Embed Size (px)

Citation preview

Risk Management and Risk Premia Investing

November 18, 2015

For Financial professional Use Only. Not for redistribution under any circumstances.

Schroder Investment Management North America Inc. 875 Third Avenue, New York, NY 10022 (212) 641-3800 www.schroders.com/us

Schroder Fund Advisors LLC, Member FINRA, SIPC 875 Third Avenue, New York, NY 10022-6225

(800) 730-2932 www.schroderfunds.com

Presenting to: CFA Society of Columbus, Ohio

Representing Schroders:

Ashley Lester, Ph.D – Head of Multi Asset and Portfolio Solutions Research

** Remove from final presentation **

Contents

Risk Management: An Abrupt Introduction 2

What Did We Learn? 5

Post-Crisis Themes 7

Three ingredients of portfolio formulation 9

Some Conclusions and Some Questions 22

Important Information 23

1

** Remove from final presentation **

Risk Management An Abrupt Introduction

2

Source: Schroders, Barclays Live .Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance

disclosures made throughout and in the Important Information pages of the appendix.

0

20

40

60

80

100

120

01/19/2006 07/19/2006 01/19/2007 07/19/2007 01/19/2008 07/19/2008 01/19/2009

AAA Subprime (ABX) Composite Price

** Remove from final presentation **

Risk Management An Abrupt Introduction

3

Source: Schroders, Barclays Live .Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance

disclosures made throughout and in the Important Information pages of the appendix.

0

20

40

60

80

100

120

01/19/2006 07/19/2006 01/19/2007 07/19/2007 01/19/2008 07/19/2008 01/19/2009

AAA Subprime (ABX) Composite Price

** Remove from final presentation **

Risk Management An Abrupt Introduction

4

Source: Schroders, Barclays Live .Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance

disclosures made throughout and in the Important Information pages of the appendix.

0

20

40

60

80

100

120

01/19/2006 07/19/2006 01/19/2007 07/19/2007 01/19/2008 07/19/2008 01/19/2009

AAA Subprime (ABX) Composite Price

** Remove from final presentation **

What did 2008 change for Risk Managers? VaR is not all encompassing

5

Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance disclosures made throughout and in the

Important Information pages of the appendix. VaR is Value at Risk.

Market Liquidity Risk

Credit Macroeconomic Liquidity

Extended Time Horizon

Need a model, not statistics

Can be quantitative or qualitative

Both have strengths and weaknesses

** Remove from final presentation **

What has changed since 2008 for investors? The Rise of Different Styles of Investing

6

Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance disclosures made throughout and in the

Important Information pages of the appendix.

Newer Investment

Styles

Risk Premium

Risk Parity/Risk Allocation

Smart Beta

Factor-Based

** Remove from final presentation **

Post-Crisis Themes Two noticeable changes

7

Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance disclosures made throughout and in the

Important Information pages of the appendix.

Seek better risk/return tradeoff

- Volatility control, risk-based allocation

Result: New thinking brought risk models

Risk managers were more worried about risk models

Short-term models did not reflect crisis conditions

Lesson:

Need models and ideas focused on the long run

1

2

** Remove from final presentation **

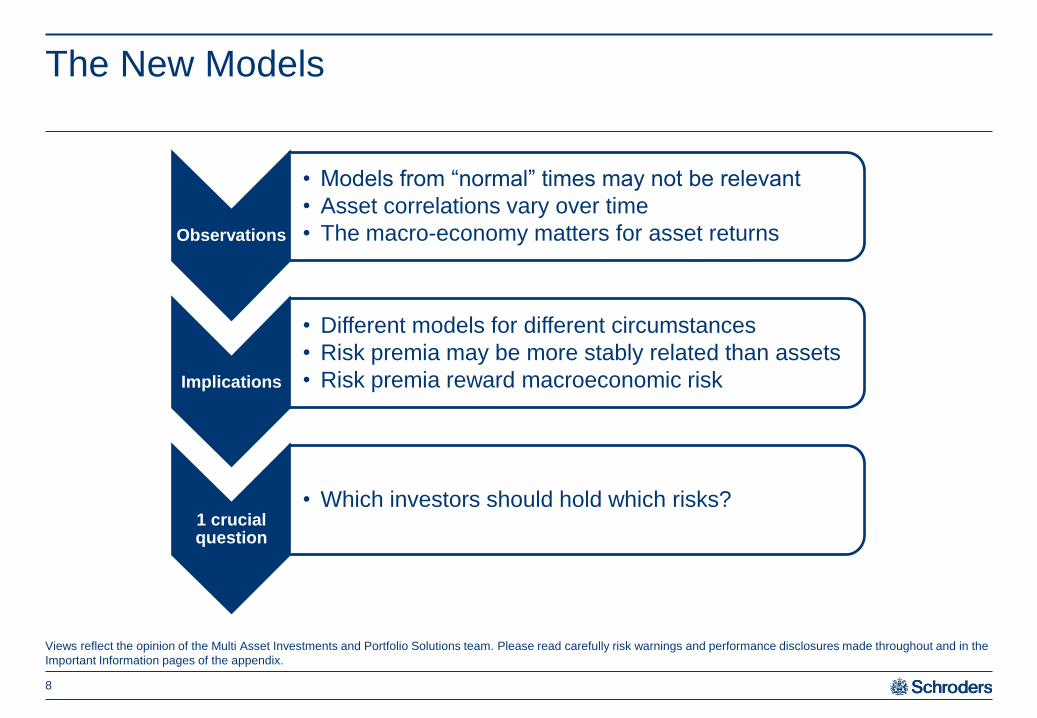

The New Models

8

Views reflect the opinion of the Multi Asset Investments and Portfolio Solutions team. Please read carefully risk warnings and performance disclosures made throughout and in the

Important Information pages of the appendix.

Observations

• Models from “normal” times may not be relevant

• Asset correlations vary over time

• The macro-economy matters for asset returns

Implications

• Different models for different circumstances

• Risk premia may be more stably related than assets

• Risk premia reward macroeconomic risk

1 crucial question

• Which investors should hold which risks?

** Remove from final presentation **

Three ingredients of portfolio formulation

9

Risk Premia Macroeconomic

Risk Investor

Differences

** Remove from final presentation **

Risk Premia

10

** Remove from final presentation **

From asset classes to risk premia Understanding real drivers of risk and return

Risk premium

Expected return for assuming a source of risk

Risk premia

Building blocks of asset classes

Asset classes

Comprised of one or more risk premia

Source: Schroders, BAML. US Investment Grade Credit is represented by BAML US Corporate Master Index, Term Premium is calculated using BAML US 7-10 year Treasury

Index. Shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell

0

1

2

3

Credit Risk Premium

Duration Risk Premium

Risk-Free Rate

Breaking an asset class down into risk premia

Example: US investment grade credit

(Yield %)

11

** Remove from final presentation **

Credit risk premium – Valuation Credit Spread Components – finding the sub premia

Source: Schroders, Markit, BAML, Barclays Capital, September 2013. Spread decomposition based on Bond and CDS spreads and Liquidity Cost Scores (LCS). LCS are a bond

level liquidity measure provided by Barclay's which represent the transaction cost to execute an instantaneous round-trip institutional trade. LCS are calculated as bid-ask spreads

multiplied spread durations for spread quoted bonds, and (Ask-Bid)/Bid for price quoted bonds. *Model history back to Dec 2007 for US IG and July 2010 for Euro IG

= + + Market

Premium

Illiquidity

Premium Default

Premium

Bond Credit

Spread

Spread (bps)

-20

80

180

280

380

480

580

680

Market Premia Default Liqudiity US IG OAS

12

** Remove from final presentation **

Credit asset class traditionally used defensively

Corporate bond returns driven by changes in the

credit premium and the underlying duration premium

The credit risk premium group focus on credit risk –

not duration risk

Credit risk premium is primarily driven by growth risk,

not duration risk

Rolling 3 year correlations

Credit risk premium Credit is a growth risk premium

Source: Schroders, Datastream, as of 21 February 2014

Growth Slowdown Inflation Alternative

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US 7 year treasuries and ML US Corporate Masters Index

US 7 year treauries and ML US Corporate Masters Index(Duration Hedged)

S&P 500 and ML US Corporate Masters Index (Duration Hedged)

13

** Remove from final presentation **

Systematic sources of returns driven by investors’ behavioral biases

Alternative risk premia (“ARP”)

Alternative Risk Premia: Research Driven & Market Neutral

Source: Schroders, for illustrative only.

Portfolio

Return

Alpha

Beta Traditional

Risk Premia

Alpha

Alternative

Risk Premia

Value

Carry

Size

Momentum

14

** Remove from final presentation **

Macroeconomics

15

** Remove from final presentation **

Asset Correlations Change Macroeconomic shocks drive asset returns and correlations

16

Surprise increase in … Equities Bonds Correlation

Economic growth + - -

Interest rates - - +

Inflation - - +

Correlations are key to understanding diversification

The return drivers in each asset are key to understanding correlations

Source: Schroders.

** Remove from final presentation **

What Do the Data Tell Us? Evidence of the drivers of returns

17

Source: Schroders. See Data slide in the appendix, and the slides on the regressions in the appendix.

** Remove from final presentation **

Growth, Inflation and Slowdown risk premia The “Big” risk premia driven by sensitivities to macro-economic factors

Source: Schroders

• Developed market equities

• Emerging market equities / Spreads

• IG Credit Spreads

• High Yield Spreads

Captures risk premia for

bearing risk of:

• Business cycle risk

• Unexpected economic weakness

• Purchasing power erosion

• Complements duration risk exposure

• Tends to outperform in rising interest

rate environments and linked to periods

of heightened inflation concerns

• Agricultural commodities

• Industrial metals

• Gold

• TIPS (duration-hedged)

• Energy

Growth

Inflation

Examples of assets with significant

exposure to this risk:

18

• Changes in interest rates

• Complements growth risk exposure

• Outperforms in falling interest rate

environments, often linked to periods of

economic weakness

• Developed market sovereign bonds Slowdown

** Remove from final presentation **

A regime-based analysis Assessing the growth/inflation sensitivities

Source: Schroders. Data is simulated and not actual performance. Past performance is no guarantee of future results. Actual results would vary. For full details regarding the

simulation and definitions, please see the information at the end of this presentation.

19

0%

5%

10%

15%

20%

25%

S&P 500 Trend Carry Value Size

High Growth Medium Growth Low Growth

0%

2%

4%

6%

8%

10%

12%

14%

S&P 500 Trend Carry Value Size

High Inflation Medium Inflation Low Inflation

Conditional returns in different “Growth” regimes Conditional returns in different “Inflation” regimes

Growth Intuition

Momentum 0 Indifferent to all. Only sensitive to past and

current prices

Carry + Like insurance. Best after a crisis and over a long

period of time with no crisis/small crises.

Value 0 Best at the end of a long departure from

fundamentals and a recognition of that.

Size + Larger relative impact on small cap as their

sources of financing become less constrained

Intuition

Inflation Intuition

Momentum 0 Indifferent to all. Only sensitive to past and

current prices

Carry + Different monetary policies lead to larger

interest rate differentials

Value - Poor market sentiment caused by high inflation

can result in investors ignoring fundamentals

Size +

Domestic corporates are less susceptible to

margin deterioration caused by rising import

costs

Liquid Alternatives Portfolio Simulated Returns - Empirical Evidence (Feb 1982 – Dec 2014)

** Remove from final presentation **

Investor Differences

20

** Remove from final presentation **

Investors: Beyond the Market Portfolio

Which risks are YOU best suited to be paid for?

21

Source; Schroders.

• Are liabilities tied closely to inflation?

1

• Are liabilities greater or smaller if there is strong growth?

2

• How important is volatility vs drawdown or worst case scenarios?

3

Conclusion?

Different answers suggest different

portfolios for each investor

** Remove from final presentation **

Some Conclusions and Some Questions

Modern investing and risk management provide the promise of:

– Better diversified portfolios

– Richer sets of return drivers, including alternative risk premia

– Greater understanding of the RIGHT kind of risk

Questions remain:

– Are alternative risk premia also rewards for economic risk?

> Are value, momentum and quality rewards for risk? Or are they a free lunch?

– What is the implication for their continued existence?

– Have we captured the right economic risks?

– How can we help investors systematically identify the right risks to take?

22

Source: Schroders.

Feb 2015 ** Remove from final presentation **

Important information

23

Schroder Fund Advisors LLC, Member FINRA, SIPC

875 Third Avenue, New York, NY 10022-6225

(800) 730-2932

www.schroderfunds.com

The value of investments can fall as well as rise as a result of market movements. Investments in smaller companies may be less liquid than in larger companies and price

swings may therefore be greater than in larger company funds. Exchange rate changes may cause the value of overseas investments to rise or fall. Less developed markets are

generally less well regulated than the US, they may be less liquid and may have less reliable custody arrangements. Investors should be aware that investments in emerging

markets involve a high degree of risk and should be seen as long term in nature. The Strategy will invest in some higher-yielding bonds (non-investment grade). The risk of

default is higher with non-investment grade bonds than with investment grade bonds. Higher yielding bonds may also have an increased potential to erode your capital sum than

lower yielding bonds. The Strategy will invest in Property Funds and Property Investment Companies. It may be difficult to deal in these investments because the underlying

properties may not be readily saleable which may affect liquidity. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing

directly in the underlying assets. The use of derivatives and leverage involves a higher degree of risk and may lead to a higher volatility in the unit prices of the funds. No

investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Past performance is no guarantee of future results. Performance shown is gross of fees. The value of an investment can go down as well as up and is not guaranteed.

Third party data are owned by the applicable third party identified above and is provided for your internal use only. Such data may not be reproduced or re-disseminated and

may not be used to create any financial instruments or products or any indices. Such data are provided without any warranties of any kind. Neither the third party data owner nor

any other party involved in the publication of this document can be held liable for any error.

Schroder Investment Management North America Inc. (“SIMNA Inc.”) is an investment advisor registered with the U.S. SEC. It provides asset management products and

services to clients in the U.S. and Canada including Schroder Capital Funds (Delaware), Schroder Series Trust and Schroder Global Series Trust, investment companies

registered with the SEC (the “Schroder Funds”). Shares of the Schroder Funds are distributed by Schroder Fund Advisors LLC, a member of the FINRA. SIMNA Inc. and

Schroder Fund Advisors LLC are indirect, wholly-owned subsidiaries of Schroders plc, a UK public company with shares listed on the London Stock Exchange.

Further information about Schroders can be found at www.schroders.com/us.

Schroder Investment Management North America Inc. is an indirect wholly owned subsidiary of Schroders plc and is a SEC registered investment adviser and registered in

Canada in the capacity of Portfolio Manager with the Securities Commission in Alberta, British Columbia, Manitoba, Nova Scotia, Ontario, Quebec, and Saskatchewan providing

asset management products and services to clients in Canada. This document does not purport to provide investment advice and the information contained in this newsletter is

for informational purposes and not to engage in a trading activities. It does not purport to describe the business or affairs of any issuer and is not being provided for delivery to or

review by any prospective purchaser so as to assist the prospective purchaser to make an investment decision in respect of securities being sold in a distribution.

This presentation intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer

or solicitation for the purchase of sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or

investment recommendations.

Further information on FINRA can be found at www.finra.org

Further information on SIPC can be found at www.sipc.org

Schroder Investment Management North America Inc.

875 Third Avenue, New York, NY 10022-6225

(212) 641-3800

www.schroders.com/us