Embed Size (px)

Citation preview

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

FINANCIAL STATEMENTS

YEAR ENDED JUNE 30, 2014

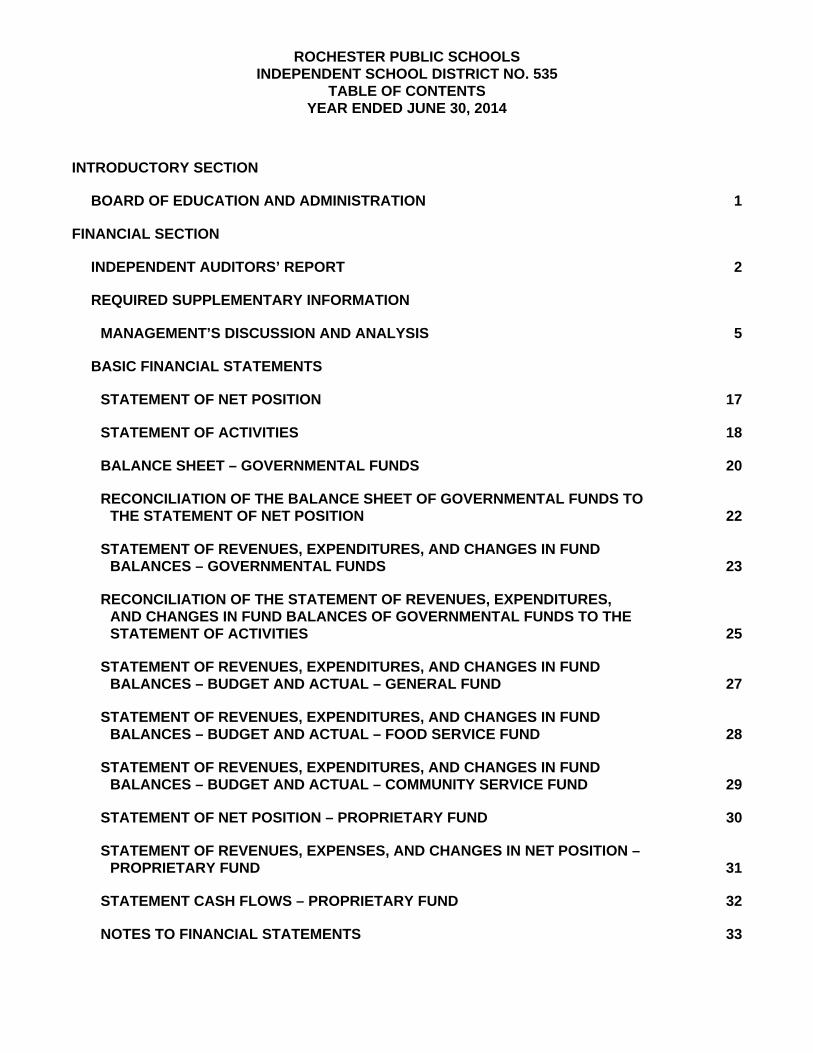

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

TABLE OF CONTENTS YEAR ENDED JUNE 30, 2014

INTRODUCTORY SECTION

BOARD OF EDUCATION AND ADMINISTRATION 1

FINANCIAL SECTION

INDEPENDENT AUDITORS’ REPORT 2

REQUIRED SUPPLEMENTARY INFORMATION

MANAGEMENT’S DISCUSSION AND ANALYSIS 5

BASIC FINANCIAL STATEMENTS

STATEMENT OF NET POSITION 17

STATEMENT OF ACTIVITIES 18

BALANCE SHEET – GOVERNMENTAL FUNDS 20

RECONCILIATION OF THE BALANCE SHEET OF GOVERNMENTAL FUNDS TO THE STATEMENT OF NET POSITION 22

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – GOVERNMENTAL FUNDS 23

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES 25

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – BUDGET AND ACTUAL – GENERAL FUND 27

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – BUDGET AND ACTUAL – FOOD SERVICE FUND 28

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – BUDGET AND ACTUAL – COMMUNITY SERVICE FUND 29

STATEMENT OF NET POSITION – PROPRIETARY FUND 30

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION – PROPRIETARY FUND 31

STATEMENT CASH FLOWS – PROPRIETARY FUND 32

NOTES TO FINANCIAL STATEMENTS 33

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

TABLE OF CONTENTS YEAR ENDED JUNE 30, 2014

REQUIRED SUPPLEMENTARY INFORMATION

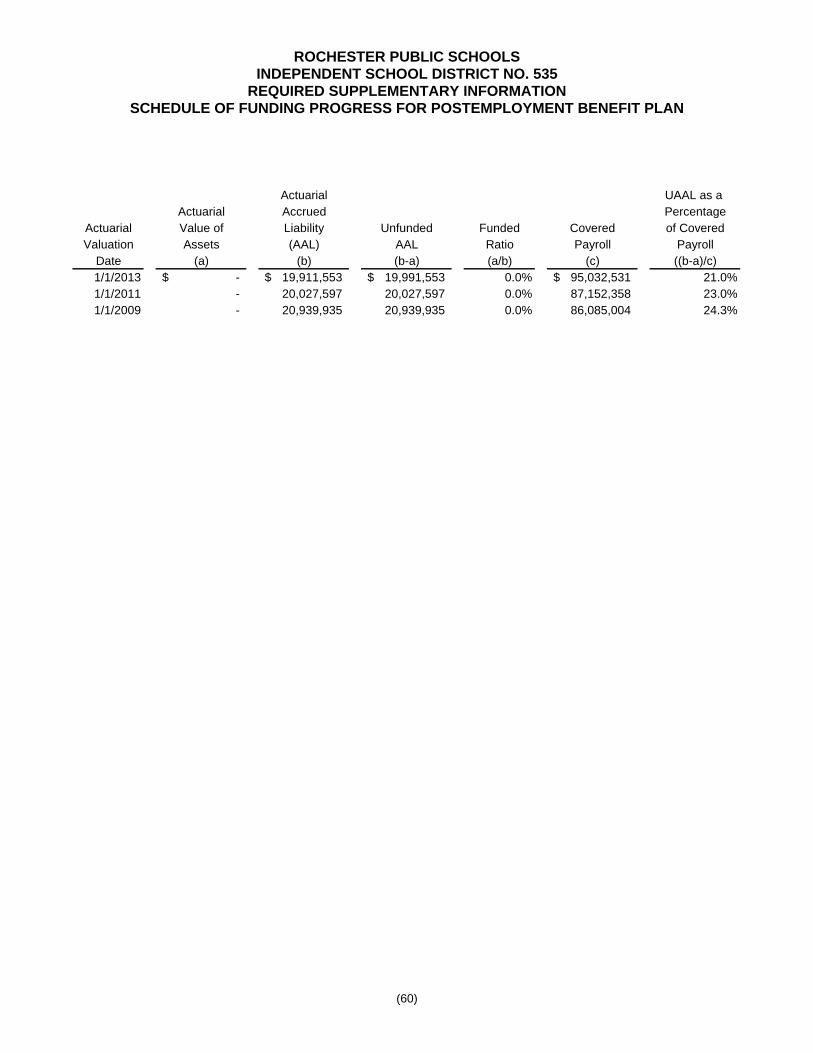

SCHEDULE OF FUNDING PROGRESS FOR POSTEMPLOYMENT BENEFIT PLAN 60

SUPPLEMENTARY INFORMATION

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE – BUDGET AND ACTUAL – CAPITAL PROJECTS FUND 61

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE – BUDGET AND ACTUAL – DEBT SERVICE FUND 62

COMBINING BALANCE SHEET – CAPITAL PROJECTS FUND 63

COMBINING STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE – BUDGET AND ACTUAL – CAPITAL PROJECTS FUND 64

COMBINING STATEMENT OF NET POSITION – PROPRIETARY FUNDS 66

COMBINING STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION – PROPRIETARY FUNDS 67

COMBINING STATEMENT OF CASH FLOWS – PROPRIETARY FUNDS 68

SINGLE AUDIT AND OTHER REQUIRED REPORTS

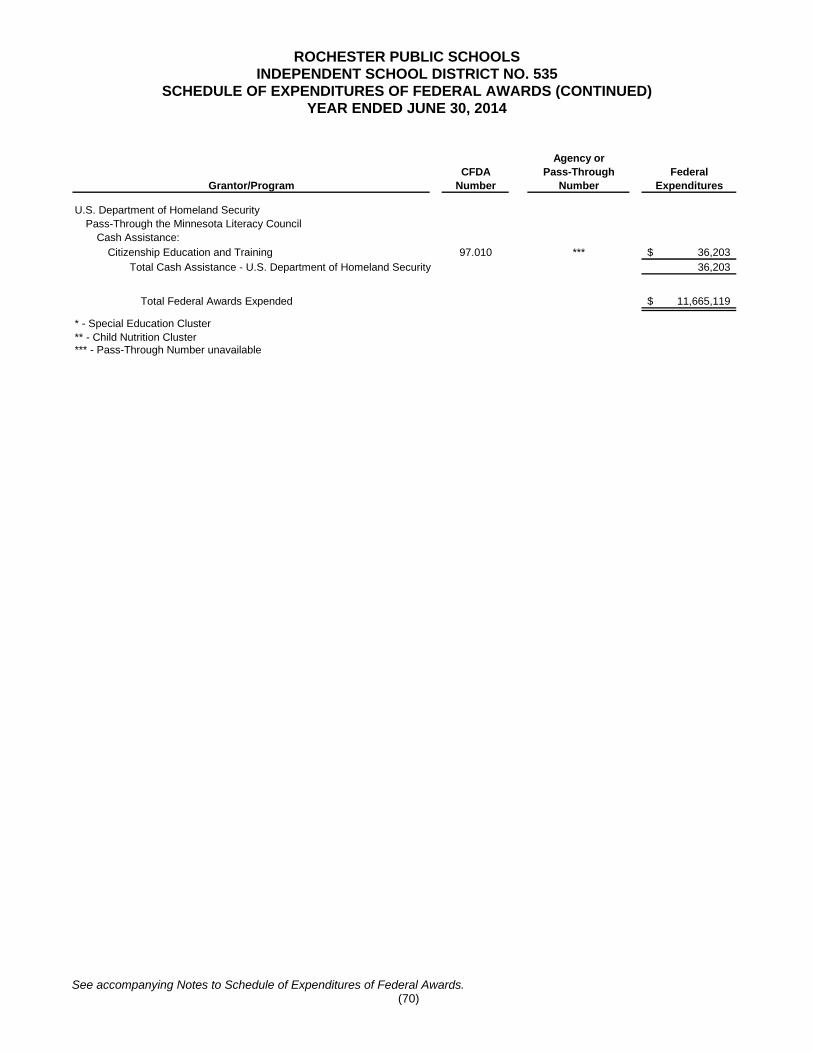

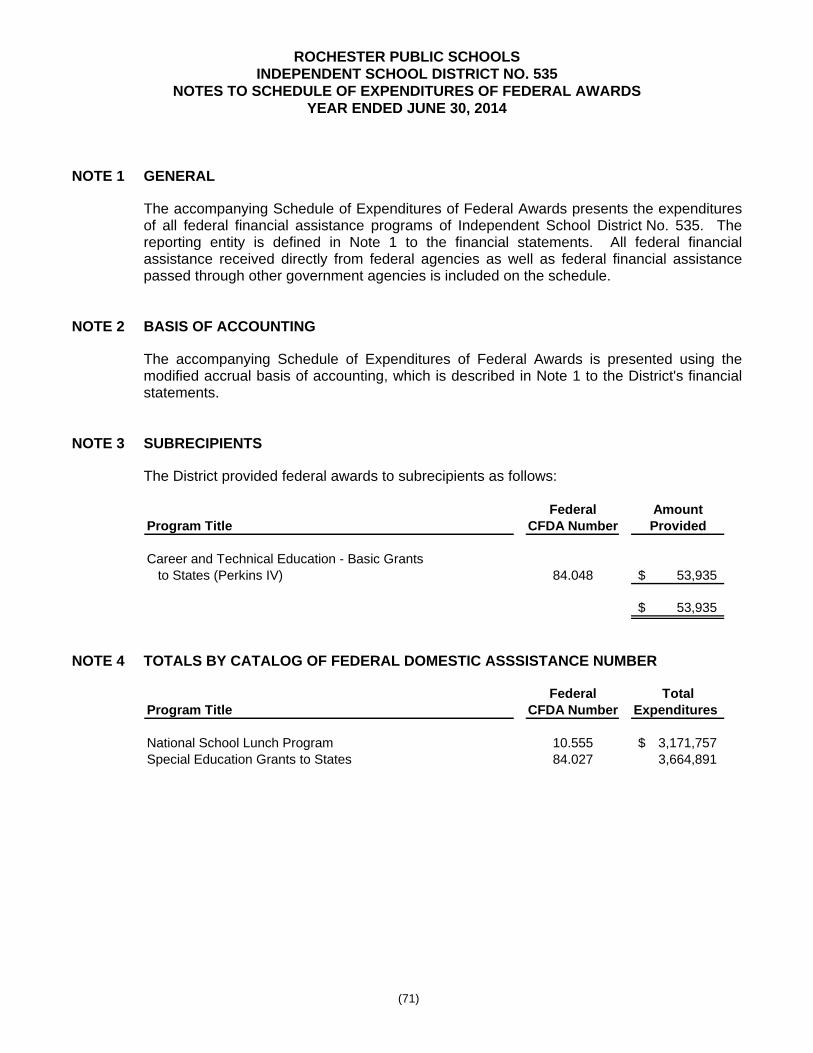

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 69

NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 71

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 72

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133 74

INDEPENDENT AUDITORS’ REPORT ON MINNESOTA LEGAL COMPLIANCE 76

SCHEDULE OF FINDINGS AND QUESTIONED COSTS 77

SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS 80

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

TABLE OF CONTENTS YEAR ENDED JUNE 30, 2014

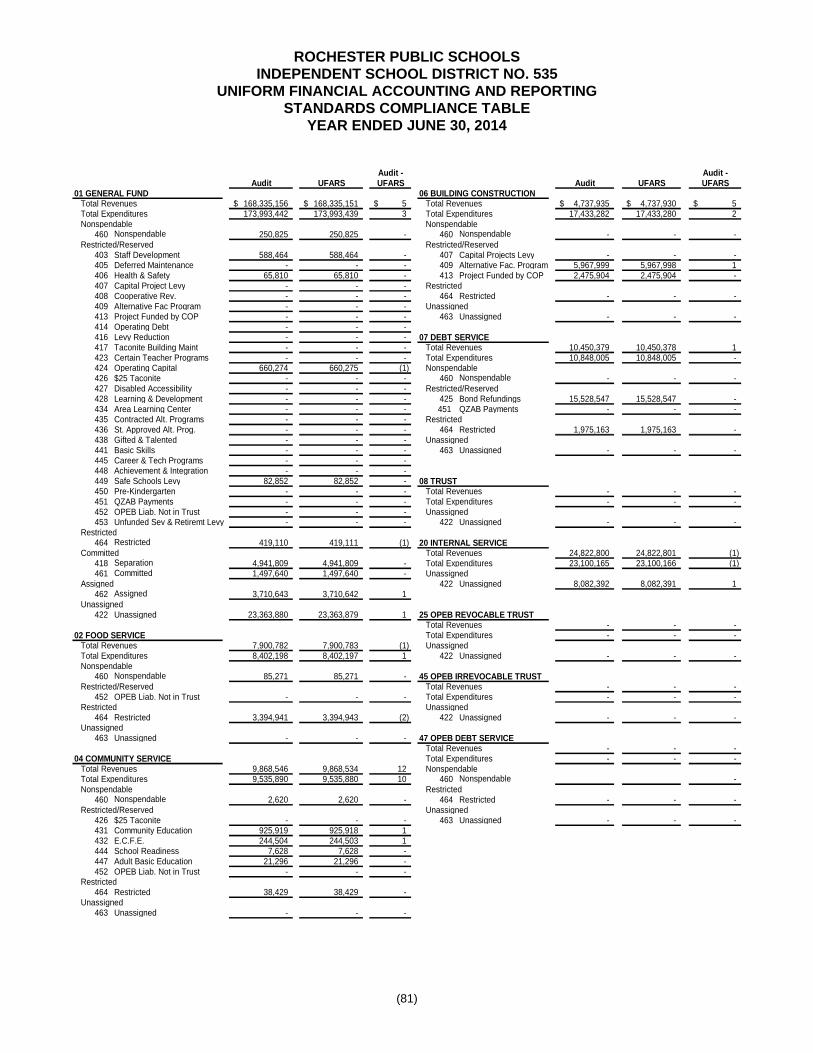

UNIFORM FINANCIAL ACCOUNTING AND REPORTING STANDARDS COMPLIANCE TABLE 81

STUDENT ACTIVITY FUNDS

INDEPENDENT AUDITORS’ REPORT 82

STATEMENT OF CASH RECEIPTS AND DISBURSEMENTS – STUDENT ACTIVITY ACCOUNTS 84

NOTE TO STUDENT ACTIVITY FUND FINANCIAL STATEMENTS 85

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE WITH THE MANUAL FOR ACTIVITY FUND ACCOUNTING 86

INTRODUCTORY SECTION

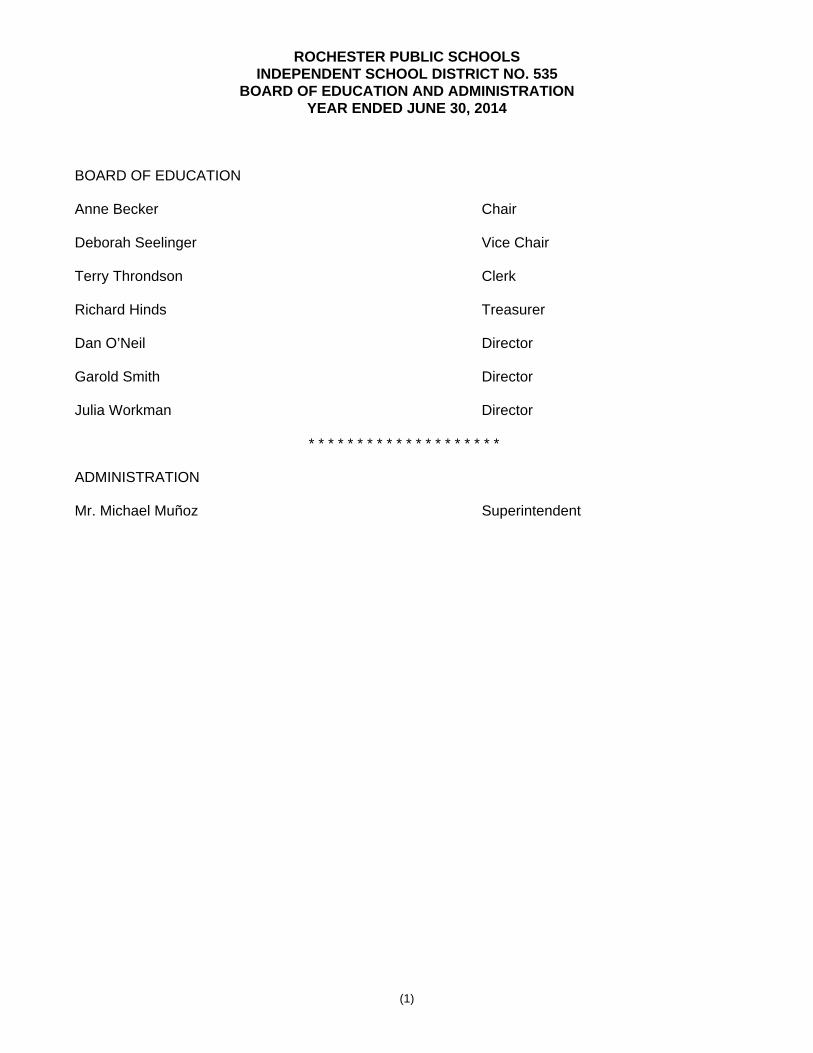

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

BOARD OF EDUCATION AND ADMINISTRATION YEAR ENDED JUNE 30, 2014

(1)

BOARD OF EDUCATION Anne Becker Chair Deborah Seelinger Vice Chair Terry Throndson Clerk Richard Hinds Treasurer Dan O’Neil Director Garold Smith Director Julia Workman Director

* * * * * * * * * * * * * * * * * * * * ADMINISTRATION Mr. Michael Muñoz Superintendent

(This page intentionally left blank)

FINANCIAL SECTION

(This page intentionally left blank)

(2) An independent member of Nexia International

INDEPENDENT AUDITORS’ REPORT Board of Education Independent School District No. 535 Rochester, Minnesota Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of Independent School District No. 535, as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the District’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the District’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the District’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Board of Education Independent School District No. 535

(3)

Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund, and the aggregate remaining fund information of Independent School District No. 535 as of June 30, 2014, and the respective changes in financial position and, where applicable, cash flows, and budgetary comparison for General Fund, Food Service Fund, and Community Service Fund thereof, for the year then ended in accordance with accounting principles generally accepted in the United States of America. Report on Summarized Comparative Information We have previously audited Independent School District No. 535’s 2013 financial statements of the governmental activities, each major fund, and the aggregate remaining fund information, and we expressed unmodified audit opinions on those audited financial statements in our report dated October 28, 2013. In our opinion, the summarized comparative information presented herein as of and for the year ended June 30, 2013 is consistent, in all material respects, with the audited financial statements from which it has been derived. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and the schedule of funding progress for postemployment benefit plan, as listed in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Independent School District No. 535’s basic financial statements. The supplementary information section and the Uniform Financial Accounting and Reporting Standards Compliance Table are presented for purposes of additional analysis and are not a required part of the basic financial statements. The schedule of expenditures of federal awards, as required by the U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, is also presented for purposes of additional analysis and is not a required part of the basic financial statements. The supplementary information section, the Uniform Financial Accounting and Reporting Standards Compliance Table, and the schedule of expenditures of federal awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America.

Board of Education Independent School District No. 535

(4)

Other Information (Continued)

In our opinion, the supplementary information section, the Uniform Financial Accounting and Reporting Standards Compliance Table, and the schedule of expenditures of federal awards are fairly stated, in all material respects, in relation to the basic financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated October 29, 2014, on our consideration of Independent School District No. 535’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the result of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Independent School District No. 535’s internal control over financial reporting and compliance.

CliftonLarsonAllen LLP Austin, Minnesota October 29, 2014

(This page intentionally left blank)

REQUIRED SUPPLEMENTARY INFORMATION

(This page intentionally left blank)

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(5)

This section of Independent School District No. 535's annual financial report presents our discussion and analysis of the District's financial performance during the fiscal year that ended on June 30, 2014. Please read it in conjunction with the District's financial statements, which immediately follows this section. FINANCIAL HIGHLIGHTS Key financial highlights for fiscal year 2013-2014 include the following: Total General Fund revenues were $168,227,860 and total General Fund expenditures were

$173,993,442 for the fiscal year ended June 30, 2014. Total revenues and expenditures for all governmental funds combined were $201,115,412 and $220,212,817 respectively.

The total fund balance in the General Fund decreased by $5,129,942 to $35,581,307. The Unassigned fund balance in the General Fund decreased by $6,208,169 to $23,363,880. Total General Fund revenues were 1.20% less than the final budget, and total General Fund expenditures were 3.92% less than the final budget. The District spent less than budgeted in several areas, with the largest savings in the area of contracted services followed by capital expenditures and supplies.

The total fund balance in the Food Services fund decreased by $495,090 to $3,480,212, with

revenue of $7,900,782 and expenditures of $8,402,198. The Food Service budget projected that expenditures would exceed revenue by approximately $1,218,229. The District spent less than the amount budgeted for food, and some replacement equipment purchased did not arrive until after June 30, 2014, and will therefore be part of the 2014-2015 expenditures..

Community Service programs offered by the District generated revenue of $9,868,546 and

expenditures of $9,535,890 for the fiscal year. The total fund balance in the Community Services fund is $1,240,396. The Community Service fund budget projected that revenue would exceed expenditures by approximately $100,053. Revenue was greater than budgeted by $243,022, primarily in the area of fees and tuition for programs and services offered. Expenditures for programs offered were $10,419 greater than budgeted.

The District spent $17,433,282 on facility construction and deferred maintenance projects during the fiscal year. Of that amount, $3,886,219 was spent to begin construction of building additions at six elementary schools to provide space necessary to implement all-day every-day kindergarten district wide beginning in 2014-2015 and $12,200,948 was spent on major maintenance projects as several district facilities. The major cost of those projects was primarily HVAC system replacement at three elementary schools.

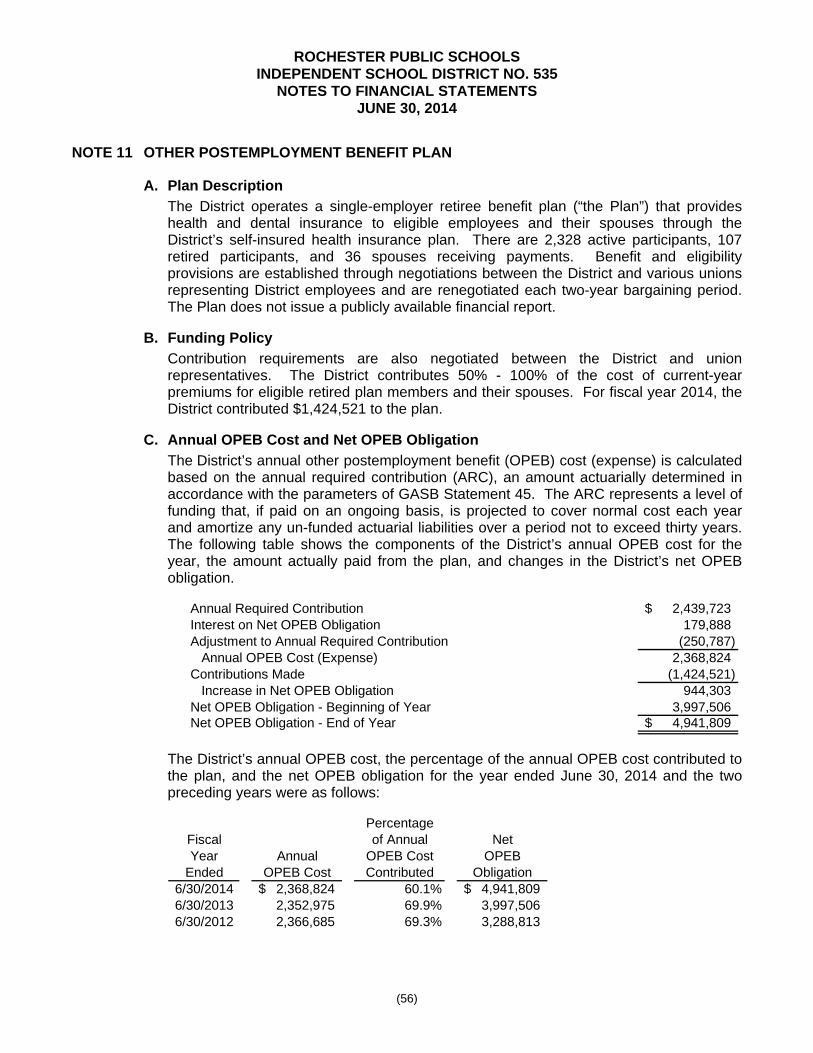

The long-term liability for compensated absences amounts to $13,557,628 at June 30, 2014. This is an increase of $81,250. The long-term liability for other postemployment benefits is $4,941,809 at June 30, 2014. This is an increase of $944,303. The District has established a committed fund balance to begin to fund the postemployment obligation. The fund balance amount is equal to the liability.

The District has general obligation bonded debt principal outstanding in the amount of $84,475,000

and certificates of participation payable principal outstanding in the amount of $28,790,000 as of June 30, 2014. This is a combined decrease of $1,955,000 from the previous fiscal year end, due to the issuance of certificates of participation offsetting most of repayment of principal for the year.

Net position of governmental activities decreased by $1,924,501 or 1.52 percent to $124,530,163.

The total expense of governmental activities was $202,933,457. Program revenues totaled $70,746,537 and general revenues totaled $130,262,419.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(6)

OVERVIEW OF THE FINANCIAL STATEMENTS

The financial section of the annual report consists of four parts - Independent Auditors’ Report, required supplementary information which includes the management's discussion and analysis (this section), the basic financial statements, and single audit and other required reports. The basic financial statements include two kinds of statements that present different views of the District:

The first two statements are district-wide financial statements that provide both short-term and long-term information about the District's overall financial status.

The remaining statements are fund financial statements that focus on individual parts of the District, reporting the District's operations in more detail than the district-wide statements.

The governmental funds statements tell how basic services such as regular and special education were financed in the short term as well as what remains for future spending.

The proprietary funds statements offer short-term and long-term financial information about the activities the School District operates in a manner similar to businesses.

DISTRICT-WIDE STATEMENTS

The District-wide statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The statement of net position includes all of the District's assets, deferred outflows of resources, liabilities, and deferred inflows of resources. All of the current year's revenues and expenses are accounted for in the statement of activities regardless of when cash is received or paid. The two district-wide statements report the District's net position and how they have changed. Net position, the difference between the District's assets and deferred outflows of resources and liabilities and deferred inflows of resources, is one way to measure the District's financial health or position.

Over time, increases or decreases in the District's net position are an indicator of whether its financial position is improving or deteriorating, respectively.

To assess the overall health of the District, you need to consider additional non-financial factors such as changes in the District's property tax base and the condition of school buildings and other facilities.

In the district-wide financial statements the District's activities are shown as Governmental activities:

Governmental activities - Most of the District's basic services are included here, such as regular and special education, transportation, administration, food services and community education. Property taxes and state aids finance most of these activities.

FUND FINANCIAL STATEMENTS

The fund financial statements provide more detailed information about the District's funds - focusing on its most significant or "major" funds - not the District as a whole. Funds are accounting devices the District uses to keep track of specific sources of funding and spending on particular programs:

Some funds are required by State law and by bond covenants.

The District establishes other funds to control and manage money for particular purposes.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(7)

FUND FINANCIAL STATEMENTS (CONTINUED)

The District has two kinds of funds:

Governmental funds - Most of the District's basic services are included in governmental funds, which generally focus on (1) how cash and other financial assets that can readily be converted to cash flow in and out and (2) the balances left at year-end that are available for spending. Consequently, the governmental funds statements provide a detailed short-term view that helps to determine whether there are more or fewer financial resources that can be spent in the near future to finance the District's programs. Because this information does not encompass the additional long-term focus of the district-wide statements, we provide additional information at the bottom of the governmental funds statements that explain the relationship (or differences) between them.

Proprietary funds – Services for which the District charges a fee are generally reported in proprietary funds. Proprietary funds are reported in the same way as the district-wide statements. The District’s sole Proprietary fund is an internal service fund. o The District uses internal service funds to report activities that provide supplies and services for

the District’s other programs and activities. The District currently uses internal service funds for the Health and Dental Care self-insurance program and the Workers’ Compensation self-insurance program.

FINANCIAL ANALYSIS OF THE DISTRICT AS A WHOLE

Net position. The District's combined net position from Governmental activities was $124,530,163 on June 30, 2014. (See Table A-1) This represents a decrease of 1.5% in net position. Total assets increased by approximately $9.2 million or 2.9%. Current and other assets increased by approximately $1.0 million or 0.7%. Capital and non-current assets increased by $8.2 million or 4.5% due to the completion and capitalization of facility major maintenance and renovation projects. Total liabilities decreased by approximately $0.3 million or 0.2% with current liabilities increasing by $17.4 million and long-term liabilities decreasing by $17.7 million primarily due to refunding and planned retirement of bonds issued in 2004, on February 1, 2015.

Percentage2014 2013 Change

Current and Other Assets 141,421,410$ 140,415,179$ 0.7%Capital and Non-Current Assets 188,782,971 180,587,554 4.5%

Total Assets 330,204,381 321,002,733 2.9%

Deferred Outflows of Resources 1,214,574 1,326,871 -8.5%

Current Liabilities 59,725,896 42,319,474 41.1%Long Term Liabilities 112,209,716 129,899,824 -13.6%

Total Liabilities 171,935,612 172,219,298 -0.2%

Deferred Inflows of Resources 34,953,180 23,655,642 47.8%

Net PositionNet Investment in Capital Assets 91,608,827 88,269,979 3.8%Restricted 16,316,996 14,485,446 12.6%Unrestricted 16,604,340 23,699,239 -29.9%

Total Net Position 124,530,163$ 126,454,664$ -1.5%

Governmental Activities

Table A-1The District's Net Position

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(8)

FINANCIAL ANALYSIS OF THE DISTRICT AS A WHOLE (CONTINUED)

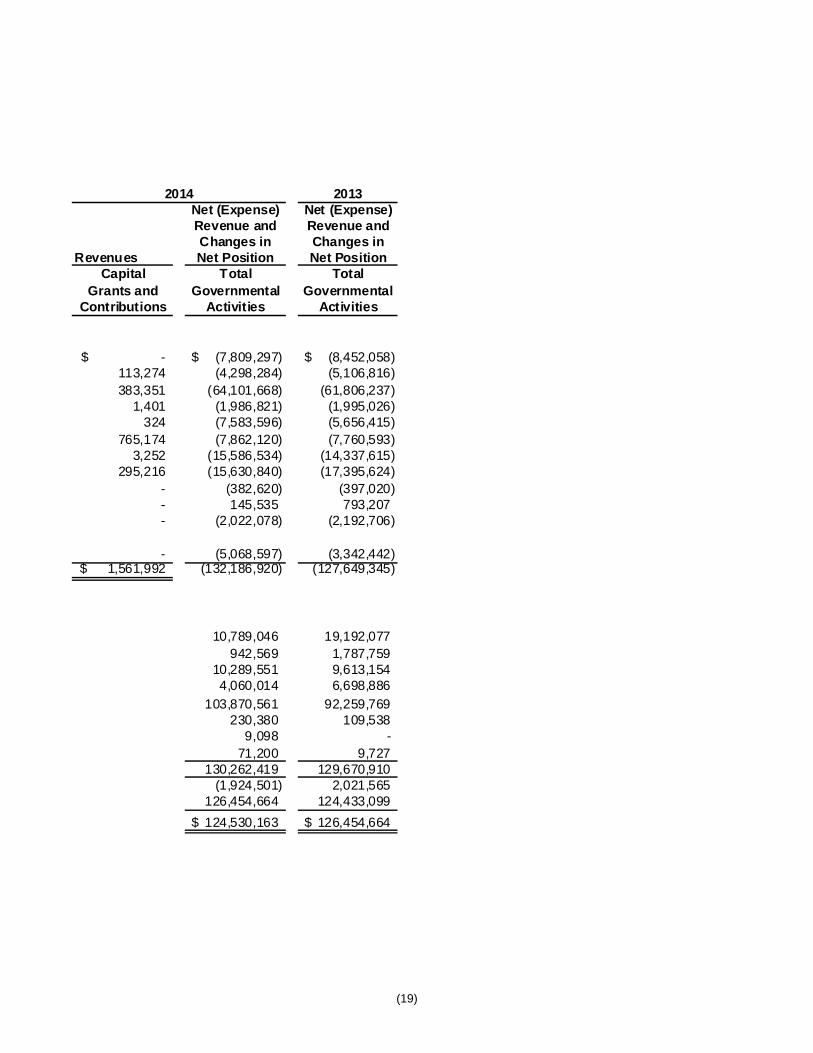

Changes in net position. The District's total revenues were $201,008,956 for the year ended June 30, 2014. Property taxes and state formula aid accounted for 64.6% of total revenue for the year (See Figure A-1). Another 35.2% came from program revenues. Less than 0.2% comes from investment earnings and other general revenues. The total cost of all programs and services was $202,933,457. The District's expenses are predominantly related to educating and caring for students, approximately 76% (See Figure A-2). The purely administrative activities of the District accounted for just 4% of total costs. Total expenses surpassed revenues, decreasing net position by $1,924,501 from the previous year.

Total %2014 2013 Change

RevenuesProgram Revenues Charges for Services 10,660,264$ 9,941,886$ 7.23% Operating Grants and Contributions 58,524,281 54,545,447 7.29% Capital Grants and Contributions 1,561,992 1,434,165 8.91%General Revenues Property Taxes 26,081,180 37,291,876 -30.06% Unrestricted State Aid 103,870,561 92,259,769 12.58% Investment Earnings 230,380 109,538 110.32% Other 80,298 9,727 725.52%

Total Revenues 201,008,956 195,592,408

ExpensesAdministration 7,889,479 8,561,090 -7.84%District Support Services 4,492,281 5,624,783 -20.13%Regular Instruction 88,780,739 85,787,088 3.49%Vocational Education Instruction 2,203,224 2,187,284 0.73%Special Education Instruction 31,349,878 27,941,248 12.20%Instructional Support Services 10,954,224 8,481,579 29.15%Pupil Support Services 16,758,849 15,385,808 8.92%Sites and Buildings 17,264,367 18,929,127 -8.79%Fiscal and Other Fixed Cost Programs 382,620 397,020 -3.63%Food Service 7,744,624 6,936,079 11.66%Community Service 10,044,575 9,941,512 1.04%Interest and Fiscal Charges on Long-Term Liabilities 5,068,597 3,398,225 49.15% Total Expenses 202,933,457 193,570,843 4.84%

Increase (Decrease) in Net Position (1,924,501) 2,021,565

Beginning Net Position 126,454,664 124,433,099 Ending Net Position 124,530,163$ 126,454,664$

Governmental Activities for the fiscal year ended June 30,

Table A-2Change in Net Position

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(9)

FINANCIAL ANALYSIS OF THE DISTRICT AS A WHOLE (CONTINUED)

Figure A-1 Rochester Public Schools

Revenues by Category

Charges for Services5%

Operating and Capital Grants30%

Property Taxes13%

Unrestricted State Aid52%

All other0%

Figure A-1 Sources of District's Revenues for Fiscal 2014

Figure A-2 Rochester Public Schools

Expenses by Category

Administration4%

Instruction-Related60%

Student Support Services

16%

Food & Comm Serv9%

Maintenance8%

Other3%

Figure A-2 District Expenses for Fiscal 2014

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(10)

FINANCIAL ANALYSIS OF THE DISTRICT AS A WHOLE (CONTINUED)

The cost of all governmental activities was $202,933,457 which is an increase of $9,362,614 or 4.8% over the previous year. Some of the cost was paid by the users of the District's programs ($10,660,264). The federal and state governments subsidized certain programs with grants and contributions

($60,086,273). Most of the District's costs ($132,186,920), however, were paid for by District taxpayers and the

taxpayers of the State of Minnesota. The net expense of governmental activities in excess of program revenue was paid for with

$26,081,180 in property taxes, $103,870,561 of state aid based on the statewide education aid formula, and $310,678 in investment earnings and other general revenues.

Percentage Percentage

2014 2013 Change 2014 2013 Change

Administration 7,889,479$ 8,561,090$ -7.8% 7,809,297$ 8,452,058$ -7.6%District Support Services 4,492,281 5,624,783 -20.1% 4,298,284 5,106,816 -15.8%Regular Instruction 88,780,739 85,787,088 3.5% 64,101,668 61,806,237 3.7%Vocational Education Instruction 2,203,224 2,187,284 0.7% 1,986,821 1,995,026 -0.4%Special Education Instruction 31,349,878 27,941,248 12.2% 7,583,596 5,656,415 34.1%Instructional Support Services 10,954,224 8,481,579 29.2% 7,862,120 7,760,593 1.3%Pupil Support Services 16,758,849 15,385,808 8.9% 15,586,534 14,337,615 8.7%Sites and Buildings 17,264,367 18,929,127 -8.8% 15,630,840 17,395,624 -10.1%Fiscal and Other Fixed Cost Programs 382,620 397,020 -3.6% 382,620 397,020 -3.6%Food Service 7,744,624 6,936,079 11.7% (145,535) (793,207) -81.7%Community Service 10,044,575 9,941,512 1.0% 2,022,078 2,192,706 -7.8%Interest and Fiscal Charges on

Long-Term Liabilities 5,068,597 3,398,225 49.2% 5,068,597 3,342,442 51.6%

Total 202,933,457$ 193,570,843$ 4.8% 132,186,920$ 127,649,345$ 3.6%

Total Cost of Services Net Cost of Services

Table A-3Change in Net Position

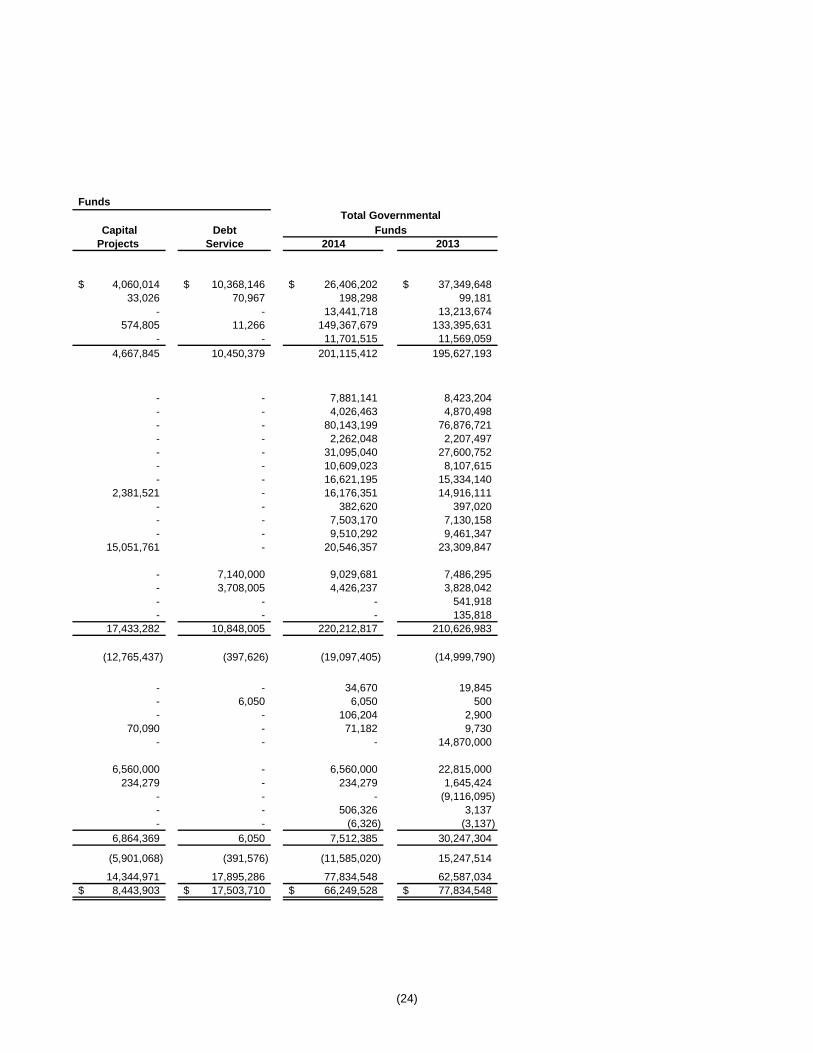

FINANCIAL ANALYSIS OF THE DISTRICT'S FUNDS The financial performance of the District as a whole is reflected in its governmental funds as well. As the District completed the year its governmental funds reported a combined fund balance of $66,249,528, which is a decrease of $11,585,020 from the prior year ending fund balance. Revenues for the District's governmental funds were $201,115,412, total expenditures were $220,212,817, and other sources and uses provided $7,512,385. The District issued Certificates of Participation, Series 2014A to finance the construction of additional kindergarten classroom space and remodeling of the alternative learning center. The District used proceeds of the newly issued debt in addition to previously issued debt to fund projects at ten school facilities. The Capital Projects fund balance decrease totaled $5,901,068. The fund balance of the General fund decreased by $5,129,942, which was also a planned and approved utilization of fund balance by the School Board. The operations of the other governmental funds: Food Service, Community Service, and Debt Service resulted in a decrease in fund balance of $554,010.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(11)

GENERAL FUND

The General Fund includes the primary operations of the District in providing educational services to students from early childhood through grade 12 including pupil transportation activities and operating capital expenditures. The following table shows that the number of students has increased slightly over the last four years, increasing by 476 students since 2010. Membership decreased slightly in 2012, 3 students less than in 2011, but increased by 224 students or 1.4% in 2013, and 215 students or 1.3% in 2014.

Table A-4 Five-Year Enrollment Trend

Average Daily Membership (ADM)

Grade 2010 2011 2012 2013 2014ECSE 126 147 172 183 182 Kdgt. 1,273 1,263 1,218 1,294 1,366 1-3 3,774 3,867 3,944 3,888 3,972 4-6 3,497 3,486 3,540 3,663 3,746 7-12 7,241 7,188 7,074 7,144 7,121

Total K-12 ADM 15,911 15,951 15,948 16,172 16,387 ADM Change N/A 40 (3) 224 215 Percent Change N/A 0.3% 0.0% 1.4% 1.3%

District enrollment peaked in 2003 at 16,222 students in average daily membership, declined to 15,689 in 2006, and has been generally increasing since then to 16,387 in 2014. The enrollment growth is occurring at the elementary grade levels, with enrollment holding fairly steady at the secondary grade levels. District projections indicate that enrollments will be steady with slight growth for the next five years. The District did realize higher than projected enrollment for 2013-2014. The previous decline in enrollment was largely due to new charter schools opening within the District boundaries. The overall population of the School District continues to increase. The following schedule presents a summary of General Fund Revenues.

Table A-5 General Fund Revenues

June 30, June 30, Increase2014 2013 (Decrease) Percent

Local SourcesProperty Taxes 11,020,964$ 19,247,115$ (8,226,151)$ -42.7%Earnings on Investments 81,317 21,066 60,251 286.0%Other 5,676,350 5,431,644 244,706 4.5%

State Sources 144,472,743 129,577,320 14,895,423 11.5%Federal Sources 6,976,486 7,138,858 (162,372) -2.3%

Total General Fund Revenue 168,227,860$ 161,416,003$ 6,811,857$ 4.2%

Fund

ChangeYear Ended

Total General Fund revenue of $168,227,860 increased by $6,811,857 or 4.2% compared to the previous year. Basic general education revenue is determined by the state per student funding formula and consists of state aid revenue. Other state-authorized revenue including excess levy referendum and operating capital involve an equalized mix of property tax and state aid revenue. The mix of property tax and state aid can change significantly from year to year without any net change of revenue.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(12)

GENERAL FUND (CONTINUED)

State sources increased by $14,895,423 or 11.5% due to legislative increases in per pupil funding formulas and state repayment of a shift in recognition of property tax and state aid which initially impacted the fiscal year ended June 30, 2012. Local sources decreased by $7,921,194 primarily as a result of the offsetting recognition of the shift with state aid. Federal sources decreased by $162,372 or 2.3%. The following schedule presents a summary of General Fund expenditures.

Table A-6 General Fund Expenditures

Amount of PercentJune 30, June 30, Increase Increase

2014 2013 (Decrease) (Decrease)Salaries 101,652,339$ 95,433,361$ 6,218,978$ 6.5%Employee Benefits 37,551,921 34,024,593 3,527,328 10.4%Purchased Services 20,268,903 20,045,453 223,450 1.1%Supplies and Materials 7,102,415 6,219,583 882,832 14.2%Capital Expenditures 4,569,970 8,480,313 (3,910,343) -46.1%Debt Service Expenditures 2,607,913 1,834,097 773,816 42.2%Other Expenditures 239,981 920,179 (680,198) -73.9% Total Expenditures 173,993,442$ 166,957,579$ 7,035,863$ 4.2%

Year Ended

The total General Fund expenditure of $173,993,442 was an increase of $7,035,863 or 4.2% over the prior year. Salaries and benefits increased by $9,746,306 combined. Salaries increased 6.5% and employee benefits increased by 10.4%. The District continues to look at cost containment measures to minimize the effect of rising health insurance premiums on the costs of the district’s employee compensation packages. Bargaining unit contracts now contain language that caps the District contribution toward health insurance premiums. Capital expenditure costs decreased by $3,910,343 or 46.1%, from the prior year. The capital expenditures for fiscal year ended June 30, 2013 were higher than normal primarily due to the purchase of student-use technology and the acquisition of a facility for maintenance and other operations. The remaining categories of purchased services, supplies and materials, debt service, and other expenditures net to an overall cost increase of $1,199,900 or 4.1% from 2013 to 2014. In 2013-2014, General Fund expenditures exceeded revenue by $5,765,582 which was $5,066,688 better than budget. Revenue received was $2,036,717 less than budgeted and expenditures were $7,103,405 less than budgeted. State special education revenue was the largest line-item lower than budget by $1,410,076. The unassigned fund balance decreased from $29,572,049 at June 30, 2013 to $23,363,880 at June 30, 2014, a decrease of $6,208,169. This was a planned utilization of fund balance to maintain opportunities for students. Expenditures were less than budgeted in several areas, including salaries, contracted services, supplies, and capital expenditures. Additional discussion of budget variances is provided in the next section – General Fund Budgetary Highlights.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(13)

GENERAL FUND (CONTINUED)

General Fund Budgetary Highlights

Over the course of the year, the District revised the annual operating budget. The budget amendments fall into two categories:

Implementing budgets for specially funded projects, which include both federal and state grants, reinstating prior year designated carryover reserves, and changes in enrollment estimates.

Increases in appropriations for significant unbudgeted costs or revenues.

The District's final budget for the general fund anticipated a net reduction in fund balance of $10,241,788 while the actual results for the year show a reduction of $5,129,942.

In our analysis of significant variances between original and final budget amounts and between final budget amounts and actual results in the General Fund, there are no variances in revenues that will have a significant effect on future services or liquidity. The main reasons for the difference between the original budget and the final budget are for additional grants awarded to the District after the original budget was adopted and revised enrollment estimates. The District historically has used the October 1 student enrollment as the basis for the final budget. The largest variance between the final budget and actual revenue is in State Sources where revenue was less than the budget amount by $1,442,999. The District earned less revenue from the Special Education funding formulas than was budgeted.

On the expenditure side of the budget, the major reasons for the variance between original and final budget amounts (approximately $8.1 million) were the addition of funding for capital projects (approximately $3.1 million); certain restricted, committed or assigned fund balances from the previous fiscal year (approximately $4.4 million); and additional grants awarded to the District after the original budget was approved.

Taking a look at the $7.1 million difference between the final expenditure budget and actual expenditures, the unspent supply budgets were approximately $1.8 million. Of this amount, approximately $1.4 million was set aside in a committed fund balance to be carried over and added to the site supply budgets in the following year. Several contracted services budgets were not fully utilized (approximately $2.7 million) because the services were not utilized this year. Of the $2.7 million, approximately $515,000 was in the area of Staff development and will get carried over and added to the budget in 2014-2015, approximately $328,000 was for student transportation, approximately $360,000 was for utilities, and $331,000 was for special education services. The remaining savings was in a variety of budgets for consulting and contracted services. Finally, there were unspent capital expenditure allocations of approximately $2.2 million. These budgets were allocated for specific projects and the unspent dollars were set aside in restricted and committed fund balances and will be included in the 2014-2015 budget for completion of these projects. Some of these variances will have a positive effect on future budgets by allowing for ongoing budget reductions in certain areas.

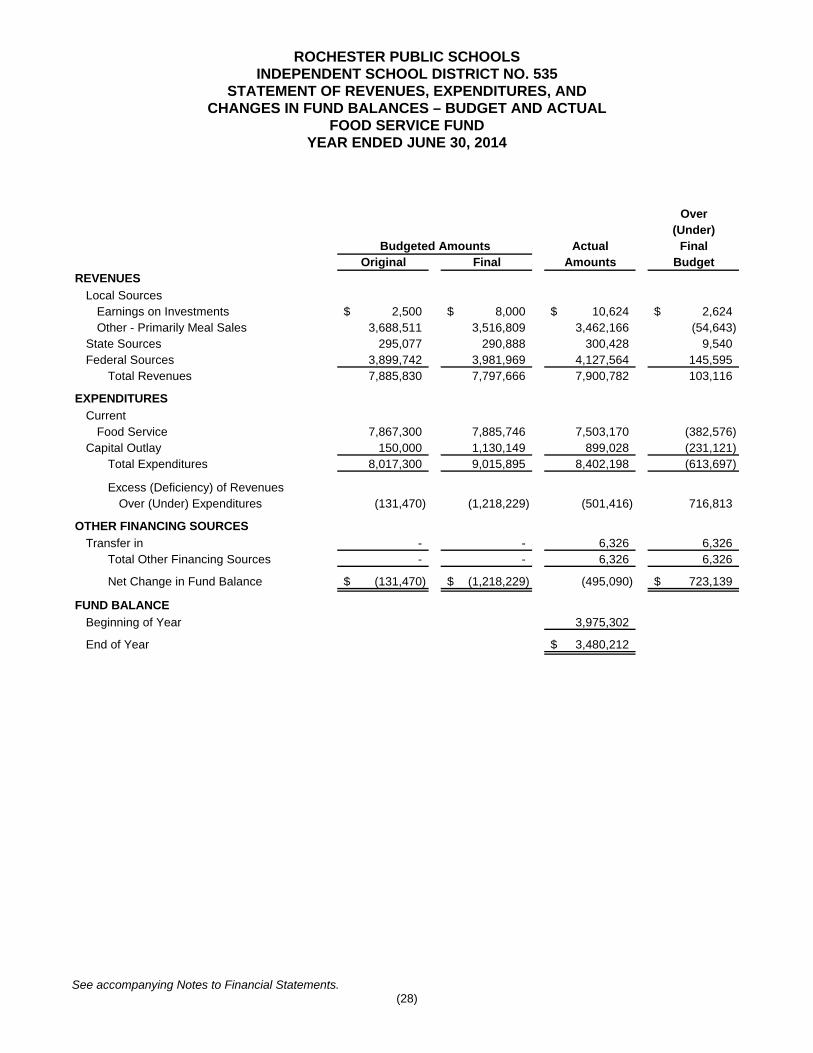

FOOD SERVICE FUND The Food Service Fund accounts for the activities related to providing nutrition services to the K-12 academic program. The fund operates on the principle of revenues exceeding expenditures on day-to-day operations so that the excess can be used to systematically replace and upgrade kitchen equipment around the district. By operating in this manner, the Student Nutrition Services program is self-contained and does not pull resources away from direct K-12 instruction. The District served 1,563,207 lunches and 476,224 breakfasts to students and staff, in addition to a la carte sales during the 2013-2014 school year.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(14)

FOOD SERVICE FUND (CONTINUED)

The fund balance decreased by $495,090 in 2013-2014. This is $723,139 better than budget. Food Service Fund revenue for 2013-2014 totaled $7,900,782 which is an increase of $167,324 or 2.2% from 2012-2013. Food Service Fund Expenditures for 2013-2014 totaled $8,402,198, an increase of $1,081,121 or 14.8% from 2012-2013. Salaries and benefits increased by $153,008; the cost of supplies, food and milk increased by $196,181; and expenditures for equipment increased by $708,109 in 2013-2014. Food and milk costs were impacted by the continued implementation of the requirements of the Healthy Hunger Free Kids Act. The increase in equipment expenditures was due to planned replacement of aging equipment and equipment needs for a new alternative learning center facility. COMMUNITY SERVICE FUND

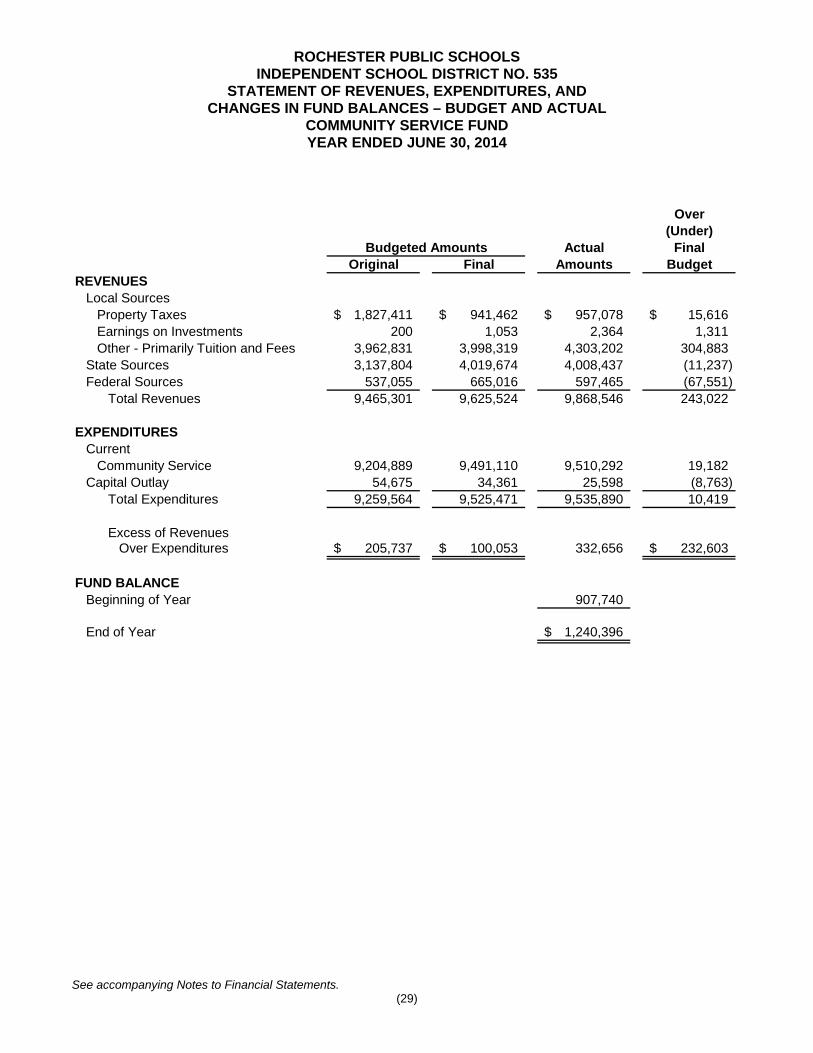

The Community Service Fund accounts for the activities related to providing education services for Pre-Kindergarten and Post-Grade 12 students. The fund operates on a principle of breaking even on a year-to-year basis so that it does not pull resources away from K-12 instruction. The fund balance increased by $332,656 in 2013-2014. Community Service Fund Revenues for 2013-2014 totaled $9,868,546. This was an increase of $376,234 or 4.0% from 2012-2013. Community Service Fund Expenditures for 2013-2014 totaled $9,535,890. This was an increase of $53,798 or 0.6% from 2012-2013. The entire fund balance is restricted to be used for specific purposes based on state requirements. The minimal change fund balance from the previous year reflects the stability of the programs provided in this fund. CAPITAL PROJECTS FUND

The Capital Projects Fund accounts for the costs of school construction, addition and renovation projects. Bond proceeds are deposited in the Capital Projects Fund and are then drawn down as the payments are made for work completed on the various building projects. The proceeds of bonds can only be used for the purpose for which the bonds were issued. In 2013-2014 the District received property tax revenue in the amount of $4,060,014, state aid in the amount of $574,805, and had interest earnings on investments and other sources of $33,026 to fund deferred maintenance projects. In addition, the District had other financing sources from the issuance of certificates of participation, bond premiums, and utility rebates totaling 6,864,369 to fund the construction of building additions and capital improvements. The District expended $17,433,282 on deferred maintenance projects and building additions at several sites as planned. The fund balance decreased by $5,901,068 in 2013-2014 to $8,443,903 at June 30, 2014. Several projects are in process at the end of the fiscal year. At such time that the district has completed all construction projects in process, the fund balance of this fund should end up at $0 as long as no further construction or facility renovation is approved. DEBT SERVICE FUND

The Debt Service Fund exists to service the principal and interest payments on long-term debt issued by the district to construct school facilities or acquire school equipment. Annual levies will provide revenue at a rate of 105% of pending debt service payments for a fiscal year. This rate is specified in statute to ensure that principal and interest payments can be made as scheduled even if there are late property tax payments or delinquencies that may arise.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(15)

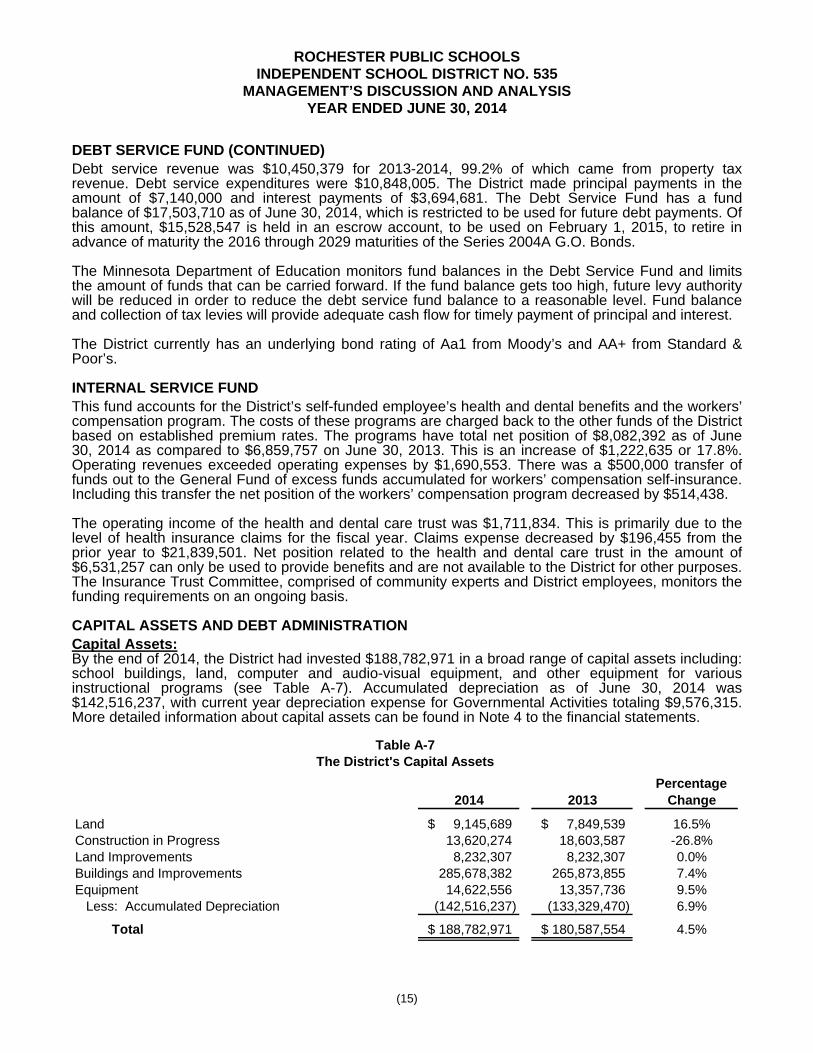

DEBT SERVICE FUND (CONTINUED) Debt service revenue was $10,450,379 for 2013-2014, 99.2% of which came from property tax revenue. Debt service expenditures were $10,848,005. The District made principal payments in the amount of $7,140,000 and interest payments of $3,694,681. The Debt Service Fund has a fund balance of $17,503,710 as of June 30, 2014, which is restricted to be used for future debt payments. Of this amount, $15,528,547 is held in an escrow account, to be used on February 1, 2015, to retire in advance of maturity the 2016 through 2029 maturities of the Series 2004A G.O. Bonds. The Minnesota Department of Education monitors fund balances in the Debt Service Fund and limits the amount of funds that can be carried forward. If the fund balance gets too high, future levy authority will be reduced in order to reduce the debt service fund balance to a reasonable level. Fund balance and collection of tax levies will provide adequate cash flow for timely payment of principal and interest. The District currently has an underlying bond rating of Aa1 from Moody’s and AA+ from Standard & Poor’s. INTERNAL SERVICE FUND This fund accounts for the District’s self-funded employee’s health and dental benefits and the workers’ compensation program. The costs of these programs are charged back to the other funds of the District based on established premium rates. The programs have total net position of $8,082,392 as of June 30, 2014 as compared to $6,859,757 on June 30, 2013. This is an increase of $1,222,635 or 17.8%. Operating revenues exceeded operating expenses by $1,690,553. There was a $500,000 transfer of funds out to the General Fund of excess funds accumulated for workers’ compensation self-insurance. Including this transfer the net position of the workers’ compensation program decreased by $514,438. The operating income of the health and dental care trust was $1,711,834. This is primarily due to the level of health insurance claims for the fiscal year. Claims expense decreased by $196,455 from the prior year to $21,839,501. Net position related to the health and dental care trust in the amount of $6,531,257 can only be used to provide benefits and are not available to the District for other purposes. The Insurance Trust Committee, comprised of community experts and District employees, monitors the funding requirements on an ongoing basis. CAPITAL ASSETS AND DEBT ADMINISTRATION Capital Assets: By the end of 2014, the District had invested $188,782,971 in a broad range of capital assets including: school buildings, land, computer and audio-visual equipment, and other equipment for various instructional programs (see Table A-7). Accumulated depreciation as of June 30, 2014 was $142,516,237, with current year depreciation expense for Governmental Activities totaling $9,576,315. More detailed information about capital assets can be found in Note 4 to the financial statements.

Percentage2014 2013 Change

Land 9,145,689$ 7,849,539$ 16.5%Construction in Progress 13,620,274 18,603,587 -26.8%Land Improvements 8,232,307 8,232,307 0.0%Buildings and Improvements 285,678,382 265,873,855 7.4%Equipment 14,622,556 13,357,736 9.5%

Less: Accumulated Depreciation (142,516,237) (133,329,470) 6.9%

Total 188,782,971$ 180,587,554$ 4.5%

Table A-7The District's Capital Assets

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

MANAGEMENT’S DISCUSSION AND ANALYSIS YEAR ENDED JUNE 30, 2014

(16)

CAPITAL ASSETS AND DEBT ADMINISTRATION (CONTINUED)

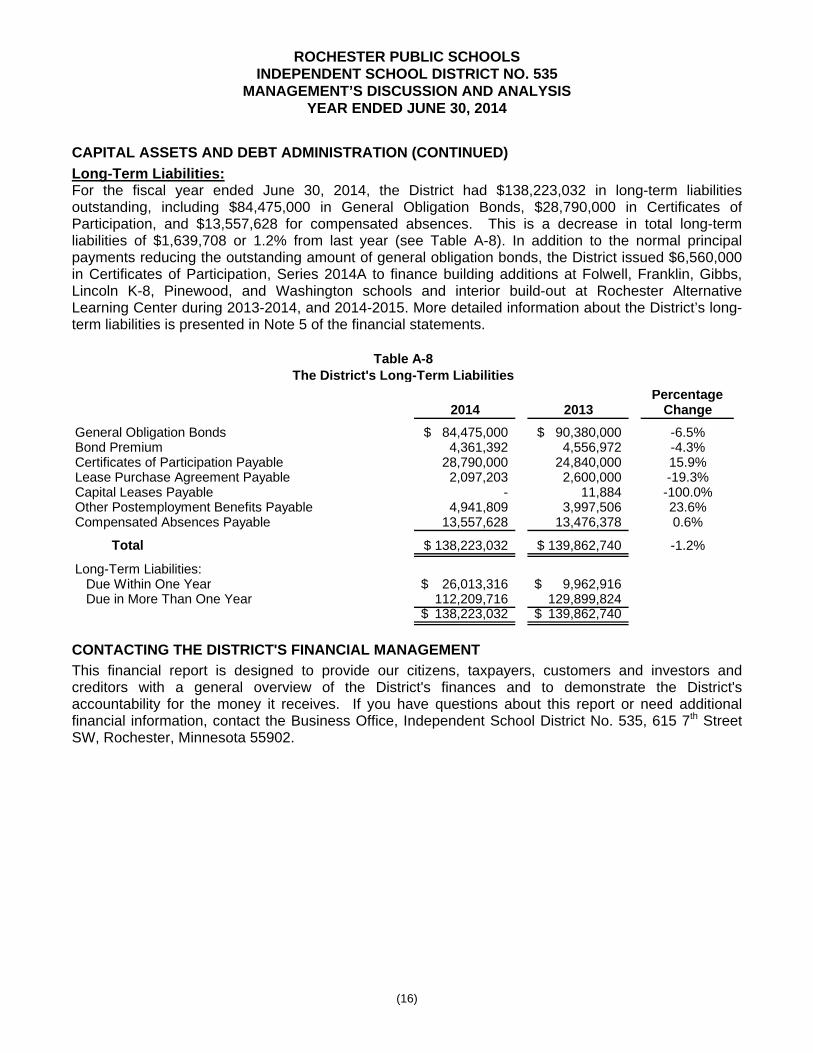

Long-Term Liabilities: For the fiscal year ended June 30, 2014, the District had $138,223,032 in long-term liabilities outstanding, including $84,475,000 in General Obligation Bonds, $28,790,000 in Certificates of Participation, and $13,557,628 for compensated absences. This is a decrease in total long-term liabilities of $1,639,708 or 1.2% from last year (see Table A-8). In addition to the normal principal payments reducing the outstanding amount of general obligation bonds, the District issued $6,560,000 in Certificates of Participation, Series 2014A to finance building additions at Folwell, Franklin, Gibbs, Lincoln K-8, Pinewood, and Washington schools and interior build-out at Rochester Alternative Learning Center during 2013-2014, and 2014-2015. More detailed information about the District’s long-term liabilities is presented in Note 5 of the financial statements.

Percentage2014 2013 Change

General Obligation Bonds 84,475,000$ 90,380,000$ -6.5%Bond Premium 4,361,392 4,556,972 -4.3%Certificates of Participation Payable 28,790,000 24,840,000 15.9%Lease Purchase Agreement Payable 2,097,203 2,600,000 -19.3%Capital Leases Payable - 11,884 -100.0%Other Postemployment Benefits Payable 4,941,809 3,997,506 23.6%Compensated Absences Payable 13,557,628 13,476,378 0.6%

Total 138,223,032$ 139,862,740$ -1.2%

Long-Term Liabilities: Due Within One Year 26,013,316$ 9,962,916$ Due in More Than One Year 112,209,716 129,899,824

138,223,032$ 139,862,740$

Table A-8The District's Long-Term Liabilities

CONTACTING THE DISTRICT'S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers and investors and creditors with a general overview of the District's finances and to demonstrate the District's accountability for the money it receives. If you have questions about this report or need additional financial information, contact the Business Office, Independent School District No. 535, 615 7th Street SW, Rochester, Minnesota 55902.

BASIC FINANCIAL STATEMENTS

(This page intentionally left blank)

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF NET POSITION JUNE 30, 2014

(WITH SUMMARIZED FINANCIAL INFORMATION AS OF JUNE 30, 2013)

See accompanying Notes to Financial Statements. (17)

Governmental Activities2014 2013

ASSETSCash and Investments 79,075,759$ 72,440,765$ Cash and Investments Held by Trustee 22,145,973 21,753,482 Receivables

Property Taxes 18,507,744 19,175,579 Other Governments 20,561,163 24,915,286 Other 786,556 749,914

Prepaid Items 262,444 261,999 Inventories 81,771 106,364 Bond Issuance Costs, Net - 1,011,790 Capital Assets

Land and Construction in Progress 22,765,963 26,453,126 Other Capital Assets, Net of Depreciation 166,017,008 154,134,428

Total Assets 330,204,381 321,002,733

DEFERRED OUTFLOWS OF RESOURCESLoss on Bond Refunding 1,214,574 1,326,871

Total Deferred Outflows of Resources 1,214,574 1,326,871

LIABILITIESSalaries Payable 17,255,946 16,292,057 Accounts and Contracts Payable 11,165,012 10,138,952 Accrued Interest 1,765,870 1,817,738 Due to Other Governmental Units 94,787 74,314 Claims Payable 2,465,945 2,887,493 Unearned Revenue 965,020 1,146,004 Long-Term Liabilities

Portion Due Within One Year 26,013,316 9,962,916 Portion Due in More Than One Year 112,209,716 129,899,824

Total Liabilities 171,935,612 172,219,298

DEFERRED INFLOWS OF RESOURCESProperty Taxes 34,953,180 23,655,642

Total Deferred Inflows of Resources 34,953,180 23,655,642

NET POSITIONNet Investment in Capital Assets 91,608,827 88,269,979 Restricted for:

Operating Capital Purposes 660,274 672,695 State-Mandated Restrictions 779,326 917,764 Food Service 3,480,212 3,975,302 Community Service 1,249,705 931,558 Debt Service 601,739 625,379 Capital Projects - Facilities 2,995,149 2,563,910 Capital Projects - Building Construction 19,334 4,654 Health and Dental Insurance Trust 6,531,257 4,794,184

Unrestricted 16,604,340 23,699,239

Total Net Position 124,530,163$ 126,454,664$

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF ACTIVITIES YEAR ENDED JUNE 30, 2014

(WITH SUMMARIZED FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2013)

See accompanying Notes to Financial Statements. (18)

ProgramOperating

Charges for Grants andFunctions Expenses Services Contributions

Governmental ActivitiesAdministration 7,889,479$ -$ 80,182$ District Support Services 4,492,281 6,773 73,950 Regular Instruction 88,780,739 961,395 23,334,325 Vocational Education Instruction 2,203,224 - 215,002 Special Education Instruction 31,349,878 1,929,349 21,836,609 Instructional Support Services 10,954,224 11,050 2,315,880 Pupil Support Services 16,758,849 216,889 952,174 Sites and Buildings 17,264,367 110,692 1,227,619 Fiscal and Other Fixed Cost Programs 382,620 - - Food Service 7,744,624 3,460,907 4,429,252 Community Service 10,044,575 3,963,209 4,059,288 Interest and Fiscal Charges on

Long-Term Liabilities 5,068,597 - - Total School District 202,933,457$ 10,660,264$ 58,524,281$

General RevenuesProperty Taxes Levied for:

General PurposesCommunity ServiceDebt ServiceCapital Projects

State Aid Not Restricted to Specific PurposesEarnings on InvestmentsGain on Sale of Fixed AssetsMiscellaneous

Total General RevenuesChange in Net Position

Net Position - Beginning

Net Position - Ending

2014

(19)

2013Net (Expense) Net (Expense)Revenue and Revenue andChanges in Changes in

Revenues Net Position Net PositionCapital Total Total

Grants and Governmental GovernmentalContributions Activities Activities

-$ (7,809,297)$ (8,452,058)$ 113,274 (4,298,284) (5,106,816) 383,351 (64,101,668) (61,806,237)

1,401 (1,986,821) (1,995,026) 324 (7,583,596) (5,656,415)

765,174 (7,862,120) (7,760,593) 3,252 (15,586,534) (14,337,615)

295,216 (15,630,840) (17,395,624) - (382,620) (397,020) - 145,535 793,207 - (2,022,078) (2,192,706)

- (5,068,597) (3,342,442) 1,561,992$ (132,186,920) (127,649,345)

10,789,046 19,192,077 942,569 1,787,759

10,289,551 9,613,154 4,060,014 6,698,886

103,870,561 92,259,769 230,380 109,538

9,098 - 71,200 9,727

130,262,419 129,670,910 (1,924,501) 2,021,565

126,454,664 124,433,099

124,530,163$ 126,454,664$

2014

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

BALANCE SHEET GOVERNMENTAL FUNDS

JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION AS OF JUNE 30, 2013)

See accompanying Notes to Financial Statements. (20)

Major

Food Community

General Service Service

ASSETSCash and Investments 41,330,684$ 3,966,987$ 2,361,596$

Cash and Investments Held by Trustee 457,661 - -

Receivables

Current Property Taxes 9,838,280 - 897,297

Delinquent Property Taxes 141,376 - 10,316

Due from Other Minnesota School Districts 36,726 - -

Due from Minnesota Department of Education 15,673,025 7,403 318,162

Due from Federal through Minnesota Department of Education 2,585,668 122,205 163,293

Due from Other Governmental Units 1,596,073 - -

Other Receivables 492,741 3,267 260,409

Prepaid Items 250,825 3,500 2,620

Inventory - 81,771 - Total Assets 72,403,059$ 4,185,133$ 4,013,693$

LIABILITIES, DEFERRED INFLOWS OF RESOURCES,

AND FUND BALANCELiabilities

Salaries Payable 16,143,624$ 437,232$ 639,816$

Accounts and Contracts Payable 1,931,843 65,732 118,459

Due to Other Governmental Units 94,787 - -

Claims Payable 166,634 - -

Unearned Revenue 578,537 201,957 184,526

Total Liabilities 18,915,425 704,921 942,801

Deferred Inflows of Resources

Property Taxes Levied for Subsequent Year 17,778,745 - 1,821,187

Unavailable Revenue - Delinquent Property Taxes 127,582 - 9,309

Total Deferred Inflows of Resources 17,906,327 - 1,830,496

Fund Balance

Nonspendable

Prepaid Items 250,825 3,500 2,620

Inventory - 81,771 -

Restricted

Staff Development 588,464 - -

Health and Safety 65,810 - -

Alternative Facilities - - - Project Funded by Certificates of Participation/Lease Purchase Agreement 419,110 - -

Operating Capital 660,274 - -

Safe Schools - Crime 82,852 - -

Community Education Programs - - 925,919

Early Childhood and Family Education Programs - - 244,504

School Readiness - - 7,628

Adult Basic Education - - 21,296

Bond Refundings - - -

Other Restricted - 3,394,941 38,429

Committed 6,439,449 - -

Assigned 3,710,643 - -

Unassigned 23,363,880 - -

Total Fund Balance 35,581,307 3,480,212 1,240,396

Total Liabilities, Deferred Inflows of Resources,and Fund Balance 72,403,059$ 4,185,133$ 4,013,693$

(21)

Funds Total Governmental

Capital Debt Funds

Projects Service 2014 2013

12,797,580$ 7,439,809$ 67,896,656$ 62,064,070$

6,182,576 15,505,736 22,145,973 21,753,482

2,248,113 5,313,954 18,297,644 18,495,129

- 58,408 210,100 680,450

- - 36,726 42,217

57,481 1,127 16,057,198 21,465,397

- - 2,871,166 2,917,966

- - 1,596,073 489,706

6,597 22,811 785,825 733,582

- - 256,945 239,242

- - 81,771 106,364 21,292,347$ 28,341,845$ 130,236,077$ 128,987,605$

12,511$ -$ 17,233,183$ 16,269,048$

8,268,111 - 10,384,145 9,320,618

- - 94,787 74,314

- - 166,634 172,809

- - 965,020 1,146,004

8,280,622 - 28,843,769 26,982,793

4,567,822 10,785,426 34,953,180 23,655,642

- 52,709 189,600 514,622

4,567,822 10,838,135 35,142,780 24,170,264

- - 256,945 239,242

- - 81,771 106,364

- - 588,464 518,386

- - 65,810 374,552

5,967,999 - 5,967,999 13,445,692 2,475,904 - 2,895,014 1,927,028

- - 660,274 672,695

- - 82,852 24,575

- - 925,919 591,629

- - 244,504 133,773

- - 7,628 41,007

- - 21,296 -

- 15,528,547 15,528,547 15,940,505

- 1,975,163 5,408,533 5,954,789

- - 6,439,449 5,525,527

- - 3,710,643 2,766,735

- - 23,363,880 29,572,049

8,443,903 17,503,710 66,249,528 77,834,548

21,292,347$ 28,341,845$ 130,236,077$ 128,987,605$

(This page intentionally left blank)

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

RECONCILIATION OF THE BALANCE SHEET OF GOVERNMENTAL FUNDS TO THE STATEMENT OF NET POSITION

JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION AS OF JUNE 30, 2013)

See accompanying Notes to Financial Statements. (22)

2014 2013

Total Fund Balance for Governmental Funds 66,249,528$ 77,834,548$

Capital assets used in governmental funds are not financial resources and therefore are not reported in the funds. Those assets consist of:

Land 9,145,689 7,849,539 Construction in Progress 13,620,274 18,603,587 Land Improvements, Net of Accumulated Depreciation 3,299,970 3,660,814 Buildings and Improvements, Net of Accumulated Depreciation 157,298,801 145,966,323 Equipment, Net of Accumulated Depreciation 5,418,237 4,507,291

Some of the District's property taxes will be collected after year-end, but are not available soon enough to pay for the current period's expenditures, and therefore are reported as deferred inflows of resources in the funds. 189,600 514,622

Interest on long-term debt is not accrued in governmental funds, but rather is recognized as an expenditure when due. (1,765,870) (1,817,738)

Bond issuance costs are reported as expenditures in the governmental funds.- 1,011,790

Deferred amounts on refundings are not current financial resources and therefore are not reported in the governmental funds. 1,214,574 1,326,871

Internal service funds are used by management to charge the costs of health and dental insurance services to individual funds. The assets and liabilities of the internal service funds are included in governmental activities in the statement of net position. Internal service fund net position at year-end is: 8,082,392 6,859,757

Long-term liabilities that pertain to governmental funds, including bonds payable, are not due and payable in the current period and therefore are not reported as fund liabilities. All liabilities - both current and long-term - are reported in the statement of net position. Balances at year-end are:

Bonds Payable (84,475,000) (90,380,000) Unamortized Premiums (4,361,392) (4,556,972) Certificates of Participation Payable (28,790,000) (24,840,000) Lease Purchase Agreement Payable (2,097,203) (2,600,000) Capital Leases Payable - (11,884) Compensated Absences Payable (13,557,628) (13,476,378) Other Postemployment Benefits Payable (4,941,809) (3,997,506)

Total Net Position of Governmental Activities 124,530,163$ 126,454,664$

Total net position reported for governmental activities in the statement of net position is different because:

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES GOVERNMENTAL FUNDS

YEAR ENDED JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2013)

See accompanying Notes to Financial Statements. (23)

Major

Food CommunityGeneral Service Service

REVENUESLocal Sources

Property Taxes 11,020,964$ -$ 957,078$ Earnings on Investments 81,317 10,624 2,364 Other 5,676,350 3,462,166 4,303,202

State Sources 144,472,743 300,428 4,008,437 Federal Sources 6,976,486 4,127,564 597,465

Total Revenues 168,227,860 7,900,782 9,868,546

EXPENDITURESCurrent

Administration 7,881,141 - - District Support Services 4,026,463 - - Regular Instruction 80,143,199 - - Vocational Education Instruction 2,262,048 - - Special Education Instruction 31,095,040 - - Instructional Support Services 10,609,023 - - Pupil Support Services 16,621,195 - - Sites and Buildings 13,794,830 - - Fiscal and Other Fixed Cost Programs 382,620 - - Food Service - 7,503,170 - Community Service - - 9,510,292

Capital Outlay 4,569,970 899,028 25,598 Debt Service

Principal 1,889,681 - - Interest and Fiscal Charges 718,232 - - Payment to Refunded Bond Escrow Agent - - - Issuance Costs on Refunding Transactions - - -

Total Expenditures 173,993,442 8,402,198 9,535,890 Excess (Deficiency) of Revenues

Over (Under) Expenditures (5,765,582) (501,416) 332,656

OTHER FINANCING SOURCES (USES)Sale of Equipment Proceeds 34,670 - - Sale of Real Property Proceeds - - - Insurance Recovery Proceeds 106,204 - - Utility Rebates 1,092 - - Sale of Bonds Proceeds - - - Certificates of Participation/Lease

Purchase Agreement Proceeds - - - Premium - - - Payment to Refunded Bond Escrow Agent - - - Transfers In 500,000 6,326 - Transfers Out (6,326) - -

Total Other Financing Sources (Uses) 635,640 6,326 -

Net Change in Fund Balances (5,129,942) (495,090) 332,656

Fund Balances - Beginning 40,711,249 3,975,302 907,740 Fund Balances - Ending 35,581,307$ 3,480,212$ 1,240,396$

(24)

FundsTotal Governmental

Capital Debt FundsProjects Service 2014 2013

4,060,014$ 10,368,146$ 26,406,202$ 37,349,648$ 33,026 70,967 198,298 99,181

- - 13,441,718 13,213,674 574,805 11,266 149,367,679 133,395,631

- - 11,701,515 11,569,059 4,667,845 10,450,379 201,115,412 195,627,193

- - 7,881,141 8,423,204 - - 4,026,463 4,870,498 - - 80,143,199 76,876,721 - - 2,262,048 2,207,497 - - 31,095,040 27,600,752 - - 10,609,023 8,107,615 - - 16,621,195 15,334,140

2,381,521 - 16,176,351 14,916,111 - - 382,620 397,020 - - 7,503,170 7,130,158 - - 9,510,292 9,461,347

15,051,761 - 20,546,357 23,309,847

- 7,140,000 9,029,681 7,486,295 - 3,708,005 4,426,237 3,828,042 - - - 541,918 - - - 135,818

17,433,282 10,848,005 220,212,817 210,626,983

(12,765,437) (397,626) (19,097,405) (14,999,790)

- - 34,670 19,845 - 6,050 6,050 500 - - 106,204 2,900

70,090 - 71,182 9,730 - - - 14,870,000

6,560,000 - 6,560,000 22,815,000 234,279 - 234,279 1,645,424

- - - (9,116,095) - - 506,326 3,137 - - (6,326) (3,137)

6,864,369 6,050 7,512,385 30,247,304

(5,901,068) (391,576) (11,585,020) 15,247,514

14,344,971 17,895,286 77,834,548 62,587,034 8,443,903$ 17,503,710$ 66,249,528$ 77,834,548$

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES

YEAR ENDED JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2013)

See accompanying Notes to Financial Statements. (25)

2014 2013

Net Change in Fund Balance-Total Governmental Funds (11,585,020)$ 15,247,514$

Governmental funds report capital outlays as expenditures. However, in the statement of activities, assets with an initial, individual cost of more than $5,000 for equipment and furnishings and $50,000 for buildings and improvements are capitalized and the cost is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capital outlays exceeded depreciation in the current period.

Capital Outlays 17,803,354 18,481,059 Gain (Loss) on Disposal of Capital Assets 9,098 (20,340) Proceeds from Sales of Capital Assets (40,720) (20,345) Depreciation Expense (9,576,315) (9,284,508)

Some capital asset additions are financed through capital leases. In governmental funds, a capital lease arrangement is considered a source of financing, but in the statement of net position, the lease obligation is reported as a liability. Repayment of capital lease principal is an expenditure in the governmental funds, but repayment reduces the lease obligation in the statement of net position.

Change in Accrued Interest - Capital Leases 2,834 (1,155) Principal Payments - Capital Leases 11,884 211,295

The governmental funds report bond proceeds as financing sources, while repayment of bond principal is reported as an expenditure. In the statement of net position, however, issuing debt increases long-term liabilities and does not affect the statement of activities and repayment of principal reduces the liability. Also, governmental funds report the effect of premiums when debt is first issued, whereas these amounts are amortized in the statement of activities. Interest is recognized as an expenditure in the governmental funds when it is due. In the statement of activities, however, interest expense is recognized as it accrues, regardless of when it is due. The net effect of these differences in the treatment of general obligation bonds and related items is as follows:

Bond Proceeds - (14,870,000) Certificate of Participation/Lease Purchase Agreement Proceeds (6,560,000) (22,815,000) Bond Premium/Discount (234,279) (1,645,424) Bond Issuance Costs - 593,646 Repayment of Certificates of Participation Payable 2,610,000 10,270,000 Change in Accrued Interest - Certificates of Participation Payable 14,461 (110,834) Repayment of Bond Principal 5,905,000 5,765,000 Change in Accrued Interest - General Obligation Bonds 34,573 (78,561) Repayment of Lease Purchase Agreement Payable 502,797 - Amortization of Bond Issuance Costs (1,011,790) (145,477) Amortization of Bond Premium 429,859 326,708 Amortization of Bond Discount - (91,039)

Delinquent property taxes receivable will be collected this year, but are not available soon enough to pay for the current period’s expenditures, and therefore are unavailable in the funds. (325,022) (57,772)

Amounts reported for governmental activities in the statement of activities are different because:

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES

(CONTINUED) YEAR ENDED JUNE 30, 2014

(WITH SUMMARIZED FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2013)

See accompanying Notes to Financial Statements. (26)

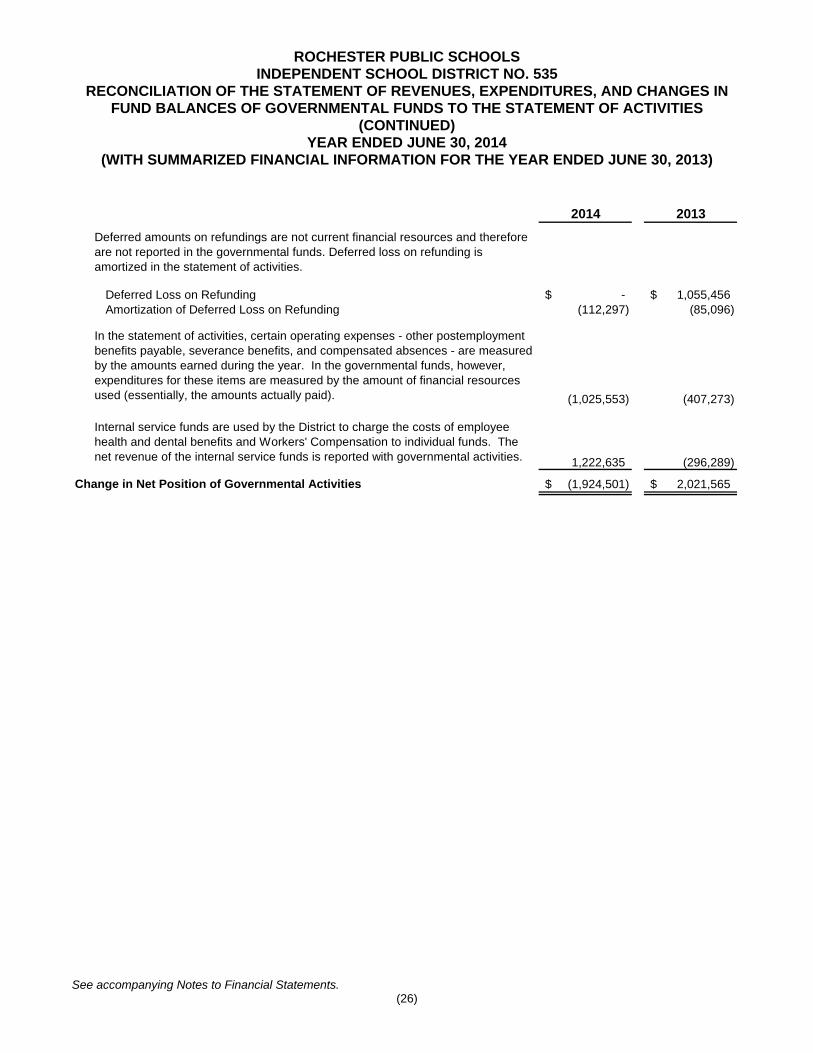

2014 2013 Deferred amounts on refundings are not current financial resources and therefore are not reported in the governmental funds. Deferred loss on refunding is amortized in the statement of activities.

Deferred Loss on Refunding -$ 1,055,456$ Amortization of Deferred Loss on Refunding (112,297) (85,096)

In the statement of activities, certain operating expenses - other postemployment benefits payable, severance benefits, and compensated absences - are measured by the amounts earned during the year. In the governmental funds, however, expenditures for these items are measured by the amount of financial resources used (essentially, the amounts actually paid). (1,025,553) (407,273)

Internal service funds are used by the District to charge the costs of employee health and dental benefits and Workers' Compensation to individual funds. The net revenue of the internal service funds is reported with governmental activities. 1,222,635 (296,289)

Change in Net Position of Governmental Activities (1,924,501)$ 2,021,565$

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – BUDGET AND ACTUAL

GENERAL FUND YEAR ENDED JUNE 30, 2014

See accompanying Notes to Financial Statements. (27)

Actual Over (Under)Original Final Amounts Final Budget

REVENUESLocal Sources

Property Taxes 21,215,930$ 11,049,687$ 11,020,964$ (28,723)$ Earnings on Investments 12,500 67,500 81,317 13,817 Other 3,032,000 5,441,794 5,676,350 234,556

State Sources 134,208,903 145,915,742 144,472,743 (1,442,999) Federal Sources 7,398,683 7,789,854 6,976,486 (813,368)

Total Revenues 165,868,016 170,264,577 168,227,860 (2,036,717)

EXPENDITURESCurrent:

Administration 7,593,906 7,463,201 7,881,141 417,940 District Support Services 6,321,113 5,039,867 4,026,463 (1,013,404) Regular Instruction 82,802,646 85,950,798 80,143,199 (5,807,599) Vocational Education Instruction 2,101,165 2,288,391 2,262,048 (26,343) Specia l Education Instruction 28,542,419 28,568,398 31,095,040 2,526,642 Instructional Support Services 9,325,748 10,819,754 10,609,023 (210,731) Pupil Support Services 15,903,369 16,457,447 16,621,195 163,748 Sites and Buildings 13,728,321 14,738,502 13,794,830 (943,672) Fiscal and Other Fixed Cost Programs 415,500 415,500 382,620 (32,880)

Capital Outlay 3,675,307 6,747,075 4,569,970 (2,177,105) Debt Service

Principal 1,918,096 1,889,766 1,889,681 (85) Interest and Fiscal Charges 677,271 718,148 718,232 84

Total Expenditures 173,004,861 181,096,847 173,993,442 (7,103,405)

Excess (Deficiency) of RevenuesOver (Under) Expenditures (7,136,845) (10,832,270) (5,765,582) 5,066,688

OTHER FINANCING SOURCES (USES)Utility Rebates - 1,000 1,092 92 Sale of Equipment Proceeds 15,000 25,000 34,670 9,670 Insurance Recovery Proceeds - 70,809 106,204 35,395 Transfers In 500,000 500,000 500,000 - Transfers Out - (6,327) (6,326) 1

Total Other Financing Sources (Uses) 515,000 590,482 635,640 45,158

Net Change in Fund Balances (6,621,845)$ (10,241,788)$ (5,129,942) 5,111,846$

FUND BALANCEBeginning of Year 40,711,249

End of Year 35,581,307$

Budgeted Amounts

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – BUDGET AND ACTUAL

FOOD SERVICE FUND YEAR ENDED JUNE 30, 2014

See accompanying Notes to Financial Statements. (28)

Over (Under)

Actual FinalOriginal Final Amounts Budget

REVENUES

Local SourcesEarnings on Investments 2,500$ 8,000$ 10,624$ 2,624$ Other - Primarily Meal Sales 3,688,511 3,516,809 3,462,166 (54,643)

State Sources 295,077 290,888 300,428 9,540 Federal Sources 3,899,742 3,981,969 4,127,564 145,595

Total Revenues 7,885,830 7,797,666 7,900,782 103,116

EXPENDITURES

CurrentFood Service 7,867,300 7,885,746 7,503,170 (382,576)

Capital Outlay 150,000 1,130,149 899,028 (231,121) Total Expenditures 8,017,300 9,015,895 8,402,198 (613,697)

Excess (Deficiency) of Revenues Over (Under) Expenditures (131,470) (1,218,229) (501,416) 716,813

OTHER FINANCING SOURCES

Transfer in - - 6,326 6,326 Total Other Financing Sources - - 6,326 6,326

Net Change in Fund Balance (131,470)$ (1,218,229)$ (495,090) 723,139$

FUND BALANCE

Beginning of Year 3,975,302

End of Year 3,480,212$

Budgeted Amounts

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCES – BUDGET AND ACTUAL

COMMUNITY SERVICE FUND YEAR ENDED JUNE 30, 2014

See accompanying Notes to Financial Statements. (29)

Over(Under)

Actual FinalOriginal Final Amounts Budget

REVENUESLocal Sources

Property Taxes 1,827,411$ 941,462$ 957,078$ 15,616$ Earnings on Investments 200 1,053 2,364 1,311 Other - Primarily Tuition and Fees 3,962,831 3,998,319 4,303,202 304,883

State Sources 3,137,804 4,019,674 4,008,437 (11,237) Federal Sources 537,055 665,016 597,465 (67,551)

Total Revenues 9,465,301 9,625,524 9,868,546 243,022

EXPENDITURESCurrent

Community Service 9,204,889 9,491,110 9,510,292 19,182 Capital Outlay 54,675 34,361 25,598 (8,763)

Total Expenditures 9,259,564 9,525,471 9,535,890 10,419

Excess of Revenues Over Expenditures 205,737$ 100,053$ 332,656 232,603$

FUND BALANCEBeginning of Year 907,740

End of Year 1,240,396$

Budgeted Amounts

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF NET POSITION PROPRIETARY FUND

JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION AS OF JUNE 30, 2013)

See accompanying Notes to Financial Statements. (30)

2014 2013

ASSETSCurrent Assets

Cash and Cash Equivalents 7,439,511$ 5,636,660$ Investments 3,739,592 4,740,035 Accounts Receivable - 10,733 Interest Receivable 731 5,599 Prepaids 5,499 22,757

Total Assets 11,185,333 10,415,784

LIABILITIESCurrent Liabilities

Salaries Payable 22,763 23,009 Accounts Payable 780,867 818,334 Claims Payable 2,299,311 2,714,684

Total Current Liabilities 3,102,941 3,556,027

NET POSITIONRestricted for Health and Dental Insurance Trust 6,531,257 4,794,184 Unrestricted 1,551,135 2,065,573

Total Net Position 8,082,392$ 6,859,757$

Governmental Activities - Internal Service Funds

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION PROPRIETARY FUND

YEAR ENDED JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2013)

See accompanying Notes to Financial Statements. (31)

2014 2013

OPERATING REVENUESCharges for Premiums, Net of Refunds 24,790,718$ 22,578,598$

Total Operating Revenues 24,790,718 22,578,598

OPERATING EXPENSESSalaries 339,139 334,080 Employee Benefits 156,828 127,064 Claim Expense 22,596,191 22,405,445 Services, Supplies, and Fees 8,007 18,655

Total Operating Expenses 23,100,165 22,885,244

Operating Income (Loss) 1,690,553 (306,646)

NONOPERATING INCOMEEarnings on Investments 32,082 10,357

Total Nonoperating Income 32,082 10,357

Net Income (Loss) Before Transfers 1,722,635 (296,289)

Transfers Out (500,000) -

Change in Net Position 1,222,635 (296,289)

Total Net Position - Beginning 6,859,757 7,156,046

Total Net Position - Ending 8,082,392$ 6,859,757$

Governmental Activities - Internal Service Funds

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

STATEMENT OF CASH FLOWS PROPRIETARY FUND

YEAR ENDED JUNE 30, 2014 (WITH SUMMARIZED FINANCIAL INFORMATION FOR THE YEAR ENDED JUNE 30, 2013)

See accompanying Notes to Financial Statements. (32)

2014 2013CASH FLOWS FROM OPERATING ACTIVITIES

Receipts from Interfund Services Provided 24,801,451$ 22,571,162$ Payments for Administrative Costs (496,213) (478,838) Payments for Claims (23,049,031) (21,978,670) Payments for Services, Supplies, and Materials 9,251 (18,268)

Net Cash Provided by Operating Activities 1,265,458 95,386

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIESTransfers Out (500,000) -

Net Cash Used by Noncapital Financing Activities (500,000) -

CASH FLOWS FROM INVESTING ACTIVITIESProceeds from Maturities of Investment Securities 1,094,813 1,000,036 Purchase of Investment Securities (94,370) (5,740,071) Interest Received 36,950 4,758

Net Cash Provided (Used) by Investing Activities 1,037,393 (4,735,277)

Net Increase (Decrease) in Cash and Cash Equivalents 1,802,851 (4,639,891)

Cash and Cash Equivalents - Beginning 5,636,660 10,276,551

Cash and Cash Equivalents - Ending 7,439,511$ 5,636,660$

RECONCILIATION OF OPERATING LOSS TO NET CASH PROVIDED BY OPERATING ACTIVITIES

Operating Income (Loss) 1,690,553$ (306,646)$ Adjustments to Reconcile Operating Income (Loss) to Net Cash

Provided by Operating Activities:(Increase) Decrease in Accounts Receivable 10,733 (7,436) Decrease in Prepaids 17,258 387 Decrease in Salaries Payable (246) (17,694) Decrease in Accounts Payable (37,467) (1,358) Increase (Decrease) in Claims Payable (415,373) 428,133

Total Adjustments (425,095) 402,032

Net Cash Provided by Operating Activities 1,265,458$ 95,386$

Governmental Activities - Internal Service Funds

(This page intentionally left blank)

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2014

(33)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. Basis of Presentation

The financial statements of Independent School District No. 535 have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing governmental accounting and financial reporting principles. The GASB pronouncements are recognized as Accounting Principles Generally Accepted in the United States of America for state and local governments.

B. Financial Reporting Entity

Independent School District No. 535 (the District) is an instrumentality of the State of Minnesota established to function as an educational institution. The elected School Board (Board) is responsible for legislative and fiscal control of the District. A Superintendent is appointed by the Board and is responsible for administrative control of the District. Accounting principles generally accepted in the United States of America (GAAP) require that the District's financial statements include all funds, departments, agencies, boards, commissions, and other organizations which are not legally separated from the District. In addition, the District's financial statements are to include all component units - entities for which the District is financially accountable. Financial accountability includes such aspects as appointing a voting majority of the organization's governing body, significantly influencing the programs, projects, activities or level of services performed or provided by the organization or receiving specific financial benefits from, or imposing specific financial burden on, the organization. The Health and Dental Care Trust, a legally separate entity, is presented as a blended component unit because its sole purpose is to manage the District’s employee health and dental insurance programs. Other legally separate organizations that provide economic resources for use by the District or the students are not included as a component unit in the financial statements of the District because they are not significant. Student activities are determined primarily by student participants under the guidance of an adult and are generally conducted outside of school hours. The School Board does have a fiduciary responsibility in establishing broad policies and ensuring that appropriate financial records are maintained for student activities. In accordance with Minnesota Statutes, the District’s School Board has elected to control or be financially accountable for certain extracurricular student activities. Accordingly, the accounts and transactions for the activity funds are included in the financial statements within the General Fund. The District's School Board has also elected to not control or exercise oversight responsibility with respect to other student activities. Accordingly, those student activity accounts are not included in these financial statements.

ROCHESTER PUBLIC SCHOOLS INDEPENDENT SCHOOL DISTRICT NO. 535

NOTES TO FINANCIAL STATEMENTS JUNE 30, 2014

(34)

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)