Embed Size (px)

Citation preview

Risk Management

1Hurricane Katrina: Landfall August 29, 2005

Fair Bet

• Cost Equals Expected Gain

• Cost = P * (Amount you Win)

• Example: Flipping a Coin– Cost = $10– P = .5– Amount You Win = $20

2

Is This A Fair Bet?

• Flipping A Coin– Cost = $50– Amount You Win = $75

3

Risk Taking Behavior

• Risk-Averse

• Risk-Neutral

• Risk-Taker (Risk-Seeker, Risk-Lover)

4

Risk and Uncertainty

• Risk: A situation in which several different outcomes are possible.

• Uncertainty: The perception that several different outcomes are possible.

5

Categorizing Risk

• Pure Risk v. Speculative Risk• Diversifiable Risk v. Nondiversifiable Risk• Fundamental Risks and Particular Risks

6

Pure Risks v. Speculative Risks

• Speculative Risks are Usually Chosen– Stock Appreciation– Manufacturing and Selling a Product– Example: Furby

• Pure Risks are Usually a Byproduct– Automobile Accident– Sports Injury

7

Diversification

• Pooling Similar Risks– INSURANCE

• Pooling Offsetting Risks– A DIVERSIFIED PORTFOLIO

8

Why Reduce Uncertainty

• Individual

• Corporations

• Government

9

Why Manage Risk? Individuals

• Reduce anxiety

• Planning

10

11

Corporation

ownersemployees

suppliers

customers

government

creditors

Why Manage Risks: Corporation

(Nexus of Contracts)

Early Historical Examplesof Risk Management

• Chinese Trading Boats

• Amish Rebuilding

12

Modern Risk Management

• Prior to 1950s: Insurance Purchaser

• Risk Managers– Finance Dept., Freestanding, or

Human Resource Dept.

– Larger Companies

– Companies Facing Greater Risk

13

Risk Manager: Minimize Adverse Consequences of Risk

• Avoidance

• Loss Control

• Self-Insurance

• Purchase Insurance

• Anticipate Risk

14

15

The Decision toManufacture a Product

Product Development: Motorcycle

• Investment: $1,000,000• Profits if there is no Loss:

$150,000• Possible Liability Losses:

– 1% Chance of $2,000,000 Loss

• Required Return on Investment: 10%

16

17

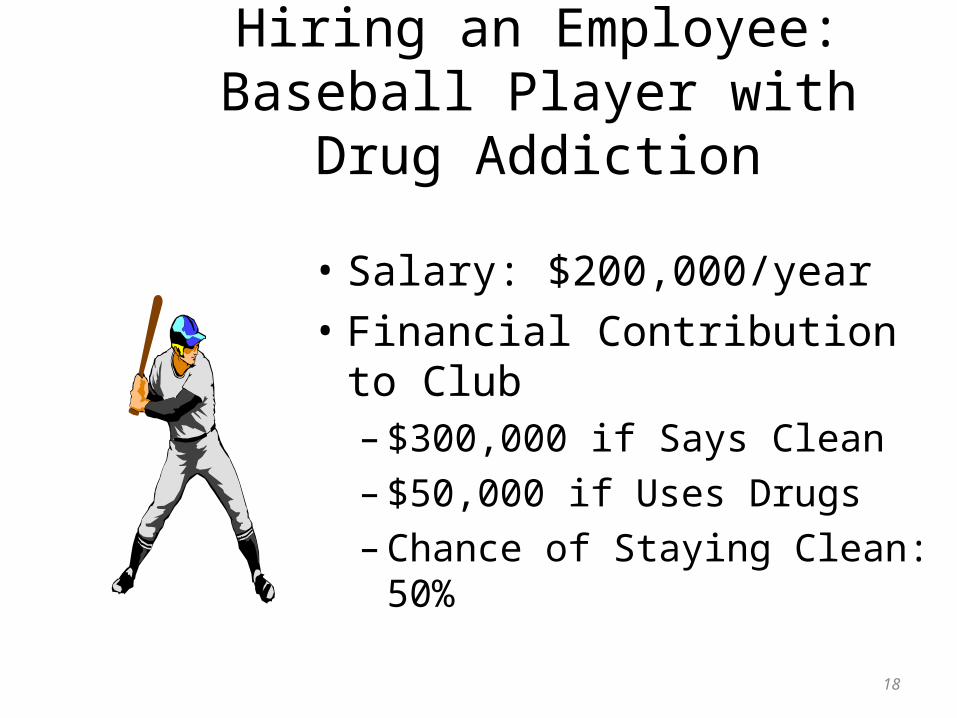

Hiring an Employee

Hiring an Employee: Baseball Player with Drug Addiction

• Salary: $200,000/year• Financial Contribution to Club

– $300,000 if Says Clean

– $50,000 if Uses Drugs

– Chance of Staying Clean: 50%

18

Major Duties of Risk Managers

• Buy Insurance• Identify Risk• Loss Prevention and Loss Control• Contract Review• Safety Training and Education• Govt. Compliance with Safety Issues• Risk Finance• Claims Mgmt. and Litigation Support• Employee Benefits 19

Risk Management Process

• Mission Identification

• Risk Identification

• Risk Analysis

• Consider Alternatives– Risk Control

– Risk Finance

• Implement and Monitor20

Mission Identification

• Goal of Organization

• Goal of Risk Management Department

21

Organization Goals

• Corporation: Maximize Profits

• Non-Profit Organizations

– Religious Organization

– Hospitals

22

Organization Goals

• Charities– Red Cross: The

American Red Cross, a humanitarian organization led by volunteers, . . . will provide relief to victims of disasters and help people prevent, prepare for, and respond to emergencies.

23

Post-Loss Objectives

• Survival of the Organization

• Continuity of Operations

• Earnings Stability

• Continued Growth

• Social Responsibility

24

Pre-Loss Objectives

• Economy• Reduction in Anxiety

– Owners– Suppliers– Lenders– Customers– Govt. Agencies

• Meeting Externally Imposed Obligations• Social Responsibility

25

Risk Management ProcessStep 2

Risk Identification and Analysis

26

Risk Identification: Key Terms

• Hazard

• Risk Factor

• Peril

• Exposure

27

Difficulties withRisk Identification

• New Laws– Examples: Building Codes, Clean Air Act

• New Discoveries– Examples: Black Lung, Second Hand Smoke

• Changing Societal Attitudes– Example: Product Liability Laws, Cigarettes

28

29

New Laws andRisk Identification

Sources of Risk

• Physical Environment

• Social Environment

• Political Environment

• Legal Environment

• Operational Environment

• Economic Environment

• Cognitive Environment30

Social Environmentand Disney Co.

• Euro-Disney

• “Powder”

• Domestic Partner Benefits

• History Theme Park at Manassas

31

Example

• Workplace Injury

32

Categories of Exposures

• Property Exposures– Direct: Immediate Result– Indirect: Secondary Results– Example: Robbery of a Store

• Liability Exposures

• Human Resource Exposures

33

Risk Identification Methods 1

• Insurance Survey

• Risk Analysis Questionnaires

• Financial Statement Analysis

• Flow Chart Method

• Systems Safety Techniques

34

Risk Identification Methods 2

• Interactions with External Resources

• Interactions with other Departments

• Past Losses

• On-Site Inspections

35

Accident Causation

• Human Relations View

• Engineering View

36

Loss Analysis Ratios

• Severity = $Losses / # Losses

• Frequency = # Losses / # Exposures

• Expected Loss = $ Losses/ # Exposures

37

Ratios Example

• Data– 1000 Restaurants– 50 Fires

• Type 1 Fires: 20, $25,000• Type 2 Fires: 30, $50,000

• Severity = [20($25,000) + 30($50,000)]/50 = $40,000• Frequency = 50 / 1000 = .05• Expected Loss = .05($40,000) = $2000

38

Concerns withMeasuring Severity

• Indirect Losses– Ex: Store robbery

• Contagion– Ex: Foot-and-Mouth Disease

• Snowball Effect– Ex: Mad Cow Disease

39

Contagion Example: Bil Mar

40

Contagion Example: Listeria

• Chicago-based Sara Lee recalled hot dogs and deli meats produced at its Bil Mar plant in Zeeland, Michigan, after the CDC found listeria contamination in unopened packages of the products.

• Affected brand names include Ball Park, Bil Mar, Sara Lee Deli Meat and Sara Lee Home Roast.

• The states reporting listeria infections are Arizona, Connecticut, Georgia, Indiana, Iowa, Kentucky, Maryland, Massachusetts, Michigan, Minnesota, New York, Ohio, Oregon, Pennsylvania, Tennessee, Vermont and West Virginia.

41

Contagion Example: Listeria

• Tainted meat – Killed 12 people– Sickened 79 others in 16 states

• 241 workers fired or layed off

42

Loss Severity Measures

• Maximum Possible Loss

• Maximum Probable Loss

43

Example

44

Year Flights Crashes Losses

2003 2004 2005 2006 2007

5,000 5,000 5,000 5,000 5,000

10 0 4 2 0

$2,000,000 0

$1,000,000 $500,000

0

Loss Statistics

45

Mean = Oi pii

n

1freq mean = .2(.002)+.2(0)+.2(.0008)+.2(.0004)+.2(0)

= .00064

sev mean = 1016

200 000 616

250 000( , ) ( , )

= $218,750

E(L) = $140

Loss Statistics

46

S.D. =pi O i E V ii

n( )

2

1

Sev S.D. = ( )( , , )

( )( , , )

1016

200 000 218 750 2

616

250 000 218 750 2

= $26,791

Normal Distn Severity

47

Distance Prob

1 S.D. 68.2%

2 S.D. 95%

$218,750

$191,959 $245,541

$165,168 $272,332

freq = .00064 sev = $272,332 E(L)95% = $174.29

Calculating the Mean and Std. Dev.

Number of Fires Probability

0 .1010 .2030 .4050 .2060 .10

48

mean = .10(0)+.20(10)+.40(30)+.20(50)+.10(60) = 30

S.D. = sq. root [.10(0-30)(0-30) +.20(10-30)(10-30) +.40(30-30)(30-30) +.20(50-30)(50-30) +.10(60-30)(60-30)] = 18.43

Important Distributions

• Loss Frequency Distribution

• Loss Severity Distribution

• Total Loss Distribution

49

Loss Frequency Distn

Taxi Accidents N = 2000

50

Ot Pt

0/2000 .1010/2000 .2030/2000 .4050/2000 .2060/2000 .10 015.

)10(.03.)20(.025.)40(.015.)20(.005.)10(.0

1.)(

n

tAvgFreqtOtptOE

.015(2000) = 30 Accidents

51

Loss Severity Distn

N = 100

Sevt Pi

$1,000 .80$2,000 .05

$10,000 .10$50,000 .05

400,4$

)05(.000,50$)10(.000,10$)05(.000,2$)80(.000,1$

1))(()(

n

i tpiSeviSevE

Drawbacks to Useof Historical Data

• CHANGE in Process

• Insufficient Data

52

Importance of Timingof Losses

• Time Value of Money

• Cash Flow Considerations

53

Loss Triangles

• Predict When Losses Will Occur

• Predict Total Losses

• Highlight Trends

54

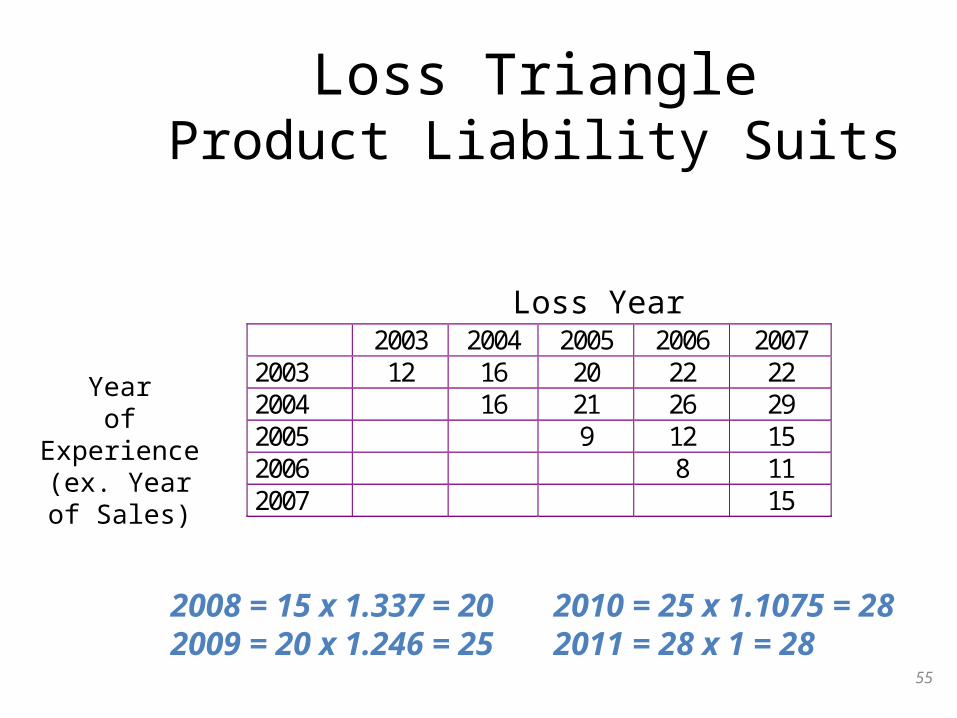

Loss TriangleProduct Liability Suits

2003 2004 2005 2006 2007 2003 12 16 20 22 22 2004 16 21 26 29 2005 9 12 15 2006 8 11 2007 15

55

Loss Year

Yearof

Experience(ex. Year of

Sales)

2008 = 15 x 1.337 = 20 2010 = 25 x 1.1075 = 282009 = 20 x 1.246 = 25 2011 = 28 x 1 = 28

Development Factors

y + 1 y + 2 y + 3 y + 4 2003 1.33 1.25 1.10 1.00 2004 1.3125 1.238 1.115 2005 1.33 1.25 2006 1.375 MEAN 1.337 1.246 1.1075 1.000

56

Development Period

Yearof

Experience

Examples2003, y+1 = 16/12 = 1.332003, y+2 = 20/16 = 1.25

Loss Development: 2007 Sales Year

2007: 15 Losses

2008: 15 x 1.337 = 202009: 20 x 1.246 = 252010: 25 x 1.107 = 282011: 28 x 1.000 = 28

57

Present Value CalculationDetermining Losses from 2003 Sales

Claim Made in Year

i%

Cost/Claim

PV in 2003

# Losses

Total Losses

2003 6% $10,000 $10,000 12 $120,000 2004 6% $12,000 $11,321 4 $45,284 2005 6% $14,000 $12,460 4 $49,840 2006 6% $15,000 $12,594 2 $25,188 2007 6% $18,000 $14,258 0 0 2008 6% $20,000 2009 6% $24,000 Losses 2003 Sales

$240,312

58

Homework Problems

• A) Determine the Number of Fully Developed Losses for 2004, 2005, and 2006.

• B) What is the PV of Losses Arising from 2005 Sales as of 2005?

59

Shapes of Different Distributions

• Medical Expenditures

• Church Fires

• Parking Tickets

60

Normal Distribution

• Bell Shaped

• Two Parameters

• Easy to Use

61

Property Losses

• Property Exposed to Loss

• Peril

• Financial Consequences

62

63

Property Exposed to Loss

Real Property

Personal Property

Non-owned Property

Non-owned Property

• Bailed Property

• Leased Property

• Property on Consignment

• Employee’s Property

• Property under Lien

• Agency Relationships

• Contingent Property64

Perils

• Commonly Insured

• Government Insured

• Uninsurable

65

Commonly Insured Perils 1

• Fire

• Lightning

• Windstorm

• Hail

• Explosion

• Smoke

66

Commonly Insured Perils 2

• Aircraft & Vehicle Damage• Riot• Vandalism (Malicious Mischief)• Falling Objects• Weight of Snow, Ice, or Sleet• Water Damage• Glass Breakage• Sprinkler Leakage• Perils of Transportation• Crime Perils

67

Difficult to Insure Perils

• Earth Movement

• Floods

• Nuclear Reaction

68

Why Are Some Perils Uninsurable?

• Against Public Policy

• Under the Control of the Insured– Ex. Suicide

• Probability of Loss is Too High

• Simultaneous Destruction

69

Generally Uninsurable Perils

• War, Terrorism, Rebellion, and Insurrection

• Intentional Losses

• Fading, Rust, Dry Rot, Settling

• Production, Marketing, and Political Risks

70

Financial Consequences

• Reduction in Value• Debris Removal• Business Interruption• Contingent Business Interruption• Loss of Rental Income• Loss of Rental Value• Loss of Leasehold Interest• Inability to Reconstruct Records• Loss of Use Value in Improvements and Betterments• Demolition Costs and Increased Cost of Reconstruction

71

Valuation of a Loss

• Market Value• Replacement Cost• Actual Cash Value

– (Replacement Cost - Depreciation)• Present Value of the Asset’s Contribution

72

Actual Cash ValueCalculation: Building

• Purchase– Date: January 1, 1987– Price: $1,000,000– Expected Lifetime: 40 years

• Fire– Date: January 1, 2007– Replacement Cost: $2,000,000

73

Actual Cash ValueCalculation: Building

• ACV = Replacement Cost - Depreciation

–As of the Time of Loss

• ACV = $1,000,000 = $2,000,000 - $1,000,000

74

Present Value of the Asset’s Contribution

75

Liability Loss

• Expenditure of TIMEand MONEY

• Investigate, Negotiate, Defense, Payment

76

Property Losses v. Liability Losses

• Parties Involved

• Measurement of Exposure

• Changing Environment

• Tail77

Types of Legal Liability

• Criminal– Agent– Punishments– Insurance

• Civil– Private Duties– Common Law, Statutes, Contracts

78

TORT

• Wrongful Act or Omission

• Independent of Contract

• Legal Remedy: DAMAGES ($$$)

79

Types of TORTS

• Intentional Torts

• Negligence

• Strict Liability

80

Intentional TORTS

• Legally Protected Right

• Intentional Interference– Voluntary– Damages Reasonably Foreseen– No Valid Defense

81

Intentional Torts: Defamation

• Types– Libel– Slander

• Plaintiff Must Show– False, Injurious Statement– Publication– Damages

82

Defenses

• Truth

• Privilege– Absolute– Qualified

• No Malice• Not Known False• No Intent to Injure• Fair, if by news media• Covered Body

83

Intentional Torts:Invasion of the Right of Privacy

• Examples– Release Confidential Information– Hidden Microphones

• Public Figures v. Private Figures

84

Intentional Torts:Assault and Battery

• Assault• Battery• Defenses

– Consent– Self-Defense– Defense of Property– Defense of Others– Allowed Discipline

85

The “Preppy Killer”: Consent??

'Preppie killer' headed back to prison on drug rap

NEW YORK (AP) -- New York's so-called "preppie killer" is headed back to prison.

Robert Chambers already served 15 years behind bars for strangling a woman in Central Park during what he said was rough sex.

He pleaded guilty Monday to selling drugs. The Manhattan district attorney's office says Chambers is promised 19 years and four months in prison when he is sentenced on September 2.

Chambers and his girlfriend were charged with dealing cocaine out of their Manhattan apartment in 2007.

Chambers pleaded guilty in 1988 to manslaughter in the death of 18-year-old Jennifer Levin two years earlier.

Stories portrayed him as a handsome, privileged, prep school youth gone bad.He was released from prison in 2003.

86

Intentional Torts:Assorted Others

• False Arrest and Wrongful Detention

• Malicious Prosecution• Trespass• Conversion• Nuisance

87

Intentional Torts: Assorted Others Continued

• Wrongful Interference with a Business Relationship– Copyright Infringement– Deception

• Bad Faith– Delaying Payment of Claims– Refusing to Pay Claims

88

Negligence

• Acts of Omission

• Acts of Commission

89

90

Elements of a Negligent Act

• Legal Duty

• Breach

• Damages

• Proximate Cause

Damages

• Compensatory Damages– Special Damages– General Damages

• Punitive Damages

91

Defenses to Negligence

• Contributory Negligence

• Comparative Negligence

• Assumption of Risk

• Statute of Limitations

• Immunities– Sovereign– Charitable Institutions– Public Officials

92

Strict Liability Torts

• Abnormally Dangerous Instrumentalities

• Ultrahazardous Activities• Dangerously Defective Products• Workers Compensation Statutes• Disability Benefit Statutes• Aviation Law• Dram Shop Laws• Contractual Assumptions

93

Goals of the Tort System

• Compensate

• Deter

94

Tort Reform Proposals

• Modify Joint and Several Liability

• Caps on Non-Economic Damages

• Caps on Punitive Damages

95

The Work Relationship

• Employer– Sets Hours– Defines and Supervises Work

• Employee– Sacrifices Time for Income– Is Told How to Work– Method of Payment Not Important to

Status• Independent Contractor

– Not an Employee– Controls Methods of Work

96

97

Workplace Injuries

• Common Law: Negligence

• Statutory Law: Workers Compensation

98

Rank Occupation Death rate/100,000 Total deaths

1 Logging workers 92.4 85

2 Aircraft pilots 92.4 109

3 Fishers and fishing workers 86.4 38

4 Structural iron and steel workers 47.0 31

5 Refuse and recyclable material collectors 43.2 35

6 Farmers and ranchers 37.5 307

7 Roofers 34.9 94

8 Electrical power line installers/repairers 30.0 36

9 Driver/sales workers and truck drivers 27.6 905

10 Taxi drivers and chauffeurs 24.2 67

America’s Most Dangerous Jobs in 2004

Some Exceptions toWorkers Compensation

• Small Firms

• Farm Workers

• Domestic Workers

99

Employers’ CommonLaw Duties

• Safe Place to Work

• Adequate Number of Competent Fellow Employees

• Provide Safe Tools and Equipment

• Warn of Inherent Dangers

• Make and Enforce Safety Rules100

Workers Compensation

• Accident

• Arising Out of and In the Course of Employment

• Only Bodily Injury

101

Workers Compensation Benefits

• Lost Wages

• Medical Care

• Body Part Payments

• Death Benefits102

Exceptions to WC as Sole Remedy for Workplace Injury

• Assault by the Employer• Retaliatory Discharge of the Employee• Dual Capacity Doctrine• Suits by 3rd Parties

– Ex. Loss of Consortium– Ex. Consequential Injuries

• Property Damage

103

Human Resource Exposures

• Loss of Personnel

• Cost of Employee Benefits

104

Employee Benefits

• Attract Workers

• Retain Workers

• Retire Workers

• Encourage Productivity105

Loss of Personnel

• Premature Death

• Disability/Poor Health

• Resign

106

Premature DeathLosses that Result

• Loss of Human Life Value

• End of Life Expenses

• Emotional Grief of Survivors

107

Premature DeathRisk Management Strategies

• Loss Prevention:– Medical Care– Good Health

• Life Insurance: Many are Underinsured

• Pension Plan

• Earnings of Surviving Spouse

108

Estimating Human Life ValueExample: Worker 3 years from Retirement

109

Year 2004 2005 2006 TOTAL

Output

50000 49000 48000

Pay

40000 38000 36000

Surplus

10000 11000 12000

PV(8%)

10000 10185 10288

30473

110

Calculating Loss ofHuman Life Value

Age 62 63 64 Total

Earnings

$40,000 $40,000 $40,000

Taxes

$16,000 $16,000 $16,000

Self

$10,000 $10,000 $10,000

Family

$14,000 $14,000 $14,000

PV(8%)

$14,000 $12,963 $12,003

$38,966

Worker dies at age 61 after being paid.At the time of death 3 working years remained.

Disability Problem

• Disability is comparatively frequent• Disability can be extremely costly• Most lost income due to disability is not

replaced• Disability insurance is confusing

– Multiple definitions of disability

• Disability insurance is subject to moral hazard– Malingering

111

Risk of a 90+ Day Disability v. DeathDuring Working Years

112

Age 22 62

P(Disability)/P(Death)

7.5 2

Risk Control

• Avoidance

• Prevention

• Reduction

• Information Management

• Some Risk Transfers

113

Risk Avoidance

• Proactive Avoidance

• Abandonment

114

Drawbacks to Avoidance

• Lost Benefits of Risk

• Perhaps not Possible$Government Imposed Risks$Nature of the Risk

• May Result in Worse Risks

115

116

Important Formsof Loss Reduction

Salvage Subrogation Litigation Management Catastrophe (or Contingency)

Plans Duplication Separation

Information Managementas Loss Control

• Customers: Enhanced Sales

• Creditors: Lower Debt Cost

• Suppliers: Better Relationships

• Owners: Greater Market Value

117

Risk Transfer

• Property or Activity Transferred

• Contractually Pass the Liability“Exculpatory Contracts”

118

Government andRisk Control

• Public Interest

• Efficiency

119

Risk Financing:General Methods

• Retention

• Transfer

120

Risk Financing: Timing

• Contemporaneous

• Prospective

• Retrospective

121

122

Approaches to Retention

Passive or Unplanned

Active or Planned

Retention: Funding Arrangements

• No Advance Funding

• Liability or Earmarked Accounts

• Earmarked Asset Accounts

• Captive Insurer123

Types of Transfers

• Insurance

• Noninsurance Transfers

• Hedging

124

Elements of Insurance

• Contract

• Premium

• Conditional Benefits

• Pooling of Resources

125

Insurance Transaction

• Buyer Side of the Market– Risk Managers– Brokers – Consultants

• Supplier Side of the Market– Insurance Company

• Underwriters, Claims Adjusters, Agent, Actuaries

– Agent

126

Noninsurance Transfers

• Do Not Satisfy Conditions to be Insurance

• Provide External Funding

127

Hedging

• Taking an Offsetting Risk

• Not Possible for Many Types of Risks

128

129

130

131

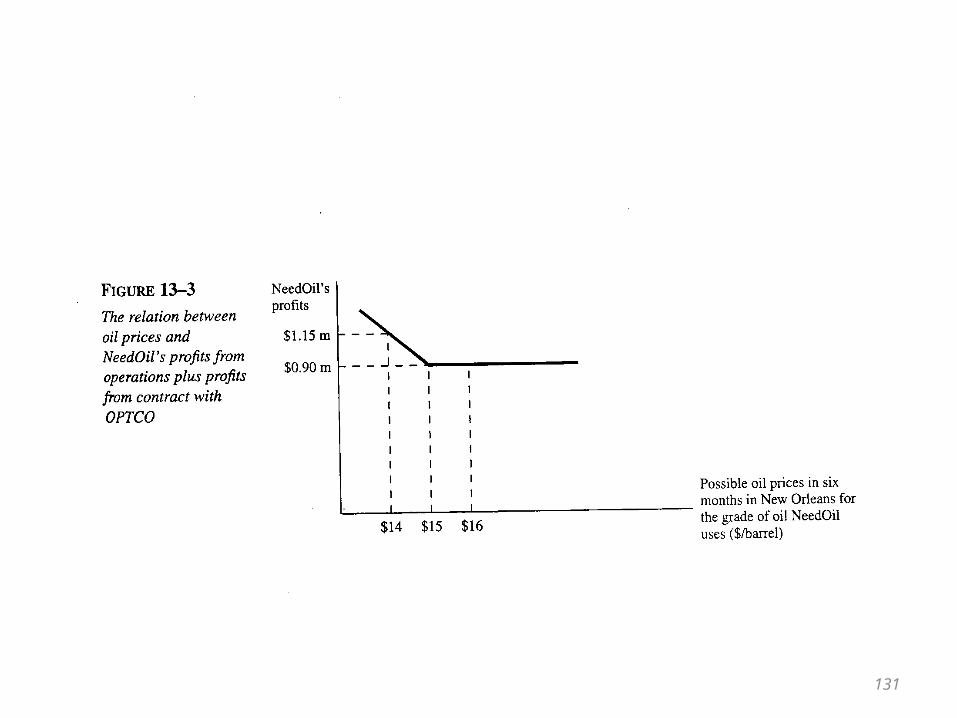

Hedging Example

132

January 1: Arrange to sell chairs for $5.00Raw materials today cost $2.50/chair

June 1: Build chairs

July 1: Deliver chairs

Hedging Example

Risk: Cost of raw materials

Options: 1. Sell chairs on a cost + basis2. Buy and hold raw materials3. Buy and have seller hold raw

materials4. Use a hedge

133

“Futures” Contract

Owner of contract on Termination Date Receives the lumber

Price of contract depends ona) Cost of lumber todayb) Risk Premium

Origination Date: September 1 Termination Date: August 31.

134

Hedging Contract

January 1: Buy Hedging ContractHedging Contract = $2.50 + xLumber = $2.50Risk Premium = x

June 1: Buy Lumber & Sell Futures ContractLumber = $2.50 + yFutures Contract = $2.50 + (x - z) + yChange in lumber cost = yDepreciation of risk premium = zTotal Cost = ($2.50 + x) + ($2.50 + y)

- ($2.50 + (x - z) + y)= $2.50 + z 135

Hedging ContractNumerical Example

Origination Date: September 1 Termination Date: August 31.Original Risk Loading: 0.60

x = .40x decreases .05 per monthz = .05(5) = .25

Total Cost = $2.50 + .25 = $2.75

136

Hedging Instruments for Financial Risks

137

Hedging Volatility

• Volatility is a measure of risk• Some sources of volatility can be hedged

– Interest Rate– Exchange Rate– Commodity Price

138

Interest Rate Volatility

• Debt is a key component of a firm’s capital structure• Interest rate hedges can stabilize borrowing costs• Some tools: forwards, futures, swaps, options

139

Exchange Rate Volatility

• International businesses are exposed to exchange rate risk• Tools for managing exchange rate risk

– forwards– futures– swaps

140

Commodity Price Volatility

•Costs of materials can be volatile:– Pricing becomes problematic– Sales demand becomes harder to predict

•Hedging allows for:– Better production decisions– Reduced volatility in cash flows

•Available tools (depending on the type of commodity): – Forwards– Futures– Swaps– Options

141

Reducing Risk Exposure

• Hedging will not normally reduce risk completely– Typically, only price risk can be hedged not quantity risk– Reducing risk completely causes loss of potential upside

• Timing– Short-run exposure can be managed in a variety of ways– Long-run exposure almost impossible to hedge

142

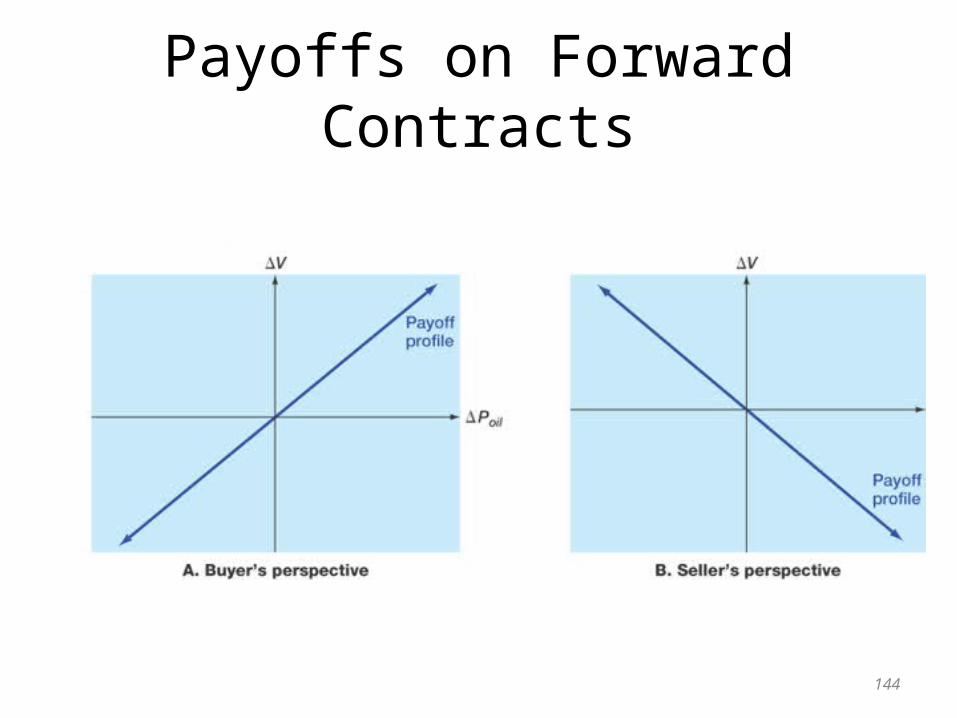

Forward Contracts• A contract between parties

– Agreement today on the price of the asset on the delivery date– Delivery and payment is specified for a future date

• Forward contracts are legally binding on both parties

• Positions– Long: Agrees to buy the asset on the future date– Short: Agrees to sell the asset on the future date

• Key points– Negotiated contract– No exchange of cash initially– Usually limited to large, creditworthy corporations

143

Payoffs on Forward Contracts

144

Hedging with Forwards

• Forward contracts can virtually eliminate price risk

• New risk created: Credit risk of the counterparty

• Forward contracts are primarily used to hedge exchange rate risk

145

Futures Contracts

• Futures traded on organized securities exchanges

• Upfront cash payment: MARGIN– Small relative to the value of the contract– “Marked-to-market” on a daily basis

• Clearinghouse guarantees contract performance

• Clearinghouse and margin requirements virtually eliminate credit risk

146

Hedging with Futures

• Futures contracts are standardized– Allows for trading– Exact hedging may be difficult or impossible

• Credit risk is virtually nonexistent

• Futures contracts are available on– physical assets– debt contracts– Currencies– equities

147

Swaps

• A long-term agreement between two parties • Can be viewed as a series of forward contracts

• Generally limited to large creditworthy institutions or companies

148

Option Contracts

• The right, but not the obligation, to buy (sell) an asset for a set price on or before a specified date

– Call – right to buy the asset– Put – right to sell the asset– Exercise or strike price –specified price– Expiration date – specified date

• Buyer has the right to exercise the option; the seller is obligated– Call – option writer is obligated to sell the asset if the option is exercised– Put – option writer is obligated to buy the asset if the option is exercised

• Options allow a firm to hedge downside risk, but still participate in upside potential

• Pay a premium for this benefit

149

Payoff Profiles: Calls

Buy a call with E = $40

0

10

20

30

40

50

60

70

0 20 40 60 80 100

Stock Price

Pay

off

Sell a Call E = $40

-70

-60

-50

-40

-30

-20

-10

0

0 20 40 60 80 100

Stock Price

Pay

off

150

Payoff Profiles: Puts

Buy a put with E = $40

05

1015202530354045

0 20 40 60 80 100

Stock Price

Pay

off

Sell a Put E = $40

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

0 20 40 60 80 100

Stock Price

Pay

off

151

Retention vs. Transfer

• Ability to Bear the Loss• Cost and Effectiveness of a Transfer• Degree of Control over the Risk• Insurance Loading Fees• Additional Insurer Services• Insurance as a Signal• Opportunity Costs• Taxes

152

Risk Financing Methods

• Guaranteed Cost Insurance

• Experience-Rated Insurance

• Retrospective Rating

153

154

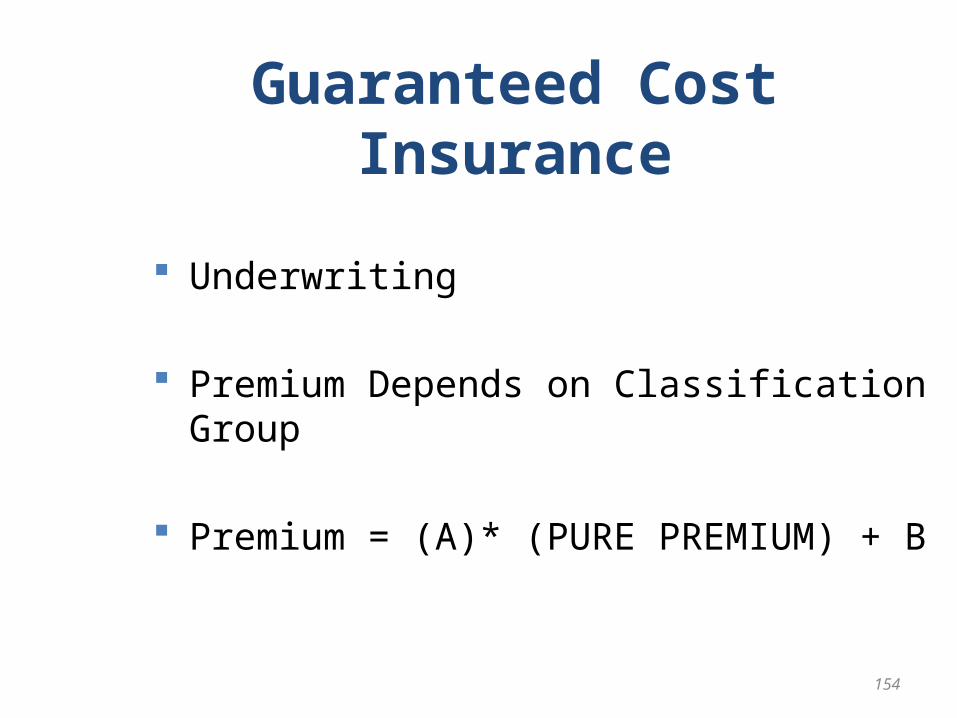

Guaranteed Cost Insurance

Underwriting

Premium Depends on Classification Group

Premium = (A)* (PURE PREMIUM) + B

Pure Premium

155

# cars = 10,000# losses = 250$ losses = $4.5 millionPure Premium = frequency x severityFrequency = 250 / 10,000 = 2.5%Severity = $4.5 million / 250 = $18,000Pure Premium = 2.5% (18,000) = $450A = 1.4 B = $501.4 (450) + 50 = $680

Underwriting Considerations

• Adverse Selection

• Misclassification

• Control

• Civil Rights

• Costs of Classification

• Social Policy

156

What’s Fair and WhyHealth Insurance Underwriting Factors

• Cigarette Smoking• Obesity• Age• Prior history of heart disease• Genetic Predisposition to Stomach Cancer• Gender• Race

157

State Underwriting Restrictions: Health Insurance

• CALIFORNIA: Blindness, Gender, Marital Status, DES

• N. DAKOTA: Blindness, Gender, Race

• WISCONSIN: Blindness, Gender, Physical Impairment

158

How Insurance WorksAn Example

Assume an individual has a 1% probability of getting cancer and incurring medical expenses of $200,000.

How much would you charge to bear this risk?

159

Central Limit TheoremMean = True Mean

Law of Large NumbersIncrease sample size by N New Mean = Old Mean x N New S.D. = Old S.D. x Sq. Root of N

160

How Insurance Works

161

HOW INSURANCE WORKS

AN ILLUSTRATIVE EXAMPLE

Sample Size = 1,000

Mean = 10

S.D. = 2

Loss per claim = $200,000 S.D. Prob.

1 68.27

2 95.45

3 99.73

4 6 8 10 12 14 16

For 99.73% survival prob. insurer will charge: 16 x $200,000 = $3,200

1,000

Increase sample size to 100,000 (100x)Mean # of Losses = 10 x 100 = 1,000S.D. = 2 x sqroot (100) = 20

Now for 99.73% survival prob. insurer will charge: 1060 x $200,000 = $2,120

100,000

HOW INSURANCE WORKSAN ILLUSTRATIVE EXAMPLE

162

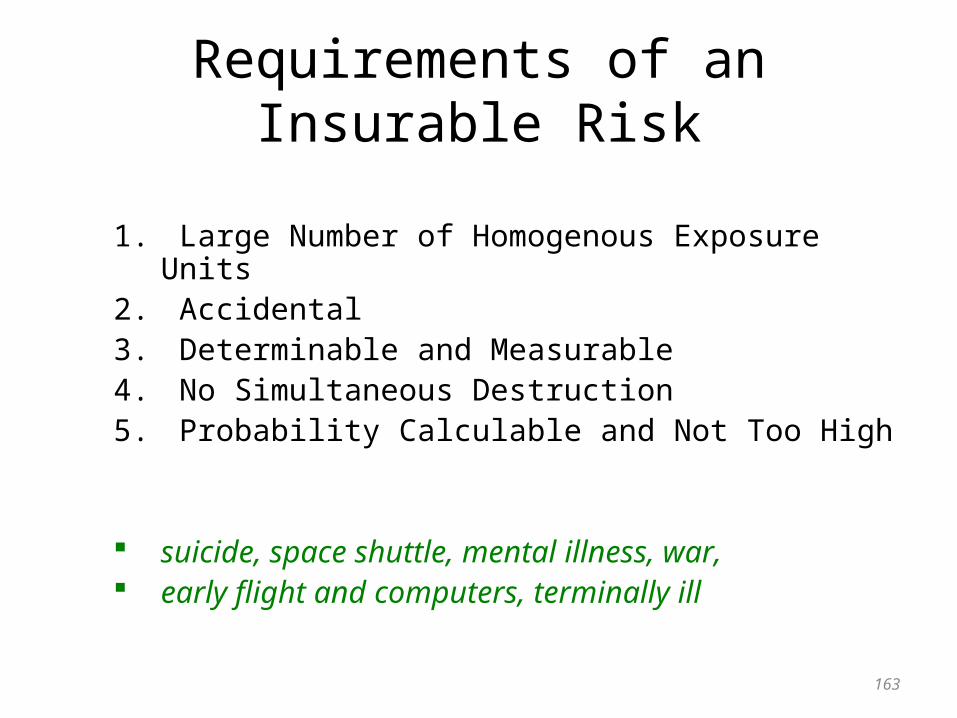

Requirements of anInsurable Risk

1. Large Number of Homogenous Exposure Units2. Accidental3. Determinable and Measurable4. No Simultaneous Destruction5. Probability Calculable and Not Too High

suicide, space shuttle, mental illness, war, early flight and computers, terminally ill

163

Social and EconomicValue of Insurance

• Stability

• Indemnification

• Reduction in Reserve Funds

• Insurers’ Ability to Invest

• Satisfies Financial Requirements

• Specialization in Loss Prevention

164

Social Costs of Insurance

• Insurers’ Operating Costs

• Moral Hazard

• Exaggeration of Losses

165

Cheating with Insurance

• Insurer– Failure to Honor the Contract– Misleading Contracts– False Advertising– Inappropriate Sales

• Insured– Fraud

166

Controlling Cheating

• Litigation

• Regulation

167

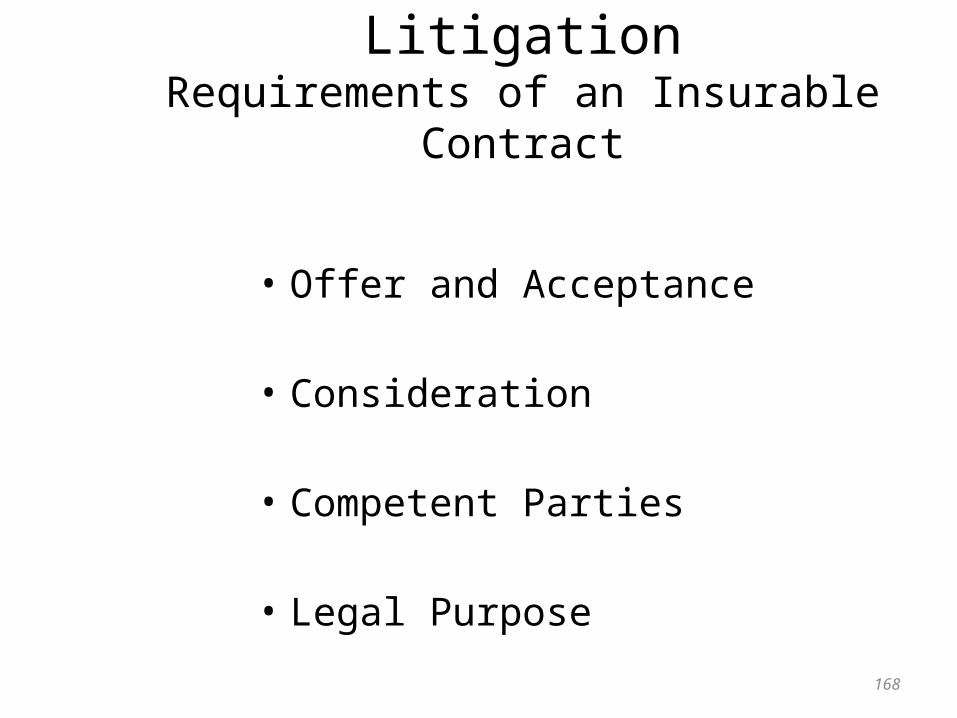

LitigationRequirements of an Insurable Contract

• Offer and Acceptance

• Consideration

• Competent Parties

• Legal Purpose

168

LitigationLegal Principles: Indemnity

• Valuation– Property: ACV– Liability: Actual Damages

• Apparent Exceptions– Valued Policies– Replacement Cost Insurance– Life Insurance

169

Actual Cash Value Example

ACV = Replacement Cost – Depreciation

1/1/04: Buy Machine for $3,000, 10 year life 1/1/06: Fire Destroys Machine; New Machine

Costs $10,000

ACV = $10,000 - $2,000 = $8,000

170

LitigationPrinciple of Insurable Interest

• Property and Liability: Time of Loss– Ownership– Potential Legal Liability– Secured Creditors

• Life Insurance: Time of Policy Purchase– Close Ties: Love, Blood, Marriage– Pecuniary Interest

171

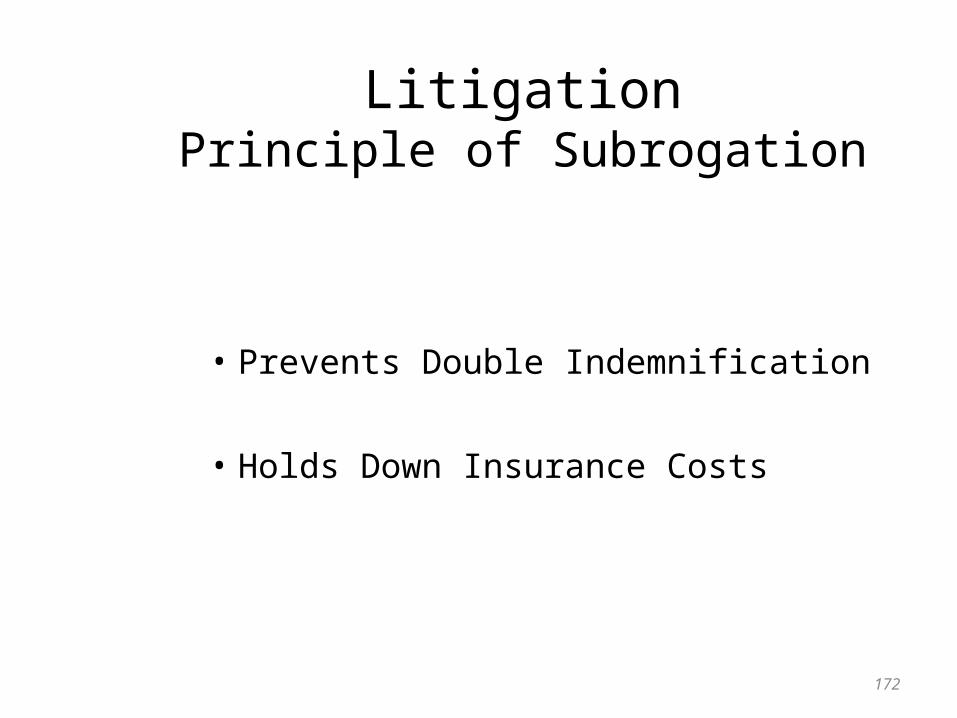

LitigationPrinciple of Subrogation

• Prevents Double Indemnification

• Holds Down Insurance Costs

172

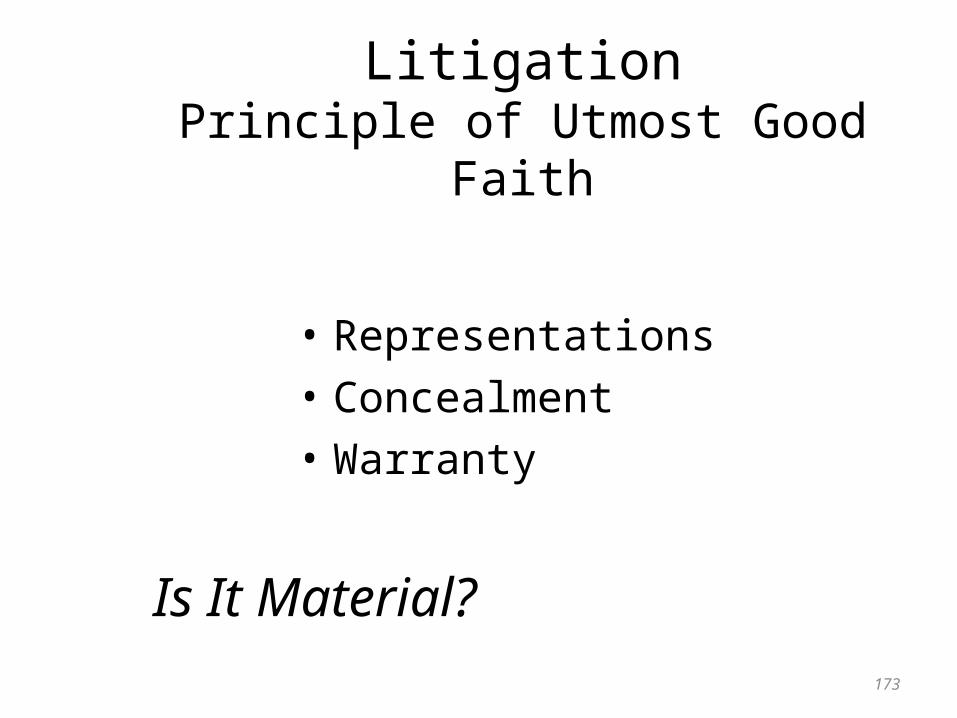

LitigationPrinciple of Utmost Good Faith

• Representations

• Concealment

• Warranty

173

Is It Material?

Why Is Insurance Regulated?

• Advance Payment of Premiums

• Complexity of Transaction

174

Types of Regulation

• Licensing• Solvency• Rate Approval• Agents’ Activities• Insurance Contracts

175

Insolvency: Major Reasons

• Bad Management• Poor Underwriting• Inadequate Reserves• Bad Investing• Inattentive to Loss Prevention• Competitive Pressures

176

Danger of Insolvency

• Most Insurers are Very Solid• 100+ Years

– 71 Life Insurers– 200 Property and Liability Insurers

• Guaranty Funds• Buyout of Failing Firms

177

Premium Regulation

• Adequate

• Fair

• Reasonable

178

Methods of Rate Regulation

• Prior Approval

• File and Use

• Open Competition

179

Advantages of Open Competition

• Flexibility• Increased Availability of Insurance • Avoid Political Fights• Frees Time of Regulators

180

Disadvantages of Open Competition

• Price Gouging (?)

• Risk of Insolvency (?)

• Fair (?)

181

Regulation of Agents’ Activities

• Licensing

• Prohibited Acts– Twisting– Rebating

182

Causes of InsuranceMarket Failure

• Adverse Selection• Individuals Underestimate

the Loss Potential• Insurance Costs Too Much• Pooling Not Possible• Insurers Can Not Estimate

the Loss Potential

183

THE END

184