Embed Size (px)

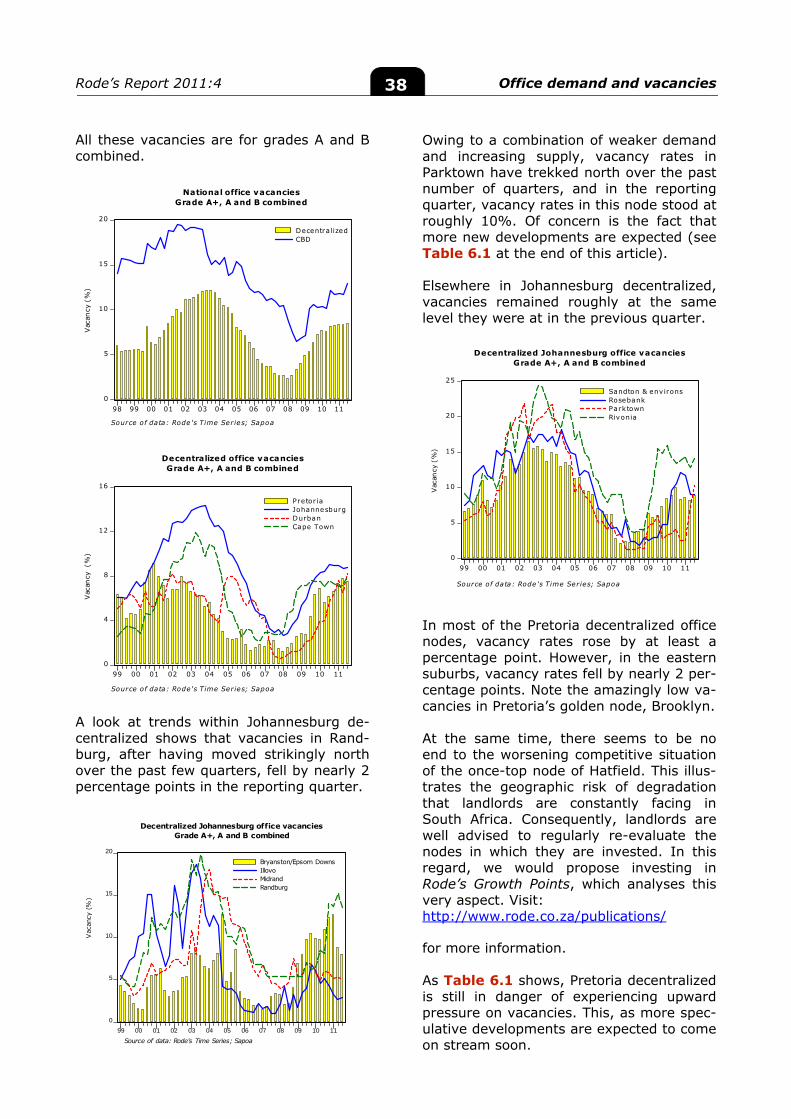

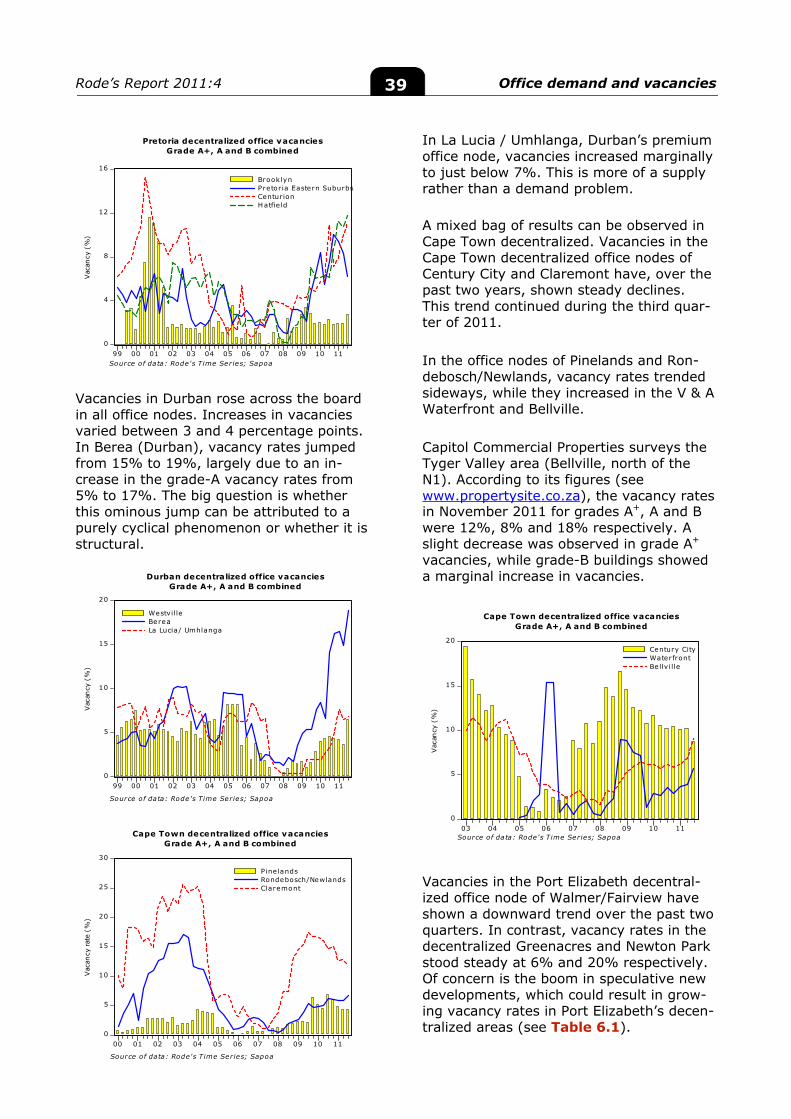

Citation preview

2011:4

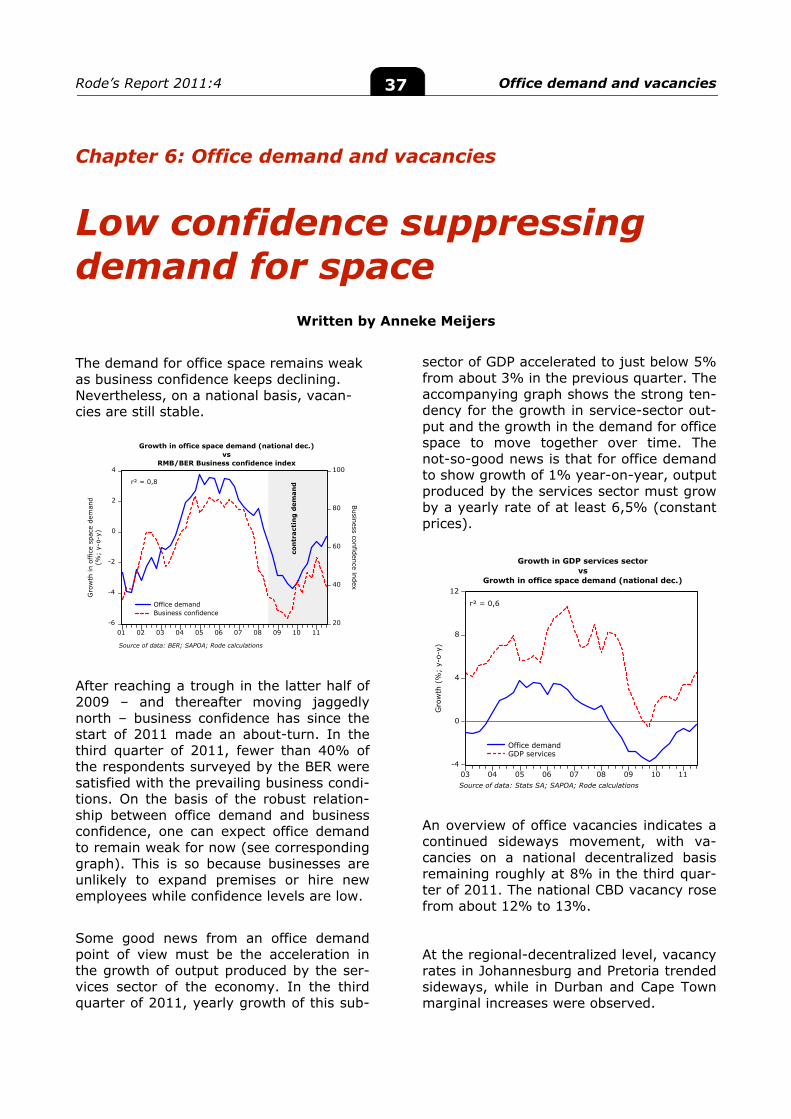

Real office rentals stutter Business cycle indicators

losing vigour, bringing with them implications for property

fundamentals Houses overvalued by 25%

PROPERTY PUBLICATIONSA DIVISION OF RODE & ASSOCIATES (PTY) LTD.www.rode.co.za

Editor-in-chiefErwin G. Rode

EditorJohn S. Lottering

Survey administratorJuwayra Januarie

AdvertisingLynette Smit

012-664 4159

SubscriptionsAngelique Claasen

021-946 2480

Annual subscription:

4 issues: R4.500,00 (excl. VAT)

Published byRode & Associates (Pty) Ltd.

Reg. No: 2009/005600/07

PO Box 1566, Bellville 7535

Tel. 021-946 2480

Fax 021-946 1238

E-mail: [email protected]

Website: www.rode.co.za

Cover illustrationKonrad Rode

082 44 66 526

www.rodegraphics.com

PrintingRSAM Printers

082 418 4878

© Rode & Associates (Pty) Ltd., December 2011. All rights reserved. No part of this publicationmay be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof the publisher. While all reasonable precaution is taken to ensure the accuracy of information,Rode & Associates (Pty) Ltd. shall not be liable to any person for inaccurate information oropinions contained in this publication. Portions of this report may be reproduced for legitimateacademic or review purposes provided due attribution is cited.

Vol. 22 no. 4

Erwin G. Rode(editor-in-chief)

John S. Lottering(editor)

on the South African Property Market2011:4

iRode’s Report 2011:4

Property is constantly in the limelight and

investors are searching for meaningful,

property-specific information. This makes

a compelling argument for finely-targeted

advertising in the Rode’s Report on the SA

Property Market. This independent analysis

is one of the most widely-read publications

of its kind.

Target audience: Rode’s Report is targeted

at investors and property practitioners such

as property developers, property managers,

landlords, merchant banks, commercial banks

and non-residential property brokers.

Continued exposure: A quarterly publication,

Rode’s Report is used as a reference source

with a long shelf life.

Rates and special advertising offers: Take

advantage of Rode’s special advertising offer:

a “first-timer” offer of 10% less on our list

price. Normal rates appear on the Rode

website.

Advertise on Rode’s website: For an

extension of your marketing, also con-

sider an advertisement on the Rode

website.

Telephone012 664 4159

Websitewww.rode.co.za

Services offered by RodeivRode’s Report 2011:4

RodePlan specialises in town and regional planning to foster pathways to enablesustainable development. This includes:

Land-use control: rezoning, subdivision, departure, consent use, removal oftitle restrictions, zoning schemesSpatial planning: spatial development frameworks (SDFs) and plans (SDPs)Governmental integrated development planning (IDP): processes andproducts, supported by a geographic information system (GIS).

RodePlan focuses on town and development planning processes and products atmacro, meso and micro level. RodePlan considers an in-depth understanding ofthe social, economic, political and environmental elements that underpin present-day society as fundamental to an SDF in order for spatial planning to complementeconomic growth and development.

Rode also advises private clients on the development potential of specific propertiesand/or land disposal strategies. This is done in collaboration with our expertiseas property economists. RodePlan's clients include property owners, developers,engineering companies and government institutions.

www.rode.co.za

SPATIAL & DEVELOPMENT PLANNERS & ECONOMISTSA DIVISION OF RODE & ASSOCIATES (PTY) LTD.

As one of South Africa's largest valuation firms, Rode annually values propertyportfolios which include shopping centres, agricultural property, residential,commercial and industrial property. Rode also undertakes municipal propertyvaluations, as well as specialized valuations such as bare dominiums.

Rode's property valuation services are underpinned by the rigorous surveying of,inter alia, market rental levels and capitalization rates. Rode's valuation servicesalso rely extensively on techniques such as regression models, as well as theopportunity cash flow (OCF) method. This ensures uniform and realistic marketvaluations, and is Rode's competitive edge.

Farm valuations

Rode's agricultural valuation department specialises in the valuation of farmsand smallholdings, and understands the value-drivers within this sector.

Bare dominiums

Rode is widely regarded by lending institutions as the authority on the valuationof bare dominiums (leased fee estates in the USA). A bare dominium propertyis usually a property with a long lease, where the cash flow of the lease has

"been" "stripped out" – e.g. by selling the present value of the cash flow of alease to a third party.

Rode Consult provides forecasts, overviews and expert opinions for corporates,government departments and private clients on a wide range of property issues.Recent outputs include:

Writing a macro overview of the South African housing market for the nationalDepartment of HousingProducing demand forecasts for specific office nodes and flats marketsProducing forecasts of rental levels using econometric modellingAnalysing property portfoliosProducing long-term forecasts of property values in South AfricaAnalysing the property market in Bloemfontein and other Free State townsActing as expert witness in arbitration and litigationConsulting for spatial and development planners and economists.

Services offered by RodevRode’s Report 2011:4

PROPERTY VALUATION & RESEARCHA DIVISION OF RODE & ASSOCIATES (PTY) LTD.

PROPERTY CONSULTANTSA DIVISION OF RODE & ASSOCIATES (PTY) LTD.

Services offered by RodeviRode’s Report 2011:4

Rode's Report on the South African Property Market

The Rode Report analyses and reports on mostsectors of the property market. It covers, amongothers, trends and levels of rentals and standardcapitalization rates by property type, grade,node/township, the listed real estate market, andbuilding construction costs and building activity.Quarterly updated; print or electronic version.

Rode's South African Property Trends

Trends is aimed at general managers with strategicdecision-making power and property investment analystswho are involved in asset allocation and viability studies.It offers a statistically-based analysis and forecast byproperty type of all key indicators affecting the propertymarket, and it covers all the major metropolitan areas toprovide a complete framework for property investmentplanning. The forecasts include those for standard capitalizationrates, prime industrial and office rentals, office take-up, officevacancies, building costs, the property cycle and expected totalreturns on a notional office-building portfolio. Biannual CD publication.

Rode's Retail Report on South Africa

Rode's Retail Report contains analyses and reports onretail property, including shop rentals, operating ex-penses and escalation rates. It covers about 100 shop-ping centres and 120 street-front micro locations (high-street shops) in six metropolitan areas. Retail sales datais presented by magisterial district and by merchandisecategory. It also contains data on new shopping centres,mooted developments and extensions to existing centres.Quarterly CD publication.

PROPERTY PUBLICATIONSA DIVISION OF RODE & ASSOCIATES (PTY) LTD.

Services offered by RodeviiRode’s Report 2011:4

Rode's Time Series database

Rode updates and rents out approximately 5 000

property time series, which offer property researchers

and analysts a unique opportunity to analyse sub-

markets – from office, industrial and residential rentals

to capitalization rates and house prices covering more

than two decades. A Pro and a Lite database is available.

The main difference between the Pro and the Lite database

is that the former contains the disaggregated or nodal data.

Electronic publication on CD, updated quarterly.

Rode's Growth Points

Target market: CEOs, general management, fund in-

vestment managers, analysts

Identifies areas of growth and stagnation in order

to direct investment strategy

Nine South African cities are included: Johannesburg,

Pretoria, Cape Town, Durban, Port Elizabeth, East London,

Bloemfontein, Nelspruit, Polokwane

Updated once a year

Price on enquiry

Rode's Sales

Target market: anyone who has to estimate market

values of commercial and industrial properties, as well

as vacant land. The report analyses and reports on actual

transactions. It estimates capitalization rates and calculates

sales prices per square metre that are based on actual

transactions in contrast to the opinion surveys underlying

Rode’s Report. Users of Rode’s Sales are advised to make use

of this information in conjunction with Rode’s Report. Monthly

electronic publication.

Rode staff

Erwin RodeBA, MBA (Stell): CEO

Garth JohnsonBCom (Stell), BComHons(Econ) (UNISA), NDREES (UNISA)

Juliana DommisseBEconHons (Stell)

John S LotteringBCom(Finance)(UWC), BComHons(Econ)(UWC),MCom(Econ) (UWC)

Angelique Claasen

Abigail Jaftha

Biancé JohnsonJournalism (City Varsity)

Elizma Hawksley

Lynette Smit

Juwayra Januarie

Karen E ScottBComHons (Stell), BComHons (UCT)

Monique VernooyBTech(QS) (Cape Tech), NDREES (UNISA)

Tobi RetiefBA (Stell), NDREES (UNISA)

Madeniah JappieBScHons (Property Studies) (UCT)

Anneke MeijersBCom(Stell), BCom Hons(Econ) (Stell)

Berchtwald RodeBA (Stell), MTRP (UOFS)

Tanya Lendis

Stephan van der WaltMA (Stell)

Janelle Van HarteParalegal (School of Paralegal Studies)

Martin CarstensB Iuris, B Admin Hons (Mun Admin), M Admin (UNISA), D Admin (UP)

Rode’s Report 2011:4 Rode staffix

Contents

State of the property market

State of the property market in quarter 3 of 2011 1

Capitalization rates

Investment demand at risk of being dampened further 4

How to estimate capitalization rates – anywhere 14

Listed property

A double whammy for listed property prices 17

Office rentals, operating expenses, and office demand &vacancies

Rental office rentals stutter 21

Low confidence suppressing demand for space 37

Non-industrial land values

Office, shopping-centre and filling-station stand value 49

Industrial rentals and vacancies and industrial stand values

Business cycle indicators losing vigour 54

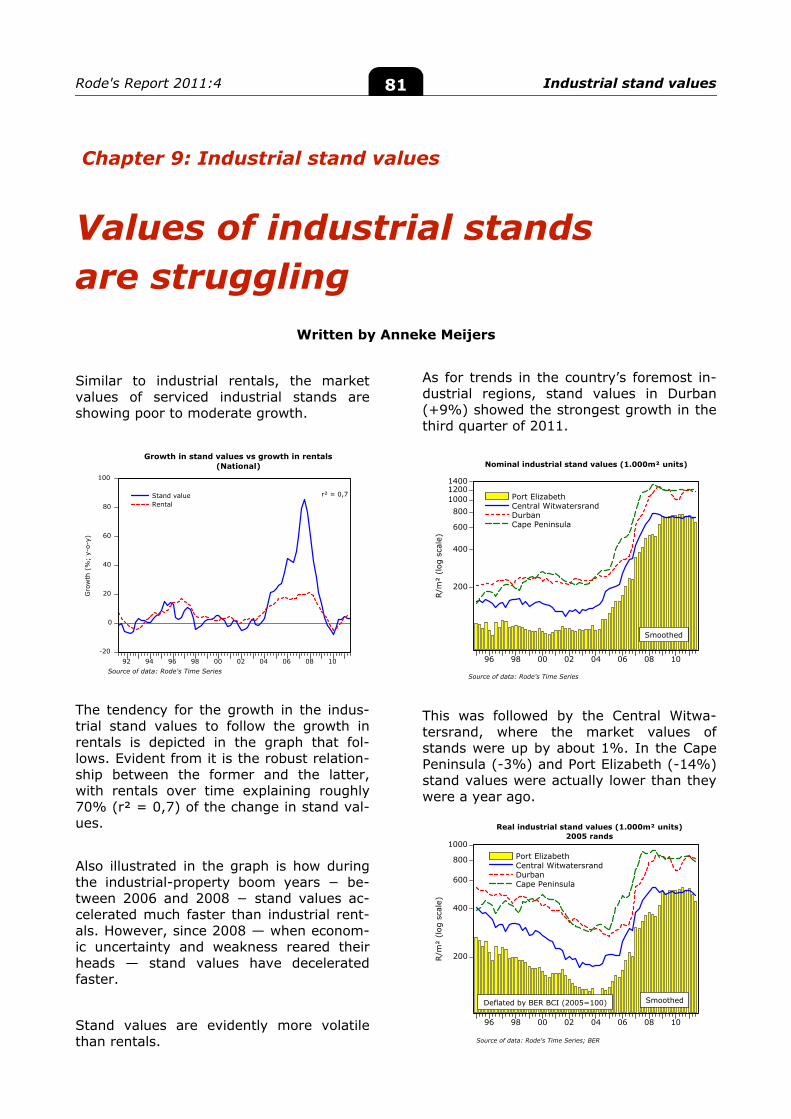

Values of industrial stands are struggling 81

Residential market

What’s up? Residential rentals stutter while retail sales are booming 104

Houses overvalued by 25% 117

Building activity & building costs

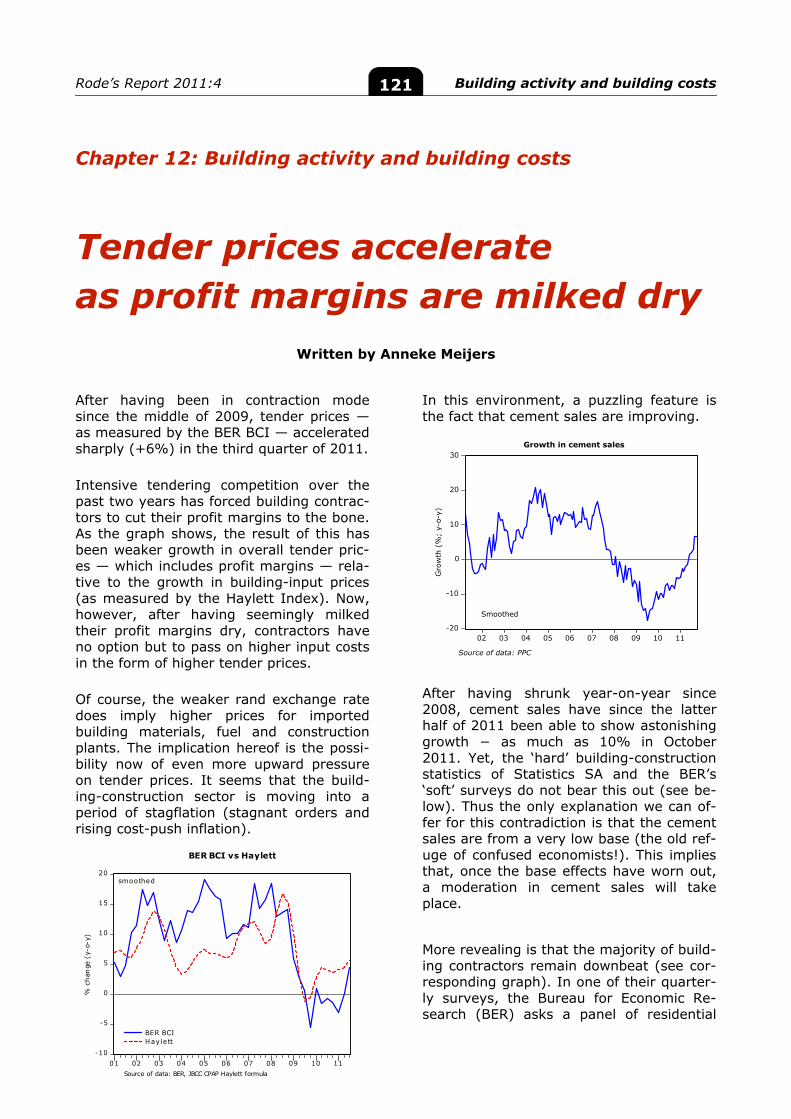

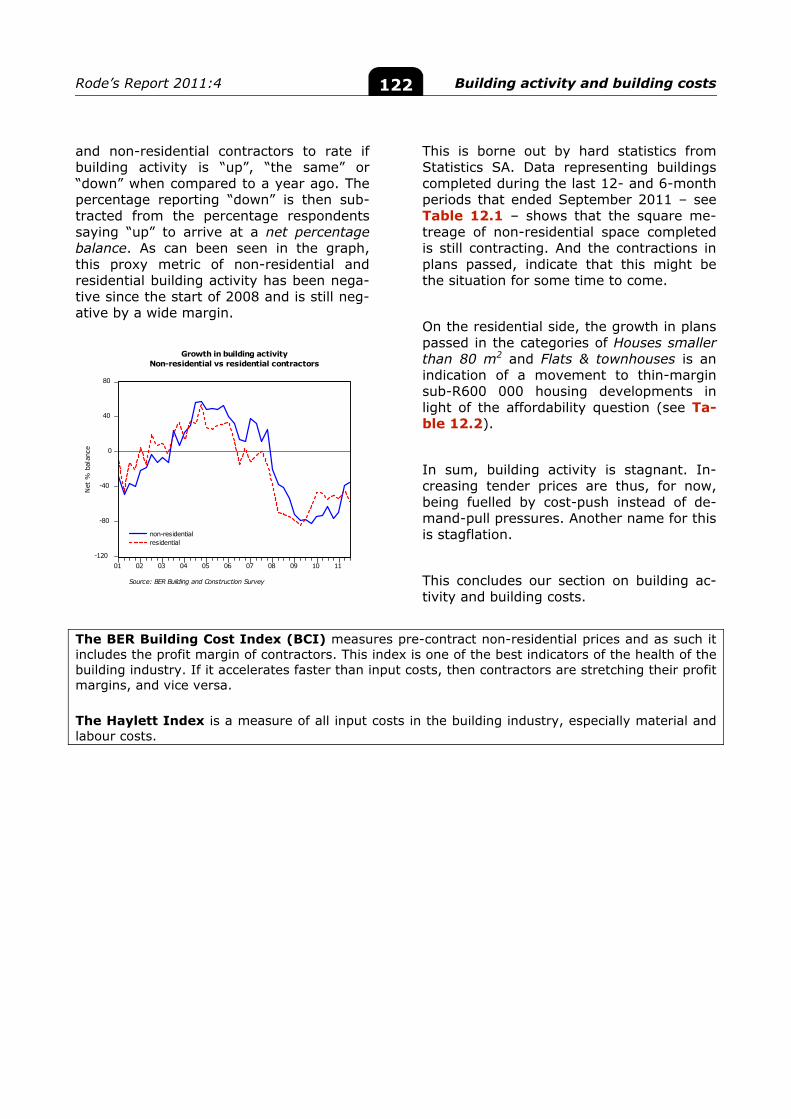

Tender prices accelerate as profit margins are milked dry 121

Rode’s Report 2011:4 Contentsxi

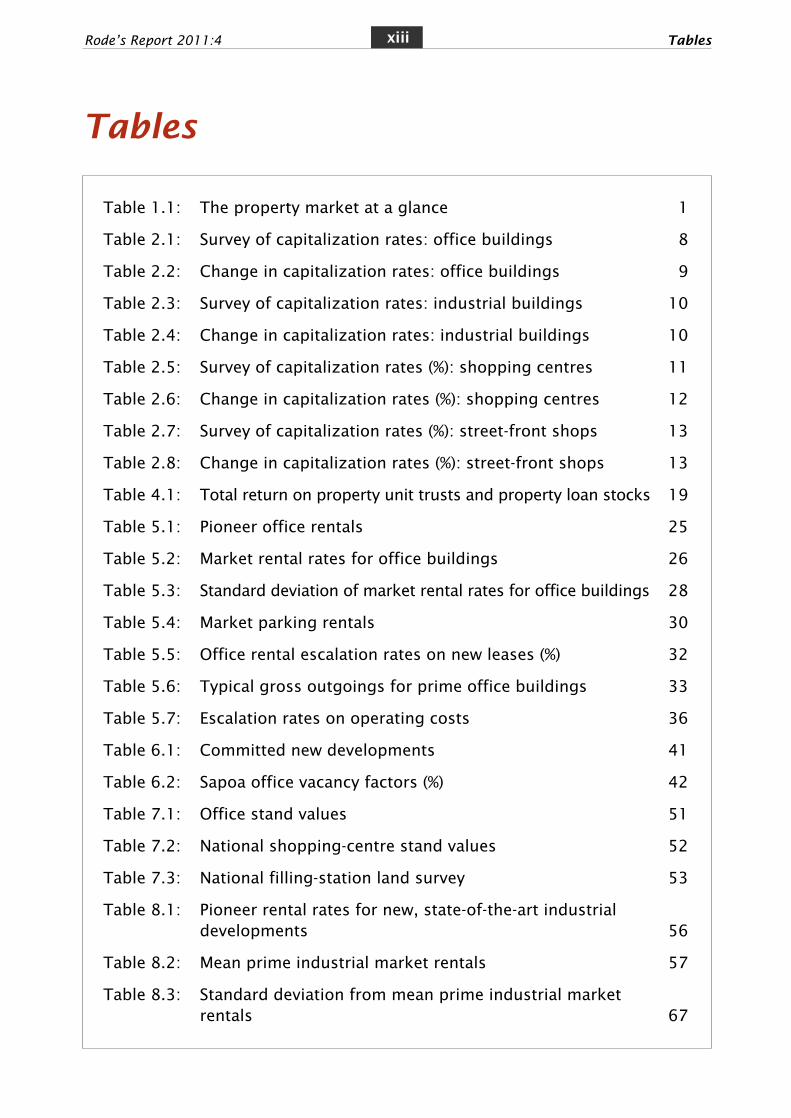

Tables

Table 1.1: The property market at a glance 1

Table 2.1: Survey of capitalization rates: office buildings 8

Table 2.2: Change in capitalization rates: office buildings 9

Table 2.3: Survey of capitalization rates: industrial buildings 10

Table 2.4: Change in capitalization rates: industrial buildings 10

Table 2.5: Survey of capitalization rates (%): shopping centres 11

Table 2.6: Change in capitalization rates (%): shopping centres 12

Table 2.7: Survey of capitalization rates (%): street-front shops 13

Table 2.8: Change in capitalization rates (%): street-front shops 13

Table 4.1: Total return on property unit trusts and property loan stocks 19

Table 5.1: Pioneer office rentals 25

Table 5.2: Market rental rates for office buildings 26

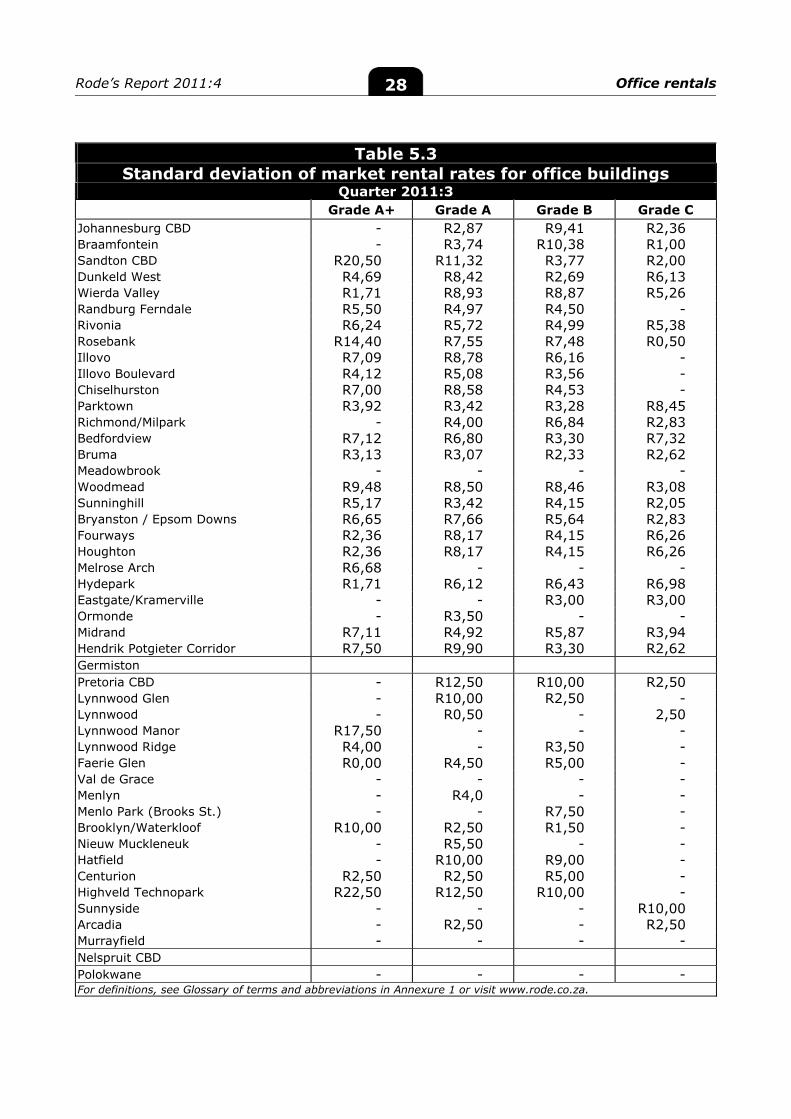

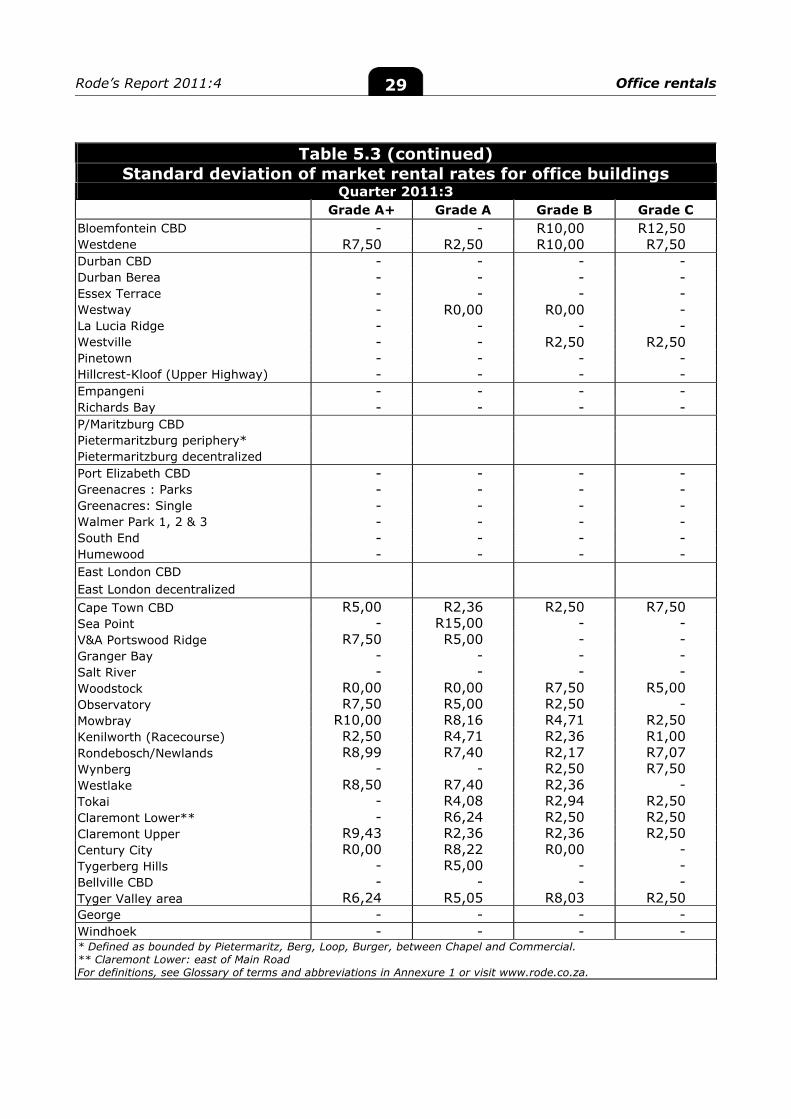

Table 5.3: Standard deviation of market rental rates for office buildings 28

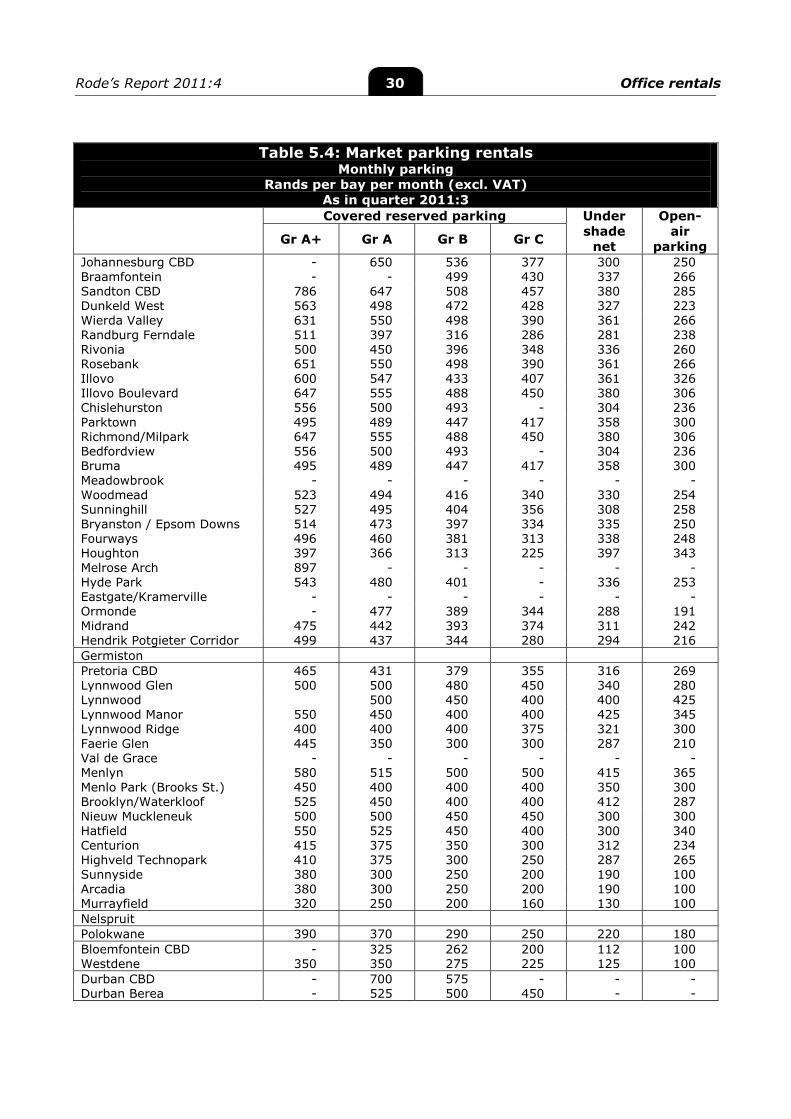

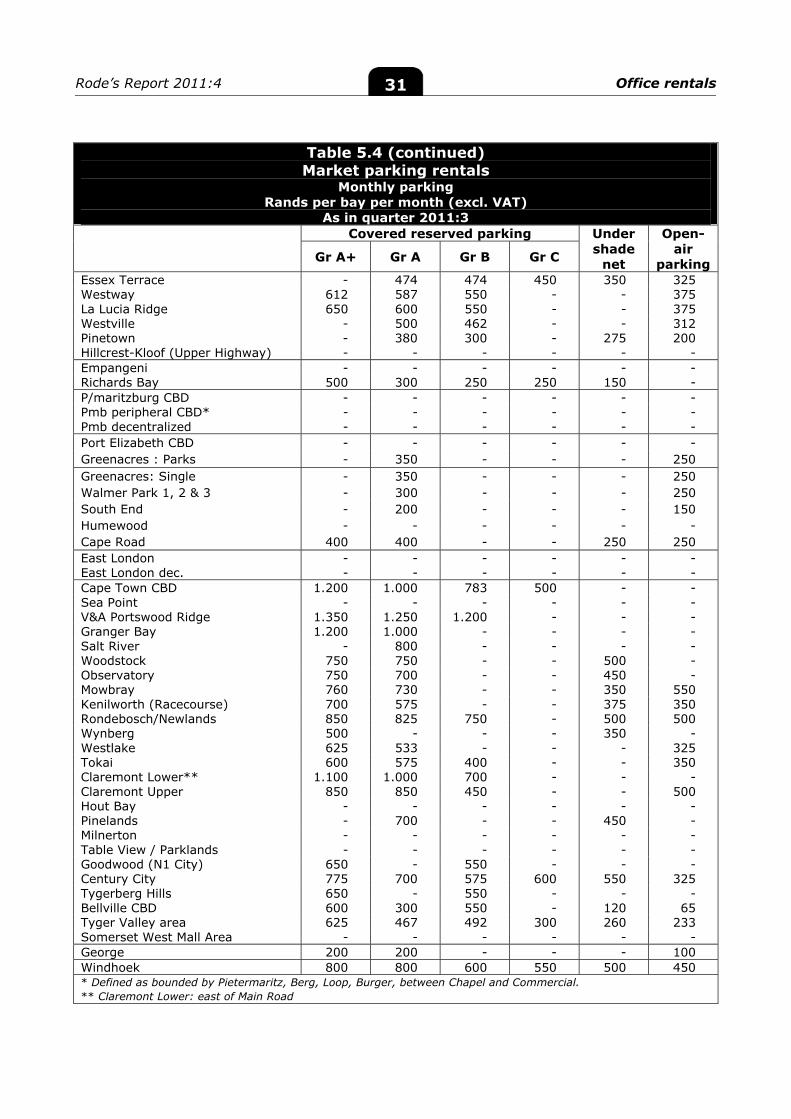

Table 5.4: Market parking rentals 30

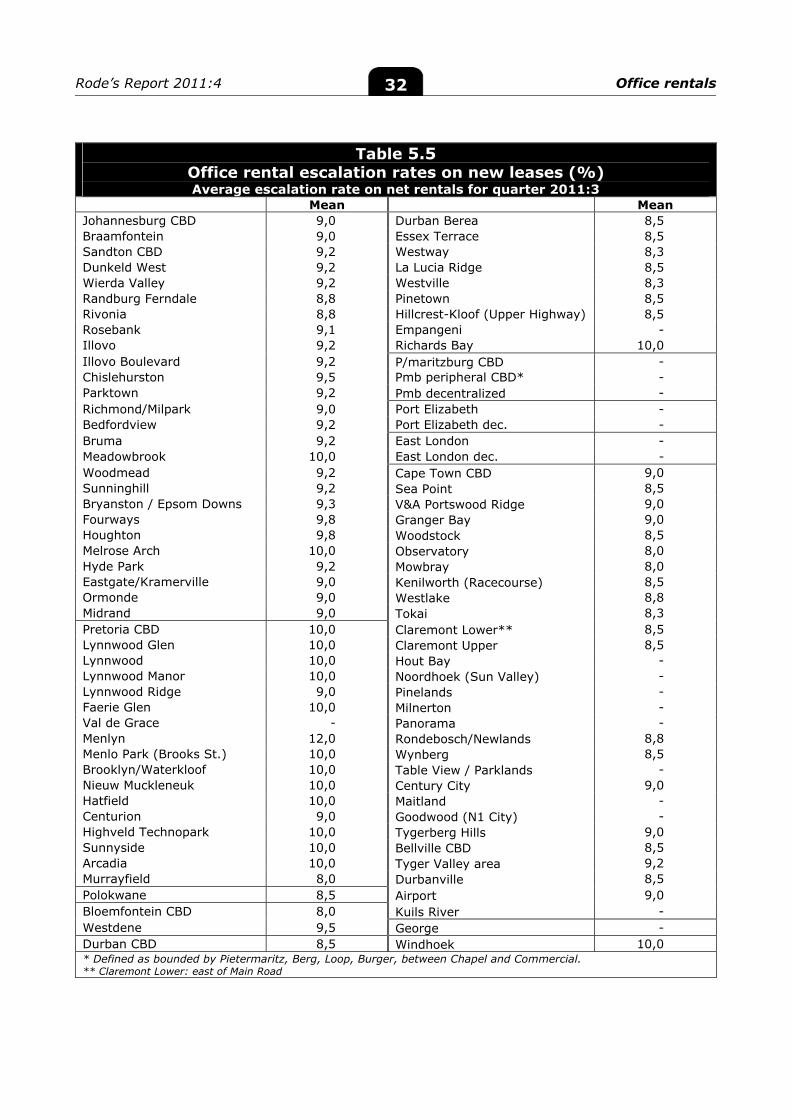

Table 5.5: Office rental escalation rates on new leases (%) 32

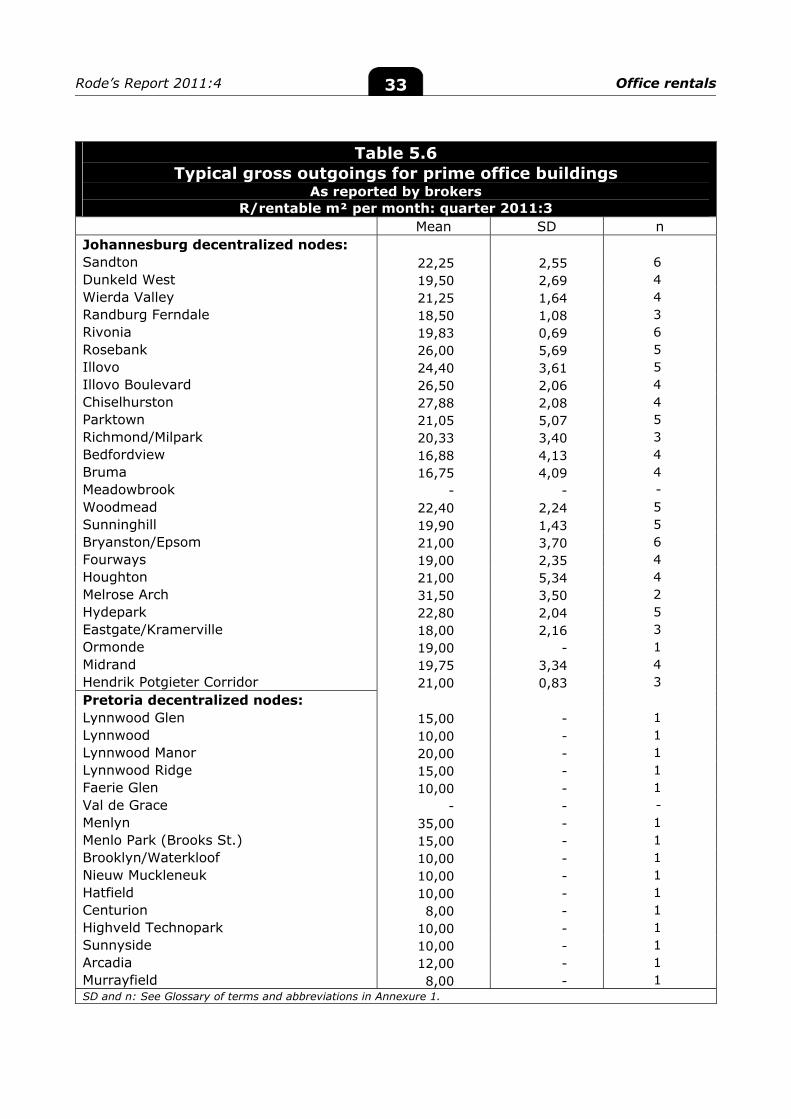

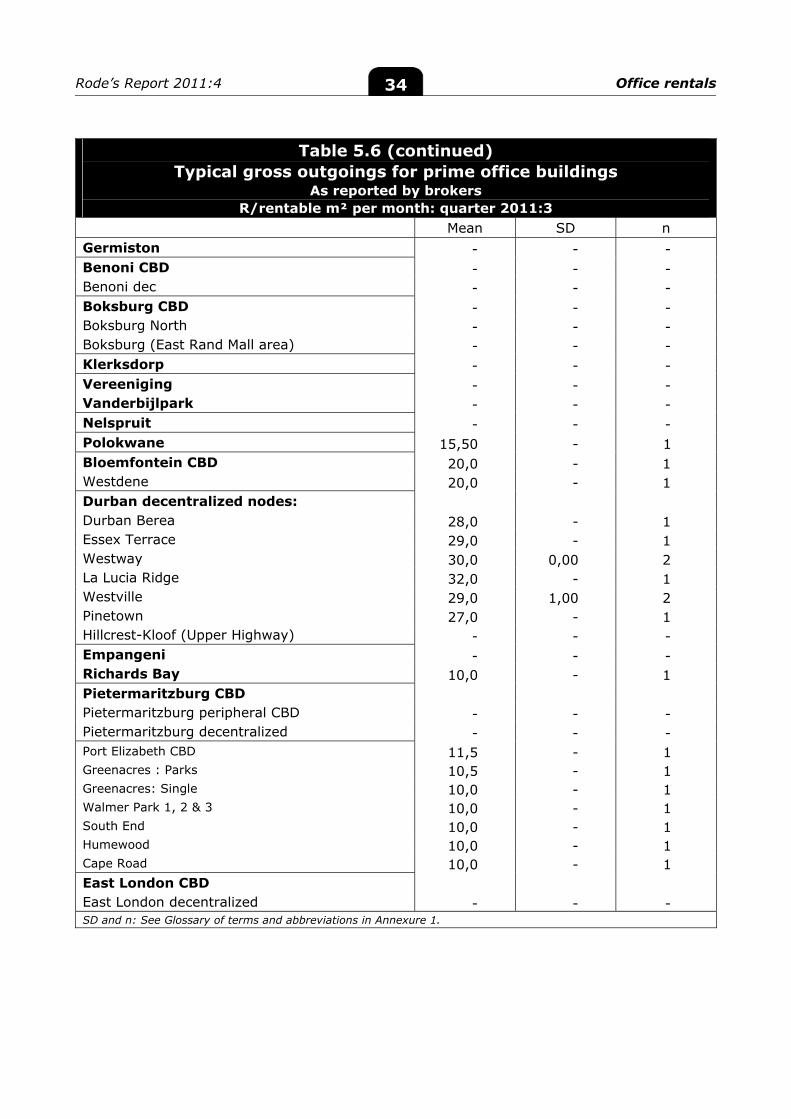

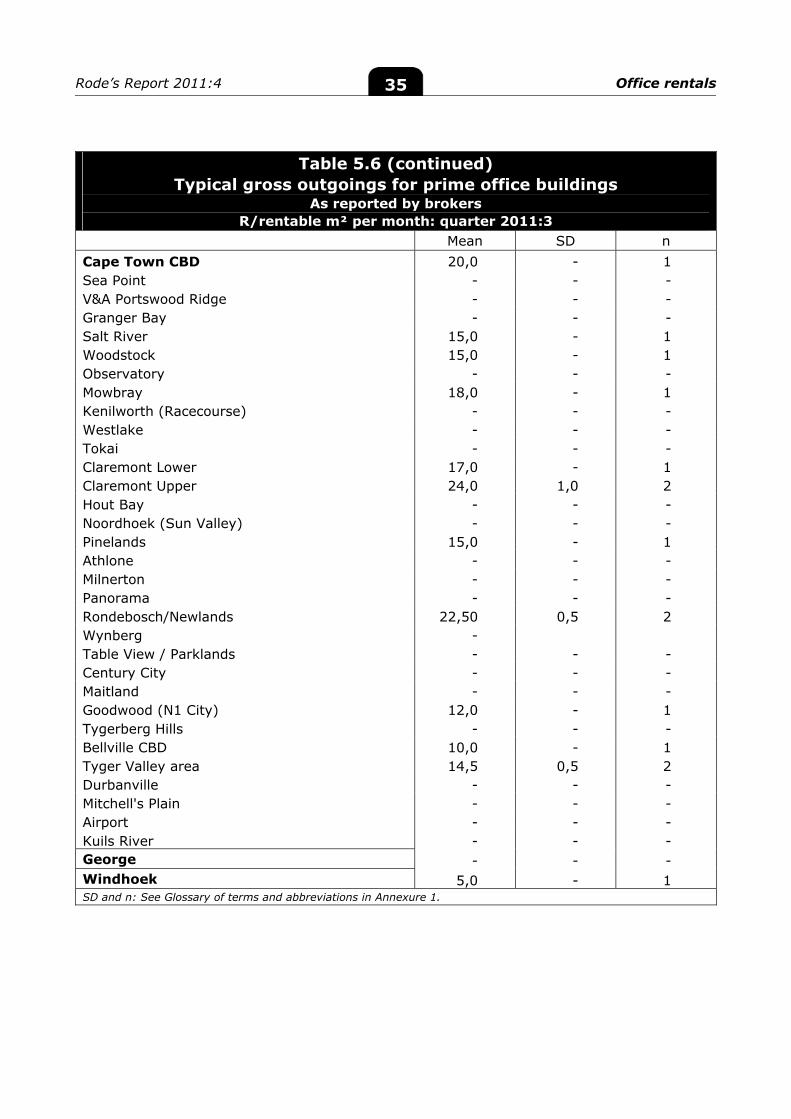

Table 5.6: Typical gross outgoings for prime office buildings 33

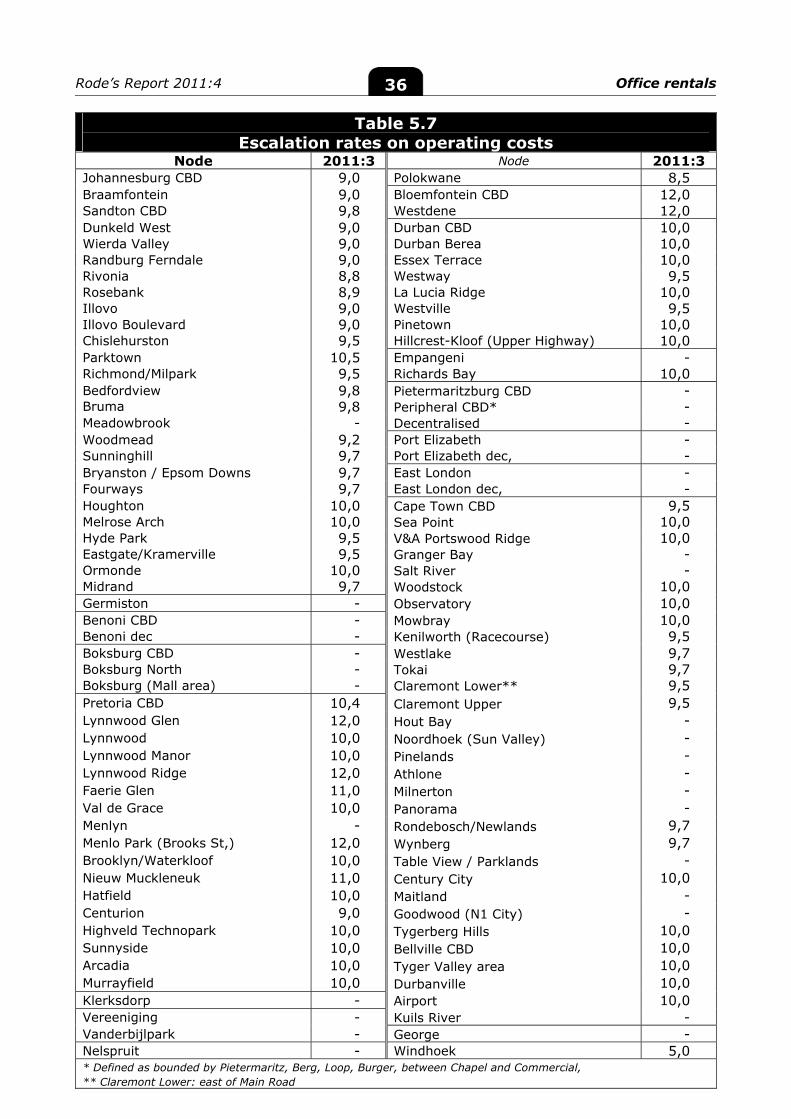

Table 5.7: Escalation rates on operating costs 36

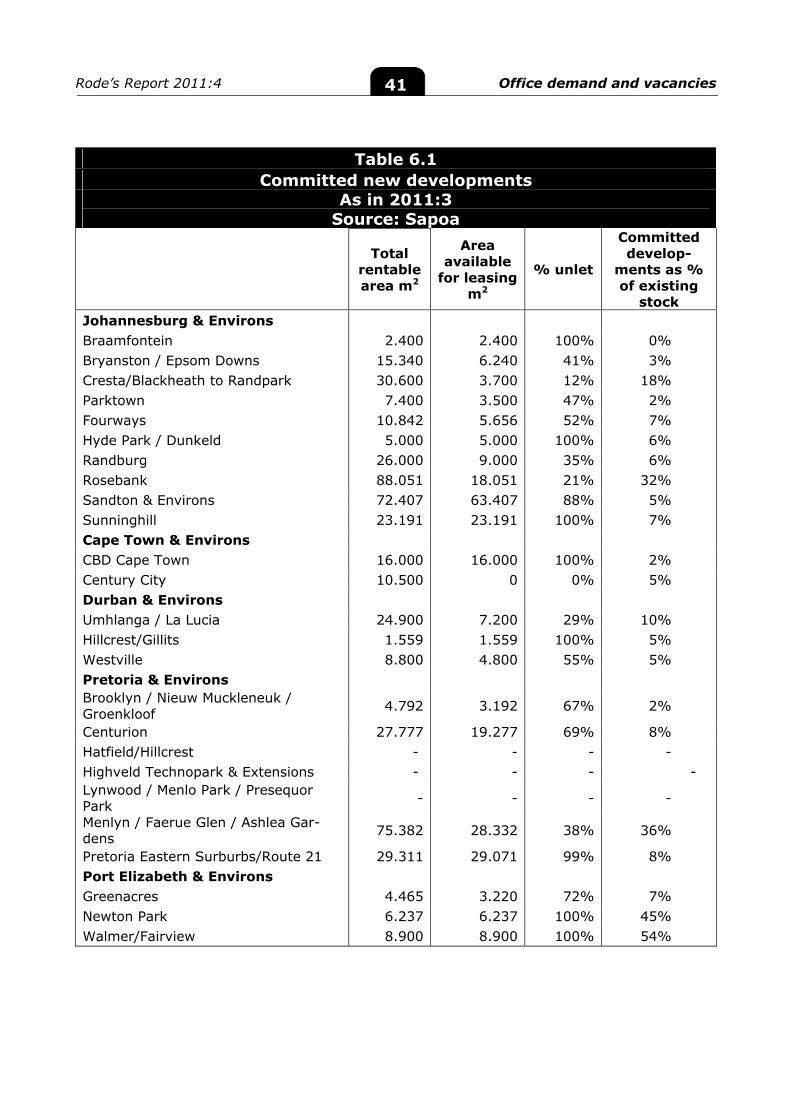

Table 6.1: Committed new developments 41

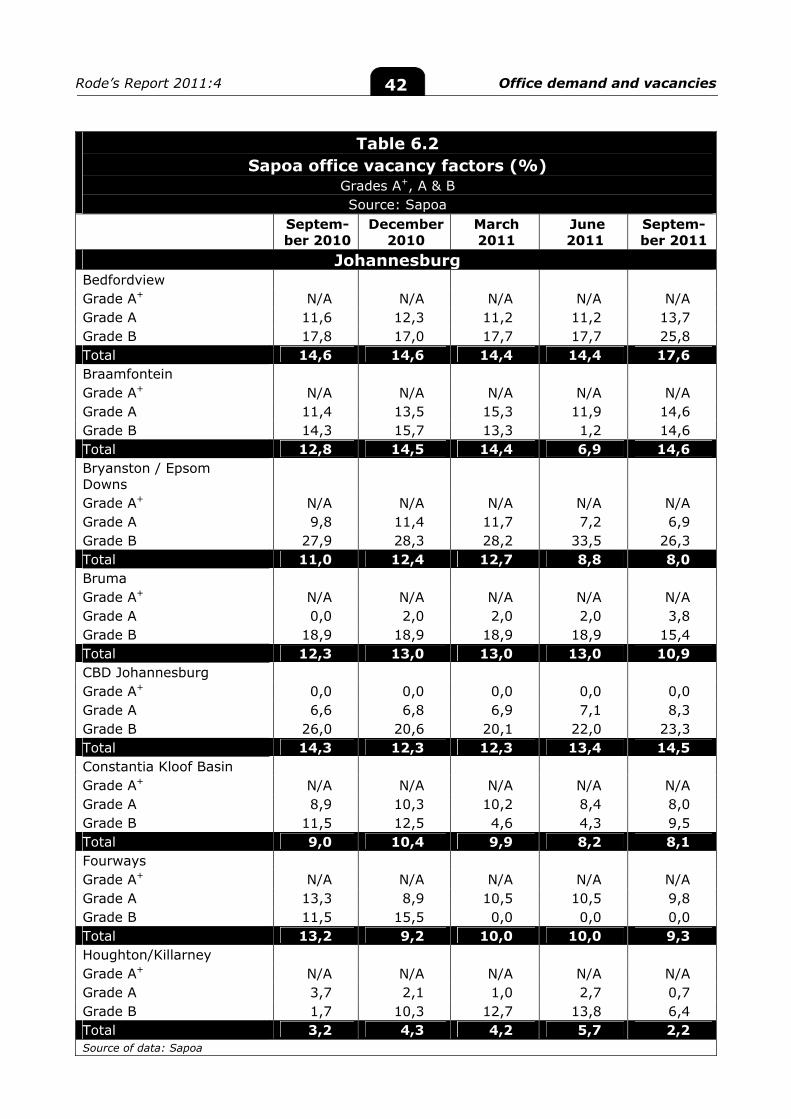

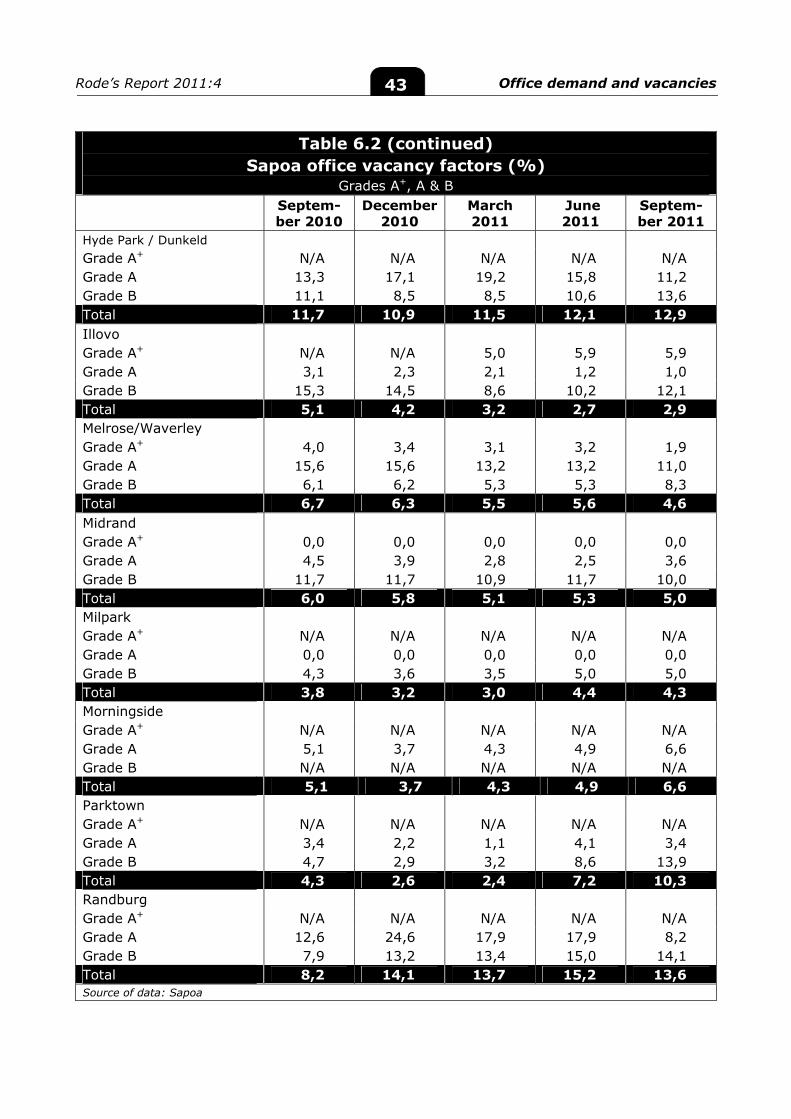

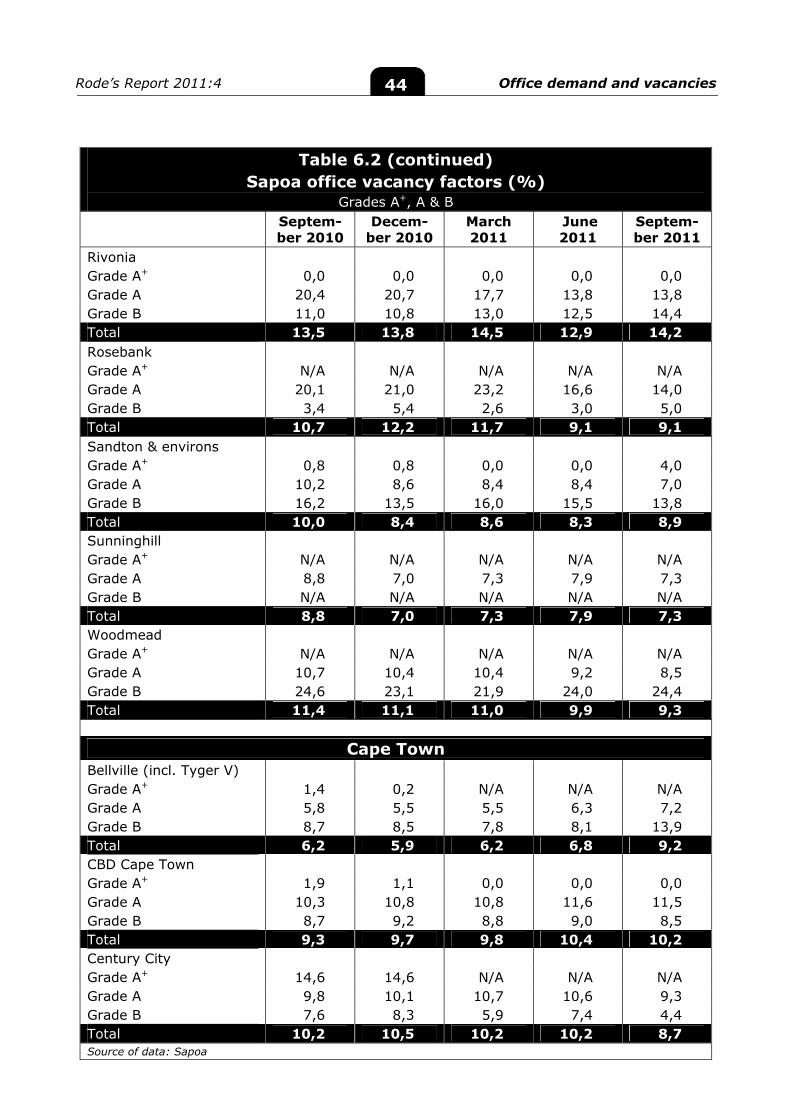

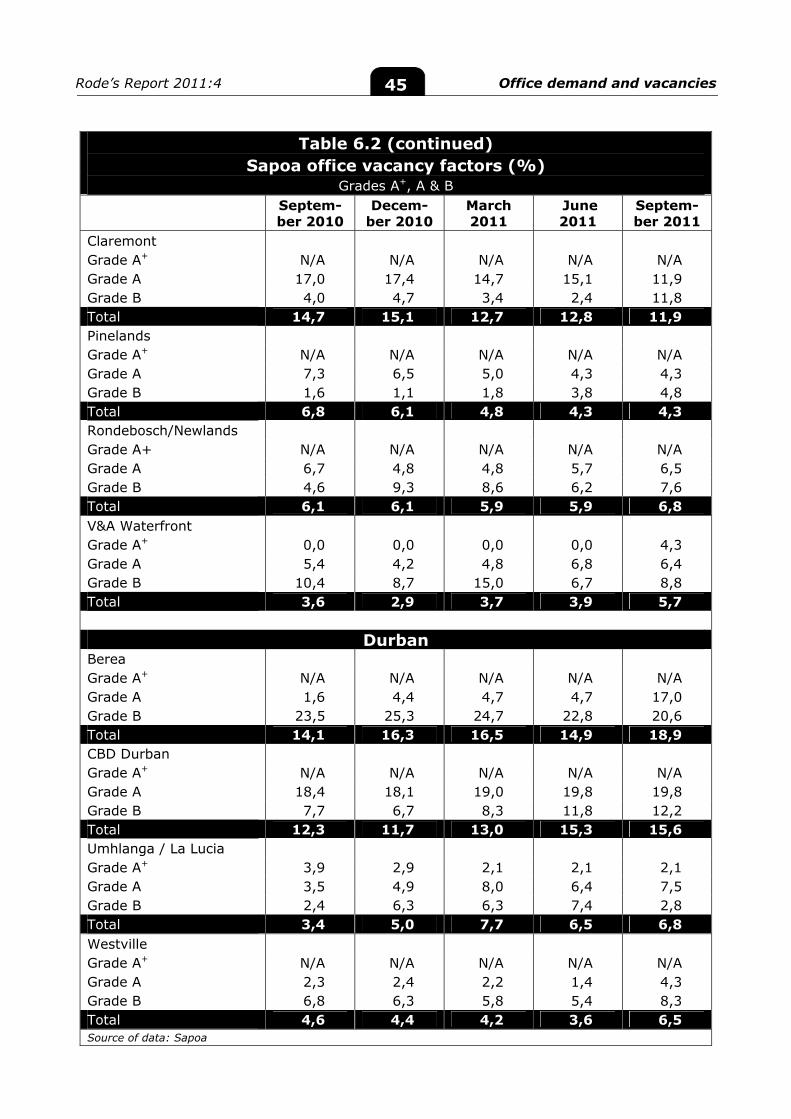

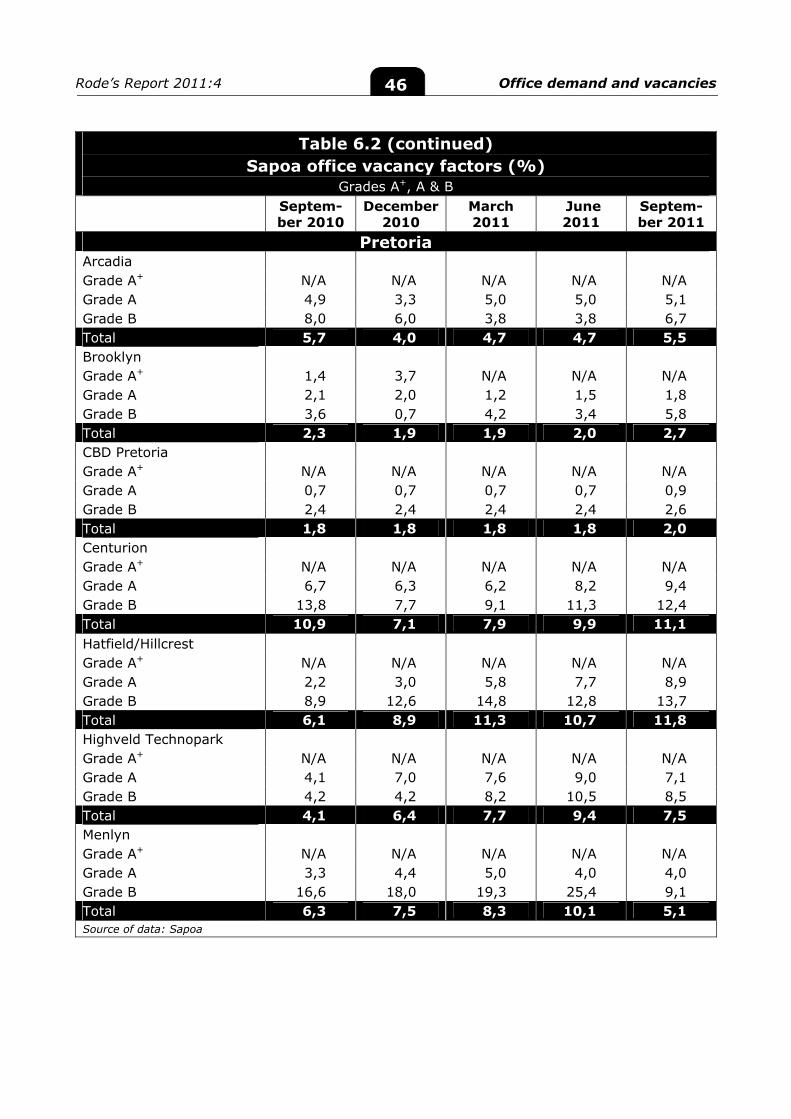

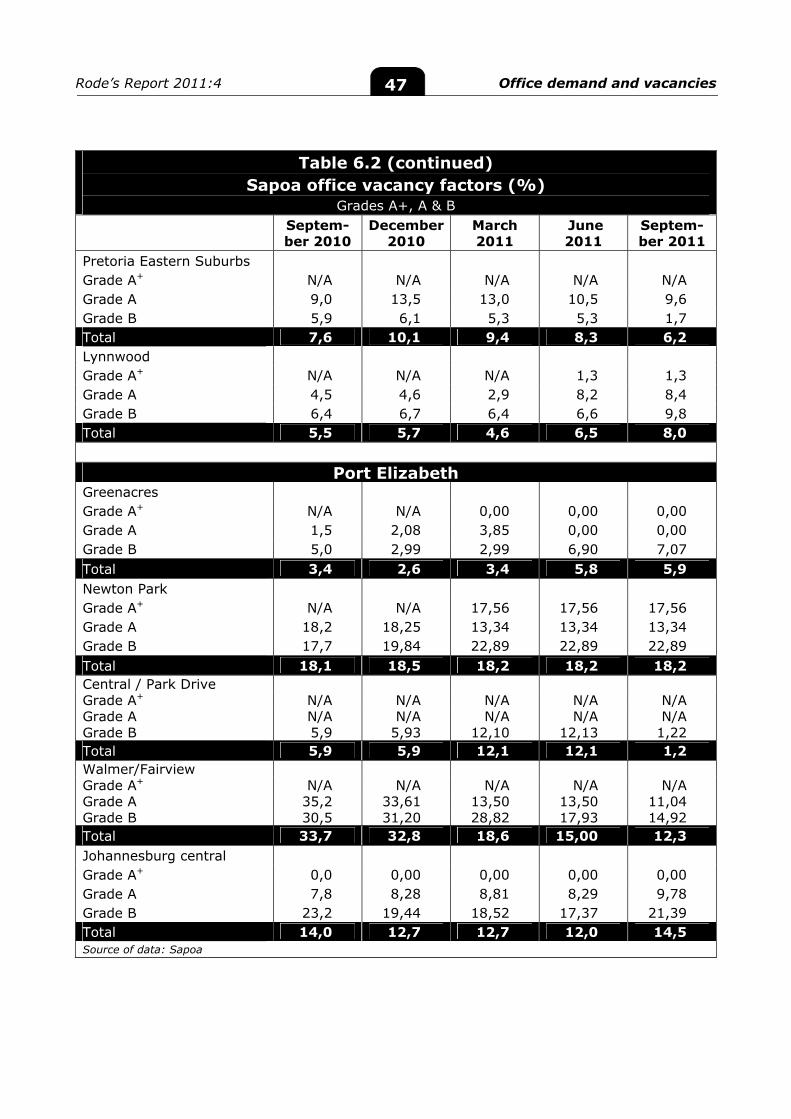

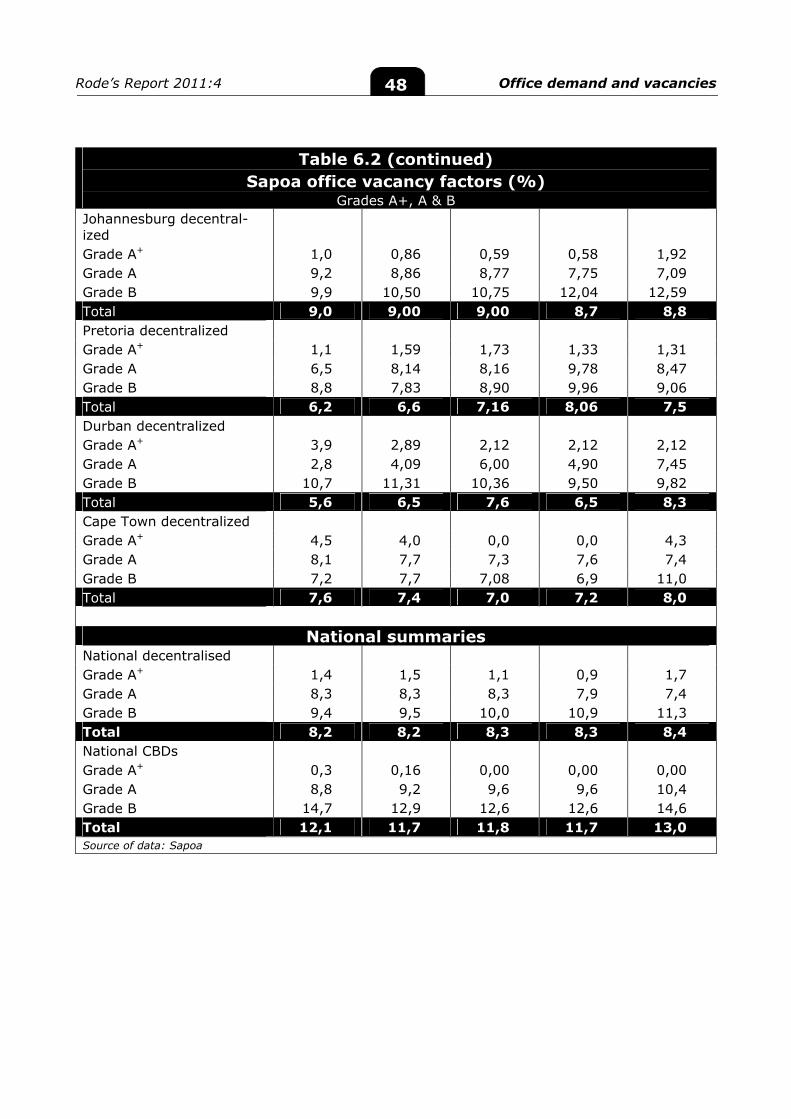

Table 6.2: Sapoa office vacancy factors (%) 42

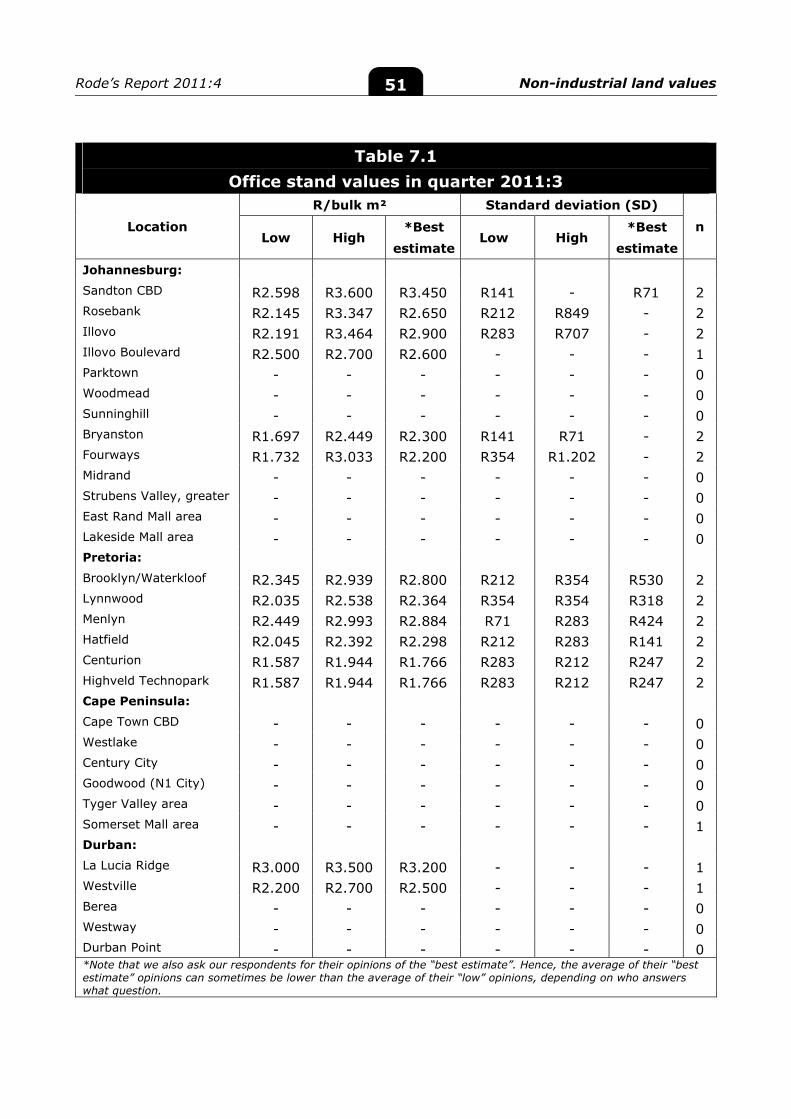

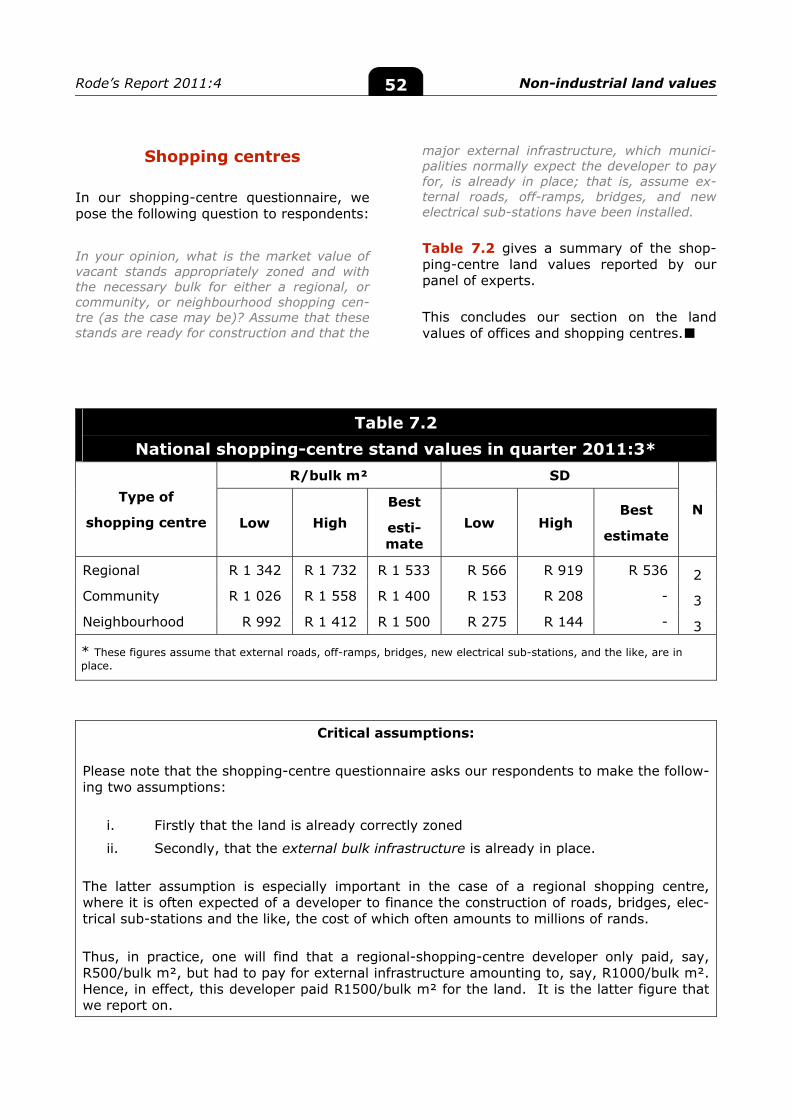

Table 7.1: Office stand values 51

Table 7.2: National shopping-centre stand values 52

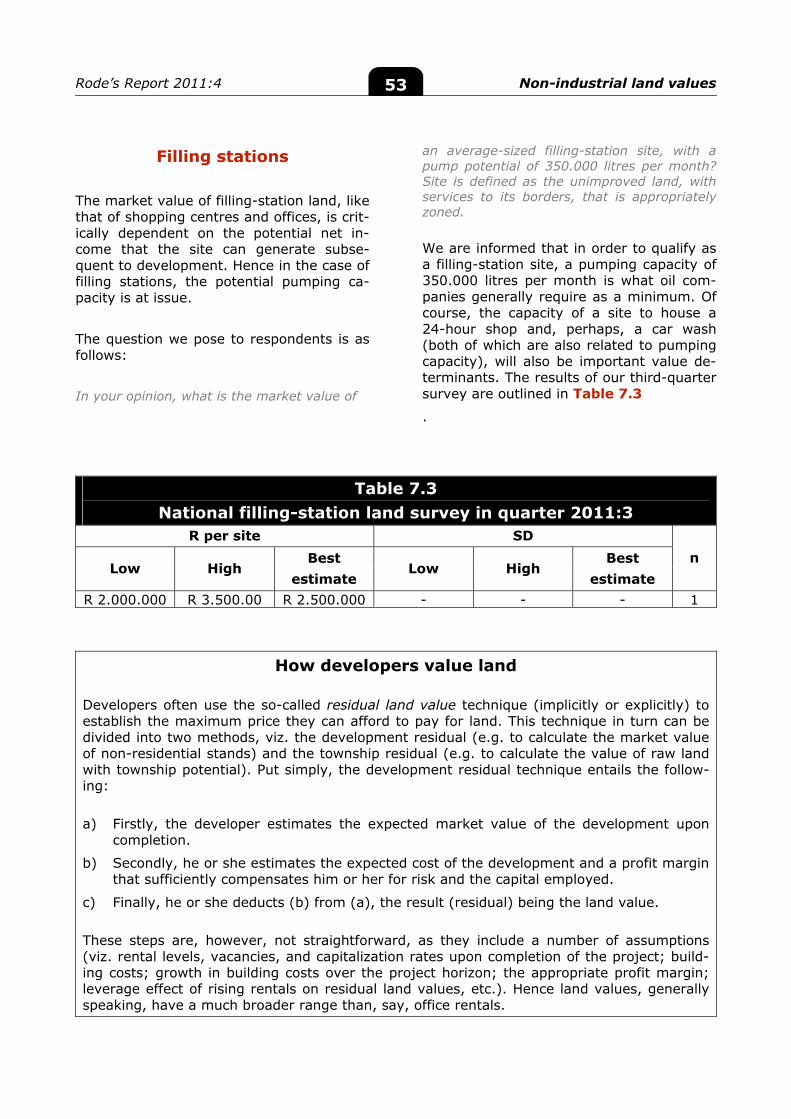

Table 7.3: National filling-station land survey 53

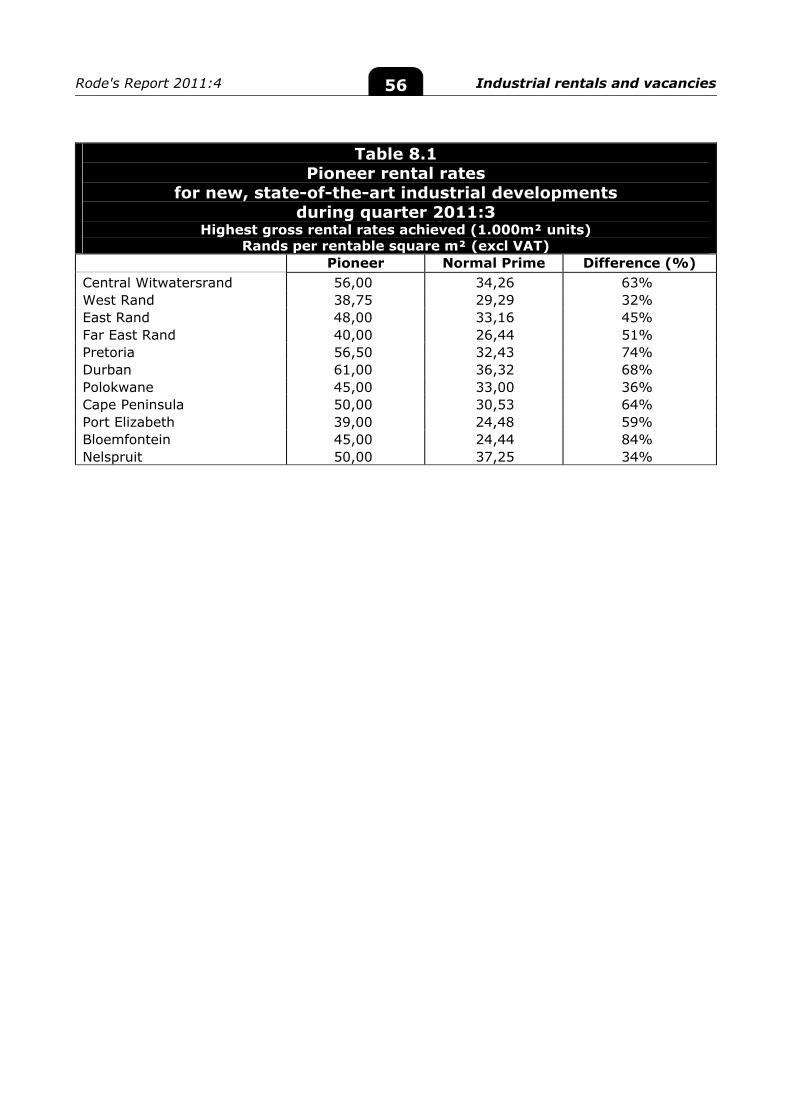

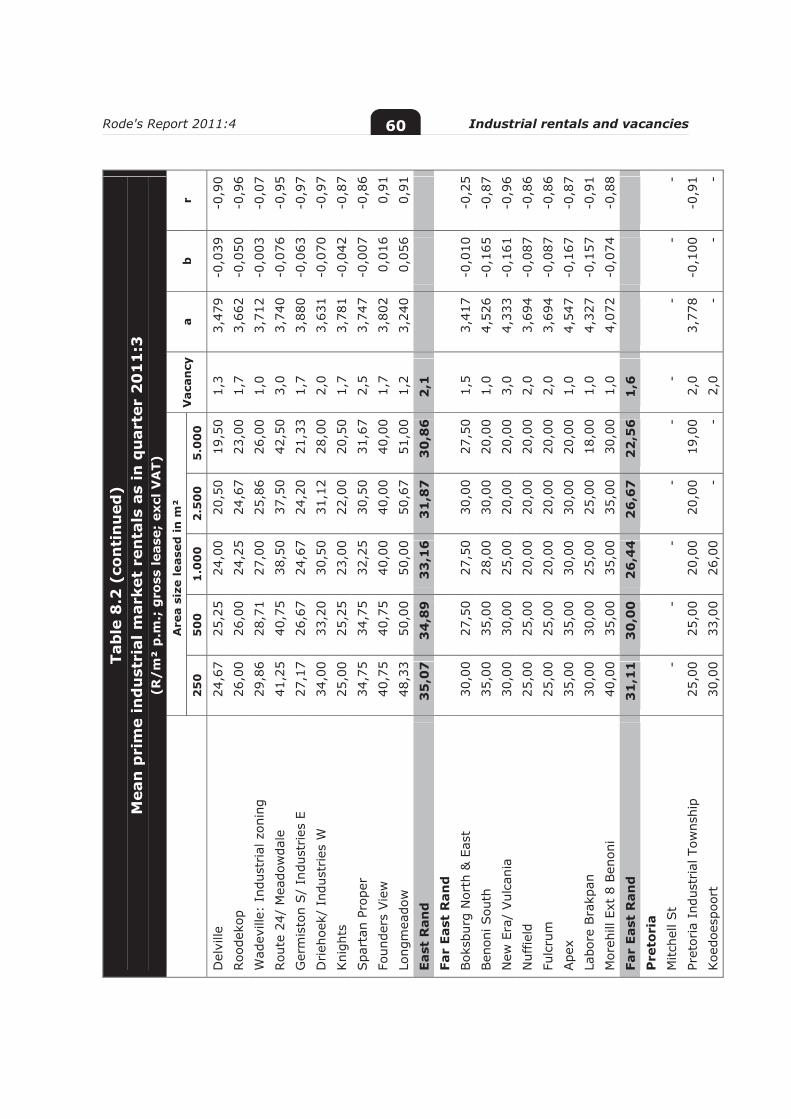

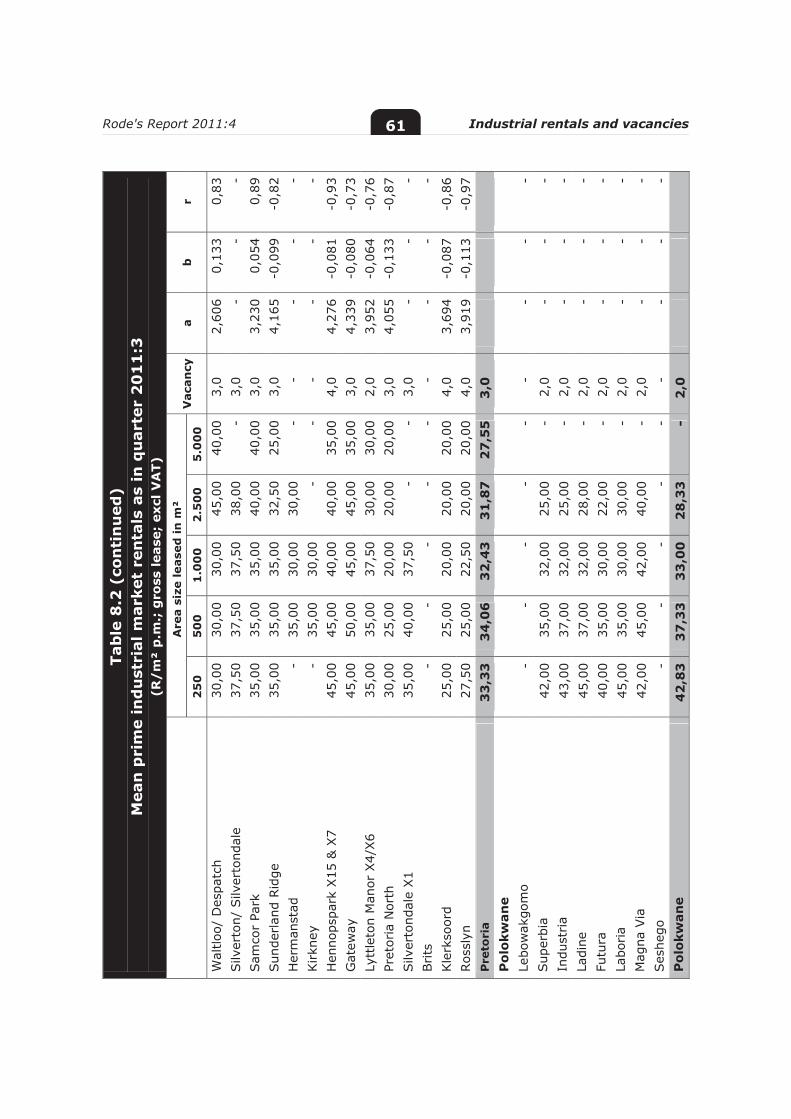

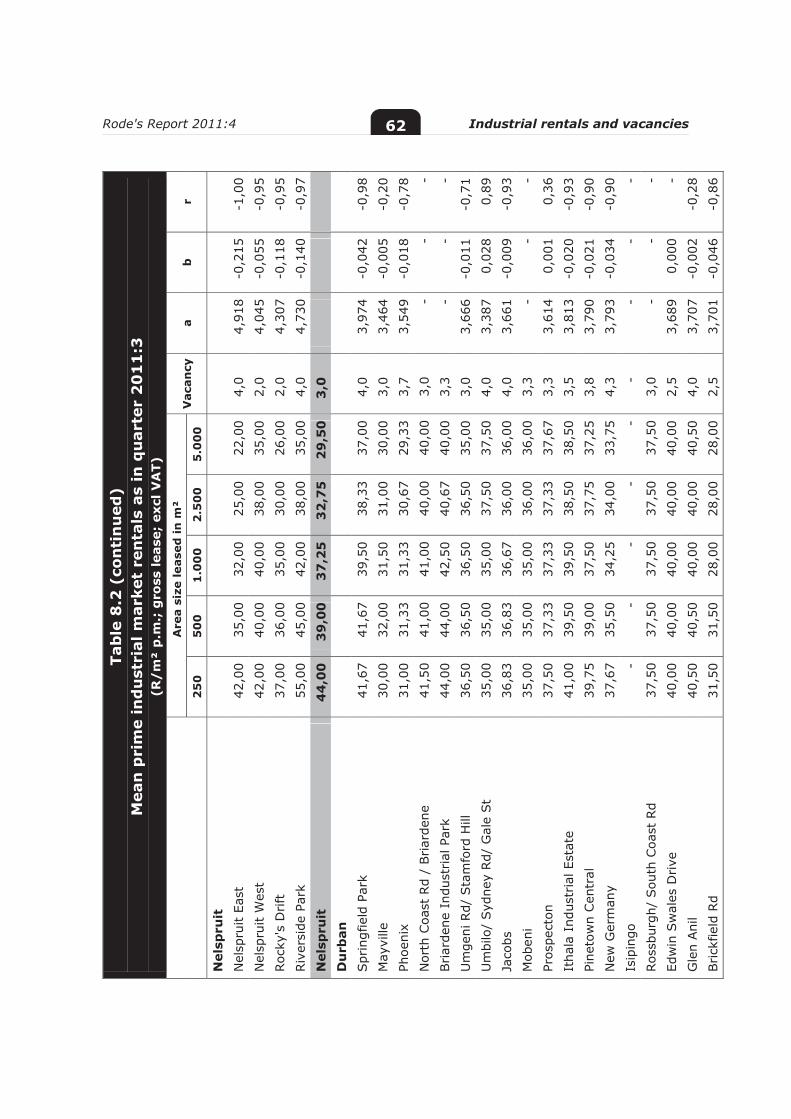

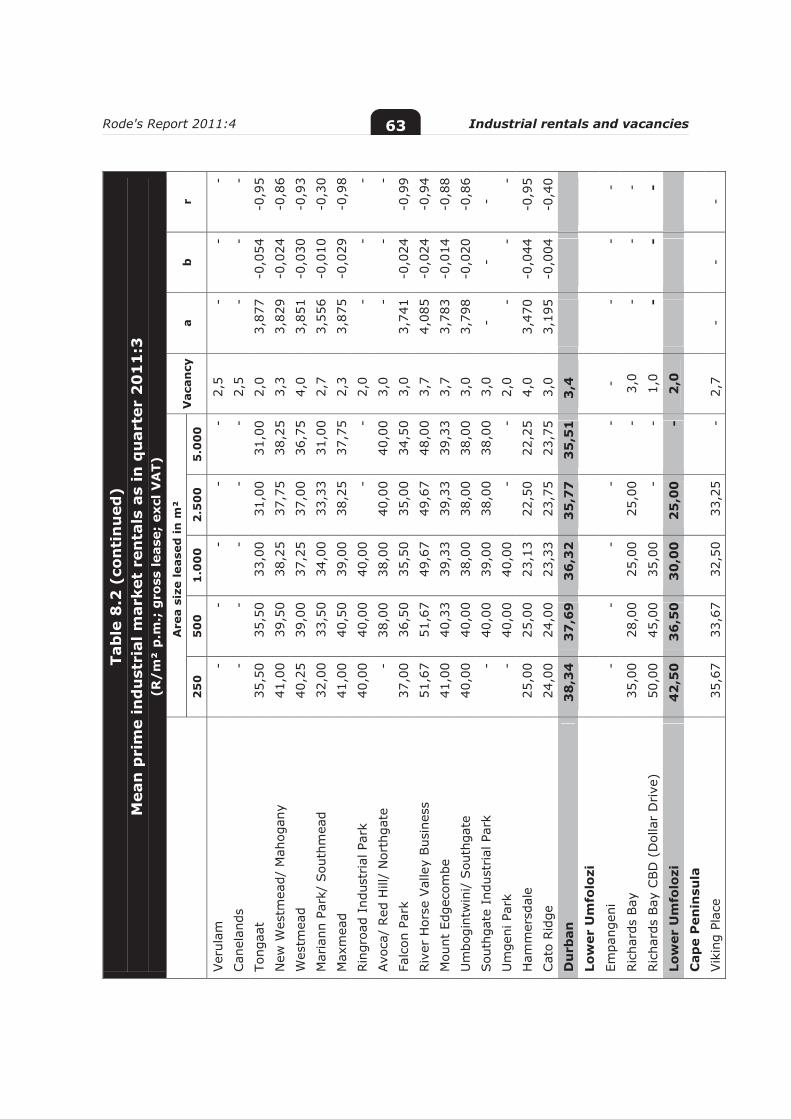

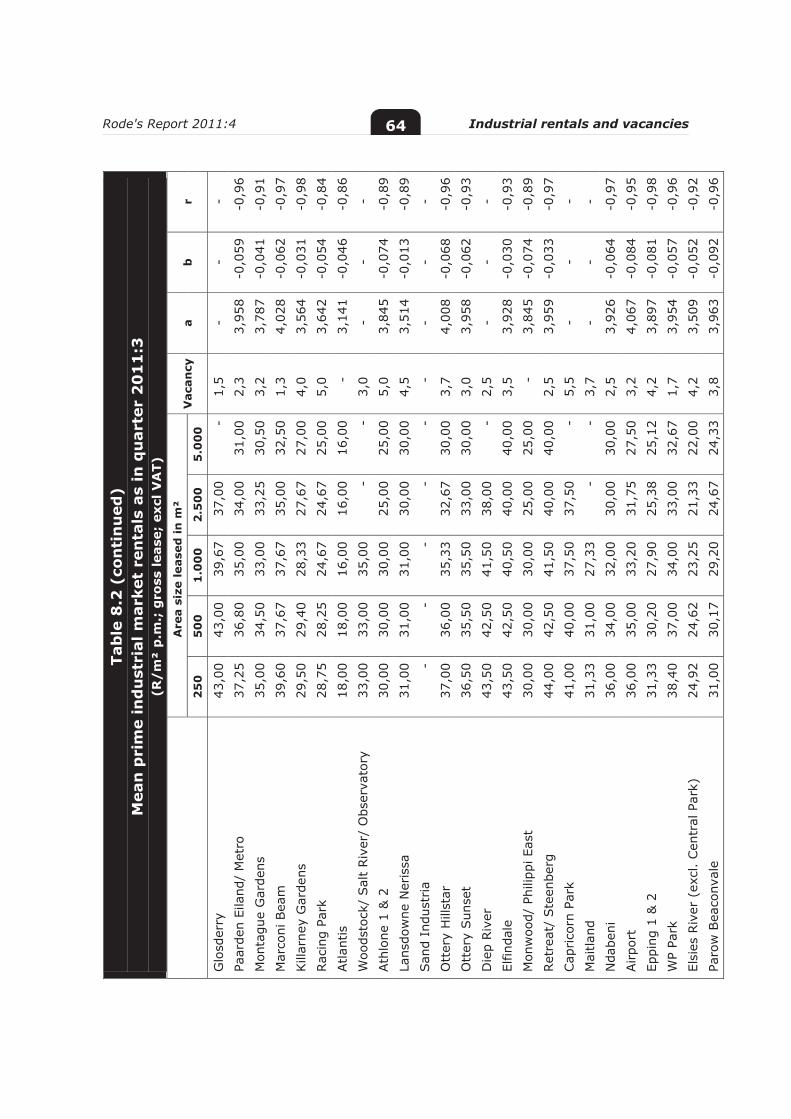

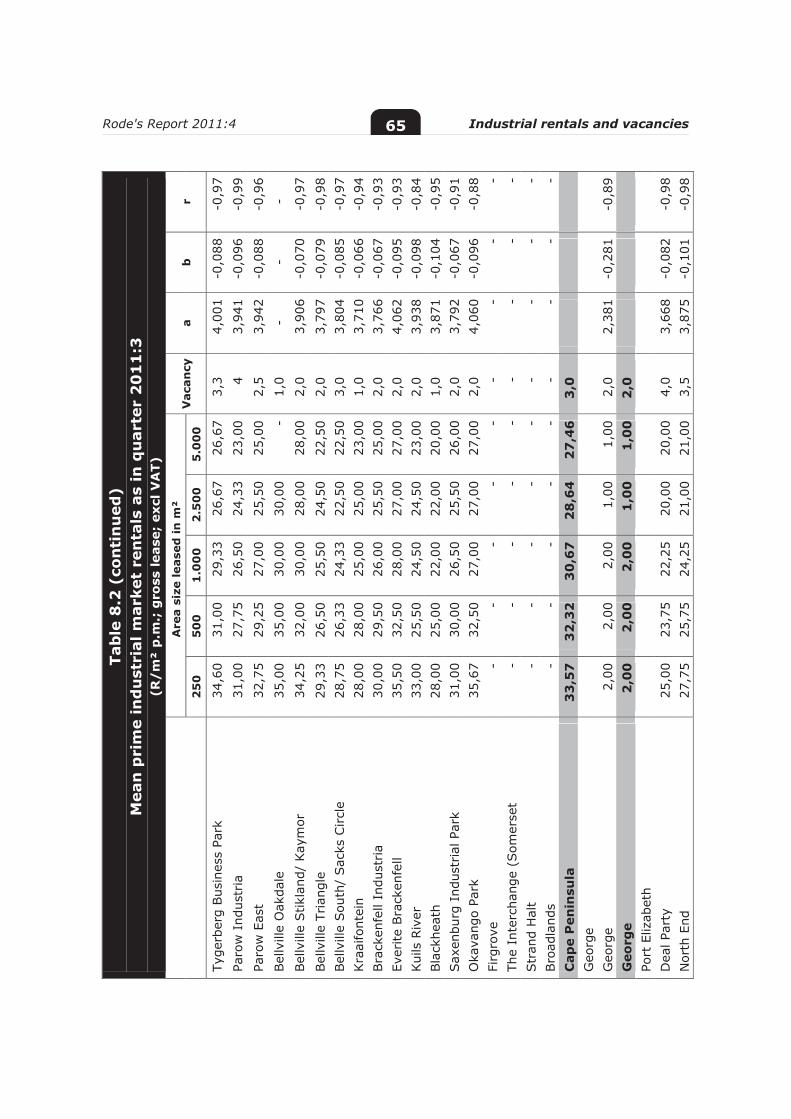

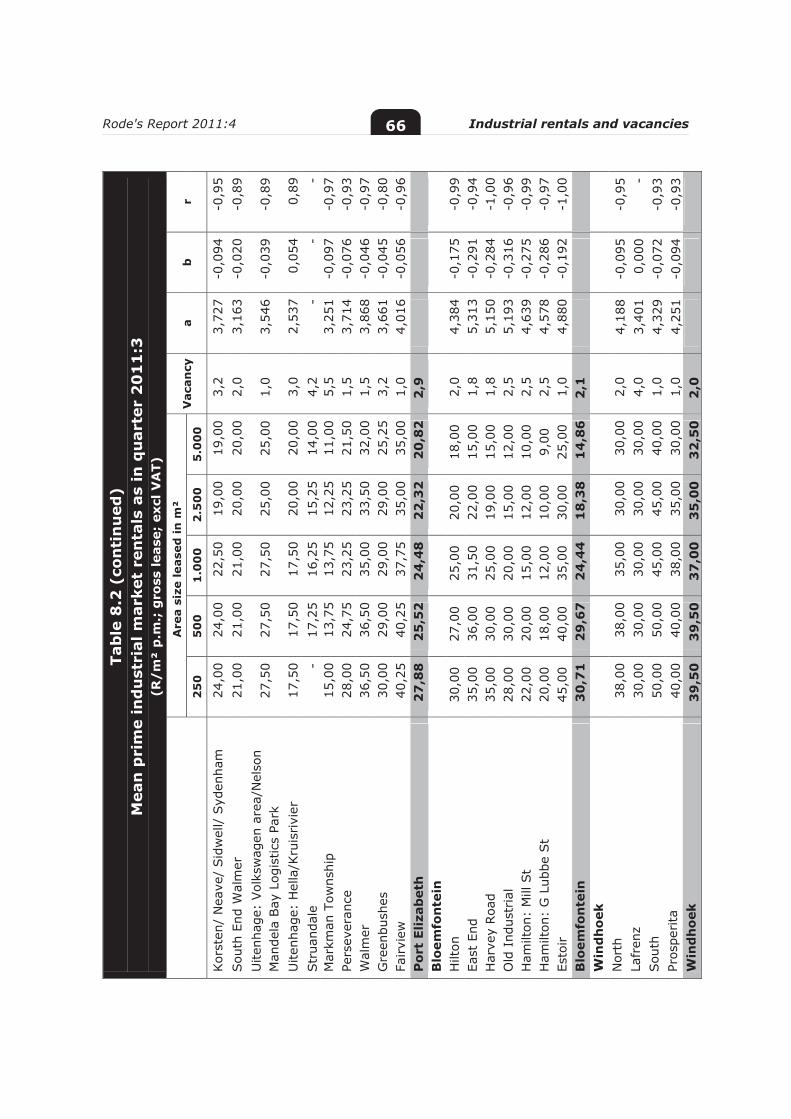

Table 8.1: Pioneer rental rates for new, state-of-the-art industrialdevelopments 56

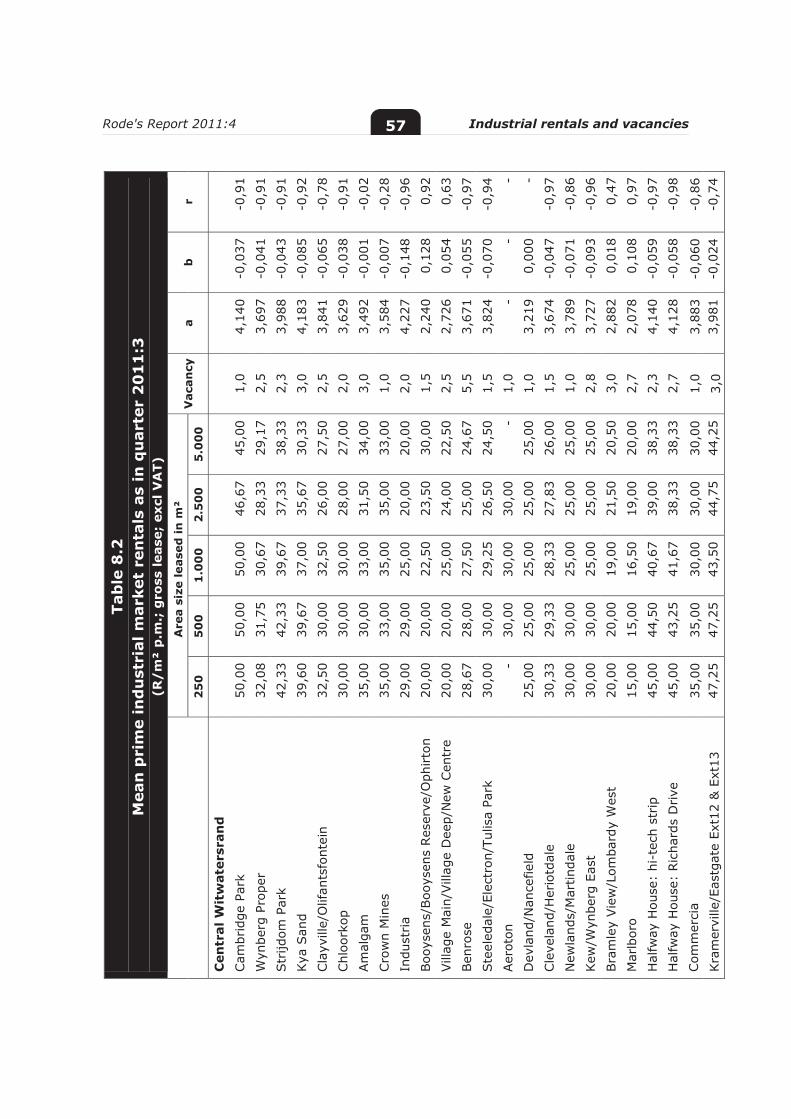

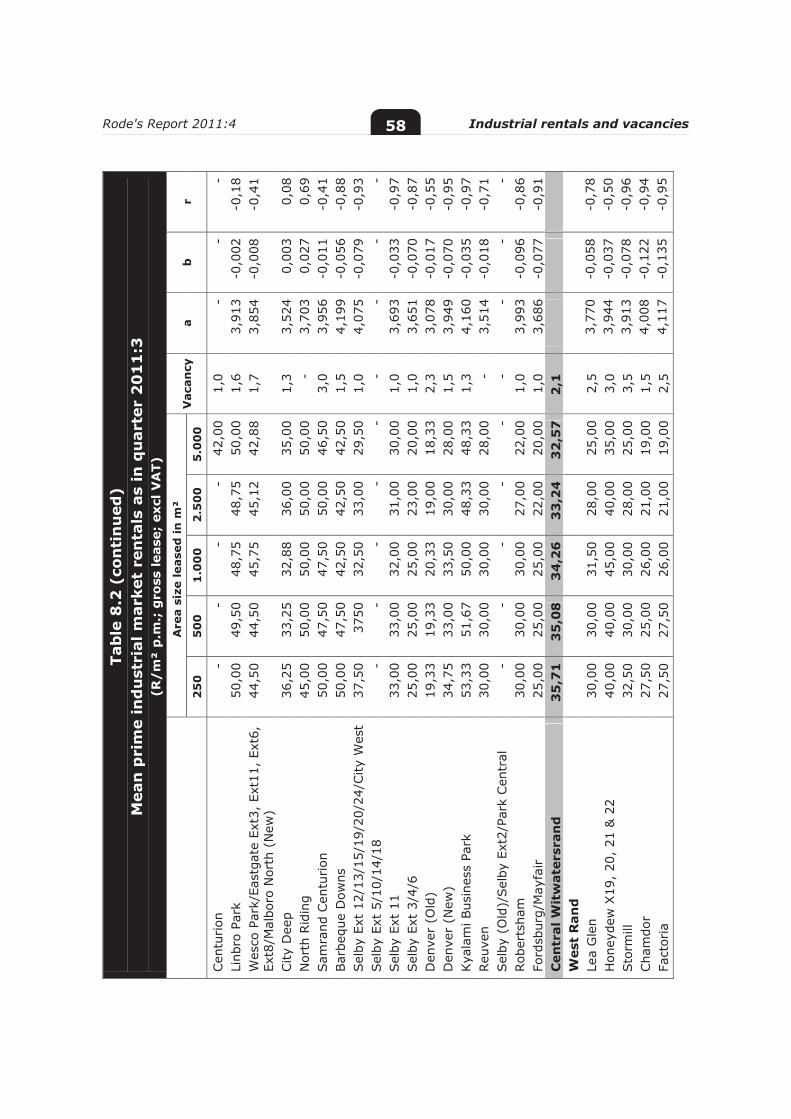

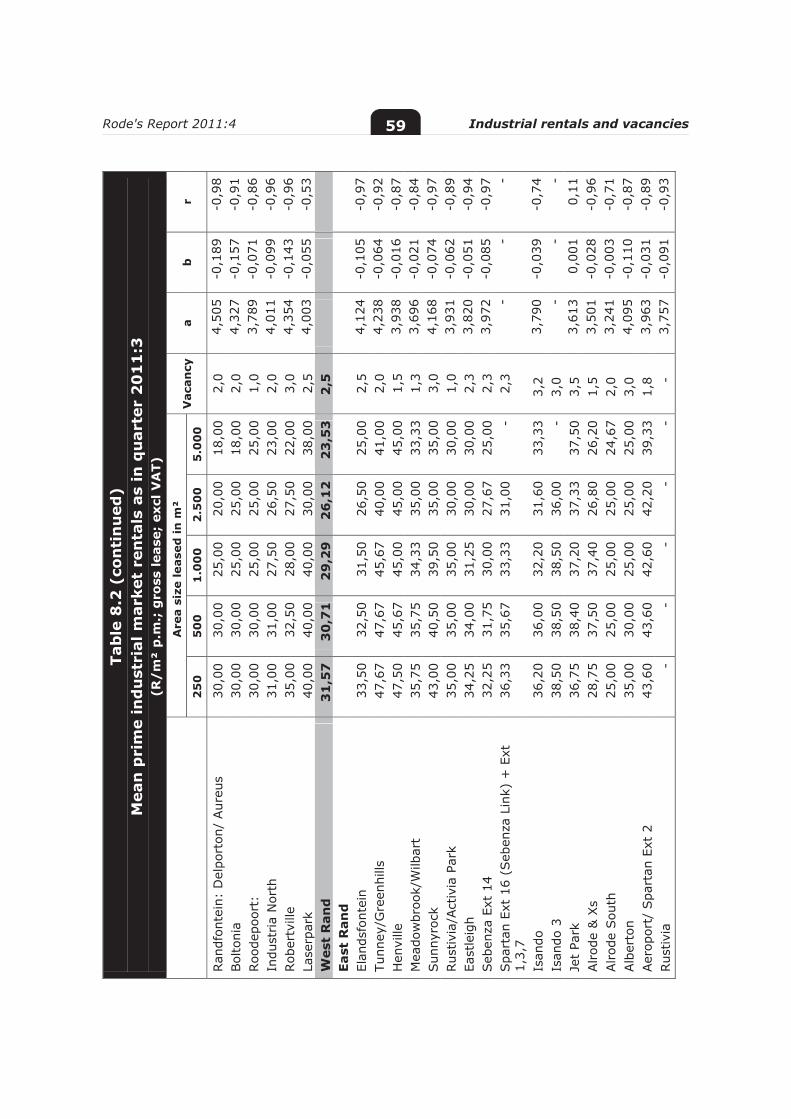

Table 8.2: Mean prime industrial market rentals 57

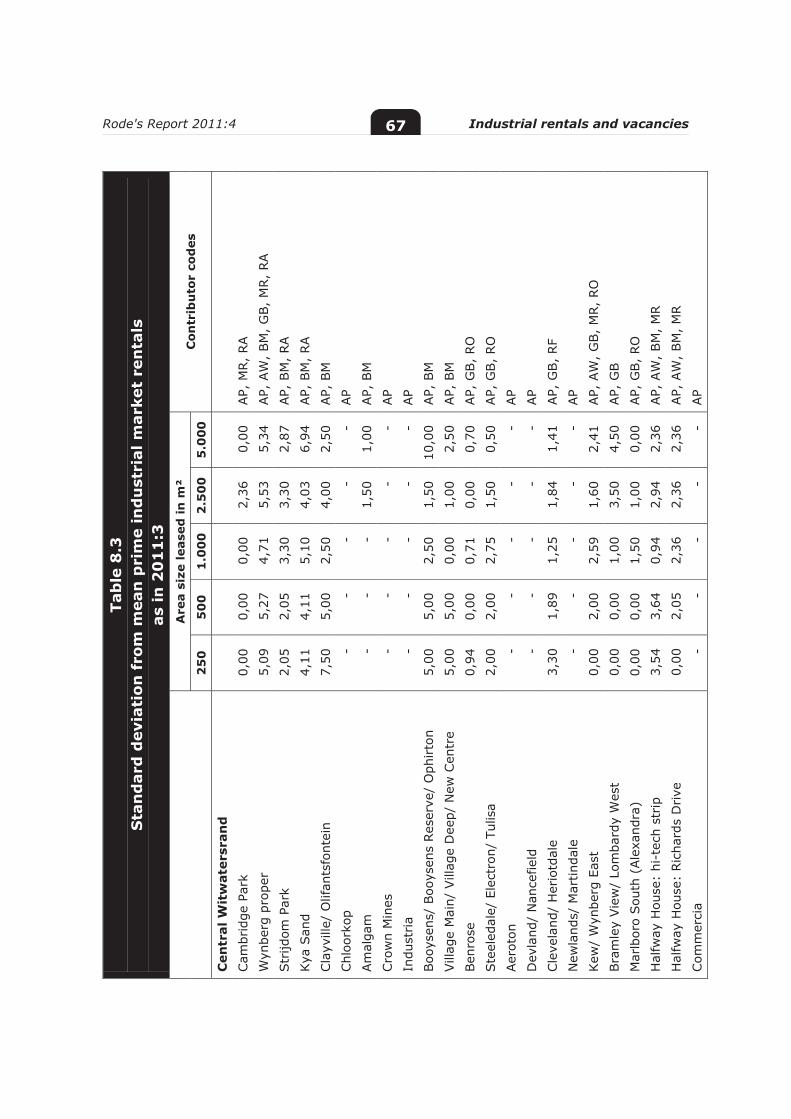

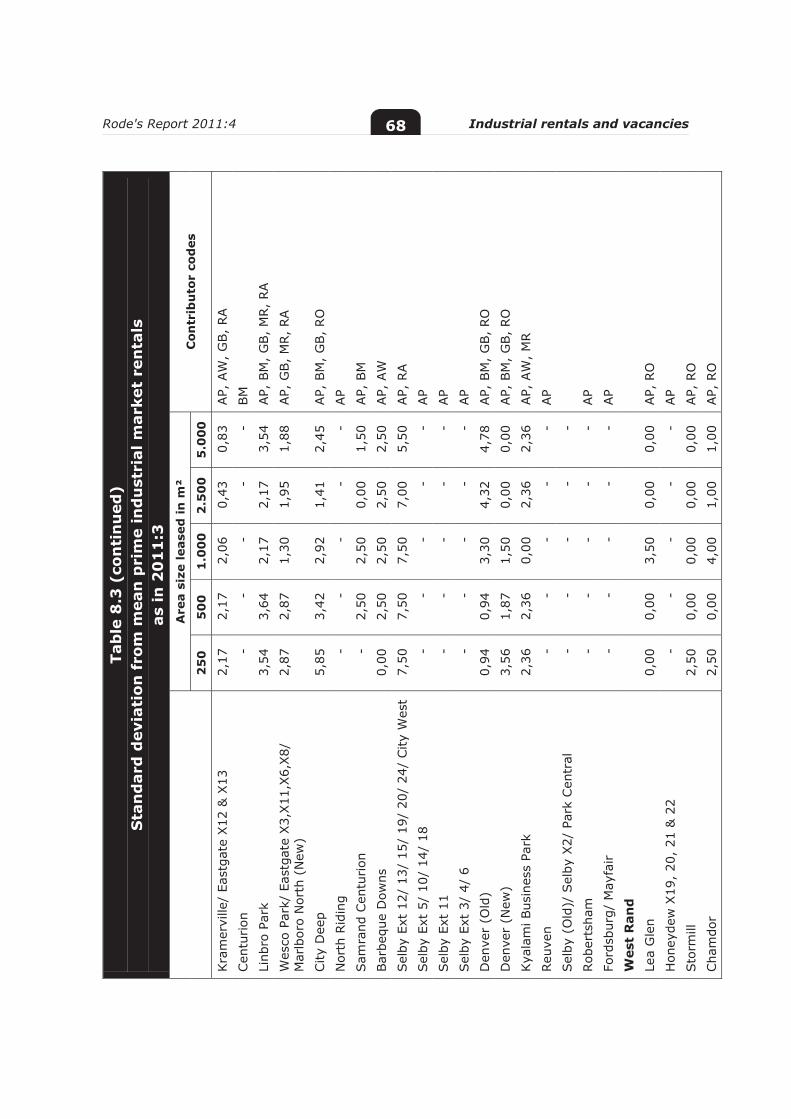

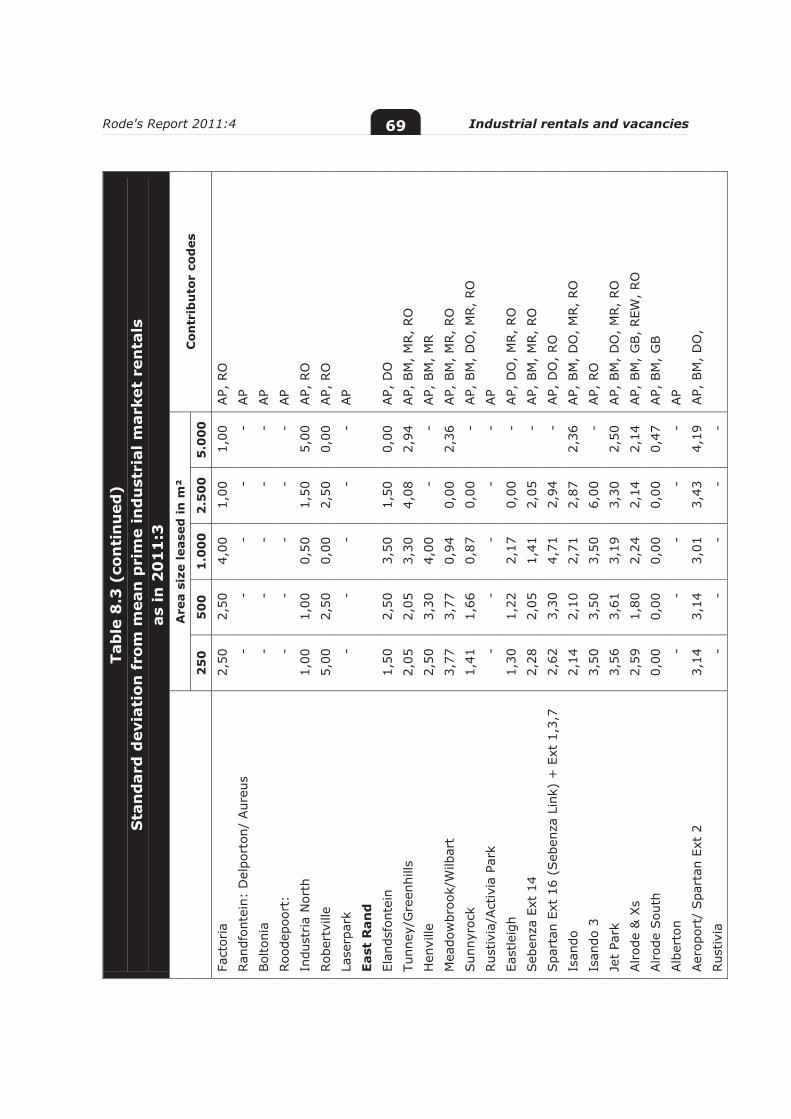

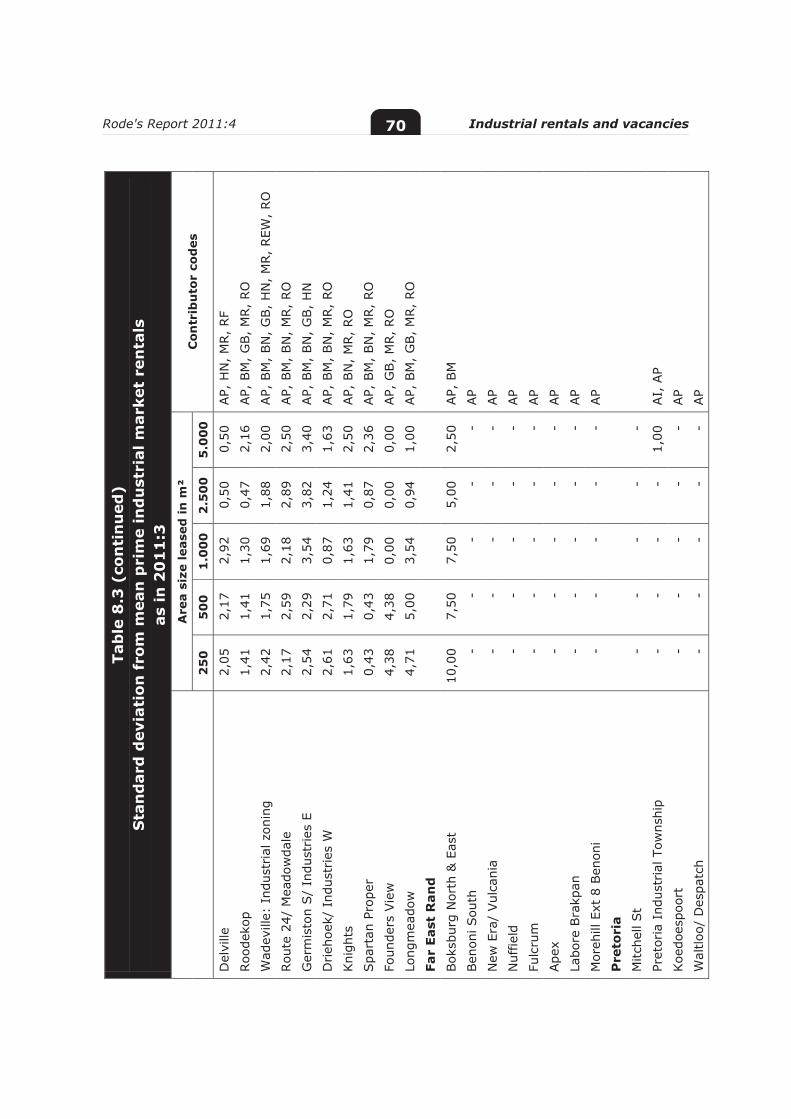

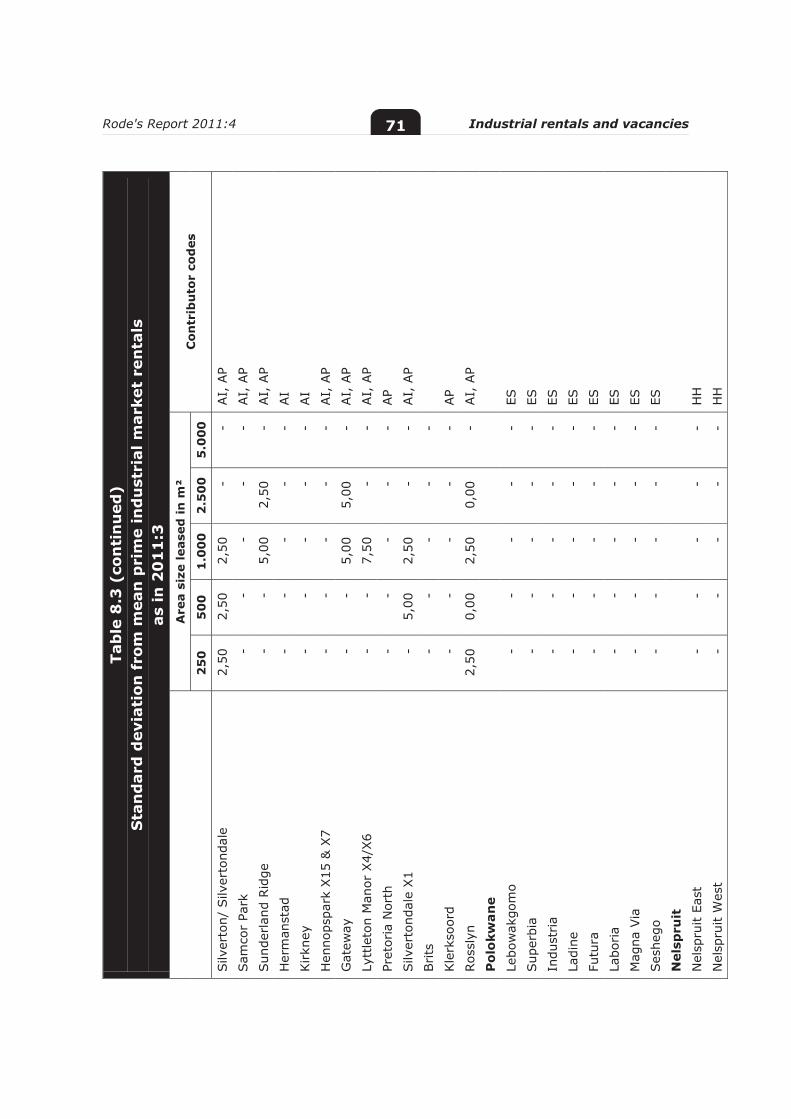

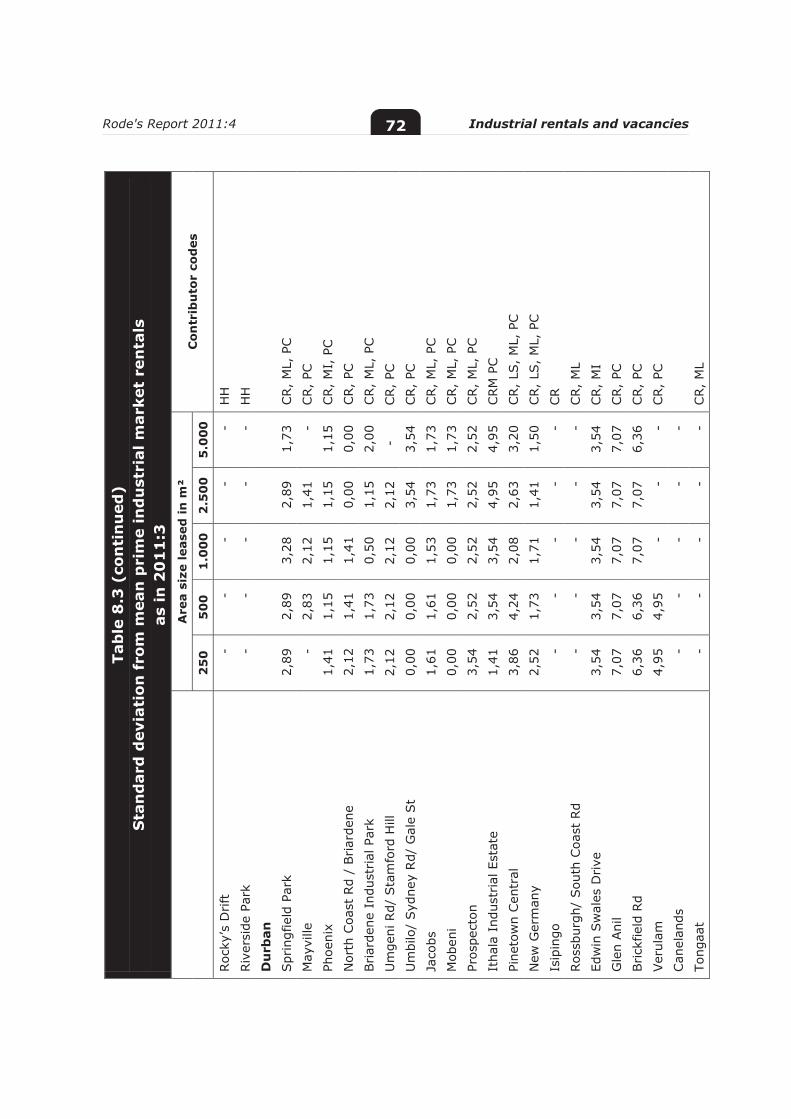

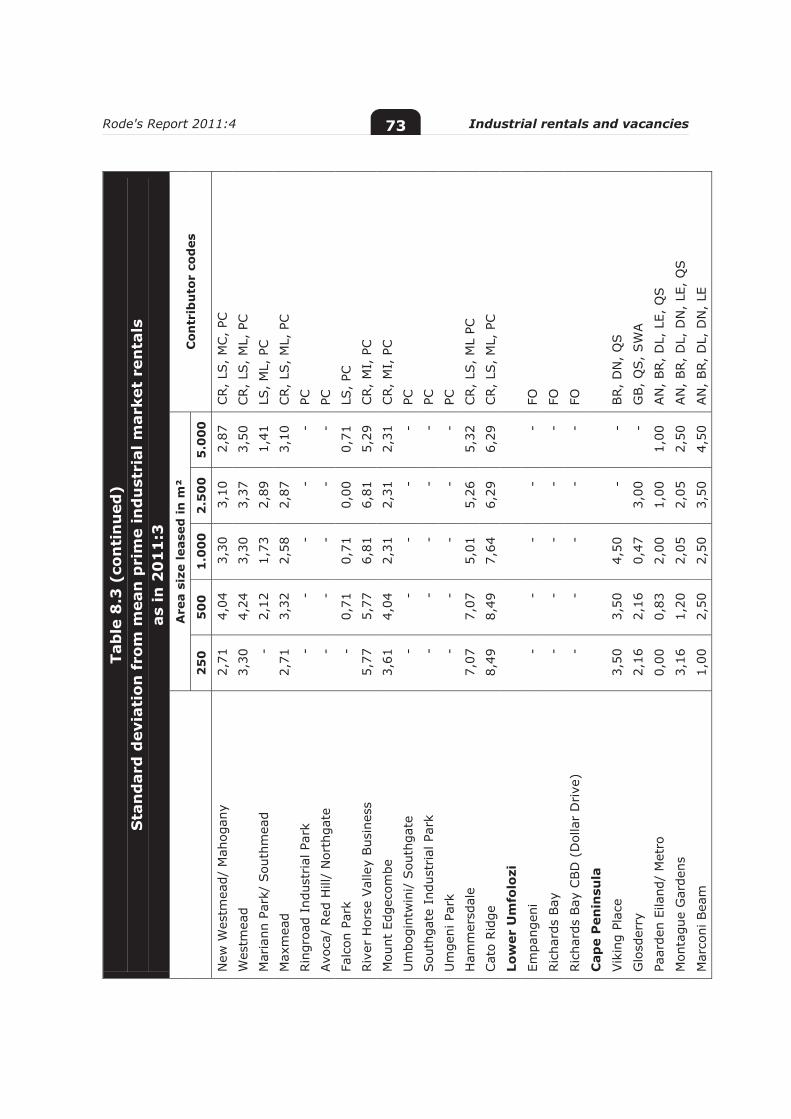

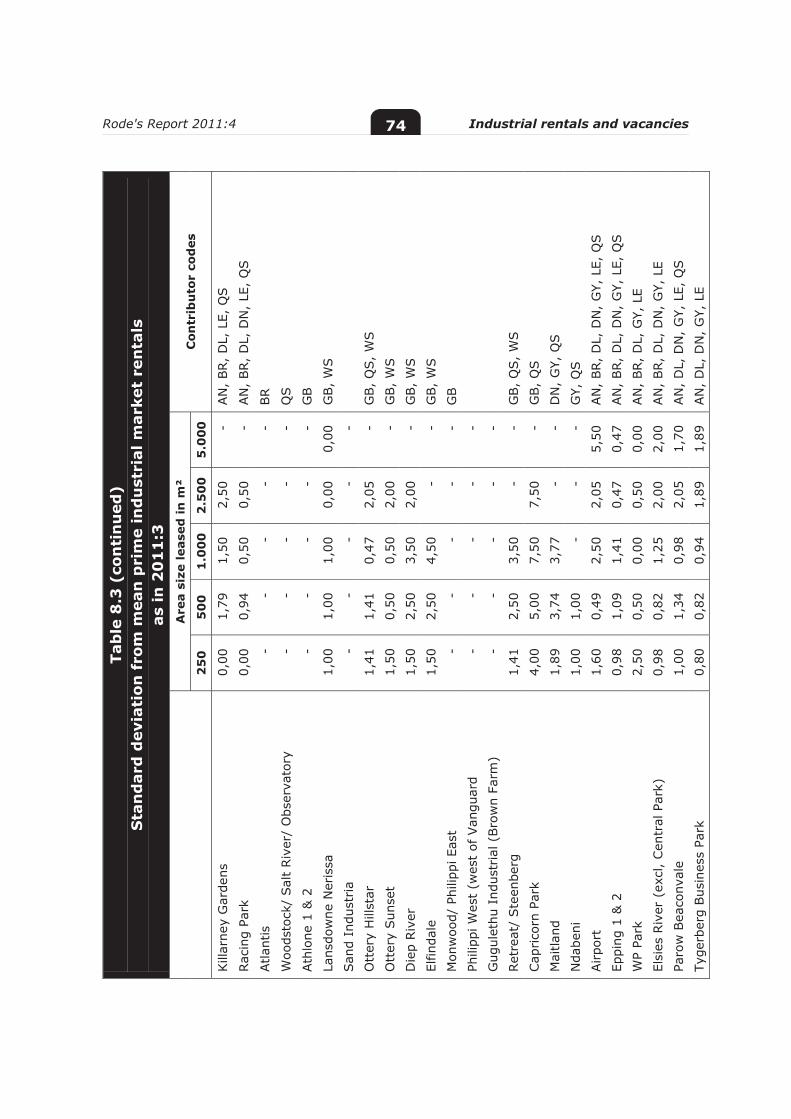

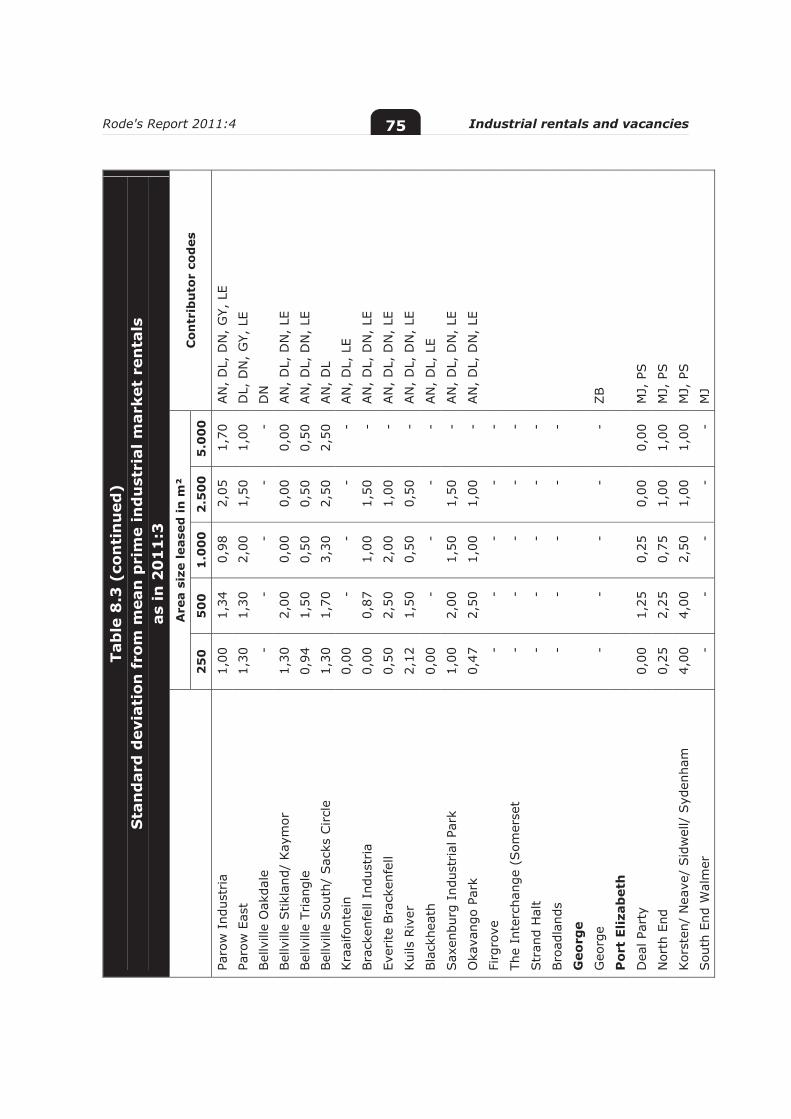

Table 8.3: Standard deviation from mean prime industrial market rentals 67

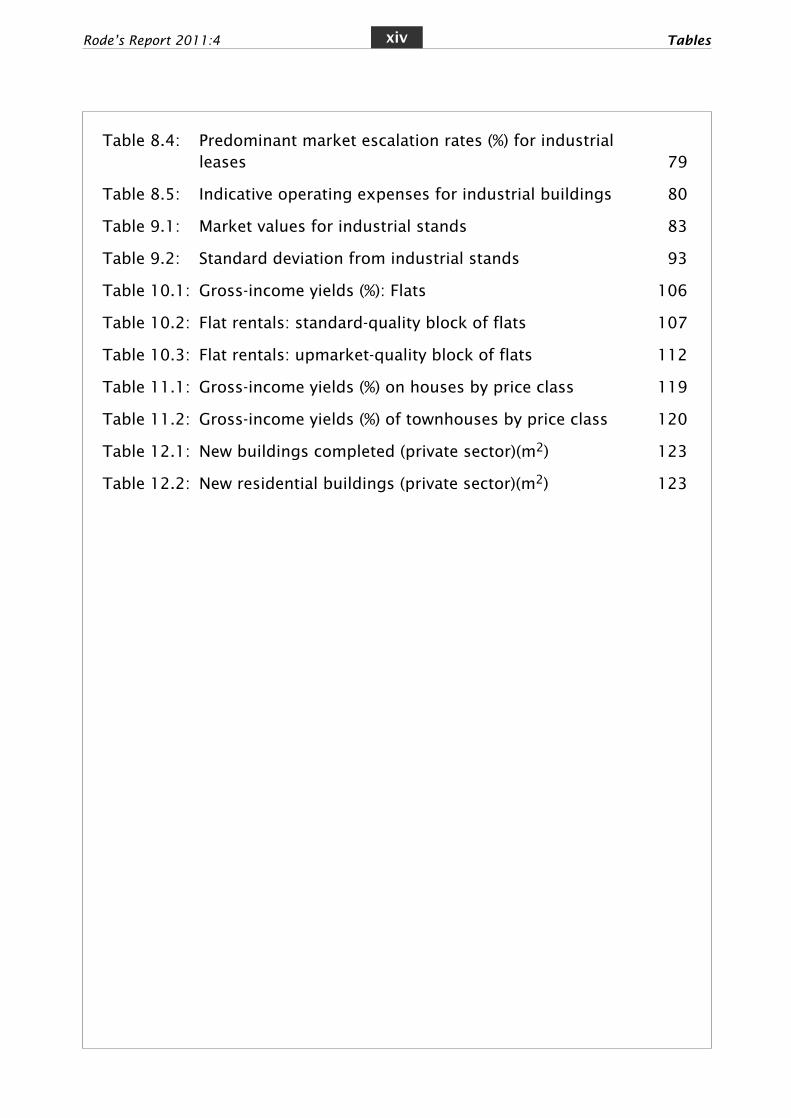

Rode’s Report 2011:4 Tablesxiii

Tables

Table 8.4: Predominant market escalation rates (%) for industrial leases 79

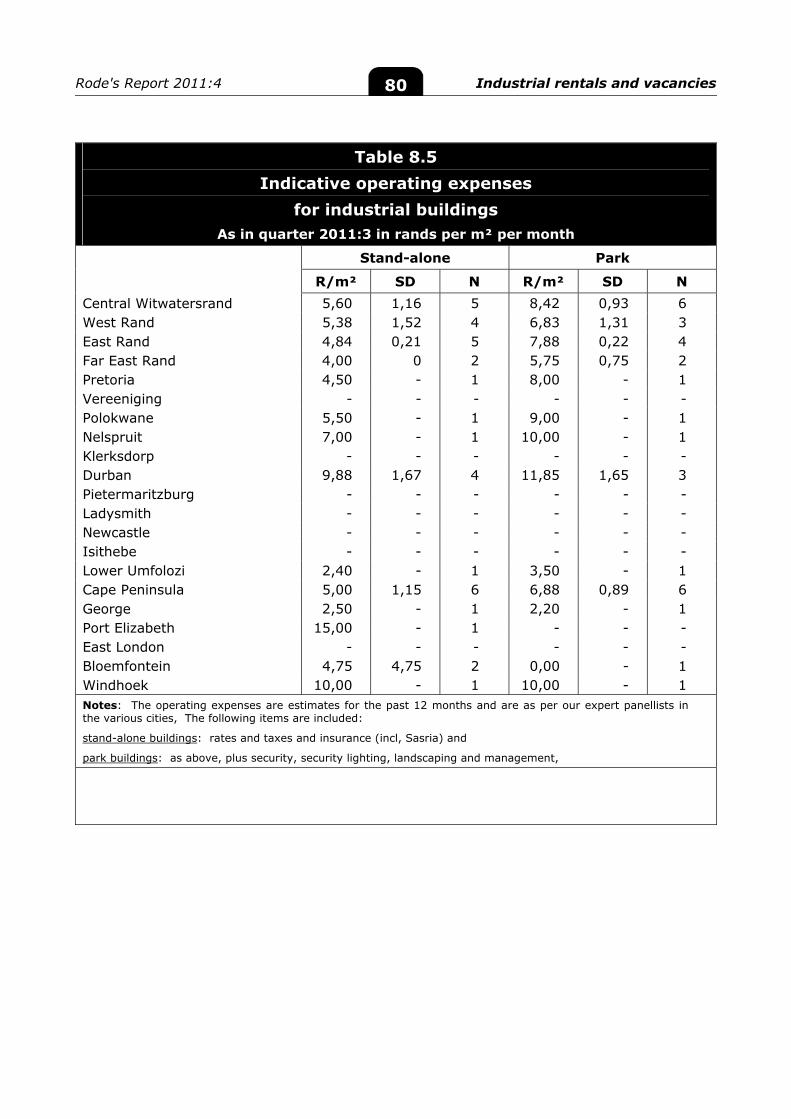

Table 8.5: Indicative operating expenses for industrial buildings 80

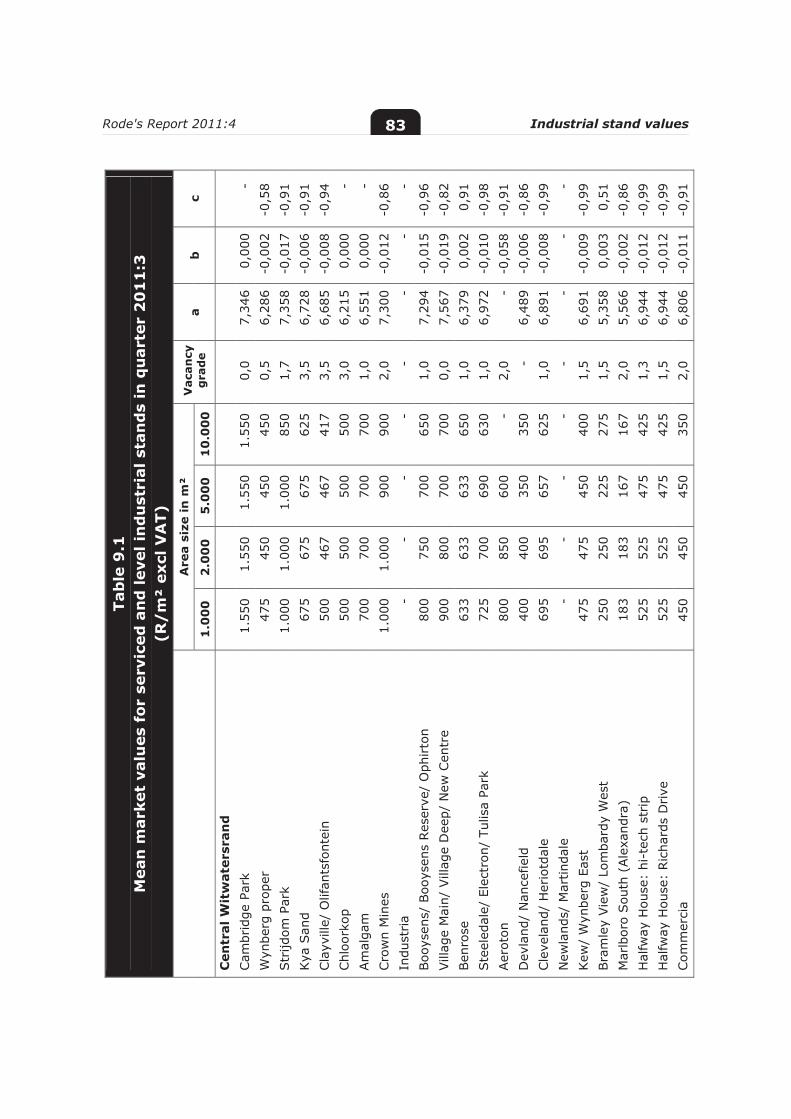

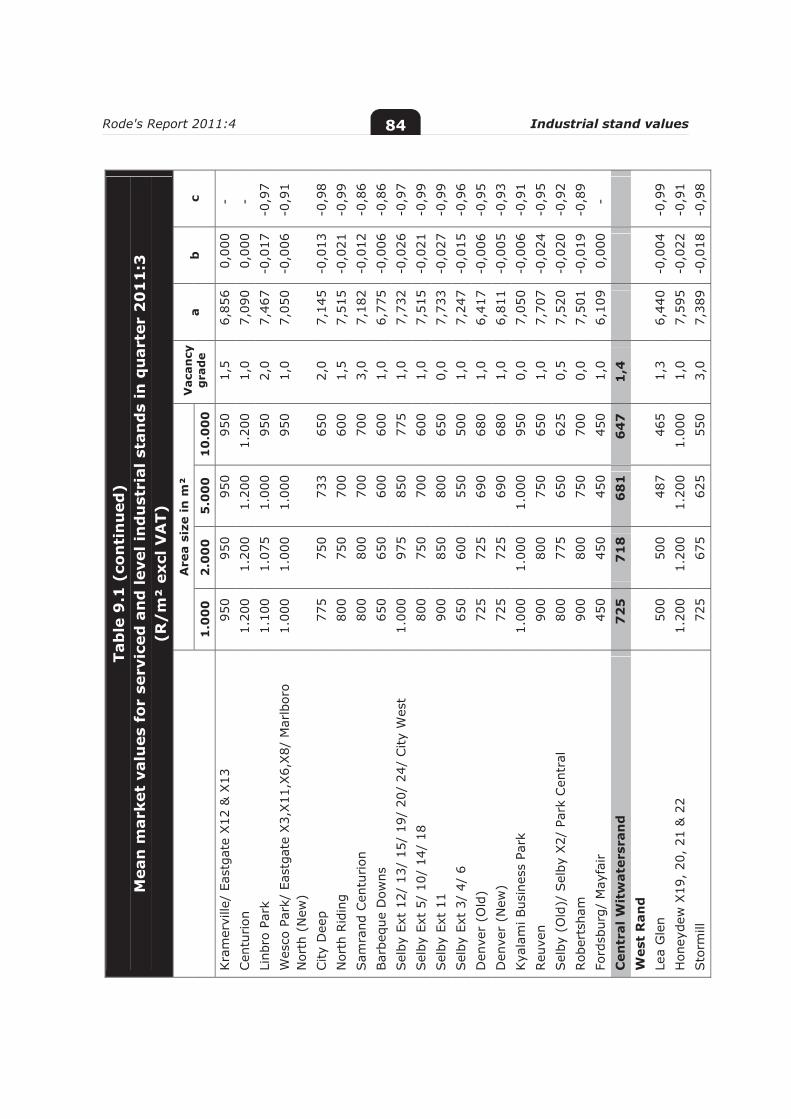

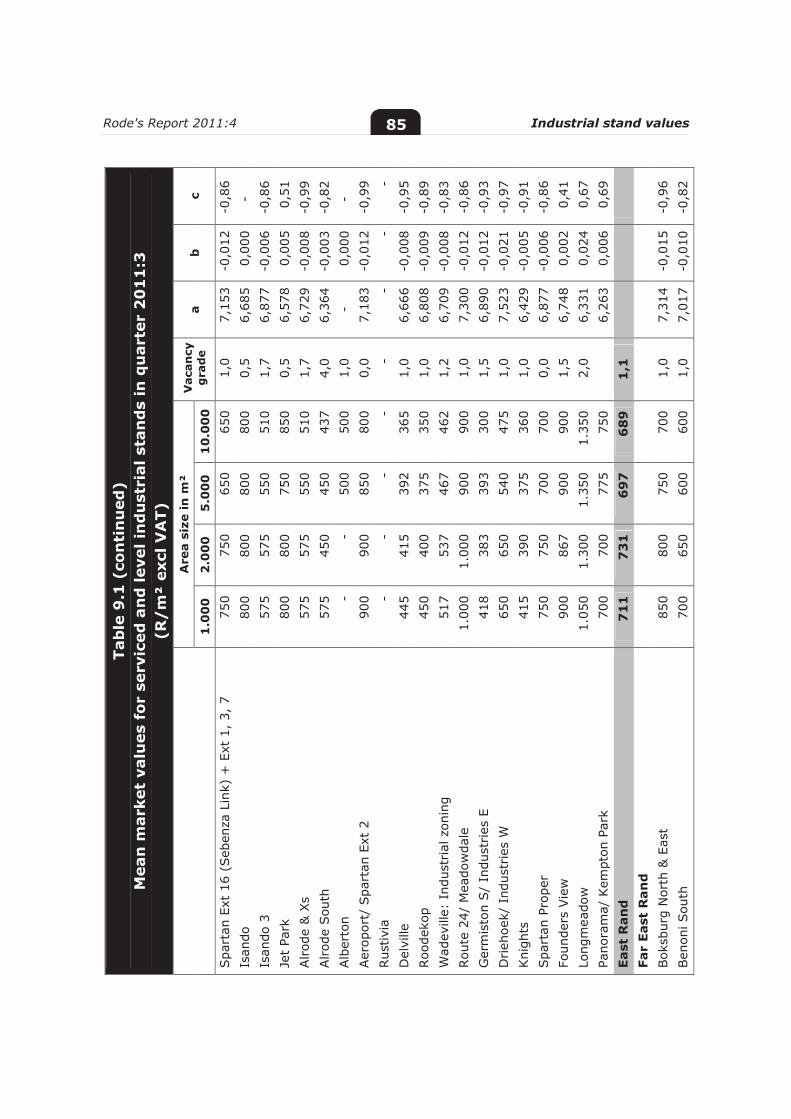

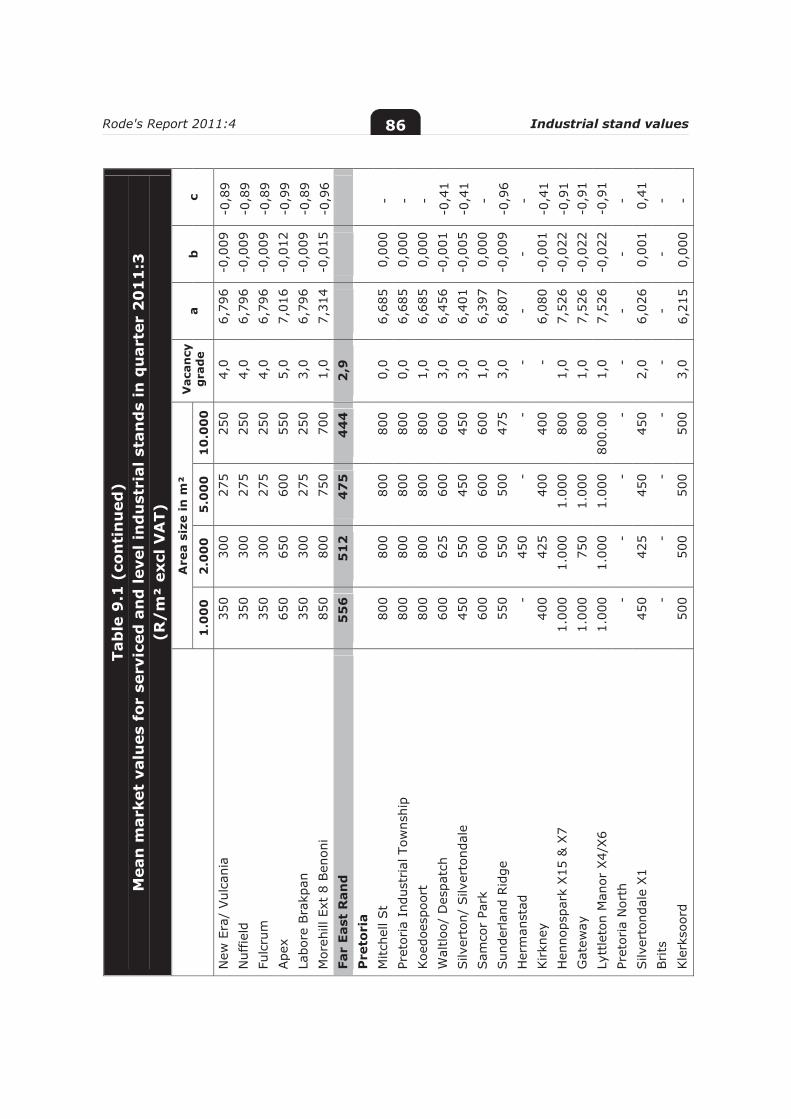

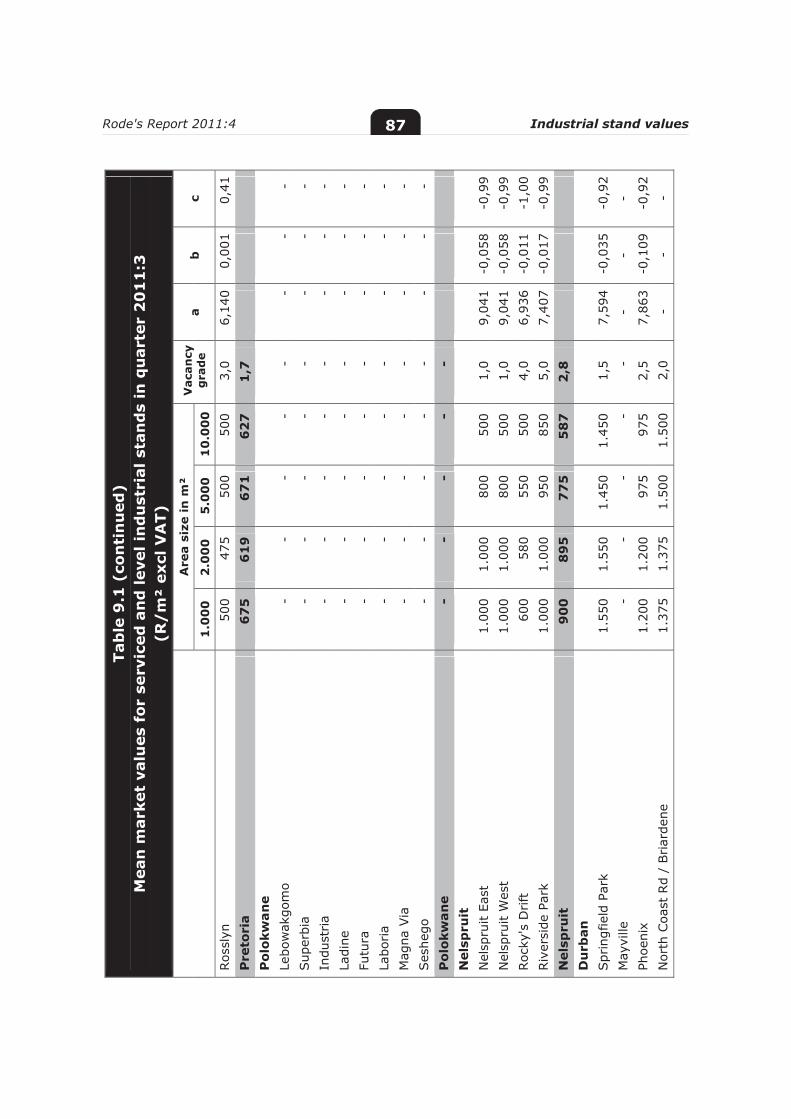

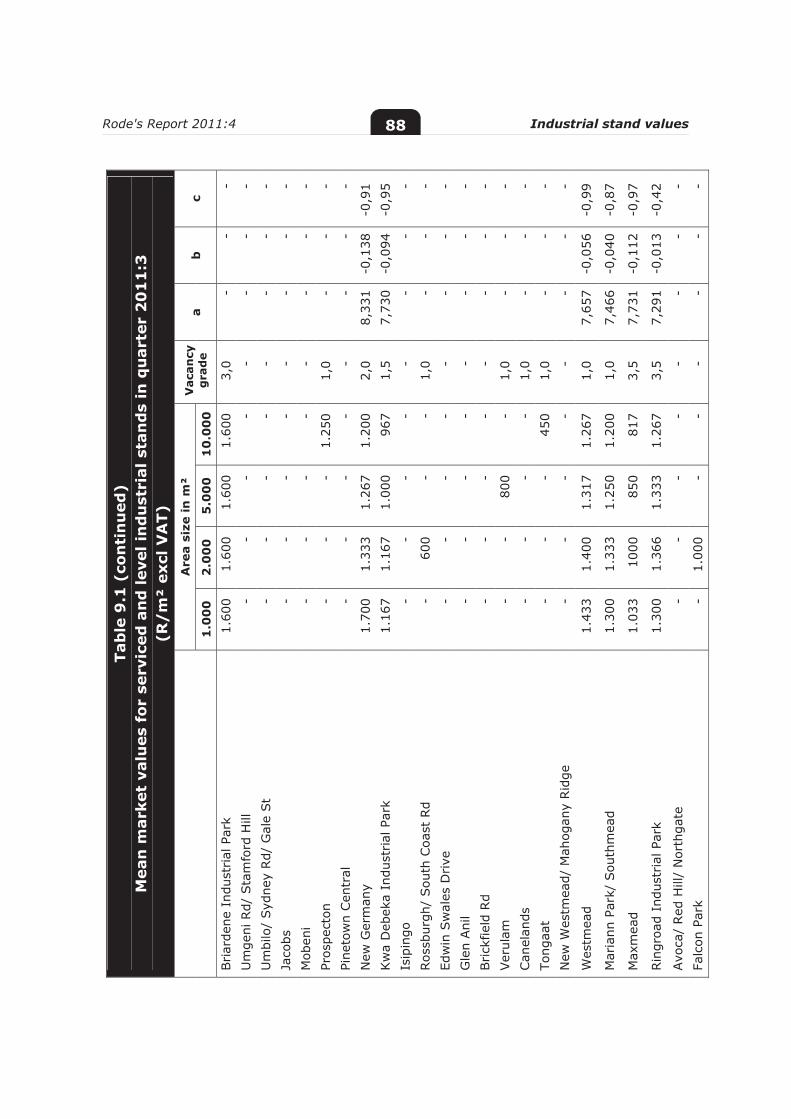

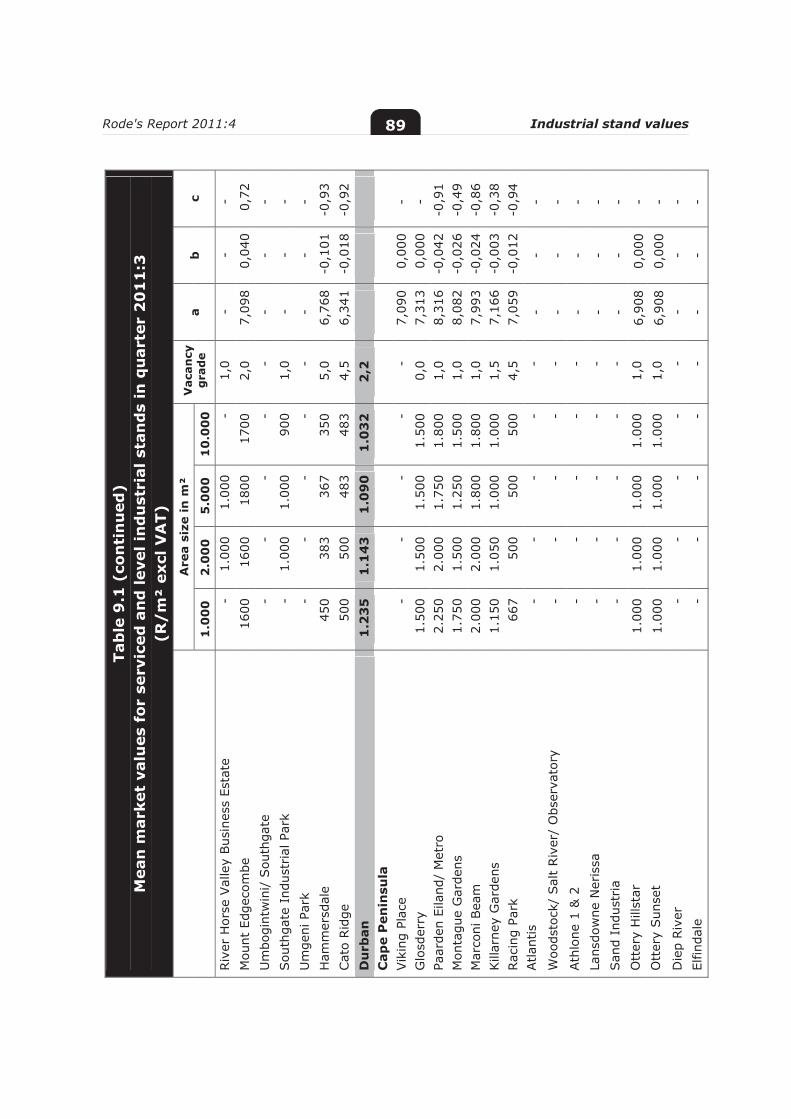

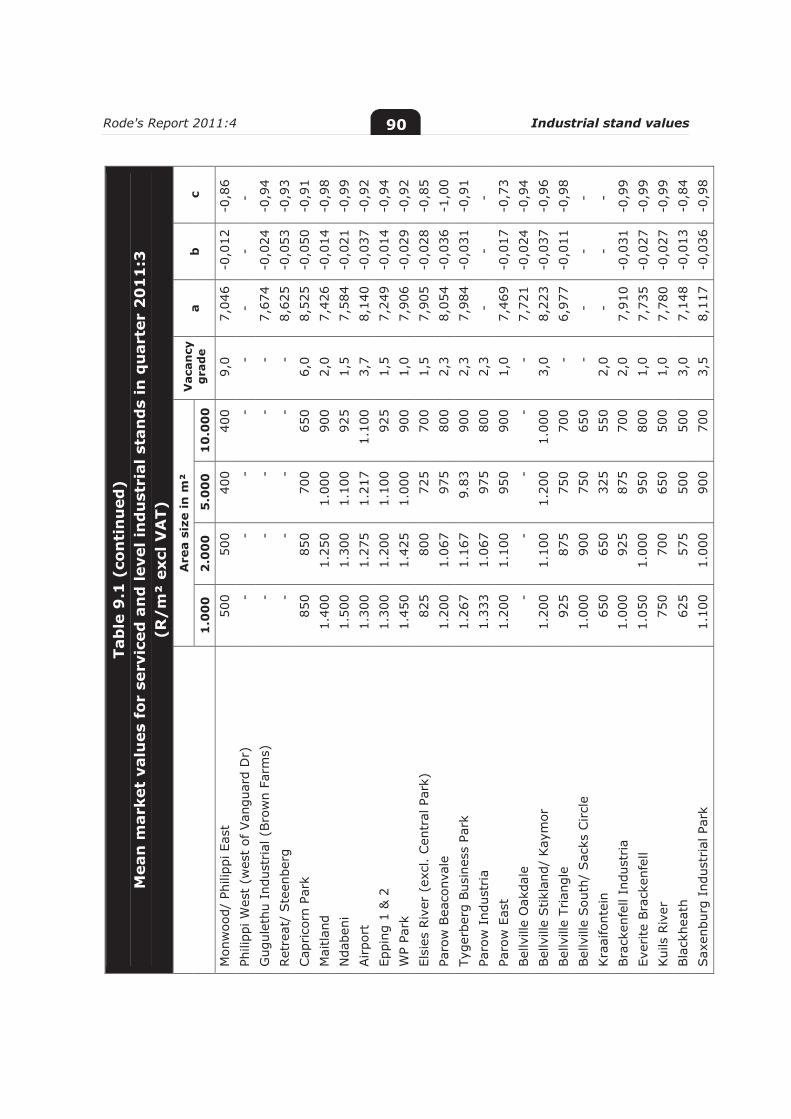

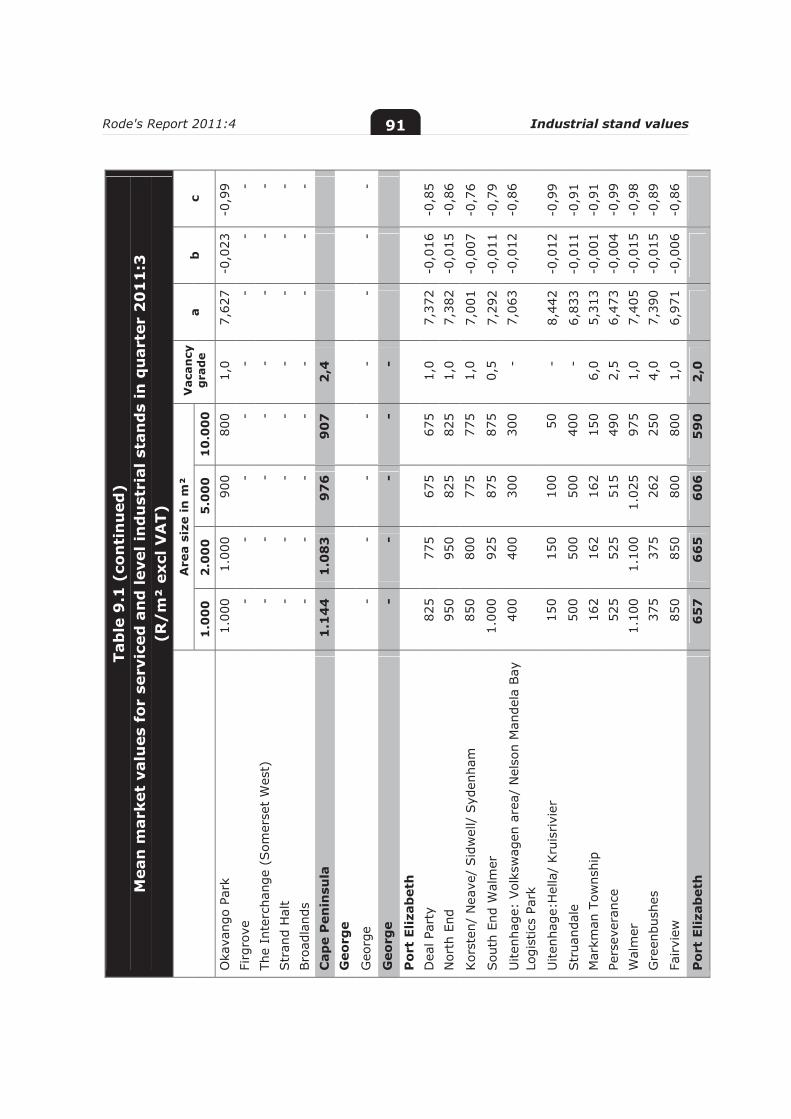

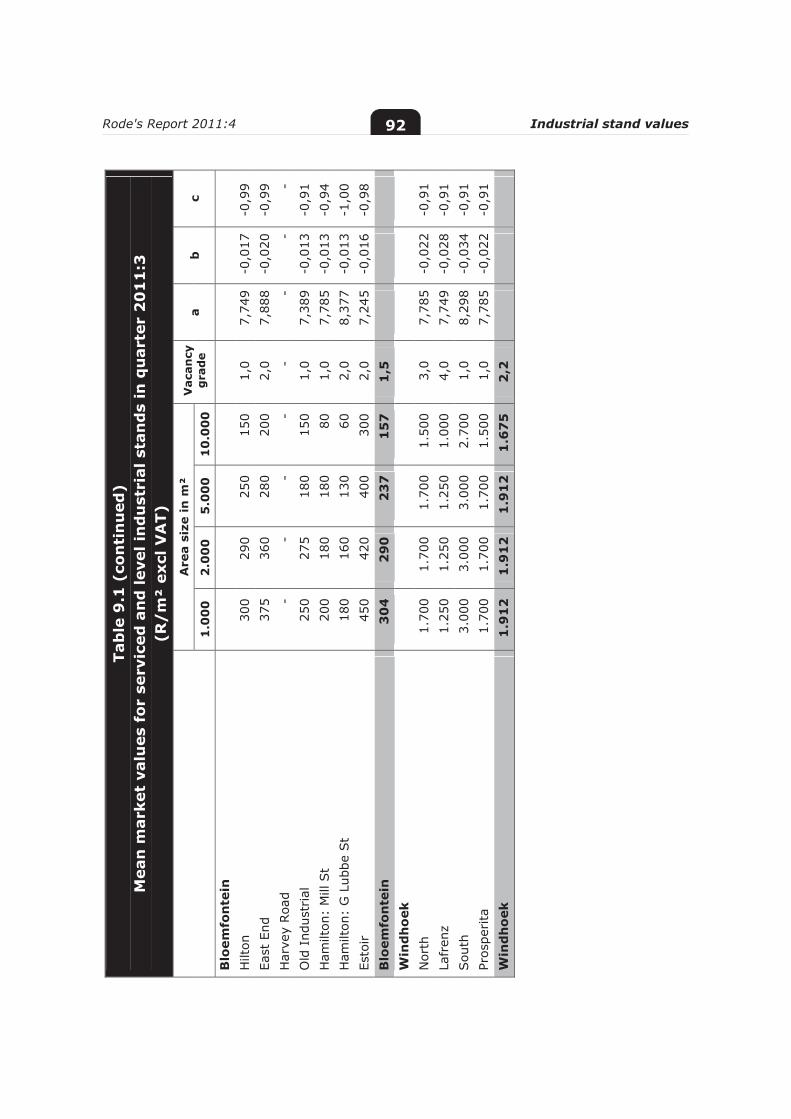

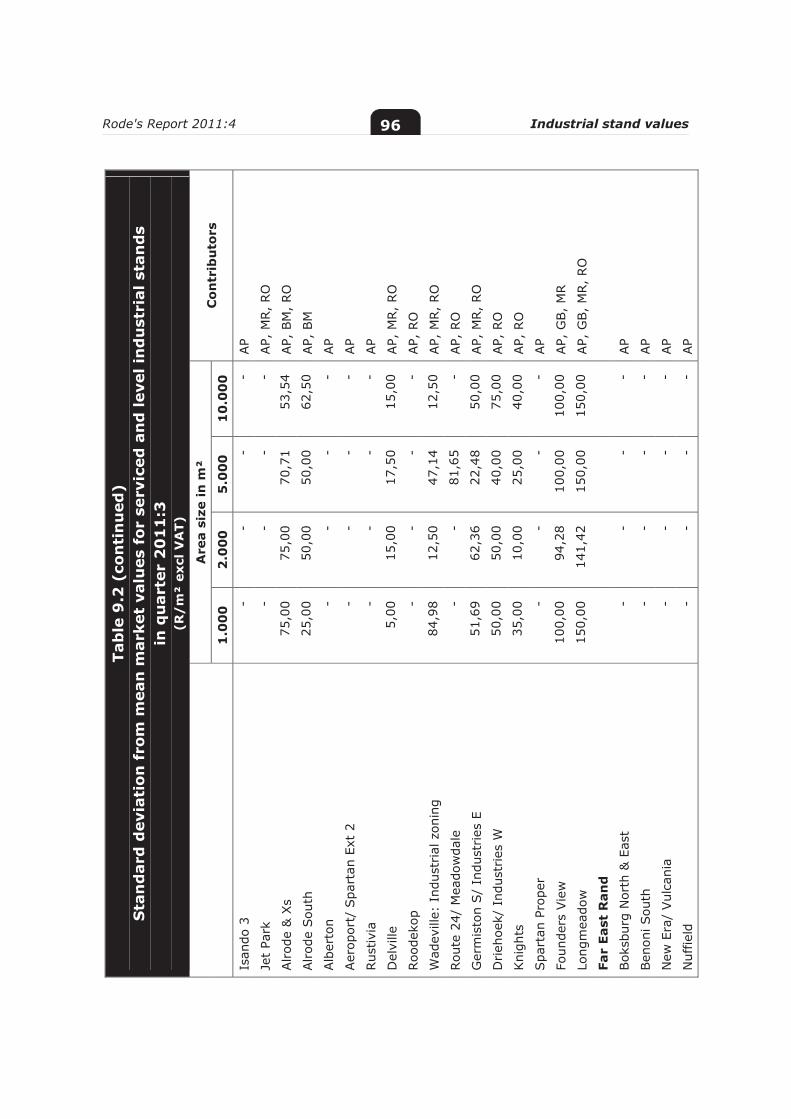

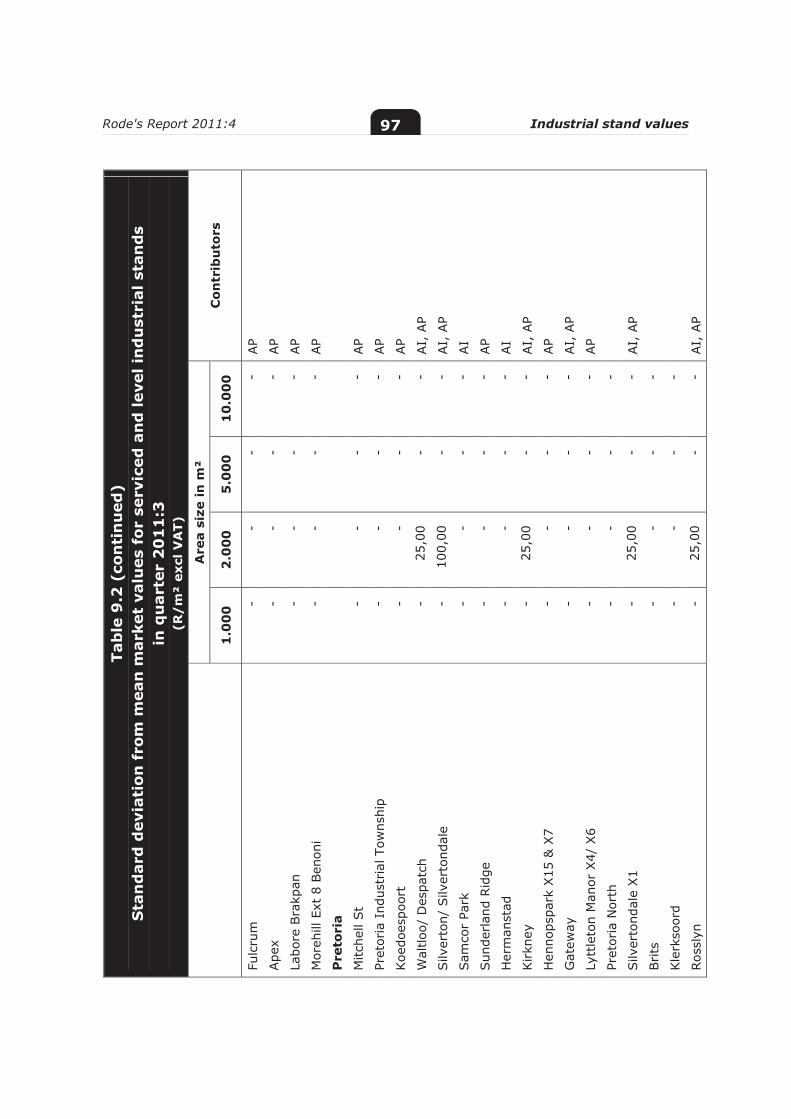

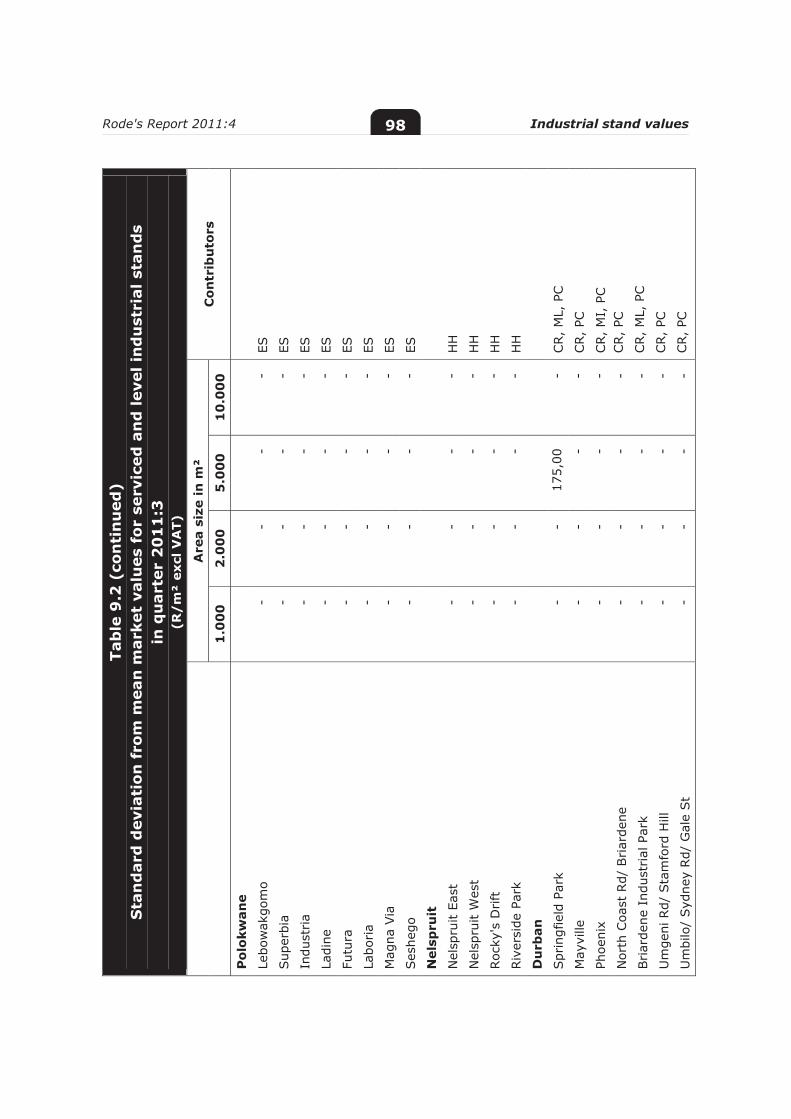

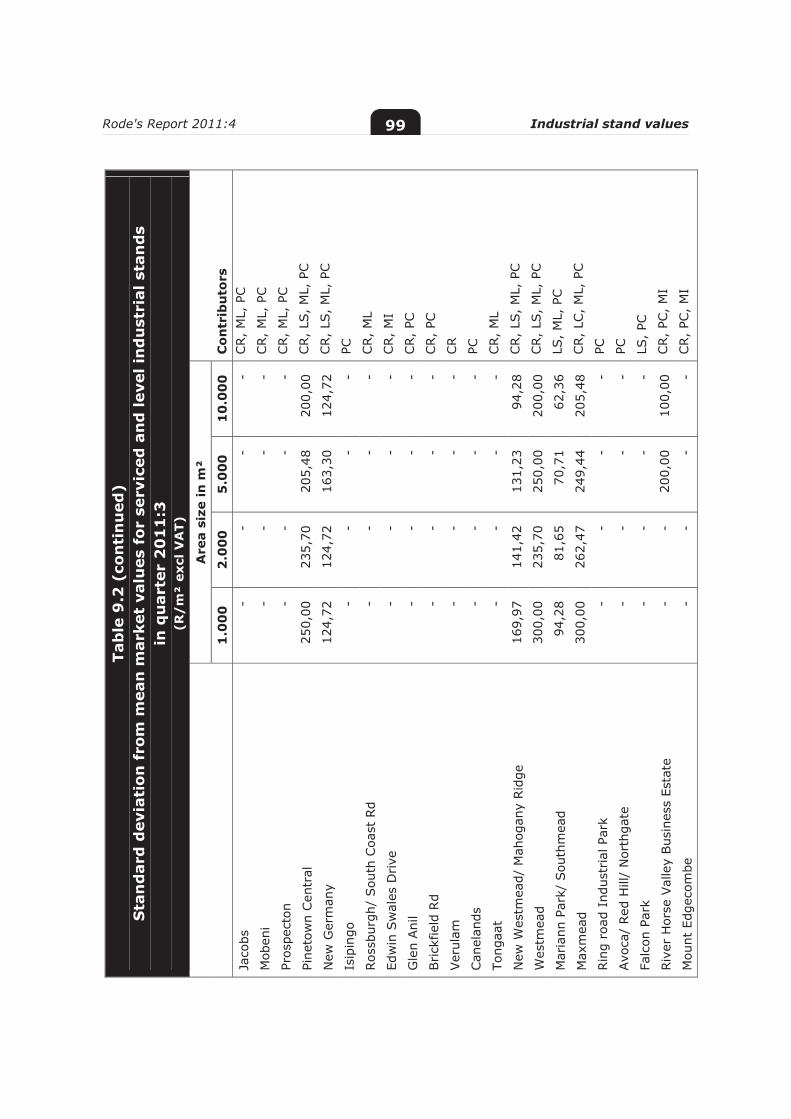

Table 9.1: Market values for industrial stands 83

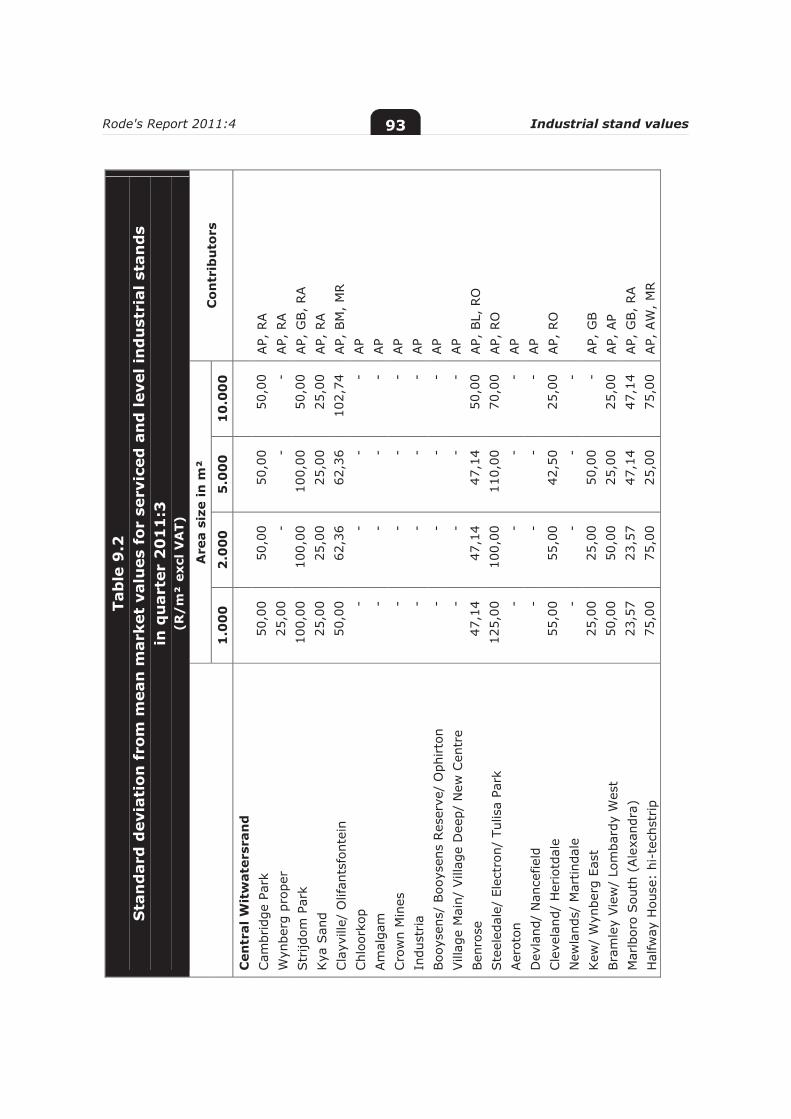

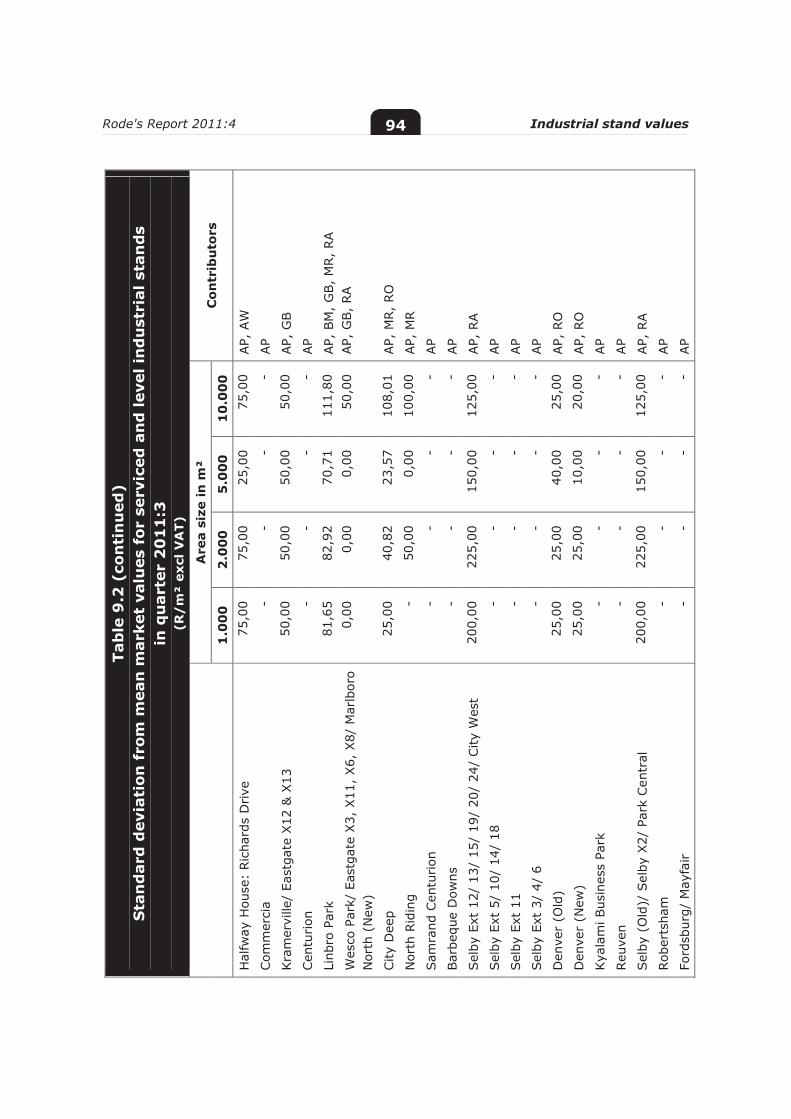

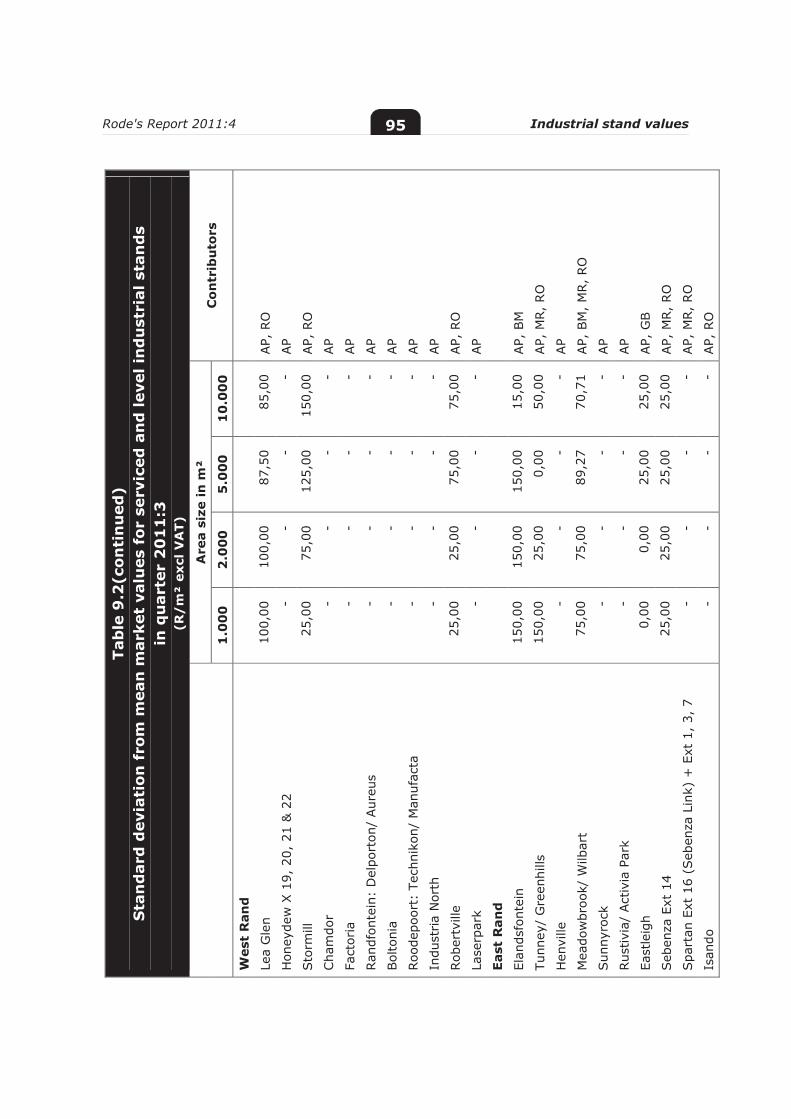

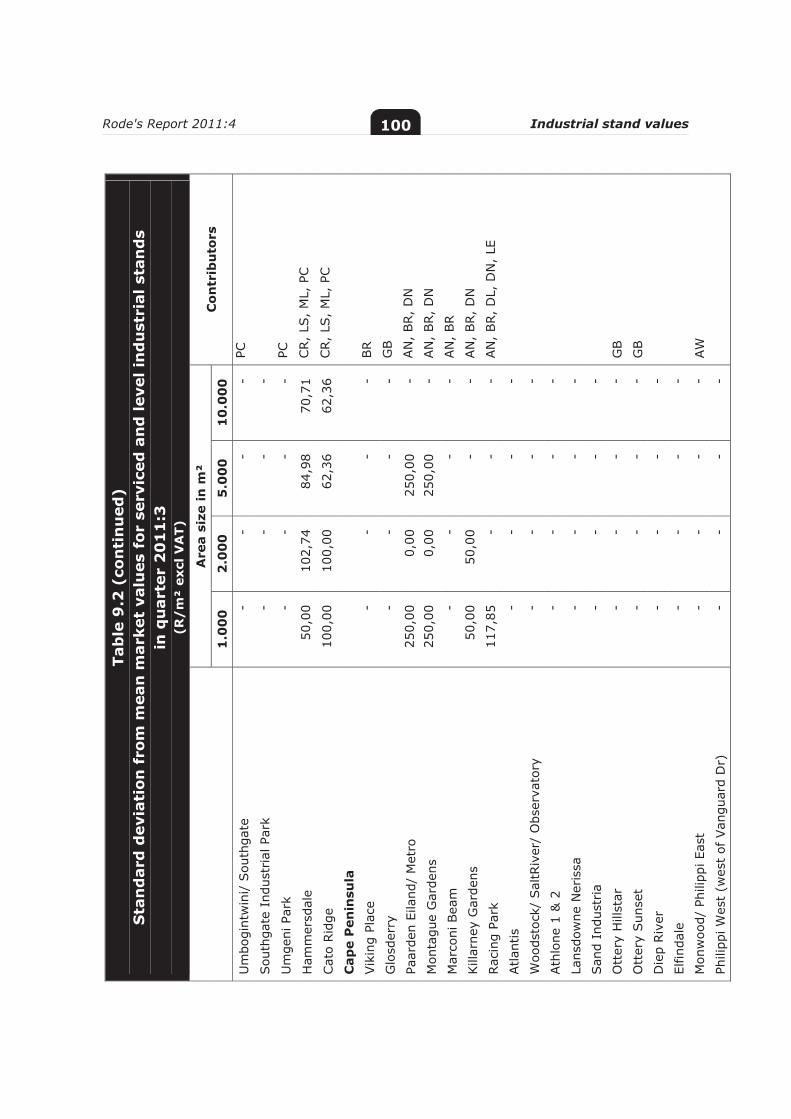

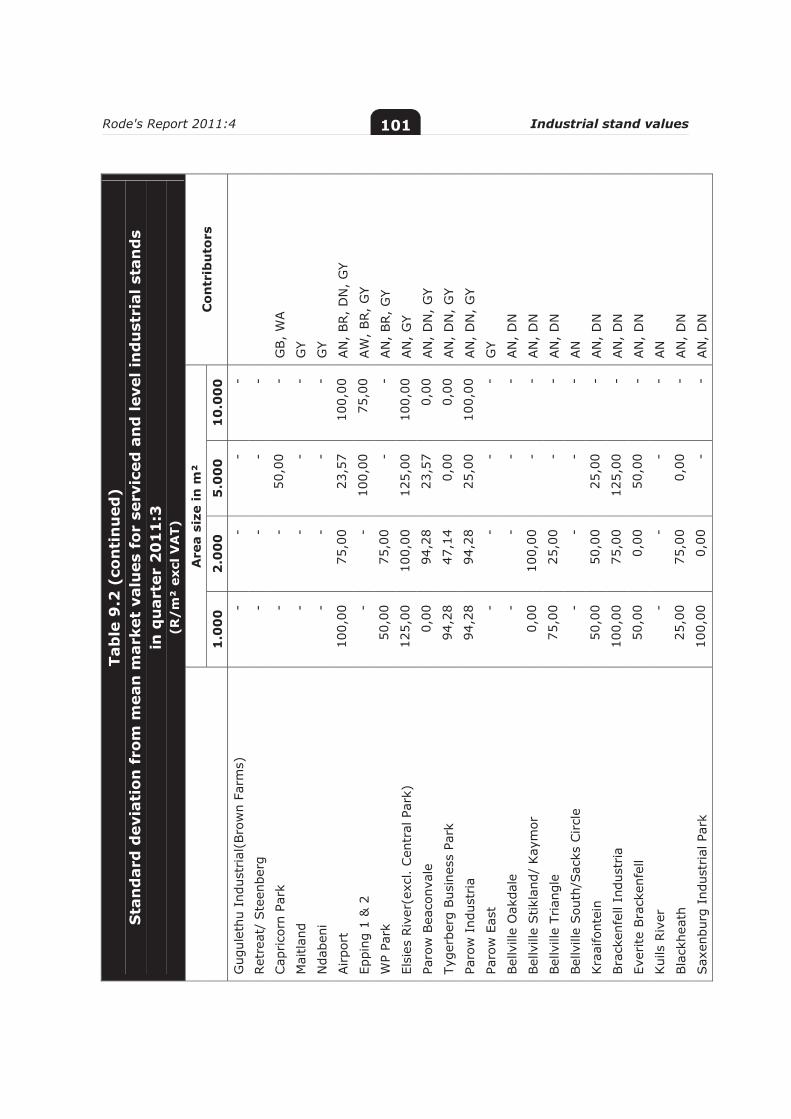

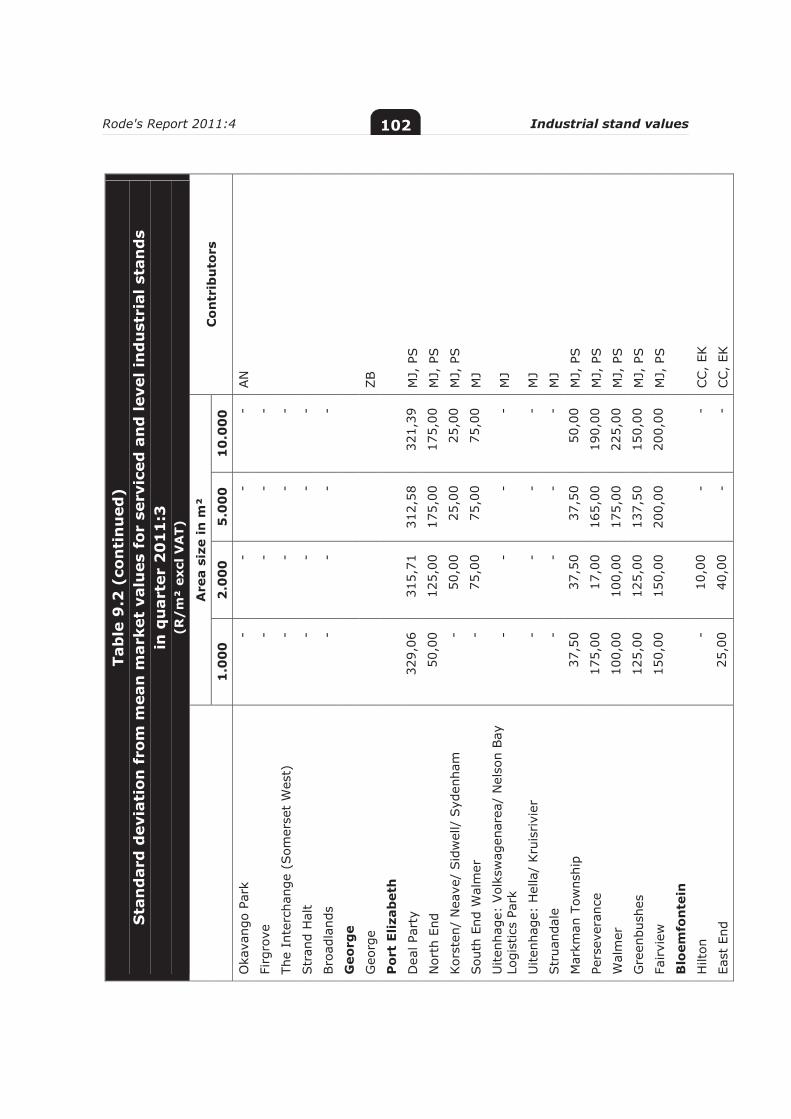

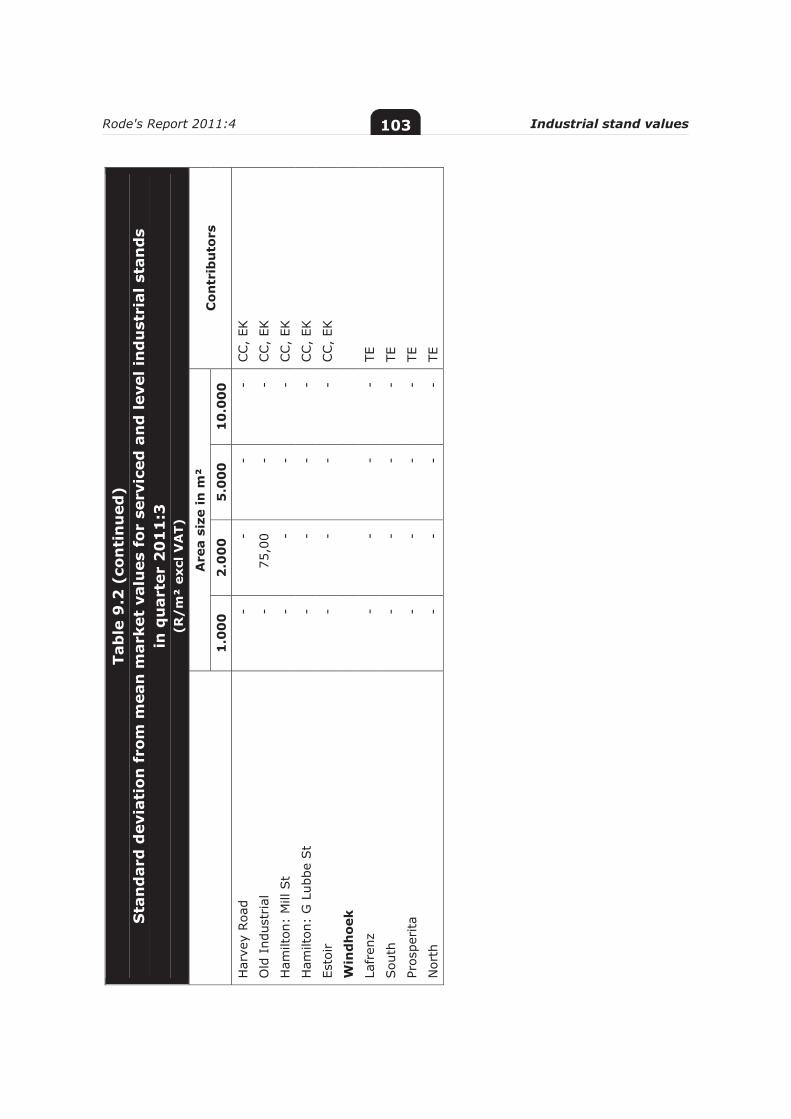

Table 9.2: Standard deviation from industrial stands 93

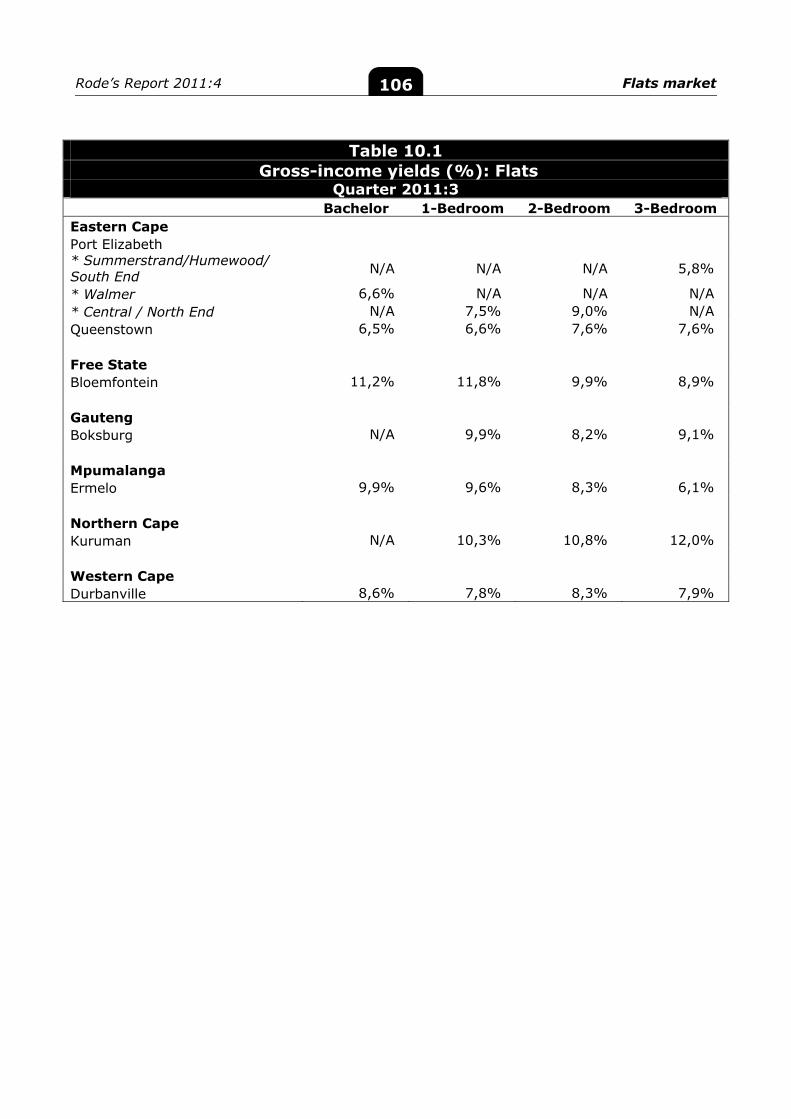

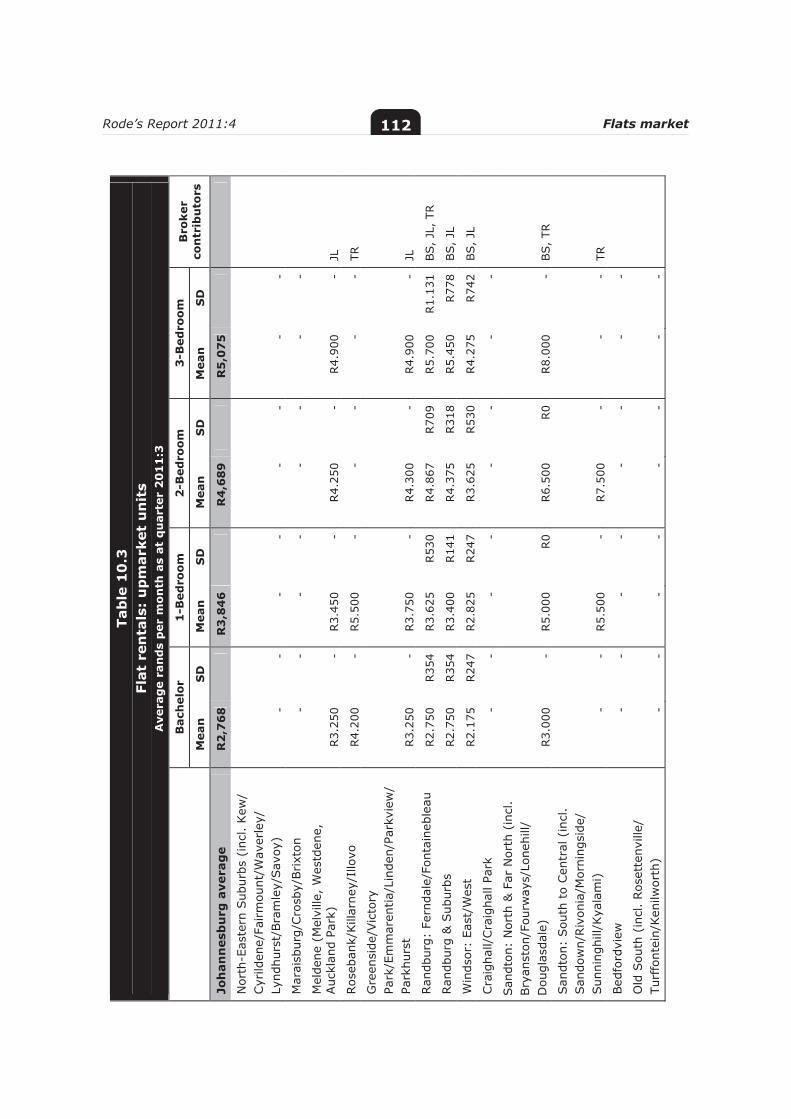

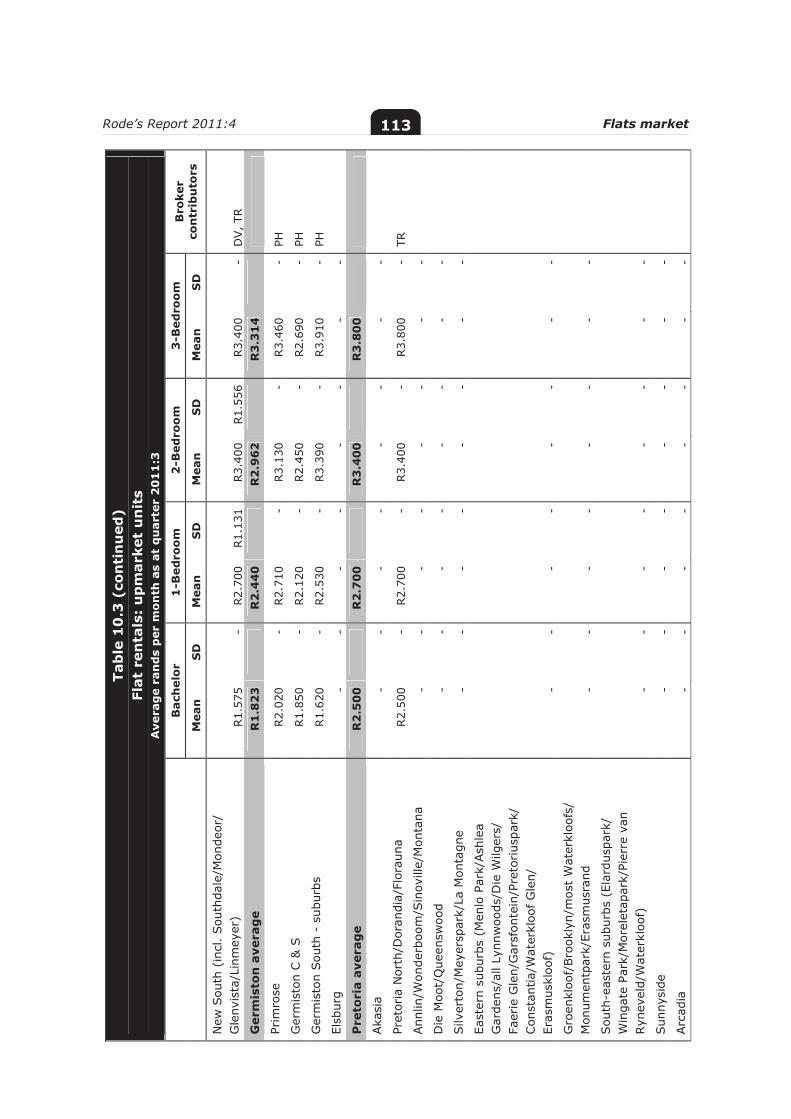

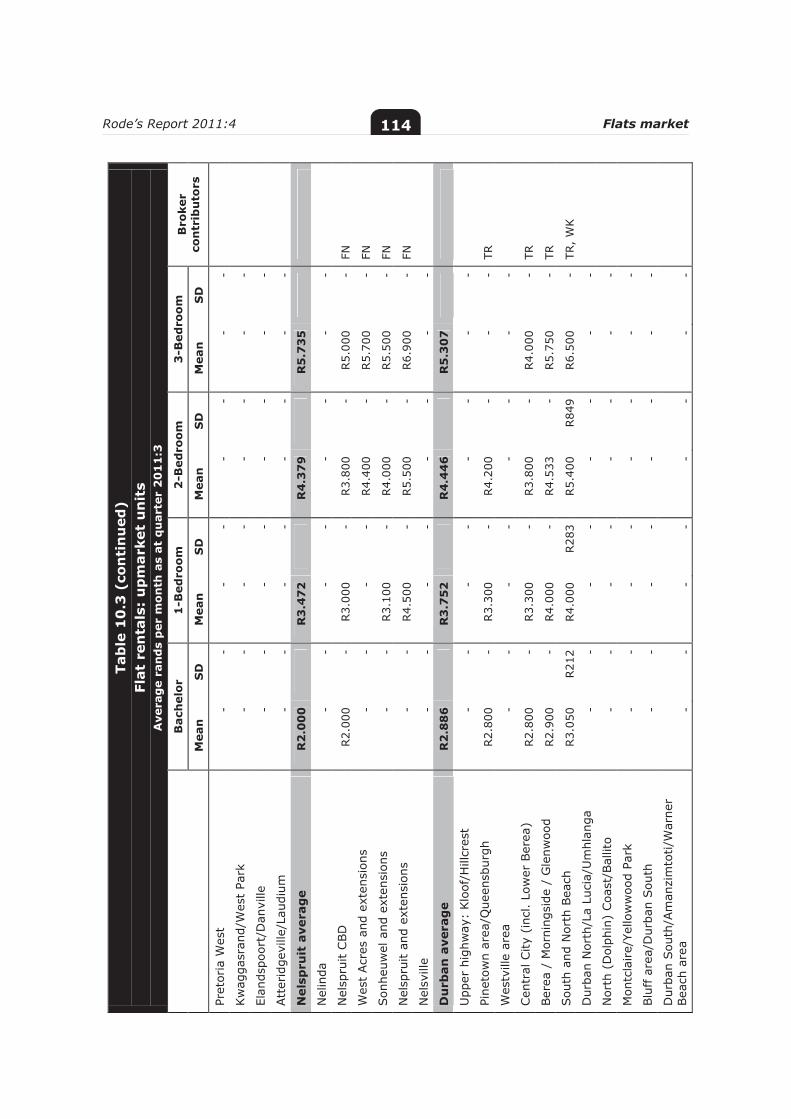

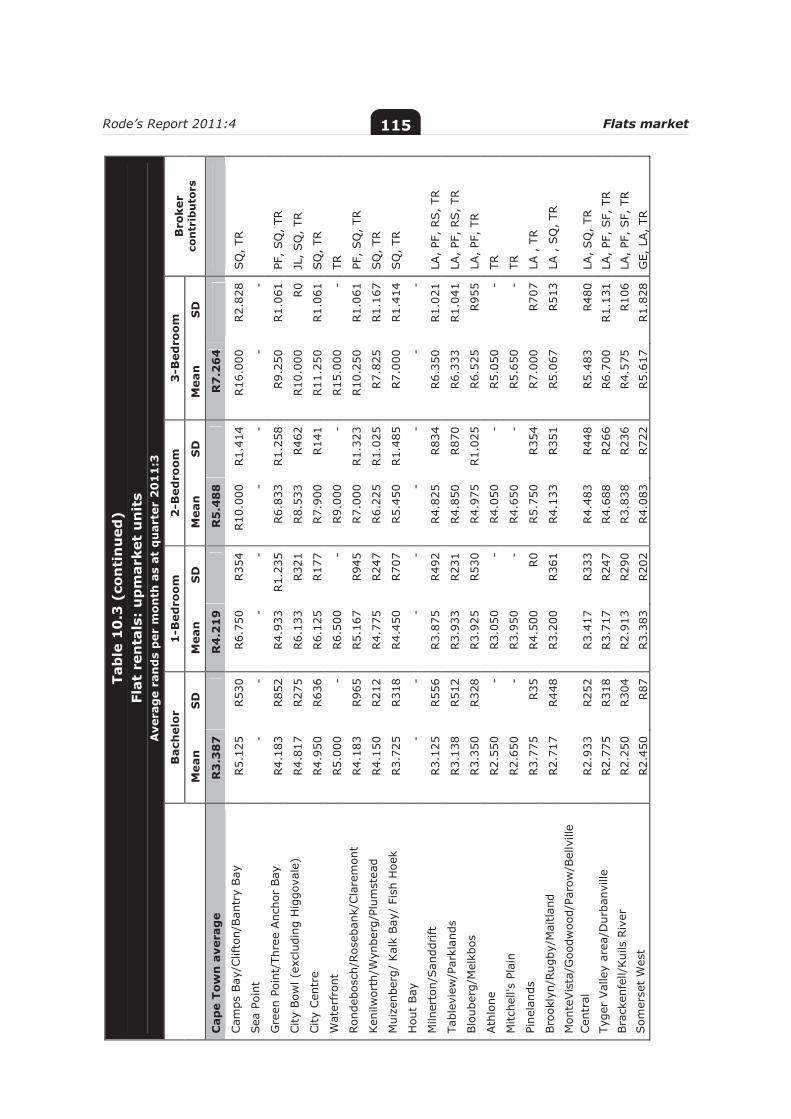

Table 10.1: Gross-income yields (%): Flats 106

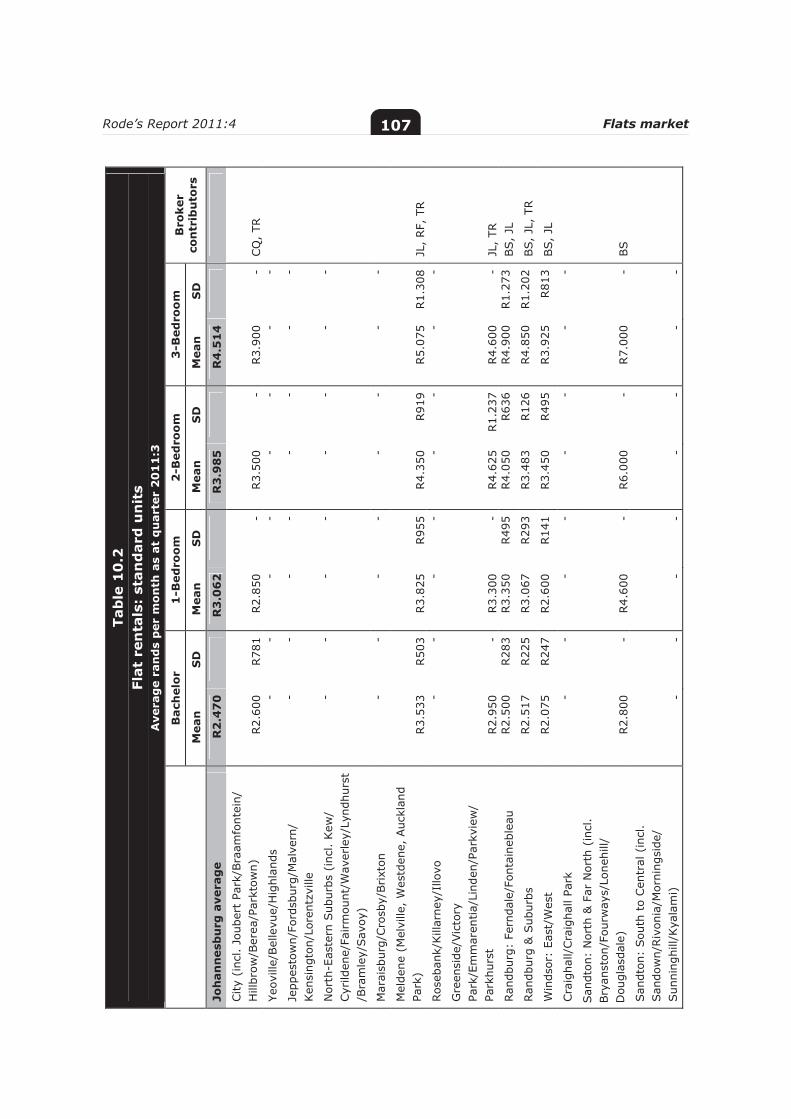

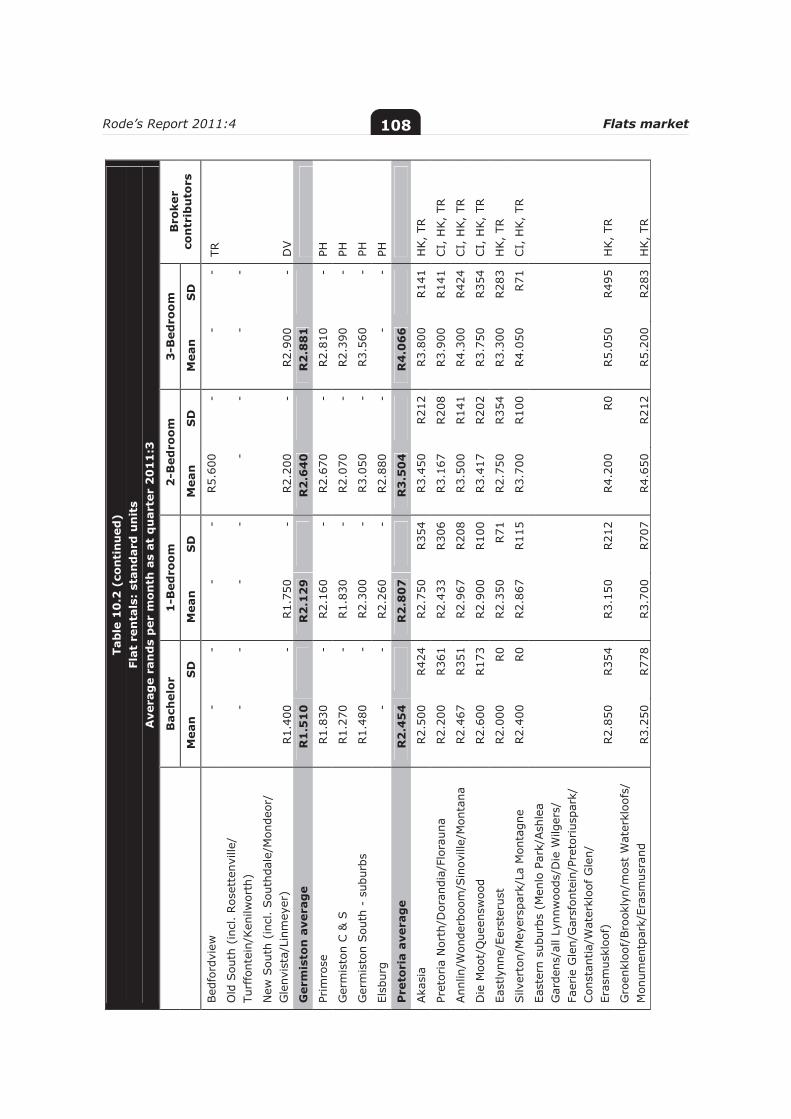

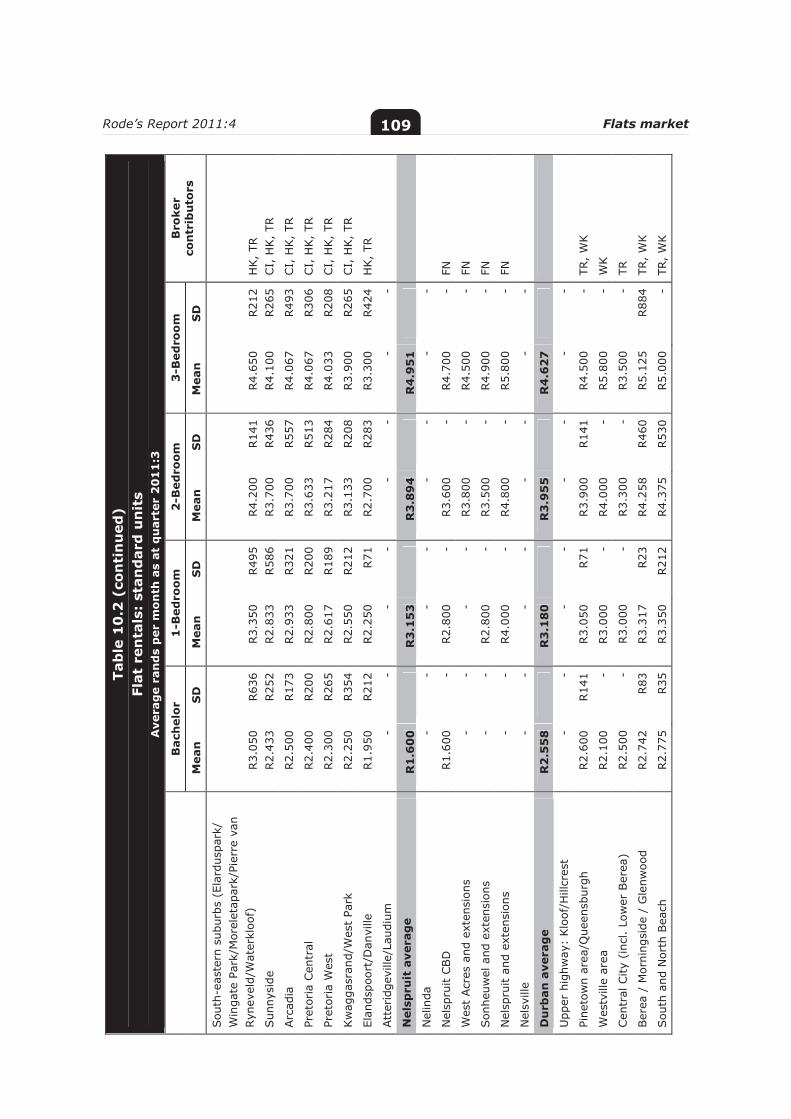

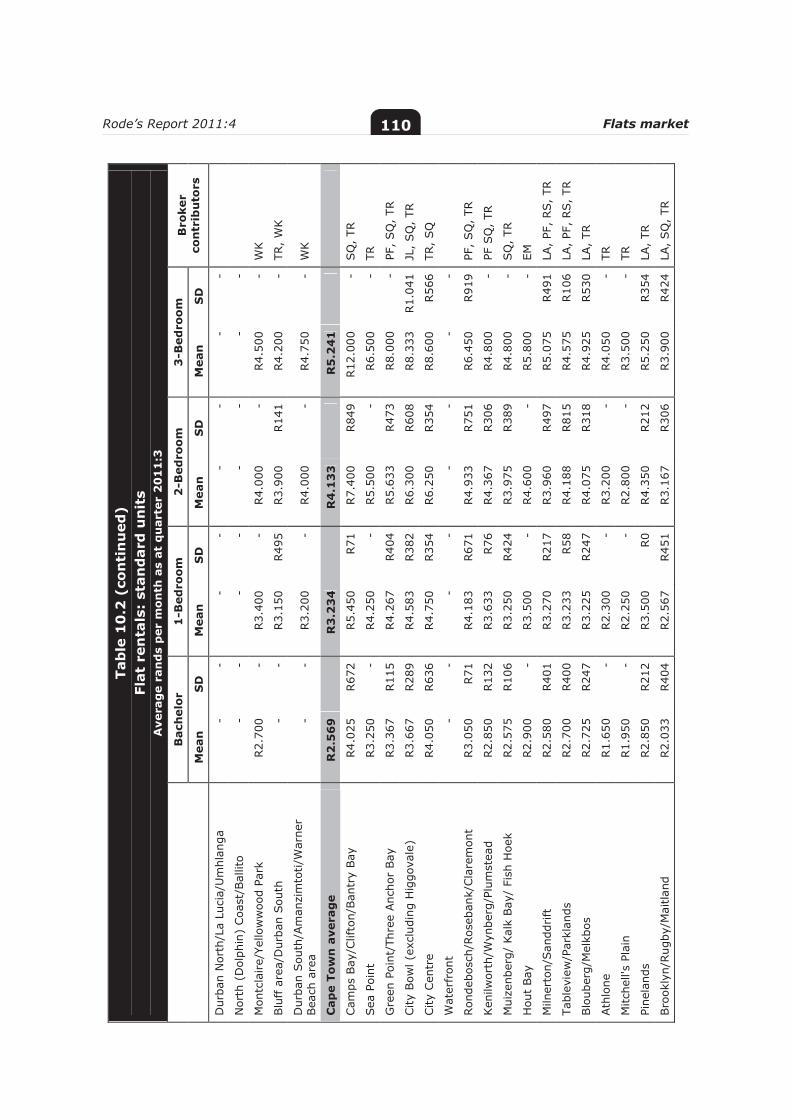

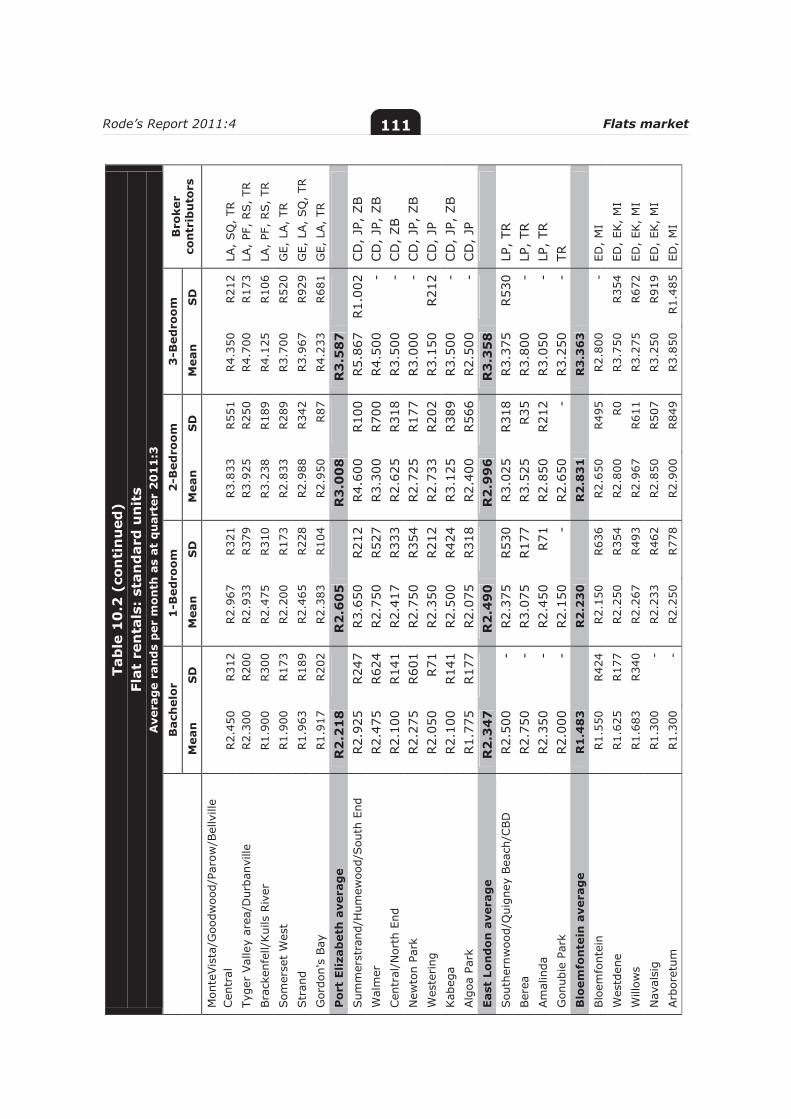

Table 10.2: Flat rentals: standard-quality block of flats 107

Table 10.3: Flat rentals: upmarket-quality block of flats 112

Table 11.1: Gross-income yields (%) on houses by price class 119

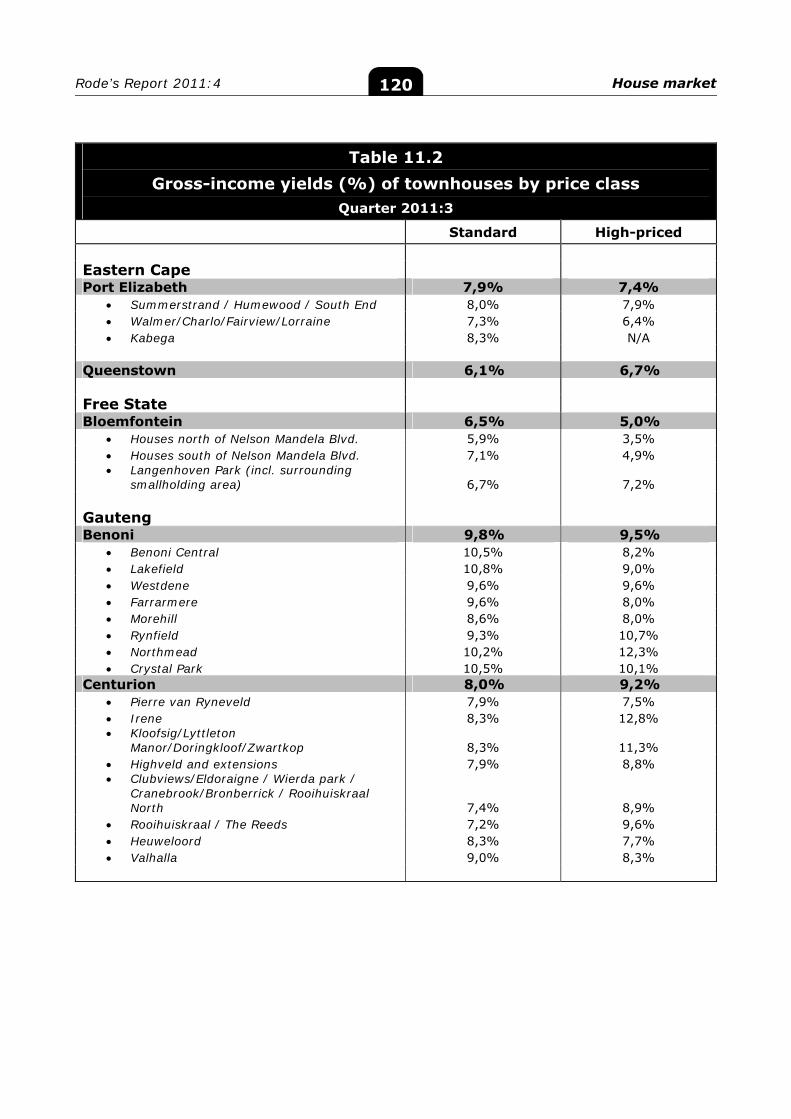

Table 11.2: Gross-income yields (%) of townhouses by price class 120

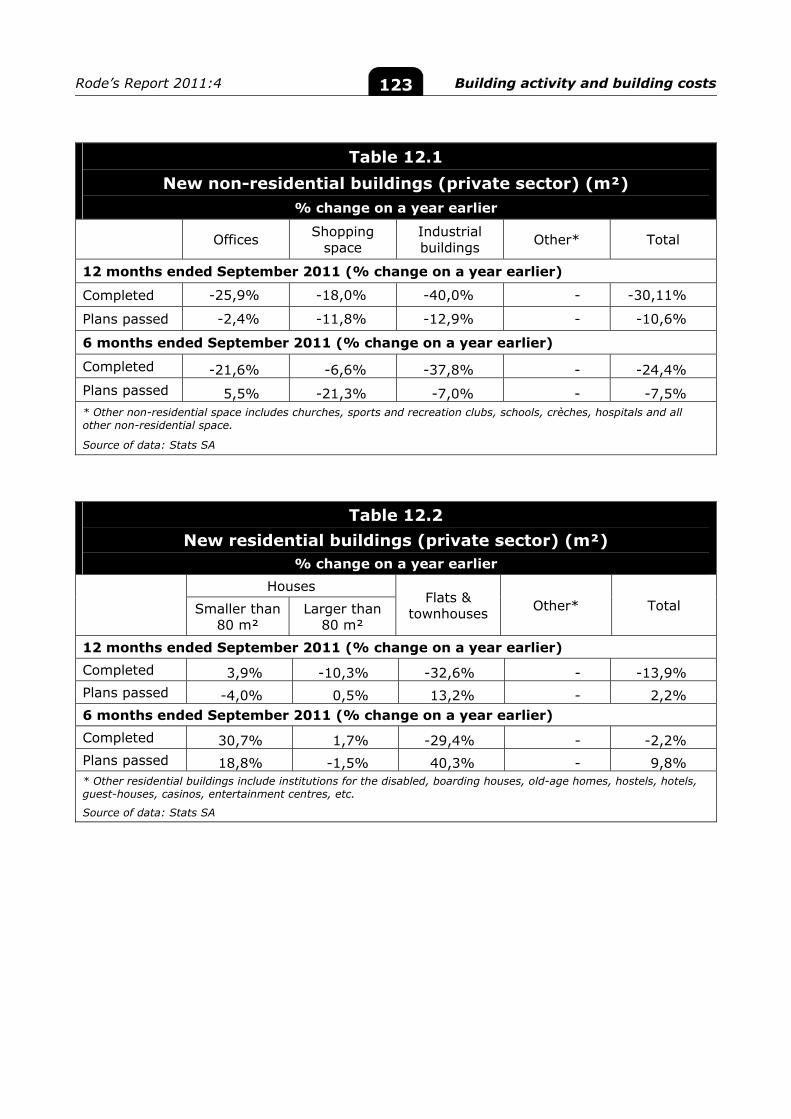

Table 12.1: New buildings completed (private sector)(m2) 123

Table 12.2: New residential buildings (private sector)(m2) 123

Rode’s Report 2011:4 xiv

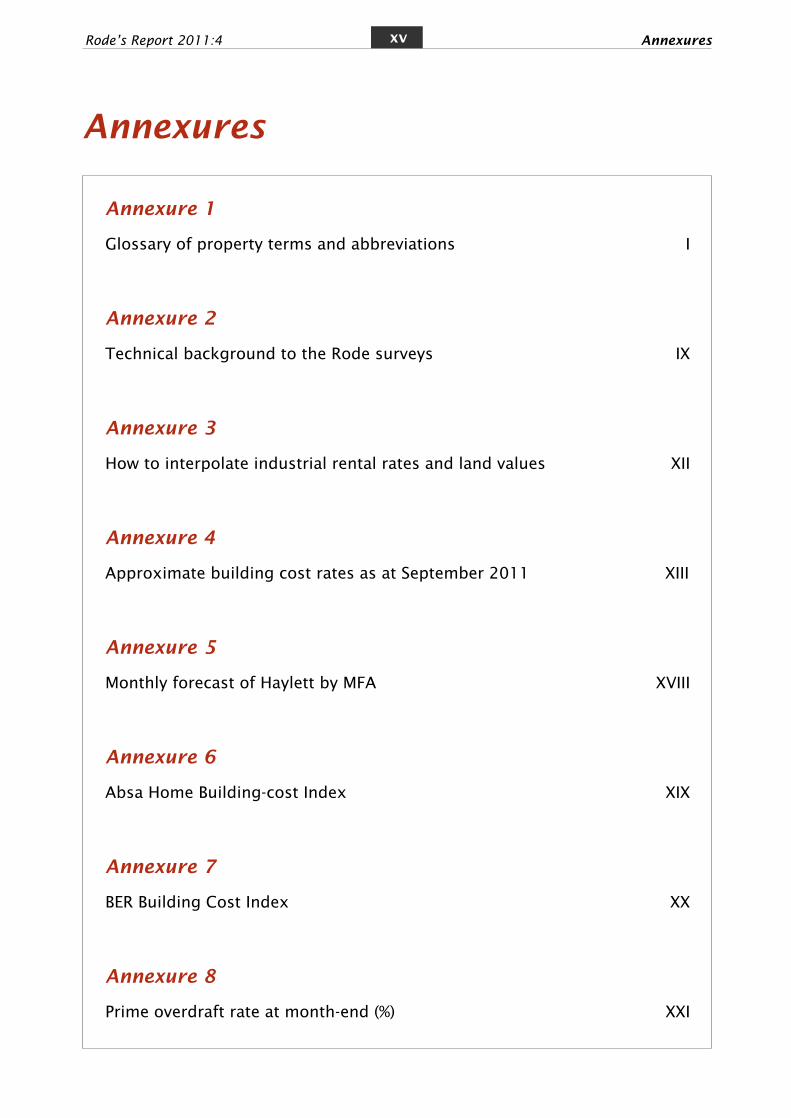

Annexures

Annexure 1

Glossary of property terms and abbreviations I

Annexure 2

Technical background to the Rode surveys IX

Annexure 3

How to interpolate industrial rental rates and land values XII

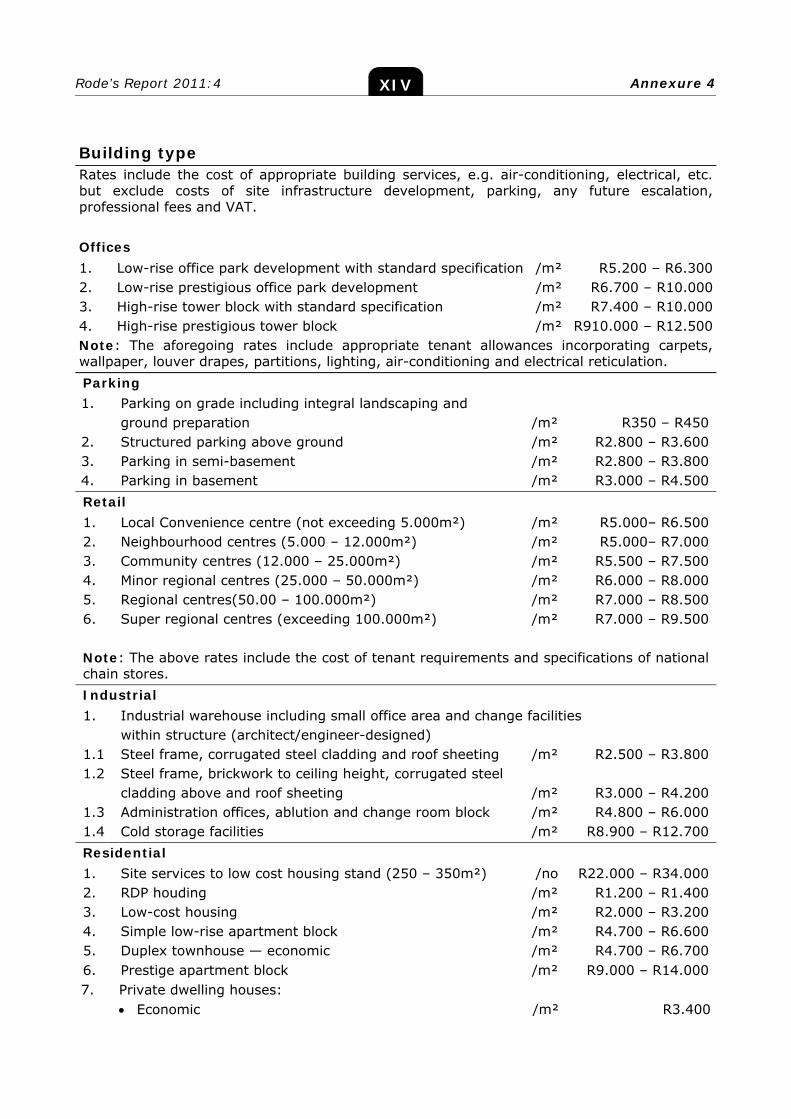

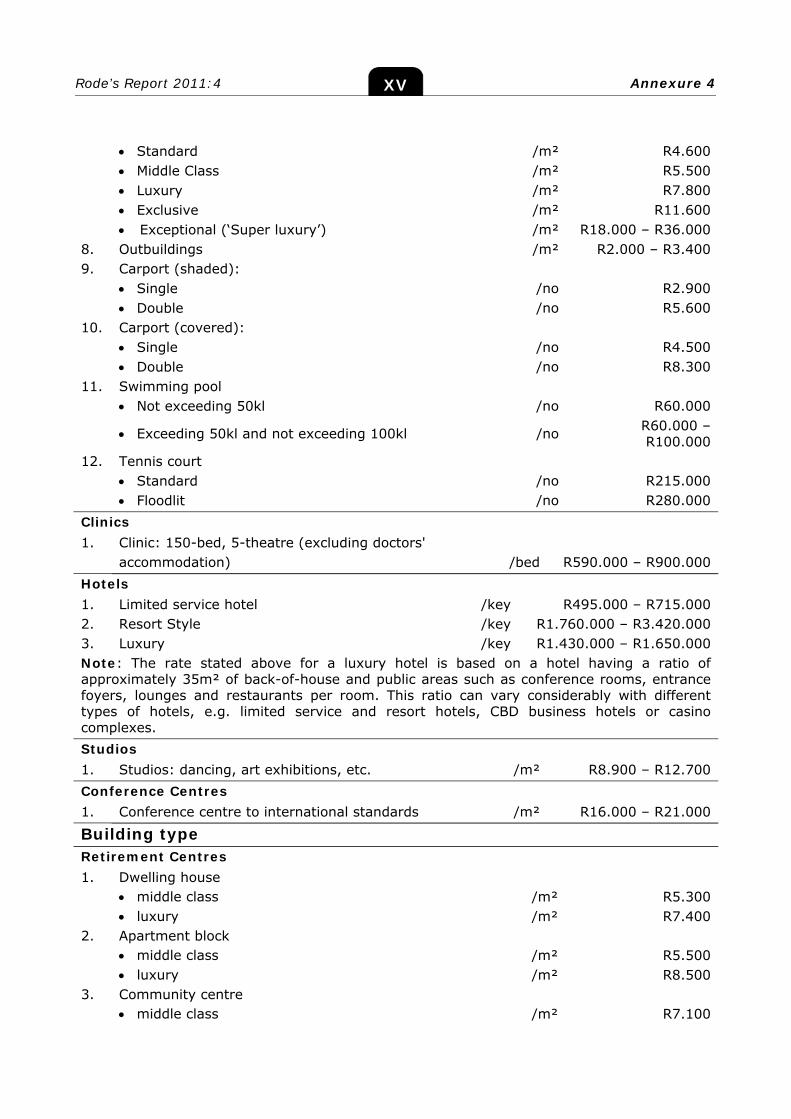

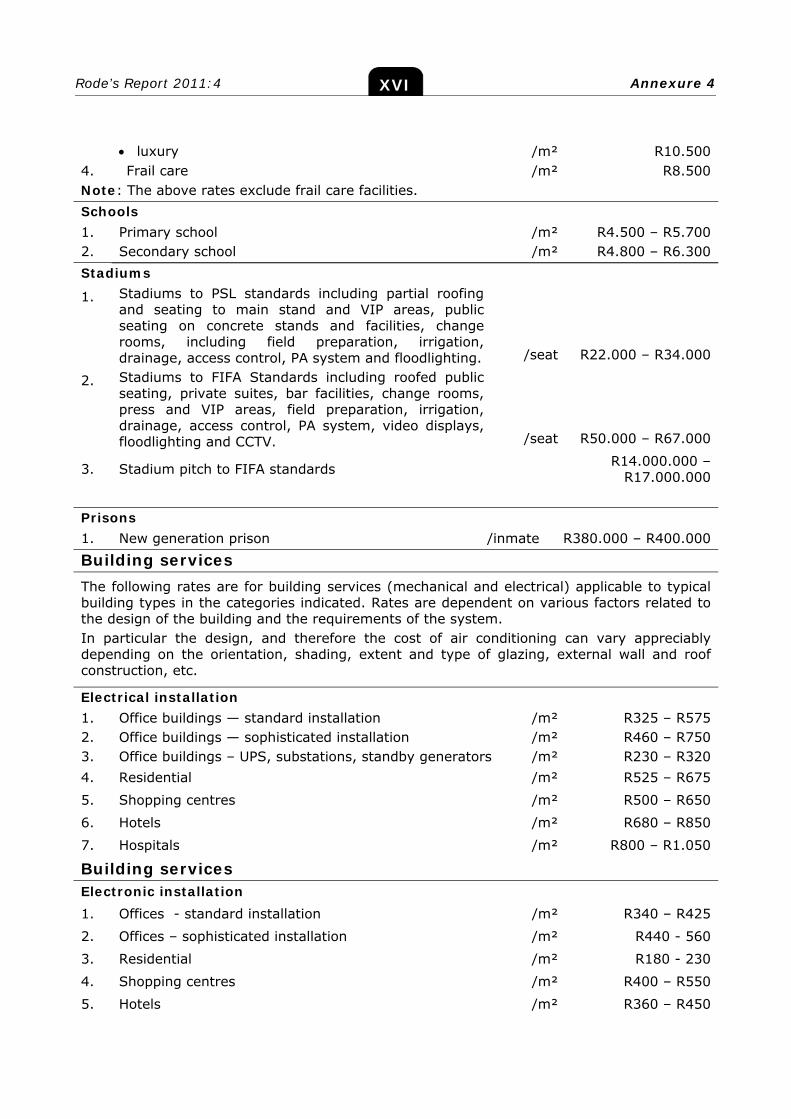

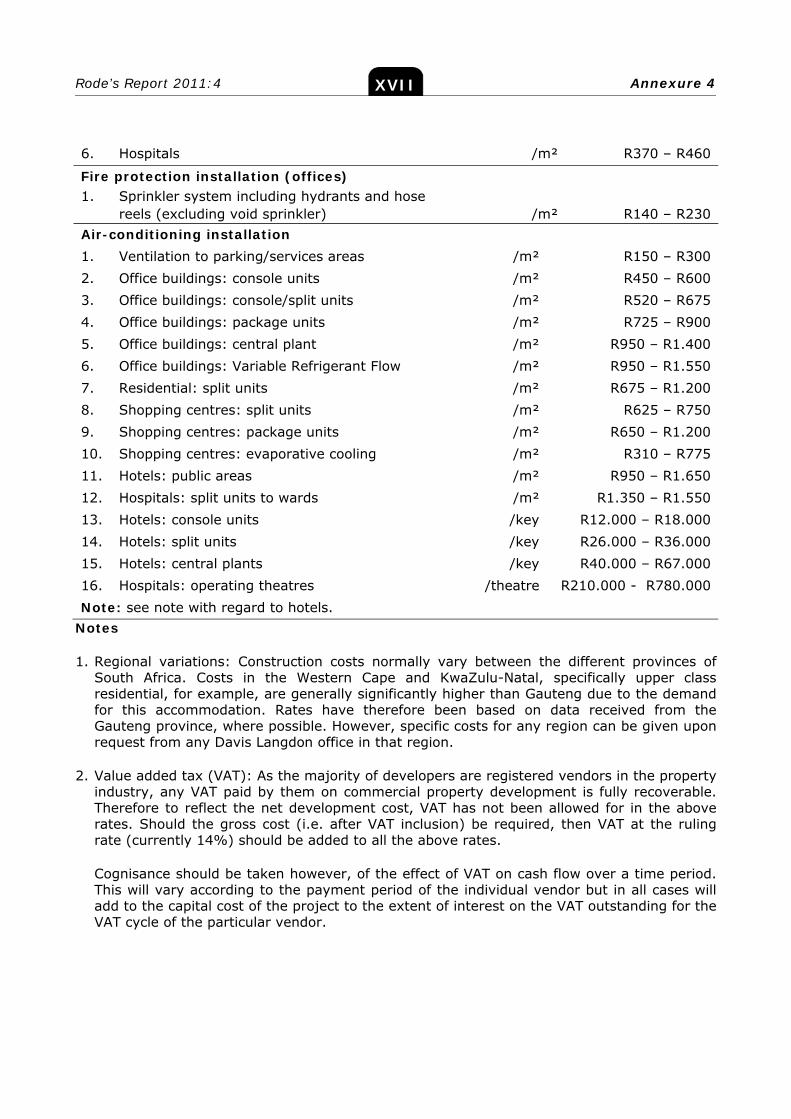

Annexure 4

Approximate building cost rates as at September 2011 XIII

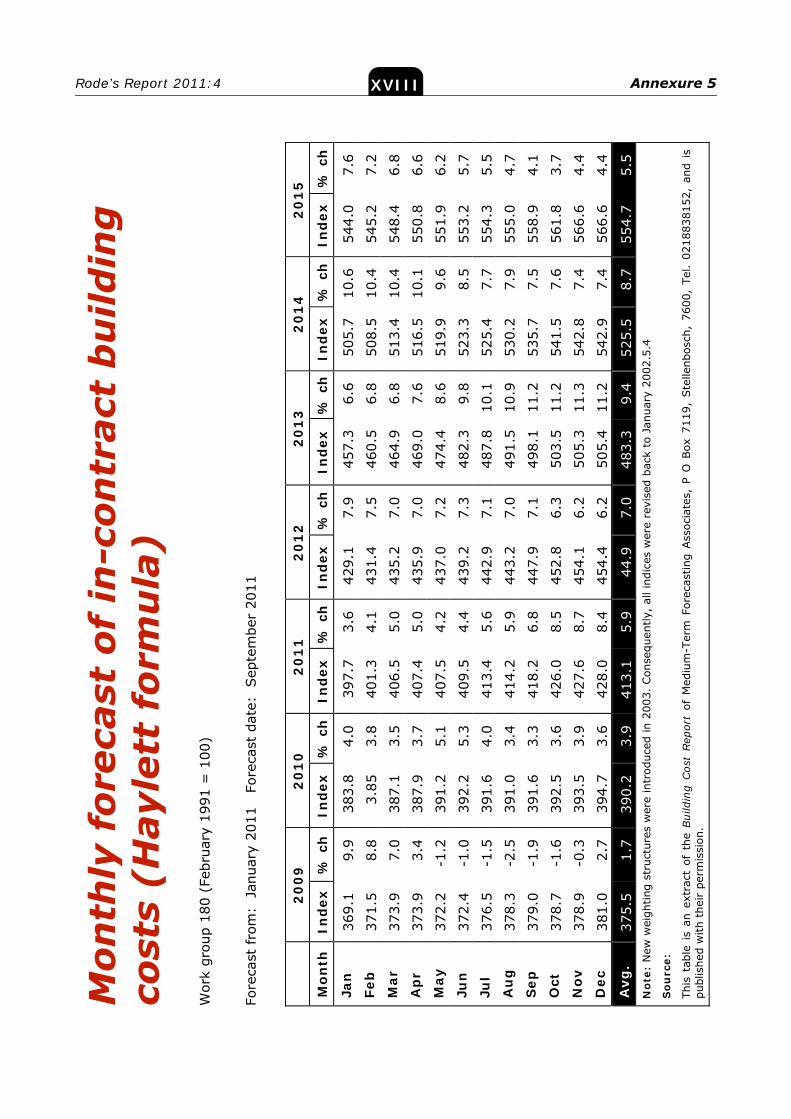

Annexure 5

Monthly forecast of Haylett by MFA XVIII

Annexure 6

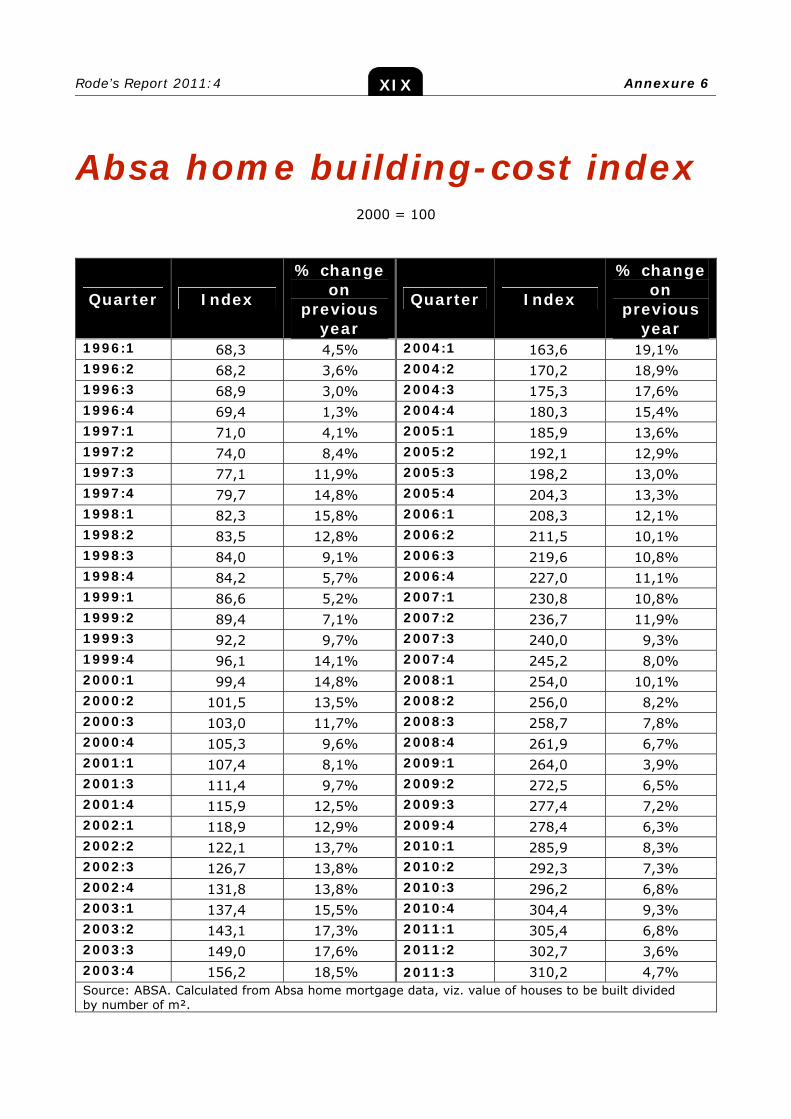

Absa Home Building-cost Index XIX

Annexure 7

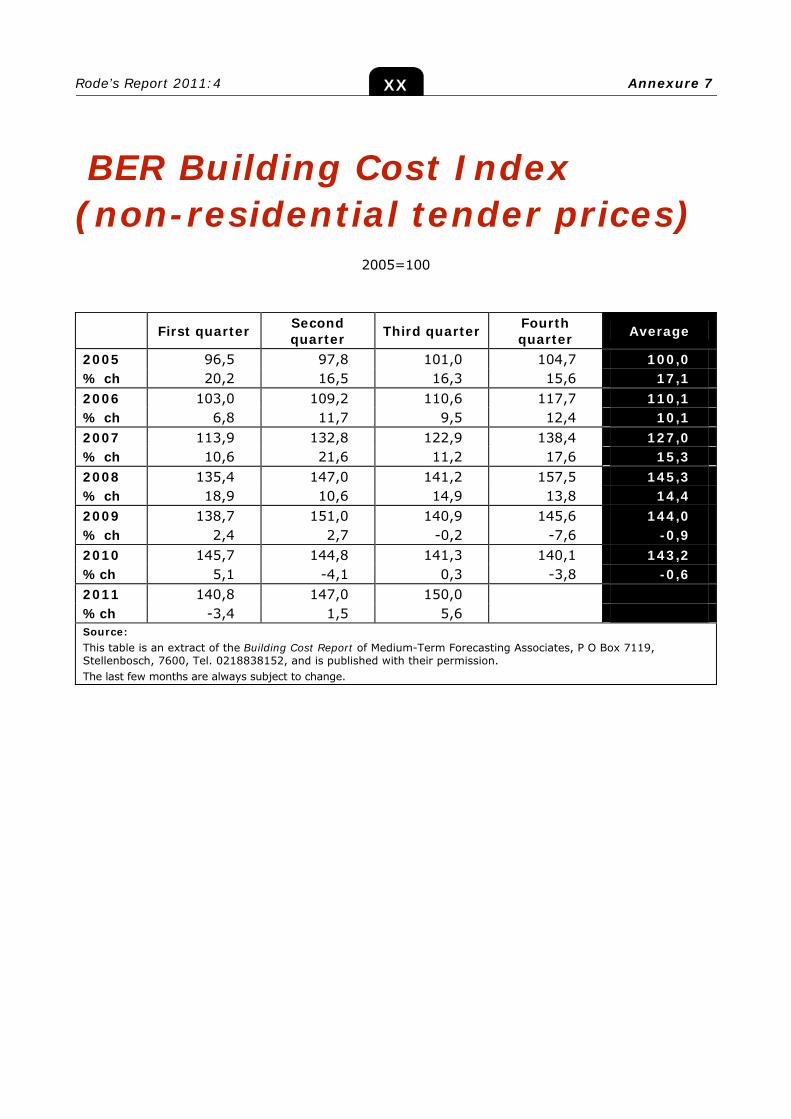

BER Building Cost Index XX

Annexure 8

Prime overdraft rate at month-end (%) XXI

Rode’s Report 2011:4 Annexuresxv

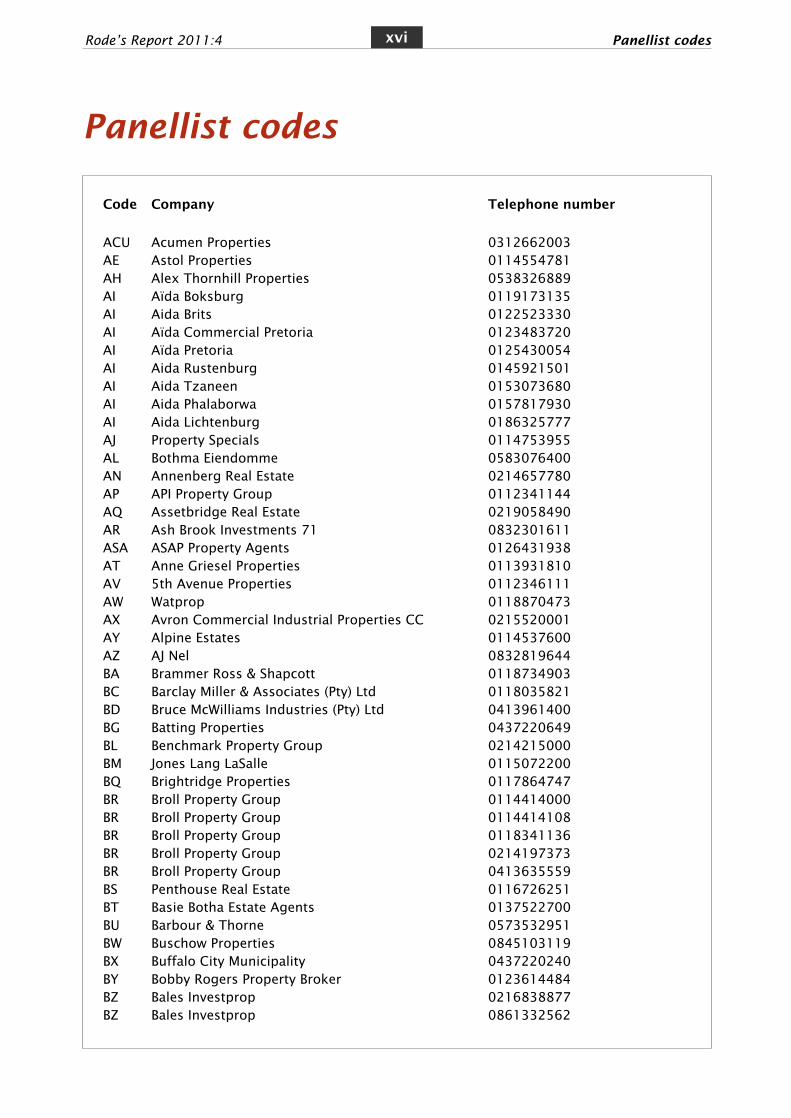

Panellist codes

Code Company Telephone number

ACU Acumen Properties 0312662003AE Astol Properties 0114554781AH Alex Thornhill Properties 0538326889AI Aïda Boksburg 0119173135AI Aida Brits 0122523330AI Aïda Commercial Pretoria 0123483720AI Aïda Pretoria 0125430054AI Aida Rustenburg 0145921501AI Aida Tzaneen 0153073680AI Aida Phalaborwa 0157817930AI Aida Lichtenburg 0186325777AJ Property Specials 0114753955AL Bothma Eiendomme 0583076400AN Annenberg Real Estate 0214657780AP API Property Group 0112341144AQ Assetbridge Real Estate 0219058490AR Ash Brook Investments 71 0832301611ASA ASAP Property Agents 0126431938AT Anne Griesel Properties 0113931810AV 5th Avenue Properties 0112346111AW Watprop 0118870473AX Avron Commercial Industrial Properties CC 0215520001AY Alpine Estates 0114537600AZ AJ Nel 0832819644BA Brammer Ross & Shapcott 0118734903BC Barclay Miller & Associates (Pty) Ltd 0118035821BD Bruce McWilliams Industries (Pty) Ltd 0413961400BG Batting Properties 0437220649BL Benchmark Property Group 0214215000BM Jones Lang LaSalle 0115072200BQ Brightridge Properties 0117864747BR Broll Property Group 0114414000BR Broll Property Group 0114414108BR Broll Property Group 0118341136BR Broll Property Group 0214197373BR Broll Property Group 0413635559BS Penthouse Real Estate 0116726251BT Basie Botha Estate Agents 0137522700BU Barbour & Thorne 0573532951BW Buschow Properties 0845103119BX Buffalo City Municipality 0437220240BY Bobby Rogers Property Broker 0123614484BZ Bales Investprop 0216838877BZ Bales Investprop 0861332562

Rode’s Report 2011:4 Panellist codesxvi

CB Centurion Letting & Sales 0126536180CC CCI Properties CC 0828211214CD Chris van der Walt Properties 0415821110CE Cenprop Real Estate 0333949595CF Cathy Cordier Eiendomme 0562121518CI City Property Administration 0123198811CL Cleomic Property Consultants 0117061591CM Capitol Commercial Properties 0219141840CN Citynet 0114833930CP Citiprop Real Estate 0214658391CQ Connaught Properties (Pty) Ltd 0117252780CR Colliers International 0215915067CR Colliers International 0312672001CR Colliers International 0413742205CS Chase & Sons 0164213170CU Africape Property Investments (Pty) Ltd. 0219144533CV Chris Hearn and Associates 0314629270DA Dallas Properties CC 0118273417DC Dave Furness Properties 0136536330DD Diamond Properties 0214340001DE Dedekind Real Estate 0366372297DG DG Ladegaard Real Estate 0169339633DK Direct @ Home Estates 0186320269DL Delta Real Estate 0219302343DN David Newham Property Management 0219480934DO Bainprop (Pty) Ltd 0116092542DP De la Porte Property Group 0215519777DQ DesKay Real Estate 0437484252DT DTZ Leadenhall (Pty) Ltd 0112742300DV Dan Viljoen Estates 0116832345DW Divaris Property Brokers 0215311551EB ERA Real Estate 0145974977EB ERA Bundu Properties 0157810589EB ERA Ermelo 0178192398EB ERA Sun Properties 0436433024EB ERA National George 0448741113EB ERA Kuruman 0537123503EC EVS Elite Valuation Services 0741922667ED Edric Trust 0514489431EH Ermelo Homenet 0178192880EJ Erasmus JoosteIng 0184734511EK Ellenberger & Kahts 0514301511EL East London Estates & Auctioneering 0437351662EM Property Management & Rental Specialist CC 0217901991EP Ecclesiate Property Specialists 0458381131ER Associated Property Brokers 0437260501ES Eli StröhEdmsBpk 0152975890EV Engel & Völkers Commercial Properties 0123467777FN Fine & Country Bethlehem 0583032333FN Fine & Country Kellaprince 0137544400

Panellist codesxviiRode’s Report 2011:4

FO Fosprops Properties/ Homenet 0357898583FP PPA Property Development CC 0123429099FR Fraser & Hurd (Pty) Ltd/Fraser Properties 0413654445GB Galetti Commercial and Industrial 0214186308GB Galetti Commercial and Industrial 0117831195GE Gustrouw Estates (Pty) Ltd 0218547220GO Pam Golding 0218711480GO Pam Golding 0583035565GO Pam Golding Commercial 0214177878GO Pam Golding Commercial 0437054040GW Goldswain Investments 0437222876GY Guy de la Porte Property Solutions 0217948879HE Homelet Grahamstown 0466222839HH Hendrik Tryhou Property Consultants 0137441671HK Huurkor 0124008600HN Harcourts Heloman 0118246028HN Harcourts Jana-Marie Real Estates 0155161526HN Harcourts Excellence 0184687089HN Harcourts Queenstown 0458382560HN Harcourts Parklane 0333423340HS Summerton Edelson Commercial CC 0415811768IP InvestPro 0437263116JL Just Letting Randburg/ Northcliff 0117932757JL Just Letting Potchefstroom 0182931858JL Just Letting City Bowl 0214233344JP John Price Estates 0415833903KA Kailas Property Bureau 0114826461KC Keith Roux Properties 0437213465KE Keydom Real Estate 0132826187KI Kitchings Agencies 0419229870KM Kirchmann-Hurry Investments Ltd 0117067131LA Landlords “We do Rentals” 0219751770LD Lendac Property Brokers 0732148655LF Louis Group Properties 0214223030LH Leader Homes 0538313955LM Louis Kruger Property Management 0219033101LP Les' Property and Rentals 0437266933LS Lock Sloane & Partners 0317011010MD Mont Blanc Projects & Properties (Pty) Ltd 0826005326MI Platinum Global 0514474711MJ Majola & Boyd (Pty) Ltd 0861111789ML Mindry Properties CC 0317834307MO Moolman Group of Companies 0152914700MP Monarch Rentals (Kingdom of Rentals) 0118494211MR Marder Properties 0114531220MW Mc William Murray Realty 0312674800NE Newbridge Property Services 0219139131NR National Real Estate 0514059933OC Omnicron Commercial Property Brokers (Pty) Ltd 0219147363OD Oudtshoorn Eiendomme 0442725895

Panellist codesxviiiRode’s Report 2011:4

OG Oscar Saunderson Group 0215914499OM Old Mutual Investment Group Property Investments 0313661811OM Old Mutual Properties 0437270990OP Omnipark Pty (Ltd) 0216836077PA Pace Property Group 0112175959PC Propco (1985) (Pty) Ltd 0312090161PE Property Scene Group 0413734146PF Permanent Trust Property Group 0214418800PG Proximo 0176312033PH President Estate & General Agents (Pty) Ltd 0118738707PI PHG Property Group 0514488831PJ Profile Property Solutions 0333472786PK Philips Property Brokers 0117826007PL Pears Property Consultants (Pty) Ltd 0217623474PM PDL Property Management (Pty) Ltd 0137527333PN Propergation Estates 0219146444PQ Pro-Net Estates 0132433113PR Harcourts Polla Scheepers 0343125841PS Property Scene Real Estate 0357923217QC Cosmoprop Commercial Property Brokers 0219148035QS Commercial Space 0216714343QU Quadrant Properties 0115309840RA Real Estate & Property Services 0878081578RD Redefine Income Fund 0112830028REW Real Estate @ Work 0836328011RF Rent-A-Flat 0117891007RM Remax Kuruman 0537123123RO Reef Property Consultants 0116821827RQ Realty Value 0357891376RR Realnet 0137532544RS Rawson Properties Milnerton 0215587102RY Rita Stipec Properties 0152954537RZ Oriprops 0137528091SC Stockton Property Consultants 0114259857SF Seeff Durbanville & Brackenfell 0219755290SO Simmons & Associates 0437221705SN Selection Estates 0867555545SQ Steer & Company 0214261026SX Status-Mark 0116680100TE Trust & Estate Co. 0026461231224TG Theo Goosen Estate Agents 0152959014TH Trevor Hosioski Investment Properties 0117834569TR Trafalgar Property Services 0112145200TR Trafalgar Property Services 0123265963TR Trafalgar Property Southern Suburbs 0214105500TR Trafalgar Property & Financial Services 0313017017TR Trafalgar Property Management 0437266066UN Unified Properties 0437482323VD Van der Westuizen Eiendomme 0536310846WA Wall & Smith Property Consultants 0217972552

Panellist codesxixRode’s Report 2011:4

WJ Warren Jack Property Group 0413656200WK Wakefields Property Management (Pty) Ltd 0312047400ZB Sotheby's International Realty PE 0413630168ZB Sotheby's International Realty George 0448732519ZB Sotheby's International Realty 0466361388ZE Zenith Properties 0562123207ZZ Anon

Panellist codesxxRode’s Report 2011:4

Acknowledgements

The writers of Rode's Report express their sincere thanks to:

1. Sapoa, for use of the basic data from their office vacancy surveys, which

we analysed further.

2. Medium-Term Forecasting Associates (MFA) of Stellenbosch, for the use

of their monthly forecast of building-input costs (Haylett), as well as

their leading indicator of building activity. Also for their kind permission

to publish the Bureau for Economic Research’s building-cost index, to

which they hold the marketing rights.

3. Absa for the use of their home-building-cost index.

4. Davis Langdon, an AECOM company, for the use of their building cost

data for various building types.

5. Juwayra Januarie, who manages the surveys and compiles the annexures

and Lynette Smit and Angelique Claasen for their technical assistance.

6. All the panellists who so kindly gave of their time and expertise in

responding to our surveys. The complete list of panellists who contribute

to the RR, together with their codes, appears on the following page.

For each of the survey tables in the RR you will find, listed against every

node or area, the codes for all the panellists who contributed information

this quarter.

7. Ken Gardner, who has the task of making sure that all gross grammar

mistakes are corrected.

8. The JSE Securities Exchange, Statistics South Africa and the Bond Exchange

of South Africa for the use of their data.

9. Other property practitioners throughout South Africa, experts in their

fields, too numerous to mention individually. Without the generous

assistance of these professionals, much of our research would be

impossible.

AcknowledgmentsxxiRode’s Report 2011:4

Foreword

Dear Reader

Welcome to the fourth issue of Rode’s Report on theSouth African Property Market (RR) for 2011, whichreports on surveys conducted in the third quarter of2011.

As usual, we report on movements of a number of criticalproperty variables, ranging from capitalization rates,rentals, escalation rates, land values, and operating costsfor the non-residential property market, to changes inhouse prices and flat rentals in the residential property market.

Readers are again reminded of our website – www.rode.co.za – which containsinteresting and relevant property-related articles, most of which are publishedin our monthly e-newsletter, to which readers can subscribe through ourwebsite. It’s free of charge.

If you want to communicate with a specific niche market, you can contactLynette on 082-323 5799 for RR advertising rates.

Juwayra Januarie and Biancé Johnson are in charge of expanding our surveypanel; their job is to give you access to the opinions of as many propertyexperts as possible. We appeal to all market participants who feel they havewhat it takes to become an RR panellist, to please contact Juwayra or Biancéon 021-946 2480 – it’s for the benefit of everyone in the industry. As apanellist you will also get invaluable exposure.

Happy reading!

Sincerely

John S. LotteringEditor

8 December 2011

ForewordxxiiRode’s Report 2011:4

Rode’s Report 2011:4 State of the property market

1

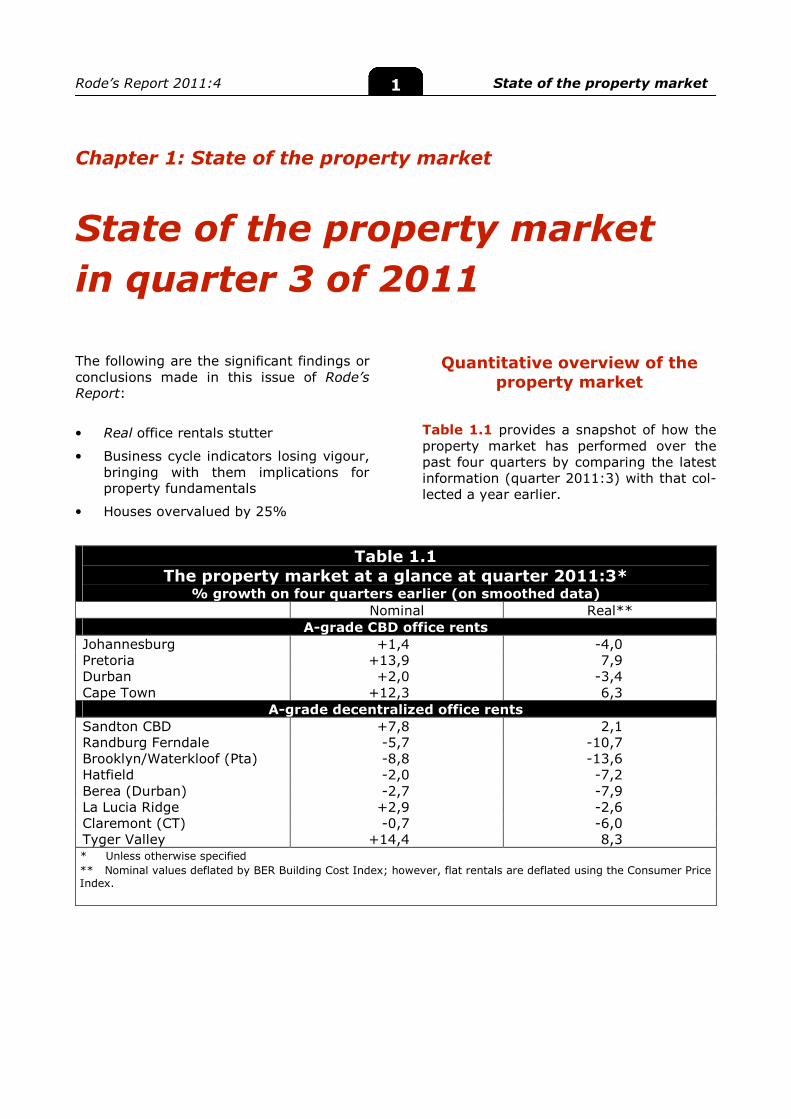

Chapter 1: State of the property market

State of the property market

in quarter 3 of 2011

The following are the significant findings or

conclusions made in this issue of Rode’s Report:

• Real office rentals stutter

• Business cycle indicators losing vigour,

bringing with them implications for property fundamentals

• Houses overvalued by 25%

Quantitative overview of the property market

Table 1.1 provides a snapshot of how the

property market has performed over the

past four quarters by comparing the latest

information (quarter 2011:3) with that col-

lected a year earlier.

Table 1.1

The property market at a glance at quarter 2011:3* % growth on four quarters earlier (on smoothed data)

Nominal Real**

A-grade CBD office rents

Johannesburg +1,4 -4,0

Pretoria +13,9 7,9

Durban +2,0 -3,4

Cape Town +12,3 6,3

A-grade decentralized office rents

Sandton CBD +7,8 2,1

Randburg Ferndale -5,7 -10,7

Brooklyn/Waterkloof (Pta) -8,8 -13,6

Hatfield -2,0 -7,2

Berea (Durban) -2,7 -7,9

La Lucia Ridge +2,9 -2,6

Claremont (CT) -0,7 -6,0

Tyger Valley +14,4 8,3 * Unless otherwise specified

** Nominal values deflated by BER Building Cost Index; however, flat rentals are deflated using the Consumer Price Index.

Rode’s Report 2011:4 State of the property market

2

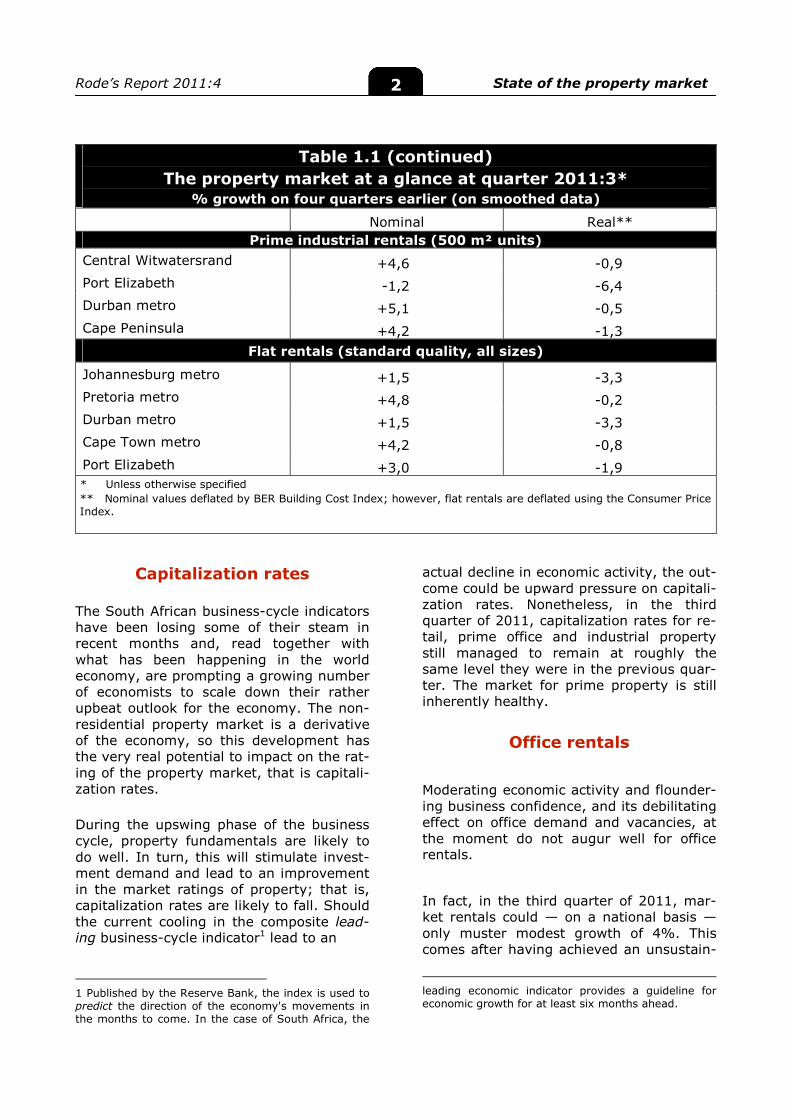

Capitalization rates

The South African business-cycle indicators

have been losing some of their steam in

recent months and, read together with

what has been happening in the world

economy, are prompting a growing number

of economists to scale down their rather

upbeat outlook for the economy. The non-

residential property market is a derivative

of the economy, so this development has

the very real potential to impact on the rat-

ing of the property market, that is capitali-

zation rates.

During the upswing phase of the business

cycle, property fundamentals are likely to

do well. In turn, this will stimulate invest-

ment demand and lead to an improvement

in the market ratings of property; that is,

capitalization rates are likely to fall. Should

the current cooling in the composite lead-ing business-cycle indicator1 lead to an

1 Published by the Reserve Bank, the index is used to predict the direction of the economy's movements in the months to come. In the case of South Africa, the

actual decline in economic activity, the out-

come could be upward pressure on capitali-

zation rates. Nonetheless, in the third

quarter of 2011, capitalization rates for re-

tail, prime office and industrial property

still managed to remain at roughly the

same level they were in the previous quar-

ter. The market for prime property is still

inherently healthy.

Office rentals

Moderating economic activity and flounder-

ing business confidence, and its debilitating

effect on office demand and vacancies, at

the moment do not augur well for office rentals.

In fact, in the third quarter of 2011, mar-

ket rentals could — on a national basis —

only muster modest growth of 4%. This

comes after having achieved an unsustain-

leading economic indicator provides a guideline for economic growth for at least six months ahead.

Table 1.1 (continued)

The property market at a glance at quarter 2011:3* % growth on four quarters earlier (on smoothed data)

Nominal Real**

Prime industrial rentals (500 m² units)

Central Witwatersrand +4,6 -0,9

Port Elizabeth -1,2 -6,4

Durban metro +5,1 -0,5

Cape Peninsula +4,2 -1,3

Flat rentals (standard quality, all sizes)

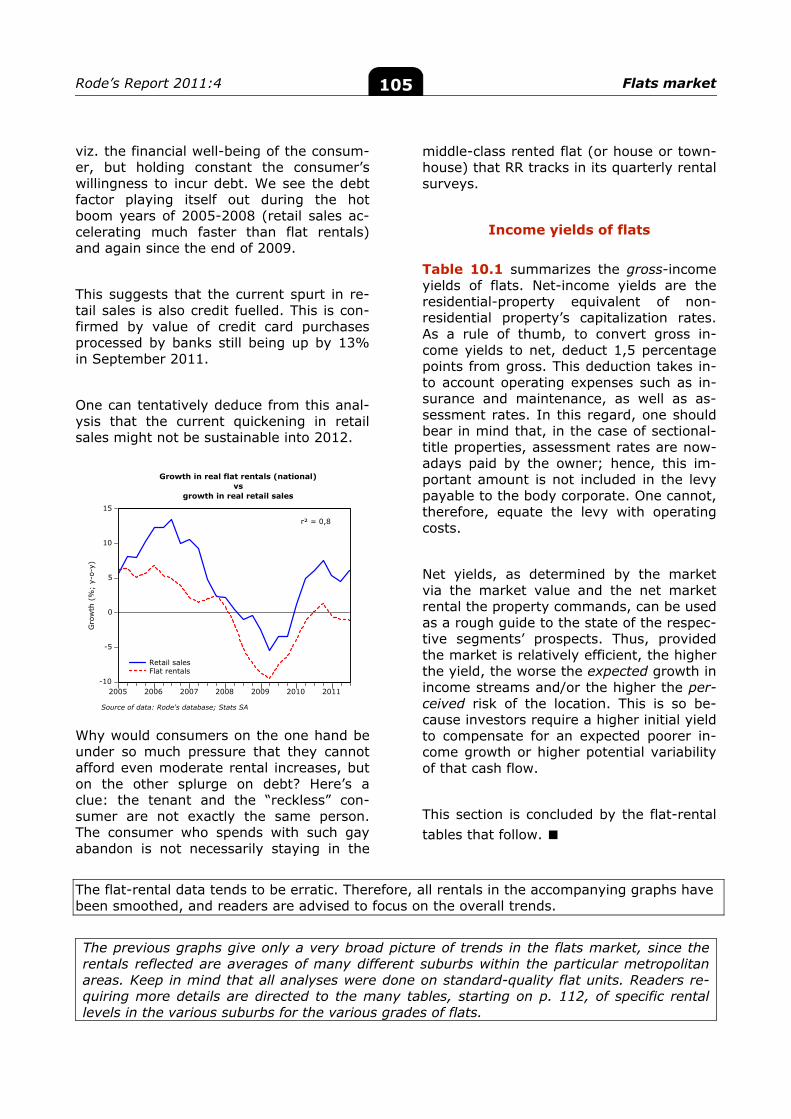

Johannesburg metro +1,5 -3,3

Pretoria metro +4,8 -0,2

Durban metro +1,5 -3,3

Cape Town metro +4,2 -0,8

Port Elizabeth +3,0 -1,9 * Unless otherwise specified

** Nominal values deflated by BER Building Cost Index; however, flat rentals are deflated using the Consumer Price Index.

Rode’s Report 2011:4 State of the property market

3

able growth of about 11% in the first quar-

ter. Meanwhile, building-cost inflation (the

cost to construct buildings, as measured by

the BER Building Cost Index) is again

growing and is clocking about 6%. This im-

plies that, in real terms, office rentals have

actually contracted. Thus, we see the busi-

ness-cycle slowdown is already a strong

depressing force on the upswing phase of the long office cycle.

The acceleration in building-cost inflation

can be explained by building contractors

having now milked their profit margins dry.

Therefore, they now have no option but to

pass on higher input costs in the form of

higher tender prices. This comes after in-

tensive tendering competition over the past

two years has forced contractors to cut

their profit margins to the bone. The result

of this was weaker growth in overall tender

prices — which includes profit margins —

relative to the growth in building-input costs (as measured by the Haylett Index).

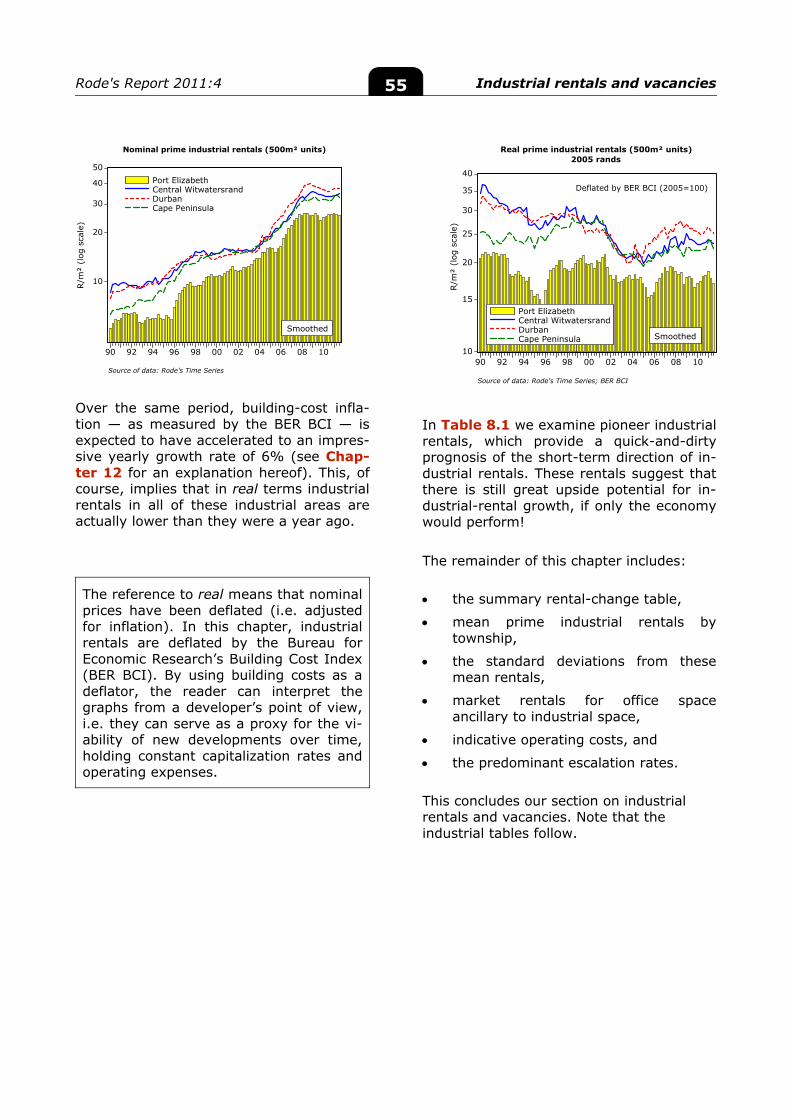

Industrial market

Slack in the demand for industrial space is

currently displayed by the poor to moder-

ate growth in market rentals. In the third

quarter of 2011, market rentals on the

Central Witwatersrand and in Durban mus-

tered growth of 5% − the best regional

performance. The Cape Peninsula followed

with growth of 4%, while in Port Elizabeth

market rentals were actually somewhat

lower (-1%) than they were a year ago.

Bearing in mind the fact that building costs

grew by 6% (y-o-y), this implies that in

real terms industrial rentals in all of these

industrial areas are actually lower than

they were a year ago.

Prospects for industrial rentals remain

weak, this as a result of an economy

struggling to find its feet amidst uncertain

global economic conditions – not to men-

tion the adverse impact that the current

slowdown in manufacturing output is likely

to have on the demand for industrial prop-erty.

Flat rentals

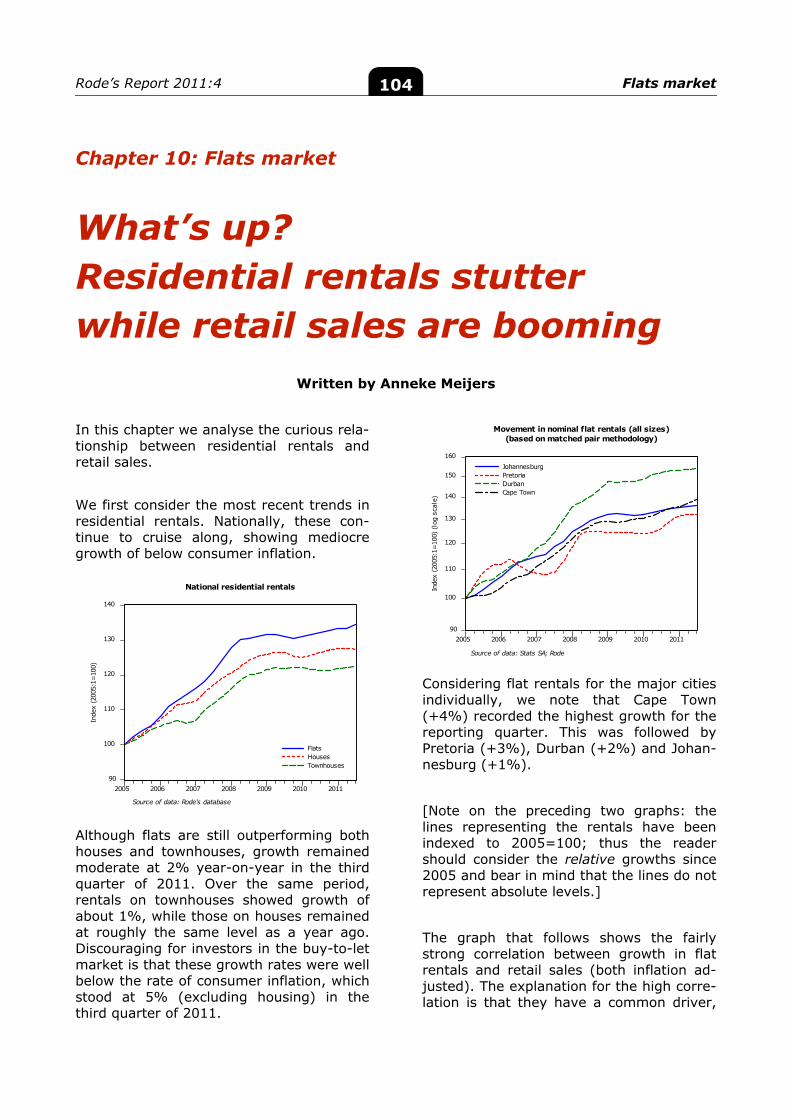

Residential rentals continue to cruise along,

showing mediocre growth below that of consumer inflation.

Although flats are still outperforming both

houses and townhouses, growth remained

moderate at 2% year-on-year in the third

quarter of 2011. Over the same period,

rentals on townhouses showed growth of

about 1%, while those on houses remained

at roughly the same level as a year ago.

Discouraging for investors in the buy-to-let

market is that these growth rates were well

below the rate of consumer inflation, which

stood at 5% (excluding housing) in the third quarter of 2011.

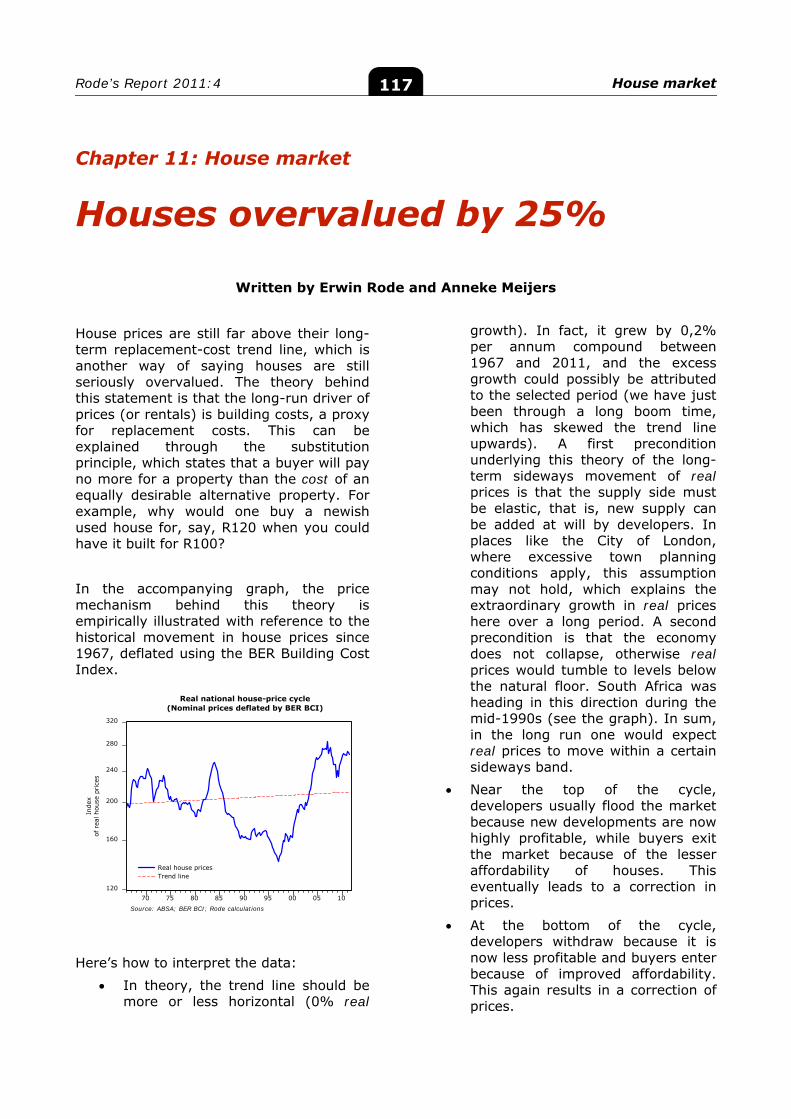

The house market

For now, no vigorous growth in house pric-

es can be expected until the magnitudes of

the key drivers of demand change signifi-

cantly. One such driver is, of course, inter-

est rates.

In the meantime, house prices remain far

above their long-term replacement-cost

trend line. In fact, houses are still 25%

more expensive than what is suggested by

their long-term trend line. Considering that

asset prices are mean-reverting, the impli-

cation is that a resumption in the down

trend in real houses prices is inevitable –

it’s only a question of time and speed. A

real decline in house prices does not neces-

sarily mean the nominal prices will decline;

a more likely outcome is that nominal pric-

es might grow at, say, 2% per annum for a

few years while inflation is at, say, 6%. �

Rode’s Report 2011:4 Standard capitalization rates 4

9

10

11

12

13

14

80

100

120

140

160

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Capitalization rates (smoothed)Business cycle indicator

Industrial leaseback capitalization ratesvs

Coincident business cycle indicator

r = -0,8

Cap

italiz

atio

n ra

tes

(%) B

usiness cycle indicator(2000=

100)

Source of data: Rode's Time Series; SARB

7

8

9

10

11

12

13

80

100

120

140

160

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Capitalization rates (smoothed)Business cycle indicator

Regional-shopping-centre capitalization ratesvs

Coincident business cycle indicator

r = -0,8

Cap

italiz

atio

n ra

tes

(%) B

usiness cycle indicator(2000=

100)

Source of data: Rode's Time Series; SARB

Chapter 2: Capitalization rates

Investment demand at risk of being dampened further

Written by John S. Lottering

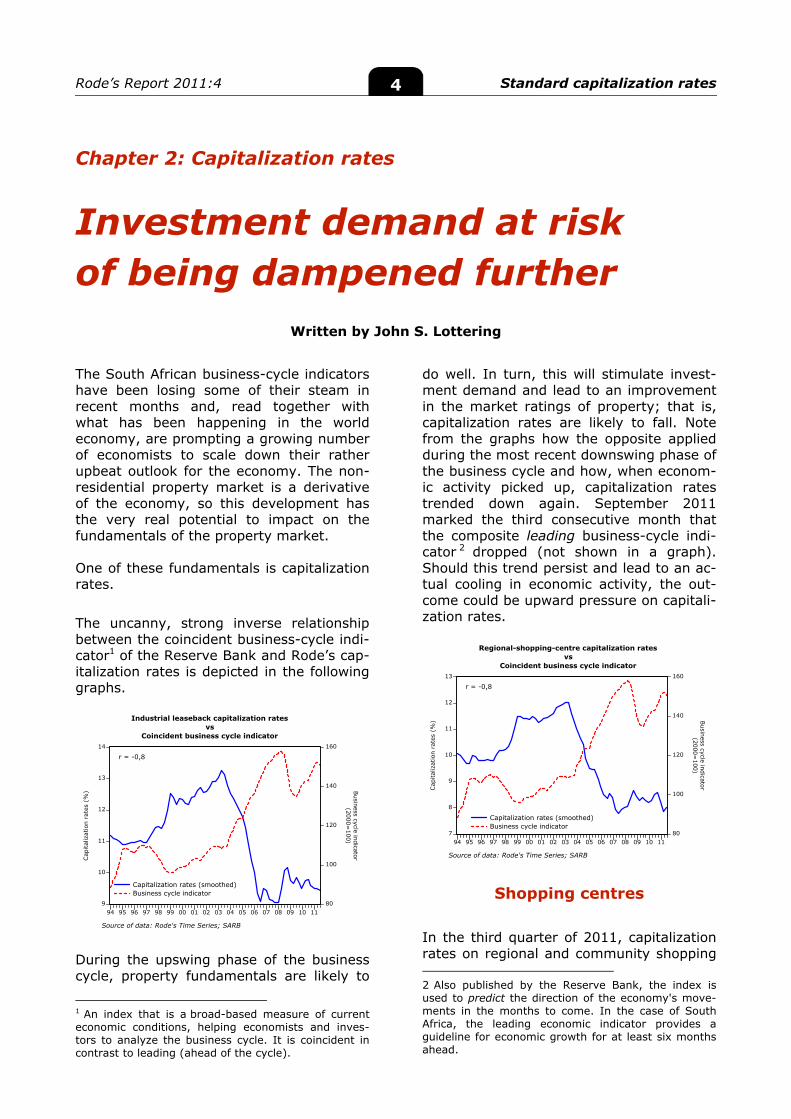

The South African business-cycle indicators have been losing some of their steam in recent months and, read together with what has been happening in the world economy, are prompting a growing number of economists to scale down their rather upbeat outlook for the economy. The non-residential property market is a derivative of the economy, so this development has the very real potential to impact on the fundamentals of the property market. One of these fundamentals is capitalization rates.

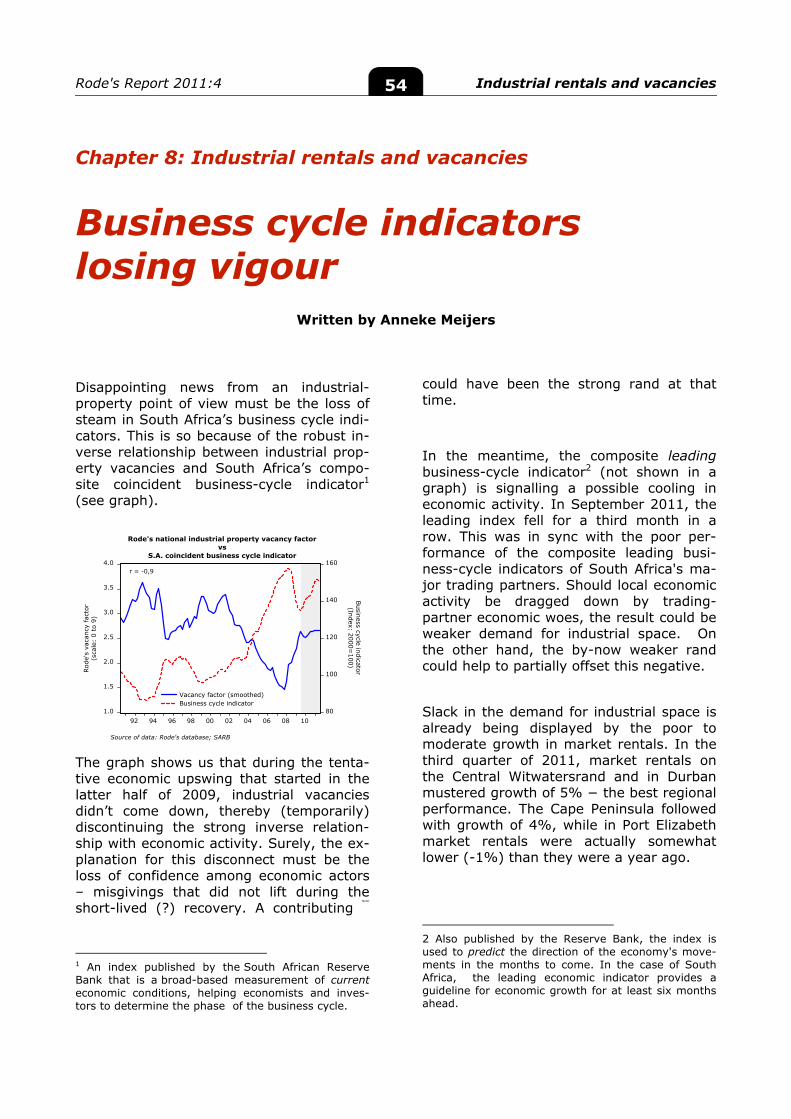

The uncanny, strong inverse relationship between the coincident business-cycle indi-cator1 of the Reserve Bank and Rode’s cap-italization rates is depicted in the following graphs.

During the upswing phase of the business cycle, property fundamentals are likely to

1 An index that is a broad-based measure of current economic conditions, helping economists and inves-tors to analyze the business cycle. It is coincident in contrast to leading (ahead of the cycle).

do well. In turn, this will stimulate invest-ment demand and lead to an improvement in the market ratings of property; that is, capitalization rates are likely to fall. Note from the graphs how the opposite applied during the most recent downswing phase of the business cycle and how, when econom-ic activity picked up, capitalization rates trended down again. September 2011 marked the third consecutive month that the composite leading business-cycle indi-cator 2 dropped (not shown in a graph). Should this trend persist and lead to an ac-tual cooling in economic activity, the out-come could be upward pressure on capitali-zation rates.

Shopping centres

In the third quarter of 2011, capitalization rates on regional and community shopping 2 Also published by the Reserve Bank, the index is used to predict the direction of the economy's move-ments in the months to come. In the case of South Africa, the leading economic indicator provides a guideline for economic growth for at least six months ahead.

Rode’s Report 2011:4 Standard capitalization rates 5

7

8

9

10

11

12

13

90 92 94 96 98 00 02 04 06 08 10

PretoriaCape PeninsulaCentral WitwatersrandDurban

Capitalization ratesRegional shopping centres

%

Source of data: Rode's Time Series

Smoothed

8

9

10

11

12

13

14

15

90 92 94 96 98 00 02 04 06 08 10

Cape PeninsulaCentral WitwatersrandPretoriaDurban

Capitalization ratesCommunity shopping centres

%

Source of data: Rode's Time Series

Smoothed

8

9

10

11

12

13

14

90 92 94 96 98 00 02 04 06 08 10

Cape PeninsulaDurbanPretoriaCentral Witwatersrand

Capitalization ratesPrime industrial leasebacks

%

Source of data: Rode's Time Series

Smoothed

8

10

12

14

16

90 92 94 96 98 00 02 04 06 08 10

Sandton CBDParktownRosebankMidrand

Capitalization ratesPrime Johannesburg decentralized offices

%

Source of data: Rode's Time Series

Smoothed

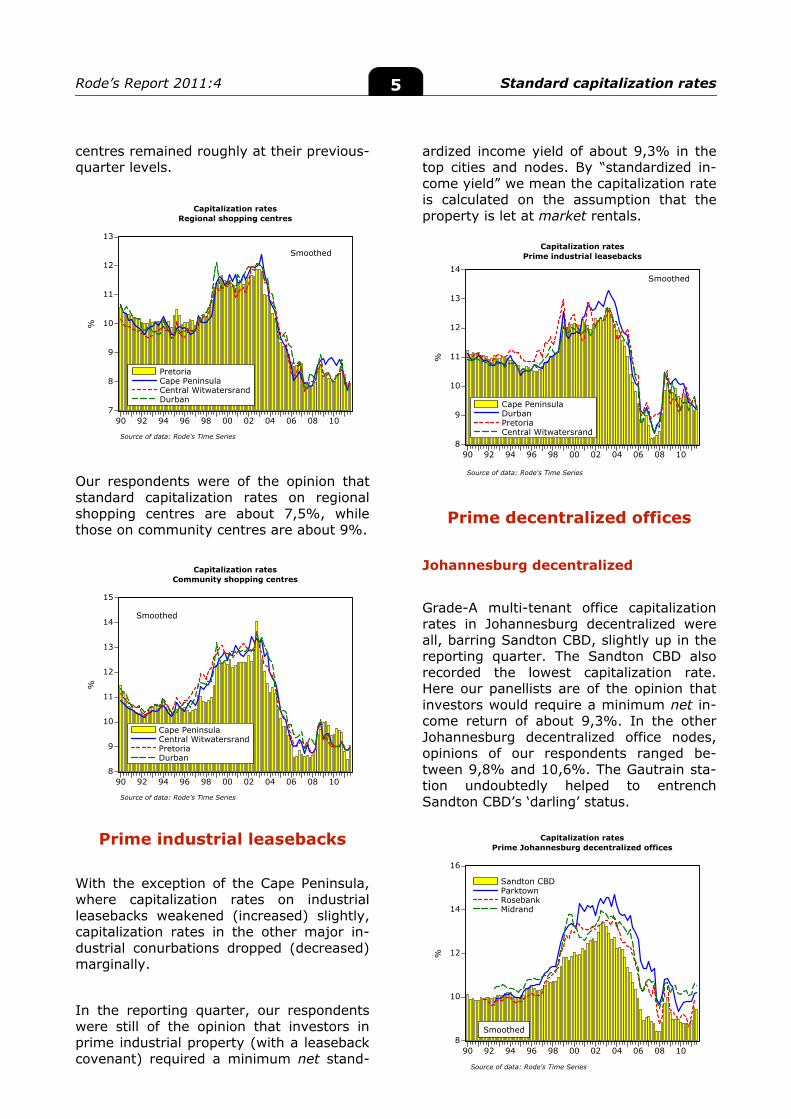

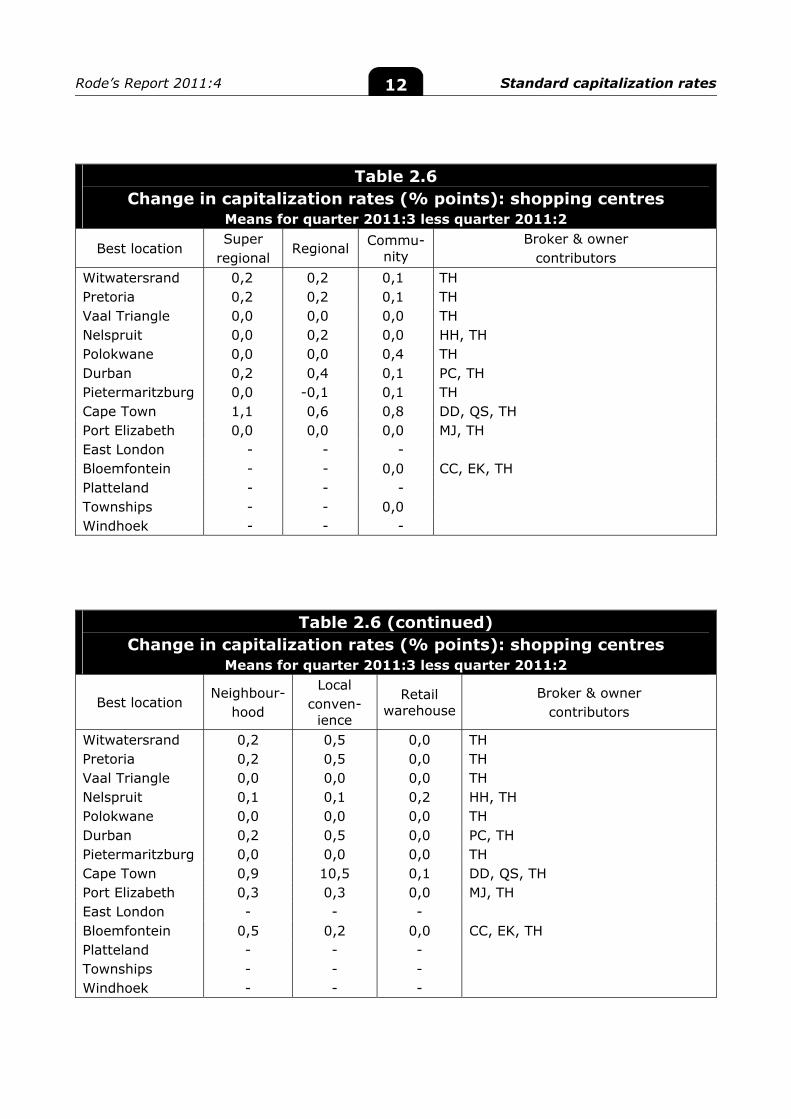

centres remained roughly at their previous-quarter levels. Our respondents were of the opinion that standard capitalization rates on regional shopping centres are about 7,5%, while those on community centres are about 9%.

Prime industrial leasebacks

With the exception of the Cape Peninsula, where capitalization rates on industrial leasebacks weakened (increased) slightly, capitalization rates in the other major in-dustrial conurbations dropped (decreased) marginally.

In the reporting quarter, our respondents were still of the opinion that investors in prime industrial property (with a leaseback covenant) required a minimum net stand-

ardized income yield of about 9,3% in the top cities and nodes. By “standardized in-come yield” we mean the capitalization rate is calculated on the assumption that the property is let at market rentals.

Prime decentralized offices

Johannesburg decentralized

Grade-A multi-tenant office capitalization rates in Johannesburg decentralized were all, barring Sandton CBD, slightly up in the reporting quarter. The Sandton CBD also recorded the lowest capitalization rate. Here our panellists are of the opinion that investors would require a minimum net in-come return of about 9,3%. In the other Johannesburg decentralized office nodes, opinions of our respondents ranged be-tween 9,8% and 10,6%. The Gautrain sta-tion undoubtedly helped to entrench Sandton CBD’s ‘darling’ status.

Rode’s Report 2011:4 Standard capitalization rates 6

9

10

11

12

13

14

15

98 99 00 01 02 03 04 05 06 07 08 09 10 11

BryanstonRivoniaSunninghillRandburg

Capitalization ratesPrime Johannesburg decentralized offices

%

Source of data: Rode's Time Series

Smoothed

8

9

10

11

12

13

14

15

96 98 00 02 04 06 08 10

BrooklynHatfieldCenturionMidrand

Capitalization ratesPrime Pretoria decentralized offices

%

Source of data: Rode's Time Series

Smoothed

8

9

10

11

12

13

14

15

99 00 01 02 03 04 05 06 07 08 09 10 11

Umhlanga RidgeWestwayEssex TerraceBerea

Capitalization ratesPrime Durban decentralized offices

%

Source of data: Rode's Time Series

Smoothed

8

10

12

14

16

94 96 98 00 02 04 06 08 10

Century CityTyger ValleyCape Town CBD

Capitalization ratesPrime Cape Town offices

%

Source of data: Rode's Time Series

Smoothed

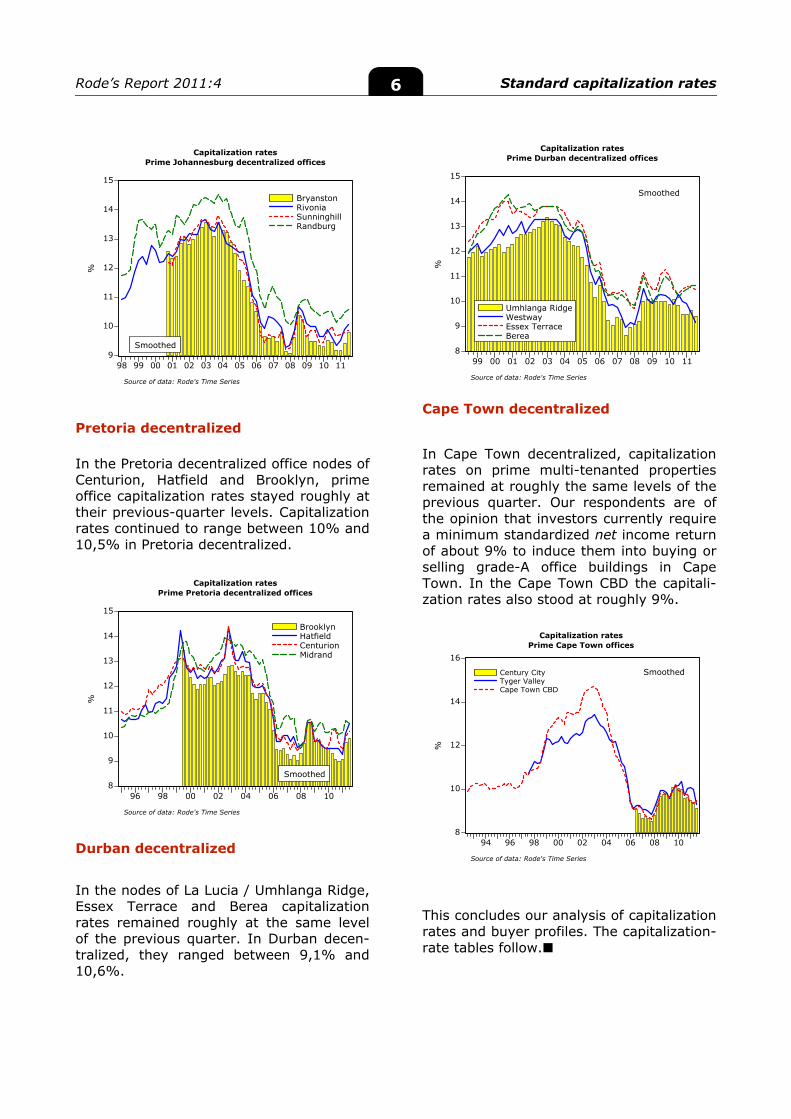

Pretoria decentralized In the Pretoria decentralized office nodes of Centurion, Hatfield and Brooklyn, prime office capitalization rates stayed roughly at their previous-quarter levels. Capitalization rates continued to range between 10% and 10,5% in Pretoria decentralized.

Durban decentralized

In the nodes of La Lucia / Umhlanga Ridge, Essex Terrace and Berea capitalization rates remained roughly at the same level of the previous quarter. In Durban decen-tralized, they ranged between 9,1% and 10,6%.

Cape Town decentralized

In Cape Town decentralized, capitalization rates on prime multi-tenanted properties remained at roughly the same levels of the previous quarter. Our respondents are of the opinion that investors currently require a minimum standardized net income return of about 9% to induce them into buying or selling grade-A office buildings in Cape Town. In the Cape Town CBD the capitali-zation rates also stood at roughly 9%.

This concludes our analysis of capitalization rates and buyer profiles. The capitalization-rate tables follow.

Rode’s Report 2011:4 Standard capitalization rates 7

Please note that figures referred to in the text may differ from the raw data in the tables owing to smoothing on our part.

Interpretation tip: It is dangerous to rely on one quarter’s figure, as it may be an outlier owing to small sample sizes. Instead, consider the trend or contemplate using the average of at least two quarters for a more accurate assessment. For this reason, the graphs accompanying this arti-cle are smoothed.

A standard capitalization rate (colloquially referred to as a cap rate) is the expected net oper-ating income for year 1, assuming the entire building is let at open-market rentals, divided by the purchase price. This calculation ignores VAT, transfer duty and income tax, and it assumes a cash transaction. All references in Rode’s Report to “cap rates” and “capitalization rates” mean “stand-ard capitalization rates”.

Capitalization rates for CBDs (excluding the Cape Town CBD) are of little use because when office properties are sold they are invariably converted to flats.

The high standard deviation from the mean capitalization rate for office and industrial properties in some nodes, as reported in the accompanying capitalization rate tables, is in-dicative of the uncertainty prevailing in these nodes or areas. With few sales taking place, the evidence on ruling capitalization rates is thin and opinions vary more than in the more popular areas. This means that the income-producing property market has become even more inefficient in these nodes — which makes the valuation of these properties a rather hazardous exercise.

We are indebted to our expert capitalization rate panel, comprising major owners and leading brokers who know their market segments intimately. This survey would not be possible without their invaluable contributions. Codes of those panellists who supplied information for this quarter's survey appear in the tables on the following pages. An explanation of the contributor codes can be found on p. xvi.

Rode’s Report 2011:4 Standard capitalization rates 8

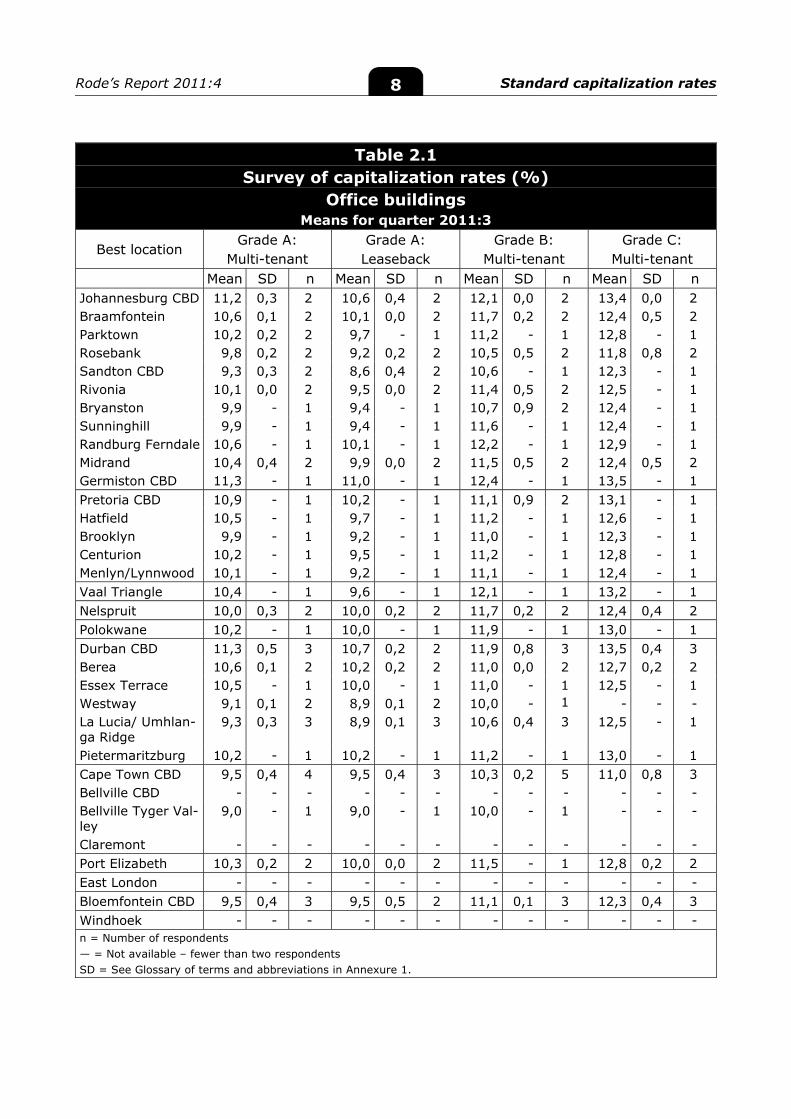

Table 2.1 Survey of capitalization rates (%)

Office buildings Means for quarter 2011:3

Best location Grade A:

Multi-tenant Grade A: Leaseback

Grade B: Multi-tenant

Grade C: Multi-tenant

Mean SD n Mean SD n Mean SD n Mean SD n Johannesburg CBD 11,2 0,3 2 10,6 0,4 2 12,1 0,0 2 13,4 0,0 2 Braamfontein 10,6 0,1 2 10,1 0,0 2 11,7 0,2 2 12,4 0,5 2 Parktown 10,2 0,2 2 9,7 - 1 11,2 - 1 12,8 - 1 Rosebank 9,8 0,2 2 9,2 0,2 2 10,5 0,5 2 11,8 0,8 2 Sandton CBD 9,3 0,3 2 8,6 0,4 2 10,6 - 1 12,3 - 1 Rivonia 10,1 0,0 2 9,5 0,0 2 11,4 0,5 2 12,5 - 1 Bryanston 9,9 - 1 9,4 - 1 10,7 0,9 2 12,4 - 1 Sunninghill 9,9 - 1 9,4 - 1 11,6 - 1 12,4 - 1 Randburg Ferndale 10,6 - 1 10,1 - 1 12,2 - 1 12,9 - 1 Midrand 10,4 0,4 2 9,9 0,0 2 11,5 0,5 2 12,4 0,5 2 Germiston CBD 11,3 - 1 11,0 - 1 12,4 - 1 13,5 - 1 Pretoria CBD 10,9 - 1 10,2 - 1 11,1 0,9 2 13,1 - 1 Hatfield 10,5 - 1 9,7 - 1 11,2 - 1 12,6 - 1 Brooklyn 9,9 - 1 9,2 - 1 11,0 - 1 12,3 - 1 Centurion 10,2 - 1 9,5 - 1 11,2 - 1 12,8 - 1 Menlyn/Lynnwood 10,1 - 1 9,2 - 1 11,1 - 1 12,4 - 1 Vaal Triangle 10,4 - 1 9,6 - 1 12,1 - 1 13,2 - 1 Nelspruit 10,0 0,3 2 10,0 0,2 2 11,7 0,2 2 12,4 0,4 2 Polokwane 10,2 - 1 10,0 - 1 11,9 - 1 13,0 - 1 Durban CBD 11,3 0,5 3 10,7 0,2 2 11,9 0,8 3 13,5 0,4 3 Berea 10,6 0,1 2 10,2 0,2 2 11,0 0,0 2 12,7 0,2 2 Essex Terrace 10,5 - 1 10,0 - 1 11,0 - 1 12,5 - 1 Westway 9,1 0,1 2 8,9 0,1 2 10,0 - 1 - - - La Lucia/ Umhlan-ga Ridge

9,3 0,3 3 8,9 0,1 3 10,6 0,4 3 12,5 - 1

Pietermaritzburg 10,2 - 1 10,2 - 1 11,2 - 1 13,0 - 1 Cape Town CBD 9,5 0,4 4 9,5 0,4 3 10,3 0,2 5 11,0 0,8 3 Bellville CBD - - - - - - - - - - - - Bellville Tyger Val-ley

9,0 - 1 9,0 - 1 10,0 - 1 - - -

Claremont - - - - - - - - - - - - Port Elizabeth 10,3 0,2 2 10,0 0,0 2 11,5 - 1 12,8 0,2 2 East London - - - - - - - - - - - - Bloemfontein CBD 9,5 0,4 3 9,5 0,5 2 11,1 0,1 3 12,3 0,4 3 Windhoek - - - - - - - - - - - - n = Number of respondents — = Not available – fewer than two respondents SD = See Glossary of terms and abbreviations in Annexure 1.

Rode’s Report 2011:4 Standard capitalization rates 9

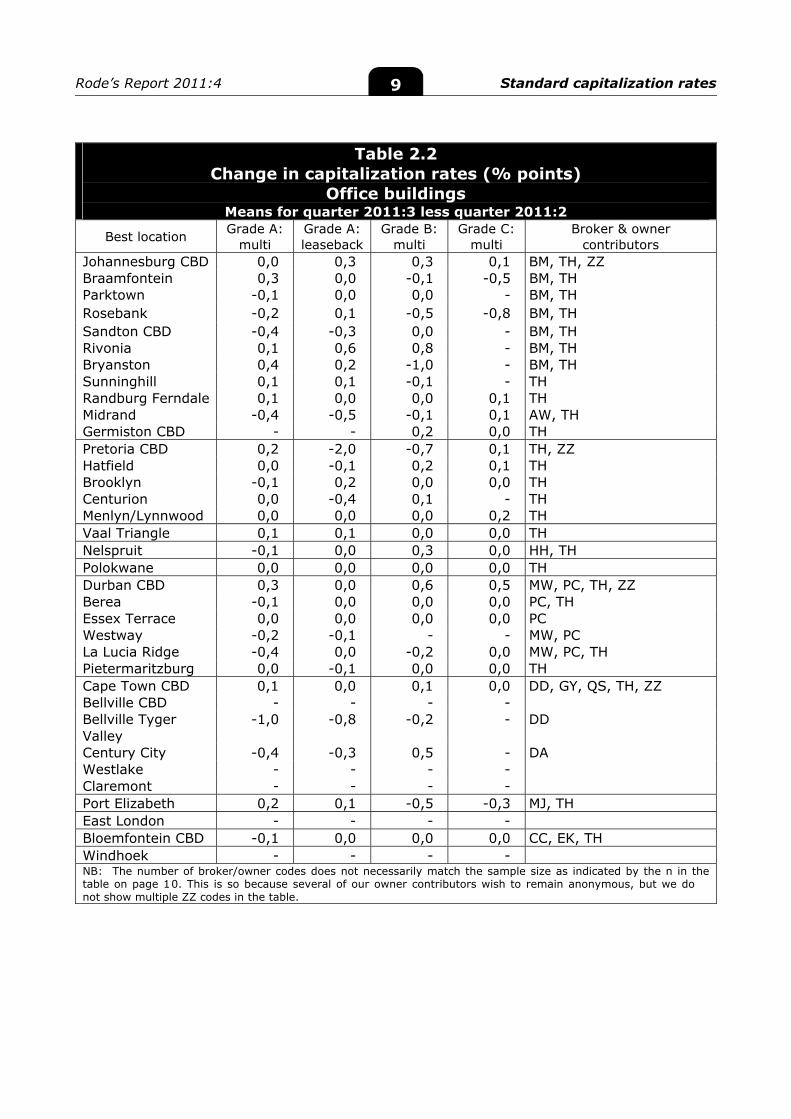

Table 2.2 Change in capitalization rates (% points)

Office buildings Means for quarter 2011:3 less quarter 2011:2

Best location Grade A: multi

Grade A: leaseback

Grade B: multi

Grade C: multi

Broker & owner contributors

Johannesburg CBD 0,0 0,3 0,3 0,1 BM, TH, ZZ Braamfontein 0,3 0,0 -0,1 -0,5 BM, TH Parktown -0,1 0,0 0,0 - BM, TH Rosebank -0,2 0,1 -0,5 -0,8 BM, TH Sandton CBD -0,4 -0,3 0,0 - BM, TH Rivonia 0,1 0,6 0,8 - BM, TH Bryanston 0,4 0,2 -1,0 - BM, TH Sunninghill 0,1 0,1 -0,1 - TH Randburg Ferndale 0,1 0,0 0,0 0,1 TH Midrand -0,4 -0,5 -0,1 0,1 AW, TH Germiston CBD - - 0,2 0,0 TH Pretoria CBD 0,2 -2,0 -0,7 0,1 TH, ZZ Hatfield 0,0 -0,1 0,2 0,1 TH Brooklyn -0,1 0,2 0,0 0,0 TH Centurion 0,0 -0,4 0,1 - TH Menlyn/Lynnwood 0,0 0,0 0,0 0,2 TH Vaal Triangle 0,1 0,1 0,0 0,0 TH Nelspruit -0,1 0,0 0,3 0,0 HH, TH Polokwane 0,0 0,0 0,0 0,0 TH Durban CBD 0,3 0,0 0,6 0,5 MW, PC, TH, ZZ Berea -0,1 0,0 0,0 0,0 PC, TH Essex Terrace 0,0 0,0 0,0 0,0 PC Westway -0,2 -0,1 - - MW, PC La Lucia Ridge -0,4 0,0 -0,2 0,0 MW, PC, TH Pietermaritzburg 0,0 -0,1 0,0 0,0 TH Cape Town CBD 0,1 0,0 0,1 0,0 DD, GY, QS, TH, ZZ Bellville CBD - - - - Bellville Tyger Valley

-1,0 -0,8 -0,2 - DD

Century City -0,4 -0,3 0,5 - DA Westlake - - - - Claremont - - - - Port Elizabeth 0,2 0,1 -0,5 -0,3 MJ, TH East London - - - - Bloemfontein CBD -0,1 0,0 0,0 0,0 CC, EK, TH Windhoek - - - - NB: The number of broker/owner codes does not necessarily match the sample size as indicated by the n in the table on page 10. This is so because several of our owner contributors wish to remain anonymous, but we do not show multiple ZZ codes in the table.

Rode’s Report 2011:4 Standard capitalization rates 10

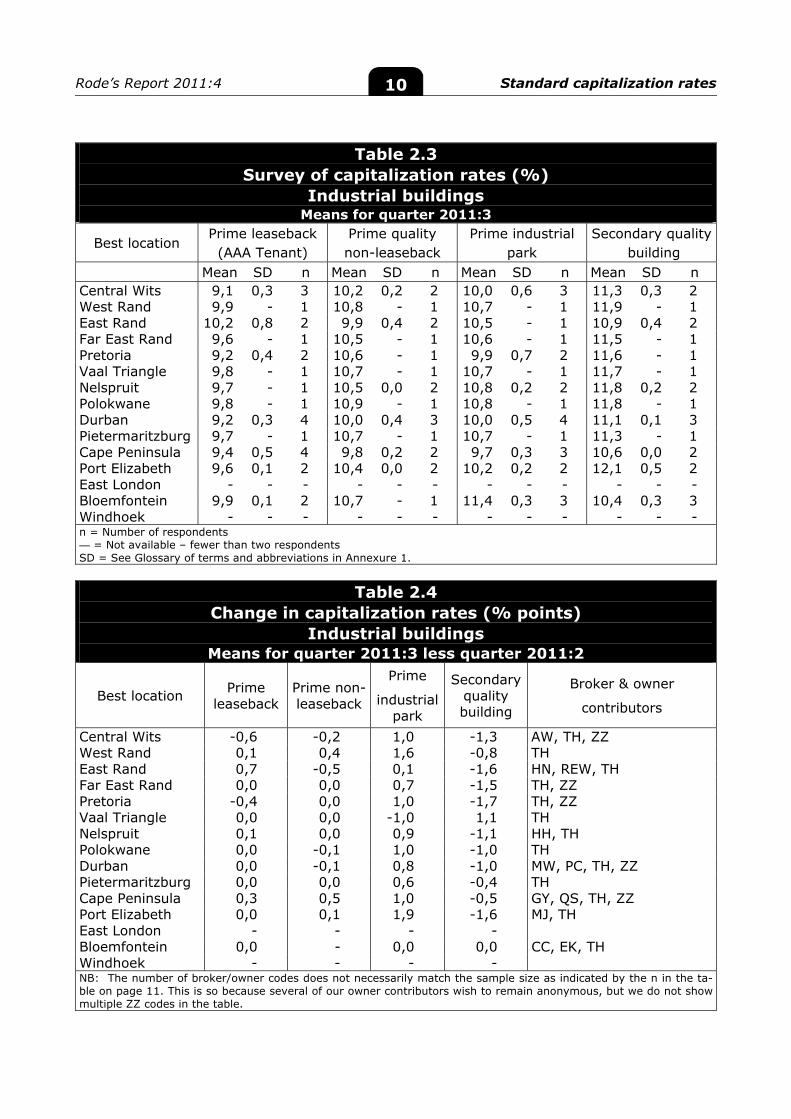

Table 2.3 Survey of capitalization rates (%)

Industrial buildings Means for quarter 2011:3

Best location Prime leaseback (AAA Tenant)

Prime quality non-leaseback

Prime industrial park

Secondary quality building

Mean SD n Mean SD n Mean SD n Mean SD n Central Wits 9,1 0,3 3 10,2 0,2 2 10,0 0,6 3 11,3 0,3 2 West Rand 9,9 - 1 10,8 - 1 10,7 - 1 11,9 - 1 East Rand 10,2 0,8 2 9,9 0,4 2 10,5 - 1 10,9 0,4 2 Far East Rand 9,6 - 1 10,5 - 1 10,6 - 1 11,5 - 1 Pretoria 9,2 0,4 2 10,6 - 1 9,9 0,7 2 11,6 - 1 Vaal Triangle 9,8 - 1 10,7 - 1 10,7 - 1 11,7 - 1 Nelspruit 9,7 - 1 10,5 0,0 2 10,8 0,2 2 11,8 0,2 2 Polokwane 9,8 - 1 10,9 - 1 10,8 - 1 11,8 - 1 Durban 9,2 0,3 4 10,0 0,4 3 10,0 0,5 4 11,1 0,1 3 Pietermaritzburg 9,7 - 1 10,7 - 1 10,7 - 1 11,3 - 1 Cape Peninsula 9,4 0,5 4 9,8 0,2 2 9,7 0,3 3 10,6 0,0 2 Port Elizabeth 9,6 0,1 2 10,4 0,0 2 10,2 0,2 2 12,1 0,5 2 East London - - - - - - - - - - - - Bloemfontein 9,9 0,1 2 10,7 - 1 11,4 0,3 3 10,4 0,3 3 Windhoek - - - - - - - - - - - - n = Number of respondents — = Not available – fewer than two respondents SD = See Glossary of terms and abbreviations in Annexure 1.

Table 2.4 Change in capitalization rates (% points)

Industrial buildings Means for quarter 2011:3 less quarter 2011:2

Best location Prime leaseback

Prime non-leaseback

Prime

industrial park

Secondary quality building

Broker & owner

contributors

Central Wits -0,6 -0,2 1,0 -1,3 AW, TH, ZZ West Rand 0,1 0,4 1,6 -0,8 TH East Rand 0,7 -0,5 0,1 -1,6 HN, REW, TH Far East Rand 0,0 0,0 0,7 -1,5 TH, ZZ Pretoria -0,4 0,0 1,0 -1,7 TH, ZZ Vaal Triangle 0,0 0,0 -1,0 1,1 TH Nelspruit 0,1 0,0 0,9 -1,1 HH, TH Polokwane 0,0 -0,1 1,0 -1,0 TH Durban 0,0 -0,1 0,8 -1,0 MW, PC, TH, ZZ Pietermaritzburg 0,0 0,0 0,6 -0,4 TH Cape Peninsula 0,3 0,5 1,0 -0,5 GY, QS, TH, ZZ Port Elizabeth 0,0 0,1 1,9 -1,6 MJ, TH East London - - - - Bloemfontein 0,0 - 0,0 0,0 CC, EK, TH Windhoek - - - - NB: The number of broker/owner codes does not necessarily match the sample size as indicated by the n in the ta-ble on page 11. This is so because several of our owner contributors wish to remain anonymous, but we do not show multiple ZZ codes in the table.

Rode’s Report 2011:4 Standard capitalization rates 11

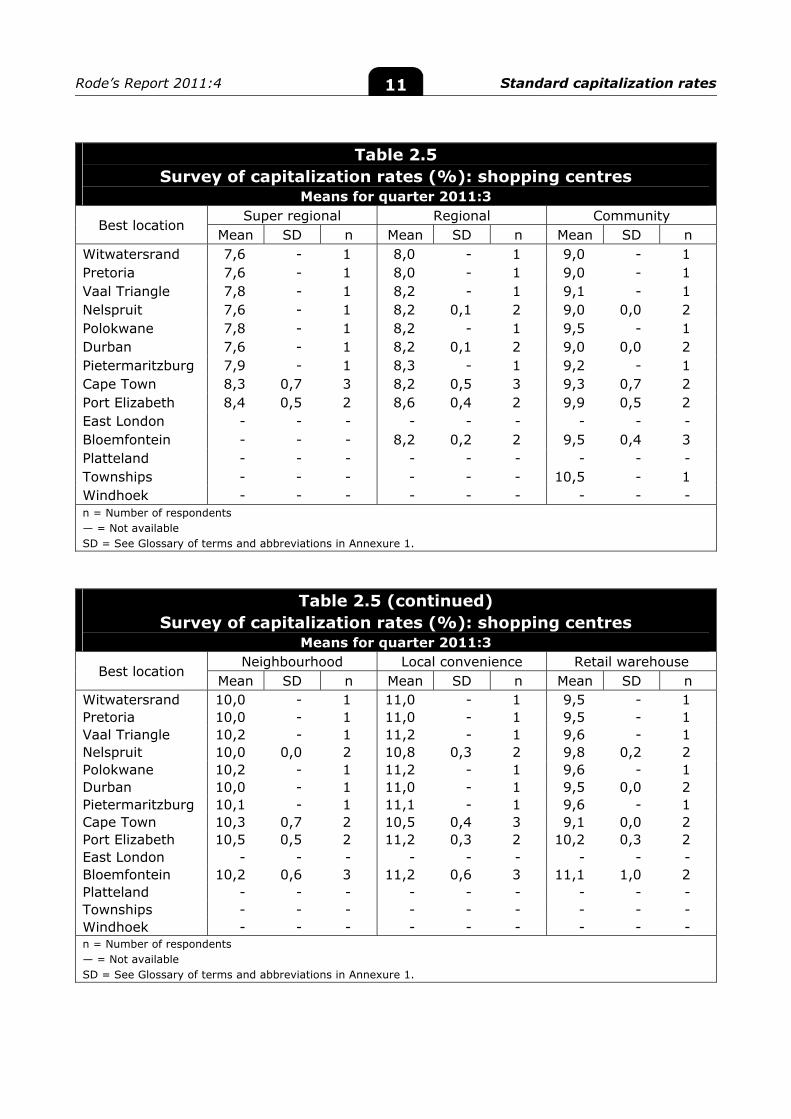

Table 2.5 Survey of capitalization rates (%): shopping centres

Means for quarter 2011:3

Best location Super regional Regional Community

Mean SD n Mean SD n Mean SD n Witwatersrand 7,6 - 1 8,0 - 1 9,0 - 1 Pretoria 7,6 - 1 8,0 - 1 9,0 - 1 Vaal Triangle 7,8 - 1 8,2 - 1 9,1 - 1 Nelspruit 7,6 - 1 8,2 0,1 2 9,0 0,0 2 Polokwane 7,8 - 1 8,2 - 1 9,5 - 1 Durban 7,6 - 1 8,2 0,1 2 9,0 0,0 2 Pietermaritzburg 7,9 - 1 8,3 - 1 9,2 - 1 Cape Town 8,3 0,7 3 8,2 0,5 3 9,3 0,7 2 Port Elizabeth 8,4 0,5 2 8,6 0,4 2 9,9 0,5 2 East London - - - - - - - - - Bloemfontein - - - 8,2 0,2 2 9,5 0,4 3 Platteland - - - - - - - - - Townships - - - - - - 10,5 - 1 Windhoek - - - - - - - - - n = Number of respondents — = Not available SD = See Glossary of terms and abbreviations in Annexure 1.

Table 2.5 (continued) Survey of capitalization rates (%): shopping centres

Means for quarter 2011:3

Best location Neighbourhood Local convenience Retail warehouse

Mean SD n Mean SD n Mean SD n Witwatersrand 10,0 - 1 11,0 - 1 9,5 - 1 Pretoria 10,0 - 1 11,0 - 1 9,5 - 1 Vaal Triangle 10,2 - 1 11,2 - 1 9,6 - 1 Nelspruit 10,0 0,0 2 10,8 0,3 2 9,8 0,2 2 Polokwane 10,2 - 1 11,2 - 1 9,6 - 1 Durban 10,0 - 1 11,0 - 1 9,5 0,0 2 Pietermaritzburg 10,1 - 1 11,1 - 1 9,6 - 1 Cape Town 10,3 0,7 2 10,5 0,4 3 9,1 0,0 2 Port Elizabeth 10,5 0,5 2 11,2 0,3 2 10,2 0,3 2 East London - - - - - - - - - Bloemfontein 10,2 0,6 3 11,2 0,6 3 11,1 1,0 2 Platteland - - - - - - - - - Townships - - - - - - - - - Windhoek - - - - - - - - - n = Number of respondents — = Not available SD = See Glossary of terms and abbreviations in Annexure 1.

Rode’s Report 2011:4 Standard capitalization rates 12

Table 2.6 Change in capitalization rates (% points): shopping centres

Means for quarter 2011:3 less quarter 2011:2

Best location Super

regional Regional Commu-

nity Broker & owner

contributors Witwatersrand 0,2 0,2 0,1 TH Pretoria 0,2 0,2 0,1 TH Vaal Triangle 0,0 0,0 0,0 TH Nelspruit 0,0 0,2 0,0 HH, TH Polokwane 0,0 0,0 0,4 TH Durban 0,2 0,4 0,1 PC, TH Pietermaritzburg 0,0 -0,1 0,1 TH Cape Town 1,1 0,6 0,8 DD, QS, TH Port Elizabeth 0,0 0,0 0,0 MJ, TH East London - - - Bloemfontein - - 0,0 CC, EK, TH Platteland - - - Townships - - 0,0 Windhoek - - -

Table 2.6 (continued) Change in capitalization rates (% points): shopping centres

Means for quarter 2011:3 less quarter 2011:2

Best location Neighbour-

hood

Local conven-

ience

Retail warehouse

Broker & owner contributors

Witwatersrand 0,2 0,5 0,0 TH Pretoria 0,2 0,5 0,0 TH Vaal Triangle 0,0 0,0 0,0 TH Nelspruit 0,1 0,1 0,2 HH, TH Polokwane 0,0 0,0 0,0 TH Durban 0,2 0,5 0,0 PC, TH Pietermaritzburg 0,0 0,0 0,0 TH Cape Town 0,9 10,5 0,1 DD, QS, TH Port Elizabeth 0,3 0,3 0,0 MJ, TH East London - - - Bloemfontein 0,5 0,2 0,0 CC, EK, TH Platteland - - - Townships - - - Windhoek - - -

Rode’s Report 2011:4 Standard capitalization rates 13

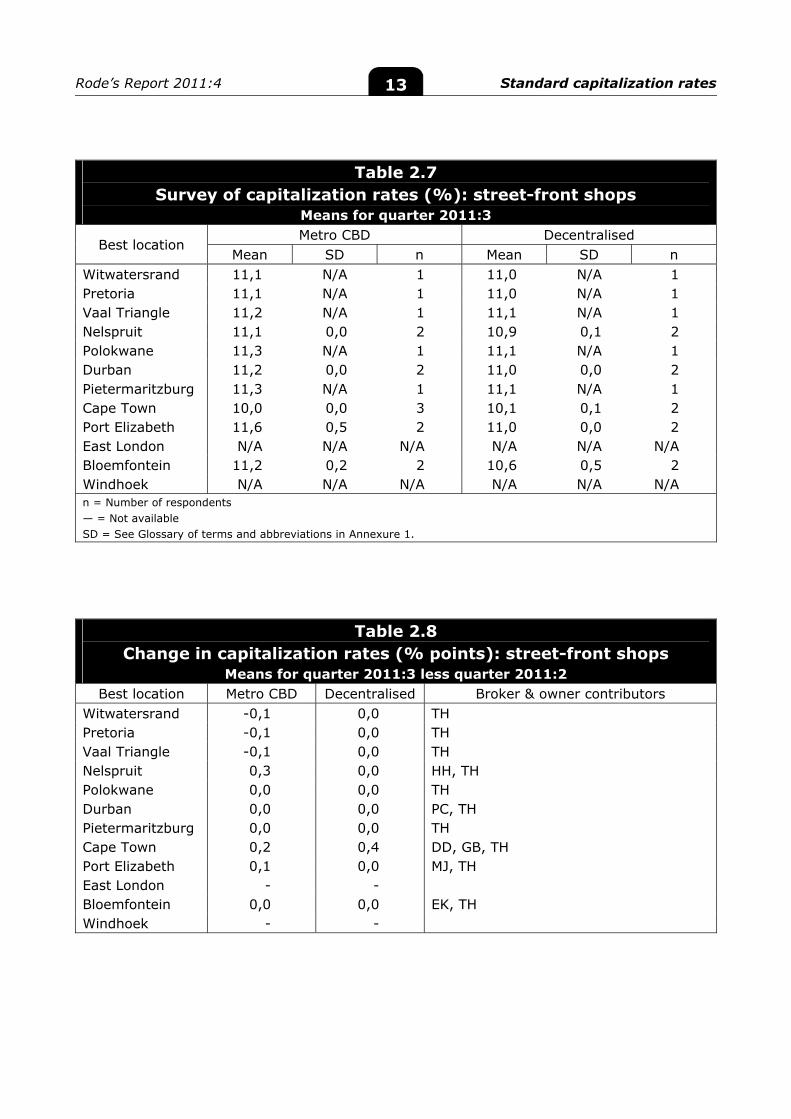

Table 2.7

Survey of capitalization rates (%): street-front shops Means for quarter 2011:3

Best location Metro CBD Decentralised

Mean SD n Mean SD n Witwatersrand 11,1 N/A 1 11,0 N/A 1 Pretoria 11,1 N/A 1 11,0 N/A 1 Vaal Triangle 11,2 N/A 1 11,1 N/A 1 Nelspruit 11,1 0,0 2 10,9 0,1 2 Polokwane 11,3 N/A 1 11,1 N/A 1 Durban 11,2 0,0 2 11,0 0,0 2 Pietermaritzburg 11,3 N/A 1 11,1 N/A 1 Cape Town 10,0 0,0 3 10,1 0,1 2 Port Elizabeth 11,6 0,5 2 11,0 0,0 2 East London N/A N/A N/A N/A N/A N/A Bloemfontein 11,2 0,2 2 10,6 0,5 2 Windhoek N/A N/A N/A N/A N/A N/A n = Number of respondents — = Not available SD = See Glossary of terms and abbreviations in Annexure 1.

Table 2.8 Change in capitalization rates (% points): street-front shops

Means for quarter 2011:3 less quarter 2011:2 Best location Metro CBD Decentralised Broker & owner contributors

Witwatersrand -0,1 0,0 TH Pretoria -0,1 0,0 TH Vaal Triangle -0,1 0,0 TH Nelspruit 0,3 0,0 HH, TH Polokwane 0,0 0,0 TH Durban 0,0 0,0 PC, TH Pietermaritzburg 0,0 0,0 TH Cape Town 0,2 0,4 DD, GB, TH Port Elizabeth 0,1 0,0 MJ, TH East London - - Bloemfontein 0,0 0,0 EK, TH Windhoek - -

Rode’s Report 2011:4 Capitalization rate equations 14

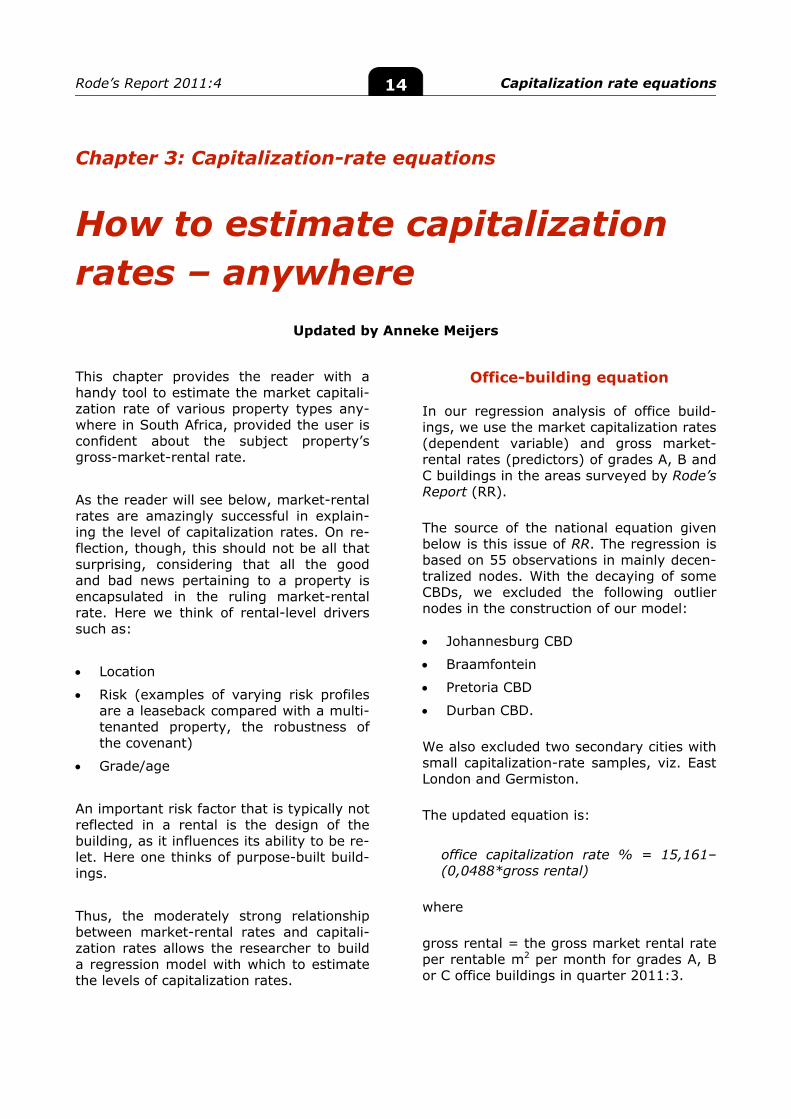

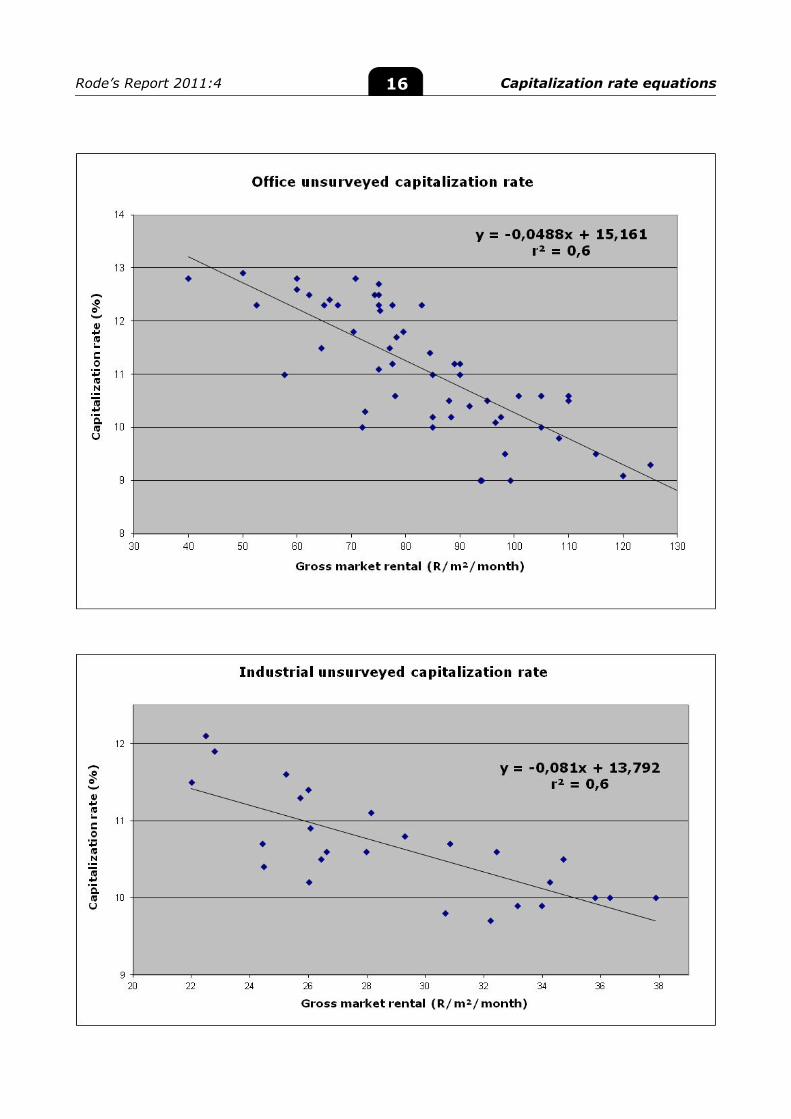

Chapter 3: Capitalization-rate equations

How to estimate capitalization rates – anywhere

Updated by Anneke Meijers

This chapter provides the reader with a handy tool to estimate the market capitali-zation rate of various property types any-where in South Africa, provided the user is confident about the subject property’s gross-market-rental rate.

As the reader will see below, market-rental rates are amazingly successful in explain-ing the level of capitalization rates. On re-flection, though, this should not be all that surprising, considering that all the good and bad news pertaining to a property is encapsulated in the ruling market-rental rate. Here we think of rental-level drivers such as:

Location

Risk (examples of varying risk profiles are a leaseback compared with a multi-tenanted property, the robustness of the covenant)

Grade/age

An important risk factor that is typically not reflected in a rental is the design of the building, as it influences its ability to be re-let. Here one thinks of purpose-built build-ings.

Thus, the moderately strong relationship between market-rental rates and capitali-zation rates allows the researcher to build a regression model with which to estimate the levels of capitalization rates.

Office-building equation

In our regression analysis of office build-ings, we use the market capitalization rates (dependent variable) and gross market-rental rates (predictors) of grades A, B and C buildings in the areas surveyed by Rode’s Report (RR).

The source of the national equation given below is this issue of RR. The regression is based on 55 observations in mainly decen-tralized nodes. With the decaying of some CBDs, we excluded the following outlier nodes in the construction of our model:

Johannesburg CBD

Braamfontein

Pretoria CBD

Durban CBD.

We also excluded two secondary cities with small capitalization-rate samples, viz. East London and Germiston.

The updated equation is:

office capitalization rate % = 15,161– (0,0488*gross rental)

where

gross rental = the gross market rental rate per rentable m2 per month for grades A, B or C office buildings in quarter 2011:3.

Rode’s Report 2011:4 Capitalization rate equations 15

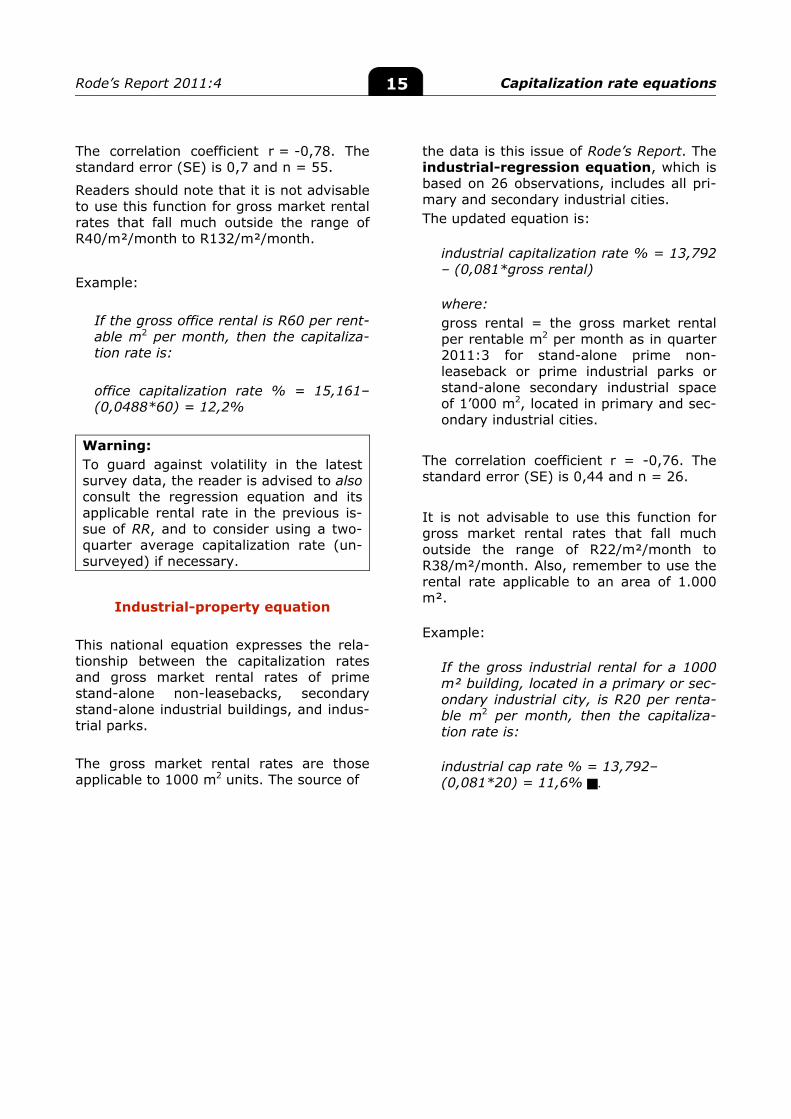

The correlation coefficient r = -0,78. The standard error (SE) is 0,7 and n = 55.

Readers should note that it is not advisable to use this function for gross market rental rates that fall much outside the range of R40/m²/month to R132/m²/month.

Example:

If the gross office rental is R60 per rent-able m2 per month, then the capitaliza-tion rate is: office capitalization rate % = 15,161– (0,0488*60) = 12,2%

Warning: To guard against volatility in the latest survey data, the reader is advised to also consult the regression equation and its applicable rental rate in the previous is-sue of RR, and to consider using a two-quarter average capitalization rate (un-surveyed) if necessary.

Industrial-property equation

This national equation expresses the rela-tionship between the capitalization rates and gross market rental rates of prime stand-alone non-leasebacks, secondary stand-alone industrial buildings, and indus-trial parks. The gross market rental rates are those applicable to 1000 m2 units. The source of

the data is this issue of Rode’s Report. The industrial-regression equation, which is based on 26 observations, includes all pri-mary and secondary industrial cities. The updated equation is:

industrial capitalization rate % = 13,792 – (0,081*gross rental)

where: gross rental = the gross market rental per rentable m2 per month as in quarter 2011:3 for stand-alone prime non-leaseback or prime industrial parks or stand-alone secondary industrial space of 1’000 m2, located in primary and sec-ondary industrial cities.

The correlation coefficient r = -0,76. The standard error (SE) is 0,44 and n = 26.

It is not advisable to use this function for gross market rental rates that fall much outside the range of R22/m²/month to R38/m²/month. Also, remember to use the rental rate applicable to an area of 1.000 m².

Example:

If the gross industrial rental for a 1000 m² building, located in a primary or sec-ondary industrial city, is R20 per renta-ble m2 per month, then the capitaliza-tion rate is:

industrial cap rate % = 13,792– (0,081*20) = 11,6% .

Rode’s Report 2011:4 Capitalization rate equations 16

Rode’s Report 2011:4 Listed property 17

-20

-10

0

10

20

30

04 05 06 07 08 09 10 11

Growth in income streams:PLS

% g

row

th (

y-o-

y)

Source of data: JSE

smoothed

5

6

7

8

9

10

11

05 06 07 08 09 10 11

BondsPLSs

Long-bond yieldsvs

PLS yields

Yiel

ds (

%)

Source of data: Rode's Time Series; Bond Exchange of SA

Chapter 4: Listed property

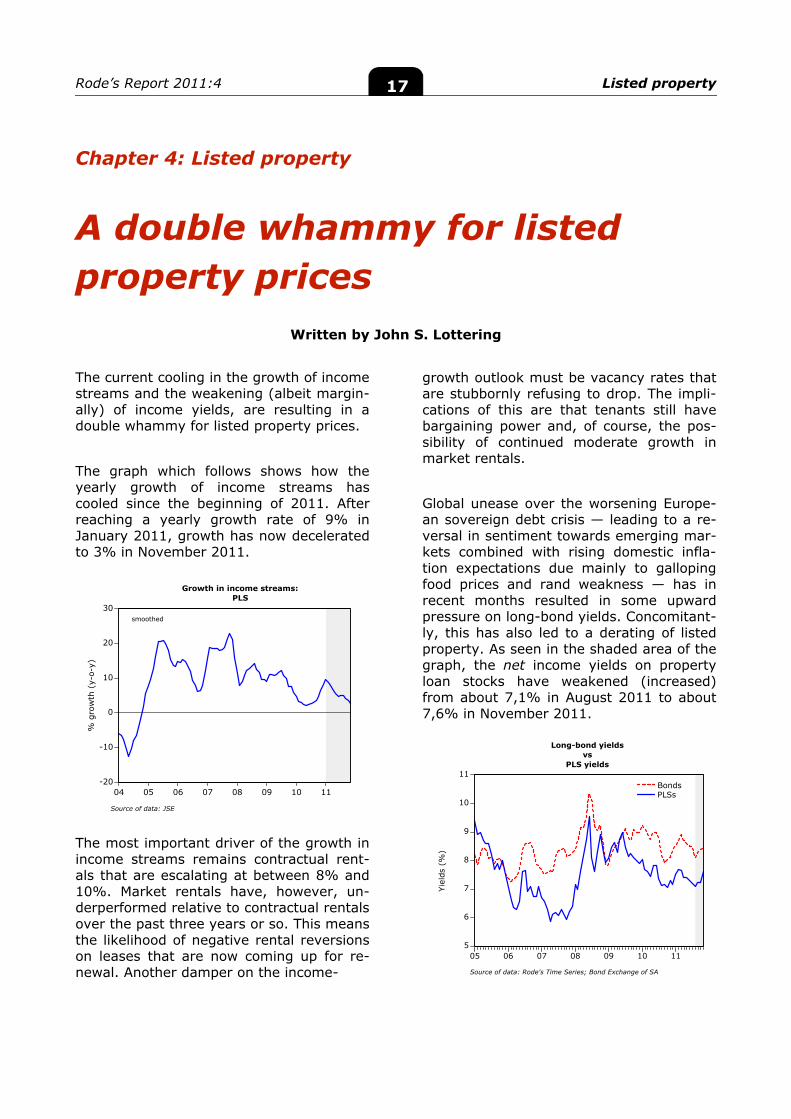

A double whammy for listed property prices

Written by John S. Lottering

The current cooling in the growth of income streams and the weakening (albeit margin-ally) of income yields, are resulting in a double whammy for listed property prices.

The graph which follows shows how the yearly growth of income streams has cooled since the beginning of 2011. After reaching a yearly growth rate of 9% in January 2011, growth has now decelerated to 3% in November 2011. The most important driver of the growth in income streams remains contractual rent-als that are escalating at between 8% and 10%. Market rentals have, however, un-derperformed relative to contractual rentals over the past three years or so. This means the likelihood of negative rental reversions on leases that are now coming up for re-newal. Another damper on the income-

growth outlook must be vacancy rates that are stubbornly refusing to drop. The impli-cations of this are that tenants still have bargaining power and, of course, the pos-sibility of continued moderate growth in market rentals.

Global unease over the worsening Europe-an sovereign debt crisis — leading to a re-versal in sentiment towards emerging mar-kets combined with rising domestic infla-tion expectations due mainly to galloping food prices and rand weakness — has in recent months resulted in some upward pressure on long-bond yields. Concomitant-ly, this has also led to a derating of listed property. As seen in the shaded area of the graph, the net income yields on property loan stocks have weakened (increased) from about 7,1% in August 2011 to about 7,6% in November 2011.

Rode’s Report 2011:4 Listed property 18

-40

-20

0

20

40

60

80

03 04 05 06 07 08 09 10 11

Growth in PLS prices

% g

row

th (

y-o-

y)

Source of data: JSE

smoothed

5

10

15

20

25

80

90

100

110

120

92 94 96 98 00 02 04 06 08 10

PLS yieldsBusiness cycle

PLS net income yieldsvs

S.A. composite leading business cycle indicator

r = -0,8

PLS y

ield

s (%

)

Business cycle indicator

(2000 = 100)

Source of data: JSE; SARB

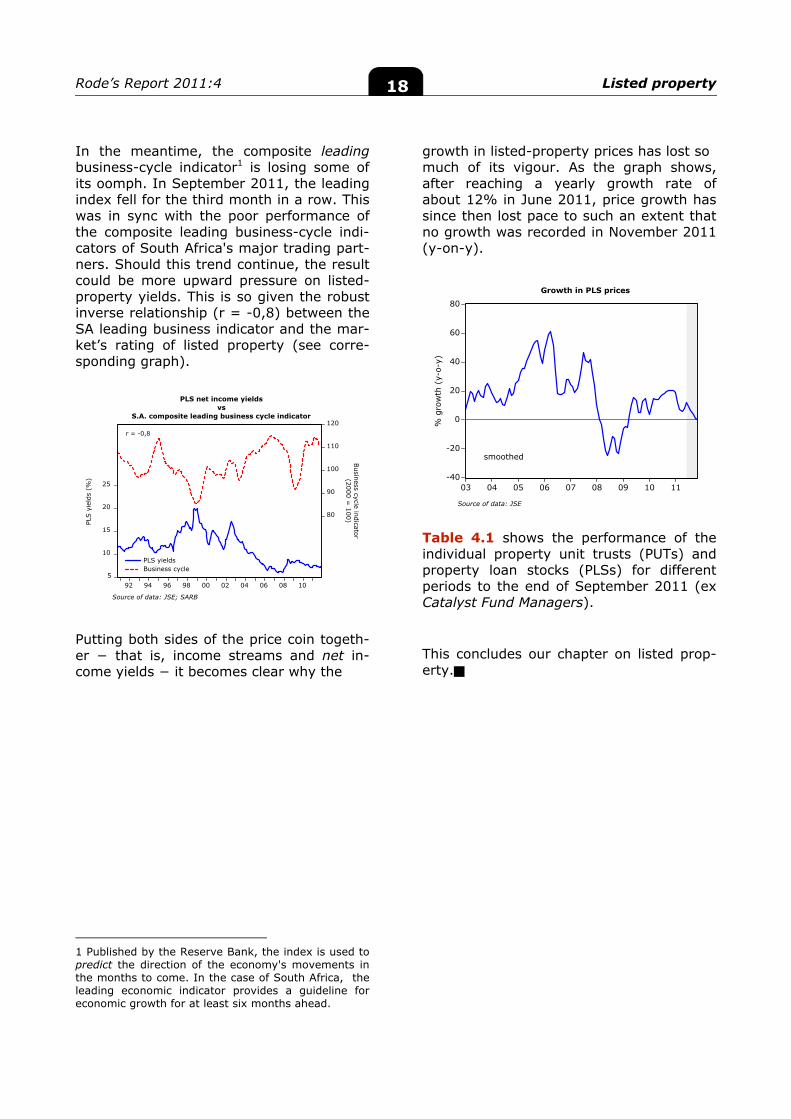

In the meantime, the composite leading business-cycle indicator1 is losing some of its oomph. In September 2011, the leading index fell for the third month in a row. This was in sync with the poor performance of the composite leading business-cycle indi-cators of South Africa's major trading part-ners. Should this trend continue, the result could be more upward pressure on listed-property yields. This is so given the robust inverse relationship (r = -0,8) between the SA leading business indicator and the mar-ket’s rating of listed property (see corre-sponding graph). Putting both sides of the price coin togeth-er − that is, income streams and net in-come yields − it becomes clear why the

1 Published by the Reserve Bank, the index is used to predict the direction of the economy's movements in the months to come. In the case of South Africa, the leading economic indicator provides a guideline for economic growth for at least six months ahead.

growth in listed-property prices has lost so much of its vigour. As the graph shows, after reaching a yearly growth rate of about 12% in June 2011, price growth has since then lost pace to such an extent that no growth was recorded in November 2011 (y-on-y).

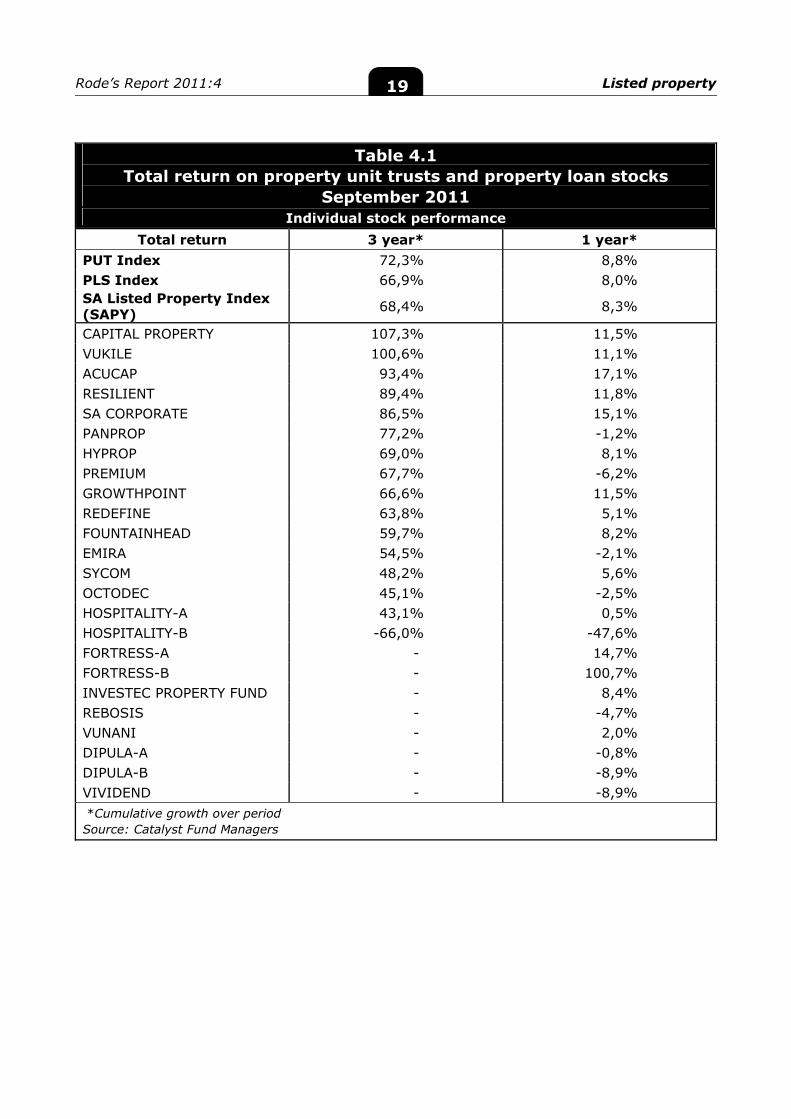

Table 4.1 shows the performance of the individual property unit trusts (PUTs) and property loan stocks (PLSs) for different periods to the end of September 2011 (ex Catalyst Fund Managers).

This concludes our chapter on listed prop-erty.

Rode’s Report 2011:4 Listed property 19

Table 4.1 Total return on property unit trusts and property loan stocks

September 2011 Individual stock performance

Total return 3 year* 1 year* PUT Index 72,3% 8,8% PLS Index 66,9% 8,0% SA Listed Property Index (SAPY) 68,4% 8,3%

CAPITAL PROPERTY 107,3% 11,5% VUKILE 100,6% 11,1% ACUCAP 93,4% 17,1% RESILIENT 89,4% 11,8% SA CORPORATE 86,5% 15,1% PANPROP 77,2% -1,2% HYPROP 69,0% 8,1% PREMIUM 67,7% -6,2% GROWTHPOINT 66,6% 11,5% REDEFINE 63,8% 5,1% FOUNTAINHEAD 59,7% 8,2% EMIRA 54,5% -2,1% SYCOM 48,2% 5,6% OCTODEC 45,1% -2,5% HOSPITALITY-A 43,1% 0,5% HOSPITALITY-B -66,0% -47,6% FORTRESS-A - 14,7% FORTRESS-B - 100,7% INVESTEC PROPERTY FUND - 8,4% REBOSIS - -4,7% VUNANI - 2,0% DIPULA-A - -0,8% DIPULA-B - -8,9% VIVIDEND - -8,9% *Cumulative growth over period Source: Catalyst Fund Managers

Rode’s Report 2011:4 Office rentals 21

20

40

60

80

100

120

94 96 98 00 02 04 06 08 10

PretoriaJohannesburgDurbanCape Town

Nominal decentralized grade-A office rentals

Smoothed

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

20

40

60

80

100

94 96 98 00 02 04 06 08 10

JohannesburgPretoriaDurbanCape Town

Nominal CBD grade-A office rentals

Smoothed

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

Chapter 5: Office rentals

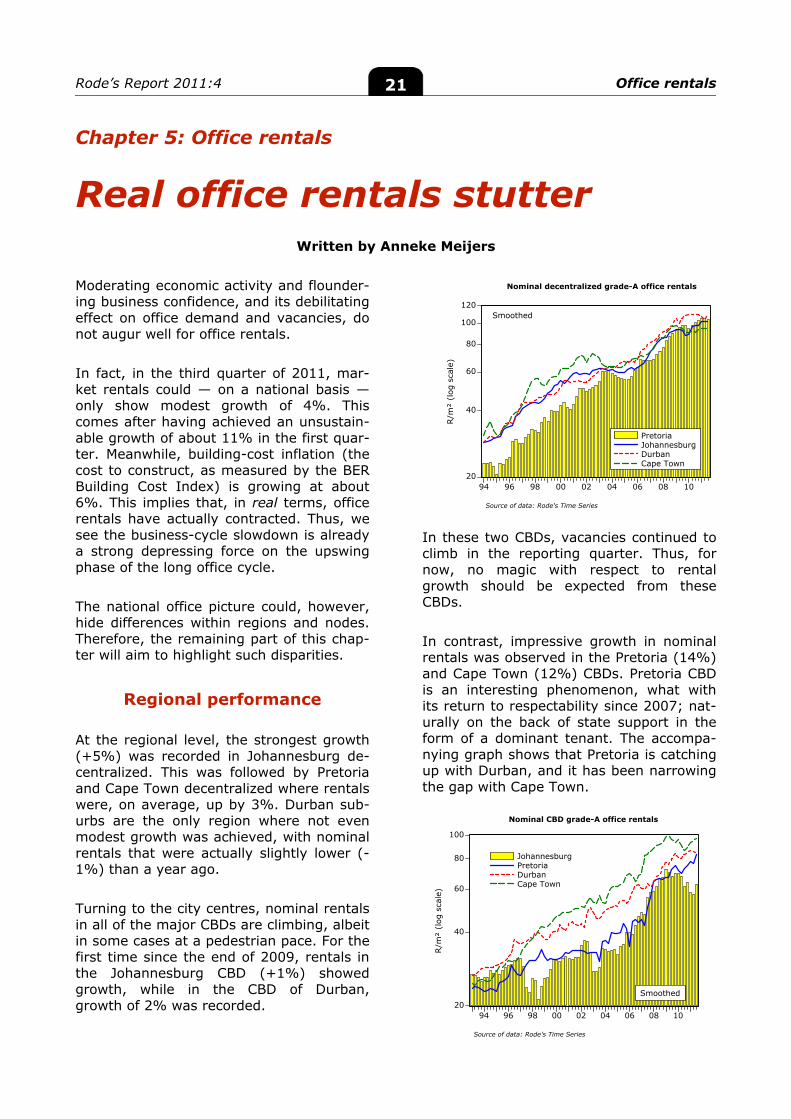

Real office rentals stutter

Written by Anneke Meijers Moderating economic activity and flounder-ing business confidence, and its debilitating effect on office demand and vacancies, do not augur well for office rentals. In fact, in the third quarter of 2011, mar-ket rentals could — on a national basis — only show modest growth of 4%. This comes after having achieved an unsustain-able growth of about 11% in the first quar-ter. Meanwhile, building-cost inflation (the cost to construct, as measured by the BER Building Cost Index) is growing at about 6%. This implies that, in real terms, office rentals have actually contracted. Thus, we see the business-cycle slowdown is already a strong depressing force on the upswing phase of the long office cycle. The national office picture could, however, hide differences within regions and nodes. Therefore, the remaining part of this chap-ter will aim to highlight such disparities.

Regional performance At the regional level, the strongest growth (+5%) was recorded in Johannesburg de-centralized. This was followed by Pretoria and Cape Town decentralized where rentals were, on average, up by 3%. Durban sub-urbs are the only region where not even modest growth was achieved, with nominal rentals that were actually slightly lower (-1%) than a year ago. Turning to the city centres, nominal rentals in all of the major CBDs are climbing, albeit in some cases at a pedestrian pace. For the first time since the end of 2009, rentals in the Johannesburg CBD (+1%) showed growth, while in the CBD of Durban, growth of 2% was recorded.

In these two CBDs, vacancies continued to climb in the reporting quarter. Thus, for now, no magic with respect to rental growth should be expected from these CBDs. In contrast, impressive growth in nominal rentals was observed in the Pretoria (14%) and Cape Town (12%) CBDs. Pretoria CBD is an interesting phenomenon, what with its return to respectability since 2007; nat-urally on the back of state support in the form of a dominant tenant. The accompa-nying graph shows that Pretoria is catching up with Durban, and it has been narrowing the gap with Cape Town.

Rode’s Report 2011:4 Office rentals 22

20

40

60

80

100

120

140

94 96 98 00 02 04 06 08 10

ParktownRosebankRivoniaSandton CBD

Nominal Johannesburg decentralized grade-A office rentals

Smoothed

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

20

40

60

80

100

120

140

94 96 98 00 02 04 06 08 10

Randburg FerndaleBryanstonIllovoSandton CBD

Nominal Johannesburg decentralized grade-A office rentals

Smoothed

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

40

60

80

100

120

140

160

94 96 98 00 02 04 06 08 10

ParktownRosebankRivoniaSandton CBD

Real Johannesburg decentralized grade-A office rentals2005 rands

Smoothed

2005

R/m

² (l

og s

cale

)

Deflated by BER BCI (2005=100)

Source of data: Rode's Time Series; BER

40

60

80

100

120

140

160

94 96 98 00 02 04 06 08 10

Randburg FerndaleBryanston IllovoSandton CBD

Real Johannesburg decentralized grade-A office rentals2005 rands

Smoothed

2005

R/m

² (l

og s

cale

)

Deflated by BER BCI (2005=100)

Source of data: Rode's Time Series; BER

30

40

50

60

70

80

90

94 96 98 00 02 04 06 08 10

JohannesburgPretoriaDurbanCape Town

Real CBD grade-A office rentals2005 rands

Smoothed

2005

R/m

² (l

og s

cale

)

Deflated by BER BCI (2005=100)

Source of data: Rode's Time Series; BER

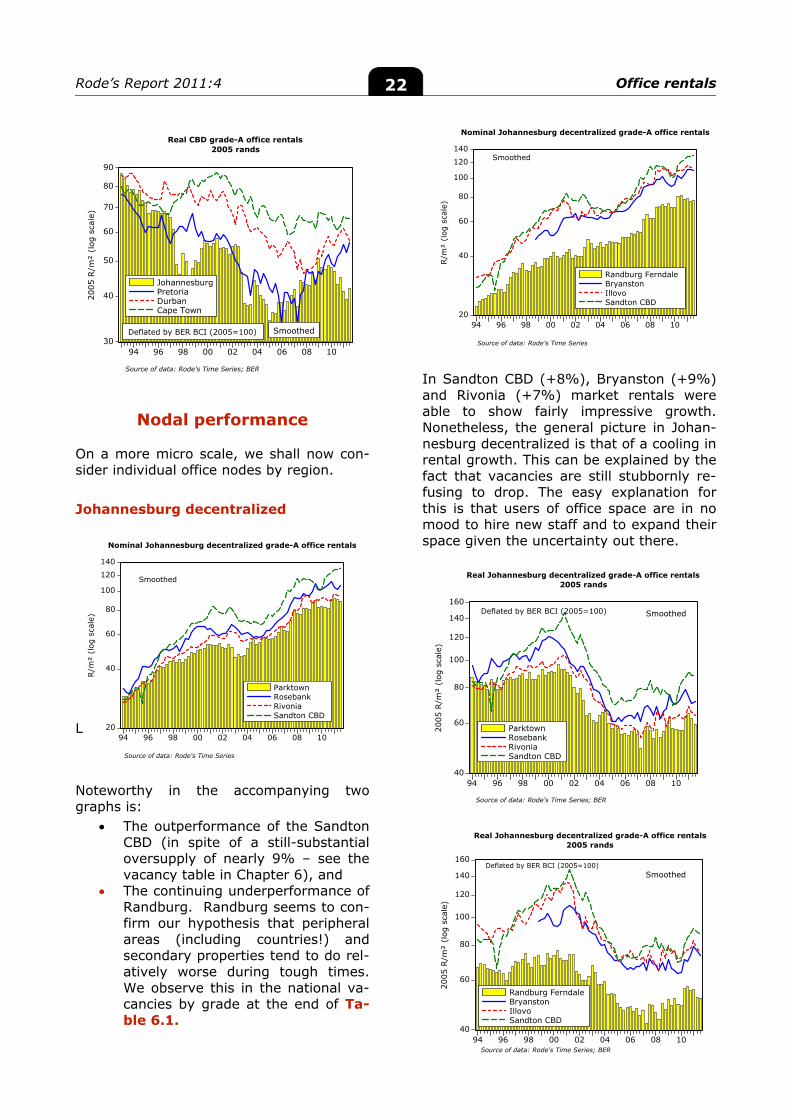

Nodal performance

On a more micro scale, we shall now con-sider individual office nodes by region. Johannesburg decentralized L Noteworthy in the accompanying two graphs is:

The outperformance of the Sandton CBD (in spite of a still-substantial oversupply of nearly 9% – see the vacancy table in Chapter 6), and

The continuing underperformance of Randburg. Randburg seems to con-firm our hypothesis that peripheral areas (including countries!) and secondary properties tend to do rel-atively worse during tough times. We observe this in the national va-cancies by grade at the end of Ta-ble 6.1.

In Sandton CBD (+8%), Bryanston (+9%) and Rivonia (+7%) market rentals were able to show fairly impressive growth. Nonetheless, the general picture in Johan-nesburg decentralized is that of a cooling in rental growth. This can be explained by the fact that vacancies are still stubbornly re-fusing to drop. The easy explanation for this is that users of office space are in no mood to hire new staff and to expand their space given the uncertainty out there.

Rode’s Report 2011:4 Office rentals 23

20

40

60

80

100

120140

94 96 98 00 02 04 06 08 10

CenturionBrooklyn/WaterkloofHatfieldMenlyn

Nominal Pretoria decentralized grade-A office rentals

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

Smoothed

50

60

70

80

90

100

110

94 96 98 00 02 04 06 08 10

CenturionBrooklyn/WaterkloofHatfieldMenlyn

Real Pretoria decentralized grade-A office rentals2005 rands

Smoothed

2005

R/m

² (l

og s

cale

)

Deflated by BER BCI (2005=100)

Source of data: Rode's Time Series; BER

20

40

60

80

100

120

140

94 96 98 00 02 04 06 08 10

Tyger ValleyClaremontCentury CityWestlake

Nominal Cape Town decentralized grade-A office rentals

Smoothed

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

40

60

80

100

120

140

94 96 98 00 02 04 06 08 10

Tyger ValleyClaremontCentury CityWestlake

Real Cape Town decentralized grade-A office rentals2005 rands

Smoothed

2005

R/m

² (l

og s

cale

)

Deflated by BER BCI (2005=100)

Source of data: Rode's Time Series; BER

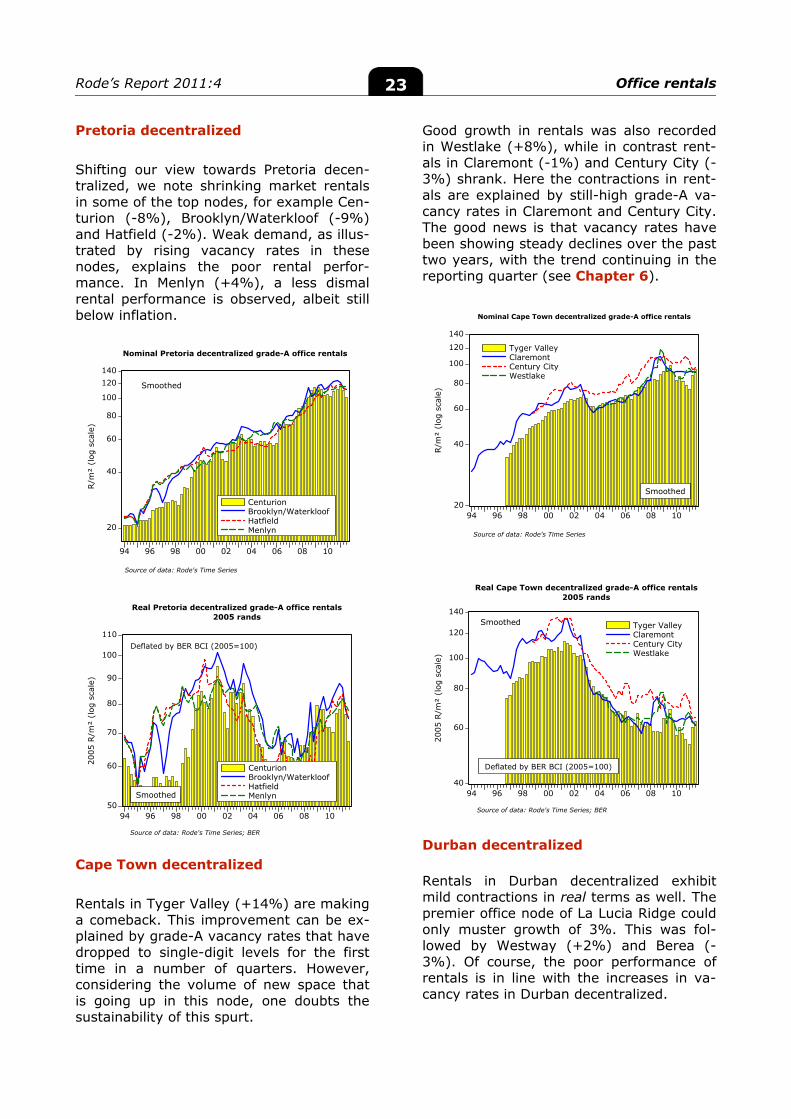

Pretoria decentralized Shifting our view towards Pretoria decen-tralized, we note shrinking market rentals in some of the top nodes, for example Cen-turion (-8%), Brooklyn/Waterkloof (-9%) and Hatfield (-2%). Weak demand, as illus-trated by rising vacancy rates in these nodes, explains the poor rental perfor-mance. In Menlyn (+4%), a less dismal rental performance is observed, albeit still below inflation. Cape Town decentralized Rentals in Tyger Valley (+14%) are making a comeback. This improvement can be ex-plained by grade-A vacancy rates that have dropped to single-digit levels for the first time in a number of quarters. However, considering the volume of new space that is going up in this node, one doubts the sustainability of this spurt.

Good growth in rentals was also recorded in Westlake (+8%), while in contrast rent-als in Claremont (-1%) and Century City (-3%) shrank. Here the contractions in rent-als are explained by still-high grade-A va-cancy rates in Claremont and Century City. The good news is that vacancy rates have been showing steady declines over the past two years, with the trend continuing in the reporting quarter (see Chapter 6). Durban decentralized

Rentals in Durban decentralized exhibit mild contractions in real terms as well. The premier office node of La Lucia Ridge could only muster growth of 3%. This was fol-lowed by Westway (+2%) and Berea (-3%). Of course, the poor performance of rentals is in line with the increases in va-cancy rates in Durban decentralized.

Rode’s Report 2011:4 Office rentals 24

20

40

60

80

100

120

140

94 96 98 00 02 04 06 08 10

BereaLa Lucia RidgeWestway

Nominal Durban decentralized grade-A office rentals

Smoothed

R/m

² (l

og s

cale

)

Source of data: Rode's Time Series

50

60

70

80

90

100

110

94 96 98 00 02 04 06 08 10

BereaLa Lucia RidgeWestway

Real Durban decentralized grade-A office rentals2005 rands

Smoothed

2005

R/m

² (l

og s

cale

)

Deflated by BER BCI (2005=100)

Source of data: Rode's Time Series; BER

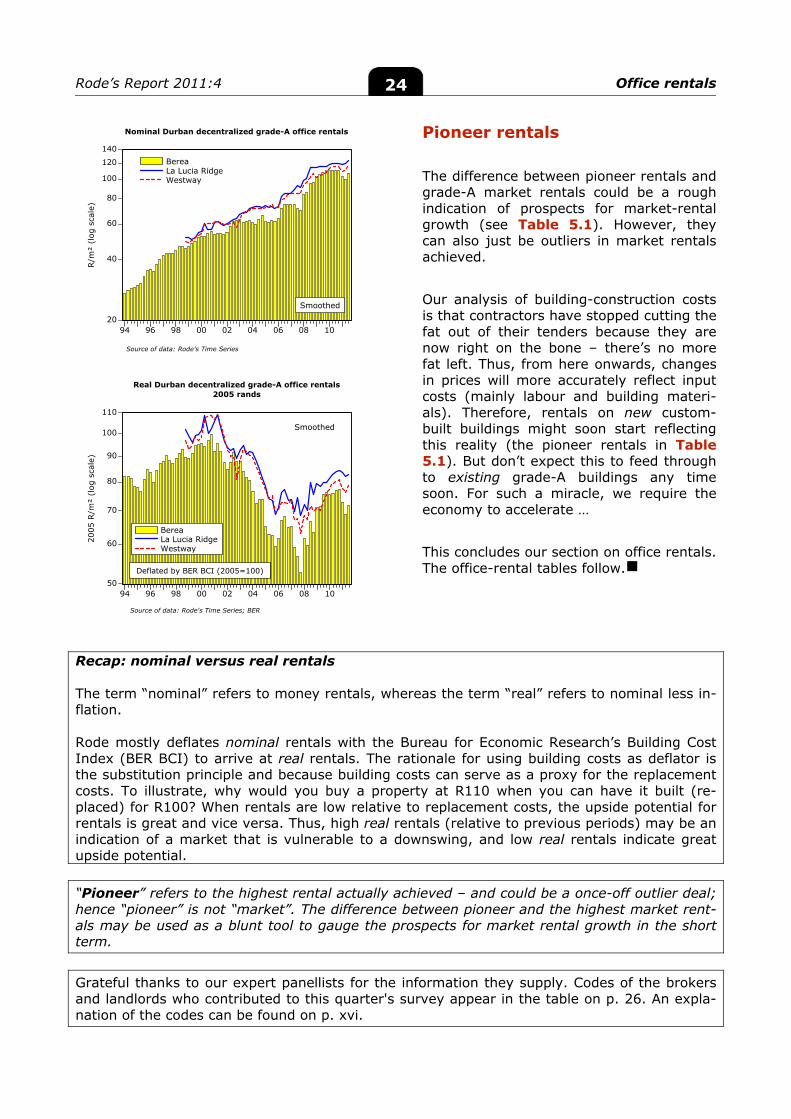

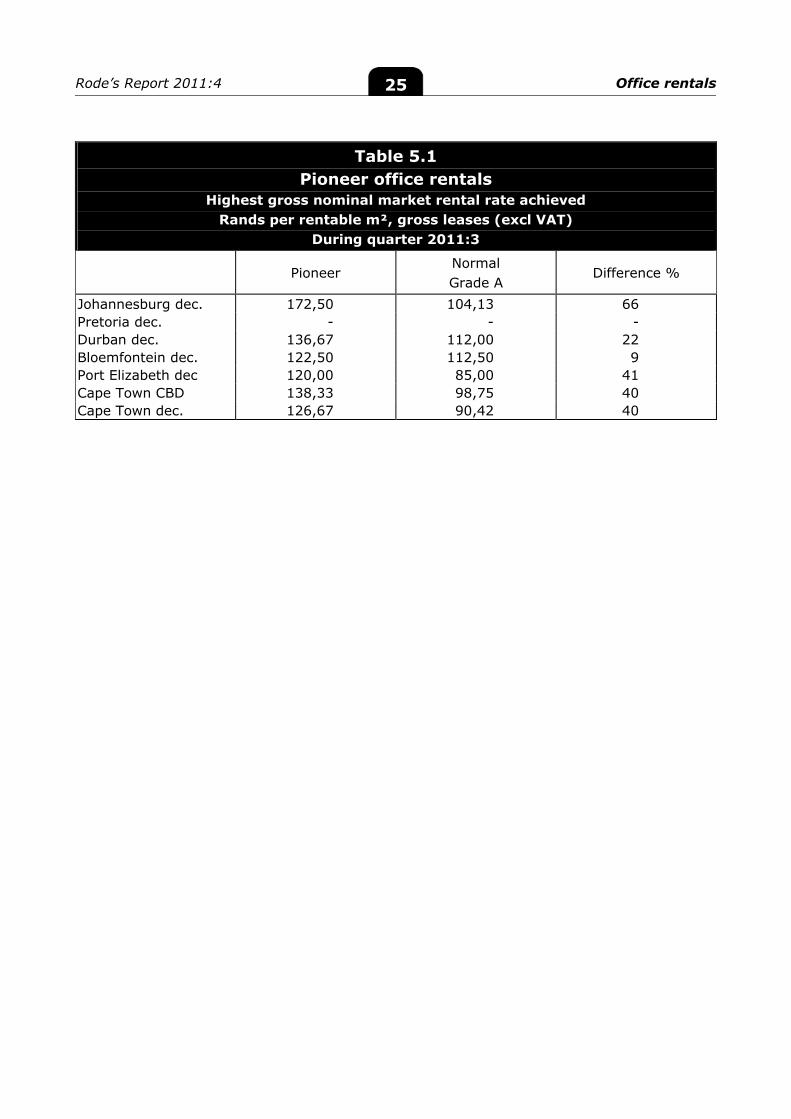

Pioneer rentals The difference between pioneer rentals and grade-A market rentals could be a rough indication of prospects for market-rental growth (see Table 5.1). However, they can also just be outliers in market rentals achieved. Our analysis of building-construction costs is that contractors have stopped cutting the fat out of their tenders because they are now right on the bone – there’s no more fat left. Thus, from here onwards, changes in prices will more accurately reflect input costs (mainly labour and building materi-als). Therefore, rentals on new custom-built buildings might soon start reflecting this reality (the pioneer rentals in Table 5.1). But don’t expect this to feed through to existing grade-A buildings any time soon. For such a miracle, we require the economy to accelerate … This concludes our section on office rentals. The office-rental tables follow.

Recap: nominal versus real rentals The term “nominal” refers to money rentals, whereas the term “real” refers to nominal less in-flation. Rode mostly deflates nominal rentals with the Bureau for Economic Research’s Building Cost Index (BER BCI) to arrive at real rentals. The rationale for using building costs as deflator is the substitution principle and because building costs can serve as a proxy for the replacement costs. To illustrate, why would you buy a property at R110 when you can have it built (re-placed) for R100? When rentals are low relative to replacement costs, the upside potential for rentals is great and vice versa. Thus, high real rentals (relative to previous periods) may be an indication of a market that is vulnerable to a downswing, and low real rentals indicate great upside potential.

“Pioneer” refers to the highest rental actually achieved – and could be a once-off outlier deal; hence “pioneer” is not “market”. The difference between pioneer and the highest market rent-als may be used as a blunt tool to gauge the prospects for market rental growth in the short term.

Grateful thanks to our expert panellists for the information they supply. Codes of the brokers and landlords who contributed to this quarter's survey appear in the table on p. 26. An expla-nation of the codes can be found on p. xvi.

Rode’s Report 2011:4 Office rentals 25

Table 5.1 Pioneer office rentals

Highest gross nominal market rental rate achieved Rands per rentable m², gross leases (excl VAT)

During quarter 2011:3

Pioneer Normal Grade A

Difference %

Johannesburg dec. 172,50 104,13 66 Pretoria dec. - - - Durban dec. 136,67 112,00 22 Bloemfontein dec. 122,50 112,50 9 Port Elizabeth dec 120,00 85,00 41 Cape Town CBD 138,33 98,75 40 Cape Town dec. 126,67 90,42 40

Rode’s Report 2011:4 Office rentals 26

Table 5.2 Market rental rates for office buildings

Quarter 2011:3 Rands per rentable m², gross leases (excl VAT)

Grade A+

Grade A mean

Grade B mean

Grade C mean Broker contributor codes

Johannesburg CBD - 64,67 55,80 51,67 AR, BM, GB, PC, QU Braamfontein 95,00 76,00 55,25 24,00 AR, BM, GB, PC, QU Sandton CBD 159,75 132,50 100,75 83,00 AR, AW, BM, GB, PC, QU Dunkeld West 127,00 111,80 92,33 87,33 AR, AW, BM, GB, KM, PC Wierda Valley 133,38 111,25 99,60 87,75 AR, BM, GB, PC, QU Randburg Ferndale 85,50 78,00 75,33 50,00 AR, BM, PC, QU Rivonia 118,33 96,58 84,42 74,30 AR, BC, BM, GB, PC, QU Rosebank 134,38 108,20 88,00 79,50 AR, AW, BM, GB, PC, QU Illovo 133,33 114,33 96,50 85,00 AR, AW, BM, GB, PC, QU Illovo Boulevard 135,00 118,80 100,25 85,00 AR, BM, GB, PC, QU Chiselhurston 118,00 114,67 106,00 85,00 AR, BM, KM, PC Parktown 97,80 88,38 77,50 70,80 AR, BM, DT, GB, PC, QU Richmond/Milpark - 81,00 78,50 63,00 AR, BM, KM, PC Bedfordview 109,50 99,75 90,67 79,67 AR, MR, PC, QU Bruma 97,12 87,62 75,38 68,67 AR, MR, PC, QU Meadowbrook - - - - Woodmead 116,40 106,60 90,00 82,00 AR, AW, BM, GM, PC Sunninghill 108,50 93,38 86,25 76,75 AR, BM, GB, PC, QU Bryanston/Epsom 121,75 109,60 90,17 83,00 AR, BM, GB, KM, PC, QU Fourways 133,33 105,75 88,75 75,75 AR, BM, GB, QU Houghton 116,67 103,75 91,33 85,00 AR, BM, GB, PC, QU Melrose Arch 188,00 180,00 - - AR, GB, PC Hydepark 123,38 115,00 92,20 81,00 AR, BM, GB, KM, PC, QU Eastgate/Kramerville - 80,00 58,00 57,00 AR, BM, PA Ormonde 89,00 78,50 76,00 71,00 AR, GB, PC Midrand 104,00 91,75 77,00 66,00 AR, BM, GB, PC, QU Hendrik Potgieter Corri-dor

117,50 92,00 80,67 68,67 AR, BM, PC

Germiston - - - - Pretoria CBD 105,00 87,50 75,00 62,50 AI, EV Lynnwood Glen 110,00 105,00 87,50 70,00 AI, EV Lynnwood 100,00 89,50 80,00 67,50 AI, EV Lynnwood Manor 137,50 110,00 85,00 60,00 AI, EV Lynnwood Ridge 116,00 115,00 86,50 65,00 AI, EV Faerie Glen 115,00 104,50 85,00 60,00 AI, EV Val de Grace - - - - Menlyn 135,00 116,00 95,00 75,00 AI, EV Menlo Park (Brooks St.) 125,00 120,00 102,50 70,00 AI, EV Brooklyn/Waterkloof 130,00 112,50 91,50 75,00 AI, EV Nieuw Muckleneuk - 120,50 85,00 70,00 AI, EV Hatfield 115,00 110,00 89,00 60,00 AI, EV Centurion 107,50 97,50 90,00 60,00 AI, EV Highveld Technopark 122,50 102,50 85,00 60,00 AI, EV Sunnyside 110,00 95,00 80,00 55,00 AI, EV Arcadia 100,00 87,50 80,00 62,50 AI, EV Murrayfield 100,00 85,00 75,00 55,00 AI Nelspruit - - - - Polokwane 160,00 125,00 87,50 75,80 ES Bloemfontein CBD 125,00 115,00 75,00 52,50 CC, EK Westdene 117,50 112,50 75,00 57,50 CC, EK For definitions, see Glossary of terms and abbreviations in Annexure 1 or visit www.rode.co.za.

Rode’s Report 2011:4 Office rentals 27

Table 5.2(continued) Market rental rates for office buildings

Quarter 2011:3 Rands per rentable m², gross leases (excl VAT)

Grade A+

Grade A mean

Grade B mean

Grade C mean Broker contributor codes

Durban CBD - 85,00 55,00 40,00 MW Durban Berea - 110,00 90,00 75,00 MW Essex Terrace - 95,00 85,00 75,00 MW Westway 125,00 120,00 105,00 - ACU, MW La Lucia Ridge - 125,00 105,00 - MW Westville - 110,00 92,50 77,50 ACU, MW Pinetown - 60,00 50,00 40,00 LS Hillcrest-Kloof (Upper Highway)

- - - -