Embed Size (px)

Citation preview

Risk Management Imperative in the New World Order

35th Asian Bankers Association (ABA) General Meeting and Conference

Kurumba Resort, Maldives

15-16 November 2018

CHUCHI G. FONACIER

Deputy Governor

Financial Supervision Sector

1 Risk Management (IMMC)

2 The Risk We Face in This New World Order

3 BSP Strategies

4 Key Takeaways

THIS PRESENTATION

2

Identifying

Measuring

Monitoring

Controlling

RISK MANAGEMENT IS AN EVOLVING PROCESS

I

M

C

M

3

THE RISKS WE FACE IN THIS GLOBALIZED WORLD

Slowdown in Global Growth

Rising Interest

Rates

Contagion

Emerging Market

4Source: IMF Global Financial Stability Report – October 2018

Macroeconomic Risks

LARGE BANKS SMALL BANKS

Institutional Risk

Cybersecurity AML Credit Risk

Technology Risk

Global

RISKS FROM THE PERSPECTIVE OF PHILIPPINE BANKS

5Source: BSP Banking Sector Outlook Survey 2018

Liquidity: Ample level of liquidity with adequate HQLAs

Capitalization: Adequate capital supporting lending activities

15.2

15.8

13.0

14.0

15.0

16.0

17.0

18.0

Mar-

14

Jun

-14

Sep

-14

Dec-

14

Mar-

15

Jun

-15

Sep

-15

Dec-

15

Mar-

16

Jun

-16

Sep

-16

Dec-

16

Mar-

17

Jun

-17

Sep

-17

Dec-

17

Mar-

18

Jun

-18

Universal and Commercial Banks: Capital Adequacy Ratio

As of End-Period Indicated, In Percent

Solo basis Consolidated basis

PERFORMANCE OF THE BANKING INDUSTRY

18

5.3

17

1.8

18

0.2

18

7.8

18

5.7

18

2.4

17

5.2

17

0.3

17

8.7

16

6.5

17

4.0

18

1.3

18

0.5

17

5.8

16

8.4

16

2.5

24

6.2

23

0.6

24

6.4

25

3.4

23

4.7

25

1.7

24

3.6

25

8.6

100

120

140

160

180

200

220

240

260

280

Sep-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr -18 May-18 Jun-18

Universal and Commercial Banks: LCR (Solo Basis)

As of End-Period Indicated, In Percent

Industry Domestic Banks Foreign Banks

6

Sources: BSP, Supervisory Data Center

Leverage: Leeway to increase bank exposure

Assets: Increasing trend of Bank Assets to Nominal GDP

9.5%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Dec-

14

Mar-

15

Jun

-15

Sep

-15

Dec-

15

Mar-

16

Jun

-16

Sep

-16

Dec-

16

Mar-

17

Jun

-17

Sep

-17

Dec-

17

Mar-

18

Jun

-18

Universal and Commercial Banks: Leverage (Solo Basis)

As of End-Period Indicated, In Percent

5% BSP’s Minimum

Requirement

95.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

100.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Bank Assets (LHS)

Nominal GDP (LHS)

In Billion Pesos

(LHS) In Percent

(RHS)

Bank Assets as a Share of GDP

As of End-Periods Indicated

Institutionalize

financial stability

BSP STRATEGIES IN IMMC RISKS

Strengthen

Financial Risk

Surveillance

Promote

Stakeholder

Engagement

Conduct Evidence

Based Research

7

Identification – Measuring – Monitoring

TRANSPARENCY and COMMUNICATION

Set Policy

Reform Agenda

BSP STRATEGIES IN IMMC RISKS

8

Controlling

ProportionatePromotes

Responsible Fintech Innovation

F INANCIAL

S ECTOR

F ORUM

F INANCIAL

S TABILITY

C OORDINATION

C OUNCIL

Microprudential regulation Systemic Approach

(Macroprudential

regulation)

9

INSTITUTIONALISATION OF FINANCIAL STABILITY MANDATE

Expanded Report on Real Estate Exposures (REE) (Sep 2012)

Uniform Stress Testing Program for Banks (Aug 2014)

Residential Real Estate Price Index (Nov 2015)

Enhanced Reports on REE and Project Finance Exposures (Sep 2017)

Cross-border Exposures Reporting to BIS (Jan 2018)

Collaboration with HLURB to develop reportorial template targeted to real estate companies

Enhanced reportorial requirements on various credit exposures

Enhanced Financial

Surveillance

STRENGTHENING FINANCIAL RISK SURVEILLANCE

10

BANKING SUPERVISION FRAMEWORK

BSP Supervised FIs Market Participants

Legislative Developments

International Best Practices

Database/ Dashboard

Industry Reports/Assessment

Existing Policy

Framework

Supervisory Outputs

Risk Management and Control Functions

IT SupportSystem and

ProcessesCapacity Building

Gen

era

l Pu

blic

Reg

ula

tory

Co

un

terp

art

s

11

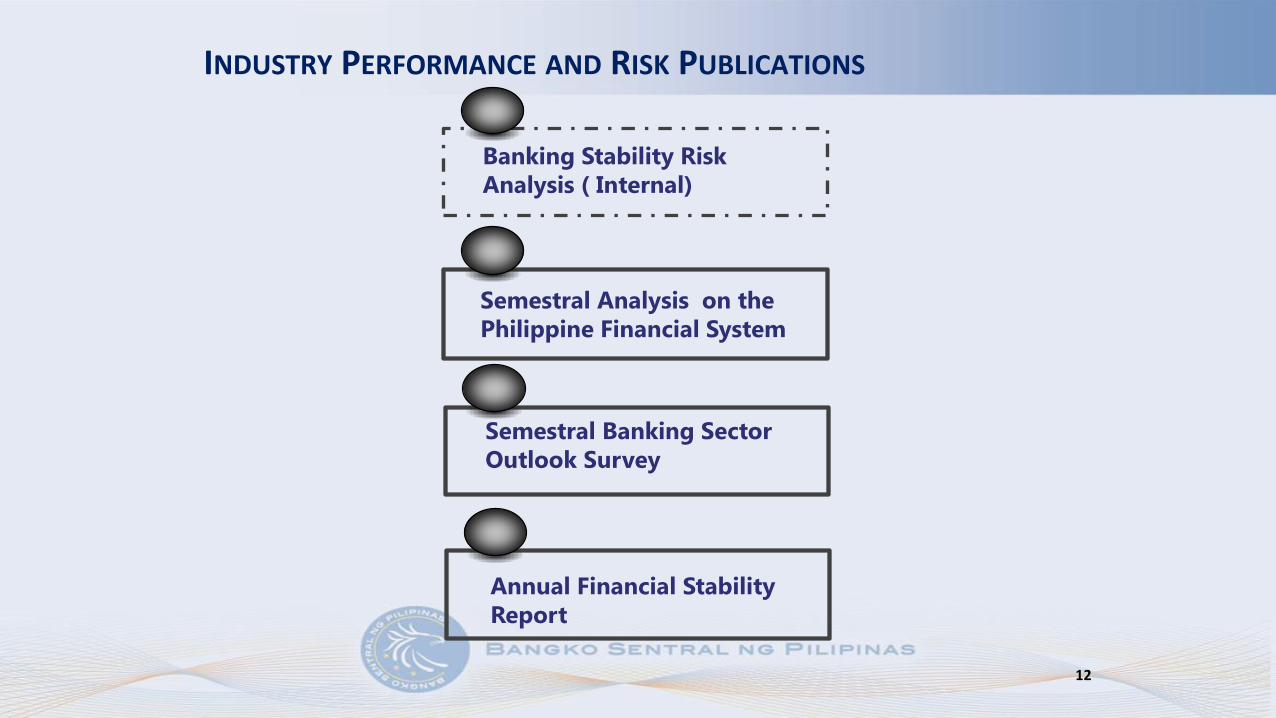

INDUSTRY PERFORMANCE AND RISK PUBLICATIONS

Semestral Analysis on the

Philippine Financial System

Semestral Banking Sector

Outlook Survey

Annual Financial Stability

Report

12

Banking Stability Risk

Analysis ( Internal)

Determinant of Bank Deposit Interest Rates (Campipi, 2018)

• Enhanced access to banking services can lead to higher deposit rates as

banks compete to retain and attract depositors.

• Allowing the establishment of bank branch-lite units results to a positive

impact because it facilitates greater access to banking services in a cost-

effective manner while at the same time benefitting depositors to higher

interest rates.

Expansion in Bank Lending and Loan Qualilty (Cachuela , 2018)

• Philippine banks continue to be risk-sensitive in their lending behavior as the

quality of loans remained relatively stable amid adverse shocks to the

macroeconomic environment.

13

EMPIRICAL STUDIES ON BANKING OPERATIONS

14

EMPIRICAL STUDIES ON BANKING OPERATIONS

Using “excess” capital from regulatory requirement (Layaoen and Domantay-Mailig, 2018)

• Most universal and commercial banks (U/KBs) and their subsidiary thrift banks

(TBs) adjust their regulatory capital ratio through changes in the level of capital

• Adoption of Basel III reforms leads to greater/increased risk sensitivity in U/KBs

Using bank loan commitments for residential real estate loans (Bayangos and De Jesus,

2018)

• Tightening of macroprudential policies, especially resilience-based instruments,

are effective in restricting growth of real bank loan commitment of banks

• Tightening of macroprudential policies, especially cyclical-based instruments, are

effective in preserving the quality of loans

• Forthcoming deeper analysis of residential real estate exposures to complement

BIS-based analysis

NATIONAL REFORM AGENDA

MACROECONOMIC STABILITY

Inflation Targeting

Floating Exchange Rate System

International Reserves

Debt Liability Management

CAPITAL MARKET

RISK MANAGEMENT

Credit and Concentration Risk

Liquidity

Market

Operational:-Technology-Business Continuity

-Cybersecurity

MARKET COMPETITION

Liberalization of Entry of Foreign

Banks REAL TIME GROSS SETTLEMENT SYSTEM

FINANCIAL STABILITY

Financial Surveillance

Macroprudential Measures

Capital Market Reforms

Philippine Payments and Settlements

System

15

CORPORATE GOVERNANCE

Duties and Responsibilities

Governance Landscape

Reputational Risk

Reporting Governance

Stress Testing

Capital

Related Party

National Retail Payment System

Establishment of Domestic Banks

Fitness and Propriety of BOD and SM

Size

PROPORTIONALITY IN BANKING OPERATIONS:

Scale

Risk Exposures

LEVEL OF COMPLEXITY OF BANKS

Systemic Importance

Products &

Services

Operational Complexity

A regulatory framework supervisory approach that is

commensurate to the financial institution’s risk profile and

systemic importance.

Simpler standards and methodologies but without

compromising regulatory objectives.

16

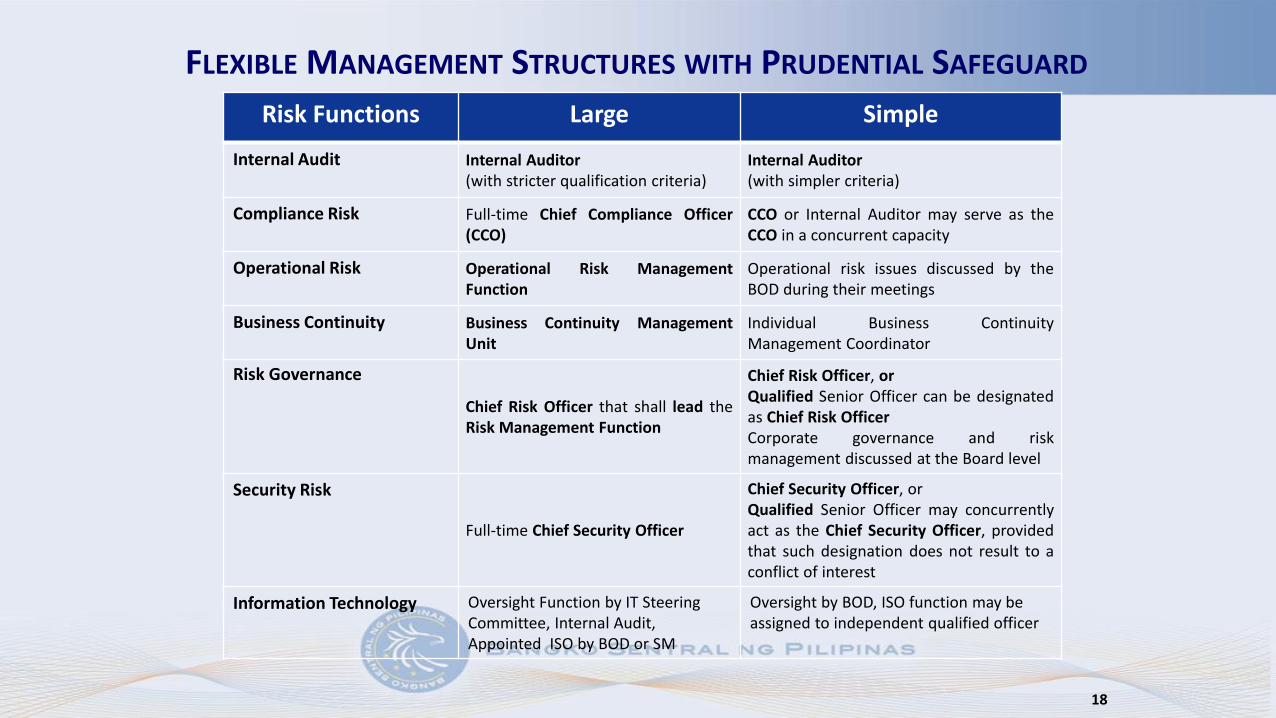

FLEXIBLE MANAGEMENT STRUCTURES WITH PRUDENTIAL SAFEGUARD

17

Governance Standards

Large Simple

BOD Composition At least 1/3 but not less than two (2) members of the Board as Independent Director

At least one Independent Director

Board-level committees

Three (3) board-level committees: Audit, Corporate Governance and Risk Oversight

Audit Committee

FLEXIBLE MANAGEMENT STRUCTURES WITH PRUDENTIAL SAFEGUARD

18

Risk Functions Large Simple

Internal Audit Internal Auditor(with stricter qualification criteria)

Internal Auditor(with simpler criteria)

Compliance Risk Full-time Chief Compliance Officer(CCO)

CCO or Internal Auditor may serve as theCCO in a concurrent capacity

Operational Risk Operational Risk ManagementFunction

Operational risk issues discussed by theBOD during their meetings

Business Continuity Business Continuity ManagementUnit

Individual Business ContinuityManagement Coordinator

Risk Governance

Chief Risk Officer that shall lead theRisk Management Function

Chief Risk Officer, orQualified Senior Officer can be designatedas Chief Risk OfficerCorporate governance and riskmanagement discussed at the Board level

Security Risk

Full-time Chief Security Officer

Chief Security Officer, orQualified Senior Officer may concurrentlyact as the Chief Security Officer, providedthat such designation does not result to aconflict of interest

Information Technology Oversight Function by IT Steering Committee, Internal Audit, Appointed ISO by BOD or SM

Oversight by BOD, ISO function may be assigned to independent qualified officer

APPROPRIATE RISK MANAGEMENT STANDARDS

19

Risk Area Large Simple

Credit RiskSound loan loss methodology that canreasonably estimate expected loan lossprovisions in a timely manner

Subject to simplified but morestringent loan loss provisioningguidelines

Liquidity Risk

Dynamic approaches and a range oftechniques that factor future changes intheir activities and impact of thesechanges on the bank’s balance sheet

Static approach to liquiditymanagement. Static models arebased on positions at a given pointin time. This may consist of a cashflow projection in a spread sheetwhere the bank’s sources and usesof funds is analyzed based oncontractual or maturity

Operational Risk

Utilize more sophisticated tools inidentifying and assessing operational riskexposures. These may include but neednot be limited to the following: risk self assessments, scenario analysis, business process mapping, or model measurement.

In identifying and assessingoperational risk exposures, banksare expected to adopt at aminimum, the (i) results ofinternal/external audit andsupervisory issues raised in theBSP ROE and internal loss datacollection analysis

APPROPRIATE RISK MANAGEMENT STANDARDS

20

Risk Area Large Simple

Stress Testing

Methodologies that could be employedmay be sensitivity analysis, scenarioanalysis and reverse stress test.

Required to report the results of thestress testing that were undertaken tothe BSP on an annual basis as part ofthe Internal Capital AdequacyAssessment Process document.

Use of simple sensitivity analysiscovering credit, liquidity andoperational risks.These banks shall consider, at aminimum, the following in their stresstesting exercises: Twenty percent (20%) and fifty

percent (50%) of the total loanportfolio turning into non-performing loans (NPL) for fullprovision of allowance for creditlosses;

Twenty percent (20%) and fiftypercent (50%) deposit withdrawal;and

Recognition of operational lossesaccounting for five percent (5%) andten percent (10%) of total assets

Results available upon request.

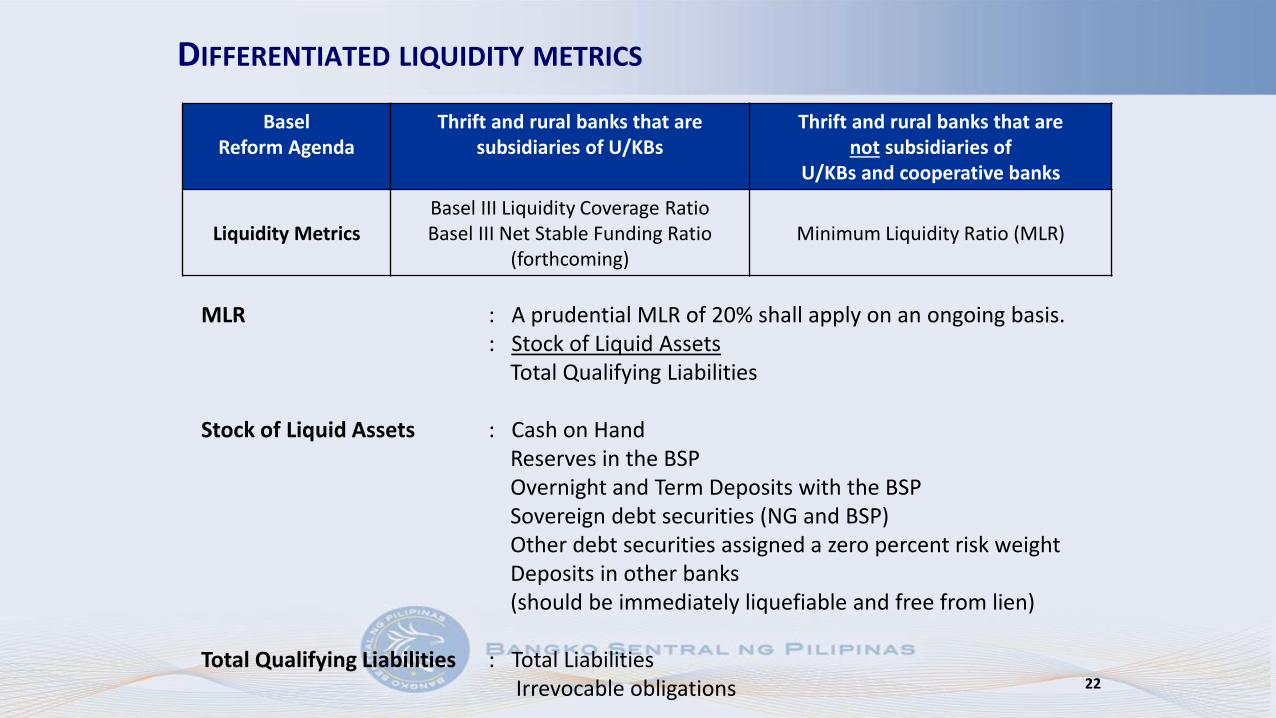

Basel Reform Agenda Thrift, rural and cooperative banks that are subsidiaries of universal and

commercial banks

Stand-alone thrift, rural and cooperative banks

Regulatory Capital Basel III (10% minimum CAR) Basel 1.5 (10% minimum CAR)

Leverage Basel III Not Applied

Minimum Capital Requirements (Pillar 1)

Supervisory Review Process

(Pillar 2)

Market Discipline (Pillar 3)

TOTAL QUALIFYING CAPITAL - Basel-III compliant, except for the adoption ofthe capital conservation buffer and the countercyclical capital buffer.

CREDIT RISK CAPITAL CHARGE - Risk-weighted assets (Basel I guidelines) plus: 50 % risk weight for FCY denominated credit exposure to Philippine

National Government (NG) and BSP in line with credit risk rating of thecountry; and

150 % risk weight for NPLs and foreclosed assets.

MARKET RISK CAPITAL CHARGE – Not applicable

OPERATIONAL RISK CAPITAL CHARGE -- 12% of the average positive annualgross income during the last 3 years of a bank.

CAPITAL PLANNING PROCESS

REQUIRED MINIMUM DISCLOSURES:

Components of qualifying capital Capital requirements for credit,

market and operational risks Total and Tier 1 capital adequacy

ratios.

SEGMENTED BASEL REGULATORY CAPITAL FRAMEWORK

21

Basel Reform Agenda

Thrift and rural banks that are subsidiaries of U/KBs

Thrift and rural banks that are not subsidiaries of

U/KBs and cooperative banks

Liquidity MetricsBasel III Liquidity Coverage RatioBasel III Net Stable Funding Ratio

(forthcoming)Minimum Liquidity Ratio (MLR)

MLR : A prudential MLR of 20% shall apply on an ongoing basis.: Stock of Liquid Assets

Total Qualifying Liabilities

Stock of Liquid Assets : Cash on HandReserves in the BSPOvernight and Term Deposits with the BSPSovereign debt securities (NG and BSP)Other debt securities assigned a zero percent risk weightDeposits in other banks(should be immediately liquefiable and free from lien)

Total Qualifying Liabilities : Total LiabilitiesIrrevocable obligations

DIFFERENTIATED LIQUIDITY METRICS

22

Risk-based and

Proportionate

Regulation

Consumer

Protection

RESPONSIBLE FINTECH INNOVATION

Active

Multi-stakeholder

Collaboration

BSP REGULATORY APPROACH

23

Clearly monitor

developments and

related issues01

02

0304

Allow for market

to develop

Adopt appropriate

regulatory

approach

Understand

operating/

business model

Proceed with

flexibility yet

with caution

THE BSP REGULATORY SANDBOX

05 BSP’s TEST

AND LEARN

APPROACH

24

REGULATORY TECHNOLOGY SOLUTIONS

Application Programming Interface (API) System

25

Risk Management is an evolving process

Communication and stakeholder collaboration is essential to shared risk management

There is a need for a domestic policy reform agenda that places due regard for

proportionality

We should embrace the use of responsible digital innovations

26

KEY TAKEAWAYS

Thank You

27