Embed Size (px)

Citation preview

Rice Global E&C Forum – July 11,2014

Rice Global E&C Forum – July 11,2014

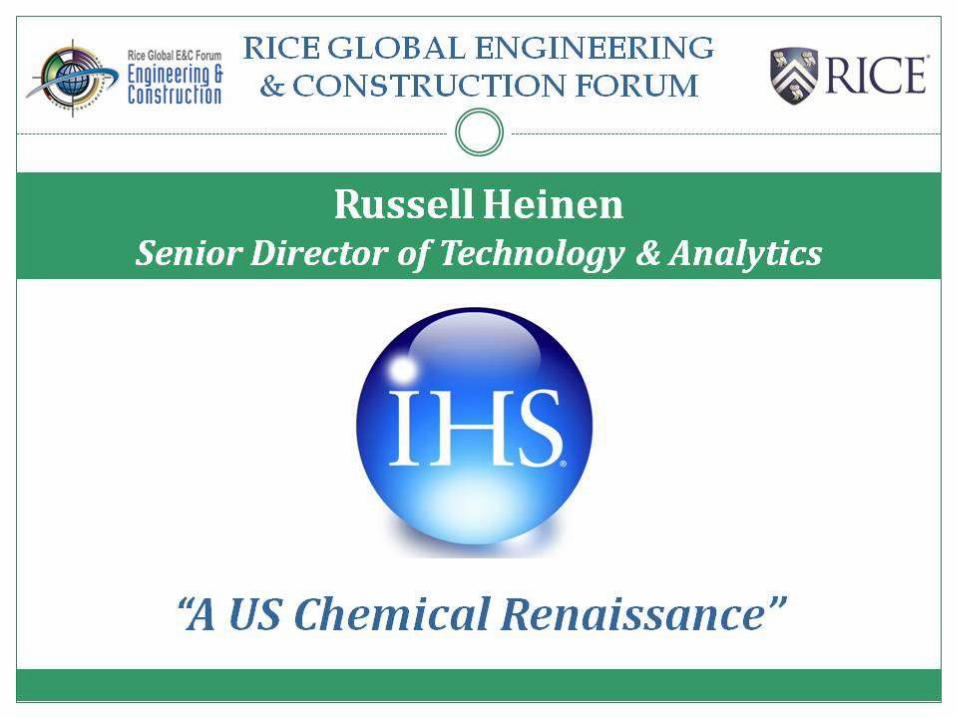

• The Chemical Industry is a key enabler of modern living.

• Investments driven by cost advantage, proximity to demand centers and technology.

• Demand growth driven by penetration of low-cost end-use products aligned with consumer markets.

• Understanding the entire value-chain is essential for long term success.

Chemical Industry Building Blocks

Ethylene Propylene

Benzene Methanol

Chlorine

Rice Global E&C Forum – July 11,2014

• Basic chemicals &

plastics are the

feedstocks for many

consumer goods

• Fundamental economic

growth drives basic

chemical demand

• Sustained global GDP

growth is needed to

support new basic

chemical capacity in the

next five years

Demand for Basic Chemicals Driven

By Durable/Non-durable Goods

The Demand Pull On Chemicals

Starts With Consumers

Energy Derivatives Petrochemicals

Consumers Retail Consumer

Goods

Rice Global E&C Forum – July 11,2014

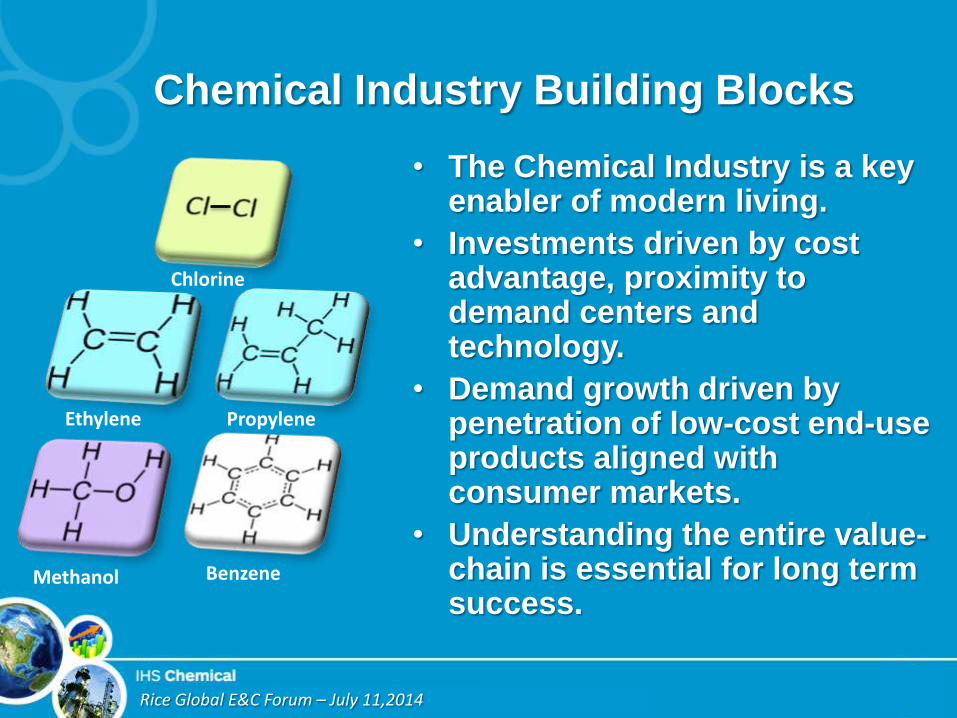

Energy &

Feedstocks …make up 60-70% of the costs of chemical

production. Investments seek a

competitive advantage in energy and feedstock costs.

Demand Growth Proximity to

demand growth essential without

distinct cost or technology

advantage. Trade access is also key.

Technology Technology to

enable competitive production costs,

economies of scale, high performance products. First to

market is important.

Chemical Investments Seek A

Sustainable Advantage

Energy and Hydrocarbon Feedstock Costs:

Key Drivers In Chemicals Manufacturing

Propylene

Ethylene

Butadiene Mixed Butylenes

Methane/Hydrogen

Benzene Toluene

Xylene

Propylene

Methanol

Naphtha

Gas Oil

Condensate

Propane

Ethane

Butane

Pygas Benzene

Toluene/Xylene

Heavy Aromatics

C5/C6 Non Aromatics

Fuel Oil

Ethylene

Unit

Gas Processing

Unit

REFORMER BTX Extraction

Raffinate FCC

Refinery

Steam

Reformer Methanol

Synthesis

SynGas

Gasifier

Gas

Coal

Rice Global E&C Forum – July 11,2014

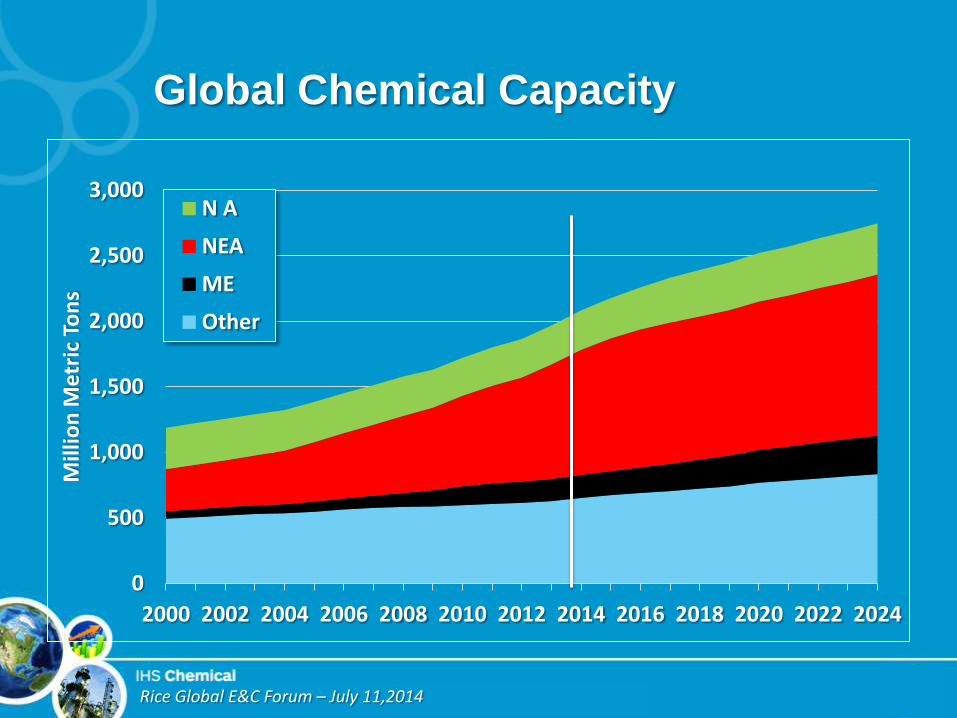

Global Chemical Capacity

0

500

1,000

1,500

2,000

2,500

3,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Mill

ion

Met

ric

Ton

s

N A

NEA

ME

Other

Rice Global E&C Forum – July 11,2014

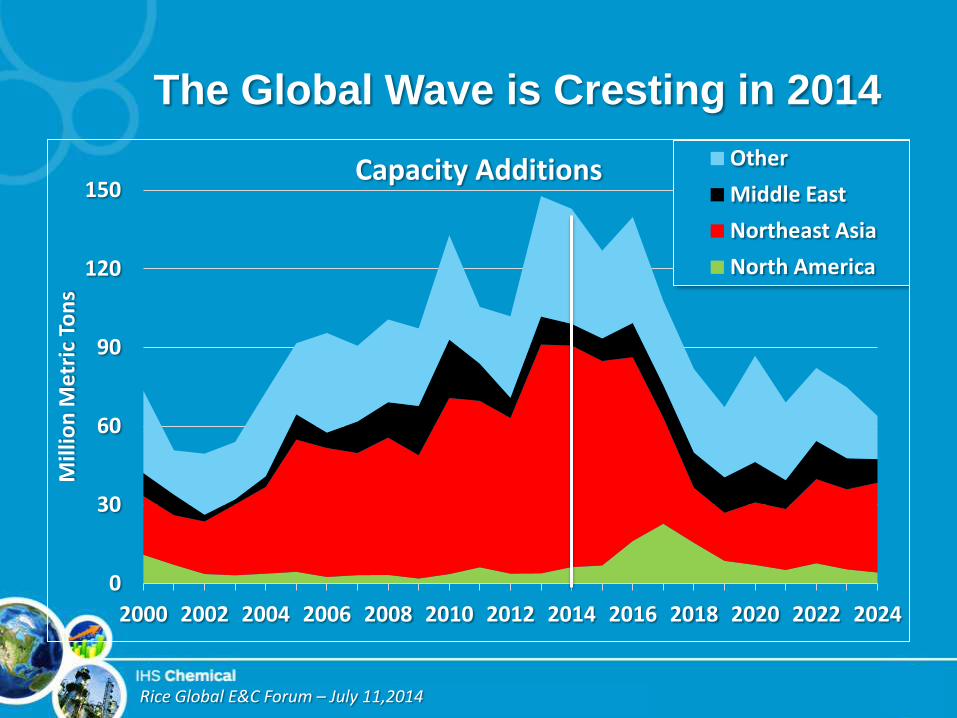

The Global Wave is Cresting in 2014

0

30

60

90

120

150

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Mill

ion

Met

ric

Ton

s

Capacity Additions Other

Middle East

Northeast Asia

North America

Rice Global E&C Forum – July 11,2014

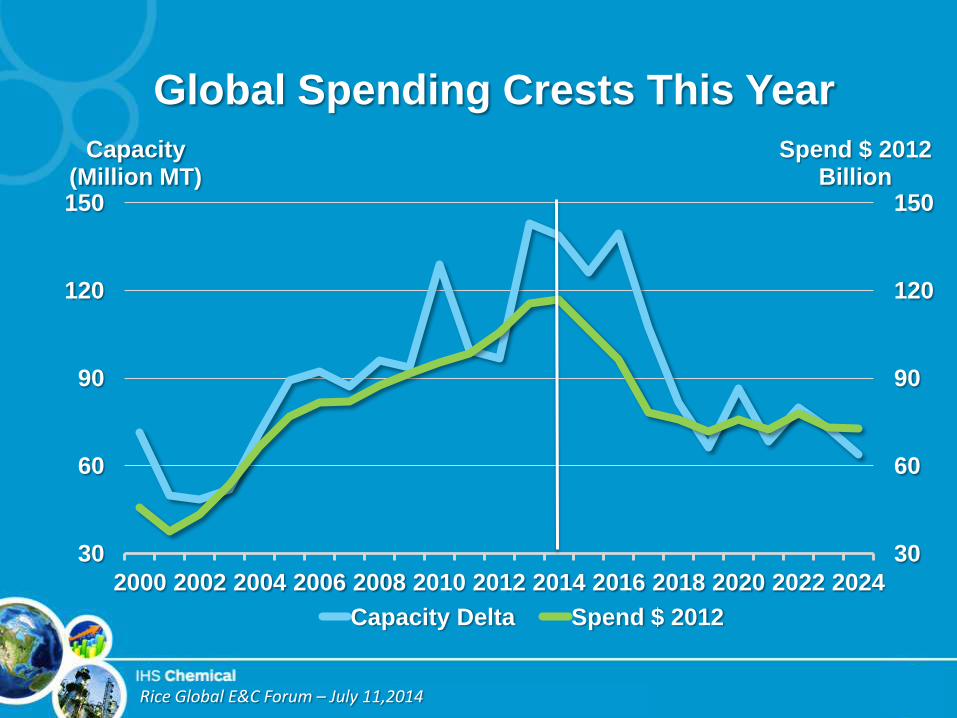

Global Spending Crests This Year

30

60

90

120

150

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Capacity (Million MT)

Capacity Delta

Rice Global E&C Forum – July 11,2014

Global Spending Crests This Year

30

60

90

120

150

30

60

90

120

150

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Spend $ 2012 Billion

Capacity (Million MT)

Capacity Delta Spend $ 2012

Rice Global E&C Forum – July 11,2014

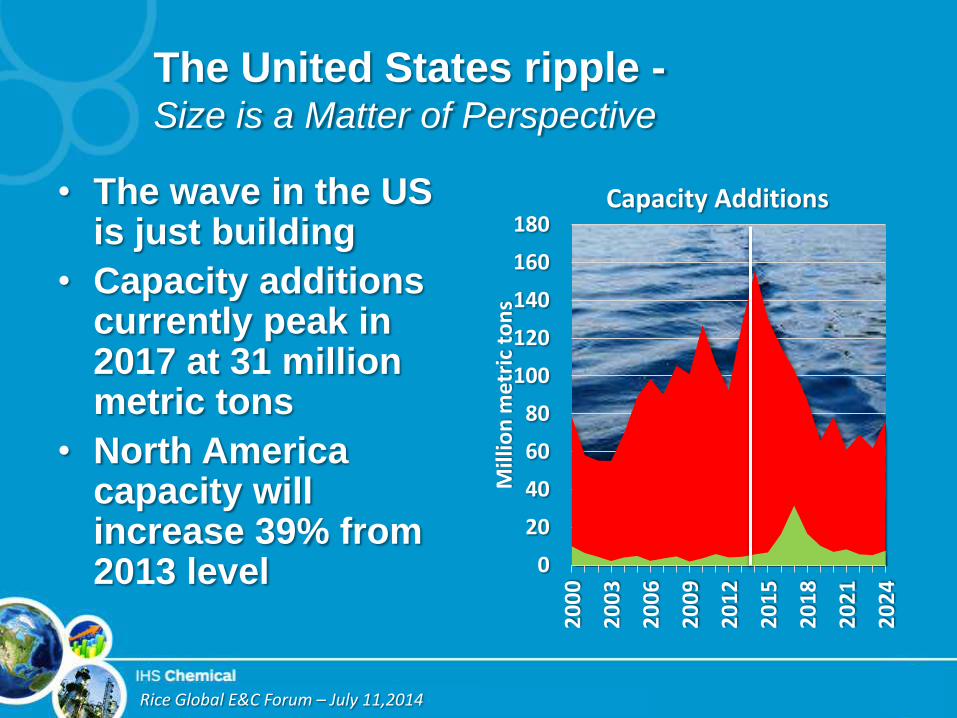

The United States ripple - Size is a Matter of Perspective

0

20

40

60

80

100

120

140

160

180

20

00

20

03

20

06

20

09

20

12

20

15

20

18

20

21

20

24

Mill

ion

me

tric

to

ns

Capacity Additions • The wave in the US is just building

• Capacity additions currently peak in 2017 at 31 million metric tons

• North America capacity will increase 39% from 2013 level

Rice Global E&C Forum – July 11,2014

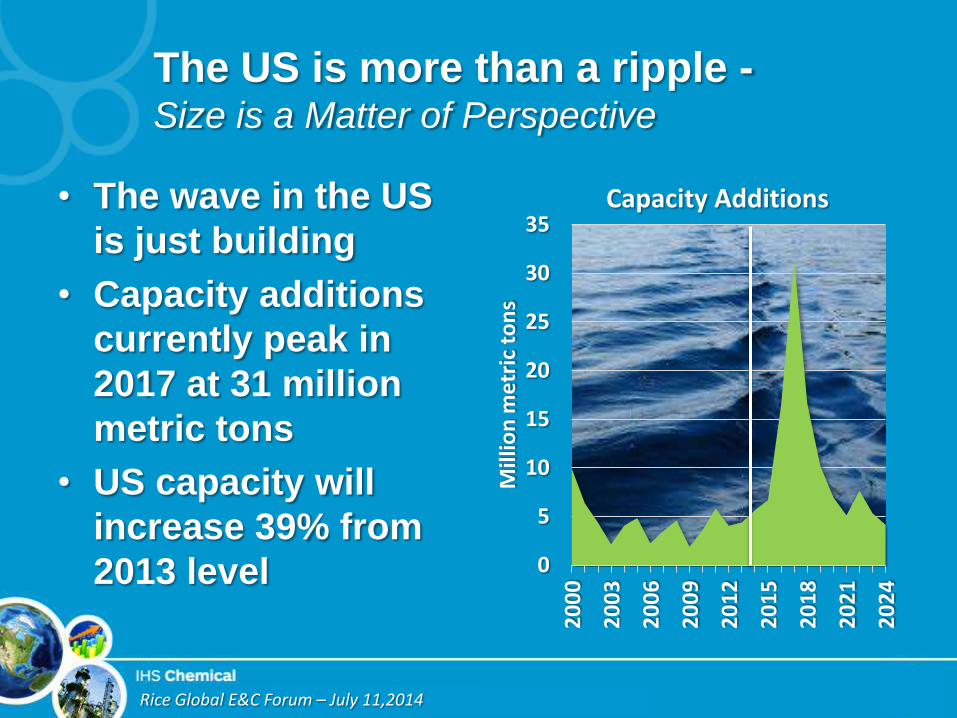

The US is more than a ripple - Size is a Matter of Perspective

0

5

10

15

20

25

30

35

20

00

20

03

20

06

20

09

20

12

20

15

20

18

20

21

20

24

Mill

ion

me

tric

to

ns

Capacity Additions • The wave in the US

is just building

• Capacity additions

currently peak in

2017 at 31 million

metric tons

• US capacity will

increase 39% from

2013 level

Rice Global E&C Forum – July 11,2014

North America: Riding the Wave

• Watching the wave

build

• Are there enough

trained surfers?

• Surf board availability

– Made in China?

• Stingrays, jellyfish and

storms

Rice Global E&C Forum – July 11,2014

North America: Riding the Wave

• Watching the wave

build

• Are there enough

trained surfers?

• Surf board availability

– Made in China?

• Stingrays, jellyfish and

storms

Rice Global E&C Forum – July 11,2014

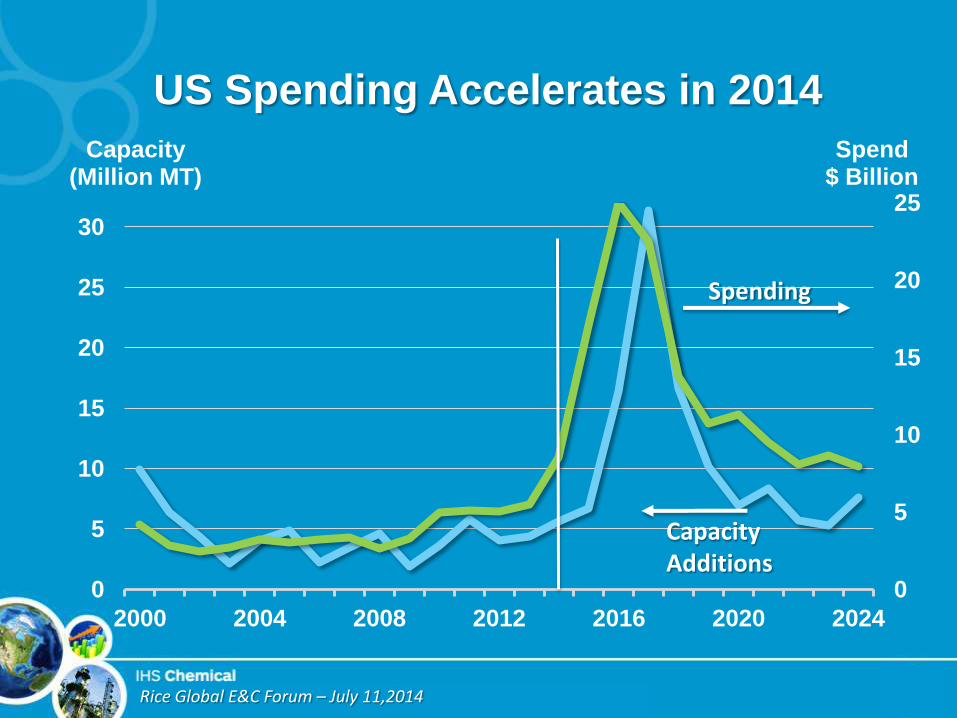

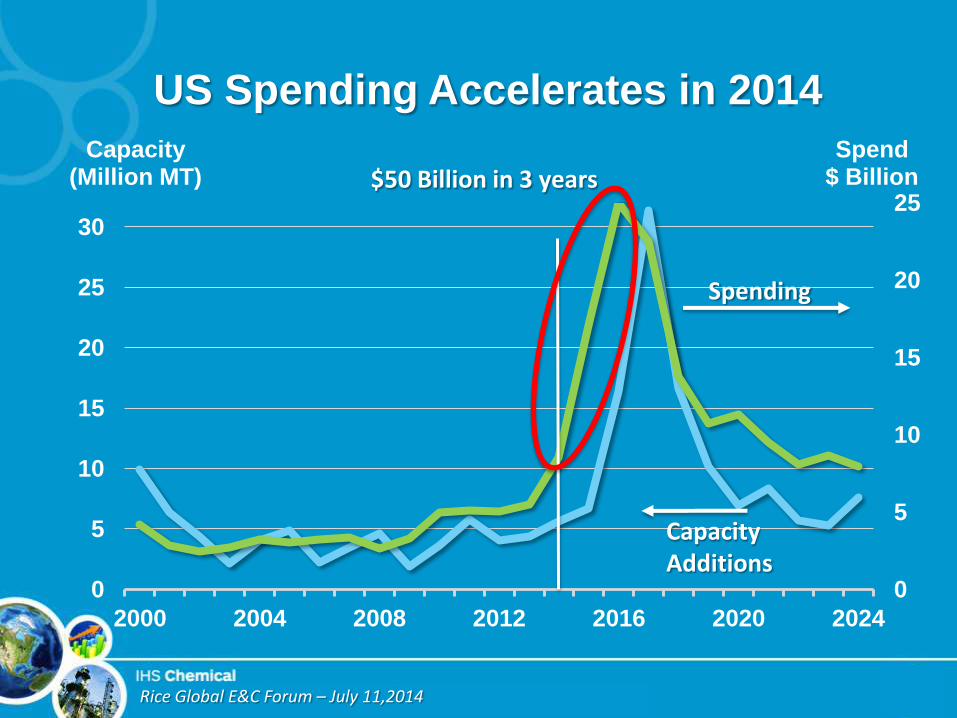

US Spending Accelerates in 2014

0

5

10

15

20

25

0

5

10

15

20

25

30

2000 2004 2008 2012 2016 2020 2024

Spend $ Billion

Capacity (Million MT)

Capacity Additions

Spending

Rice Global E&C Forum – July 11,2014

US Spending Accelerates in 2014

0

5

10

15

20

25

0

5

10

15

20

25

30

2000 2004 2008 2012 2016 2020 2024

Spend $ Billion

Capacity (Million MT)

Capacity Additions

Spending

$50 Billion in 3 years

Rice Global E&C Forum – July 11,2014

Why is this happening?

….Fracking

-

2

4

6

8

10

12

14

16

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

$/M

M B

tu

US Oil & Gas Prices

0

5

10

15

20

25

30

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

TCF

US Natural Gas Production

Rice Global E&C Forum – July 11,2014

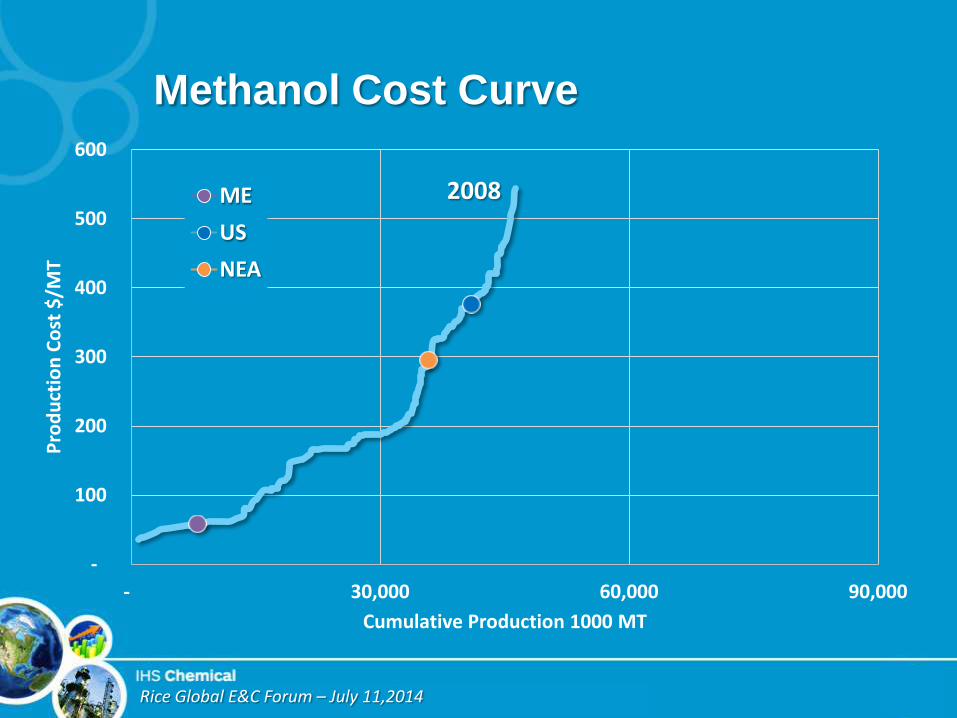

Methanol Cost Curve

-

100

200

300

400

500

600

- 30,000 60,000 90,000

Pro

du

ctio

n C

ost

$/M

T

Cumulative Production 1000 MT

ME

US

NEA

2008

Rice Global E&C Forum – July 11,2014

Methanol Cost Curve

-

100

200

300

400

500

600

- 30,000 60,000 90,000

Pro

du

ctio

n C

ost

$/M

T

Cumulative Production 1000 MT

ME

US

NEA

2008 2014

Rice Global E&C Forum – July 11,2014

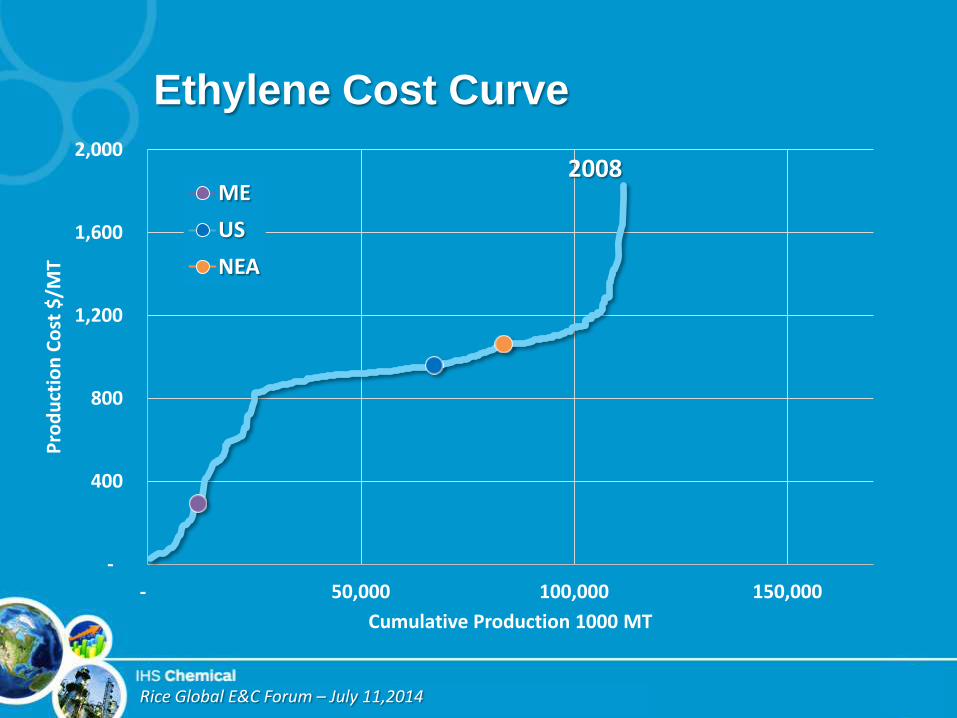

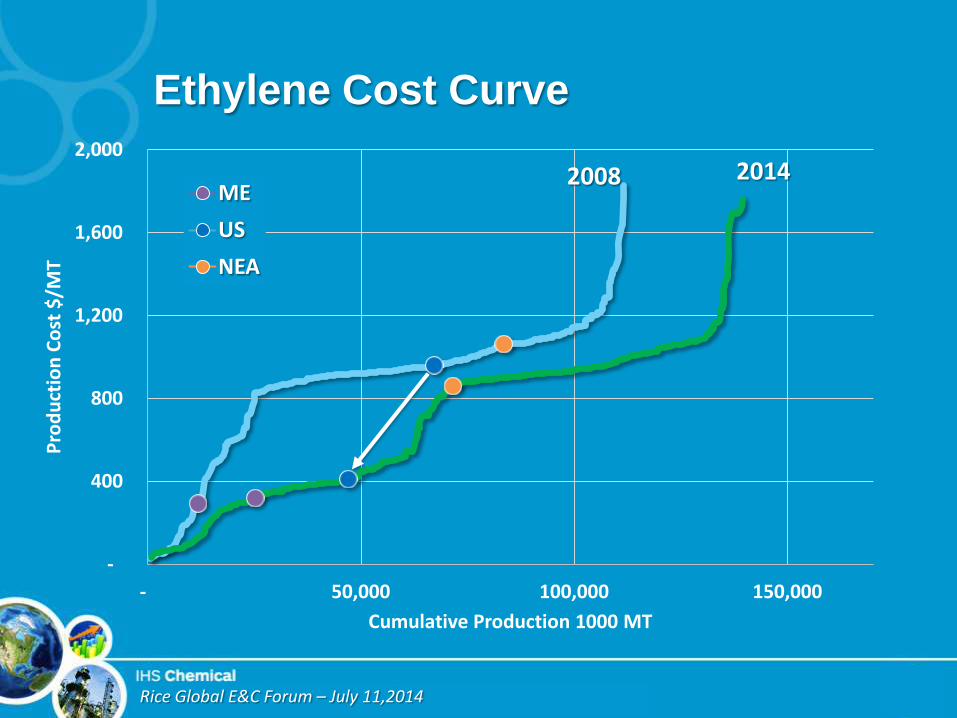

Ethylene Cost Curve

-

400

800

1,200

1,600

2,000

- 50,000 100,000 150,000

Pro

du

ctio

n C

ost

$/M

T

Cumulative Production 1000 MT

ME

US

NEA

2008

Rice Global E&C Forum – July 11,2014

Ethylene Cost Curve

-

400

800

1,200

1,600

2,000

- 50,000 100,000 150,000

Pro

du

ctio

n C

ost

$/M

T

Cumulative Production 1000 MT

ME

US

NEA

2008 2014

Rice Global E&C Forum – July 11,2014

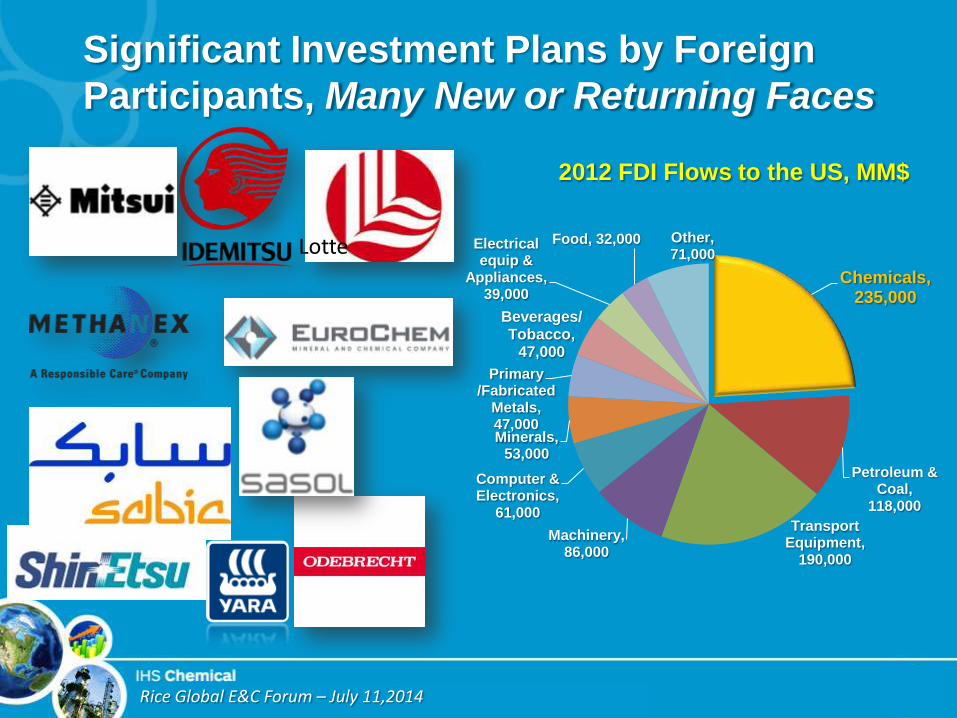

Significant Investment Plans by Foreign

Participants, Many New or Returning Faces

2012 FDI Flows to the US, MM$

Lotte Chemicals,

235,000

Petroleum & Coal,

118,000

Transport Equipment,

190,000

Machinery, 86,000

Computer & Electronics,

61,000

Minerals, 53,000

Primary /Fabricated

Metals, 47,000

Beverages/Tobacco,

47,000

Electrical equip &

Appliances, 39,000

Food, 32,000 Other, 71,000

Rice Global E&C Forum – July 11,2014

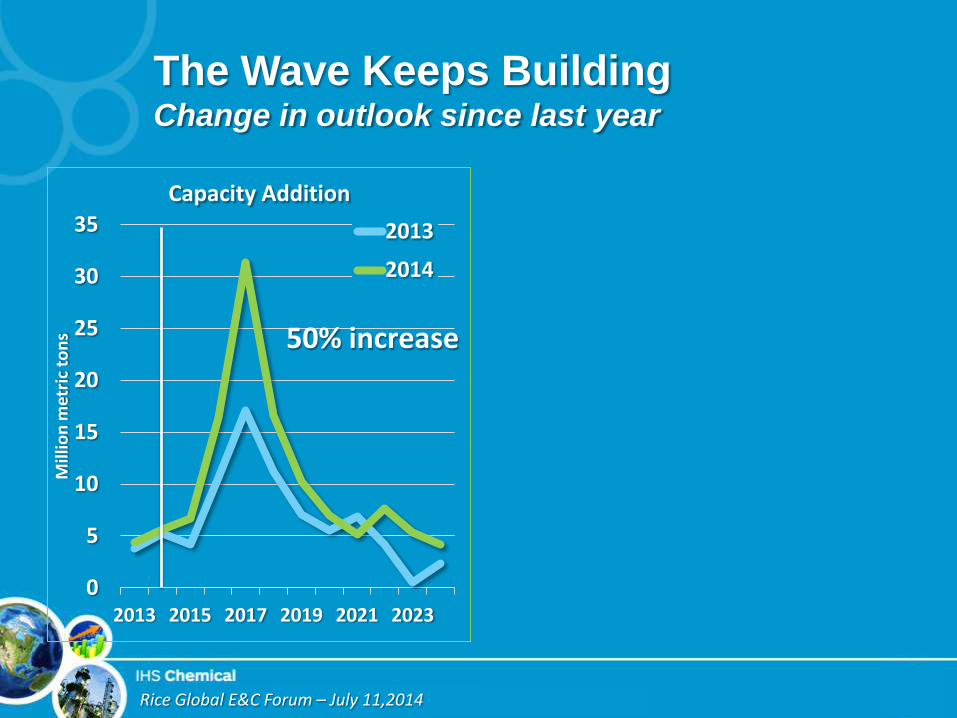

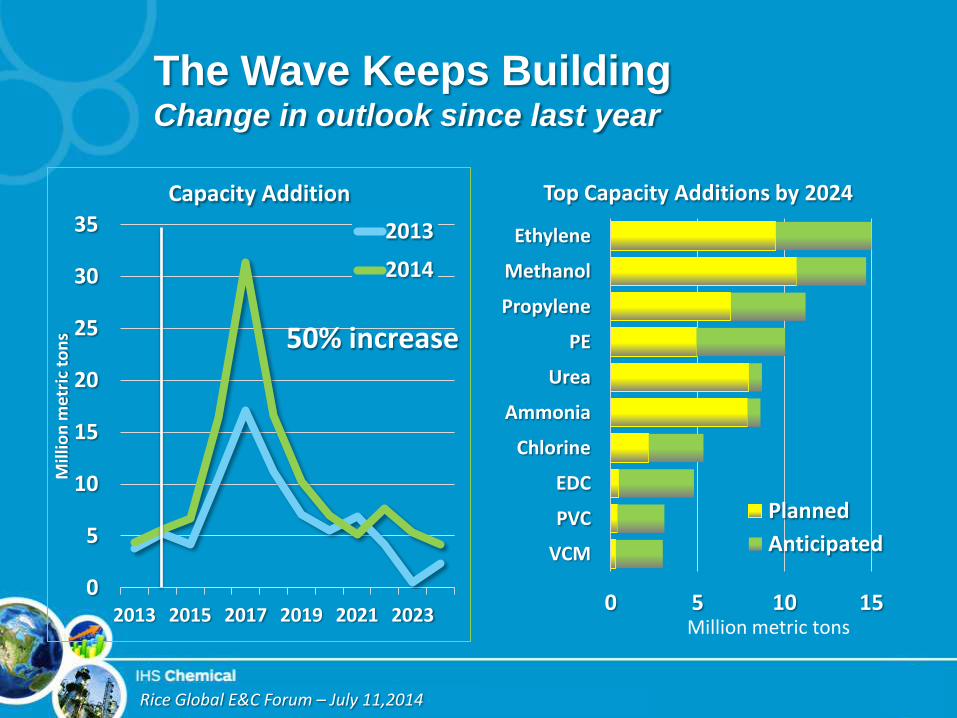

The Wave Keeps Building Change in outlook since last year

0

5

10

15

20

25

30

35

2013 2015 2017 2019 2021 2023

Mill

ion

met

ric

ton

s

Capacity Addition

2013

2014

50% increase

Rice Global E&C Forum – July 11,2014

The Wave Keeps Building Change in outlook since last year

0

5

10

15

20

25

30

35

2013 2015 2017 2019 2021 2023

Mill

ion

met

ric

ton

s

Capacity Addition

2013

2014

50% increase

0 5 10 15

VCM

PVC

EDC

Chlorine

Ammonia

Urea

PE

Propylene

Methanol

Ethylene

Million metric tons

Top Capacity Additions by 2024

Planned

Anticipated

Rice Global E&C Forum – July 11,2014

The Wave Crests in 2017 but…

• New players continue to enter the water

• Others remain on shore waiting to see how

good the surf is

• Feedstock availability continues to expand

keeping pricing attractive

• This wave has the potential to keep building

Rice Global E&C Forum – July 11,2014

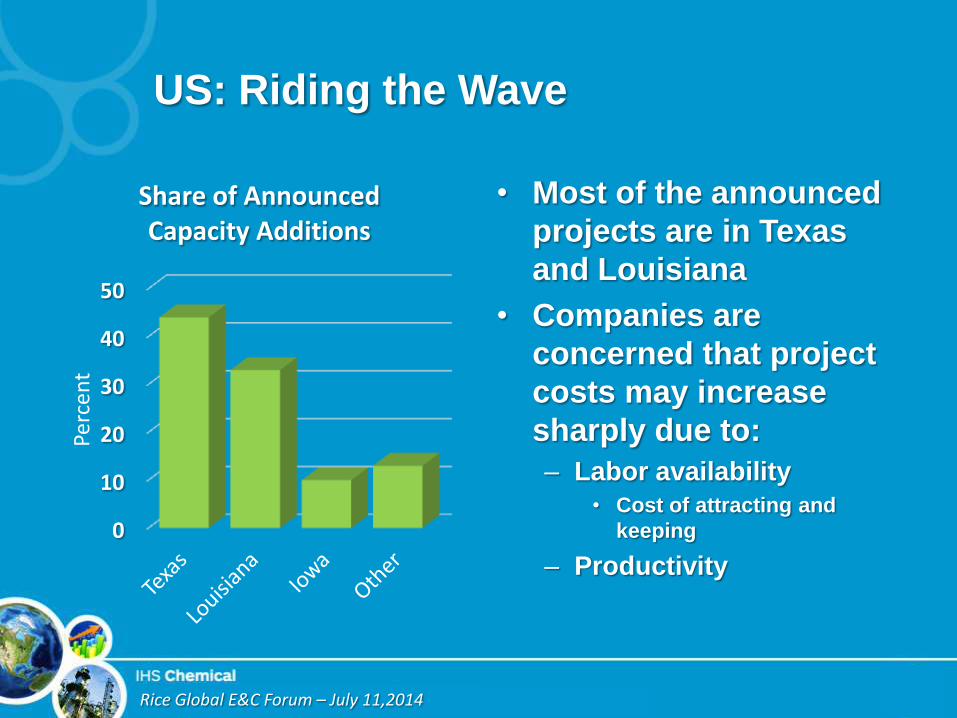

US: Riding the Wave

• Most of the announced

projects are in Texas

and Louisiana

• Companies are

concerned that project

costs may increase

sharply due to:

– Labor availability

• Cost of attracting and

keeping

– Productivity

0

10

20

30

40

50

Perc

ent

Share of Announced Capacity Additions

Rice Global E&C Forum – July 11,2014

A Self-fulfilling Prophesy?

• Costs remain a major

growing concern

• Most announcements

seem to include

healthy escalations as

a result

• Are expectations

driving cost?

Rice Global E&C Forum – July 11,2014

North America: Riding the Wave

• Watching the wave

build

• Are there enough

trained surfers?

• Surf board availability

– Made in China?

• Stingrays, jellyfish and

storms

Rice Global E&C Forum – July 11,2014

Calling All Surfers

• Labor is the major

concern

– Engineering

– Skilled

– Unskilled

Rice Global E&C Forum – July 11,2014

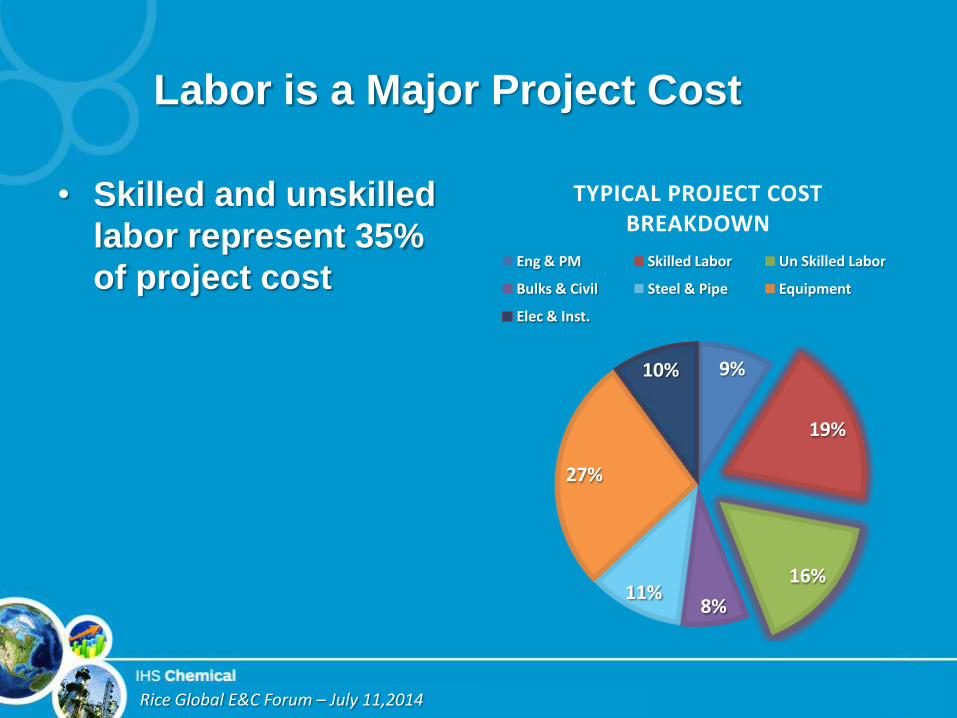

Labor is a Major Project Cost

• Skilled and unskilled

labor represent 35%

of project cost

9%

19%

16%

8% 11%

27%

10%

TYPICAL PROJECT COST BREAKDOWN

Eng & PM Skilled Labor Un Skilled Labor

Bulks & Civil Steel & Pipe Equipment

Elec & Inst.

Rice Global E&C Forum – July 11,2014

Labor is a Major Project Cost

• Skilled and unskilled

labor represent 35%

of project cost

• Add engineering and

project management

total labor related

costs total 46%

• Based on this it is

easy to see why this

is a major concern

9%

19%

16%

8% 11%

27%

10%

TYPICAL PROJECT COST BREAKDOWN

Eng & PM Skilled Labor Un Skilled Labor

Bulks & Civil Steel & Pipe Equipment

Elec & Inst.

Rice Global E&C Forum – July 11,2014

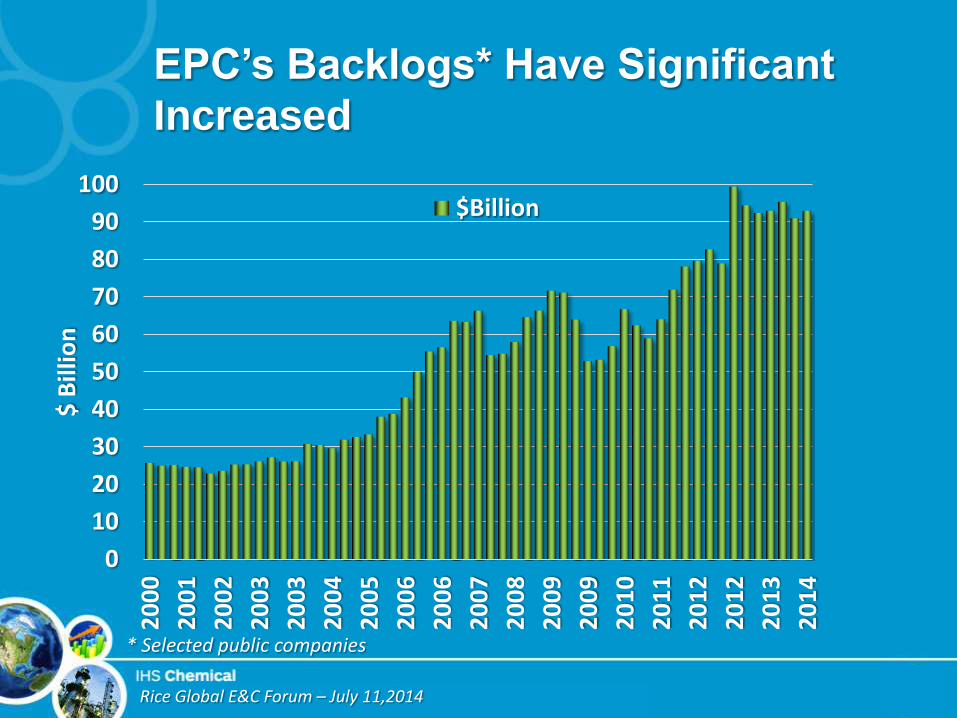

EPC’s Backlogs* Have Significant

Increased

0

10

20

30

40

50

60

70

80

90

100

20

00

20

01

20

02

20

03

20

03

20

04

20

05

20

06

20

06

20

07

20

08

20

09

20

09

20

10

20

11

20

12

20

12

20

13

20

14

$ B

illio

n

$Billion

* Selected public companies

Rice Global E&C Forum – July 11,2014

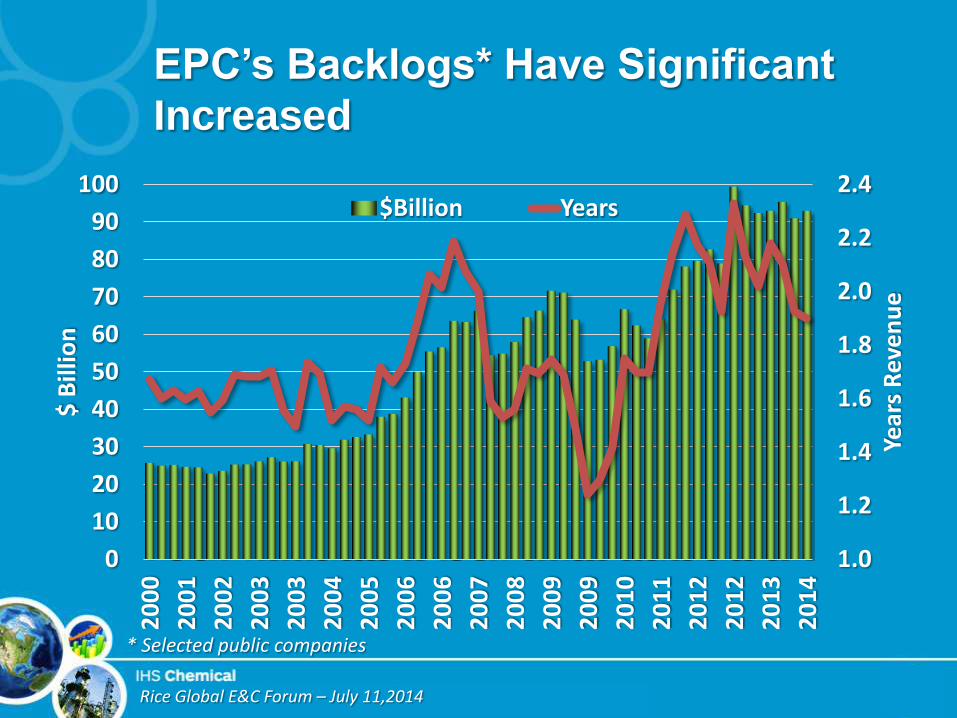

EPC’s Backlogs* Have Significant

Increased

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

0

10

20

30

40

50

60

70

80

90

100

20

00

20

01

20

02

20

03

20

03

20

04

20

05

20

06

20

06

20

07

20

08

20

09

20

09

20

10

20

11

20

12

20

12

20

13

20

14

Year

s R

eve

nu

e

$ B

illio

n

$Billion Years

* Selected public companies

Rice Global E&C Forum – July 11,2014

Skilled Labor is a Major Concern

• Key concerns

– Project foremen

– Welders

– Pipefitters

– Electricians

• Rates are rising

• Companies are being

proactive

• Higher rates encourage

relocations 0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Ind

ex 2

00

5 =

1.0

USGC Skilled Labor Index Welders Pipefitters Electricians

Rice Global E&C Forum – July 11,2014

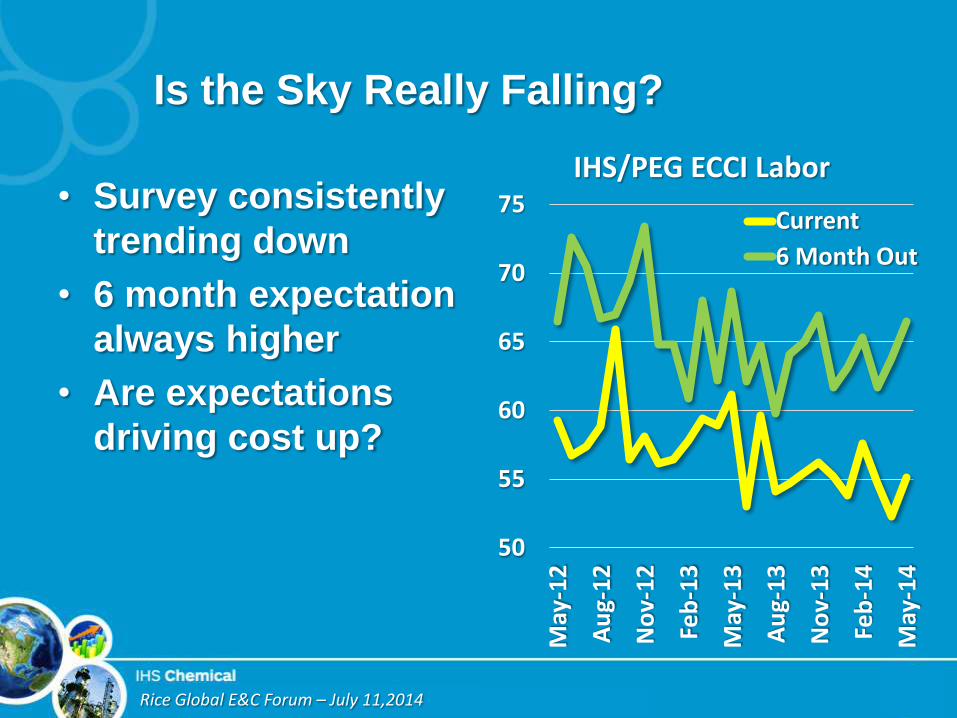

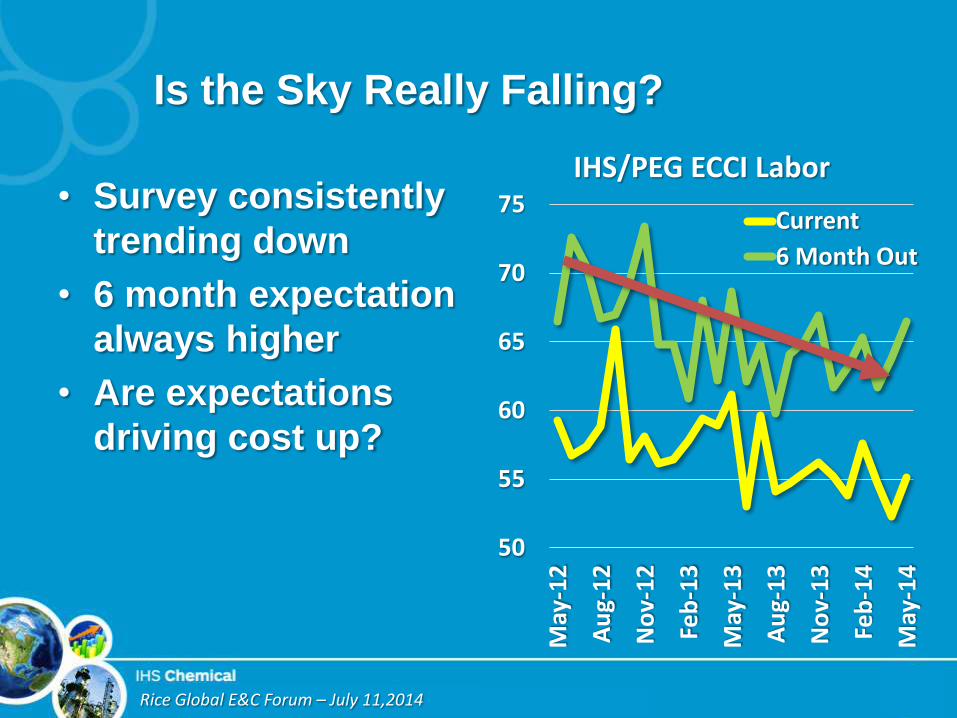

Is the Sky Really Falling?

• Survey consistently

trending down

• 6 month expectation

always higher

• Are expectations

driving cost up?

50

55

60

65

70

75

May

-12

Au

g-1

2

No

v-1

2

Feb

-13

May

-13

Au

g-1

3

No

v-1

3

Feb

-14

May

-14

IHS/PEG ECCI Labor

Current

6 Month Out

Rice Global E&C Forum – July 11,2014

Is the Sky Really Falling?

• Survey consistently

trending down

• 6 month expectation

always higher

• Are expectations

driving cost up?

50

55

60

65

70

75

May

-12

Au

g-1

2

No

v-1

2

Feb

-13

May

-13

Au

g-1

3

No

v-1

3

Feb

-14

May

-14

IHS/PEG ECCI Labor

Current

6 Month Out

Rice Global E&C Forum – July 11,2014

Other Labor Costs

• To attract and retain

workers companies

are also providing:

– Good dining facilities

– Per-diems

– Retention bonuses

– On-site smoking

areas

• Productivity issues

Rice Global E&C Forum – July 11,2014

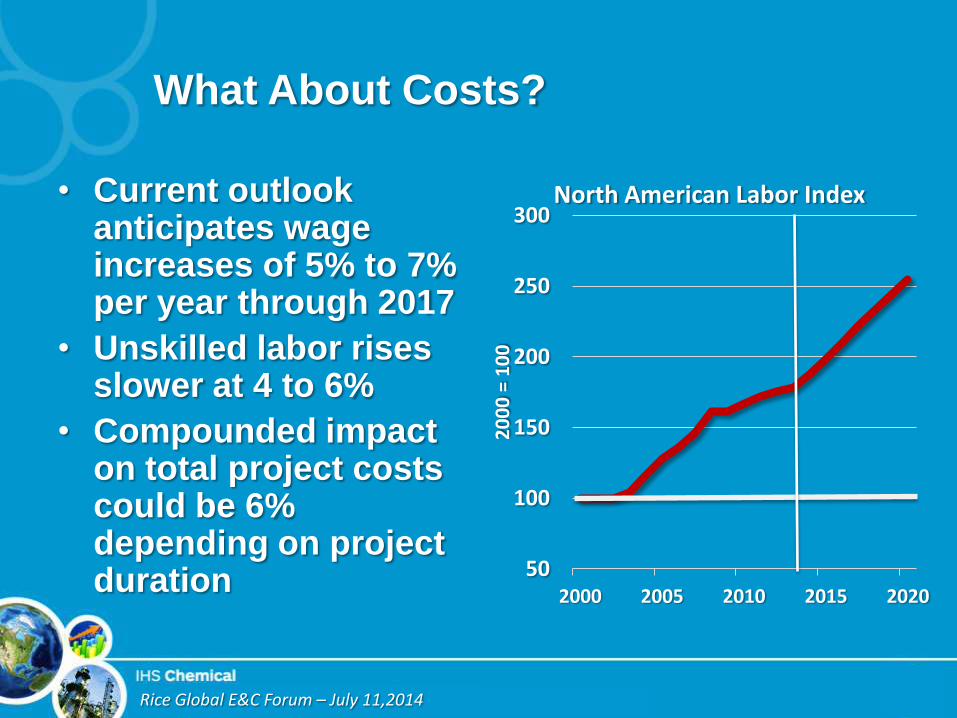

What About Costs?

• Current outlook anticipates wage increases of 5% to 7% per year through 2017

• Unskilled labor rises slower at 4 to 6%

• Compounded impact on total project costs could be 6% depending on project duration

50

100

150

200

250

300

2000 2005 2010 2015 2020

20

00

= 1

00

North American Labor Index

Rice Global E&C Forum – July 11,2014

North America: Riding the Wave

• Watching the wave

build

• Are there enough

trained surfers?

• Surf board availability

– Made in China?

• Stingrays, jellyfish and

storms

Rice Global E&C Forum – July 11,2014

Getting the Right Board When You

Need It

• Major concerns

– Lead times on major

items

– Some equipment has

limited suppliers

– Will metal prices

remain in check

Rice Global E&C Forum – July 11,2014

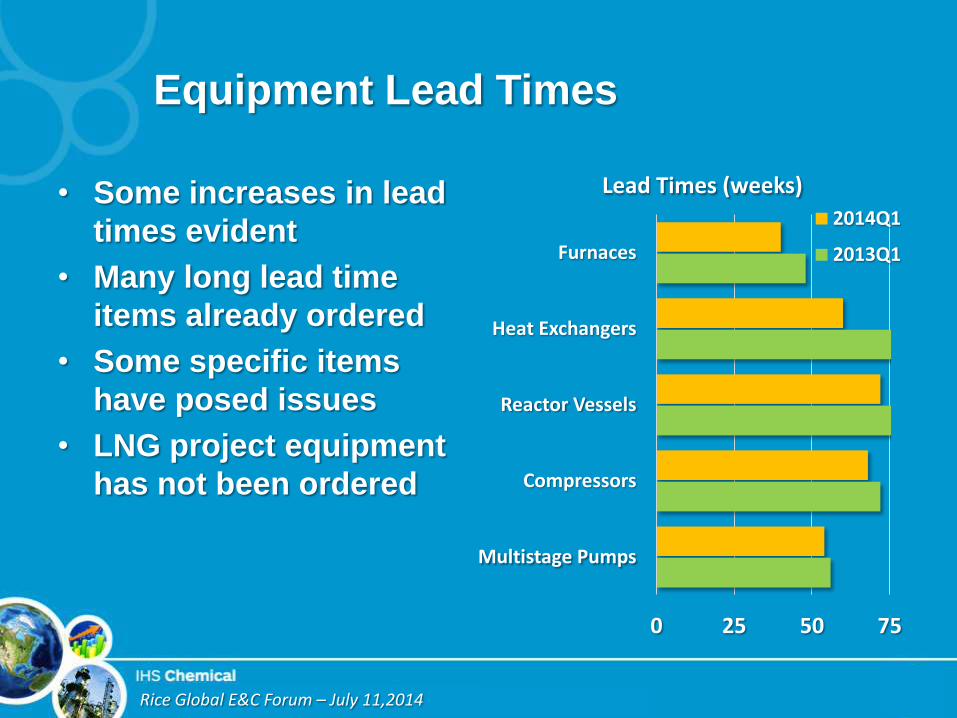

Equipment Lead Times

• Some increases in lead

times evident

• Many long lead time

items already ordered

• Some specific items

have posed issues

• LNG project equipment

has not been ordered

0 25 50 75

Multistage Pumps

Compressors

Reactor Vessels

Heat Exchangers

Furnaces

Lead Times (weeks)

2014Q1

2013Q1

Rice Global E&C Forum – July 11,2014

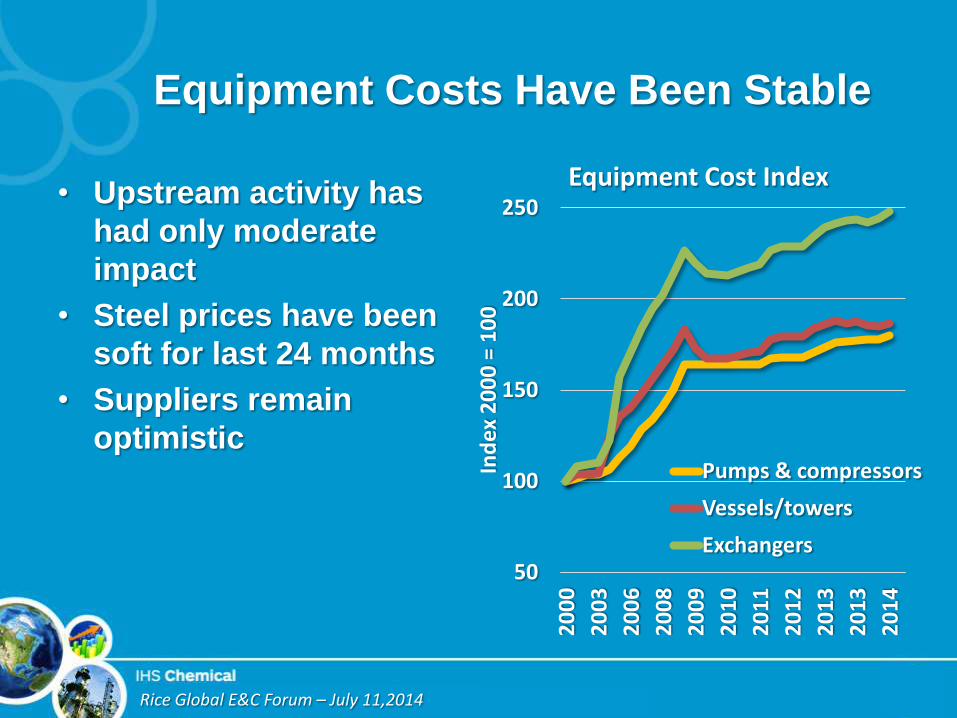

Equipment Costs Have Been Stable

• Upstream activity has

had only moderate

impact

• Steel prices have been

soft for last 24 months

• Suppliers remain

optimistic

50

100

150

200

250

20

00

20

03

20

06

20

08

20

09

20

10

20

11

20

12

20

13

20

13

20

14

Ind

ex 2

00

0 =

10

0

Equipment Cost Index

Pumps & compressors

Vessels/towers

Exchangers

Rice Global E&C Forum – July 11,2014

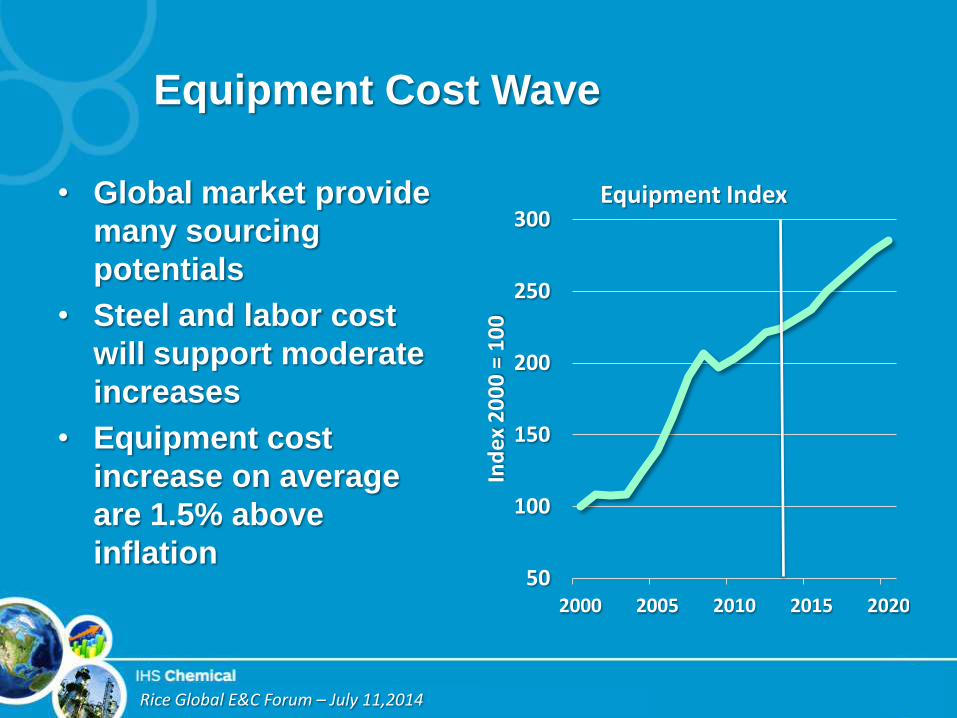

Equipment Cost Wave

• Global market provide

many sourcing

potentials

• Steel and labor cost

will support moderate

increases

• Equipment cost

increase on average

are 1.5% above

inflation 50

100

150

200

250

300

2000 2005 2010 2015 2020

Ind

ex 2

00

0 =

10

0

Equipment Index

Rice Global E&C Forum – July 11,2014

Can we Off-shore?

• Prefabrication offshore

is one countermeasure

• China growing as

alternate supply option

for some equipment

• Modularization option

provide one way to

move project forward

and reduce site labor

requirements

Rice Global E&C Forum – July 11,2014

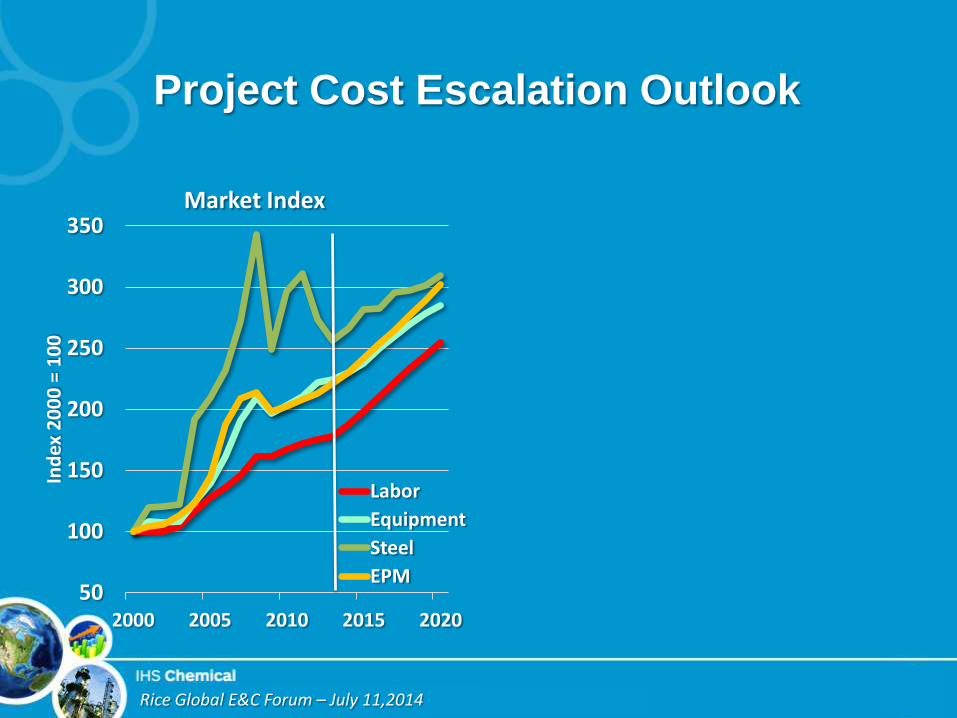

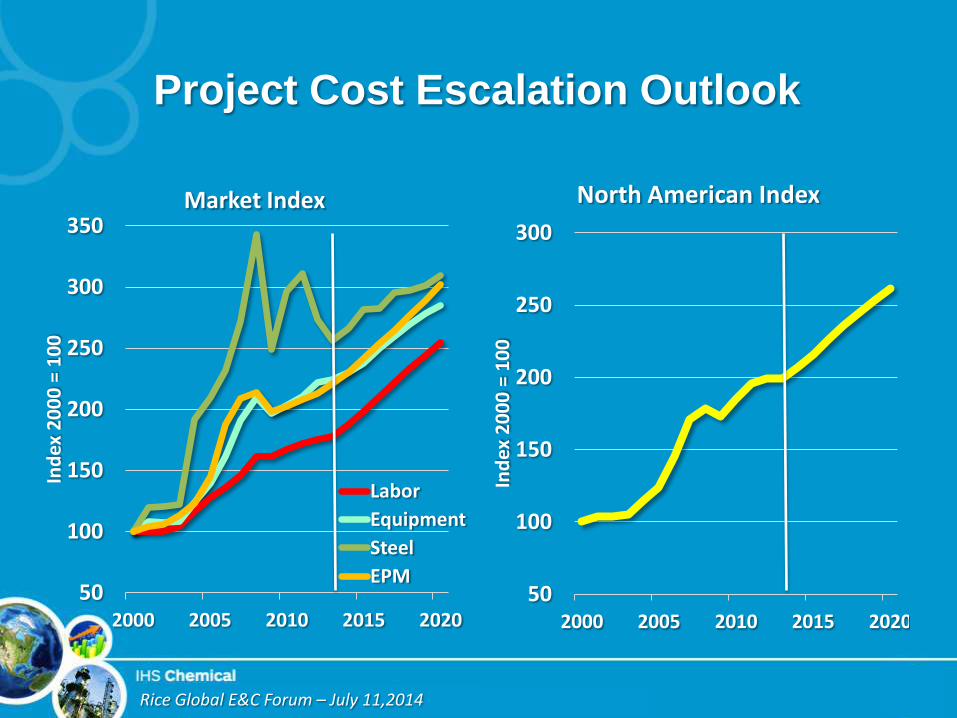

Project Cost Escalation Outlook

50

100

150

200

250

300

350

2000 2005 2010 2015 2020

Ind

ex 2

00

0 =

10

0

Market Index

Labor

Equipment

Steel

EPM

Rice Global E&C Forum – July 11,2014

Project Cost Escalation Outlook

50

100

150

200

250

300

2000 2005 2010 2015 2020

Ind

ex 2

00

0 =

10

0

North American Index

50

100

150

200

250

300

350

2000 2005 2010 2015 2020

Ind

ex 2

00

0 =

10

0

Market Index

Labor

Equipment

Steel

EPM

Rice Global E&C Forum – July 11,2014

North America: Riding the Wave

• Watching the wave

build

• Are there enough

trained surfers?

• Surf board availability

– Made in China?

• Stingrays, jellyfish and

storms

Rice Global E&C Forum – July 11,2014

Hazards

• Factors that could

cause problems:

– Permit delays

– Regulatory changes

– Hurricanes

Rice Global E&C Forum – July 11,2014

Permitting

• Many projects are

awaiting permits –

approvals taking up to

16 months

• Texas GHG permit

situation adds new

unknown.

• Environmental groups

impacting process

Rice Global E&C Forum – July 11,2014

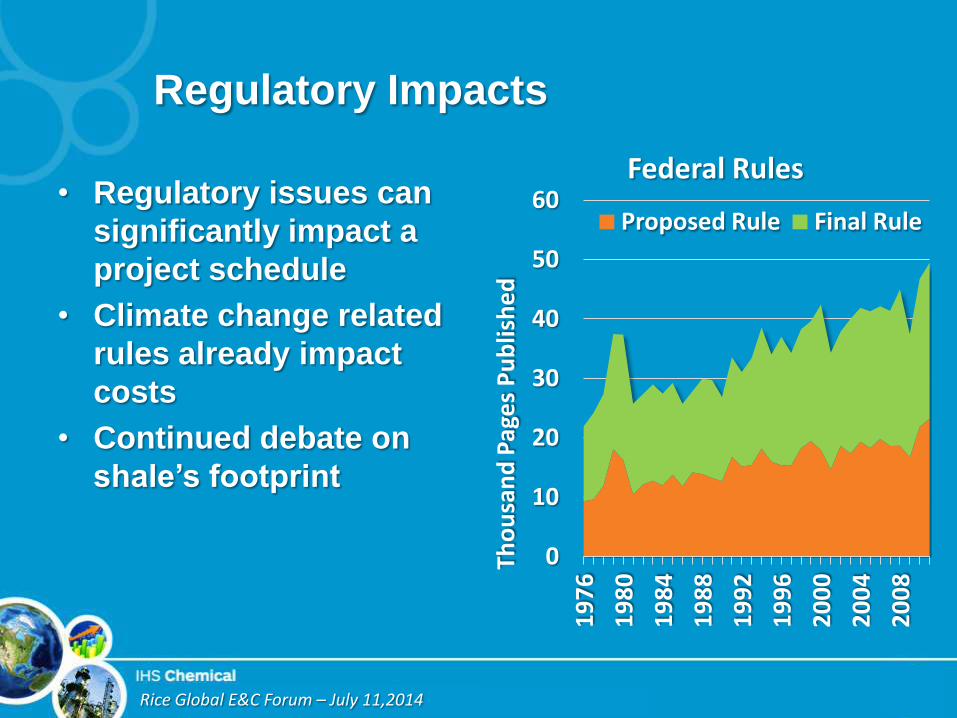

Regulatory Impacts

• Regulatory issues can

significantly impact a

project schedule

• Climate change related

rules already impact

costs

• Continued debate on

shale’s footprint

0

10

20

30

40

50

60

19

76

19

80

19

84

19

88

19

92

19

96

20

00

20

04

20

08

Tho

usa

nd

Pag

es

Pu

blis

he

d

Federal Rules

Proposed Rule Final Rule

Rice Global E&C Forum – July 11,2014

Weather Watch

• Hurricanes are hard

to predict

• Impact of Katrina

and Rita were

profound

• Strengths and

weaknesses of

being in the USGC

Rice Global E&C Forum – July 11,2014

Conclusions

• The wave will continue to build

– New project will be added

• Project delays can be anticipated

– Permitting is biggest risk here

• Project costs will increase from current levels

– Labor is the main risk factor

– Average project cost increases generally below levels

anticipated by many

• Modularization can help mitigate delays and

labor risks

Rice Global E&C Forum – July 11,2014

Better Hold On for a Good Ride

The Texas Outlook can be simply summed up in one word –

Great