Embed Size (px)

Citation preview

@uktisa@uktisa

Robo-Pensions: The Digital Revolution

Hogan Lovells International LLP, Atlantic House, Holborn Viaduct, London EC1A 2FG

@uktisa@uktisa

Adrian BouldingDirector of Retirement, TISA – Seminar Chair

@uktisa@uktisa

Agenda

• Opening remarks by Adrian Boulding, Director of Retirement, TISA

• Ben Goss, CEO, Distribution Technology ‘The Digital Distribution Review’

• Andrew Martin, Product Strategy Director, Dunstan Thomas ‘A statement of purpose’

• Panel Session: Debate Chair Dirk Paterson, Director, Corporate Comms Shop

• Pro Inertia: Baroness Drake CBE, former Pensions Commissioner

• Pro Inertia: Andy Tarrant, Head of Policy and Government Relations, B&CE Benefits

• Pro Engagement: Paul Sturgess, Director Private Sector, Equiniti

• Pro Engagement: Phillip Walter, Group Chief Executive, Aquila Heywood

• Coffee Break

• Marc Hommel, Wobi ‘Dramatic improvement in consumer experience and financial health: a country case study’

• John Salmon, Partner and Susan McKiernan, Counsel, Hogan Lovells International LLP ‘Digital Innovation: Risk vs Reward’

• My pension is not big enough: Interview by Dirk Paterson, with John Greer, Pensions Technical Manager, Old Mutual Wealth

• Closing remarks by Adrian Boulding, Chair

• Network reception with wine and canapes

@uktisa@uktisa

Ben GossCEO, Distribution Technology

Ensuring Investment Suitability©2017 Distribution Technology Ltd. All Rights Reserved.

Ben Goss CEO, Distribution Technology

24th May, 2017

[email protected] | @BenGoss

tisa seminar Robo-Pensions: The Digital Revolution

©2017 Distribution Technology Ltd. All Rights Reserved.

Technology comes in waves

6

Source: NMG Research IFA Census and DT. Illustrative only

©2017 Distribution Technology Ltd. All Rights Reserved.

These waves are becoming more powerful

7

Source: Elektormagazine.com, 2015

©2017 Distribution Technology Ltd. All Rights Reserved.

We have seen several waves impact on our industry

8

Desk top

cashflow

modelling

US online

advice

SaaS based

financial

planning

services FAMR support

for automated

advice

Insurers’

laptop needs

analysis UK online

advice

FSA

Ensuring

Suitability

Widespread use of risk

based stochastic modelling

©2017 Distribution Technology Ltd. All Rights Reserved.

Financial planning on its best day

9

“Helping customers achieve their goals

at a risk and cost that’s right for them”

©2017 Distribution Technology Ltd. All Rights Reserved.

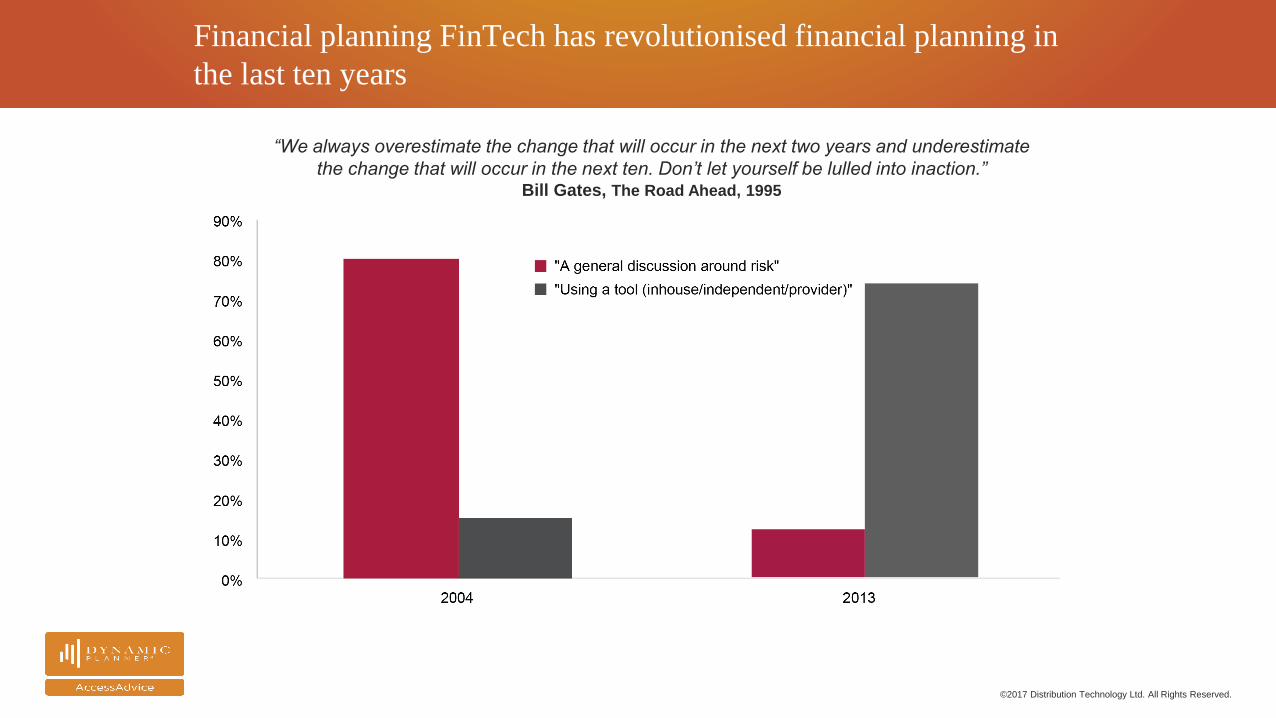

Financial planning FinTech has revolutionised financial planning in

the last ten years

“We always overestimate the change that will occur in the next two years and underestimate

the change that will occur in the next ten. Don’t let yourself be lulled into inaction.”Bill Gates, The Road Ahead, 1995

©2017 Distribution Technology Ltd. All Rights Reserved.

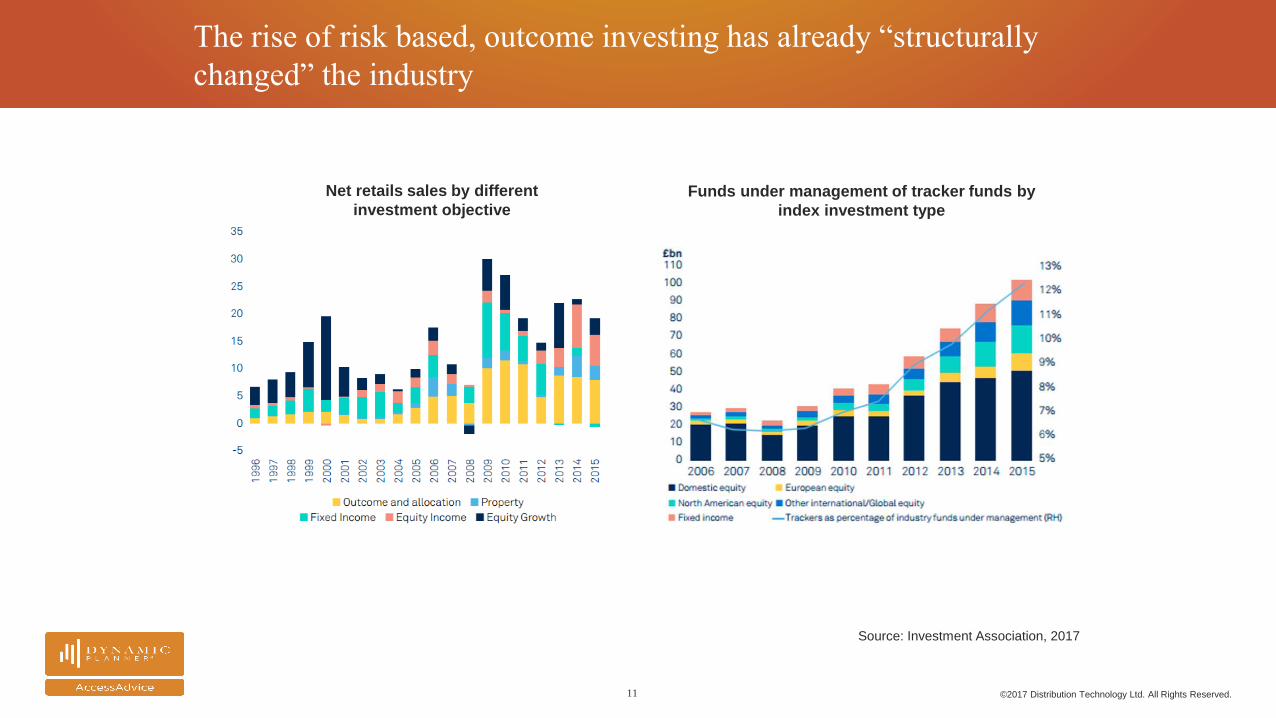

The rise of risk based, outcome investing has already “structurally

changed” the industry

11

Net retails sales by different

investment objectiveFunds under management of tracker funds by

index investment type

Source: Investment Association, 2017

©2017 Distribution Technology Ltd. All Rights Reserved.

Demographics are increasingly challenging

12

Mean client age

2011: 51

2016: 56

Median wealth for

client under 45

2011: £27k

2016: £45k

Source: Dynamic Planner data, 150,000 records September 2016.

Age distribution of clients pre and post RDR

©2017 Distribution Technology Ltd. All Rights Reserved.

Digital potentially changes everything

13

“Who do you trust?”

Agents

Internet

Source: ABTA 2004, Mintel 2012

©2017 Distribution Technology Ltd. All Rights Reserved.

The question is; ‘How far can it go?’

14

Level

4

Holistic

Planning

Level

3

Personal

Recommendations

Level

2Guidance

Level

1Needs

©2017 Distribution Technology Ltd. All Rights Reserved.

Financial planning is not holiday planning. Customers need advice

15

Long term

thinking hurts!

Risk, trust and

capability

The tyranny of

choice

©2017 Distribution Technology Ltd. All Rights Reserved.

5 big challenges to the use of FinTech

16

Priorities

and

delivery

Bringing

advisers

with you

Building

bridges

Engaging

customers

Ensuring

suitability

©2017 Distribution Technology Ltd. All Rights Reserved.

Enhance

services

Reduce

risk

The potential benefits though are significant

17

Reduce

costs

Transform

access

©2017 Distribution Technology Ltd. All Rights Reserved.

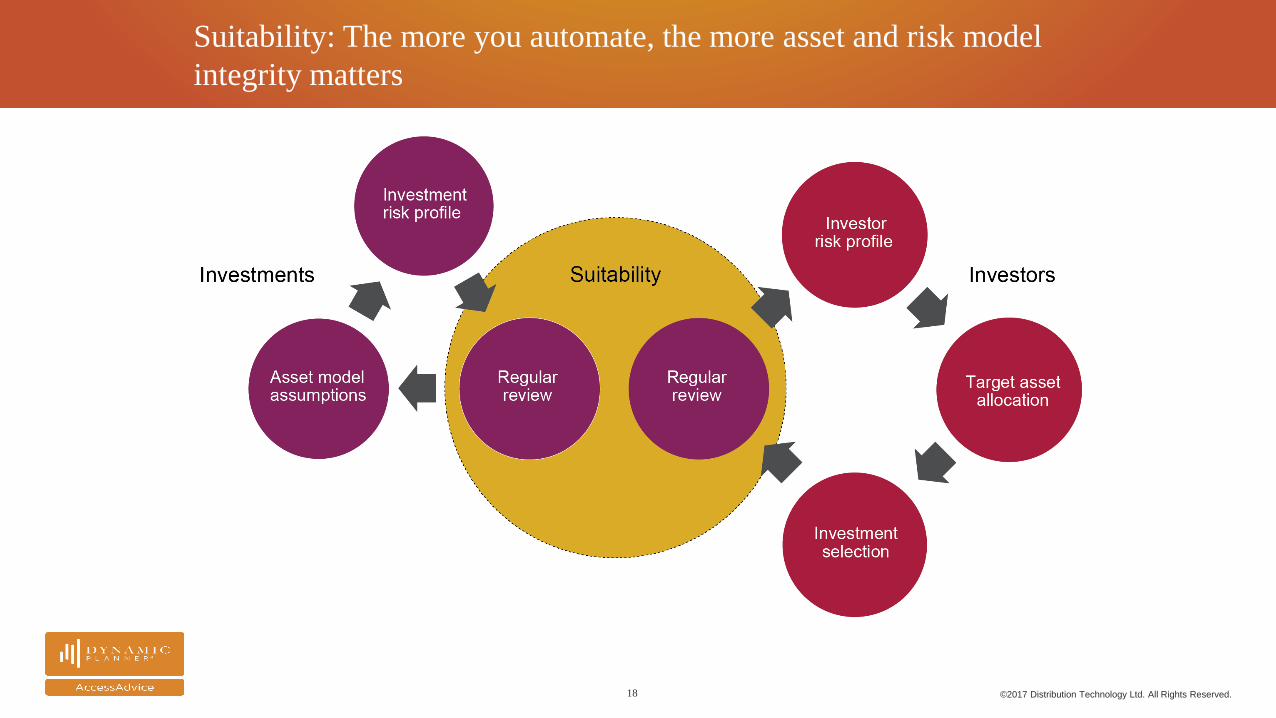

Suitability: The more you automate, the more asset and risk model

integrity matters

18

©2017 Distribution Technology Ltd. All Rights Reserved.

The aim is to create a mandate and relevant benchmark for investment management

19

Source: Dynamic Planner, illustrative

©2017 Distribution Technology Ltd. All Rights Reserved.

Risk targeting - there is a new IA sector and the FCA asset management review is looking

for relevant benchmarks

20

Source: Dynamic Planner, Risk Profile target asset allocation performance

©2017 Distribution Technology Ltd. All Rights Reserved.

With the right building blocks in place, future developments will

change the game

21

Account

aggregation

Automated

advice

Artificial

intelligence

Social

networks

Frictionless

financial planning

©2017 Distribution Technology Ltd. All Rights Reserved.

AccessAdvice. Hybrid model turns painful to profitable

22

Reduces time to

serve ISA from 4 hrs

to 30 mins

Investors pay less for

regulated, whole of

market advice

Powered by Dynamic

Planner’s trusted asset

and risk model

Fully configurable white label

automated advice service for

adviser website “robo in a box”

Ensuring Investment Suitability©2017 Distribution Technology Ltd. All Rights Reserved.

Ben Goss CEO, Distribution Technology

24th May, 2017

[email protected] | @BenGoss

@uktisa@uktisa

Andrew MartinProduct Strategy Director, Dunstan Thomas

@uktisa@uktisa

Panel Session: To engage or not to engage

Debate Chair: Dirk Paterson, Director, Corporate Comms Shop• Pro Inertia: Baroness Drake CBE, former Pensions Commissioner

• Pro Inertia: Andy Tarrant, Head of Policy and Government Relations, B&CE Benefits

• Pro Engagement: Paul Sturgess, Director Private Sector, Equiniti

• Pro Engagement: Phillip Walter, Group Chief Executive, Aquila Heywood

@uktisa@uktisa

Marc HommelWobi

Consumer empowermentThe Israeli experience of aligning consumer

needs and provider commercial success

Marc Hommel

+44 780 176 7373

ROBO-PENSIONS: THE DIGITAL REVOLUTION

24 MAY 2017

Imagine …

• Instantaneous on-line access to dashboard

covering all retirement savings…

Imagine …

• Instantaneous access to on-line dashboard

covering all retirement savings…

Imagine …

• Instantaneous access to on-line dashboard

covering all retirement savings…

• Clarity around contribution of investment

performance and charges

Imagine …

• Instantaneous access to on-line dashboard

covering all retirement savings…

• Clarity around contribution of investment

performance and charges

• Transfers from an employer or provider to a

new provider within 72 hours

Imagine…

• … plus rest of your financial health (debt, wealth, expediture, protection and healthcare)

Imagine…

• … plus rest of your financial health (debt, wealth, expediture, protection and healthcare)

Imagine…

• … plus rest of your financial health (debt, wealth, expediture, protection and healthcare)

• Insight in easily understandable format and language

• Actions for improving your financial health

• Guarantee that your data won’t be shared without your consent

Information

and Insights + Options for

Actions

A world in which people are engaged in their retirement savings and beyond

Yuk! Pensions• For old people

• Distant

• Complex /opaque

• Jargon

• Boring

• Remote

• Standardised

• Not relevant

Engaged! Money• My money

• Like a bank account

• Transparent

• Meaningful

• Impactful

• Accessible

• Personalised with convenience

• I want to be involved

A world in which people are engaged in their retirement savings and beyond

• Propensity to save 25% increase

• Charges paid 20%-50% saving

• New business acquisition costs 40% lower

• Transfers 10% of Retirement Accounts have been transferred, more than last 20 years combined

… due to a better alignment between providers and consumers

• Line of sight

• Transparency

• Improved and more intimate customer relationships

• Lower business acquisition costs / lower lapse rates

• Choice of customers

• Lower costs

How did we get here?

Changing consumer demands

• Diversity

• Instant gratification

• Lack of trust

• Data ownership

• Empowerment

Affordable

technology

User

experience

Database

+

Failure of

industry to

act

Enforced by

law changes

+

Lessons learnt

• Forget asking people what they want

• Ditch the jargon

• Consumer (not product) centric

• Focus on the “Why” and not on the “Why not”

• Simplify!

• Consumer interests includes having robust successful providers

• Beware the financial services “mindset”

• Adapt or die!

Providers must adapt or die

Customer

Interface

Data

Working with providers and consumer groups in the UK to bring this experience here

• Diversity of fear versus hope

• Business case informed by ambition, pain threshold or law?

• Ownership of the opportunity?

• Consultant-fest

• Product focus

• Extent of congruency between words and behaviours?

CHALLENGE OR OPPORTUNITY?

@uktisa@uktisa

John Salmon and Susan McKiernanHogan Lovells International LLP

John Salmon, Partner, Hogan Lovells

Susan McKiernan, Counsel, Hogan Lovells

Robo-pensions: The Digital Revolution

Digital Innovation: Risk v Reward

45

Digital Revolution?

1876 2017onwards

Innovations in communication

First telephone

call

Western Union Telegraph Company establishes its Telex

system in the US

Xerox introduces the Long Distance Xerography – the first modern day

fax machine

First inter-industry EDI standard (covering air, motor, ocean, rail and

some banking applications)

IBM launch the first

smartphone, Simon

Apple release the iPad

1991

The World Wide Web

1962 201019921964 1971 1975

First email sent

1983: Microsoft Word launched

2007: Apple launch the iPhone

1981: IBM PC launched

1993

Birth of 2G, first SMS text messages

sent & data services begin to appear on

phones

1999: Blackberry launch first device

1982

TCP/IP emerges as the standard

protocol for the internet

The internet ageThe beginning The mobile era

Hogan Lovells

Digital innovation

Risk

Leading edge or bleeding

edge

Technology risk

Staying on the right side

of law & regulation

Failure

Cost

Reward

Efficiencies & cost

savings

Customer engagement

Competitive advantage

New products,

channels & partners

Brand value

Hogan Lovells

Leading edge or bleeding edge

Ludwig von Mises

“Innovation is the whim of an elite before it becomes a need of the public.”

Is the market ready?

Are your customers

ready?

Reputational impact

Law and regulation

cannot keep up with new technology?

Data and privacy

Regulator focus

Immune to regulation?

Fairness, transparency,

anti-discrimination

Law and regulation

Hogan Lovells

• Robo-advice and FAMR - advice v guidance

• GDPR and complex value chains

Law and regulation

Scheme administrators

Advisers / EBCs

Trustees Employers

Pension providers

NEST

Service providers (e.g.

payroll, platforms,

data services)

Hogan Lovells

Risk depends on the technology and how

you implement itTransition risk Risk appetite

What are the risks? Am I taking on more

risk?How can I manage the

risk?How can I mitigate

the risk?

Importance of governance

Technology risk

Hogan Lovells

• Is the goal to make up lost ground or carve a new path?

• Incumbent v start-up mentality

– Culture

– Priorities

– Cost

Risk of failure

Gary Hamel

“Most companies don’t have the luxury of focusing exclusively on innovation. They have to innovate while stamping out zillions of widgets or processing billions of transactions.”

Hogan Lovells

Promise of efficiencies and cost savings

• True innovation or just digitising the offline world?

• Can these best be achieved alone or through collaboration?

– Data standards

– Technical standards (e.g. Open Banking and open APIs)

What is Open Banking?

APIs (Application Programming

Interface)

Payment Initiation Service

Provider ('PISP')

Account information

Service Provider ('AISP')

Hogan Lovells

Customer engagement

Cuvva

Trōv

• Potential to improve engagement

Hogan Lovells

New channels

New products

New customers

New partnerships

New horizons and competitive advantage

Brand value

Reputation

“Innovation distinguishes between a leader and a follower.”

Steve Jobs Loyalty

Publicity

Hogan Lovells

The risk of doing nothing

Theodore Levitt

“Creativity is thinking up new things. Innovation is doing new things.”

• Nothing improves

• If you don't do it, someone else might:

– Competitors

– Disruptors

– Regulators and law makers

"Hogan Lovells" or the "firm" is an international legal practice that includes Hogan Lovells International LLP, Hogan LovellsUS LLP and their affiliated businesses.

The word “partner” is used to describe a partner or member of Hogan Lovells International LLP, Hogan Lovells US LLP or any of their affiliated entities or any employee or consultant with equivalent standing.. Certain individuals, who are designated

as partners, but who are not members of Hogan Lovells International LLP, do not hold qualifications equivalent to members.

For more information about Hogan Lovells, the partners and their qualifications, see www.hoganlovells.com.

Where case studies are included, results achieved do not guarantee similar outcomes for other clients. Attorney advertising. Images of people may feature current or former lawyers and employees at Hogan Lovells or models not

connected with the firm.

© Hogan Lovells 2017. All rights reserved

www.hoganlovells.com

@uktisa@uktisa

Networking reception with wine and canapes

Thank you to

Hogan Lovells International LLP

@uktisa

Thank You!

TISADakota House

25 Falcon CourtPreston Farm Business Park

STOCKTON-ON-TEESTS18 3TX

www.tisa.uk.com01642 666999

@uktisa