-

8/11/2019 Risk Return Diversification

1/10

Risk and Return - IIDiversifcation:What happens to the riskiness

o an average 1-stockportolio as more stocks are added?

Risk would decrease because the added stocks wouldnot be

perectly correlated but Return would remainrelatively constant

Market risk is that part o a security!s stand-alone risk

thacannotbe eliminated by diversifcationFirm-specifc risk is that

part o a security!s stand-alonerisk which can be eliminated by

proper diversifcation

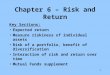

"s more stocks are added# each new stock has a smalle

risk-reducing impact $y orming portolios# we can eliminate about

hal the

riskiness o individual stocks %&'( vs 1)(*

# Stocks in Portfolio10 20 30 40 2000+

Company Specific Risk

MarketRisk

35

18

0

Stand!lone Risk"

p

p$%

-

8/11/2019 Risk Return Diversification

2/10

spalls very slowly ater about +, stocks are included

he lower limit or spis about s./ 1)(

0 you choose to hold a one-stock portolio and thus ar

eposed to more risk than diversifed investors# woul

you be compensated or the total risk you bear? 234 5ou can get

rid o diversifable risk easily#

cheaply 0 you choose not to diversiy# you won!t be

compensated with a higher epected return or risk youcould

eliminate so easily

5ou will only receive a higher return or risk that you

can!t diversiy away 6 market risk

Beta = Cov (X,Y)/Var (X)

Where X = Market Returns

Y = Security Returns

Total Risk = Variance o Security

Syste!atic Risk = Beta X Variance o Market

"nsyste!atic Risk = Total Risk # Syste!atic Risk

-

8/11/2019 Risk Return Diversification

3/10

Markowitz Model

Harry M. Markowitz is credited with introducing new

concepts of risk measurement and their application to

thselection of portfolios.

Started idea with risk aversion of average investors andesire to

maximize return with given risk or vice versa

He used statistical analysis for selection of assets in th

portfolio in an efficient manner.

Markowitz generated a number of portfolios within a give

amount of money

Combined risk of two assets taken separately is not thsame risk

of two assets together, thus two securities likata Motors !nd

"#$%!&C# don't have same risk class

he "isk index is measured by the variance or th

distribution around the mean, its range etc. ()ariance

anCovariance*

his led to what is called the Modern +ortfolio heory Combination

of securities called +ortfolio

!ssumption of Markowitz heory. %nvestors are rational-. ree

access to fair and correct information/. Markets are efficient and

absorb information 0uickly

1. %nvestors are risk averse and try to minimize risk2.

%nvestors' decision based on return and S.3.4. %nvestors prefer

higher returns to lower for given leve

of risk

-

8/11/2019 Risk Return Diversification

4/10

What is the CAPM?"n e7uilibrium model speciying the

relationship

betweenrisk and re7uired return on assets held

indiversifedportolios

Assumptions o the CAPM 0nvestors all think in terms o a single

period

"ll investors have the same epectations

0nvestors can borrow or lend unlimited amounts at the

risk ree rate "ll assets are perectly divisible

here are no taes or transactions costs

"ll investors are price takers# ie# can!t in8uence thestock

prices 9uantities o all assets are given and fed

&fficient Portfolio

'

rf

Risk (reeRet)rn *

Market Ret)rn * rm

&,!1'0

SM$5 ri6 r

f7 8

i(r

M 9 r

f*

-

8/11/2019 Risk Return Diversification

5/10

-

8/11/2019 Risk Return Diversification

6/10

0ndi=erence curve / investor!s attitude toward risk as

re8ected in risk>return tradeo= unction 3ptimal portolio /

tangency point between the e

-

8/11/2019 Risk Return Diversification

7/10

;

-

8/11/2019 Risk Return Diversification

8/10

The CM* '+uation

What does the CML tell us?hat any investor can achieve a

portolio with a total

risk>return tradeo= on the G. easily /H mi themarket portolio

and treasury bills

he epected rate o return on any ereturn

tradeo= o any portolioThis tells us aout portolios! "hat aout

indi#idual

securities??? 0t turns out# that i you Jump %mathematically* on

the

G. long enough# you get the K. 6 the Kecurity .arkeine

0nvestors like r and dislike L

"s number o securities increases# only covariance

matter

he L o a well diversifed portolio depends only on.arket Risk

Gontribution o a security to mkt portolio relative to

the average / M$eta and .arket Risk

kp* k

R(+

Slope

/ntercept

7

p'

kM k

R(

7

M

-

8/11/2019 Risk Return Diversification

9/10

$ecurit% Market Line

0 beta / 1,# stock is average risk

0 beta H 1,# stock is riskier than average

0 beta N 1,# stock is less risky than average

Covariance ith the!arket

-

m

im

iB

=

Variance o the !arket

&fficient

Portfolio

'

rf

Risk (ree

Ret)rn *

Market Ret)rn * rm

&,!1'0

SM$5 ri6 r

f7 8

i(r

M 9 r

f*

-

8/11/2019 Risk Return Diversification

10/10

.ost stocks have betas in the range o ,' to 1'

G. and K.

Cse G. to value portolios

Cse K. to value securities %portolios* that will be heldin a

well diversifed portolio

CM*.

K.: ri / r I Mi%r. - r*

P

M

fM

fP

rrrr

=

+