Embed Size (px)

Citation preview

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 1 of 25 Page ID #:397

ROBBINS GELLER RUDMAN & DOWD LLP

DARREN J. ROBBINS (168593) ROBERT R. HENSSLER JR. (216165) 655 West Broadway, Suite 1900 San Diego, CA 92101-3301 Telephone: 619/231-1058 619/231-7423 (fax) darrenrrgrd1aw.com bhensslerrgrd1aw.com

Lead Counsel for Plaintiff C)

UNITED STATES DISTRICT COURT

CENTRAL DISTRICT OF CALIFORNA

SOUTHERN DIVISION 171 1 0

PAWEL I. KMIEC, Individually and on No. 8: 12-cv-0022-iJPgj) Behalf of All Others Similarly Situated, )

CLASS ACTIO( Plaintiff, -

CONSOLIDATEO COMPLAINT FOR vs. VIOLATIONS OF THE FEDERAL

SECURITIES LAWS POWERWAVE TECHNOLOGIES INC., et al.,

Defendants.

1

2

3

4

5

6

7

8

9

10

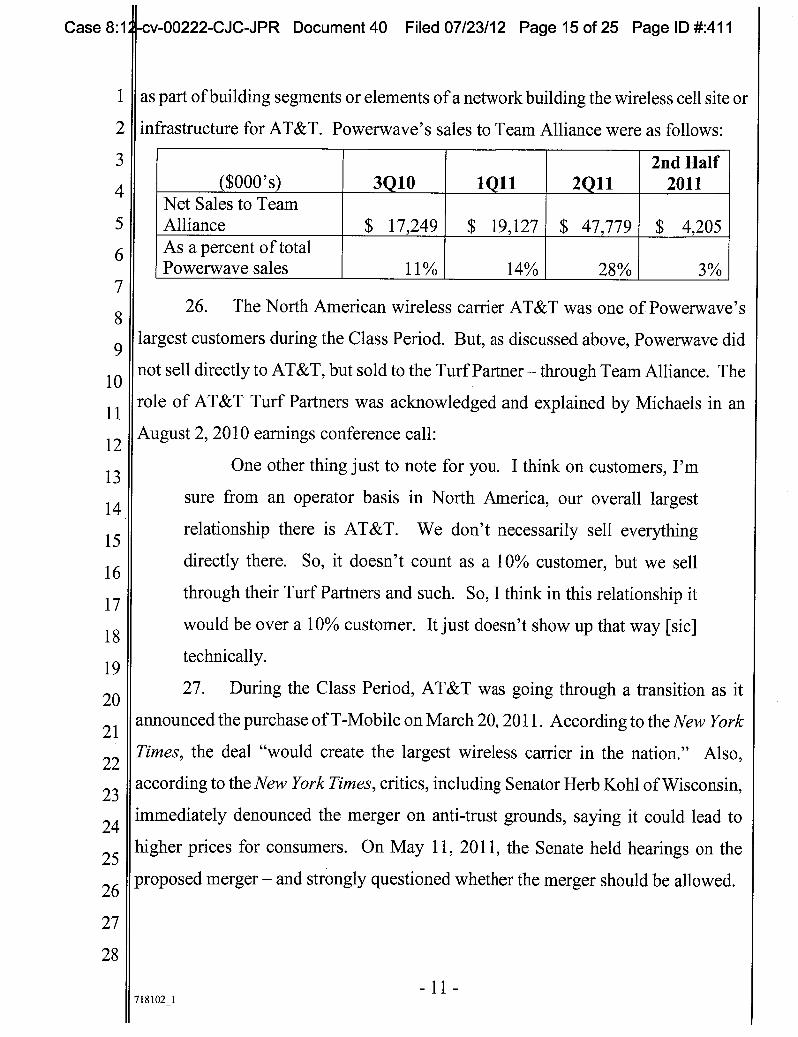

11

12

13

14

15

16

17

18

19

21

22

23

24

25

26

27

718102_i

28

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 2 of 25 Page ID #:398

1 TABLE OF CONTENTS

Page

II. JURISDICTION AND VENUE .....................................................................1

III

INTRODUCTION AND OVERVIEW ........................................................... 1

'III

CLAIMS ASSERTED IN THE COMPLAINT..............................................3

IV. PLAINTIFFS...................................................................................................3

V. DEFENDANTS...............................................................................................4

I VI. SOURCES OF ALLEGATIONS....................................................................6

VII. FACTUAL BACKGROUND TO DEFENDANTS' SCHEME...................10

Nature of Powerwave's Business .......................................................10

Because of Declining Demand Powerwave Engaged in a Revenue Recognition Scheme that Masked the True Demand forIts Products....................................................................................12

VIII. DEFENDANTS' FALSE STATEMENTS AND OMISSIONS ISSUED DURING THE CLASS PERIOD...................................................19

IX. THE TRUTH BEGINS TO EMERGE .........................................................31

X. DEFENDANTS' MATERIALLY FALSE AND MISLEADING FINANCIAL REPORTING AND GAAP VIOLATIONS DURING THECLASS PERIOD ..................................................................................44

A. Powerwave Improperly Recognized Revenue on Contingent Sales with Team Alliance, in Violation of GAAP .............................. 45

Sales of Defective Product............................................................................46

BulkOrders ..................................................

B. Powerwave Recorded Premature and Inflated Revenue in Violation of GAAP and the SEC's Revenue Recognition Requirements......................................................................................47

Powerwave '5 Disclosures Regarding Revenue Recognition Were False and Misleading and in Violation of GAAP and SEC Guidance............................................................................................. 50

Powerwave's Revenue Recognition Scheme Is Supported by the 92% Increase in DSO in 3Q11.....................................................52

Powerwave's Revenue Recognition Scheme Also Affected Inventory............................................................................................. 55

-i-

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

IV

E.

718102_i

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 3 of 25 Page ID #:399

1 TABLE OF CONTENTS

Page

F. Powerwave 'S Financial Statements Violated Fundamental AccountingConcepts.......................................................................... 57

XI. DEFENDANTS' KNOWLEDGE OR RECKLESS DISREGARD OF THE TRUTH ABOUT POWERWAVE'S BUSINESS ............................... 58

I XII. FRAUDULENT SCHEME AND COURSE OF BUSINESS ......................61

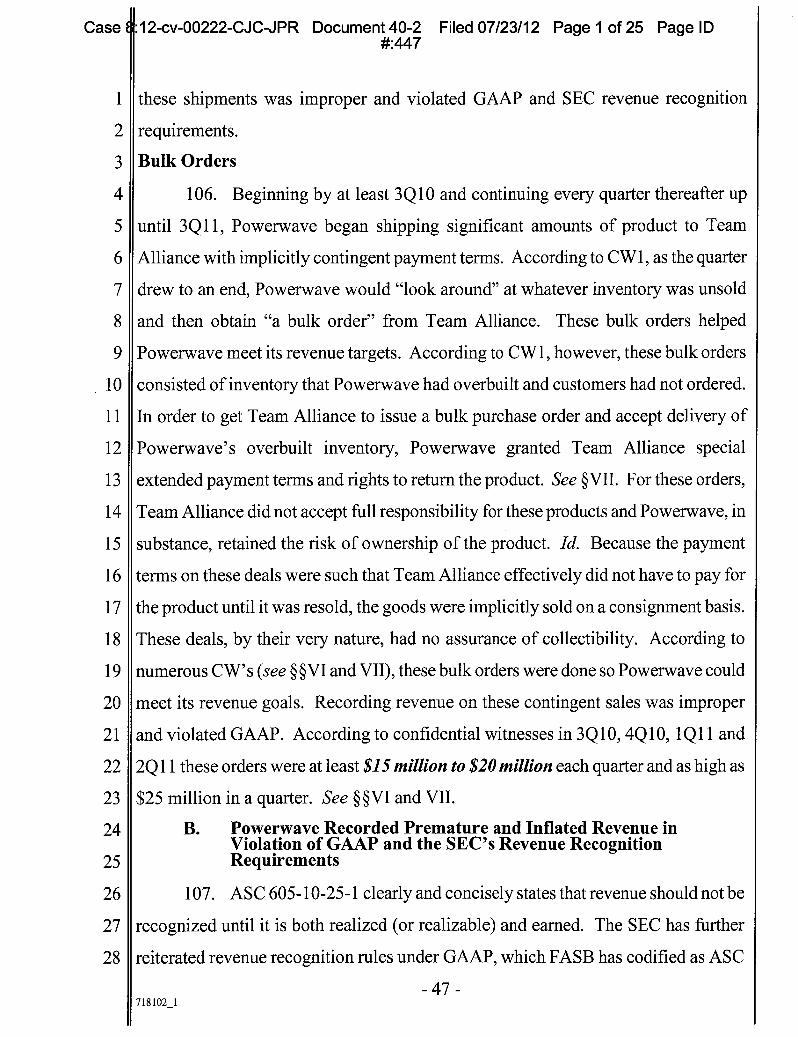

XIII. ADDITIONAL SCIENTER ALLEGATIONS.............................................61

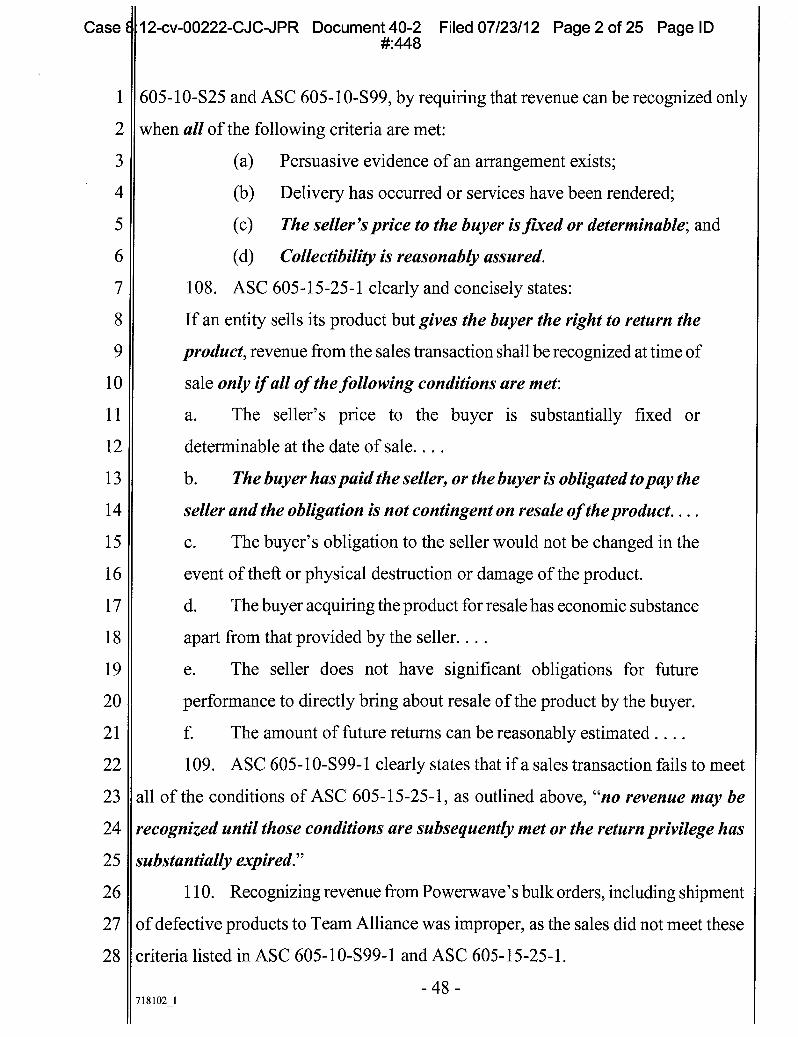

Defendants' Post Class Period Conduct of Shipping Unneeded Products to Customers Supports a Strong Inference of Scienter........62

Each of Defendants' False Statements and Omissions Involved One of Powerwave's Core Operations................................................62

Powerwave's Incentive Compensation Structure Created an Incentive for Fraud and Strongly Supports an Inference of Scienter................................................................................................ 63

D. Defendants' Fraudulent Conduct Allowed Defendants to Preserve Powerwave's Credit and Debt Ratings and Raise $100

n Million in the July 20, 2011 Offeng................................................. 65

Defendants' Misleading Statements About the Reasons for the 3Q11 "Nightmare" Support a Strong Inference of Scienter...............66

SOXCertification ...............................................................................68

1. Defendants Signed False Statements Regarding Powerwave's Internal Controls and Procedures.......................68

2. Reasons Why Defendants' Internal Controls and Procedure Statements Were Materially False and Misleading ................................................... 70

XIV. LOSS CAUSATION/ECONOMIC LOSS....................................................72

XV. ANY PURPORTED TUSK WARNING WERE INADEQUATE OR MATERIALLY FALSE AND MISLEADING ............................................ 74

XVI. NO SAFE HARBOR..................................................................................... 75

XVII. APPLICABILITY OF PRESUMPTION OF RELIANCE: FRAUD-ON-THE MARKET......................................................................................75

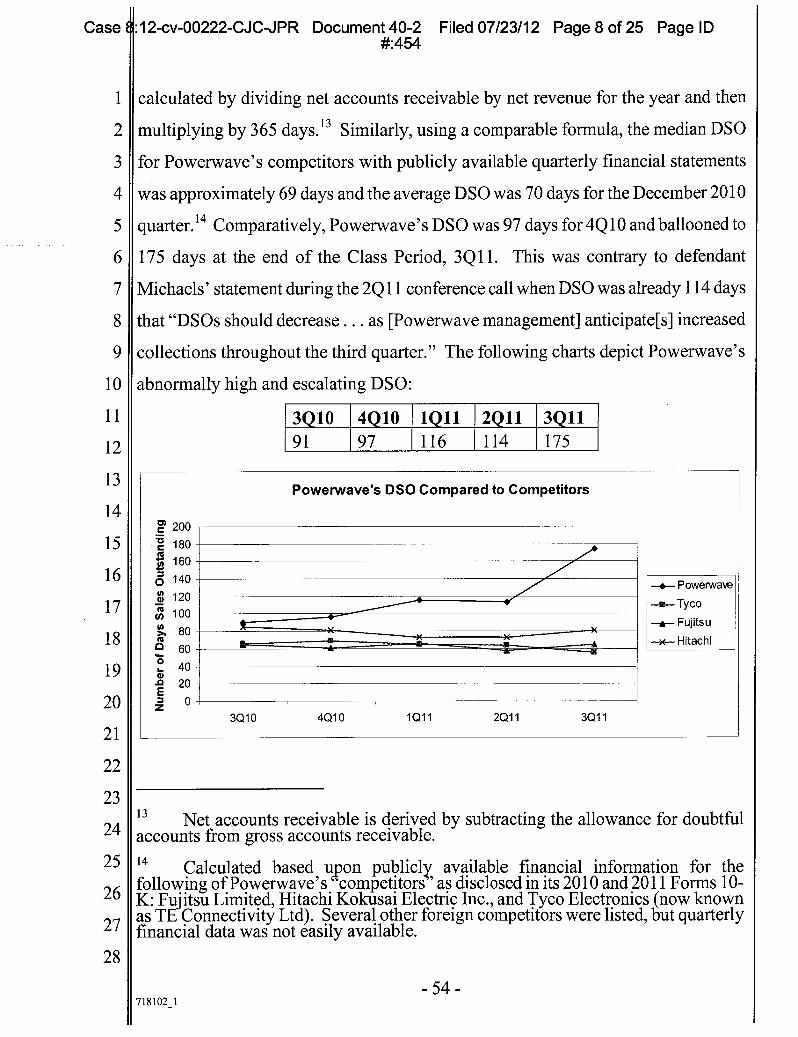

XVIII. CLASS ACTION ALLEGATIONS...................................................76

CLAIMS FOR RELIEF...........................................................................................78

COUNTI .................................................................................................................78

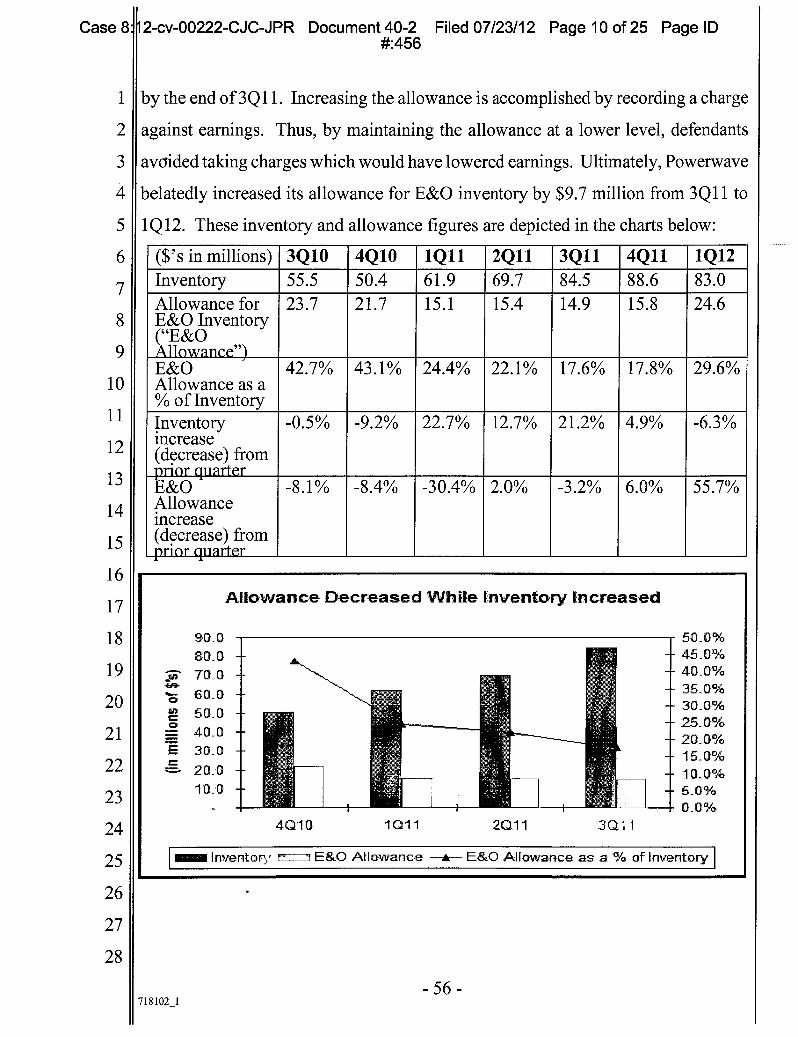

- ii -

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

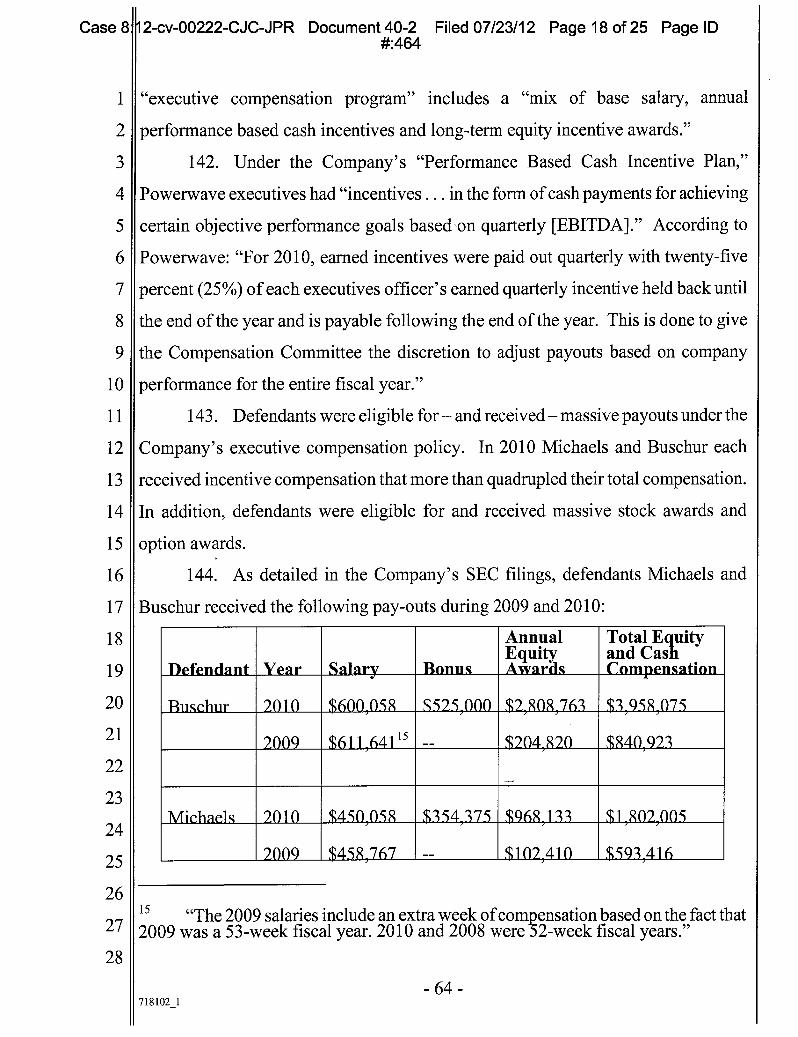

21

22

23

24

25

26

27

28

E

F.

FA

I"

C.

718102_i

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 4 of 25 Page ID #:400

1

TABLE OF CONTENTS

2

Page

3

COUNTII ................................................................................................................ 78

4

PRAYERFOR RELIEF..........................................................................................79

5

JURYDEMAND ..................................................................................................... 79

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

- 111 - 718102_i

Case 8:1 -c

C-JPR Document 40 Filed 07/23/12 Page 5 of 25 Page ID #:401

1 I. JURISDICTION AND VENUE

2

1. The claims asserted herein arise under § § 10(b) and 20(a) of the Securities

3 Exchange Act of 1934 ("1934 Act") (15 U.S.C. §78j(b) and 78t(a)) and Rule lOb-5

4 (17 C.F.R. §240.10b-5) promulgated thereunder by the Securities and Exchange

5 I commission ("SEC"). Jurisdiction is conferred by §22 of the Securities Act of 1933

6 I ("1933 Act") (15 u.s.C. §77v) and §27 of the 1934 Act (15 U.S.C. §78aa). Venue is

7 proper pursuant to §22 of the 1933 Act and §27 of the 1934 Act. Powerwave

8 Technologies, Inc.'s ("Powerwave" or the "Company") headquarters are located at

9 1801 East St. Andrew Place, Santa Ana, CA 92705 and many of the acts and

10 transactions constituting the violations of the securities laws alleged herein occurred

11 in this District.

12

2. In connection with the acts and conduct alleged herein, defendants,

13 directly and indirectly, used the means and instrumentalities of interstate commerce,

14 including, but not limited to, the United States mails, interstate telephone

15 communications and the facilities of the national securities exchanges and markets.

16 II. INTRODUCTION AND OVERVIEW

17

3. This is a securities class action on behalf of all persons who purchased or

18 otherwise acquired the securities of Powerwave between October 28, 2010 and

19 October 18, 2011, inclusive (the "Class Period"), against Powerwave and certain of its

20 officers and/or directors for violations of the 1934 Act. These claims are asserted

21 against Powerwave and certain of its officers and/or directors who made materially

22 false and misleading statements during the Class Period in press releases, analyst

23 conference calls and filings with the SEC.

24

4. Powerwave engages in the design, manufacture, marketing and sale of

25 wireless solutions for wireless communications networks worldwide. This action

26 concerns defendants' false statements and omissions regarding demand, and the

27 Company's financial statements. During the Class Period, defendants caused

28 Powerwave to report artificially inflated financial results in an effort to meet or exceed

- 1 - 718102_i

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 6 of 25 Page ID #:402

Powerwave's financial guidance in the face of a market that analysts believed would

experience slow growth through the 2011 fiscal year. Defendants' false explanation

for their tremendous feat was that Powerwave' s products were technically superior to

the competition and that, as a result, Powerwave's growth would exceed that of the

market as a whole.

6

5. In truth, defendants knew or recklessly disregarded that demand for

7 Powerwave's products was actually steeply declining. To off-set the declining

8 demand, and cloak the Company's deteriorating financial condition, defendants

9 engaged in an accounting scheme to artificially inflate its revenue and earnings by: (1)

10 shipping "bulk orders" of unsold and/or unsellable inventory to resellers on a

11 contingent basis whereby Powerwave would grant special extended payment terms

12 and rights to return the product; and (2) knowingly and deliberately shipping product

13 that Powerwave knew did not function "with the promise to replace" the defective

14 products in a later quarter. Defendants' false statements and omissions artificially

15 inflated Powerwave's stock price, allowing defendants and the Company to complete

16 a $100 million bond offering and collect millions in performance bonuses. As the

17 truth about defendants' false statements and omissions were revealed, Powerwave

18 shareholders suffered millions of dollars in damages and the Company's common

19 stock price plummeted from a Class Period high of $4.69 per share to $.68 per share

N) on October 19, 2011 - a 85% decline in little over five months, from which

21 Powerwave's stock price never recovered.

22

23

24

25

26

27

28

-2- 7181021

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 7 of 25 Page ID #:403

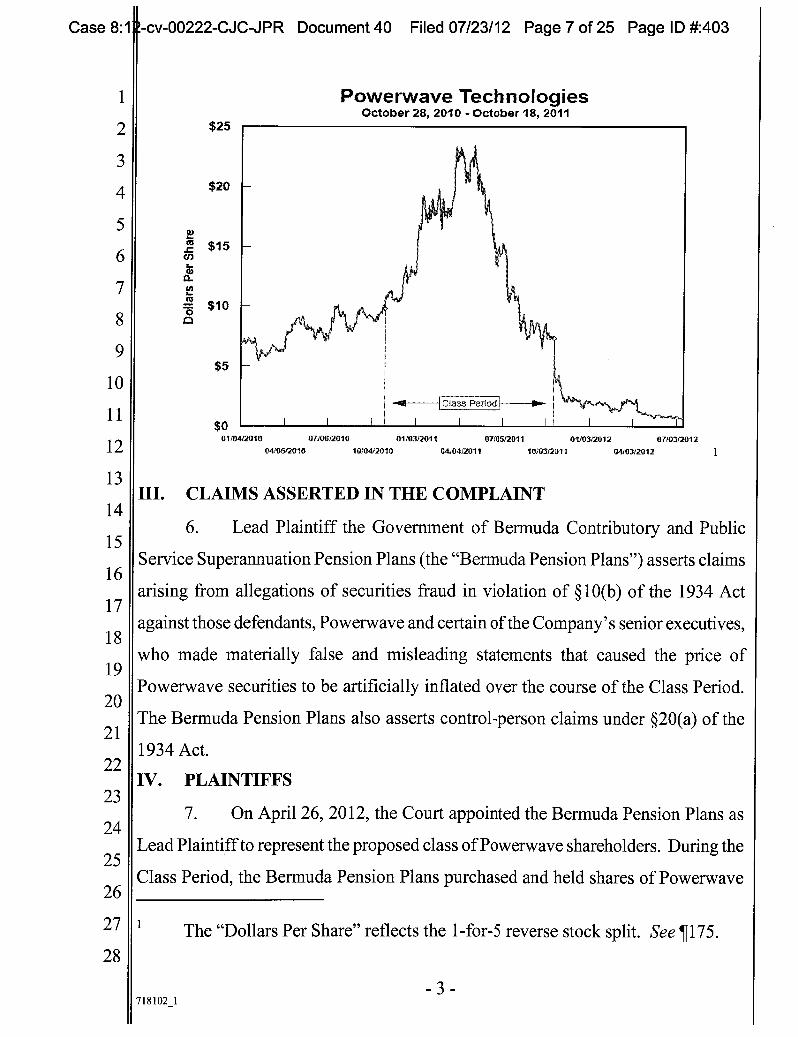

1 Powerwave Technologies October 28, 2010 - October 18, 2011

$25

$20

Is- CS

$10

$5

$01 I I I I I I I H I I

0110412010 07.104,2010 0110412011 0710512011 01/03/2012 0710312012 04/0642010 1010412010 04/0412011 1010312011 04/03/2012

0

III. CLAIMS ASSERTED IN THE COMPLAINT

6. Lead Plaintiff the Government of Bermuda Contributory and Public

Service Superannuation Pension Plans (the "Bermuda Pension Plans") asserts claims

arising from allegations of securities fraud in violation of § 10(b) of the 1934 Act

against those defendants, Powerwave and certain of the Company's senior executives,

who made materially false and misleading statements that caused the price of

Powerwave securities to be artificially inflated over the course of the Class Period.

The Bermuda Pension Plans also asserts control-person claims under §20(a) of the

1934 Act.

IV. PLAINTIFFS

7. On April 26, 2012, the Court appointed the Bermuda Pension Plans as

Lead Plaintiff to represent the proposed class of Powerwave shareholders. During the

Class Period, the Bermuda Pension Plans purchased and held shares of Powerwave

The "Dollars Per Share" reflects the 1-for-S reverse stock split. See ¶175.

-3-

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

7(1

21

22

23

24

25

26

27

28

718102_i

Case 8:1

C-JPR Document 40 Filed 07/23/12 Page 8 of 25 Page ID #:404

1 common stock. As a result of the defendants' conduct detailed herein, the Bermuda

2 Pension Plans suffered damages in connection with its purchases of Powerwave

3 securities.

4 V. DEFENDANTS

5 : 8. Defendant Powerwave engages in the design, manufacture, marketing

6 and sale of wireless solutions for wireless communications networks worldwide. The

7 Company offers antennas, boosters, combiners, cabinets, shelters, filters, radio

8 frequency power amplifiers, remote radio head transceivers, repeaters, tower-mounted

9 amplifiers ("TMI's"), and advanced coverage solutions for use in frequency bands,

10 including cellular, PCS, 3G, and 4G wireless communications networks.

11 Powerwave's common stock was listed and traded on the National Association of

12 Securities Dealers Automated Quotations ("NASDAQ") under the symbol PWAV

13 during the Class Period.

14

9. Defendant Ronald J. Buschur ("Buschur") served as the Company's

15 President and Chief Executive Officer ("CEO") during the Class Period. During the

16 Class Period, Buschur participated in the issuance of false and misleading statements

17 and failed to disclose the true facts about Powerwave's business. At no time during

18 the Class Period did Buschur or any other defendant assert that they were not aware of

19 material aspects of Powerwave's business or finances. Moreover, Buschur issued

70 statements in press releases and led the Company's conference calls with analysts and

21 investors, representing himself as a primary person with knowledge about the

22 Company's business, outlook, financial reports and business practices. In addition to

23 issuing statements throughout the Class Period, Buschur repeatedly had the

24 opportunity to correct the misstatements and omissions by and on behalf of

25 Powerwave, and failed to do so.

26

10. Defendant Kevin Michaels ("Michaels") served as the Company's Chief

27 Financial Officer ("CFO") during the Class Period. During the Class Period, Michaels

28 participated in the issuance of false and misleading statements and failed to disclose

718102_i

A

Case 8:

C-JPR Document 40 Filed 07/23/12 Page 9 of 25 Page ID #:405

1 the true facts about Powerwave's business. At no time during the Class Period did

2 Michaels or any other defendant assert that they were not aware of material aspects of

3 Powerwave's business or finances. Moreover, Michaels issued statements in press

4 releases and led the Company's conference calls with analysts and investors,

5 representing himself as a primary person with knowledge about the Company's

6 business, outlook, financial reports and business practices. In addition to issuing

7 statements throughout the Class Period, Michaels repeatedly had the opportunity to

8 correct the misstatements and omissions by and on behalf of Powerwave, and failed to

9 Idoso.

10

11. Buschur has been with the Company since 2001 and became CEO of

11 Powerwave and a member of the Board of Directors (the "Board") in February 2005.

12 Michaels has been with the Company since 1996. According to the Company's 2010

13 Form 10-K, which was filed with the SEC on February 17, 2011, the Company was

14 small, consisting of approximately 2,100 employees throughout the entire Class

15 Period. The vast majority of these employees - approximately 1,900 - were on

16 manufacturing, quality, supply chain, sales and research and development.

17

12. Defendants Buschur and Michaels (collectively, the "Individual

18 Defendants"), by virtue of their high-level positions with the Company, had access to

19 adverse, undisclosed information about Powerwave's business, operations, financial

statements, markets and present and future business prospects, via internal corporate

21 documents, conversations and connections with other corporate officers and

22 employees, attendance at management and Board meetings and committees thereof,

23 and reports and other information was provided to them as part of their positions.

24

13. By virtue of their high level positions with the Company, the Individual

25 Defendants possessed the power and authority to control the contents ofPowerwave's

26 quarterly reports and other public filings, press releases and presentations to securities

27 analysts, money and portfolio managers and institutional investors, i.e., the market.

28 Each of the Individual Defendants, by virtue of their high level positions with

-5- 718102_i

PR Document 40 Filed 07/23/12 Page 10 of 25 Page ID #:406 Case 8:1

Powerwave, directly participated in the management of the Company and was directly

involved in the day-to-day operations of the Company. The Individual Defendants

were involved in drafting, producing, reviewing and/or disseminating the false and

misleading statements and information alleged herein, and were aware, or recklessly

disregarded, that false and misleading statements regarding Powerwave were being

issued, and approved or ratified these statements, in violation of the federal securities

Ilaws.

14. Powerwave had internal systems that allowed senior management - the

Individual Defendants - to monitor up-to-date quarterly revenues. According to

former employees, the Company used a Hyperion system and a salesforce.com system

Ito provide senior management with updated forecasts and revenues.

15. As officers and controlling persons of a publicly-held company whose

common stock was traded on the NASDAQ during the Class Period, and governed by

the federal securities laws, each of the Individual Defendants had a duty to

disseminate promptly accurate and truthful information regarding the Company's

financial condition and performance, growth, operations, financial statements,

business, markets, management, earnings and present and future business prospects,

and to correct any previously-issued statements that had become materially misleading

or untrue, so that the market price of Powerwave common stock would be based upon

truthful and accurate information. The Individual Defendants' misrepresentations and

omissions during the Class Period violated these specific requirements and

obligations.

VI. SOURCES OF ALLEGATIONS

16. Plaintiffs' allegations are based upon the investigation of plaintiffs'

counsel, including information contained in SEC filings by Powerwave, regulatory

filings and reports, securities analysts' reports and advisories about the Company,

press releases, conference call transcripts and other public statements issued by the

Company, as well as media reports and other sources of information about the

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

71)

21

22

23

24

25

26

27

28

718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 11 of 25 Page ID #:407

1 Company, including information obtained from more than 15 former employees of

2 Powerwave. Information provided by the former employees of Powerwave are

3 reliable and credible because: (a) each of the witnesses worked at Powerwave during

4 or immediately prior to the Class Period; (b) each witness stated that they had personal

5 knowledge of the information provided; (c) the witnesses' job titles and

6 responsibilities show that they had personal knowledge of the information provided;

7 (d) the witness accounts corroborate one another; and (e) the witness accounts are

8 corroborated by other information alleged herein.

9

17. CW1 was a Senior Demand Planner at Powerwave from 2008 until

10 November 2011, when CW1 was laid off. CW1 's duties included analyzing the sales

11 forecasts for Powerwave's North and South American network operator customers for

12 all of Powerwave's products. CW1 's network operator customers included AT&T,

13 Verizon, T-Mobile and several others. During 2011, CW1 reported to Materials

14 Manager Alain Ducharme ("Ducharme"). Ducharme reported to Senior Director of

15 Supply Chain Operations Mike Ryberg ("Ryberg") who reported to Chief Operating

16 Officer ("COO") Mary MaGee ("MaGee"). CWI was involved in determining how

17 and when Powerwave could realize revenues on product sales to North and South

18 American customers. To that end CW1 participated in weekly Sales Operations

19 meetings held every Monday morning in which CW1 assessed just how confident the

7() sales personnel were that projected orders were going to materialize. After those

21 meetings, on Monday afternoons, CW1 met with Powerwave's corporate planning

22 group as part of the larger objective of determining how many orders had already been

23 invoiced in a given quarter (and thereby revenue already recognized), how many

24 orders were "in backlog" (i.e., orders that had been received, but had yet to be

25 fulfilled), and how many orders were projected to come in during the quarter, as well

26 as how many orders needed to come in to meet projected revenue targets for a given

27 quarter. CW1 prepared a Sales and Operations Planning Report - known internally as

28 an "S&OP Report" - that was discussed in the Monday meetings. CW1 also

-7- 718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 12 of 25 Page ID #:408

1 performed a "risk analysis" so that executives could closely monitor the Company's

2 progress in achieving its projected revenues over a given quarter. As part of the risk

3 analysis, CW1 prepared a "Gap Report" which showed Powerwave's present

4 forecasted revenue vs. actual revenue.

5

18. CW2 was a Director of Financial Planning at Powerwave from January

6 12007 until November 2011, when CW2 was laid off. As Director of Financial

Planning, CW2 was responsible for "developing and executing" a forecasting process

8 that began with a "bottoms-up" sales forecast from the Company's sales force and

9 then forecasting expenses and costs to derive forecasts of margins and profits. This

10 forecasting process was undertaken annually and then updated on a quarterly basis.

11 CW2 reported directly to Michaels, but once Treasurer Tom Spaeth ("Spaeth") was

12 hired, CW2 reported to Spaeth, who reported to Michaels. At the end of quarters,

13 CW2 met with Michaels and Spaeth in Michaels' office to discuss end of quarter

14 margins.

15

19. CW3 was a Senior Manager of Strategic Sourcing with Goodman

16 Networks ("Goodman") (an AT&T "Turf Partner" and Powerwave customer), from

17 November 2009 until February 2012 when he was laid off. CW3's role included

18 ordering equipment and products from three primary vendors that Goodman used to

19 build cell-sites on behalf of AT&T. These vendors included Andrews/CommScope,

Powerwave, and a German firm - Kathrein. According to CW3, the primary products

21 purchased from Powerwave were antennas, diplexers and TMIs. Goodman's activity

22 on behalf of AT&T covered the entire U.S.

23

20. CW4 worked at Powerwave as a Senior Inside Sales Rep on

24 Powerwave's Customer Relationship Management ("CRM") team from 1994 until

25 March, 2012 when CW4 was laid off. CW4 was the CRM team member assigned to

26 AT&T. As an Inside Sales Rep, CW4 dealt directly with the Powerwave sales team

27 assigned to AT&T as well as with AT&T personnel. The AT&T personnel CW4 most

28 often dealt with were members of AT&T's supply chain management group which

718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 13 of 25 Page ID #:409

1 was located in Seattle. As an Inside Sales Rep CW4 was essentially responsible for

2 receiving AT&T orders and ensuring that the order terms were not only entered into

3 Powerwave's Oracle system, but also that the orders were fulfilled according to

4 AT&T's delivery requirements. This entailed dealing with Powerwave's supply chain

5 organization to ensure that the products necessary to fulfill orders were being

6 manufactured.

7

21. CW5 started at the Company in 2004 and worked as National Sales

8 Manager for Powerwave's Tier 2 accounts in the U.S. and Canada. These Tier 2

9 accounts included US Cellular, Cricket and MetroPCS. As part of his job, CW5

10 participated in regular sales calls with the various Account Managers, MaGee, and the

11 V.P. of Sales. CW5 left Powerwave of his own volition in June 2011.

12

22. CW6 worked at Powerwave from around February 2007 through

13 November 2011 when CW6, and numerous other employees, were laid off. During

14 CW6's time at the Company CW6 had been Global Inventory Manager. Initially,

15 CW6 reported to Ryberg, but at some point, began reporting to Martin Cooper

16 ("Cooper"). Both Ryberg and Cooper reported to current COO MaGee. CW6

17 continued having dealings with Ryberg even after he began reporting to Cooper. As

18 Global Inventory Manager, CW6 had been primarily responsible for monitoring the

19 levels of component/raw material inventory held by Powerwave facilities around the

7n world. CW6 ensured that Powerwave had adequate quantities of such materials to

21 meet production demands and would also facilitate the movement of component

22 inventory from one location to another depending on the respective needs of the

23 'locations. Another function of CW6's job was to dispose of Excess and Obsolete

24 component inventory. In addition, as part of CW6's job duties, CW6 had insight to

25 the forecasted demand for Powerwave's products. In this regard, CW6 worked with

26 Powerwave's Planners to determine the component and raw material inventory that

27 would be needed to fulfill expected demand.

718102_i

28

Case 8:t

PR Document 40 Filed 07/23/12 Page 14 of 25 Page ID #:410

II VII. FACTUAL BACKGROUND TO DEFENDANTS' SCHEME

A. Nature of Powerwave's Business

23. Powerwave was founded in 1985 and became a public company through

an initial public offering ("IPO") in 1996. The Company sells its products through its

direct sales force, independent sales representatives, and resellers to wireless original

equipment manufacturers ("OEM's") and individual wireless network operators.

Powerwave's customers include the OEM's: Alcatel-Lucent, Ericsson, Huawei,

Motorola, Nokia Siemens and Samsung. Powerwave's network operator customers

include AT&T, Bouygues, Orange, Sprint, T-Mobile, Verizon Wireless and

Vodafone. While defendants repeatedly claimed to have technically superior

products, there were other companies competing for the same business - including

CommScope, Comba Telecom, Fujitsu Limited, Hitachi Kokusai, Japan Radio and

Tyco Electronics. In addition, Powerwave also competes with the OEM's - who are

also customers - Alcatel-Lucent, Ericsson, Huawei, Motorola, Nokia Siemens and

Samsung.

24. During the Class Period, Powerwave sold a relatively few products to a

handful of customers. In fact, according to the Company, Powerwave's sale of its

antennas and base stations represented 90% of Powerwave's business during the Class

Period. In addition, according to the Company, sales to North American customers

represented over 40% of Powerwave' s business during the Class Period.

25. During the Class Period, a substantial portion of Powerwave's sales were

made through resellers or various "Turf Partners." 2 Powerwave's major reseller for

AT&T was Team Alliance. Turf Partners typically purchased Powerwave product

through resellers such as Team Alliance. The Turf Partner would then use the product

2 These "Turf Partners" included: Goodman, Black & Veatch, NSORO and Bechtel.

_10-

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 15 of 25 Page ID #:411

as part of building segments or elements of a network building the wireless cell site or

infrastructure for AT&T. Powerwave's sales to Team Alliance were as follows:

2nd Half ($000's) 3Q10 1Q11 2Q11 2011

Net Sales to Team Alliance $ 171249 $ 19,127 $ 47,779 $ 4,205 As a percent of total Powerwave sales 11% 14% 28% 3%

26. The North American wireless carrier AT&T was one of Powerwave's

largest customers during the Class Period. But, as discussed above, Powerwave did

not sell directly to AT&T, but sold to the Turf Partner - through Team Alliance. The

role of AT&T Turf Partners was acknowledged and explained by Michaels in an

I August 2, 2010 earnings conference call:

One other thing just to note for you. I think on customers, I'm

sure from an operator basis in North America, our overall largest

relationship there is AT&T. We don't necessarily sell everything

directly there. So, it doesn't count as a 10% customer, but we sell

through their Turf Partners and such. So, I think in this relationship it

would be over a 10% customer. It just doesn't show up that way [sic]

technically.

27. During the Class Period, AT&T was going through a transition as it

announced the purchase of T-Mobile on March 20, 2011. According to the New York

Times, the deal "would create the largest wireless carrier in the nation." Also,

according to the New York Times, critics, including Senator Herb Kohl of Wisconsin,

immediately denounced the merger on anti-trust grounds, saying it could lead to

higher prices for consumers. On May 11, 2011, the Senate held hearings on the

proposed merger - and strongly questioned whether the merger should be allowed.

- 11 -

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

718102_i

PR Document 40 Filed 07/23/12 Page 16 of 25 Page ID #:412 Case 8:1

Because of Declining Demand Powerwave Engaged in a Revenue Recognition Scheme that Masked the True Demand for Its Products

Former employees of Powerwave have confirmed that contrary to the

Individual Defendants' claims of strong demand, demand was actually steeply

declining during the Class Period. In fact, contrary to defendants' claims, according

to CW1 and CW3, Powerwave began "seeing a slowdown" with AT&T at least as

soon as when the T-Mobile merger was announced in March 2011. In order to

artificially counteract the slow down in demand, Powerwave engaged in what CW1

called "shady" business practices to try to hide the Company's true financial

condition. Powerwave's "shady" business practices occurred in 3Q10, 4Q10, 1Q11,

and 2Q11 and included improper revenue recognition accounting practices that

violated GAAP and SEC guidance as detailed in §X.

29. CW1, CW4, CW5 and CW6 explained that Powerwave's relationship

with AT&T involved third-party "Turf Partners" that actually built different segments

or elements of AT&T's network and a reseller - Team Alliance - that also processed

orders from the Turf Partners for Powerwave products. In essence, according to CW1,

CW4, CW5 and CW6, a Turf Partner would place its order with Team Alliance, which

would then issue an order to Powerwave and purchase the products with instructions

for Powerwave to drop ship the products directly to the Turf Partner's premises. CW3

confirmed that the Turf Partner Goodman placed its orders for Powerwave products

through Team Alliance.

30. But, according to CW1, the Team Alliance arrangement had another,

"shady benefit" for Powerwave because beginning in 3Q10 and then continuing every

quarter thereafter up until 3Q11, Powerwave was able to ship unneeded product to

Team Alliance in order for Powerwave to make revenue goals. As a quarter drew to

an end, CW1 explained that Powerwave personnel would "look around" at whatever

inventory was unsold and would then obtain "a bulk order" from Team Alliance that

permitted Powerwave to ship these items prior to the end of the quarter. According to

-12-

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

2(1

21

22

23

24

25

26

27

28

IQH-11

718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 17 of 25 Page ID #:413

1 CW1, if Powerwave had "overbuilt" inventory that could not be sold because actual

2 orders for the inventory had not been received, Powerwave could persuade Team

3 Alliance to issue orders for a portion of the inventory. Powerwave would purposely

4 ship the inventory to Team Alliance by boat rather than air from China so as to ensure

5 that the products had shipped and were in transit while delaying delivery by three to

6 four weeks. The delayed delivery was important to Team Alliance because it did not

7 need the product. CW1 understood that Powerwave granted Team Alliance special

8 extended payment terms and rights of return in order to get Team Alliance to accept

9 delivery of the products - products Team Alliance did not need - without having to

10 assume the full responsibility of paying for the products. CW2, CW5 and CW6

11 confirmed that Powerwave engaged in this end-of-quarter practice.

12

31. According to CW1, Powerwave's quarters always ended on a Sunday.

13 I CW1 knew that CW1 would be working that weekend because the bulk orders would

14 I be arranged on the Saturday - the day before the last day of the quarter.

15

32. CW5 stated that from CW5's participation in sales calls, CW5 knew that

16 Powerwave routinely shipped large volumes of inventory to Team Alliance at the ends

17 of quarters. CW5's impression from what CW5 heard on the sales calls was that

18 Powerwave was typically "trying to make a deal" by informing Team Alliance of the

19 inventory Powerwave had on hand and asking what Team Alliance was willing to

7(1 order of that inventory.

21

33. In addition, CW5 stated that the end-of-quarter orders required the

22 extension of discounts and incentives to the customer. It was CW5 's understanding

23 that such discounts and incentives had to be approved by Buschur. CW5 based this

24 perception on "word of mouth" that CW5 heard during various sales calls in which the

25 Account Managers working on a particular deal discussed the terms of the transaction.

26 In those calls, MaGee and the VP of Sales (CW5 could not recall this person's name)

27 would make comments to the effect that a proposed discount or incentive needed

28

- 13 - 718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 18 of 25 Page ID #:414

1 Buschur's approval and/or that a particular discount or incentive had received

2 Buschur's approval.

3

34. According to CW6, "Team Alliance was our best friend at the end of the

4 quarter" and Powerwave was "dependent on Team Alliance to meet numbers," in

5 1Q11 and 2Q11. CW6 said it was definitely the case that Powerwave made large

6 shipments to Team Alliance at the ends of 1Q11 and 2Q11. CW6 knew about the

7 large, end-of-quarter shipments to Team Alliance from CW6's regular meetings and

8 discussions with Planning personnel where it would be discussed that Team Alliance

9 would be taking a particular amount of product from Powerwave. CW6 stated that

10 MaGee knew about the shipments to Team Alliance, but it was Ryberg who seemed to

11 deal directly with Team Alliance so far as getting the orders.

12

35. Once CW6 found out about the Team Alliance shipments at the ends of

13 quarters CW6 began to consider them problematic. Even though these shipments

14 were not under the scope of CW6's responsibility, CW6 questioned why Powerwave

15 would ship so much product to Team Alliance since CW6 did not believe there was

16 any identified end-user for the products. CW6 could not recall the exact size of the

17 end-of-quarter shipments to Team Alliance, but believed they were typically worth

18 millions of dollars.

19

36. In addition, CW6 observed on a number of occasions that the finished

20 goods inventory accounts would increase shortly after the fifth or sixth day of the new

21 quarter. In essence, at the end of a quarter CW6 would see the finished goods

22 inventory levels go down as goods were shipped and then go back up shortly after the

23 new quarter got underway. Although CW6 did not handle product returns - returns

24 were handled by Cooper and MaGee - CW6 strongly suspected that these increases in

25 finished goods reflected returns from Team Alliance.

26

37. CW3 confirmed that in order to get Goodman to accept Powerwave

27 inventory for which AT&T did not order, Powerwave would extend special

28 concessions that were not reflected in theformal documentation for the transactions

-14- 718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 19 of 25 Page ID #:415

1 (e.g., purchase order and invoice). CW3 stated that concessions, made through verbal

2 side agreements, were extended to Goodman by Powerwave in order to get Goodman

3 to issue Purchase Orders and accept delivery. These sales were often authorized by

4 Powerwave employee Ryberg and Powerwave's District Manager assigned to

5 Goodman, Isaac Bustamante ("Bustamante").

6

38. Thus, these special contingent arrangements with reseller Team Alliance

7 and Turf Partner, Goodman, allowed Powerwave to artificially inflate and manipulate

8 its revenues. According to CW1, Powerwave was well aware of the inventory levels

9 at Team Alliance and how much product was needed to fulfill true customer

10 I requirements. CW1 stated that Team Alliance sent their inventory report to

11 Powerwave on an regular basis. According to CW1, Powerwave had to keep track of

12 the inventory being held by Team Alliance because there were times when

13 Powerwave received orders from other customers and Powerwave would use Team

14 Alliance's inventory to fill those other customer orders.

15

39. According to CW2, the approval for the large end-of-quarter deals came

16 from Buschur and Michaels. CW2 based CW2's awareness that Buschur and

17 Michaels were directly involved in approving the end-of-quarter deals and terms

18 because the internal controls at Powerwave required that deals above a certain

19 threshold - say, several million dollars - and involving discounts and other

20 concessions had to be approved by Buschur and Michaels. And "culturally" CW2

21 said that Powerwave was tightly controlled and managed by Buschur and Michaels.

22

40. CW1 knew about the "shady" end-of-quarter "orders" from Team

23 Alliance and the terms of these "orders" through "countless conversations" with

24 CW1 's manager Ducharme - who dealt directly by phone with Team Alliance - in

25 which they would discuss how much unsold inventory was on-hand. In addition,

26 according to CW1, CW1 received e-mails where the last-minute, end-of-quarter Team

27 Alliance orders were discussed. According to CW1, once the amount of unsold

28 inventory was determined "we'd have Team Alliance cut a Purchase Order" for that

- 15 - 718102_i

PR Document 40 Filed 07/23/12 Page 20 of 25 Page ID #:416 Case 8:1

amount of product. CW2 also confirmed that large end-of-quarter "orders" were

obtained from Team Alliance during the Class Period.

41. According to CW1, the "last minute" "orders" that Powerwave got from

Team Alliance in 3Q10, 4Q10, 1Q1 1 and 2Q11 were very big - at least $15 million

each quarter and as high as $25 million in a quarter. CW1 stated that the last-minute

bulk orders to Team Alliance were done to close the gap in forecasted sales for the

quarter. Additionally, according to CW1, salesmen Lance Craft ("Craft") and Greg

Moetl ("Moetl") were forced by COO MaGee to inflate forecasted sales.

42. CW2 corroborated CW1, explaining that the large end-of-quarter deals

made up a large portion of quarterly revenue during this time. CW2 said that CW2

"didn't like" the large end-of-quarter orders, but "was powerless to change it." CW2

and other personnel often wondered "why we were operating this way" and concluded

that "management was not competent."

43. Bogus revenue from Team Alliance was critical to Powerwave during the

Class Period. This is confirmed in Powerwave's SEC filings. See ¶25. On May 5,

2011, Powerwave filed its Form 10-Q for the quarterly period ended April 3, 2011 and

disclosed that "[for the first quarter of 2011, Nokia Siemens accounted for

approximately 25% of total net sales, [and] Team Alliance, one of the Company's

North American resellers accounted for approximately 14% of total net sales." On

August 10, 2011, Powerwave filed its Form 10-0 for the six months ended July 3,

2011 and disclosed that "for the first half of 2011, total sales to Team Alliance, one of

our North American resellers, accounted for approximately 22% of sales." In

addition, the August 10, 2011 Form 10-Q revealed that "[for the second quarter of

- 16-

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

718102_i

Case 8:1

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

PR Document 40 Filed 07/23/12 Page 21 of 25 Page ID #:417

112011, sales to Team Alliance, one of our North American resellers, accounted for

II approximately 28% of our total sales. ,3

44. One particularly egregious shipment of product to Team Alliance

occurred at the very end of 1Q11. At that time, CW1 said that Powerwave knowingly

and deliberately shipped product that it knew did notfunction and which had been

"put aside by quality" because it was "bad product. ,4 According to CW1,

Powerwave shipped the product - which were a new type of LTE Antenna - to Team

Alliance as part of the end-of-quarter bulk order "with the promise to replace" the

defective products once Powerwave had functional products available in a later

quarter. CW1 recalled being in a meeting in which Ryberg spoke by phone to the

Powerwave factory in China directing them to ship the defective products and in a

later meeting hearing Ryberg tell the Chinese factory the specific products that needed

to be replaced.

45. CW1 could not recall exactly how many of the defective products went

out in the 1Q11 shipment, but estimated that many thousands of the products were

shipped; the selling price of the products ranged from $700413,000 so the aggregate

amount was significant and at least $15 million. Throughout 2011, "we were working

on swapping out" the defective products, but the situation had not been resolved as of

CW1 's lay-off in November 2011 at which time "we were still trying to get [the

products] built correctly" and Pow..eve "still owed Team Alliance good"

replacements.

46. During 3Q11 Team Alliance balked at accepting anymore of the

Powerwave inventory and, according to CW1, "said 'no more." In essence,

In the February 28, 2012 Form 10-K, for the fiscal year ended January 1, 2012, Powerwave revealed that "[for fiscal 2011, sales to Team Alliance, one of our North American resellers, accounted for approximately 16% of revenues." 4

All citations are omitted and emphasis is added unless otherwise noted.

-17- 718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 22 of 25 Page ID #:418

1 according to CW1, Team Alliance "wouldn't allow us" to ship any more product and

2 "drew the line." By 3Q11, Team Alliance was holding very large quantities of

3 Powerwave product for which there was no identified or confirmed end-user demand

4 - CW1 estimated there was as much as $40 million of such inventory (per its "retail

5 value"). In fact, CW1 heard from Ducharme during 3Q11 that far from taking on

6 additional Powerwave product, Team Alliance wanted to return to Powerwave the

7 excessive product it was already holding.

8

47. CW2 confirmed that because of the large end-of-quarter "orders" in

9 1Q11 and 2Q11, Powerwave was unable to duplicate such deals in 3Q11. During the

10 Class Period, CW2 heard from co-workers at Powerwave that "we had filled the

11 channels in 1Q and 2Q" 2011.

12

48. Because ofCWI's position as Senior Demand Planner, CW1 was acutely

13 aware of the Company's business with AT&T. CW1 said that Powerwave began

14 "seeing a slowdown" in business with AT&T as soon as the AT&T/T-Mobile merger

15 I was announced in March 2011.

16

49. CW3 confirmed this. According to CW3, around the time of AT&T's

17 proposed merger with T-Mobile, March 2011, AT&T began drastically slowing down

18 when it wanted new cell-sites built. CW3 emphasized that not only was Powerwave

19 fully apprised of the drop-off in AT&T new cell-site construction and attendant drop-

20 off in purchasing by Goodman, but also that there was no indication whatsoever going

21 into and during 3Q11 that the situation would improve. When the drop-off in new

22 AT&T cell-site construction activity began, in 1Q11 according to CW3, CW3

23 promptly notified various Powerwave personnel by email, telephone conversation, and

24 in-person meetings that Goodman was going to delay and push-out the delivery of any

25 existing orders they had placed with Powerwave.

26

27

718102_i

28

Case 8:t

PR Document 40 Filed 07/23/12 Page 23 of 25 Page ID #:419

1 VIII. DEFENDANTS' FALSE STATEMENTS AND OMISSIONS ISSUED DURING THE CLASS PERIOD

2

3 50. The Class Period commences on October 28, 2010. On that date

4 Powerwave issued a press release announcing its financial results for its third quarter,

5 the period ending October 3, 2010. For the quarter, the Company reported net sales of

6 $156.8 million, compared with $139.0 million in the third quarter of fiscal 2009.

7 Defendant Buschur commented on the results, stating, in pertinent part, as follows:

8 "For the third quarter of 2010, we were able to show growth of 12.8%

9 over the same period last year.... " "More importantly, we were able to

10 continue our improvements in our gross margins for this year, with the

11 added benefit of demonstrating strong profitability on both a GAAP and

12 pro forma basis for the third quarter. While we continue to experience

13 longer than normal supply chain lead times and global macro economic

14 issues which continue to impact our business, we see signs of

15 improvement in overall demandfor wireless infrastructure equipment.

16 In particular, we believe that strong North American wireless capital

17 spending patterns should remain throughout the next year. We will

18 continue to work to position Powerwave to capitalize on the long-term

19 growth opportunities within the global wireless infrastructure

20 marketplace."

21 51. Following the issuance of the press release, also on October 28, 2010,

22 Powerwave held a conference call with analysts and investors to discuss the

23 Company's earnings and operations. During the conference call, defendants Michaels

24 and Buschur made positive statements about the Company, current demand, and its

25 operations.

26 52. On November 2,2010, Powerwave filed its quarterly report on Form 10-

27 Q for the quarterly period ending October 3, 2010. In the 3Q10 Form 10-Q

28 defendants emphasized that Powerwave has "maintained [its] overall market share

7181021 -19-

Case 8:1

PR Document 40 Filed 07/23/12 Page 24 of 25 Page ID #:420

1 within the wireless communications infrastructure equipment market," and that its

2 "proprietary design technology is a further differentiator for our products."

3

53. On February 1, 2011, the Company issued a press release announcing

4 financial results for 4Q10, the period ending January 2, 2011, which reported net sales

5 of $175.6 million, compared to $142.6 million for the same period the prior year.

6 Defendant Buschur commented on the results, stating, in pertinent part, as follows:

7

"For the fourth quarter of 2010, we were able to show growth of 23%

8

over the same period last year and 12% sequentially over the third

9

quarter of this year. . . ." "More importantly, we were able to continue

10

our improvements in our operating income for this year, with the added

11

benefit of demonstrating strong profitability on both a GAAP and pro

12

forma basis for the fourth quarter and year results. We continue to see

13

signs of improvement in overall demand for wireless infrastructure

14

equipment, driven globally by the continued increase in demand for

15

smartphones and the requirements for faster data transmission rates. We

16

are continuing to work to position Powerwave to capitalize on the long-

17

term growth opportunities we believe are available within the global

18

wireless infrastructure marketplace."

19

54. Following the issuance of the press release, also on February 1, 2011,

20 Powerwave held a conference call with analysts and investors to discuss the

21 Company's fiscal 2010 earnings and operations. During the conference call,

22 defendants Michaels and Buschur made positive statements about the Company and

23 its current operations. Buschur bragged that for the fiscal year 2010, "we met our

24 annual guidance," and that 2010 was Powerwave' s "first fully profitable year on a

25 GAAP basis since 2005." Michaels stated that Powerwave was establishing a fiscal

26 2011 annual revenue range "of $650 million to $680 million." Michaels added that

27 "[t]he midpoint of this range represents annual growth of 12% which we believe is

28 above the expected growth rates for the industry."

-20- 718102_i

Case 8:1

PR Document 40 Filed 07/23/12 Page 25 of 25 Page ID #:421

1

55. During the February 1, 2011 conference call, Buschur also made the

2 II following statements:

3

As you know, during the last few years we completed our

4

manufacturing consolidation activities, which has enabled Powerwave to

5

have a highly competitive, low costs manufacturing structure that is

6

highly flexible and scalable without compromising our superior quality

7

and our leading edge technology and product solutions. Our focus on

8

expense management has positioned this Company to be truly a lean and

9

mean operation.

10 * * *

11

The demand in the Wireless data is exploding, as can be seen by the

12

exponential growth in the use of Smart Phones utilizing voice, video and

13

data. This demand is fueling requirements for cost effective

14

infrastructure deployments for both upgrading to existing 2G, 3G, and

15

4G deployment technologies. We believe that Powerwave has the

16

products and solutions necessary for these types of cost effective

17

deployments, and we are well positioned to benefit from this demand.

18 * * *

19

Charles Johns - Canaccord Genuity - Analyst

20

Great. And then Ron, maybe a last one for you. Just wondering,

21

when you look out longer term and think of the LTE and the various

22

carrier deployments that should occur this year, maybe you could just

23

talk about Powerwave's strategic position relative to these LTE builds.

24

Ron Buschur - Powerwave Technologies - President and CEO

25

I think we're in an excellent position, when I look at the selection

26

criteria of our products and solutions across the carrier arena. I think, as

27

you can see from our antenna deployments, as well as our tower

28

mounted amplifiers in some of our base stations subsystems, we have

718102_i -21-

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 1 of 25 Page ID

#:422

had tremendous growth in the LTE segment of our business, specifically

with two large operators here in North America that are building out and

one in Europe. So I'm very happy with the selection criteria and

certainly our ability to deliver large quantities - not samples, but large

volume quantities - all of these solution sets across the product portfolio. * * *

We think that we have a technology advantage today in our

product offering when you look at the companies that have chosen us

and the awards and the percentage of the awards that we've been

awarded, when you look at percent of business.

56. During the February 1, 2011 conference call, Michaels emphasized that

I Powerwave was actually being "conservative" in its 2011 guidance:

I think to further on what Ron's saying, we obviously think that we're

going to grow faster than the market in our segment. But I think the

point you're asking, which I would agree with, is that no, we're not

looking for huge upsides. We think the market, we think we're

positioned well, and it isn't counting on our verticals like the government

business to be major contributors in the year. As Ron mentioned, we're

still at the early stage there. The actual revenue contribution is quite

1 rx- r r T fh t-ilr c 11 x tcvi 11 rl c ,

arm' r lc i- 1.J VV • L)tJ I Lj1jjjj. J /%.1 I11 VV %. VV %.J 41I L/I11

reasonably conservative in our guidance and that there is good upside

potential.

57. On February 1, 2011, Deutsche Bank issued a report on Powerwave.

Based on defendants' positive statements about demand, Deutsche Bank adjusted their

estimates for Powerwave's 2011 revenue as follows: (1) 1Q11E was $156m, is

$160m; (2) 2Q11E was $158m, is $162m; and (3) 2011E was $639m, is $654m.

Deutsche Bank also noted that "[t]he company again said that the second half of the

year will provide most of the growth."

-22- 17181021

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

'WI

21

22

23

24

25

26

27

28

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 2 of 25 Page ID

#:423

1

58. On February 17, 2011 Powerwave filed its annual report on Form 10-K

2 for the fiscal year 2010, ended January 2, 2011. In the 2010 Form 10-K, defendants

3 emphasized that Powerwave has "maintained [its] overall market share within the

4 wireless communications infrastructure equipment market," and that its "proprietary

5 design technology is a further differentiator for our products." In its 2010 Form 10-K,

6 I Powerwave also reported revenues of $591.5 million and earnings of $0.03 for the

7 I fiscal year.

8

59. By virtue of the facts alleged in §VI, VII and X, and the other facts set

9 forth herein, it may be strongly inferred that defendants knew or recklessly

10 disregarded that the statements in the October 28, 2010 and February 1, 2011 press

11 releases, the October 28, 2010 and February 1, 2011 conference calls, and the

12 financial information discussed therein and in the February 17, 2011 Report on Form

13 10-K and November 2, 2010 Form 10-Q, would be, and were, misleading to and

14 operated as a fraud upon investors. Considered as a whole, defendants'

15 representations about the Company's revenue and the purported continuing strength of

16 Powerwave's performance along with its prospects for driving further growth,

17 continued to mislead investors by presenting an overly-optimistic picture of

18 Powerwave's results, while failing to disclose, and actively concealing or recklessly

19 ignoring, conditions which created material and significant risks to the Company.

Together, these facts and the other allegations herein give rise to a strong inference

21 that defendants knew or recklessly disregarded the actual condition of the Company at

22 the time they delivered their statements. In particular, the foregoing statements were

23 false and recklessly misleading in at least the following respects:

24

(a) Defendants concealed the extent to which the Company's revenues

25 had been achieved through improper and unsustainable sales practices, including their

26 over-reliance on quarter-end bulk sales that were unconnected to actual demand. See

27 §VI, VII and X.

28

718102_i -23-

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 3 of 25 Page ID

#:424

1

(b) Defendants omitted disclosure of the true nature and substance of

2 I the sales with Team Alliance and Turf Partners in the February 17, 2011 Report on

3 I Form 10-K and statements detailed above, or the material risks those practices created

4 Ito Powerwave's future financial results. See §VI, VII and X.

5

(c) Powerwave's reported financial results were the result of an

6 accounting scheme employing improper accounting practices in violation of GAAP

7 and SEC revenue recognition requirements. See § § VI, VII and X.

8

(d) At the time the statements were made, internal forecasting data and

9 sales reports that were circulated among the Company's executives and management

10 contradicted the positive outlook the defendants' public statements were intended to

11 create. See §VI, VII and X.

12

(e) The financial results created a false and misleading appearance of

13 demand for Powerwave's products because the reported revenues had been artificially

14 inflated. See §VI, VII and X

15

(f) Powerwave's purported demand was a result of unsustainable

16 business practices of forcing more products through its sales channels with end-of-

17 quarter bulk sales than Powerwave's customers could reasonably expect to absorb,

18 thereby cannibalizing sales from future periods. See §VI, VII and X.

19

(g) Powerwave's financial guidance was false and lacked a reasonable

2 00 basis, because it included fiCttOU5 bulk sales that were improperly recorded in

21 violation of GAAP. See §VI, VII and X.

22

60. On March 17, 2011, Brigantine Advisors issued a report on Powerwave,

23 "Initiating Coverage with a Buy Rating." The report noted that Powerwave had

24 exhibited new products to the analyst, Kevin Dede, "behind closed doors at Mobile

25 World Congress in Barcelona this past February," which led the analyst to make his

26 recommendation and set a $5 price target. Powerwave was then trading at $3.78. One

27 of the new products that Powerwave demonstrated was its "MIMO Active Array

28 Antenna solution that integrates basestation electronics for improved coverage and

718102_i -24-

Case 8

:12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 4 of 25 Page ID

I #:425

lower operating costs on account of both the space and energy savings." According to

Powerwave, the MIMO integrated antenna was "involved in network testing" at that

time, "and should be generally available in [the] September quarter."

61. The March 17, 2011, Brigantine Advisors report went on to discuss the

5 "mobile infrastructure industry" generally and noted that "third party research

6 providers appear to believe that the mobile infrastructure industry should see

7 lackluster growth this year." Specifically, the report noted that iSuppli - a

8 technology market research firm - "projects that the global mobile infrastructure

9 market should return to modest growth of 3.6% in 2011." And, the Dell'Oro Group -

10 a networking and telecommunications industries market research firm - "concurs with

11 iSuppli" and projects "roughly 4%" growth in 2011. The Brigantine Advisors report

12 contrasts what the market experts are expecting with what Powerwave said it expects

13 for 2011, "the mid-point" of Powerwave' s 2011 guidance, "$655 million represents

14 12% annual growth for the current year."

15

62. On March 24, 2011, after meeting with Powerwave's management on

16 March 23, 2011, CL King & Associates issued an analyst report on Powerwave,

17 "[u]pgrading to Buy from Neutral." The report noted that the "overall tenor of the

18 meeting was highly upbeat." That same day, March 24, 2011, WJB Capital Group

19 issued an analyst report, noting that they had met with CFO Michaels, "who suggested

that wireless spending trends remain strong, driven by North America."

21

63. Following the release of these misleading statements, Powerwave's stock

22 began climbing steadily from $1.91 on October 28, 2010 to $4.69 on May 2, 2011.

23

64. On May 5, 2011, Powerwave issued a press release announcing its

24 financial results for its first quarter, the period ending April 3, 2011. For the quarter,

25 the Company reported net sales of $136.6 million, compared to $114.5 million for the

26 same period the prior year. Defendant Buschur commented on the results, stating, in

27 pertinent part, as follows:

28

718102_i - 25 -

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 5 of 25 Page ID

#:426

1

The first quarter revenue was impacted by delays we encountered

2

ramping up one of our new LTE products. . .. "We believe that we

3

have resolved the production issues that impacted our revenues for the

4

first quarter. Looking ahead for the remainder of this year, we continue

5

to believe that we are on track for meeting our annual revenue

6

guidance. There are signs of improving demand for global wireless

7

infrastructure for the remainder of 2011. We believe that Powerwave is

8

in an excellent position to build upon and capture the long-term growth

9

opportunities that are in the wireless infrastructure marketplace."

10

65. Following the issuance of the press release, on May 5, 2011, Powerwave

11 held a conference call with analysts and investors to discuss the Company's earnings

12 and operations. During the conference call, defendants Michaels and Buschur made

13 positive statements about the Company and its operations. Michaels stated that 1Q11

14 revenues were impacted by the fact that "the first quarter is usually the slowest quarter

15 of the year." Michaels also explained that 1Q revenues "were impacted by production

16 delays we encountered while ramping up one of our new LTE products." He added

17 that the production delays on the new LTE product "impacted our revenue for the first

18 quarter by approximately $8 million." Michaels emphasized that Powerwave had

19 "resolved this issue going forward to meet our customers' increased demand."

7(1 Further bolstering his statements about increased demand, Michaels said that

21 Powerwave had "reviewed [its] market forecast and current demand trends and we

22 continue to believe that we will achieve our fiscal 2011 annual revenue range of $650

23 million to $680 million."

24

66. On the same May 5, 2011 conference call, Buschur explained that the

25 disappointing first-quarter results were due to "unique issues" that "are behind us,"

26 and emphasized that "[t]he demand for Powerwave's advanced products are

27 extremely strong." In addition, Buschur added:

28

718102_i -26-

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 6 of 25 Page ID II #:427

1

As Kevin noted, we continue to believe that we will be able to

2

achieve our annual revenue guidance of $650 million to $680 million.

3

As you know, we typically do not give quarterly guidance, but due to

4

the current results and the fact that we have been seeing an increase in

5

demand for our products, we believe the revenue for Q2 will be

6

between $170 million and $180 million. We are confident that the

7

demand should continue to improve throughout this year.

8 * * *

9

We believe that Powerwave has the product and solutions necessary for

10

these types of cost-effective deployments, as well as we are well

11

positioned to benefit from this demand.

12

67. During the May 5, 2011 conference call, defendants also responded to a

13 number of questions regarding the "surge in demand" that defendants were reporting:

14

Mike Walkley - Canaccord Genuity - Analyst

15 • . . Ron, with the strong sequential guidance it appears you didn't lose

16

any sales to a competitor due to issues with LTE delays. Can you give

17

us a little more color on maybe what caused the delay and also, can you

18

update us on the competitive environment?

19

Ron Buschur - Powerwave Technologies - President and CEO

20 • . . We may have underestimated the ability to ramp that product so

21

quickly with the volume demand that was placed upon us, but we have

22

that behind us, and you're correct, we don't believe that it hurt our

23

market share. In fact, we're seeing demand across the board, not just

24

with the one operator for our LTE products.

25 * * *

26

Ted Moreau - WBJ Capital - Analyst

27

28

718102_i -27-

Case 8

2-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 7 of 25 Page ID #:428

1 • . . On the guidance for Q2, it's a pretty big snap back and so I'm just

2

wondering if— how comfortable do you feel about your manufacturing

3

capacity and your ability to handle the surge in demand for Q2?

4

Ron Buschur - Powerwave Technologies - President and CEO

5

Well, I think, Ted, we feel very comfortable that we can achieve that

6

range.

7

Ted Moreau - WBJ Capital - Analyst

8

Okay, great. And then one of the North American carriers spent heavily

9

in Qi, really seems like they're front-end loading their full year. So, do

10 you think once you get through Q2 does 2011 for North America flatten

11

out a little bit, or do you still - would you still see nice growth as the

12

year progresses?

13

Ron Buschur - Powerwave Technologies - President and CEO

14

We - I guess I don't see that same type of rollout, Ted, yet. I see a

15 pretty healthy growth in North America across most of the operators

16

the remainder of 2011, and then assuming that the merger of the two

17

large operators takes place as scheduled, I think 2012 should be a pretty

18

good year, as well.

19

68. Powerwave's constant assurances of increased revenue from strong

20 demand was adopted by financial analysts. The next day, May 6, 2011, Brigantine

21 Advisors issued a report on Powerwave titled: "Disappointing March Report, but

22 Raising Sales Estimates on Expected Strong June Demand; Reiterate Buy." The

23 report notes that "Powerwave's March quarter report of $136.6M . . . missed our

24 $150.0 and $0.04 estimate and consensus estimates of$151.8M and $0.03 last night."

25

69. That same day, May 6, 2011, WJB Capital Group issued a report on

26 Powerwave titled "Messier Than It Should Have Been." The report noted that

27 Powerwave "missed" analyst expectations. "Despite the Q miss," given

28 Powerwave' s positive statements on May 5, 2011, WJB Capital Group stated that

- 28 - 718102_i

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 8 of 25 Page ID

#:429

1 Powerwave "doesn't appear to have lost market share or demand." Merriman Capital

2 also issued a report that day, "remain[ing] positive" on Powerwave given defendants'

3 claims of "broad based demand from operators as well as an alleviation of production

4 issues."

5

70. On May 9, 2011, Powerwave filed its quarterly report on Form 10-Q for

6 the quarterly period ending April 3, 2011. In the 1Q11 Form 10-Q defendants again

7 emphasized that Powerwave has "maintained [its] overall market share within the

8 wireless communications infrastructure equipment market," and that its "proprietary

9 design technology is a further differentiator for our products."

10

71. On May 10, 2011, following meeting with management at the 2011

11 I TIMT Conference, Jefferies issued a report on Powerwave. In the report, Jefferies

12 I noted that Powerwave said that "order patterns are tracking well."

13

72. On May 24, 2011, Powerwave participated in the Barclays Capital Global

14 I Communications, Media, and Technology Conference and reiterated that demand was

15 "improving and strong." Michaels made the following statements:

16

Last quarter, we had some production issues on a new product.

17

We had yield issues on it. We did not get as high yield as we expected.

18

We, since the end of the quarter, have significantly improved our yield.

19

We have caught up with the stuff that we missed in that quarter.

20

At the same time, demand has continued to be improving and

21

strong, so we're feeling fairly confident today in the outlook in the

22

demand side of the market. It is tracking to what we expected, which

23

initially in the first quarter, the very beginning of the first quarter, was a

24

little slower than we expected. It didn't start picking up until toward the

25 end of the first quarter and a little too late for us, but it certainly has

26

improved now. So we're fairly - things are tracking what we expect.

27

On the production side, we're feeling reasonably confident with

28 our production capabilities and think that we have things under control

718102_i -29-

Case 8 :12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 9 of 25 Page ID

#:430

1

and can meet the requirements that are out there. So, we're feeling

2

reasonably confident.

3

73. By virtue of the facts alleged in §VI, VII and X, and the other facts set

4 forth herein, it may be strongly inferred that defendants knew or recklessly

5 disregarded that the statements in the May 5, 2011 press release, the May 5, 2011

6 conference call, the May 24, 2011 Conference, and the financial information discussed

7 there and in the 1Q11 Report on Form 10-Q, would be, and were, misleading to and

8 operated as a fraud upon investors. Considered as a whole, defendants'

9 representations about the Company's revenues and the purported continuing strength

10 of Powerwave's performance along with its prospects for driving further growth,

11 continued to mislead investors by presenting an overly-optimistic picture of

12 Powerwave's results, while failing to disclose, and actively concealing or recklessly

13 ignoring, conditions which created material and significant risks to the Company.

14 Together, these facts and the other allegations herein give rise to a strong inference

15 that defendants knew or recklessly disregarded the actual condition of the Company at

16 the time they delivered their statements. In particular, the foregoing statements were

17 false and recklessly misleading in at least the following respects:

18

(a) Defendants concealed the extent to which the Company's revenues

19 had been achieved through improper and unsustainable sales practices, including their

20 over-reliance on quarter-end bulk sales that were unconnected to actual demand. See

21 §VI, VII and X.

22

(b) Defendants omitted disclosure of the true nature and substance of

23 the sales with Team Alliance and Turf Partners in the May 9, 2011, Form 10-Q and

24 statements detailed above, or the material risks those practices created to Powerwave's

25 future financial results. See §VI, VII and X.

26

(c) Powerwave's reported financial results were the result of an

27 accounting scheme employing improper accounting practices in violation of GAAP

28 and SEC revenue recognition requirements. See §VI, VII and X.

7181021 -30-

Case 8:12-cv-00222-CJC-JPR Document 40-1 Filed 07/23/12 Page 10 of 25 Page ID I #:431

1

(d) At the time the statements were made, internal forecasting data and

2 sales reports that were circulated among the Company's executives and management

3 1 contradicted the positive outlook the defendants' public statements were intended to

4 create. See §VI, VII and X.

5

(e) The financial results created a false and misleading appearance of

6 demand for Powerwave's products because the reported revenues had been artificially

7 I inflated. See §VI, VII and X.

8

(f) Powerwave's purported demand was a result of unsustainable

9 business practices of forcing more products through its sales channels with end-of-

10 I quarter bulk sales than Powerwave's customers could reasonably expect to absorb,

11 I thereby cannibalizing sales from future periods. See §VI, VII and X.

12

(g) Powerwave's financial guidance was false and lacked a reasonable

13 I basis because it included fictitious bulk sales that were improperly recorded in

14 violation of GAAP. See §VI, VII and X.

15 IX. THE TRUTH BEGINS TO EMERGE

16

74. On July 12, 2011, Powerwave issued a press release to provide a "Second

17 Quarter Update." In the press release, the Company reduced the 2Q11 guidance it had

18 given on May 5, 2011. The Company reported that for its second fiscal quarter, the

19 period ending July 3, 2011, it "anticipates that revenues for its fiscal second quarter

"Ii ended July 3, 2011 willbe in the range of $168 million to $172 million. This updates

21 Powerwave's previously announced expectations of revenues for the second quarter."

22 Defendant Buschur commented on the announcement, stating, in pertinent part, as

23 follows:

24