Embed Size (px)

Citation preview

Risk Factors as Building Blocks of Asset AllocationMaster Thesis

Josef Zorn

University of Innsbruck

Value Day, Dornbirn, March 12, 2015

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Road Map

1 Traditional Approach

2 Risk Factors - Factor Loadings

3 Portfolio Performance

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Road Map

1 Traditional ApproachIntroductionModern portfolio theoryCritique

2 Risk Factors - Factor LoadingsThe concept of risk factorsEmpirical analysis - factor loadings

3 Portfolio PerformanceEx post performanceEx ante performanceConclusion

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Motivation - Research Question

• Examine an alternative to traditional portfolio approaches

• Construct portfolios with risk factors

• Which factors?• Assets’ sensitivity to factors• Performance of risk factor portfolios

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Motivation - Research Question

• Examine an alternative to traditional portfolio approaches

• Construct portfolios with risk factors

• Which factors?• Assets’ sensitivity to factors• Performance of risk factor portfolios

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Motivation - Research Question

• Examine an alternative to traditional portfolio approaches

• Construct portfolios with risk factors

• Which factors?• Assets’ sensitivity to factors• Performance of risk factor portfolios

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Motivation - Research Question

• Examine an alternative to traditional portfolio approaches

• Construct portfolios with risk factors• Which factors?

• Assets’ sensitivity to factors• Performance of risk factor portfolios

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Motivation - Research Question

• Examine an alternative to traditional portfolio approaches

• Construct portfolios with risk factors• Which factors?• Assets’ sensitivity to factors

• Performance of risk factor portfolios

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Motivation - Research Question

• Examine an alternative to traditional portfolio approaches

• Construct portfolios with risk factors• Which factors?• Assets’ sensitivity to factors• Performance of risk factor portfolios

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

Asset Allocation:Balance risk and reward of a portfolios assets w.r.t individual’s goals,risk tolerance and investment horizon.

• Markowitz (1952) approach:

Mean-Variance-Optimization

minweights

Var [Rp] Subject to E [Rp] = Target and wi ≥ 0. (1)

• Diversification among Asset Classes!

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

World Investment

Opportunities

Traditional

Investments

Stocks

Bonds

Modern

Alternatives

Hedge Funds

Managed Futures

Traditional

Alternatives

Private Equity

Real Estate

Commodities

Figure: Asset Classes. Source: Schneeweis et al. (2010)

Asset classes: share common economic factors, similar risk/return,share legal/regulatory structure. Low correlation across each other(!?)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

World Investment

Opportunities

Traditional

Investments

Stocks

Bonds

Modern

Alternatives

Hedge Funds

Managed Futures

Traditional

Alternatives

Private Equity

Real Estate

Commodities

Figure: Asset Classes. Source: Schneeweis et al. (2010)

Asset classes: share common economic factors, similar risk/return,share legal/regulatory structure. Low correlation across each other(!?)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Modern Portfolio Theory

World Investment

Opportunities

Traditional

Investments

Stocks

Bonds

Modern

Alternatives

Hedge Funds

Managed Futures

Traditional

Alternatives

Private Equity

Real Estate

Commodities

Figure: Asset Classes. Source: Schneeweis et al. (2010)

Asset classes: share common economic factors, similar risk/return,share legal/regulatory structure. Low correlation across each other(!?)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)

• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)

• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)

• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)

• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)

• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)• Correlation is non-linear (unstable and asymmetric)

• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)

• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets

• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

• ‘What is an Asset Class, Anyway?’ (Greer 1997)

• Kritzman (1999): Marketing defines asset classes

• The Myth of Diversification (Page & Taborsky 2011)

• Diversification disappears when most needed (!)• Correlation is non-linear (unstable and asymmetric)• Regime shifts occur (risk on - risk off)• Macro driven markets• Crisis phenomenon ‘Market of one’ (The Economist 2007)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

0.2

0.4

0.6

0.8

1.0

Dec-74 Dec-79 Dec-84 Dec-89 Dec-94 Dec-99 Dec-04 Dec-09

Corr

elat

ion

Coeffi

cien

ts

10 year

5 year

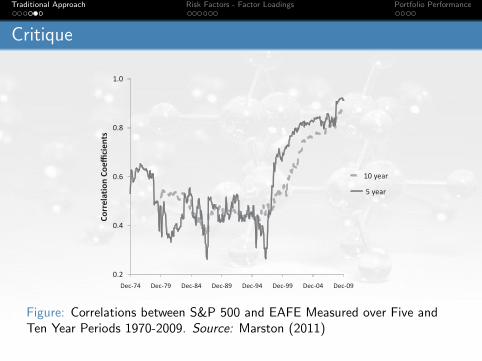

F IGURE 5.9 Correlations between S&P 500 and EAFE Measured over Fiveand Ten Year Periods, 1970–2009Data Sources: MSCI, ©Morningstar, and S&P.

Figure: Correlations between S&P 500 and EAFE Measured over Five andTen Year Periods 1970-2009. Source: Marston (2011)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Critique

y

Figure: Correlation Profile between U.S. and World Ex-U.S. 1979-2009.Source: Chua et al. (2009)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Road Map

1 Traditional ApproachIntroductionModern portfolio theoryCritique

2 Risk Factors - Factor LoadingsThe concept of risk factorsEmpirical analysis - factor loadings

3 Portfolio PerformanceEx post performanceEx ante performanceConclusion

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

The concept of risk factors

Risk Factors

• Microscopic elements that shape risk and return

• Analogy from chemistry: If factors are atoms then asset classesare molecules

• Conceptual difference to asset class approach : Approach startsfrom the microscopic level

• Bottom up approach

• −→ Correlation between factors substantially lower (!)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

The concept of risk factors

Risk Factors

• Microscopic elements that shape risk and return

• Analogy from chemistry: If factors are atoms then asset classesare molecules

• Conceptual difference to asset class approach : Approach startsfrom the microscopic level

• Bottom up approach

• −→ Correlation between factors substantially lower (!)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

The concept of risk factors

Risk Factors

• Microscopic elements that shape risk and return

• Analogy from chemistry: If factors are atoms then asset classesare molecules

• Conceptual difference to asset class approach : Approach startsfrom the microscopic level

• Bottom up approach

• −→ Correlation between factors substantially lower (!)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

The concept of risk factors

Risk Factors

• Microscopic elements that shape risk and return

• Analogy from chemistry: If factors are atoms then asset classesare molecules

• Conceptual difference to asset class approach : Approach startsfrom the microscopic level

• Bottom up approach

• −→ Correlation between factors substantially lower (!)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

The concept of risk factors

Risk Factors

• Microscopic elements that shape risk and return

• Analogy from chemistry: If factors are atoms then asset classesare molecules

• Conceptual difference to asset class approach : Approach startsfrom the microscopic level

• Bottom up approach

• −→ Correlation between factors substantially lower (!)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

The concept of risk factors

Risk Factors

• Microscopic elements that shape risk and return

• Analogy from chemistry: If factors are atoms then asset classesare molecules

• Conceptual difference to asset class approach : Approach startsfrom the microscopic level

• Bottom up approach

• −→ Correlation between factors substantially lower (!)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Which factors?

GDP Growth

Macroeconomic Regional Fundamental Fixed Income Other

SovereignExposure

Size Duration Liquidity

Productivity Currency Value Convexity Leverage

Real Interest Rates

Emerging Markets

(Institutions + Transparency)

Momentum Credit Spread Real Estate

Inflation Default Risk Commodities

Volatility Capital Structure

Private Markets

Figure: Sampling of Risk Factors and Potential Groupings. Source: Based onPodkaminer (2013)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Which factors?

GDP Growth

Macroeconomic Regional Fundamental Fixed Income Other

SovereignExposure

Size Duration Liquidity

Productivity Currency Value Convexity Leverage

Real Interest Rates

Emerging Markets

(Institutions + Transparency)

Momentum Credit Spread Real Estate

Inflation Default Risk Commodities

Volatility Capital Structure

Private Markets

Figure: Sampling of Risk Factors and Potential Groupings. Source: Based onPodkaminer (2013)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Estimation

Econometric model based on Chen et al. (1986) , Connor & Korajczyk(2010), Kaya et al. (2012).

Factor loadings

r = a0 + Bf + ε. (2)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Estimation

Econometric model based on Chen et al. (1986) , Connor & Korajczyk(2010), Kaya et al. (2012).

Factor loadings

r = a0 + Bf + ε. (2)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Data

Table: Indices (y-Variable)Ticker Index Asset Class Source

CBNK NASDAQ Bank Index Equity Banks BloombergDAX German Stock Index DAX Equity Foreign BloombergEURUSD e-US$ Exchange Rate Currency BloombergGBPUSD $ -US$ Exchange Rate Currency BloombergGOLD Gold spot price Commodity BloombergHSI Hang Seng Index Equity Foreign BloombergINDU Dow Jones Industrial Average Index Equity BloombergIXIC NASDAQ Composite Index Equity BloombergLBUSTRUU Barclays Capital Aggreg. Bond Index Corporate Bonds BloombergMBAVREFI MBAVREFI Index Real Estate BloombergMXEA MSCI EAFE Index Equity Foreign BloombergMXEF MSCI Emerging Markets Index Equity Emerg. Markets BloombergMXWO MSCI World Index Equity BloombergNAREIT NAREIT Real Estate Index Real Estate BloombergNDX NASDAQ-100 Equity Technolog. BloombergRUA Russell 3000 Equity BloombergRUT Russell 2000 Equity Small Cap BloombergS5ENRS S&P 500 Energy Sector Index Equity Energy BloombergS5FINL S&P 500 Financials Sector Index Equity Financial BloombergSPGSCI Goldman Sachs Commodity Index Commodities BloombergSPX S&P 500 Equity BloombergTNX CBOE InterestRate10-YearT-Note Government Bonds BloombergUKX FTSE 100 Index Equity Foreign BloombergUTIL Dow Jones Utilities Average Equity Utilities BloombergXAG PHLX Gold/Silver Sector Commodities Bloomberg

Table: Factors (x-Variable)Symbol Variable Source

IP Industrial production Survey of Current BusinessE [πt+1|t ] Expected Inflation Federal Reserve Bank of St. Louisπt Inflation rate (log of CPI) Bureau of Labor Statisticsvol CBOE volatility index Bloomberggovbondlong 30 year government bond returns Bloomberggovbondshort 1 year government bond returns BloombergBaa bond Moody’s Seasoned Baa Corp. Bond Yield Federal Reserve Bank of St. LouisSMB,HML,M size, value, momentum factors Fama-French Database

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

DataTable: Indices (y-Variable)

Ticker Index Asset Class Source

CBNK NASDAQ Bank Index Equity Banks BloombergDAX German Stock Index DAX Equity Foreign BloombergEURUSD e-US$ Exchange Rate Currency BloombergGBPUSD $ -US$ Exchange Rate Currency BloombergGOLD Gold spot price Commodity BloombergHSI Hang Seng Index Equity Foreign BloombergINDU Dow Jones Industrial Average Index Equity BloombergIXIC NASDAQ Composite Index Equity BloombergLBUSTRUU Barclays Capital Aggreg. Bond Index Corporate Bonds BloombergMBAVREFI MBAVREFI Index Real Estate BloombergMXEA MSCI EAFE Index Equity Foreign BloombergMXEF MSCI Emerging Markets Index Equity Emerg. Markets BloombergMXWO MSCI World Index Equity BloombergNAREIT NAREIT Real Estate Index Real Estate BloombergNDX NASDAQ-100 Equity Technolog. BloombergRUA Russell 3000 Equity BloombergRUT Russell 2000 Equity Small Cap BloombergS5ENRS S&P 500 Energy Sector Index Equity Energy BloombergS5FINL S&P 500 Financials Sector Index Equity Financial BloombergSPGSCI Goldman Sachs Commodity Index Commodities BloombergSPX S&P 500 Equity BloombergTNX CBOE InterestRate10-YearT-Note Government Bonds BloombergUKX FTSE 100 Index Equity Foreign BloombergUTIL Dow Jones Utilities Average Equity Utilities BloombergXAG PHLX Gold/Silver Sector Commodities Bloomberg

Table: Factors (x-Variable)Symbol Variable Source

IP Industrial production Survey of Current BusinessE [πt+1|t ] Expected Inflation Federal Reserve Bank of St. Louisπt Inflation rate (log of CPI) Bureau of Labor Statisticsvol CBOE volatility index Bloomberggovbondlong 30 year government bond returns Bloomberggovbondshort 1 year government bond returns BloombergBaa bond Moody’s Seasoned Baa Corp. Bond Yield Federal Reserve Bank of St. LouisSMB,HML,M size, value, momentum factors Fama-French Database

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Results - loadings

Figure: Factor Decomposition Chart - Sample 1990-2013

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Results - loadings

Figure: Factor Decomposition Chart - Sample 1990-2013

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

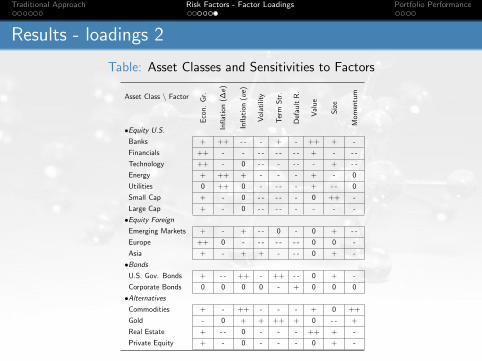

Results - loadings 2

Table: Asset Classes and Sensitivities to Factors

Eco

n.

Gr.

Infl

atio

n(∆

e)

Infl

atio

n(ue

)

Vol

atili

ty

Ter

mS

tr.

Def

ault

R.

Val

ue

Siz

e

Mom

entu

mAsset Class \ Factor

•Equity U.S.

Banks + ++ - - - + - ++ + -

Financials ++ - - - - - - - - + - - -

Technology ++ - 0 - - - - - - + - -

Energy + ++ + - - - + - 0

Utilities 0 ++ 0 - - - - + - - 0

Small Cap + - 0 - - - - - 0 ++ -

Large Cap + - 0 - - - - - - - -

•Equity Foreign

Emerging Markets + - + - - 0 - 0 + - -

Europe ++ 0 - - - - - - - 0 0 -

Asia + - + + - - - 0 + -

•BondsU.S. Gov. Bonds + - - ++ - ++ - - 0 + -

Corporate Bonds 0 0 0 0 - + 0 0 0

•AlternativesCommodities + - ++ - - - + 0 ++

Gold - 0 + + ++ + 0 - - +

Real Estate + - - 0 - - - ++ + -

Private Equity + - 0 - - - 0 + -

Note: + and ++ represent positive and highly positive factor loadings, respectively. - and - - represent negative andhighly negative factor loadings. 0 denotes factor loadings near zero.

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Results - loadings 2

Table: Asset Classes and Sensitivities to Factors

Eco

n.

Gr.

Infl

atio

n(∆

e)

Infl

atio

n(ue

)

Vol

atili

ty

Ter

mS

tr.

Def

ault

R.

Val

ue

Siz

e

Mom

entu

mAsset Class \ Factor

•Equity U.S.

Banks + ++ - - - + - ++ + -

Financials ++ - - - - - - - - + - - -

Technology ++ - 0 - - - - - - + - -

Energy + ++ + - - - + - 0

Utilities 0 ++ 0 - - - - + - - 0

Small Cap + - 0 - - - - - 0 ++ -

Large Cap + - 0 - - - - - - - -

•Equity Foreign

Emerging Markets + - + - - 0 - 0 + - -

Europe ++ 0 - - - - - - - 0 0 -

Asia + - + + - - - 0 + -

•BondsU.S. Gov. Bonds + - - ++ - ++ - - 0 + -

Corporate Bonds 0 0 0 0 - + 0 0 0

•AlternativesCommodities + - ++ - - - + 0 ++

Gold - 0 + + ++ + 0 - - +

Real Estate + - - 0 - - - ++ + -

Private Equity + - 0 - - - 0 + -

Note: + and ++ represent positive and highly positive factor loadings, respectively. - and - - represent negative andhighly negative factor loadings. 0 denotes factor loadings near zero.

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Road Map

1 Traditional ApproachIntroductionModern portfolio theoryCritique

2 Risk Factors - Factor LoadingsThe concept of risk factorsEmpirical analysis - factor loadings

3 Portfolio PerformanceEx post performanceEx ante performanceConclusion

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Comparison Asset Class vs. Risk Factor

Approach:

• Risk factor portfolio: Mimic factor with long/shortcombinations of investable indices based on low/high loadings inprevious empirical part: 8 factors

• Asset class portfolio: same indices as the previous portfolio butwithout long/short combination: 11 indices

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Comparison Asset Class vs. Risk Factor

Approach:

• Risk factor portfolio: Mimic factor with long/shortcombinations of investable indices based on low/high loadings inprevious empirical part: 8 factors

• Asset class portfolio: same indices as the previous portfolio butwithout long/short combination: 11 indices

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Comparison Asset Class vs. Risk Factor

Approach:

• Risk factor portfolio: Mimic factor with long/shortcombinations of investable indices based on low/high loadings inprevious empirical part: 8 factors

• Asset class portfolio: same indices as the previous portfolio butwithout long/short combination: 11 indices

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Ex post

0 2% 4% 6% 8% 10% 12% 14% 16% 18%0

2%

4%

6%

8%

10%

12%

14%

16%

Risk (Standard Deviation)

Exp

ecte

d R

etur

n

Optimal Capital Allocation -- Zero-Beta-CAPM

Optimal Overall Portfolio

Optimal Risky Portfolio

Rz=1.1%

(a) Risk Factor Portfolio

0 2% 4% 6% 8% 10% 12% 14% 16%5%

6%

7%

8%

9%

10%

11%

12%

13%

Risk (Standard Deviation)

Exp

ecte

d R

etur

n

Optimal Capital Allocation -- Zero-Beta-CAPM

Optimal Overall Portfolio

Optimal Risky Portfolio

Rz=5.4%

(b) Asset Class Portfolio

Figure: Comparison of Portfolios with Zero-β-CAPM

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Ex post

0 2% 4% 6% 8% 10% 12% 14% 16% 18%0

2%

4%

6%

8%

10%

12%

14%

16%

Risk (Standard Deviation)

Exp

ecte

d R

etur

n

Optimal Capital Allocation -- Zero-Beta-CAPM

Optimal Overall Portfolio

Optimal Risky Portfolio

Rz=1.1%

(a) Risk Factor Portfolio

0 2% 4% 6% 8% 10% 12% 14% 16%5%

6%

7%

8%

9%

10%

11%

12%

13%

Risk (Standard Deviation)

Exp

ecte

d R

etur

n

Optimal Capital Allocation -- Zero-Beta-CAPM

Optimal Overall Portfolio

Optimal Risky Portfolio

Rz=5.4%

(b) Asset Class Portfolio

Figure: Comparison of Portfolios with Zero-β-CAPM

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Ex ante

$100

$120

$140

$160

$180

$200

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Factor PortfolioAsset Class Portfolio60/40 Portfolio

Figure: Cumulative Return of Risk Factor, Asset Class and 60/40 Portfolio

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Ex ante

$100

$120

$140

$160

$180

$200

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Factor PortfolioAsset Class Portfolio60/40 Portfolio

Figure: Cumulative Return of Risk Factor, Asset Class and 60/40 Portfolio

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:

• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:

• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:

• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:

• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:• Identify multi-faceted risk, envision true underlying factors

• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)

• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Summary

Risk factor allocation - a worthwhile concept?

• Risk factor portfolio not superior to traditional portfolio

• Some interesting characteristics (e.g. max. drawdown), mitigationof risk (return); better performance than 60/40 portfolio

• Practical importance:• Identify multi-faceted risk, envision true underlying factors• Allows for scenario analysis (macro environments)• Potential to build robust portfolios (min. drawdown)

• Evidence mixed in literature [Bender et al. (2010), Bird et al.(2013), Idzorek & Kowara (2013)]

• Still more research needed (more factors, better instruments)

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Thank you for your attention!

Questions?

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Bender, J., Briand, R., Nielsen, F. & Stefek, D. (2010), ‘Portfolio ofRisk Premia: A New Approach to Diversification’, The Journal ofPortfolio Management 36(2), pp. 17–25.

Bird, R., Liem, H. & Thorp, S. (2013), ‘The tortoise and the hare:Risk premium versus alternative asset portfolios’, The Journal ofPortfolio Management 39(3), pp. 112–122.

Chen, N.-F., Roll, R. & Ross, S. A. (1986), ‘Economic forces and thestock market’, The Journal of Business 59(3), pp. 383–403.

Chua, D. B., Kritzman, M. & Page, S. (2009), ‘The Myth ofDiversification’, The Journal of Portfolio Management 36(1), pp.26–35.

Connor, G. & Korajczyk, R. A. (2010), Factor Models in Portfolio andAsset Pricing Theory, in J. Guerard, ed., ‘Handbook of PortfolioConstruction: Contemporary Applications of Markowitz Techniques’,Springer, London, pp. 401–418.

Greer, R. J. (1997), ‘What is an Asset Class, Anyway?’, The Journalof Portfolio Management 23(2), pp. 86–91.

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Idzorek, T. M. & Kowara, M. (2013), ‘Factor-Based Asset Allocationvs. Asset-Class-Based Asset Allocation ’, Financial Analyst Journal69(3), pp. 19–30.

Kaya, H., Lee, W. & Wan, Y. (2012), ‘Risk Budgeting with AssetClass and Risk Class Approaches’, The Journal of Investing21(1), pp. 109–115.

Kritzman, M. (1999), ‘Toward Defining an Asset Class’, The Journalof Portfolio Management 2(1), pp. 79–82.

Markowitz, H. M. (1952), ‘Portfolio Selection’, The Journal of Finance7(1), pp. 77–91.

Marston, R. C. (2011), Portfolio Design: A Modern Approach to AssetAllocation (Wiley Finance), 1 edn, Wiley.

Page, S. & Taborsky, M. A. (2011), ‘The Myth of Diversification: RiskFactors versus Asset Classes’, The Journal of Portfolio Management37(4), pp. 1–2.

Podkaminer, E. L. (2013), ‘Risk Factors as Building Blocks forPortfolio Diversification: The Chemistry of Asset Allocation’,

Traditional Approach Risk Factors - Factor Loadings Portfolio Performance

Investment Risk and Performance Feature Articles, CFA Institute .acessed February 25, 2013.

Schneeweis, T., Crowder, G. B. & Kazemi, H. (2010), The NewScience of Asset Allocation, 1 edn, John Wiley & Sons, Inc.,Hoboken, New Jersey.

The Economist (2007), ‘We All Fall Down’, The Economist p. 68.March 10.URL: http://www.economist.com/node/8829603