Embed Size (px)

Citation preview

RWE Thames Water12th August 2003, London

Bill Alexander, CEO RWE Thames Water & American Water

Chris Bunker, CFO RWE Thames Water

Ellen Wolf, CFO American Water

2

Agenda

n Introduction Harry Roels

n Overall Picture Bill Alexander

n Financial Review Chris Bunker

n Business Reviews

– Germany & Eastern Europe Chris Bunker

– United Kingdom Chris Bunker

– Americas Ellen Wolf

n Future Outlook & Conclusions Bill Alexander

2

The Overall Picture

4

RWE WaterStrong Position in Core Markets

Americas OtherGermanyUK

Sal

es

4

5

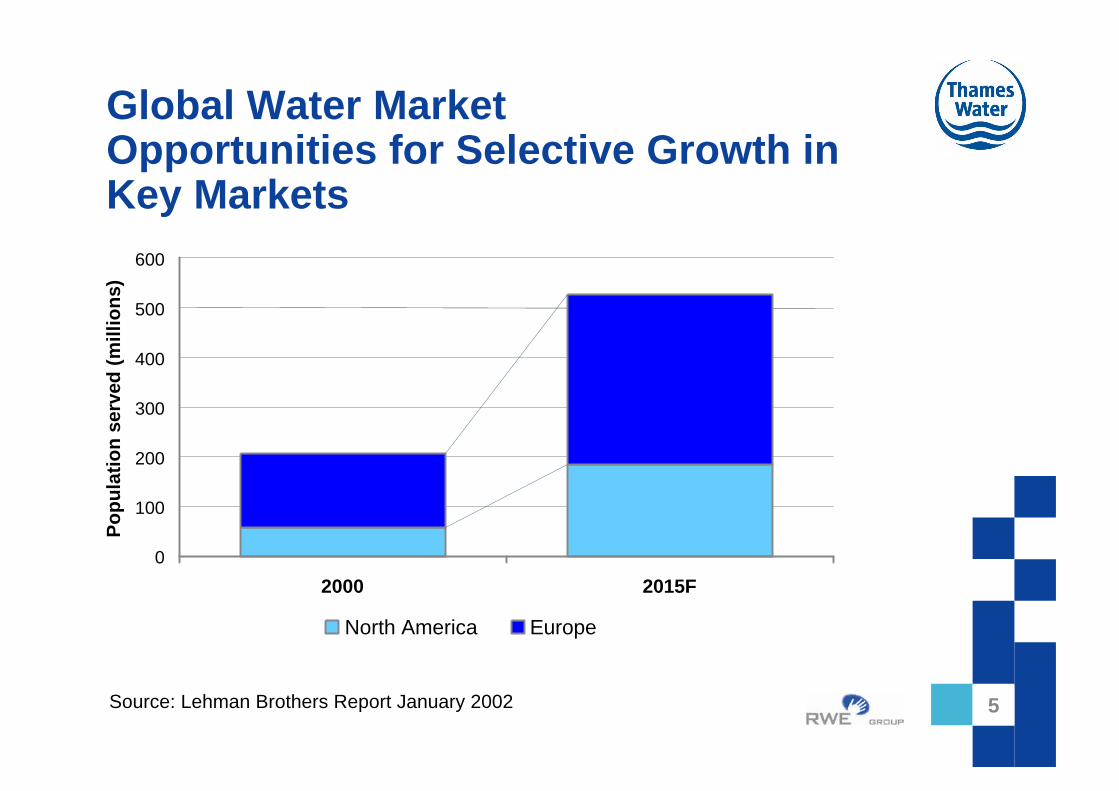

Global Water MarketOpportunities for Selective Growth in Key Markets

Source: Lehman Brothers Report January 2002 5

0

100

200

300

400

500

600

2000 2015F

Po

pu

lati

on

ser

ved

(mill

ion

s)

North America Europe

6

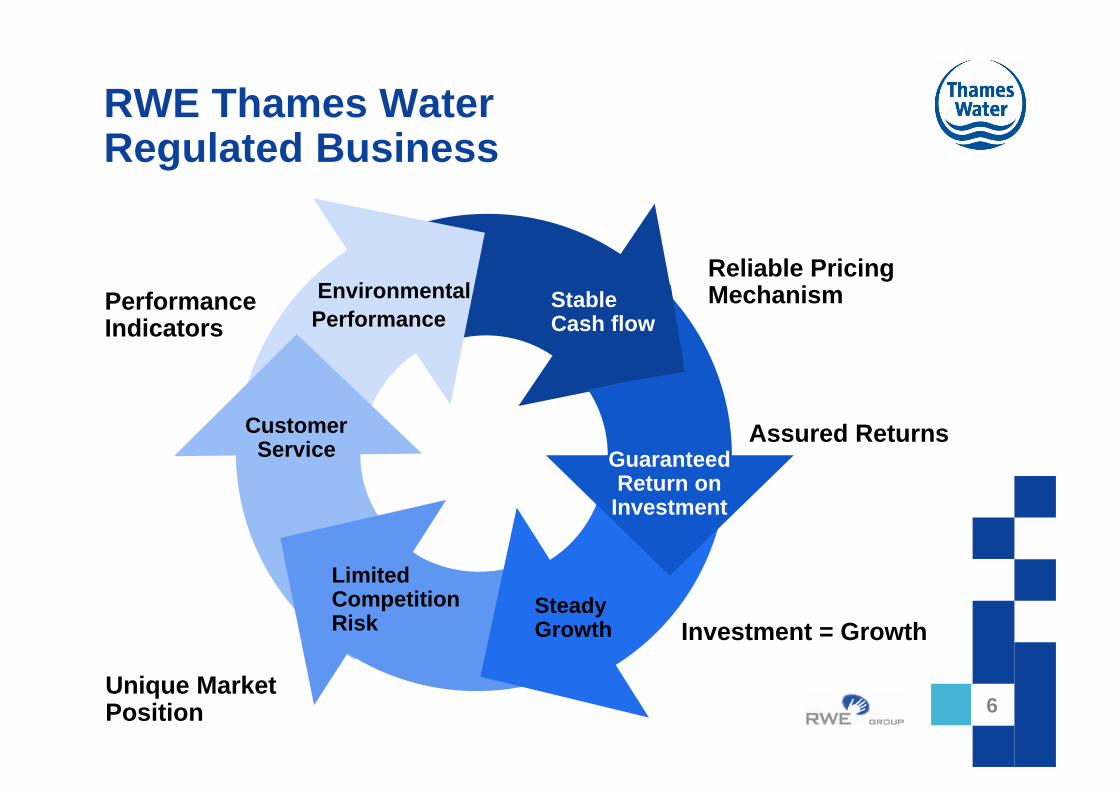

RWE Thames WaterRegulated Business

Assured ReturnsCustomerService

PerformanceIndicators

Investment = GrowthSteadyGrowth

Unique MarketPosition

LimitedCompetitionRisk

Reliable Pricing Mechanism

Guaranteed Return on Investment

Environmental Performance

Stable Cash flow

6

7

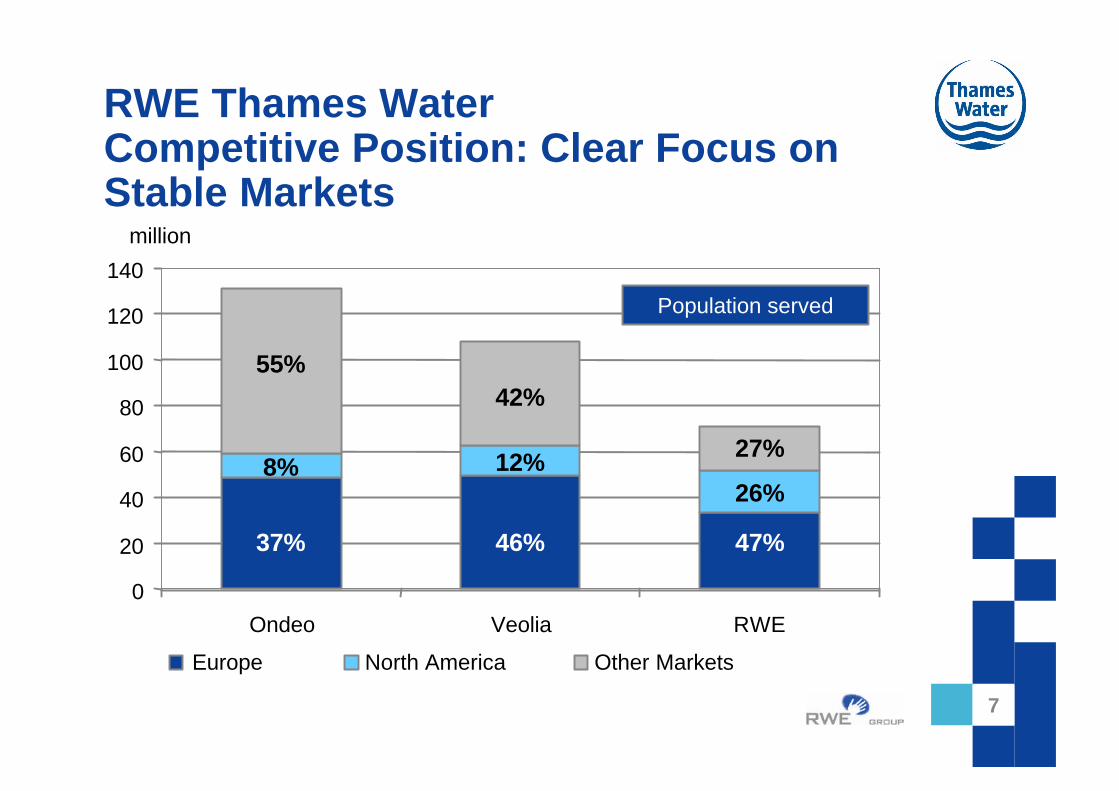

RWE Thames WaterCompetitive Position: Clear Focus on Stable Markets

0

20

40

60

80

100

120

140

Ondeo Veolia RWE

Europe North America Other Markets

55%42%

27%

37%

8%

46%

12%

47%

26%

Population served

7

million

8

RWE Thames WaterEfficiency Opportunities

n Business Integration is a core strength and delivers value through

– Combination benefits

– Greater purchasing power in procurement

– Best practice and knowledge transfer

n Further benefits as part of the RWE Group

– Shared Service Centres and Cross-selling initiatives

– Leverage of German business streams through RWE Energy

8

9

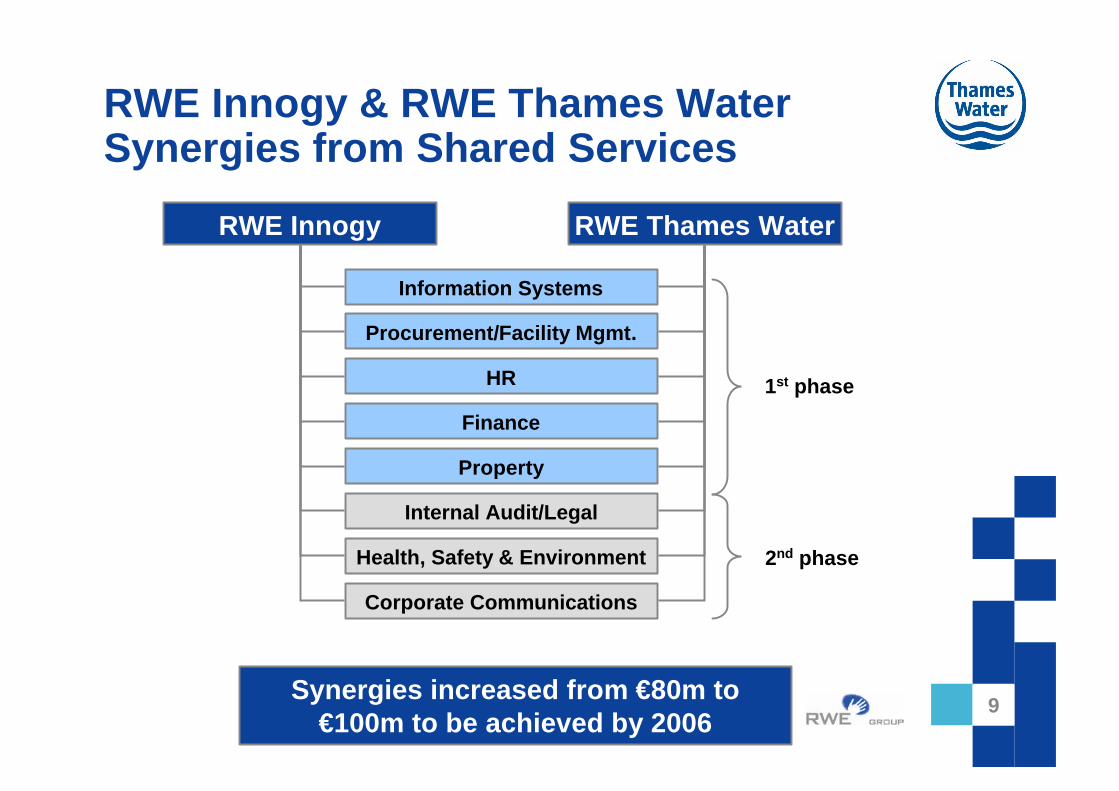

RWE Innogy RWE Thames Water

Information Systems

HR

Procurement/Facility Mgmt.

Finance

Property

Internal Audit/Legal

Health, Safety & Environment

Corporate Communications

Synergies increased from €80m to €100m to be achieved by 2006

1st phase

2nd phase

RWE Innogy & RWE Thames WaterSynergies from Shared Services

9

Financial Review

11

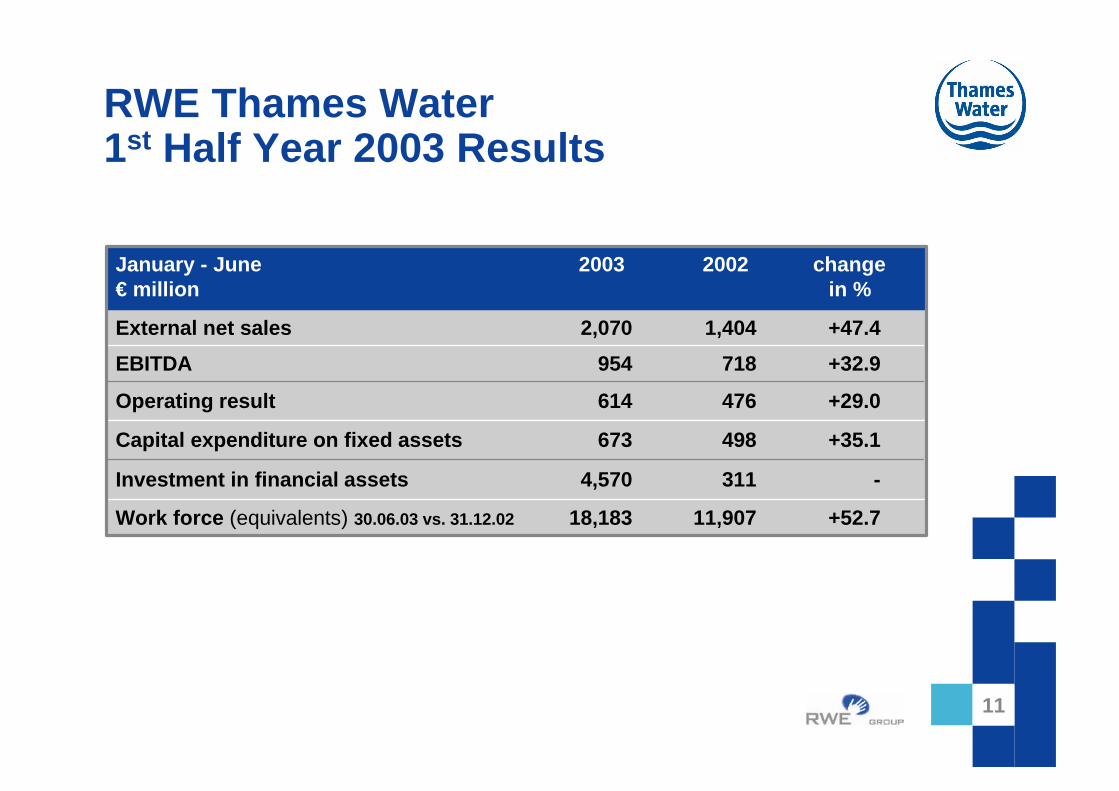

RWE Thames Water1st Half Year 2003 Results

Work force (equivalents) 30.06.03 vs. 31.12.02 18,183 11,907 +52.7

External net sales 2,070 1,404 +47.4

EBITDA 954 718 +32.9

Operating result 614 476 +29.0

January - June 2003 2002 change€ million in %

Investment in financial assets 4,570 311 -

Capital expenditure on fixed assets 673 498 +35.1

11

12

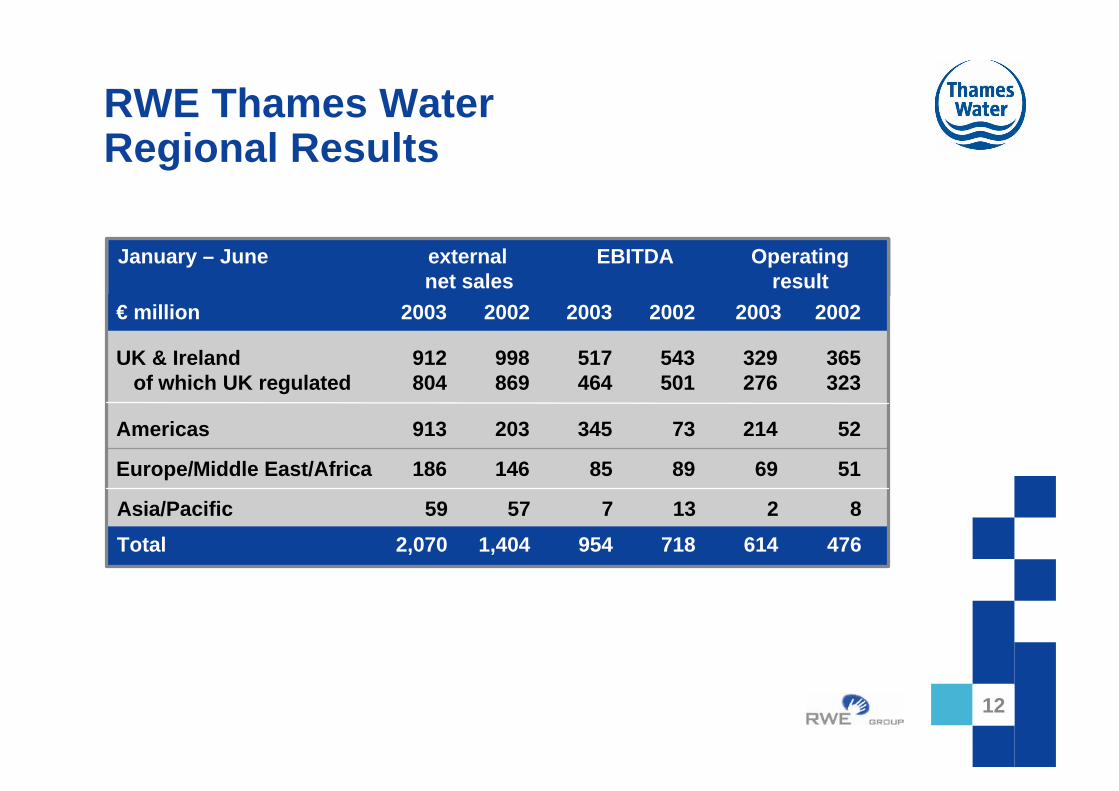

RWE Thames WaterRegional Results

Asia/Pacific 59 57 7 13 2 8

UK & Ireland 912 998 517 543 329 365of which UK regulated 804 869 464 501 276 323

Europe/Middle East/Africa 186 146 85 89 69 51

Americas 913 203 345 73 214 52

January – June external EBITDA Operatingnet sales result

Total 2,070 1,404 954 718 614 476

€ million 2003 2002 2003 2002 2003 2002

12

13

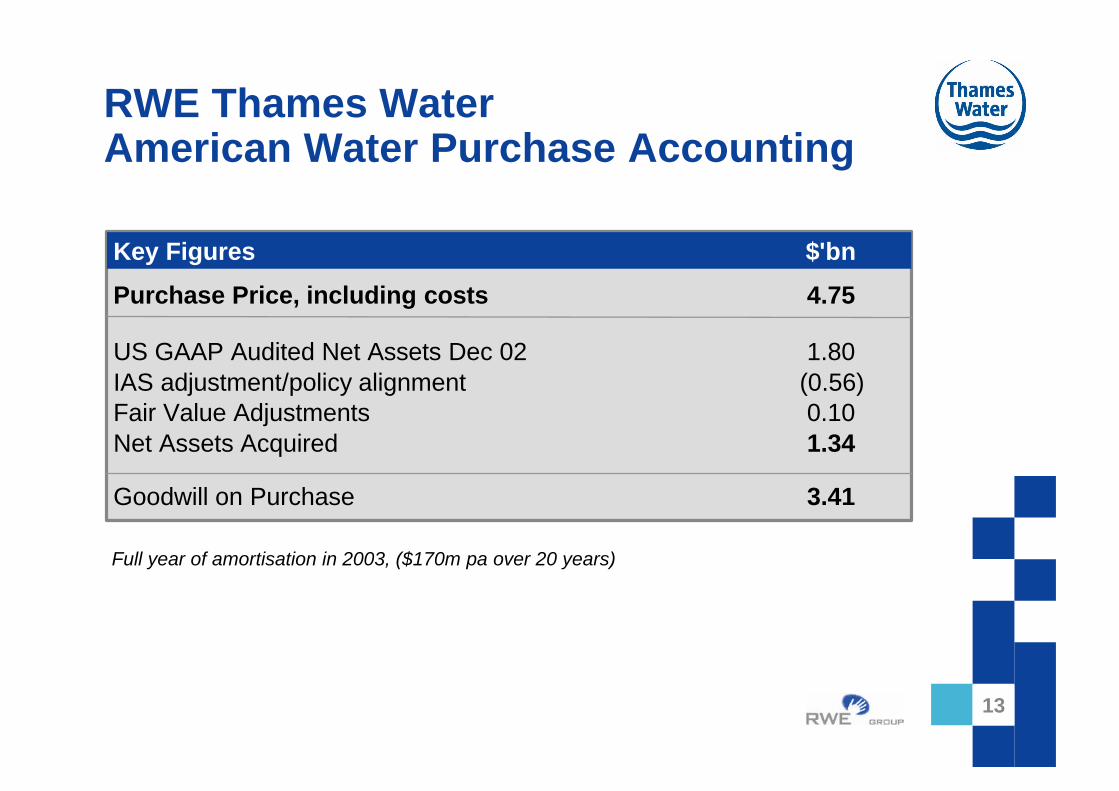

RWE Thames WaterAmerican Water Purchase Accounting

13

Key Figures $'bn

Purchase Price, including costs 4.75

US GAAP Audited Net Assets Dec 02 1.80IAS adjustment/policy alignment (0.56)Fair Value Adjustments 0.10Net Assets Acquired 1.34

Goodwill on Purchase 3.41

Full year of amortisation in 2003, ($170m pa over 20 years)

14

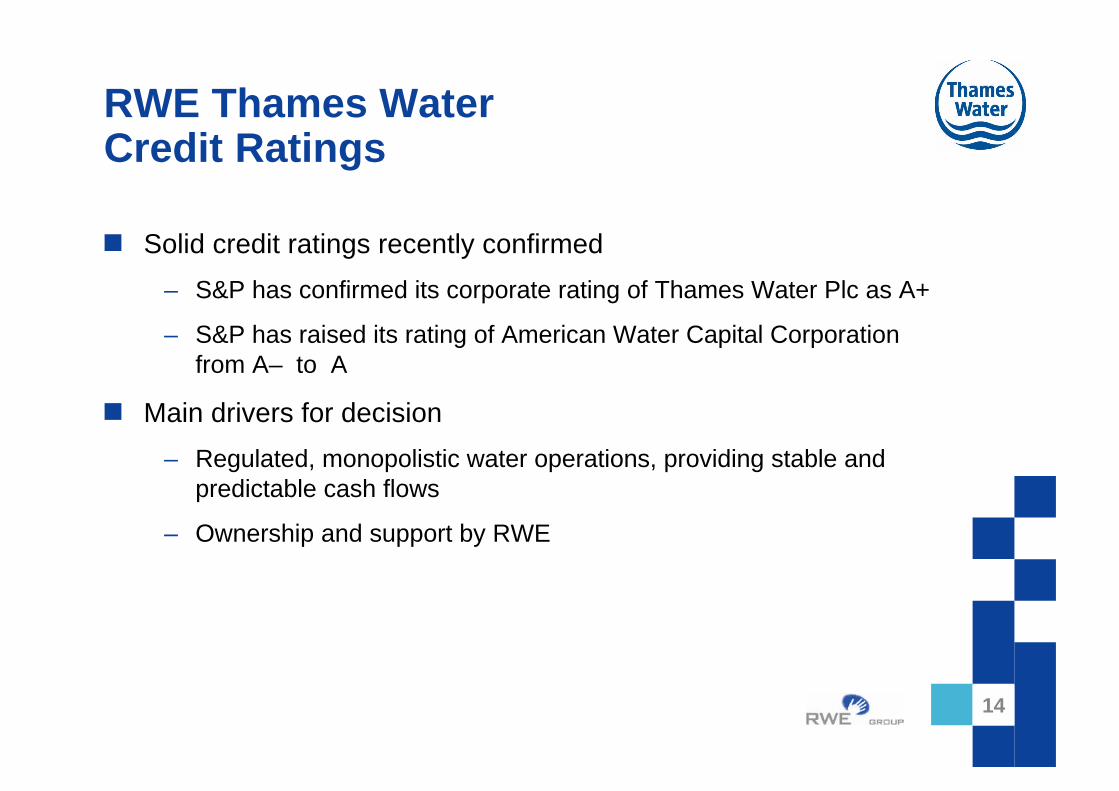

RWE Thames WaterCredit Ratings

n Solid credit ratings recently confirmed

– S&P has confirmed its corporate rating of Thames Water Plc as A+

– S&P has raised its rating of American Water Capital Corporation from A– to A

n Main drivers for decision

– Regulated, monopolistic water operations, providing stable and predictable cash flows

– Ownership and support by RWE

14

Business Review

Germany & Eastern Europe

17

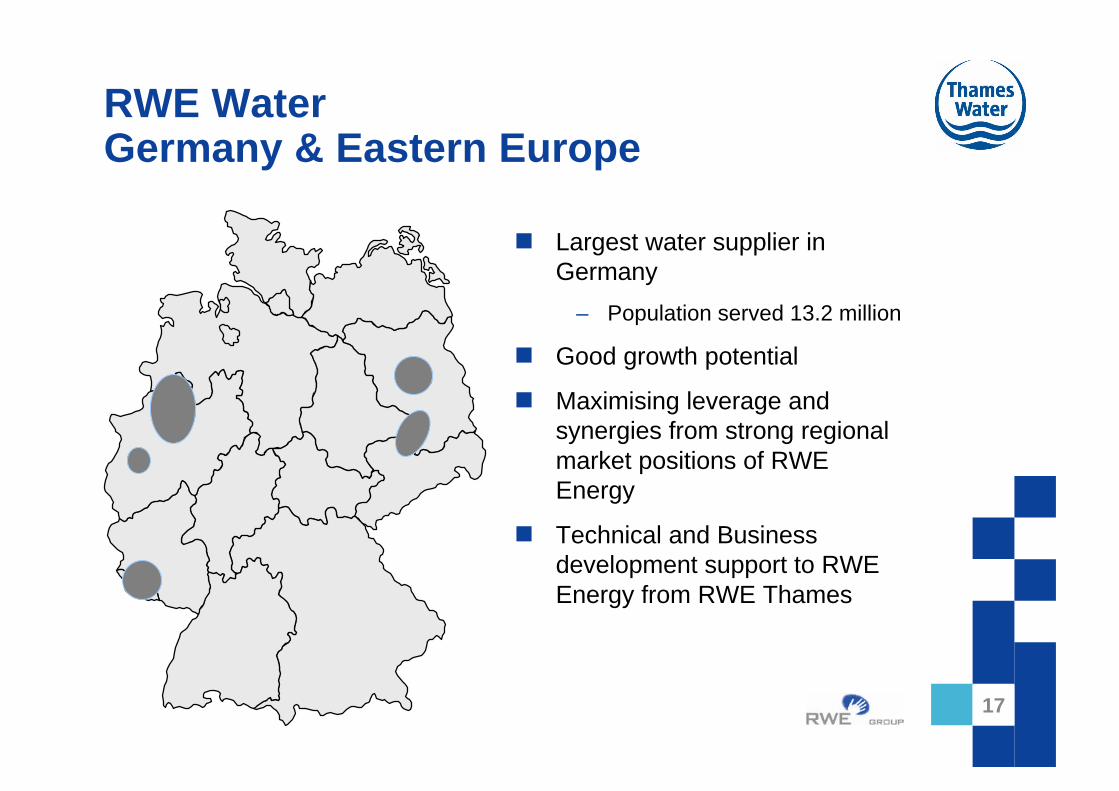

RWE WaterGermany & Eastern Europe

n Largest water supplier in Germany

– Population served 13.2 million

n Good growth potential

n Maximising leverage and synergies from strong regional market positions of RWE Energy

n Technical and Business development support to RWE Energy from RWE Thames

17

18

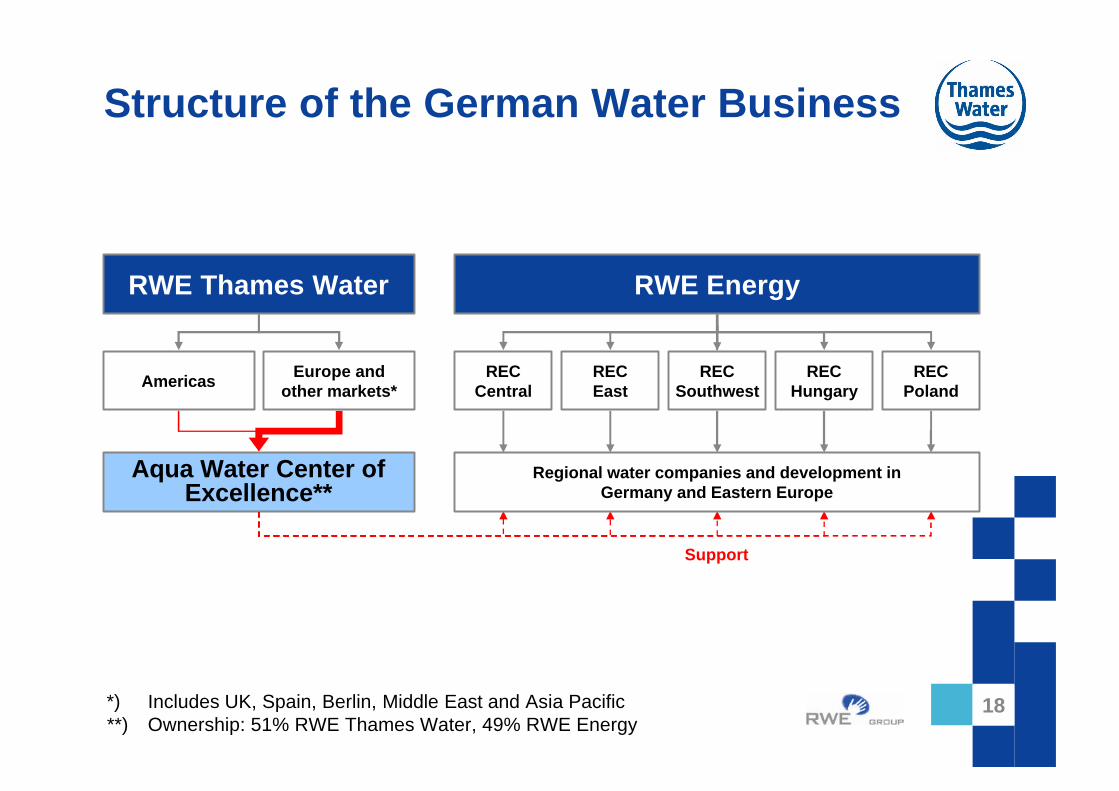

Structure of the German Water Business

*) Includes UK, Spain, Berlin, Middle East and Asia Pacific**) Ownership: 51% RWE Thames Water, 49% RWE Energy

RECCentral

RECEast

RECSouthwest

RECHungary

RECPoland

RWW enviaMaqua

SüwagWater

Budapest Water

DabrowaGornicza

RWE Energy

Americas Europe and other markets*

RWE Thames Water

Aqua Water Center of Excellence**

Support

Regional water companies and development inGermany and Eastern Europe

18

United Kingdom

20

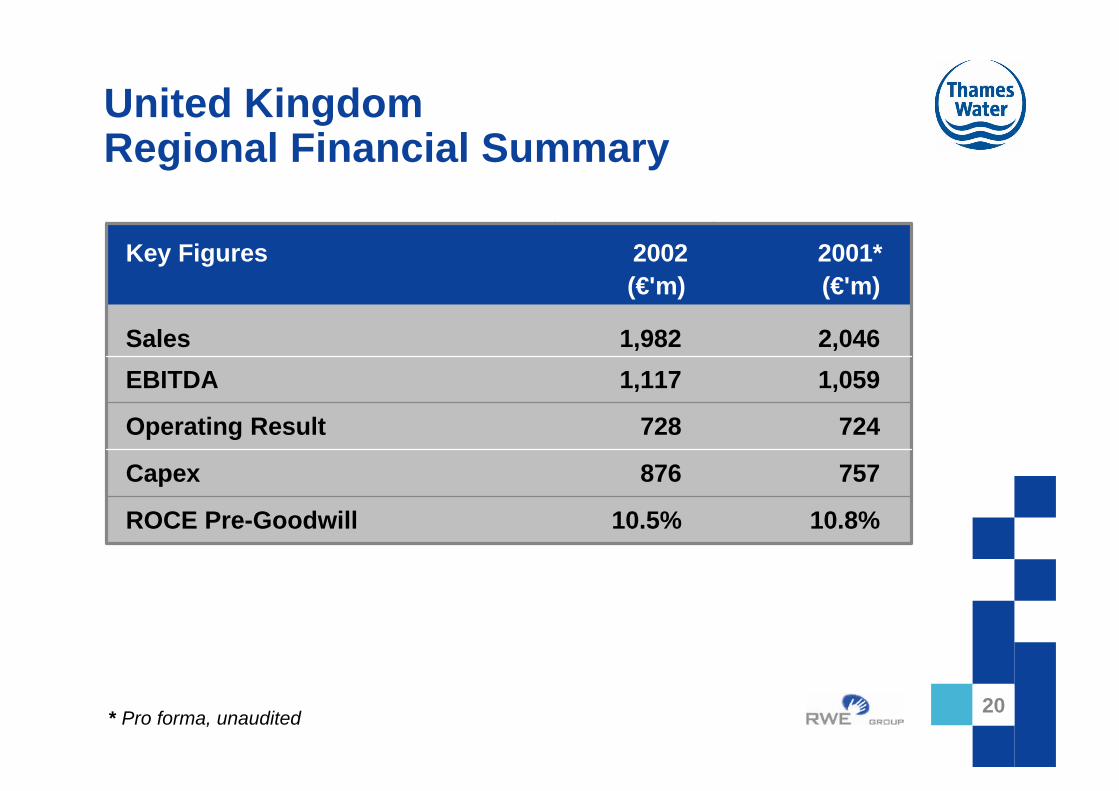

United KingdomRegional Financial Summary

* Pro forma, unaudited20

Key Figures 2002 2001*(€'m) (€'m)

Sales 1,982 2,046

EBITDA 1,117 1,059

Operating Result 728 724

Capex 876 757

ROCE Pre-Goodwill 10.5% 10.8%

21

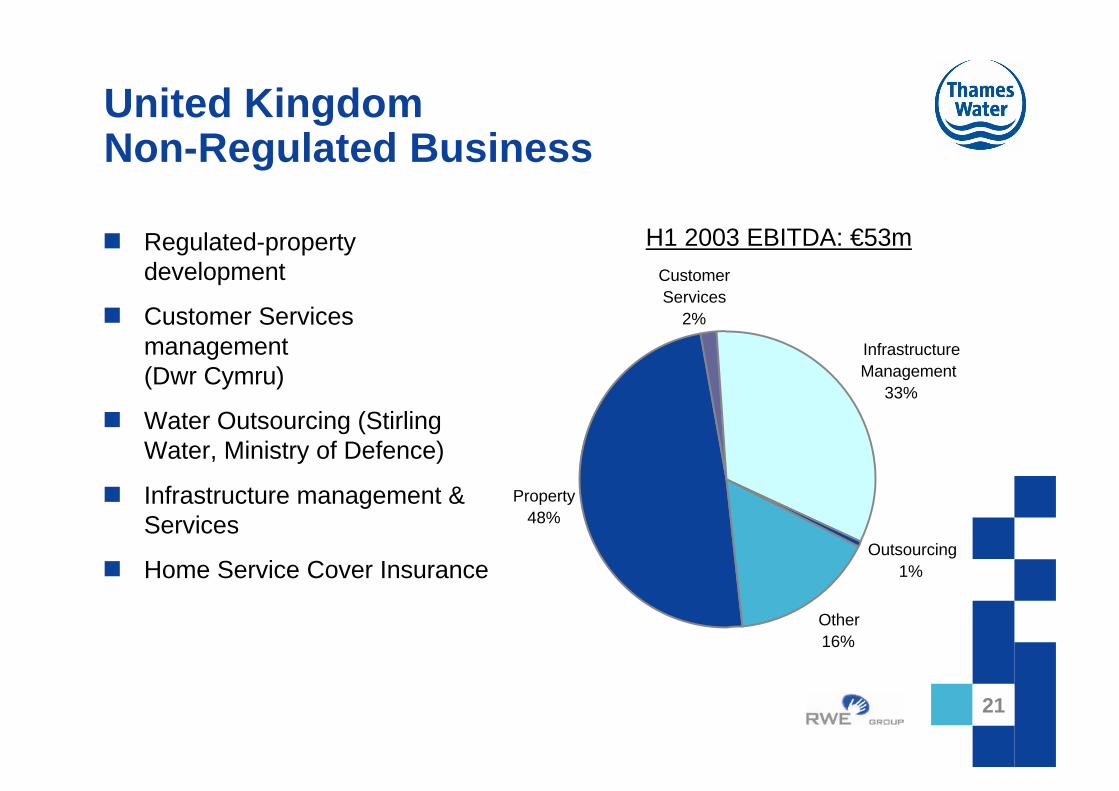

United KingdomNon-Regulated Business

H1 2003 EBITDA: €53mn Regulated-property development

n Customer Services management(Dwr Cymru)

n Water Outsourcing (Stirling Water, Ministry of Defence)

n Infrastructure management & Services

n Home Service Cover Insurance

21

CustomerServices

2%

InfrastructureManagement

33%

Outsourcing1%

Other16%

Property48%

22

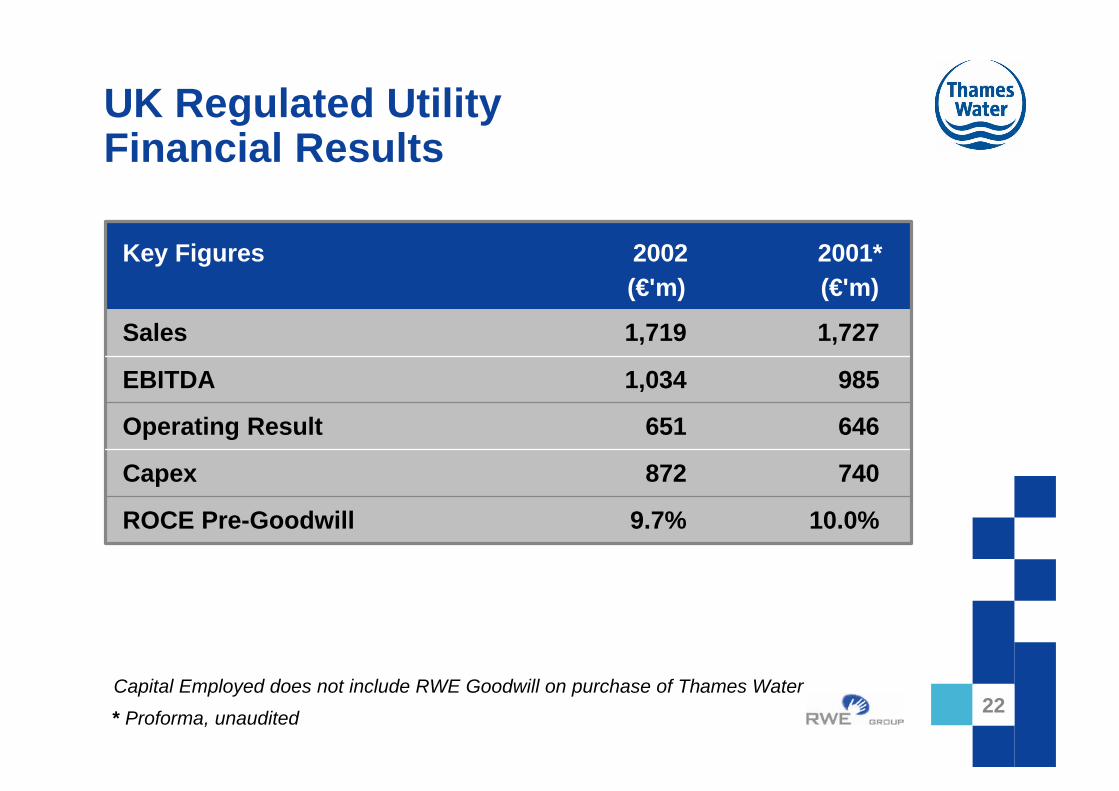

UK Regulated UtilityFinancial Results

* Proforma, unaudited

Capital Employed does not include RWE Goodwill on purchase of Thames Water22

Key Figures 2002 2001*(€'m) (€'m)

Sales 1,719 1,727

EBITDA 1,034 985

Operating Result 651 646

Capex 872 740

ROCE Pre-Goodwill 9.7% 10.0%

23

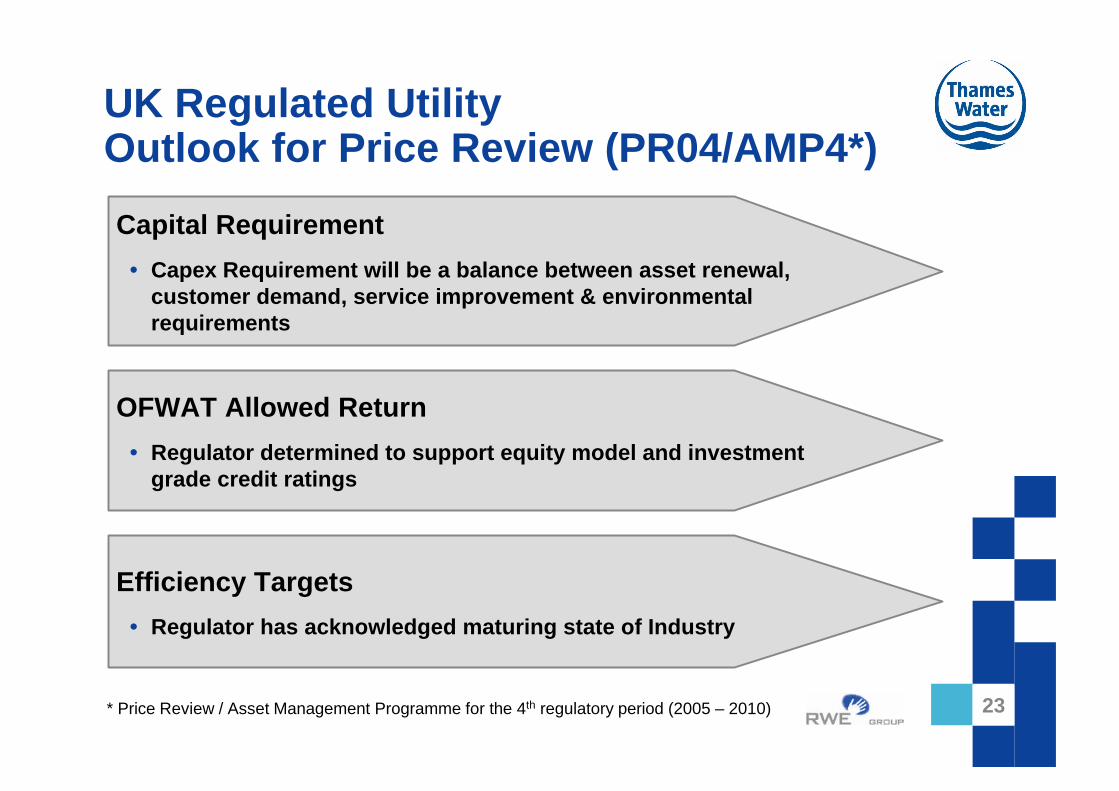

UK Regulated UtilityOutlook for Price Review (PR04/AMP4*)

* Price Review / Asset Management Programme for the 4th regulatory period (2005 – 2010)

Capital Requirement

• Capex Requirement will be a balance between asset renewal, customer demand, service improvement & environmental requirements

OFWAT Allowed Return

• Regulator determined to support equity model and investment grade credit ratings

Efficiency Targets

• Regulator has acknowledged maturing state of Industry

23

24

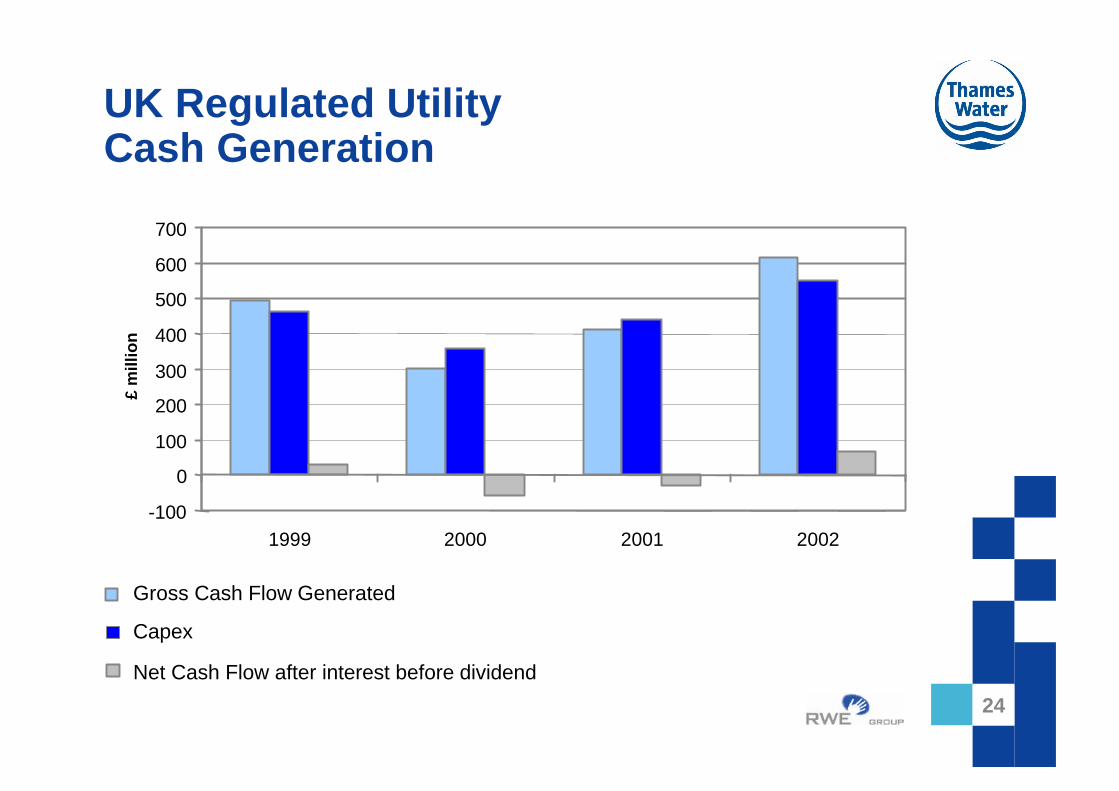

UK Regulated UtilityCash Generation

24

-100

0

100

200

300

400

500

600

700

1999 2000 2001 2002

£m

illio

n

Gross Cash Flow Generated

Capex

Net Cash Flow after interest before dividend

25

United KingdomSummary

n Largest UK Water Company

n A strong track record of regulatory out-performance and service excellence

n Well positioned for the upcoming price review (PR04)

n Water Balance (Supply-Demand) is a central issue

– OFWAT acknowledge that London is different(e.g. legacy infrastructure, geology, metropolis character, traffic)

– Investment required in London infrastructure to supply growing demand

n Further growth in the non-regulated segment through water industry outsourcing and leveraging our regulated capabilities

n Continuous efficiency improvements25

Americas

27

AmericasOverview

n Leading regulated water service provider in North America & Number two in Chile

n Managed by American Water

n ‘Regulated’ business– American Water (USA)

– E’town (USA)

– ESSEL/ESSBIO, ANSM (Chile)

– Puerto Rico

n ‘Unregulated’ business

– American Water Products & Services (USA/Canada)

Chile

USAUSA

PuertoRico

Canada

27

28

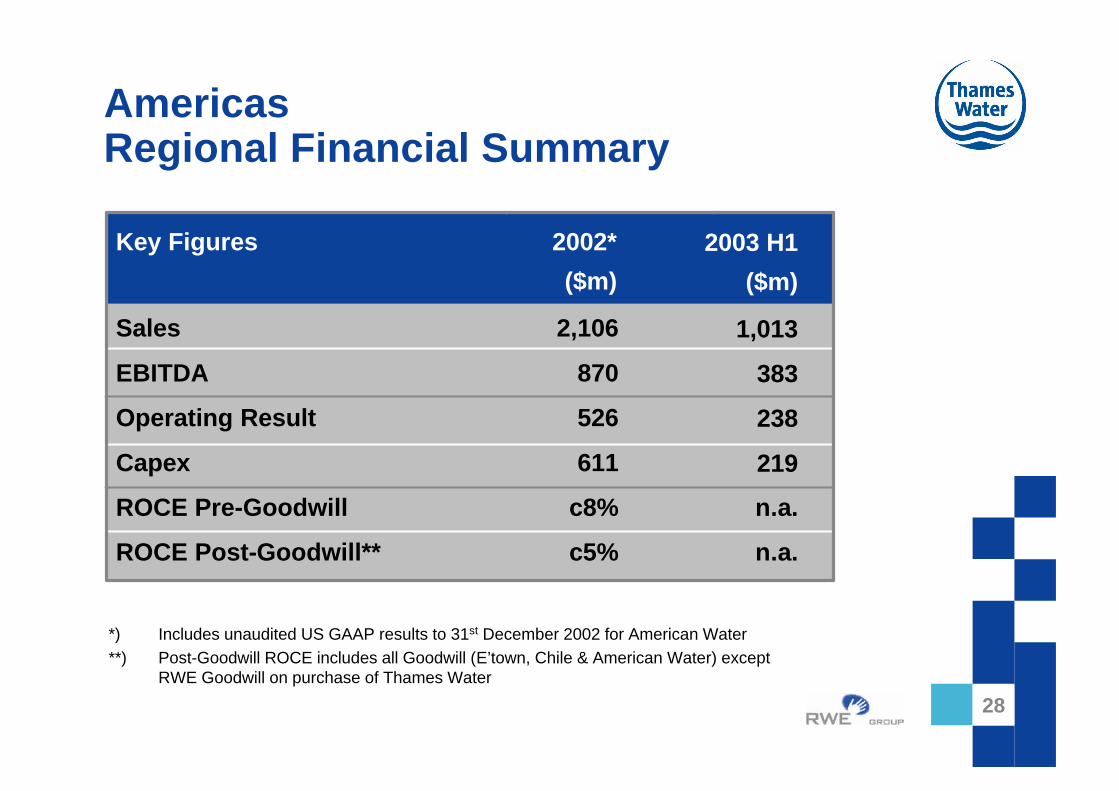

Americas Regional Financial Summary

*) Includes unaudited US GAAP results to 31st December 2002 for American Water**) Post-Goodwill ROCE includes all Goodwill (E’town, Chile & American Water) except

RWE Goodwill on purchase of Thames Water

28

Key Figures 2002*

($m)

Sales 2,106

EBITDA 870

Operating Result 526

Capex 611

ROCE Pre-Goodwill c8%

ROCE Post-Goodwill** c5%

2003 H1

($m)

1,013

383

238

219

n.a.

n.a.

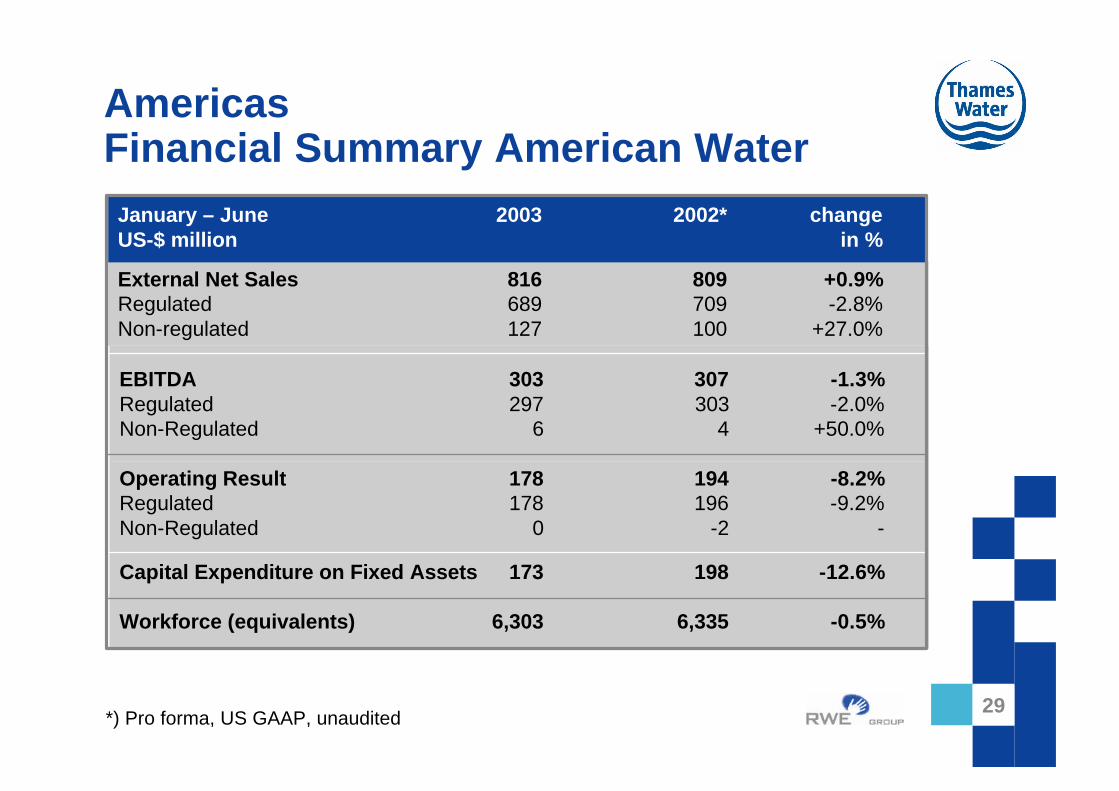

29

AmericasFinancial Summary American Water

*) Pro forma, US GAAP, unaudited

Capital Expenditure on Fixed Assets 173 198 -12.6%

External Net Sales 816 809 +0.9%Regulated 689 709 -2.8%Non-regulated 127 100 +27.0%

EBITDA 303 307 -1.3%Regulated 297 303 -2.0%Non-Regulated 6 4 +50.0%

January – June 2003 2002* change US-$ million in %

Operating Result 178 194 -8.2%Regulated 178 196 -9.2%Non-Regulated 0 -2 -

Workforce (equivalents) 6,303 6,335 -0.5%

29

30

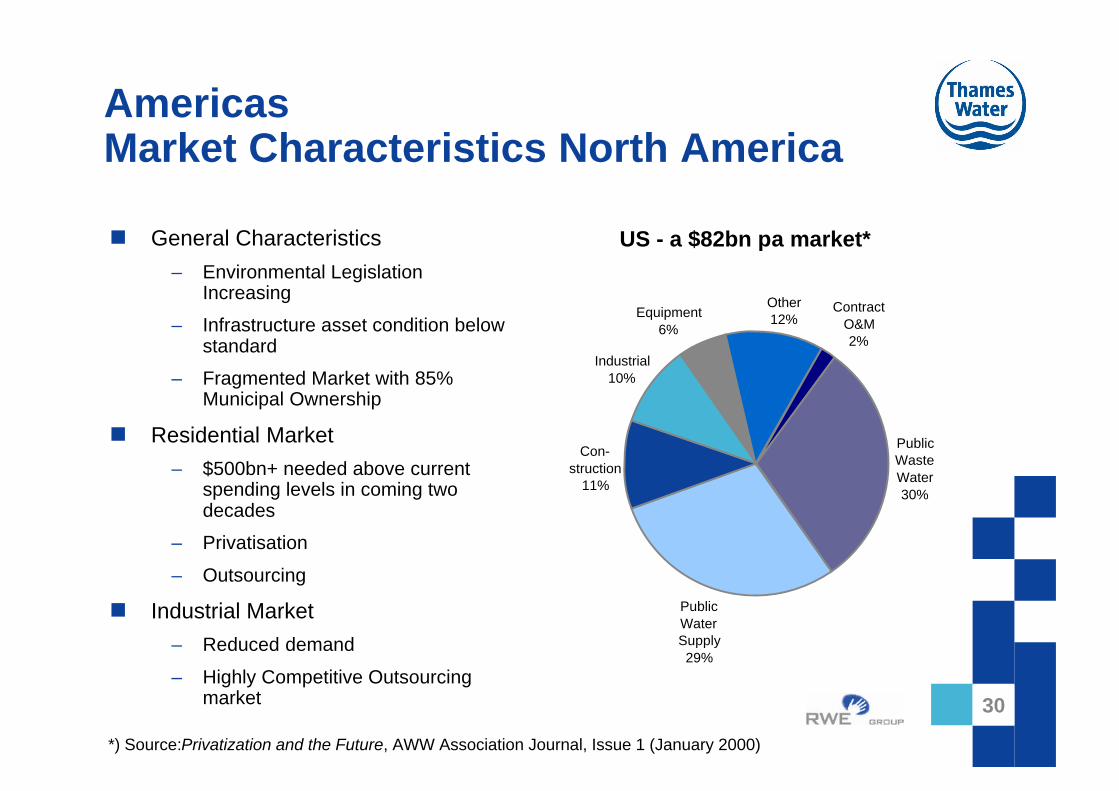

AmericasMarket Characteristics North America

n General Characteristics– Environmental Legislation

Increasing

– Infrastructure asset condition below standard

– Fragmented Market with 85% Municipal Ownership

n Residential Market– $500bn+ needed above current

spending levels in coming two decades

– Privatisation

– Outsourcing

n Industrial Market– Reduced demand

– Highly Competitive Outsourcing market

*) Source:Privatization and the Future, AWW Association Journal, Issue 1 (January 2000)

30

US - a $82bn pa market*

ContractO&M2%

Public WasteWater30%

Public WaterSupply29%

Industrial10%

Equipment6%

Other12%

Con-struction

11%

31

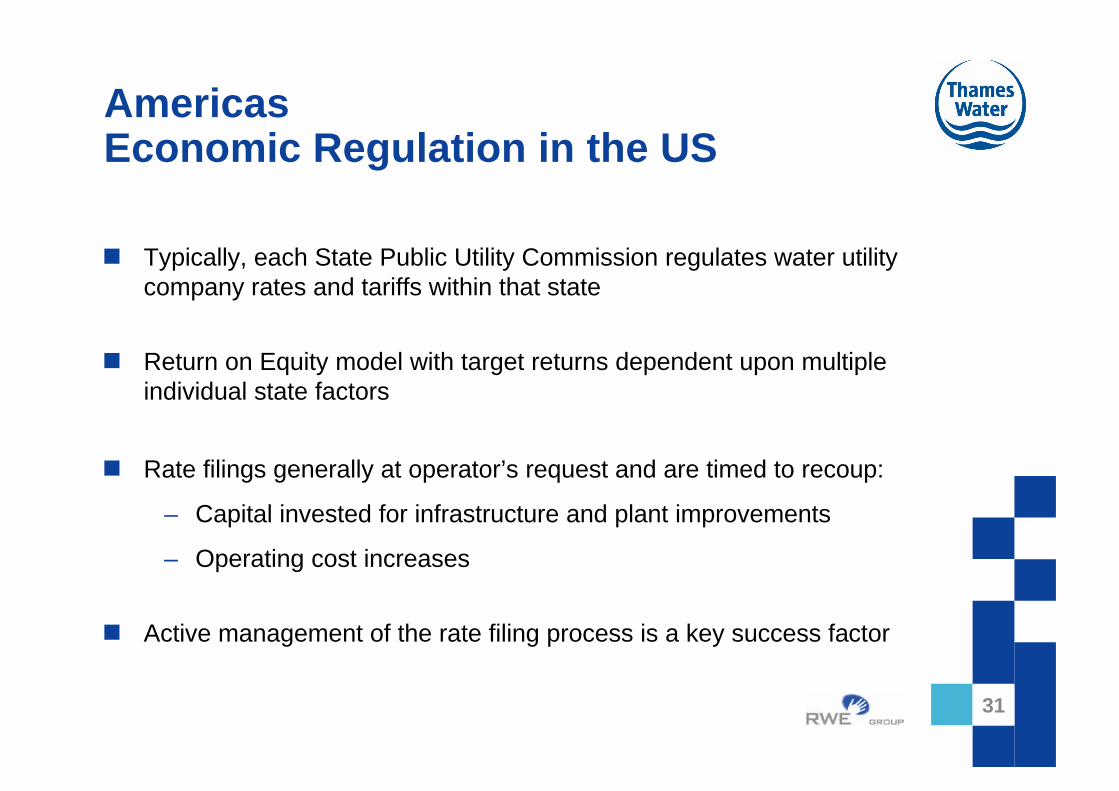

AmericasEconomic Regulation in the US

n Typically, each State Public Utility Commission regulates water utility company rates and tariffs within that state

n Return on Equity model with target returns dependent upon multiple individual state factors

n Rate filings generally at operator’s request and are timed to recoup:

– Capital invested for infrastructure and plant improvements

– Operating cost increases

n Active management of the rate filing process is a key success factor

31

32

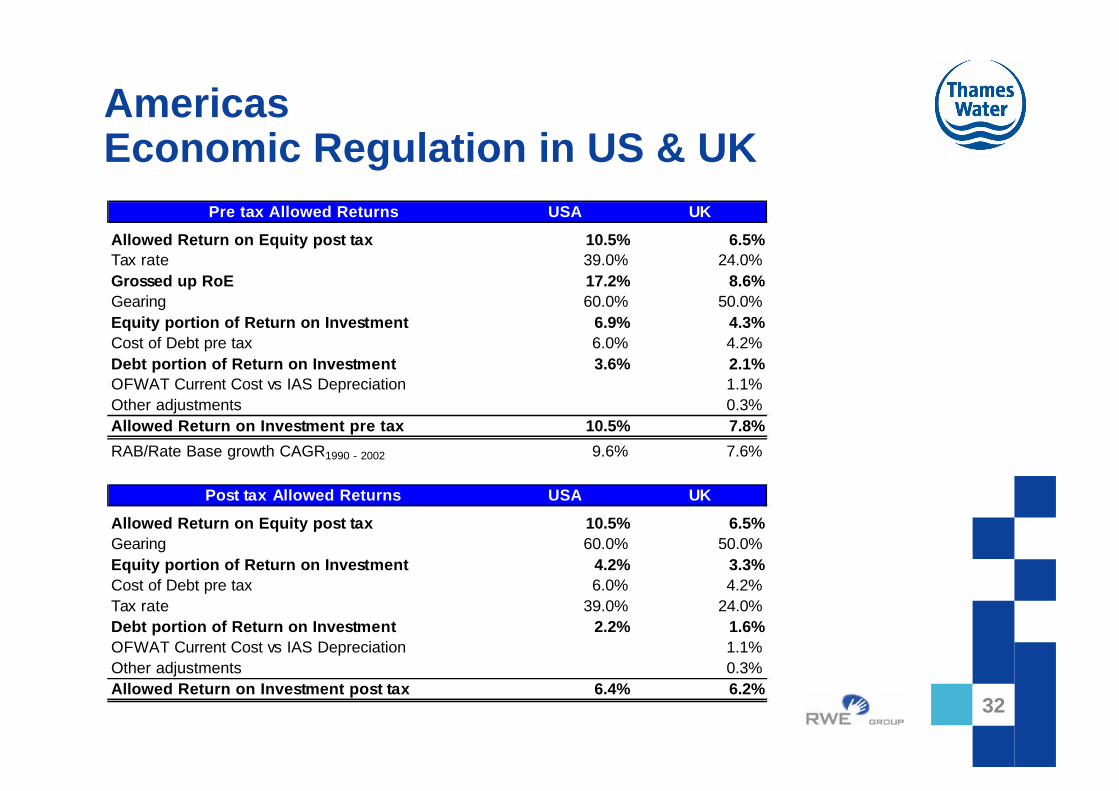

AmericasEconomic Regulation in US & UK

Pre tax Allowed Returns USA UK

Allowed Return on Equity post tax 10.5% 6.5%Tax rate 39.0% 24.0%Grossed up RoE 17.2% 8.6%Gearing 60.0% 50.0%Equity portion of Return on Investment 6.9% 4.3%Cost of Debt pre tax 6.0% 4.2%Debt portion of Return on Investment 3.6% 2.1%OFWAT Current Cost vs IAS Depreciation 1.1%Other adjustments 0.3%Allowed Return on Investment pre tax 10.5% 7.8%

RAB/Rate Base growth CAGR1990 - 2002 9.6% 7.6%

Post tax Allowed Returns USA UK

Allowed Return on Equity post tax 10.5% 6.5%Gearing 60.0% 50.0%Equity portion of Return on Investment 4.2% 3.3%Cost of Debt pre tax 6.0% 4.2%Tax rate 39.0% 24.0%Debt portion of Return on Investment 2.2% 1.6%OFWAT Current Cost vs IAS Depreciation 1.1%Other adjustments 0.3%Allowed Return on Investment post tax 6.4% 6.2%

32

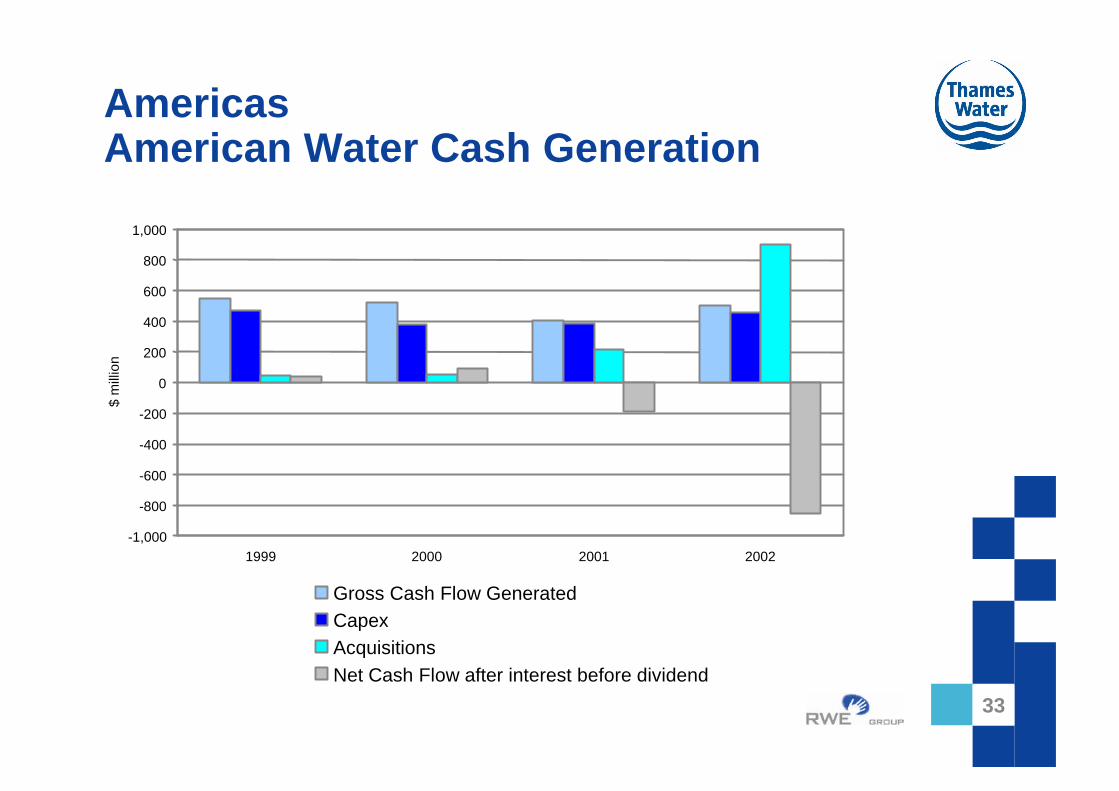

33

AmericasAmerican Water Cash Generation

33

-1,000

-800

-600

-400

-200

0

200

400

600

800

1,000

1999 2000 2001 2002

$ m

illio

n

Gross Cash Flow GeneratedCapexAcquisitionsNet Cash Flow after interest before dividend

34

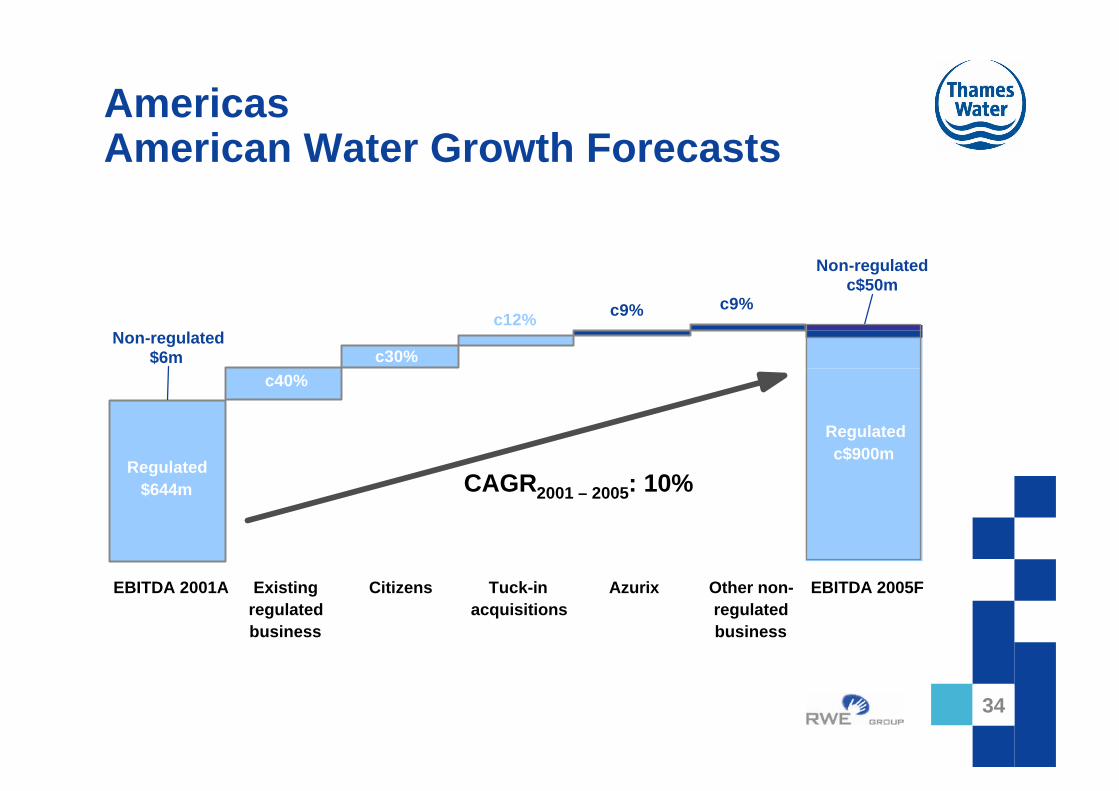

AmericasAmerican Water Growth Forecasts

EBITDA 2001A Existingregulatedbusiness

Citizens Tuck-inacquisitions

Azurix Other non-regulatedbusiness

EBITDA 2005F

c40%c30%

c12% c9% c9%

Non-regulated$6m

Non-regulatedc$50m

Regulated c$900m

CAGR2001 – 2005: 10%Regulated

$644m

34

35

AmericasSummary

n 10% EBITDA growth remains the target for American Water

– Clearing the rate case backlog through focussed rate case programme and managing our relationships with regulators

– Further growth through small tuck-in acquisitions and through opportunities in the municipal O&M market (incl. Military bases)

– Extract value from private sector involvement in the Wastewater segment

n Adding further value through integration

– Best practice transfer and procurement initiatives

– Back-office consolidation across the region

– Value break-even target 2006

– Earnings pre-goodwill accretive in 2003

35

Future Outlook and Conclusions

37

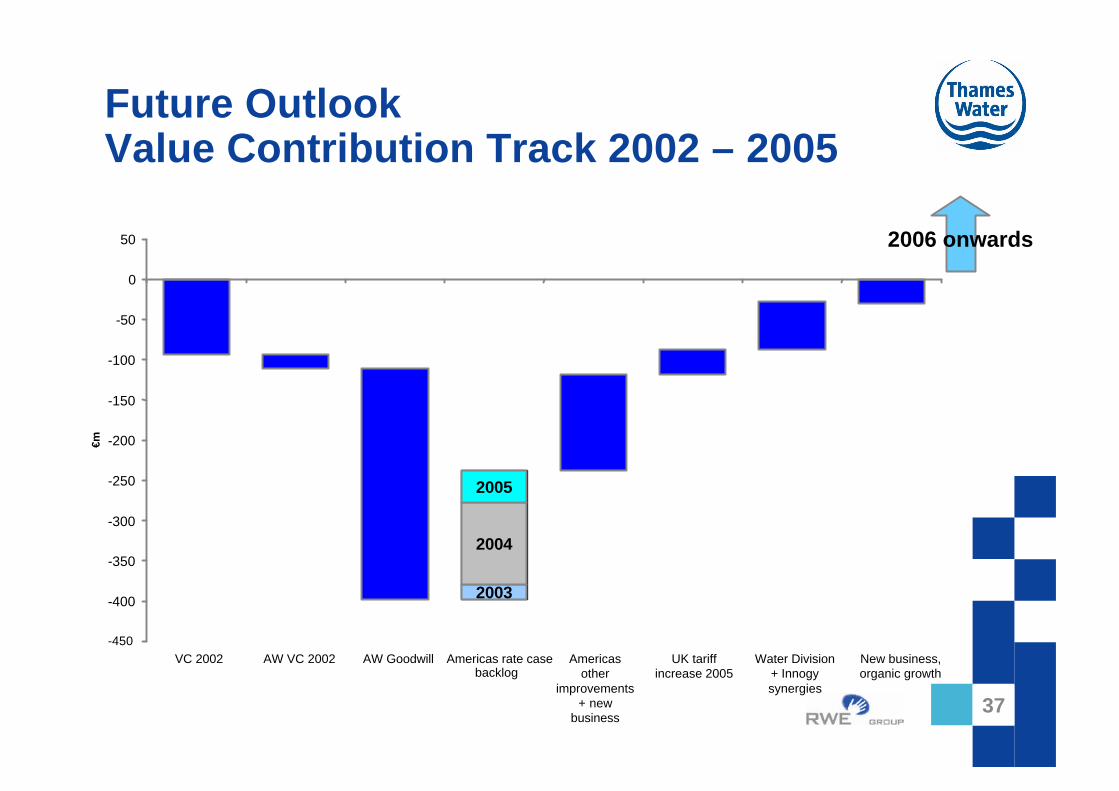

Future OutlookValue Contribution Track 2002 – 2005

2006 onwards

-450

-400

-350

-300

-250

-200

-150

-100

-50

0

50

VC 2002 AW VC 2002 AW Goodwill Americas rate casebacklog

Americas other

improvements + new

business

UK tariff increase 2005

Water Division + Innogy synergies

New business, organic growth

€m

2003

2004

2005

37

38

RWE Thames WaterConclusions

n Water Division is a key component of RWE Group

n Drivers in our core water markets remain strong

n Primary focus is on key markets: USA, UK & Germany

n US market has strong potential for organic growth

n Our core capabilities enable us to extract value from the regulatory framework

n Regulated water provides stable, predictable earnings and steady growth and contributes to the strong, stable RWE credit rating

38

![Thames Region Land Drainage - gov.uk · Thames Water Authority LAND DRAINAGE BYELAWS 1981 [as amended by the Thames Region FLOOD DEFENCE BYELAWS 1991] The Thames Water Authority,](https://img.pdfslide.us/doc/110x75/5ead899913c7690cc165ecc9/thames-region-land-drainage-govuk-thames-water-authority-land-drainage-byelaws.jpg)