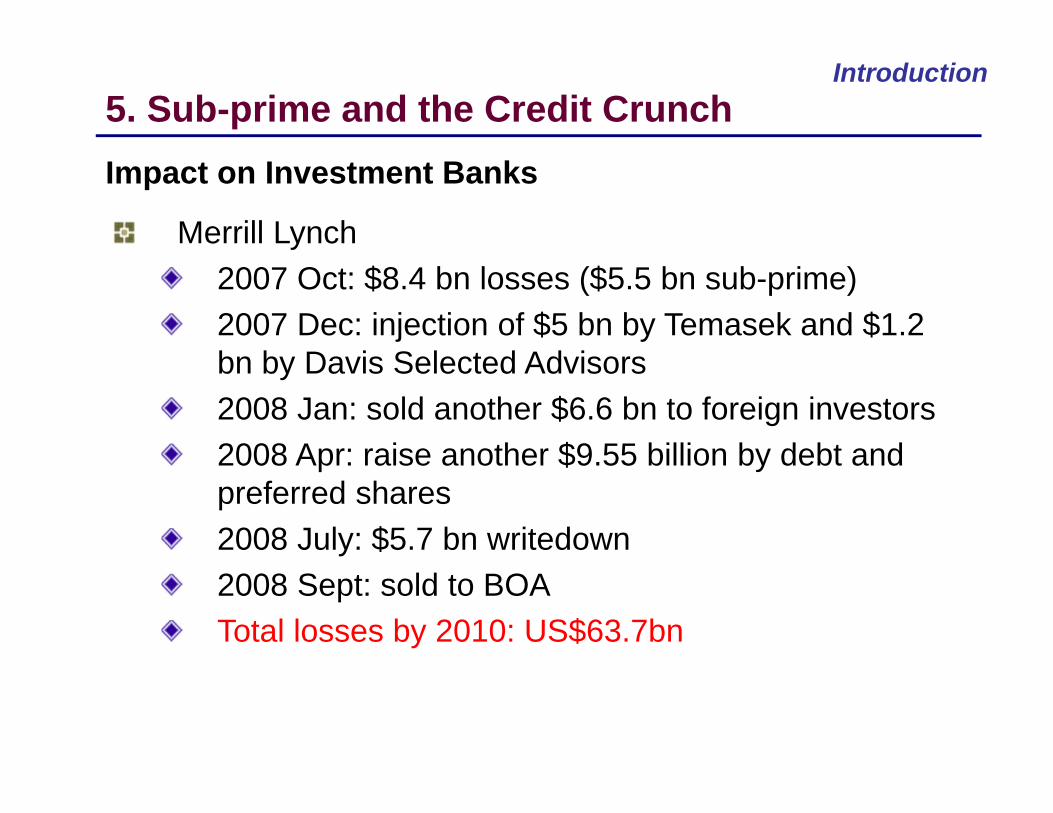

Merrill Lynch 2007 Oct: $8.4 bn losses ($5.5 bn sub-prime)2007 Dec: injection of $5 bn by Temasek and $1.2 bn by Davis Selected Advisors2008 Jan: sold another $6.6 bn to foreign investors2008 Apr: raise another $9.55 billion by debt and preferred shares2008 July: $5.7 bn writedown2008 Sept: sold to BOATotal losses by 2010: US$63.7bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

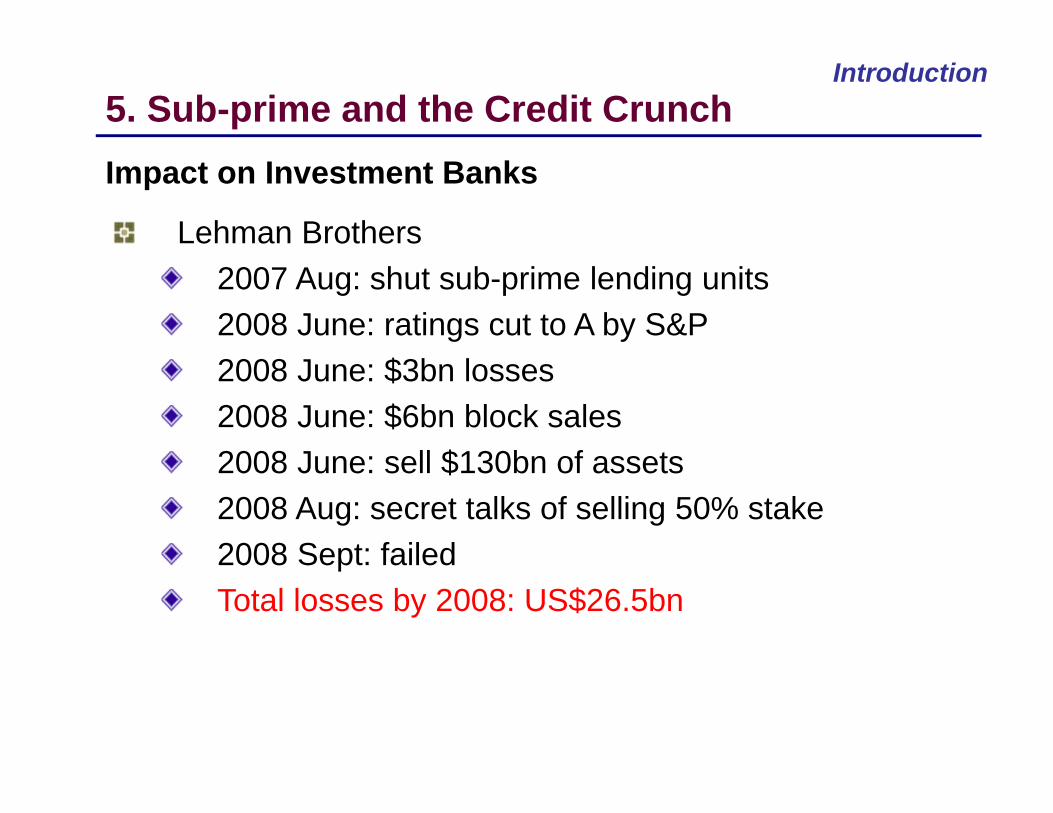

Lehman Brothers2007 Aug: shut sub-prime lending units2008 June: ratings cut to A by S&P2008 June: $3bn losses2008 June: $6bn block sales2008 June: sell $130bn of assets2008 Aug: secret talks of selling 50% stake2008 Sept: failedTotal losses by 2008: US$26.5bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction

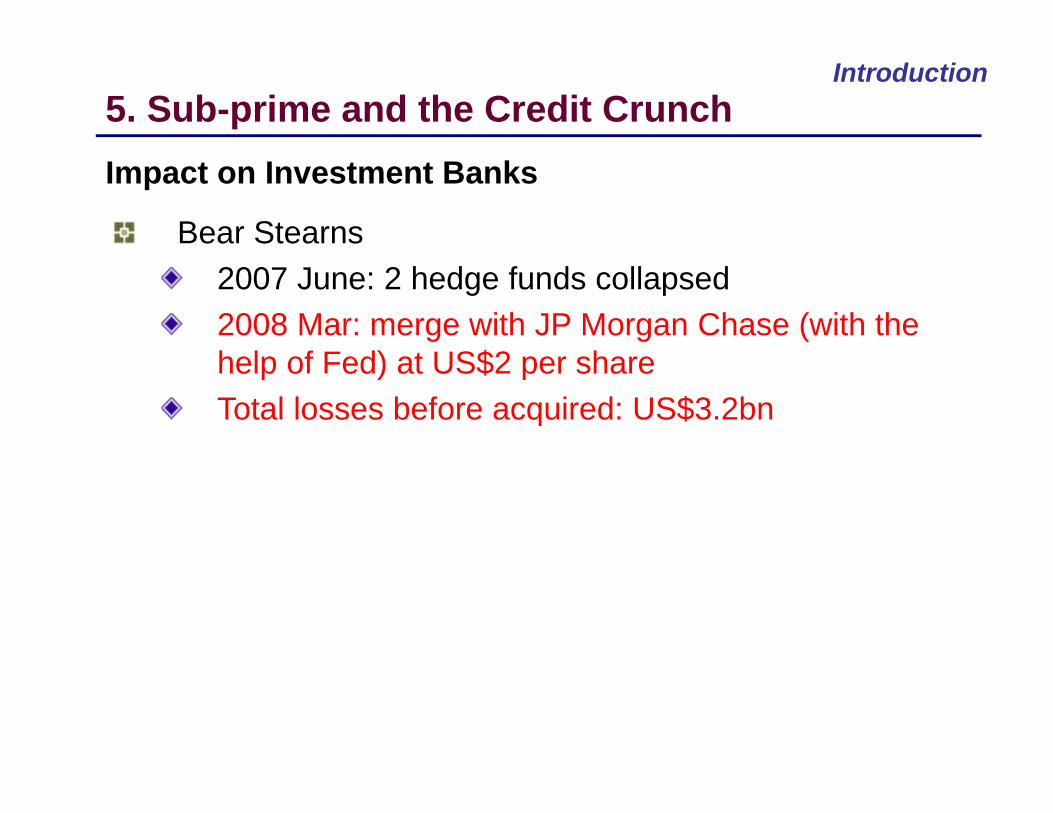

Bear Stearns2007 June: 2 hedge funds collapsed2008 Mar: merge with JP Morgan Chase (with the help of Fed) at US$2 per shareTotal losses before acquired: US$3.2bn

5. Sub-prime and the Credit Crunch Impact on Investment Banks

Introduction5. Sub-prime and the Credit Crunch

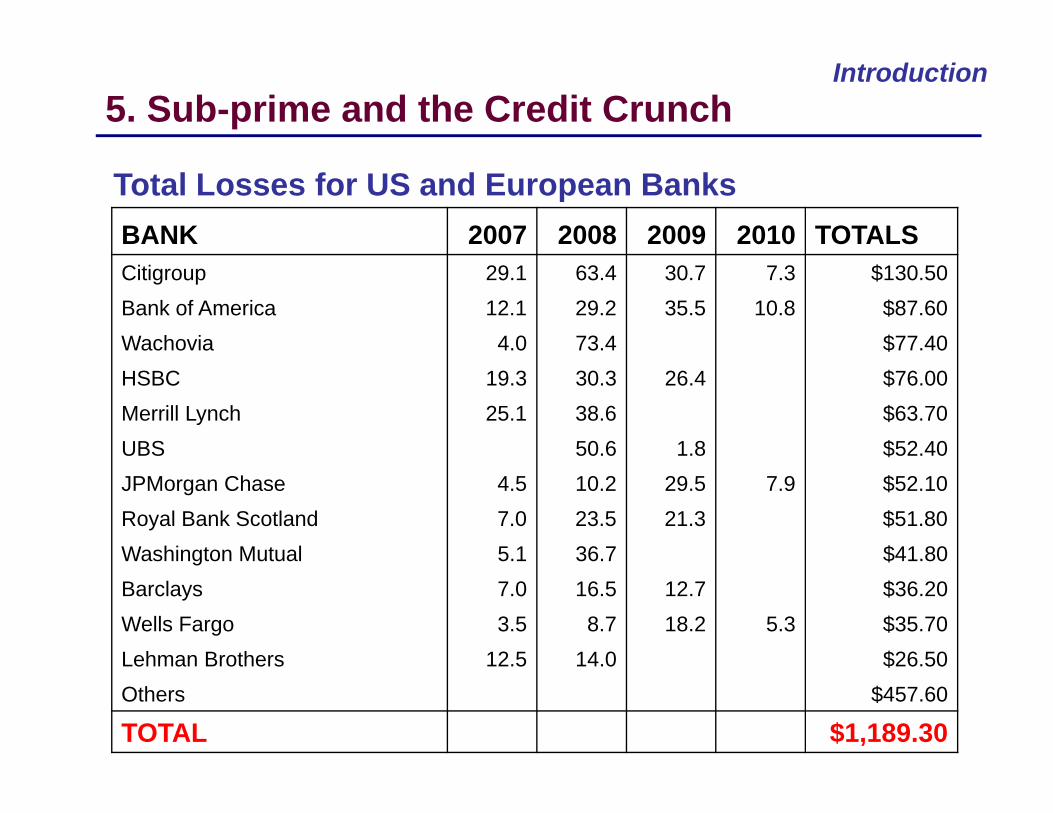

Total Losses for US and European BanksBANK 2007 2008 2009 2010 TOTALSCitigroup 29.1 63.4 30.7 7.3 $130.50 Bank of America 12.1 29.2 35.5 10.8 $87.60 Wachovia 4.0 73.4 $77.40 HSBC 19.3 30.3 26.4 $76.00 Merrill Lynch 25.1 38.6 $63.70 UBS 50.6 1.8 $52.40 JPMorgan Chase 4.5 10.2 29.5 7.9 $52.10 Royal Bank Scotland 7.0 23.5 21.3 $51.80 Washington Mutual 5.1 36.7 $41.80 Barclays 7.0 16.5 12.7 $36.20 Wells Fargo 3.5 8.7 18.2 5.3 $35.70 Lehman Brothers 12.5 14.0 $26.50 Others $457.60

TOTAL $1,189.30

![M ] D f ]kaken-techno.co.jp/.../632dec2515d7e5de4bbd01041d602e5e.pdf6 D MCA5203SE-S01 MCA3203SE-S01 MCA6202S0-S01 MCA4202S0-S01 MCA2202S0-S01 MCA8201S0-S01 MCE6202S0-S01 C"(ãTS ¥1,114,000](https://img.pdfslide.us/doc/110x75/60b7e1ebae35d90dba2d7a96/m-d-f-kaken-6-d-mca5203se-s01-mca3203se-s01-mca6202s0-s01-mca4202s0-s01-mca2202s0-s01.jpg)

![Investment banking []](https://img.pdfslide.us/doc/110x75/55a493e51a28ab131b8b45a1/investment-banking-wwwlearnerareablogspotcom.jpg)