Embed Size (px)

Citation preview

Russian energy policyin a broader context

Vladimir MilovPresident, Institute of Energy Policyhttp://www.energypolicy.ru

New York City, March 15, 2006

Popular mythology on the Russian energy policies and politics

• ‘President Putin is restoring justice by re-nationalizing the assets ‘stolen’ by oligarchs in the 1990s’

• ‘Re-nationalization of the Russian oil & gas industries benefits the public interests’

• ‘Russia may be able to build a successful economic policy through financing social programs and industrial development from oil & gas export revenues’

• ‘Russia will be able to establish competitive ‘national champions’ in energy to develop new ambitious projects and establish global leadership in energy’

None of these assertions are actually true

...in reality, however...

• Old oligarchs are simply replaced with new ones

• The state does not formally become the owner of oil & gas assets that are taken away from private owners

• National oil & gas companies pay far less taxes to the state than the old oligarchs did and do

• National oil & gas companies are so inefficient and corrupt that they are not capable of developing new ambitious projects

• ‘Petro-state’ concept simply does not work because there are not enough resources to implement it

The authorities clearly become obsessed with the ‘energy factor’ as the dominant component of the domestic and foreign policy

President Putin:

‘Today, energy serves as the key driving factor of the global economic progress. [???] Current and future condition of Russia depends on the place that we occupy in the global energy context. Such an ambitious task [as achieving global energy leadership] will act as a serious catalyst for modernization and qualitative breakthrough of the whole Russian economy’ (December 25, 2005)

Top Putin’s ideological aide Surkov:

‘Let’s just take what we are already capable of doing, and just do it better. I think that the concept of Russia as energy superpower fits such an approach just fine. If you have strong legs, better do the long-jumping, but not play chess’ (February 7, 2006)

But are there enough resources for a ‘superpower’?

Petro-state: too much population and too heavy domestic energy consumption to implement this concept

1162

2993

3319

3638

3744

4414

6319

6419

6686

7396

9746

10654

11100

12772

13399

19838

26774

29986

38590

0 20000 40000

Nigeria

Angola

Indonesia

Iraq

Ecuador

Azerbaijan

Venezuela

Algeria

Kazakhstan

Iran

Russia

Malaysia

Libya

Oman

Saudi Arabia

Kuwait

Qatar

UAE

Norway

0,2

0,9

1,0

1,0

1,4

1,7

1,9

2,7

3,0

3,9

4,0

4,9

10,8

16,5

17,4

44,5

45,7

45,8

59,2

0 20 40 60

Indonesia

Nigeria

Ecuador

Azerbaijan

Malaysia

Iraq

Iran

Kazakhstan

Russia

Angola

Algeria

Venezuela

Libya

Saudi Arabia

Oman

Kuwait

UAE

Norway

Qatar

Hydrocarbon exports per capita in various petro-states, 2003 (tons per capita, including oil, gas & petroleum products)

GDP per capita in various petro-states, 2004 (in 2004 USD by purchase power parity)

Source: The World Bank, IMF, IEA, CIA

However, the negative effects of petro-dollar pressure are already becoming visible...

• Softening budget policy: the non-interest expenses of the federal budget grew from 12.3% of GDP in 2004 to 16.7% of GDP in 2006

• Government’s financial plan for 2006-2008 is based on Urals price USD 51/bbl in 2006, USD 46/bbl in 2007-2008

• Yegor Gaidar: severe budget problems may occur if Urals price falls below USD 25/bbl

• Pension Fund deficits will rise to above USD 20bn from 2010

• Economic reforms are abandoned and replaced with ‘national projects’ (simply a budget spending related activities)

• RTSI grew by 2.4 times from May 2005 to March 2006

• Land prices in Moscow region jumped up 8-10 times in 2001-2006

• Apartment prices in Moscow jumped up 4-5 times in 2001-2006

Can Putin’s policy in the energy sector succeed?

2005: unsuccessful year for theRussian oil & gas sector

6,1

7,7

9

11

8,9

2,42,4

4,2

1,81,1

-1,1 -0,5

-2

0

2

4

6

8

10

12

2000 2001 2002 2003 2004 2005

OilGas

Source: Institute of Energy Policy

Annual growth rates in oil & gas production in Russia in 2000-2005, %

A few notes on oligarchs and their role...

300

400

500

600

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

crud

e oi

l out

put i

n R

ussi

a, m

mtp

a

Beginning of restructuring and privatization

Beginning of active growth phase after 1998 price crisis

'Small economic miracle' - unexpected production growth led by private oil comapnies

Beginning of interventionist state policies - growth slowdown

Companies' consolidation, beginning of transnationalisation

1987 peak

Dramatic downfall of the centralized Soviet oil industry

Source: BP

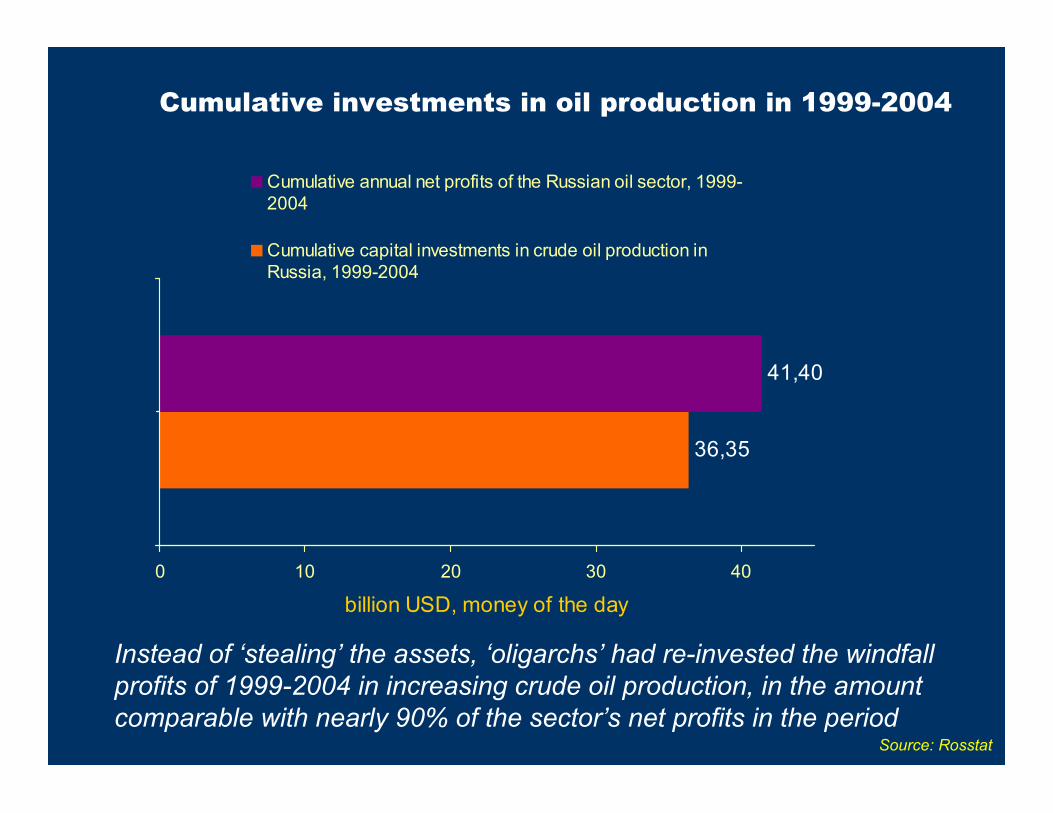

Cumulative investments in oil production in 1999-2004

36,35

41,40

0 10 20 30 40

billion USD, money of the day

Cumulative annual net profits of the Russian oil sector, 1999-2004

Cumulative capital investments in crude oil production inRussia, 1999-2004

Source: Rosstat

Instead of ‘stealing’ the assets, ‘oligarchs’ had re-invested the windfall profits of 1999-2004 in increasing crude oil production, in the amount comparable with nearly 90% of the sector’s net profits in the period

Privatized Russian oil sector had contributed most to the success of the Russian oil industry 2001-2004

Source: Oil & Capital

125

11

0

50

100

150

Annual surplus in oil production, 2004 as compared to 2000 (mtoe/year)

Private companies(Lukoil, Yukos,Surgutneftegaz, TNK-BP, Sibneft, Slavneft)State companies(Rosneft, Tatneft,Bashneft, Gazprom)

2004-2006: private sector not affected by state’s actions still doing much better

Average daily crude oil output by companies, 2004 – January 2006

Source: Oil & Capital

80%

90%

100%

110%

120%

Jan-04 May-04 Sep-04 Jan-05 May-05 Sep-05 Jan-06

% o

f the

Jan

uary

200

4 le

vel

Private-owned companies (Lukoil, Surgutneftegaz, TNK-BP, Slavneft)

Sibneft

Yukos + Yuganskneftegaz

State companies (Rosneft without YNG, Tatneft, Bashneft, Gazprom)

There was an alternative to Putin’s re-nationalization: trans-nationalization through mergers and acquisitions with IOCs, leading to de-politicized, internationally integrated and competitive oil sector in Russia

• Privatization of the 1990s was not fair

• But, it had created a well-established, internationally competitive oil sector in Russia

• Influence of oligarchs on the state’s policy was a strong negative factor

• But, privatized Russian oil sector was undergoing the process of M&As and internationalisation of oil companies (TNK-BP, YukosSibneft-ExxonMobil)

Source: Oil & Capital

Russian average daily crude output:can we reach 10.5-11 mbd?

7,5

8

8,5

9

9,5

Dec

embe

r 200

2

Febr

uary

200

3

April

200

3

June

200

3

Augu

st 2

003

Oct

ober

200

3

Dec

embe

r 200

3

Febr

uary

200

4

April

200

4

June

200

4

Augu

st 2

004

Oct

ober

200

4

Dec

embe

r 200

4

Febr

uary

200

5

April

200

5

June

200

5

Augu

st 2

005

Oct

ober

200

5

Dec

embe

r 200

5Aver

age

daily

pro

duct

ion

of o

il in

Rus

sia

milli

on b

arre

ls p

er d

ay

‘Great leap forward’ of the private Russian oil sector

Stagnation in average daily production caused by increased

administrative pressure on the sector But...

Some believed the growth had resumed...

Why sustainable growth of crude oil production was interrupted?

• Hostile ownership changes

• Increase of oil export taxes in 2004

• Ban over private oil pipeline Western Siberia-Murmansk and remaining oil export pipeline bottleneck

• Speculation on ‘barbaric production practices’

• The Yukos case

Current developments:towards state-dominated oil sector?

State-dominated companies

12%

Priv ate companies

88%

The structure of Russian crude production

2003 End of 2005

Who’s next – Slavneft? Tomskneft? Samaranegtegaz? Surgutneftegaz? If that scenario proceeds, the share of private oil companies in Russian crude production will be limited to less than 35%

Source: Institute of Energy Policy

State-dominated companies

35%

SurgutNG14%

Priv ate companies

51%

End of 2006 ?

State-dominated companies

67%

Priv ate companies

33%

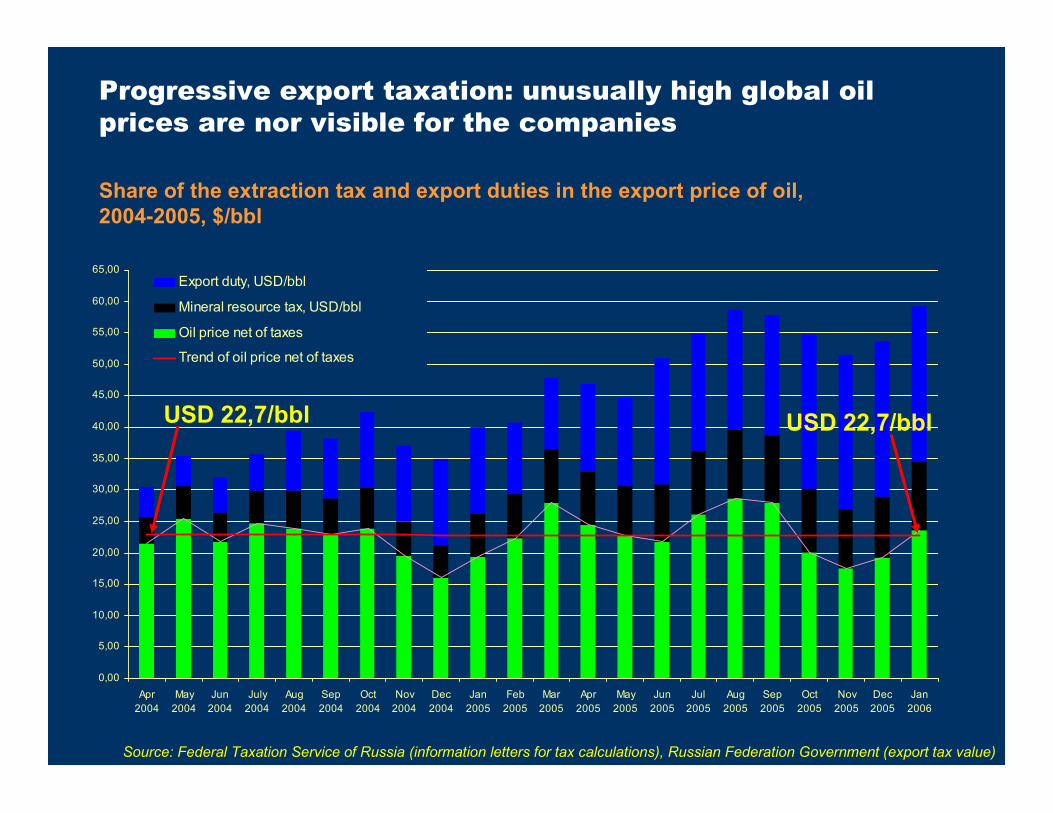

Source: Federal Taxation Service of Russia (information letters for tax calculations), Russian Federation Government (export tax value)

Progressive export taxation: unusually high global oil prices are nor visible for the companies

Share of the extraction tax and export duties in the export price of oil, 2004-2005, $/bbl

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

50,00

55,00

60,00

65,00

Apr2004

May2004

Jun2004

July2004

Aug2004

Sep2004

Oct2004

Nov2004

Dec2004

Jan2005

Feb2005

Mar2005

Apr2005

May2005

Jun2005

Jul2005

Aug2005

Sep2005

Oct2005

Nov2005

Dec2005

Jan2006

Export duty, USD/bbl

Mineral resource tax, USD/bbl

Oil price net of taxes

Trend of oil price net of taxes

USD 22,7/bbl USD 22,7/bbl

Russian oil pipeline infrastructure: the bottleneck continues to exist

Structure of 2004 Russian oil exports(including transit), mtoe

The Baltic:shallow waters,icing, Danish straits’marine trafficlimitations

Druzhba:a limited continentalmarket withunfavorable pricingenvironment

The Black Sea:Bosphorustraffic limitations

Other directionsare simplyunderdeveloped

Source: Institute of Energy Policy

East Siberian pipeline:too expensive to help Western Siberian exports

Source: Institute of Energy Policy estimate

15,7

20,1

20,8

86,3

94,3

99,0

101,2

0 20 40 60 80 100

West Siberia-western border

West Siberia-Novorossijsk

West Siberia-Primorsk

Taischet-Perevoznaya

Surgut-Omsk-Taischet-Perevoznaya

Surgut-Alexandrovskaya-Taischet-Perevoznaya

Surgut-Yurgamysh-Omsk-Taischet-Perevoznaya

USD/ton

The pipeline is too expensive to help more Western Siberian exports, whereas there’s

clearly not enough oil in Eastern Siberia to fill it

Oil production decline by Yukos subsidiaries in 2004-2005

Source: Oil & Capital

The Yukos factor made it’s obvious contribution to slowdown in production growth: minus 11 mmt in 2005.

If that did not happen, Russian oil production growth could have reached 4.8% in 2005 instead of just 2.4%

-24,70% -25,20%

-36,00%-37,10%

-40,00%

-35,00%

-30,00%

-25,00%

-20,00%

-15,00%

-10,00%

-5,00%

0,00%

Decline in % to August 2004

Decline in % toFebruary 2004

SamaraNefteGazTomskNeft

Average daily production decline in January 2006...

Gazprom: production decline on matured gas fields appears to be RATHER SHARP

545,6523

505477

460,7441,5

427,8

7

37 6488

100

8,115,5 15,6 15

4,5

1999 2000 2001 2002 2003 2004 2005*

Northgaz (taken over in 2005)

Purgaz (taken over in 2002)

Zapolyarnoye gas field

Gazprom production net of Zapolyarnoye and Purgaz

Source: Institute of Energy Policy; * - preliminary

Matured fields: over 20% decline in 6 years!

Gas production on Gazprom’s mature gas fields would continue to rapidly decline

2004 2010 2015 2020

bcm

pa

OtherOrenburgAstrakhanUrengoy (achimov)Yeti-PurovskoyeSouth RusskoyeVyngayakhinskoyePestsovoyeYubilyeynoeWest TarkosalinskoyeKomsomolskoyeZapolyarnoyeMedvezheAneryakhinskoyeKharvutinskoyeYamburgYen-YakhinskoyeUrengoy

Source: Jonathan Stern, Oxford Institute for Energy Studies, ‘The future of Russian gas and Gazprom’, 2005

Urengoy and Yamburg will decline by 30% by 2010 as compared to 2004!

The same story in the gas sector: increasing state domination kills the growth in the independent gas producers’ sector

5,7

9,712

4

13

30,3

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005Source: Institute of Energy Policy

Annual growth rates in gas production by Russian independent gasproducers in 1999-2005, %

State-dominated energy monsters: dinosaurs of Soviet* and early 1990s**economic practices

* Gazprom** Rosneft

Development of new Yamal gas fields is delayed again

The story repeats itself: in 2000, Gazprom had asked for prolongation of the licenses for large Yamal fields, which, under previous license terms, should have been brought on-stream by second half of the 1990s

Even the project rationale is not yet approved by Gazprom management. It is clear that these fields will not be brought on-stream before 2011-2012

No clear on-stream introduction schedule

In 2001, on-stream introduction term was postponed from 1997 to 2007

In 2001, on-stream introduction term was postponed from 1995 to 2012

In 2001, on-stream introduction term was postponed from 1995 to 2009

Bovanenkovskoye

Kharasaveyskoye

Novoportovskoye

Rosneft: profile of the new ‘champion’

Oil production of the core Rosneft subsidiaries had been stagnating during the whole period of 2000-2005

Source: Oil & Capital

Average daily crude oil production by major Rosneft subsidiaries in 2000-2005, thousand tons per day

0,0

2,0

4,0

6,0

8,0

10,0

SakhalinmorneftegazKrasnodarneftegazStavropolneftegazPurneftegaz (right axis)

Heavy debt burden of state-linked oil & gas corporations complicates financing of new investment projects

• Gazprom’s debt after 9m 2005 – USD 26.8 bn

• Extra borrowings made to finance Sibneftacquisitions – USD 13 bn

• Financing of Yamal, Shtokman, NEP would require over USD 80 bn

• Rosneft’s debt after 9m 2005 – USD 11.4 bn

• Financing of East Siberian and Far East projects would require over USD 20 bn

State oil & gas companies are obviously not efficient as compared to private Russian and international oil & gas companies

-2,87,3

9,513,4

14,816,4

17,919,619,7

21,322,222,3

23,525,8

28,830,430,6

33

Pemex

Rosneft

Gazprom

BP

Novatek

ConocoPhillips

Shell

British Gas

PetroCanada

Lukoil

Total

ExxonMobil

Chevron Texaco

PetroChina

ENI

Statoil

Yukos (2002)

Sibneft

ROTA (return on total assets)of international oil & gas companies, 2004 (unless otherwise indicated)

Source: companies’ financial reports

State companies are ‘champions’ in hostile takeovers, not in the payment of taxes

19,223,0

50,8

68,0

53,1

83,0

51,1

93,7

74,4

112,6

0,0

20,0

40,0

60,0

80,0

100,0

2003 2004

Taxe

s pa

id to

Rus

sian

bud

get,

US

D p

er to

e(m

oney

of 2

004)

Gazprom Rosneft TNK-BP

Sibneft Lukoil

Source: companies’ IFRS financial reports

Are Russian policies in the oil & gas sector adequate to future challenges?

The strategic crossroads of the Russian oil & gas sector policy

Future of the oil & gassector depends on

greenfield development

New era requires new oil & gas sector policies

Brownfield ageis expiring

Are Russian oil & gas sector policies adequateto the new greenfield era?

Tax policy

Restoration ofstate domination

Closing doors todirect foreign

investment

• Green fields obviously require tax incentives• Particularly long-term and capital consuming projects

require restoration of adequate PSA regime

• Debt burden complicates new investment• Corruption and non-transparency increase costs and

threaten projects’ efficiency

• Russian financial system is not ready to provide long-term financing for capital consuming and risky projects as development of the new greenfield areas requires

• Russian companies do not possess the necessary technologies

Under present policies, successful development of new greenfield areas is impossible

Energy imperialism

Things important to understand about the Russian-Ukrainian gas crisis

• WHY did not Russia follow the path of compromise and the rule oflaw (arbitration), if this was just about prices?

• WHY had Russia outrageously demanded reconsideration of a 5-year ‘unchangeable’ agreement signed just a year ago and cheeredby Gazprom even in June 2005?

• WHY the most risky and inefficient option of cutting off gas supplies was chosen, which brought limited effect and put European gas consumers at risk?

• WHY did not Russia undertake measures to protect European consumers from possible transit risks (reserved relevant amounts of gas in European storage facilities etc.)?

• WEREN’T Russian officials irresponsible, ignorant, and lying?

Was the price issue important at all?

The importance of Ukrainian gas transit for Russia

Belarus

Blue Stream

Ukraine

Baltic pipeline

Belarus

Blue Stream

Ukraine

The structure of Russian gas export corridors

Today After the Baltic pipeline is fully commenced (55 bcmpa, 2012?)

We need a clear, sustainable and mutually respectfulgas transit solution with Ukraine, not muscles

Source: Gazprom

Gazprom: 2004 agreement with Ukraine‘very advantageous’

• A.Ryazanov, deputy CEO of Gazprom, June 7 2005:

‘The gas supply price to Ukraine is not high, but I think that the agreement [of August 2004] with Ukraine is very advantageous to us, since we have low transit fare’

• Original of the briefing:http://www.gazprom.ru/articles/article16998.shtml

• 15 bcm of reexport through RosUkrEnergo

• 57 bcm – Ukrainian imports

• 17 bcm of Russian gas• 8 bcm of Kazakh gas• 7 bcm of Uzbek gas• 41 bcm of Turkmenian gas

• WHY did Russia transfer to RosUkrEnergo the rights to export 15 bcm of Kazakh and Uzbek gas and the option for gas reexport?

• DOES the switch from direct 12-year contract relations between Gazprom and Naftogaz Ukrainy to operations through a non-transparent intermediary mean ‘transfer to transparent market relations’?

• WHY in Gazprombank’s IFRS report of H1 2005 RosUkrEnergo is listed among companies whose results are not consolidated because the bank ‘does not execute control or significant influence’ over them, despite 50% equity ownership in RosUkrEnergo by Gazprombank and a member of Gazprom’s executive board being a co-chair of RUE?

• WHO’S REALLY BEHIND ROSUKRENERGO?

RosUkrEnergo: is that what it is all about?

With this background, Russian official G8 energy security proposals are a bit ‘out of this world’...

• A sharp contrast between rhetoric and official Russian policies

• Who’s the first to blame for ‘energy egoism’?

• Why the issue of uneven distribution of oil & gas resources and access of the IOCs to their development is not addressed in the Russian proposals?

• Are we being set for a ‘fake summit’?

Some conclusions

• Various forms of administrative intervention policies had brought the era of growth in the Russian oil & gas sectors to an end

• Oil & gas corporations linked to the state obviously are ill-equipped to sustain further growth and development, Gazprom in particular

• Economic regime in the oil & gas sectors is simply not adapted to ‘greenfield challenge’

• The new environment in the Russian oil & gas sectors is obviously not adequate for the goals of development

• Re-nationalization of oil & gas assets does not benefit the public interests

• Russia has not enough resources to build a successful ‘petro-state’• Energy imperialism of the Russian authorities is quite a worrying trend• It looks like, in the long run, the policies of the Russian authorities

may lead to a total failure on all dimensions