Embed Size (px)

Citation preview

Russian Banking as an Active Volcano

Koen SchoorsKsenia Yudaeva

Historical problems of Russian banking sector I

• Poor institutional environment (see other chapters)– Property rights– Land rights– Information asymmetries– Court system

• Poor regulatory environment– Unclear and inconsistent rules– Enforcement of the rules relatively poor

Historical problems of Russian banking sector II

• Lack of foreign and domestic competition– Protection of market against foreigners– Dominance of a few big state-owned players– Regional fragmentation

• Very volatile economic environment– Repeated economic crises (1990-1996, 1998-1999,

2008-2009)– Repeated bank crises (1994, 1995, 1998, 2004,

2008)

How to enforce regulations?

Schoors and Claeys 2007Is the CBR willing to enforce bank supervision?

• Banks are less likely to face delicensing IF they– are in highly concentrated regional bank markets– are large (Too Big To Fail)– are money center banks (To Central To Fail)– are too many failing banks (Too Many To Fail)

•Forbearance is related to systemic stability issues– N11 (capital to household deposits) forborne since

enforcement would affect large deposit banks and trust– Regular liquidity breaches forborne in underbanked regions– Regular capital breaches forborne if banks are large– Severe liquidity breaches are forborne if there are too many

failing banks

Is the CBR able to enforce bank standards?

Bank supervision staff

• Bad institutional environment– Banks preferred speculation to lending

• Soft legal constraints, monitoring skills, information

– Lending to connected agents• Insider lending, pocket banks

– Dominance of state players with CBR backing• Bad regulatory environment

– poor capitalization (Revealed by 1998 crisis)– Waves of fraudulent bankruptcies that dent trust

Consequences of these fundamental problems I

Consequences of these fundamental problems II

• Lack of foreign and domestic competition– Private banks less efficient (Karas, Schoors, Weill,

2010)– Fragmentation of the banking market

• Very volatile economic environment– institutional instability of normal Russian banks – Massive bank failures

• Reaction 1: sophisticated discipline (Karas, Pyle, Schoors, 2010)

• Reaction 2: flight to quality, domination by public banks• Reaction 3: Stay away from banks alltogether

Alexei Karas, Koen Schoors, Laurent Weill

Main results, production approachTable 4 The inefficiency of public banks according to the production approach Panel A: Public banks defined as state-owned banks

Before generalised deposit insurance (2002) Frontier characteristics

(a) Baseline

(b) environment

(c) Equity and environment

Intercept Yes Yes Yes

Public banks -2.321 (1.37)

-2.346 (1.38)

-2.226 (1.24)

Foreign banks -2.393* (1.95)

-2.544*** (2.67)

-2.560 (1.34)

Log-likelihood -2203.909 -2192.782 -2189.672 Panel B: Public banks defined as banks that receive a high share of interest income from the government bodies Intercept Yes Yes Yes

Public banks -2.125 (0.88)

-2.357 (1.01)

-2.172 (0.84)

Foreign banks -2.370** (1.97)

-2.535*** (2.80)

-2.550 (1.54)

Log-likelihood -2205.207 -2194.002 -2190.745

Main results, production approachTable 4 The inefficiency of public banks according to the production approach Panel A: Public banks defined as state-owned banks

Before generalised deposit insurance (2002) After generalised deposit insurance (2006) Frontier characteristics

(a) Baseline

(b) environment

(c) Equity and environment

(d) Baseline

(e) environment

(f) Equity and environment

Intercept Yes Yes Yes Yes Yes Yes

Public banks -2.321 (1.37)

-2.346 (1.38)

-2.226 (1.24)

-2.915*** (4.19)

-3.527*** (4.34)

-1.924*** (4.04)

Foreign banks -2.393* (1.95)

-2.544*** (2.67)

-2.560 (1.34)

-6.325*** (3.88)

-6.594*** (4.00)

-4.788*** (3.35)

Log-likelihood -2203.909 -2192.782 -2189.672 -1278.612 -1270.417 -1200.630 Panel B: Public banks defined as banks that receive a high share of interest income from the government bodies Intercept Yes Yes Yes Yes Yes Yes

Public banks -2.125 (0.88)

-2.357 (1.01)

-2.172 (0.84)

-3.398*** (4.35)

-3.633*** (3.70)

-2.903*** (4.66)

Foreign banks -2.370** (1.97)

-2.535*** (2.80)

-2.550 (1.54)

-6.519*** (3.31)

-6.739*** (3.30)

-4.965*** (2.95)

Log-likelihood -2205.207 -2194.002 -2190.745 -1282.249 -1274.881 -1202.208

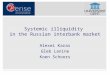

Alexei Karas, William Pyle, Koen Schoors

Sophisticated DisciplineDeposit Growth Sensitivity to Interest Rates

-5%

-2%

1%

4%

7%

10

%

13

%0%

30%

61%

-100,0%

-50,0%

0,0%

50,0%

100,0%

150,0%

200,0%

Imp

lied

de

po

sit g

row

th

Deposit rate

Capital ratio

Temporary conclusion• Until 2000 the Russian banking system does a

horrible job in financing growth (See Pyle and Spicer, 2002, Overbanked and credit-starved)

• But banking does a much better job thereafter (Berkowitz and Dejong, 2010)

• There have been considerable improvements since then– Macroeconomic stabilization in 2000– Land reform and court reforms improve property rights– Deposit insurance restores some of the trust– Improved supervision restores institutional stability– Improved enforcement of regulation

Deposit insurance and market discipline after deposit insurance

Are household deposit growth and deposit rates less sensitive to capital after deposit insurance?

FE (Z=λBtjB+μBij B) FE (Z=λBtjB+μBijB)

(5) (6) (7) (8) (13) (14) (15) (16)

-1/+1q -2/+2q -15/+13q -22/+13q -1/+1q -2/+2q -15/+13q -22/+13q

C 3.10*** 2.06*** 0.59*** 0.52*** -0.45** -0.22** -0.35*** -0.36***

(0.74) (0.27) (0.05) (0.04) (0.20) (0.09) (0.04) (0.04)

C*H -1.59* -1.02*** -0.45*** -0.44*** -1.10** -0.82** -0.58*** -1.91***

(0.84) (0.38) (0.08) (0.06) (0.54) (0.33) (0.15) (0.49)

C*I 0.38** 0.17 0.32*** 0.32*** -0.08 -0.05 -0.03 -0.02

(0.18) (0.13) (0.06) (0.06) (0.06) (0.06) (0.05) (0.05)

C*H*I -0.68*** -0.42** -0.34*** -0.32*** 0.41* 0.38** 0.29* 1.64***

(0.26) (0.18) (0.09) (0.08) (0.24) (0.18) (0.17) (0.46)

L 0.18** -0.01 0.06*** 0.05*** -0.05 -0.04 0.00 0.00

(0.08) (0.07) (0.01) (0.01) (0.04) (0.02) (0.01) (0.01)

L*H -0.11 0.03 -0.01 -0.01 0.08 0.00 -0.06* -0.18**

(0.11) (0.08) (0.02) (0.02) (0.09) (0.05) (0.03) (0.09)

L*I -0.16*** 0.01 -0.04 -0.04 0.02 0.03* 0.02 0.02*

(0.06) (0.06) (0.03) (0.03) (0.03) (0.02) (0.01) (0.01)

L*H*I 0.20** 0.00 0.04 0.03 -0.06 -0.04 -0.01 0.03

(0.08) (0.07) (0.04) (0.04) (0.08) (0.06) (0.05) (0.11)

Obs 3594 7188 46676 59097 3452 6922 44466 55449

R² 0.317 0.190 0.092 0.080 0.113 0.062 0.084 0.377

Source: alain-bertaud.com

Socialist-era impact on post-socialist city

Slvn

Pol

Ukr Bel

Hun

Cz

Slvk

Rom

Bul

Mol

Lat

Lit

Est

Geo

Arm

Kaz

Az

Uz

Rus

Taj

Kyr

1020

3040

2005

0 10 20 30 402002

Figure 1. Percentage of firms considering land title or leasing an obstacle to development

Russia’s outlier status (BEEPS)

Firms considering land title or leasing an obstacle

2002 2005 EU and FSU 21 FSU 11 EU and FSU 21 FSU 11 Size 0.009 0.003 -0.003 -0.003 [0.008] [0.013] [0.008] [0.013]

Private 0.042 0.073 -0.004 0.021 [0.014]*** [0.022]*** [0.018] [0.028]

Foreign 0.042 0.074 0.014 0.051 [0.021]** [0.036]** [0.023] [0.039]

De novo 0.019 0.042 0.024 0.043 [0.012] [0.019]** [0.012]** [0.018]**

Russia 0.137 0.110 -0.014 -0.076 [0.025]*** [0.026]*** [0.020] [0.020]***

Sector controls Yes Yes Yes Yes Institutional controls Yes Yes Yes Yes Observations 4814 2109 7696 3353 Pseudo R2 0.1150 0.1213 0.1042 0.1148 Prob > chi2 0.0000 0.0000 0.0000 0.0000

Russia’s outlier status (2)

Firms considering land title or leasing an obstacle

Collateral type and provision of external finance

Immovable assets more attractive to lenders than movable assets:

relatively greater probability (increasing in time) of recovering

value if borrower defaults

For borrowers being able to pledge land and real estate as collateral:

* Increased loan maturities

* Increased loan volumes

For lenders lending on pledge of land and real estate as collateral:

* Increased propensity to try and seize pledged assets

Ownership and use patterns in urban settlements Millions of hectares in urban settlements (7.89 total)

Government, 7.15

Physical persons, 0.55

J uridical persons, 0.17

Millions of hectares in urban settlements (7.89 total)

Agricultural, 2.03

Forests, 1.41

Developed (without industrial structures),

1.61

Developed (with industrial structures),

0.39

Roads, 0.79

Other, 1.65

Findings Pyle and Schoors, 2011

• Regional differences in industrial land owned by legal persons explain– Regional differences in bank credit

• More credit in the better regions

– Regional differences in capital investment• More capital investment in better regions

– Firm-level differences in financial constraints• firms in the good regions are less financially

constrained

BUT there were remaining weaknesses on the eve of the crisis

• Still weak institutional environment • Lack of competition and implied inefficiency

(Karas, Schoors and Weill, 2010)• Lack of trust and implied failure to attract the

deposits needed to finance lending I Implied dependence on short term

finance from interbank markets and foreign finance to finance lending (very risky)

Table 1. Some Indicators of recent developments in the Russian banking sector Data are at the start of period unless indicated otherwise 2001 2002 2003 2004 2005 2006

Number of credit organizations 2126 2003 1828 1668 1518 1409

with banking license 1311 1319 1329 1329 1299 1253

license to attract private deposits 1239 1223 1202 1190 1165 1045

license to conduct foreign currency operations 764 810 839 845 839 827

general license 244 262 293 310 311 301

license for operations with precious metals 163 171 175 181 182 184

Foreign credit organizations with banking license 130 125 126 128 131 136

fully foreign owned 22 23 27 32 33 41

50 to 100% foreign owned 11 12 10 9 9 11

Total number of branches 3793 3433 3326 3219 3238 3295

of which branches of Sberbank 1529 1233 1162 1045 1011 1009

of which branches of fully foreign owned banks 7 9 12 15 16 29

Corporate Lending/ GDP (eop) 17% 19% 22% 25% 27% 32%

Private deposits/ GDP 8% 10% 11% 12% 13% 14%

Lending/ Gross fixed capital formation (eop) 92% 105% 120% 137% 149% 177%

Inflation (eop) 18.6% 15.1% 12.0% 11.7% 10.9% 9.0%

Deposit rate (period average) 4.9% 5.0% 4.5% 3.8% 4.0% 4.1%

Lending rate (period average) 17.9% 15.7% 13.0% 11.4% 10.7% 10.5%

Crisis response on institutions• October 2008: Duma improves powers and tools of Deposit

Insurance Agency (DIA) for resolving failing banks:1. provide financial assistance to individuals/entities buying

shares of a distressed bank (DB) giving them control; to banks buying assets and liabilities of a DB to prevent its bankruptcy; to buyers of shares of a DB giving the buyer control and preventing bankruptcy; to shareholders of a DB to prevent its bankruptcy;

2. organize asset auctions of collateral offered by insolvent banks, including collateral pledged to the CBR;

3. acquire provisional administration functions based on decisions made by the CBR.

Peformance DIA in 2008

• In Q4 2008, the DIA dealt with 20 banks– Participations in 5 failing banks resolutions were

rejected as their rehabilitation was not viable– 10 failing banks received financial support and

were sold to new owners, – in 2 failing banks the DIA became the owner,– assets and liabilities of 3 failing banks were

transferred to other banks and those banks were sent into liquidation.

How the banking system was saved

• Pump money honey– Huge liquidity injections of CBR liquidity and also from

the government– Non-collateralized central bank loans– Interbank market guaranteees– Lower mandatory reserves (4 pp down)

• Capital injections– Subordinate loans from from the government

• Deposit insurance– threshoid raised to 700000 rubles

Have all needed changes been implemented?

• High cost of saving banks (4% of GDP)• Good

– Some operational restructuring, but fairly little• Bad

– Regulation and monitoring practices have not changed dramatically

– Bank market structure is still unchanged and not very competitive

– Competition is still not taking off– There is still too little consolidation and too high

fragmentation and fragility

Remaining research questions• Role of Sberbank in all this?

– Depositary of trust of the population– Recycle deposits through the interbank market to provide

liquidity– Ensure the integration of the banking market as apublic good– Bad for competition?

• The point is probably not to privatise Sberbank but rather– To further improve institutions– And stimulate competition (through foreign access)– And only if private banks get more efficient a privatisation

makes much sense.