Embed Size (px)

Citation preview

This English translation of the Offering Circular is being provided for the convenience of certain investors only. The official Offering Circular has been prepared in Chinese, and investors are only entitled to rely on the official Chinese Offering Circular. If there are any differences between the Chinese Offering Circular and this English translation of the Offering Circular, the Chinese Offering Circular will prevail.

Offering Circular

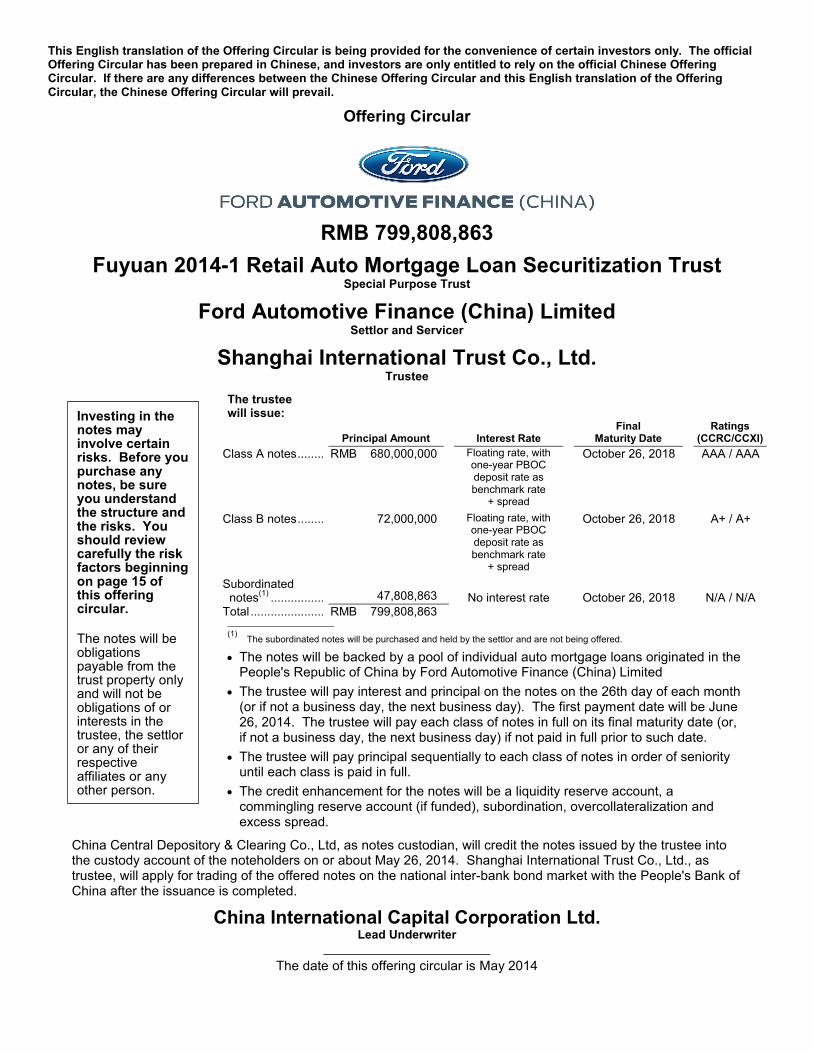

RMB 799,808,863

Fuyuan 2014-1 Retail Auto Mortgage Loan Securitization Trust Special Purpose Trust

Ford Automotive Finance (China) LimitedSettlor and Servicer

Shanghai International Trust Co., Ltd.Trustee

The trustee will issue:

Principal Amount Interest RateFinal

Maturity DateRatings

(CCRC/CCXI)

Class A notes................................RMB 680,000,000 Floating rate, with one-year PBOC deposit rate as benchmark rate

+ spread

October 26, 2018 AAA / AAA

Class B notes................................72,000,000 Floating rate, with one-year PBOC deposit rate as benchmark rate

+ spread

October 26, 2018 A+ / A+

Subordinated notes

(1)................................47,808,863 No interest rate October 26, 2018 N/A / N/A

Total ................................RMB 799,808,863________________________

(1)The subordinated notes will be purchased and held by the settlor and are not being offered.

The notes will be backed by a pool of individual auto mortgage loans originated in the People's Republic of China by Ford Automotive Finance (China) Limited

The trustee will pay interest and principal on the notes on the 26th day of each month (or if not a business day, the next business day). The first payment date will be June 26, 2014. The trustee will pay each class of notes in full on its final maturity date (or, if not a business day, the next business day) if not paid in full prior to such date.

The trustee will pay principal sequentially to each class of notes in order of seniority until each class is paid in full.

The credit enhancement for the notes will be a liquidity reserve account, a commingling reserve account (if funded), subordination, overcollateralization and excess spread.

China Central Depository & Clearing Co., Ltd, as notes custodian, will credit the notes issued by the trustee into the custody account of the noteholders on or about May 26, 2014. Shanghai International Trust Co., Ltd., as trustee, will apply for trading of the offered notes on the national inter-bank bond market with the People's Bank of China after the issuance is completed.

China International Capital Corporation Ltd.Lead Underwriter

_________________________

The date of this offering circular is May 2014

Investing in the notes may involve certain risks. Before you purchase any notes, be sure you understand the structure and the risks. You should review carefully the risk factors beginning on page 15 of this offering circular.

The notes will be obligations payable from the trust property only and will not be obligations of or interests in the trustee, the settlor or any of their respective affiliates or any other person.

2

TABLE OF CONTENTS

Reading this Offering Circular ........................4

Important Information ......................................4

Transaction Parties ..........................................5

Transaction Structure Diagram.......................6

Transaction Parties and Documents Diagram..........................................................7

Rights and Responsibilities of Transaction Parties.......................................8

Summary ...........................................................9

Risk Factors....................................................15

Settlor and Servicer .......................................23

General ......................................................23

Registration and Financial Information..............................................23

Securitization Experience ..........................24

Origination and Underwriting .....................24

Portfolio Quality .........................................26

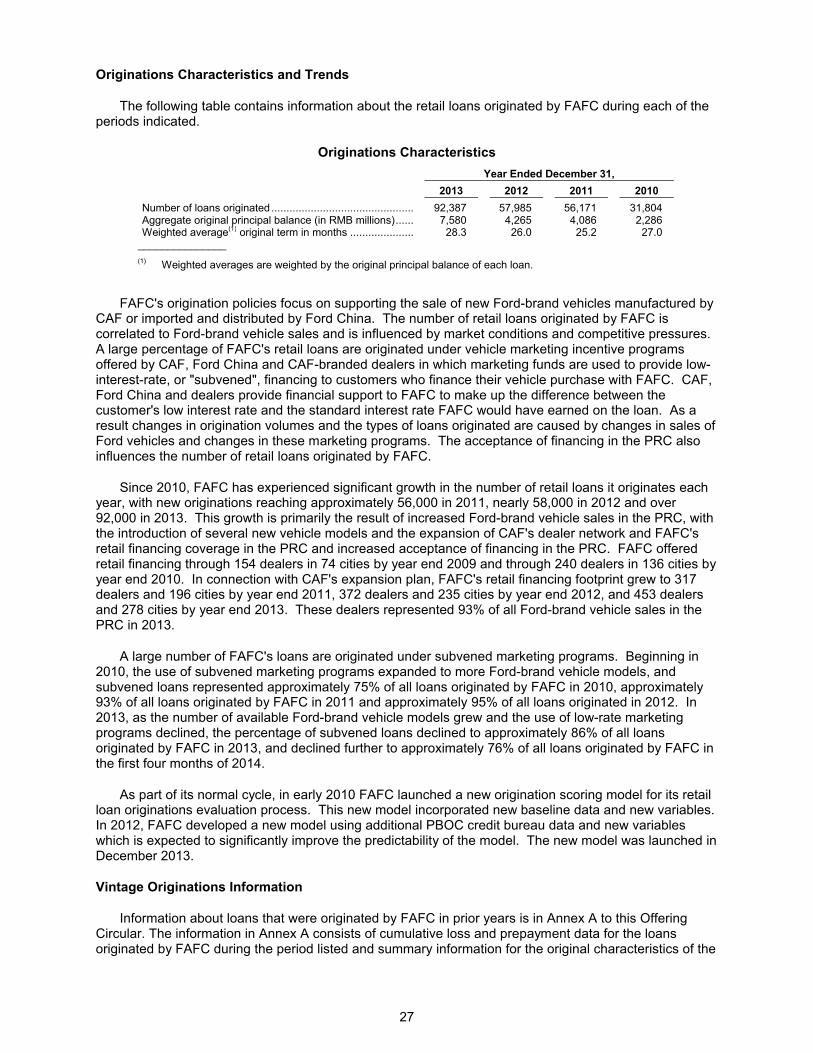

Originations Characteristics and Trends ....................................................27

Vintage Originations Information ...............27

Servicing Experience .................................28

Servicing and Collections ..........................28

Delinquency and Credit Loss Experience and Trends ..........................29

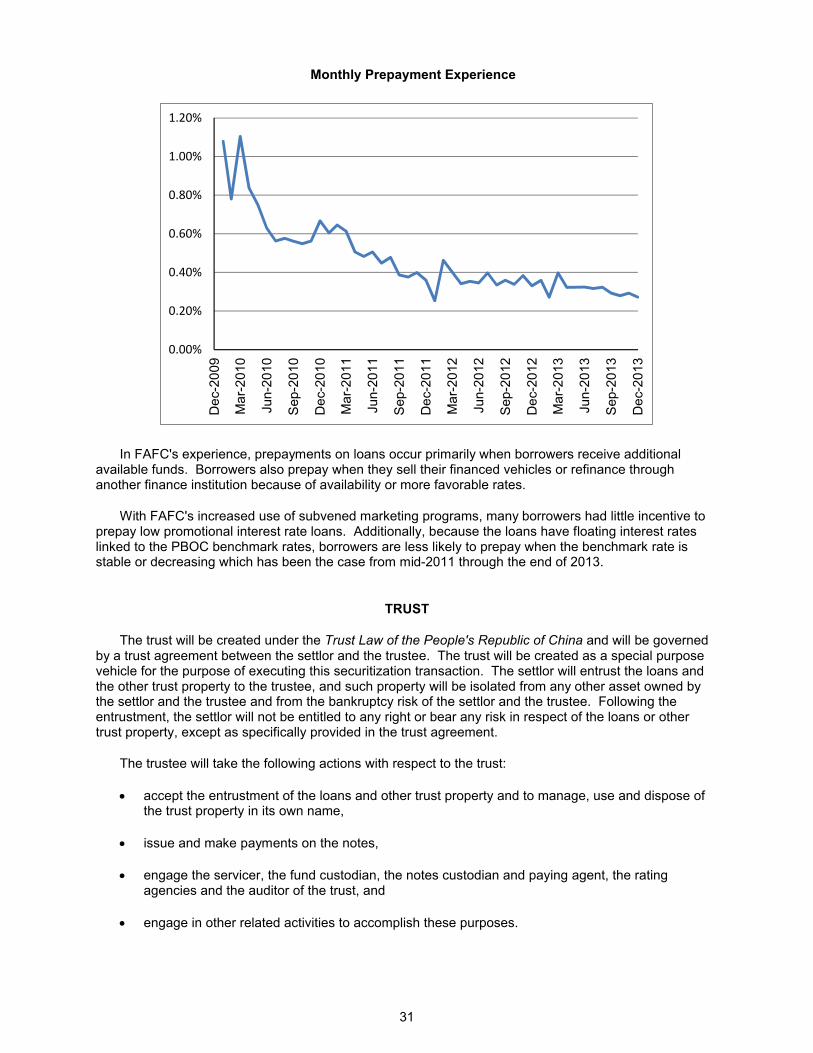

Prepayment Experience and Trends .........30

Trust.................................................................31

Trustee.............................................................32

General ......................................................32

Registration and Financial Information..............................................32

Securitization Experience ..........................32

Fund Custodian ..............................................33

General ......................................................33

Registration and Financial Information..............................................33

Securitization Experience ..........................33

Lead Underwriter............................................33

General ......................................................33

Registration Information.............................34

Securitization Experience ..........................34

Statement of Affiliations ................................34

Loans...............................................................34

Eligibility Criteria for the Loans ..................34

Types of Loans ..........................................35

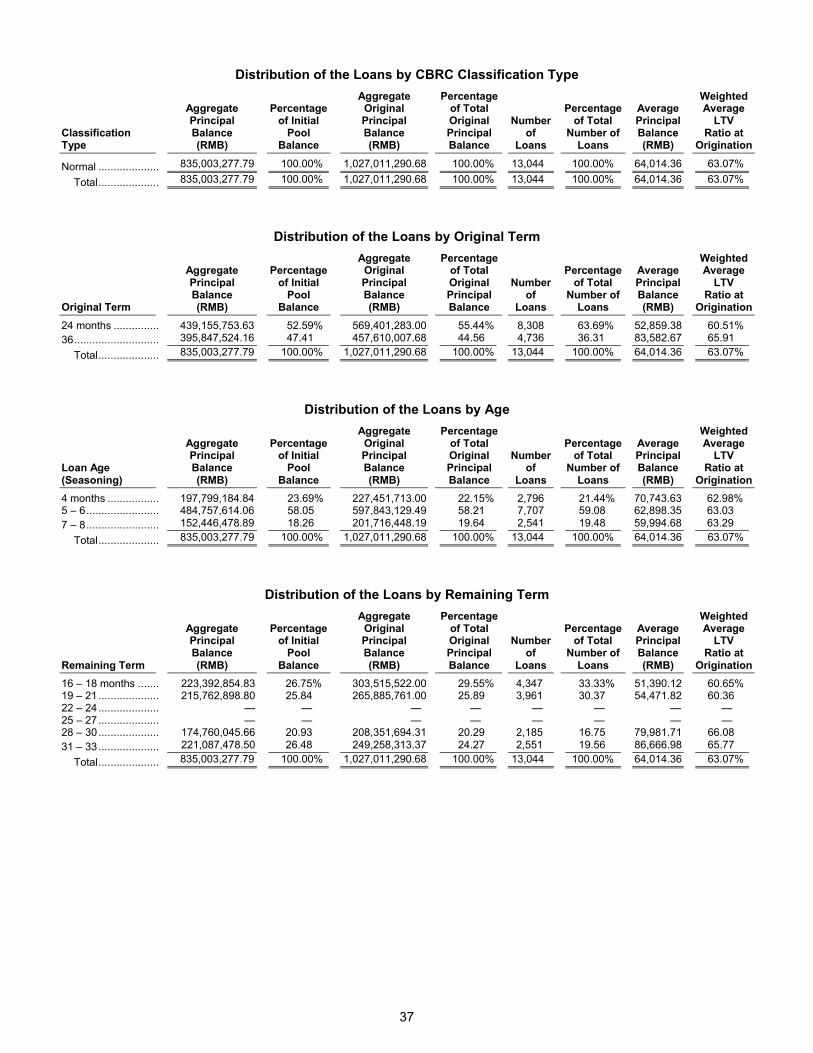

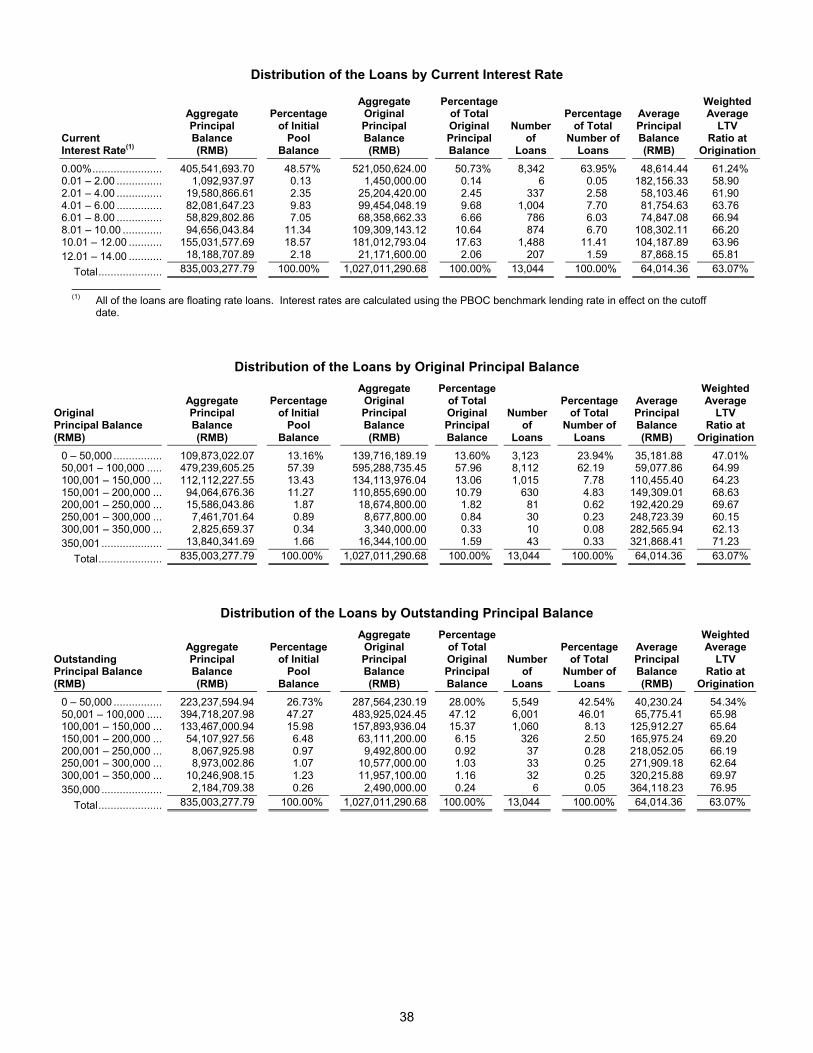

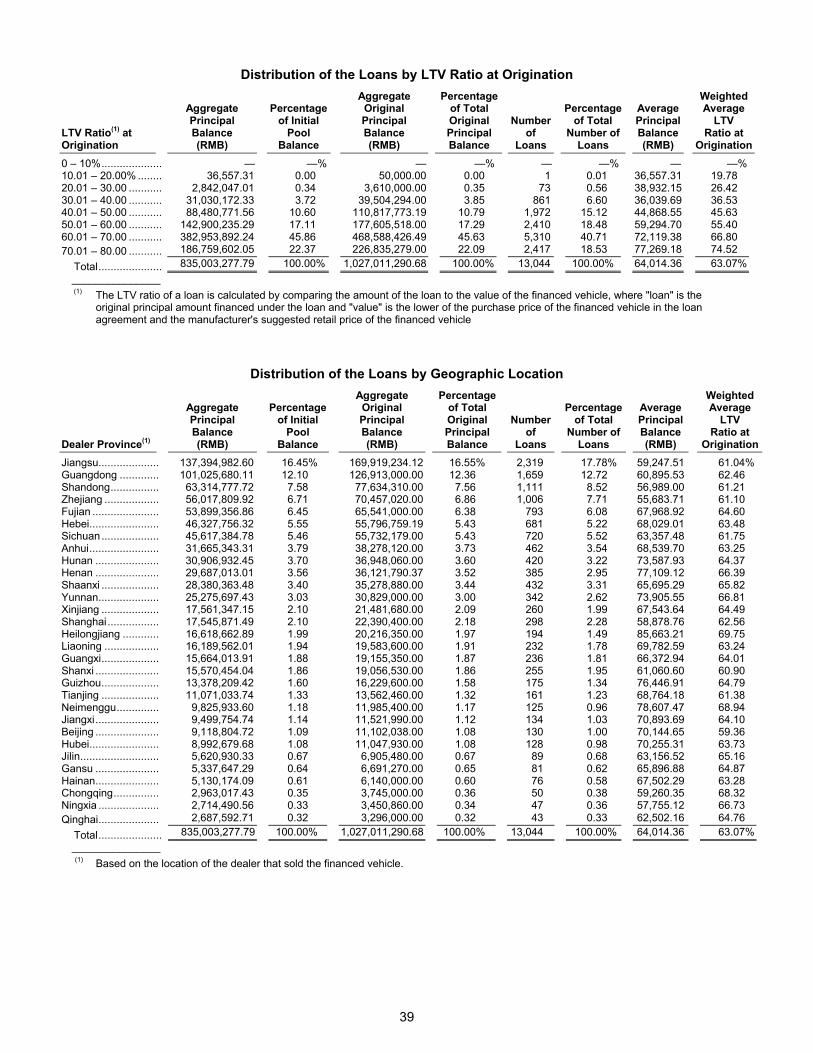

Composition of the Loans ..........................36

Description of the Trust Agreement and the Notes.............................................. 41

Trust Property............................................ 41

Representations About the Loans ............. 41

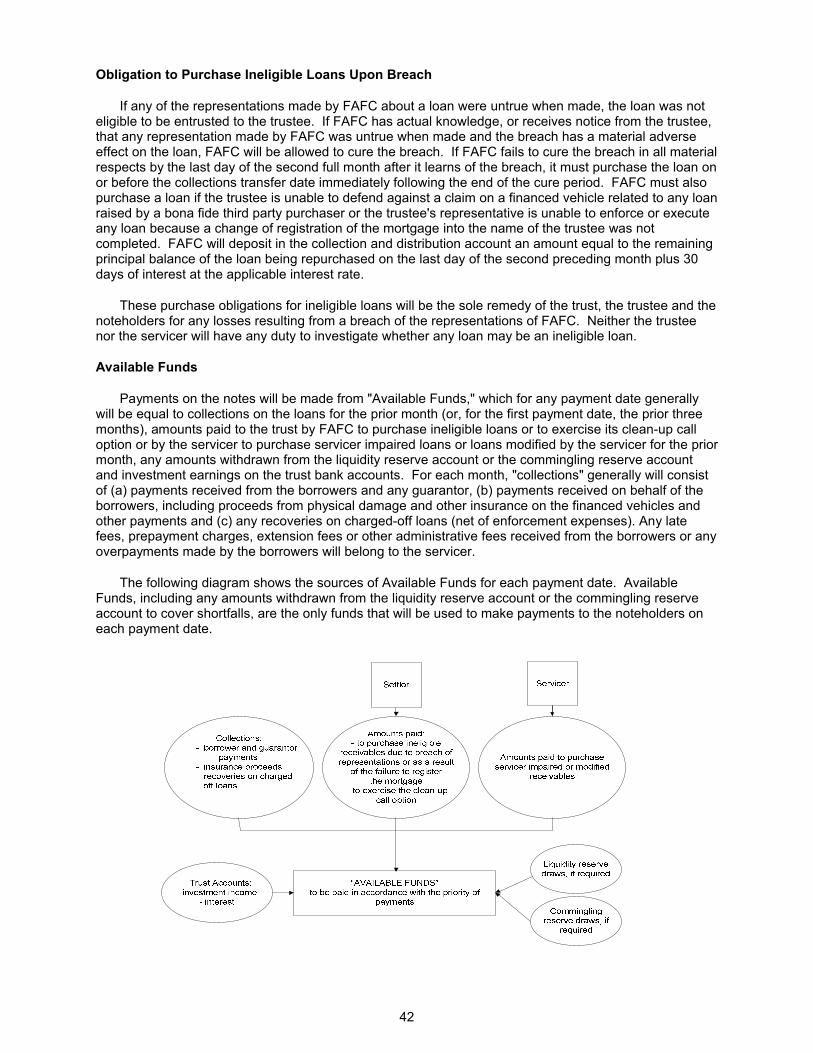

Obligation to Purchase Ineligible Loans Upon Breach ............................... 42

Available Funds ......................................... 42

Payment and Reporting Timeline .............. 43

Key Terms of the Notes............................. 44

Risk Retention ........................................... 44

Payments of Interest.................................. 44

Payments of Principal................................ 45

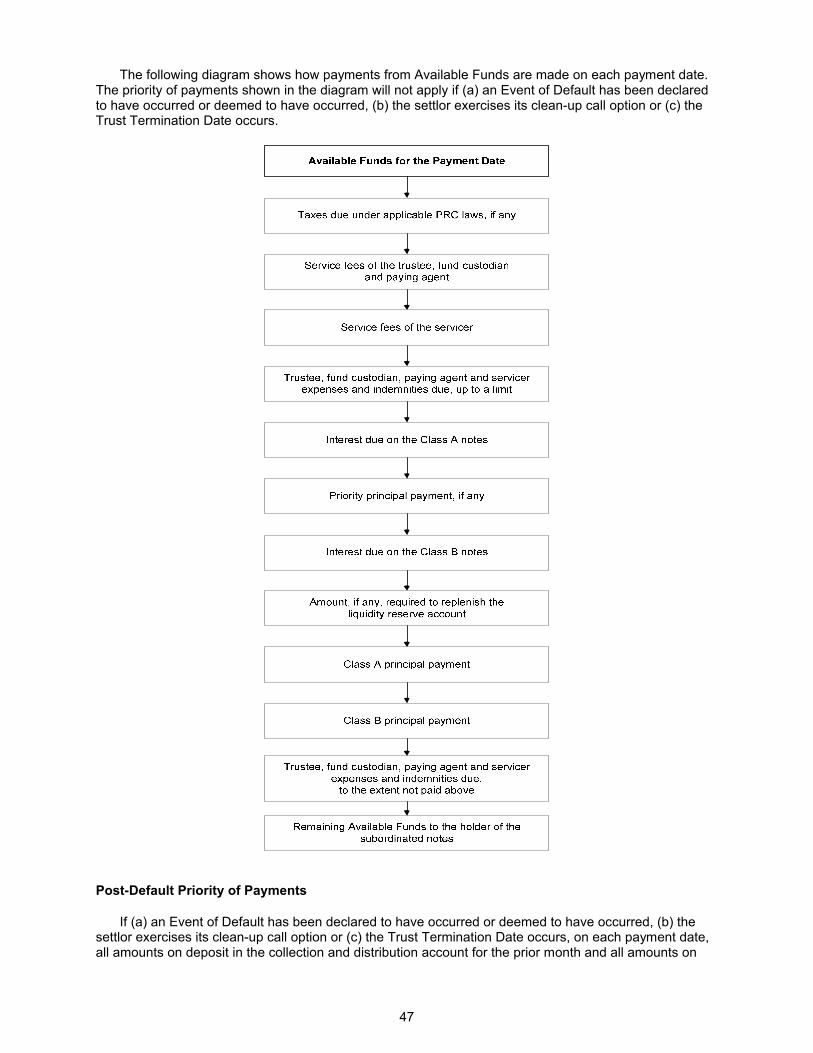

Priority of Payments .................................. 46

Post-Default Priority of Payments ............. 47

Events of Default ....................................... 48

Right Perfection Event............................... 49

Meetings of Noteholders ........................... 49

Trustee Standard of Care and Limitation on Liability.............................. 50

Trustee Eligibility Criteria; Representations and Warranties ........... 50

Termination of Trustee .............................. 51

Amendments to Trust Agreement ............. 51

Optional Redemption or "Clean-up call" Option ............................................. 52

Termination and Liquidation of the Trust ....................................................... 52

Credit Enhancement ...................................... 53

Liquidity Reserve Account......................... 53

Commingling Reserve Account ................. 53

Subordination ............................................ 54

Overcollateralization .................................. 54

Excess Spread .......................................... 55

Description of the Fund Custody Agreement ................................................... 55

Fund Custodian Duties .............................. 55

Trust Bank Accounts ................................. 56

Fund Custodian Eligibility Criteria; Representations and Warranties ........... 56

Termination of Fund Custodian ................. 56

Amendments to Fund Custody Agreement.............................................. 57

Description of the Servicing Agreement and the Servicing of the Loans ........................................................... 57

Servicing Duties......................................... 57

Deposit of Collections................................ 58

3

Servicer Modifications and Obligation to Purchase Certain Loans......................................................58

Custodial Obligations for Loan Files ..........58

Delegation of Duties ..................................59

Servicer Service Fees................................59

Limitations on Liability................................59

Appointment of Back-up Servicer ..............59

Resignation and Termination of Servicer ..................................................59

Amendments to Servicing Agreement ..............................................60

Interest Rate and Prepayment Sensitivity of the Notes ..............................60

Interest Rate Sensitivity .............................61

Prepayment Sensitivity ..............................61

Taxes and Expenses Paid from the Trust Property .............................................63

Taxes to be Paid from the Trust Property ..................................................63

Expenses to be Paid from the Trust Property ..................................................64

Information Disclosure ..................................64

Types of Information Disclosure ................64

Timing and Content of Information Reports................................................... 64

Some Important Legal Considerations ........................................... 66

Legal and Supervisory Framework for the Securitization of Credit Assets .................................................... 66

Special Purpose Trust ............................... 67

Transfer of Individual Auto Mortgage Loans and Related Security................... 68

Enforcement of Mortgage Right ................ 68

Summary of Legal Opinions ......................... 69

Summary of Credit Ratings........................... 70

Tax Considerations........................................ 71

Business Tax or Value Added Tax ............ 71

Income Tax................................................ 71

Stamp Duty................................................ 72

Plan of Distribution........................................ 72

Index of Defined Terms in this Offering Circular ......................................... 73

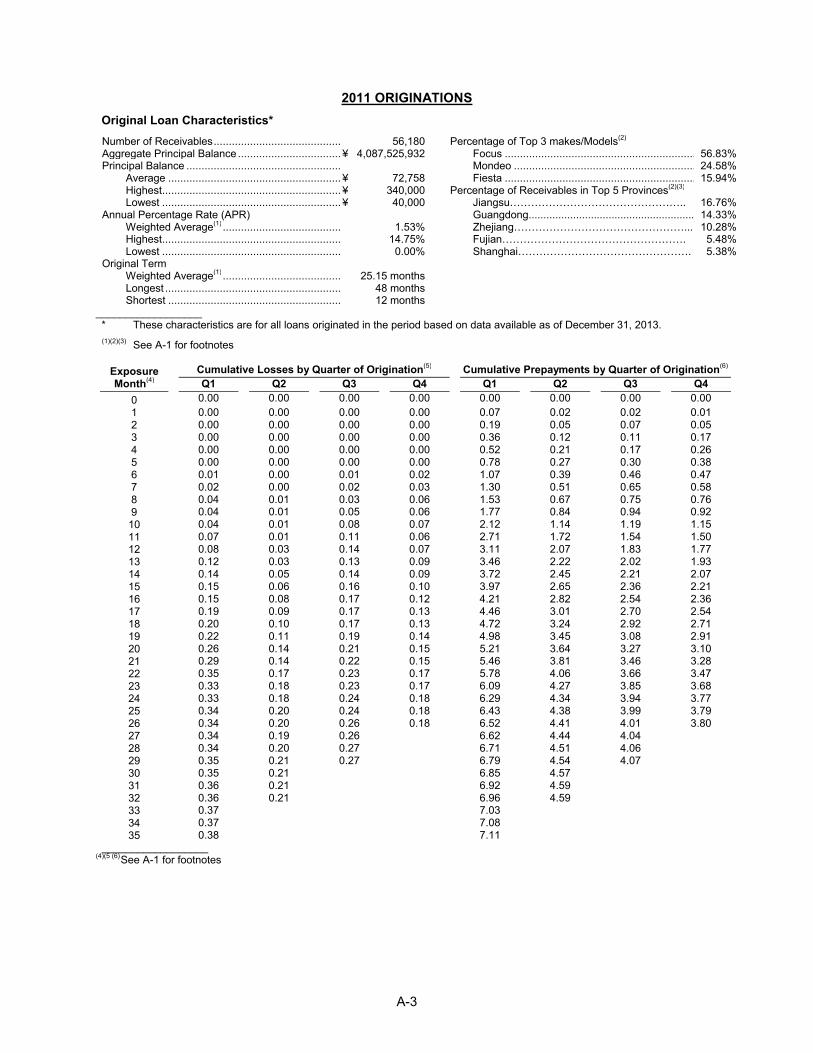

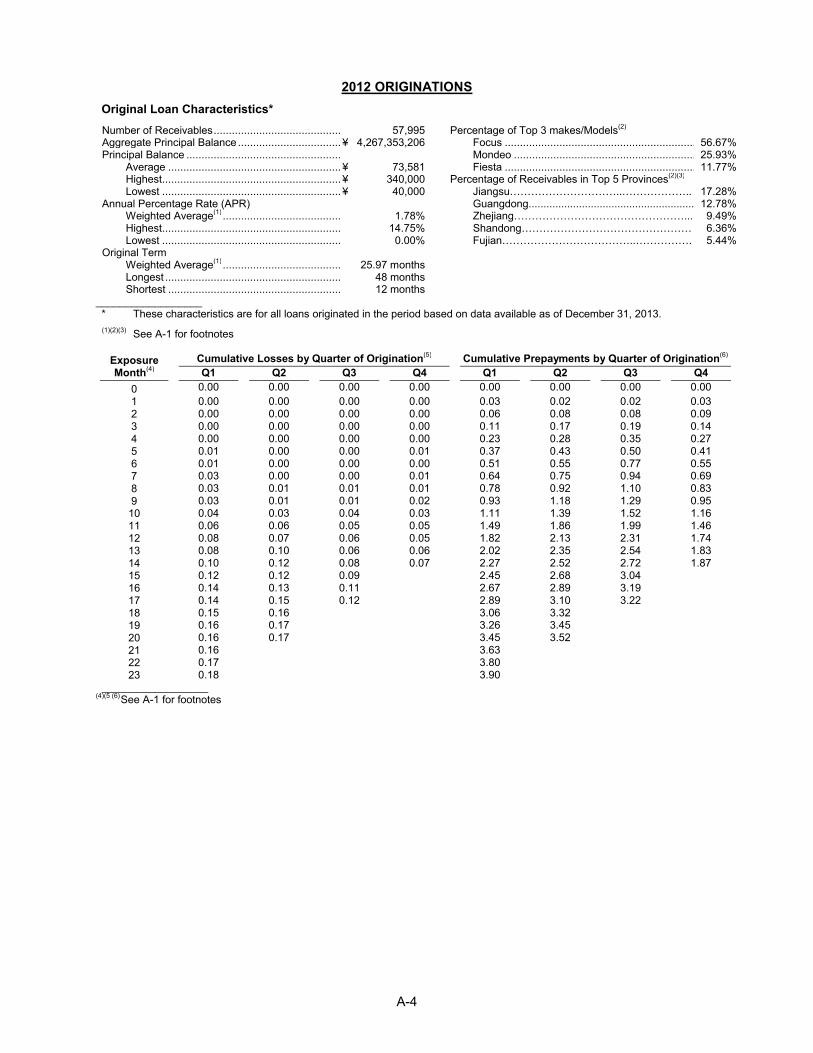

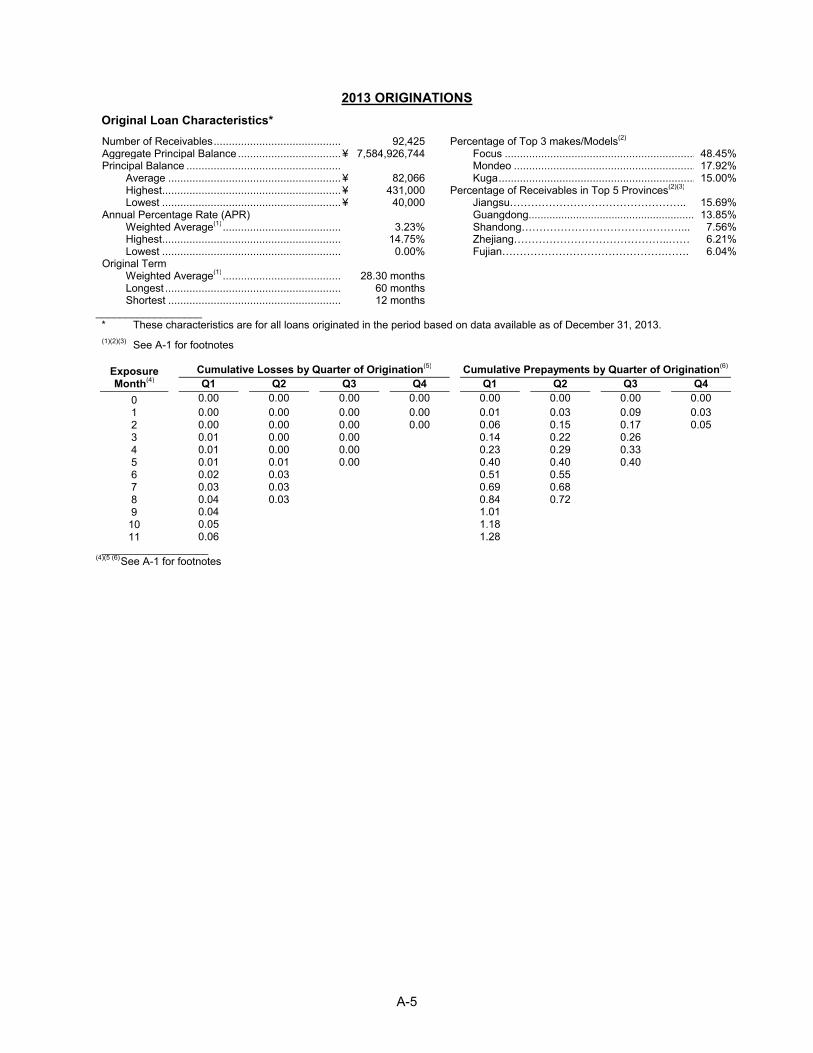

Annex A – Vintage Originations Data......... A-1

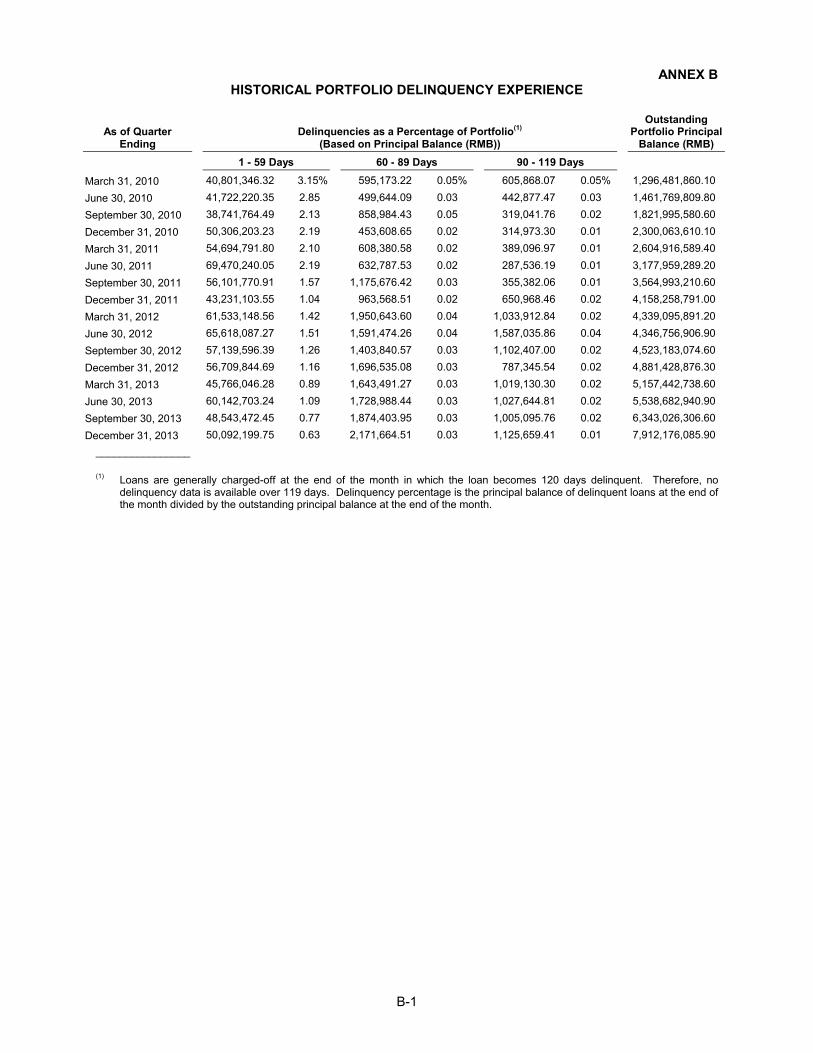

Annex B – Historical Portfolio Delinquency Experience .......................... B-1

4

READING THIS OFFERING CIRCULAR

This offering circular provides information about Fuyuan 2014-1 Retail Auto Mortgage Loan Securitization Trust and the terms of the notes to be issued by the trustee. You should only rely on information provided or referenced in this offering circular. Neither FAFC nor the trustee has authorized anyone to provide you with different information.

This offering circular begins with the following brief introductory sections:

Transaction Parties — lists the parties involved in this securitization transaction, and provides address and contact information,

Transaction Structure Diagram — illustrates the structure of this securitization transaction, including the credit enhancement available for the notes,

Transaction Parties and Documents Diagram — illustrates the role that each transaction party and transaction document plays in this securitization transaction,

Summary — describes the main terms of the notes, the cash flows in this securitization transaction and the credit enhancement available for the notes, and

Risk Factors — describes the most significant risks of investing in the notes.

The other sections of this offering circular contain more detailed descriptions of the notes and the structure of this securitization transaction. Cross-references refer you to more detailed descriptions of a particular topic or related information elsewhere in this offering circular. The Table of Contents contains references to key topics.

An index of defined terms is at the end of this offering circular.

IMPORTANT INFORMATION

The notes are being issued with the approval of China Banking Regulatory Commission, or "CBRC,"by Reply and Approval of China Banking Regulatory Commission on the Project of Securitization Pilot Program Undertaken by Ford Automotive Finance (China) Limited and Shanghai International Trust Co., Ltd. (CBRC Approval [2014] No.125) and of the People's Bank of China, or "PBOC," by People's Bank of China, Determination on Approval for Administrative License (PBOC Market Access Administrative Permission [2014] No. 36).

The notes issued by the trustee include the offered notes and the subordinated notes, which represent the respective beneficial rights in the trust and will not constitute obligations of the settlor, the trustee or any other person. The notes do not represent interests in the settlor, the servicer, the trustee (other than solely in its capacity as trustee of the trust), the fund custodian, the notes custodian, the paying agent, the lead underwriter or any of their affiliates. The notes represent limited recourse obligations payable only from the trust property. The settlor has no obligation to pay the interest or principal on the notes to the investors and, apart from its obligations as settlor under the trust agreement and as servicer under the servicing agreement, the settlor assumes no obligation or responsibility for any losses on the notes.

The settlor and the trustee confirm that, as of the date of this offering circular, this offering circular does not contain any untrue statement of a material fact or omit to state a material fact necessary in order to make the statements in this offering circular, in the light of the circumstances under which they were made, not misleading. Investors should carefully read this offering circular and the other information disclosure referenced in this offering circular and make an independent investment decision before purchasing the notes. The approval of the issuance of the notes by the relevant authorities does not constitute an evaluation by the authorities of the suitability of an investment in the notes or a judgment on the risks of an investment in the notes.

5

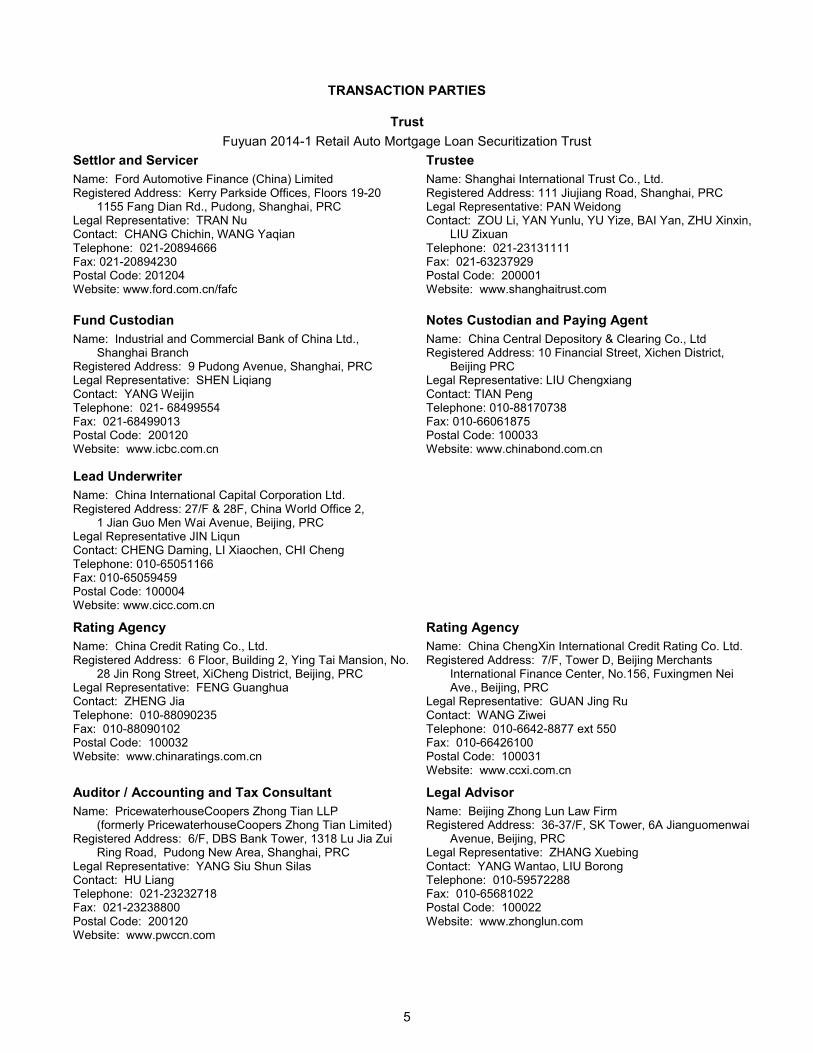

TRANSACTION PARTIES

Trust

Fuyuan 2014-1 Retail Auto Mortgage Loan Securitization Trust

Settlor and Servicer

Name: Ford Automotive Finance (China) LimitedRegistered Address: Kerry Parkside Offices, Floors 19-20

1155 Fang Dian Rd., Pudong, Shanghai, PRCLegal Representative: TRAN NuContact: CHANG Chichin, WANG YaqianTelephone: 021-20894666Fax: 021-20894230Postal Code: 201204Website: www.ford.com.cn/fafc

Trustee

Name: Shanghai International Trust Co., Ltd.Registered Address: 111 Jiujiang Road, Shanghai, PRCLegal Representative: PAN WeidongContact: ZOU Li, YAN Yunlu, YU Yize, BAI Yan, ZHU Xinxin,

LIU ZixuanTelephone: 021-23131111Fax: 021-63237929Postal Code: 200001Website: www.shanghaitrust.com

Fund Custodian

Name: Industrial and Commercial Bank of China Ltd., Shanghai Branch

Registered Address: 9 Pudong Avenue, Shanghai, PRCLegal Representative: SHEN LiqiangContact: YANG WeijinTelephone: 021- 68499554Fax: 021-68499013Postal Code: 200120Website: www.icbc.com.cn

Notes Custodian and Paying Agent

Name: China Central Depository & Clearing Co., LtdRegistered Address: 10 Financial Street, Xichen District,

Beijing PRCLegal Representative: LIU ChengxiangContact: TIAN PengTelephone: 010-88170738Fax: 010-66061875Postal Code: 100033Website: www.chinabond.com.cn

Lead Underwriter

Name: China International Capital Corporation Ltd.Registered Address: 27/F & 28F, China World Office 2,

1 Jian Guo Men Wai Avenue, Beijing, PRCLegal Representative JIN LiqunContact: CHENG Daming, LI Xiaochen, CHI ChengTelephone: 010-65051166Fax: 010-65059459Postal Code: 100004Website: www.cicc.com.cn

Rating Agency

Name: China Credit Rating Co., Ltd.Registered Address: 6 Floor, Building 2, Ying Tai Mansion, No.

28 Jin Rong Street, XiCheng District, Beijing, PRC Legal Representative: FENG Guanghua Contact: ZHENG JiaTelephone: 010-88090235Fax: 010-88090102Postal Code: 100032Website: www.chinaratings.com.cn

Rating Agency

Name: China ChengXin International Credit Rating Co. Ltd.Registered Address: 7/F, Tower D, Beijing Merchants

International Finance Center, No.156, Fuxingmen Nei Ave., Beijing, PRC

Legal Representative: GUAN Jing RuContact: WANG ZiweiTelephone: 010-6642-8877 ext 550Fax: 010-66426100Postal Code: 100031Website: www.ccxi.com.cn

Auditor / Accounting and Tax Consultant

Name: PricewaterhouseCoopers Zhong Tian LLP(formerly PricewaterhouseCoopers Zhong Tian Limited)

Registered Address: 6/F, DBS Bank Tower, 1318 Lu Jia Zui Ring Road, Pudong New Area, Shanghai, PRC

Legal Representative: YANG Siu Shun SilasContact: HU LiangTelephone: 021-23232718Fax: 021-23238800Postal Code: 200120Website: www.pwccn.com

Legal Advisor

Name: Beijing Zhong Lun Law FirmRegistered Address: 36-37/F, SK Tower, 6A Jianguomenwai

Avenue, Beijing, PRCLegal Representative: ZHANG XuebingContact: YANG Wantao, LIU BorongTelephone: 010-59572288Fax: 010-65681022Postal Code: 100022Website: www.zhonglun.com

6

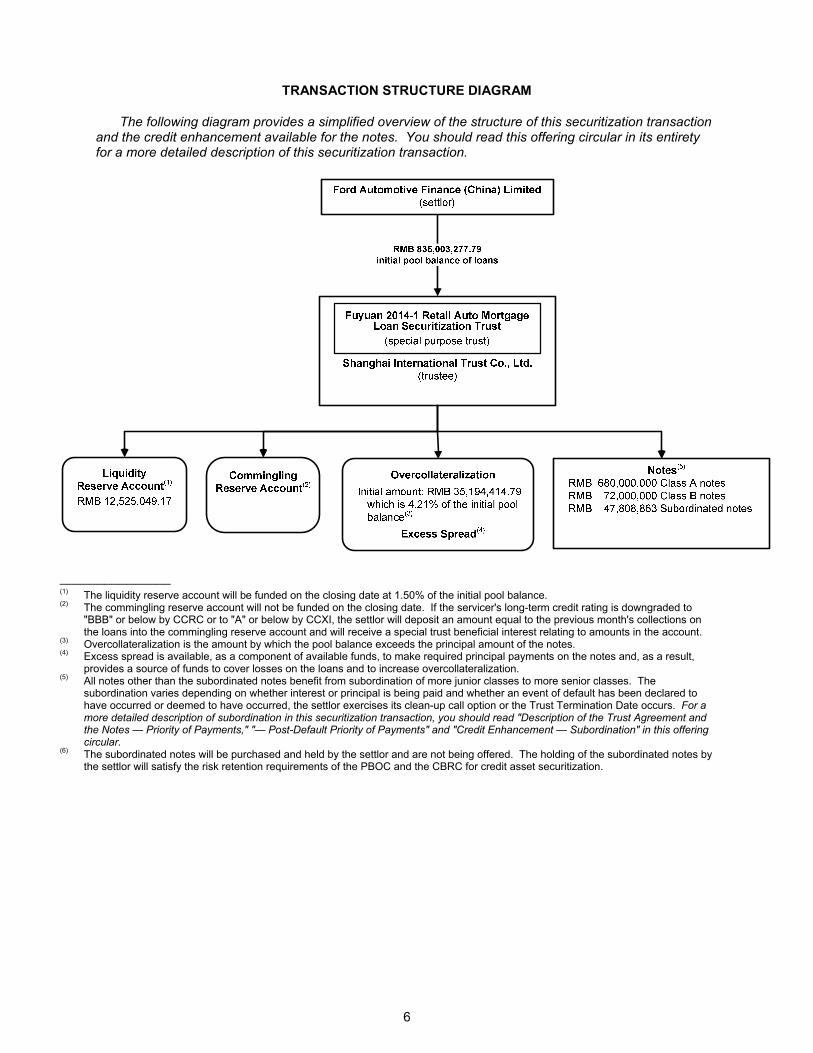

TRANSACTION STRUCTURE DIAGRAM

The following diagram provides a simplified overview of the structure of this securitization transaction and the credit enhancement available for the notes. You should read this offering circular in its entirety for a more detailed description of this securitization transaction.

_______________(1) The liquidity reserve account will be funded on the closing date at 1.50% of the initial pool balance.(2) The commingling reserve account will not be funded on the closing date. If the servicer's long-term credit rating is downgraded to

"BBB" or below by CCRC or to "A" or below by CCXI, the settlor will deposit an amount equal to the previous month's collections on the loans into the commingling reserve account and will receive a special trust beneficial interest relating to amounts in the account.

(3) Overcollateralization is the amount by which the pool balance exceeds the principal amount of the notes.(4) Excess spread is available, as a component of available funds, to make required principal payments on the notes and, as a result,

provides a source of funds to cover losses on the loans and to increase overcollateralization.(5) All notes other than the subordinated notes benefit from subordination of more junior classes to more senior classes. The

subordination varies depending on whether interest or principal is being paid and whether an event of default has been declared to have occurred or deemed to have occurred, the settlor exercises its clean-up call option or the Trust Termination Date occurs. For a more detailed description of subordination in this securitization transaction, you should read "Description of the Trust Agreement and the Notes — Priority of Payments," "— Post-Default Priority of Payments" and "Credit Enhancement — Subordination" in this offering circular.

(6) The subordinated notes will be purchased and held by the settlor and are not being offered. The holding of the subordinated notes by the settlor will satisfy the risk retention requirements of the PBOC and the CBRC for credit asset securitization.

7

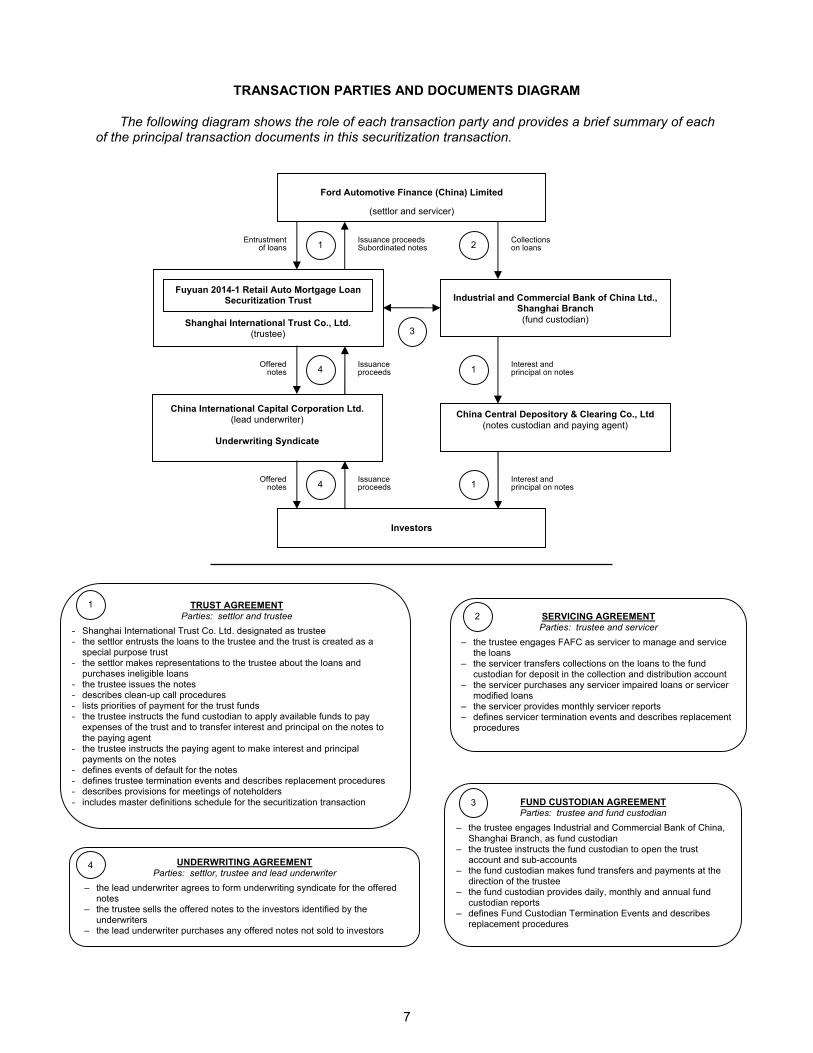

TRANSACTION PARTIES AND DOCUMENTS DIAGRAM

The following diagram shows the role of each transaction party and provides a brief summary of each of the principal transaction documents in this securitization transaction.

Shanghai International Trust Co., Ltd.(trustee)

Fuyuan 2014-1 Retail Auto Mortgage Loan Securitization Trust

Ford Automotive Finance (China) Limited

(settlor and servicer)

China International Capital Corporation Ltd.(lead underwriter)

Underwriting Syndicate

Industrial and Commercial Bank of China Ltd.,Shanghai Branch(fund custodian)

China Central Depository & Clearing Co., Ltd(notes custodian and paying agent)

Investors

1 2

4 1

4 1

3

Issuance proceedsSubordinated notes

Issuance proceeds

Issuance proceeds

Collectionson loans

Interest and principal on notes

Interest and principal on notes

Entrustment of loans

Offered notes

Offered notes

SERVICING AGREEMENTParties: trustee and servicer

– the trustee engages FAFC as servicer to manage and service the loans

– the servicer transfers collections on the loans to the fund custodian for deposit in the collection and distribution account

– the servicer purchases any servicer impaired loans or servicer modified loans

– the servicer provides monthly servicer reports– defines servicer termination events and describes replacement

procedures

2

FUND CUSTODIAN AGREEMENTParties: trustee and fund custodian

– the trustee engages Industrial and Commercial Bank of China, Shanghai Branch, as fund custodian

– the trustee instructs the fund custodian to open the trust account and sub-accounts

– the fund custodian makes fund transfers and payments at the direction of the trustee

– the fund custodian provides daily, monthly and annual fund custodian reports

– defines Fund Custodian Termination Events and describes replacement procedures

3

TRUST AGREEMENTParties: settlor and trustee

– Shanghai International Trust Co. Ltd. designated as trustee– the settlor entrusts the loans to the trustee and the trust is created as a

special purpose trust– the settlor makes representations to the trustee about the loans and

purchases ineligible loans– the trustee issues the notes – describes clean-up call procedures – lists priorities of payment for the trust funds – the trustee instructs the fund custodian to apply available funds to pay

expenses of the trust and to transfer interest and principal on the notes to the paying agent

– the trustee instructs the paying agent to make interest and principal payments on the notes

– defines events of default for the notes– defines trustee termination events and describes replacement procedures– describes provisions for meetings of noteholders – includes master definitions schedule for the securitization transaction

1

UNDERWRITING AGREEMENTParties: settlor, trustee and lead underwriter

– the lead underwriter agrees to form underwriting syndicate for the offered notes

– the trustee sells the offered notes to the investors identified by the underwriters

– the lead underwriter purchases any offered notes not sold to investors

4

8

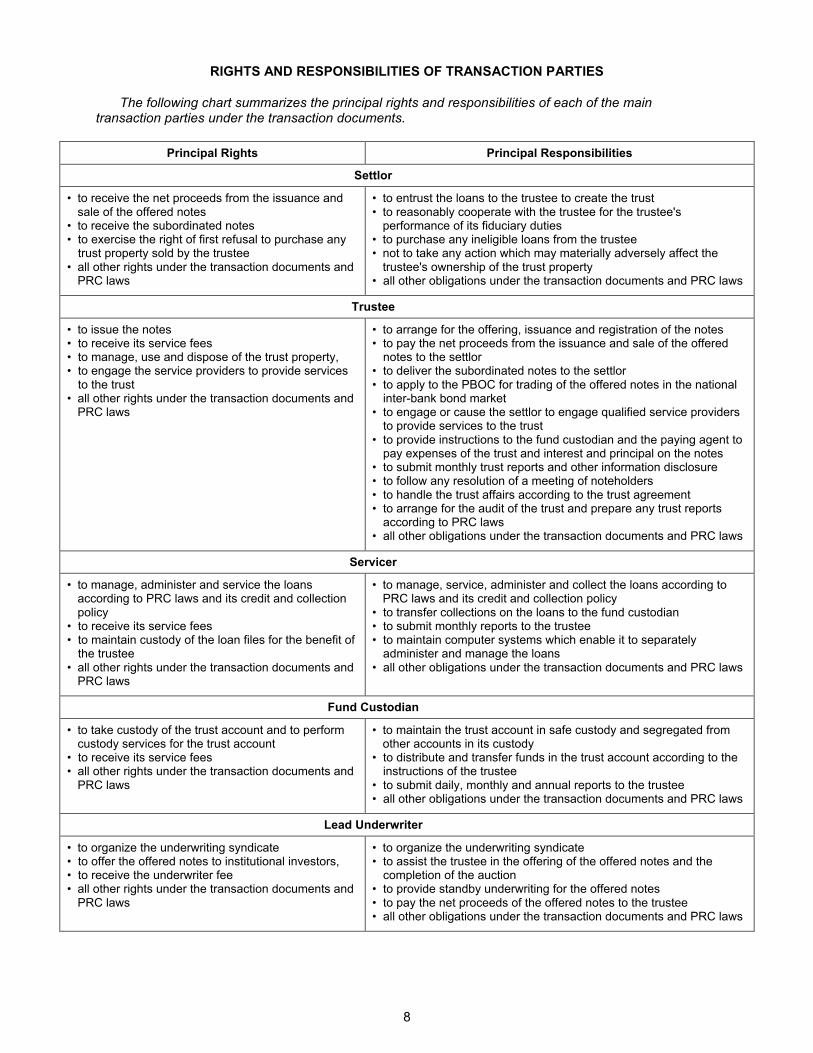

RIGHTS AND RESPONSIBILITIES OF TRANSACTION PARTIES

The following chart summarizes the principal rights and responsibilities of each of the main transaction parties under the transaction documents.

Principal Rights Principal Responsibilities

Settlor

• to receive the net proceeds from the issuance and sale of the offered notes

• to receive the subordinated notes• to exercise the right of first refusal to purchase any

trust property sold by the trustee• all other rights under the transaction documents and

PRC laws

• to entrust the loans to the trustee to create the trust• to reasonably cooperate with the trustee for the trustee's

performance of its fiduciary duties• to purchase any ineligible loans from the trustee• not to take any action which may materially adversely affect the

trustee's ownership of the trust property• all other obligations under the transaction documents and PRC laws

Trustee

• to issue the notes• to receive its service fees• to manage, use and dispose of the trust property,• to engage the service providers to provide services

to the trust• all other rights under the transaction documents and

PRC laws

• to arrange for the offering, issuance and registration of the notes • to pay the net proceeds from the issuance and sale of the offered

notes to the settlor• to deliver the subordinated notes to the settlor• to apply to the PBOC for trading of the offered notes in the national

inter-bank bond market• to engage or cause the settlor to engage qualified service providers

to provide services to the trust• to provide instructions to the fund custodian and the paying agent to

pay expenses of the trust and interest and principal on the notes• to submit monthly trust reports and other information disclosure• to follow any resolution of a meeting of noteholders• to handle the trust affairs according to the trust agreement• to arrange for the audit of the trust and prepare any trust reports

according to PRC laws• all other obligations under the transaction documents and PRC laws

Servicer

• to manage, administer and service the loans according to PRC laws and its credit and collection policy

• to receive its service fees• to maintain custody of the loan files for the benefit of

the trustee• all other rights under the transaction documents and

PRC laws

• to manage, service, administer and collect the loans according to PRC laws and its credit and collection policy

• to transfer collections on the loans to the fund custodian• to submit monthly reports to the trustee• to maintain computer systems which enable it to separately

administer and manage the loans• all other obligations under the transaction documents and PRC laws

Fund Custodian

• to take custody of the trust account and to perform custody services for the trust account

• to receive its service fees• all other rights under the transaction documents and

PRC laws

• to maintain the trust account in safe custody and segregated from other accounts in its custody

• to distribute and transfer funds in the trust account according to the instructions of the trustee

• to submit daily, monthly and annual reports to the trustee• all other obligations under the transaction documents and PRC laws

Lead Underwriter

• to organize the underwriting syndicate• to offer the offered notes to institutional investors,• to receive the underwriter fee• all other rights under the transaction documents and

PRC laws

• to organize the underwriting syndicate• to assist the trustee in the offering of the offered notes and the

completion of the auction• to provide standby underwriting for the offered notes• to pay the net proceeds of the offered notes to the trustee• all other obligations under the transaction documents and PRC laws

9

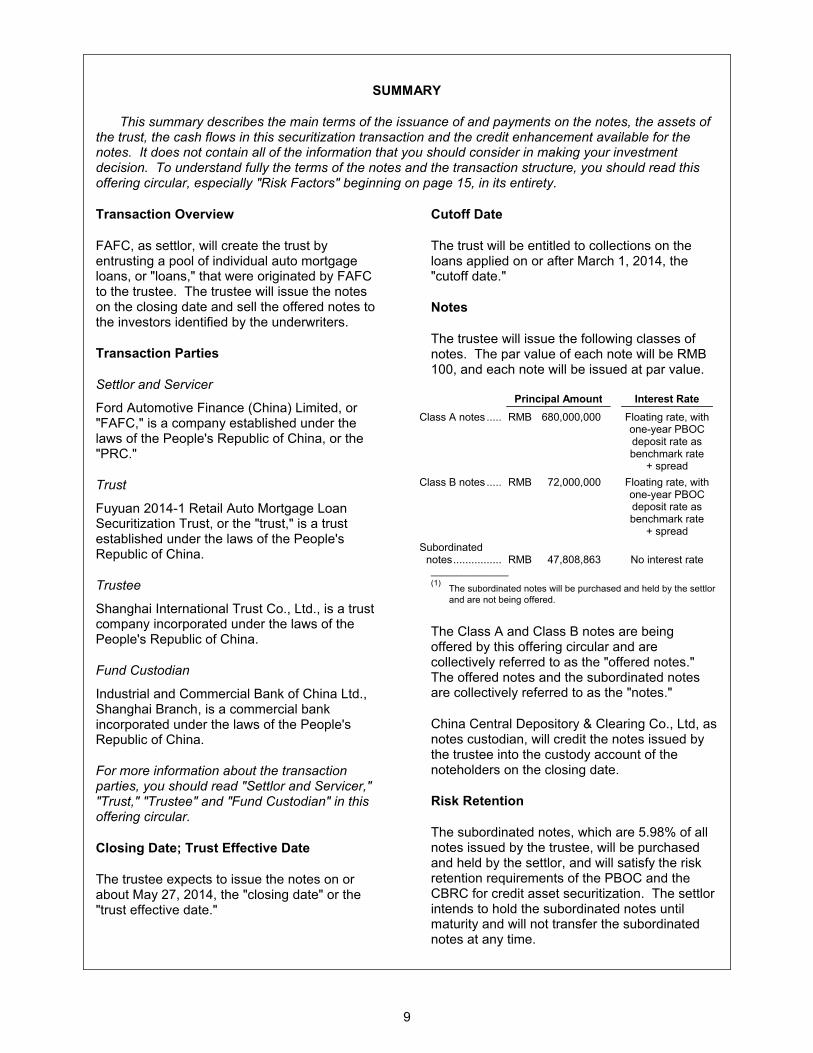

SUMMARY

This summary describes the main terms of the issuance of and payments on the notes, the assets of the trust, the cash flows in this securitization transaction and the credit enhancement available for the notes. It does not contain all of the information that you should consider in making your investment decision. To understand fully the terms of the notes and the transaction structure, you should read this offering circular, especially "Risk Factors" beginning on page 15, in its entirety.

Transaction Overview

FAFC, as settlor, will create the trust by entrusting a pool of individual auto mortgage loans, or "loans," that were originated by FAFC to the trustee. The trustee will issue the notes on the closing date and sell the offered notes to the investors identified by the underwriters.

Transaction Parties

Settlor and Servicer

Ford Automotive Finance (China) Limited, or "FAFC," is a company established under the laws of the People's Republic of China, or the "PRC."

Trust

Fuyuan 2014-1 Retail Auto Mortgage Loan Securitization Trust, or the "trust," is a trust established under the laws of the People's Republic of China.

Trustee

Shanghai International Trust Co., Ltd., is a trust company incorporated under the laws of the People's Republic of China.

Fund Custodian

Industrial and Commercial Bank of China Ltd., Shanghai Branch, is a commercial bank incorporated under the laws of the People's Republic of China.

For more information about the transaction parties, you should read "Settlor and Servicer,""Trust," "Trustee" and "Fund Custodian" in this offering circular.

Closing Date; Trust Effective Date

The trustee expects to issue the notes on or about May 27, 2014, the "closing date" or the "trust effective date."

Cutoff Date

The trust will be entitled to collections on the loans applied on or after March 1, 2014, the "cutoff date."

Notes

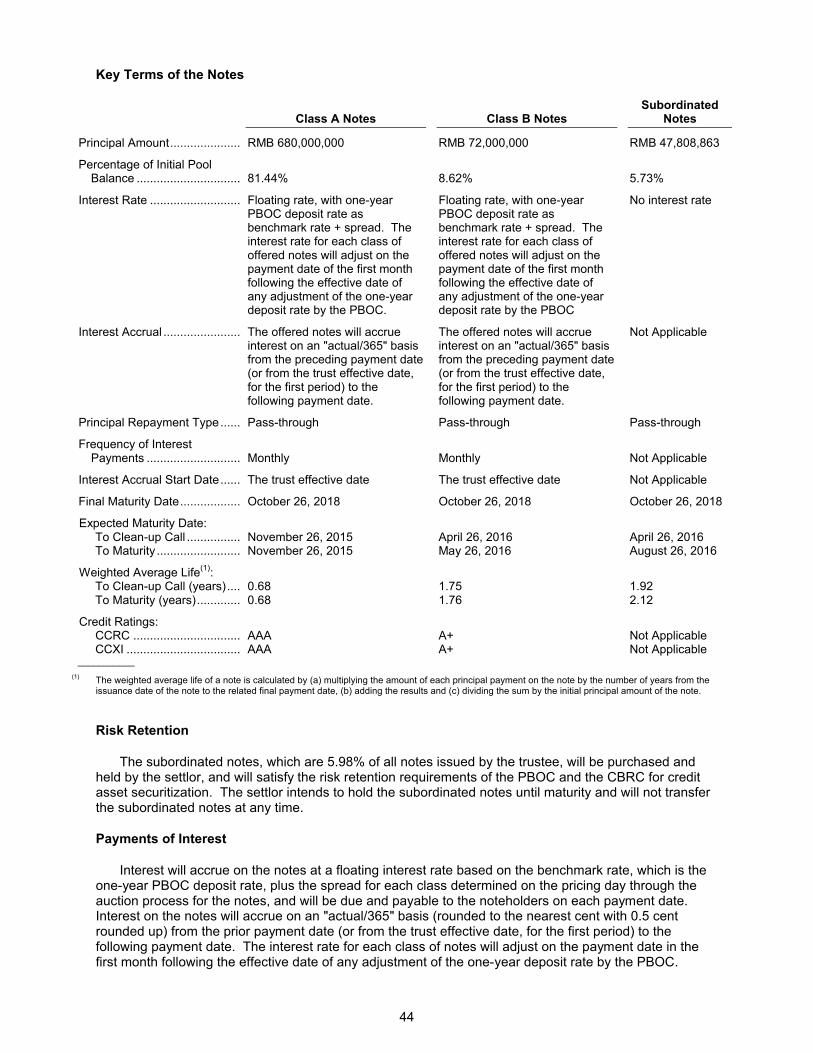

The trustee will issue the following classes of notes. The par value of each note will be RMB 100, and each note will be issued at par value.

Principal Amount Interest Rate

Class A notes ..............RMB 680,000,000 Floating rate, with one-year PBOC deposit rate as benchmark rate

+ spread

Class B notes ..............RMB 72,000,000 Floating rate, with one-year PBOC deposit rate as benchmark rate

+ spread

Subordinated notes.........................RMB 47,808,863 No interest rate_______________(1)

The subordinated notes will be purchased and held by the settlorand are not being offered.

The Class A and Class B notes are being offered by this offering circular and are collectively referred to as the "offered notes." The offered notes and the subordinated notes are collectively referred to as the "notes."

China Central Depository & Clearing Co., Ltd, as notes custodian, will credit the notes issued by the trustee into the custody account of the noteholders on the closing date.

Risk Retention

The subordinated notes, which are 5.98% of all notes issued by the trustee, will be purchased and held by the settlor, and will satisfy the risk retention requirements of the PBOC and the CBRC for credit asset securitization. The settlor intends to hold the subordinated notes until maturity and will not transfer the subordinated notes at any time.

10

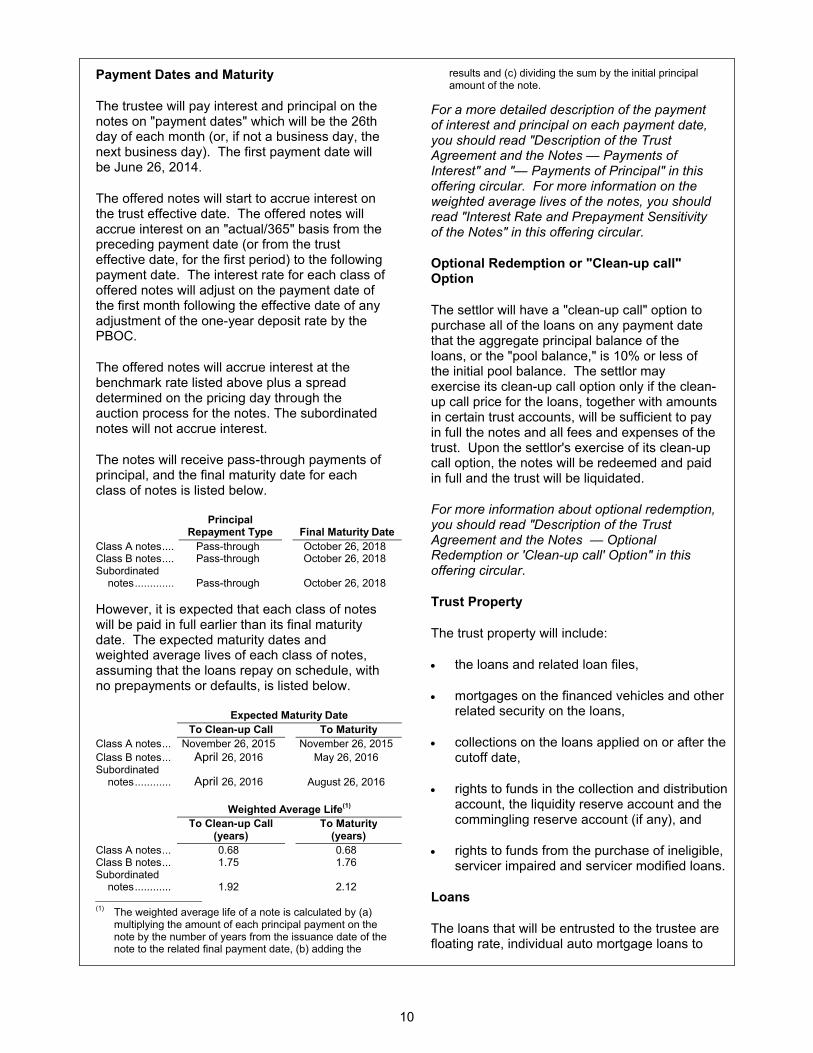

Payment Dates and Maturity

The trustee will pay interest and principal on the notes on "payment dates" which will be the 26th day of each month (or, if not a business day, the next business day). The first payment date will be June 26, 2014.

The offered notes will start to accrue interest on the trust effective date. The offered notes will accrue interest on an "actual/365" basis from the preceding payment date (or from the trust effective date, for the first period) to the following payment date. The interest rate for each class of offered notes will adjust on the payment date of the first month following the effective date of any adjustment of the one-year deposit rate by the PBOC.

The offered notes will accrue interest at the benchmark rate listed above plus a spread determined on the pricing day through the auction process for the notes. The subordinated notes will not accrue interest.

The notes will receive pass-through payments of principal, and the final maturity date for each class of notes is listed below.

Principal Repayment Type Final Maturity Date

Class A notes.........................Pass-through October 26, 2018Class B notes.........................Pass-through October 26, 2018Subordinated

notes................................Pass-through October 26, 2018

However, it is expected that each class of notes will be paid in full earlier than its final maturity date. The expected maturity dates and weighted average lives of each class of notes, assuming that the loans repay on schedule, with no prepayments or defaults, is listed below.

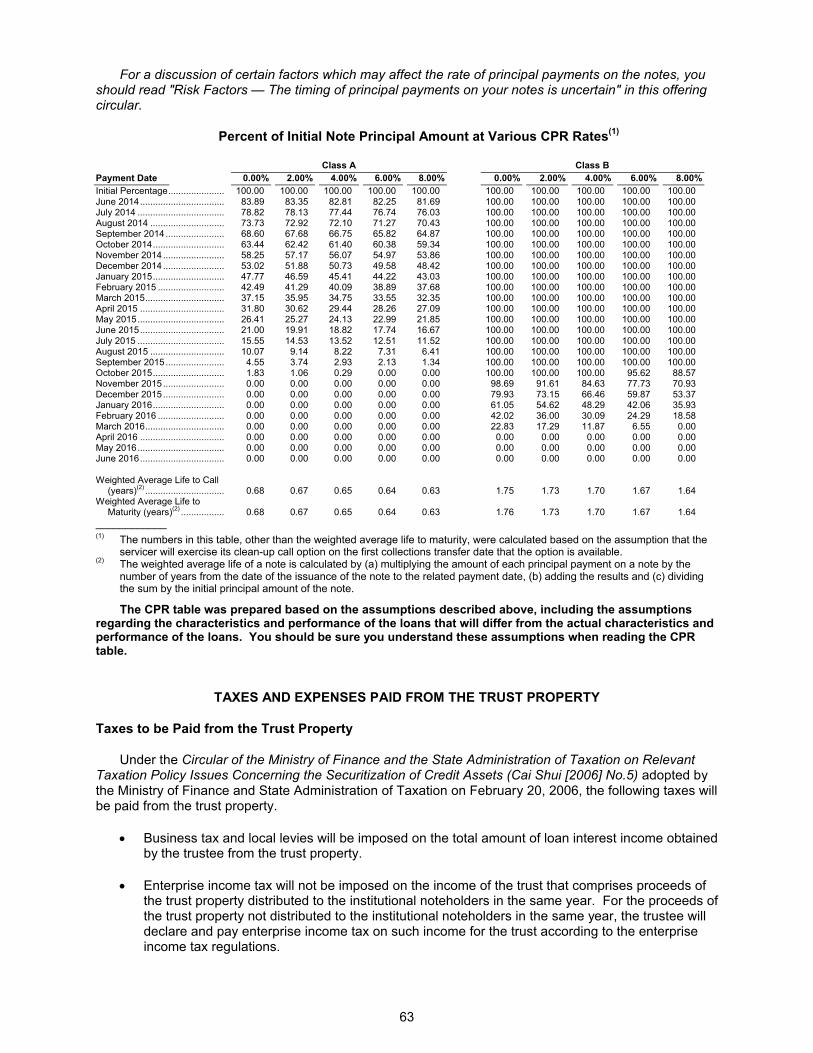

Expected Maturity Date

To Clean-up Call To Maturity

Class A notes.........................November 26, 2015 November 26, 2015

Class B notes.........................April 26, 2016 May 26, 2016Subordinated

notes................................April 26, 2016 August 26, 2016

Weighted Average Life(1)

To Clean-up Call(years)

To Maturity(years)

Class A notes.........................0.68 0.68Class B notes.........................1.75 1.76Subordinated

notes................................1.92 2.12________________________

(1) The weighted average life of a note is calculated by (a) multiplying the amount of each principal payment on thenote by the number of years from the issuance date of the note to the related final payment date, (b) adding the

results and (c) dividing the sum by the initial principal amount of the note.

For a more detailed description of the payment of interest and principal on each payment date, you should read "Description of the Trust Agreement and the Notes — Payments of Interest" and "— Payments of Principal" in this offering circular. For more information on the weighted average lives of the notes, you should read "Interest Rate and Prepayment Sensitivity of the Notes" in this offering circular.

Optional Redemption or "Clean-up call"Option

The settlor will have a "clean-up call" option to purchase all of the loans on any payment date that the aggregate principal balance of the loans, or the "pool balance," is 10% or less of the initial pool balance. The settlor may exercise its clean-up call option only if the clean-up call price for the loans, together with amounts in certain trust accounts, will be sufficient to pay in full the notes and all fees and expenses of the trust. Upon the settlor's exercise of its clean-up call option, the notes will be redeemed and paid in full and the trust will be liquidated.

For more information about optional redemption, you should read "Description of the Trust Agreement and the Notes — Optional Redemption or 'Clean-up call' Option" in this offering circular.

Trust Property

The trust property will include:

the loans and related loan files,

mortgages on the financed vehicles and other related security on the loans,

collections on the loans applied on or after the cutoff date,

rights to funds in the collection and distribution account, the liquidity reserve account and the commingling reserve account (if any), and

rights to funds from the purchase of ineligible,servicer impaired and servicer modified loans.

Loans

The loans that will be entrusted to the trustee are floating rate, individual auto mortgage loans to

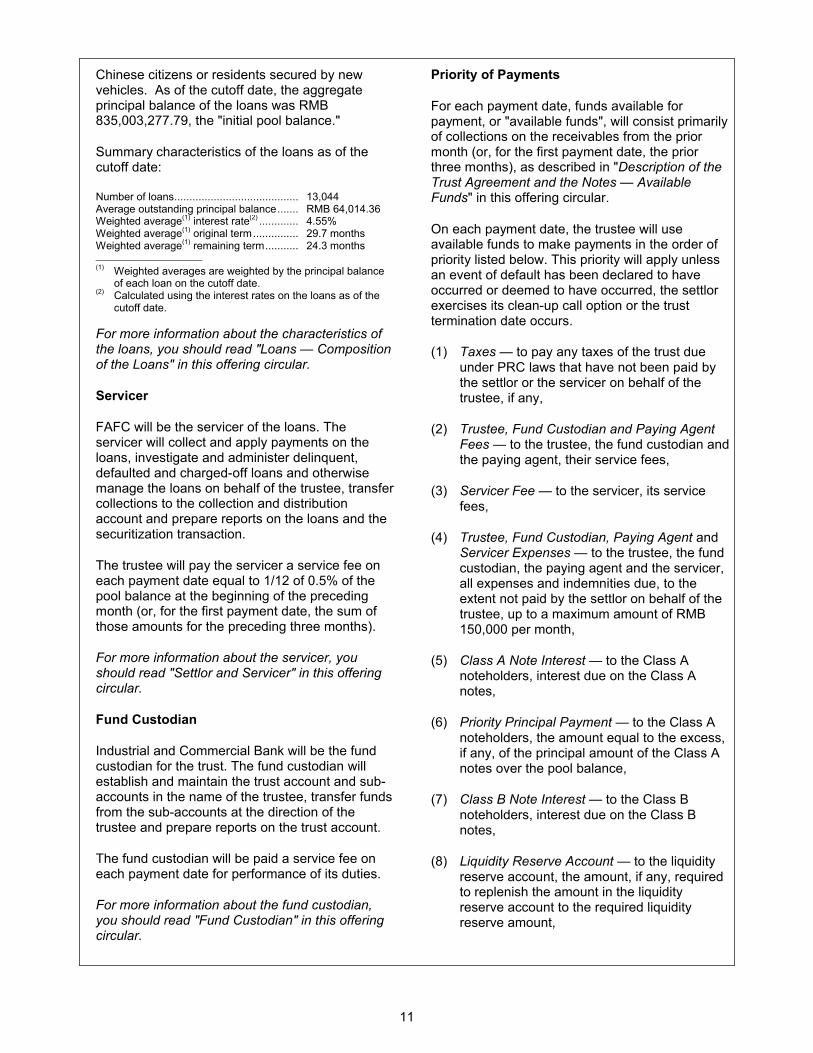

11

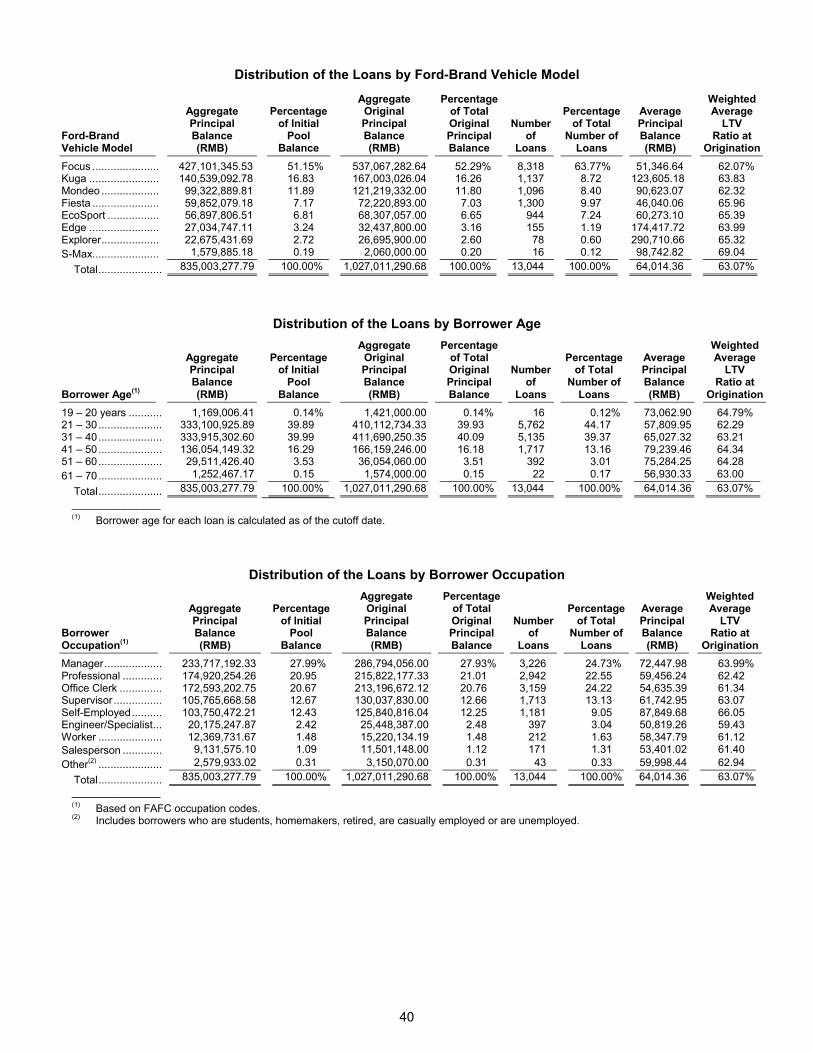

Chinese citizens or residents secured by new vehicles. As of the cutoff date, the aggregate principal balance of the loans was RMB 835,003,277.79, the "initial pool balance."

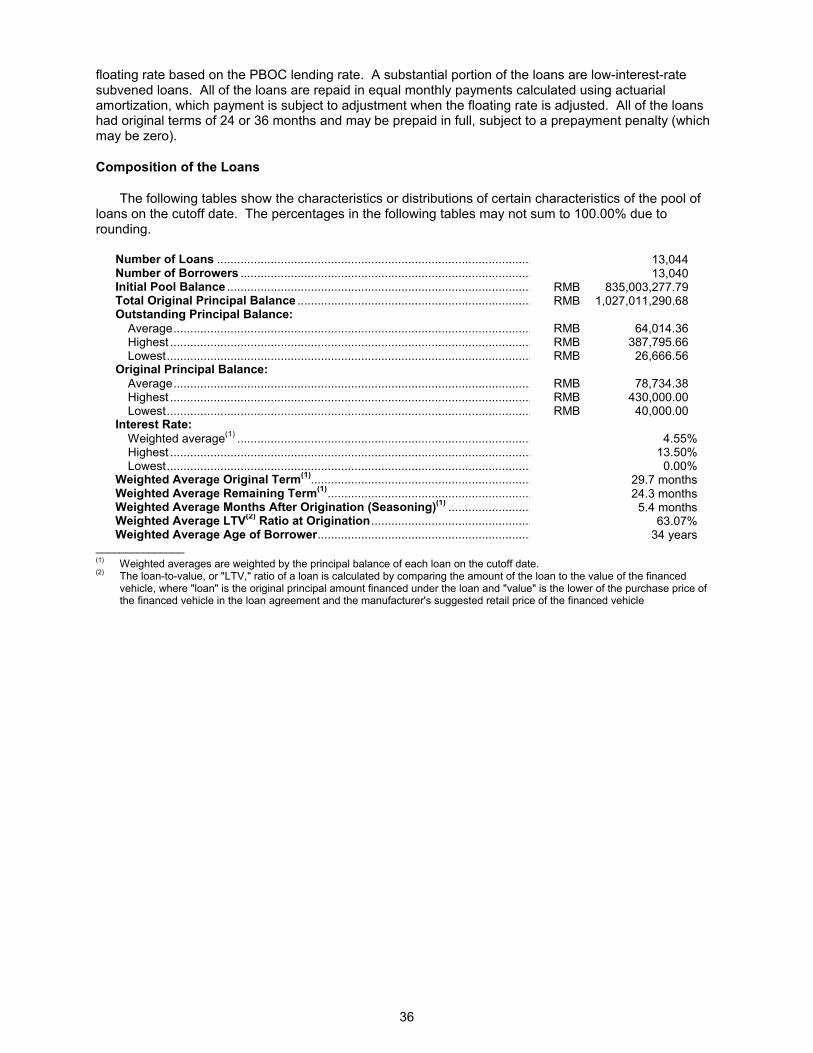

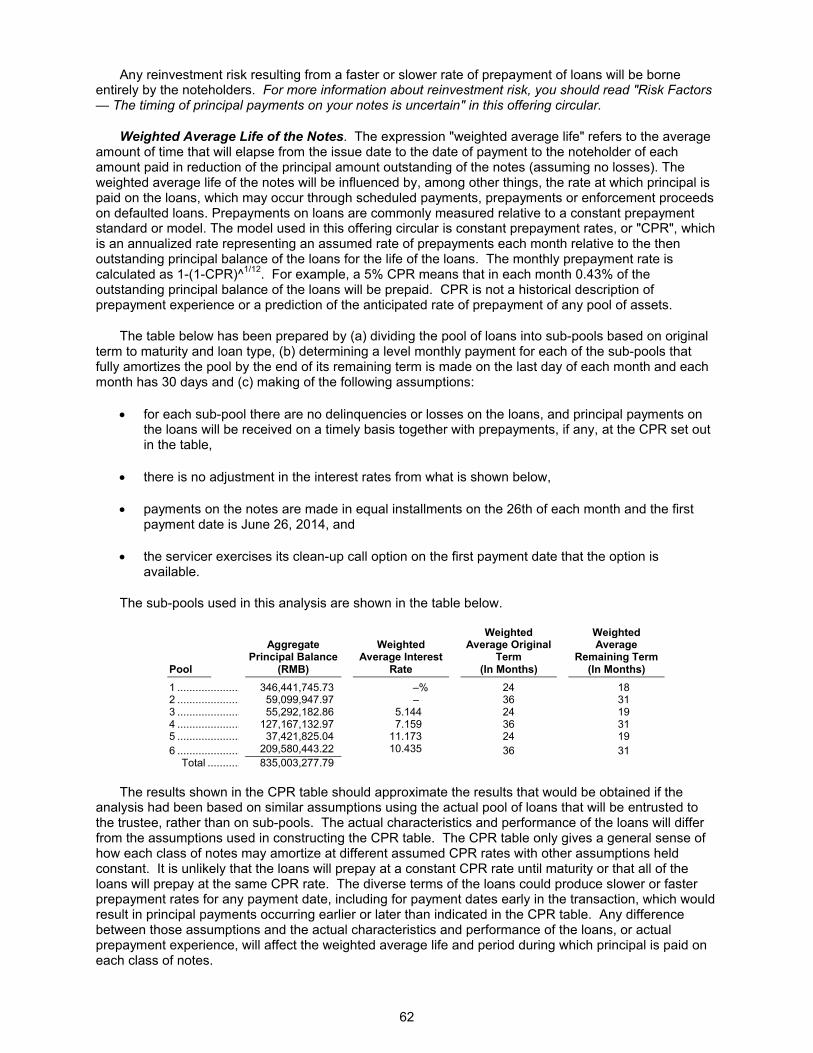

Summary characteristics of the loans as of the cutoff date:

Number of loans.....................................................13,044Average outstanding principal balance...................RMB 64,014.36Weighted average(1) interest rate(2) .........................4.55%Weighted average(1) original term...........................29.7 monthsWeighted average(1) remaining term.......................24.3 months________________________

(1) Weighted averages are weighted by the principal balance of each loan on the cutoff date.

(2) Calculated using the interest rates on the loans as of the cutoff date.

For more information about the characteristics of the loans, you should read "Loans — Composition of the Loans" in this offering circular.

Servicer

FAFC will be the servicer of the loans. The servicer will collect and apply payments on the loans, investigate and administer delinquent, defaulted and charged-off loans and otherwise manage the loans on behalf of the trustee, transfer collections to the collection and distributionaccount and prepare reports on the loans and the securitization transaction.

The trustee will pay the servicer a service fee on each payment date equal to 1/12 of 0.5% of the pool balance at the beginning of the preceding month (or, for the first payment date, the sum of those amounts for the preceding three months).

For more information about the servicer, you should read "Settlor and Servicer" in this offering circular.

Fund Custodian

Industrial and Commercial Bank will be the fund custodian for the trust. The fund custodian will establish and maintain the trust account and sub-accounts in the name of the trustee, transfer funds from the sub-accounts at the direction of the trustee and prepare reports on the trust account.

The fund custodian will be paid a service fee on each payment date for performance of its duties.

For more information about the fund custodian, you should read "Fund Custodian" in this offering circular.

Priority of Payments

For each payment date, funds available for payment, or "available funds", will consist primarily of collections on the receivables from the prior month (or, for the first payment date, the prior three months), as described in "Description of the Trust Agreement and the Notes — Available Funds" in this offering circular.

On each payment date, the trustee will use available funds to make payments in the order of priority listed below. This priority will apply unless an event of default has been declared to have occurred or deemed to have occurred, the settlor exercises its clean-up call option or the trust termination date occurs.

(1) Taxes — to pay any taxes of the trust due under PRC laws that have not been paid by the settlor or the servicer on behalf of the trustee, if any,

(2) Trustee, Fund Custodian and Paying AgentFees — to the trustee, the fund custodian and the paying agent, their service fees,

(3) Servicer Fee — to the servicer, its service fees,

(4) Trustee, Fund Custodian, Paying Agent and Servicer Expenses — to the trustee, the fund custodian, the paying agent and the servicer, all expenses and indemnities due, to the extent not paid by the settlor on behalf of the trustee, up to a maximum amount of RMB 150,000 per month,

(5) Class A Note Interest — to the Class Anoteholders, interest due on the Class A notes,

(6) Priority Principal Payment — to the Class A noteholders, the amount equal to the excess, if any, of the principal amount of the Class A notes over the pool balance,

(7) Class B Note Interest — to the Class B noteholders, interest due on the Class B notes,

(8) Liquidity Reserve Account — to the liquidity reserve account, the amount, if any, required to replenish the amount in the liquidity reserve account to the required liquidity reserve amount,

12

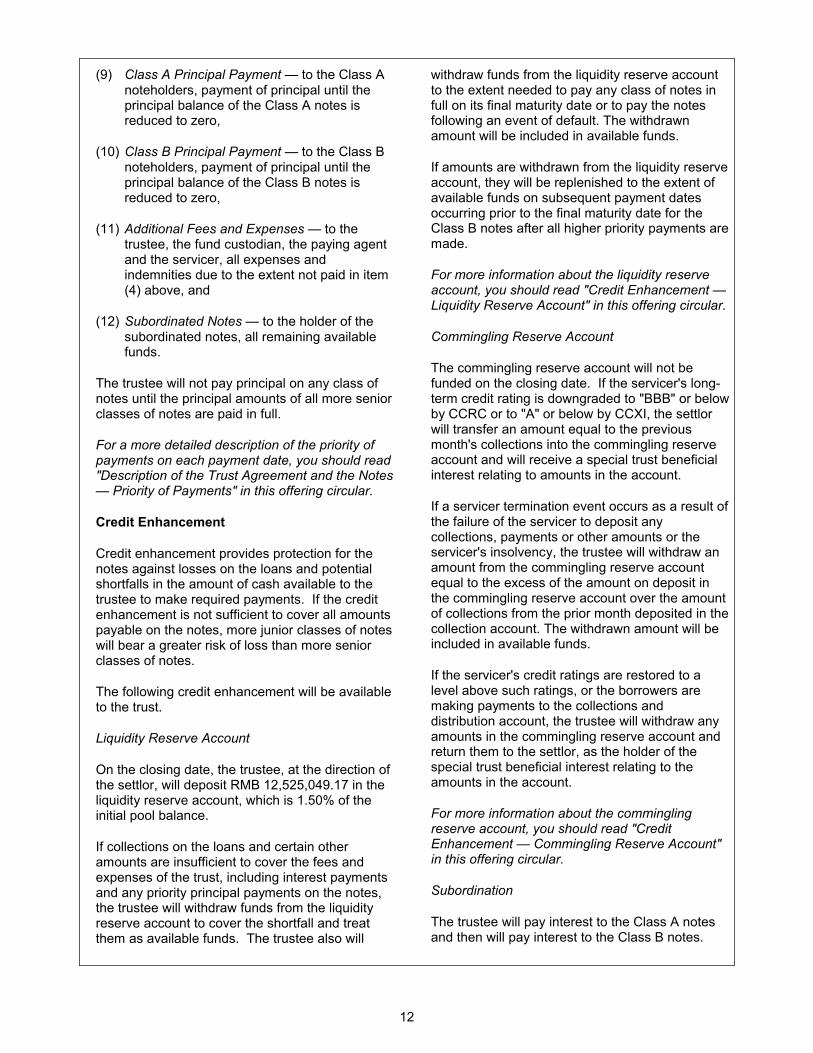

(9) Class A Principal Payment — to the Class A noteholders, payment of principal until the principal balance of the Class A notes is reduced to zero,

(10) Class B Principal Payment — to the Class B noteholders, payment of principal until the principal balance of the Class B notes is reduced to zero,

(11) Additional Fees and Expenses — to the trustee, the fund custodian, the paying agent and the servicer, all expenses and indemnities due to the extent not paid in item (4) above, and

(12) Subordinated Notes — to the holder of the subordinated notes, all remaining available funds.

The trustee will not pay principal on any class of notes until the principal amounts of all more senior classes of notes are paid in full.

For a more detailed description of the priority of payments on each payment date, you should read "Description of the Trust Agreement and the Notes — Priority of Payments" in this offering circular.

Credit Enhancement

Credit enhancement provides protection for the notes against losses on the loans and potential shortfalls in the amount of cash available to the trustee to make required payments. If the credit enhancement is not sufficient to cover all amounts payable on the notes, more junior classes of notes will bear a greater risk of loss than more senior classes of notes.

The following credit enhancement will be available to the trust.

Liquidity Reserve Account

On the closing date, the trustee, at the direction of the settlor, will deposit RMB 12,525,049.17 in the liquidity reserve account, which is 1.50% of the initial pool balance.

If collections on the loans and certain other amounts are insufficient to cover the fees and expenses of the trust, including interest payments and any priority principal payments on the notes, the trustee will withdraw funds from the liquidity reserve account to cover the shortfall and treat them as available funds. The trustee also will

withdraw funds from the liquidity reserve account to the extent needed to pay any class of notes in full on its final maturity date or to pay the notes following an event of default. The withdrawn amount will be included in available funds.

If amounts are withdrawn from the liquidity reserve account, they will be replenished to the extent of available funds on subsequent payment dates occurring prior to the final maturity date for the Class B notes after all higher priority payments are made.

For more information about the liquidity reserve account, you should read "Credit Enhancement —Liquidity Reserve Account" in this offering circular.

Commingling Reserve Account

The commingling reserve account will not be funded on the closing date. If the servicer's long-term credit rating is downgraded to "BBB" or below by CCRC or to "A" or below by CCXI, the settlor will transfer an amount equal to the previous month's collections into the commingling reserve account and will receive a special trust beneficial interest relating to amounts in the account.

If a servicer termination event occurs as a result of the failure of the servicer to deposit any collections, payments or other amounts or the servicer's insolvency, the trustee will withdraw an amount from the commingling reserve account equal to the excess of the amount on deposit in the commingling reserve account over the amount of collections from the prior month deposited in the collection account. The withdrawn amount will be included in available funds.

If the servicer's credit ratings are restored to a level above such ratings, or the borrowers are making payments to the collections and distribution account, the trustee will withdraw any amounts in the commingling reserve account and return them to the settlor, as the holder of the special trust beneficial interest relating to the amounts in the account.

For more information about the commingling reserve account, you should read "Credit Enhancement — Commingling Reserve Account"in this offering circular.

Subordination

The trustee will pay interest to the Class A notes and then will pay interest to the Class B notes.

13

The trustee will not pay interest on the Class B notes until all interest due on the Class A notes is paid in full.

The trustee will pay principal sequentially to each class of notes in order of seniority. The trustee will not pay principal on any class of notes until the principal amounts of all more senior classes of notes are paid in full.

In addition, if a priority principal payment is required on any payment date, the trustee will pay principal to the Class A notes prior to the payment of interest on the Class B notes on that payment date.

For a more detailed description of the priority of payments, including changes to the priority after an event of default, you should read "Description of the Trust Agreement and the Notes — Priority of Payments," "— Post-Default Priority of Payments" and "Credit Enhancement —Subordination" in this offering circular.

Overcollateralization

Overcollateralization is the amount by which the pool balance exceeds the principal amount of the notes. Overcollateralization means there will be additional loans generating collections that will be available to cover shortfalls in interest collections due to any low-interest-rate loans and losses on the loans. The initial amount of overcollateralization for the notes will be RMB 35,194,414.79 or 4.21% of the initial pool balance.

Because a large portion of the loans are subvened loans with low promotional interest rates, theovercollateralization is intended to support the payment of interest on the offered notes and expenses of the trust. Although the overcollateralization is not primarily designed to cover losses on the loans, which are intended to be mitigated by the other credit enhancement factors listed above, the fact that the pool balance exceeds the principal amount of the offered notes will have the effect of creating additional collections that will be available to cover any credit losses.

The initial overcollateralization amount approximates the present value, as of the cut-off date, of the amount by which future payments on the loans with current interest rates below a specified rate are less than what future payments would have been on the loans if their interest rates

were equal to the specified rate. The specified rate is set at a level that will result in an amount of excess spread sufficient to obtain the required ratings on the notes.

This securitization transaction is structured to use all available funds remaining after payments in respect of the senior fees and expenses of the trust, the interest on the notes, any required priority principal payments and any required deposits in the liquidity reserve account, including the portion of such remaining available funds that constitutes excess spread, to make principal payments on the notes until the principal amount of the notes is reduced to zero. As a result, the overcollateralization, as well as the principal amount of the subordinated notes relative to the principal amount of the offered notes, is expected to increase over the life of the transaction as the principal amount of the offered notes is paid more rapidly than the principal of the loans and the principal amount of the subordinated notes.

For a description of low-interest-rate loans originated by the settlor, you should read "Loans –Types of Loans" in this offering circular.

Excess Spread

For any payment date, excess spread is equal to the excess of (a) the interest collections for the preceding month, over (b) the sum of the senior fees and expenses of the trust, the interest on the notes and any required deposits in the liquidity reserve account on the payment date. Any excess spread will be applied on each payment date, as a part of available funds, to make principal payments on the most senior class of notes.

In general, excess spread provides a source of funds to cover losses on the loans. To the extent the amount of excess spread exceeds the amount of any losses, it is available to pay principal on the notes. This causes the principal of the notes to be paid more rapidly than the principal of the loans, which increases the overcollateralization as described under "Description of the Trust Agreement and the Notes — Payments of Principal" in this offering circular.

For a more detailed description of the use of excess spread as credit enhancement for your notes, you should read "Credit Enhancement —Overcollateralization" and "— Excess Spread" in this offering circular.

14

Purchases of Loans

FAFC will make representations about the origination, characteristics and entrustment of the loans. If a representation is later discovered to have been untrue and has a material adverse effect on any loan, or if the trustee's rights with respect to any loan are impaired because a change of registration of the mortgage was not completed, then FAFC must purchase the affectedloan unless it cures the breach. Similarly, if FAFC as servicer materially impairs any loan, it must purchase the impaired loan unless it cures the impairment. In addition, FAFC as servicer will purchase a loan from the trust if it makes certain modifications to the loan or rewrites or reschedules the loan.

For a more detailed description of the representations made about the loans and the purchase obligation if these representations are breached, you should read "Description of the Trust Agreement and the Notes —Representations About the Loans" and "—Obligation to Purchase Ineligible Loans Upon Breach" in this offering circular. For a more detailed description of servicer impaired and servicer modified loans and the purchase obligation for these loans, you should read "Description of the Servicing Agreement and the Servicing of the Loans — Servicer Modifications and Obligation to Purchase Certain Loans" in this offering circular.

Legal Opinions

Beijing Zhong Lun Law Firm will provide legal opinions on certain matters relating to the loans, the trust and this securitization transaction, including that this securitization transaction complies with applicable PRC laws.

For more information about the legal opinions forthis securitization transaction, you should read "Summary of Legal Opinions" in this offering circular.

Tax Status

PricewaterhouseCoopers will provide opinions and analysis on the tax issues for this securitization transaction, including the treatment of payments received by institutional investors in the notes.

For more information about the application of PRC tax laws to this securitization transaction, you should read "Tax Considerations" in this offering circular.

Ratings

The trust expects that the notes will receive the following credit ratings from China Credit Rating Co. Ltd., or "CCRC," and China ChengXin International Credit Rating Co. Ltd., or "CCXI,"and together, the "rating agencies."

CCRC CCXI

Class A notes AAA AAAClass B notes A+ A+

The ratings of the notes will reflect the likelihood of the timely payment of interest on, and the ultimate payment of principal of, the notes according to their terms. Each rating agency rating the notes will monitor the ratings using its normal surveillance procedures. Any rating agency may change or withdraw an assigned rating at any time. Any rating action taken by one rating agency may not necessarily be taken by the other rating agency

15

RISK FACTORS

You should consider the following risk factors in deciding whether to purchase any of the offerednotes.

The trust property is limited and is the only source of payment foryour notes

The trust will not have any assets or sources of funds other than the loans and related property it owns and any credit enhancement described in this offering circular. Any credit enhancement is limited. Your notes will not be insured or guaranteed by the trustee, FAFC or any of their respective affiliates or any other person. If these assets or sources of funds are insufficient to pay your notes in full, you will incur losses on your notes.

Mitigating Factors. Although the trust assets are the only source of payment on your notes, the credit enhancement features of this securitization transaction have been included to support repayment of the notes under various scenarios, including worse than expected performance of the loans and certain unexpected disruptions to collections. This credit enhancement includes a liquidity reserve account that will be funded at closing, a commingling reserve account that will be funded by the settlor in certain situations, subordination, overcollateralization and excess spread. In addition, the criteria used to select the loans and the representations and warranties made by the transaction parties help to ensure that the collections on the loans will be maximized.

Performance of the loans is uncertain

The performance of the loans depends on a number of factors, including general economic conditions, the circumstances of individual borrowers, FAFC's underwriting standards at origination and FAFC's servicing and collection strategies. Consequently, the performance of the loans cannot be predicted with accuracy. If the loans perform worse than expected, you could incur losses on your notes.

Mitigating Factors. FAFC has maintained consistent underwriting and servicing practices and applies these same procedures for all of the loans entrusted to the trustee in this securitization transaction. In addition, the credit enhancement features of this transaction have been included to support repayment of the notes under various scenarios, including worse than expected performance of the loans and certain unexpected disruptions to collections. These features will reduce the likelihood of losses on your notes in the event of unexpected changes in economic conditions and asset pool performance.

The Class B notes will be subject to greater risk because of subordination

The Class B notes will bear greater risk than the Class A notes because no interest will be paid on the Class B notes until all interest due on the Class A notes is paid in full, and no principal will be paid on the Class B notes until the principal amount of the Class A notes is paid in full. In addition, the occurrence or deemed occurrence of an Event of Default, the settlor's exercise of its clean-up call option or the occurrence of a trust termination date may result in a change in the priority of payments on the Class B notes. If you hold Class B notes, you will bear more

16

credit risk than the Class A noteholders and you will incur losses, if any, prior to the Class A noteholders.

Mitigating Factors. Although the Class B notes have a lower payment priority and bear greater risk than the Class A notes, the Class B notes will benefit from other credit enhancement features, including the subordination of the subordinated notes, overcollateralization, excess spread and the liquidity reserve account and commingling reserve account (if funded). These features reduce the possibility that the Class B noteholders will suffer any losses.

The timing of principal payments on your notes is uncertain

The trustee does not have an obligation to pay a specified amount of principal on any note on any date other than its outstanding principal amount on its final maturity date. Failure to pay principal on a note will not constitute an Event of Default until five business days after its final maturity date.

Faster than expected rates of prepayments on the loans will cause the trustee to make payments of principal on the notes earlier than expected and will shorten the maturity of the notes. Prepayments on the loans may occur as a result of:

prepayments of loans by borrowers,

receipts of enforcement proceeds on defaulted loans,

receipts of proceeds from claims on any physical damage and other insurance policies covering the financed vehicles,

purchases by the servicer of loans modified by the servicer or impaired by the servicer, and

purchases of ineligible loans by FAFC.

A variety of economic, social and other factors will influence the rate of prepayments on the loans. No prediction can be made as to the actual prepayment rates that will be experienced on the loans. In addition, the notes will be paid in full prior to maturity if the settlor exercises its clean-up call option.

You will bear all reinvestment risk resulting from receiving payments of principal on your notes earlier or later than expected.

For more information about the timing of repayment and other sources of prepayments, you should read "Interest Rate and Prepayment Sensitivity of the Notes" in this offering circular.

Mitigating Factors. A majority of loans are subvened loans with below market interest rates, which reduces the likelihood that the borrower will prepay the loan. In addition, the loans accrueinterest at a floating rate which adjusts according to changes in the PBOC base lending rate. This also reduces the likelihood of borrowers making prepayments due to reductions in market interest rates. In addition, because the offered notes accrue interest at a floating rate, the impact of changes in timing of

17

repayment on the price and yield of the offered notes will be less than if the offered notes had a fixed interest rate.

Changes in interest rates may impact the price of your notes or reduce excess spread in the transaction

Changes in market interest rates may negatively impact the price of your notes. Also, changes in the PBOC base lending rates will cause adjustments in the interest rates payable on the loans, which may reduce the amount of excess spread in the transaction and negatively impact the performance of yournotes. In addition, since the interest rates on the loans are based on the PBOC lending rate and the interest rates on the notes are based on the PBOC deposit rate there is risk that these rates may diverge and there can be no assurance that these rates will change in a similar manner, which could reduce the amount of interest collections on the loans relative to the amount of interest accruing on your notes.

Mitigating Factors. The offered notes have floating interest rates indexed to the one-year PBOC deposit rate, which will limit the impact of any changes in market interest rates on the price of the offered notes. Furthermore, because the loans are also floating rate and indexed to the PBOC base lending rates, and the PBOC lending and deposit rates are generally adjusted at the same time, the impact on excess spread from changes in market interest rates should be relatively limited.

Interests of other persons in the loans or the related financed vehicles could reduce funds available to pay your notes

If another person acquires an interest in a loan or a related financed vehicle that is superior to the trust's interest, the collections on that loan or the proceeds from the enforcement of that loan may not be available to make payments on your notes. The trustee's interest in the loan is secured by a mortgage over the related financed vehicle, but there are interests under PRC law which could be superior to the trustee’s mortgage right. A person could acquire an interest in a financed vehicle that is superior to the trustee's interest if such person is a property lien creditor according to Article 230 of the Property Law. The tax authority could also have priority over the mortgage if a delinquent tax were incurred before the registration of the mortgage.

In addition, a mortgage on a financed vehicle is registered with the motor vehicle office in the name of FAFC. Due to the administrative burden and cost of changing the mortgage registrations on the large number of loans entrusted to the trustee, the mortgages will not be re-registered in the name of the trustee. If a default on a loan requires exercise of the mortgage rights on the financed vehicle, the failure to change the mortgage registration could prevent the trustee from using the mortgage as a defense against any bona fide third party purchaser, which could result in delays in payments or losses on your notes.

Mitigating Factors. The scope of statutory property lien and priority of the tax authority is limited. The loan is made and the mortgage is registered at the time or immediately after the financed vehicle is purchased. The vehicle tax is usually paid before the registration of the financed vehicle. This limits the likelihood that any delinquent tax could be incurred prior to the registration of the mortgage. With respect to the registration of the mortgage, according to the Property Law, failure to change

18

the mortgage registrations after the settlor has entrusted the loans (including the mortgage rights) to the trustee will have no effect on the legality and validity of the transfer of the mortgages by the settlor to the trustee. The servicing agreement requires the settlor, in its capacity as servicer, to continue to be registered as mortgagee. In addition, the settlor, in its capacity as servicer, holds the originals of the vehicle registration certificates (indicating the settlor as the mortgagee) on behalf of the trustee. Therefore, it is unlikely that a bona fide third party purchaser could prevent the trustee's exercise of its mortgage rights. In addition, if the trustee's rights with respect to any loan are impaired because a change of registration of the mortgage was not completed, the settlor must purchase the affected loanfrom the trustee.

The failure to notify the borrowers of the entrustment of the loans affects the validity of the transfer of the loan with respect to the borrowers

The borrowers will not be notified of the entrustment of the loans to the trustee. Under Article 80 of the Contract Law, such transfer of the loan will not be effective against the borrower until the borrower is notified of such transfer. This means that even after the transfer, the borrower is still entitled to repay the loan to FAFC as the original creditor and claim any offset right towards FAFC, which could result in delays in payments or losses on your notes.

Mitigating Factors. Although not effective against the borrowers, the transfer of the loans will become effective between FAFC and the trustee at the time of the creation of the trust. The guarantors (if any) of the loans will continue to be bound by their guarantees. As servicer, FAFC will continue to collect the payments on the loans from borrowers on behalf of the trustee. If FAFC is terminated as the servicer, FAFC will notify the borrowers of the transfer of the loans, and the transfer will then become effective against the borrowers. In addition, there is no opportunity for offset of payments by the borrowers against FAFC because there are no other contractual relationshipsbetween FAFC and the borrowers.

Regulatory uncertainty may result in delays in certain risks to your investment in the notes

The rules for credit securitization were adopted in 2005 and the Enterprise Bankruptcy Law was adopted in 2006. The practice of credit asset securitization is still at the pilot stage in the PRC. Such short history, together with limited court precedents for these laws and possible future changes in laws relating to securitization, could cause uncertainty. No assurance can be given that any specific performance or particular remedy in connection with the rights under your notes will be upheld or given effect by the PRC courts or arbitration panels. In addition, possible future changes in laws relating to securitization may also adversely affect your investment in the notes.

Mitigating Factors. The trustee and the sponsor of a proposed securitization transaction must submit to the CBRC and the PBOC for review and approval under the securitization pilot program. This means that the regulatory agencies will ensure that this securitization complies with the regulations for asset securitizations. Because the offered notes will be outstanding for a relatively short time, there is less opportunity for changes in law or regulation to affect your notes.

19

Geographic concentration couldresult in delays in payments or losses on your notes

As of the cutoff date, the location of the dealers that sold the financed vehicles were concentrated in the provinces of Jiangsu (16.45%), Guangdong (12.10%), Shangdong (7.58%), Zhejiang (6.71%), Fujian (6.45%), Hebei (5.55%) and Sichuan (5.46%). No other province constituted more than 5% of the initial pool balance. Economic conditions or other factors affecting these provinces, or borrowers in these provinces, in particular could adversely affect the delinquency or credit loss experience of the loans and could result in delays in payments or losses on your notes.

Mitigating Factors. The provinces listed above are located in relatively more economically developed and accessible coastal regions of the PRC. This may lessen the probability or severity of any negative economic factors concentrated in these provinces. In addition, the credit enhancement features of the transaction have been included to support repayment of the notes under various scenarios, including worse than expected performance of the loans and certain unexpected disruptions to collections. These features will help to reduce the likelihood of losses on your notes in the event of unexpected changes in economic conditions and other factors and worse than expectedperformance of the loans.

The secondary market for your notes may be limited and may be disrupted by external factors which are difficult to predict

The trustee will apply for trading of the offered notes in the national inter-bank bond market within 30 days of the completion of the issuance of the offered notes. However, no assurance can be given that the PBOC will approve the offered notes for trading or, if they are approved, that there will be sufficient liquidity in the market to enable noteholders to resell any of the offered notes. You may not be able to trade your notes on the secondary market or may experience loss upon trading in the secondary market due to limited liquidity.

Furthermore, other potential future events including disruptions in the global or Chinese financial markets or reduction, withdrawal or qualification of the ratings on the notes by the rating agencies, are difficult to predict and may occur. These events may cause a reduction in liquidity, drop in market value or an increase in volatility in the secondary market for yournotes.

Mitigating Factors. The weighted average lives of the offerednotes are relatively short, which is expected to benefit the liquidity of the notes and reduce the possibility of unexpected external factors impacting the performance of the notes. In addition, as the asset securitization market develops and the scale of issuance increases and investors' understanding of the market deepens, the liquidity of the market is expected to improve further.

20

An economic downturn could adversely affect the performance of the loans, which could result in losses on your notes

If the PRC experiences an economic downturn, it could adversely affect the performance of the loans entrusted to the trustee. During a downturn, higher unemployment and a lack of availability of credit may lead to increased delinquency and default rates by borrowers and decreased consumer demand for automobiles. If the economic downturn worsens or continues for a prolonged period of time, delinquencies and losses on the loans could increase, which could result in losses on your notes.

Mitigating Factors. The weighted average lives of offered notes are relatively short, which lessens the likelihood that a prolonged economic downturn would significantly impact the performance of the notes. The loan portfolio for this securitization transaction is very diverse, with no single loan making up more than 0.1% of the loans entrusted to the trustee. In addition, the credit enhancement features of the transaction have been included to support repayment of the notes under various scenarios,including worse than expected performance of the loans and certain unexpected disruptions to collections. These features are designed to reduce the likelihood of losses on your notes in the event of unexpected changes in economic conditions and worse than expected performance of the loans.

Delays in collecting payments could occur if FAFC is not the servicer

If FAFC resigns or is terminated as servicer, the processing of payments on the loans and information relating to collections could be delayed or terminated altogether. This could cause payments on your notes to be delayed or reduced. FAFC may be removed as servicer if it defaults on its servicing obligations or becomes subject to bankruptcy proceedings. Further, because the bankruptcy laws in the PRC are relatively new and precedent is limited, no assurance can be given that FAFC would be able to continue servicing the loans or processing payments if it were to become subject to bankruptcy proceedings, which could result in losses on your notes.

Mitigating Factors. A variety of features in this securitization transaction are designed to mitigate these risks. The liquidity reserve account is designed to support timely payment of interest on the offered notes, along with senior fees and trust expenses in the event of short term cash flow disruptions. Thecommingling reserve account is designed to cover potential payment disruptions in the event of the servicer's insolvency. The other credit enhancement features, including subordination, overcollateralization and excess spread, will cover losses on the loans in the event of an extended disruption in collections activity, reducing the likelihood or severity of losses occurring on the offered notes.

The servicer's ability to commingle collections with its own funds could result in reduced or delayed payments onyour notes

The servicer will only be required to deposit collections on the loans in the trust's collection and distribution account on a monthly basis or within three business days of applying collected amounts to the borrower's account, depending on itscredit ratings. Until it deposits collections, the servicer may use them at its own risk and for its own benefit and may commingle collections on the loans with its own funds and collections on other loans in its portfolio. If the servicer does not deposit these amounts into the collection and distribution account when

21

required, you could experience delays in payments or losses on your notes.

Mitigating Factors. If the ratings of the servicer are downgradedbelow specified ratings, the settlor is required to fund thecommingling reserve account. If a servicer termination event occurs as a result of the failure of the servicer to deposit any collections, payments or other amounts or as a result of the occurrence of an insolvency event with respect to the servicer, the funds in the commingling reserve account will be available to cover any shortfall in collections received by the servicer which are not transferred to the collection and distribution account as required.

If FAFC resigns or is terminated as servicer, a replacement servicer may not be available or the servicing fee may be insufficient to attract a replacement servicer

Because the market for auto financing in the PRC is relatively new, if FAFC resigns or is terminated as servicer, there can be no assurance that a replacement servicer could be located and engaged. Even if a replacement servicer can be found, the servicing fee, which is calculated as a fixed percentage of the pool balance, may be insufficient to attract a replacement servicer or cover the actual cost of servicing the loans. In particular, as the pool balance declines, the amount of the servicing fee will decline each month as the pool balance declines, but the servicing costs on each account will remain essentially fixed. This risk is greatest toward the end of a securitization transaction when the pool balance has declined significantly. A delay or inability to find a replacement servicer would delay collection activities on the loans and could delay payments and reports to the noteholders and the trustee, have an adverse impact on amounts collected on defaulted loans and ultimately lead to delays in payments or losses on your notes.

Mitigating Factors. The circumstances in which FAFC may resign or be terminated as servicer are limited. Noteholders may choose to waive any servicer termination event. If the ratings of the servicer are downgraded below specified ratings, the noteholders may select a back-up servicer to be the successor servicer if the servicer is terminated, which would reduce servicing disruptions. If the servicer is terminated or resigns, the credit enhancement features of this securitizationtransaction will help to protect noteholders from disruption in collection activities. In addition, if a successor servicer is appointed, the noteholders may agree to pay the successor servicer a higher servicing fee.

Seizing vehicles relating to defaulted loans may be difficult, and the value of the vehicles are subject to market factors, which could result in delays in payments or losses on your notes

Financed vehicles relating to defaulted loans may only be seized and sold at auction through court proceedings. Initiating legal proceedings, obtaining a favorable judgment and executing on that judgment are time consuming and expensive and are subject to uncertain outcomes. As a result, the inability of the servicer to repossess the financed vehicles relating to defaulted loans could ultimately lead to delays in payments or losses on your notes.

22

Mitigating Factors. FAFC has historically been successful in recovering a portion of the outstanding amount of defaulted loans over time. For more information on the credit loss experience of FAFC, you should read "Settlor and Servicer —Delinquency and Credit Loss Experience and Trends" in this offering circular. In addition, the credit enhancement features of the transaction have been included to support repayment of the notes under various scenarios, including worse than expected performance of the loans and certain unexpected disruptions to collections. These features are designed to absorb losses on the loans in the event of higher frequency vehicle liquidations and lower than expected used vehicles prices, reducing the likelihood or severity of losses occurring on the notes.

A reduction, withdrawal or qualification of the ratings on your notes could adversely affect the market value of your notes and/or your ability to resell your notes

The ratings on the offered notes are not recommendations to purchase, hold or sell the offered notes and do not address market value or investor suitability. The ratings reflect eachrating agency's assessment of the future performance of the loans, the credit enhancement on the offered notes and the likelihood of repayment of the offered notes. There can be no assurance that the offered notes will perform as expected or that the ratings will not be reduced, withdrawn or qualified in the future as a result of a change of circumstances, deterioration in the performance of the loans, errors in analysis or otherwise. Except as described in this offering circular, none of the settloror any of its affiliates will have any obligation to replace or supplement any credit enhancement or to take any other action to maintain any ratings on the offered notes. If the ratings on your notes are reduced, withdrawn or qualified, it could adversely affect the market value of your notes and/or limit your ability to resell your notes. You should make your own evaluation of the future performance of the offered notes and the loans, the credit enhancement on the offered notes and the likelihood of repayment of the offered notes, and not rely solely on the ratings on the offered notes.

Mitigating Factors. The notes are structured with a "turbo"feature that applies all amounts remaining after the payment of interest on the notes and certain senior fees and expenses of the trust to pay principal on the offered notes. This results in the principal amount of the offered notes being paid down faster relative to the reduction in the principal balance of loans, which increases overcollateralization over the life of the transaction, which will support the ratings on the offered notes. In addition, the average lives of the offered notes are relatively short. Therefore, the likelihood of a change in ratings occurring and such change having a negative impact on your notes is relatively limited.

23

SETTLOR AND SERVICER

General

FAFC was established on June 6, 2005 in Shanghai to provide financing services to dealers and end customers for the purchase of Ford-brand vehicles manufactured and sold by Chang'an Ford Automobile, or "CAF," and imported vehicles manufactured by Ford Motor Company (USA), or "Ford," and distributed by Ford Motor China Ltd., or "Ford China," and other vehicles manufactured and distributed by Ford-affiliated companies and joint ventures. FAFC is a non-bank financial institution established under the laws of the PRC and is a wholly-owned subsidiary of Ford Motor Credit Company LLC (USA). FAFC is licensed to conduct all activities within the business scope of an auto finance company, with the exception of leasing. These activities include providing loans for the purchase of automobiles, making loans to automobile dealers for the purpose of purchasing automobiles from the manufacturer and other business approved by the CBRC.

FAFC's primary financing products are:

Retail financing — making auto loans to retail customers to finance the purchase of vehicles from motor vehicle dealers, and

Wholesale financing — making loans to dealers to finance the purchase of vehicle inventory, also known as floorplan financing.

FAFC also services the loans it originates. As servicer, FAFC collects and applies payments on the loans, investigates and administers delinquent, defaulted and charged-off loans and otherwise manages the loans.

FAFC earns its revenue primarily from:

payments on retail loans that it originates and subvention and other support payments from CAF, Ford China and their motor vehicle dealers on low interest-rate financing programs, and

payments on wholesale financing programs.

FAFC will be the settlor of the securitization transaction in which the notes will be issued. FAFC will be the servicer of the loans and the securitization transaction.

Registration and Financial Information

The registration information for FAFC is:

Chinese Name: 福特汽车金融(中国)有限公司English Name: Ford Automotive Finance (China) LimitedRegistered Address: Kerry Parkside Offices, Floors 19-20

1155 Fang Dian Rd.Pudong, Shanghai, PRC

Legal Representative: TRAN NuRegistered Capital: RMB 1,170,000,000

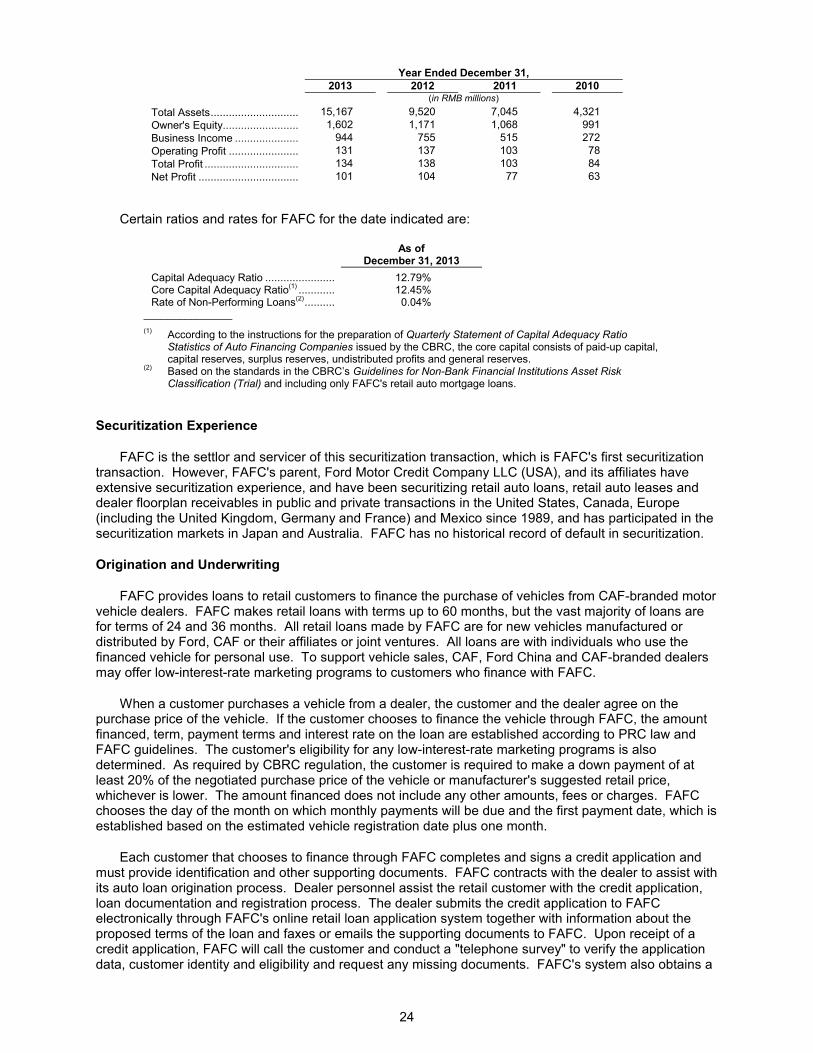

Certain financial information for FAFC for the prior four years is below. The financial information was obtained from the financial reports of FAFC for the periods indicated, which were prepared according togenerally accepted accounting principles. PricewaterhouseCoopers Zhong Tian LLP or its predecessorentity has audited the financial reports for these four years according to generally accepted accounting principles and has presented an audit report with a standard, unqualified opinion.

24

Year Ended December 31,2013 2012 2011 2010

(in RMB millions)

Total Assets................................ 15,167 9,520 7,045 4,321

Owner's Equity................................ 1,602 1,171 1,068 991

Business Income ................................ 944 755 515 272

Operating Profit ................................ 131 137 103 78