Embed Size (px)

Citation preview

ASIAN DEVELOPMENT BANK PCR: PHI 25351

PROJECT COMPLETION REPORT

ON THE

RURAL MICROENTERPRISE FINANCE PROJECT (Loan 1435-PHI[SF])

IN THE

PHILIPPINES

February 2005

CURRENCY EQUIVALENTS

Currency Unit – Peso (P)

At Appraisal At Project Completion (March 1996) (December 2002)

P1.00 = $0.0384 $0.0186 $1.00 = P26.00 P53.52

ABBREVIATIONS

ASA – Association of Social Advancement ASHI – Ahon sa Hirap BSP – Bangko Sentral ng Pilipinas BME – benefit monitoring and evaluation CARD – Center for Agriculture and Rural Development EO – executive order GFI – government financial institutions IFAD – International Fund for Agricultural Development LBP – Land Bank of the Philippines MIS – management information systems MFI – microfinance institutions NCC – National Credit Council NLSF – National Livelihood Support Fund NWTF – Negros Women for Tomorrow Foundation PCFC – People’s Credit and Finance Corporation RMFP – Rural Microenterprise Finance Project SHG – self-help groups SEC – Securities and Exchange Commission SDR – Special Drawing Rights TSKI – Taytay sa Kauswagan, Inc. TCC – Training Coordinating Committee

NOTES

(i) The fiscal year (FY) of the Government ends on 31 December. (ii) In this report, "$" refers to US dollars.

CONTENTS

Page

BASIC DATA i

MAP v

I. PROJECT DESCRIPTION 1

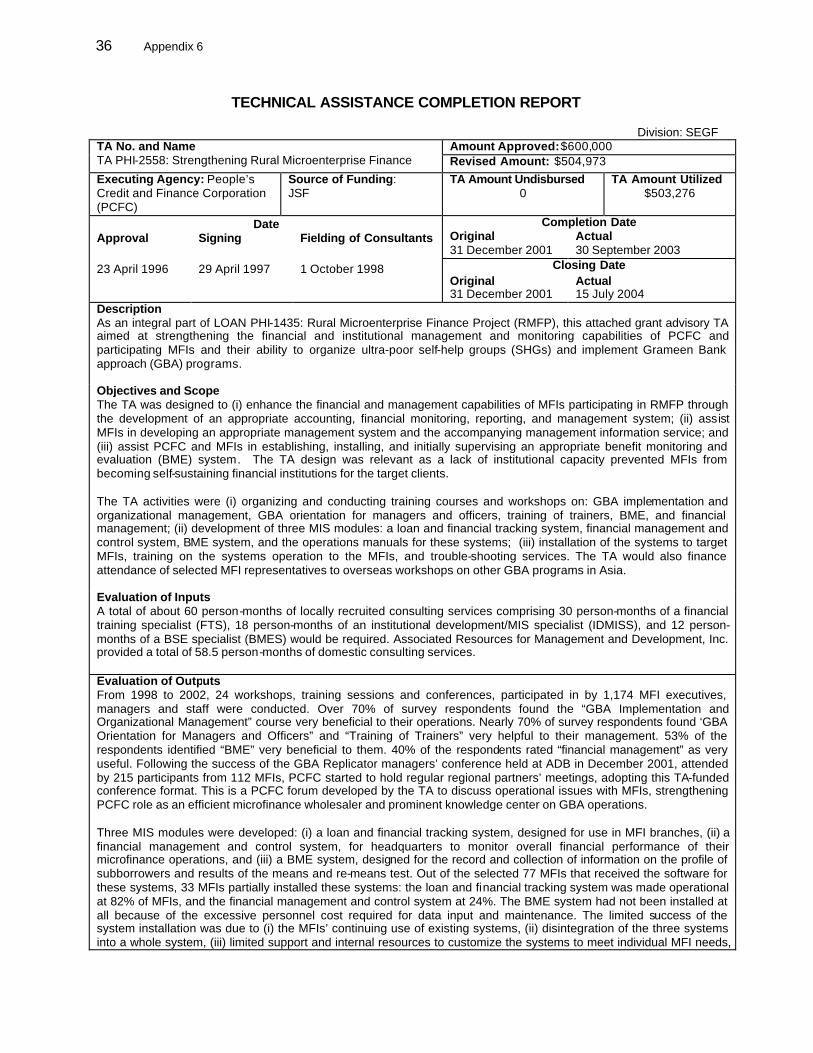

II. EVALUATION OF DESIGN AND IMPLEMENTATION 2 A. Relevance of Design and Formulation 2 B. Project Outputs 4 C. Project Costs 5 D. Disbursement Performance 6 E. Project Schedule 7 F. Implementation Arrangements 7 G. Covenants 7 H. Related Technical Assistance 7 I. Consultant Recruitment and Procurement 8 J. Performance of Consultants, Contractors and Suppliers 9 K. Performance of the Borrower and the Executing Agency 9 L. Performance of the Asian Development Bank 10

III. EVALUATION OF PERFORMANCE 11 A. Relevance 11 B. Efficacy in Achievement of Purpose 11 C. Efficiency in Achievement of Outputs and Purpose 14 D. Preliminary Assessment of Sustainability 14 E. Institutional Development and Other Impacts 15 F. Environmental, Sociocultural, and Other Impacts 15

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 15 A. Overall Assessment 15 B. Lessons Learned 16 C. Recommendations 16

APPENDIXES 1. Project Framework 19 2. Flow of Funds and lending Terms 22 3. Project Achievements 23 4. Graphical Presentation of Disbursement 25 5. Status of Compliance with Major Loan Covenants 26 6. Technical Assistance Completion Report 36 7. PCFC Accreditation Criteria 38

SUPPLEMENTARY APPENDIXES A. Impact Study B. IFAD RMFP Interim Evaluation Report C. Profile of Conduits

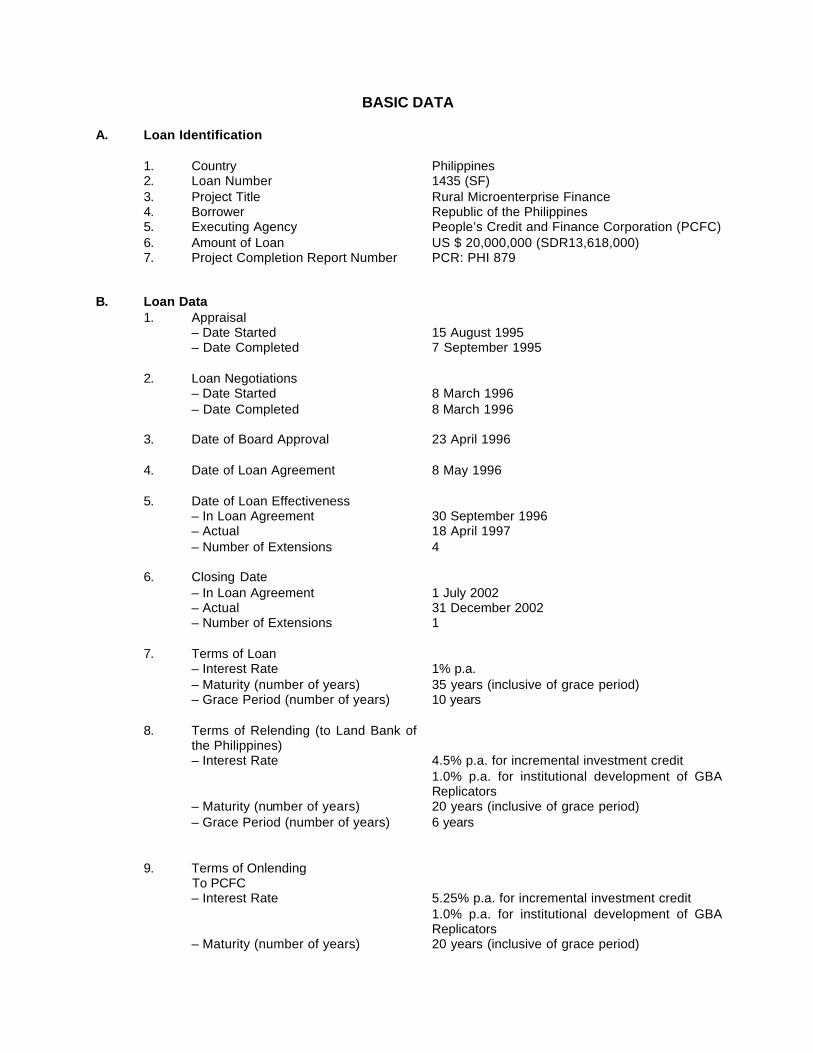

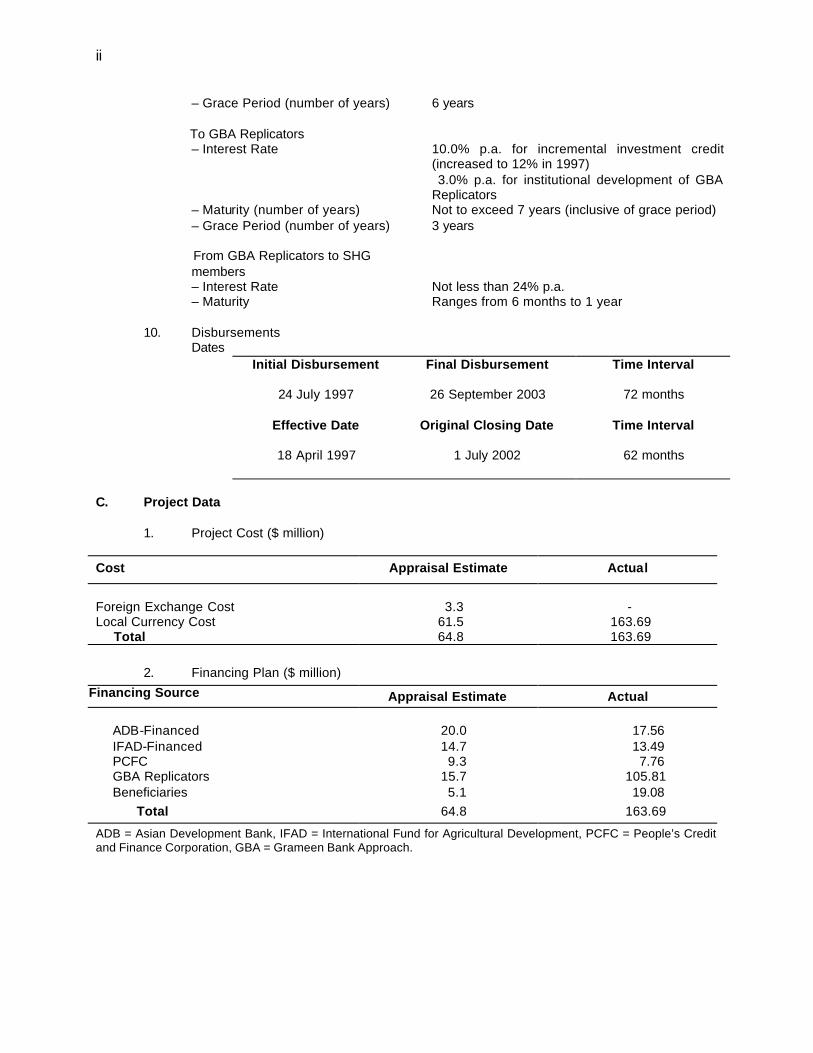

BASIC DATA A. Loan Identification 1. Country 2. Loan Number 3. Project Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Project Completion Report Number

Philippines 1435 (SF) Rural Microenterprise Finance Republic of the Philippines People’s Credit and Finance Corporation (PCFC) US $ 20,000,000 (SDR13,618,000) PCR: PHI 879

B. Loan Data 1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 6. Closing Date – In Loan Agreement – Actual – Number of Extensions 7. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years) 8. Terms of Relending (to Land Bank of

the Philippines) – Interest Rate – Maturity (number of years) – Grace Period (number of years)

9. Terms of Onlending To PCFC

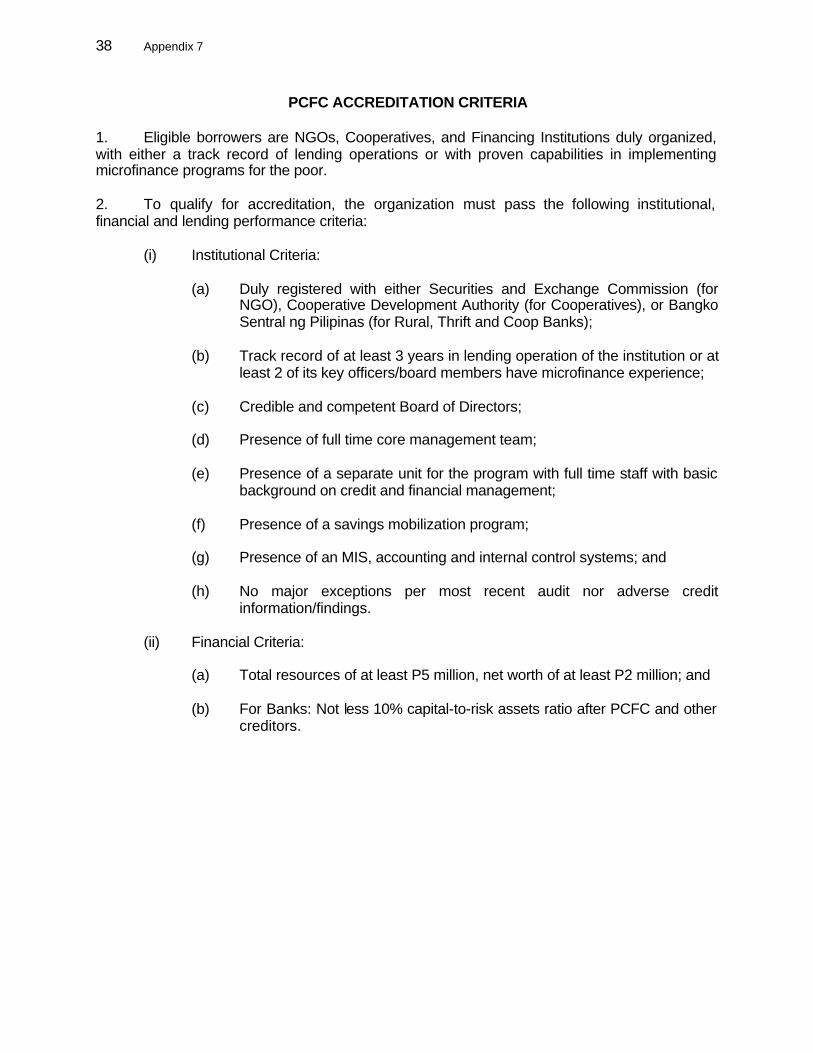

– Interest Rate – Maturity (number of years)

15 August 1995 7 September 1995 8 March 1996 8 March 1996 23 April 1996 8 May 1996 30 September 1996 18 April 1997 4 1 July 2002 31 December 2002 1 1% p.a. 35 years (inclusive of grace period) 10 years 4.5% p.a. for incremental investment credit 1.0% p.a. for institutional development of GBA Replicators 20 years (inclusive of grace period) 6 years 5.25% p.a. for incremental investment credit 1.0% p.a. for institutional development of GBA Replicators 20 years (inclusive of grace period)

ii

– Grace Period (number of years) To GBA Replicators – Interest Rate – Maturity (number of years) – Grace Period (number of years) From GBA Replicators to SHG

members – Interest Rate – Maturity

6 years 10.0% p.a. for incremental investment credit (increased to 12% in 1997) 3.0% p.a. for institutional development of GBA Replicators Not to exceed 7 years (inclusive of grace period) 3 years Not less than 24% p.a. Ranges from 6 months to 1 year

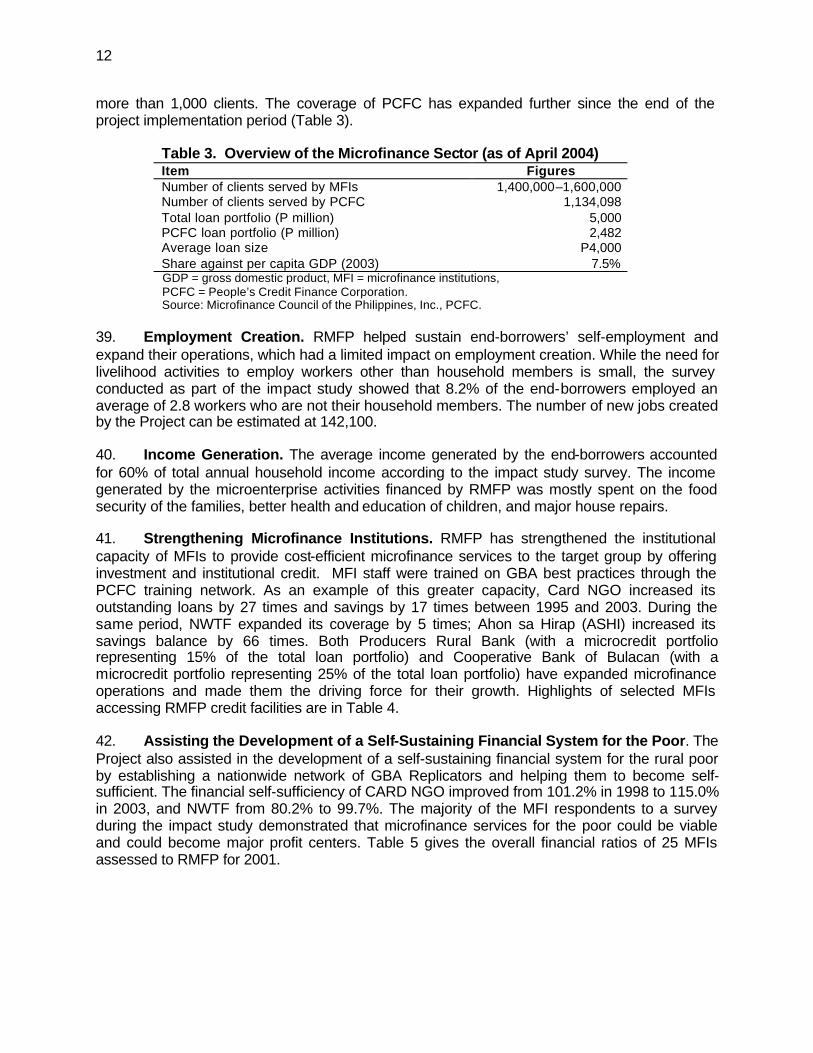

10. Disbursements Dates Initial Disbursement

24 July 1997

Final Disbursement

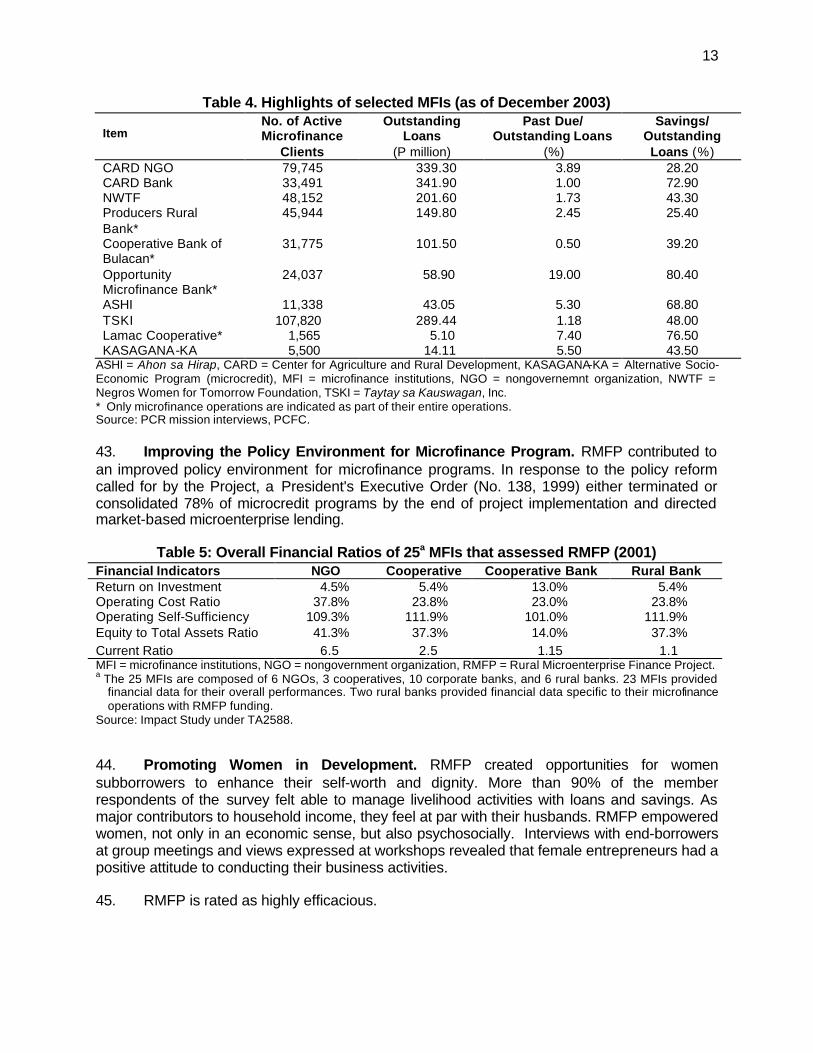

26 September 2003

Time Interval

72 months

Effective Date

18 April 1997

Original Closing Date

1 July 2002

Time Interval

62 months

C. Project Data

1. Project Cost ($ million)

Cost Appraisal Estimate Actual

Foreign Exchange Cost 3.3 - Local Currency Cost 61.5 163.69 Total 64.8 163.69

2. Financing Plan ($ million)

Financing Source Appraisal Estimate Actual ADB-Financed 20.0 17.56 IFAD-Financed 14.7 13.49 PCFC 9.3 7.76 GBA Replicators 15.7 105.81 Beneficiaries 5.1 19.08 Total 64.8 163.69

ADB = Asian Development Bank, IFAD = International Fund for Agricultural Development, PCFC = People’s Credit and Finance Corporation, GBA = Grameen Bank Approach.

iii

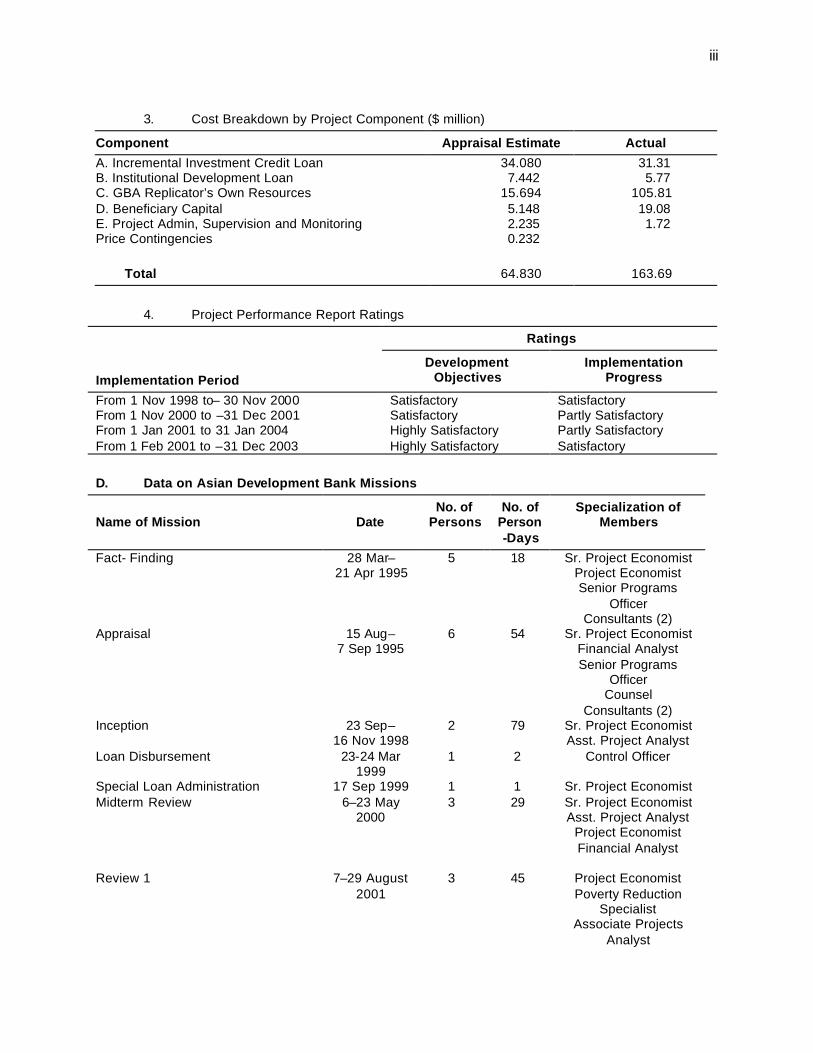

3. Cost Breakdown by Project Component ($ million)

Component Appraisal Estimate Actual

A. Incremental Investment Credit Loan 34.080 31.31 B. Institutional Development Loan 7.442 5.77 C. GBA Replicator’s Own Resources 15.694 105.81 D. Beneficiary Capital 5.148 19.08 E. Project Admin, Supervision and Monitoring 2.235 1.72 Price Contingencies 0.232 Total 64.830 163.69

4. Project Performance Report Ratings

Ratings Implementation Period

Development Objectives

Implementation Progress

From 1 Nov 1998 to– 30 Nov 2000 Satisfactory Satisfactory From 1 Nov 2000 to –31 Dec 2001 Satisfactory Partly Satisfactory From 1 Jan 2001 to 31 Jan 2004 Highly Satisfactory Partly Satisfactory From 1 Feb 2001 to –31 Dec 2003 Highly Satisfactory Satisfactory D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Members

Fact- Finding 28 Mar– 21 Apr 1995

5 18 Sr. Project Economist Project Economist Senior Programs

Officer Consultants (2)

Appraisal 15 Aug– 7 Sep 1995

6 54 Sr. Project Economist Financial Analyst Senior Programs

Officer Counsel

Consultants (2) Inception 23 Sep–

16 Nov 1998 2 79 Sr. Project Economist

Asst. Project Analyst Loan Disbursement 23-24 Mar

1999 1 2 Control Officer

Special Loan Administration 17 Sep 1999 1 1 Sr. Project Economist Midterm Review 6–23 May

2000 3 29 Sr. Project Economist

Asst. Project Analyst Project Economist Financial Analyst

Review 1 7–29 August

2001 3 45 Project Economist

Poverty Reduction Specialist

Associate Projects Analyst

iv

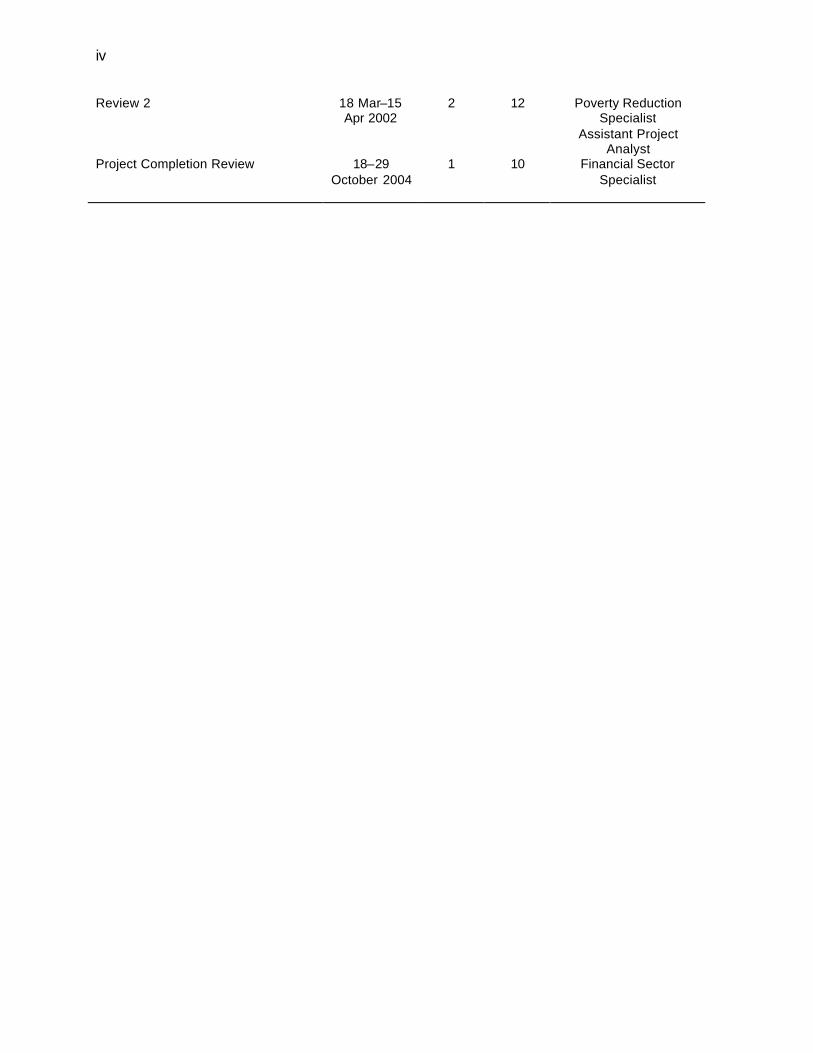

Review 2 18 Mar–15 Apr 2002

2 12 Poverty Reduction Specialist

Assistant Project Analyst

Project Completion Review 18–29 October 2004

1 10 Financial Sector Specialist

I. PROJECT DESCRIPTION

1. In 1996, the Asian Development Bank (ADB) approved a loan of $20 million equivalent to the Government of the Philippines for the Rural Microenterprise Finance Project (RMFP), which aimed to support the Government’s efforts to strengthen rural financial institutions by assisting organizations that employed the Grameen Bank approach (GBA) of providing credit to the poor. The objective of the Project was to reduce poverty, create employment opportunities, and enhance incomes of the poorest of the rural poor (the ultra poor) – the bottom 30% of the rural population as measured by income.1 The promotion of women in development was the Project’s secondary objective. 2. To achieve these objectives, RMFP sought to (i) increase the availability of credit assistance through GBA Replicators to the target group for investment in income and employment-generating microenterprises; (ii) expand the formation, growth, and strengthening of self-help groups (SHGs), composed primarily of poor rural women; (iii) promote and achieve rapid growth in savings and savings mobilization schemes among the target group; (iv) strengthen the institutional capacity of GBA Replicators to provide simple and accessible financial intermediation services (credit and savings) to the target group; (v) assist in the development of a self-sustaining financial system for the rural poor by establishing a nationwide network of GBA Replicators; and (vi) improve the policy environment for the microfinance program. 3. RMFP was formulated in response to the need to expand a proven system for organizing SHGs and delivering savings and credit services directly to the rural ultra poor. Prior to RMFP, ADB had approved three microenterprise credit loans in the Philippines, totaling $113 million.2 Generally, these projects had successfully addressed the credit needs of rural enterprises and landholding poor. However, by design, they did not specifically target the landless poor or women, although the enterprises financed under the projects may have provided employment to the ultra poor indirectly. The GBA has been recognized as a long-term, successful and sustainable system for bridging effective financial services to the ultra poor, and has produced significant income, employment and other social benefits in Bangladesh, Malaysia, and the Philippines. In response to the Government’s commitment to providing financial services to the ultra poor through the adoption of the Social Reform Agenda in 1994 and the creation of the People’s Credit and Finance Corporation (PCFC) in 1995, the Project was designed to support the training and credit needs of a nationwide program that could meet the needs of a significant percentage of the country’s ultra poor through the expansion of the GBA over the following 6 years (1996-2001). 4. RMFP included the following two credit lines:

1 The project was classified as Poverty Reduction (primary objective) and Gender and Development (secondary

objective) under the old project classification system. 2 ADB. 1988. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the

Republic of the Philippines for the NGO Microcredit Project. Manila (Loan 940-PHI, for $8 million, approved in December 1988, completed in October 1991); ADB. 1991. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the Republic of the Philippines for the Second NGO Microcredit Project. Manila (Loan 1137-PHI, for $30 million, approved in November 1991, completed in May 1997); and ADB. 1992. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to the Republic of the Philippines for the Small Farmers Credit Project. Manila (Loan 1216-PHI, for $75 million, approved in December 1992, completed in March 1998).

2

(i) Investment credit facility. A credit line to the accredited GBA Replicators or microfinance institutions (MFIs) for onlending to about 300,000 target SHG members for incremental investment in their microenterprises.

(ii) Institutional credit facility. A credit line to provide institutional development

loans to the accredited MFIs to support a portion of (a) the start-up costs for about 270 new MFI branches and ongoing development costs for about 35 existing branches; (b) the training of about 2,500 GBA branch managers and field and office staff; and (c) the costs associated with institutional preparation and formation of SHGs.

5. ADB provided a loan of $20 million (SDR13,618,000) from its Special Funds resources . The International Fund for Agricultural Development (IFAD) provided a loan of $14.7 million (SDR10,150,000). The two loans with a total amount of $34.7 million were to finance 80% ($27.3 million equivalent) of the MFIs’ total incremental investment credit requirements through the investment credit facility and a portion ($7.4 million equivalent) of the institutional development costs for new and expanded programs of MFIs through the institutional credit facility. 6. ADB also provided an advisory technical assistance (TA)3 aimed at strengthening the financial and institutional management and monitoring capacities of PCFC and participating MFIs. It was designed to (i) enhance the financial and management capabilities of MFIs participating in the Project through the development of an appropriate accounting, financial monitoring, reporting, and management system; (ii) assist MFIs to develop appropriate management systems and accompanying management information service; and (iii) assist PCFC and MFIs to establish, install, and initially supervise an appropriate benefit monitoring and evaluation (BME) system. The project framework is in Appendix 1.

II. EVALUATION OF DESIGN AND IMPLEMENTATION

A. Relevance of Design and Formulation

7. RMFP was consistent with ADB’s country strategy and program and the country’s development objectives. It was consistent with the ADB’s country operational strategy for the Philippines, which was also in line with the Government’s 6-year Medium-Term Philippine Development Plan (MTPDP) 1993-1998.4 The Project was designed to increase income and employment opportunities in rural areas by providing financial resources to microfinance institutions for onlending to the ultra poor, and by strengthening the capacity of MFIs to become self-sufficient. The Project was designed to provide two credit lines for microfinancing and institution-building, develop efficient and effective market-based rural financial services, and increase savings mobilization in rural financial markets, particularly among the poor. To guide the microfinance sector towards a healthy development path, the policy reform agenda was incorporated in the loan covenants calling for (i) the consolidation of nonagriculturally-based microcredit programs, (ii) regulation of deposit taking by MFIs, (iii) the removal of an interest rate ceiling for nonagriculturally-based microcredit programs, and (iv) the privatization of PCFC.

3 ADB. 1996. Technical Assistance to the Republic of the Philippines for Strengthening Rural Microfinance. Manila

(TA 2558–PHI, for $600,000, approved in April 1996, completed in December 2003). 4 Which was designed to achieve poverty alleviation, social equity and sustainable development through (i) strong

and sustainable economic growth, (ii) nurturing international competitiveness, (iii) fostering the private sector as the engine of economic growth, (iv) promoting human development for “people empowerment,” and (v) combating poverty.

3

RMFP was formulated through extensive dialogue with the Government and stakeholders, with good levels of participation and ownership. 8. The project preparatory technical assistance (PPTA)5 provided an in-depth study on Philippine rural finance and concluded that, at the time of the project formulation, a sound microfinance industry was hampered by an inconsistent and inefficient Government credit program. It also pointed out that many nongovernment organizations (NGOs) and cooperatives could not optimize their potential to become self-sustaining grassroots financial intermediaries because of a lack of institutional capability. It recommended a comprehensive rural financing project designed to develop a sustainable microfinance system through capacity building of MFIs, policy dialogue to consolidate and rationalize Government credit programs, and decentralized credit operations by viable NGOs and cooperatives targeting the rural poor. Overall, it was identified that financial services affordable and accessible to the rural poor was a major constraint to increasing incomes. 9. With a growing number of NGOs successfully undertaking commercially viable microfinance operations and committed to international best practices and donor-funded assistance since the project appraisal, the Government had been encouraging microfinance NGOs to develop sustainable microfinance programs. RMFP was therefore timely and relevant and complemented the Government’s efforts to develop sustainable microfinance institutions by expanding the operations of the GBA Replicators. RMFP has provided much needed long-term funding sources (up to 7 years) through PCFC to a greater number of MFIs than targeted. It has not only helped cooperatives and NGOs but also rural banks, thrift banks and cooperative rural banks strengthen their institutional capabilities and expand their microfinance operations. Greater self-sufficiency has been achieved over the years, although microfinance institutions have not yet reached 100% self-sufficiency6 on average. This shows that RMFP was relevant at completion, and contributed to progress towards a sustainable microfinance sector. While MFIs have provided lending at market interest rates affordable to the end-clients, that has been possible only through the provision of concessionary loans from ADB and IFAD to the Government. The application of ADF resources and the IFAD concessionary loan was relevant in this aspect. The flow of funds and lending terms are in Appendix 2. 10. In the implementation of the Project, there were two major divergences from the original design. At the appraisal stage, the Project aimed to provide financial and institutional assistance through PCFC to NGOs and cooperatives. In reality, conduit organizations were expanded to include regulated financial institutions: rural banks, cooperative banks, cooperative rural banks, and thrift banks. Second, the Project supported modified GBAs in addition to the original GBA. These two major changes enabled RMFP to respond to market needs and expand its outreach successfully to the target beneficiaries. 11. There were several other design changes made during implementation. In September 1997, ADB agreed that the interest rate for onlending from PCFC to participating MFIs be increased from 10% to 12% in order to cover all the operational costs of PCFC. PCFC realized the need to conduct a stricter credit evaluation of candidate MFIs before the beginning of the project’s operations and to monitor all lending activities during implementation more closely. Subloan size limits were increased in November 1998 by: (i) increasing the ceiling of investment 5 ADB. 1991. Technical Assistance to the Republic of the Philippines for the Rural Credit Study. Manila (TA 1617–

PHI, for $640,000, approved in November 1991, completed in October 1994). 6 The average financial self-sufficiency (FSS) ratio of all microfinance institutions (MFIs) as of July 2000 was 90.0%.

Majority of MFIs could barely cover operational costs if they were not subsidized, and if they were following international accounting standards and funding its expansion with commercial-cost liabilities.

4

loans to any one branch of a MFI from P2.5 million to P3.5 million per year, or from P7 million to P10 million over the course of the Project; (ii) increasing the ceiling of institutional loans to any one branch of an MFI from P0.7 million to P1.0 million over the course of the Project; (iii) initiating separate institutional loans of not more than P2.5 million to MFIs with the training coordinating committee (TCC) recognized and endorsed training program; and (iv) increasing end-borrower loan size limits from P5,000 to P6,000 maximum for first cycle loans, and up to a P25,000 maximum for end-borrowers who have successfully completed a minimum of three loan cycles (increased from P14,000). These changes were necessary in order to conduct effective onlending in response to market needs while maintaining outreach to the ultra poor. B. Project Outputs

12. The project outputs by component as anticipated during appraisal were as follows.

(i) For the investment component

(a) creation or expansion of about 300,000 microenterprises; and (b) savings generated equivalent of at least 10% of cumulative GBA branch

loans.

(ii) For the institutional component

(a) about 270 branches established and 35 branches expanded, reaching an average client level of 1,500 per branch;

(b) improvement and expansion of training facilities and materials, expansion in the number of trainers at three training centers, evaluation and classification of about 25 qualified GBA branches as training branches;

(c) 2,500 field staff trained for 3-6 months each in GBA concepts and skills; and

(d) international exposure of at least 30 managerial staff to other GBA-type programs.

(iii) In addition, the following policy reforms were anticipated:

(a) consolidation of 50% of the nonagriculturally-based microcredit program; (b) regulation of deposit-taking activities of microfinance institutions; (c) removal of the interest rate ceiling for nonagriculturally-based microcredit

programs; and (d) privatization of PCFC.

13. Expected outputs under the investment component were fully achieved. Funds onlent by the participating MFIs have benefited 618,906 microenterprises, more than twice as many as the target number. More than 97% of the end-borrowers were women, exceeding the target of 90% women clients. Savings generation was strongly promoted by the Project. Savings mobilized as of end-2002 were estimated at P839 million, accounting for 36% of the total loan proceeds disbursed. Savings included the center fund of typically 5% against the loan amount, and capital-build up of a minimum of P25 per week (2.5–12.5% against the loan amount), both of which are compulsory, and other voluntary savings. Expected outputs under the institutional component were fully achieved. The institutional loan has supported a portion of the start-up and expansion costs of the 505 GBA Replicator branches, comprising 94 cooperatives, 85 cooperative banks, 90 NGOs, 213 rural banks, 14 lending investors, and 9 thrift banks. It has

5

also supported the training of 2,505 branch managers and field officers of 125 MFIs, of which 317 were from cooperatives, 530 from cooperative banks, 571 from NGOs, 1,048 from rural banks, 12 from lending investors, and 27 from thrift banks. 14. Three of the four government actions called for under the policy component were taken. A President's Executive Order (EO) (No. 138, 10 August 1999), directed government nonfinancial agencies and government-owned and controlled corporations (GOCC) to immediately begin rationalizing their ongoing directed credit programs in accordance with the rationalization program of the National Credit Council (NCC).7 Of the 27 nonagriculturally-based microcredit programs, 21 (78%), were either terminated or consolidated with existing credit programs and transferred to government financial institutions (GFIs) by the end of project implementation. EO 138 also directed GFIs to operate wholesale lending based on the prevailing market rates. BSP placed all deposit-taking institutions that collect savings beyond the compensating balance under its prudential supervision. 15. Privatization of PCFC was held up by an unsuccessful bidding process in October 2000. The Social Reform and Poverty Alleviation Act (Republic Act 8425 of 1998) limited the eligible private investors, if PCFC was to be privatized, to qualified nongovernment organizations, people’s organizations and cooperatives. PCFC did not receive enough bids for privatization in the bidding. Recent government actions, however, seem to have made the PCFC privatization plan irrelevant. On 22 September 2004, a President's Executive Order (EO 362) directed that the National Livelihood Support Fund (NLSF) be merged with PCFC according to guidelines, rules and regulations to be formulated by the Land Bank of the Philippines (LBP) and the NLSF secretariat. The announcement may lead to the scrapping of the PCFC privatization plan, as it paved the way for PCFC to have access to NLSF financial resources under a fund management contract. From a project operation’s point of view, noncompliance with the privatization clause did not affect project costs, time schedules, expected benefits, or other measures of efficiency. The PCFC privatization issue is further discussed in para 56. A table of project achievement is in Appendix 3 C. Project Costs

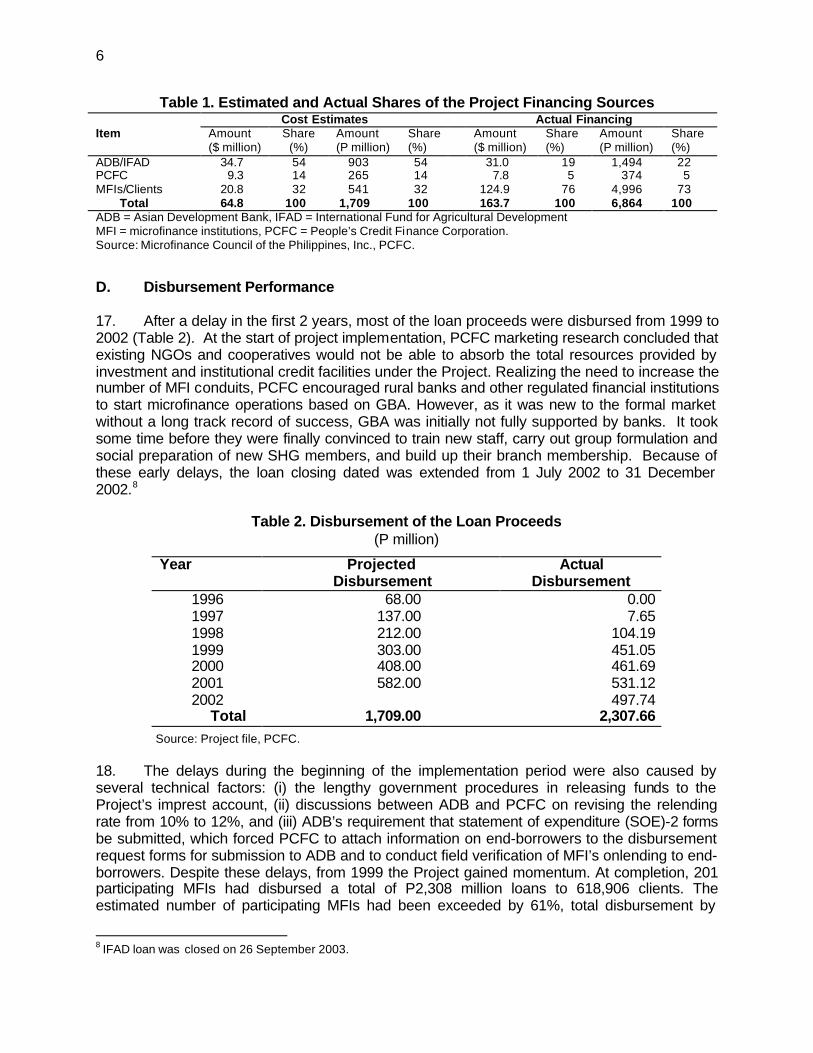

16. It was estimated that the total cost of the Project would be $64.8 million equivalent, which would include financial contributions from MFIs and PCFC as well as the financial and in-kind contributions of SHG members. It was estimated that the ADB and IFAD loans would account for 54% of the total Project cost (42% for investment credit and 12% for institutional development loans). PCFC would provide a portion of investment credit funds and the project administration cost, amounting to 14% of the total Project cost. Finally it was estimated that MFIs would finance 24% and their clients 8% of the total Project cost. The actual contribution of the ADB and IFAD loans was 19%, much lower than the estimated 54%, and the contribution of PCFC was 5% compared with an estimated 14%. MFIs and clients made a greater than estimated contributions with a combined share of 76%. This was because of greater mobilization of savings and diversification of MFI funding sources beyond the Project’s investment credit facility. Table 1 shows the estimated and actual shares of the Project financing sources.

7 The United States Agency for International Development (USAID) through its Credit Policy Improvement Project

diagnosed the Government credit policy and assisted the Government to prepare EO 138.

6

Table 1. Estimated and Actual Shares of the Project Financing Sources Cost Estimates Actual Financing Item Amount

($ million) Share

(%) Amount (P million)

Share (%)

Amount ($ million)

Share (%)

Amount (P million)

Share (%)

ADB/IFAD 34.7 54 903 54 31.0 19 1,494 22 PCFC 9.3 14 265 14 7.8 5 374 5 MFIs/Clients 20.8 32 541 32 124.9 76 4,996 73

Total 64.8 100 1,709 100 163.7 100 6,864 100 ADB = Asian Development Bank, IFAD = International Fund for Agricultural Development MFI = microfinance institutions, PCFC = People’s Credit Finance Corporation. Source: Microfinance Council of the Philippines, Inc., PCFC. D. Disbursement Performance

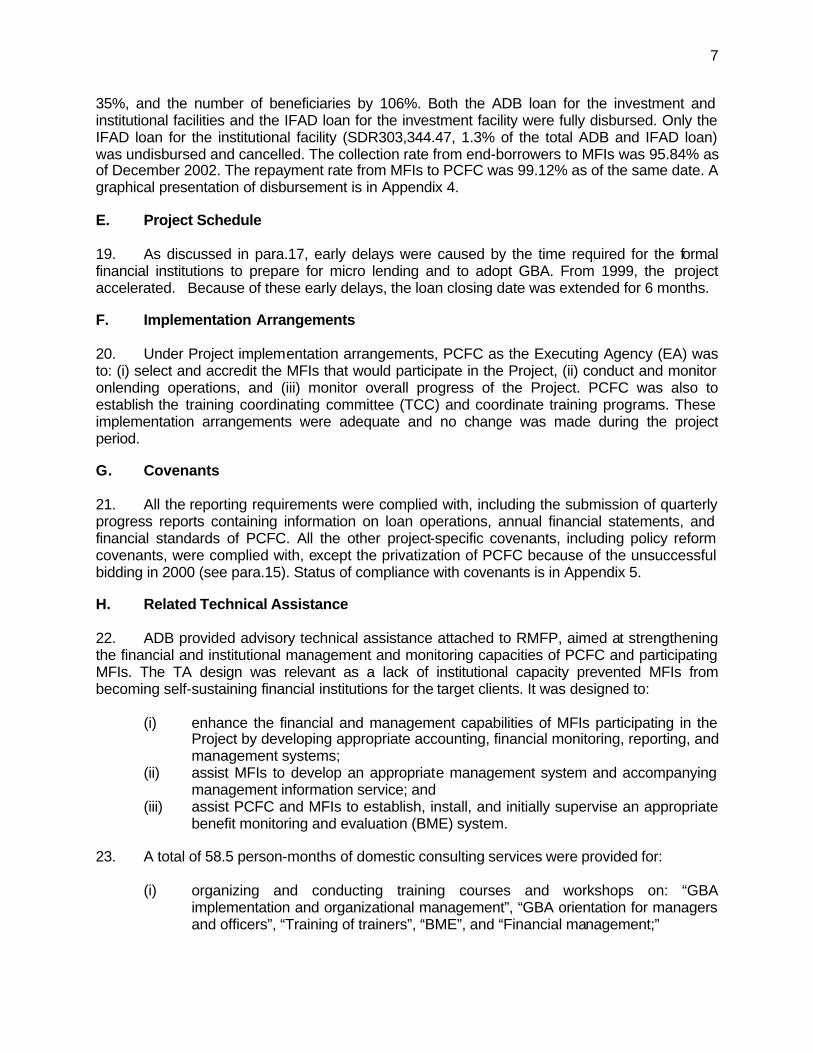

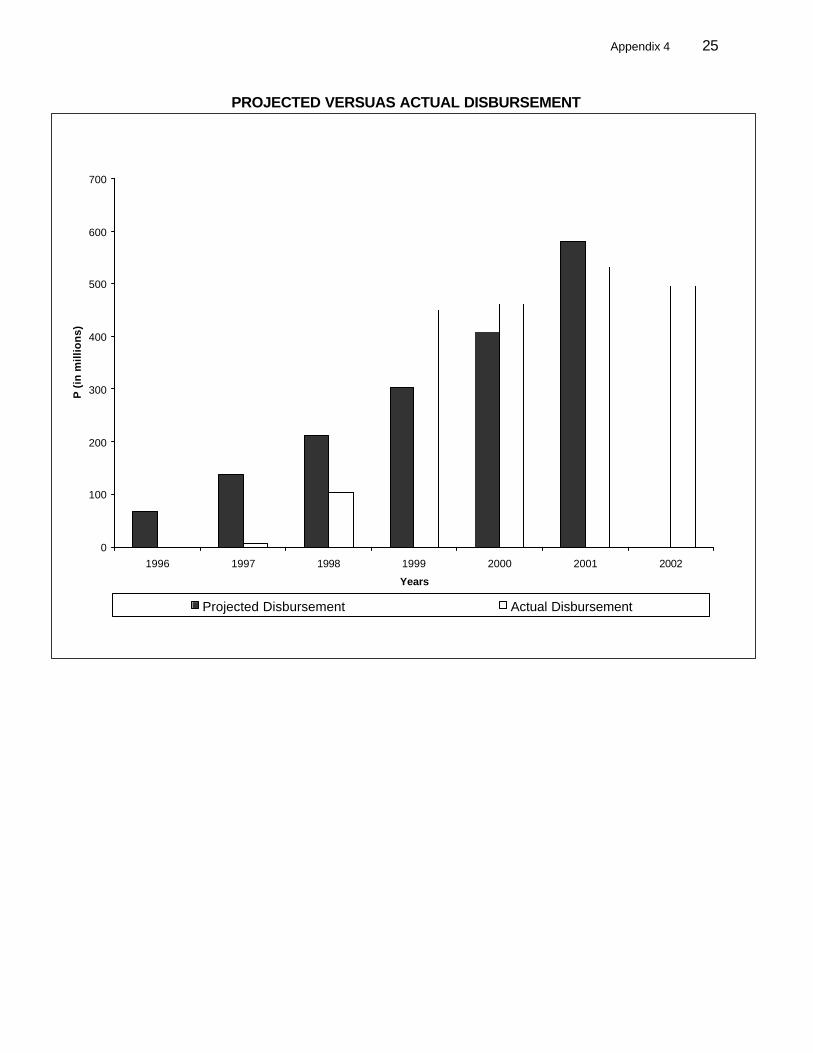

17. After a delay in the first 2 years, most of the loan proceeds were disbursed from 1999 to 2002 (Table 2). At the start of project implementation, PCFC marketing research concluded that existing NGOs and cooperatives would not be able to absorb the total resources provided by investment and institutional credit facilities under the Project. Realizing the need to increase the number of MFI conduits, PCFC encouraged rural banks and other regulated financial institutions to start microfinance operations based on GBA. However, as it was new to the formal market without a long track record of success, GBA was initially not fully supported by banks. It took some time before they were finally convinced to train new staff, carry out group formulation and social preparation of new SHG members, and build up their branch membership. Because of these early delays, the loan closing dated was extended from 1 July 2002 to 31 December 2002.8

Table 2. Disbursement of the Loan Proceeds (P million)

Source: Project file, PCFC. 18. The delays during the beginning of the implementation period were also caused by several technical factors: (i) the lengthy government procedures in releasing funds to the Project’s imprest account, (ii) discussions between ADB and PCFC on revising the relending rate from 10% to 12%, and (iii) ADB’s requirement that statement of expenditure (SOE)-2 forms be submitted, which forced PCFC to attach information on end-borrowers to the disbursement request forms for submission to ADB and to conduct field verification of MFI’s onlending to end-borrowers. Despite these delays, from 1999 the Project gained momentum. At completion, 201 participating MFIs had disbursed a total of P2,308 million loans to 618,906 clients. The estimated number of participating MFIs had been exceeded by 61%, total disbursement by

8 IFAD loan was closed on 26 September 2003.

Year Projected Disbursement

Actual Disbursement

1996 68.00 0.00 1997 137.00 7.65 1998 212.00 104.19 1999 303.00 451.05 2000 408.00 461.69 2001 582.00 531.12 2002 497.74

Total 1,709.00 2,307.66

7

35%, and the number of beneficiaries by 106%. Both the ADB loan for the investment and institutional facilities and the IFAD loan for the investment facility were fully disbursed. Only the IFAD loan for the institutional facility (SDR303,344.47, 1.3% of the total ADB and IFAD loan) was undisbursed and cancelled. The collection rate from end-borrowers to MFIs was 95.84% as of December 2002. The repayment rate from MFIs to PCFC was 99.12% as of the same date. A graphical presentation of disbursement is in Appendix 4. E. Project Schedule

19. As discussed in para.17, early delays were caused by the time required for the formal financial institutions to prepare for micro lending and to adopt GBA. From 1999, the project accelerated. Because of these early delays, the loan closing date was extended for 6 months. F. Implementation Arrangements

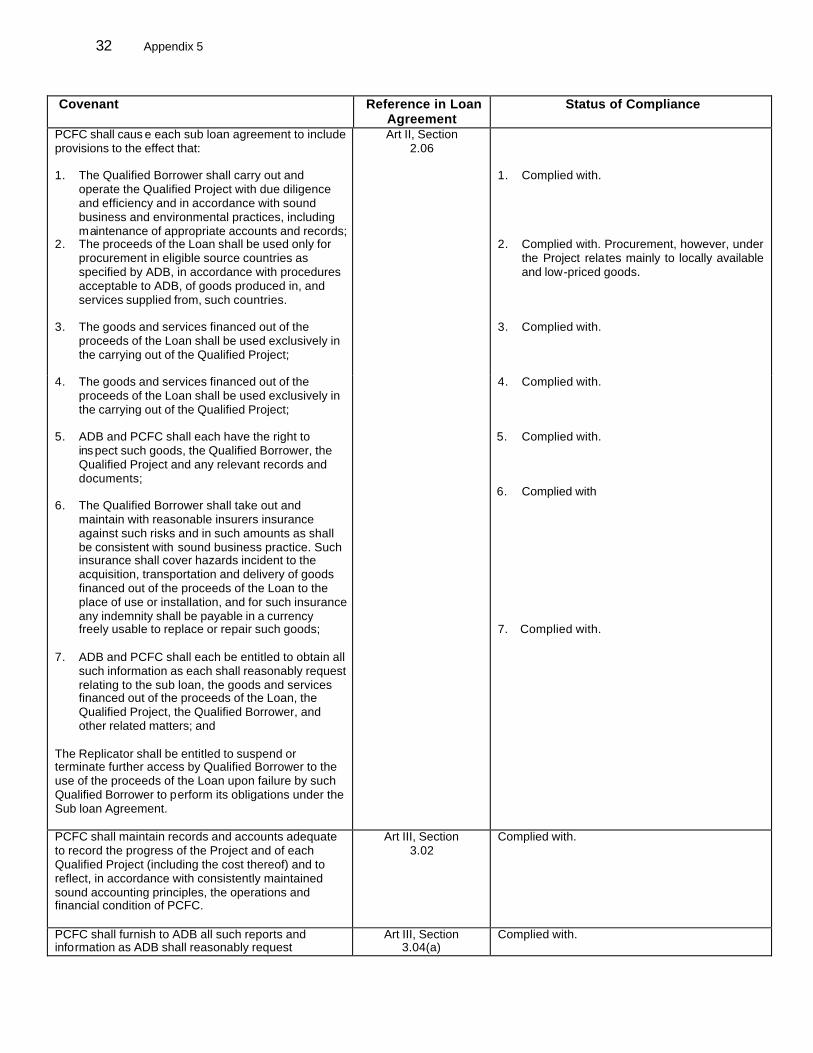

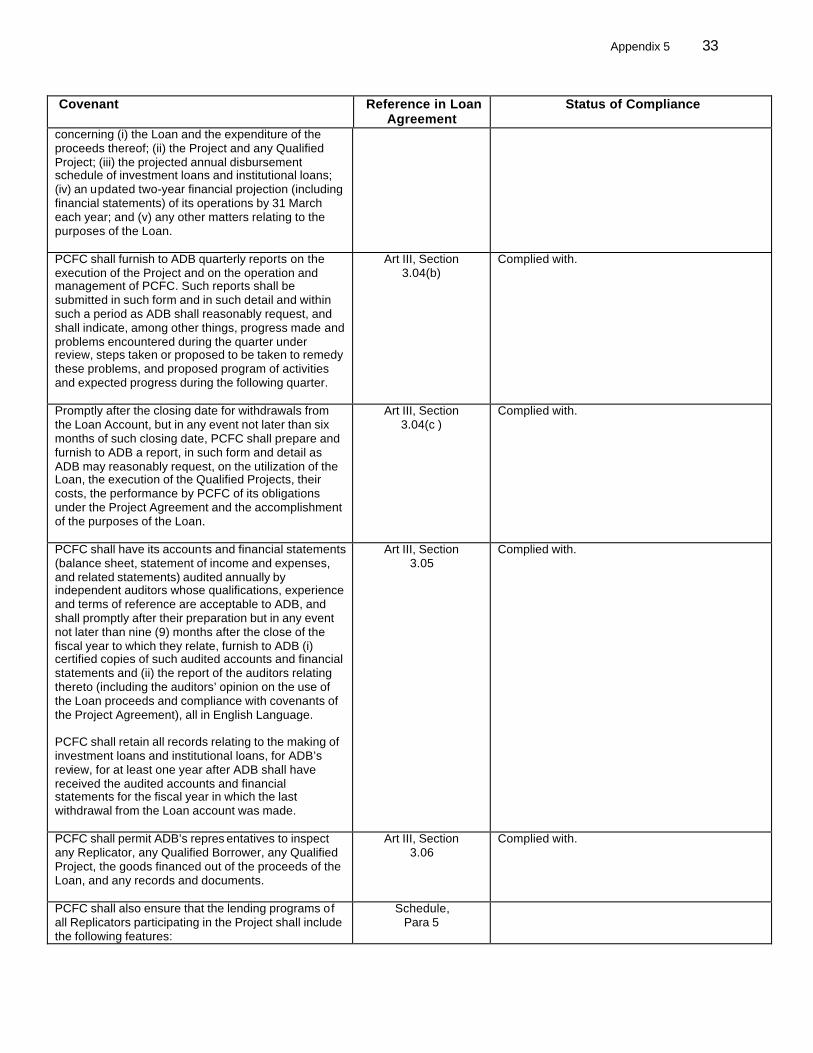

20. Under Project implementation arrangements, PCFC as the Executing Agency (EA) was to: (i) select and accredit the MFIs that would participate in the Project, (ii) conduct and monitor onlending operations, and (iii) monitor overall progress of the Project. PCFC was also to establish the training coordinating committee (TCC) and coordinate training programs. These implementation arrangements were adequate and no change was made during the project period. G. Covenants

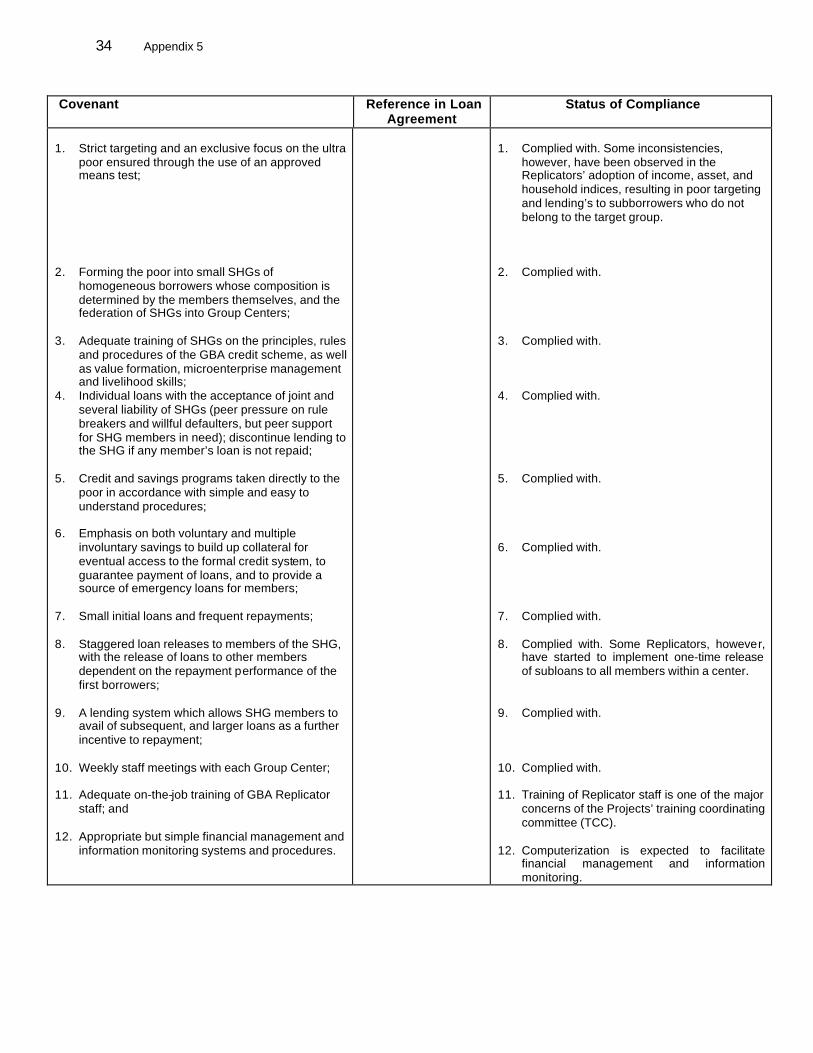

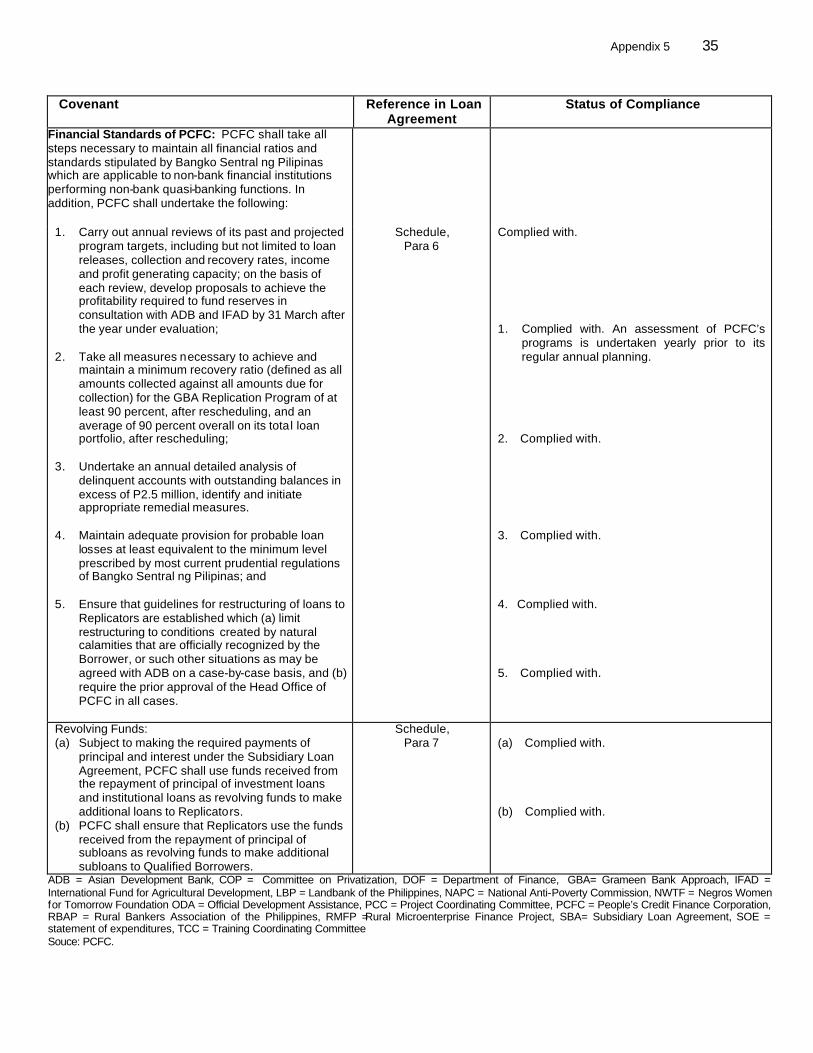

21. All the reporting requirements were complied with, including the submission of quarterly progress reports containing information on loan operations, annual financial statements, and financial standards of PCFC. All the other project-specific covenants, including policy reform covenants, were complied with, except the privatization of PCFC because of the unsuccessful bidding in 2000 (see para.15). Status of compliance with covenants is in Appendix 5. H. Related Technical Assistance

22. ADB provided advisory technical assistance attached to RMFP, aimed at strengthening the financial and institutional management and monitoring capacities of PCFC and participating MFIs. The TA design was relevant as a lack of institutional capacity prevented MFIs from becoming self-sustaining financial institutions for the target clients. It was designed to:

(i) enhance the financial and management capabilities of MFIs participating in the Project by developing appropriate accounting, financial monitoring, reporting, and management systems;

(ii) assist MFIs to develop an appropriate management system and accompanying management information service; and

(iii) assist PCFC and MFIs to establish, install, and initially supervise an appropriate benefit monitoring and evaluation (BME) system.

23. A total of 58.5 person-months of domestic consulting services were provided for:

(i) organizing and conducting training courses and workshops on: “GBA implementation and organizational management”, “GBA orientation for managers and officers”, “Training of trainers”, “BME”, and “Financial management;”

8

(ii) convening a PCFC forum to discuss operational issues with MFIs, strengthening PCFC’s role as an efficient microfinance wholesaler and prominent knowledge center on GBA operations;

(iii) developing three management information system (MIS) modules (a loan and financial tracking system, a financial management and control system, and a BME system), and the operations manuals for these systems;

(iv) installing systems to target MFIs, conducting training on the systems for MFIs, and carrying out trouble-shooting services; and

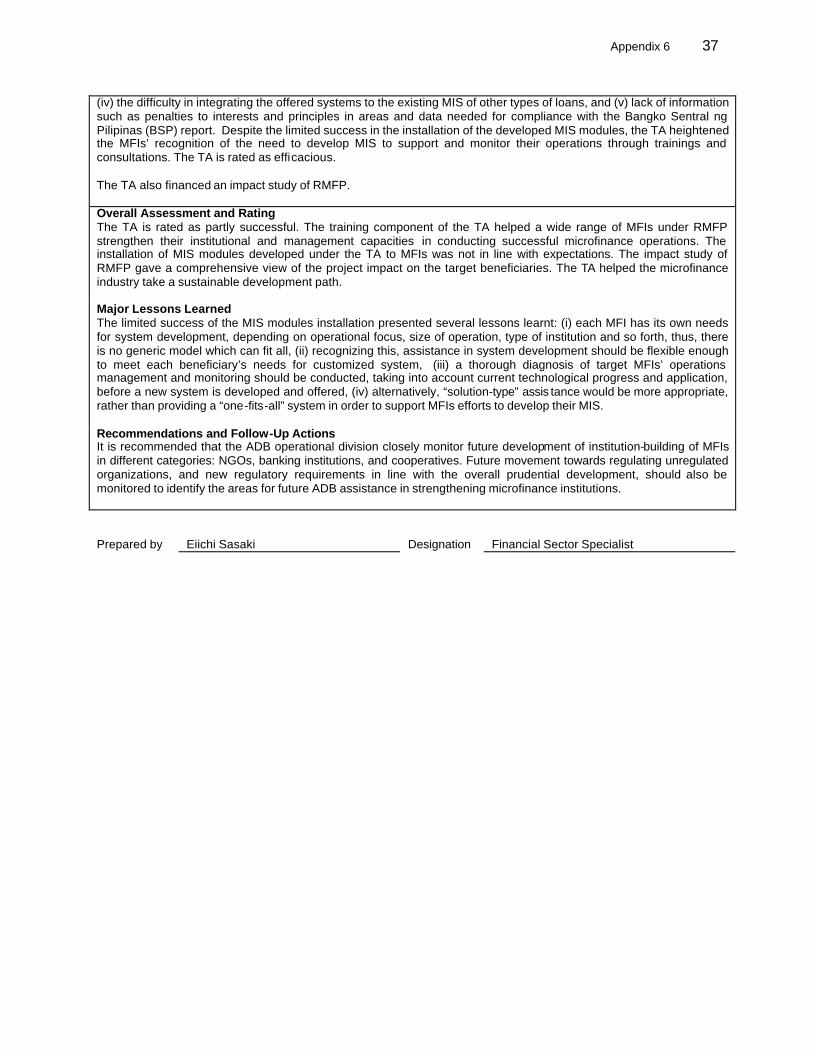

(v) preparing an impact study of RMFP. PCFC as the EA for the TA conducted TA activities efficiently. 24. The TA is rated as partly successful. The training component of the TA helped a wide range of MFIs under RMFP strengthen their institutional and management capacity to conduct successful microfinance operations. The installation of MIS modules developed under the TA to MFIs was not in line with expectations because:

(i) MFIs continued to use existing systems; (ii) the developed three systems were not intefrated into a whole system; (iii) limited support and internal resources were devoted to customizing the systems

to meet individual MFI needs; (iv) there were difficulties in integrating the systems with the existing MIS for other

types of loans; and (v) lack of information on such issues as penalties to interests and principal in areas

and data needed for compliance with the BSP report. 25. The major lessons from the TA were as follows:

(i) each MFI has particular needs for system development, depending on its operational focus, the size of its operations, the type of institution, and other characteristics, so there is no generic model which can fit all;

(ii) recognizing this, assistance for system development should be flexible enough to meet each beneficiary’s need for a customized system;

(iii) a thorough diagnosis of target MFIs’ operations management and monitoring should be conducted, taking into account current technological progress and application, before new systems are developed and offered; and

(iv) alternatively, assistance geared towards offering solutions would be more appropriate than a “one-fits-all” system.

26. Despite limited success in installing the MIS modules, the TA heightened the MFIs’ recognition of the need to develop MIS to support and monitor their operations through training and consultations. The RMFP impact study provided a comprehensive view of the project impact on the target beneficiaries. The TA is rated as efficacious. The TA completion report has been prepared concurrently with this project completion report (see Appendix 6). The TA helped the microfinance industry take a sound development path. I. Consultant Recruitment and Procurement

27. Associated Resources for Management and Development, Inc. was selected in accordance with ADB’s Guidelines on the Use of Consultants and other arrangements satisfactory to ADB for the selection of domestic consultants.

9

J. Performance of Consultants, Contractors and Suppliers

28. No significant problem was encountered in packaging contracts, preparing tender documents, and evaluating bids. K. Performance of the Borrower and the Executing Agency

29. Performance of the Government. Before the announcement of EO 138 in August 1999, which provided for a phase-out of directed credit programs operated by government nonfinancial agencies, three programs were targeted at poor households: Tulong sa Tao of the Department of Trade and Industry, the Self-employment Assistance Program of the Department of Social Welfare and Development, and the Grameen Bank Replication Project of the Agricultural Credit Policy Council. These programs had a combined client base of 150,000 reached through over 2,000 conduits. However, they had been heavily criticized for being inefficient, highly politicized, uncoordinated and unsustainable. EO 138 aimed to use government financial resources more efficiently and to place a greater focus on small-scale borrowers and the basic sectors. NCC formulated and implemented a national microfinance strategy, eliminating overlapping and duplicated credit programs and employing rural banks, credit cooperatives and viable credit NGOs to increase access to financial services by the poor. The Government positively responded to the policy reforms called for by the Project, namely, (i) consolidation of 50% of nonagriculturally-based microcredit programs, (ii) regulation of deposit-taking activities of microfinance institutions, and (iii) removal of the interest rate ceiling for nonagriculturally-based microcredit programs (see para 14). 30. Performance of the Executing Agency. PCFC is a government-owned finance company registered at the Securities and Exchange Commission (SEC). It is supervised by LBP and has a capital of P1 billion, comprising preferred shares of P900 million and common shares of P100 million, wholly owned by NLSF, a national fund operating under the supervision of LBP. PCFC provides wholesale funds to some 200 active MFIs for onlending to poor clients. Its loan portfolio, exclusively for microfinance, amounted to P2.55 billion as of June 2004. This is estimated to be about 50% of the total microfinance loan portfolio in the Philippines, according to the Microfinance Council of the Philippines. PCFC has 96 employees including 38 account officers in charge of its accredited MFI accounts. As of end-2003, PCFC was audited to have total resources of P 2.87 billion, a loan portfolio of P2.46 billion, a net worth of P1.15 billion, total liabilities of P1.65 billion including the ADB and IFAD Loan of P1.35 billion, and a net income after tax of P53 million. It reported a past due rate on loans of 1.55%. 31. PCFC’s performance as the Executing Agency (EA) was highly satisfactory. Its efforts in expanding a panel of conduit MFIs to regulated financial institutions (rural banks, cooperative banks, cooperative rural banks and thrift banks) and qualified new NGOs and cooperatives were highly commendable, and contributed to a greater than targeted outreach to beneficiaries, and to nearly full utilization of the ADB and IFAD Loan. As of 1995, potential GBA Replicators had a total cumulative lending of P119 million or $4.6 million at the exchange rate then prevailing. This was far short of the $34.7 million ADB and IFAD loan for onlending facilities, which indicates the important role played by PCFC as the EA. 32. The established accreditation criteria and rating system for MFIs, and the vigorous marketing, consultative and training activities of PCFC, helped the Philippine microfinance institutions expand towards higher profitability and self-sufficiency during the RMFP implementation period. PCFC accreditation criteria is in Appendix 7. The PCR mission

10

confirmed the strategic importance of microfinance operations for the rural banks, cooperative rural banks and thrift banks that were visited. These institutions regarded microfinance as (i) a profitable banking business, (ii) a way to reach the landless poor and expand their client base, (iii) a means of product bridging to other financial services, and (iv) a contributor to income generation and job creation in regional economies. The combined share of loan disbursement by banking institutions in the RMFP facilities was 61.5%, while the share of NGOs was 23.5%, and that of cooperatives was 13.1%. 33. PCFC also acts as a knowledge center for microfinance best practices. Regular training programs, workshops, and seminars are organized by PCFC for its new and potential MFIs in cooperation with its 7 accredited training centers: training institutes of the Negros Women for Tomorrow Foundation (NWTF), the Center for Agriculture and Rural Development (CARD), Taytay sa Kauswagan, Inc. (TSKI), Producers Rural Bank, People’s Bank of Caraga, Mallig Plains Rural Bank, and Enterprise Bank. Such training programs are in line with PCFC’s marketing strategy for MFI accreditation and strengthening regional forum and network among MFIs. 34. PCFC has supported a modified GBA in response to market needs. Modifications to the GBA were necessary because of the Philippine context, and regional and demographic characteristics of clients. The main features of the modified GBA are as follows:

(i) Limited group liability. Whereas the original GBA was based on the group liability applied to the entire loan period, the modified model limits it to the three past due loan repayments and transfers collection duty to MFI after that point. This relieves group members from an excessive burden of loan repayment in lieu of nonrepayers and helps sustainability of group lending.

(ii) Revised induction training schedule. The original GBA includes 7-day

induction training with a 1-hour class each day. The modified model offers 3-day training with a three-hour class each day, which suits clients’ needs.

(vi) Introduction of an oral test. An oral test at the end of induction training ensures

rules and disciplines of group lending are kept. (vii) Simultaneous disbursement to all five members. Instead of staggered

disbursement (known as 2-2-1), disbursement is made simultaneously to all members. This nurtures a sense of equity among group members and strengthens group solidarity.

(viii) Flexibility in the repayment period. The standard 1-year (52-week) loan

repayment period was modified to an optional 3-month or 6-month period, depending on the borrower’s capacities and funding needs.

(ix) Flexibility in repayment schedule. A modified repayment schedule in response

to a seasonal cash flow pattern suits a micorenterprise activity, e.g. higher levels of repayment are scheduled for the dry season when the rural economy expands.

L. Performance of the Asian Development Bank

35. ADB conducted four loan review missions (excluding the PCR mission) in September 1998, May 2000 (mid-term review), August 2001 and March 2002. ADB also launched a loan

11

disbursement mission in August 2001. The first loan review mission responded to the slow implementation at the early stage of the Project, which stemmed from low recognition of microfinance among banking institutions, the restrictive features of the Project (i.e. the fact that it supported only MFIs that adopted GBA), the multi-step structure of credit facilities, the premature institution of PCFC (it was established in 1995), and the time needed to assess demand for investment and institutional credit of MFIs. The mid-term review mission found and verified the improved overall progress of the Project, confirming Project outreach to the target beneficiaries and provided an action plan for further expansion of GBA to end-borrowers and savings mobilization of MFIs. The last two missions especially recognized the need to accelerate the attached TA activity for installation of developed MIS modules to MFIs and proposed future ADB assistance to further strengthen capacities of MFIs and end-borrowers, and to develop financial products other than GBA. 36. The overall performance of ADB is rated as highly satisfactory, for the adequate monitoring of the progress of the Project and for its response to market needs. ADB workshops and forums on microfinance funded by the attached TA helped disseminate microfinance best practices and sector issues to a broad range of stakeholders.9

III. EVALUATION OF PERFORMANCE

A. Relevance

37. RMFP was highly relevant in helping microfinance intuitions strengthen their capacities to meet the credit needs of the landless poor based on market lending and best operational practices. The inclusion of regulated financial institutions in addition to NGOs and cooperatives and the support for a modified GBA made a positive impact on the project outputs, and contributed to the overall development of the industry by helping banking institutions to become increasingly important players in the microfinance market.10 Participating MFIs have provided microcredit to and mobilized savings from more than the targeted number of microenterprises in all 79 provinces, helping the targeted poor clients sustain self-employment and expand their operations. This has had a positive impact on income generation and employment creation. RMFP promoted the economic interests of women by supporting their livelihood activities. B. Efficacy in Achievement of Purpose

38. Outreach. Participating MFIs benefited 618,906 microenterprises in all 79 provinces during the implementation period. The impact study conducted under the attached TA estimated that 20% of member-respondents were non-poor when they became members, if the sizes of houses and value of assets as of 1998 were used as proxy indicators. 80% was well over the target for poor members. Moreover, a portion of the end-borrowers have successfully expanded their businesses to become eligible for larger livelihood credit or even small enterprise loans. As of 30 June 2002, 68% of the NGOs that accessed RMFP had reached more than 1,000 clients. 45% of the cooperatives, 83% of the cooperative banks and 61% of the rural banks also served

9 From 1998 to 2002, a total of 24 workshops, trainings and conference were conducted, attended by 1,174 MFI

executives, managers and staff. In December 2001, the “GBA Replicator Managers’ Conference” was held at ADB, attended by over 200 participants from 112 MFIs, the Government, donors, universities, cooperative and microfinance federations and other organizations.

10 Under the Microenterprise Access to Banking Services (MABS) program of USAID, 81 rural banks are participating using individual microfinance lending approach, with the following features: repayment are adjusted to a client’s cash flow; customization of loan size; terms and repayment schedule based on client’s needs; flexible loan size; and the use of movable assets and other collateral substitutes. MABS targets a larger client segment than RMFP.

12

more than 1,000 clients. The coverage of PCFC has expanded further since the end of the project implementation period (Table 3).

Table 3. Overview of the Microfinance Sector (as of April 2004) Item Figures Number of clients served by MFIs 1,400,000–1,600,000 Number of clients served by PCFC 1,134,098 Total loan portfolio (P million) 5,000 PCFC loan portfolio (P million) 2,482 Average loan size P4,000 Share against per capita GDP (2003) 7.5%

GDP = gross domestic product, MFI = microfinance institutions, PCFC = People’s Credit Finance Corporation. Source: Microfinance Council of the Philippines, Inc., PCFC.

39. Employment Creation. RMFP helped sustain end-borrowers’ self-employment and expand their operations, which had a limited impact on employment creation. While the need for livelihood activities to employ workers other than household members is small, the survey conducted as part of the impact study showed that 8.2% of the end-borrowers employed an average of 2.8 workers who are not their household members. The number of new jobs created by the Project can be estimated at 142,100. 40. Income Generation. The average income generated by the end-borrowers accounted for 60% of total annual household income according to the impact study survey. The income generated by the microenterprise activities financed by RMFP was mostly spent on the food security of the families, better health and education of children, and major house repairs. 41. Strengthening Microfinance Institutions. RMFP has strengthened the institutional capacity of MFIs to provide cost-efficient microfinance services to the target group by offering investment and institutional credit. MFI staff were trained on GBA best practices through the PCFC training network. As an example of this greater capacity, Card NGO increased its outstanding loans by 27 times and savings by 17 times between 1995 and 2003. During the same period, NWTF expanded its coverage by 5 times; Ahon sa Hirap (ASHI) increased its savings balance by 66 times. Both Producers Rural Bank (with a microcredit portfolio representing 15% of the total loan portfolio) and Cooperative Bank of Bulacan (with a microcredit portfolio representing 25% of the total loan portfolio) have expanded microfinance operations and made them the driving force for their growth. Highlights of selected MFIs accessing RMFP credit facilities are in Table 4. 42. Assisting the Development of a Self-Sustaining Financial System for the Poor. The Project also assisted in the development of a self-sustaining financial system for the rural poor by establishing a nationwide network of GBA Replicators and helping them to become self-sufficient. The financial self-sufficiency of CARD NGO improved from 101.2% in 1998 to 115.0% in 2003, and NWTF from 80.2% to 99.7%. The majority of the MFI respondents to a survey during the impact study demonstrated that microfinance services for the poor could be viable and could become major profit centers. Table 5 gives the overall financial ratios of 25 MFIs assessed to RMFP for 2001.

13

Table 4. Highlights of selected MFIs (as of December 2003) Item

No. of Active Microfinance

Clients

Outstanding Loans

(P million)

Past Due/ Outstanding Loans

(%)

Savings/ Outstanding Loans (%)

CARD NGO 79,745 339.30 3.89 28.20 CARD Bank 33,491 341.90 1.00 72.90 NWTF 48,152 201.60 1.73 43.30 Producers Rural Bank*

45,944 149.80 2.45 25.40

Cooperative Bank of Bulacan*

31,775 101.50 0.50 39.20

Opportunity Microfinance Bank*

24,037 58.90 19.00 80.40

ASHI 11,338 43.05 5.30 68.80 TSKI 107,820 289.44 1.18 48.00 Lamac Cooperative* 1,565 5.10 7.40 76.50 KASAGANA-KA 5,500 14.11 5.50 43.50

ASHI = Ahon sa Hirap, CARD = Center for Agriculture and Rural Development, KASAGANA-KA = Alternative Socio-Economic Program (microcredit), MFI = microfinance institutions, NGO = nongovernemnt organization, NWTF = Negros Women for Tomorrow Foundation, TSKI = Taytay sa Kauswagan, Inc. * Only microfinance operations are indicated as part of their entire operations. Source: PCR mission interviews, PCFC. 43. Improving the Policy Environment for Microfinance Program. RMFP contributed to an improved policy environment for microfinance programs. In response to the policy reform called for by the Project, a President's Executive Order (No. 138, 1999) either terminated or consolidated 78% of microcredit programs by the end of project implementation and directed market-based microenterprise lending.

Table 5: Overall Financial Ratios of 25a MFIs that assessed RMFP (2001) Financial Indicators NGO Cooperative Cooperative Bank Rural Bank Return on Investment 4.5% 5.4% 13.0% 5.4% Operating Cost Ratio 37.8% 23.8% 23.0% 23.8% Operating Self-Sufficiency 109.3% 111.9% 101.0% 111.9% Equity to Total Assets Ratio 41.3% 37.3% 14.0% 37.3% Current Ratio 6.5 2.5 1.15 1.1 MFI = microfinance institutions, NGO = nongovernment organization, RMFP = Rural Microenterprise Finance Project. a The 25 MFIs are composed of 6 NGOs, 3 cooperatives, 10 corporate banks, and 6 rural banks. 23 MFIs provided

financial data for their overall performances. Two rural banks provided financial data specific to their microfinance operations with RMFP funding.

Source: Impact Study under TA2588. 44. Promoting Women in Development. RMFP created opportunities for women subborrowers to enhance their self-worth and dignity. More than 90% of the member respondents of the survey felt able to manage livelihood activities with loans and savings. As major contributors to household income, they feel at par with their husbands. RMFP empowered women, not only in an economic sense, but also psychosocially. Interviews with end-borrowers at group meetings and views expressed at workshops revealed that female entrepreneurs had a positive attitude to conducting their business activities. 45. RMFP is rated as highly efficacious.

14

C. Efficiency in Achievement of Outputs and Purpose

46. The requirement that SOE-2 forms should be submitted from the onset of Project implementation until May 2000 was one of the reasons for the early delay. Together with the Government’s internal processes to transfer the loan proceeds to the imprest account, the SOE-2 requirement increased the annual operational costs of RMFP by P14 million (as estimated by PCFC). Recognizing the impact that the requirement was having, ADB changed the requirement from an SOE-2 to a certificate of subloan release in May 2001. Despite this, the efficiency of RMFP is demonstrated by the fact that it exceeded the targeted number of end-borrowers. RMFP is rated efficient. D. Preliminary Assessment of Sustainability

47. RMFP to participating MFIs considerably strengthened microfinance institutions as a whole, and improved the likelihood of their sustainability in the future. The size of the total loan portfolio under PCFC wholesale lending is estimated to be 50% of the entire microfinance loan portfolio in the Philippines. All 201 participating MFIs have benefited from the long-term investment loan provided by RMFP, which enabled them to conduct profitable microcredit operations, generate savings, and lay the foundation for sustainable operations. The RMFP’s institutional loan helped 125 MFIs strengthen their capacity to conduct successful and sustainable microfinance operations. PCFC also continues to conduct training programs for MFIs in cooperation with its accredited training centers. Such training programs are organized by PCFC and conducted on a commercial basis to promote new MFIs and strengthen institutional and operational capacities of existing MFIs. 48. Meanwhile, RMFP loan repayment from PCFC to LBP, which started in 2002, is already a significant part of PCFC operations, since the loan accounted for 78% of its total liabilities and the loan portfolio accounted for 85% of its total assets as of 31 December 2003. Additional funding is necessary for PCFC to fully realize its potential as the leading microfinance wholesaler. A President's Executive Order (No. 362, September 2004) paved the way for PCFC to have access to the NLSF financial resources. Several donors are investigating the possibility of rendering financial assistance to PCFC. Meanwhile, LBP will start full-scale wholesale microlending operations in 2005 by increasing the number of partner MFIs from the current total of 12. The Development Bank of the Philippines and Small Business Guarantee and Finance Corporation, both of which are Government-owned wholesale lending institutions for SMEs, started to increase microfinance loan portfolios in response to the Barangay Microenterprise and Business Enterprises (BMBE) Act of 2002 (RA 9178).11 With three other government financial institutions entering the microfinance wholesale market, PCFC urgently needs to secure funding resources to retain its competitive and comparative advantage and expand its

11 On 11 February 2003, EO 176 was announced in line with BMBE Act for involvement of Government Financial

Institutions (GFIs) in microcredit operations, which mandated GFIs to set up a special credit window for microenterprises and the promotion of microfinance programs for the poor.

15

operations for sustainable sector development.12 The foundation laid by RMFP for successful microfinance wholesale lending operations will contribute to the sustainability of mirofinance institutions, especially if new financial resources to support PCFC operations as the lead wholesale microfinance institution are forthcoming. The Project’s sustainability is rated as likely. E. Institutional Development and Other Impacts

49. RMFP strengthened Philippine microfinance institutions by providing institutional and investment credit loans and by undertaking the activities under the attached TA. The policy component contributed to the Government taking action to reduce market distortions for sound sector development. It also empowered women nationwide to conduct livelihood activities. F. Environmental, Sociocultural, and Other Impacts

50. As the micorenterprises financed by RMFP operate mainly in the areas of vending, trading, agriculture, food processing, and light manufacturing, no significant adverse environmental impact was identified through project monitoring. RMFP had a positive sociocultural impact on women by financing their livelihood activities. The institutional development and other impacts of RMFP are rated as substantial.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment

51. RMFP had a major impact on the institutional structure of the microfinance industry. It brought formal, regulated small-scale financial institutions into the industry and made it more diverse. Many banking institutions that started microfiannce operations by participating in the Project are expanding their financial services to the poor, which are becoming strategically more important to them. RMFP in a sense broke a barrier to entry into microfinance for many rural banks and other regulated financial institutions. 52. RMF exceeded its goals: (i) 618,906 microenterprises were reached, 106% more than the target, (ii) 97% of the end-borrowers were women, 8% more than the target, (iii) savings mobilized accounted for 36% of total loan proceeds disbursed, 260% more than the target, (iv) the start-up and expansion of 505 MFI branches were supported, 66% more than the target, and (v) 2,505 branch managers were trained, about the same level as the target. Three of the four policy reform outputs were delivered: (i) consolidation of 50% of the nonagriculturally-based micro credit program (78% was consolidated), (ii) regulation of deposit-taking activities of microfinance institutions, and (iii) removal of the interest rate ceiling for nonagriculturally-based microcredit programs. Privatization of PCFC did not materialize, but this output is no longer relevant (para. 15) and the failure to achieve it has not had any impact on project implementation. The attached TA did not achieve part of its target, but it helped to strengthen MFIs’ capacity to conduct successful microfinance operations through training programs and produced a project impact study which gave a comprehensive view of the project impact on the target beneficiaries. RMFP is rated highly successful.

12 While LBP and DBP have extensive networks and wide experience working with countryside financial institutions,

they have little experience in microfinance loans. PCFC’s strengths are established network with over 200 MFIs nationwide and wide experience in operating wholesale lending, while the current constraints to additional funding is the largest operational issue. SBGFC’s strength lies in wide experience in assisting smaller legal businesses to grow, with very little experience in microfinance.

16

B. Lessons Learned

53. The major lessons learned from RMFP are as follows.

(i) Close coordination with a reliable EA and implementing agencies and quick responses to any required changes in loans conditions and MFI accreditation are keys to success. ADB’s interaction with PCFC to modify the loan conditions in response to market needs significantly enhanced project implementation.

(ii) A simple loan structure and minimum reporting requirements would minimize

operational costs. In future, ADB loans could be lent directly to LDP (as for the World Bank Countryside Loan Facility, which provides funding for onlending over the limit of RMFP, channeled through PCFC). The early delays in implementation could have been eased if the SOE-2 form were not required. A large amount of end-borrowers’ information does not help in effective project monitoring, which largely relies on field verification conducted by PCFC and ADB missions.

(iii) RMFP offered a uniform lending rate of 12% per annum to any accredited MFI.

However, a more flexible means of setting interest rates to reflect the credit standing of individual MFIs may have to be considered. This would keep the RMFP investment credit facility attractive to those MFIs that have a higher credit status and access to alternative funding sources.

(iv) MIS development should take a tailor-made approach to the needs of individual

MFIs, rather than providing a generic model which does not reflect the diversity of types of operations, the size of the institution, its operational focus, its geographic location and the local market demand.

C. Recommendations

54. Project-specific and general recommendations that may affect microfinance projects or programs are as follows.

1. Project-Related

55. Future Monitoring. Rigorous mission reviews and timely impact studies on sample cases are more effective at assessing project impacts than monitoring every subloan through detailed reporting requirements which provide a huge amount of data on end-borrowers but cannot be verified without field missions. 56. Covenants. The clause for PCFC privatization was not relevant. Under the current Philippine conditions, in order to provide commercial funding resources at the retail level, a concessionary loan is still needed at the wholesale level, given that less than 100% of the industry is financially self-sufficient and 30-40% of savings mobilization. Privatization would substantially limit the opportunity for wholesale funding institutions to have access to concessionary loans, and may make such access impossible. 57. Design of the Project. The diversity of participating institutions and the different types of products need to be considered in future microfinance projects in order to meet client needs and expand outreach.

17

58. Additional Assistance. Following a successful outcome of RMFP, possible areas of future ADB assistance are set forth below.

(i) Strengthening the Regulatory Framework for Microfinance Institutions. Despite the fiduciary duty involved in de facto savings mobilization, NGOs and cooperatives are not properly regulated. SEC and the Cooperative Development Agency (CDA) would benefit from assistance to strengthen their supervisory capacity. An NCC performance standard applicable to MFIs could be applied to savings mobilization by NGOs and cooperatives. Despite the fact that they conduct the same microfinance operations, banks are subject to gross receipt tax and corporate income tax, but NGOs and cooperatives are not. This needs to be addressed, and incentives to marginalized local operations to compensate them for higher operational costs need to be considered.

(ii) Institutional building of MFIs. MFIs’ capacity to reach the unserved poor can

be strengthened, perhaps in collaboration with the People’s Development Trust Fund (PDTF), which is mandated to build institutional capacities of microfinance institutions. Support may be given for some of the larger NGOs to upgrade themselves to become banks so they can mobilize more savings and offer a wider variety of financial products. Products such as the Association of Social Advancement (ASA) model (a standardized lending model based on individual liability), and financing of larger microenterprises with larger loans can be supported.

(iii) Addressing credit pollution. In some areas where there is a high competition,

MFIs increasingly suffer from duplication of end-borrowers. Credit pollution can be minimized through support for a mutual credit information sharing system, perhaps with credit bureaus, provided the costs do not reduce the efficiency of MFIs.

(iv) Meeting unmet demand for microfinance. The current coverage of

microfinance services is estimated to be from 1.4 million to 1.6 million. Given that the total number of poor households is estimated to be 5.2 million, further concessionary funding resources from donors to microfinance wholesalers will be needed because the overall financial self-sufficiency of the industry falls short of 100%. Furthermore, microsavings are still at low levels (30-40% of outstanding loans). Assistance to equity and/or second-tier capital to augment the bank capital base can leverage financial resources in expanding microfinance operations. Investment in equities or subordinated loans of microfinance banks through ADB private sector operations can be considered.

59. Timing of the Project Performance Audit Report (PPAR). In order to effectively capture the impact of the Project, the PPAR can be prepared later than 2006 with an assessment to guide the future development of the microfinance industry.

2. General

60. Future microenterprise credit facilities should be simplified as much as possible in order to minimize operational costs and help MFIs to move towards full financial self-sufficiency. It would be helpful if PCFC could borrow directly from donor institutions, with the sovereign guarantee, which is currently being discussed. Monitoring requirements should also be

18

restricted to securing basic data, as the status of project implementation and its impact on beneficiaries can be obtained more efficiently by field verification.

Appendix 1 19

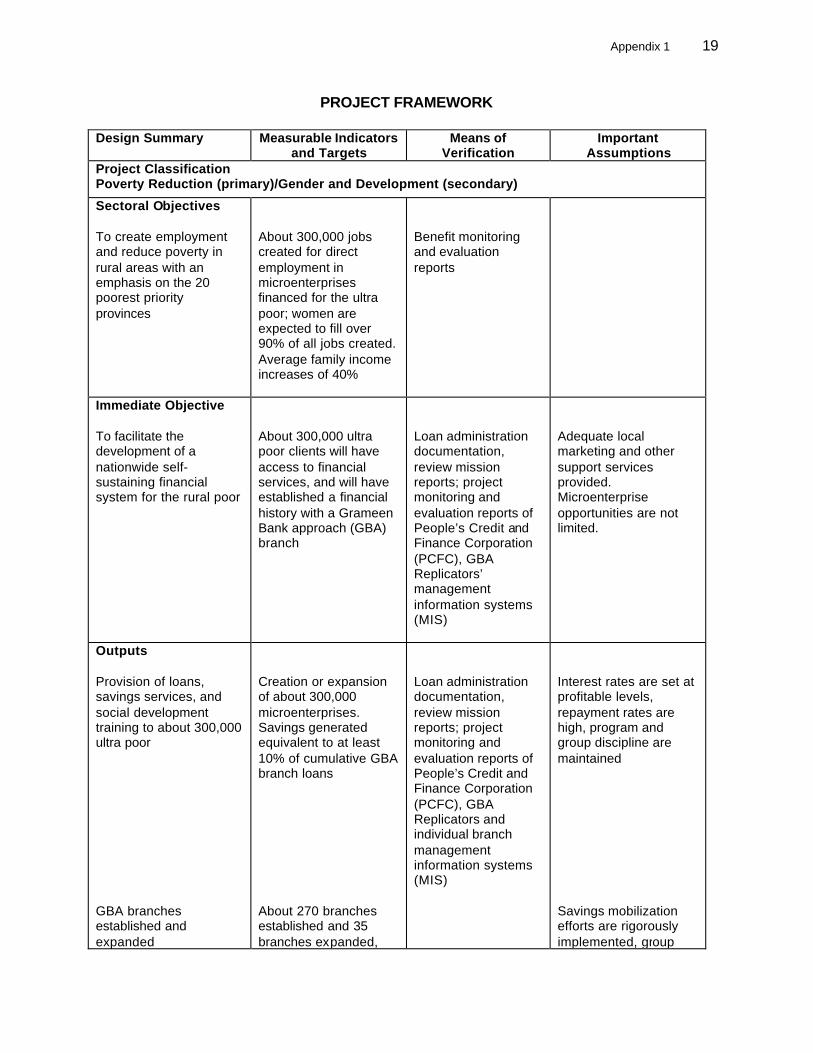

PROJECT FRAMEWORK Design Summary Measurable Indicators

and Targets Means of

Verification Important

Assumptions Project Classification Poverty Reduction (primary)/Gender and Development (secondary)

Sectoral Objectives To create employment and reduce poverty in rural areas with an emphasis on the 20 poorest priority provinces

About 300,000 jobs created for direct employment in microenterprises financed for the ultra poor; women are expected to fill over 90% of all jobs created. Average family income increases of 40%

Benefit monitoring and evaluation reports

Immediate Objective To facilitate the development of a nationwide self-sustaining financial system for the rural poor

About 300,000 ultra poor clients will have access to financial services, and will have established a financial history with a Grameen Bank approach (GBA) branch

Loan administration documentation, review mission reports; project monitoring and evaluation reports of People’s Credit and Finance Corporation (PCFC), GBA Replicators’ management information systems (MIS)

Adequate local marketing and other support services provided. Microenterprise opportunities are not limited.

Outputs Provision of loans, savings services, and social development training to about 300,000 ultra poor GBA branches established and expanded

Creation or expansion of about 300,000 microenterprises. Savings generated equivalent to at least 10% of cumulative GBA branch loans About 270 branches established and 35 branches expanded,

Loan administration documentation, review mission reports; project monitoring and evaluation reports of People’s Credit and Finance Corporation (PCFC), GBA Replicators and individual branch management information systems (MIS)

Interest rates are set at profitable levels, repayment rates are high, program and group discipline are maintained Savings mobilization efforts are rigorously implemented, group

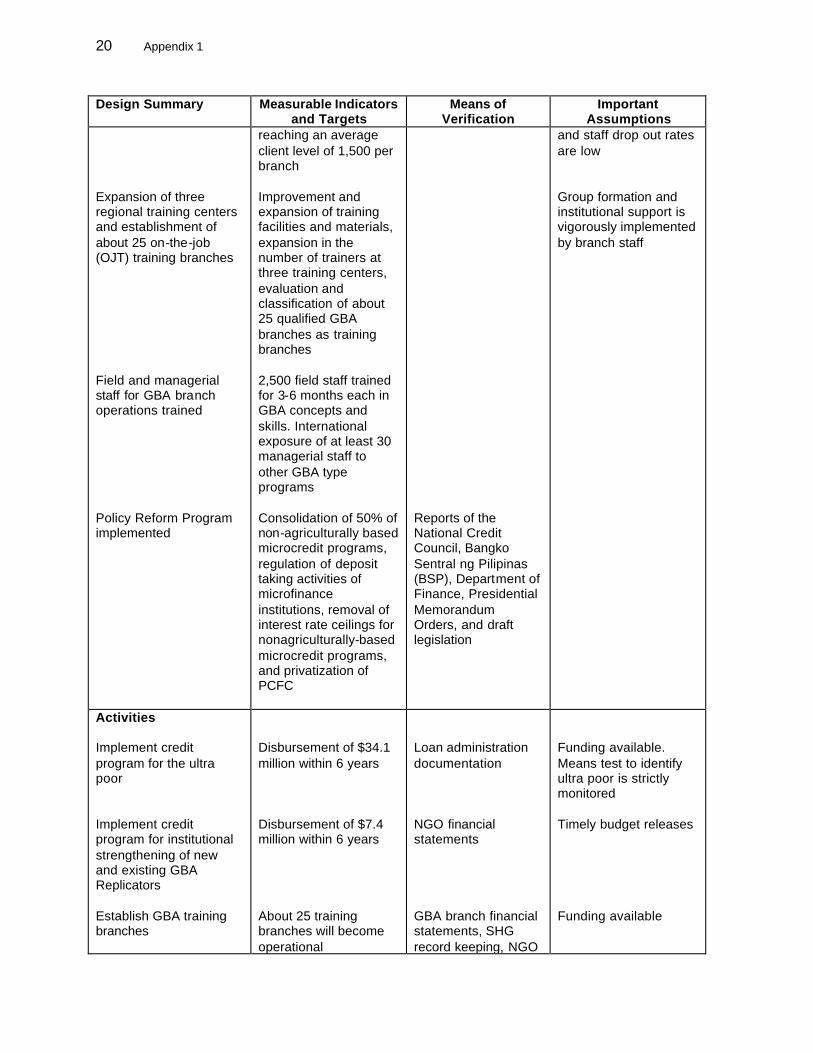

20 Appendix 1

Design Summary Measurable Indicators and Targets

Means of Verification

Important Assumptions

Expansion of three regional training centers and establishment of about 25 on-the-job (OJT) training branches Field and managerial staff for GBA branch operations trained Policy Reform Program implemented

reaching an average client level of 1,500 per branch Improvement and expansion of training facilities and materials, expansion in the number of trainers at three training centers, evaluation and classification of about 25 qualified GBA branches as training branches 2,500 field staff trained for 3-6 months each in GBA concepts and skills. International exposure of at least 30 managerial staff to other GBA type programs Consolidation of 50% of non-agriculturally based microcredit programs, regulation of deposit taking activities of microfinance institutions, removal of interest rate ceilings for nonagriculturally-based microcredit programs, and privatization of PCFC

Reports of the National Credit Council, Bangko Sentral ng Pilipinas (BSP), Department of Finance, Presidential Memorandum Orders, and draft legislation

and staff drop out rates are low Group formation and institutional support is vigorously implemented by branch staff

Activities Implement credit program for the ultra poor Implement credit program for institutional strengthening of new and existing GBA Replicators Establish GBA training branches

Disbursement of $34.1 million within 6 years Disbursement of $7.4 million within 6 years About 25 training branches will become operational

Loan administration documentation NGO financial statements GBA branch financial statements, SHG record keeping, NGO

Funding available. Means test to identify ultra poor is strictly monitored Timely budget releases Funding available

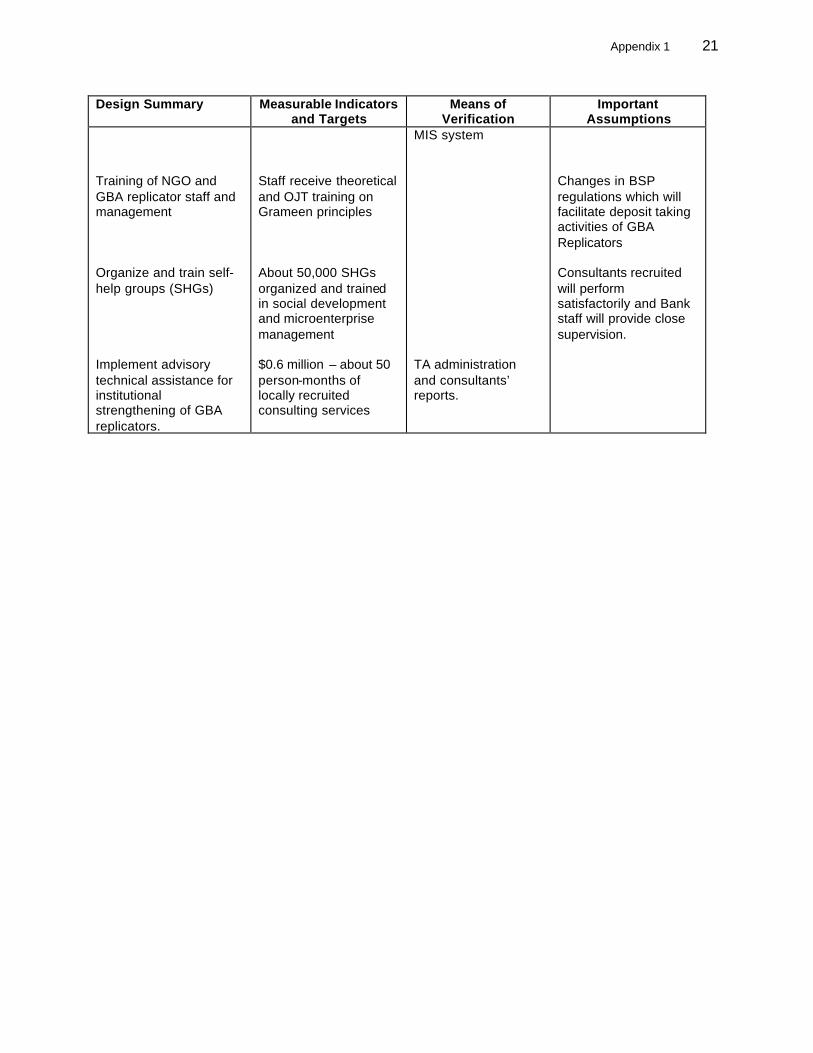

Appendix 1 21

Design Summary Measurable Indicators and Targets

Means of Verification

Important Assumptions

Training of NGO and GBA replicator staff and management Organize and train self-help groups (SHGs) Implement advisory technical assistance for institutional strengthening of GBA replicators.

Staff receive theoretical and OJT training on Grameen principles About 50,000 SHGs organized and trained in social development and microenterprise management $0.6 million – about 50 person-months of locally recruited consulting services

MIS system TA administration and consultants’ reports.

Changes in BSP regulations which will facilitate deposit taking activities of GBA Replicators Consultants recruited will perform satisfactorily and Bank staff will provide close supervision.

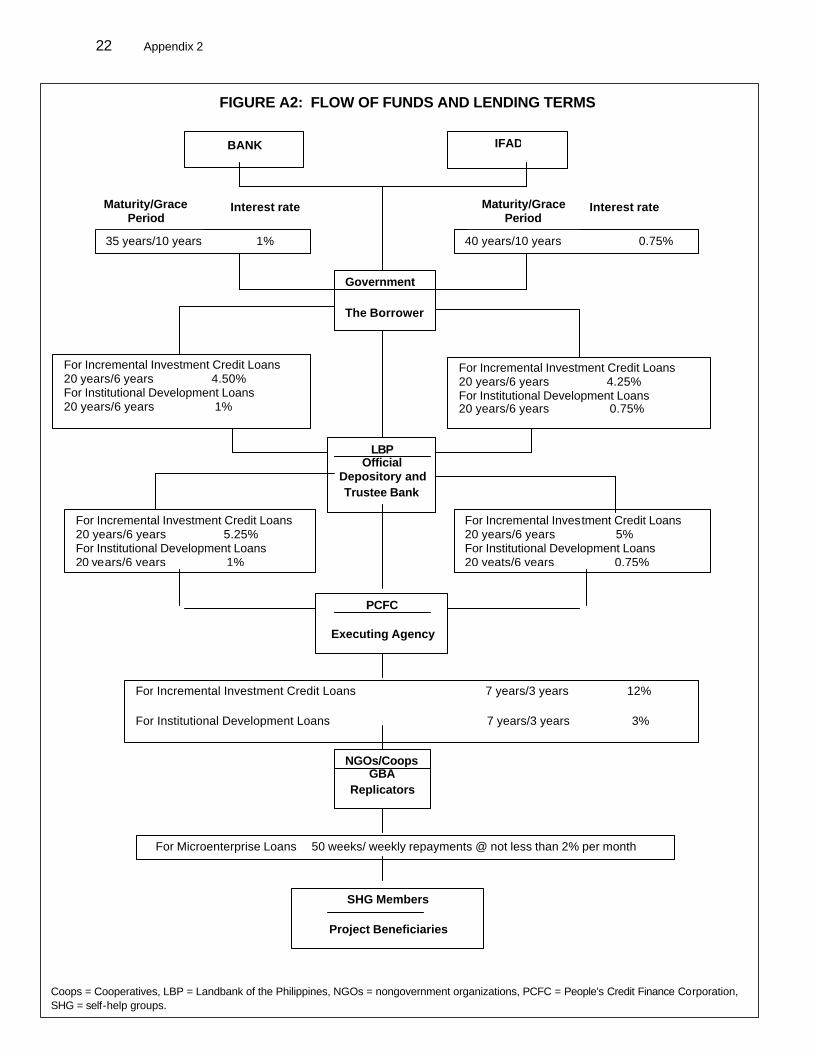

22 Appendix 2

FIGURE A2: FLOW OF FUNDS AND LENDING TERMS

BANK IFAD

35 years/10 years 1% 40 years/10 years 0.75%

Government

The Borrower

For Incremental Investment Credit Loans 20 years/6 years 4.50% For Institutional Development Loans 20 years/6 years 1%

For Incremental Investment Credit Loans 20 years/6 years 4.25% For Institutional Development Loans 20 years/6 years 0.75%

LBP Official

Depository and Trustee Bank

For Incremental Investment Credit Loans 20 years/6 years 5.25% For Institutional Development Loans 20 years/6 years 1%

For Incremental Investment Credit Loans 20 years/6 years 5% For Institutional Development Loans 20 yeats/6 years 0.75%

PCFC

Executing Agency

For Incremental Investment Credit Loans 7 years/3 years 12% For Institutional Development Loans 7 years/3 years 3%

For Microenterprise Loans 50 weeks/ weekly repayments @ not less than 2% per month

NGOs/Coops GBA

Replicators

Maturity/Grace Period

Maturity/Grace Period

Interest rate Interest rate

SHG Members

Project Beneficiaries

Coops = Cooperatives, LBP = Landbank of the Philippines, NGOs = nongovernment organizations, PCFC = People’s Credit Finance Corporation, SHG = self-help groups.

Appendix 3 23

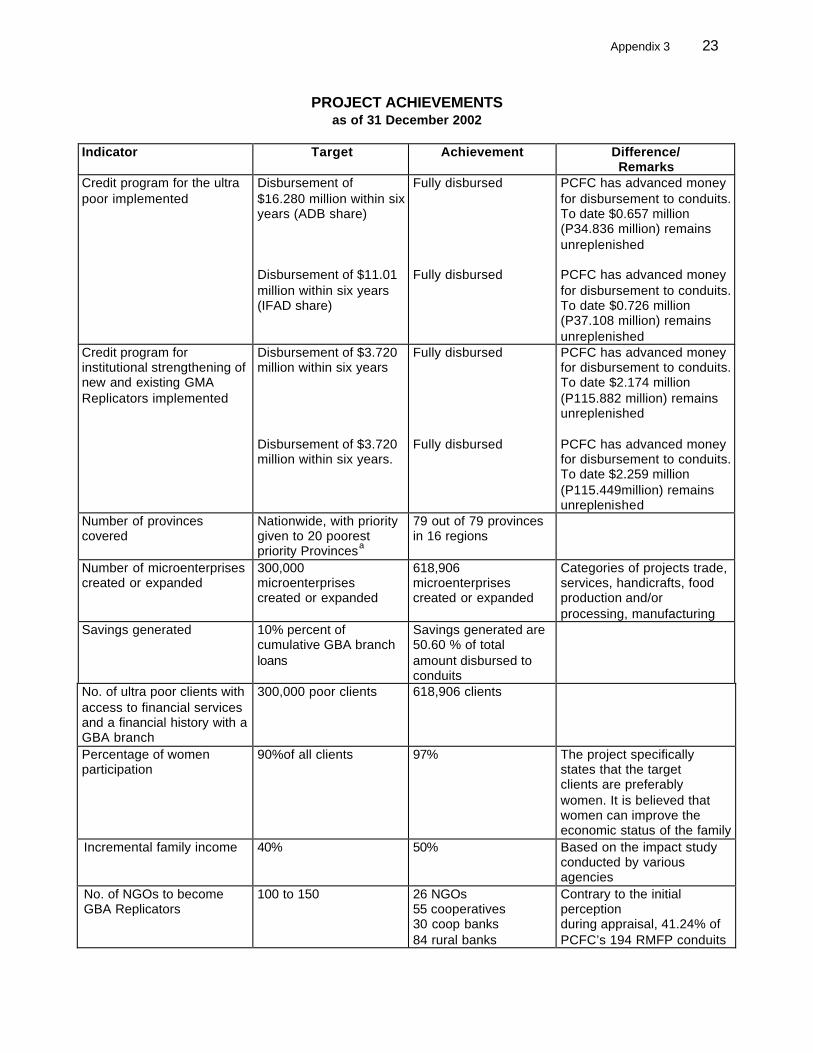

PROJECT ACHIEVEMENTS as of 31 December 2002

Indicator Target Achievement Difference/

Remarks Credit program for the ultra poor implemented

Disbursement of $16.280 million within six years (ADB share) Disbursement of $11.01 million within six years (IFAD share)

Fully disbursed Fully disbursed

PCFC has advanced money for disbursement to conduits. To date $0.657 million (P34.836 million) remains unreplenished PCFC has advanced money for disbursement to conduits. To date $0.726 million (P37.108 million) remains unreplenished

Credit program for institutional strengthening of new and existing GMA Replicators implemented

Disbursement of $3.720 million within six years Disbursement of $3.720 million within six years.

Fully disbursed Fully disbursed

PCFC has advanced money for disbursement to conduits. To date $2.174 million (P115.882 million) remains unreplenished PCFC has advanced money for disbursement to conduits. To date $2.259 million (P115.449million) remains unreplenished

Number of provinces covered

Nationwide, with priority given to 20 poorest priority Provincesa

79 out of 79 provinces in 16 regions

Number of microenterprises created or expanded

300,000 microenterprises created or expanded

618,906 microenterprises created or expanded

Categories of projects trade, services, handicrafts, food production and/or processing, manufacturing

Savings generated

10% percent of cumulative GBA branch loans

Savings generated are 50.60 % of total amount disbursed to conduits

No. of ultra poor clients with access to financial services and a financial history with a GBA branch

300,000 poor clients 618,906 clients

Percentage of women participation

90%of all clients 97% The project specifically states that the target clients are preferably women. It is believed that women can improve the economic status of the family

Incremental family income 40% 50%

Based on the impact study conducted by various agencies

No. of NGOs to become GBA Replicators

100 to 150 26 NGOs 55 cooperatives 30 coop banks 84 rural banks

Contrary to the initial perception during appraisal, 41.24% of PCFC’s 194 RMFP conduits

24 Appendix 3

Indicator Target Achievement Difference/ Remarks

2 lending investor 3 thrift bank 1 development bank

are private financial institutions

No. of branches (or viable village level financial institutions) established/expanded

305 branches 505 (including 57 branches of the inactive conduits)

Average number of clients served per branch

1,500 clients per branch 1,750 clients per branch (350 clients per PO x 5 PO in an average branch)

No. of self-help groups organized and trained

50,000 SHG organized and trained

128,790 SHG organized and trained

Regional training centers expanded

3 4 identified training centers (Negros Women for Tomorrow Foundation and Center for Agriculture and Rural Dev’t and Mallig Plains Rural Bank, Inc., Enterprise Bank, Inc., People’s Bank of Caraga)

The criteria for the selection of qualified training centers and the minimum training requirement for RMFP were defined by the Project’s Training Coordinating Committee (TCC); the TCC is composed of mature GBA Replicators Additional TCC training centers are being considered

No. of managers and field staff of participating Replicators trained at a TCC-accredited training center

2,500 15. 2,505

No. of managerial staff sent for international exposure to other GBA-type programs

30 8

Appropriation for the exposure trips was reallocated for Microcredit World Summit

Policy reform program implemented, including the consolidation of non-agriculturally based microcredit programs.

Reflected in the loan and project covenants

Complied with Appendix “b.2” provides details of status of compliance with loan and project covenants

Implementation of Technical Assistance for institutional strengthening of GBA Replicators by a group of locally-recruited consultants

$600,000 60 pm

$477.500 60 pm

ADB = Asian Development Bank, GBA= Grameen Bank Approach, IFAD = International Fund for Agricultural Development, PCFC = People’s Credit Finance Corporation, Rural Microenterprise Finance Project, TCC = Training Coordinating Committee a Identified by the Government’s Social Reform Agenda for accelerated countryside development. Source: PCFC

Appendix 4 25

PROJECTED VERSUAS ACTUAL DISBURSEMENT

0

100

200

300

400

500

600

700

1996 1997 1998 1999 2000 2001 2002

Years

P (

in m

illio

ns)

Projected Disbursement Actual Disbursement

26 Appendix 5

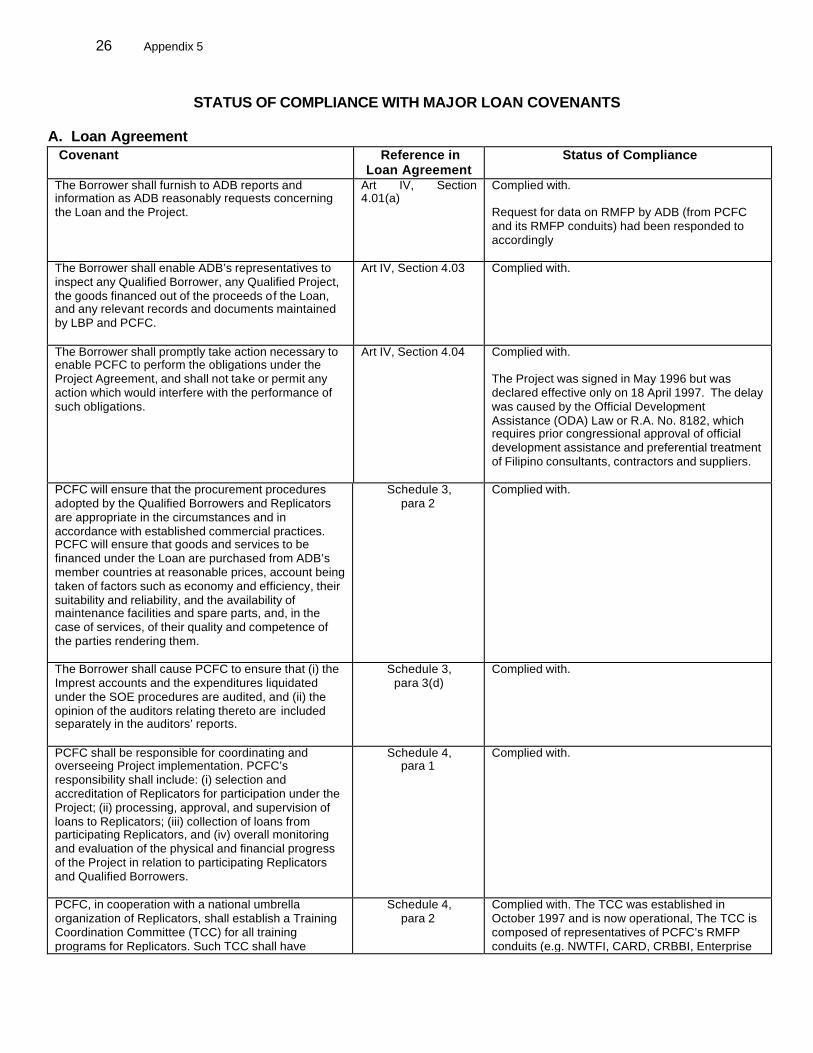

STATUS OF COMPLIANCE WITH MAJOR LOAN COVENANTS

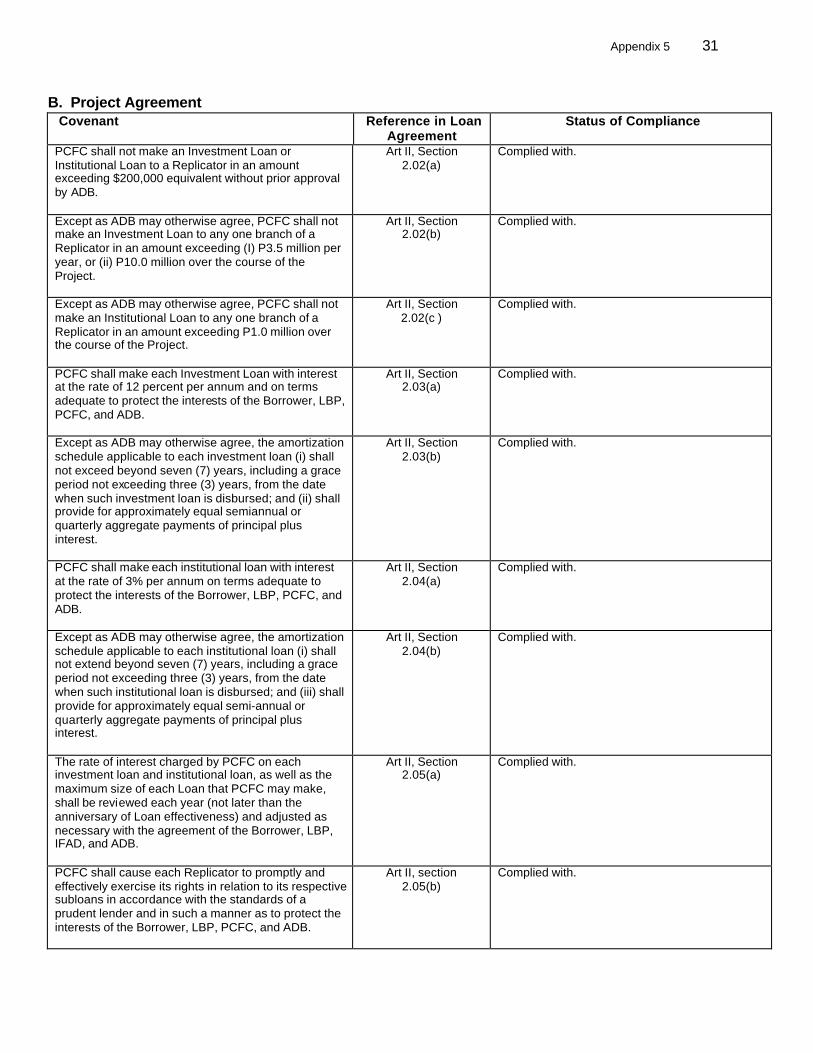

A. Loan Agreement Covenant Reference in

Loan Agreement Status of Compliance

The Borrower shall furnish to ADB reports and information as ADB reasonably requests concerning the Loan and the Project.

Art IV, Section 4.01(a)

Complied with. Request for data on RMFP by ADB (from PCFC and its RMFP conduits) had been responded to accordingly

The Borrower shall enable ADB’s representatives to inspect any Qualified Borrower, any Qualified Project, the goods financed out of the proceeds of the Loan, and any relevant records and documents maintained by LBP and PCFC.

Art IV, Section 4.03 Complied with.

The Borrower shall promptly take action necessary to enable PCFC to perform the obligations under the Project Agreement, and shall not take or permit any action which would interfere with the performance of such obligations.

Art IV, Section 4.04 Complied with. The Project was signed in May 1996 but was declared effective only on 18 April 1997. The delay was caused by the Official Development Assistance (ODA) Law or R.A. No. 8182, which requires prior congressional approval of official development assistance and preferential treatment of Filipino consultants, contractors and suppliers.

PCFC will ensure that the procurement procedures adopted by the Qualified Borrowers and Replicators are appropriate in the circumstances and in accordance with established commercial practices. PCFC will ensure that goods and services to be financed under the Loan are purchased from ADB’s member countries at reasonable prices, account being taken of factors such as economy and efficiency, their suitability and reliability, and the availability of maintenance facilities and spare parts, and, in the case of services, of their quality and competence of the parties rendering them.

Schedule 3, para 2

Complied with.

The Borrower shall cause PCFC to ensure that (i) the Imprest accounts and the expenditures liquidated under the SOE procedures are audited, and (ii) the opinion of the auditors relating thereto are included separately in the auditors’ reports.

Schedule 3, para 3(d)

Complied with.

PCFC shall be responsible for coordinating and overseeing Project implementation. PCFC’s responsibility shall include: (i) selection and accreditation of Replicators for participation under the Project; (ii) processing, approval, and supervision of loans to Replicators; (iii) collection of loans from participating Replicators, and (iv) overall monitoring and evaluation of the physical and financial progress of the Project in relation to participating Replicators and Qualified Borrowers.

Schedule 4, para 1

Complied with.

PCFC, in cooperation with a national umbrella organization of Replicators, shall establish a Training Coordination Committee (TCC) for all training programs for Replicators. Such TCC shall have adequate full-time staff from PCFC and the national

Schedule 4, para 2

Complied with. The TCC was established in October 1997 and is now operational, The TCC is composed of representatives of PCFC’s RMFP conduits (e.g. NWTFI, CARD, CRBBI, Enterprise Bank and Mallig Plains Rural Bank).

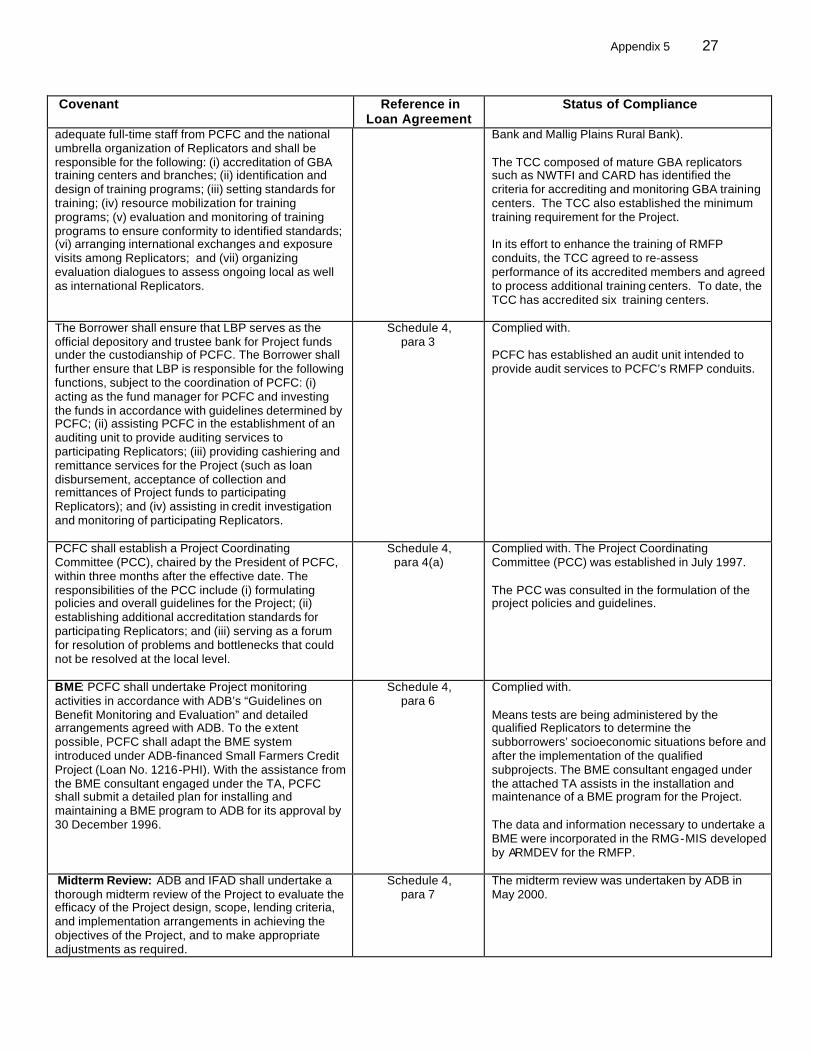

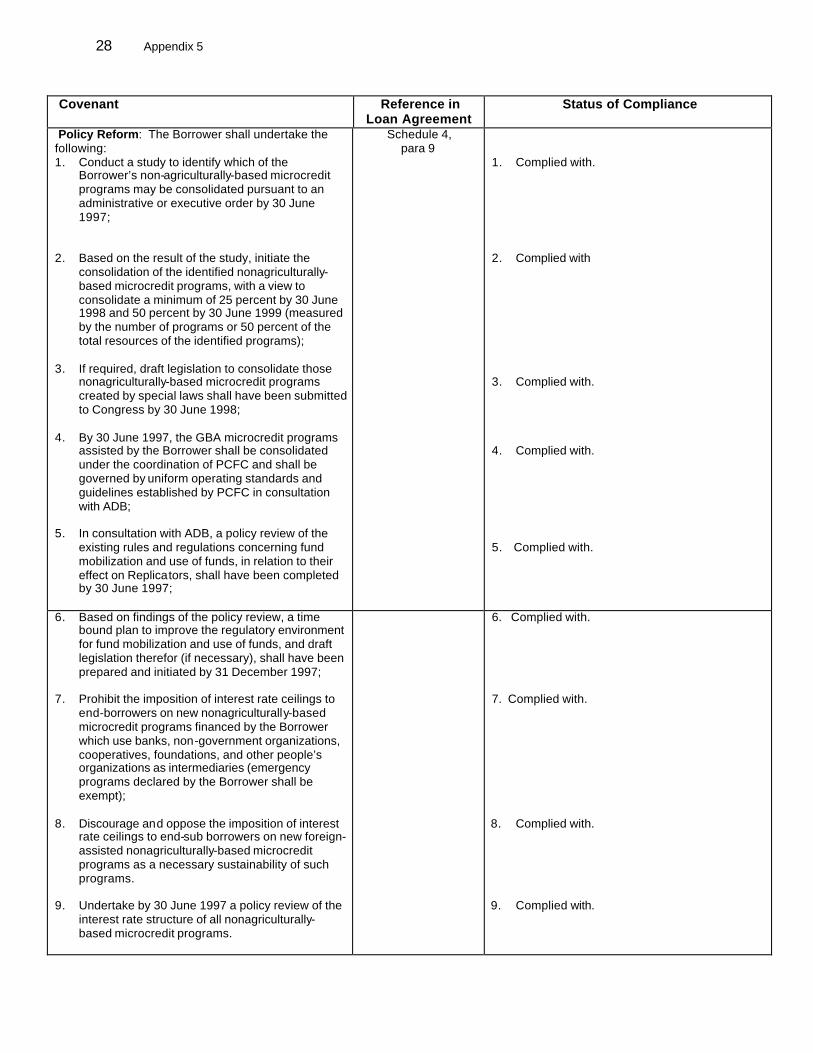

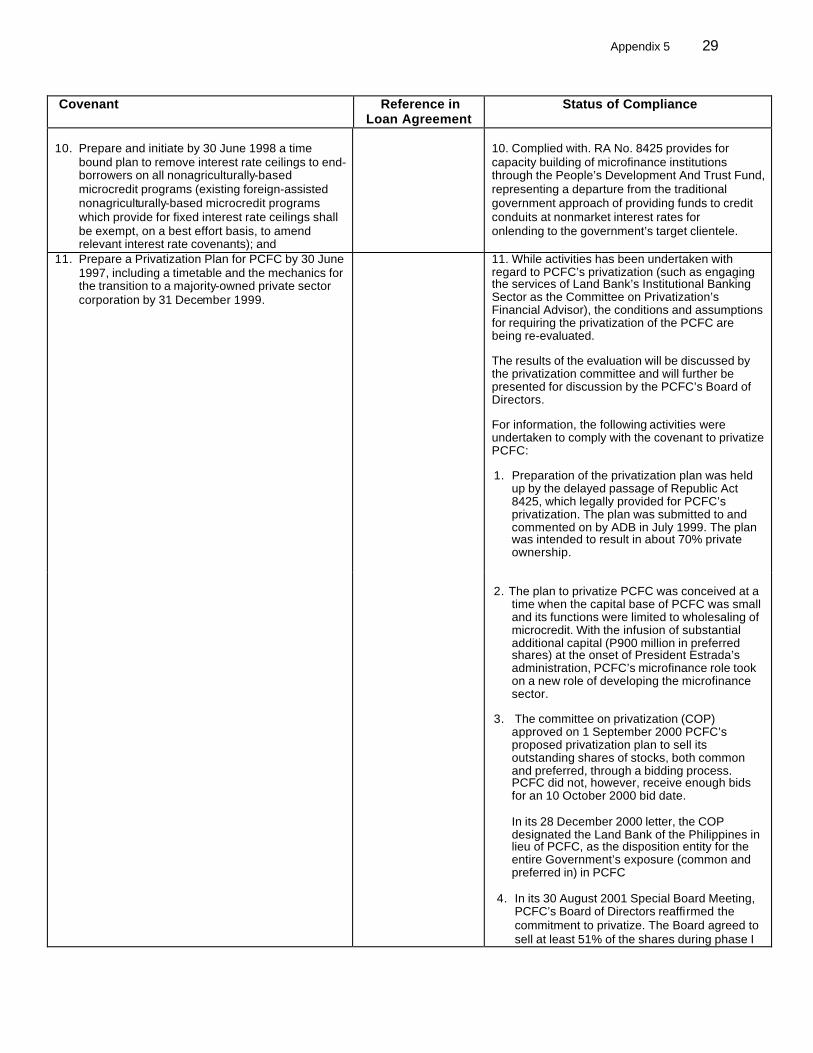

Appendix 5 27

Covenant Reference in Loan Agreement

Status of Compliance