Embed Size (px)

Citation preview

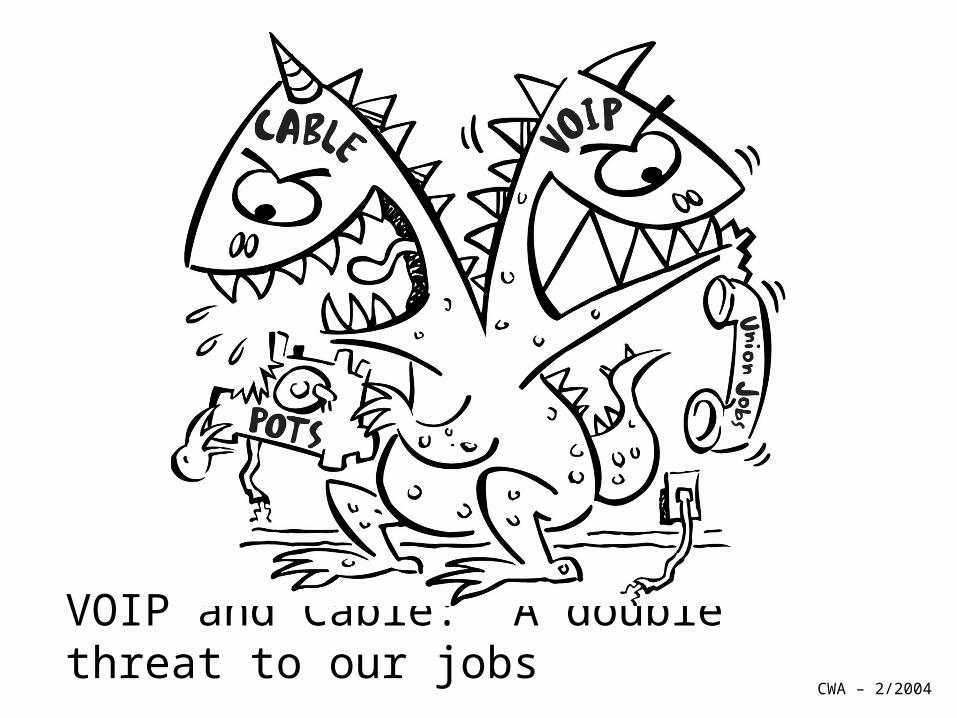

VOIP and Cable: A double threat to our jobsCWA – 2/2004

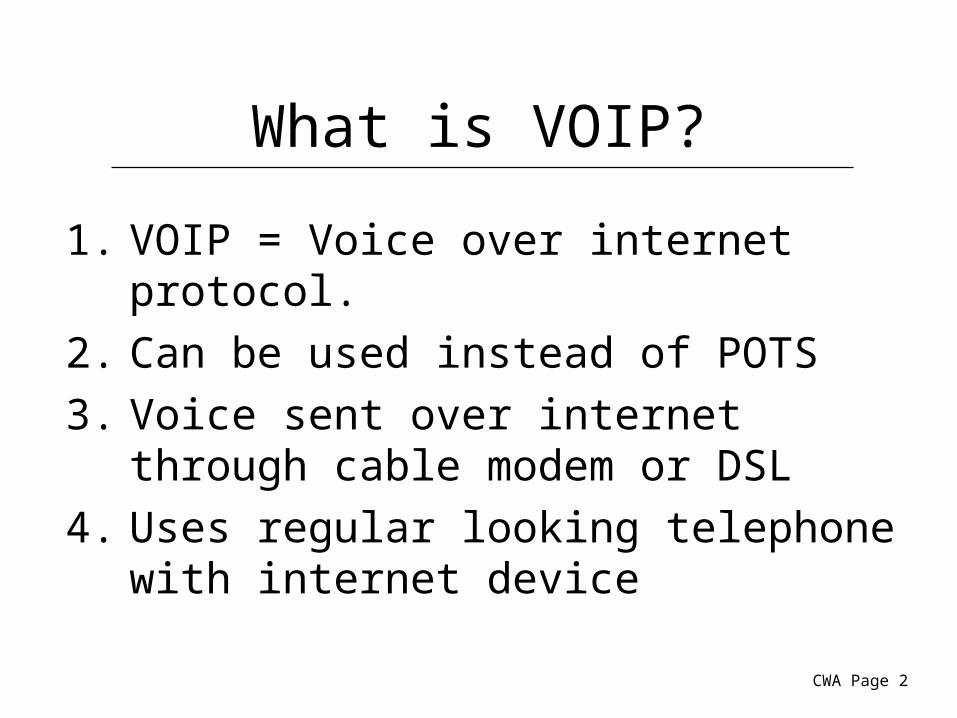

What is VOIP?

1. VOIP = Voice over internet protocol.

2. Can be used instead of POTS

3. Voice sent over internet through cable modem or DSL

4. Uses regular looking telephone with internet device

CWA Page 2

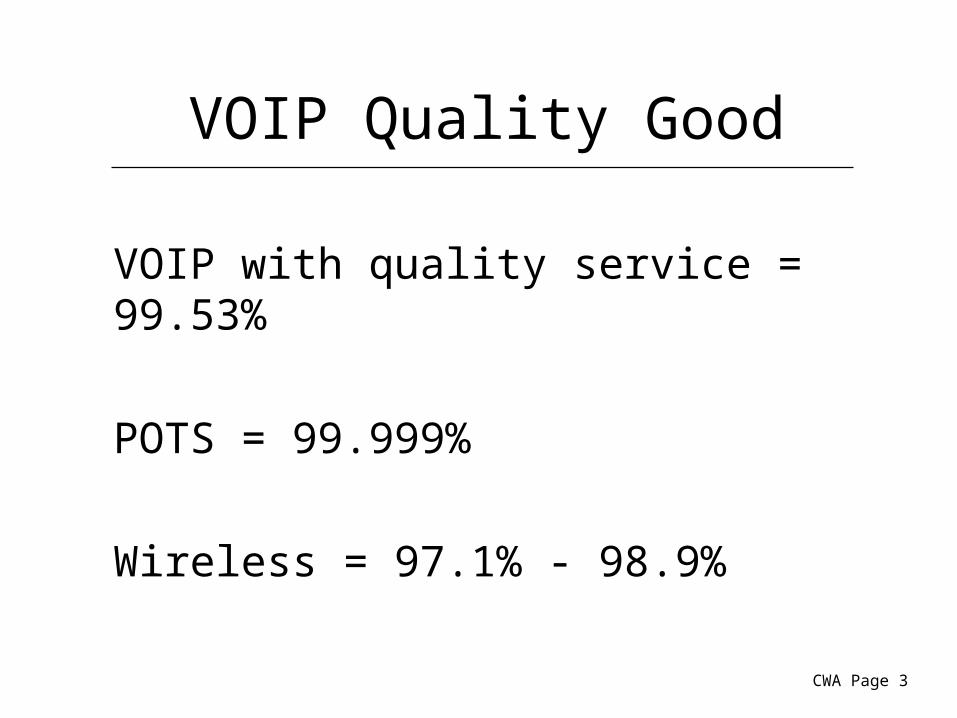

VOIP Quality Good

VOIP with quality service = 99.53%

POTS = 99.999%

Wireless = 97.1% - 98.9%

CWA Page 3

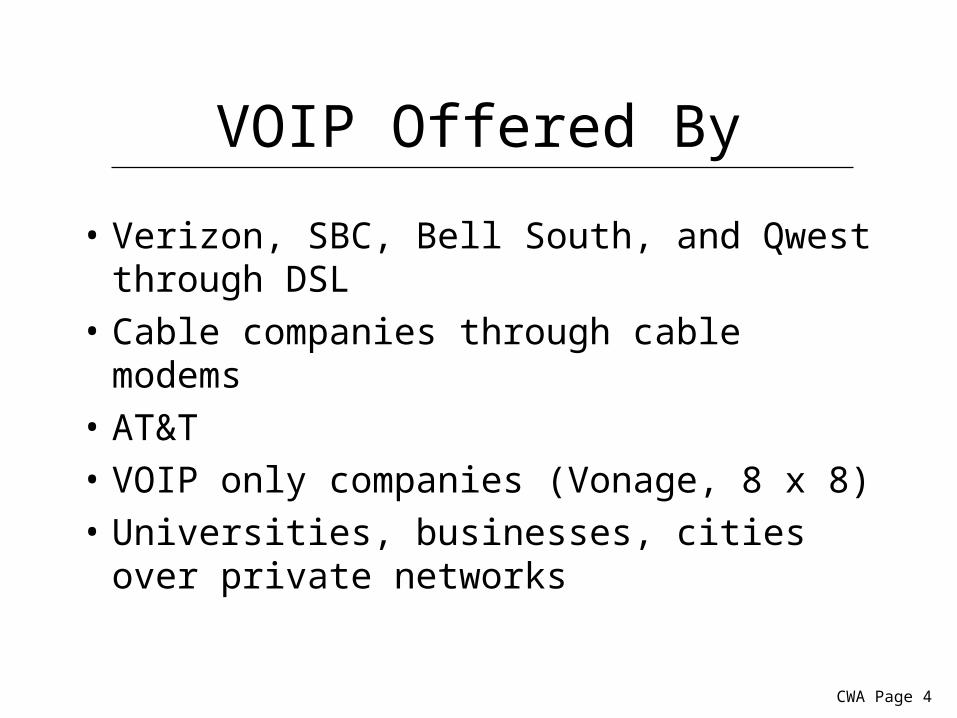

VOIP Offered By

• Verizon, SBC, Bell South, and Qwest through DSL

• Cable companies through cable modems

• AT&T

• VOIP only companies (Vonage, 8 x 8)

• Universities, businesses, cities over private networks

CWA Page 4

Proprietary material for authorized CWA use only. This material may not be reproduced, distributed, or used without permission from CWA.

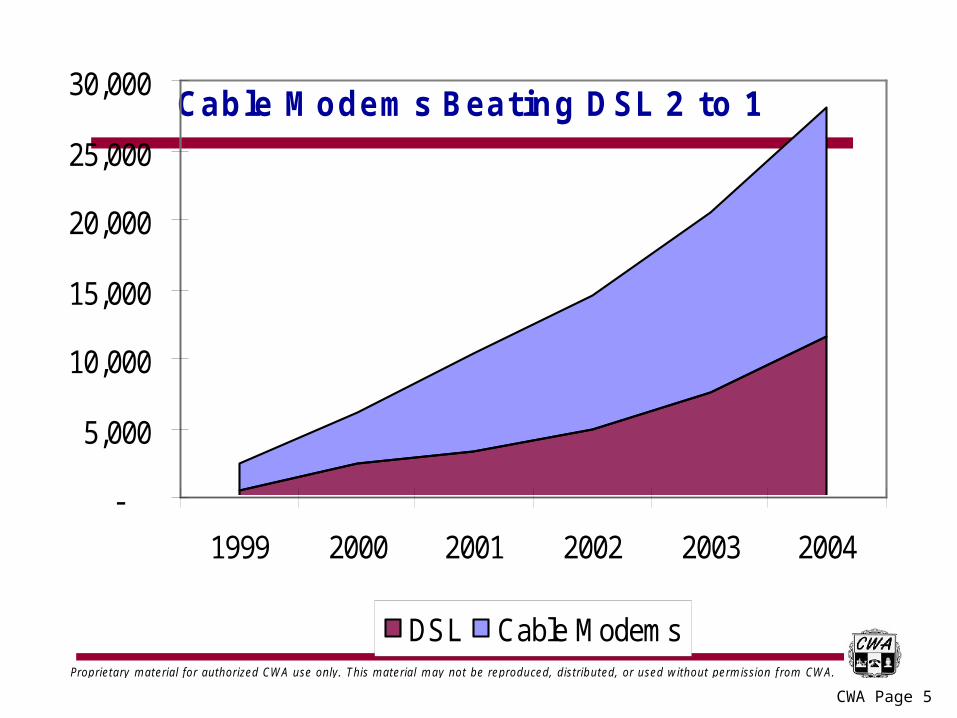

Cable Modems Beating DSL 2 to 1

-

5,000

10,000

15,000

20,000

25,000

30,000

1999 2000 2001 2002 2003 2004

DSL Cable Modems

CWA Page 5

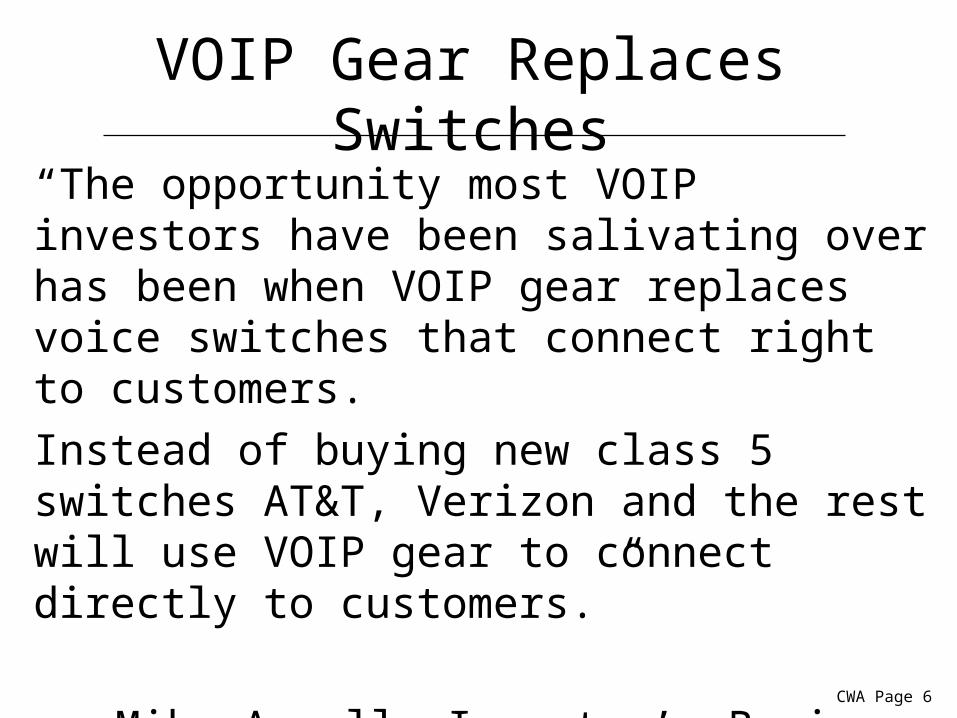

VOIP Gear Replaces Switches

“The opportunity most VOIP investors have been salivating over has been when VOIP gear replaces voice switches that connect right to customers.

Instead of buying new class 5 switches AT&T, Verizon and the rest will use VOIP gear to connect directly to customers.”

Mike Angell, Investor’s Business Daily

January 29, 2004CWA Page 6

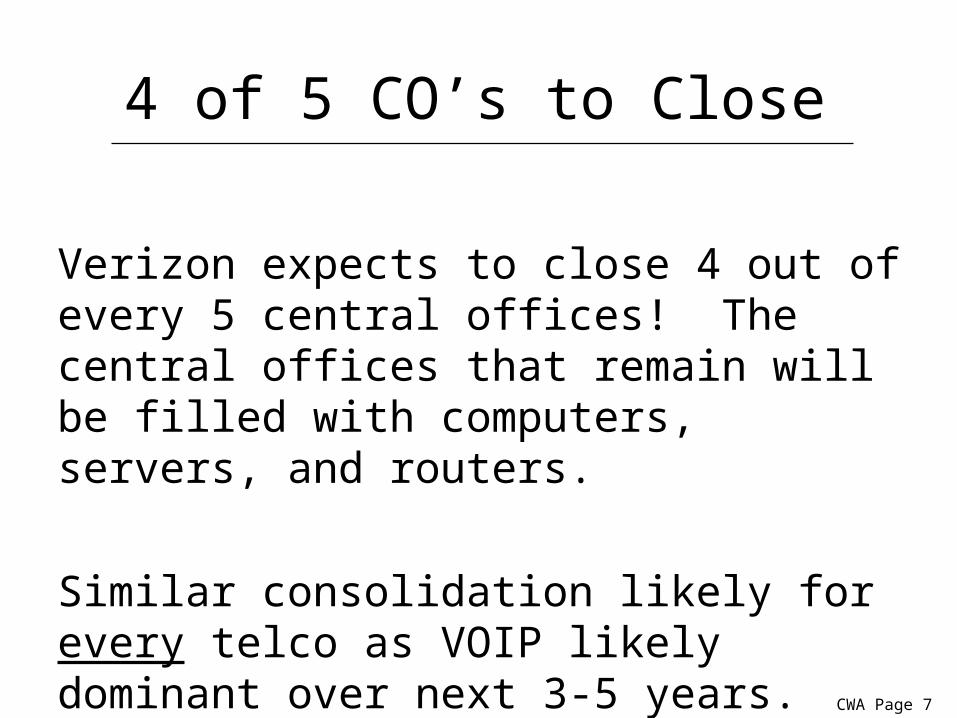

4 of 5 CO’s to Close

Verizon expects to close 4 out of every 5 central offices! The central offices that remain will be filled with computers, servers, and routers.

Similar consolidation likely for every telco as VOIP likely dominant over next 3-5 years.

CWA Page 7

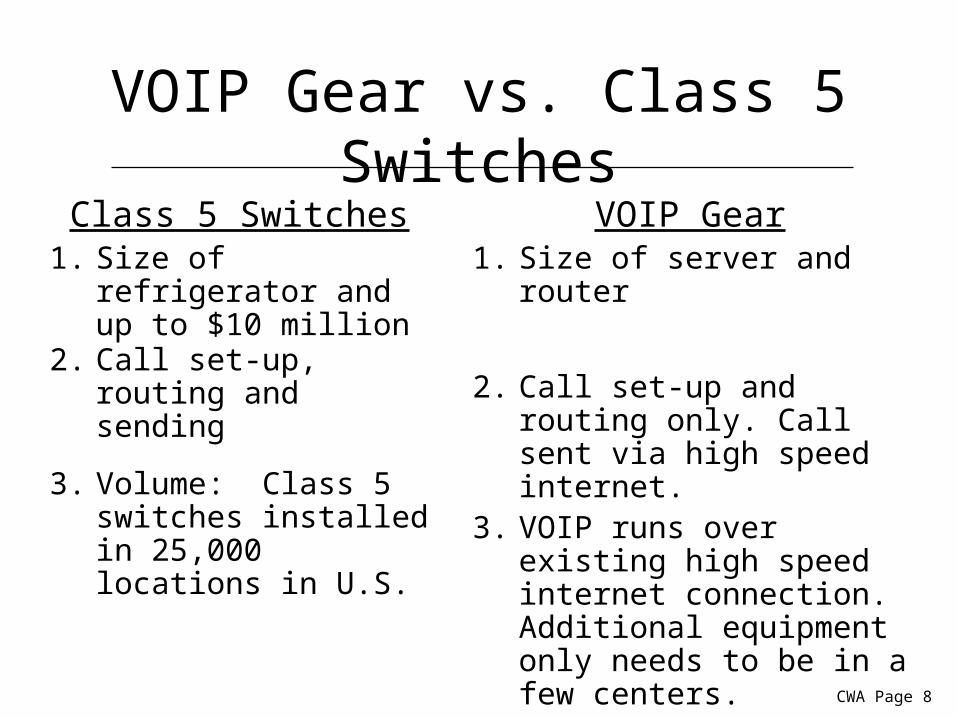

VOIP Gear vs. Class 5 Switches

Class 5 Switches1. Size of refrigerator

and up to $10 million2. Call set-up, routing

and sending

3. Volume: Class 5 switches installed in 25,000 locations in U.S.

VOIP Gear1. Size of server and router

2. Call set-up and routing only. Call sent via high speed internet.

3. VOIP runs over existing high speed internet connection. Additional equipment only needs to be in a few centers.

CWA Page 8

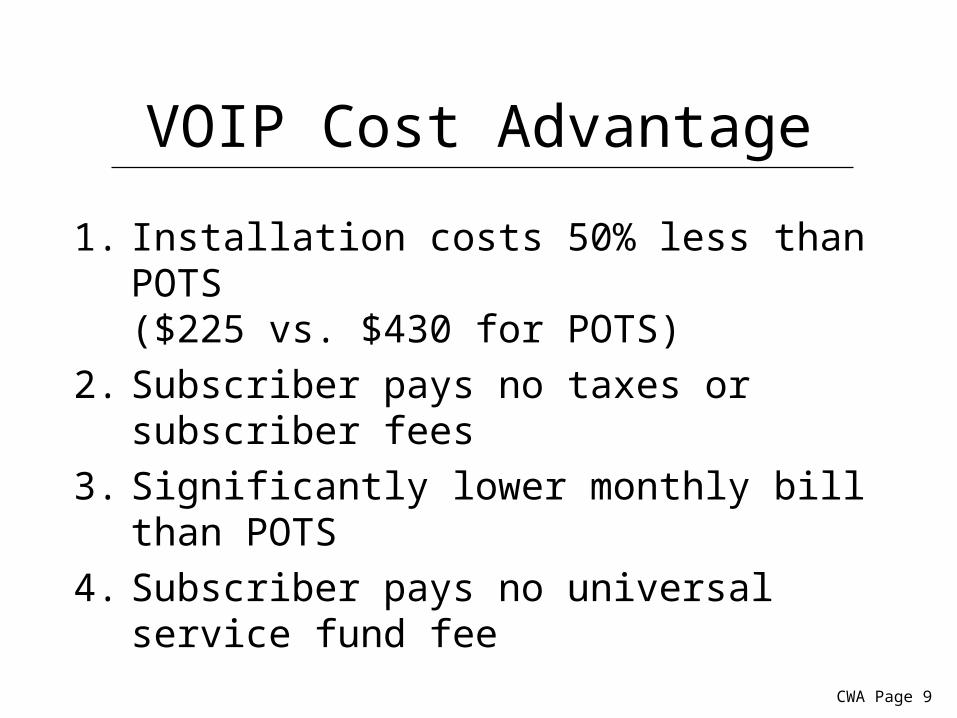

VOIP Cost Advantage

1. Installation costs 50% less than POTS($225 vs. $430 for POTS)

2. Subscriber pays no taxes or subscriber fees

3. Significantly lower monthly bill than POTS

4. Subscriber pays no universal service fund fee

CWA Page 9

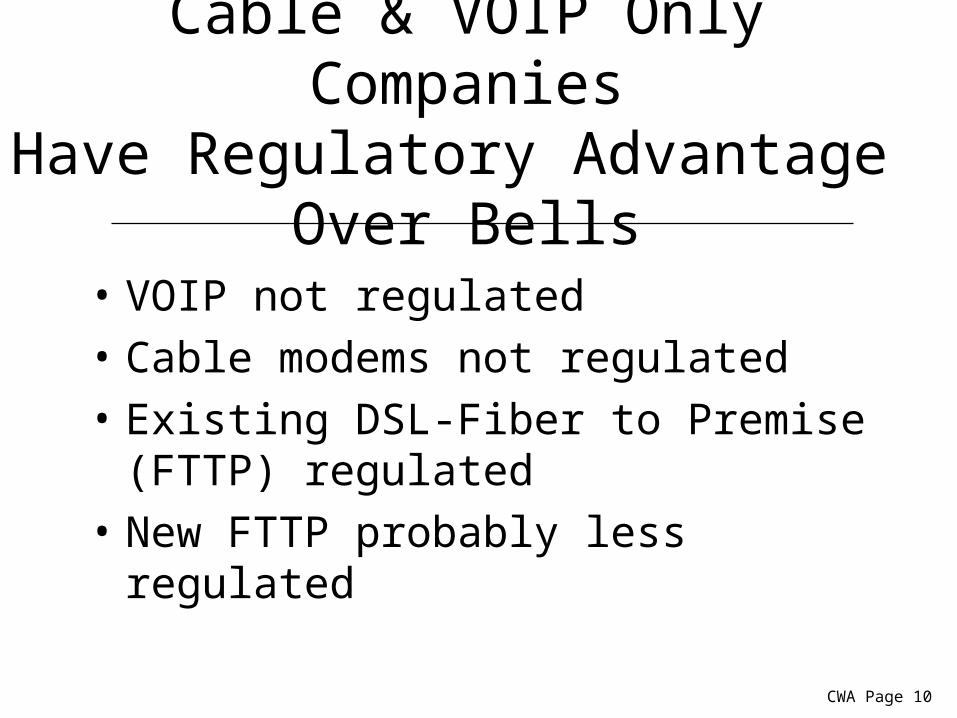

Cable & VOIP Only CompaniesHave Regulatory Advantage

Over Bells

• VOIP not regulated

• Cable modems not regulated

• Existing DSL-Fiber to Premise (FTTP) regulated

• New FTTP probably less regulated

CWA Page 10

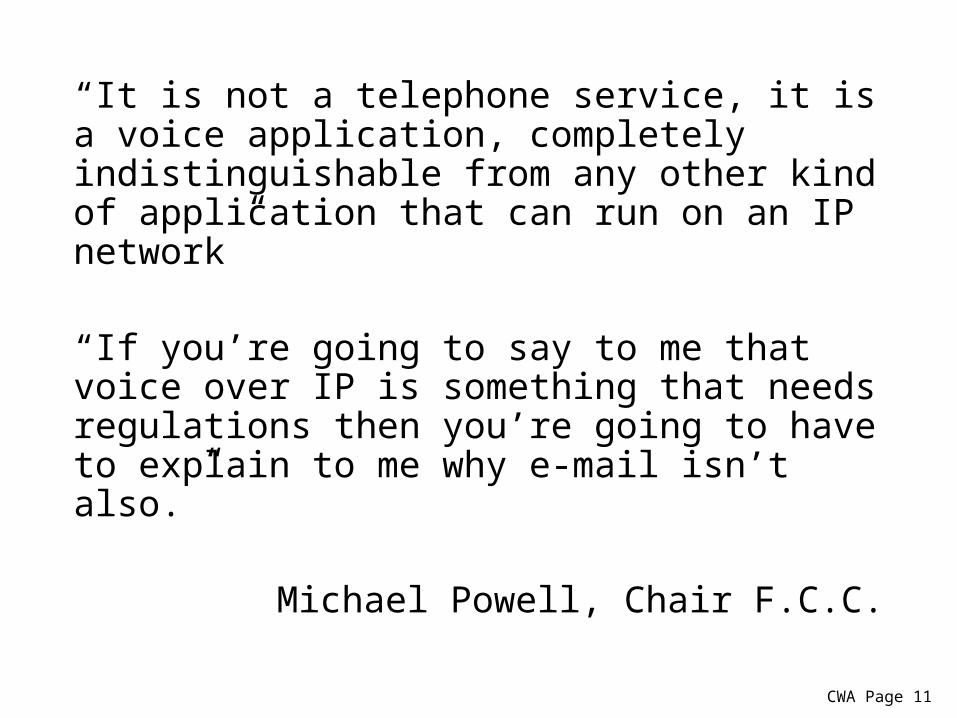

“It is not a telephone service, it is a voice application, completely indistinguishable from any other kind of application that can run on an IP network”

“If you’re going to say to me that voice over IP is something that needs regulations then you’re going to have to explain to me why e-mail isn’t also.”

Michael Powell, Chair F.C.C.

CWA Page 11

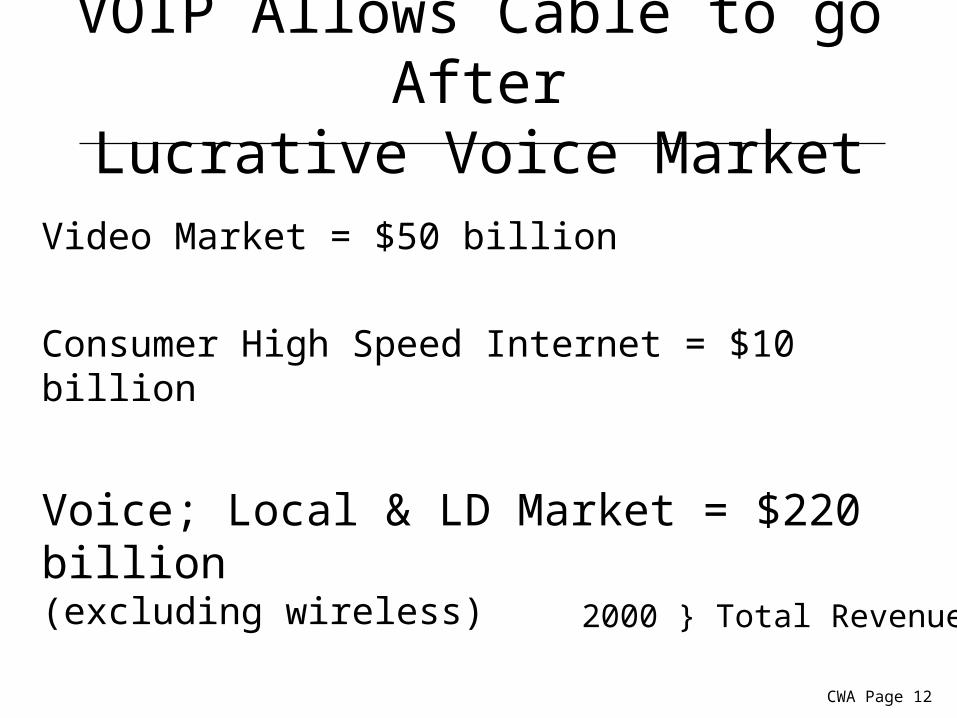

VOIP Allows Cable to go AfterLucrative Voice Market

Video Market = $50 billion

Consumer High Speed Internet = $10 billion

Voice; Local & LD Market = $220 billion(excluding wireless)

2000 } Total Revenue

CWA Page 12

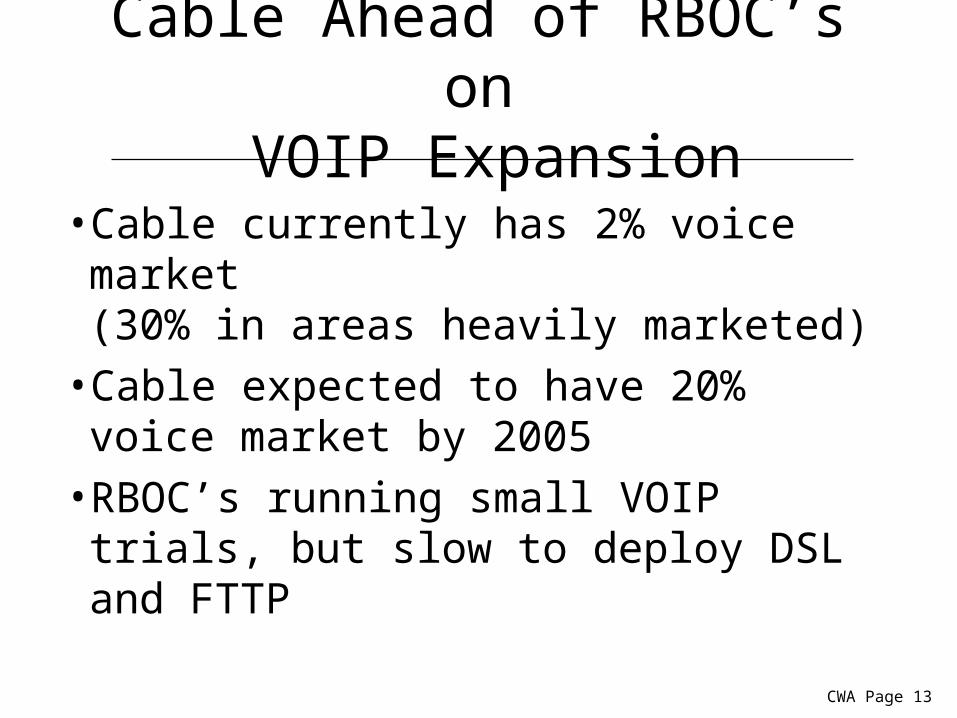

Cable Ahead of RBOC’s on VOIP Expansion

• Cable currently has 2% voice market (30% in areas heavily marketed)

• Cable expected to have 20% voice market by 2005

• RBOC’s running small VOIP trials, but slow to deploy DSL and FTTP

CWA Page 13

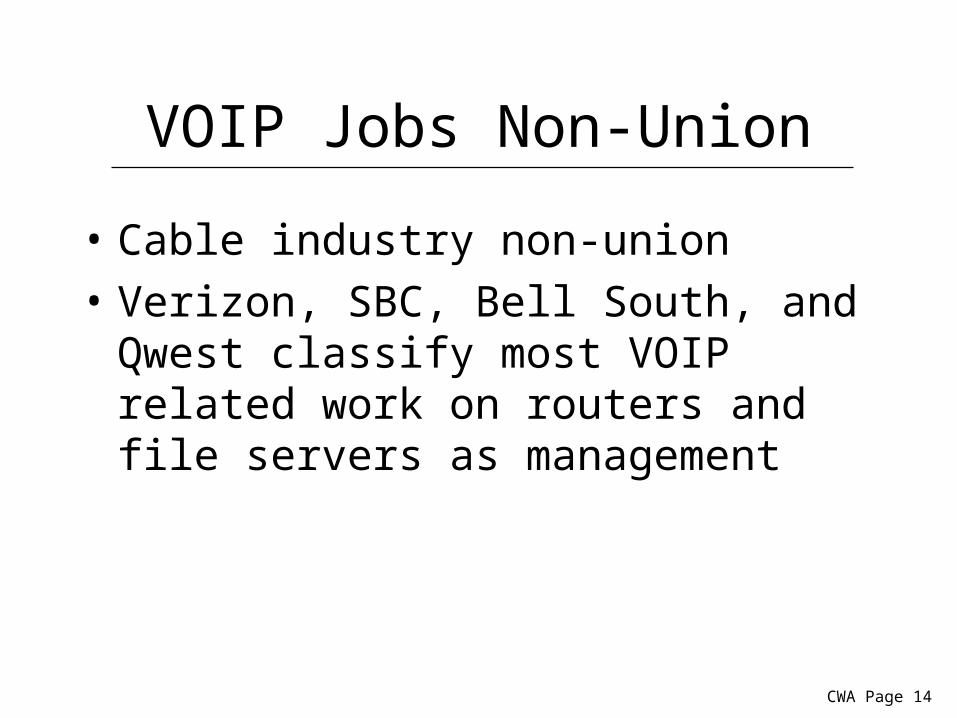

VOIP Jobs Non-Union

• Cable industry non-union

• Verizon, SBC, Bell South, and Qwest classify most VOIP related work on routers and file servers as management

CWA Page 14

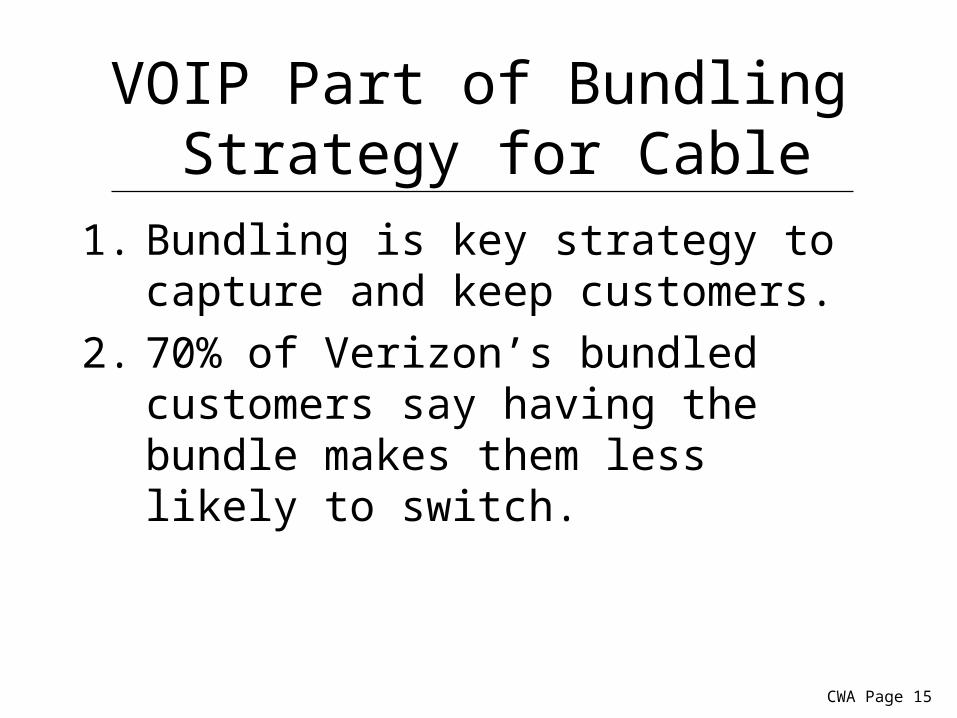

VOIP Part of Bundling Strategy for Cable

1. Bundling is key strategy to capture and keep customers.

2. 70% of Verizon’s bundled customers say having the bundle makes them less likely to switch.

CWA Page 15

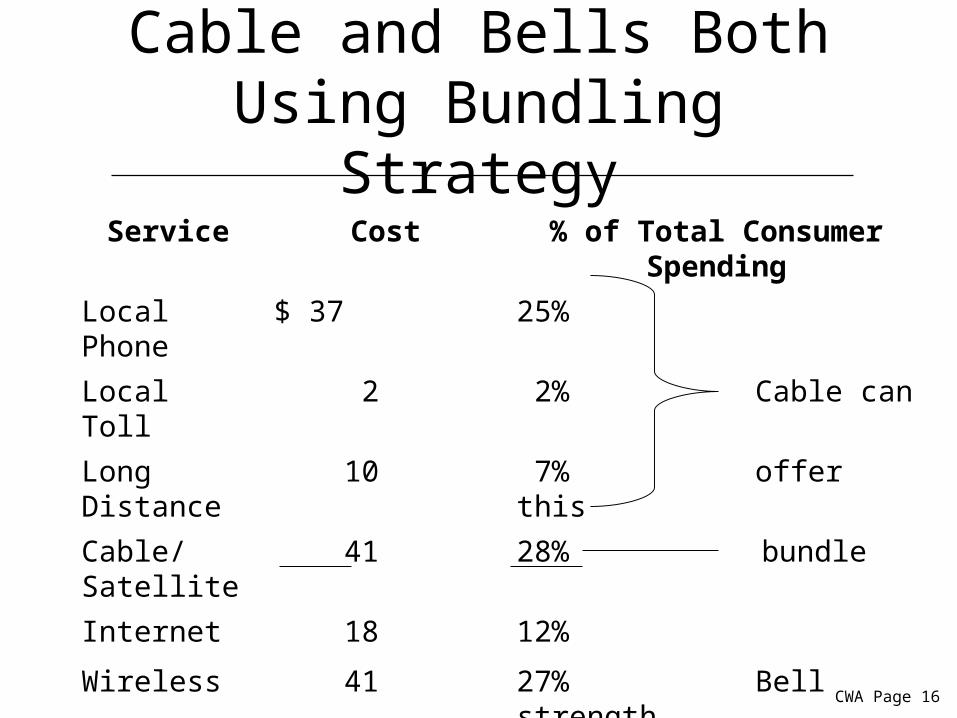

Cable and Bells Both Using Bundling Strategy

Service Cost % of Total Consumer Spending

Local Phone $ 37 25%

Local Toll 2 2% Cable can

Long Distance 10 7% offer this

Cable/Satellite 41 28% bundle

Internet 18 12%

Wireless 41 27% Bell strength

$149

CWA Page 16

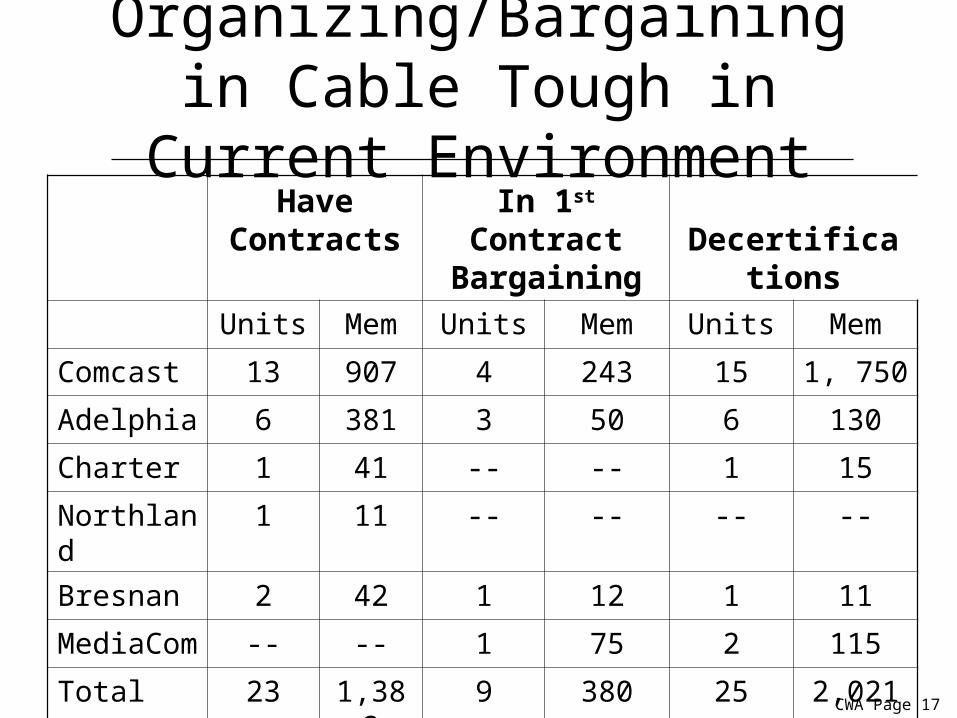

Organizing/Bargaining in Cable Tough in Current Environment

Have Contracts

In 1st Contract Bargaining Decertifications

Units Mem Units Mem Units Mem

Comcast 13 907 4 243 15 1, 750

Adelphia 6 381 3 50 6 130

Charter 1 41 -- -- 1 15

Northland 1 11 -- -- -- --

Bresnan 2 42 1 12 1 11

MediaCom -- -- 1 75 2 115

Total 23 1,382 9 380 25 2,021

CWA Page 17

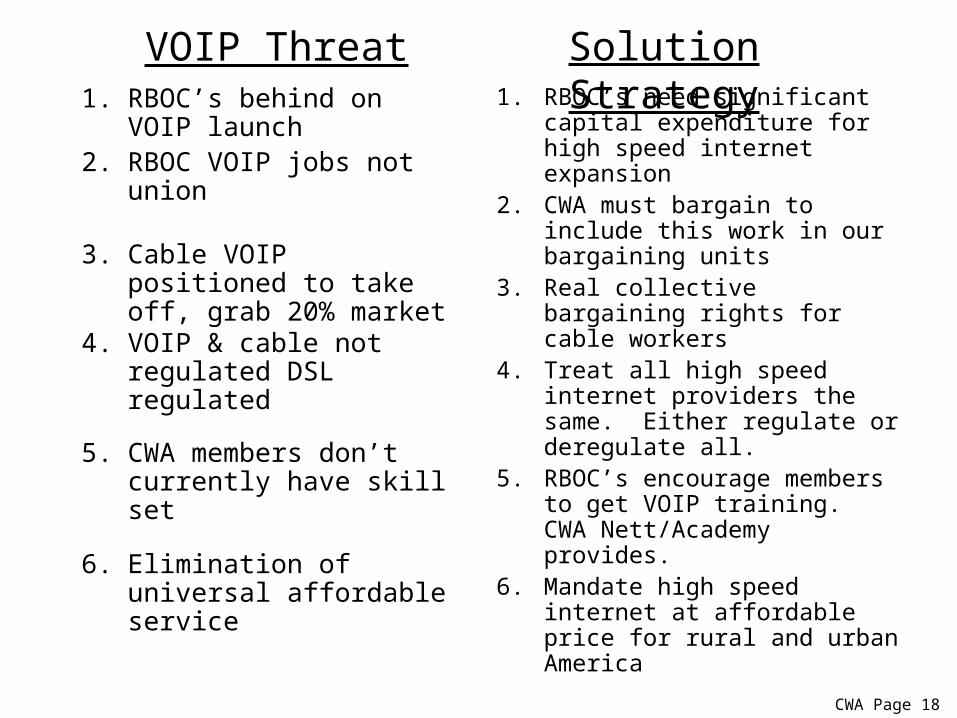

1. RBOC’s behind on VOIP launch

2. RBOC VOIP jobs not union

3. Cable VOIP positioned to take off, grab 20% market

4. VOIP & cable not regulated DSL regulated

5. CWA members don’t currently have skill set

6. Elimination of universal affordable service

1. RBOC’s need significant capital expenditure for high speed internet expansion

2. CWA must bargain to include this work in our bargaining units

3. Real collective bargaining rights for cable workers

4. Treat all high speed internet providers the same. Either regulate or deregulate all.

5. RBOC’s encourage members to get VOIP training. CWA Nett/Academy provides.

6. Mandate high speed internet at affordable price for rural and urban America

VOIP Threat Solution Strategy

CWA Page 18

What Can My Local Do?

• Educate members on VOIP and future nature of jobs

• Fight to make these jobs, at telco’s union job• Fight for a fair regulatory structure in my

state• Fight to keep universal affordable service• Promote CWA/Nett Academy to upgrade

member skills – www.cwanett.org

CWA Page 19