Embed Size (px)

Citation preview

www.KlineGroup.com

© 2009 Kline & Company

September 17, 2009

A presentation at:

RUSSIA: The Jewel of the European Personal Care MarketRUSSIA: The Jewel of the European Personal Care Market

© 2009 Kline & Company 1

Russian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

About Kline

© 2009 Kline & Company 2

Russian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

About Kline

© 2009 Kline & Company 3

Global Headquarters− Little Falls, NJ

Kline Europe− Brussels, Belgium− Oxford, UK− Milan, Italy− Prague, Czech Republic

Kline Asia− Shanghai, China− Tokyo, Japan− New Delhi, India− Dubai, UAE

Kline Latin America− São Paulo, Brazil

We serve clients around the globe

About Kline

© 2009 Kline & Company

Kline has an extensive series of market research reports that cover various markets

4

About Kline

© 2009 Kline & Company 5

Indian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

Kline & Co.

© 2009 Kline & Company 6

0

50

100

150

200

250

300

2003 2004 2005 2006 2007 2008

US$

Billi

on re

tail

CAGR: 5.1%CAGR: 5.1%

The global personal care market surpassed US $280 billion at theretail level in 2008

Global Market Review

© 2009 Kline & Company 7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2004 2005 2006 2007 2008 2009-a

Cha

nge,

%

Growth has slowed considerably due to the economic crisis

Global Market Review

a- projected.

© 2009 Kline & Company 8

Emerging markets are advancing at the fastest pace

ArgentinaBrazilChinaRussia

DOUBLE-DIGIT

GROWTH

India MexicoPolandSouth Korea

MODERATE GROWTH

CanadaFranceGermanyItalyJapanSpainUnited KingdomUnited States

BELOW AVERAGE GROWTH

Global Market Review

© 2009 Kline & Company 9

Russia has been moving up the ranks

2003 Rank 2008

United States 1 United StatesJapan 2 JapanFrance 3 ChinaGermany 4 BrazilUnited Kingdom 5 FranceChina 6 GermanyItaly 7 United KingdomBrazil 8 RussiaSouth Korea 9 South KoreaRussia 10 Italy

Global Market Review

© 2009 Kline & Company 10

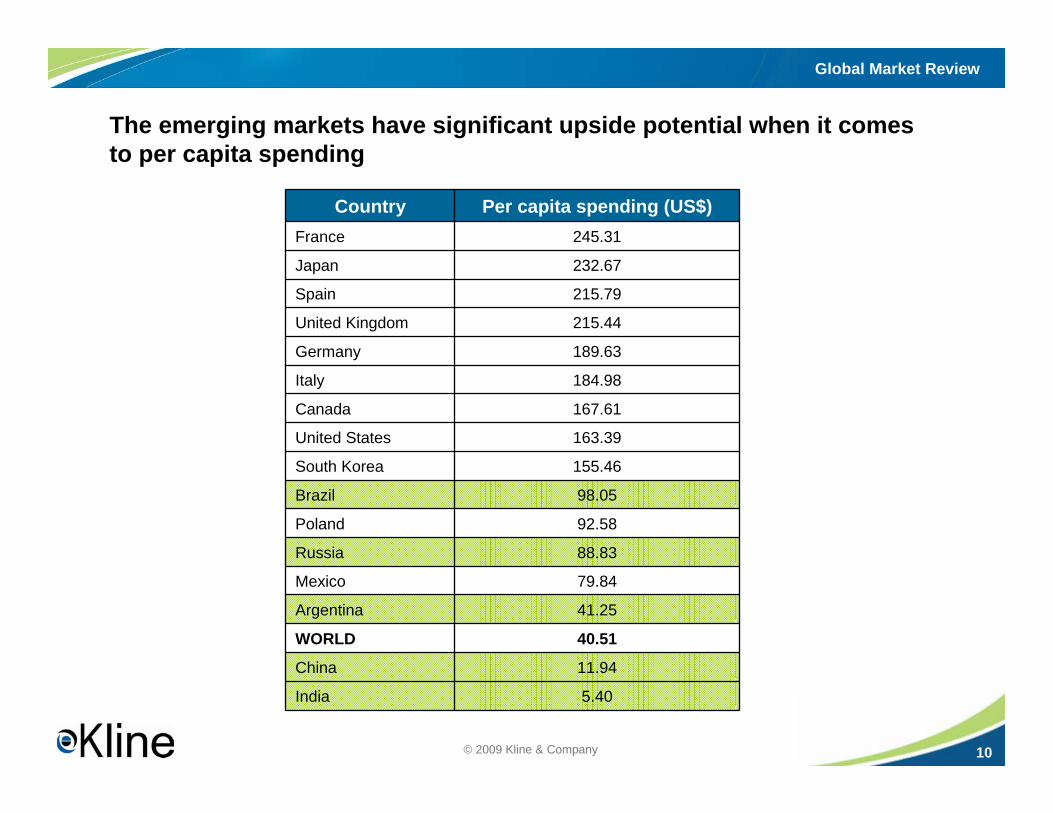

The emerging markets have significant upside potential when it comes to per capita spending

Country Per capita spending (US$)France 245.31

Japan 232.67

Spain 215.79

United Kingdom 215.44

Germany 189.63

Italy 184.98

Canada 167.61

United States 163.39

South Korea 155.46

Brazil 98.05

Poland 92.58

Russia 88.83

Mexico 79.84

Argentina 41.25

WORLD 40.51

China 11.94

India 5.40

Global Market Review

© 2009 Kline & Company 11

Russian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

Kline & Co.

© 2009 Kline & Company 12

Macroeconomic developments

High growth in GDP and real disposable income− Russian consumers are now prepared to

pay good money for good products− Rising inflation is starting to slow down

growth and resulting in price hikes

Consumers have a higher purchasing power since the majority own a house without the burden of mortgage repayments, having inherited housing from the state following the collapse of communism

The wealth of the Russian population has seen substantial growth in recent years− Salaries have increased by 15% in the

past two years and are forecast to continue double-digit growth for the next several years

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 13

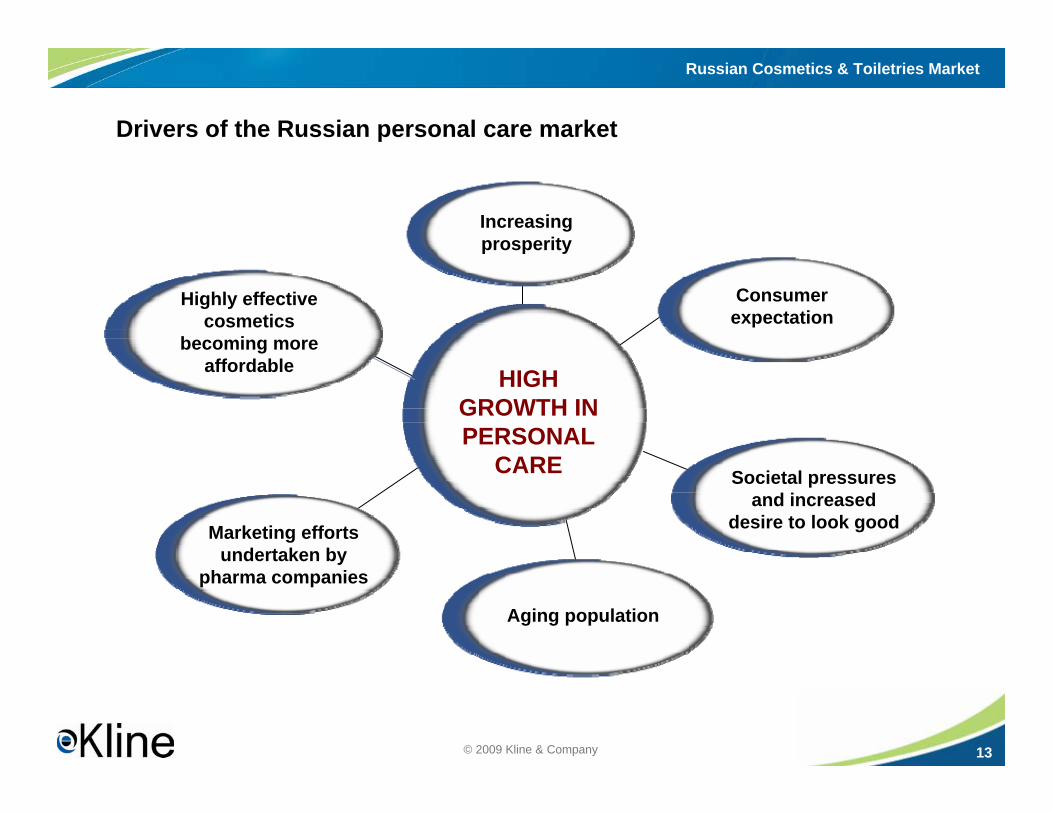

Drivers of the Russian personal care market

Increasing prosperity

Consumer expectation

Societal pressures and increased

desire to look good

Aging population

Marketing efforts undertaken by

pharma companies

Highly effective cosmetics

becoming more affordable HIGH

GROWTH IN PERSONAL

CARE

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 14

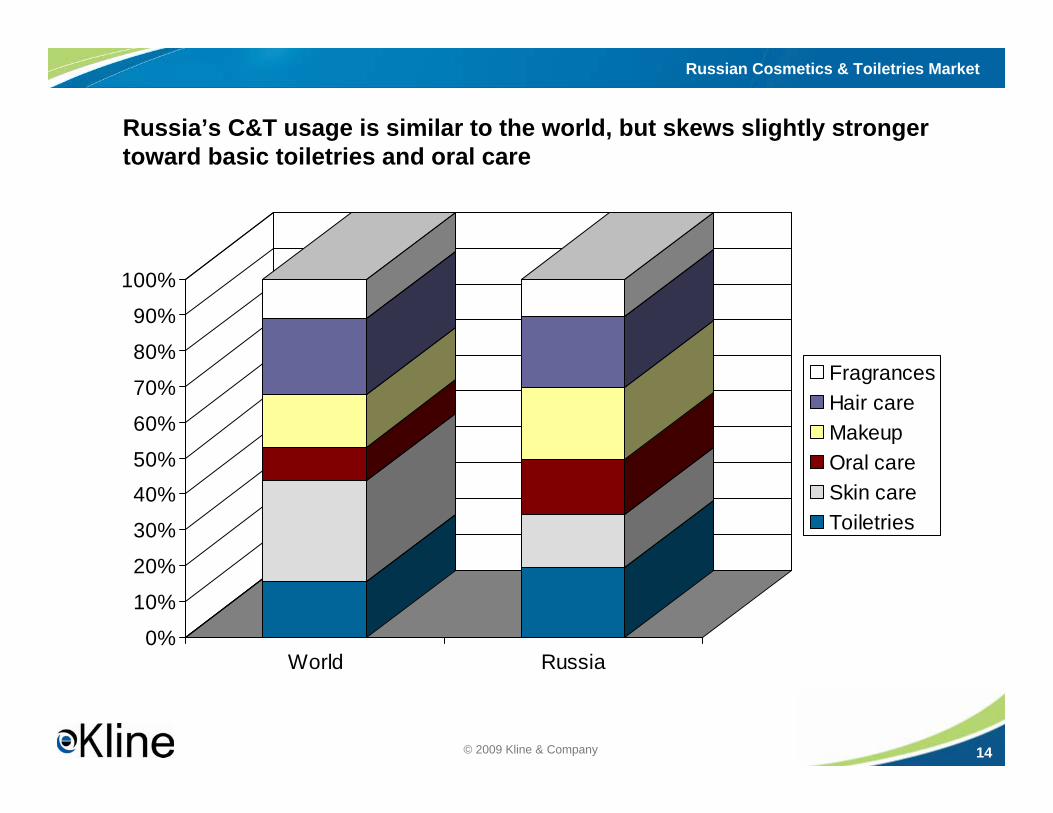

Russia’s C&T usage is similar to the world, but skews slightly strongertoward basic toiletries and oral care

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

World Russia

FragrancesHair careMakeupOral careSkin careToiletries

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 15

Russia’s unique usage patterns

Facial treatmentsWorld proportion: 19.4%Russia proportion: 8.1%

Facial treatmentsWorld proportion: 19.4%Russia proportion: 8.1%

Lipsticks and lip glossesWorld proportion: 3.8%

Russia proportion: 7.8%

Lipsticks and lip glossesWorld proportion: 3.8%

Russia proportion: 7.8%

ToothpastesWorld proportion: 5.6%

Russia proportion: 10.3%

ToothpastesWorld proportion: 5.6%

Russia proportion: 10.3%

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 16

Consumer dynamics

Consumers are becoming less price sensitive, choosing quality over price− As regional centers develop, consumers are actively

switching from low cost generic products to higher cost branded products

Consumers previously were drawn to colorful packaging but are now more interested in the ingredients and functional characteristicsConsumers consistently choose locally made skin care as they believe they are more natural and better suited to Russian skin.This belief is slowly changing. Russian consumers can be characterized into two distinct segments:− The older generation believes natural ingredients are more

healthy, is skeptical of foreign-made products containing chemicals, and does not trust advertising or salespeople

− The younger generation tends to want the advice of retail store staff, is heavily influenced by western advertising campaigns, and buys popular brands as a status symbol

There is increasing interest in health care, naturalness and newtechnologies

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2003 2004 2005 2006 2007 2008

17

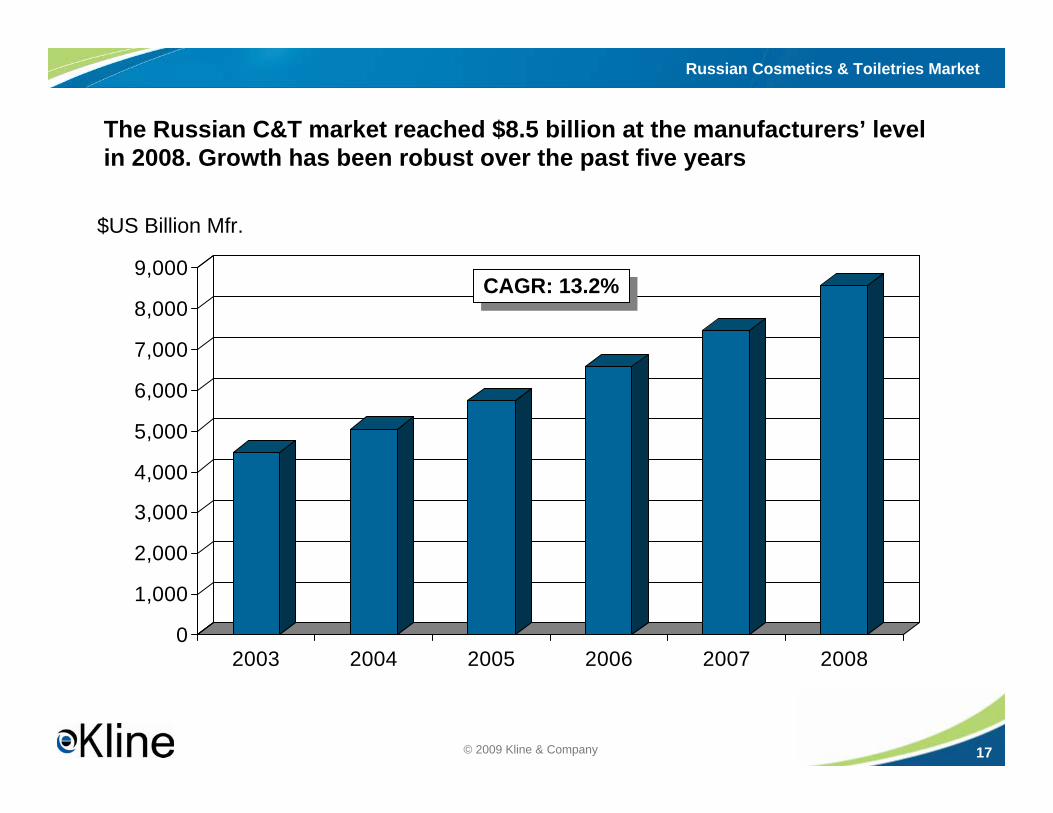

The Russian C&T market reached $8.5 billion at the manufacturers’ level in 2008. Growth has been robust over the past five years

$US Billion Mfr.

CAGR: 13.2%CAGR: 13.2%

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 18

Russia outpaces world growth in all categories by a substantial margin

Fragrances Hair care Skin care Makeup Othertoiletries

Oral care

Change, % 2007 vs 2008

Russia World

Per

cent

age

grow

th

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 19

Hot product trends and key new launches

Products with natural ingredients are increasingly in demand

Beauty salons and spas are becoming an increasingly important part of the market

Major shift toward unscented deodorants, as consumers can now afford to also buy a luxury fragrance

Value-added products in demand (e.g., color cosmetics, men’s grooming products, baby care, anti-aging, and anti-cellulite products)

More sophisticated and niche products are gaining market share (e.g., shampoo and bath and shower products for men)

Baby fragrances from local manufacturers emerge as a new segment

Lip balms containing a patented combination of ingredients claims to curb appetite and leads to weight loss

Cosmeceuticals and nutricosmetics both gaining ground

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

Products with natural and organic ingredients are growing in popularity

20

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 21

HAIR CARE PRODUCTS: Snapshot

0

2

4

6

8

10

12

Percentage growth

Hair ColoringProducts

Hair stylingproducts and

sprays

Conditioners Shampoos

Change, % 2007 vs 2008

HenkelProcter & GambleUnileverL’OréalOriflame

Shampoos

Hair coloring products

Conditioners

LEADING PLAYERS

SALES GROWTH BY CATEGORY

SALES SHARE BY CATEGORY

Hair styling products

and sprays

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

Shampoos and hair coloring product represent 70% of sales in this product category

Two-in-one products are declining in popularity and products addressing particular hair problems, such as dandruff and hair loss are growing in strength in terms of salesMore than 50% of Russian women use colorants and have a preference for permanent colorsDespite the fact that Russian consumers still consider imported to be of better quality than those produced locally, the hair coloring segment sees increased interest in local products due to new product launches, improvement in quality and increased production volumesThe long Russian cold winters are an obstacle against the fast growth of the styling products as people spend around 6 months of the year wearing hats to protect themselves from coldRussian consumers in the cities like to buy modern sophisticated products such as gels, wax, cream and balm, whereas sprays are more preferred outside big citiesThere is little brand loyalty for hair care products among Russian consumers

22

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 23

MAKEUP PRODUCTS: Snapshot

0

2

4

6

8

10

12

14

16

18

Percentage growth

Face makeup Lipsticks & lipglosses

Eye makeup Nail polishes

Change, % 2007 vs 2008

AvonOriflameL’OréalFaberlic

Lipsticks and lip glosses

Eye makeup

Face makeup

Nail polishes

LEADING PLAYERS

SALES GROWTH BY CATEGORY

SALES SHARE BY CATEGORY

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

Makeup is the second leading category in Russia

Lipsticks and lip glosses account for more than 40% of category salesLipstick is considered by Russian women as the main feature of all makeup; it is the most popular makeup product Russian women are becoming increasingly selective in choosing makeup products as quality and reputation became the most important criteria when choosing a particular brand of makeup products Direct sales companies like Avon, Oriflame and Faberlic lead the makeup market in RussiaGrowth is mainly fueled by the improvement in the income of the Russian consumers

24

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 25

OTHER TOILETRIES: Snapshot

0

5

10

15

20

25

Percentage growth

Shaving Products Personal CleansingProducts

Deodorants andantiperspirants

Change, % 2007 vs 2008

EvyapProcter & Gamble UnileverBeiersdorf

Personalcleansing products

Deodorantsand

antiperspirantsShavingproducts

SALES SHARE BY CATEGORY

LEADING PLAYERS

SALES GROWTH BY CATEGORY

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

Personal cleansing products is the leading product category while shaving products are the fastest growing

Bar soaps are the most significant contributor to sales in the personal cleansing products category, however this market is already close to the saturation point and is growing at the slowest pace of all personal cleansing product segmentsRussian women comprise the largest group of consumers of deodorants and antiperspirants Aerosols, roll-ons, and solid sticks are the three product forms that are the most popular among Russian consumersRussia represents a large market for shaving products, as there are over 54 million males in Russia over the age of 15

26

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 27

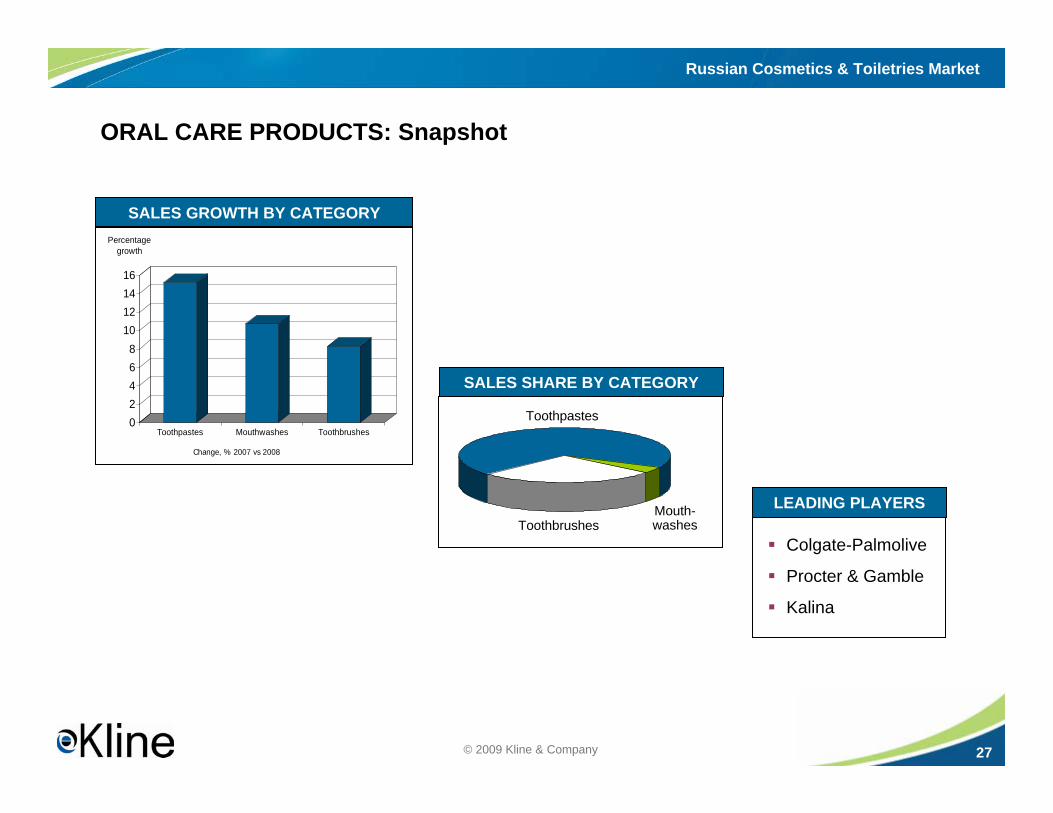

ORAL CARE PRODUCTS: Snapshot

Colgate-Palmolive

Procter & Gamble

Kalina

02468

10121416

Percentage growth

Toothpastes Mouthwashes Toothbrushes

Change, % 2007 vs 2008

Toothbrushes

Toothpastes

SALES GROWTH BY CATEGORY

SALES SHARE BY CATEGORY

Mouth-washes

LEADING PLAYERS

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

The collaboration with dental experts and pharmacists in order to improve the awareness of dental issues helped to grow sales within the product class

28

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 29

SKIN CARE PRODUCTS: Snapshot

0

5

10

15

20

25

Percentage growth

Men's skincare

Sun care Facialtreatments

Hand/bodylotions

Baby care

Change, % 2007 vs 2008

KalinaJohnson & JohnsonL’OréalBeiersdorfMary Kay

Facial treatments

Baby careHand/bodylotions

Sun care LEADING PLAYERS

Men’s skin care

SALES GROWTH BY CATEGORY

SALES SHARE BY CATEGORY

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

Growth in income, an increase in the Russian birth rate, and the aging of the Russian population are the main factors of growth in this sector

30

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 31

FRAGRANCES: Snapshot

12

12.5

13

13.5

14

14.5

Percentage growth

Fragrances for Men Fragrances for Women

Change, % 2007 vs. 2008

LVMHL’OréalProcter & GambleChanel

Fragrances for men

Fragrances for women

SALES GROWTH BY CATEGORY

SALES SHARE BY CATEGORY

LEADING PLAYERS

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company

Fragrances account for more than 10% of market sales in Russia

Russian consumers purchase Western (particularly European) brands as a sign of affluence

The luxury trade class is the largest with more than 75% of market share.

Eau de toilette products are the most popular format among Russian consumers

There is a continuing shift in the sales channels for fragrances in favor of specialized shops that position themselves as boutiques

The markets in Moscow and St. Petersburg are the most important markets in Russia, although there is increasing development in other cities and regions

32

Russian Cosmetics & Toiletries Market

© 2009 Kline & Company 33

Russian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

Kline & Co.

© 2009 Kline & Company 34

On the competitive front

Multinationals are increasing their presence in Russia, including in-country manufacturing− Foreign companies report larger sales than Russian

brands across all beauty segments, with the exception of skin care

Local Russian manufacturers are fighting back against foreign companies

Direct sales has traditionally had a strong position in the less developed regions

As competition in both Moscow and Saint Petersburg intensifies, both specialty retail networks and manufacturers are seeing new growth opportunities open up over the coming five years in Russia’s vast and often untapped regions

Competition

© 2009 Kline & Company 35

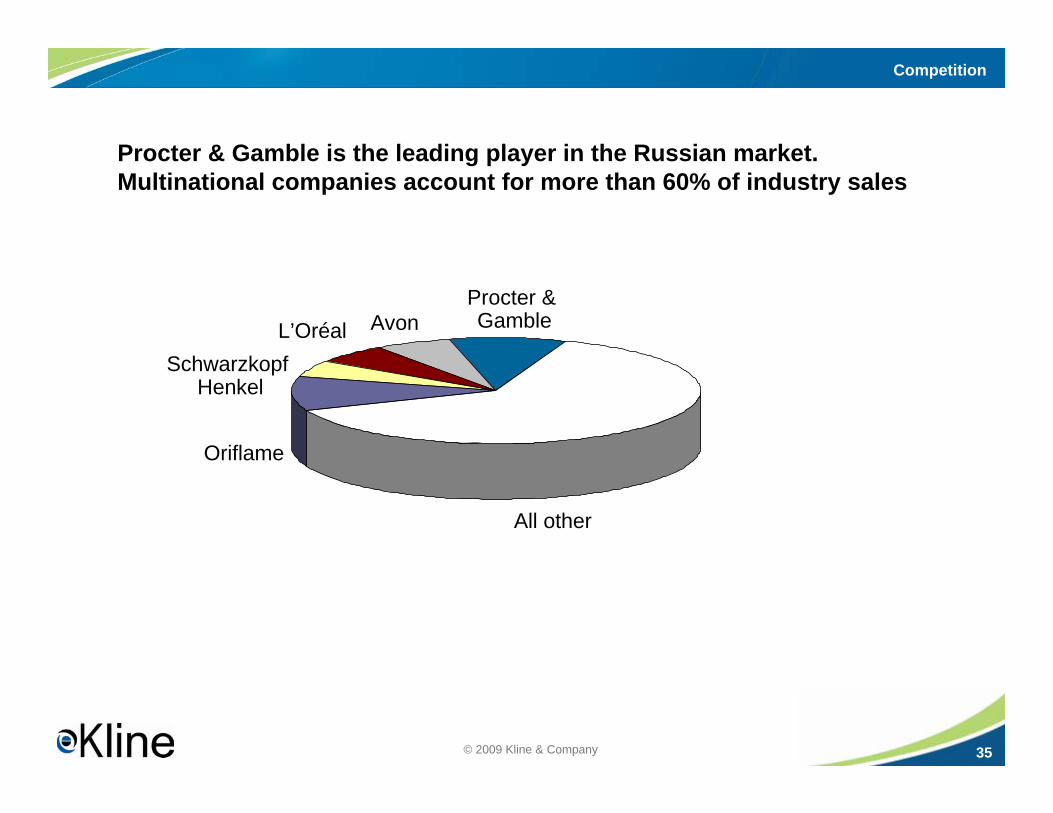

Procter & Gamble is the leading player in the Russian market. Multinational companies account for more than 60% of industry sales

Procter &GambleAvonL’Oréal

Schwarzkopf Henkel

Oriflame

All other

Competition

© 2009 Kline & Company 36

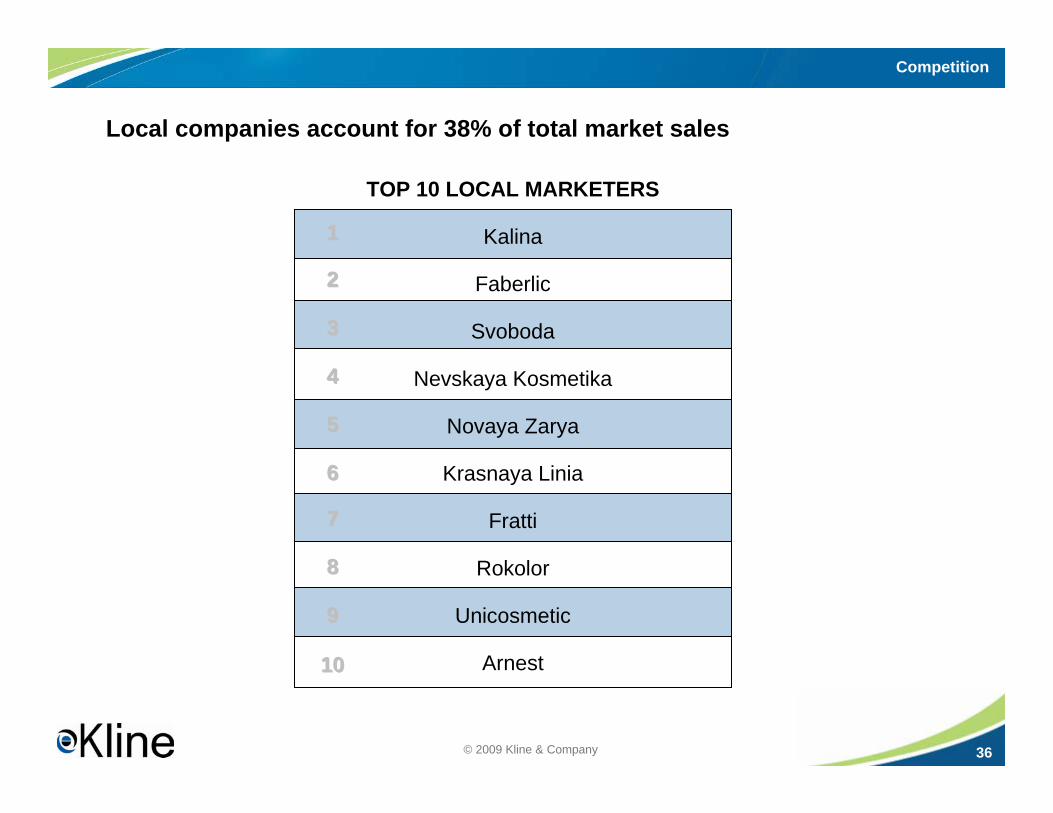

Local companies account for 38% of total market sales

TOP 10 LOCAL MARKETERS

Kalina

Faberlic

Svoboda

Nevskaya Kosmetika

Novaya Zarya

Krasnaya Linia

Fratti

Rokolor

Unicosmetic

Arnest

11

22

33

44

55

66

77

88

99

1010

Competition

© 2009 Kline & Company

Local manufacturers compete in the mass market and middle marketsegments

37

Competition

© 2009 Kline & Company 38

Russian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

Kline & Co.

© 2009 Kline & Company 39

Retail developmentThe Russian beauty retail market has been restructuring since the nineties Retails focus shifted to the regions as a new market to conquer, leading to fast expansion and many door opening especially in the last three years.Open markets are constantly losing their market share to other channels especially mass merchandisers Department stores are facing tough times especially the lower end onesSpecialty stores channel reshuffles as giant Arbat Prestige left the market in 2008New distribution channels for cosmetics and toiletries, such as the Internet and drogueries or drug stores, have appeared and are growing in popularityPharmacies are increasing their focus on parapharmaceuticals, in particular skin care products, with non medical products reaching as much as 40% in some pharmaceutical chains.

Retail Distribution

© 2009 Kline & Company 40

Direct marketing: the biggest winner

The bulk of sales is generated by person-to-person sales represented predominantly by Avon and Oriflame.Makeup is the leading product class in this channel followed by skin care.The economic crisis has had a positive effect on the direct sales channel as many manufacturers such as Avon and Faberlic have witnessed a significant increase in the number of their consultants. The boom in sales through the Internet as a way of direct marketing also played a role in the growth of the channel.

Retail Distribution

© 2009 Kline & Company 41

Specialty stores: fast expansion through the regions

Second largest distribution channel for cosmetics and toiletries in Russia The big expansion in the regions and the increase in the income of the Russian consumer were the main drivers for the channel’s growthOffer a special shopping experience as well as in-store beauty treatment corners and beauty institutes Professional aestheticians, consultants, and makeup artists provide clients expert advice on various products Big focus on online sales and loyalty programsMain channel for sale of prestige brandsShare of mass brands is growing

Retail Distribution

© 2009 Kline & Company 42

Department stores: interesting format but losing popularity

Specialty department stores repositioned themselves as luxury destinations

Traditional department stores are facing many difficulties in Russia mainly the lack of interest among the Russian consumers to such store formats as it reminds them of the “Univermags” of the Soviet era and the poor quality of products that these were offering

Lower end department stores, “Univermags”, are facing increasing competition from shopping centers and mass merchandisers

Other toiletries and hair care products are the dominating product categories in this channel and they are sold mainly in low end department stores

Retail Distribution

© 2009 Kline & Company 43

Russian Cosmetics & Toiletries Market

Competition

Retail Distribution

Outlook

Global Market Overview

Agenda

Kline & Co.

© 2009 Kline & Company 44

Plenty of potential left

The increasing wealth and purchasing power of the Russian consumers will boost the sales of cosmetics and toiletries

Beauty retailers will continue expanding in the regions and differentiating themselves

Big opportunities in emerging channels of distribution such as drogueries and mass merchandisers

Expansion of mass merchandisers and supermarkets in the regions will provide additional opportunities and convenience for consumers to purchase products

More opportunities for private label, exclusive, and niche brands

Outlook

© 2009 Kline & Company 45

Economic prosperity will drive further changes in buying patterns

The aging of the Russian population will further boost the demand for anti-aging products

Interest in niche brands will continue increasing

Interest in natural and organic cosmetics will keep on growing

Men’s products will continue to grow as an important target segment across categories

Demand for added value products at competitive prices will further grow

With changes in the lifestyle, spa procedures and professional hair care and skin care products will become even more popular

Outlook

© 2009 Kline & Company 4646

Questions & Answers

Americas____________

Asia ___________

Europe___________

Kline & Company, Inc.Overlook at Great Notch150 Clove RoadLittle Falls, NJ 07424-0410Phone: +1-973-435-6262Fax: +1-973-435-6291

www.KlineGroup.com

If you require additional information about the contents of this document or the services that Kline provides, please contact:

Kline is a worldwide consulting and research firm dedicated to providing the kind of insight and knowledge that helps companies find a clear path to success. The firm has served the management consulting and market research needs of organizations in the chemicals, materials, energy, life sciences, and consumer products industries for nearly 50 years. For more information, visit www.KlineGroup.com.

Carrie MellageDirector, Consumer ProductsPhone: +1-973-435-3412E-mail: [email protected]

Kristy AltenburgClient Relations Supervisor, North AmericaPhone: +1-973-435-3367E-mail: [email protected]