Embed Size (px)

Citation preview

S Venkatraman,

Rabo India Finance Ltd

Delhi,

1 February 2008

Time to reflect

Biodiesel: Indian opportunity?

2

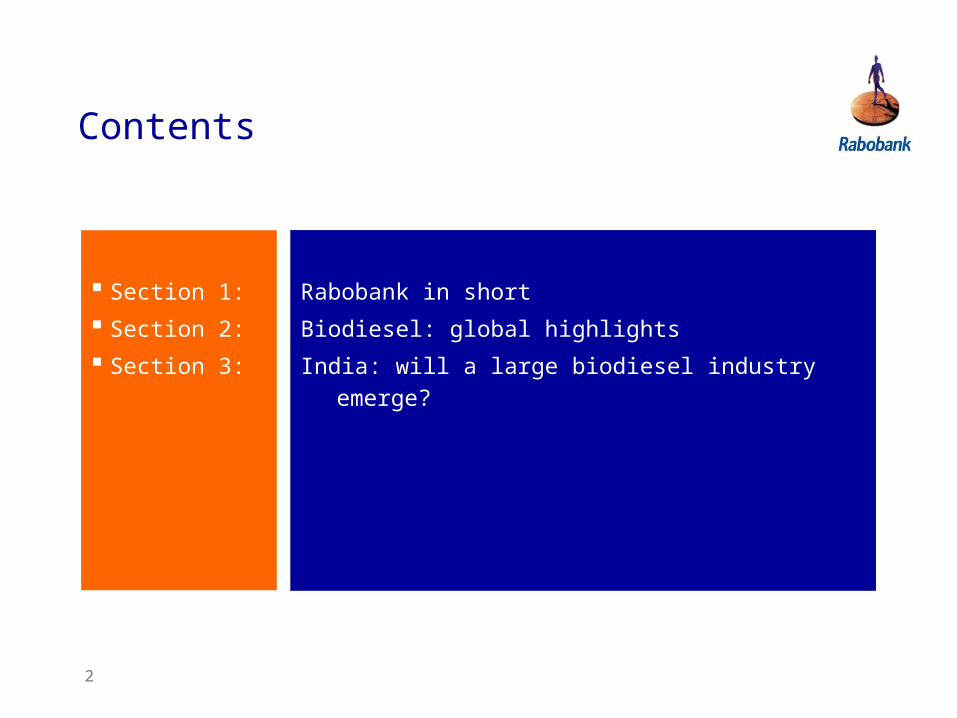

Contents

Section 1:

Section 2:

Section 3:

Rabobank in short

Biodiesel: global highlights

India: will a large biodiesel industry emerge?

Rabobank in short

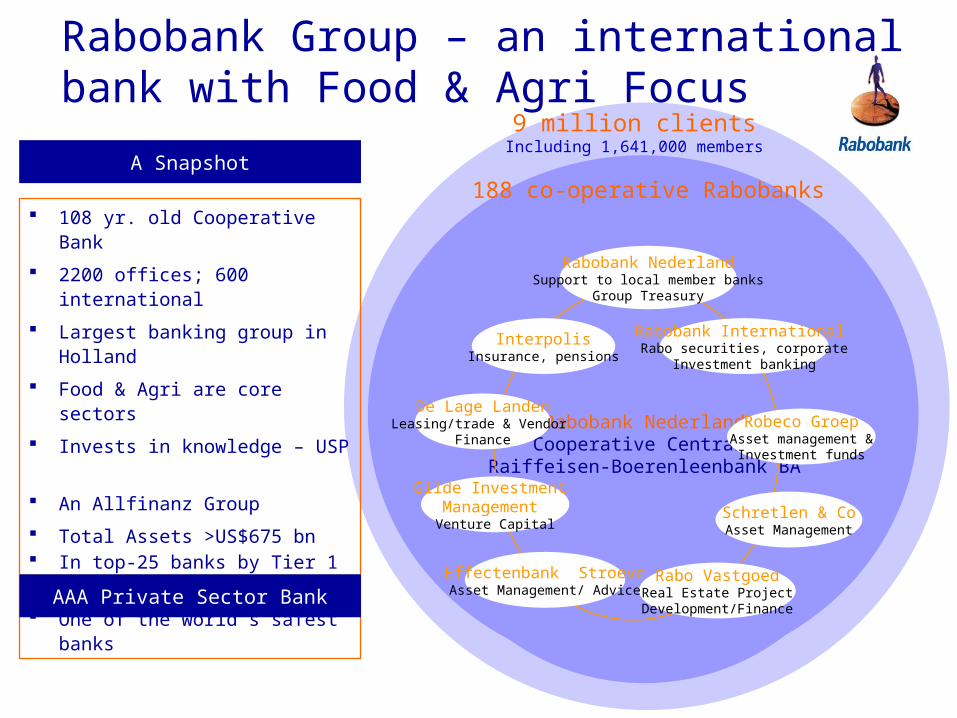

Rabobank NederlandCooperative Centrale

Raiffeisen-Boerenleenbank BA

9 million clientsIncluding 1,641,000 members

InterpolisInsurance, pensions

188 co-operative Rabobanks

Rabobank NederlandSupport to local member banks

Group Treasury

Schretlen & CoAsset Management

Robeco GroepAsset management &

Investment funds

De Lage LandenLeasing/trade & Vendor

Finance

Rabo VastgoedReal Estate Project

Development/Finance

Effectenbank StroeveAsset Management/ Advice

Gilde Investment Management Venture Capital

Rabobank International Rabo securities, corporate

Investment banking

A SnapshotA Snapshot

108 yr. old Cooperative Bank

2200 offices; 600 international

Largest banking group in Holland

Food & Agri are core sectors

Invests in knowledge – USP

An Allfinanz Group

Total Assets >US$675 bn In top-25 banks by Tier 1

capital

One of the world’s safest banks

Rabobank Group – an international bank with Food & Agri Focus

AAA Private Sector BankAAA Private Sector Bank

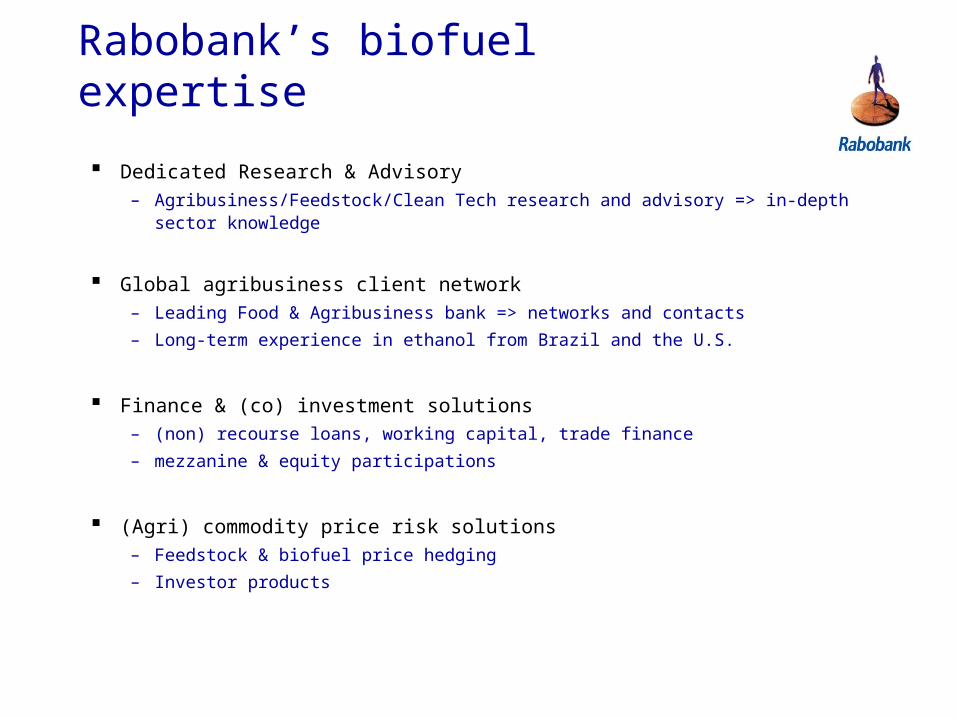

Rabobank’s biofuel expertise

Dedicated Research & Advisory– Agribusiness/Feedstock/Clean Tech research and advisory => in-depth

sector knowledge

Global agribusiness client network– Leading Food & Agribusiness bank => networks and contacts

– Long-term experience in ethanol from Brazil and the U.S.

Finance & (co) investment solutions– (non) recourse loans, working capital, trade finance

– mezzanine & equity participations

(Agri) commodity price risk solutions– Feedstock & biofuel price hedging

– Investor products

Biodiesel: global highlights

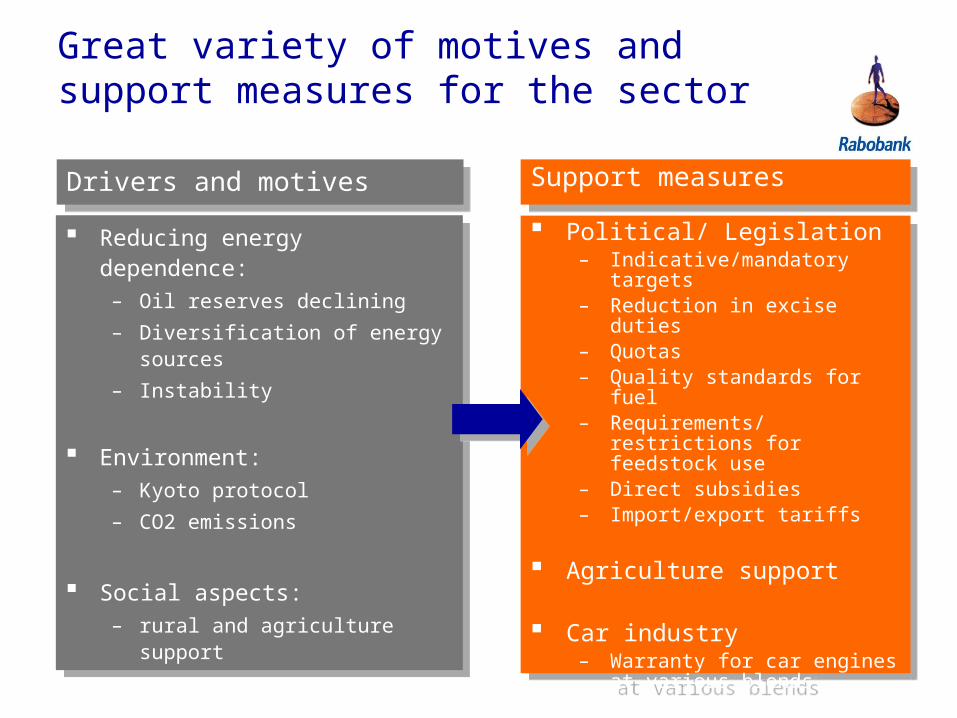

Great variety of motives and support measures for the sector

Reducing energy dependence:– Oil reserves declining

– Diversification of energy sources

– Instability

Environment: – Kyoto protocol

– CO2 emissions

Social aspects: – rural and agriculture support

Reducing energy dependence:– Oil reserves declining

– Diversification of energy sources

– Instability

Environment: – Kyoto protocol

– CO2 emissions

Social aspects: – rural and agriculture support

Political/ Legislation– Indicative/mandatory targets– Reduction in excise duties– Quotas – Quality standards for fuel– Requirements/restrictions

for feedstock use– Direct subsidies– Import/export tariffs

Agriculture support

Car industry– Warranty for car engines at

various blends

Political/ Legislation– Indicative/mandatory targets– Reduction in excise duties– Quotas – Quality standards for fuel– Requirements/restrictions

for feedstock use– Direct subsidies– Import/export tariffs

Agriculture support

Car industry– Warranty for car engines at

various blends

Drivers and motivesDrivers and motives Support measuresSupport measures

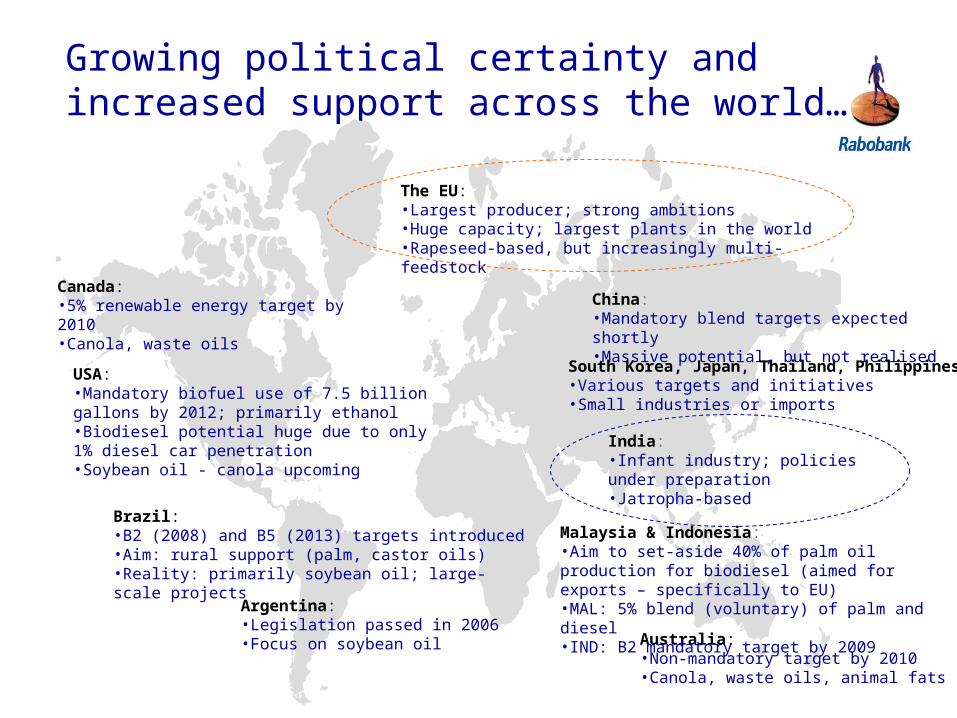

Growing political certainty and increased support across the world…

USA:•Mandatory biofuel use of 7.5 billion gallons by 2012; primarily ethanol•Biodiesel potential huge due to only 1% diesel car penetration•Soybean oil - canola upcoming

Brazil:•B2 (2008) and B5 (2013) targets introduced•Aim: rural support (palm, castor oils)•Reality: primarily soybean oil; large-scale projects

The EU:•Largest producer; strong ambitions•Huge capacity; largest plants in the world•Rapeseed-based, but increasingly multi-feedstock

China: •Mandatory blend targets expected shortly•Massive potential, but not realised

Australia: •Non-mandatory target by 2010•Canola, waste oils, animal fats

Argentina: •Legislation passed in 2006•Focus on soybean oil

Canada: •5% renewable energy target by 2010•Canola, waste oils

South Korea, Japan, Thailand, Philippines:•Various targets and initiatives•Small industries or imports

India: •Infant industry; policies under preparation•Jatropha-based

Malaysia & Indonesia: •Aim to set-aside 40% of palm oil production for biodiesel (aimed for exports – specifically to EU)•MAL: 5% blend (voluntary) of palm and diesel•IND: B2 mandatory target by 2009

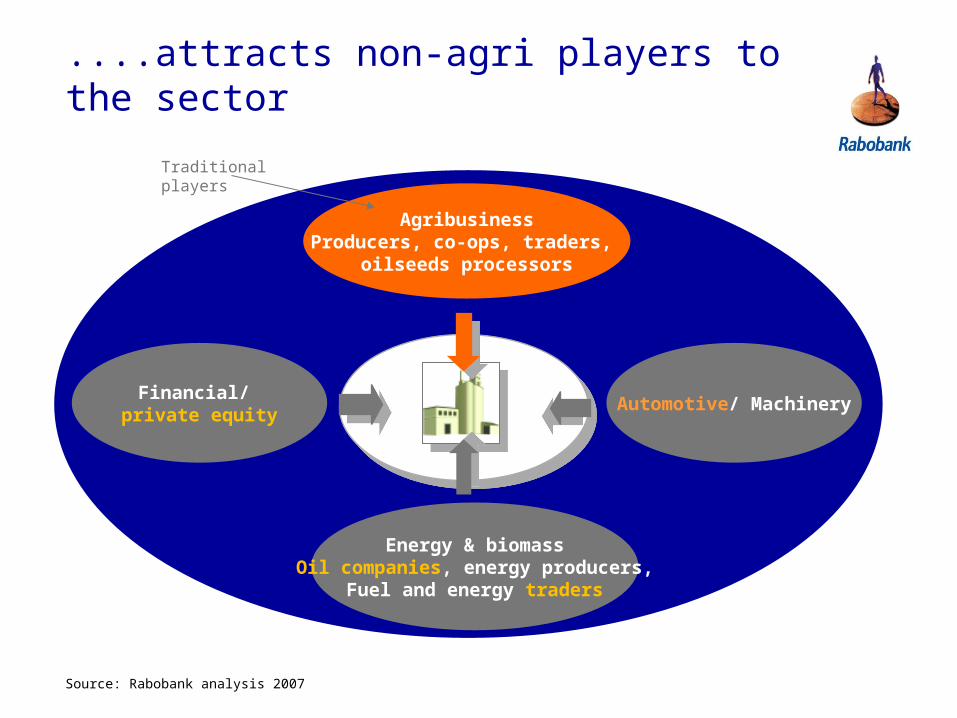

....attracts non-agri players to the sector

AgribusinessProducers, co-ops, traders,

oilseeds processors

Energy & biomassOil companies, energy producers,

Fuel and energy traders

Financial/ private equity

Automotive/ Machinery

Source: Rabobank analysis 2007

Traditional players

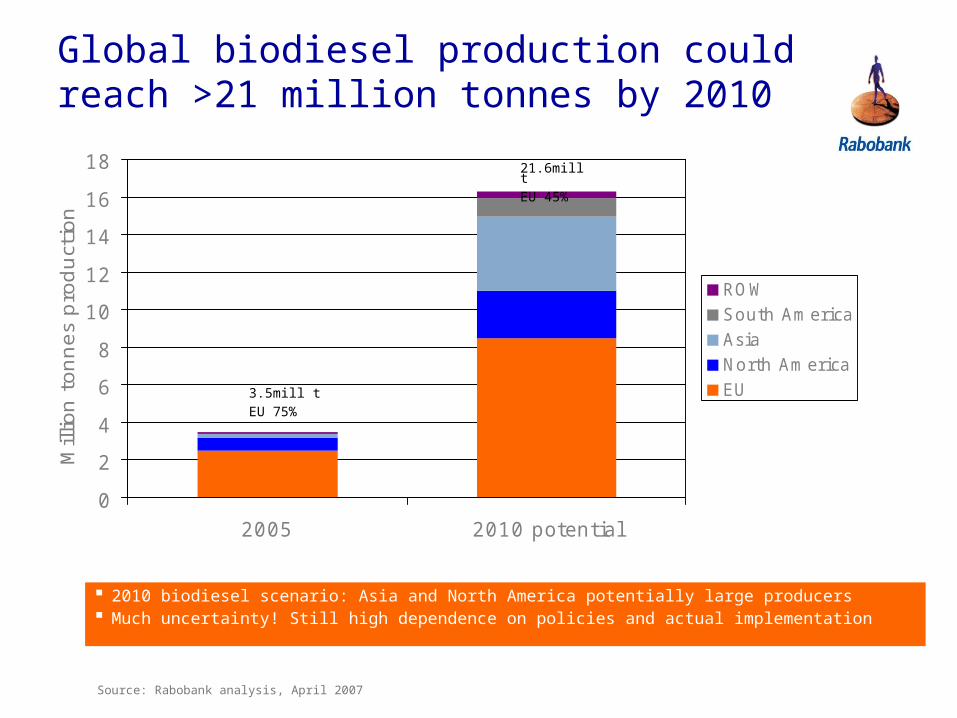

Global biodiesel production could reach >21 million tonnes by 2010

2010 biodiesel scenario: Asia and North America potentially large producers Much uncertainty! Still high dependence on policies and actual implementation

Source: Rabobank analysis, April 2007

0

2

4

6

8

10

12

14

16

18

2005 2010 potential

Mill

ion

ton

nes

pro

du

ctio

n

ROWSouth AmericaAsiaNorth AmericaEU

21.6mill tEU 45%

3.5mill tEU 75%

0

20

40

60

80

100

120

140

2005 demand Add. demandfood

Add. demandbiodiesel

2010 est.demand

Millio

n t

on

nes 96

13

18 127

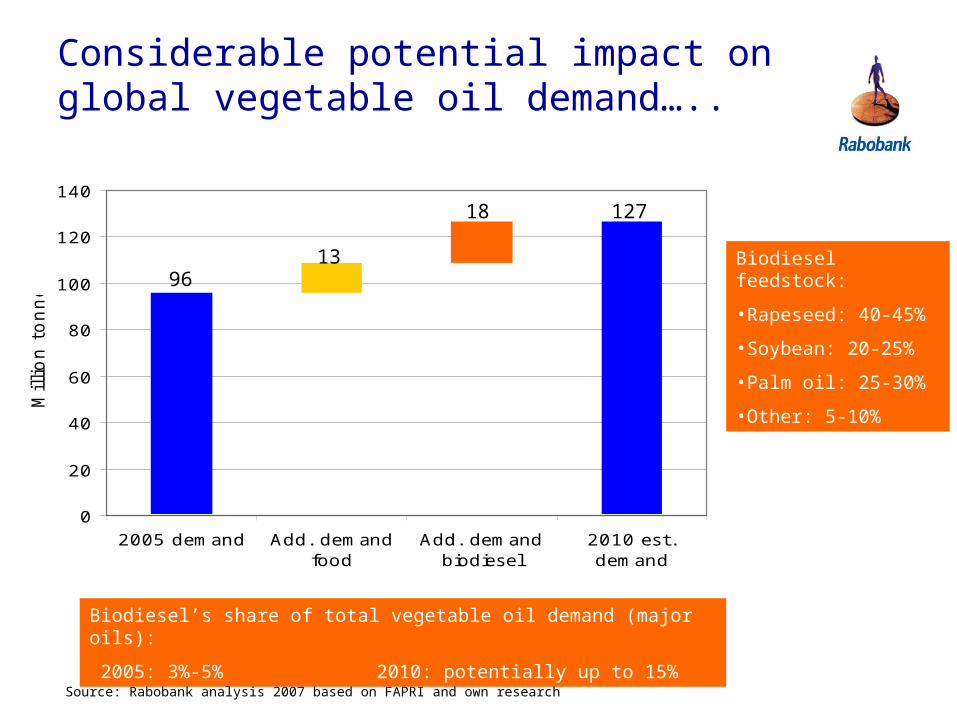

Considerable potential impact on global vegetable oil demand…..

Biodiesel’s share of total vegetable oil demand (major oils):

2005: 3%-5% 2010: potentially up to 15%

Source: Rabobank analysis 2007 based on FAPRI and own research

Biodiesel feedstock:

•Rapeseed: 40-45%

•Soybean: 20-25%

•Palm oil: 25-30%

•Other: 5-10%

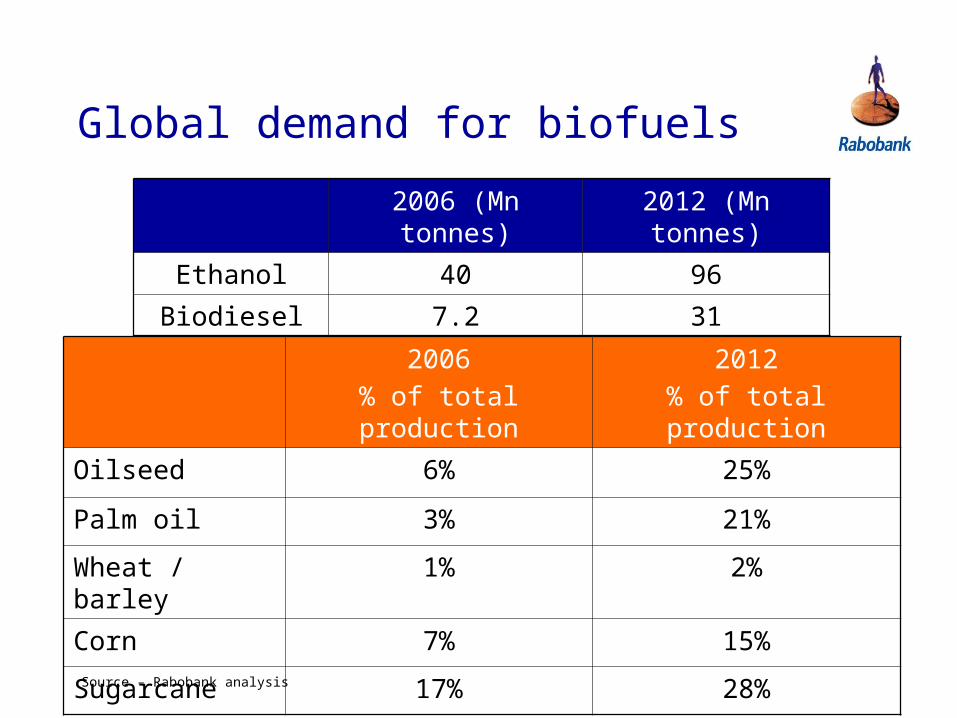

Global demand for biofuels

2006% of total production

2012% of total production

Oilseed 6% 25%

Palm oil 3% 21%

Wheat / barley 1% 2%

Corn 7% 15%

Sugarcane 17% 28%

Source – Rabobank analysis

2006 (Mn tonnes)

2012 (Mn tonnes)

Ethanol 40 96

Biodiesel 7.2 31

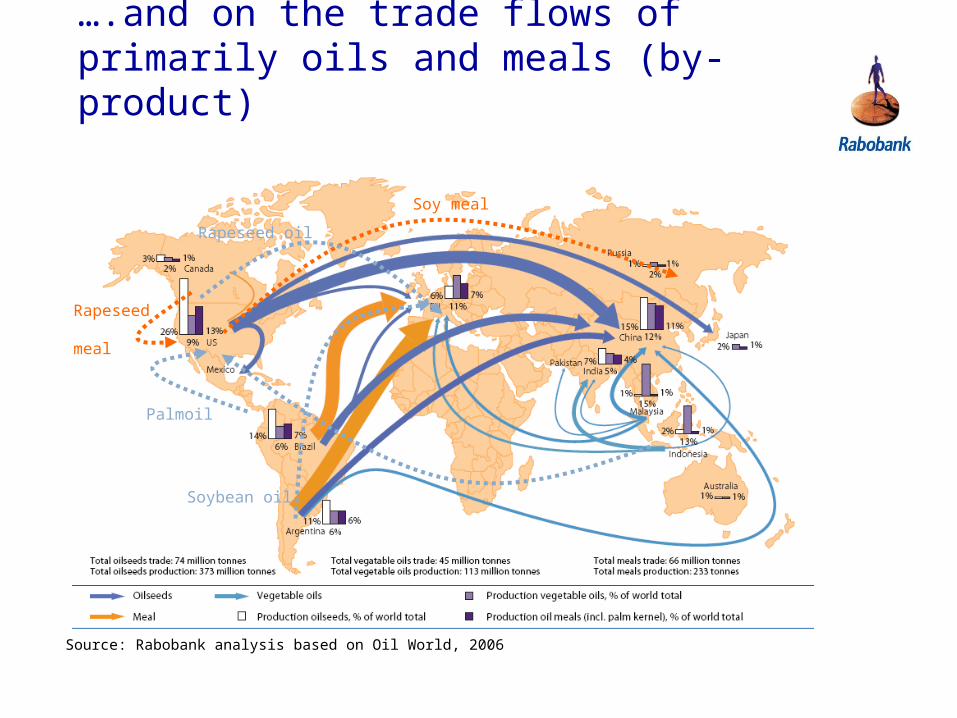

….and on the trade flows of primarily oils and meals (by-product)

Soy meal

Palmoil

Rapeseed oil

Rapeseed meal

Source: Rabobank analysis based on Oil World, 2006

Soybean oil

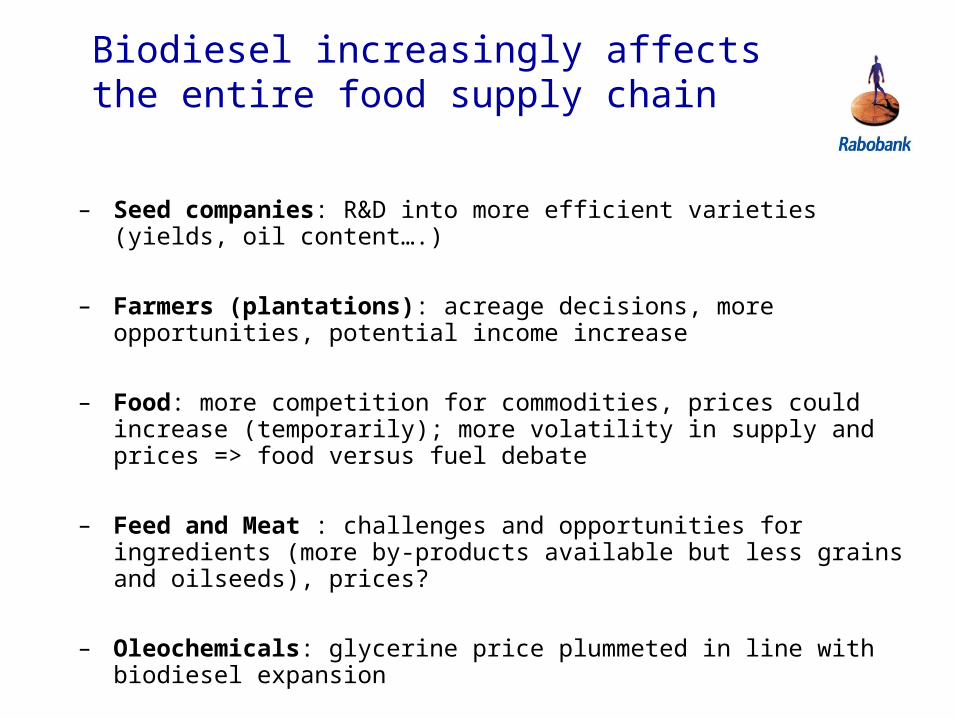

Biodiesel increasingly affects the entire food supply chain

– Seed companies: R&D into more efficient varieties (yields, oil content….)

– Farmers (plantations): acreage decisions, more opportunities, potential income increase

– Food: more competition for commodities, prices could increase (temporarily); more volatility in supply and prices => food versus fuel debate

– Feed and Meat : challenges and opportunities for ingredients (more by-products available but less grains and oilseeds), prices?

– Oleochemicals: glycerine price plummeted in line with biodiesel expansion

India: will a large biodiesel industry emerge?

What do the global developments mean for India?

Availability of vegetable oils is under pressure More competition for vegetable oils for food plus biodiesel use

Potentially higher prices; certainly more volatility

India is already dependant on oil imports for food (priority), so most likely a biodiesel sector would not be based on imported oils

Learning points from countries with similar issues; e.g. Brazil Brazil’s policy is closest to India’s intentions; however, even though the

Brazilian government aimed at supporting the rural population with their policies by promoting the use of niche crops like palm and castor oil, in reality most projects are large scale, based on soybean oil

The most important learning point is that without a concerted effort between the government, agriculture, and industry, such a policy is not likely to benefit smallholders directly

Tackling the barriers in India

Legislation and policies: necessary, but still not well-defined

– Learning points from all other countries show that a biodiesel sector need a long-term, consistent, policy to develop large scale

– Most successful policies include mandatory blending and tax credits

– Subsidies required in the initial years

Supply chain and infrastructure need to be developed

– There is no established world commodity market for jatropha (like e.g rapeseed) so a ‘new’ supply chain from farmer to consumer should be set up

– Guaranteed off-take is needed to a large extent if farmers should be convinced to grow the plant

– Education of the parties in the chain, particularly of farmers is needed

– Extraction plants close to catchment area – participation of cooperatives

– Soft loans for developing storage infrastructure

– Local energy production in small scale power generators

Tackling the barriers ...(2)

R&D thrust– defining benckmarks and best practices

– developing high oil-content varieties for different climate zones;

– identification and control of different pests and diseases;

– facilitating intercropping,

– minimising water whilst maintaining yields;

– developing other uses for jatropha oil;

– detoxification of the waste products of the jatropha seeds

– new applications of glycerine as well as other chemicals

– biodiesel from high FFA oil

– GM technologies

– Second generation biofuels

– PPP model

Tackling the barriers … (3)

Commercially viable option?

– Profitability open for debate due to large variation in estimates

– biodiesel is generally not profitable except with government support (or very high oil prices)!

– seed price to be completely market linked / linked to final biodiesel price in the long run

– there is a strong case for subsidising jatropha seed production, and also biodiesel production, for the initial period.

Financing is a challenge

– Pre-financing needed for 4 years

– costs of high-quality planting material and other material inputs, labour costs, irrigation and other expenses incurred in the initial years

– considerable obstacle for small-holders

– Banks and financial institutes hesitant to lend money unless projects are economically viable and/or there is ‘certain’ policy support

“The financial link in the global food chain”™

S Venkatraman

Director – Strategic Advisory and Research

Food and Agribusiness

Rabo India Finance Ltd

Mumbai (INDIA)

Tel – 91-22-22034567

Email – [email protected]