Embed Size (px)

Citation preview

RTR Telecom Monitor4th Qua r t e r 2 0 0 9

Data up to June 2009

PREFACE 2

SECTION 1

Fixed-link network 3

SECTION 2

Leased lines 14

SECTION 3

Mobile communications 18

SECTION 4

Comparisons of fixed-link 28

and mobile networks

SECTION 5

Broadband 31

SECTION 6

Business indicators 39

SECTION 7

Appendix 42

Publishing information: Owner, publisher, producer and editor: Austrian RegulatoryAuthority for Broadcasting and Telecommunications (RTR-GmbH), MariahilferStrasse 77-79, A-1060 Vienna, Austria. Tel.: +43 (0)1 58058-0, Fax: +43 (0)1 58058-9191,e-mail: [email protected], http://www.rtr.at. Company Register No. (FN) 208312t – publishedand produced in Vienna, Austria.

PREFACE 2

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Preface

Dear Readers,

This section provides information about how the data for the Telecom Monitor is collected and aboutthe basis for data collection and statistical analyses.

Communications Survey Ordinance (KEV)

Under the Communications Survey Ordinance (KEV, Federal Law Gazette II No. 365/2004), which wentinto effect on October 10, 2004, the Austrian Regulatory Authority for Broadcasting and Telecommuni -cations (RTR) is required to carry out statistical surveys and data analyses on a quarterly basis. Thedata collected is to be made available to the public in such a way that information on specific compa-nies can not be deduced. The ordinance essentially pursues two objectives: First, the quarterly collection and publication of keymarket indicators is meant to increase the efficiency of RTR's monitoring process in order to maintainthe authority's transparent, forward-looking and competition-oriented regulatory approach for allmarket participants (companies and consumers) as a means of promoting and ensuring growth,investment and innovation in the sector. Second, these activities serve to inform the interested publicabout the development of the telecommunications markets with current market data. In addition, RTRmakes the KEV data available to Statistics Austria.

Data collection

In order to minimize expenses for the operators, RTR has defined the sample based on Art. 4 Par. 1KEV in such a way that, on the basis of the overall population from the most recent market analyses,a minimum market share of 90% is covered in each cluster (fixed-link, mobile communications, leasedlines and broadband), thus ensuring a representative view of the market situation. RTR then uses thissample as a basis for extrapolation regarding the overall population.

Statistical evaluations and data values

In line with its publishing obligation under Art. 7 Par. 2 KEV, RTR reports the statistics explicitlymentioned in that provision separately for the fixed-link network, mobile communications, leasedlines and broadband using a cluster approach. Due to occasional post-hoc data corrections, the valuesin the charts presented here may differ slightly from the information provided in earlier issues of theTelecom Monitor. Where major deviations (> 5%) arise in individual data values, a comment to thiseffect is provided for the figure in question.

The RTR Team

3

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 1 Fixed-link network

SECTION 1 I FIXED-LINK NETWORK 4

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Fixed-link penetration (households) n Fixed-link penetration (businesses)

0%

50%

100%

150%

200%

250%

300%

Q12007

Q22007

60%

240%

59%

241%

Q32006

63%

240%

Q42006

62%

239%

Q32007

Q42007

58%

240%

57%

238%

Q12008

58%

222%

Q22008

57%

221%

Q32008

57%

220%

Q42008

57%

222%

Q12009

58%

208%

Q22009

57%

207%

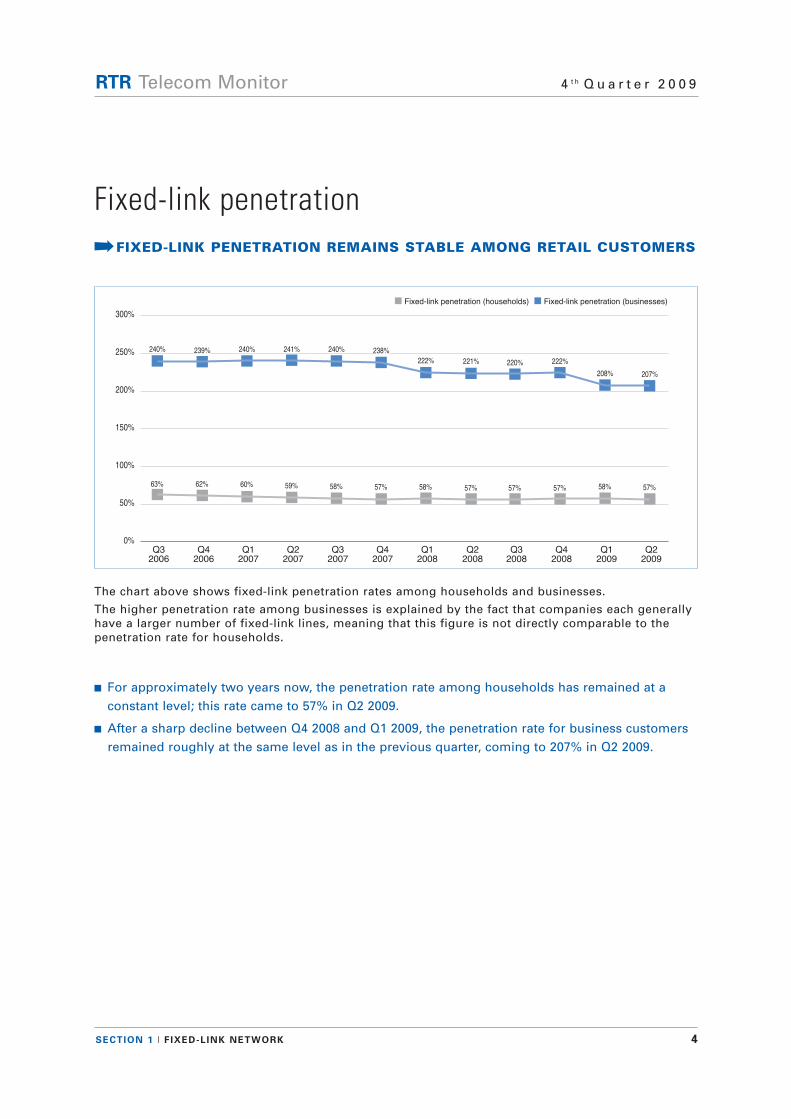

The chart above shows fixed-link penetration rates among households and businesses.

The higher penetration rate among businesses is explained by the fact that companies each generallyhave a larger number of fixed-link lines, meaning that this figure is not directly comparable to thepenetration rate for households.

n For approximately two years now, the penetration rate among households has remained at a constant level; this rate came to 57% in Q2 2009.

n After a sharp decline between Q4 2008 and Q1 2009, the penetration rate for business customers remained roughly at the same level as in the previous quarter, coming to 207% in Q2 2009.

Fixed-link penetration·FIXED-LINK PENETRATION REMAINS STABLE AMONG RETAIL CUSTOMERS

SECTION 1 I FIXED-LINK NETWORK 5

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Retail revenues from access services (residential customers) n Retail revenues from access services (business customers)

€ 0

€ 20,000

€ 40,000

€ 60,000

€ 80,000

€ 100,000

€ 120,000

Q12007

91,700

51,7

00

Q22007

89,200

51,5

00

Q32006

96,600

50,1

00

Rev

enue

s (t

hous

ands

)

Q42006

95,300

50,0

00

Q32007

86,400

51,0

00

Q42007

83,600

51,4

00

Q12008

86,400

49,5

00

Q22008

83,900

49,3

00

Q32008

82,000

48,8

00

Q42008

80,300

48,1

00

Q12009

83,500

45,9

00

Q22009

82,200

45,4

00

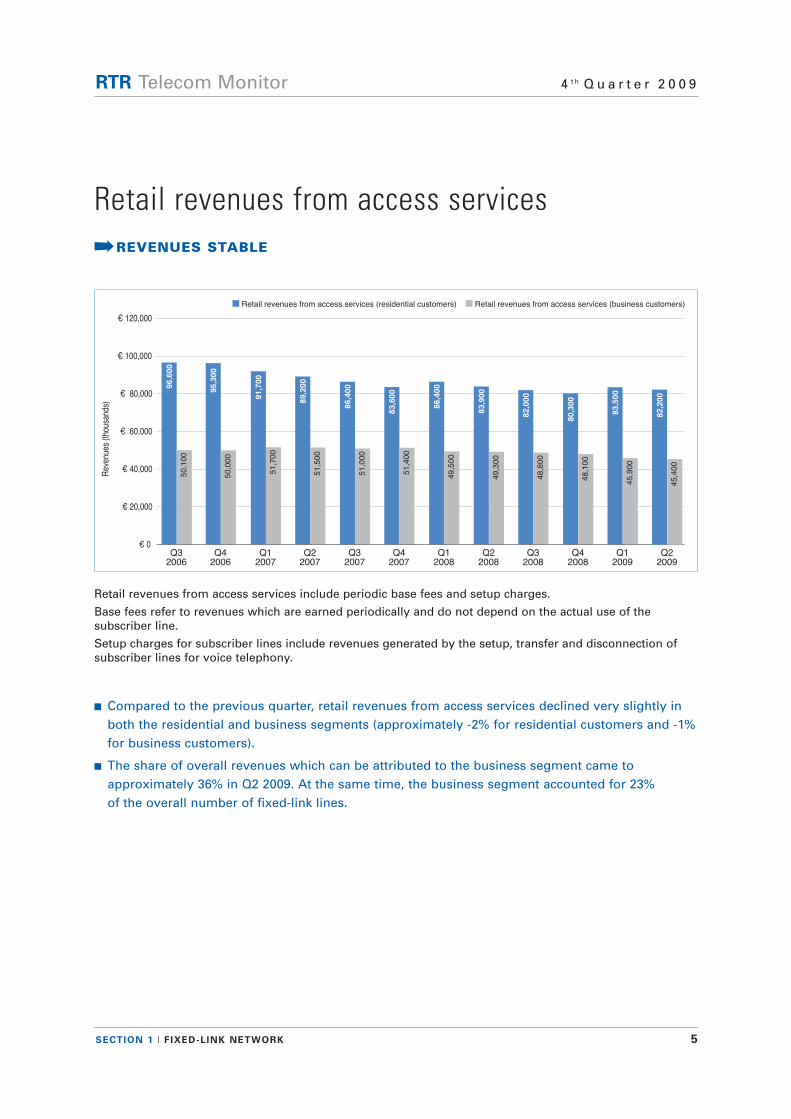

Retail revenues from access services include periodic base fees and setup charges.

Base fees refer to revenues which are earned periodically and do not depend on the actual use of the subscriber line.

Setup charges for subscriber lines include revenues generated by the setup, transfer and disconnection ofsubscriber lines for voice telephony.

n Compared to the previous quarter, retail revenues from access services declined very slightly in both the residential and business segments (approximately -2% for residential customers and -1%for business customers).

n The share of overall revenues which can be attributed to the business segment came to approximately 36% in Q2 2009. At the same time, the business segment accounted for 23% of the overall number of fixed-link lines.

Retail revenues from access services·REVENUES STABLE

SECTION 1 I FIXED-LINK NETWORK 6

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

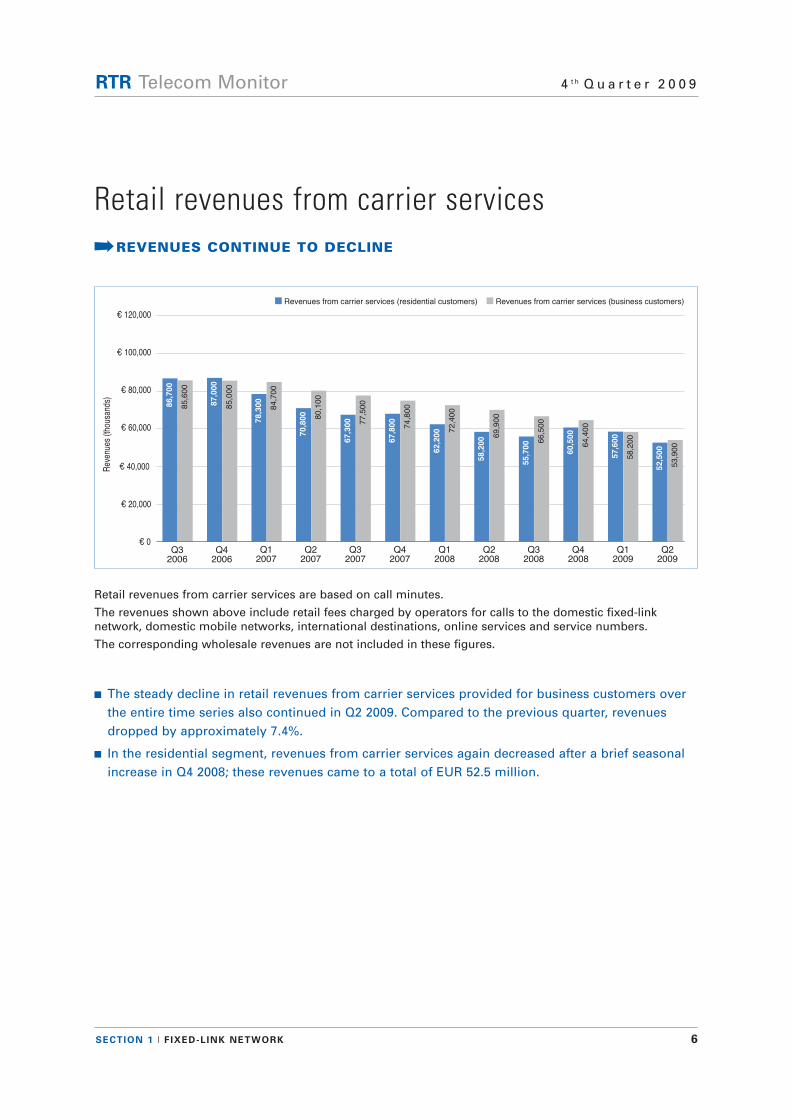

n Revenues from carrier services (residential customers) n Revenues from carrier services (business customers)

€ 0Q1

2007

78,300

84,7

00

Q22007

70,800 80,1

00

€ 20,000

€ 40,000

€ 60,000

€ 80,000

€ 100,000

€ 120,000

Rev

enue

s (t

hous

ands

)

Q32006

86,700

85,6

00

Q42006

87,000

85,0

00

Q32007

67,300 77,5

00

Q42007

67,800

74,8

00

Q12008

62,200 7

2,4

00

Q22008

58,200 6

9,9

00

Q32008

55,700 6

6,5

00

Q42008

60,500

64,4

00

Q12009

57,600

58,2

00

Q22009

52,500

53,9

00

Retail revenues from carrier services are based on call minutes.

The revenues shown above include retail fees charged by operators for calls to the domestic fixed-link network, domestic mobile networks, international destinations, online services and service numbers.

The corresponding wholesale revenues are not included in these figures.

n The steady decline in retail revenues from carrier services provided for business customers over the entire time series also continued in Q2 2009. Compared to the previous quarter, revenues dropped by approximately 7.4%.

n In the residential segment, revenues from carrier services again decreased after a brief seasonal increase in Q4 2008; these revenues came to a total of EUR 52.5 million.

Retail revenues from carrier services·REVENUES CONTINUE TO DECLINE

SECTION 1 I FIXED-LINK NETWORK 7

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

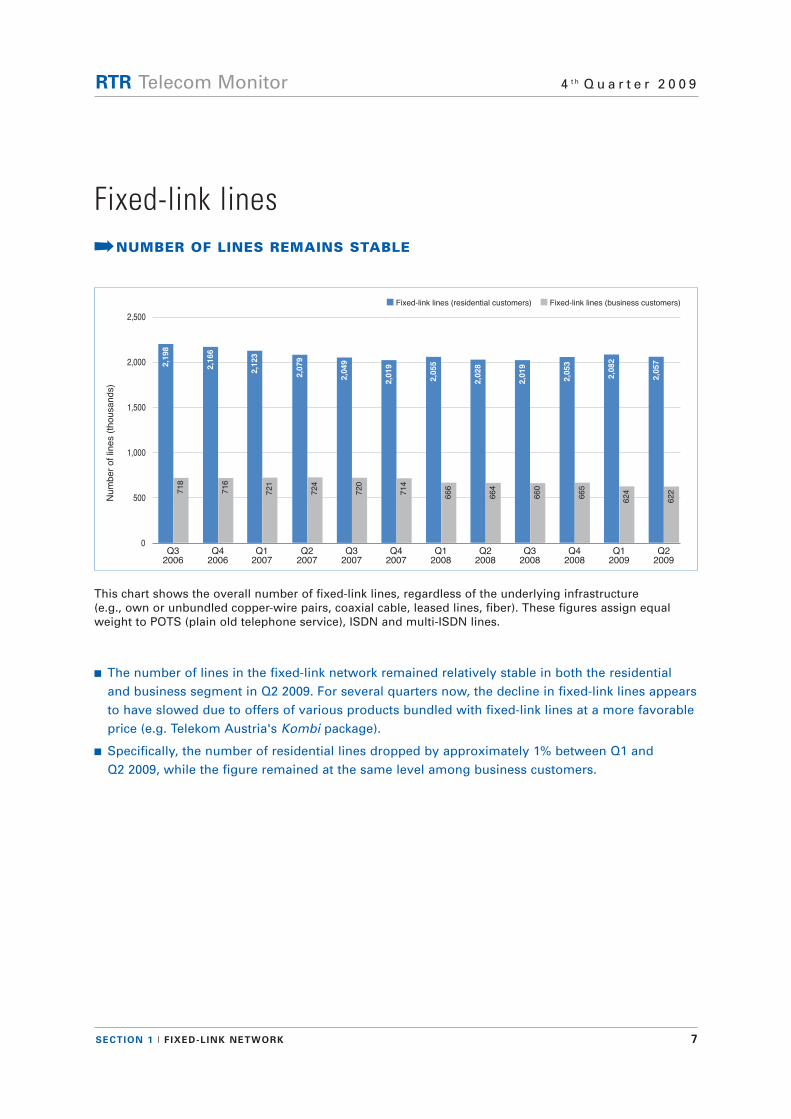

n Fixed-link lines (residential customers) n Fixed-link lines (business customers)

0Q1

2007

2,123

721

Q22007

2,079

724

500

Q32006

2,198

718

Q42006

2,166

716

1,000

1,500

2,000

2,500

Q32007

2,049

720

Q42007

2,019

714

Num

ber

of

lines (

tho

usa

nd

s)

Q12008

2,055

666

Q22008

2,028

664

Q32008

2,019

660

Q42008

2,053

665

Q12009

2,082

624

Q22009

2,057

622

This chart shows the overall number of fixed-link lines, regardless of the underlying infrastructure (e.g., own or unbundled copper-wire pairs, coaxial cable, leased lines, fiber). These figures assign equalweight to POTS (plain old telephone service), ISDN and multi-ISDN lines.

n The number of lines in the fixed-link network remained relatively stable in both the residential and business segment in Q2 2009. For several quarters now, the decline in fixed-link lines appearsto have slowed due to offers of various products bundled with fixed-link lines at a more favorableprice (e.g. Telekom Austria's Kombi package).

n Specifically, the number of residential lines dropped by approximately 1% between Q1 and Q2 2009, while the figure remained at the same level among business customers.

Fixed-link lines·NUMBER OF LINES REMAINS STABLE

SECTION 1 I FIXED-LINK NETWORK 8

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

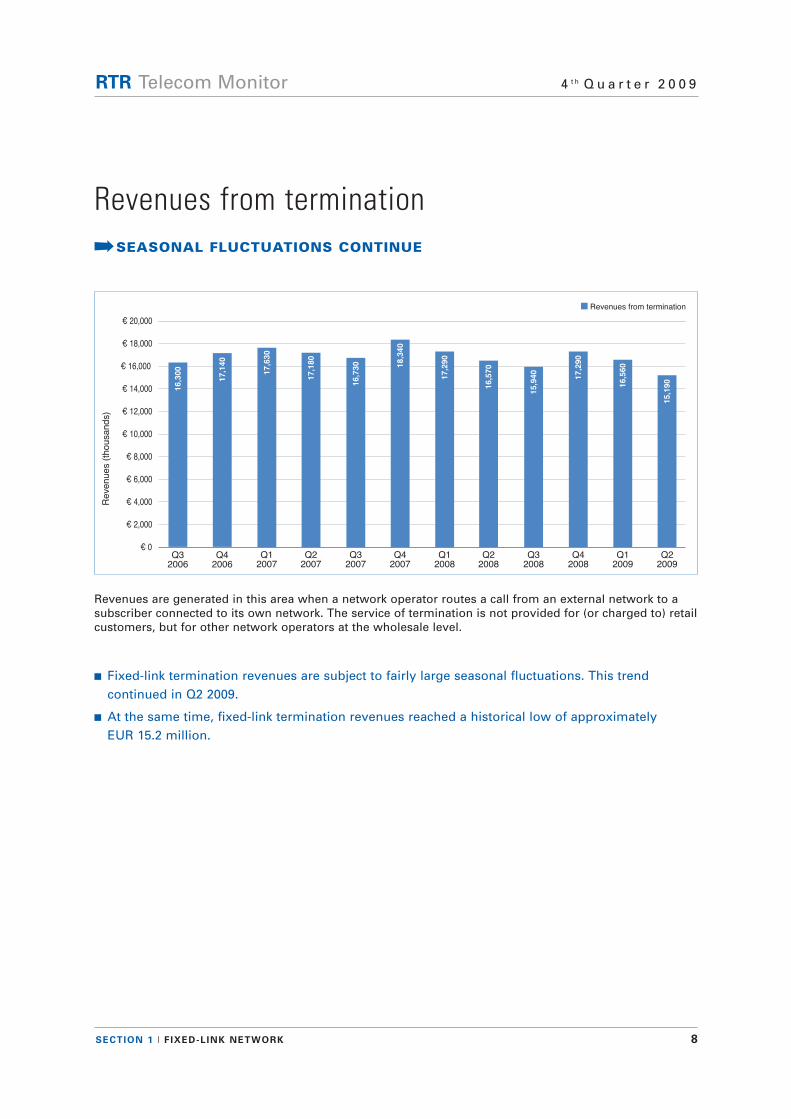

n Revenues from termination

€ 0Q1

2007

17,630

Q22007

17,180

€ 2,000

€ 4,000

€ 6,000

€ 8,000

€ 10,000

€ 12,000

€ 14,000

€ 16,000

€ 18,000

€ 20,000

Revenues (

thousa

nd

s)

Q32006

16,300

Q42006

17,140

Q32007

16,730

Q42007

18,340

Q12008

17,290

Q22008

16,570

Q32008

15,940

Q42008

17,290

Q12009

16,560

Q22009

15,190

Revenues are generated in this area when a network operator routes a call from an external network to asubscriber connected to its own network. The service of termination is not provided for (or charged to) retailcustomers, but for other network operators at the wholesale level.

n Fixed-link termination revenues are subject to fairly large seasonal fluctuations. This trend continued in Q2 2009.

n At the same time, fixed-link termination revenues reached a historical low of approximately EUR 15.2 million.

Revenues from termination·SEASONAL FLUCTUATIONS CONTINUE

SECTION 1 I FIXED-LINK NETWORK 9

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

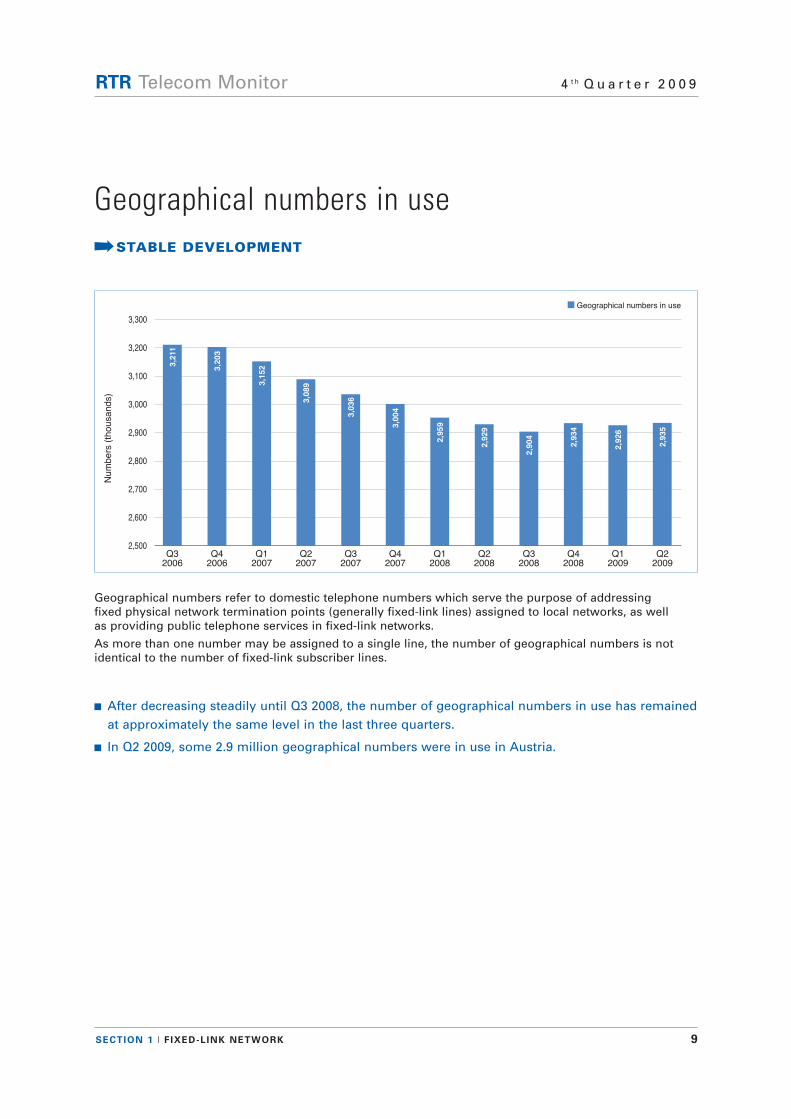

n Geographical numbers in use

2,500Q4

2007

3,004

Num

bers

(th

ou

sa

nd

s)

Q32006

3,211

Q42006

3,203

Q12007

3,152

Q22007

3,089

2,600

2,700

2,800

2,900

3,000

3,100

3,200

3,300

Q32007

3,036

Q12008

2,959

Q22008

2,929

Q32008

2,904

Q42008

2,934

Q12009

2,926

Q22009

2,935

Geographical numbers refer to domestic telephone numbers which serve the purpose of addressing fixed physical network termination points (generally fixed-link lines) assigned to local networks, as well as providing public telephone services in fixed-link networks.

As more than one number may be assigned to a single line, the number of geographical numbers is notidentical to the number of fixed-link subscriber lines.

n After decreasing steadily until Q3 2008, the number of geographical numbers in use has remainedat approximately the same level in the last three quarters.

n In Q2 2009, some 2.9 million geographical numbers were in use in Austria.

Geographical numbers in use·STABLE DEVELOPMENT

SECTION 1 I FIXED-LINK NETWORK 10

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

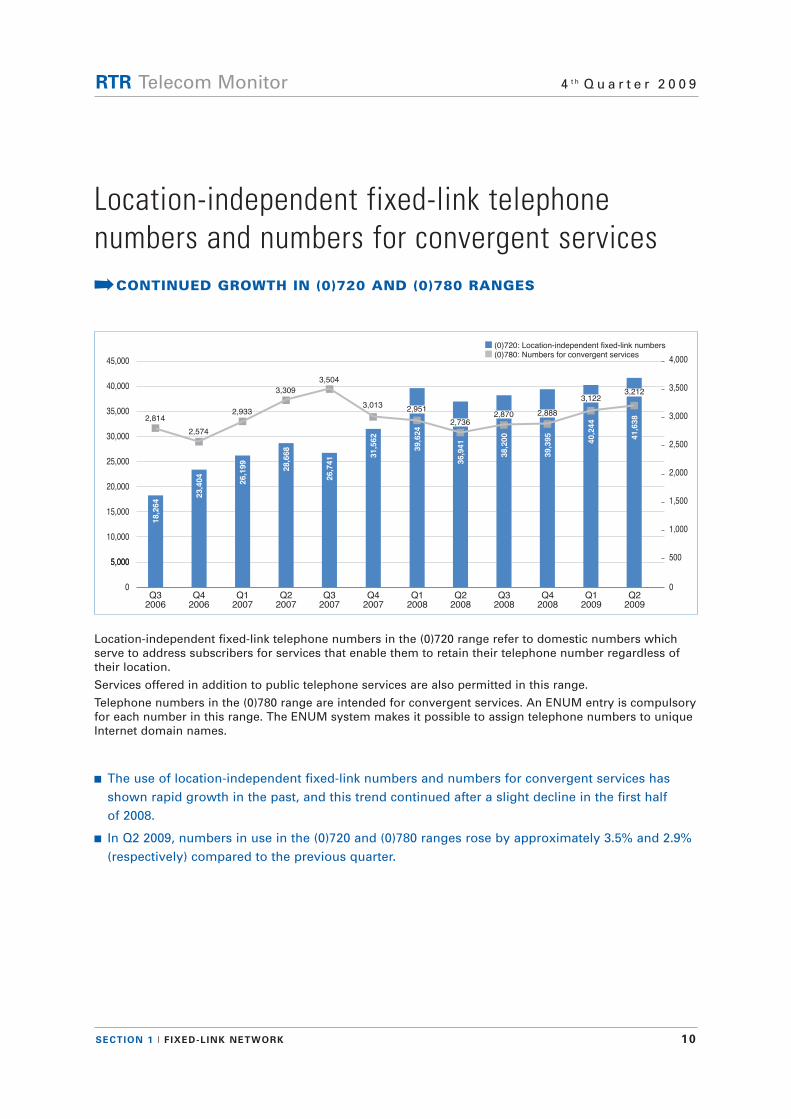

n (0)720: Location-independent fixed-link numbersn (0)780: Numbers for convergent services

0Q3

2006

18,264

Q42006

23,404

Q12007

26,199

Q22007

28,668

Q42007

31,562

0

4,000

Q32007

26,741

3,500

3,000

2,500

2,000

1,500

1,000

500

2,814

2,574

2,933

3,309

3,504

3,013

Q12008

39,624

2,951

5,0005,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q22008

36,941

2,736

Q32008

38,200

2,870

Q42008

39,395

2,888

Q12009

40,244

3,122

Q22009

41,638

3,212

Location-independent fixed-link telephone numbers in the (0)720 range refer to domestic numbers whichserve to address subscribers for services that enable them to retain their telephone number regardless oftheir location.

Services offered in addition to public telephone services are also permitted in this range.

Telephone numbers in the (0)780 range are intended for convergent services. An ENUM entry is compulsoryfor each number in this range. The ENUM system makes it possible to assign telephone numbers to uniqueInternet domain names.

n The use of location-independent fixed-link numbers and numbers for convergent services has shown rapid growth in the past, and this trend continued after a slight decline in the first half of 2008.

n In Q2 2009, numbers in use in the (0)720 and (0)780 ranges rose by approximately 3.5% and 2.9% (respectively) compared to the previous quarter.

Location-independent fixed-link telephone numbers and numbers for convergent services·CONTINUED GROWTH IN (0)720 AND (0)780 RANGES

SECTION 1 I FIXED-LINK NETWORK 11

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

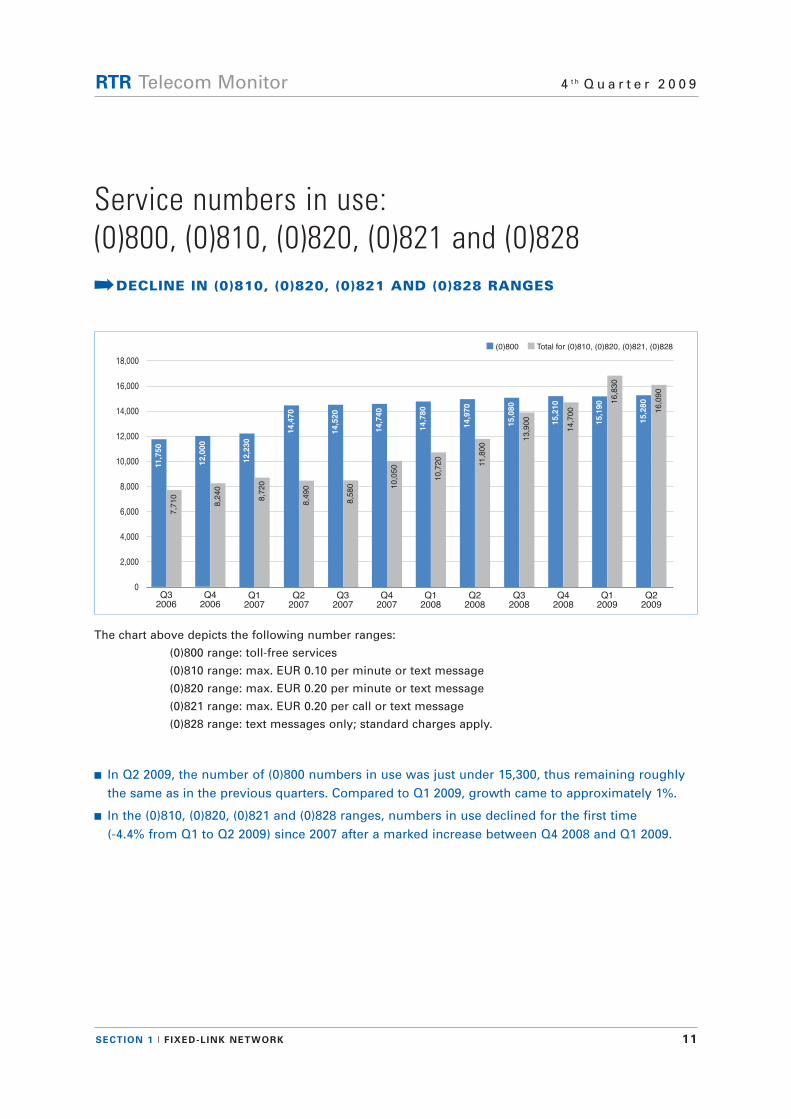

n (0)800 n Total for (0)810, (0)820, (0)821, (0)828

0Q1

2007

12,230

8,7

20

Q22007

14,470

8,4

90

Q32007

14,520

8,5

80

Q32006

11,750

7,7

10

Q42006

12,000

8,2

40

Q42007

14,740

10,0

50

Q12008

14,780

10,7

20

Q22008

14,970

11,8

00

Q32008

15,080

13,9

00

Q42008

15,210

14,7

00

Q12009

15,190 1

6,8

30

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Q22009

15,280

16,0

90

The chart above depicts the following number ranges:

(0)800 range: toll-free services

(0)810 range: max. EUR 0.10 per minute or text message

(0)820 range: max. EUR 0.20 per minute or text message

(0)821 range: max. EUR 0.20 per call or text message

(0)828 range: text messages only; standard charges apply.

n In Q2 2009, the number of (0)800 numbers in use was just under 15,300, thus remaining roughly the same as in the previous quarters. Compared to Q1 2009, growth came to approximately 1%.

n In the (0)810, (0)820, (0)821 and (0)828 ranges, numbers in use declined for the first time (-4.4% from Q1 to Q2 2009) since 2007 after a marked increase between Q4 2008 and Q1 2009.

Service numbers in use: (0)800, (0)810, (0)820, (0)821 and (0)828·DECLINE IN (0)810, (0)820, (0)821 AND (0)828 RANGES

SECTION 1 I FIXED-LINK NETWORK 12

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

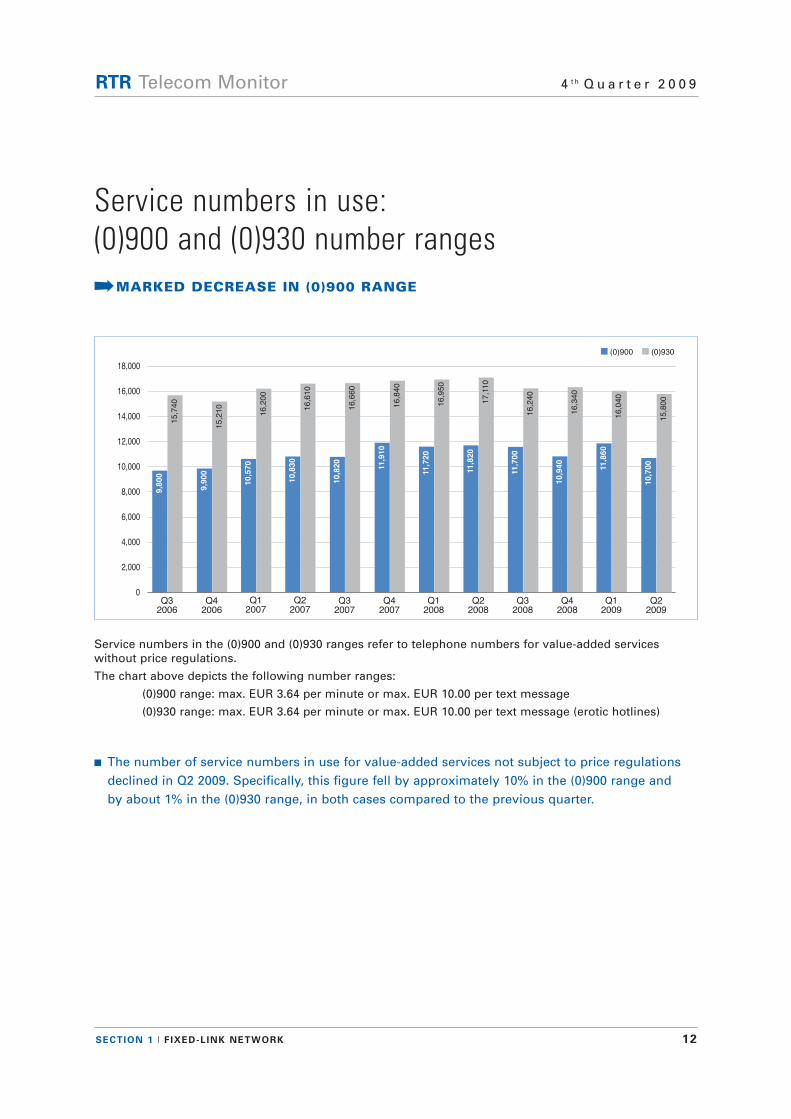

n (0)900 n (0)930

0Q1

2007

10,570

16,2

00

Q22007

10,830

16,6

10

Q32007

10,820

16,6

60

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Q32006

9,800

15,7

40

Q42006

9,900

15,2

10

Q42007

11,910

16,8

40

Q12008

11,720

16,9

50

Q22008

11,820

17,1

10

Q32008

11,700

16,2

40

Q42008

10,940

16,3

40

Q12009

11,860

16,0

40

Q22009

10,700

15,8

00

Service numbers in the (0)900 and (0)930 ranges refer to telephone numbers for value-added services without price regulations.

The chart above depicts the following number ranges:

(0)900 range: max. EUR 3.64 per minute or max. EUR 10.00 per text message

(0)930 range: max. EUR 3.64 per minute or max. EUR 10.00 per text message (erotic hotlines)

n The number of service numbers in use for value-added services not subject to price regulations declined in Q2 2009. Specifically, this figure fell by approximately 10% in the (0)900 range and by about 1% in the (0)930 range, in both cases compared to the previous quarter.

Service numbers in use: (0)900 and (0)930 number ranges·MARKED DECREASE IN (0)900 RANGE

SECTION 1 I FIXED-LINK NETWORK 13

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

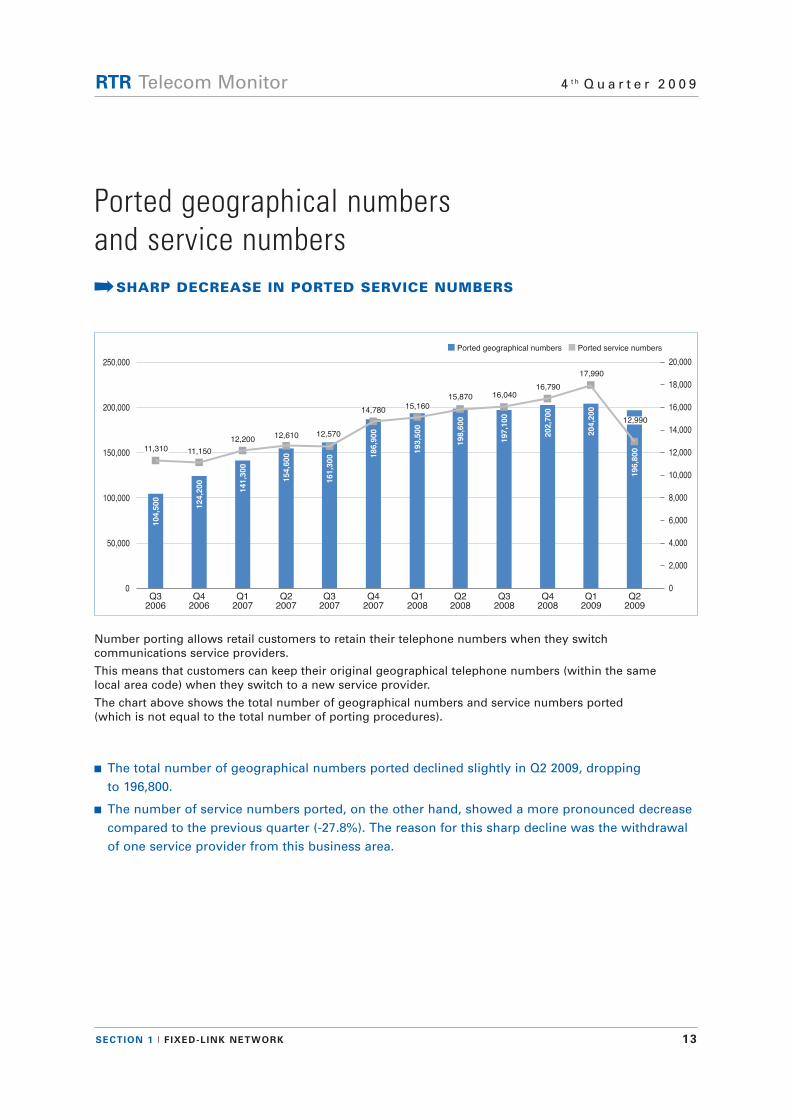

n Ported geographical numbers n Ported service numbers

0

50,000

Q32006

104,500

Q42006

124,200

Q12007

141,300

Q22007

154,600

Q42007

186,900

0Q3

2007

161,300

11,310 11,150

12,20012,610 12,570

14,780

Q12008

193,500

15,160

Q22008

198,600

15,870

100,000

150,000

200,000

250,000

Q32008

197,100

16,040

Q42008

202,700

16,790

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Q12009

204,200

17,990

Q22009

196,800

12,990

Number porting allows retail customers to retain their telephone numbers when they switch communications service providers.

This means that customers can keep their original geographical telephone numbers (within the same local area code) when they switch to a new service provider.

The chart above shows the total number of geographical numbers and service numbers ported (which is not equal to the total number of porting procedures).

n The total number of geographical numbers ported declined slightly in Q2 2009, dropping to 196,800.

n The number of service numbers ported, on the other hand, showed a more pronounced decreasecompared to the previous quarter (-27.8%). The reason for this sharp decline was the withdrawalof one service provider from this business area.

Ported geographical numbers and service numbers·SHARP DECREASE IN PORTED SERVICE NUMBERS

14

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 2 Leased lines

SECTION 2 I LEASED LINES 15

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Number of retail leased lines <= 2 Mbit/s n Number of retail leased lines > 2 Mbit/s

0 0Q4

2007

34,690

674

Q32006

40,250

886

Q42006

39,620

Q32007

35,280

1,370

Q22007

36,270

1,269

Q12007

37,500

1,225

Q12008

33,530

1,1521,117

Q22008

33,200

1,298

Q32008

32,140

1,263

Q42008

32,190

1,420

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

200

Q12009

30,880

1,535

Q22009

29,890

1,809

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Retail leased lines are those which are not provided for communications network operators or communications service providers (i.e., holders of general licensing approvals).

With regard to data transmission rates, a distinction is drawn between leased lines with a capacity of 2 Mbit/s or less and those with a capacity exceeding 2 Mbit/s.

n Since Q3 2008, a substantial increase in the number of leased lines with bandwidths exceeding2 Mbit/s has been observed. This trend is also visible in the figure for Q2 2009. In the last year, the number of lines of this type has increased by nearly 40% to a total of 1,800.

n On the other hand, the slight downward trend in the number of retail leased lines with a capacity of less than 2 Mbit/s also persisted in Q2 2009. For the first time, this figure dropped below 30,000.

Number of retail leased lines in Austria·BANDWIDTHS OVER 2 MBIT/S CONTINUE UPWARD TREND

SECTION 2 I LEASED LINES 16

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Revenues from retail leased lines <= 2 Mbit/s n Revenues from retail leased lines > 2 Mbit/s

0Q1

2007

13,750

5,9

86

Q22007

13,530

5,8

18

Q32007

13,100

5,6

57

€ 2,000

Q32006

14,290

4,8

38

Q42006

14,670

7,1

15

Q42007

13,120

6,7

43

€ 4,000

€ 6,000

€ 8,000

€ 10,000

€ 12,000

€ 14,000

€ 16,000

€ 18,000

Revenues (

tho

usa

nd

s)

Q12008

12,310

6,0

02

Q22008

13,060

8,1

41

Q32008

13,170

7,3

41

Q42008

13,090

8,5

94

Q12009

12,870

7,2

07

Q22009

12,230

6,2

71

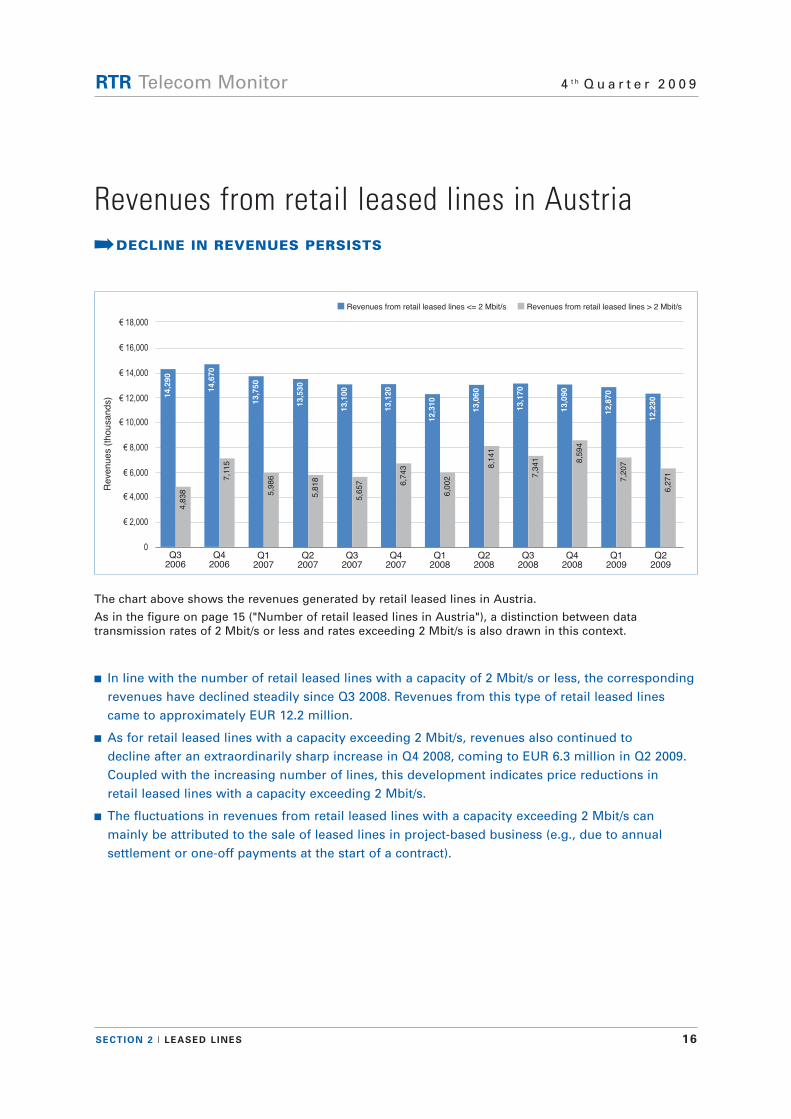

The chart above shows the revenues generated by retail leased lines in Austria.

As in the figure on page 15 ("Number of retail leased lines in Austria"), a distinction between data transmission rates of 2 Mbit/s or less and rates exceeding 2 Mbit/s is also drawn in this context.

n In line with the number of retail leased lines with a capacity of 2 Mbit/s or less, the correspondingrevenues have declined steadily since Q3 2008. Revenues from this type of retail leased lines came to approximately EUR 12.2 million.

n As for retail leased lines with a capacity exceeding 2 Mbit/s, revenues also continued to decline after an extraordinarily sharp increase in Q4 2008, coming to EUR 6.3 million in Q2 2009. Coupled with the increasing number of lines, this development indicates price reductions in retail leased lines with a capacity exceeding 2 Mbit/s.

n The fluctuations in revenues from retail leased lines with a capacity exceeding 2 Mbit/s can mainly be attributed to the sale of leased lines in project-based business (e.g., due to annual settlement or one-off payments at the start of a contract).

Revenues from retail leased lines in Austria·DECLINE IN REVENUES PERSISTS

SECTION 2 I LEASED LINES 17

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Total revenues from wholesale leased lines <= 2 Mbit/s n Total revenues from wholesale leased lines > 2 Mbit/s

€ 0Q1

2007

31,780

Q22007

31,640

Q32007

31,950

Revenues (

tho

usa

nd

s)

€ 5,000

€ 10,000

€ 15,000

€ 20,000

€ 25,000

€ 30,000

€ 35,000

€ 40,000

Q32006

33,480

Q42006

37,740

Q42007

32,270

€ 0

€ 1,000

€ 2,000

€ 3,000

€ 4,000

€ 5,000

€ 6,000

€ 7,000

€ 8,000

€ 9,000

6,108

6,644

5,643

6,176 6,0686,374

Q12008

31,160

6,049

Q22008

31,270

6,261

Q32008

30,220

5,586

Q42008

32,620

6,451

Q12009

34,080

6,221

Q22009

33,570

6,395

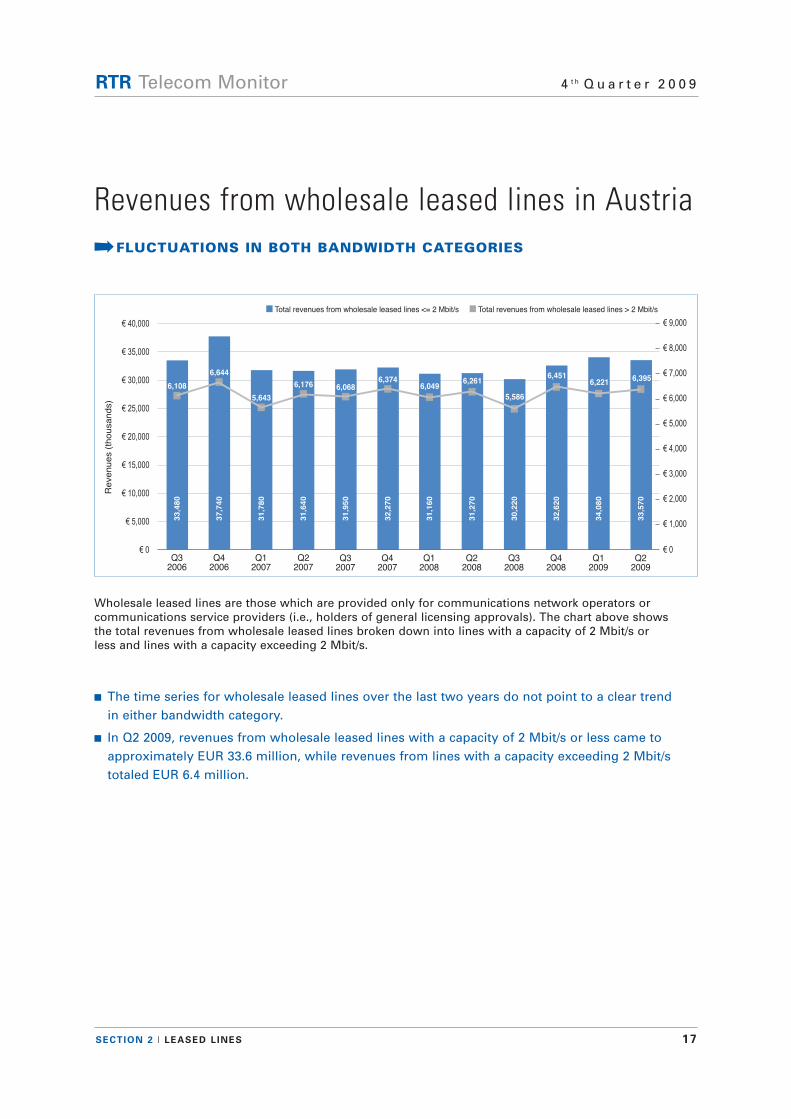

Wholesale leased lines are those which are provided only for communications network operators or communications service providers (i.e., holders of general licensing approvals). The chart above shows the total revenues from wholesale leased lines broken down into lines with a capacity of 2 Mbit/s or less and lines with a capacity exceeding 2 Mbit/s.

n The time series for wholesale leased lines over the last two years do not point to a clear trend in either bandwidth category.

n In Q2 2009, revenues from wholesale leased lines with a capacity of 2 Mbit/s or less came to approximately EUR 33.6 million, while revenues from lines with a capacity exceeding 2 Mbit/s totaled EUR 6.4 million.

Revenues from wholesale leased lines in Austria·FLUCTUATIONS IN BOTH BANDWIDTH CATEGORIES

18

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 3 Mobile communications

SECTION 3 I MOBILE COMMUNICATIONS 19

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

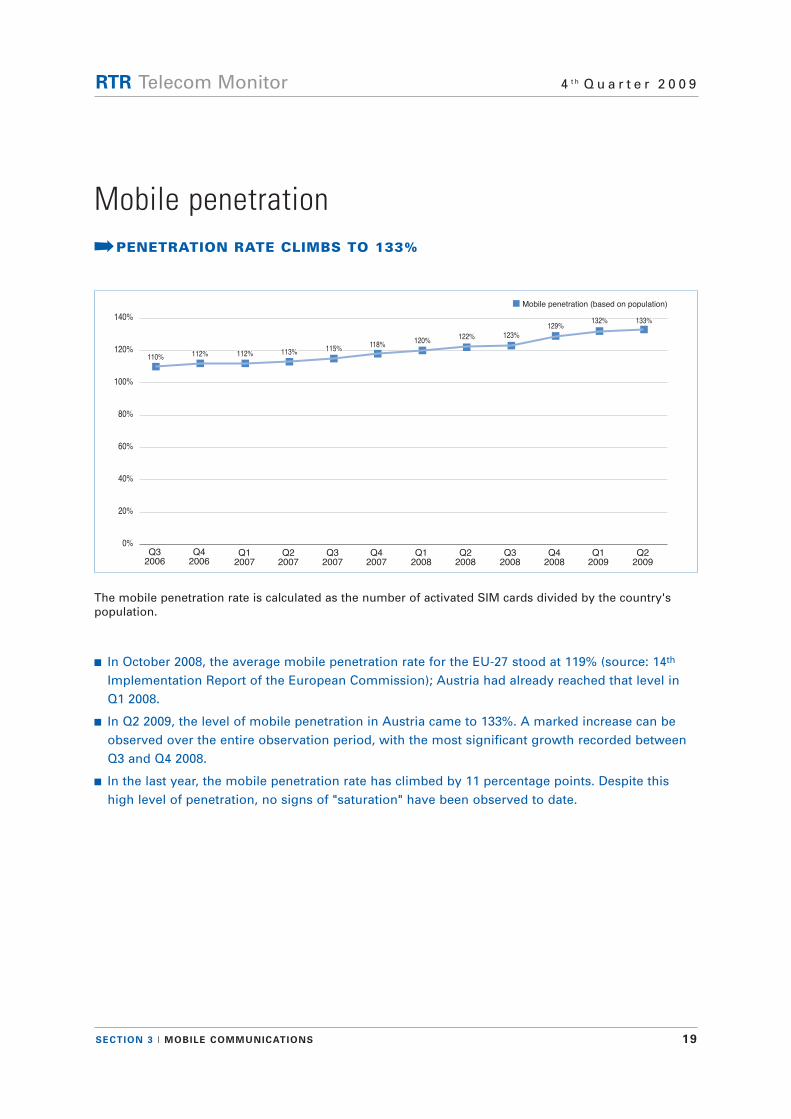

n Mobile penetration (based on population)

0%Q3

2006Q1

2007Q2

2007

112% 113%

Q32007

115%110% 112%

Q42006

20%

40%

60%

80%

100%

120%

140%

Q42007

118%

Q12008

120%

Q22008

122%

Q32008

123%

Q42008

129%

Q12009

132%

Q22009

133%

The mobile penetration rate is calculated as the number of activated SIM cards divided by the country'spopulation.

n In October 2008, the average mobile penetration rate for the EU-27 stood at 119% (source: 14th

Implementation Report of the European Commission); Austria had already reached that level in Q1 2008.

n In Q2 2009, the level of mobile penetration in Austria came to 133%. A marked increase can be observed over the entire observation period, with the most significant growth recorded between Q3 and Q4 2008.

n In the last year, the mobile penetration rate has climbed by 11 percentage points. Despite this high level of penetration, no signs of "saturation" have been observed to date.

Mobile penetration·PENETRATION RATE CLIMBS TO 133%

SECTION 3 I MOBILE COMMUNICATIONS 20

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

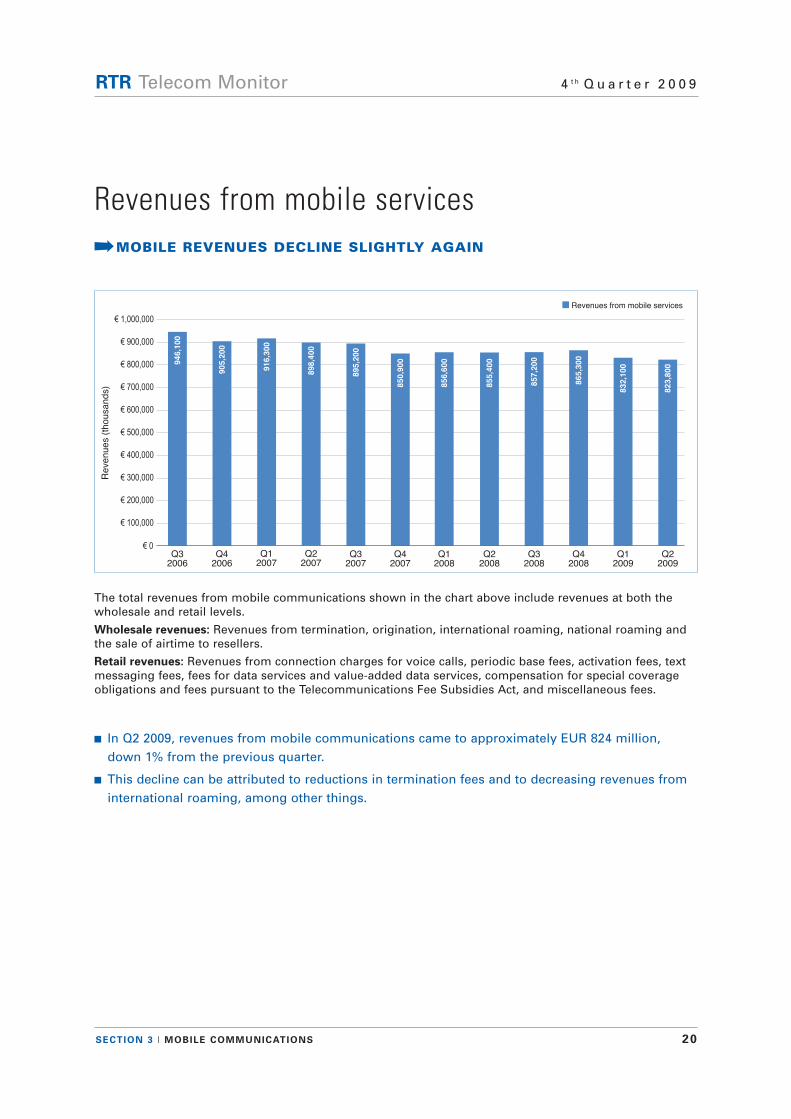

n Revenues from mobile services

€ 0Q1

2007

916,300

Q22007

898,400

Q32007

895,200

€ 100,000

Revenues (

tho

usa

nd

s)

Q32006

946,100

Q42006

905,200

€ 200,000

€ 300,000

€ 400,000

€ 500,000

€ 600,000

€ 700,000

€ 800,000

€ 900,000

€ 1,000,000

Q42007

850,900

Q12008

856,600

Q22008

855,400

Q32008

857,200

Q42008

865,300

Q12009

832,100

Q22009

823,800

The total revenues from mobile communications shown in the chart above include revenues at both thewholesale and retail levels.

Wholesale revenues: Revenues from termination, origination, international roaming, national roaming andthe sale of airtime to resellers.

Retail revenues: Revenues from connection charges for voice calls, periodic base fees, activation fees, textmessaging fees, fees for data services and value-added data services, compensation for special coverageobligations and fees pursuant to the Telecommunications Fee Subsidies Act, and miscellaneous fees.

n In Q2 2009, revenues from mobile communications came to approximately EUR 824 million, down 1% from the previous quarter.

n This decline can be attributed to reductions in termination fees and to decreasing revenues from international roaming, among other things.

Revenues from mobile services·MOBILE REVENUES DECLINE SLIGHTLY AGAIN

SECTION 3 I MOBILE COMMUNICATIONS 21

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

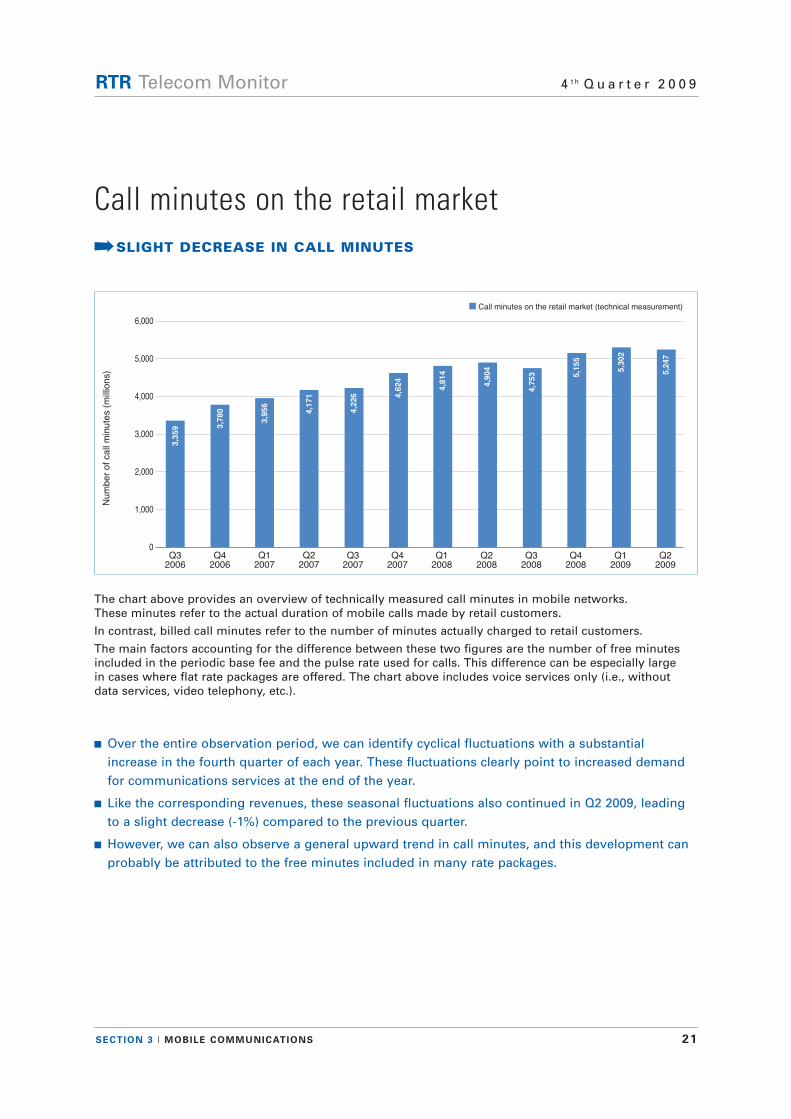

n Call minutes on the retail market (technical measurement)

Q12007

0

3,956

Q22007

4,171

Q32007

4,226

Num

ber

of

call

min

ute

s (

mill

ion

s)

Q32006

3,359

Q42006

3,780

Q42007

4,624

Q12008

4,814

Q22008

4,904

Q32008

4,753

1,000

2,000

3,000

4,000

5,000

6,000

Q42008

5,155

Q12009

5,302

Q22009

5,247

The chart above provides an overview of technically measured call minutes in mobile networks. These minutes refer to the actual duration of mobile calls made by retail customers.

In contrast, billed call minutes refer to the number of minutes actually charged to retail customers.

The main factors accounting for the difference between these two figures are the number of free minutesincluded in the periodic base fee and the pulse rate used for calls. This difference can be especially large in cases where flat rate packages are offered. The chart above includes voice services only (i.e., withoutdata services, video telephony, etc.).

n Over the entire observation period, we can identify cyclical fluctuations with a substantial increase in the fourth quarter of each year. These fluctuations clearly point to increased demand for communications services at the end of the year.

n Like the corresponding revenues, these seasonal fluctuations also continued in Q2 2009, leading to a slight decrease (-1%) compared to the previous quarter.

n However, we can also observe a general upward trend in call minutes, and this development can probably be attributed to the free minutes included in many rate packages.

Call minutes on the retail market·SLIGHT DECREASE IN CALL MINUTES

SECTION 3 I MOBILE COMMUNICATIONS 22

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

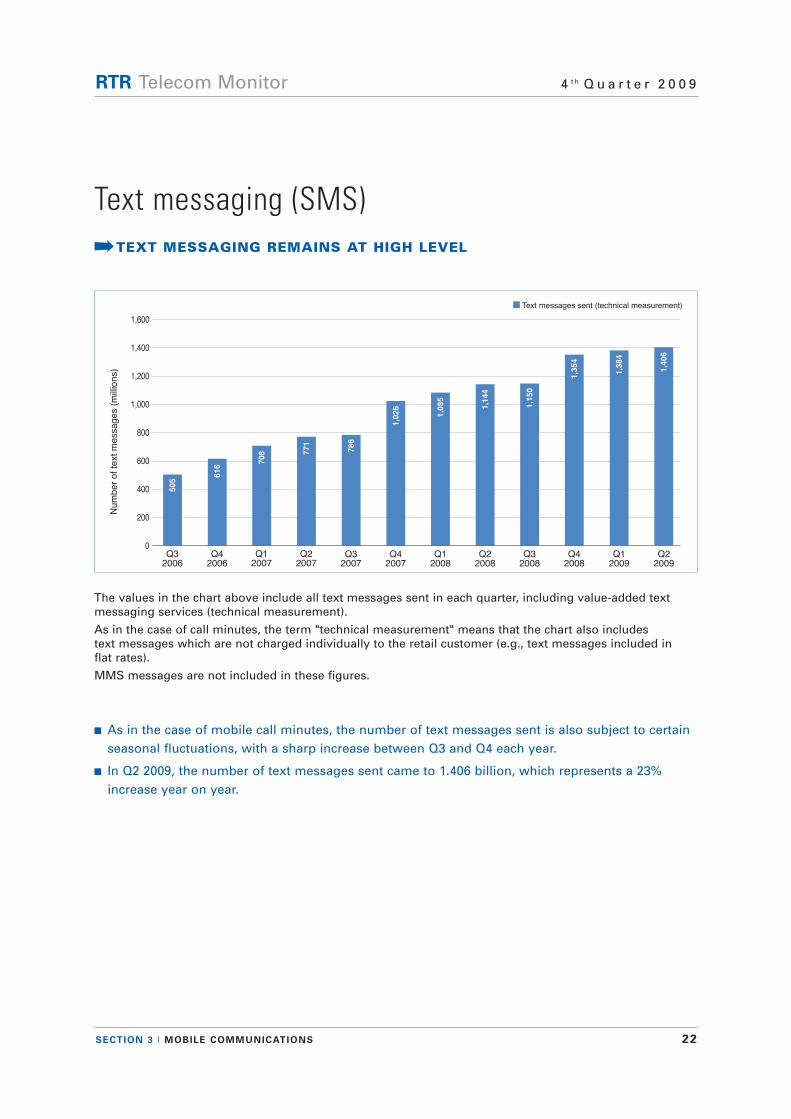

n Text messages sent (technical measurement)

0Q1

2007

708

Q22007

771

Q32007

786

Num

ber

of

text

messa

ge

s (

mill

ion

s)

Q32006

505

Q42006

616

Q42007

1,026

Q12008

1,085

Q22008

1,144

Q32008

1,150

Q42008

1,354

200

400

600

800

1,000

1,200

1,400

1,600

Q12009

1,384

Q22009

1,406

The values in the chart above include all text messages sent in each quarter, including value-added textmessaging services (technical measurement).

As in the case of call minutes, the term "technical measurement" means that the chart also includes text messages which are not charged individually to the retail customer (e.g., text messages included in flat rates).

MMS messages are not included in these figures.

n As in the case of mobile call minutes, the number of text messages sent is also subject to certain seasonal fluctuations, with a sharp increase between Q3 and Q4 each year.

n In Q2 2009, the number of text messages sent came to 1.406 billion, which represents a 23% increase year on year.

Text messaging (SMS)·TEXT MESSAGING REMAINS AT HIGH LEVEL

SECTION 3 I MOBILE COMMUNICATIONS 23

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

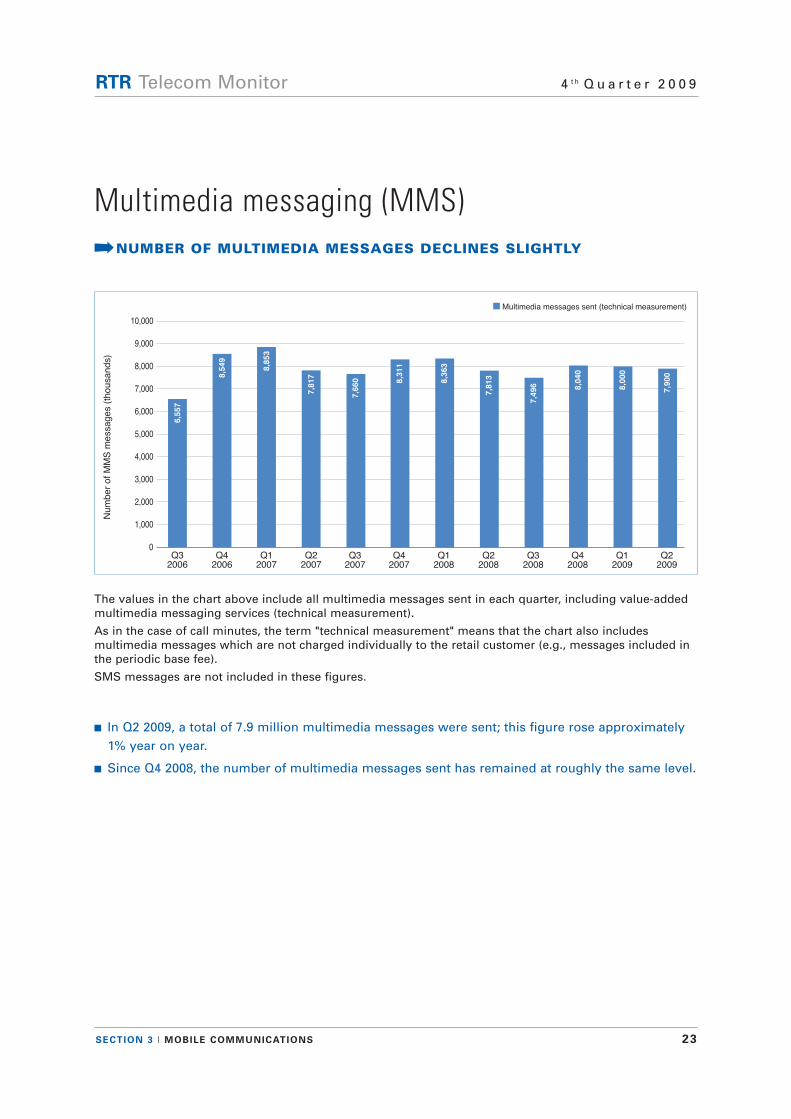

n Multimedia messages sent (technical measurement)

0Q3

2007

7,660

Num

ber

of

MM

S m

essa

ge

s (

tho

usa

nd

s)

Q32006

6,557

Q42006

8,549

Q12007

8,853

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Q22007

7,817

Q42007

8,311

Q12008

8,363

Q22008

7,813

Q32008

7,496

Q42008

8,040

Q12009

8,000

Q22009

7,900

The values in the chart above include all multimedia messages sent in each quarter, including value-addedmultimedia messaging services (technical measurement).

As in the case of call minutes, the term "technical measurement" means that the chart also includes multimedia messages which are not charged individually to the retail customer (e.g., messages included inthe periodic base fee).

SMS messages are not included in these figures.

n In Q2 2009, a total of 7.9 million multimedia messages were sent; this figure rose approximately 1% year on year.

n Since Q4 2008, the number of multimedia messages sent has remained at roughly the same level.

Multimedia messaging (MMS)·NUMBER OF MULTIMEDIA MESSAGES DECLINES SLIGHTLY

SECTION 3 I MOBILE COMMUNICATIONS 24

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

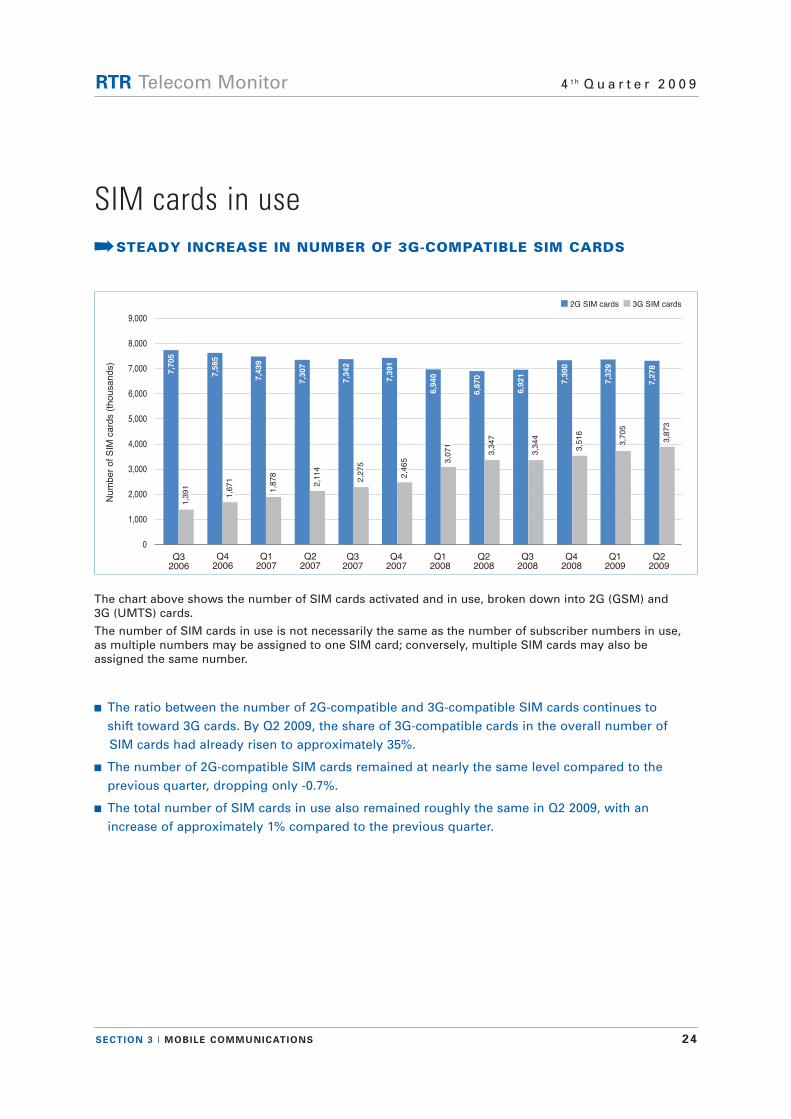

n 2G SIM cards n 3G SIM cards

0

Q32007

7,342

2,2

75

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Q32006

7,705

1,3

91

Q42006

7,585

1,6

71

Q12007

7,439

1,8

78

Q22007

7,307

2,1

14

Num

ber

of

SIM

ca

rds (

tho

usa

nd

s)

Q42007

7,391

2,4

65

Q12008

6,940

3,0

71

Q22008

6,870

3,3

47

Q32008

6,921

3,3

44

Q42008

7,300

3,5

16

Q12009

7,329

3,7

05

Q22009

7,278

3,8

73

The chart above shows the number of SIM cards activated and in use, broken down into 2G (GSM) and 3G (UMTS) cards.

The number of SIM cards in use is not necessarily the same as the number of subscriber numbers in use, as multiple numbers may be assigned to one SIM card; conversely, multiple SIM cards may also be assigned the same number.

n The ratio between the number of 2G-compatible and 3G-compatible SIM cards continues to shift toward 3G cards. By Q2 2009, the share of 3G-compatible cards in the overall number of SIM cards had already risen to approximately 35%.

n The number of 2G-compatible SIM cards remained at nearly the same level compared to the previous quarter, dropping only -0.7%.

n The total number of SIM cards in use also remained roughly the same in Q2 2009, with an increase of approximately 1% compared to the previous quarter.

SIM cards in use·STEADY INCREASE IN NUMBER OF 3G-COMPATIBLE SIM CARDS

SECTION 3 I MOBILE COMMUNICATIONS 25

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

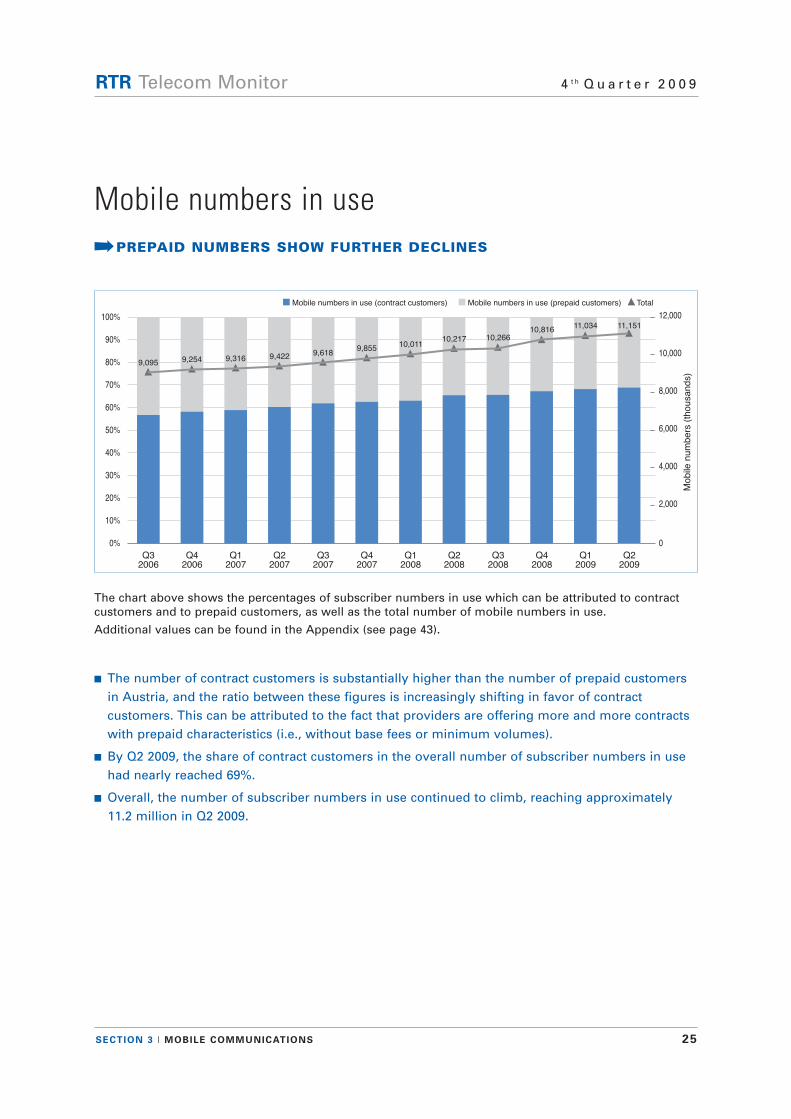

n Mobile numbers in use (contract customers) n Mobile numbers in use (prepaid customers) Total

0%

Q42007

Mobile

num

be

rs (

tho

usa

nd

s)

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q32007

Q22007

Q12007

Q42006

Q32006

9,095 9,254 9,316 9,422 9,6189,855

0

2,000

4,000

6,000

8,000

10,000

12,000

Q12008

10,011

Q22008

10,217

Q32008

10,266

Q42008

10,816

Q12009

11,034

Q22009

11,151

The chart above shows the percentages of subscriber numbers in use which can be attributed to contractcustomers and to prepaid customers, as well as the total number of mobile numbers in use.

Additional values can be found in the Appendix (see page 43).

n The number of contract customers is substantially higher than the number of prepaid customers in Austria, and the ratio between these figures is increasingly shifting in favor of contract customers. This can be attributed to the fact that providers are offering more and more contracts with prepaid characteristics (i.e., without base fees or minimum volumes).

n By Q2 2009, the share of contract customers in the overall number of subscriber numbers in use had nearly reached 69%.

n Overall, the number of subscriber numbers in use continued to climb, reaching approximately 11.2 million in Q2 2009.

Mobile numbers in use·PREPAID NUMBERS SHOW FURTHER DECLINES

SECTION 3 I MOBILE COMMUNICATIONS 26

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

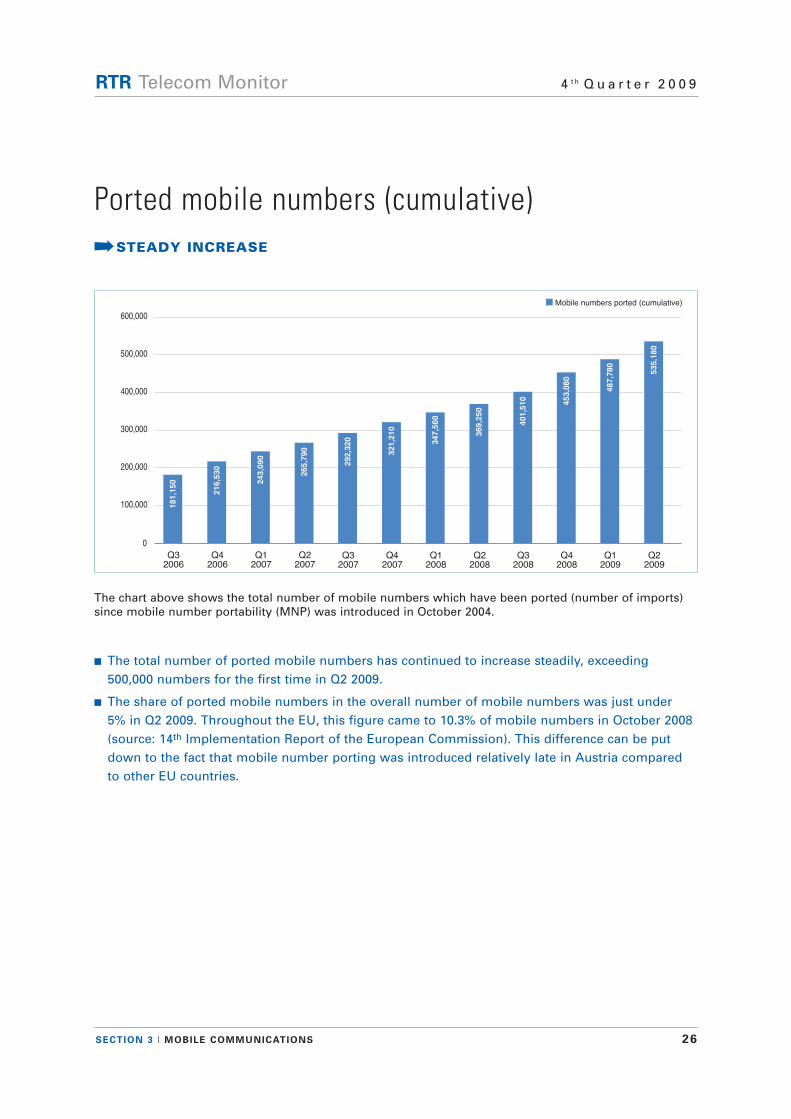

n Mobile numbers ported (cumulative)

0

Q32007

Q32006

181,150

Q42006

216,530

Q12007

243,090

Q22007

265,790

292,320

Q42007

321,210

Q12008

347,560

Q22008

369,250

Q32008

401,510

Q42008

453,080

100,000

Q12009

487,780

Q22009

535,180

200,000

300,000

400,000

500,000

600,000

The chart above shows the total number of mobile numbers which have been ported (number of imports)since mobile number portability (MNP) was introduced in October 2004.

n The total number of ported mobile numbers has continued to increase steadily, exceeding500,000 numbers for the first time in Q2 2009.

n The share of ported mobile numbers in the overall number of mobile numbers was just under 5% in Q2 2009. Throughout the EU, this figure came to 10.3% of mobile numbers in October 2008 (source: 14th Implementation Report of the European Commission). This difference can be put down to the fact that mobile number porting was introduced relatively late in Austria compared to other EU countries.

Ported mobile numbers (cumulative)·STEADY INCREASE

SECTION 3 I MOBILE COMMUNICATIONS 27

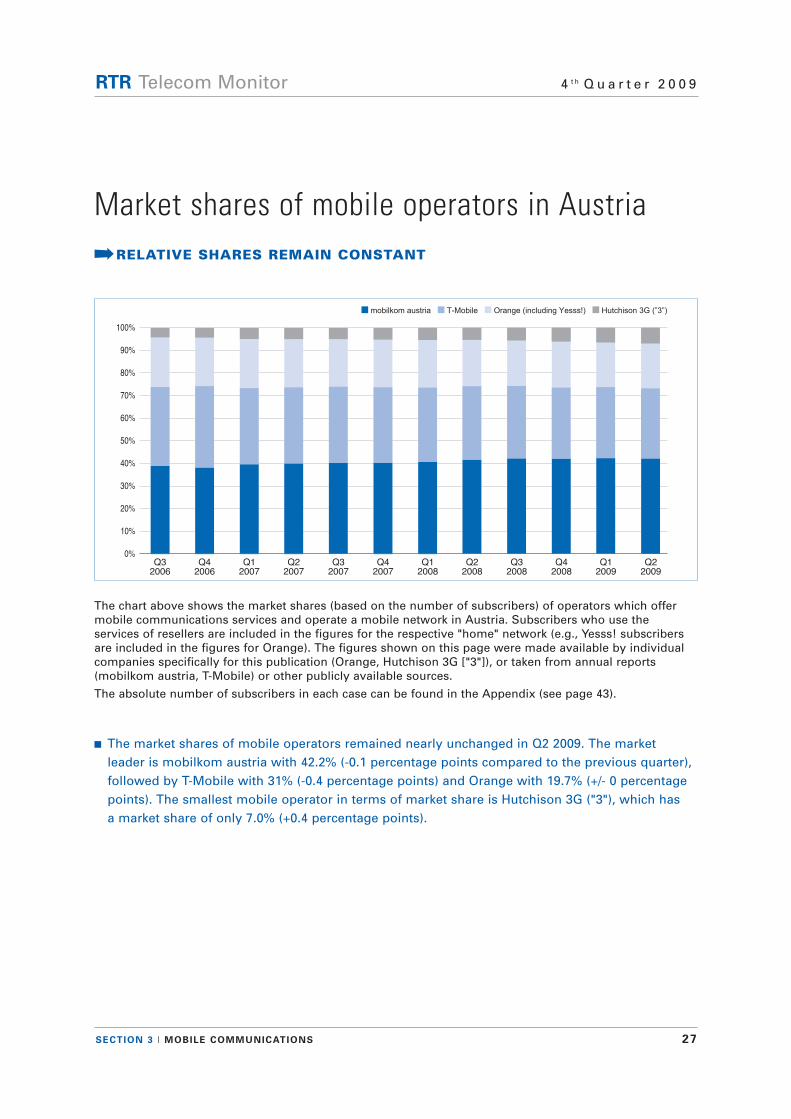

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

0%

100%

n mobilkom austria n T-Mobile n Orange (including Yesss!) n Hutchison 3G (”3”)

Q32006

Q12007

Q42006

Q22007

Q32007

Q42007

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

The chart above shows the market shares (based on the number of subscribers) of operators which offermobile communications services and operate a mobile network in Austria. Subscribers who use the services of resellers are included in the figures for the respective "home" network (e.g., Yesss! subscribersare included in the figures for Orange). The figures shown on this page were made available by individualcompanies specifically for this publication (Orange, Hutchison 3G ["3"]), or taken from annual reports (mobilkom austria, T-Mobile) or other publicly available sources.

The absolute number of subscribers in each case can be found in the Appendix (see page 43).

n The market shares of mobile operators remained nearly unchanged in Q2 2009. The market leader is mobilkom austria with 42.2% (-0.1 percentage points compared to the previous quarter), followed by T-Mobile with 31% (-0.4 percentage points) and Orange with 19.7% (+/- 0 percentage points). The smallest mobile operator in terms of market share is Hutchison 3G ("3"), which has a market share of only 7.0% (+0.4 percentage points).

Market shares of mobile operators in Austria

·RELATIVE SHARES REMAIN CONSTANT

28

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 4 Comparisons of fixed-link and mobile networks

SECTION 4 I COMPARISONS OF FIXED-LINK AND MOBILE NETWORKS 29

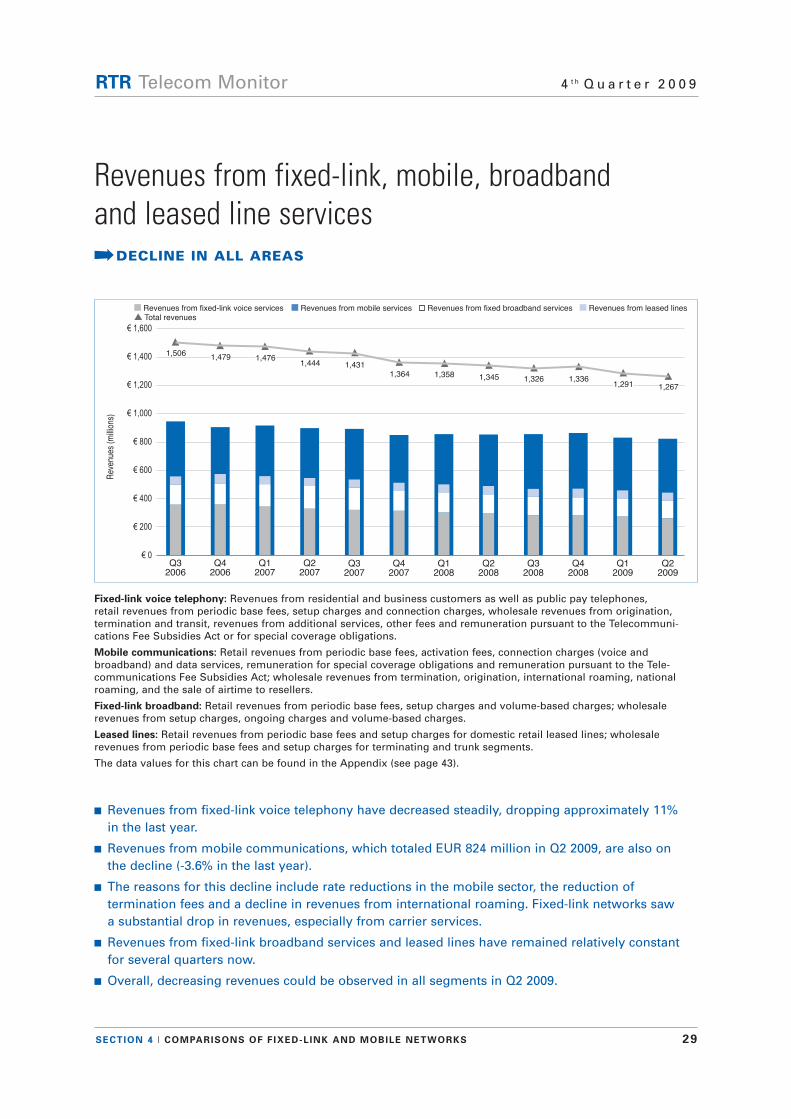

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

€ 200

€ 400

€ 600

€ 800

€ 1,000

€ 1,200

Rev

enue

s (m

illio

ns)

€ 0Q3

2007Q3

2006Q4

2006Q1

2007Q2

2007Q4

2007Q1

2008Q2

2008Q3

2008

€ 1,400

€ 1,600

1,5061,479 1,476

1,444 1,4311,364 1,358 1,345 1,326

Q42008

1,336

Q12009

1,291

Q22009

1,267

n Revenues from fixed-link voice services n Revenues from mobile services Revenues from fixed broadband services n Revenues from leased lines Total revenues

Fixed-link voice telephony: Revenues from residential and business customers as well as public pay telephones, retail revenues from periodic base fees, setup charges and connection charges, wholesale revenues from origination, termination and transit, revenues from additional services, other fees and remuneration pursuant to the Telecommuni -cations Fee Subsidies Act or for special coverage obligations.

Mobile communications: Retail revenues from periodic base fees, activation fees, connection charges (voice and broadband) and data services, remuneration for special coverage obligations and remuneration pursuant to the Tele -communications Fee Subsidies Act; wholesale revenues from termination, origination, international roaming, nationalroaming, and the sale of airtime to resellers.

Fixed-link broadband: Retail revenues from periodic base fees, setup charges and volume-based charges; wholesale revenues from setup charges, ongoing charges and volume-based charges.

Leased lines: Retail revenues from periodic base fees and setup charges for domestic retail leased lines; wholesale revenues from periodic base fees and setup charges for terminating and trunk segments.

The data values for this chart can be found in the Appendix (see page 43).

n Revenues from fixed-link voice telephony have decreased steadily, dropping approximately 11% in the last year.

n Revenues from mobile communications, which totaled EUR 824 million in Q2 2009, are also on the decline (-3.6% in the last year).

n The reasons for this decline include rate reductions in the mobile sector, the reduction of termination fees and a decline in revenues from international roaming. Fixed-link networks saw a substantial drop in revenues, especially from carrier services.

n Revenues from fixed-link broadband services and leased lines have remained relatively constantfor several quarters now.

n Overall, decreasing revenues could be observed in all segments in Q2 2009.

Revenues from fixed-link, mobile, broadband and leased line services·DECLINE IN ALL AREAS

SECTION 4 I COMPARISONS OF FIXED-LINK AND MOBILE NETWORKS 30

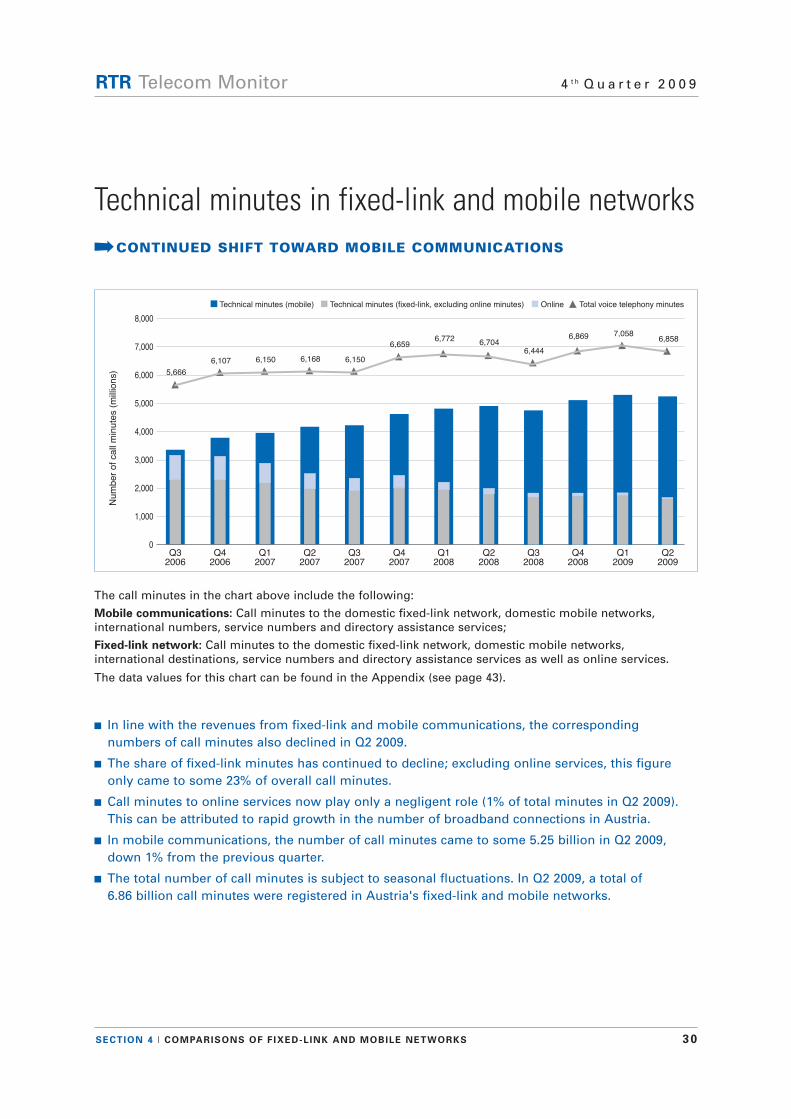

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Num

ber

of call

min

ute

s (

mill

ions)

n Technical minutes (mobile) Technical minutes (fixed-link, excluding online minutes) n Online Total voice telephony minutes

0Q3

2006Q1

2007Q4

2006Q2

2007Q3

2007Q4

2007Q1

2008Q2

2008Q3

2008

5,666

6,107 6,150 6,168 6,150

6,6596,772

6,7046,444

Q42008

6,869

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Q12009

7,058

Q22009

6,858

The call minutes in the chart above include the following:

Mobile communications: Call minutes to the domestic fixed-link network, domestic mobile networks, international numbers, service numbers and directory assistance services;

Fixed-link network: Call minutes to the domestic fixed-link network, domestic mobile networks, international destinations, service numbers and directory assistance services as well as online services.

The data values for this chart can be found in the Appendix (see page 43).

n In line with the revenues from fixed-link and mobile communications, the corresponding numbers of call minutes also declined in Q2 2009.

n The share of fixed-link minutes has continued to decline; excluding online services, this figure only came to some 23% of overall call minutes.

n Call minutes to online services now play only a negligent role (1% of total minutes in Q2 2009). This can be attributed to rapid growth in the number of broadband connections in Austria.

n In mobile communications, the number of call minutes came to some 5.25 billion in Q2 2009, down 1% from the previous quarter.

n The total number of call minutes is subject to seasonal fluctuations. In Q2 2009, a total of 6.86 billion call minutes were registered in Austria's fixed-link and mobile networks.

Technical minutes in fixed-link and mobile networks·CONTINUED SHIFT TOWARD MOBILE COMMUNICATIONS

31

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 5 Broadband

SECTION 5 I BROADBAND 32

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

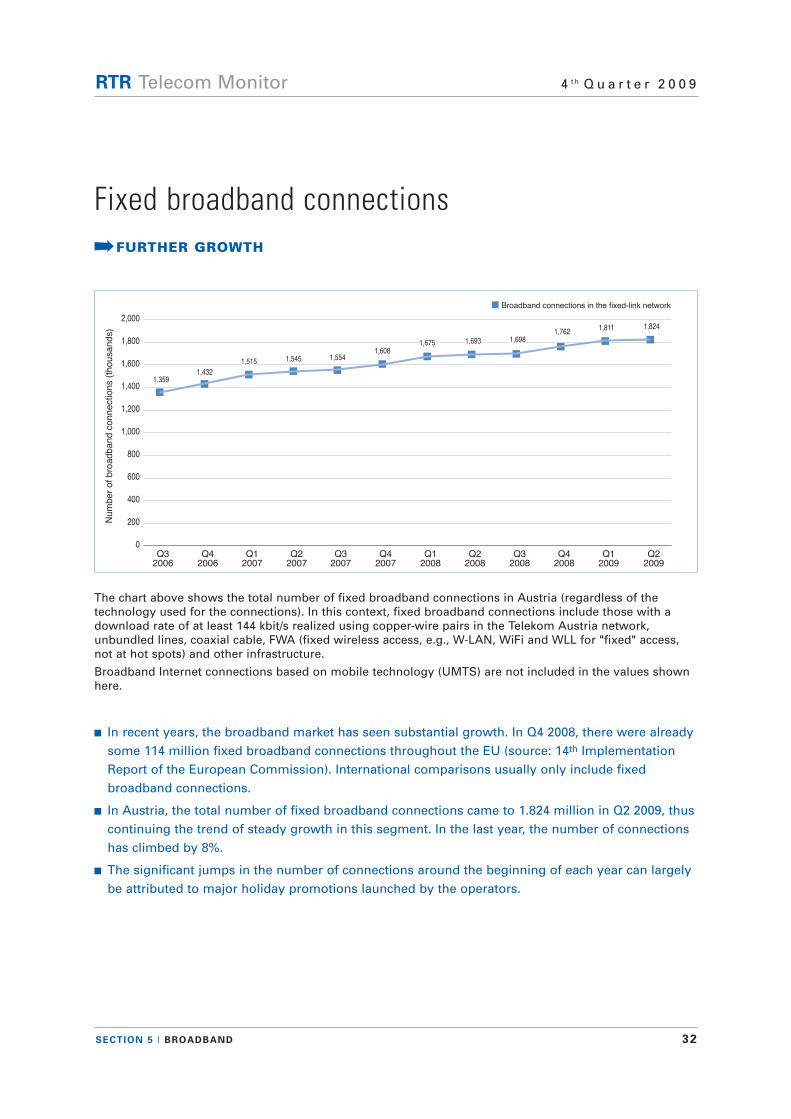

n Broadband connections in the fixed-link network

0Q3

2006

1,359

Q42006

1,432

Q12007

1,515

Q22007

1,545

Q32007

1,554

Q42007

1,608

Num

ber

of

bro

adband

co

nn

ectio

ns (

tho

usa

nd

s)

Q12008

1,675

Q22008

1,693

Q32008

1,698

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1,762

Q42008

1,811

Q12009

1,824

Q22009

The chart above shows the total number of fixed broadband connections in Austria (regardless of the technology used for the connections). In this context, fixed broadband connections include those with adownload rate of at least 144 kbit/s realized using copper-wire pairs in the Telekom Austria network,unbundled lines, coaxial cable, FWA (fixed wireless access, e.g., W-LAN, WiFi and WLL for "fixed" access,not at hot spots) and other infrastructure.

Broadband Internet connections based on mobile technology (UMTS) are not included in the values shownhere.

n In recent years, the broadband market has seen substantial growth. In Q4 2008, there were already some 114 million fixed broadband connections throughout the EU (source: 14th Implementation Report of the European Commission). International comparisons usually only include fixed broadband connections.

n In Austria, the total number of fixed broadband connections came to 1.824 million in Q2 2009, thuscontinuing the trend of steady growth in this segment. In the last year, the number of connections has climbed by 8%.

n The significant jumps in the number of connections around the beginning of each year can largely be attributed to major holiday promotions launched by the operators.

Fixed broadband connections·FURTHER GROWTH

SECTION 5 I BROADBAND 33

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Fixed broadband penetration in % of households n Fixed and mobile broadband penetration in % of households

0%Q3

2006

44%

10%

Q12007

51%

Q42006

47%

Q22007

54%

Q32007

58%

Q42007

62%

Q12008

66%

20%

30%

40%

50%

60%

Q22008

68%

Q32008

70%

70%

80%

39%

43%41%

44% 44% 45%47% 48% 48%

90%

Q42008

76%

49%

Q12009

80%

50%

Q22009

81%

51%

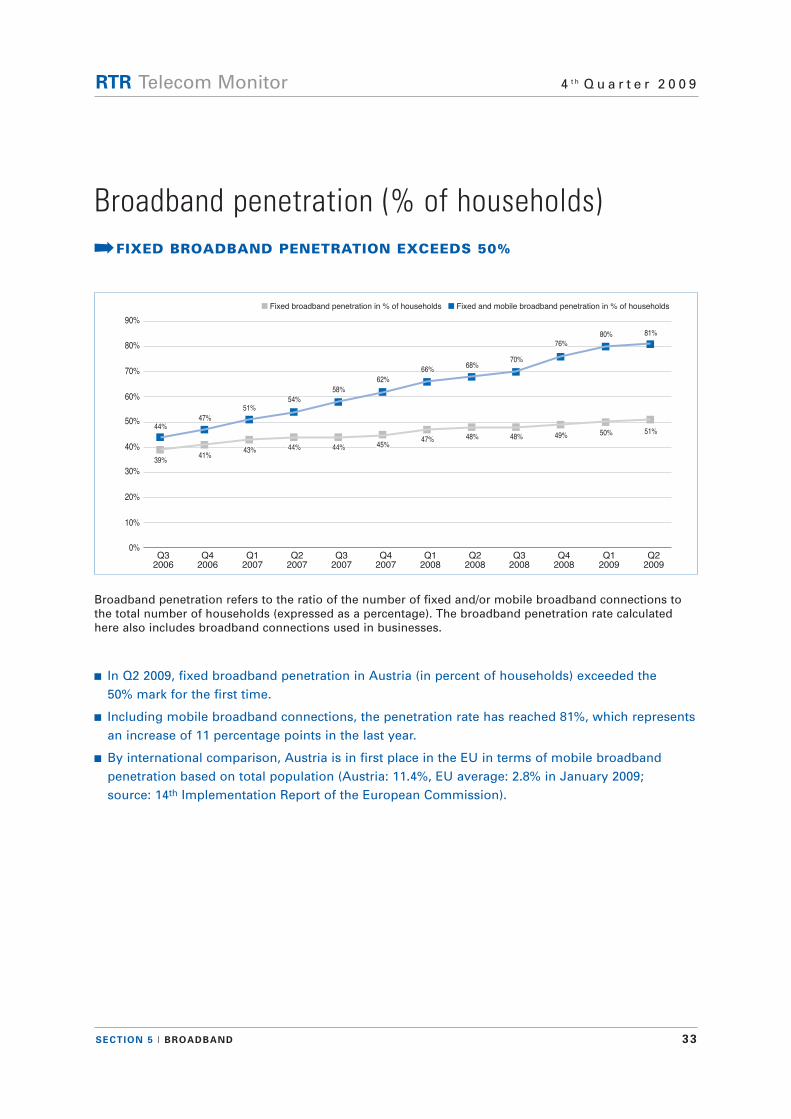

Broadband penetration refers to the ratio of the number of fixed and/or mobile broadband connections tothe total number of households (expressed as a percentage). The broadband penetration rate calculatedhere also includes broadband connections used in businesses.

n In Q2 2009, fixed broadband penetration in Austria (in percent of households) exceeded the 50% mark for the first time.

n Including mobile broadband connections, the penetration rate has reached 81%, which representsan increase of 11 percentage points in the last year.

n By international comparison, Austria is in first place in the EU in terms of mobile broadband penetration based on total population (Austria: 11.4%, EU average: 2.8% in January 2009; source: 14th Implementation Report of the European Commission).

Broadband penetration (% of households)·FIXED BROADBAND PENETRATION EXCEEDS 50%

SECTION 5 I BROADBAND 34

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

0

n TA DSL lines (copper-wire pairs) Bitstreaming in TA network nn Unbundled lines n Coaxial cable n FWA Mobile broadband Other infrastructure

Q32006

Q12007

Q42006

Q22007

Q32007

Q42007

Q12008

200,000

400,000

600,000

800,000

1,000,000

Q22008

Q32008

1,200,000

Q42008

Q12009

Q22009

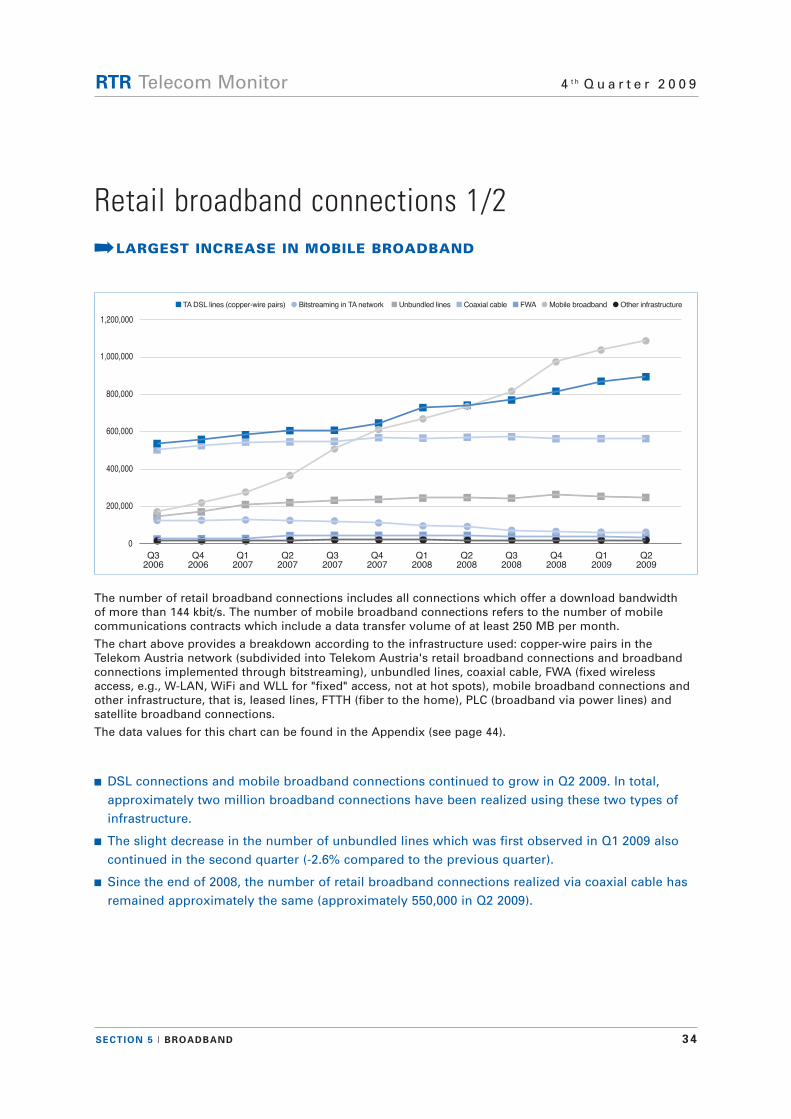

The number of retail broadband connections includes all connections which offer a download bandwidth of more than 144 kbit/s. The number of mobile broadband connections refers to the number of mobilecommunications contracts which include a data transfer volume of at least 250 MB per month.

The chart above provides a breakdown according to the infrastructure used: copper-wire pairs in theTelekom Austria network (subdivided into Telekom Austria's retail broadband connections and broadbandconnections implemented through bitstreaming), unbundled lines, coaxial cable, FWA (fixed wirelessaccess, e.g., W-LAN, WiFi and WLL for "fixed" access, not at hot spots), mobile broadband connections andother infrastructure, that is, leased lines, FTTH (fiber to the home), PLC (broadband via power lines) andsatellite broadband connections.

The data values for this chart can be found in the Appendix (see page 44).

n DSL connections and mobile broadband connections continued to grow in Q2 2009. In total, approximately two million broadband connections have been realized using these two types of infrastructure.

n The slight decrease in the number of unbundled lines which was first observed in Q1 2009 also continued in the second quarter (-2.6% compared to the previous quarter).

n Since the end of 2008, the number of retail broadband connections realized via coaxial cable has remained approximately the same (approximately 550,000 in Q2 2009).

Retail broadband connections 1/2·LARGEST INCREASE IN MOBILE BROADBAND

SECTION 5 I BROADBAND 35

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

0%

100%

n TA DSL lines (copper-wire pairs) n Bitstreaming in TA network nn Unbundled lines n Coaxial cable n FWA n Other infrastructure Mobile broadband

Q32006

Q12007

Q42006

Q22007

Q32007

Q42007

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

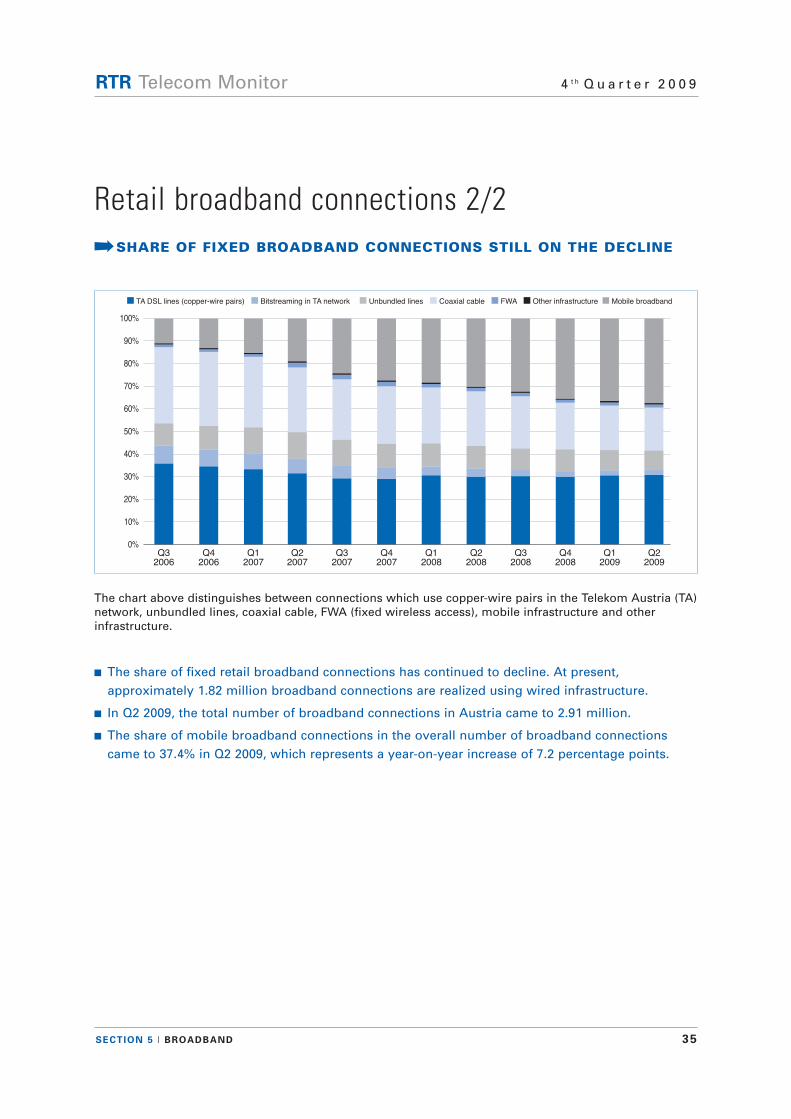

The chart above distinguishes between connections which use copper-wire pairs in the Telekom Austria (TA)network, unbundled lines, coaxial cable, FWA (fixed wireless access), mobile infrastructure and other infrastructure.

n The share of fixed retail broadband connections has continued to decline. At present, approximately 1.82 million broadband connections are realized using wired infrastructure.

n In Q2 2009, the total number of broadband connections in Austria came to 2.91 million.

n The share of mobile broadband connections in the overall number of broadband connections came to 37.4% in Q2 2009, which represents a year-on-year increase of 7.2 percentage points.

Retail broadband connections 2/2·SHARE OF FIXED BROADBAND CONNECTIONS STILL ON THE DECLINE

SECTION 5 I BROADBAND 36

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Mobile broadband connections

0Q3

2006

168,200

Q42006

216,000

Q12007

273,100

Q22007

361,900

Q32007

504,600

Q42007

607,000

Q12008

664,800

200,000

400,000

600,000

800,000

Q22008

730,700

Q32008

812,700

1,000,000

1,200,000

Q42008

969,500

Q12009

1,043,700

Q22009

1,087,600

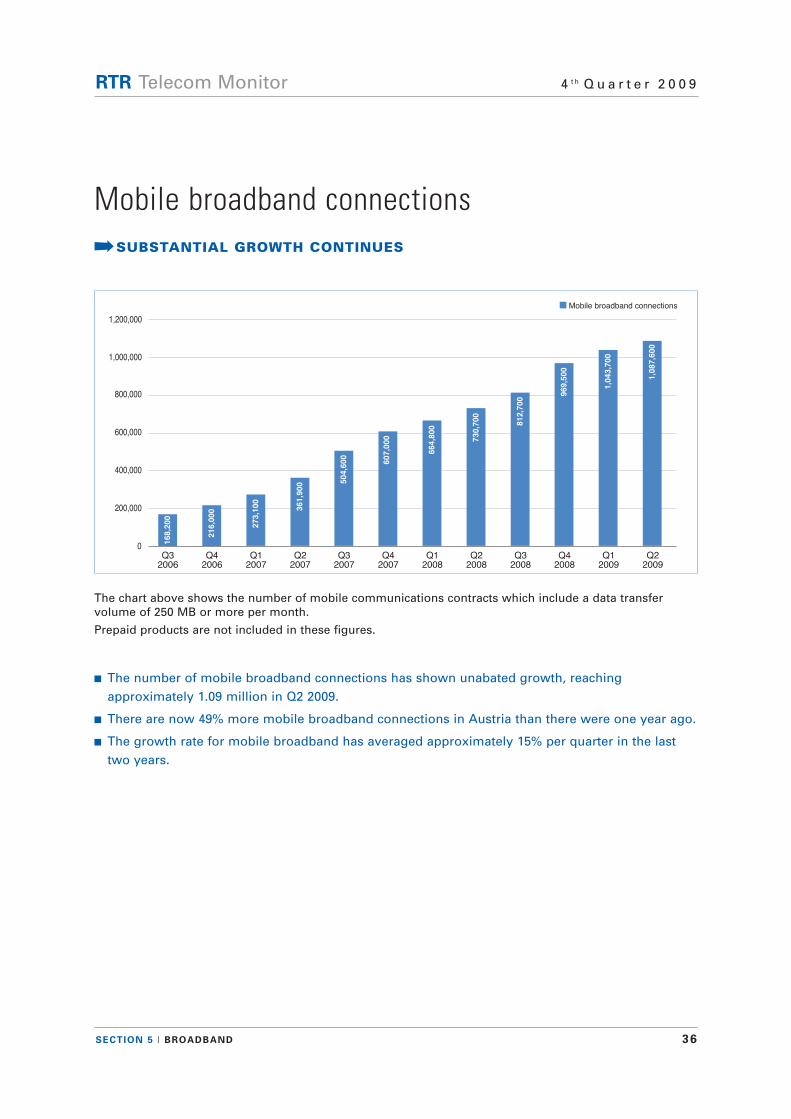

The chart above shows the number of mobile communications contracts which include a data transfer volume of 250 MB or more per month.

Prepaid products are not included in these figures.

n The number of mobile broadband connections has shown unabated growth, reaching approximately 1.09 million in Q2 2009.

n There are now 49% more mobile broadband connections in Austria than there were one year ago.

n The growth rate for mobile broadband has averaged approximately 15% per quarter in the last two years.

Mobile broadband connections·SUBSTANTIAL GROWTH CONTINUES

SECTION 5 I BROADBAND 37

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

140,000

n Wholesale broadband connections (bitstreaming in TA network) n Wholesale broadband connections (bitstreaming via unbundled lines)

Wholesale broadband connections (bitstreaming via coaxial cable; open access)

0

20,000

40,000

60,000

80,000

100,000

120,000

Q32006

121,250

Q12007

123,980

Q42006

122,640

Q22007

121,480

Q32007

119,080

Q42007

108,290

0

2,000

7,100 7,170 7,2107,970

7,5307,190

10,590 10,53010,610

15,220 15,220 15,340

Q12008

92,350

3,010

15,720

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Q22008

88,930

1,190

15,460

Q32008

68,930

1,150

15,140

Q42008

66,950

1,130

14,520

Q12009

63,350

3,210

14,610

Q22009

62,620

3,720

14,370

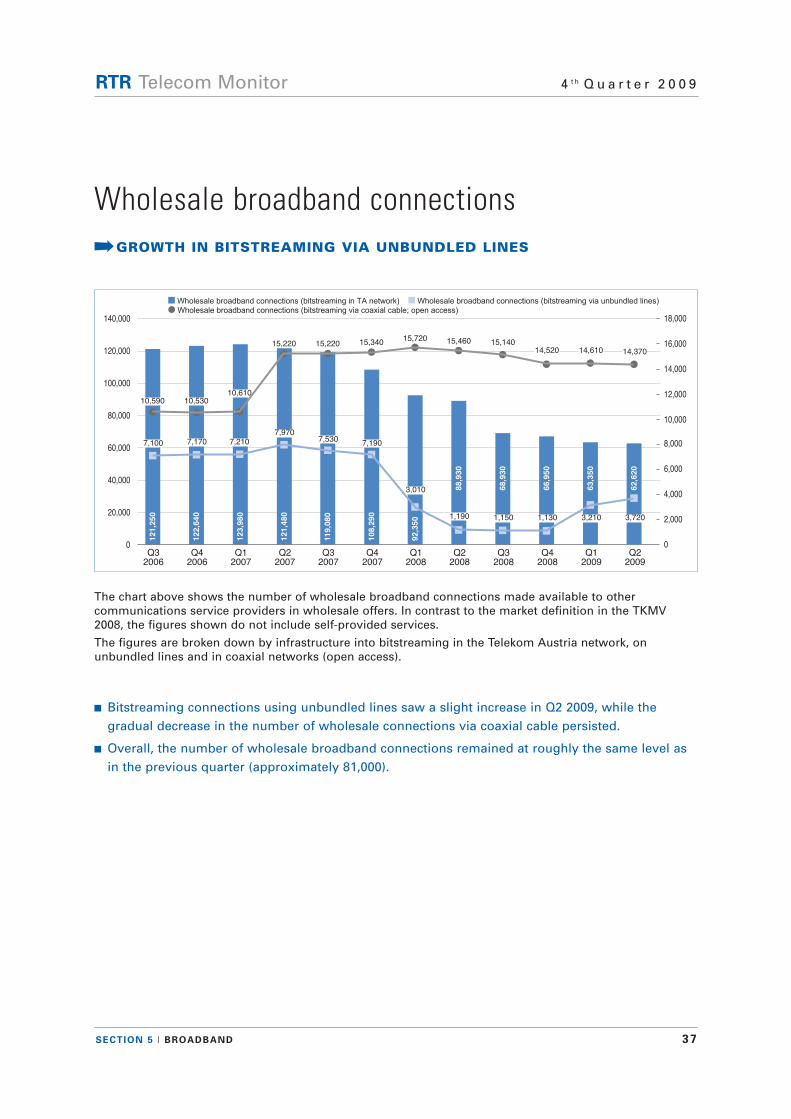

The chart above shows the number of wholesale broadband connections made available to other communications service providers in wholesale offers. In contrast to the market definition in the TKMV2008, the figures shown do not include self-provided services.

The figures are broken down by infrastructure into bitstreaming in the Telekom Austria network, on unbundled lines and in coaxial networks (open access).

n Bitstreaming connections using unbundled lines saw a slight increase in Q2 2009, while the gradual decrease in the number of wholesale connections via coaxial cable persisted.

n Overall, the number of wholesale broadband connections remained at roughly the same level as in the previous quarter (approximately 81,000).

Wholesale broadband connections·GROWTH IN BITSTREAMING VIA UNBUNDLED LINES

SECTION 5 I BROADBAND 38

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

n Revenues from retail broadband connections Revenues from wholesale broadband connections

€ 0

Revenues (

tho

usa

nd

s)

€ 20,000

€ 40,000

€ 60,000

€ 80,000

€ 100,000

€ 120,000

€ 140,000

Q32006

130,700

Q42006

137,200

Q12007

144,800

Q22007

148,200

€ 160,000

Q32007

147,500

Q42007

129,700

€ 0

€ 2,000

€ 4,000

€ 6,000

€ 8,000

€ 10,000

€ 12,000

10,400 10,60010,800 10,800 10,900

9,700

Q12008

136,100

6,700

Q22008

130,400

6,100

Q32008

126,300

4,800

Q42008

122,300

4,900

Q12009

120,200

4,100

Q22009

118,200

4,700

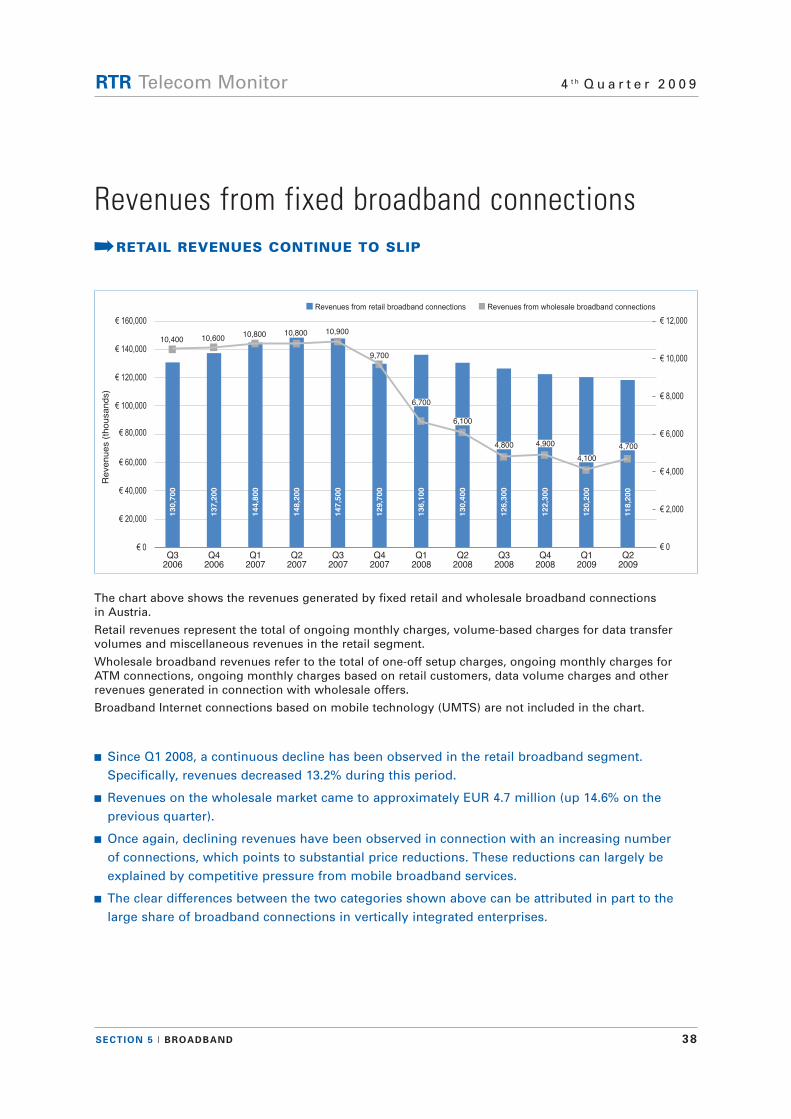

The chart above shows the revenues generated by fixed retail and wholesale broadband connections in Austria.

Retail revenues represent the total of ongoing monthly charges, volume-based charges for data transfervolumes and miscellaneous revenues in the retail segment.

Wholesale broadband revenues refer to the total of one-off setup charges, ongoing monthly charges forATM connections, ongoing monthly charges based on retail customers, data volume charges and otherrevenues generated in connection with wholesale offers.

Broadband Internet connections based on mobile technology (UMTS) are not included in the chart.

n Since Q1 2008, a continuous decline has been observed in the retail broadband segment. Specifically, revenues decreased 13.2% during this period.

n Revenues on the wholesale market came to approximately EUR 4.7 million (up 14.6% on the previous quarter).

n Once again, declining revenues have been observed in connection with an increasing number of connections, which points to substantial price reductions. These reductions can largely be explained by competitive pressure from mobile broadband services.

n The clear differences between the two categories shown above can be attributed in part to the large share of broadband connections in vertically integrated enterprises.

Revenues from fixed broadband connections·RETAIL REVENUES CONTINUE TO SLIP

39

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 6 Business indicators

SECTION 6 I BUSINESS INDICATORS 40

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

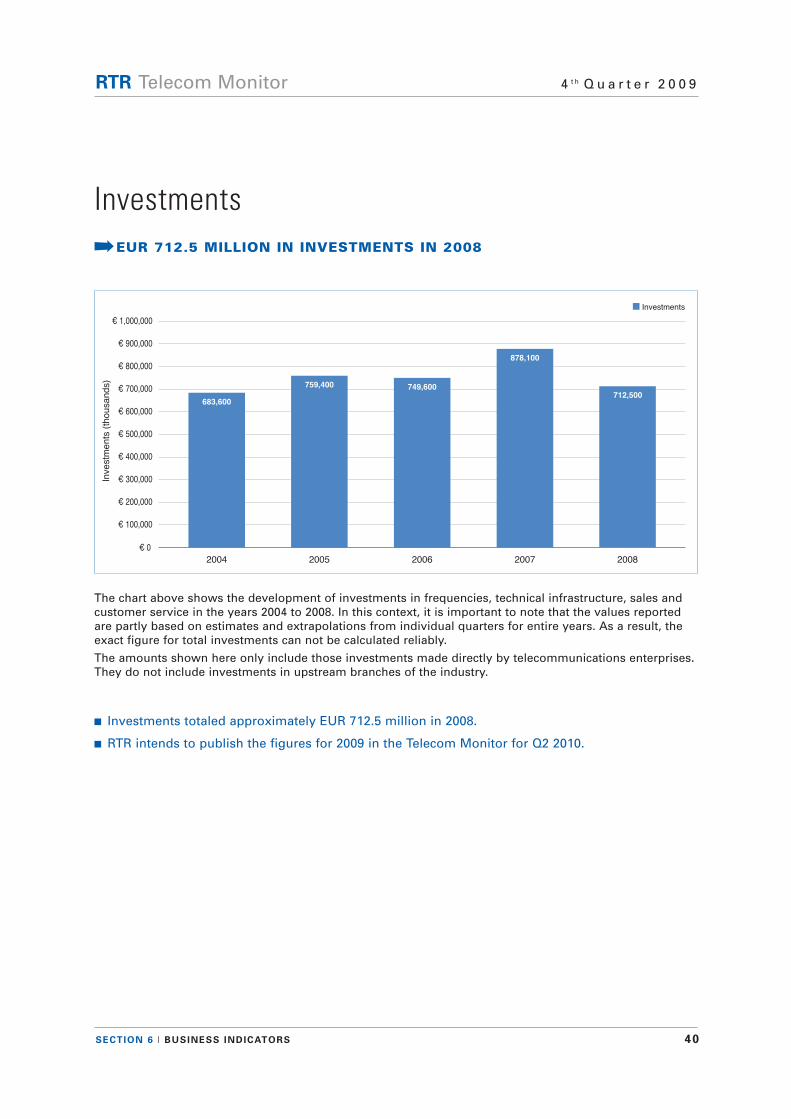

n Investments

€ 0

2004 2005

759,400

683,600

€ 100,000

Investm

ents

(th

ou

sa

nd

s)

2006

749,600

2007

878,100

€ 200,000

€ 300,000

€ 400,000

€ 500,000

€ 600,000

€ 700,000

€ 800,000

€ 900,000

€ 1,000,000

2008

712,500

The chart above shows the development of investments in frequencies, technical infrastructure, sales andcustomer service in the years 2004 to 2008. In this context, it is important to note that the values reportedare partly based on estimates and extrapolations from individual quarters for entire years. As a result, theexact figure for total investments can not be calculated reliably.

The amounts shown here only include those investments made directly by telecommunications enterprises.They do not include investments in upstream branches of the industry.

n Investments totaled approximately EUR 712.5 million in 2008.

n RTR intends to publish the figures for 2009 in the Telecom Monitor for Q2 2010.

Investments·EUR 712.5 MILLION IN INVESTMENTS IN 2008

SECTION 6 I BUSINESS INDICATORS 41

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

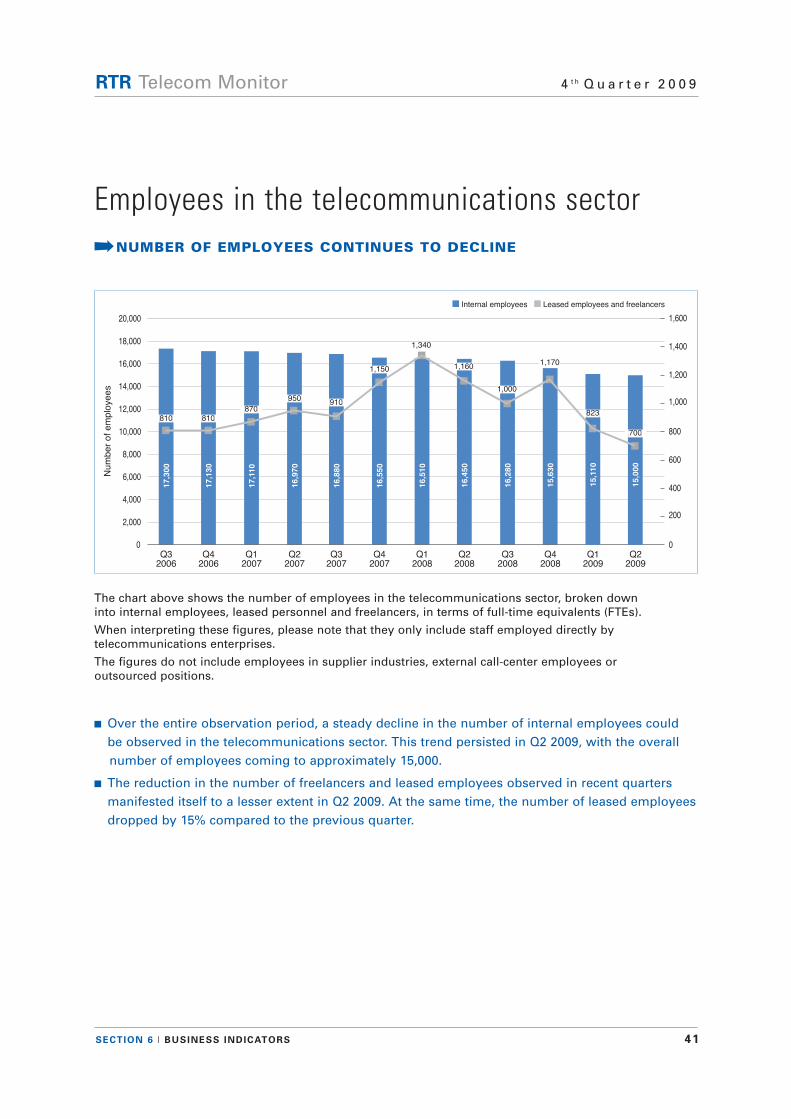

n Internal employees n Leased employees and freelancers

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Num

ber

of e

mp

loye

es

Q32006

17,300

Q12007

17,110

Q42006

17,130

Q22007

16,970

Q32007

16,880

Q42007

16,550

0

200

400

600

800

1,000

1,200

1,400

08100 0810008700

0950009100

1,150

Q12008

16,510

1,340

Q22008

16,450

1,160

Q32008

16,280

1,000

Q42008

15,630

1,170

1,600

Q12009

15,110

08230

Q22009

15,000

07000

The chart above shows the number of employees in the telecommunications sector, broken down into internal employees, leased personnel and freelancers, in terms of full-time equivalents (FTEs).

When interpreting these figures, please note that they only include staff employed directly by telecommunications enterprises.

The figures do not include employees in supplier industries, external call-center employees or outsourced positions.

n Over the entire observation period, a steady decline in the number of internal employees could be observed in the telecommunications sector. This trend persisted in Q2 2009, with the overall number of employees coming to approximately 15,000.

n The reduction in the number of freelancers and leased employees observed in recent quarters manifested itself to a lesser extent in Q2 2009. At the same time, the number of leased employeesdropped by 15% compared to the previous quarter.

Employees in the telecommunications sector·NUMBER OF EMPLOYEES CONTINUES TO DECLINE

42

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

Section 7 Appendix

SECTION 7 I APPENDIX 43

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

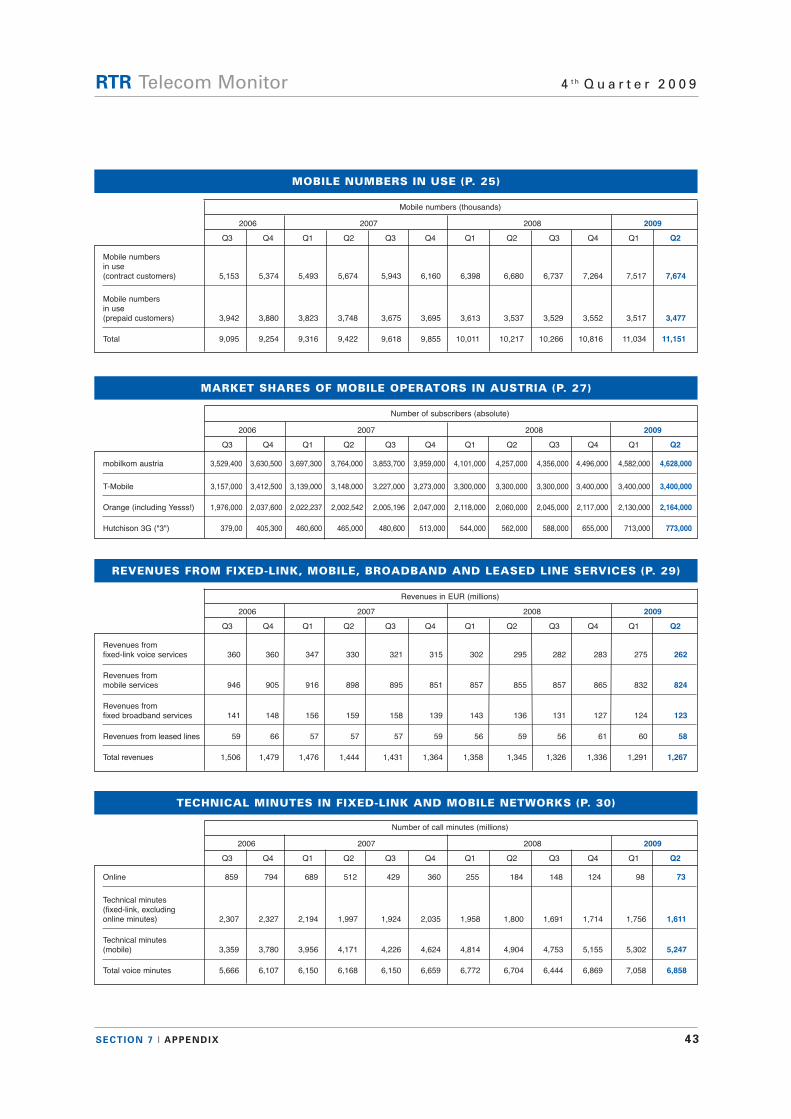

MOBILE NUMBERS IN USE (P. 25)

Mobile numbers

in use

(contract customers) 5,153 5,374 5,493 5,674 5,943 6,160 6,398 6,680 6,737 7,264 7,517 7,674

Mobile numbers

in use

(prepaid customers) 3,942 3,880 3,823 3,748 3,675 3,695 3,613 3,537 3,529 3,552 3,517 3,477

Total 9,095 9,254 9,316 9,422 9,618 9,855 10,011 10,217 10,266 10,816 11,034 11,151

Mobile numbers (thousands)

2006 2007 2008 2009

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

MARKET SHARES OF MOBILE OPERATORS IN AUSTRIA (P. 27)

mobilkom austria 3,529,400 3,630,500 3,697,300 3,764,000 3,853,700 3,959,000 4,101,000 4,257,000 4,356,000 4,496,000 4,582,000 4,628,000

T-Mobile 3,157,000 3,412,500 3,139,000 3,148,000 3,227,000 3,273,000 3,300,000 3,300,000 3,300,000 3,400,000 3,400,000 3,400,000

Orange (including Yesss!) 1,976,000 2,037,600 2,022,237 2,002,542 2,005,196 2,047,000 2,118,000 2,060,000 2,045,000 2,117,000 2,130,000 2,164,000

Hutchison 3G ("3") 379,00 405,300 460,600 465,000 480,600 513,000 544,000 562,000 588,000 655,000 713,000 773,000

2006 2007 2008 2009

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

REVENUES FROM FIXED-LINK, MOBILE, BROADBAND AND LEASED LINE SERVICES (P. 29)

Revenues from

fixed-link voice services 360 360 347 330 321 315 302 295 282 283 275 262

Revenues from

mobile services 946 905 916 898 895 851 857 855 857 865 832 824

Revenues from

fixed broadband services 141 148 156 159 158 139 143 136 131 127 124 123

Revenues from leased lines 59 66 57 57 57 59 56 59 56 61 60 58

Total revenues 1,506 1,479 1,476 1,444 1,431 1,364 1,358 1,345 1,326 1,336 1,291 1,267

Revenues in EUR (millions)

2006 2007 2008 2009

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

TECHNICAL MINUTES IN FIXED-LINK AND MOBILE NETWORKS (P. 30)

Online 859 794 689 512 429 360 255 184 148 124 98 73

Technical minutes

(fixed-link, excluding

online minutes) 2,307 2,327 2,194 1,997 1,924 2,035 1,958 1,800 1,691 1,714 1,756 1,611

Technical minutes

(mobile) 3,359 3,780 3,956 4,171 4,226 4,624 4,814 4,904 4,753 5,155 5,302 5,247

Total voice minutes 5,666 6,107 6,150 6,168 6,150 6,659 6,772 6,704 6,444 6,869 7,058 6,858

Number of call minutes (millions)

2006 2007 2008 2009

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Number of subscribers (absolute)

SECTION 7 I APPENDIX 44

RTR Telecom Monitor 4 t h Q u a r t e r 2 0 0 9

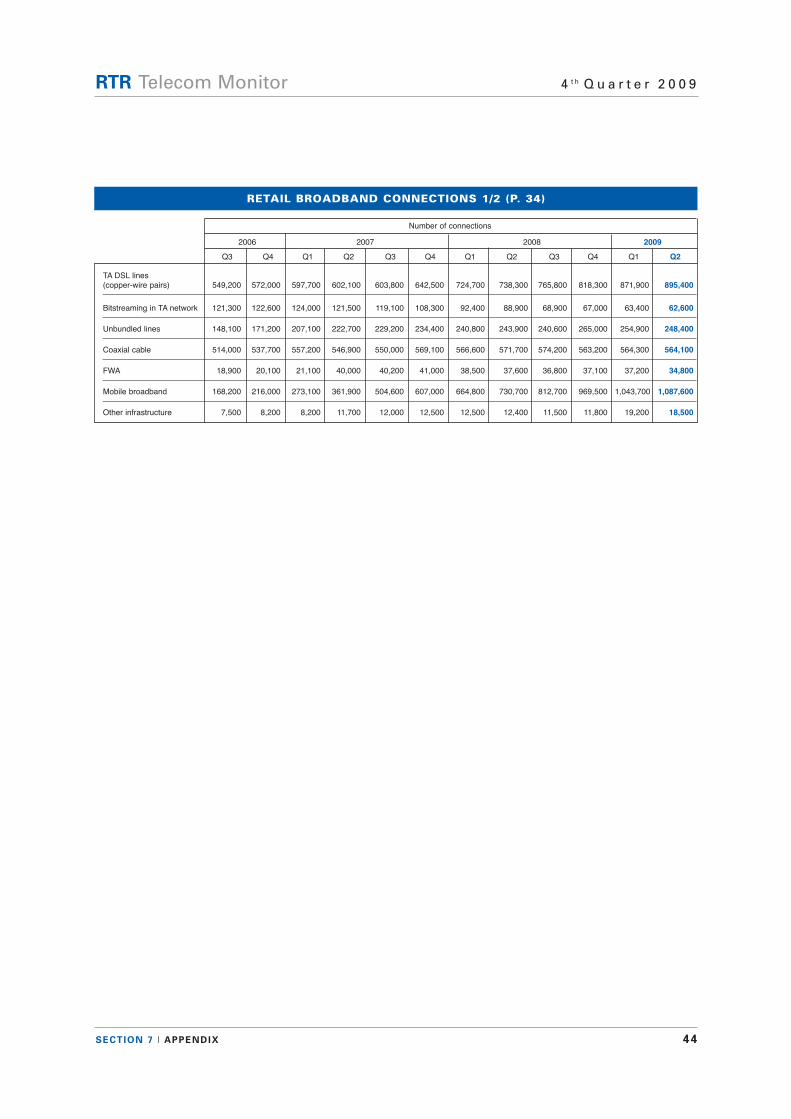

RETAIL BROADBAND CONNECTIONS 1/2 (P. 34)

TA DSL lines

(copper-wire pairs) 549,200 572,000 597,700 602,100 603,800 642,500 724,700 738,300 765,800 818,300 871,900 895,400

Bitstreaming in TA network 121,300 122,600 124,000 121,500 119,100 108,300 92,400 88,900 68,900 67,000 63,400 62,600

Unbundled lines 148,100 171,200 207,100 222,700 229,200 234,400 240,800 243,900 240,600 265,000 254,900 248,400

Coaxial cable 514,000 537,700 557,200 546,900 550,000 569,100 566,600 571,700 574,200 563,200 564,300 564,100

FWA 18,900 20,100 21,100 40,000 40,200 41,000 38,500 37,600 36,800 37,100 37,200 34,800

Mobile broadband 168,200 216,000 273,100 361,900 504,600 607,000 664,800 730,700 812,700 969,500 1,043,700 1,087,600

Other infrastructure 7,500 8,200 8,200 11,700 12,000 12,500 12,500 12,400 11,500 11,800 19,200 18,500

Number of connections

2006 2007 2008 2009

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2