Embed Size (px)

Citation preview

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

73

REVISITING SECTORAL LIBERALIZATION:AN ALTERNATIVE TO THE FREE TRADE AREA

OF THE ASIA-PACIFIC? IMPLICATIONSFOR THE PHILIPPINES

George Manzano and Myrene Bedano*

This paper develops a modality of liberalization for APEC, based ona sectoral level, as an alternative to the Free Trade Area of theAsia-Pacific (FTAAP). This model, originally developed by Wonnacott(1994), argues for the liberalization, on a Most Favoured Nation (MFN)basis, of sectors where APEC members are principal suppliers. The mainadvantage of this option is that it skirts the free rider problem that usuallyafflicts MFN liberalization. While this approach would benefit APEC asa group, it impacts different members differently. The paper examines theimplications of such a liberalization modality in APEC on the Philippines,as a case study.

JEL Classification: F13, F14, F15.

Key words: Asia-Pacific Economic Cooperation (APEC), Early Voluntary SectoralLiberalization (EVSL), Free Trade Area of the Asia-Pacific (FTAAP), “principal supplier”approach, sectoral liberalization, trade liberalization.

I. INTRODUCTION

The concept of open regionalism is a fuzzy one. As echoed by Bergsten(1997), this concept was first understood as a concerted unilateral liberalization.

* George Manzano is an Assistant Professor at the School of Economics, University of Asia and thePacific (UA&P), Philippines and Myrene Bedaño is a Trade and Industry Development Specialist, Bureau ofInternational Trade Relations, Department of Trade and Industry (DTI), Philippines. The authors wish toacknowledge the research support of the Philippine APEC Study Center Network. This paper is a revisedversion of the paper presented at the ARTNeT Conference on 2-3 November 2009 at UNESCAP,Bangkok, at the 35th Annual Conference of the Federation of ASEAN Economics Associations at Bali,Indonesia on 1-3 December 2010 and at the APEC Study Center Consortium Conference in Singapore inJuly 2009. Please direct queries to George Manzano at [email protected] [email protected].

¨

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

74

However, the euphoria in the APEC process that emanated from the Bogor meetingswaned as the Asian financial crisis struck in 1997. As most of Asia grappled with thecrippling effects of the crisis, the political support for trade liberalization across APECfaltered or at least failed to match the rhetoric of the leaders’ declarations. Inaddition, as the Doha Round bogged down amid disagreements on agriculture trade,regional trade agreements (RTAs) proliferated. Even within APEC, a multitude of RTAsbloomed, threatening to overshadow APEC’s role as a driver of trade. In an effort toput the APEC profile back to its prominence, the Free Trade Area of the Asia-Pacific(FTAAP) was proposed in 2004. However, given the current trade tensions amongsome members, the political support for such an agreement has becomequestionable. Yet, there remains the imperative for fresh initiatives to keep the bicycleof trade liberalization moving. Given this backdrop, this paper presents anothermodality to support APEC’s trade liberalization pillar and to provide an alternative tothe FTAAP proposal.

This paper develops a modality based on sectoral liberalization, reminiscentof the Early Voluntary Sectoral Liberalization (EVSL). However, in contrast to theill-fated EVSL, where the “voluntary” nomination of sectors for early liberalization isbased, to some extent, on the mercantilist interests of individual members, theproposed modality will employ a more analytical method for identifying the sector tobe slated for liberalization. Central to this modality is the basis for selection ofsectors to be liberalized. Following Wonnacott’s (1994) methodology, the paper willuse the “principal supplier” criterion in identifying the sectors that can be consideredfor MFN liberalization. To highlight the implications of the sectoral liberalization onindividual members, a case study of the Philippines will be conducted.

II. TRADE LIBERALIZATION IN APEC AND THE FTAAP

There are concerns that APEC will miss the Bogor goals, launched in 1994.One initiative to push for the Bogor goals is via the preferential route, i.e., creatinga massive RTA encompassing all APEC members. The proposed RTA, dubbed as theFTAAP, represents a significant departure from APEC’s initial approach to tradeliberalization. APEC distinguishes itself from conventional preferential models with itsstrict adherence to “open regionalism”. Specifically, the organization subscribes tothe “concerted unilateralism” approach that entails the simultaneous unilateral actionon the part of APEC members to liberalize trading regimes in a less discriminatorymanner. This unique character of APEC seeks to ensure that it will serve asa “building block” to global trade liberalization, rather than a “stumbling block”.Clearly, an RTA would involve a complete overhaul of the APEC modality to tradeliberalization – from a non-discriminatory approach to trade liberalization underpinned

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

75

by voluntary and non-binding commitments, towards an explicit preferentialarrangement established through negotiations of reciprocal trade concessions thatare legally binding.

The interest in the APEC RTA concept is motivated by a set of reinforcingfactors. As mentioned earlier, the primary motive emanates from the challenge forAPEC to revitalize its faltering trade agenda. Critics point to the demise of the EVSLscheme and the ineffectiveness of the Individual Action Plan (IAP) process as thedrag on APEC’s credibility and momentum. The failure of the EVSL in the late1990s revealed that the mechanisms by which the organization operates, whilewell-received, are practicably flawed. Further, the experience demonstrated thatsignificant trade liberalization may not be easily achieved by the mere reliance onvoluntary action by members kept in check only by friendly reminders by peer groups.Thus, the FTAAP is considered to be an effective way to energize APEC and to get itright back on the trade liberalization track. A single RTA that would meld themultitude of RTAs in the region and rationalize the different provisions contained inthese arrangements could well be the solution to the “spaghetti bowl” or “noodlebowl” effect of overlapping RTAs. In addition, the FTAAP is a response to thegridlocked WTO negotiations.

While the FTAAP possesses certain merits there are serious questions aboutits feasibility in the foreseeable future. One difficulty pertains to the plethora ofinterests and sensitive political dynamics among major players, which makes itdifficult to peddle the FTAAP (Morrison, 2007; Aggarwal, 2007). There are alsoa number of practical difficulties in negotiating such a large-scale arrangement, whichcould dampen the expectations of a successful conclusion in the near future.Designing, negotiating and implementing RTAs consume significant policymaking andcapital resources and the capacity to take part in the RTA is not symmetric amongAPEC members.

More recently however, another modality that involves widening themembership of the Trans-Pacific Economic Partnership Agreement (TPP) topotentially include most APEC members has been proposed. All original members ofthe TPP are APEC members and there is active interest among other APEC membersto join.1 Because the scope for liberalization in the TPP agreement is comprehensive,an expansion of members to include all APEC members could then be a substitute tothe formation of the FTAAP.

1 Brunei Darussalam, Chile, New Zealand and Singapore, the four original members, signed the TPP in2005 which entered into force in May 2006. The United States of America, Australia, Peru and Viet Namexpressed interest in joining the TPP.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

76

In view of these issues revolving around the FTAAP and the gridlock on themultilateral forums, the Doha Development Agenda (DDA), the search of a suitablealternative for trade liberalization agenda in the APEC looms large. Certainly,unilateral liberalization, liberally interpreted as open regionalism, is one. While theeconomic arguments for this modality are many, a negative feature is that it wouldamount to giving the rest of the world a “free ride” as non-members automaticallybenefit from the tariff reductions by APEC members without making correspondingliberalization measures. Another avenue is sectoral liberalization.

III. PRINCIPAL SUPPLIER APPROACH TO SECTORALLIBERALIZATION

Theoretical Foundations

To the knowledge of the authors, there is no paper in the literature thatspecifically provides a theoretical justification for sectoral liberalization on an MFNbasis, along the “principal supplier” criteria in Wonnacott (1994). There is a relatedliterature that explains the merits of a non-preferential trading club, which is oneinterpretation of “open regionalism”.

Raimondos-Moller and Woodland (2006) wrote the first paper that discussedthe theoretical foundation of the advantages of “open regionalism”. One variant of“open regionalism” is the non-preferential club which is a group of countries thatagree to coordinate their non-discriminatory tariff policies and to undertake internalincome transfers. They argue that a non-preferential trading club, by undertakingcoordinated tariff reforms, can improve the efficiency of the resource allocationand welfare of the members of the club, at the same time leave the welfare of thenon-members untouched, i.e. a Pareto-improvement. An important feature though isthat the “coordinated tariff reforms” of the club members requires some members toraise their tariffs and some to reduce theirs or even allow subsidies. They argue thata non-preferential club is consistent with the spirit of the WTO in that whateverarrangements members make to improve their welfare, does not harm the welfare ofthe rest of the world.2

The sectoral liberalization modality proposed in this paper, share manycharacteristics of a non-preferential trading club. First, the liberalization, beingundertaken on an MFN basis, is non-discriminatory. Second, it is to be undertaken bya subset of the global economy, in this case, APEC members. Third, it should not

2 This outcome is similar to Kemp-Wan (1976) proposition except that the latter pertains to customsunions.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

77

make the rest of the world worse-off, by keeping the relative prices to non-membersunchanged despite the internal changes among club members. Obviously, worldprices would not be held constant in the process of the APEC sectoral liberalization,as the APEC members are dominant producers and consumers in the aforementionedsectors. However, one may argue that because the tariff movements of theAPEC members are, of course, downwards, and granted on an MFN basis, the non-members will not likely be harmed.

The “Principal Supplier” criteria

To lessen the possibility of outsiders free riding3 on the trade liberalizationefforts by APEC, the challenge is to identify those areas in which the benefits of tradeliberalization would redound mostly on APEC members than on non-members. Earlierwork that addressed the issue of free riding is by Wonnacott (1994) that suggesteda trade liberalization scheme on a selective product-by-product basis whereincountries choose the commodities for early liberalization based on a pre-definedcriteria. Specifically, the methodology by Wonnacott prescribes that, in order tominimize the free rider problem, tariff reduction should be undertaken on the goodswhere APEC is a dominant global supplier. Intuitively, the benefits of tariff reductions,in terms of enhanced market access, on these goods would largely accrue to APECmembers, simply, because non-APEC members are not major exporters of suchproducts.

In the selection of potential candidates for liberalization, the share of APEC inthe world exports of goods was used as basis. A large percentage share of exports istaken to indicate that “free riding” by non-members would be less problematic. As inWonnacott’s study, the export shares of APEC in total world trade are compared withtheir share in total world exports less intra-European Union trade. Trade betweenEuropean Union member countries is discounted, as stipulated in Wonnacott (1994)on the ground that it is becoming more and more intraregional. For this exercise,commodities are examined at the 6-digit level based on the Harmonized System (HS)Commodity Classification Code.

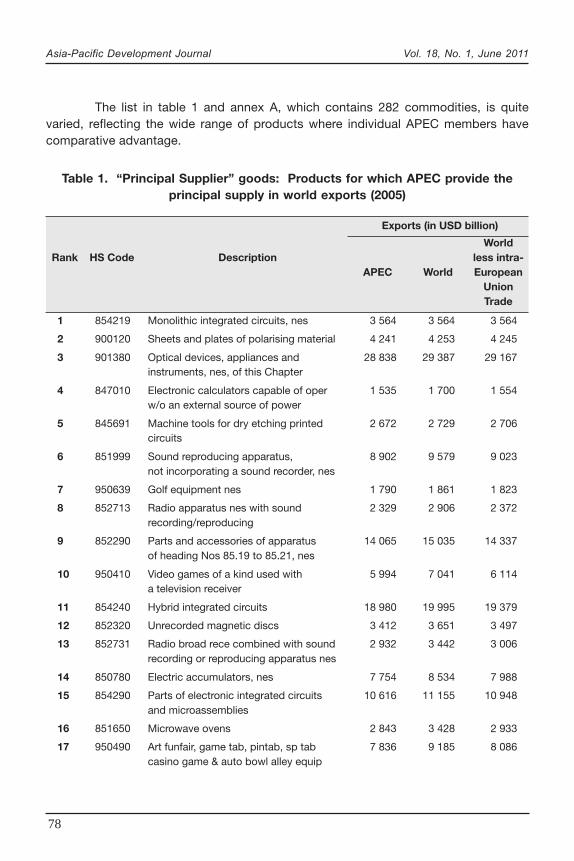

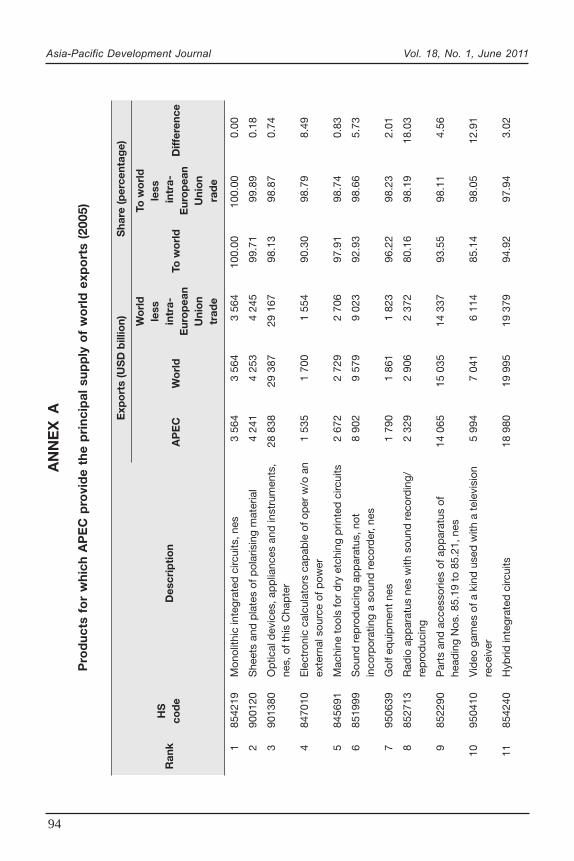

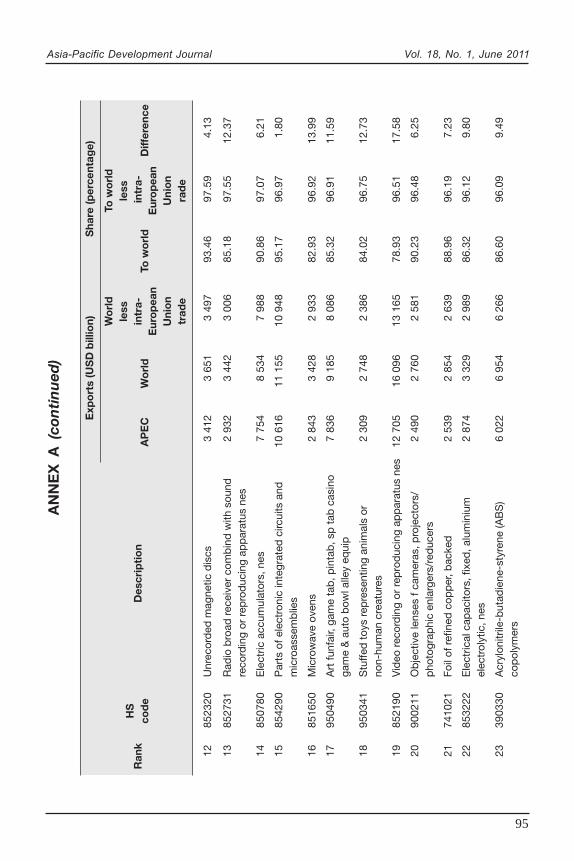

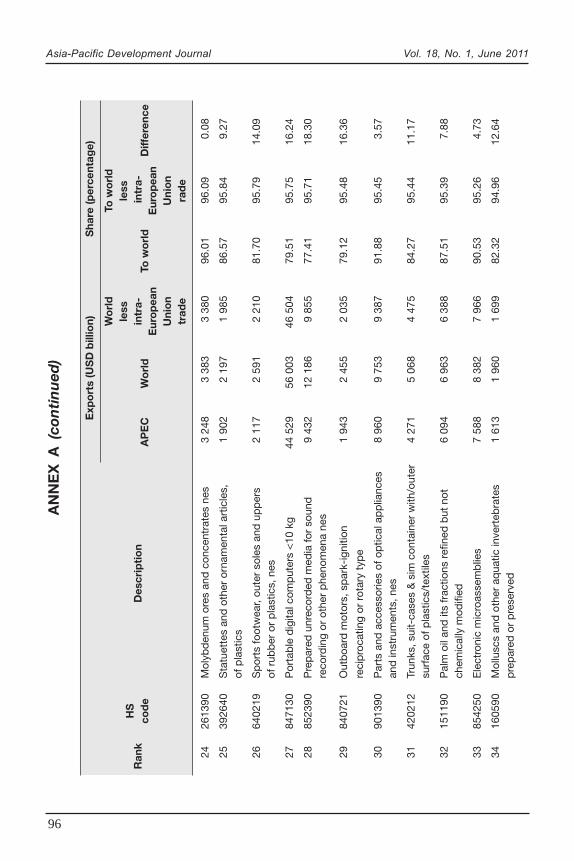

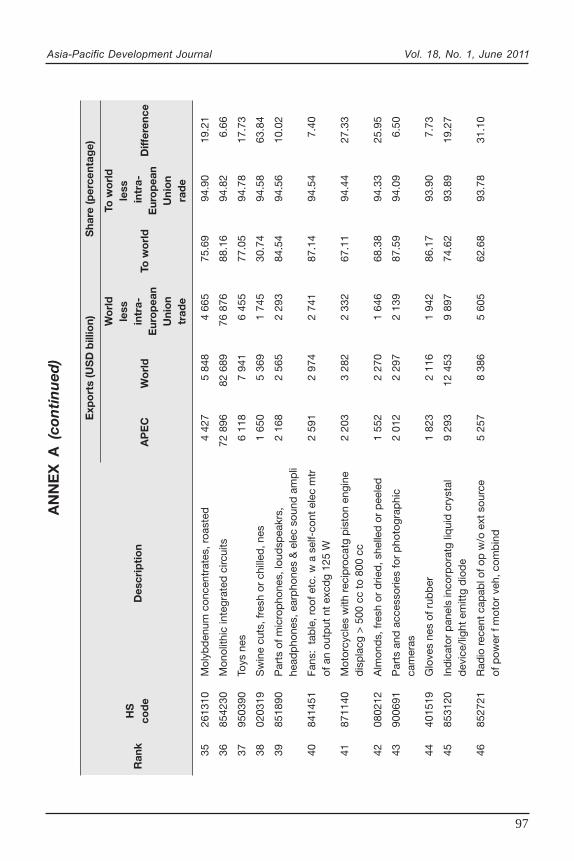

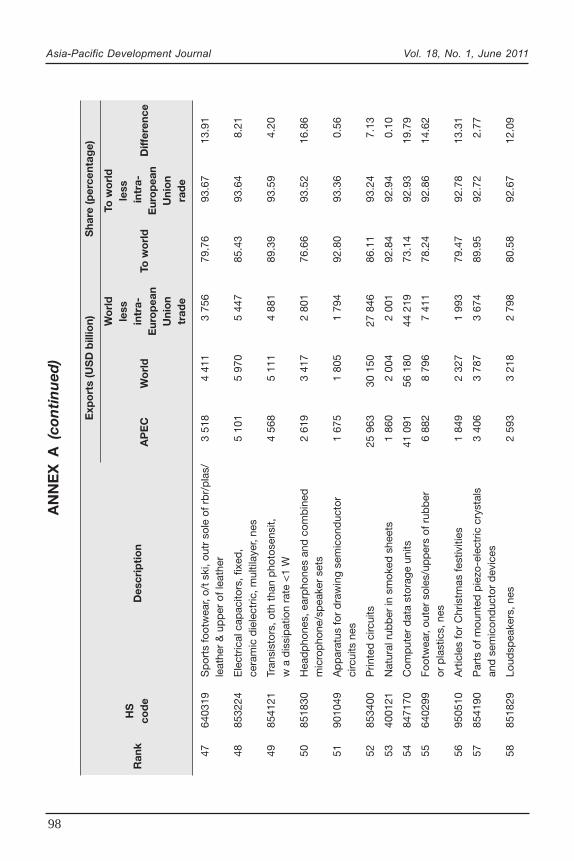

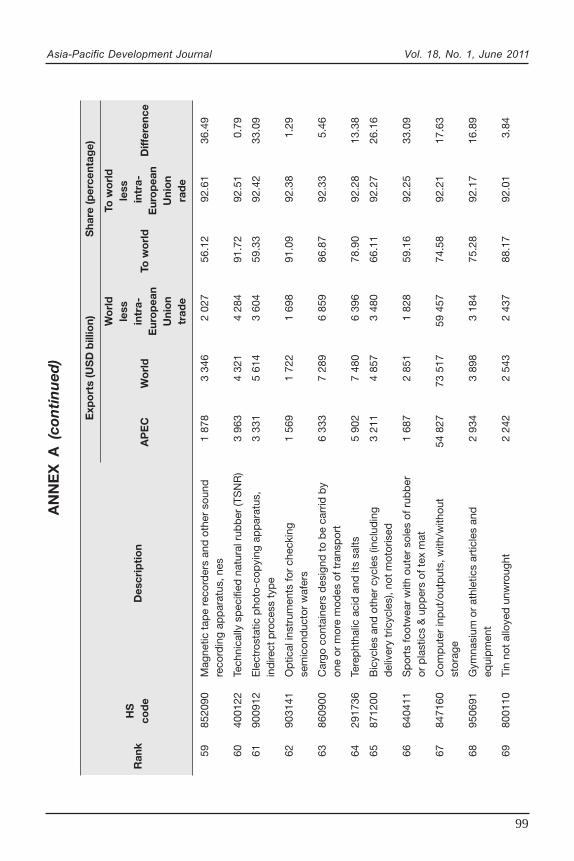

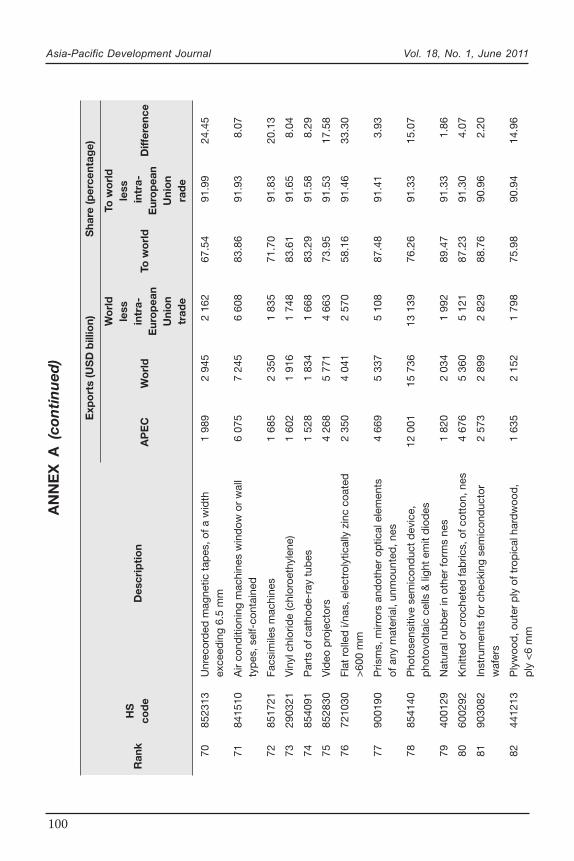

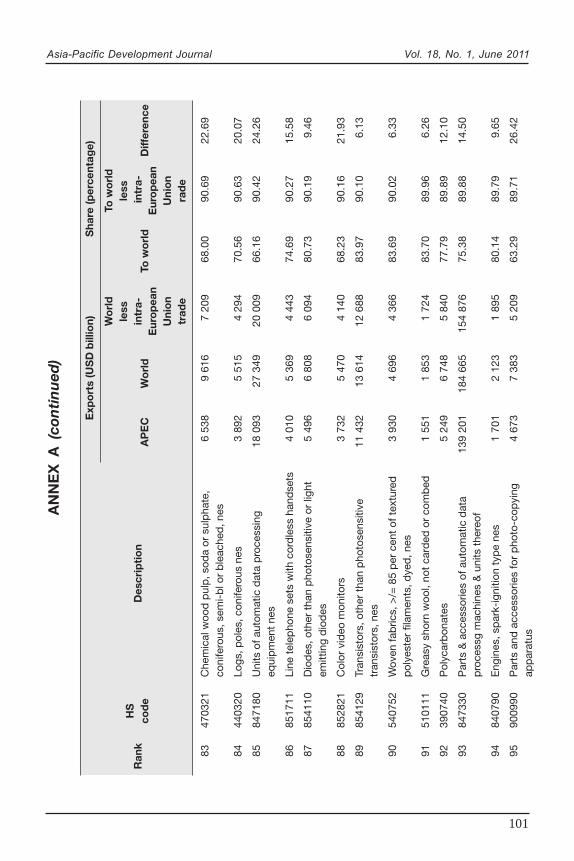

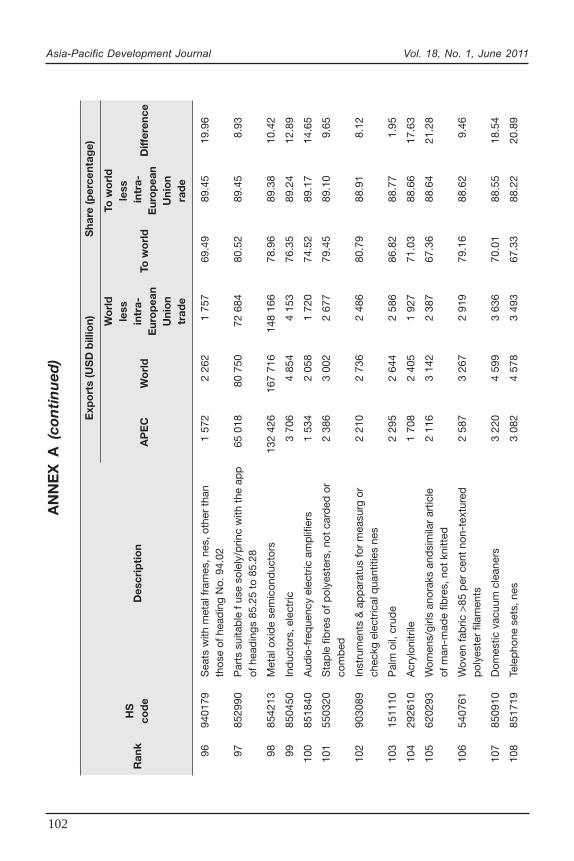

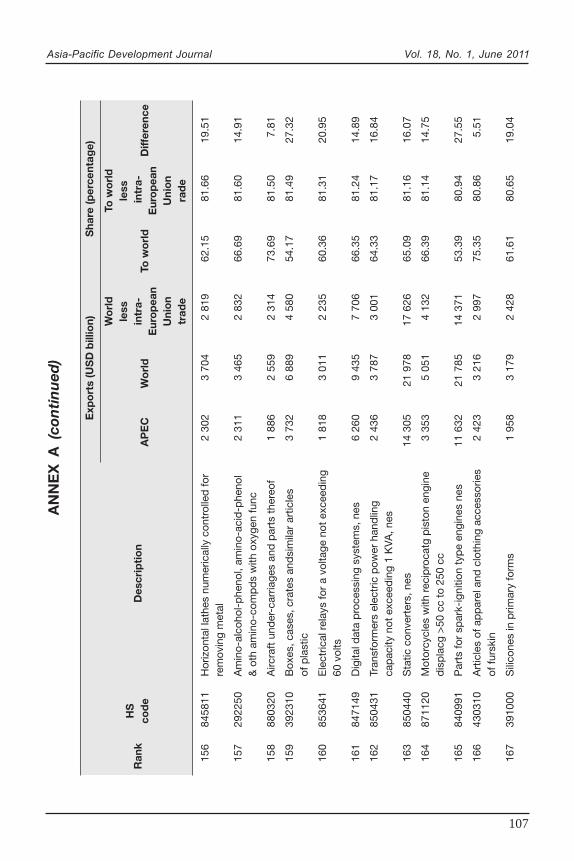

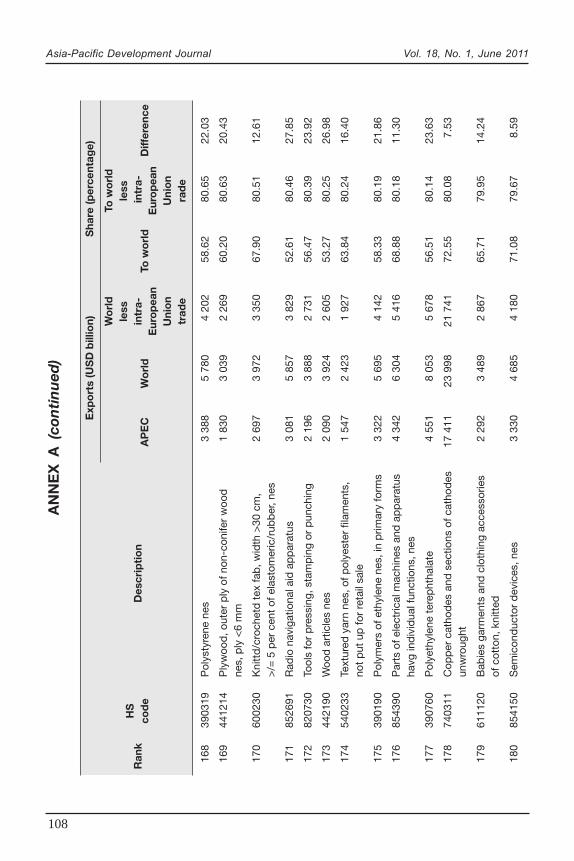

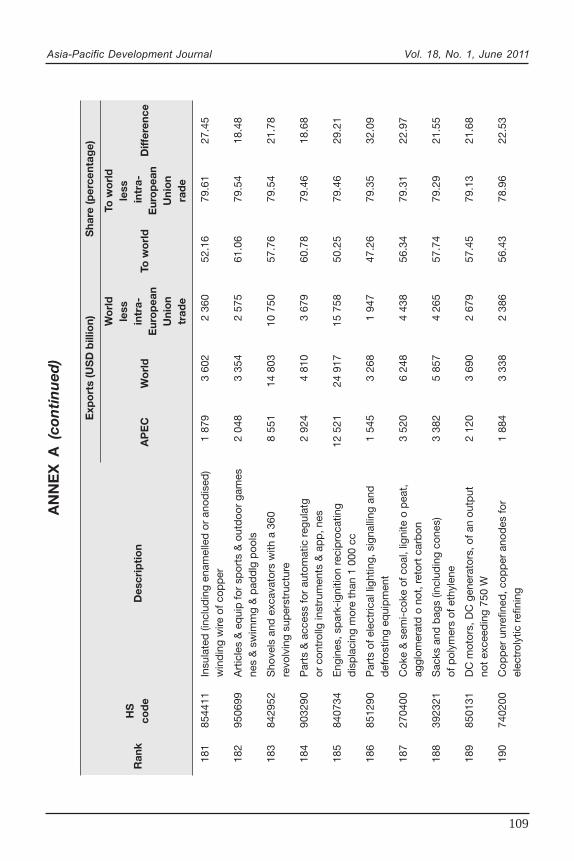

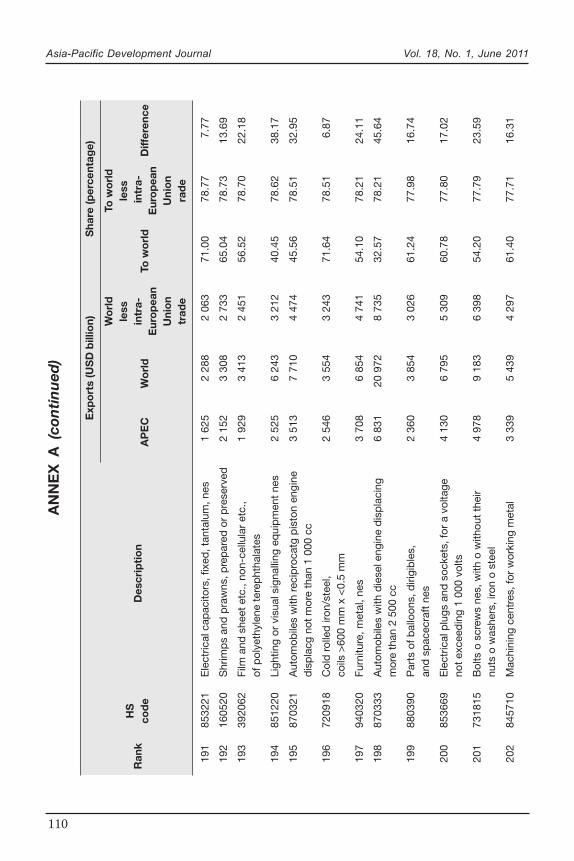

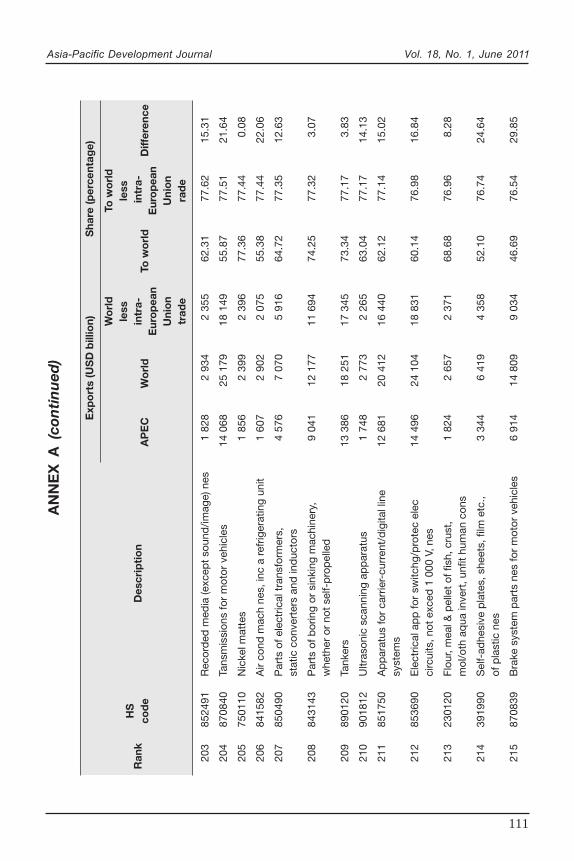

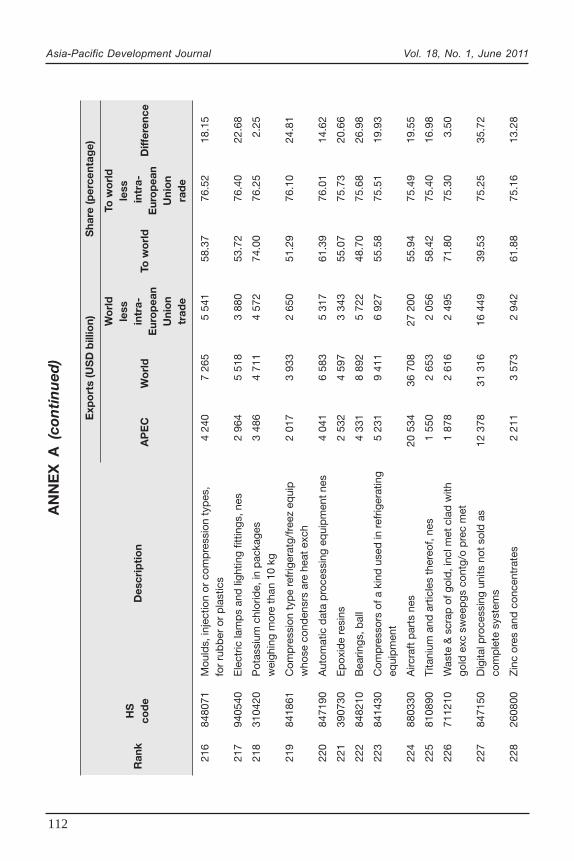

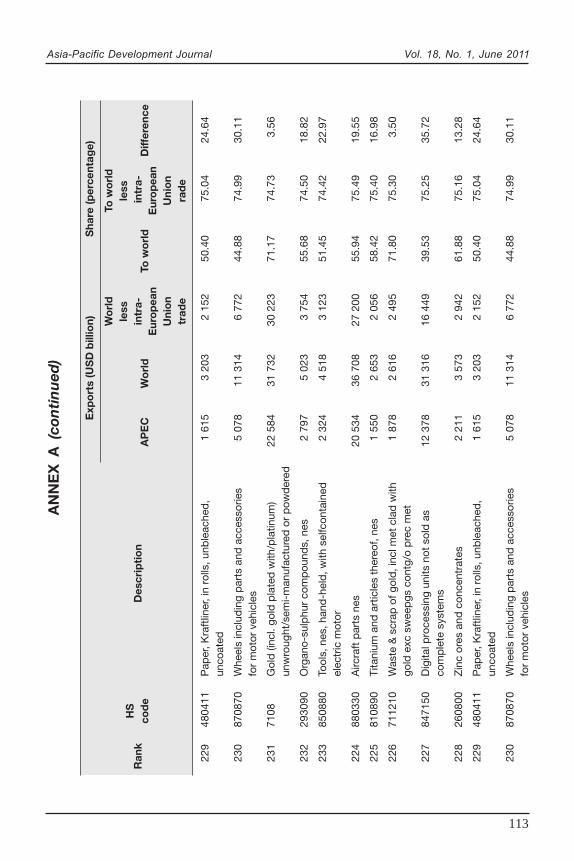

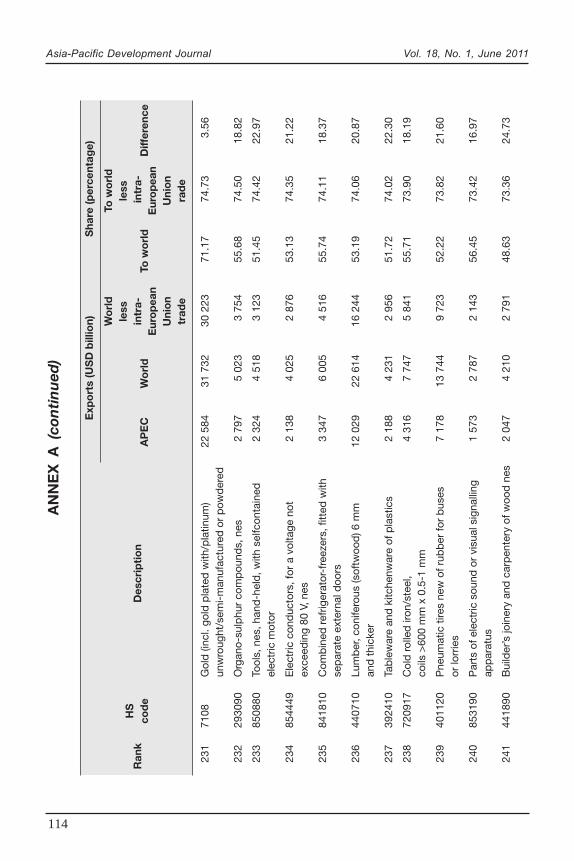

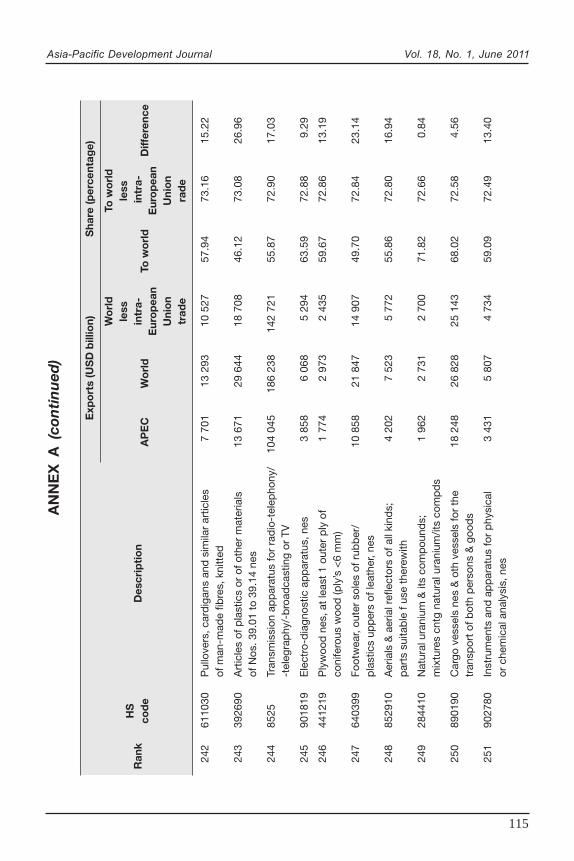

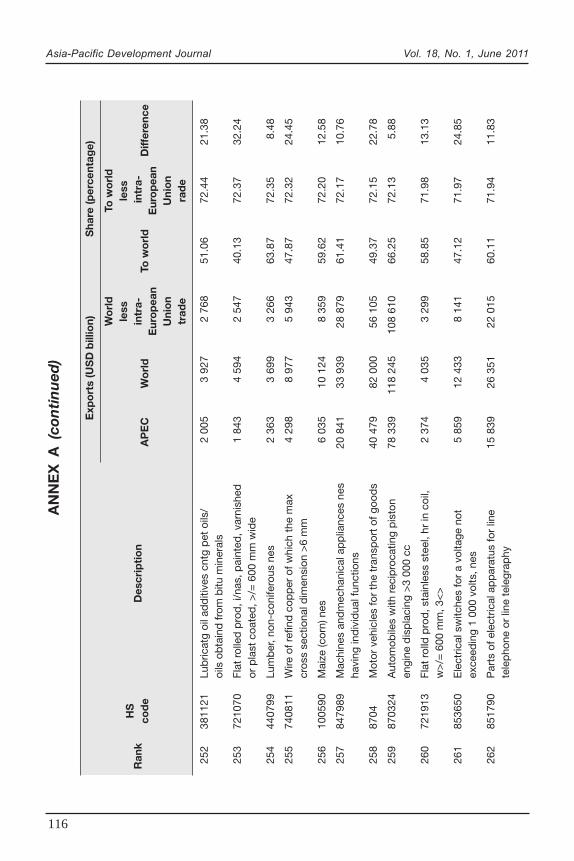

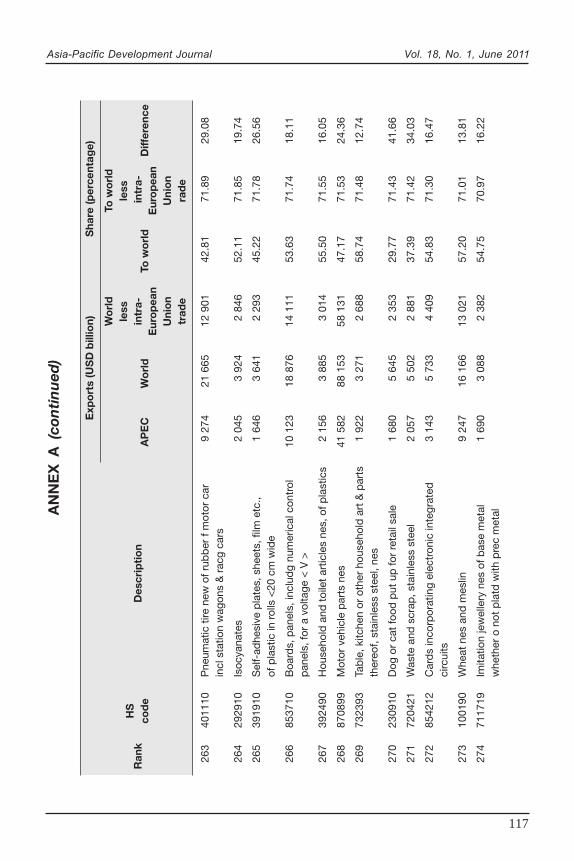

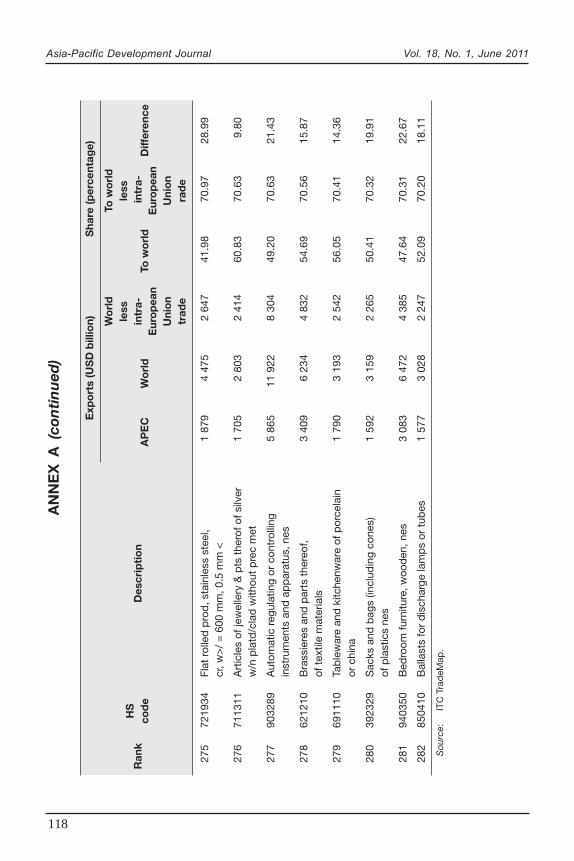

The products in which the APEC members are principal suppliers arereported in table 1. These are the products where APEC members, as a whole, enjoya share of at least 70 per cent of world exports in 2005 (not counting intra-EuropeanUnion trade).

3 Free riding is considered a cost because third countries will enjoy market acess without giving ‘quid-pro-quo’ concessions on access to their own markets.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

78

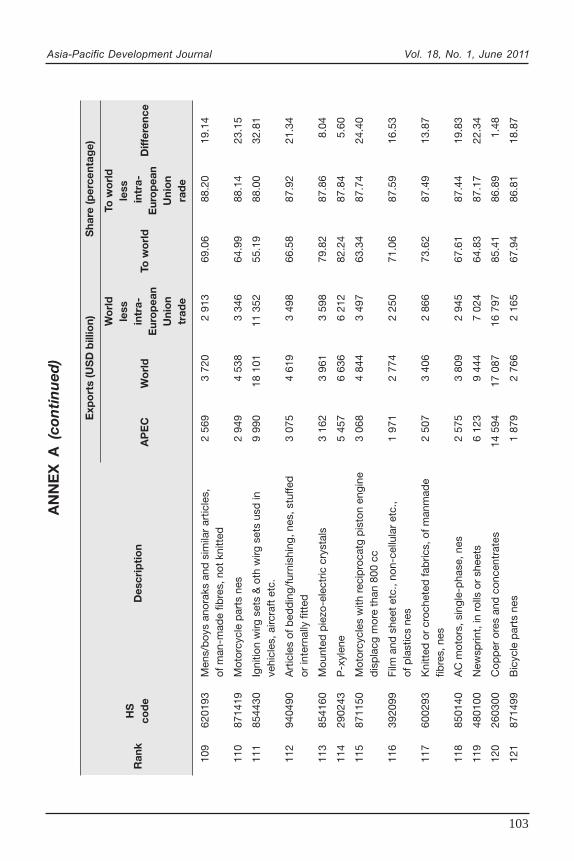

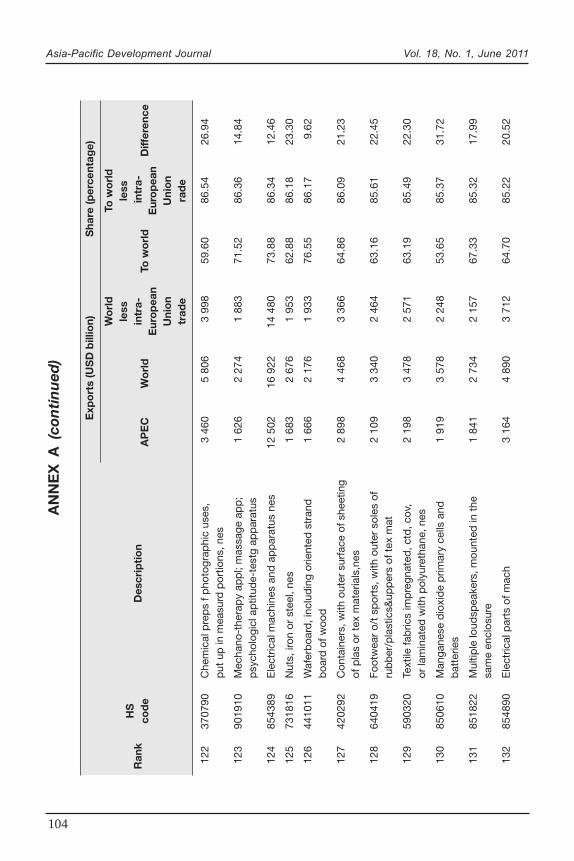

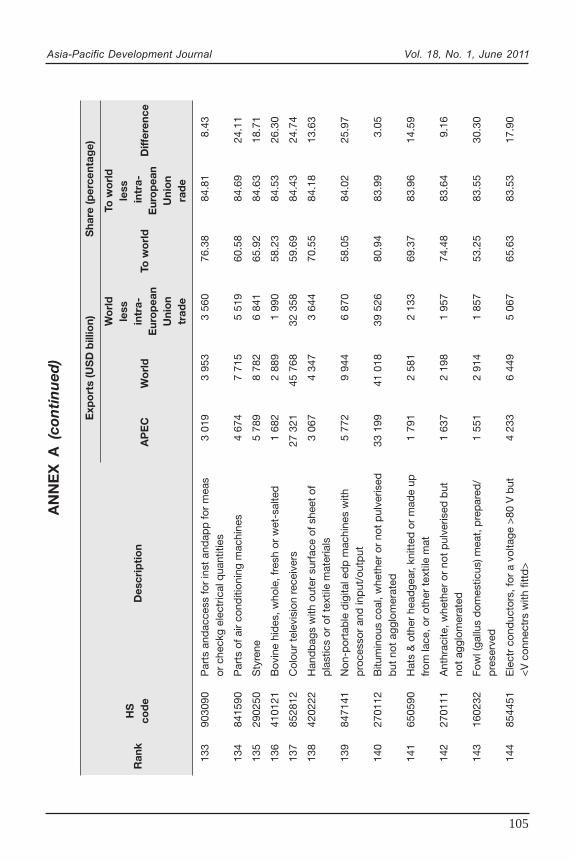

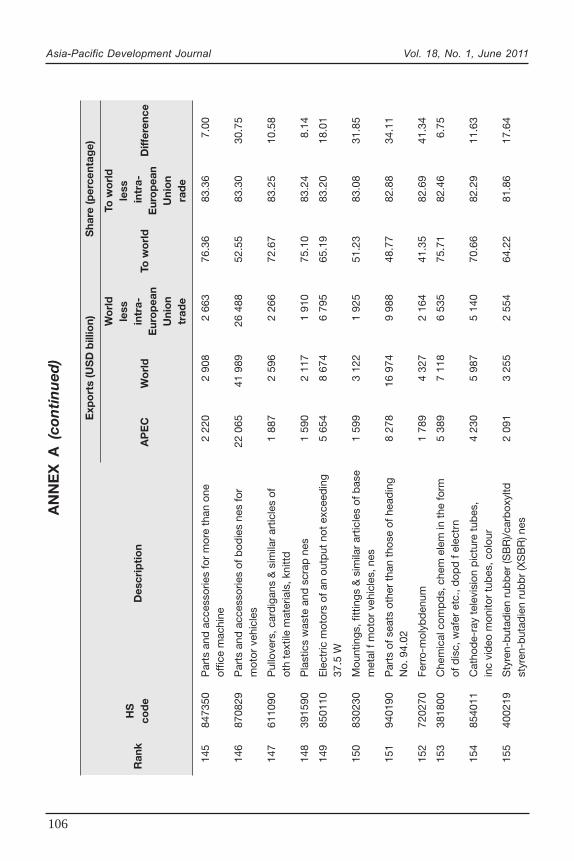

The list in table 1 and annex A, which contains 282 commodities, is quitevaried, reflecting the wide range of products where individual APEC members havecomparative advantage.

Table 1. “Principal Supplier” goods: Products for which APEC provide theprincipal supply in world exports (2005)

Exports (in USD billion)

WorldRank HS Code Description less intra-

APEC World EuropeanUnionTrade

1 854219 Monolithic integrated circuits, nes 3 564 3 564 3 564

2 900120 Sheets and plates of polarising material 4 241 4 253 4 245

3 901380 Optical devices, appliances and 28 838 29 387 29 167instruments, nes, of this Chapter

4 847010 Electronic calculators capable of oper 1 535 1 700 1 554w/o an external source of power

5 845691 Machine tools for dry etching printed 2 672 2 729 2 706circuits

6 851999 Sound reproducing apparatus, 8 902 9 579 9 023not incorporating a sound recorder, nes

7 950639 Golf equipment nes 1 790 1 861 1 823

8 852713 Radio apparatus nes with sound 2 329 2 906 2 372recording/reproducing

9 852290 Parts and accessories of apparatus 14 065 15 035 14 337of heading Nos 85.19 to 85.21, nes

10 950410 Video games of a kind used with 5 994 7 041 6 114a television receiver

11 854240 Hybrid integrated circuits 18 980 19 995 19 379

12 852320 Unrecorded magnetic discs 3 412 3 651 3 497

13 852731 Radio broad rece combined with sound 2 932 3 442 3 006recording or reproducing apparatus nes

14 850780 Electric accumulators, nes 7 754 8 534 7 988

15 854290 Parts of electronic integrated circuits 10 616 11 155 10 948and microassemblies

16 851650 Microwave ovens 2 843 3 428 2 933

17 950490 Art funfair, game tab, pintab, sp tab 7 836 9 185 8 086casino game & auto bowl alley equip

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

79

18 950341 Stuffed toys representing animals 2 309 2 748 2 386or non-human creatures

19 852190 Video recording or reproducing 12 705 16 096 13 165apparatus nes

20 900211 Objective lenses f cameras, projectors/ 2 490 2 760 2 581photographic enlargers/reducers

21 741021 Foil of refined copper, backed 2 539 2 854 2 639

22 853222 Electrical capacitors, fixed, aluminium 2 874 3 329 2 989electrolytic, nes

23 390330 Acrylonitrile-butadiene-styrene (ABS) 6 022 6 954 6 266copolymers

24 261390 Molybdenum ores and concentrates nes 3 248 3 383 3 380

25 392640 Statuettes and other ornamental articles, 1 902 2 197 1 985of plastics

26 640219 Sports footwear, outer soles and uppers 2 117 2 591 2 210of rubber or plastics, nes

27 847130 Portable digital computers <10 kg 44 529 56 003 46 504

28 852390 Prepared unrecorded media for sound 9 432 12 186 9 855recording or other phenomena nes

29 840721 Outboard motors, spark-ignition 1 943 2 455 2 035reciprocating or rotary type

30 901390 Parts and accessories of optical 8 960 9 753 9 387appliances and instruments, nes

Source: Authors’ calculations using ITC TradeMap data.

Note: The complete list is reported in annex A.

Table 1. (continued)

Exports (in USD billion)

WorldRank HS Code Description less intra-

APEC World EuropeanUnionTrade

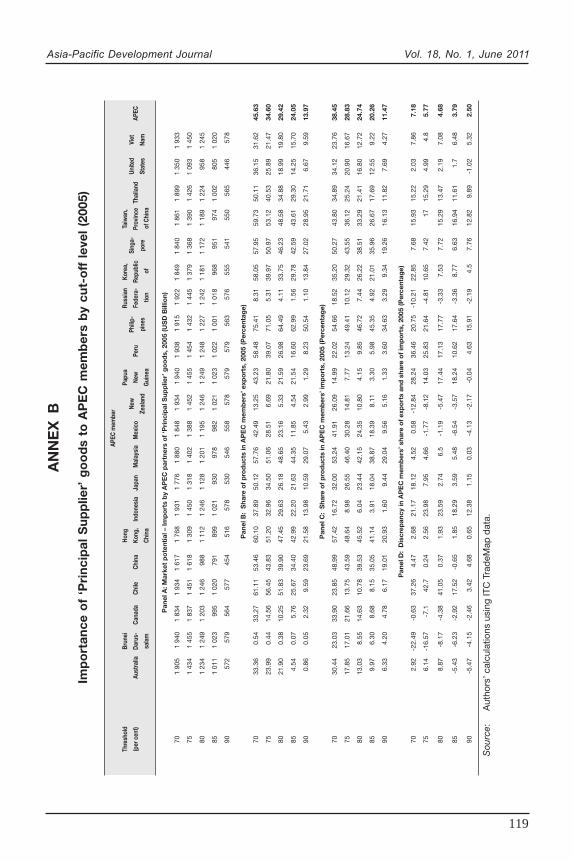

To analyse the importance of the selected products in the trade of individualAPEC members, these products are classified based on their trade shares. Panel A inannex B shows the imports of APEC partners above each cut-off level. The figuresreported in panel A in annex B give a rough approximation of the value of the marketthat would be opened for each APEC member indicated when APEC partners bringdown their tariffs on the items that lie above the chosen cut-off lines. Panels B and C

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

80

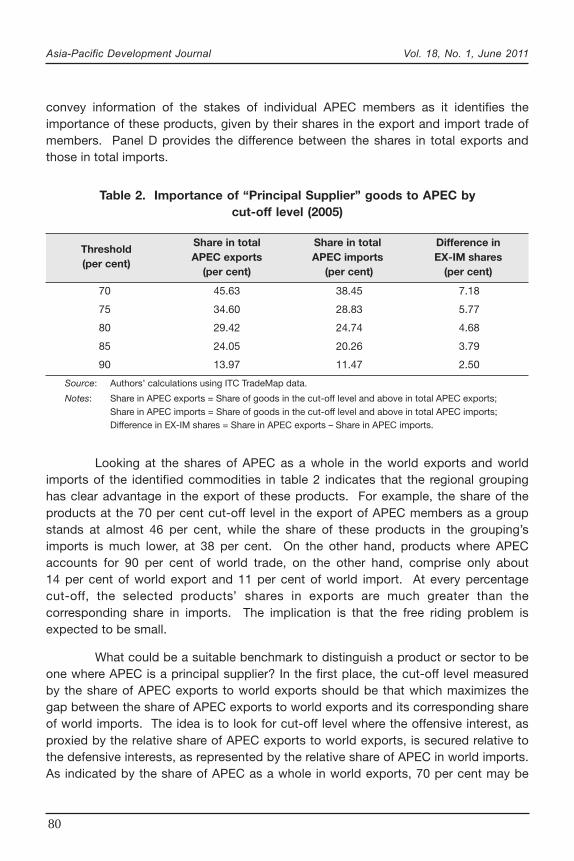

convey information of the stakes of individual APEC members as it identifies theimportance of these products, given by their shares in the export and import trade ofmembers. Panel D provides the difference between the shares in total exports andthose in total imports.

Table 2. Importance of “Principal Supplier” goods to APEC bycut-off level (2005)

ThresholdShare in total Share in total Difference in

(per cent)APEC exports APEC imports EX-IM shares

(per cent) (per cent) (per cent)

70 45.63 38.45 7.18

75 34.60 28.83 5.77

80 29.42 24.74 4.68

85 24.05 20.26 3.79

90 13.97 11.47 2.50

Source: Authors’ calculations using ITC TradeMap data.

Notes: Share in APEC exports = Share of goods in the cut-off level and above in total APEC exports;Share in APEC imports = Share of goods in the cut-off level and above in total APEC imports;Difference in EX-IM shares = Share in APEC exports – Share in APEC imports.

Looking at the shares of APEC as a whole in the world exports and worldimports of the identified commodities in table 2 indicates that the regional groupinghas clear advantage in the export of these products. For example, the share of theproducts at the 70 per cent cut-off level in the export of APEC members as a groupstands at almost 46 per cent, while the share of these products in the grouping’simports is much lower, at 38 per cent. On the other hand, products where APECaccounts for 90 per cent of world trade, on the other hand, comprise only about14 per cent of world export and 11 per cent of world import. At every percentagecut-off, the selected products’ shares in exports are much greater than thecorresponding share in imports. The implication is that the free riding problem isexpected to be small.

What could be a suitable benchmark to distinguish a product or sector to beone where APEC is a principal supplier? In the first place, the cut-off level measuredby the share of APEC exports to world exports should be that which maximizes thegap between the share of APEC exports to world exports and its corresponding shareof world imports. The idea is to look for cut-off level where the offensive interest, asproxied by the relative share of APEC exports to world exports, is secured relative tothe defensive interests, as represented by the relative share of APEC in world imports.As indicated by the share of APEC as a whole in world exports, 70 per cent may be

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

81

a reasonable cut-off level because going this far would cover almost half of APECexports. Additionally, as table 2 reports, it is at the 70 per cent cut-off level where thediscrepancy between the share of APEC exports and imports is greatest (fourthcolumn). The implication here is that the offensive interest of APEC, as a whole, iswell-served at the benchmark for the “principal supplier” at the 70 per cent level. Inaddition, it appears that there will be much to gain from a negotiation which coversproducts where APEC members provide 70 per cent or more of world exports. Asmentioned earlier, at a cut-off rate of 70 per cent, the percentage of APEC exportscovered is close to 46 per cent which is quite sizeable already. At the same time, theportion of APEC exports covered by a negotiation that only considers the next upperbracket of 75 per cent is only about 35 per cent of APEC exports. As the secondcolumn of table 2 shows, the average coverage of APEC exports that will not beincluded in the sectoral negotiations is greatest when the cut-off point is raised from70 per cent to 75 per cent. Specifically, the portion of APEC exports that is notcovered declines by 11.03 per cent, representing an average decrease of 2.21 percent per percentage rise of cut-off between 70 per cent and 75 per cent.

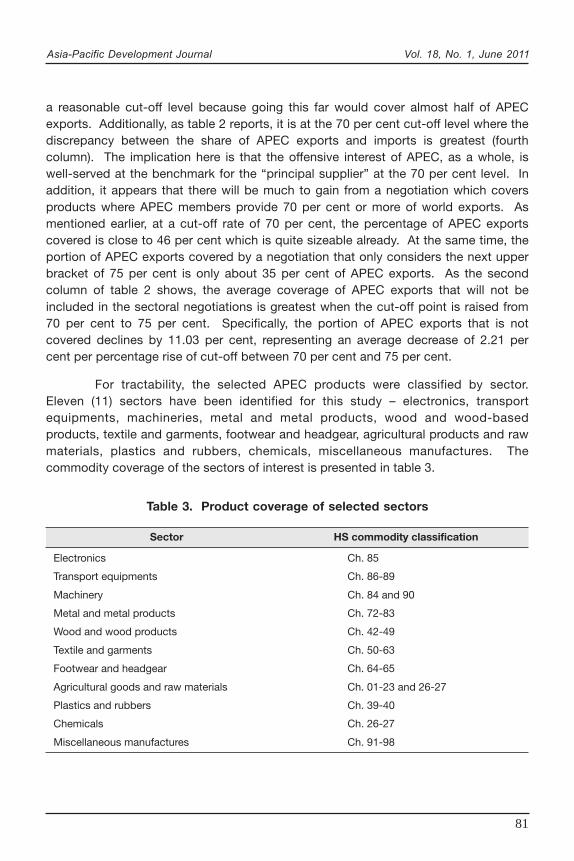

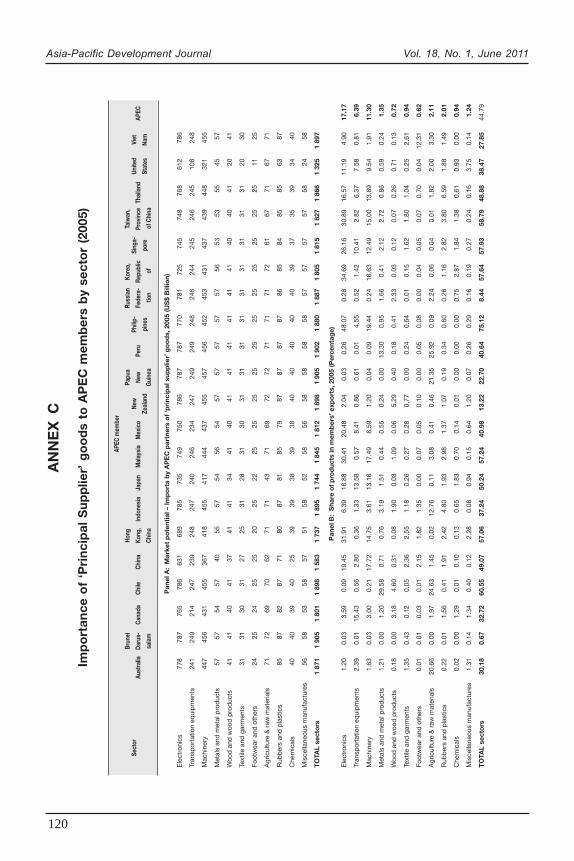

For tractability, the selected APEC products were classified by sector.Eleven (11) sectors have been identified for this study – electronics, transportequipments, machineries, metal and metal products, wood and wood-basedproducts, textile and garments, footwear and headgear, agricultural products and rawmaterials, plastics and rubbers, chemicals, miscellaneous manufactures. Thecommodity coverage of the sectors of interest is presented in table 3.

Table 3. Product coverage of selected sectors

Sector HS commodity classification

Electronics Ch. 85

Transport equipments Ch. 86-89

Machinery Ch. 84 and 90

Metal and metal products Ch. 72-83

Wood and wood products Ch. 42-49

Textile and garments Ch. 50-63

Footwear and headgear Ch. 64-65

Agricultural goods and raw materials Ch. 01-23 and 26-27

Plastics and rubbers Ch. 39-40

Chemicals Ch. 26-27

Miscellaneous manufactures Ch. 91-98

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

82

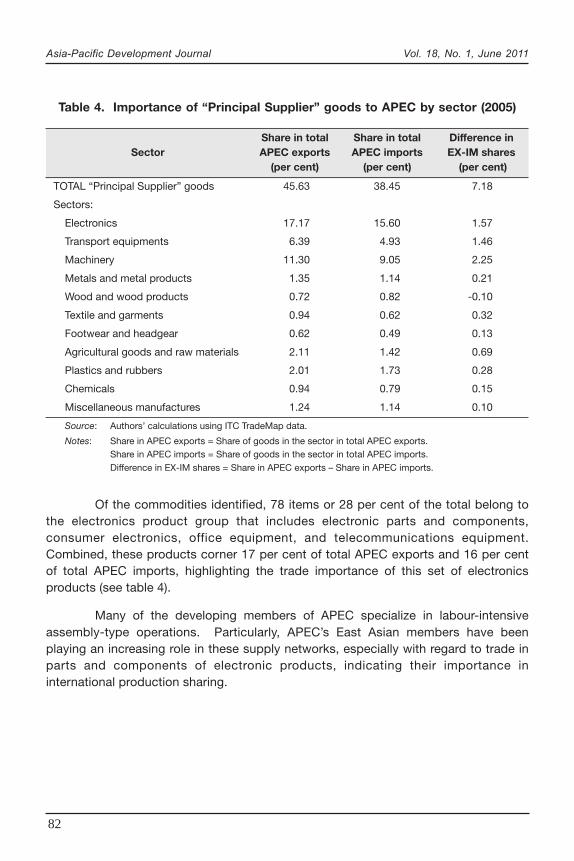

Of the commodities identified, 78 items or 28 per cent of the total belong tothe electronics product group that includes electronic parts and components,consumer electronics, office equipment, and telecommunications equipment.Combined, these products corner 17 per cent of total APEC exports and 16 per centof total APEC imports, highlighting the trade importance of this set of electronicsproducts (see table 4).

Many of the developing members of APEC specialize in labour-intensiveassembly-type operations. Particularly, APEC’s East Asian members have beenplaying an increasing role in these supply networks, especially with regard to trade inparts and components of electronic products, indicating their importance ininternational production sharing.

Table 4. Importance of “Principal Supplier” goods to APEC by sector (2005)

Share in total Share in total Difference inSector APEC exports APEC imports EX-IM shares

(per cent) (per cent) (per cent)

TOTAL “Principal Supplier” goods 45.63 38.45 7.18

Sectors:

Electronics 17.17 15.60 1.57

Transport equipments 6.39 4.93 1.46

Machinery 11.30 9.05 2.25

Metals and metal products 1.35 1.14 0.21

Wood and wood products 0.72 0.82 -0.10

Textile and garments 0.94 0.62 0.32

Footwear and headgear 0.62 0.49 0.13

Agricultural goods and raw materials 2.11 1.42 0.69

Plastics and rubbers 2.01 1.73 0.28

Chemicals 0.94 0.79 0.15

Miscellaneous manufactures 1.24 1.14 0.10

Source: Authors’ calculations using ITC TradeMap data.

Notes: Share in APEC exports = Share of goods in the sector in total APEC exports.Share in APEC imports = Share of goods in the sector in total APEC imports.Difference in EX-IM shares = Share in APEC exports – Share in APEC imports.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

83

For each of the sectors identified in table 3, APEC’s share in world exports isgreater than its share in world imports. However, the discrepancy is very minimal atan average of 2 per cent for all sectors, indicating that while APEC members arestrong suppliers of these goods, they are also strong consumers of such items.4

IV. IMPLICATIONS FOR THE PHILIPPINE TRADENEGOTIATION STRATEGY: CASE STUDY

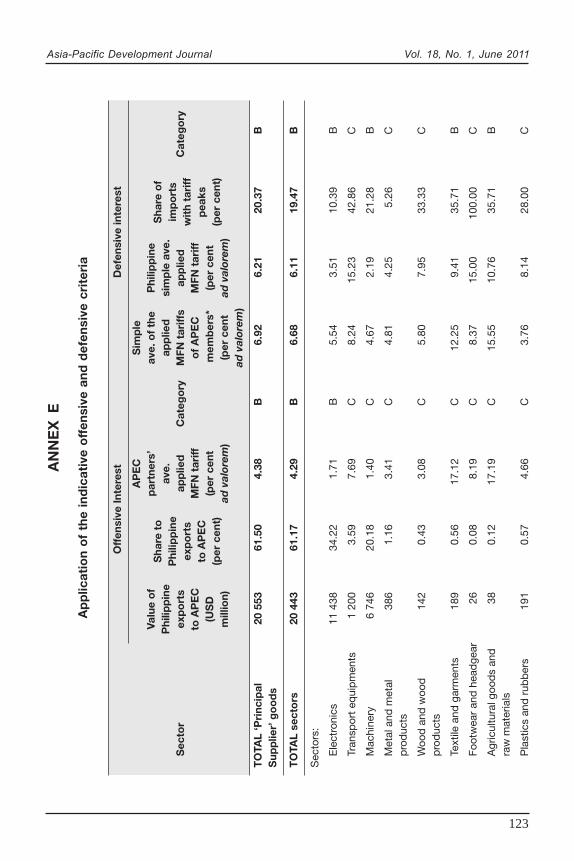

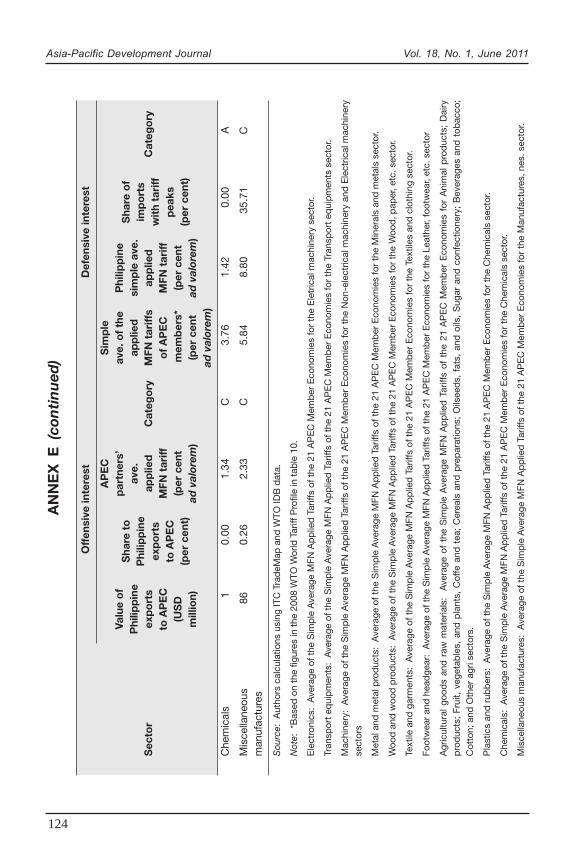

Earlier, it was argued that the sectoral liberalization based on the “principalsupplier” approach would be beneficial to APEC as a whole. However, the impact onthe individual members would vary as in the case of multilateral and regionalliberalization. What are the implications of the proposed modality of liberalization onthe trade negotiation of the Philippines? More specifically, to what extent does thesectoral liberalization serve its offensive and defensive interests?5

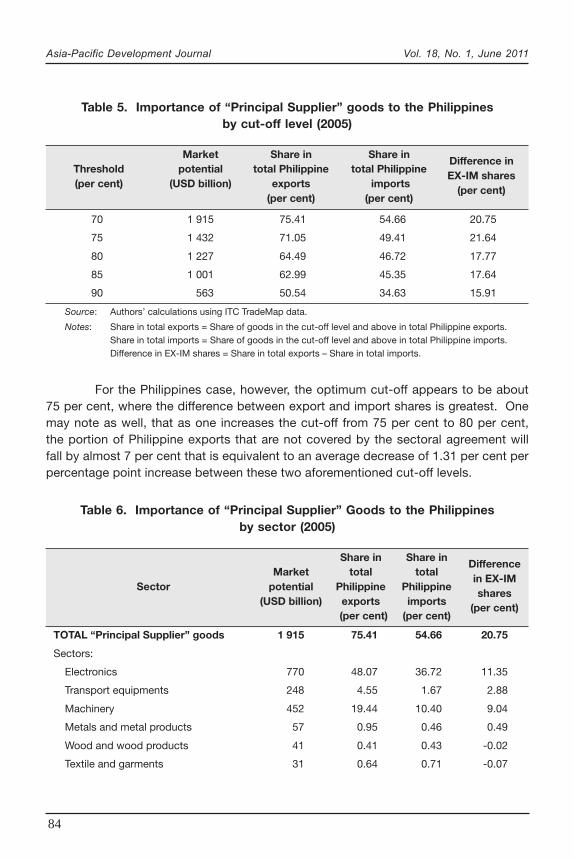

Based on table 5, for the products in which APEC members provide 70 percent and more of world exports (less intra-European Union trade), the Philippines’APEC partners imported $1,915 billion in 2005 from the world. This means thatthe Philippines along with everybody else have improved market access (due tosectoral liberalization) equivalent to the aforementioned value, keeping all otherfactors such as income constant. It could be seen that at the 90 per cent cut-offlevel, market potential available to the Philippines is significantly reduced by morethan two-thirds to $563 billion.

As annex B reports, the products where APEC supplies 70 per cent of theworld’s exports constitute close to 75 per cent of total Philippine exports in 2005.This indicates that the Philippines is a dominant supplier for the set of products wherethere is relatively little free riding if liberalized unilaterally. Furthermore, the differenceat the 70 per cent and 75 per cent between share of selected products in totalexports and imports respectively, are quite substantial.

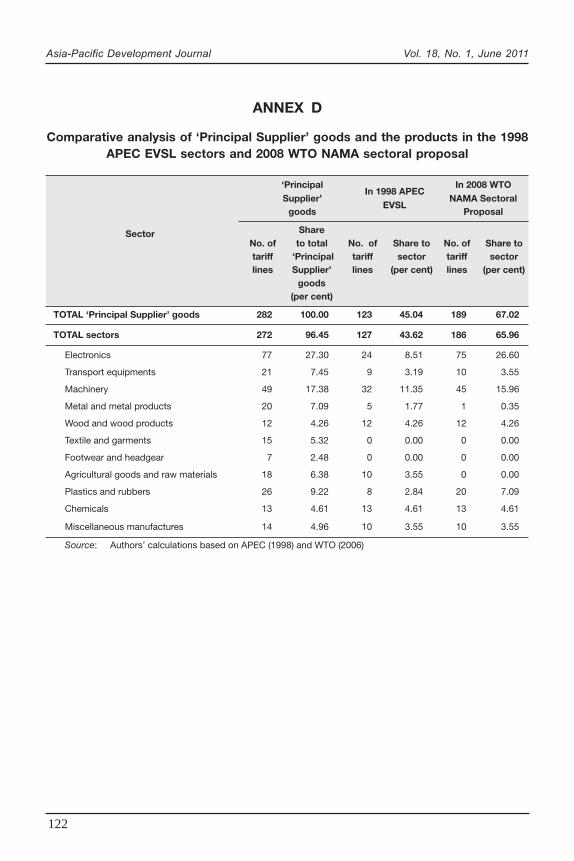

4 A comparison of the ‘principal supplier’ goods with the products proposed for sectoral liberalization inthe WTO Non-Agricultural Market Access (NAMA) in August 2008 is reported in annex D. One notes that65 per cent of goods under the NAMA correspond to the items in the ‘principal supplier’ goods. Amongthe sectors with the highest incidence of correspondence are: electronics, machineries, wood, andchemicals. Annex D also reports the correspondence of the ‘principal supplier’ goods with the goodsproposed under the 1998 APEC EVSL. In contrast to the NAMA comparsion, only 45 per cent of the1998 APEC EVSL ‘goods’ are found in the list of the ‘principal supplier’ goods indicating that the latterhas a wider scope for liberalization than the EVSL.5 Gaining greater market access for exportables constitutes the ‘offensive interest’ in trade negotiationsin this paper. By ‘defensive interest’ is meant preventing the erosion of current levels of protection oncertain ‘sensitive’ sectors.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

84

For the Philippines case, however, the optimum cut-off appears to be about75 per cent, where the difference between export and import shares is greatest. Onemay note as well, that as one increases the cut-off from 75 per cent to 80 per cent,the portion of Philippine exports that are not covered by the sectoral agreement willfall by almost 7 per cent that is equivalent to an average decrease of 1.31 per cent perpercentage point increase between these two aforementioned cut-off levels.

Table 5. Importance of “Principal Supplier” goods to the Philippinesby cut-off level (2005)

Market Share in Share inDifference in

Threshold potential total Philippine total PhilippineEX-IM shares

(per cent) (USD billion) exports imports(per cent)

(per cent) (per cent)

70 1 915 75.41 54.66 20.75

75 1 432 71.05 49.41 21.64

80 1 227 64.49 46.72 17.77

85 1 001 62.99 45.35 17.64

90 563 50.54 34.63 15.91

Source: Authors’ calculations using ITC TradeMap data.

Notes: Share in total exports = Share of goods in the cut-off level and above in total Philippine exports.Share in total imports = Share of goods in the cut-off level and above in total Philippine imports.Difference in EX-IM shares = Share in total exports – Share in total imports.

Table 6. Importance of “Principal Supplier” Goods to the Philippinesby sector (2005)

Share in Share inDifference

Market total totalin EX-IM

Sector potential Philippine Philippineshares

(USD billion) exports imports(per cent)

(per cent) (per cent)

TOTAL “Principal Supplier” goods 1 915 75.41 54.66 20.75

Sectors:

Electronics 770 48.07 36.72 11.35

Transport equipments 248 4.55 1.67 2.88

Machinery 452 19.44 10.40 9.04

Metals and metal products 57 0.95 0.46 0.49

Wood and wood products 41 0.41 0.43 -0.02

Textile and garments 31 0.64 0.71 -0.07

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

85

At the sectoral level, however, there are only two major sectors – electronicsand machineries, which dominate Philippine exports. Eight of the broad sectorsaccount for less than 1 per cent of total Philippine exports (see table 6).

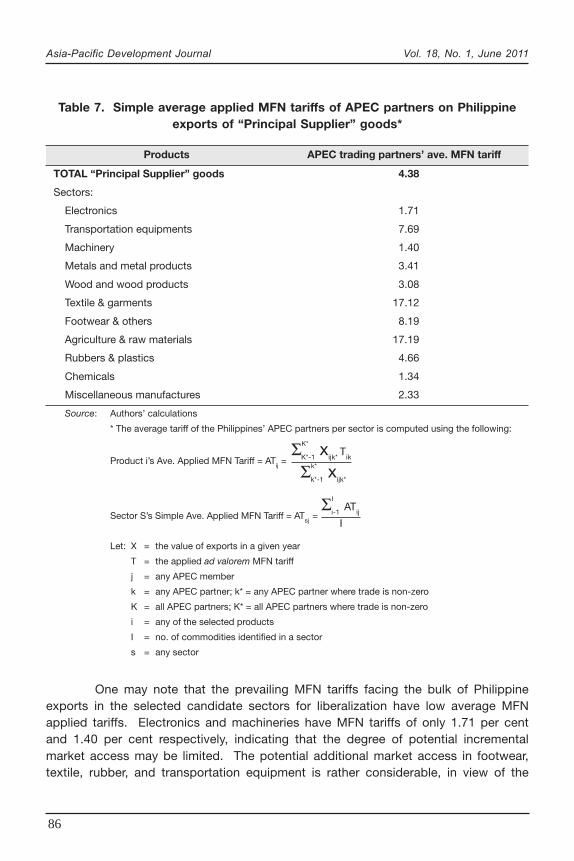

Table 7 reports the MFN tariffs of the Philippine’s APEC partners in the broadsectoral categories for which sectoral liberalization is proposed. To illustrate, theaverage applied MFN tariffs facing Philippine exporters of electronics (or electronicproducts where APEC’s share in the world exports is 70 per cent or greater) in theAPEC market is 4.38 per cent. If the proposed sectoral liberalization proceeds, thenthis figure represents the maximum extent of additional market access made availableto the Philippines, i.e. if there is full elimination of tariffs. As such, the average tariffscan be a measure of the offensive interest of an APEC member served by the sectoralliberalization. The larger the prevailing tariffs facing the member in a particular sector,the greater the market access accorded under a sectoral liberalization programme.Note, however, that the tariffs as reported in the table may be overstated because ofthe overlapping preferential trade agreements currently in place among many APECmembers. One limitation of this study is that it does not take into account the currentRTAs of APEC members in computing for the incremental market access due tosectoral liberalization.

Footwear and headgear 25 0.08 0.05 0.03

Agricultural goods and raw materials 71 0.09 2.28 -2.19

Plastics and rubbers 87 0.60 1.11 -0.51

Chemicals 40 0.00 0.44 -0.44

Miscellaneous manufactures 58 0.29 0.14 0.15

Source: Authors’ calculations using ITC TradeMap data.

Notes: Share in total exports = Share of goods in the sector in total Philippine exports.Share in total imports = Share of goods in the sector in total Philippine imports.Difference in EX-IM shares = Share in total exports – Share in total imports.

Table 6. (continued)

Share in Share inDifference

Market total totalin EX-IM

Sector potential Philippine Philippineshares

(USD billion) exports imports(per cent)

(per cent) (per cent)

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

86

One may note that the prevailing MFN tariffs facing the bulk of Philippineexports in the selected candidate sectors for liberalization have low average MFNapplied tariffs. Electronics and machineries have MFN tariffs of only 1.71 per centand 1.40 per cent respectively, indicating that the degree of potential incrementalmarket access may be limited. The potential additional market access in footwear,textile, rubber, and transportation equipment is rather considerable, in view of the

Table 7. Simple average applied MFN tariffs of APEC partners on Philippineexports of “Principal Supplier” goods*

Products APEC trading partners’ ave. MFN tariff

TOTAL “Principal Supplier” goods 4.38

Sectors:

Electronics 1.71

Transportation equipments 7.69

Machinery 1.40

Metals and metal products 3.41

Wood and wood products 3.08

Textile & garments 17.12

Footwear & others 8.19

Agriculture & raw materials 17.19

Rubbers & plastics 4.66

Chemicals 1.34

Miscellaneous manufactures 2.33

Source: Authors’ calculations

* The average tariff of the Philippines’ APEC partners per sector is computed using the following:

Product i’s Ave. Applied MFN Tariff = ATij =

Sector S’s Simple Ave. Applied MFN Tariff = ATsj

=

Let: X = the value of exports in a given year

T = the applied ad valorem MFN tariff

j = any APEC member

k = any APEC partner; k* = any APEC partner where trade is non-zero

K = all APEC partners; K* = all APEC partners where trade is non-zero

i = any of the selected products

I = no. of commodities identified in a sector

s = any sector

Σk*-1

xijk*

k*

ΣK*-1

xijk*

Tik

K*

Σi-1 AT

ij

I

I

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

87

magnitude of tariffs that will be cut by the rest of the APEC members. However, thevolume of Philippine exports in the aforementioned sectors, save transportationequipment, is not very substantial (see table 6). Perhaps the reason for the lowvolume of exports of the Philippines in footwear, textile, etc. to other APECeconomies is due to high tariff barriers. Thus, the existing profile of tariffs facingPhilippine exports also influences the current distribution and volume of exportsamong the sectors.

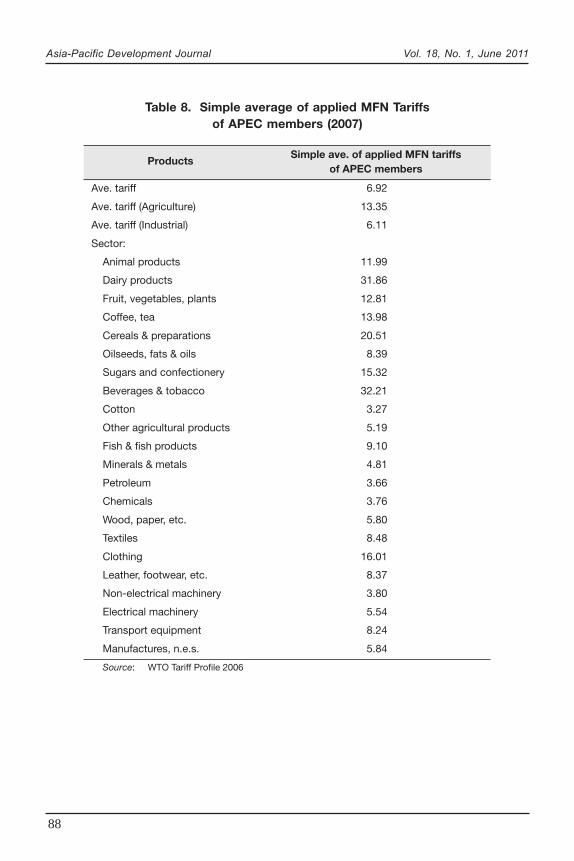

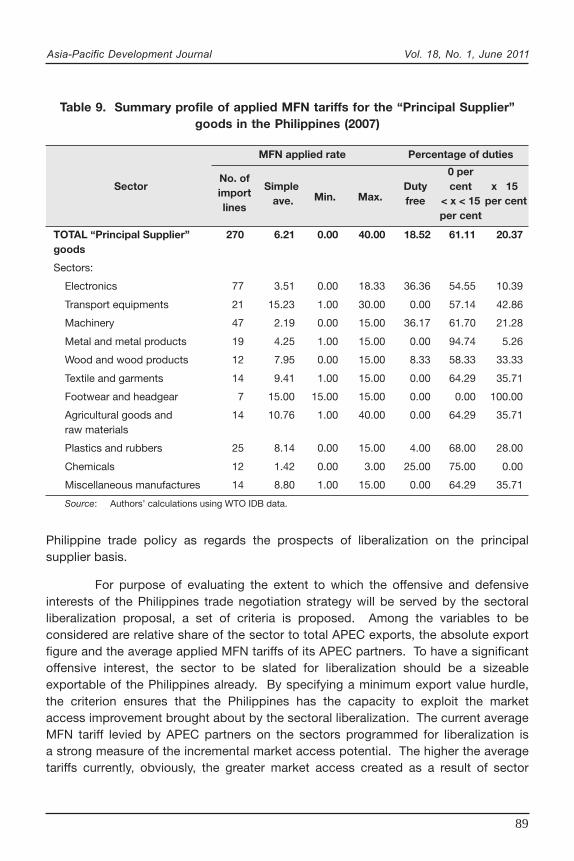

The defensive interest of the Philippines can partially be gauged from thecurrent levels of tariffs it imposes on the candidate sectors for sectoral liberalization,with emphasis on the prevalence of tariff peaks. Table 8 reports the tariff profile of thePhilippines on the sectors of interest. In many instances, the average tariff levels ofthe Philippines on the products selected on the basis of the principal supplier criterion(referred to as “selected” products) are higher than the corresponding average tariffsof its APEC trade partners. As expected, the MFN tariffs on electronics andmachineries are quite low indicating that the selected sectors are not “sensitive”.Interestingly the average tariff of the selected chemical sectors is also quite low. Onthe whole, the average tariff of the selected products for the Philippines is slightlyhigher than the simple average for the whole range of products in the Philippinesindicating that there could be sensitivities in the sample of selected products.Actually, 20 per cent of the tariff lines in the selected products have tariff peaks,defined as tariffs beyond 15 per cent, in the Philippines. Table 9 presents the profileof applied MFN tariffs for the selected goods in the Philippines and highlights theextent of tariff peaks. As reported in table 9, tariff peaks abound in the footwear,transport equipment, textile/garments and miscellaneous sectors indicating thedefensive stance of current trade policy.

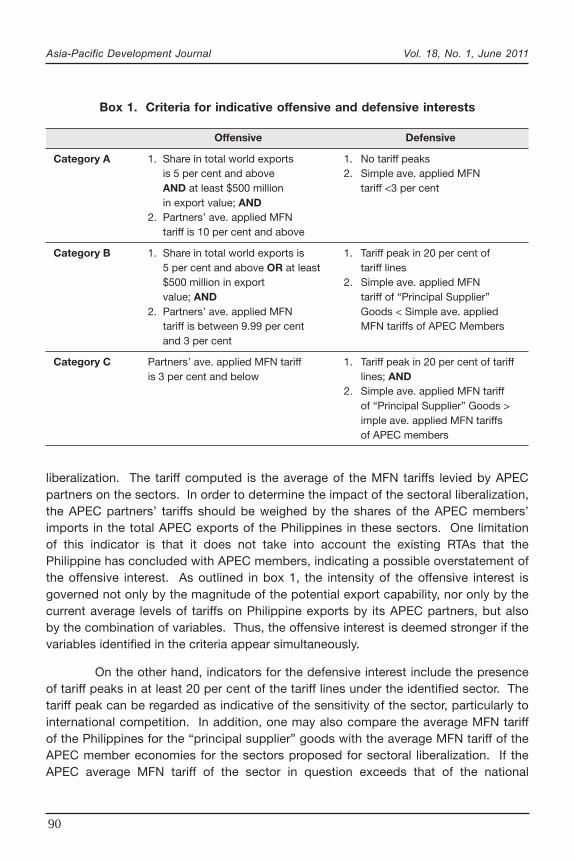

The previous discussion reveals the overlapping defensive and offensiveinterests attached to the selected products for sectoral liberalization. Of interesthowever, is the overall assessment of the proposed modality insofar as it impactsPhilippine trade negotiation strategy. This could be important because the sectoralliberalization that is proposed is essentially a package. In fact, the analytical baseprecludes the practice of picking sectors for the liberalization on mercantilist groundsas was done in previous attempts at sectoral liberalization. One method of evaluatingthe desirability of the proposed modality is to classify the intensity of interest intolevels (Categories A, B or C) consistent with a set of criteria that defines the level. Ofcourse, this method suffers from being static, short term, and ad hoc in formulation.On the other hand, it is quite flexible (the policymaker can devise their own criteria tosuit their priorities) and could easily be understood by the stakeholders. Thus, theoverall assessment of the list of sectors is always dependent on the set of criteria, i.e.subjective. Box 1 is one set of criteria for specifying levels of offensive and interest of

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

88

Table 8. Simple average of applied MFN Tariffsof APEC members (2007)

ProductsSimple ave. of applied MFN tariffs

of APEC members

Ave. tariff 6.92

Ave. tariff (Agriculture) 13.35

Ave. tariff (Industrial) 6.11

Sector:

Animal products 11.99

Dairy products 31.86

Fruit, vegetables, plants 12.81

Coffee, tea 13.98

Cereals & preparations 20.51

Oilseeds, fats & oils 8.39

Sugars and confectionery 15.32

Beverages & tobacco 32.21

Cotton 3.27

Other agricultural products 5.19

Fish & fish products 9.10

Minerals & metals 4.81

Petroleum 3.66

Chemicals 3.76

Wood, paper, etc. 5.80

Textiles 8.48

Clothing 16.01

Leather, footwear, etc. 8.37

Non-electrical machinery 3.80

Electrical machinery 5.54

Transport equipment 8.24

Manufactures, n.e.s. 5.84

Source: WTO Tariff Profile 2006

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

89

Philippine trade policy as regards the prospects of liberalization on the principalsupplier basis.

For purpose of evaluating the extent to which the offensive and defensiveinterests of the Philippines trade negotiation strategy will be served by the sectoralliberalization proposal, a set of criteria is proposed. Among the variables to beconsidered are relative share of the sector to total APEC exports, the absolute exportfigure and the average applied MFN tariffs of its APEC partners. To have a significantoffensive interest, the sector to be slated for liberalization should be a sizeableexportable of the Philippines already. By specifying a minimum export value hurdle,the criterion ensures that the Philippines has the capacity to exploit the marketaccess improvement brought about by the sectoral liberalization. The current averageMFN tariff levied by APEC partners on the sectors programmed for liberalization isa strong measure of the incremental market access potential. The higher the averagetariffs currently, obviously, the greater market access created as a result of sector

Table 9. Summary profile of applied MFN tariffs for the “Principal Supplier”goods in the Philippines (2007)

MFN applied rate Percentage of duties

No. of0 per

Sectorimport

SimpleMin. Max.

Duty cent x 15

lines ave. free < x < 15 per cent

per cent

TOTAL “Principal Supplier” 270 6.21 0.00 40.00 18.52 61.11 20.37goods

Sectors:

Electronics 77 3.51 0.00 18.33 36.36 54.55 10.39

Transport equipments 21 15.23 1.00 30.00 0.00 57.14 42.86

Machinery 47 2.19 0.00 15.00 36.17 61.70 21.28

Metal and metal products 19 4.25 1.00 15.00 0.00 94.74 5.26

Wood and wood products 12 7.95 0.00 15.00 8.33 58.33 33.33

Textile and garments 14 9.41 1.00 15.00 0.00 64.29 35.71

Footwear and headgear 7 15.00 15.00 15.00 0.00 0.00 100.00

Agricultural goods and 14 10.76 1.00 40.00 0.00 64.29 35.71raw materials

Plastics and rubbers 25 8.14 0.00 15.00 4.00 68.00 28.00

Chemicals 12 1.42 0.00 3.00 25.00 75.00 0.00

Miscellaneous manufactures 14 8.80 1.00 15.00 0.00 64.29 35.71

Source: Authors’ calculations using WTO IDB data.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

90

Box 1. Criteria for indicative offensive and defensive interests

Offensive Defensive

Category A 1. Share in total world exports 1. No tariff peaksis 5 per cent and above 2. Simple ave. applied MFNAND at least $500 million tariff <3 per centin export value; AND

2. Partners’ ave. applied MFNtariff is 10 per cent and above

Category B 1. Share in total world exports is 1. Tariff peak in 20 per cent of5 per cent and above OR at least tariff lines$500 million in export 2. Simple ave. applied MFNvalue; AND tariff of “Principal Supplier”

2. Partners’ ave. applied MFN Goods < Simple ave. appliedtariff is between 9.99 per cent MFN tariffs of APEC Membersand 3 per cent

Category C Partners’ ave. applied MFN tariff 1. Tariff peak in 20 per cent of tariffis 3 per cent and below lines; AND

2. Simple ave. applied MFN tariffof “Principal Supplier” Goods >imple ave. applied MFN tariffsof APEC members

liberalization. The tariff computed is the average of the MFN tariffs levied by APECpartners on the sectors. In order to determine the impact of the sectoral liberalization,the APEC partners’ tariffs should be weighed by the shares of the APEC members’imports in the total APEC exports of the Philippines in these sectors. One limitationof this indicator is that it does not take into account the existing RTAs that thePhilippine has concluded with APEC members, indicating a possible overstatement ofthe offensive interest. As outlined in box 1, the intensity of the offensive interest isgoverned not only by the magnitude of the potential export capability, nor only by thecurrent average levels of tariffs on Philippine exports by its APEC partners, but alsoby the combination of variables. Thus, the offensive interest is deemed stronger if thevariables identified in the criteria appear simultaneously.

On the other hand, indicators for the defensive interest include the presenceof tariff peaks in at least 20 per cent of the tariff lines under the identified sector. Thetariff peak can be regarded as indicative of the sensitivity of the sector, particularly tointernational competition. In addition, one may also compare the average MFN tariffof the Philippines for the “principal supplier” goods with the average MFN tariff of theAPEC member economies for the sectors proposed for sectoral liberalization. If theAPEC average MFN tariff of the sector in question exceeds that of the national

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

91

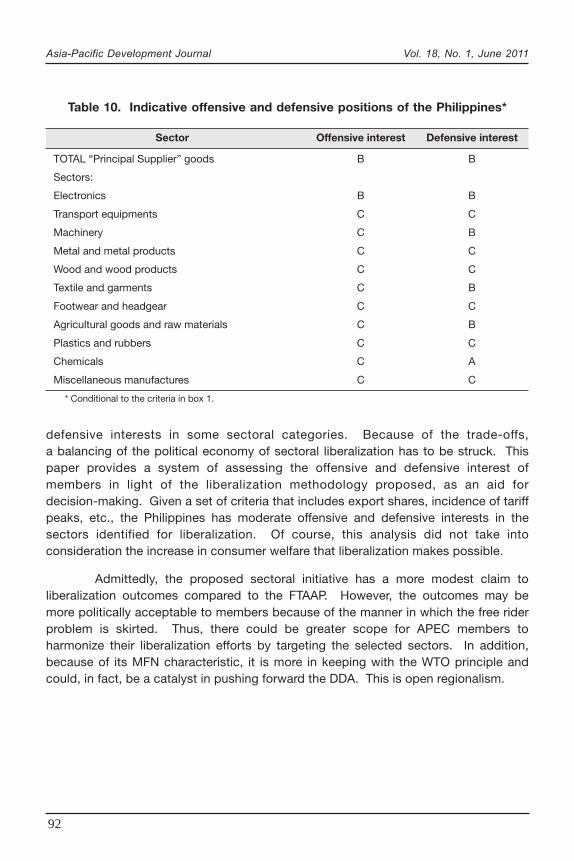

average, then one can infer that the defensive interest in that sector is relativelypronounced. As the box shows, the intensity of the defensive interest is a function ofthe prevalence of tariff peaks and relative magnitudes of the MFN tariffs of the sectorin the region against the national average. Under this scheme, defensive interest isconsidered strong when the criteria of the incidence of tariff peaks and the magnitudeof average sectoral tariffs are simultaneously met. The position is said to bemoderate or weak when either one of the criteria are met, but not simultaneously.Table 10 summarizes the degree of offensive and defensive interests of thePhilippines in each of the product groups identified for liberalization on a sectorallevel, according to categories and criteria outlined in box 1.

Again, the criteria outlined in the box can be modified depending on thepreference of the policymakers. Consequently, the definitions of strong, moderate orweak interest could vary depending on the criteria set. While this feature may renderthe process quite ad hoc, it nevertheless makes it quite flexible for purpose of policyresearch.

V. FINAL REMARKS

APEC has been at a crossroads for a number of years already. After theinitial enthusiasm of Bogor waned in the wake of the Asian financial crisis, APEC triedto revive the trade liberalization agenda. The current initiative, FTAAP, has not beenfully supported by all members. While ambitious, a multitude of political sensitivitiesand the general RTA “fatigue” factor prevent the FTAAP from advancing forwardstrongly. Yet, it is still one of the most concrete ideas tabled to advance the pillar oftrade liberalization.

This paper puts forward an alternative to FTAAP. The modality is sectoralliberalization on an MFN basis, founded on the analytical basis of “principal supplier”approach and a variant of the non-preferential trading club. In a departure from theill-fated EVSL, the proposed initiative chooses the sectors to be liberalized on thebasis of minimizing free riding by non-APEC members. Candidates for sectoralliberalization are those sectors where APEC economies supply a significant portion ofworld exports. Using a benchmark or cut-off rate of 70 per cent, over 282 productsare identified for sectoral liberalization. These products, in total, constitute close tohalf of all APEC exports and about 40 per cent of APEC imports in 2005.

Of course, while the APEC, as a collective, stands to benefit from theproposed sectoral liberalization, the impact on the individual member differs from oneeconomy to another. The case study on the Philippines showed that sectoralliberalization, whilst serving its offensive interests, have a negative impact on the

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

92

defensive interests in some sectoral categories. Because of the trade-offs,a balancing of the political economy of sectoral liberalization has to be struck. Thispaper provides a system of assessing the offensive and defensive interest ofmembers in light of the liberalization methodology proposed, as an aid fordecision-making. Given a set of criteria that includes export shares, incidence of tariffpeaks, etc., the Philippines has moderate offensive and defensive interests in thesectors identified for liberalization. Of course, this analysis did not take intoconsideration the increase in consumer welfare that liberalization makes possible.

Admittedly, the proposed sectoral initiative has a more modest claim toliberalization outcomes compared to the FTAAP. However, the outcomes may bemore politically acceptable to members because of the manner in which the free riderproblem is skirted. Thus, there could be greater scope for APEC members toharmonize their liberalization efforts by targeting the selected sectors. In addition,because of its MFN characteristic, it is more in keeping with the WTO principle andcould, in fact, be a catalyst in pushing forward the DDA. This is open regionalism.

Table 10. Indicative offensive and defensive positions of the Philippines*

Sector Offensive interest Defensive interest

TOTAL “Principal Supplier” goods B B

Sectors:

Electronics B B

Transport equipments C C

Machinery C B

Metal and metal products C C

Wood and wood products C C

Textile and garments C B

Footwear and headgear C C

Agricultural goods and raw materials C B

Plastics and rubbers C C

Chemicals C A

Miscellaneous manufactures C C

* Conditional to the criteria in box 1.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

93

REFERENCES

Aggarwal, Vinod K. (2007). “The political economy of a free trade area of the Asia-Pacific: A USperspective”. In Charles Morrison and Eduardo Pedrosa, eds. An APEC Trade Agenda?:The Political Economy of a Free Trade Area of the Asia-Pacific. (Singapore: Institute ofSoutheast Asian Studies). Available from www.waseda-giari.jp/sysimg/imgs/200908_si_aggarwal_rp_2.pdf.

Asia-Pacific Economic Cooperation (1998). APEC SOM Chair’s report to the Ministers responsible fortrade, Kuching, Sarawak, Malaysia, 22-23 June.

Bergsten, C. Fred (1997). “Open regionalism”. Peterson Institute for International EconomicsWorking Paper 97-3. (Washington, D.C.: Peterson Institute for International Economics).Available from www.iie.com/publications/wp/wp.cfm?ResearchID=152.

(2007). “Towards a Free Trade Area of the Pacific”. Institute for International EconomicsPolicy Briefs in International Economics No. PB07-02. (Washington, D.C.: PetersonInstitute for International Economics). Available from http://www.piie.com/publications/pb/pb07-2.pdf.

Bhagwati, Jagdish and Arvind Panagariya (1996). “Preferential trading areas and multilateralism:strangers, friends or foes?” in Jagdish Bhagwati and Arvind Panagariya, eds., TheEconomics of Preferential Trade Agreements (Washington, D.C.: AEI Press).

International Trade Center (2010). TradeMap. Available from http://www.trademap.org

Kemp, Maurray C. and Henry Y. Wan (1976). “An elementary proposition concerning the formation ofcustoms unions”, Journal of International Economics, vol. 6 (February), pp. 95-97.Available from www2.econ.iastate.edu/classes/econ655/lapan/Readings/ElementaryPropositionConcerningCustomsUnionsKEMPWAN.pdf.

Raimondos-Moller, Pascalis and Alan Woodland (2006), “Non-preferential trading clubs”, Journal ofInternational Economics, vol. 68, No. 1 (January), pp 79-91.

United States Census Bureau (2010). “Foreign Trade Statistics”. Available from www.census.gov.

Wonnacott, Paul (1994). “Merchandise Trade in the APEC Region: is there scope for liberalization onan MFN basis?”, The World Economy, Special Issue on Global Trade Policy, pp. 33-51.

World Trade Organization (1998). APEC’s “Accelerated Tariff Liberalization” (ATL) Initiative –Communication from New Zealand. WT/GC/W/138/Add.1.

Negotiating Group on Market Access (2008). Draft Modalities for Non-agricultural MarketAccess, 3rd rev. TN/MA/W/103/Rev. 2 (10 July). Available from www.wto.org/english/tratop_e/markacc_e/markacc_chair_texts07_e.htm.

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

94

AN

NE

X A

Pro

du

cts

for

wh

ich

AP

EC

pro

vid

e th

e p

rin

cip

al s

up

ply

of

wo

rld

exp

ort

s (2

005)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

185

4219

Mon

olith

ic in

tegr

ated

circ

uits

, nes

3 56

43

564

3 56

410

0.00

100.

000.

00

290

0120

She

ets

and

pla

tes

of p

olar

isin

g m

ater

ial

4 24

14

253

4 24

599

.71

99.8

90.

18

390

1380

Op

tical

dev

ices

, ap

plia

nces

and

inst

rum

ents

,28

838

29 3

8729

167

98.1

398

.87

0.74

nes,

of t

his

Cha

pte

r

484

7010

Ele

ctro

nic

calc

ulat

ors

cap

able

of o

per

w/o

an

1 53

51

700

1 55

490

.30

98.7

98.

49ex

tern

al s

ourc

e of

pow

er

584

5691

Mac

hine

too

ls fo

r d

ry e

tchi

ng p

rinte

d c

ircui

ts2

672

2 72

92

706

97.9

198

.74

0.83

685

1999

Sou

nd r

epro

duc

ing

app

arat

us, n

ot8

902

9 57

99

023

92.9

398

.66

5.73

inco

rpor

atin

g a

soun

d r

ecor

der

, nes

795

0639

Gol

f eq

uip

men

t ne

s1

790

1 86

11

823

96.2

298

.23

2.01

885

2713

Rad

io a

pp

arat

us n

es w

ith s

ound

rec

ord

ing/

2 32

92

906

2 37

280

.16

98.1

918

.03

rep

rod

ucin

g

985

2290

Par

ts a

nd a

cces

sorie

s of

ap

par

atus

of

14 0

6515

035

14 3

3793

.55

98.1

14.

56he

adin

g N

os. 8

5.19

to

85.2

1, n

es

1095

0410

Vid

eo g

ames

of a

kin

d u

sed

with

a t

elev

isio

n5

994

7 04

16

114

85.1

498

.05

12.9

1re

ceiv

er

1185

4240

Hyb

rid in

tegr

ated

circ

uits

18 9

8019

995

19 3

7994

.92

97.9

43.

02

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

95

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

1285

2320

Unr

ecor

ded

mag

netic

dis

cs3

412

3 65

13

497

93.4

697

.59

4.13

1385

2731

Rad

io b

road

rec

eive

r co

mb

ind

with

sou

nd2

932

3 44

23

006

85.1

897

.55

12.3

7re

cord

ing

or r

epro

duc

ing

app

arat

us n

es

1485

0780

Ele

ctric

acc

umul

ator

s, n

es7

754

8 53

47

988

90.8

697

.07

6.21

1585

4290

Par

ts o

f ele

ctro

nic

inte

grat

ed c

ircui

ts a

nd10

616

11 1

5510

948

95.1

796

.97

1.80

mic

roas

sem

blie

s

1685

1650

Mic

row

ave

oven

s2

843

3 42

82

933

82.9

396

.92

13.9

9

1795

0490

Art

funf

air,

gam

e ta

b, p

inta

b, s

p t

ab c

asin

o7

836

9 18

58

086

85.3

296

.91

11.5

9ga

me

& a

uto

bow

l alle

y eq

uip

1895

0341

Stu

ffed

toy

s re

pre

sent

ing

anim

als

or2

309

2 74

82

386

84.0

296

.75

12.7

3no

n-hu

man

cre

atur

es

1985

2190

Vid

eo r

ecor

din

g or

rep

rod

ucin

g ap

par

atus

nes

12 7

0516

096

13 1

6578

.93

96.5

117

.58

2090

0211

Ob

ject

ive

lens

es f

cam

eras

, pro

ject

ors/

2 49

02

760

2 58

190

.23

96.4

86.

25p

hoto

grap

hic

enla

rger

s/re

duc

ers

2174

1021

Foil

of r

efin

ed c

opp

er, b

acke

d2

539

2 85

42

639

88.9

696

.19

7.23

2285

3222

Ele

ctric

al c

apac

itors

, fix

ed, a

lum

iniu

m2

874

3 32

92

989

86.3

296

.12

9.80

elec

trol

ytic

, nes

2339

0330

Acr

ylon

itrile

-but

adie

ne-s

tyre

ne (A

BS

)6

022

6 95

46

266

86.6

096

.09

9.49

cop

olym

ers

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

96

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

2426

1390

Mol

ybd

enum

ore

s an

d c

once

ntra

tes

nes

3 24

83

383

3 38

096

.01

96.0

90.

08

2539

2640

Sta

tuet

tes

and

oth

er o

rnam

enta

l art

icle

s,1

902

2 19

71

985

86.5

795

.84

9.27

of p

last

ics

2664

0219

Sp

orts

foot

wea

r, ou

ter

sole

s an

d u

pp

ers

2 11

72

591

2 21

081

.70

95.7

914

.09

of r

ubb

er o

r p

last

ics,

nes

2784

7130

Por

tab

le d

igita

l com

put

ers

<10

kg

44 5

2956

003

46 5

0479

.51

95.7

516

.24

2885

2390

Pre

par

ed u

nrec

ord

ed m

edia

for

soun

d9

432

12 1

869

855

77.4

195

.71

18.3

0re

cord

ing

or o

ther

phe

nom

ena

nes

2984

0721

Out

boa

rd m

otor

s, s

par

k-ig

nitio

n1

943

2 45

52

035

79.1

295

.48

16.3

6

reci

pro

catin

g or

rot

ary

typ

e

3090

1390

Par

ts a

nd a

cces

sorie

s of

op

tical

ap

plia

nces

8 96

09

753

9 38

791

.88

95.4

53.

57an

d in

stru

men

ts, n

es

3142

0212

Trun

ks, s

uit-

case

s &

sim

con

tain

er w

ith/o

uter

4 27

15

068

4 47

584

.27

95.4

411

.17

surf

ace

of p

last

ics/

text

iles

3215

1190

Pal

m o

il an

d it

s fr

actio

ns r

efin

ed b

ut n

ot6

094

6 96

36

388

87.5

195

.39

7.88

chem

ical

ly m

odifi

ed

3385

4250

Ele

ctro

nic

mic

roas

sem

blie

s7

588

8 38

27

966

90.5

395

.26

4.73

3416

0590

Mol

lusc

s an

d o

ther

aq

uatic

inve

rteb

rate

s1

613

1 96

01

699

82.3

294

.96

12.6

4p

rep

ared

or

pre

serv

ed

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

97

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

3526

1310

Mol

ybd

enum

con

cent

rate

s, r

oast

ed4

427

5 84

84

665

75.6

994

.90

19.2

1

3685

4230

Mon

olith

ic in

tegr

ated

circ

uits

72 8

9682

689

76 8

7688

.16

94.8

26.

66

3795

0390

Toys

nes

6 11

87

941

6 45

577

.05

94.7

817

.73

3802

0319

Sw

ine

cuts

, fre

sh o

r ch

illed

, nes

1 65

05

369

1 74

530

.74

94.5

863

.84

3985

1890

Par

ts o

f mic

rop

hone

s, lo

udsp

eakr

s,2

168

2 56

52

293

84.5

494

.56

10.0

2he

adp

hone

s, e

arp

hone

s &

ele

c so

und

am

pli

4084

1451

Fans

: ta

ble

, roo

f etc

. w a

sel

f-co

nt e

lec

mtr

2 59

12

974

2 74

187

.14

94.5

47.

40of

an

outp

ut n

t ex

cdg

125

W

4187

1140

Mot

orcy

cles

with

rec

ipro

catg

pis

ton

engi

ne2

203

3 28

22

332

67.1

194

.44

27.3

3d

isp

lacg

> 5

00 c

c to

800

cc

4208

0212

Alm

ond

s, fr

esh

or d

ried

, she

lled

or

pee

led

1 55

22

270

1 64

668

.38

94.3

325

.95

4390

0691

Par

ts a

nd a

cces

sorie

s fo

r p

hoto

grap

hic

2 01

22

297

2 13

987

.59

94.0

96.

50ca

mer

as

4440

1519

Glo

ves

nes

of r

ubb

er1

823

2 11

61

942

86.1

793

.90

7.73

4585

3120

Ind

icat

or p

anel

s in

corp

orat

g liq

uid

cry

stal

9 29

312

453

9 89

774

.62

93.8

919

.27

dev

ice/

light

em

ittg

dio

de

4685

2721

Rad

io r

ecen

t ca

pab

l of o

p w

/o e

xt s

ourc

e5

257

8 38

65

605

62.6

893

.78

31.1

0of

pow

er f

mot

or v

eh, c

omb

ind

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

98

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

4764

0319

Sp

orts

foot

wea

r, o/

t sk

i, ou

tr s

ole

of r

br/

pla

s/3

518

4 41

13

756

79.7

693

.67

13.9

1le

athe

r &

up

per

of l

eath

er

4885

3224

Ele

ctric

al c

apac

itors

, fix

ed,

5 10

15

970

5 44

785

.43

93.6

48.

21ce

ram

ic d

iele

ctric

, mul

tilay

er, n

es

4985

4121

Tran

sist

ors,

oth

tha

n p

hoto

sens

it,4

568

5 11

14

881

89.3

993

.59

4.20

w a

dis

sip

atio

n ra

te <

1 W

5085

1830

Hea

dp

hone

s, e

arp

hone

s an

d c

omb

ined

2 61

93

417

2 80

176

.66

93.5

216

.86

mic

rop

hone

/sp

eake

r se

ts

5190

1049

Ap

par

atus

for

dra

win

g se

mic

ond

ucto

r1

675

1 80

51

794

92.8

093

.36

0.56

circ

uits

nes

5285

3400

Prin

ted

circ

uits

25 9

6330

150

27 8

4686

.11

93.2

47.

13

5340

0121

Nat

ural

rub

ber

in s

mok

ed s

heet

s1

860

2 00

42

001

92.8

492

.94

0.10

5484

7170

Com

put

er d

ata

stor

age

units

41 0

9156

180

44 2

1973

.14

92.9

319

.79

5564

0299

Foot

wea

r, ou

ter

sole

s/up

per

s of

rub

ber

6 88

28

796

7 41

178

.24

92.8

614

.62

or p

last

ics,

nes

5695

0510

Art

icle

s fo

r C

hris

tmas

fest

iviti

es1

849

2 32

71

993

79.4

792

.78

13.3

1

5785

4190

Par

ts o

f mou

nted

pie

zo-e

lect

ric c

ryst

als

3 40

63

787

3 67

489

.95

92.7

22.

77an

d s

emic

ond

ucto

r d

evic

es

5885

1829

Loud

spea

kers

, nes

2 59

33

218

2 79

880

.58

92.6

712

.09

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

99

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

5985

2090

Mag

netic

tap

e re

cord

ers

and

oth

er s

ound

1 87

83

346

2 02

756

.12

92.6

136

.49

reco

rdin

g ap

par

atus

, nes

6040

0122

Tech

nica

lly s

pec

ified

nat

ural

rub

ber

(TS

NR

)3

963

4 32

14

284

91.7

292

.51

0.79

6190

0912

Ele

ctro

stat

ic p

hoto

-cop

ying

ap

par

atus

,3

331

5 61

43

604

59.3

392

.42

33.0

9in

dire

ct p

roce

ss t

ype

6290

3141

Op

tical

inst

rum

ents

for

chec

king

1 56

91

722

1 69

891

.09

92.3

81.

29se

mic

ond

ucto

r w

afer

s

6386

0900

Car

go c

onta

iner

s d

esig

nd t

o b

e ca

rrid

by

6 33

37

289

6 85

986

.87

92.3

35.

46on

e or

mor

e m

odes

of t

rans

por

t

6429

1736

Tere

pht

halic

aci

d a

nd it

s sa

lts5

902

7 48

06

396

78.9

092

.28

13.3

8

6587

1200

Bic

ycle

s an

d o

ther

cyc

les

(incl

udin

g3

211

4 85

73

480

66.1

192

.27

26.1

6d

eliv

ery

tric

ycle

s), n

ot m

otor

ised

6664

0411

Sp

orts

foot

wea

r w

ith o

uter

sol

es o

f rub

ber

1 68

72

851

1 82

859

.16

92.2

533

.09

or p

last

ics

& u

pp

ers

of t

ex m

at

6784

7160

Com

put

er in

put

/out

put

s, w

ith/w

ithou

t54

827

73 5

1759

457

74.5

892

.21

17.6

3st

orag

e

6895

0691

Gym

nasi

um o

r at

hlet

ics

artic

les

and

2 93

43

898

3 18

475

.28

92.1

716

.89

equi

pm

ent

6980

0110

Tin

not

allo

yed

unw

roug

ht2

242

2 54

32

437

88.1

792

.01

3.84

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

100

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

7085

2313

Unr

ecor

ded

mag

netic

tap

es, o

f a w

idth

1 98

92

945

2 16

267

.54

91.9

924

.45

exce

edin

g 6.

5 m

m

7184

1510

Air

cond

ition

ing

mac

hine

s w

ind

ow o

r w

all

6 07

57

245

6 60

883

.86

91.9

38.

07ty

pes

, sel

f-co

ntai

ned

7285

1721

Facs

imile

s m

achi

nes

1 68

52

350

1 83

571

.70

91.8

320

.13

7329

0321

Vin

yl c

hlor

ide

(chl

oroe

thyl

ene)

1 60

21

916

1 74

883

.61

91.6

58.

04

7485

4091

Par

ts o

f cat

hod

e-ra

y tu

bes

1 52

81

834

1 66

883

.29

91.5

88.

29

7585

2830

Vid

eo p

roje

ctor

s4

268

5 77

14

663

73.9

591

.53

17.5

8

7672

1030

Flat

rol

led

i/na

s, e

lect

roly

tical

ly z

inc

coat

ed2

350

4 04

12

570

58.1

691

.46

33.3

0>

600

mm

7790

0190

Pris

ms,

mirr

ors

and

othe

r op

tical

ele

men

ts4

669

5 33

75

108

87.4

891

.41

3.93

of a

ny m

ater

ial,

unm

ount

ed, n

es

7885

4140

Pho

tose

nsiti

ve s

emic

ond

uct

dev

ice,

12 0

0115

736

13 1

3976

.26

91.3

315

.07

pho

tovo

ltaic

cel

ls &

ligh

t em

it d

iod

es

7940

0129

Nat

ural

rub

ber

in o

ther

form

s ne

s1

820

2 03

41

992

89.4

791

.33

1.86

8060

0292

Kni

tted

or

croc

hete

d fa

bric

s, o

f cot

ton,

nes

4 67

65

360

5 12

187

.23

91.3

04.

07

8190

3082

Inst

rum

ents

for

chec

king

sem

icon

duc

tor

2 57

32

899

2 82

988

.76

90.9

62.

20w

afer

s

8244

1213

Ply

woo

d, o

uter

ply

of t

rop

ical

har

dw

ood

,1

635

2 15

21

798

75.9

890

.94

14.9

6p

ly <

6 m

m

Asia-Pacific Development Journal Vol. 18, No. 1, June 2011

101

AN

NE

X A

(co

nti

nu

ed)

Exp

ort

s (U

SD

bill

ion)

Sha

re (p

erce

ntag

e)

Wo

rld

To w

orl

d

HS

less

less

Ran

kco

de

Des

crip

tio

nA

PE

CW

orl

din

tra-

To w

orl

d in

tra-

Diff

eren

ceE

uro

pea

nE

uro

pea

nU

nio

nU

nio

ntr

ade

rad

e

8347

0321

Che

mic

al w

ood

pul

p, s

oda

or s

ulp

hate

,6

538

9 61

67

209

68.0

090

.69

22.6

9co

nife

rous

, sem

i-b

l or

ble

ache

d, n

es

8444

0320

Logs

, pol

es, c

onife

rous

nes

3 89

25

515

4 29

470

.56

90.6

320

.07

8584

7180

Uni

ts o

f aut

omat

ic d

ata

pro

cess

ing

18 0

9327

349

20 0

0966

.16

90.4

224

.26

equi

pm

ent

nes

8685

1711

Line

tel

epho

ne s

ets

with

cor

dle

ss h

and

sets

4 01

05

369

4 44

374

.69

90.2

715

.58

8785

4110

Dio

des

, oth

er t

han

pho

tose

nsiti

ve o

r lig

ht5

496

6 80

86

094

80.7

390

.19

9.46

emitt

ing

dio

des

8885

2821

Col

or v

ideo

mon

itors

3 73

25

470

4 14

068

.23

90.1

621

.93

8985

4129

Tran

sist

ors,

oth

er t

han

pho

tose

nsiti

ve11

432

13 6

1412

688

83.9

790

.10

6.13

tran

sist

ors,

nes

9054

0752

Wov

en fa

bric

s, >

/= 8

5 p

er c

ent

of t

extu

red

3 93

04

696

4 36

683

.69

90.0

26.

33p

olye

ster

fila

men

ts, d

yed

, nes

9151

0111

Gre

asy

shor

n w

ool,

not

card

ed o

r co

mb

ed1

551

1 85

31

724

83.7

089

.96

6.26

9239

0740

Pol

ycar

bon

ates

5 24

96

748

5 84

077

.79

89.8

912

.10

9384

7330

Par

ts &

acc

esso

ries

of a

utom

atic

dat

a13

9 20

118

4 66

515

4 87

675

.38

89.8

814

.50

pro

cess

g m

achi