Embed Size (px)

DESCRIPTION

Risk tolerance and optimal portfolio choice. Marek Musiela, BNP Paribas, London. Joint work with T. Zariphopoulou (UT Austin). Investments and forward utilities, Preprint 2006 - PowerPoint PPT Presentation

Citation preview

Corporate

Bankingand Investment

Risk tolerance and optimal portfolio choice

Marek Musiela, BNP Paribas, London

2

Corporate

Banking

and Investment

Joint work with T. Zariphopoulou (UT Austin)

Investments and forward utilities, Preprint 2006

Backward and forward dynamic utilities and their associated pricing systems: Case study of the binomial model, Indifference pricing, PUP (2005)

Investment and valuation under backward and forward dynamic utilities in a stochastic factor model, to appear in Dilip Madan’s Festschrift (2006)

Investment performance measurement, risk tolerance and optimal portfolio choice, Preprint 2007

3

Corporate

Banking

and Investment

Contents

Investment banking and martingale theory

Investment banking and utility theory

The classical formulation

Remarks

Dynamic utility

Example – value function

Weaknesses of such specification

Alternative approach

Optimal portfolio

Portfolio dynamics

Explicit solution

Example

4

Corporate

Banking

and Investment

Investment banking and martingale theory

Mathematical logic of the derivative business perfectly in line with the theory

Pricing by replication comes down to calculation of an expectation with respect to a martingale measure

Issues of the measure choice and model specification and implementation dealt with by the appropriate reserves policy

However, the modern investment banking is not about hedging (the essence of pricing by replication)

Indeed, it is much more about return on capital - the business of hedging offers the lowest return

5

Corporate

Banking

and Investment

Investment banking and utility theory

No clear idea how to specify the utility function

The classical or recursive utility is defined in isolation to the investment opportunities given to an agent

Explicit solutions to the optimal investment problems can only be derived under very restrictive model and utility assumptions - dependence on the Markovian assumption and HJB equations

The general non Markovian models concentrate on the mathematical questions of existence of optimal allocations and on the dual representation of utility

No easy way to develop practical intuition for the asset allocation

Creates potential intertemporal inconsistency

6

Corporate

Banking

and Investment

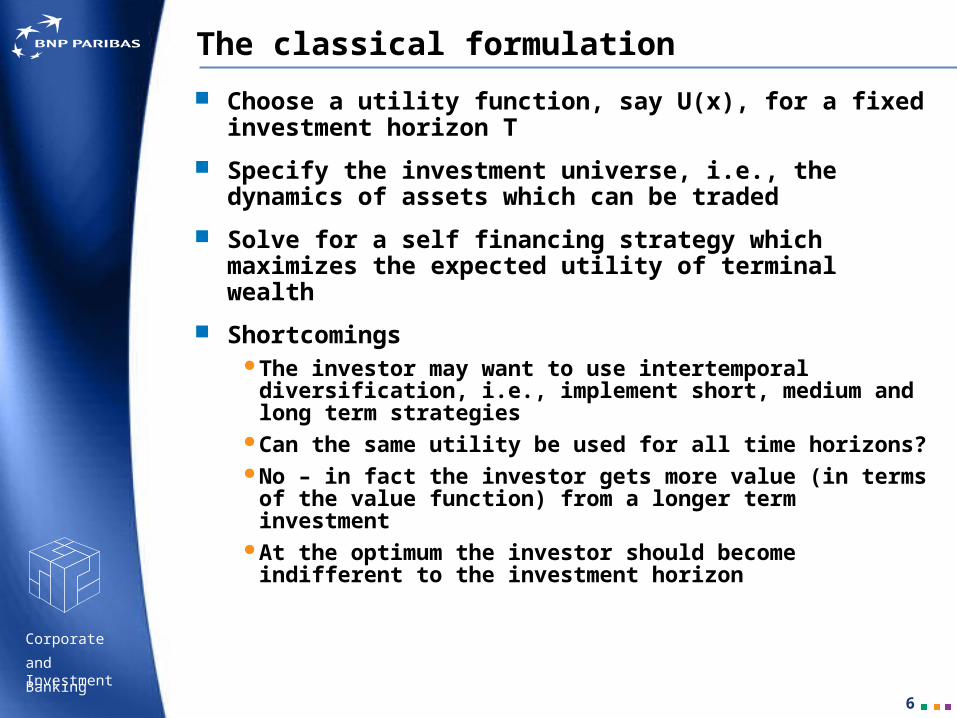

The classical formulation

Choose a utility function, say U(x), for a fixed investment horizon T

Specify the investment universe, i.e., the dynamics of assets which can be traded

Solve for a self financing strategy which maximizes the expected utility of terminal wealth

ShortcomingsThe investor may want to use intertemporal

diversification, i.e., implement short, medium and long term strategies

Can the same utility be used for all time horizons?No – in fact the investor gets more value (in terms of the

value function) from a longer term investmentAt the optimum the investor should become indifferent to

the investment horizon

7

Corporate

Banking

and Investment

Remarks

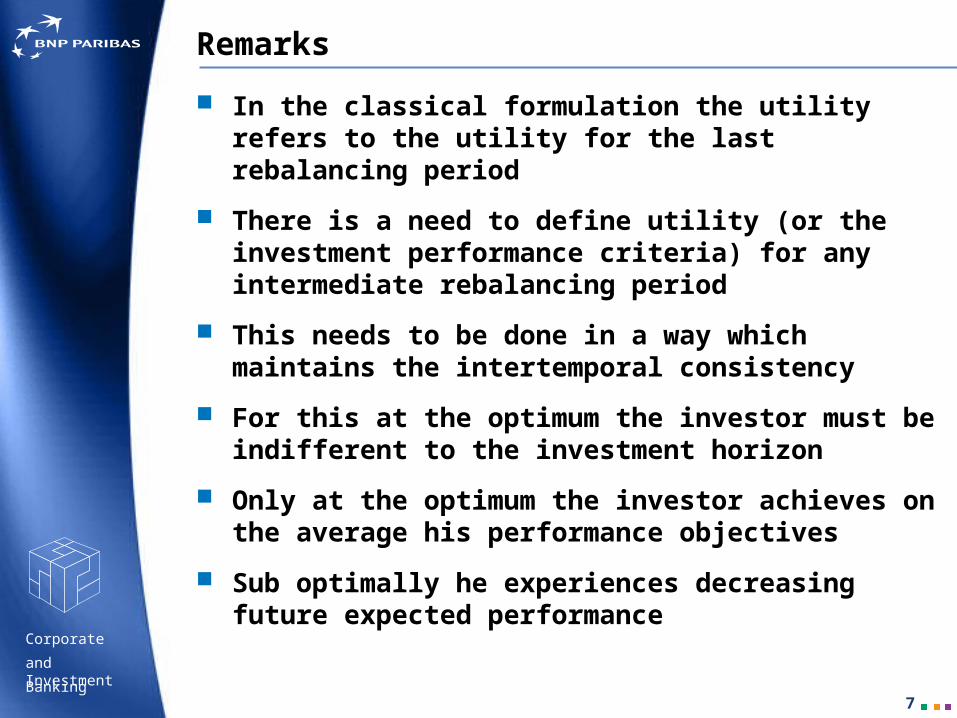

In the classical formulation the utility refers to the utility for the last rebalancing period

There is a need to define utility (or the investment performance criteria) for any intermediate rebalancing period

This needs to be done in a way which maintains the intertemporal consistency

For this at the optimum the investor must be indifferent to the investment horizon

Only at the optimum the investor achieves on the average his performance objectives

Sub optimally he experiences decreasing future expected performance

8

Corporate

Banking

and Investment

Dynamic performance process

U(x,t) is an adapted process

As a function of x, U is increasing and concave

For each self-financing strategy the associated (discounted) wealth satisfies

There exists a self-financing strategy for which the associated (discounted) wealth satisfies

tssXUFtXUE sstP 0,,

tssXUFtXUE sstP 0,,**

9

Corporate

Banking

and Investment

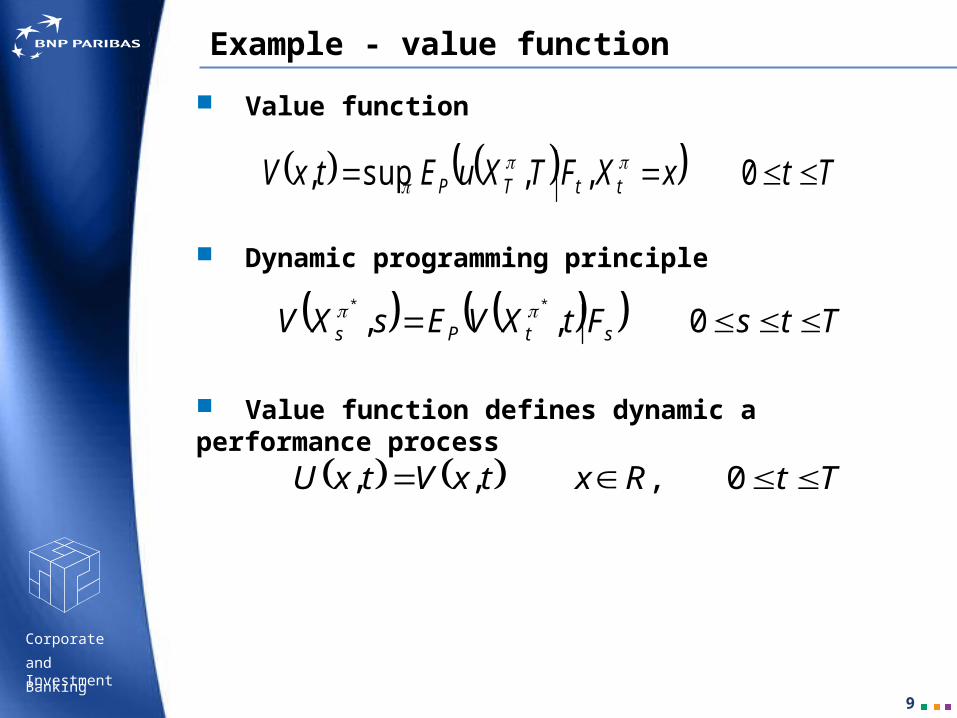

Example - value function

Value function

Dynamic programming principle

Value function defines dynamic a performance process

TtxXFTXuEtxV ttTP 0,,sup,

TtsFtXVEsXV stPs 0,,**

TtRxtxVtxU 0,,,

10

Corporate

Banking

and Investment

Weaknesses of such specification

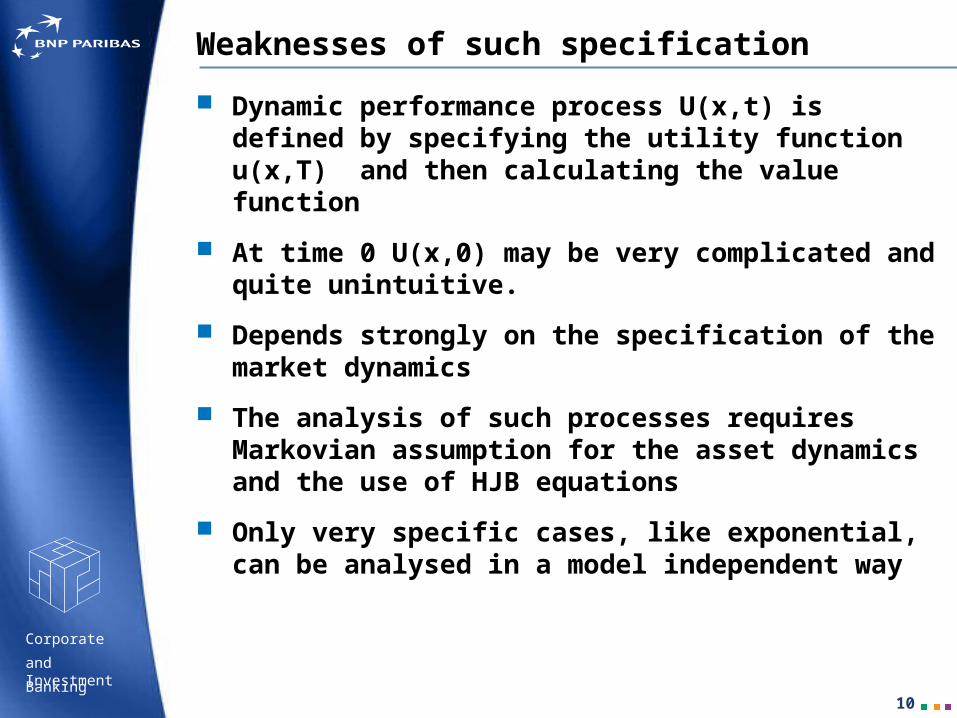

Dynamic performance process U(x,t) is defined by specifying the utility function u(x,T) and then calculating the value function

At time 0 U(x,0) may be very complicated and quite unintuitive.

Depends strongly on the specification of the market dynamics

The analysis of such processes requires Markovian assumption for the asset dynamics and the use of HJB equations

Only very specific cases, like exponential, can be analysed in a model independent way

11

Corporate

Banking

and Investment

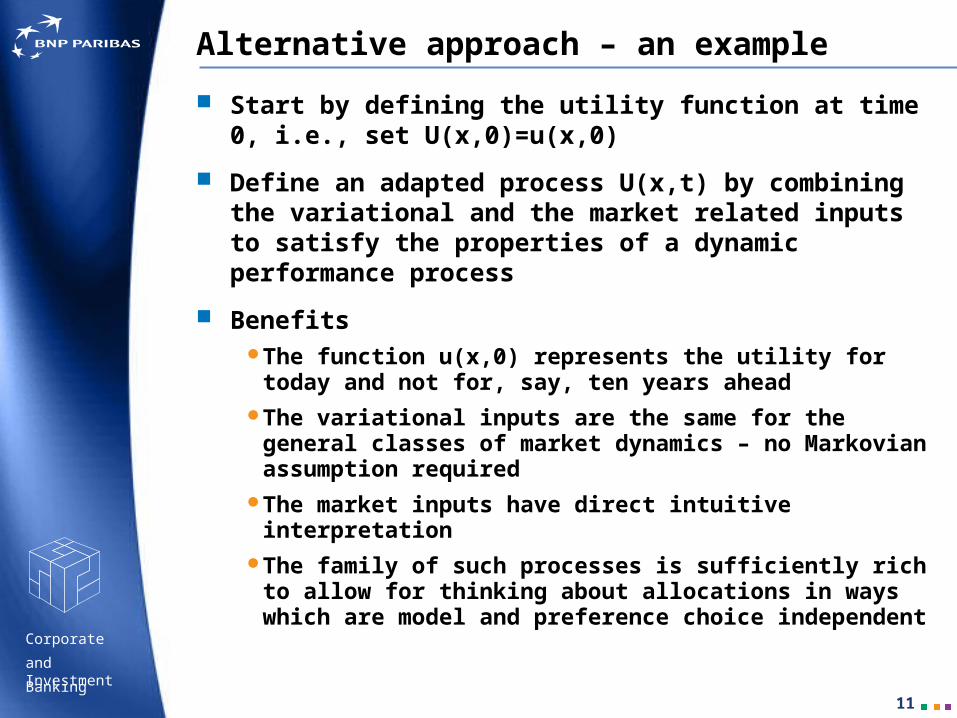

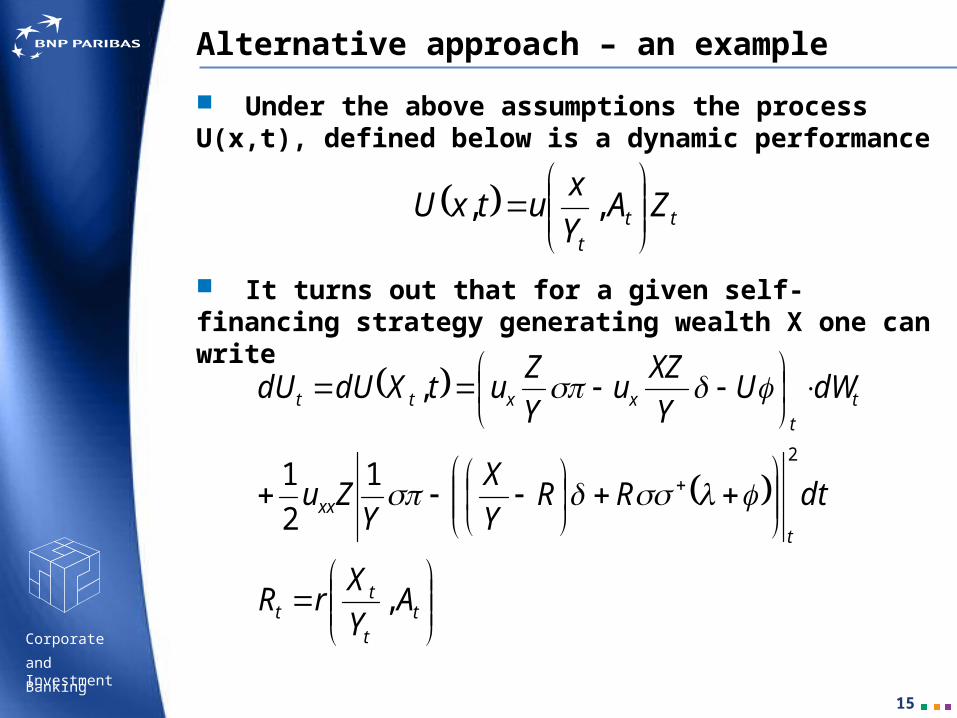

Alternative approach – an example

Start by defining the utility function at time 0, i.e., set U(x,0)=u(x,0)

Define an adapted process U(x,t) by combining the variational and the market related inputs to satisfy the properties of a dynamic performance process

BenefitsThe function u(x,0) represents the utility for today and not

for, say, ten years aheadThe variational inputs are the same for the general classes

of market dynamics – no Markovian assumption required The market inputs have direct intuitive interpretationThe family of such processes is sufficiently rich to allow

for thinking about allocations in ways which are model and preference choice independent

12

Corporate

Banking

and Investment

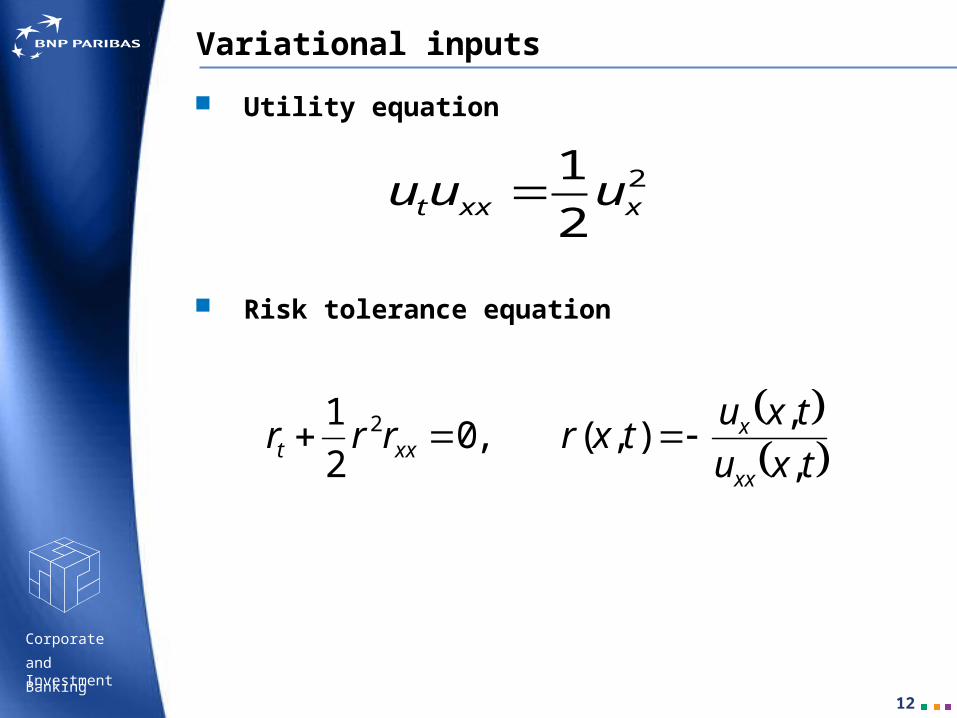

Variational inputs

Utility equation

Risk tolerance equation

2

2

1xxxt uuu

txu

txutxrrrr

xx

xxxt ,

,),(,0

2

1 2

13

Corporate

Banking

and Investment

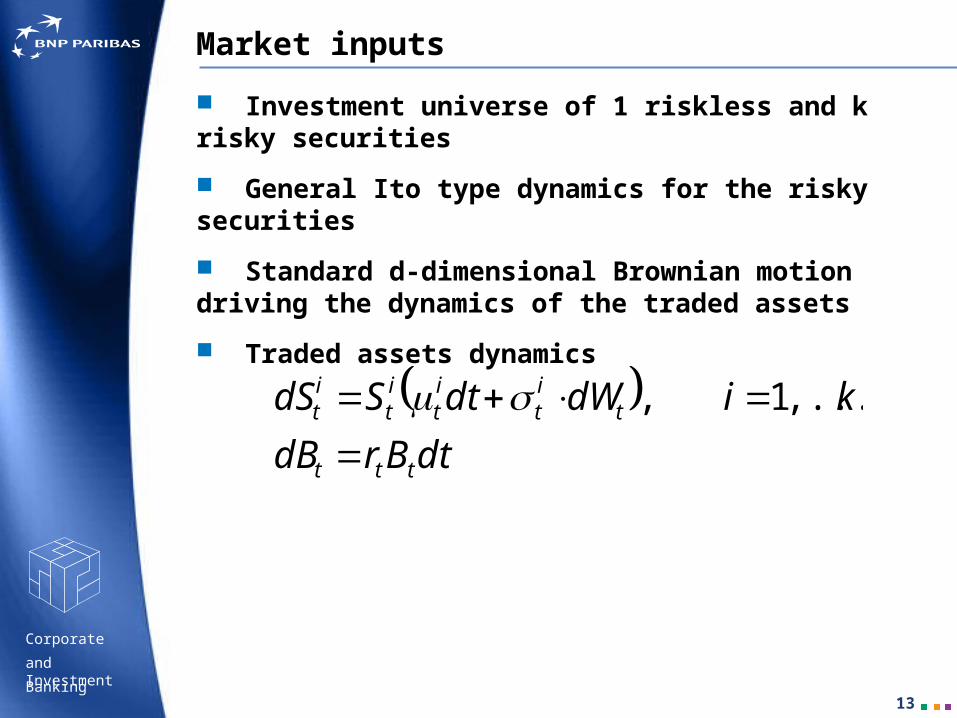

Market inputs

Investment universe of 1 riskless and k risky securities

General Ito type dynamics for the risky securities

Standard d-dimensional Brownian motion driving the dynamics of the traded assets

Traded assets dynamics

dtBrdB

kidWdtSdS

ttt

tit

it

it

it

,...,1,

14

Corporate

Banking

and Investment

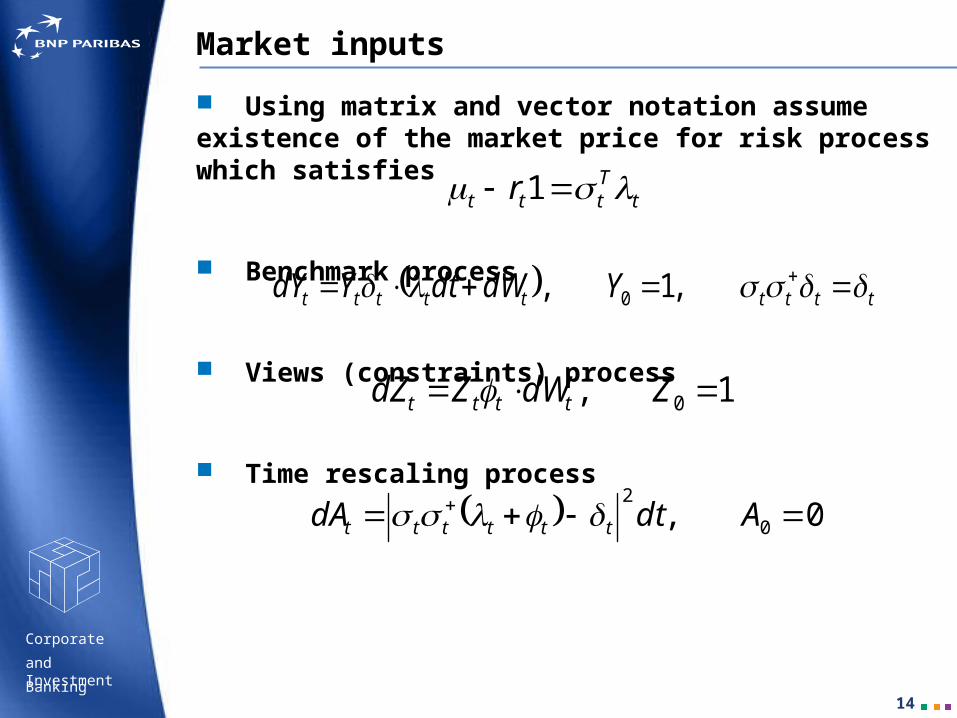

Market inputs

Using matrix and vector notation assume existence of the market price for risk process which satisfies

Benchmark process

Views (constraints) process

Time rescaling process

tTttt r 1

ttttttttt YdWdtYdY ,1, 0

1, 0 ZdWZdZ tttt

0, 0

2 AdtdA tttttt

15

Corporate

Banking

and Investment

Alternative approach – an example

Under the above assumptions the process U(x,t), defined below is a dynamic performance

It turns out that for a given self-financing strategy generating wealth X one can write

ttt

ZAY

xutxU

,,

tt

tt

t

xx

tt

xxtt

AY

XrR

dtRRY

X

YZu

dWUY

XZu

Y

ZutXdUdU

,

1

2

1

,

2

16

Corporate

Banking

and Investment

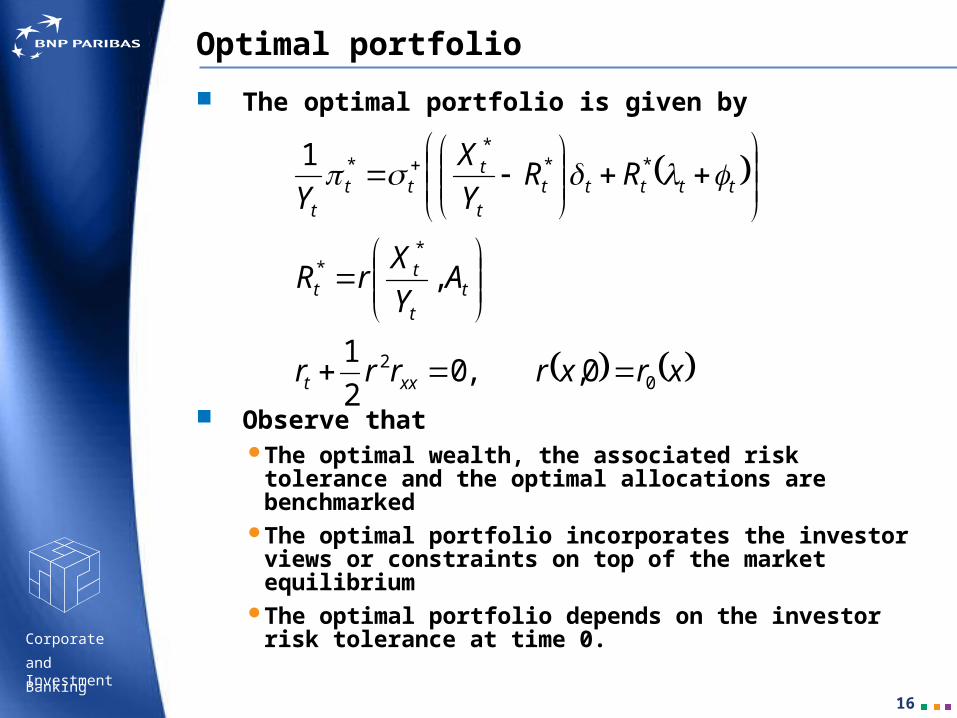

Optimal portfolio

The optimal portfolio is given by

Observe thatThe optimal wealth, the associated risk tolerance and

the optimal allocations are benchmarkedThe optimal portfolio incorporates the investor views or

constraints on top of the market equilibriumThe optimal portfolio depends on the investor risk

tolerance at time 0.

xrxrrrr

AY

XrR

RRY

X

Y

xxt

tt

tt

tttttt

ttt

t

02

**

***

*

0,,02

1

,

1

17

Corporate

Banking

and Investment

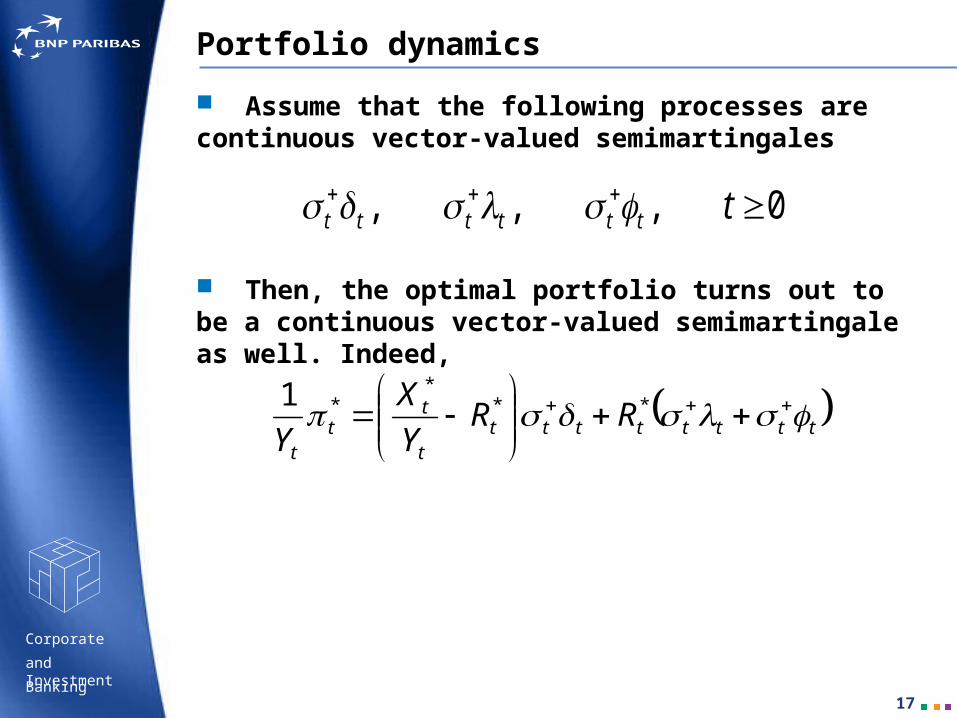

Portfolio dynamics

Assume that the following processes are continuous vector-valued semimartingales

Then, the optimal portfolio turns out to be a continuous vector-valued semimartingale as well. Indeed,

ttttttttt

tt

t

RRY

X

Y

**

**1

0,,, ttttttt

18

Corporate

Banking

and Investment

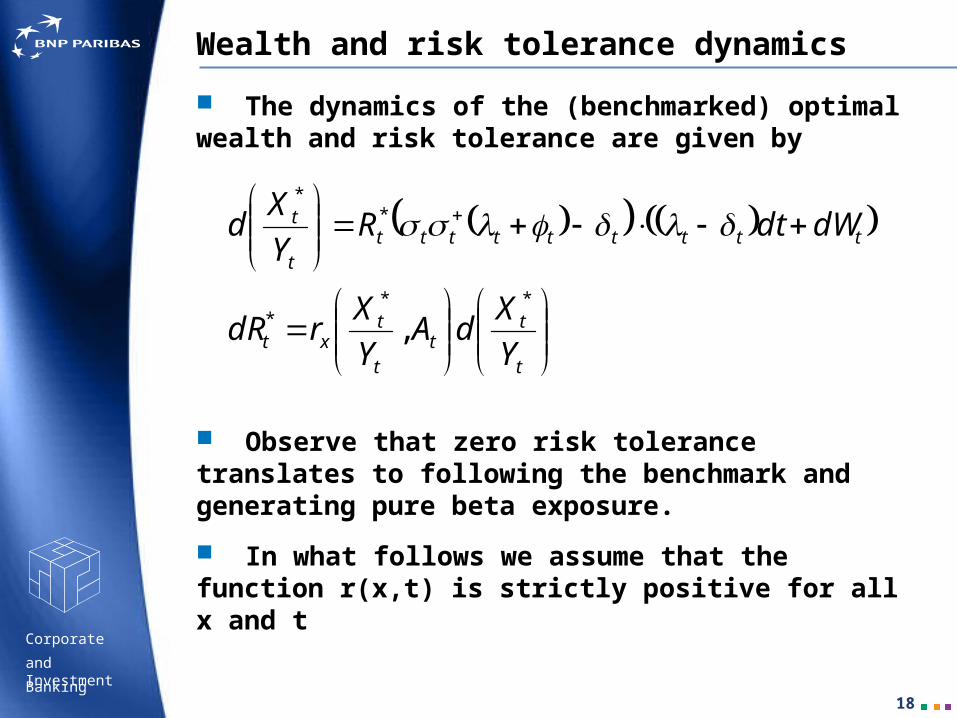

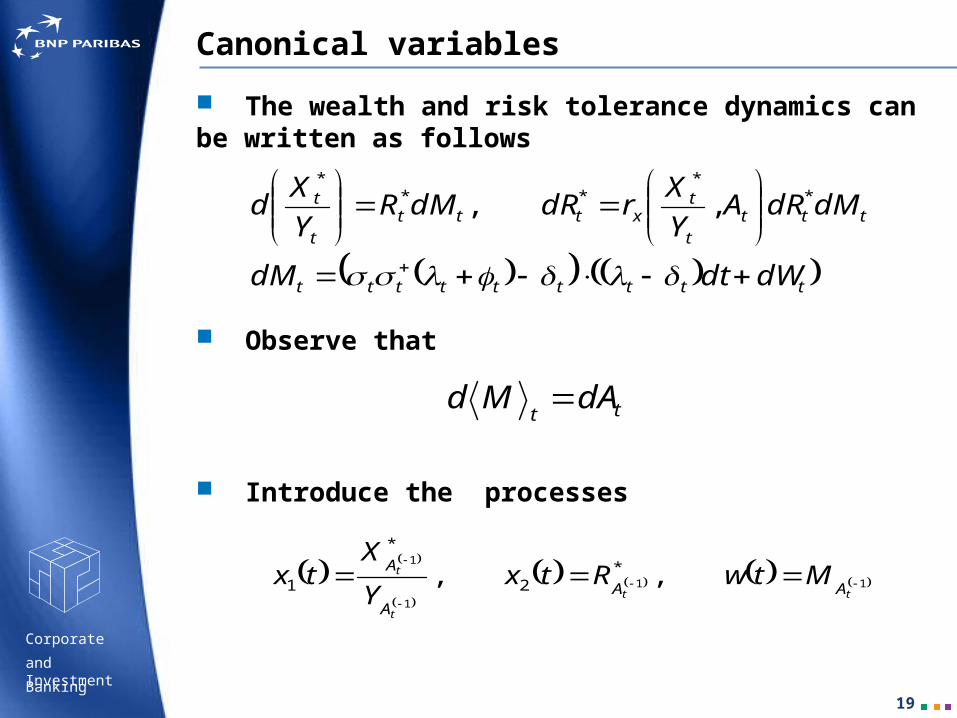

Wealth and risk tolerance dynamics

The dynamics of the (benchmarked) optimal wealth and risk tolerance are given by

Observe that zero risk tolerance translates to following the benchmark and generating pure beta exposure.

In what follows we assume that the function r(x,t) is strictly positive for all x and t

t

tt

t

txt

tttttttttt

t

Y

XdA

Y

XrdR

dWdtRY

Xd

***

**

,

19

Corporate

Banking

and Investment

Canonical variables

The wealth and risk tolerance dynamics can be written as follows

Observe that

Introduce the processes

ttttttttt

tttt

txttt

t

t

dWdtdM

dMdRAY

XrdRdMR

Y

Xd

**

***

,,

ttdAMd

11

1

1

,, *2

*

1

tt

t

t

AAA

A MtwRtxY

Xtx

20

Corporate

Banking

and Investment

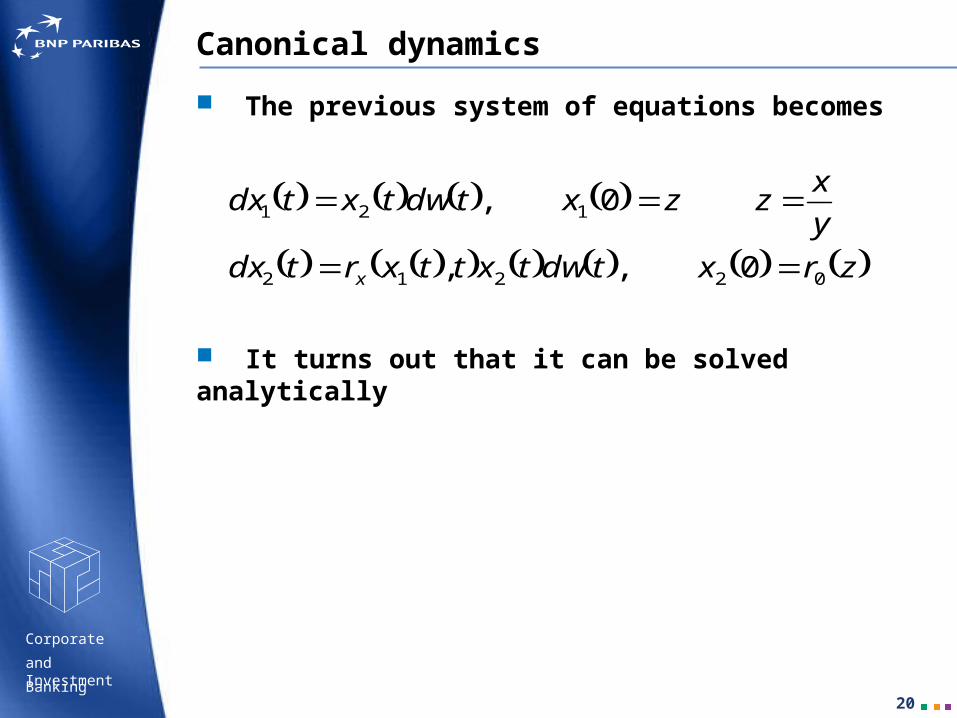

Canonical dynamics

The previous system of equations becomes

It turns out that it can be solved analytically

zrxtdwtxttxrtdx

y

xzzxtdwtxtdx

x 02212

121

0,,

0,

21

Corporate

Banking

and Investment

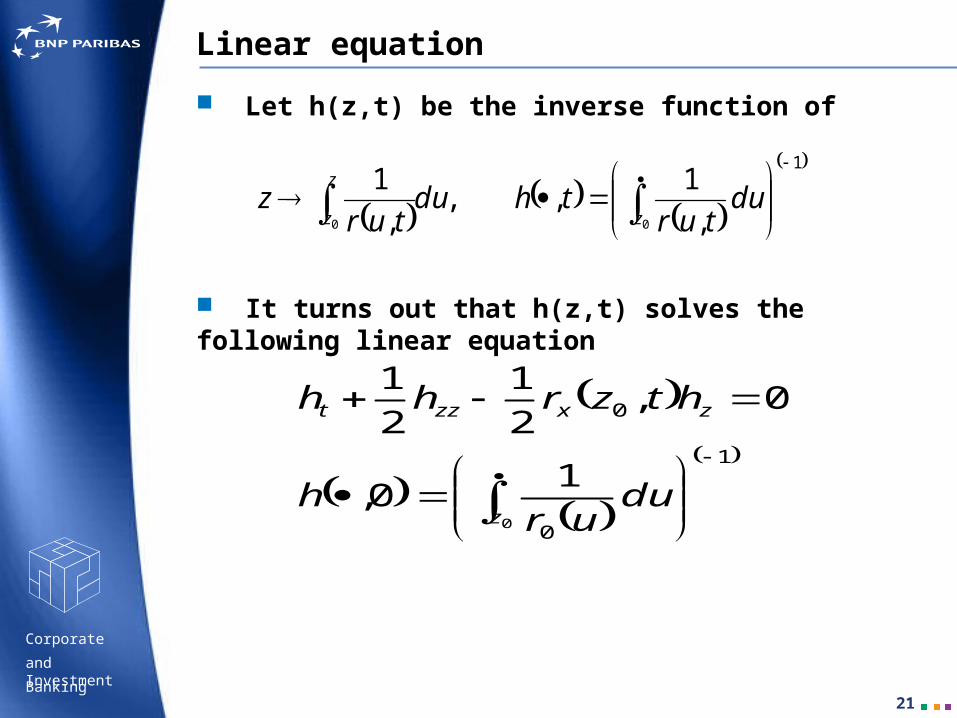

Linear equation

Let h(z,t) be the inverse function of

It turns out that h(z,t) solves the following linear equation

1

00 ,

1,,

,

1

z

z

zdu

turthdu

turz

1

0

0

0

10,

0,2

1

2

1

z

zxzzt

duur

h

htzrhh

22

Corporate

Banking

and Investment

Explicit representation

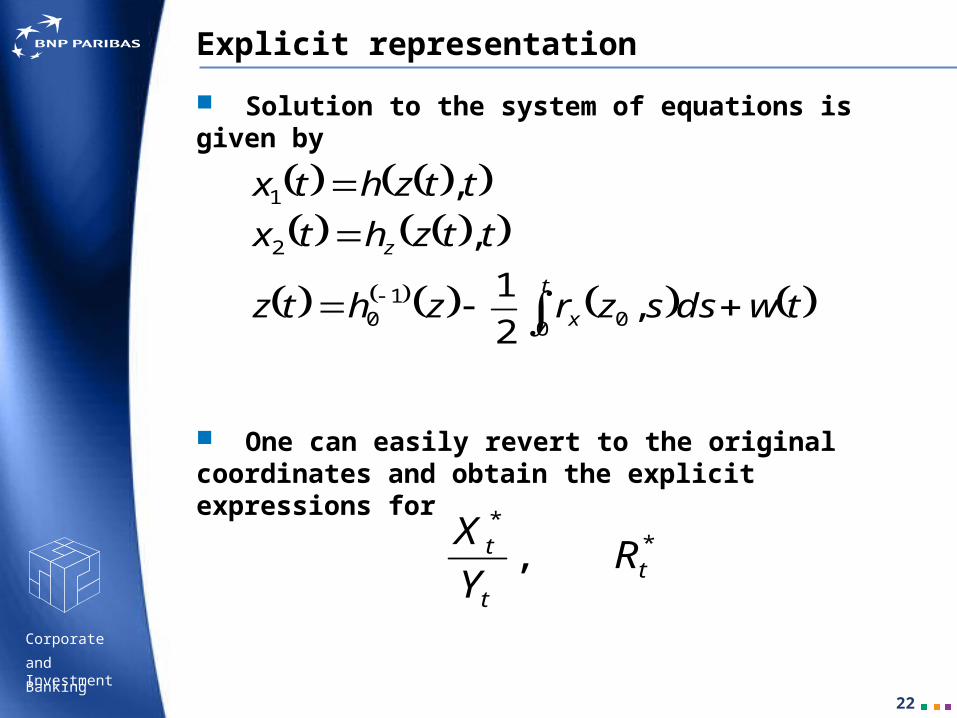

Solution to the system of equations is given by

One can easily revert to the original coordinates and obtain the explicit expressions for

t

x

z

twdsszrzhtz

ttzhtx

ttzhtx

0 01

0

2

1

,2

1

,

,

**

, tt

t RY

X

23

Corporate

Banking

and Investment

Optimal wealth

The optimal (benchmarked) wealth can be written as follows

dtMddA

dWdtdM

MdAAzrzhAz

dutur

thAAzhAxY

X

ttttttt

ttttttttt

tss

t

xt

ztttt

t

2

00

10

1

1

*

,2

1

,

1,,

0

24

Corporate

Banking

and Investment

Corresponding risk tolerance

The risk tolerance process can be written as follows

dtMddA

dWdtdM

MdAAzrzhAz

dutur

thAAzhAxR

ttttttt

ttttttttt

tss

t

xt

zttztt

2

00

10

1

2*

,2

1

,

1,,

0

25

Corporate

Banking

and Investment

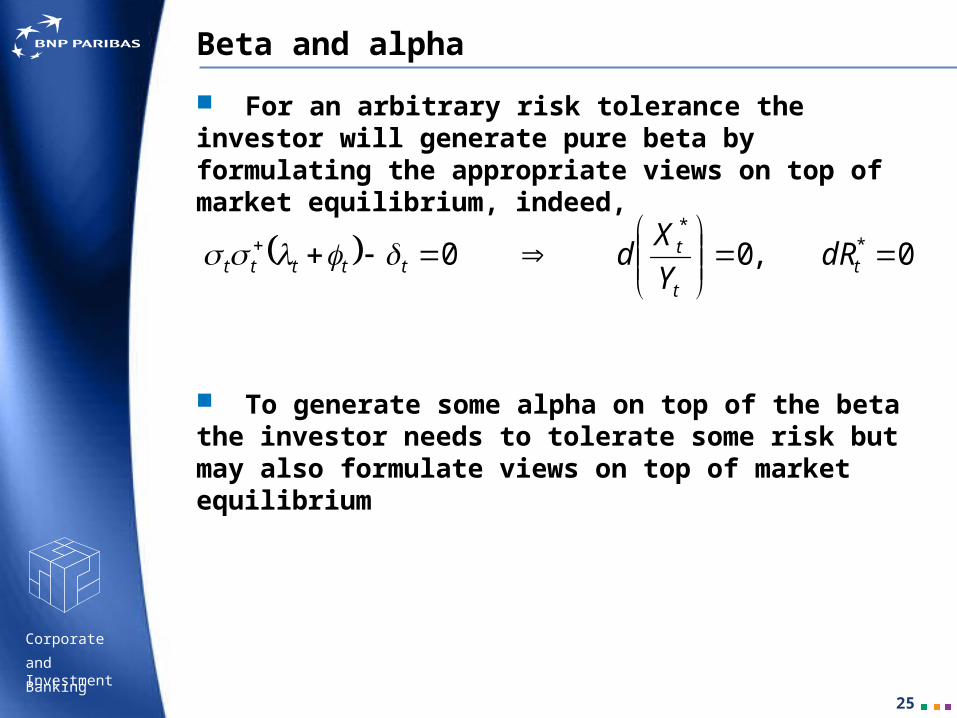

Beta and alpha

For an arbitrary risk tolerance the investor will generate pure beta by formulating the appropriate views on top of market equilibrium, indeed,

To generate some alpha on top of the beta the investor needs to tolerate some risk but may also formulate views on top of market equilibrium

0,00 **

tt

tttttt dR

Y

Xd

26

Corporate

Banking

and Investment

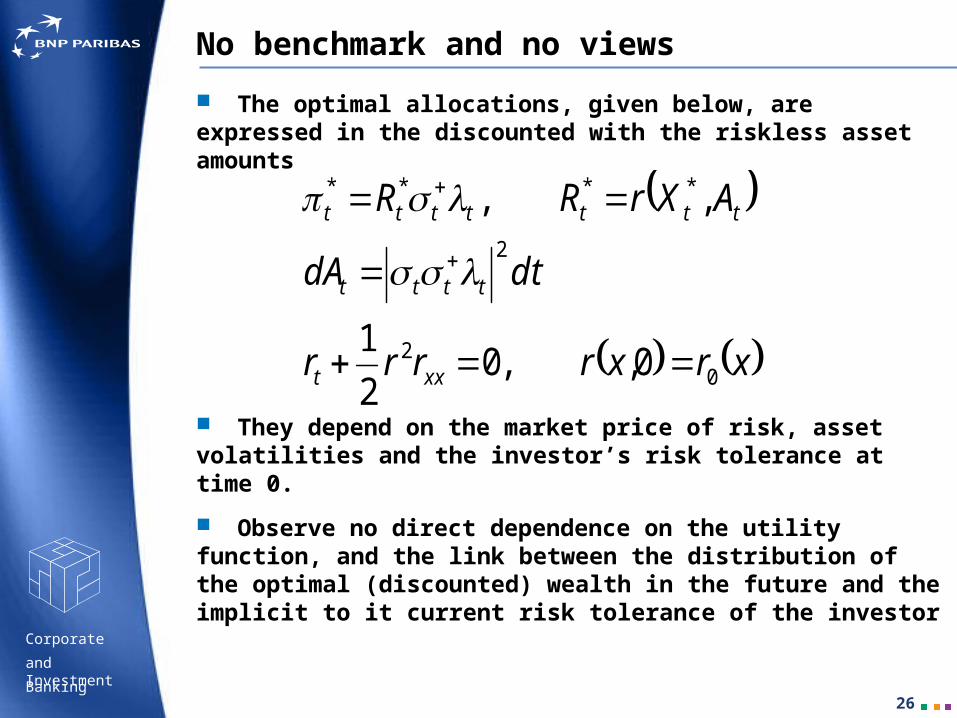

No benchmark and no views

The optimal allocations, given below, are expressed in the discounted with the riskless asset amounts

They depend on the market price of risk, asset volatilities and the investor’s risk tolerance at time 0.

Observe no direct dependence on the utility function, and the link between the distribution of the optimal (discounted) wealth in the future and the implicit to it current risk tolerance of the investor

xrxrrrr

dtdA

AXrRR

xxt

tttt

ttttttt

02

2

****

0,,02

1

,,

27

Corporate

Banking

and Investment

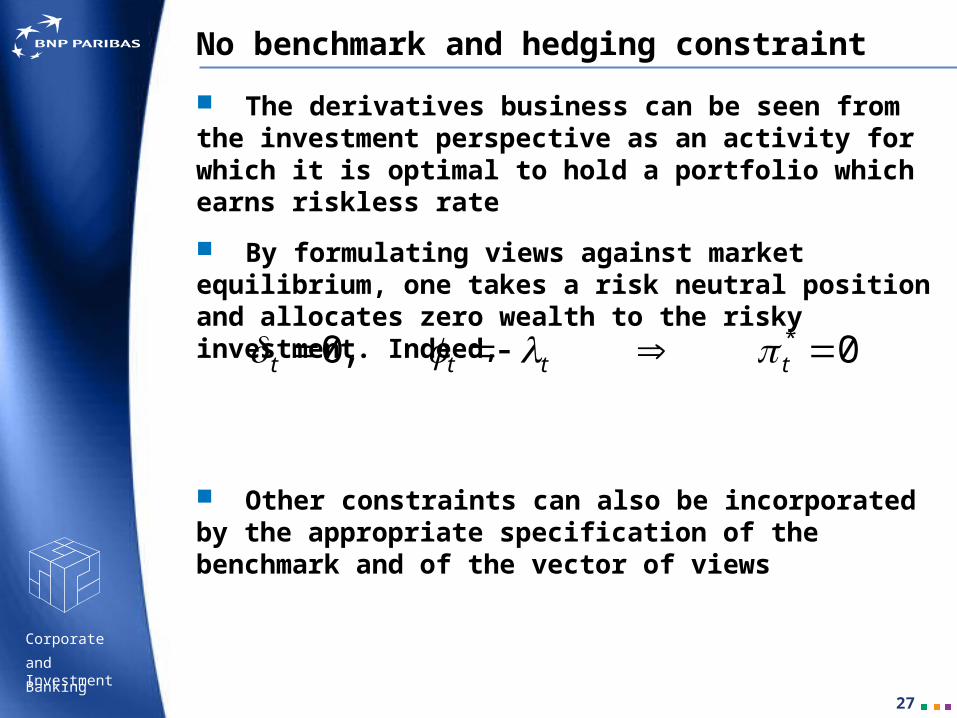

No benchmark and hedging constraint

The derivatives business can be seen from the investment perspective as an activity for which it is optimal to hold a portfolio which earns riskless rate

By formulating views against market equilibrium, one takes a risk neutral position and allocates zero wealth to the risky investment. Indeed,

Other constraints can also be incorporated by the appropriate specification of the benchmark and of the vector of views

0,0 * tttt

28

Corporate

Banking

and Investment

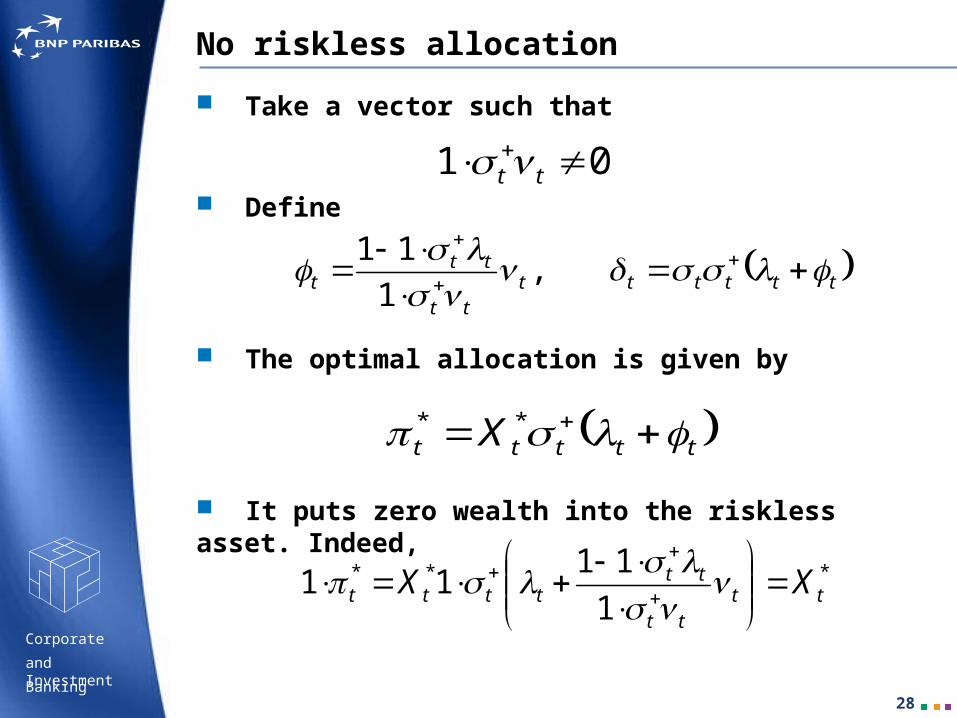

No riskless allocation

Take a vector such that

Define

The optimal allocation is given by

It puts zero wealth into the riskless asset. Indeed,

01 tt

tttttttt

ttt

,1

11

ttttt X **

***

1

1111 tt

tt

tttttt XX

29

Corporate

Banking

and Investment

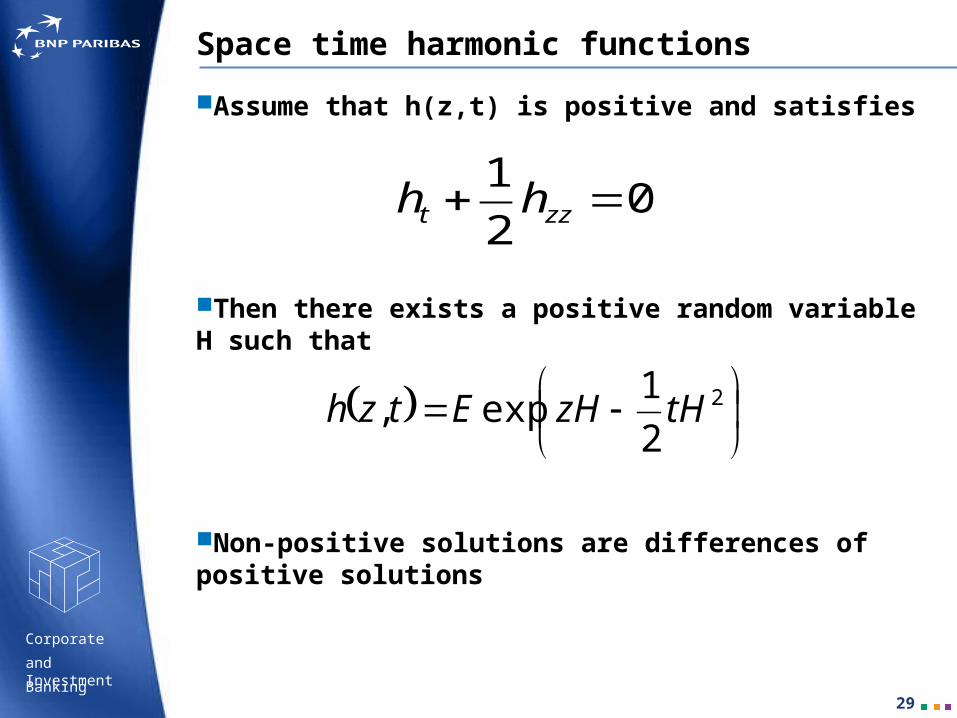

Space time harmonic functions

Assume that h(z,t) is positive and satisfies

Then there exists a positive random variable H such that

Non-positive solutions are differences of positive solutions

02

1 zzt hh

2

2

1exp, tHzHEtzh

30

Corporate

Banking

and Investment

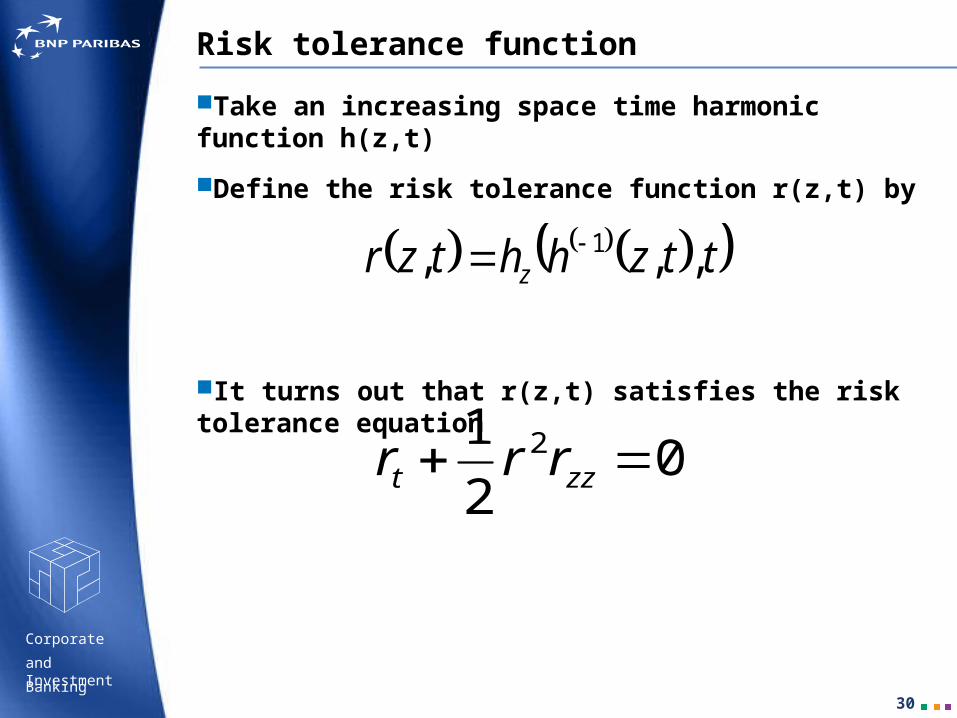

Risk tolerance function

Take an increasing space time harmonic function h(z,t)

Define the risk tolerance function r(z,t) by

It turns out that r(z,t) satisfies the risk tolerance equation

ttzhhtzr z ,,, 1

02

1 2 zzt rrr

31

Corporate

Banking

and Investment

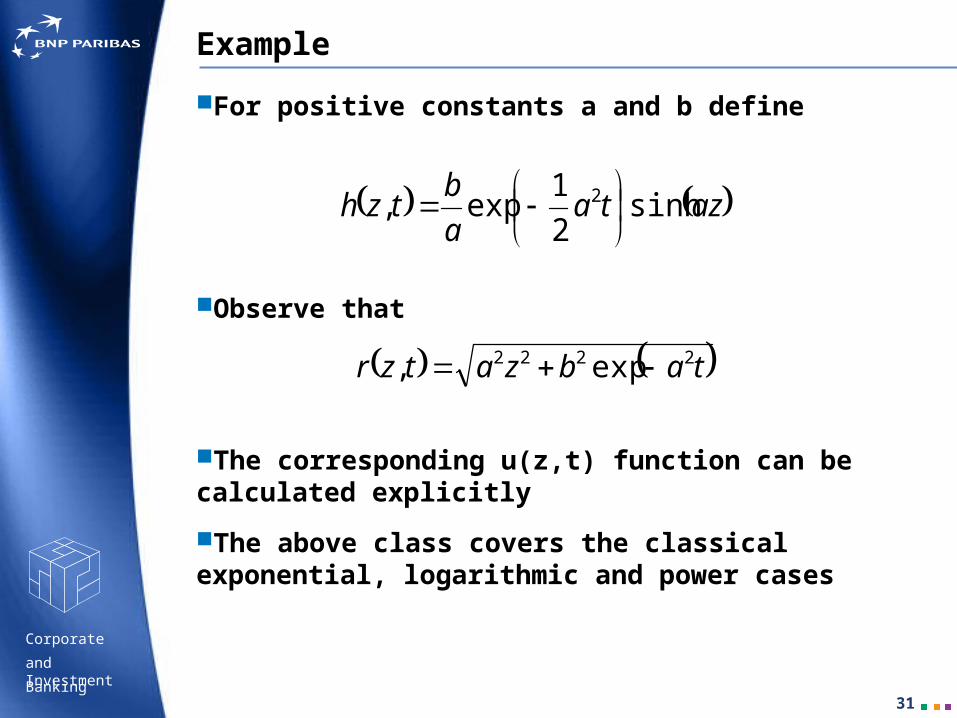

Example

For positive constants a and b define

Observe that

The corresponding u(z,t) function can be calculated explicitly

The above class covers the classical exponential, logarithmic and power cases

aztaa

btzh sinh

2

1exp, 2

tabzatzr 2222 exp,