Embed Size (px)

Citation preview

Background Material

Seminar on

Revised Schedule VI

16th June 2012

Hotel EROS, Nehru Place, New Delhi

Organised by

Northern India Regional Council of The Institute of Chartered Accountants of India

Northern India Regional Council ofTHE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

"ICAI Bhawan", 4th & 5th Floor, "Annexe" Indraprastha Marg, New Delhi - 110 002, IndiaTel. : 011 30100500 Fax : 30100509

E-mail : [email protected], Website : nirc-icai.org

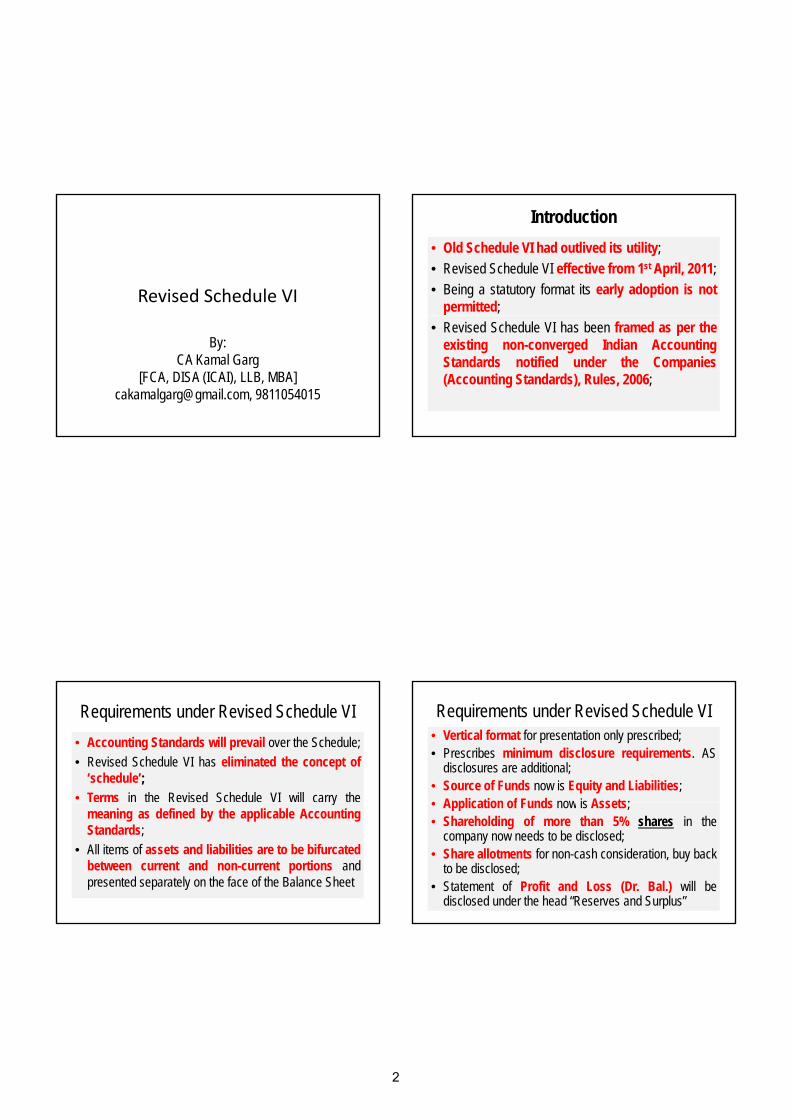

Revised Schedule VI

By:CA Kamal Garg

[FCA, DISA (ICAI), LLB, MBA][email protected], 9811054015

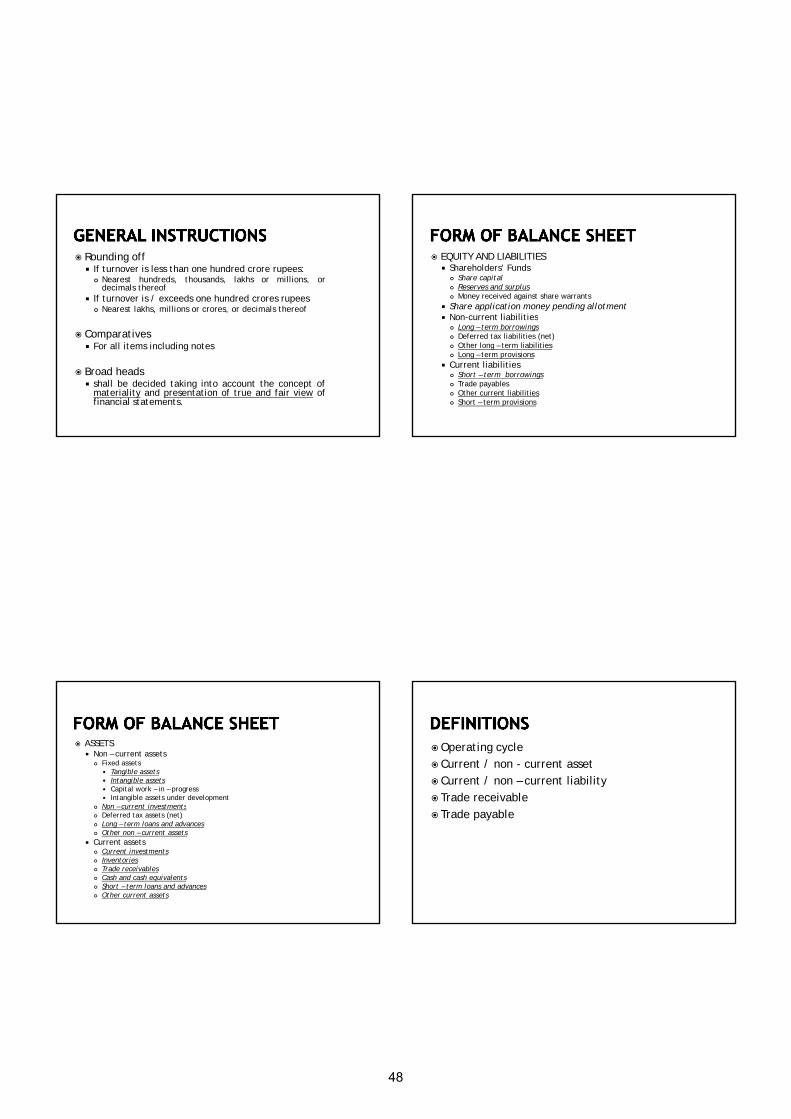

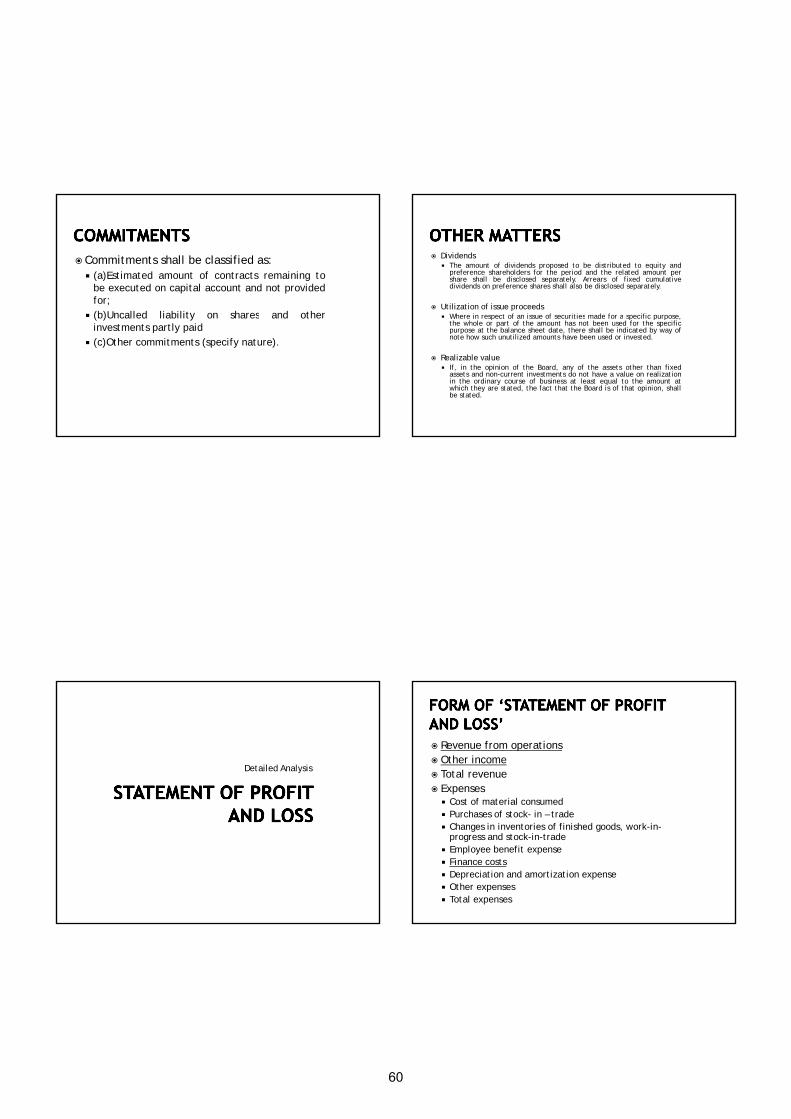

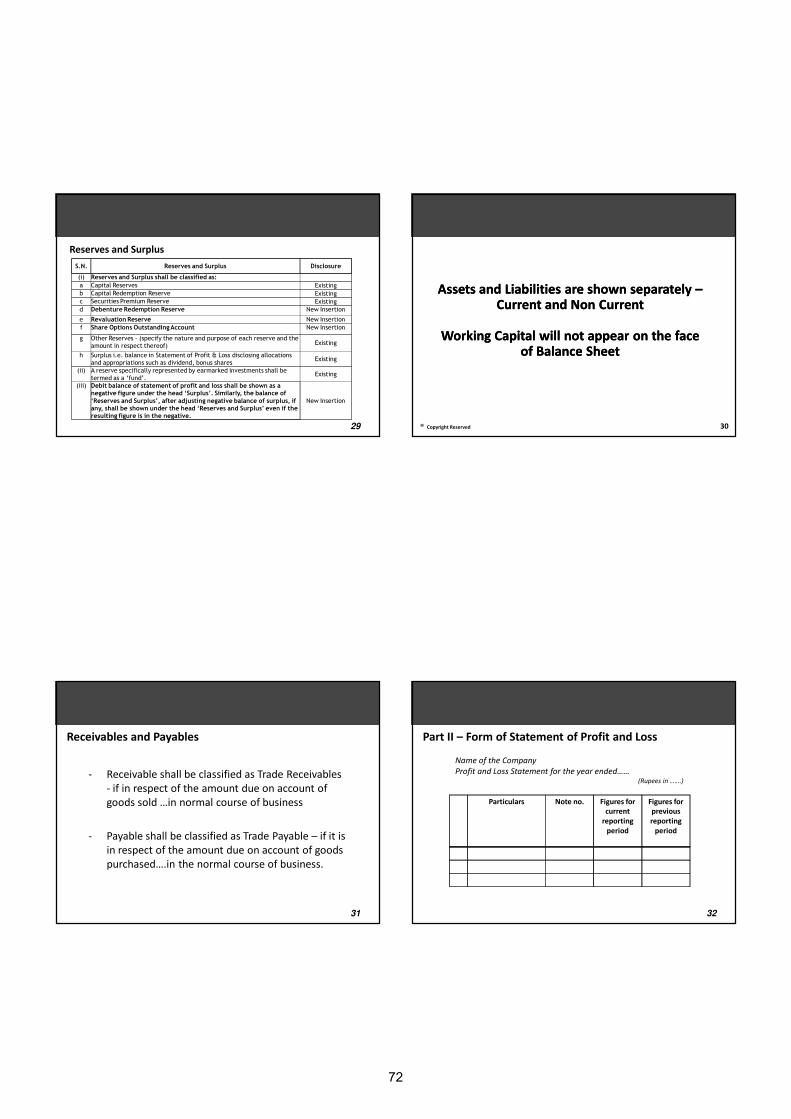

Introduction• Old Schedule VI had outlived its utility;• Revised Schedule VI effective from 1st April, 2011;• Being a statutory format its early adoption is not

permitted;• Revised Schedule VI has been framed as per the

existing non-converged Indian AccountingStandards notified under the Companies(Accounting Standards), Rules, 2006;

Requirements under Revised Schedule VI• Accounting Standards will prevail over the Schedule;• Revised Schedule VI has eliminated the concept of

‘schedule’;• Terms in the Revised Schedule VI will carry they

meaning as defined by the applicable AccountingStandards;

• All items of assets and liabilities are to be bifurcatedbetween current and non-current portions andpresented separately on the face of the Balance Sheet

Requirements under Revised Schedule VI• Vertical format for presentation only prescribed;• Prescribes minimum disclosure requirements. AS

disclosures are additional;• Source of Funds now is Equity and Liabilities;• Application of Funds now is Assets;• Application of Funds now is Assets;• Shareholding of more than 5% shares in the

company now needs to be disclosed;• Share allotments for non-cash consideration, buy back

to be disclosed;• Statement of Profit and Loss (Dr. Bal.) will be

disclosed under the head “Reserves and Surplus”

2

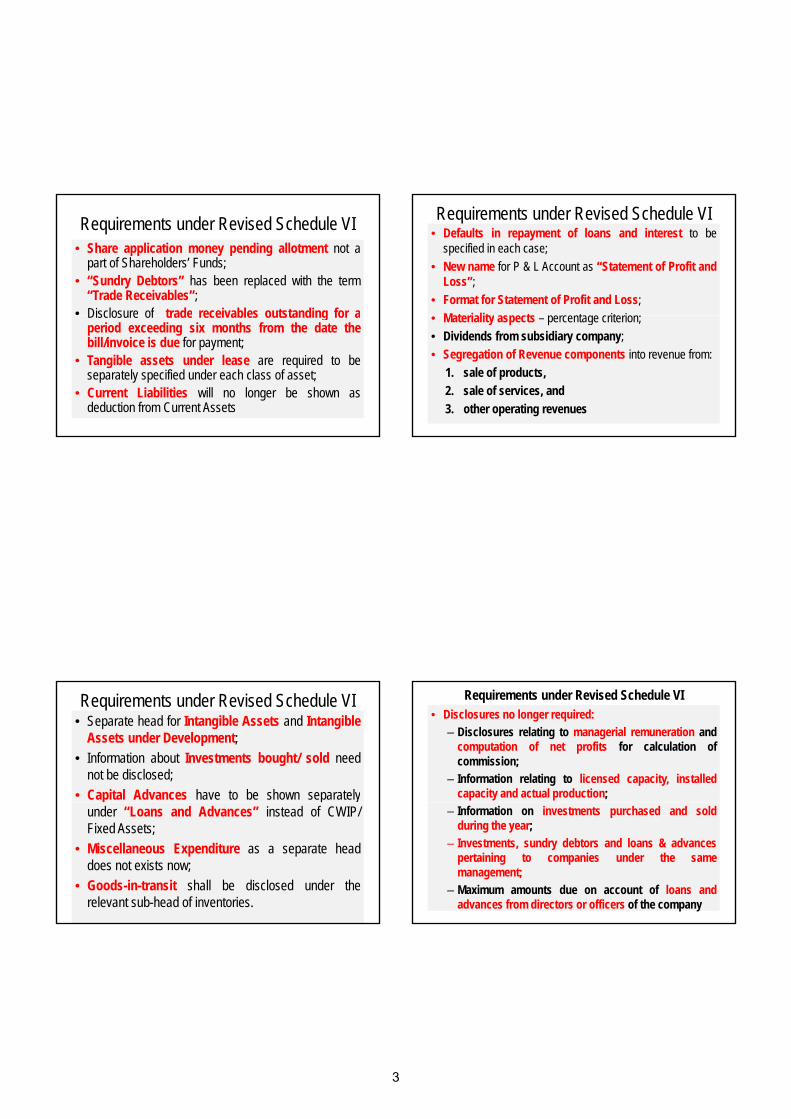

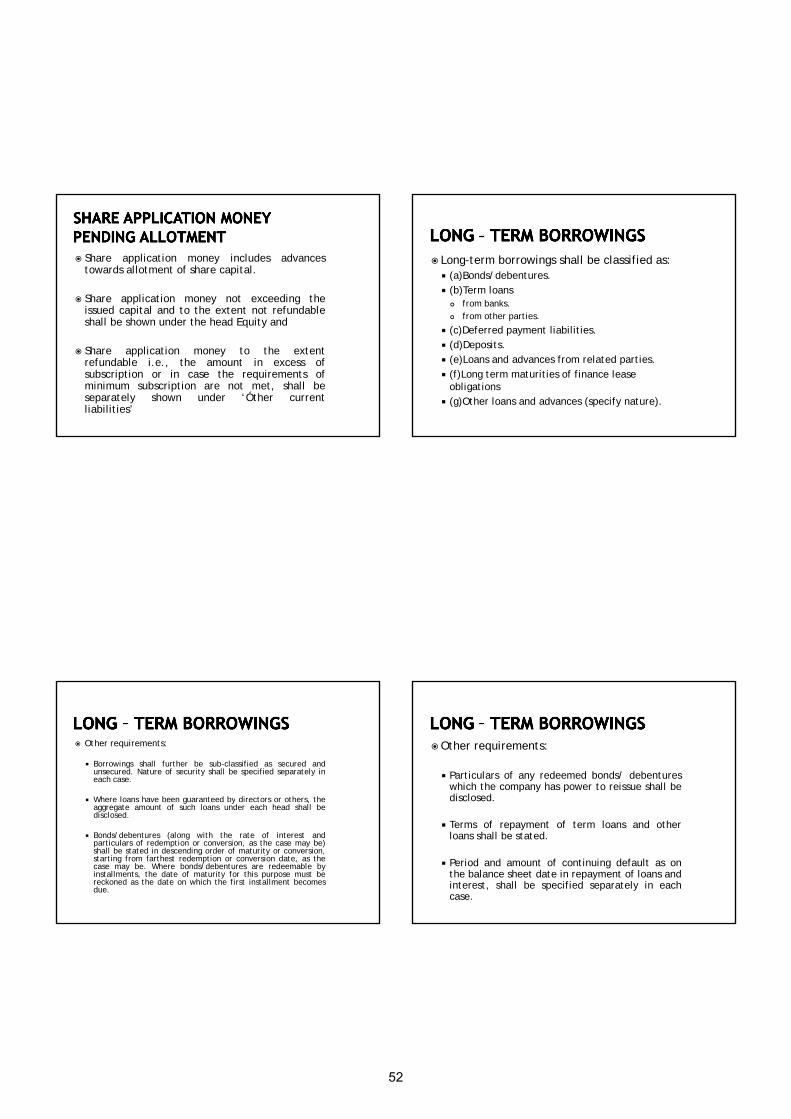

Requirements under Revised Schedule VI• Share application money pending allotment not a

part of Shareholders’ Funds;• “Sundry Debtors” has been replaced with the term

“Trade Receivables”;• Disclosure of trade receivables outstanding for aDisclosure of trade receivables outstanding for a

period exceeding six months from the date thebill/invoice is due for payment;

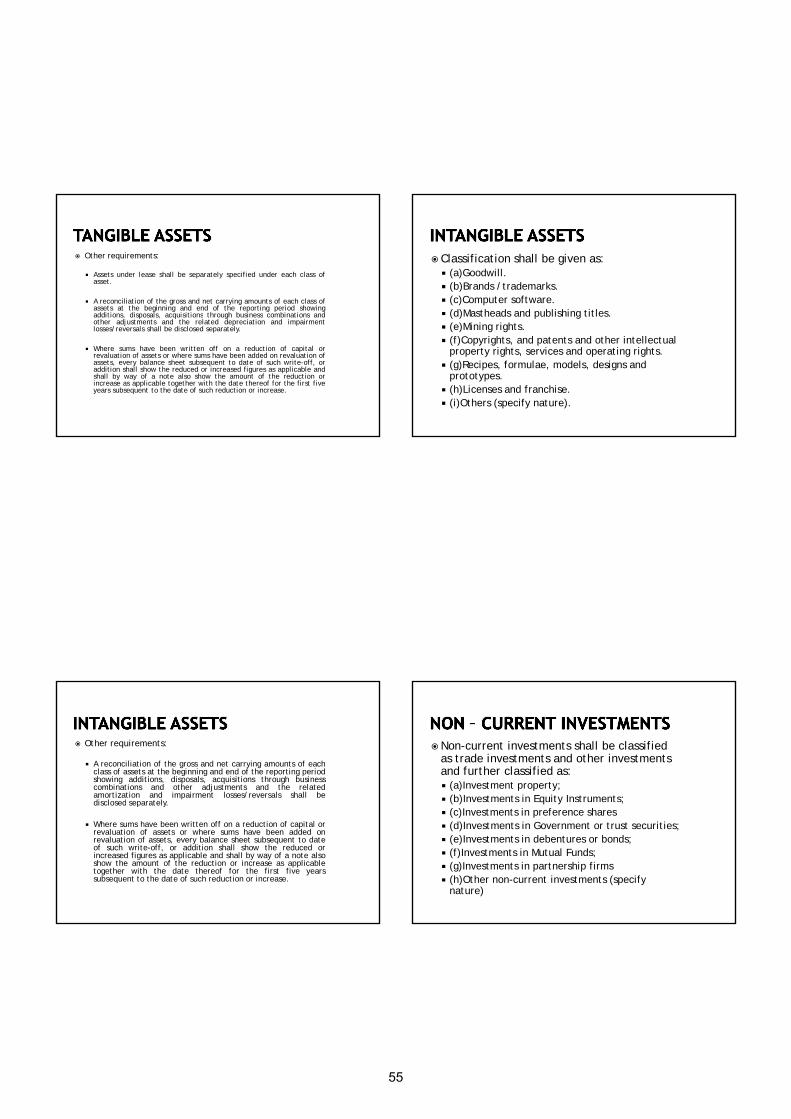

• Tangible assets under lease are required to beseparately specified under each class of asset;

• Current Liabilities will no longer be shown asdeduction from Current Assets

Requirements under Revised Schedule VI• Defaults in repayment of loans and interest to be

specified in each case;• New name for P & L Account as “Statement of Profit and

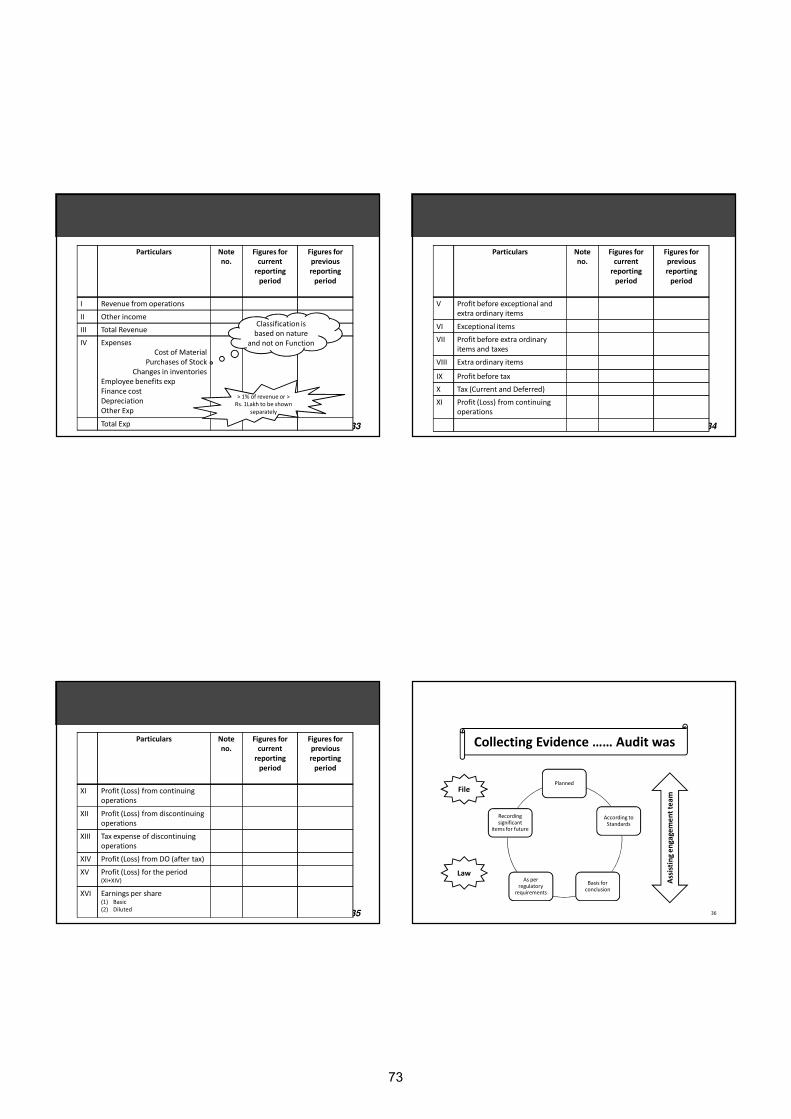

Loss”;• Format for Statement of Profit and Loss;

M t i lit t t it i• Materiality aspects – percentage criterion;• Dividends from subsidiary company;• Segregation of Revenue components into revenue from:

1. sale of products,2. sale of services, and3. other operating revenues

Requirements under Revised Schedule VI• Separate head for Intangible Assets and Intangible

Assets under Development;• Information about Investments bought/ sold need

not be disclosed;• Capital Advances have to be shown separatelyy

under “Loans and Advances” instead of CWIP/Fixed Assets;

• Miscellaneous Expenditure as a separate headdoes not exists now;

• Goods-in-transit shall be disclosed under therelevant sub-head of inventories.

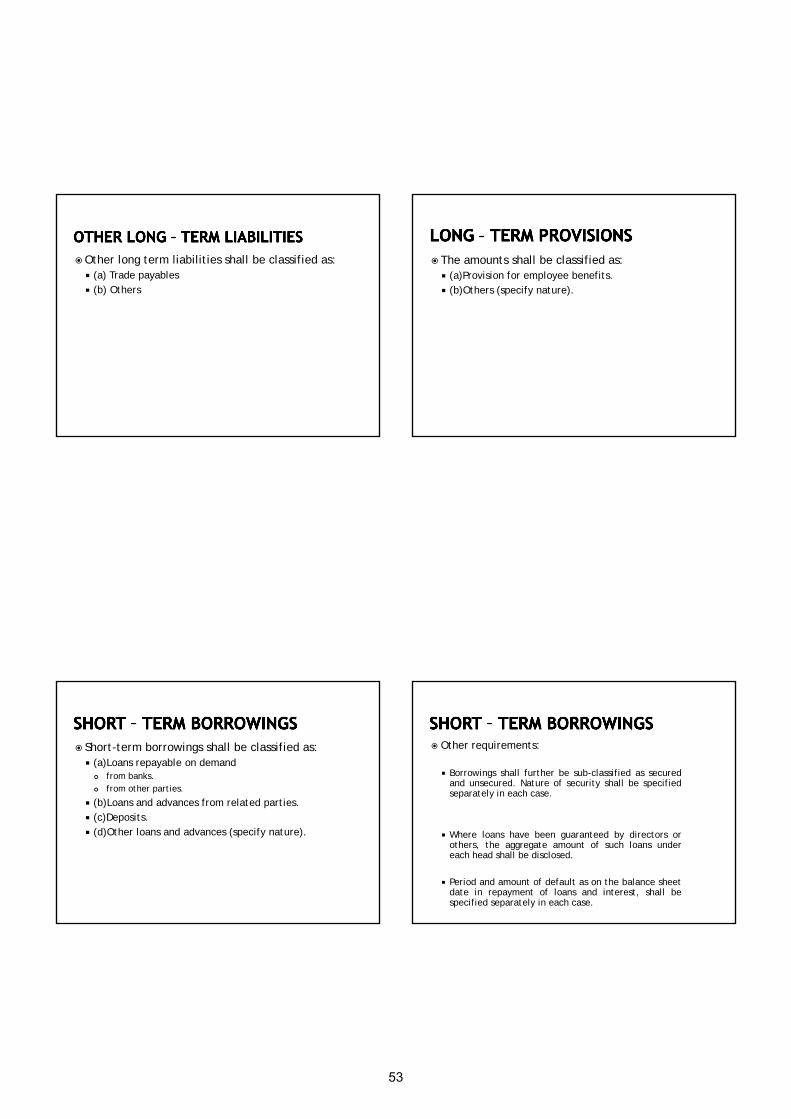

Requirements under Revised Schedule VI• Disclosures no longer required:

– Disclosures relating to managerial remuneration andcomputation of net profits for calculation ofcommission;

– Information relating to licensed capacity, installedcapacity and actual production;

– Information on investments purchased and soldduring the year;

– Investments, sundry debtors and loans & advancespertaining to companies under the samemanagement;

– Maximum amounts due on account of loans andadvances from directors or officers of the company

3

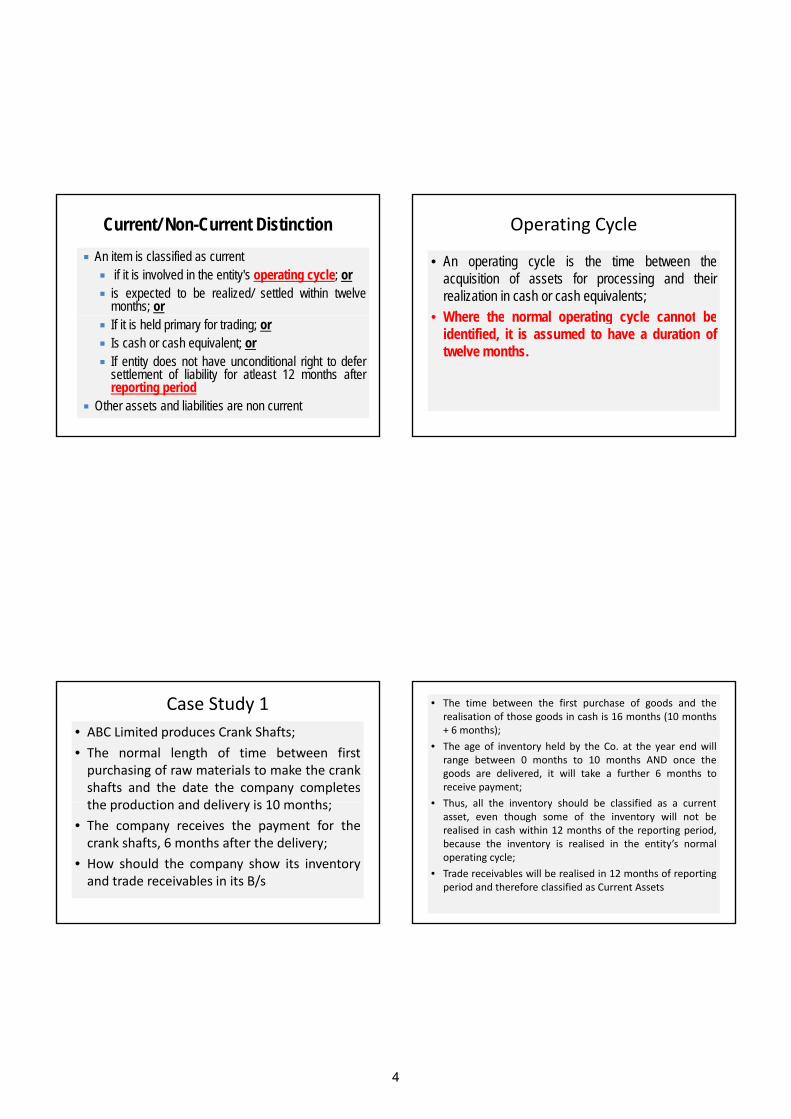

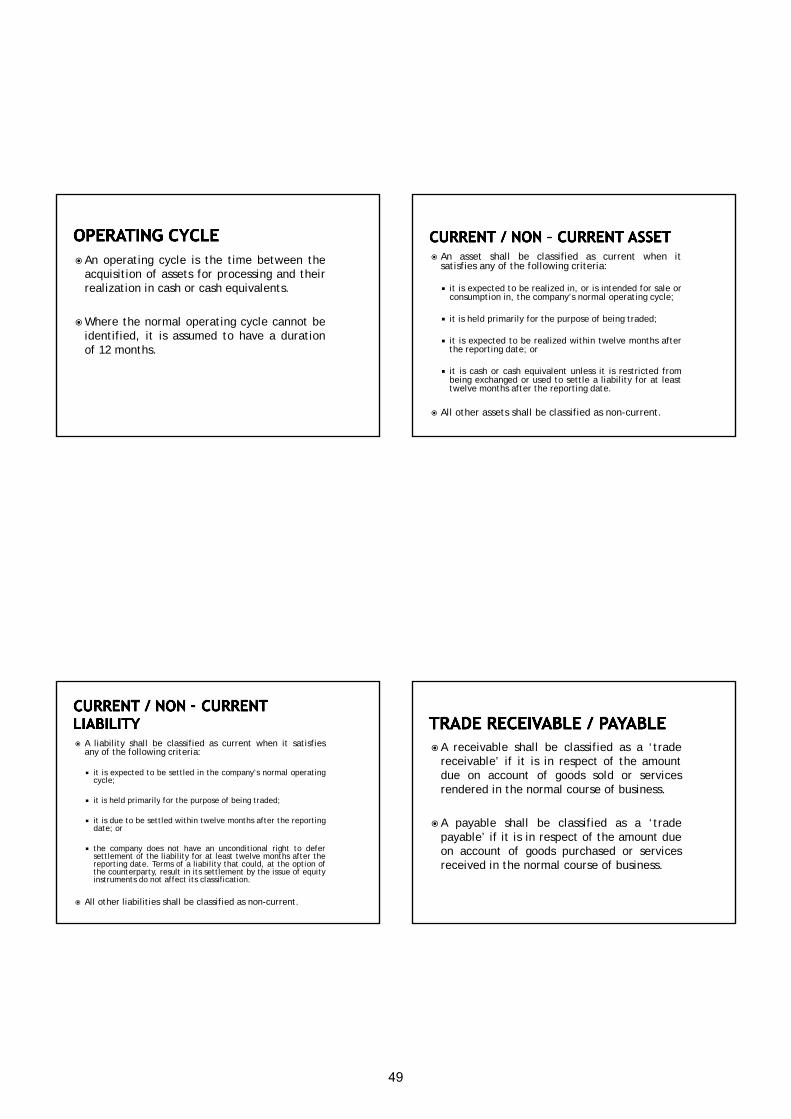

An item is classified as currentif it is involved in the entity's operating cycle; oris expected to be realized/ settled within twelvemonths; or

Current/ Non-Current Distinction

If it is held primary for trading; orIs cash or cash equivalent; orIf entity does not have unconditional right to defersettlement of liability for atleast 12 months afterreporting period

Other assets and liabilities are non current

Operating Cycle

• An operating cycle is the time between theacquisition of assets for processing and theirrealization in cash or cash equivalents;

• Where the normal operating cycle cannot be• Where the normal operating cycle cannot beidentified, it is assumed to have a duration oftwelve months.

Case Study 1• ABC Limited produces Crank Shafts;

• The normal length of time between firstpurchasing of raw materials to make the crankshafts and the date the company completesthe prod ction and deli er is 10 monthsthe production and delivery is 10 months;

• The company receives the payment for thecrank shafts, 6 months after the delivery;

• How should the company show its inventoryand trade receivables in its B/s

• The time between the first purchase of goods and therealisation of those goods in cash is 16 months (10 months+ 6 months);

• The age of inventory held by the Co. at the year end willrange between 0 months to 10 months AND once thegoods are delivered, it will take a further 6 months toreceive payment;

• Thus all the inventory should be classified as a current• Thus, all the inventory should be classified as a currentasset, even though some of the inventory will not berealised in cash within 12 months of the reporting period,because the inventory is realised in the entity’s normaloperating cycle;

• Trade receivables will be realised in 12 months of reportingperiod and therefore classified as Current Assets

4

Case Study 2• ABC Limited produces Crank Shafts;

• The normal length of time between firstpurchasing of raw materials to make the crankshafts and the date the company completesthe prod ction and deli er is 14 monthsthe production and delivery is 14 months;

• The company receives the payment for thecrank shafts, 15 months after the delivery;

• Would your answer be different now

• The answer will remain the same;

• In this case, the inventory is on an averageolder, but nevertheless it is realised in cash inentity’s normal operating cycle;

Si il l th t d i bl li d i• Similarly, the trade receivables are realised incash as a part of the entity’s normal operatingcycle, even though not within 12 months ofthe reporting period

Case Study 3• ABC Limited has taken a seven year loan from PunjabNational Bank;

• The loan contains certain debt covenants, e.g., filing ofquarterly information, failing which the bank can recall theloan and demand repayment thereof;

Th h t fil d h i f ti i th i• The company has not filed such information in the previousquarter and as a result of which the bank has the right torecall the loan;

• The management of the company based on the pastexperience with the bank believes that default is minor andthe bank will not demand the repayment of loan;

• Shall this loan now be classified as current liability.

• The enterprise has to assess on the reporting date/ balancesheet date, as to whether it being a borrower has anunconditional right at the Balance Sheet date to defer thesettlement irrespective of the nature of default andwhether or not a bank can exercise its right to recall theloan. If the borrower does not have such right, theclassification would be “current.”

• It is pertinent to note that as per the terms and conditionsof the aforesaid loan, the loan was not repayable ondemand from day one;

• The loan became repayable on demand only on default inthe debt covenant and bank has not demanded therepayment of loan up to the date of approval of theaccounts;

5

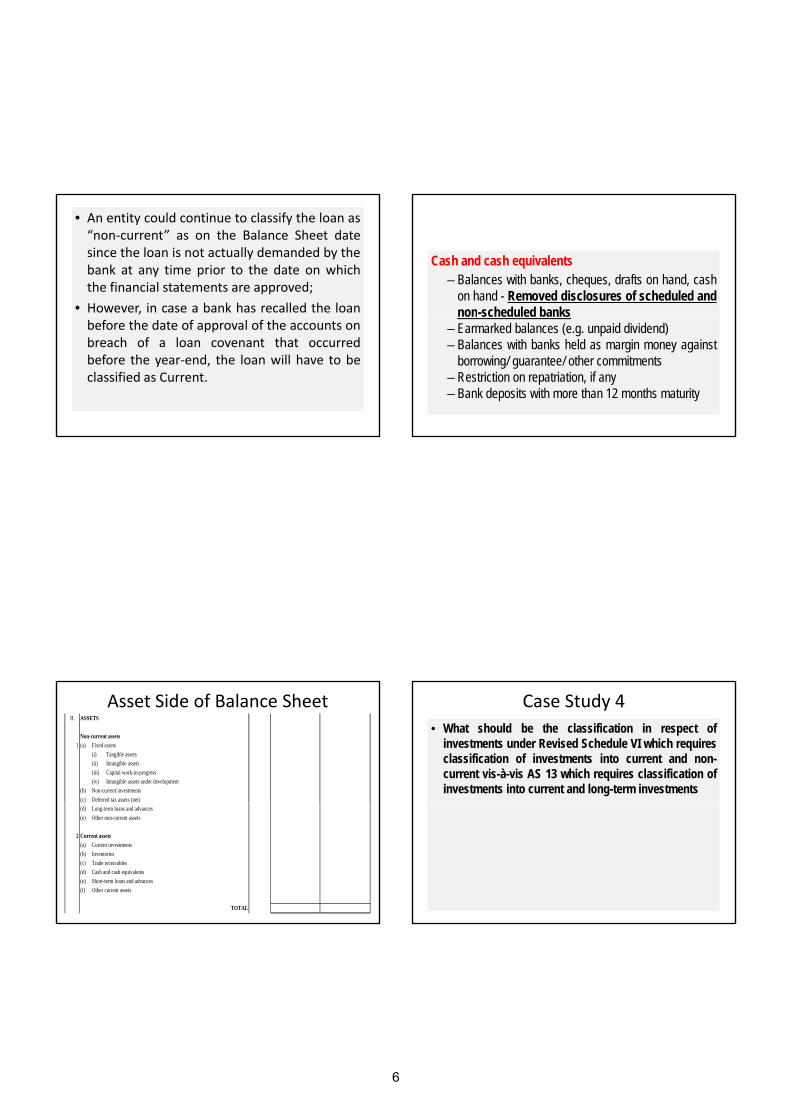

• An entity could continue to classify the loan as“non‐current” as on the Balance Sheet datesince the loan is not actually demanded by thebank at any time prior to the date on whichthe financial statements are approved;

• However, in case a bank has recalled the loanbefore the date of approval of the accounts onbreach of a loan covenant that occurredbefore the year‐end, the loan will have to beclassified as Current.

Cash and cash equivalents– Balances with banks, cheques, drafts on hand, cash

on hand - Removed disclosures of scheduled andnon-scheduled banksnon scheduled banks

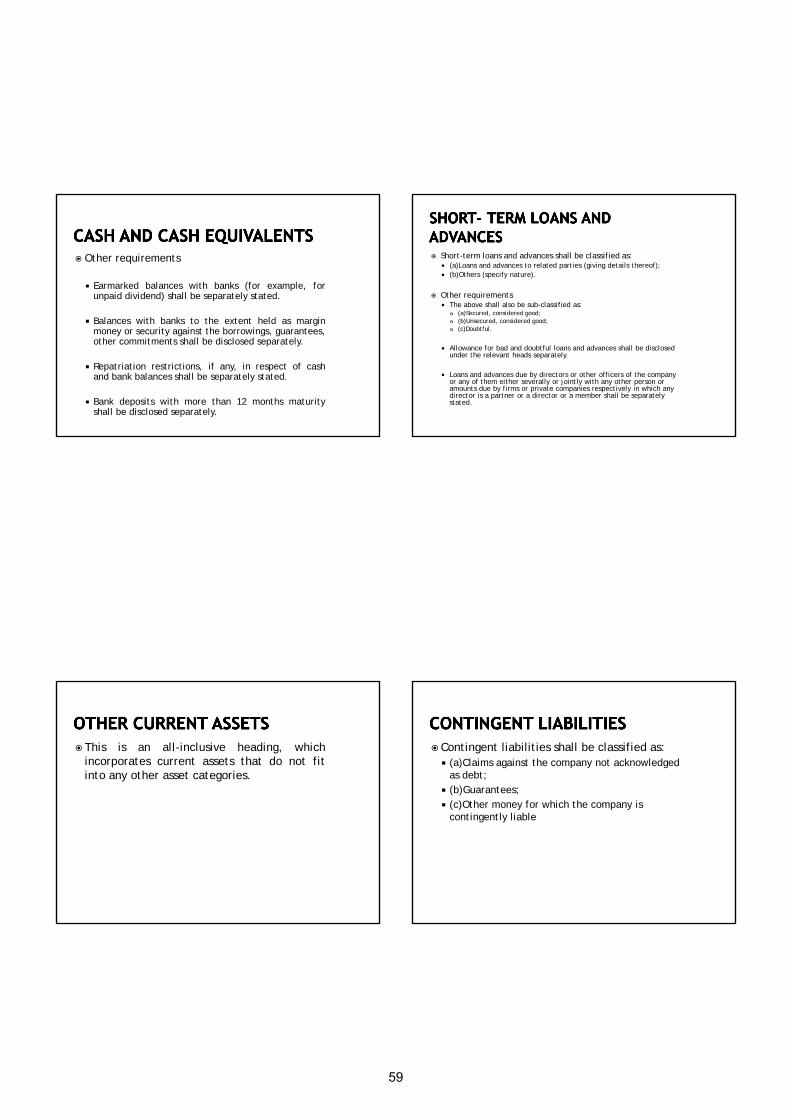

– Earmarked balances (e.g. unpaid dividend)– Balances with banks held as margin money against

borrowing/ guarantee/ other commitments– Restriction on repatriation, if any– Bank deposits with more than 12 months maturity

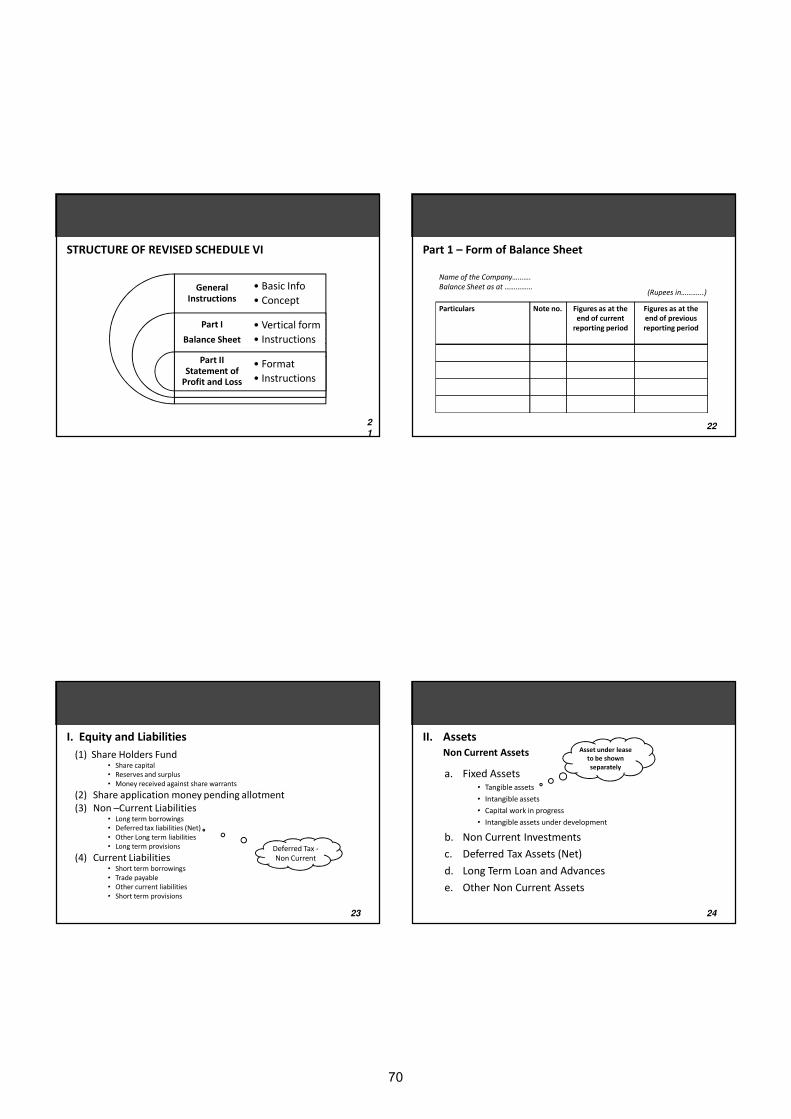

Asset Side of Balance SheetII. ASSETS

Non-current assets1 (a) Fixed assets

(i) Tangible assets(ii) Intangible assets(iii) Capital work-in-progress(iv) Intangible assets under development

(b) Non-current investments(c) Deferred tax assets (net)( ) ( )(d) Long-term loans and advances(e) Other non-current assets

2 Current assets(a) Current investments(b) Inventories(c) Trade receivables(d) Cash and cash equivalents(e) Short-term loans and advances(f) Other current assets

TOTAL

Case Study 4• What should be the classification in respect of

investments under Revised Schedule VI which requiresclassification of investments into current and non-current vis-à-vis AS 13 which requires classification ofinvestments into current and long-term investments

6

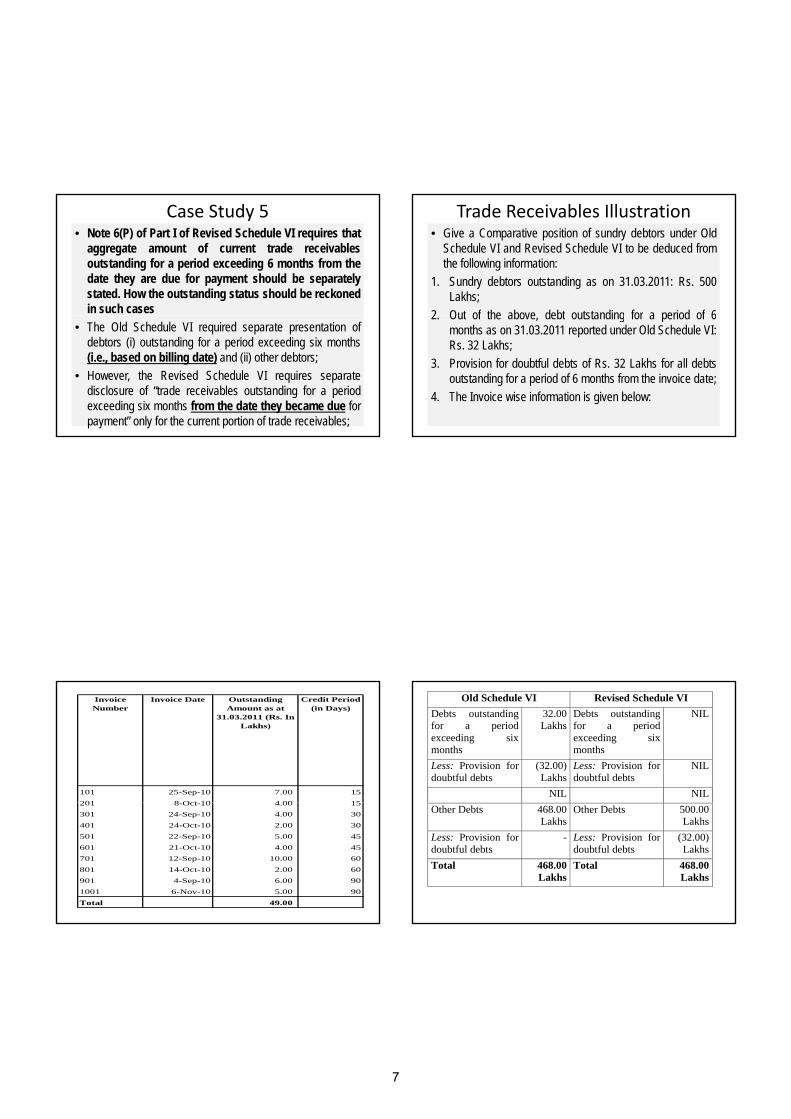

Case Study 5• Note 6(P) of Part I of Revised Schedule VI requires that

aggregate amount of current trade receivablesoutstanding for a period exceeding 6 months from thedate they are due for payment should be separatelystated. How the outstanding status should be reckonedin such cases

• The Old Schedule VI required separate presentation ofdebtors (i) outstanding for a period exceeding six months(i.e., based on billing date) and (ii) other debtors;

• However, the Revised Schedule VI requires separatedisclosure of “trade receivables outstanding for a periodexceeding six months from the date they became due forpayment” only for the current portion of trade receivables;

Trade Receivables Illustration• Give a Comparative position of sundry debtors under Old

Schedule VI and Revised Schedule VI to be deduced fromthe following information:

1. Sundry debtors outstanding as on 31.03.2011: Rs. 500Lakhs;

2 Out of the above debt outstanding for a period of 62. Out of the above, debt outstanding for a period of 6months as on 31.03.2011 reported under Old Schedule VI:Rs. 32 Lakhs;

3. Provision for doubtful debts of Rs. 32 Lakhs for all debtsoutstanding for a period of 6 months from the invoice date;

4. The Invoice wise information is given below:

101 25-Sep-10 7.00 15201 8 Oct 10 4 00 15

Invoice Number

Invoice Date Outstanding Amount as at

31.03.2011 (Rs. In Lakhs)

Credit Period (in Days)

201 8-Oct-10 4.00 15301 24-Sep-10 4.00 30401 24-Oct-10 2.00 30501 22-Sep-10 5.00 45601 21-Oct-10 4.00 45701 12-Sep-10 10.00 60801 14-Oct-10 2.00 60901 4-Sep-10 6.00 901001 6-Nov-10 5.00 90

Total 49.00

Old Schedule VI Revised Schedule VI Debts outstanding for a period exceeding six months

32.00 Lakhs

Debts outstanding for a period exceeding six months

NIL

Less: Provision for doubtful debts

(32.00) Lakhs

Less: Provision for doubtful debts

NIL

NIL NILOther Debts 468.00

Lakhs Other Debts 500.00

LakhsLess: Provision for doubtful debts

- Less: Provision for doubtful debts

(32.00) Lakhs

Total 468.00 Lakhs

Total 468.00 Lakhs

7

• CA. KAMAL GARG

REVISED SCHEDULE VI – AN ANALYSIS

With the emergence of multinationalcorporations and rapid increase in cross bordertransactions, it is essential that our financialstatements speak the global language for attractingforeign funds into India. Internationally, theobservance of universally accepted reportingnorms is perceived as an important measure ofgood corporate governance, ensuring financialtransparency to the stakeholders of the company.The transparency in financial statements of acompany has a significant bearing on the decisionof a stakeholder to invest, as well as the quantumof his investment.The classification under the old Schedule VI was,however, not in line with the internationalpractices followed by many developed countries,making investors reluctant to invest in the Indiancompanies. The Indian companies were requiredto prepare another set of financial statementsto make foreign investors understand theperformance and position of their companies,which not only resulted in higher costs, but alsoconsumed considerable time and effort.With India moving towards convergence to IFRS,there was an urgent call to revise the old ScheduleVI, as it was not compatible to meet either thedisclosure requirements or the provisions of theupcoming accounting standards. Though therevised Schedule VI has been framed as per theexisting non-converged Indian AccountingStandards notified under the Companies(Accounting Standards), Rules, 2006 and hasnothing to do with the converged Indian AccountingStandards, still, it has taken into consideration theclassification accepted internationally.This compilation makes an attempt to throwsome light on the need for revision of old scheduleVI, salient features of the revised Schedule VI andthe issues which may initially arise while preparingfinancial statements as per revised Schedule VI.

Old Schedule VI had outlived its utility

Classification in old Schedule VI was not in line withthe disclosure requirements under AS:After introduction of Accounting Standards onLeases, Consolidated Financial Statements,Accounting for Taxes, Discontinuing Operations,Impairments of Assets, Provisions etc., thedisclosure requirements of old Schedule VI onthe face of balance sheet were felt to be insufficient.Further, appropriate heads, under whichdisclosures prescribed in the accounting standardshave to be made, were missing in the Balance Sheetunder old Schedule VI. For instance, AccountingStandard 22 requires that deferred tax assets (DTA)and deferred tax liabilities (DTL) should bedisclosed under a separate heading in the balancesheet of the enterprise, separately from currentassets and current liabilities. In other words, asper AS 22, DTA and DTL have to be disclosed underthe heading “non-current assets” or “non-currentliabilities”, which classification was not providedfor in the old schedule VI.

No place for industry specific requirements: Old Schedule VI had a fixed format in which everyindustry has to present its financial statements.However, the industry specific requirements couldnot always fit into such format. The old scheduleVI did not address such problems which made itdifficult for a preparer of financial statements toidentify the appropriate head for their industryspecific items.

No specific format for Profit and Loss Account:One of the shortcomings of old Schedule VI wasthat it did not contain any specific format for Profitand loss account as it had for the Balance Sheet,though the requirements for preparing profit andloss account were detailed in Part II of ScheduleVI. However, it was felt that a specific format forpresentation of the profit and loss account wouldhave conveyed a clear cut picture to the preparersof financial statements.

Measurement principles under Schedule VI notin line with Accounting Standards:Apart from the disclosure requirements, even themeasurement principles as per old Schedule VIwere different from what was given in theaccounting standards. For instance, AS 11 requiresthat any exchange difference in foreign currencytranslation is to be charged / recognized in the Profitand loss account. However, as per old scheduleVI, such exchange difference in foreign currencytranslation should be capitalised. On account ofsuch differences in the measurement principles,it can be said that the old schedule VI was not inconformity with the mandatory requirements ofthe accounting standards.

Revised Schedule VI: Effective from 1stApril, 2011

8

The Ministry of Corporate Affairs vide its Notification no. F.No.2/6/2008-C.L-V dated 30-3-2011, notified that the Revised Schedule VI is applicable for the Balance Sheet and Profit and Loss Account to be prepared for the financial year commencing on or after April 1, 2011. It should be noted that Revised Schedule VI to the Companies Act, 1956, being a statutory format its early adoption is not permitted. This revised ScheduleVI has been framed as per the existing non-convergedIndian Accounting Standards notifiedunder the Companies (Accounting Standards),Rules, 2006. The Revised Schedule VI shall comeinto force for the Balance Sheet and Profit and LossAccount to be prepared for the financial yearcommencing on or after 1.4.2011.

Objectives for Revising Schedule VI

In November, 2008, the Ministry of CorporateAffairs issued an Explanatory Memorandum for revising Schedule VI to the Companies Act, 1956which clearly stated its objectives as follows:

(a) To have a ‘readable, useful, transparent anduser friendly’ form of Schedule VI. (b) To set out minimum disclosure requirementswhich are considered essential to ensure trueand

fair presentation of the financial positionand financial performance of the company andcomparability both with the company’sprevious periods and with other companies.

(c) The Balance Sheet and the Statement of Profitand Loss should not be burdened with toomany disclosure requirements.

(d) To remove the requirements of disclosures nolonger considered relevant in view of thechanged socio-economic structure and levelof development of the economy.

(e) To remove disclosure requirements which aremeant for statistical purposes only e.g. Part IVof Schedule VI.

(f) To have inherent flexibility for amendmentsand industry/sector specific improvementsfrom time to time and to cater to industry/sector specific disclosure requirements.

(g) To harmonize and synchronize the generaldisclosure requirements with those prescribedin the Accounting Standards by removing theexisting inherent anomalies.

(h) The specific disclosure requirementsprescribed in the Accounting Standards arenot incorporated here so that amendment inthe Accounting Standard does not necessitatean amendment in the Schedule VI.

(i) To attain compatibility and convergence withthe International Accounting Standards andpractice.

FEATURES OF REVISED SCHEDULE VI

1. Accounting Standards will prevail over the Schedule: The Revised Schedule VI requires that if compliance with the requirements of the Act and / or the Accounting standards requires a change in the treatment or disclosure in the financial statements as compared to that is provided in the Revised Schedule VI, the requirements of the Act and / or the Accounting Standards will prevail over the Schedule;

2. Requirements mentioned therein for disclosure on the face of the financial statements or in the notes are minimum requirements: The Revised Schedule VI clarifies that the requirements mentioned therein for disclosure on the face of the financial statements or in the notes are minimum requirements. Line items, sub-line items and sub-totals can be presented as an addition or substitution on the face of the financial statements when such presentation is relevant for understanding of the company’s financial position and /or performance;

3. Revised Schedule VI has eliminated the concept of ‘schedule’: In the Old Schedule VI, break-up of amounts disclosed in the main Balance Sheet and Profit and Loss Account was given in the Schedules. Additional information was furnished in the notes to account. The Revised Schedule VI has eliminated the concept of ‘schedule’ and such information is now to be furnished in the notes to accounts;

4. Terms in the Revised Schedule VI will carry the meaning as defined by the applicable Accounting Standards: The terms used in the Revised Schedule VI will carry the meaning as defined by the applicable Accounting Standards. For example, the terms such as ‘associate’, ‘related parties’, etc will have the same meaning as defined under the Accounting Standards notified under Companies (Accounting Standards) Rules, 2006;

5. Balance to be maintained between providing excessive detail that may not assist users of financial statements and not providing important information: In preparing the financial

9

statements including the notes to accounts, a balance will have to be maintained between providing excessive detail that may not assist users of financial statements and not providing important information as a result of too much aggregation;

6. Current and Non-current bifurcation: All items of assets and liabilities are to be bifurcated between current and non-current portions and presented separately on the face of the Balance Sheet. Such classification was not required by the Old Schedule VI. Current and non-current classification has been introduced for presentation of assets and liabilities in the Balance Sheet. The application of this classification will require assets and liabilities to be segregated into their current and non-current portions. For instance, current maturities of a long term borrowing will have to be classified under the head “Other current liabilities”;

7. Rounding off requirements: There is an explicit requirement to use the same unit of measurement uniformly throughout the financial statements. Moreover, rounding off requirements have been changed to eliminate the option of presenting figures in terms of hundreds and thousands if turnover exceeds Rs. 100 crores;

8. Vertical format for presentation only prescribed: The Revised Schedule VI prescribes only the vertical format for presentation of financial statements. Thus, a company will now not have an option to use horizontal format for the presentation of financial statements as prescribed in Old Schedule VI;

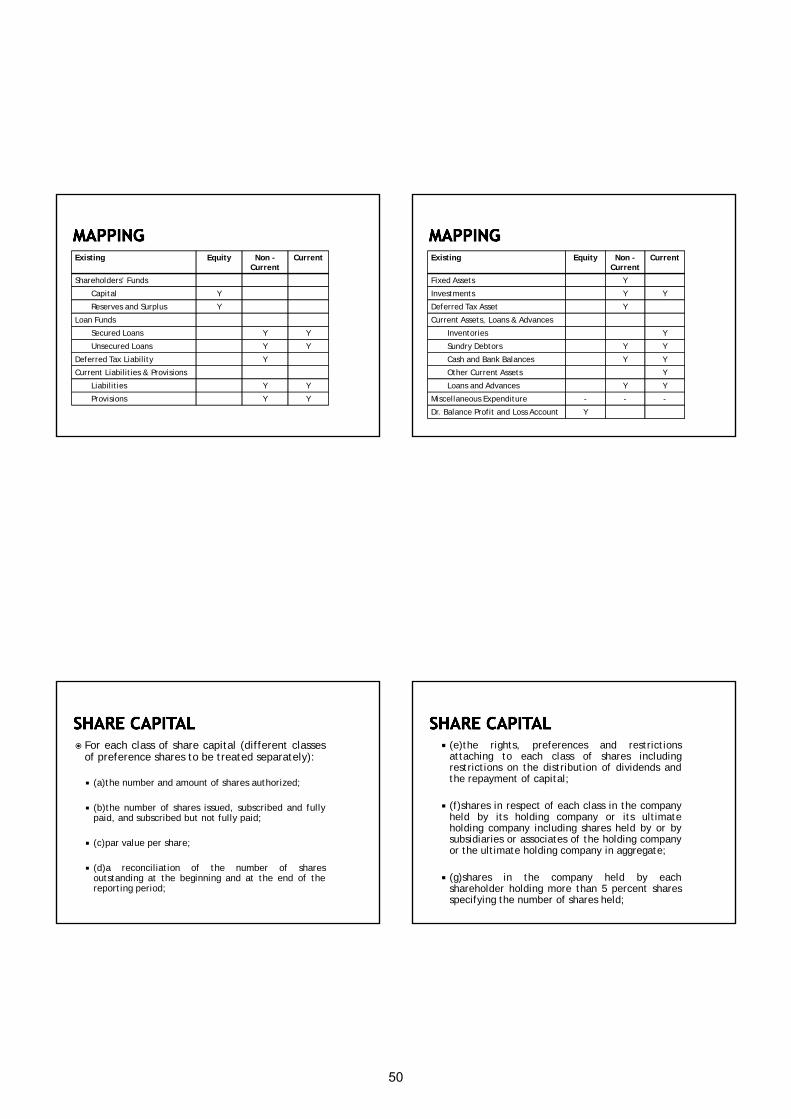

9. Shareholding of more than 5% shares in the company now needs to be disclosed: Number of shares held by each shareholder holding more than 5% shares in the company now needs to be disclosed. In the absence of any specific indication of the date of holding, such information should be based on shares held as on the Balance Sheet date;

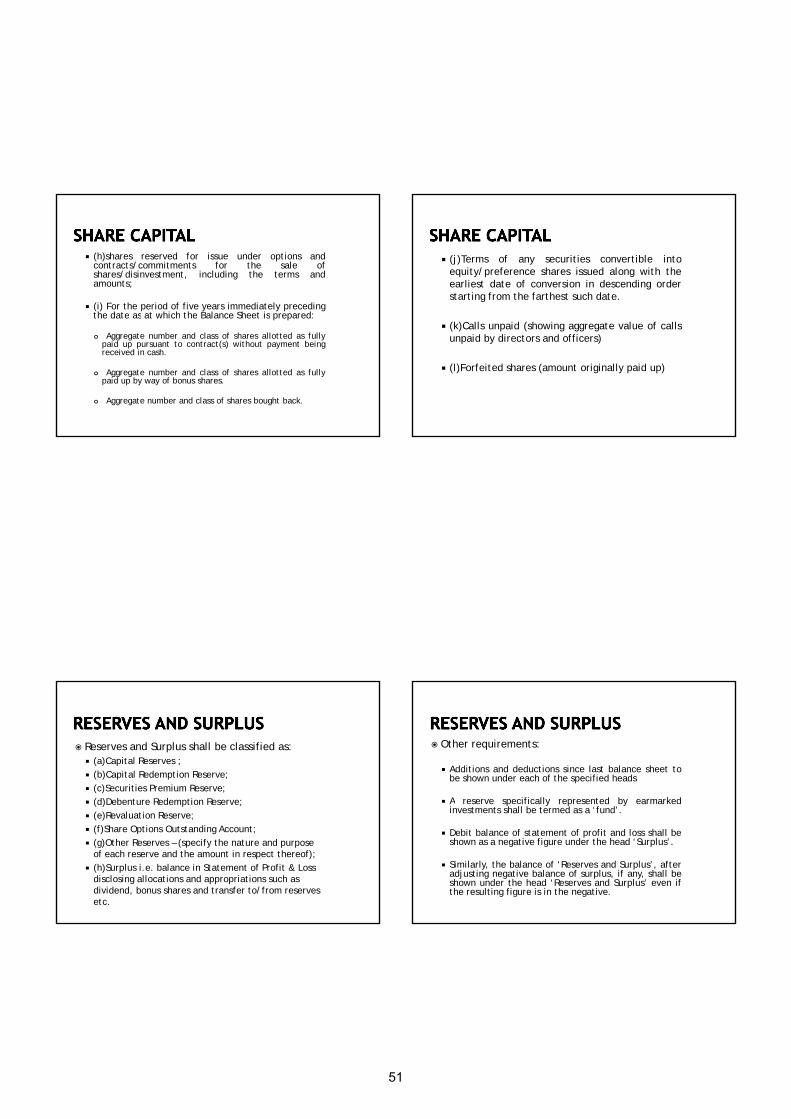

10. Share allotments for non-cash consideration, buy back to be disclosed: Details pertaining to aggregate number and class of shares allotted for consideration other than cash, bonus shares and shares bought back will need to be disclosed only for a period of five years immediately preceding the Balance Sheet date;

11. Debit balance in the Statement of Profit and Loss will be disclosed under the head “Reserves and surplus: Any debit balance in the Statement of Profit and Loss will be disclosed under the head “Reserves and surplus.” Earlier, any debit balance in Profit and Loss Account carried forward after deduction from uncommitted reserves was required to be shown as the last item on the asset side of the Balance Sheet;

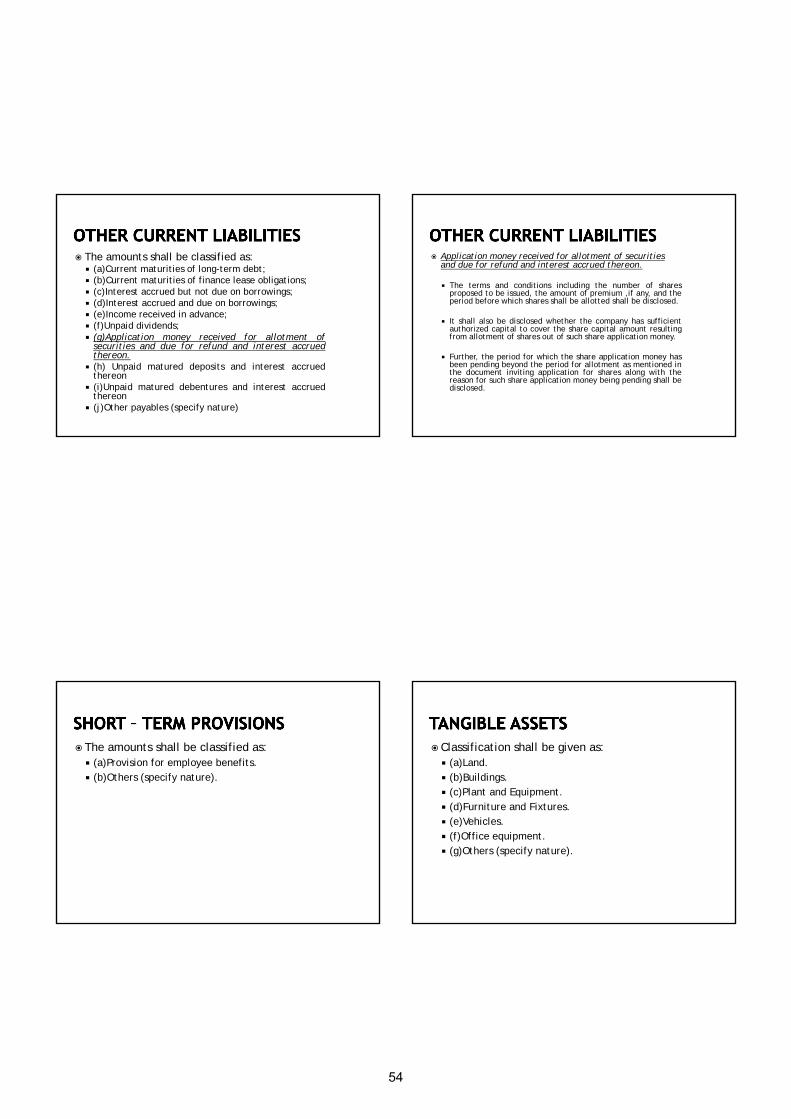

12. Share Application money: Specific disclosures are prescribed for Share Application money. The application money not exceeding the capital offered for issuance and to the extent not refundable will be shown separately on the face of the Balance Sheet. The amount in excess of subscription or if the requirements of minimum subscription are not met will be shown under “Other current liabilities”;

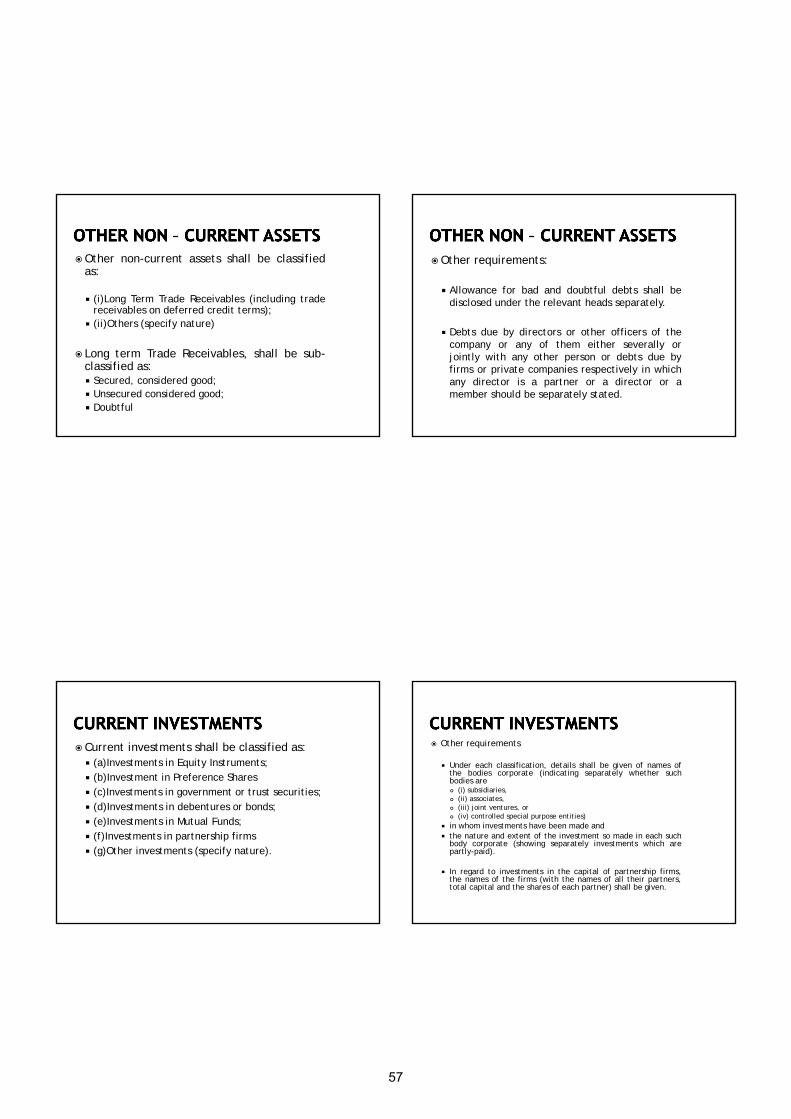

13. “Sundry Debtors” has been replaced with the term “Trade Receivables”: The term “sundry debtors” has been replaced with the term “trade receivables.” ‘Trade receivables’ are defined as dues arising only from goods sold or services rendered in the normal course of business. Hence, amounts due on account of other contractual obligations can no longer be included in the trade receivables;

14. Disclosure of trade receivables outstanding for a period exceeding six months from the date the bill/invoice is due for payment: The Old Schedule VI required separate presentation of debtors outstanding for a period exceeding six months based on date on which the bill/invoice was raised whereas, the Revised Schedule VI requires separate disclosure of “trade receivables outstanding for a period exceeding six months from the date the bill/invoice is due for payment”;

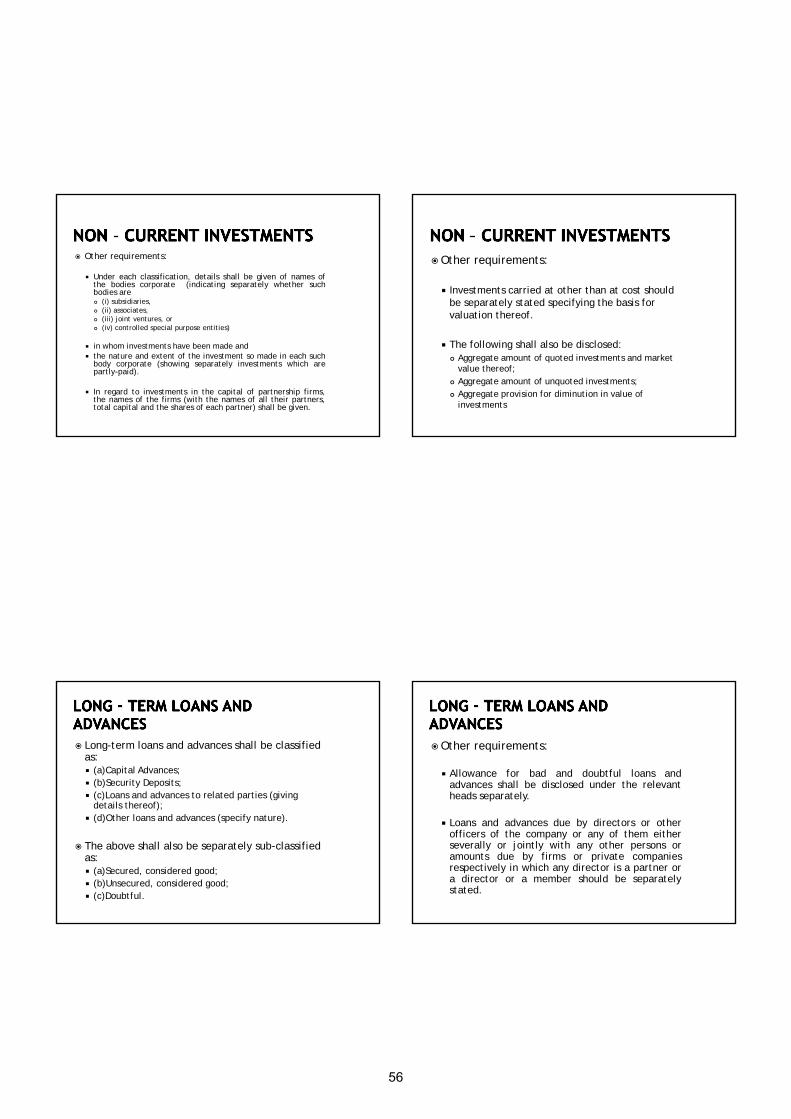

15. Capital Advances: “Capital advances” are specifically required to be presented separately under the head “Loans & advances” rather than including elsewhere;

16. Tangible assets under lease: Tangible assets under lease are required to be separately specified under each class of asset. In the absence of any further clarification, the term “under lease” should be taken to mean assets given on operating lease in the case of lessor and assets held under finance lease in the case of lessee;

10

17. Capital commitments and Other Commitments: In the Old Schedule VI, details of only capital commitments were required to be disclosed. Under the Revised Schedule VI, other commitments also need to be disclosed;

18. Defaults in repayment of loans and interest to be specified in each case: The Revised Schedule VI requires disclosure of all defaults in repayment of loans and interest to be specified in each case. Earlier, no such disclosure was required in the financial statements. However, disclosures pertaining to defaults in repayment of dues to a financial institution, bank and debenture holders continue to be required in the report under Companies Auditor’s Report Order, 2003 (CARO);

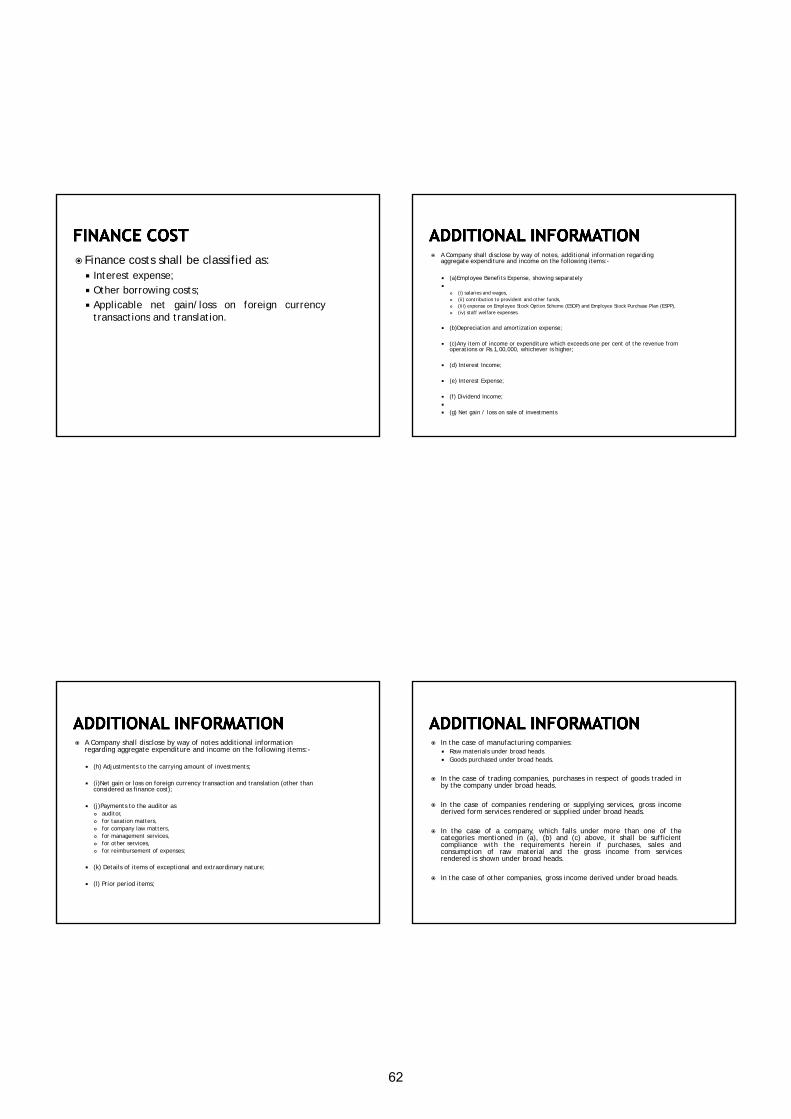

19. Additional disclosures: The Revised Schedule VI introduces a number of other additional disclosures. Some examples are:

(a) Rights, preferences and restrictions attaching to each class of shares, including restrictions on the distribution of dividends and the repayment of capital;

(b) Terms of repayment of long-term loans;

(c) In each class of investment, details regarding names of the bodies corporate in whom investments have been made, indicating separately whether such bodies are (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities, and the nature and extent of the investment made in each such body corporate (showing separately partly-paid investments);

(d) Aggregate provision for diminution in value of investments separately for current and long-term investments;

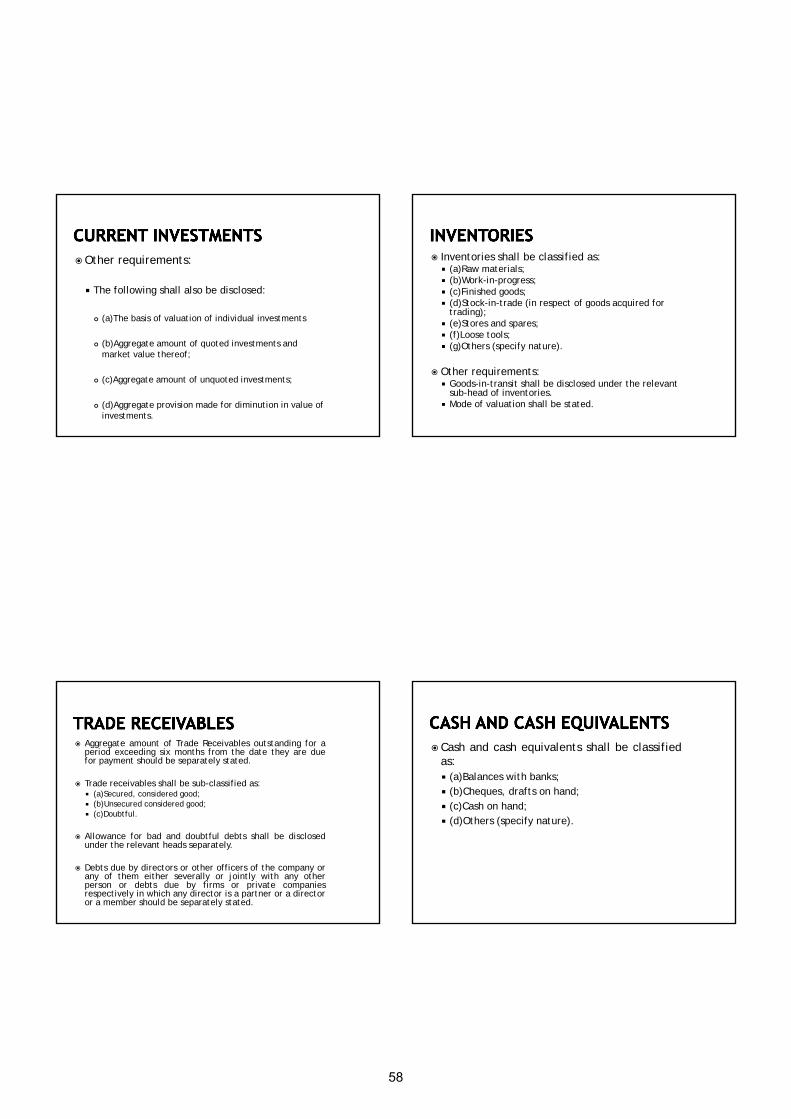

(e) Stock-in-trade held for trading purposes, separately from other finished goods.

20. New name for P & L Account: The name has been changed to “Statement of Profit and Loss” as against ‘Profit and Loss Account’ as contained in the Old Schedule VI;

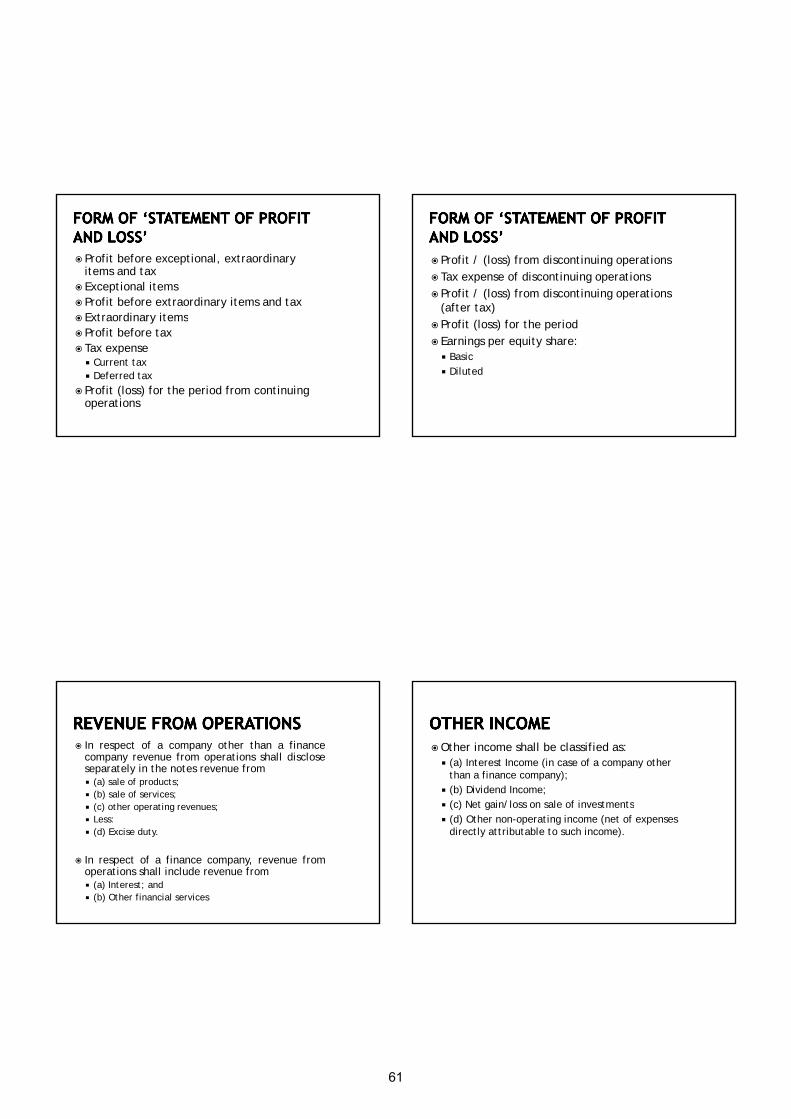

21. Format for Statement of Profit and Loss: Unlike the Old Schedule VI, the Revised Schedule VI lays down a format for the presentation of Statement of Profit and Loss. This format of Statement of Profit and Loss does not mention any appropriation item on its face. Further, the Revised Schedule VI format prescribes such ‘below the line’ adjustments to be presented under “Reserves and Surplus” in the Balance Sheet;

22. Materiality aspects – percentage criterion: In addition to specific disclosures prescribed in the Statement of Profit and Loss, any item of income or expense which exceeds one percent of the revenue from operations or Rs. 100,000 (earlier 1 % of total revenue or Rs. 5,000), whichever is higher, needs to be disclosed separately;

23. Dividends from subsidiary company: The Old Schedule VI required the parent company to recognize dividends declared by subsidiary companies even after the date of the Balance Sheet if they were pertaining to the period ending on or before the Balance Sheet date. Such requirement no longer exists in the Revised Schedule VI. Accordingly, as per AS-9 Revenue Recognition, dividends should be recognized as income only when the right to receive dividends is established as on the Balance Sheet date;

24. Segregation of Revenue components: In respect of companies other than finance companies, revenue from operations need to be disclosed separately as revenue from (a) sale of products, (b) sale of services and (c) other operating revenues;

25. Foreign Currency Borrowings: Net exchange gain/loss on foreign currency borrowings to the extent considered as an adjustment to interest cost needs to be disclosed separately as finance cost;

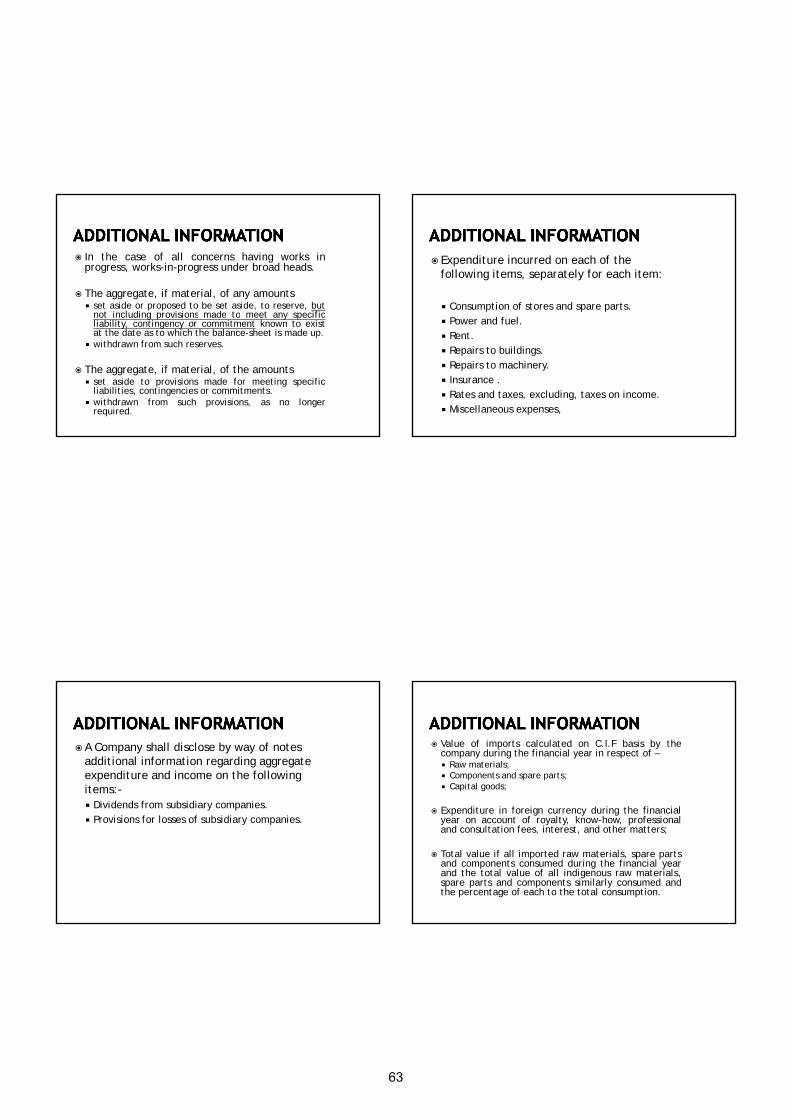

26. Break-up in terms of quantitative disclosures for significant items: Break-up in terms of quantitative disclosures for significant items of Statement of Profit and Loss, such as raw material consumption, stocks, purchases and sales have been simplified and replaced with the disclosure of “broad heads” only. The broad heads need to be decided based on materiality and presentation of true and fair view of the financial statements;

27. Disclosures no longer required: The Revised Schedule VI has removed a number of disclosure requirements that were not considered relevant in the present day context. Examples include:

11

(a) Disclosures relating to managerial remuneration and computation of net profits for calculation of commission;

(b) Information relating to licensed capacity, installed capacity and actual production; (c) Information on investments purchased and sold during the year; (d) Investments, sundry debtors and loans & advances pertaining to companies under the

same management; (e) Maximum amounts due on account of loans and advances from directors or officers of the

company; (f) Commission, brokerage and non-trade discounts

However, there are certain disclosures such as value of imports calculated on CIF basis and expenditure in foreign currency, etc. that still continue in the Revised Schedule VI.

Some Issues arising on application of Revised Schedule VI

1. Do the companies need to furnish comparatives also in the Revised Schedule VI format.

The Revised Schedule VI requires that except in the case of the first financial statements laid before the company after incorporation, the corresponding amounts for the immediately preceding period are to be disclosed in the financial statements including the notes to accounts. Accordingly, comparative information will have to be presented starting from the first year of application of the Revised Schedule VI. Thus for the financial statements prepared for the year 2011-12 (1st April 2011 to 31st March 2012), comparative amounts need to be given for the financial year 2010-11.

2. On which date the bifurcation into current and non-current category has to assessed.

The Revised Schedule VI defines “current assets” and “current liabilities”, with the non-current category being the residual. It is therefore necessary that the balance pertaining to each item of assets and liabilities contained in the Balance Sheet be split into its current and non-current portions and be classified accordingly as on the reporting date.

3. A company is into multiple businesses. Doesit need to consider operating cycle of all business put together or for each business on individual basis?

The expression “Operating Cycle” is defined as the time between the acquisition of assets for processing and their realization in cash or cash equivalents. A company’s normal operating cycle may be longer than twelve months e.g. companies manufacturing wines, etc. However, where the normal operating cycle cannot be identified, it is assumed to have a duration of twelve months. Where a company is engaged in running multiple businesses, the operating cycle could be different for each line of business. Such a company will have to classify all the assets and liabilities of the respective businesses into current and non-current, depending upon the operating cycles for the respective businesses.

4. Whether the preference shares should be presented as share capital only or does it mean that a company compulsorily needs to decide whether a preference shares are liability or equity based on its economic substance using AS 31 Financial Instruments: Presentation principles.

As per the ICAI Guidance Note on Terms used in Financial Statements, ‘Capital’ refers “to the amount invested in an enterprise by its owners, e.g. paid-up share capital in a corporate enterprise. It is also used to refer to the interest of owners in the assets of the enterprise.” This Guidance Note also defines ‘Share Capital’ as “the aggregate amount of money paid or credited as paid on the shares and/or stocks of a corporate enterprise.”

In respect of disclosure requirements for Share Capital, the Revised Schedule VI states that “different classes of preference share capital to be treated separately. The Revised Schedule VI deals only with presentation and disclosure requirements. Accounting for various items is governed by the applicable Accounting Standards. Thus,

1. If a company has early adopted AS 30 Financial Instruments: Recognition and Measurement, AS 31 and AS 32 Financial Instruments: Disclosures, it will decide the liability and equity classification of preference shares based on the principles laid down in AS. If the application of these principles results in all or part of preference shares being classified as liability, it will use the same classification, for presentation in the Balance Sheet;

12

2. However, if a company has not early adopted AS 30, AS 31 and AS 32, it should continue to classify the preference shares as part of “share capital”. Section 85(1) of the Act also refers to Preference Shares as a kind of share capital.

5. The Revised Schedule VI requires proposed dividend to be disclosed in the notes. Does this mean that proposed dividend is not required to be provided for when applying the Revised Schedule VI.

The Revised Schedule VI requires disclosure of the amount of dividends proposed to be distributed to equity and preference shareholders for the period and the related amount per share to be disclosed separately. It also requires separate disclosure of the arrears of fixed cumulative dividends on preference shares. The Old Schedule VI specifically required proposed dividend to be disclosed under the head “Provisions.” In the Revised Schedule VI, this needs to be disclosed in the notes. Hence, a question that arises is as to whether this means that proposed dividend is not required to be provided for when applying the Revised Schedule VI. AS-4 Contingencies and Events Occurring After the Balance Sheet Date of Companies (Accounting Standards) Rules, 2006 issued and notified by the National Advisory Committee on Accounting Standards of the Central Government, under Section 211(3C) of the Companies Act, 1956, requires that dividends stated to be in respect of the period covered by the financial statements, which are proposed or declared by the enterprise after the Balance Sheet date but before approval of the financial statements, should be adjusted. Keeping this in view and the fact that the Accounting Standards override the Revised Schedule VI, companies will have to continue to create a provision for dividends in respect of the period covered by the financial statements and disclose the same as a provision in the Balance Sheet, unless AS-4 is revised. Hence, the disclosure to be made in the notes is over and above the disclosures pertaining to (a) the appropriation items to be disclosed under Reserves and Surplus and (b) Provisions in the Balance Sheet.

6. Revised Schedule VI requires that aggregate amount of current trade receivables outstanding for a period exceeding 6 months from the date they are due for payment should be separately stated. How the outstanding status should be reckoned in such cases.

The Old Schedule VI required separate presentation of debtors (i) outstanding for a period exceeding six months (i.e., based on billing date) and (ii) other debtors. However, the Revised Schedule VI requires separate disclosure of “trade receivables outstanding for a period exceeding six months from the date they became due for payment” only for the current portion of trade receivables. Where no due date is specifically agreed upon, normal credit period allowed by the company should be taken into consideration for computing the due date which may vary depending upon the nature of goods or services sold and the type of customers, etc.

7. How should we disclose unamortized portion of expense items such as share issue expenses, ancillary borrowing cost and discount or premium relating to borrowings under Revised Schedule VI.

The Revised Schedule VI does not contain any specific disclosure requirement for the unamortized portion of expense items such as share issue expenses, ancillary borrowing cost and discount or premium relating to borrowings. The Old Schedule VI required these items to be included under the head “Miscellaneous Expenditure.”

As per AS 16 Borrowing Costs ancillary borrowing costs and discount or premium relating to borrowings could be amortized over the loan period. Further, share issue expenses, discount on shares, ancillary cost-discount/ premium on borrowing, etc., being a special nature item are excluded from the scope of AS 26 Intangible Assets. Keeping this in view, certain companies have taken a view that it is an acceptable practice to amortize these expenses over the period of benefit, i.e., normally 3 to 5 years. The Revised Schedule VI does not deal with any accounting treatment and the same continues to be governed by the respective Accounting Standards/ practices. Further, the Revised Schedule VI is clear that additional line items can be added on the face or in the notes. Keeping this in view, the companies can disclose the unamortized portion of such expenses as “Unamortized expenses”, under the head “other current/ non-current assets”, depending on whether the amount will be amortized in the next twelve months or thereafter.

13

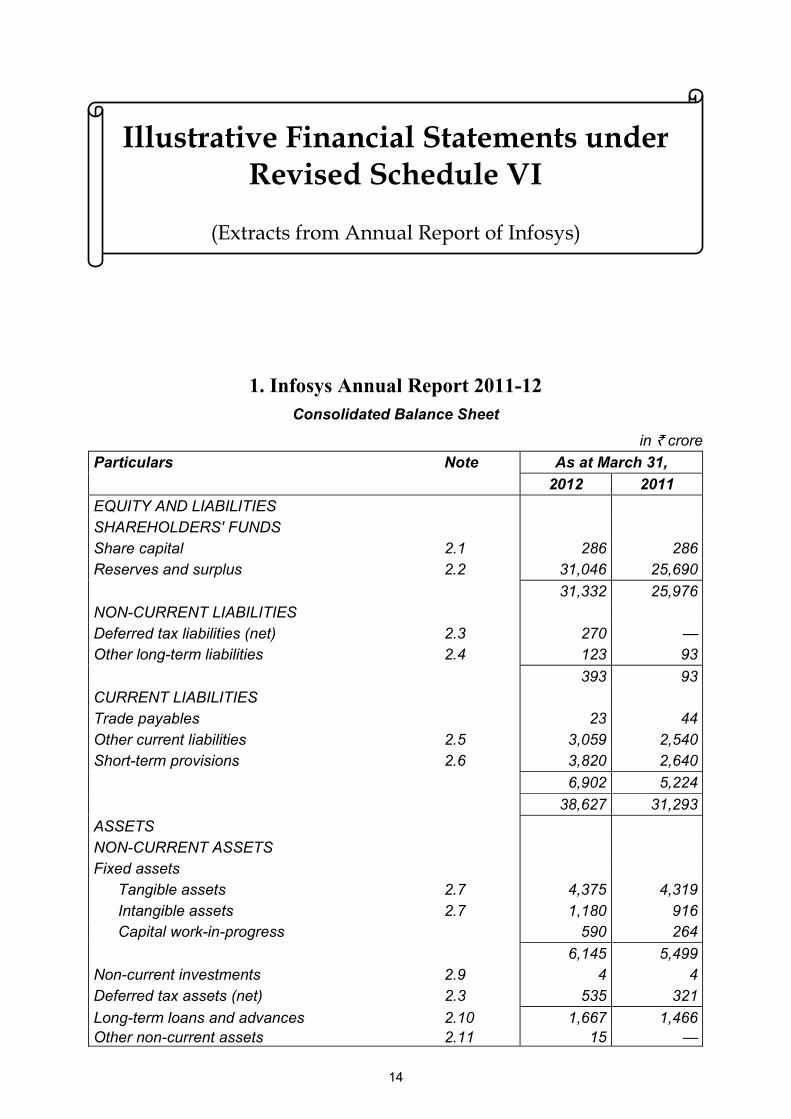

Illustrative Financial Statements under

Revised Schedule VI

(Extracts from Annual Report of Infosys)

1. Infosys Annual Report 2011-12Consolidated Balance Sheet

in ` crore

Particulars Note As at March 31, 2012 2011

EQUITY AND LIABILITIES

SHAREHOLDERS' FUNDS

Share capital 2.1 286 286

Reserves and surplus 2.2 31,046 25,690

31,332 25,976

NON-CURRENT LIABILITIES

Deferred tax liabilities (net) 2.3 270 —

Other long-term liabilities 2.4 123 93

393 93

CURRENT LIABILITIES

Trade payables 23 44

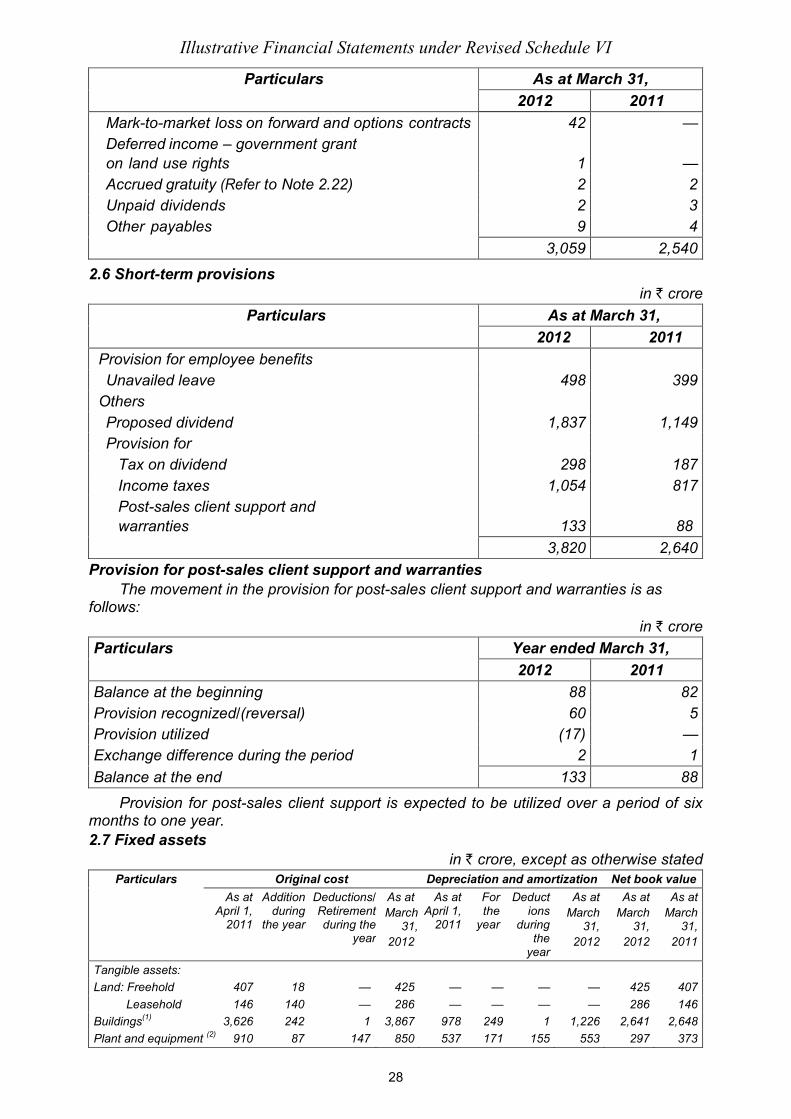

Other current liabilities 2.5 3,059 2,540

Short-term provisions 2.6 3,820 2,640

6,902 5,224

38,627 31,293

ASSETS

NON-CURRENT ASSETS

Fixed assets

Tangible assets 2.7 4,375 4,319

Intangible assets 2.7 1,180 916

Capital work-in-progress 590 264

6,145 5,499

Non-current investments 2.9 4 4

Deferred tax assets (net) 2.3 535 321

Long-term loans and advances 2.10 1,667 1,466

Other non-current assets 2.11 15 —

14

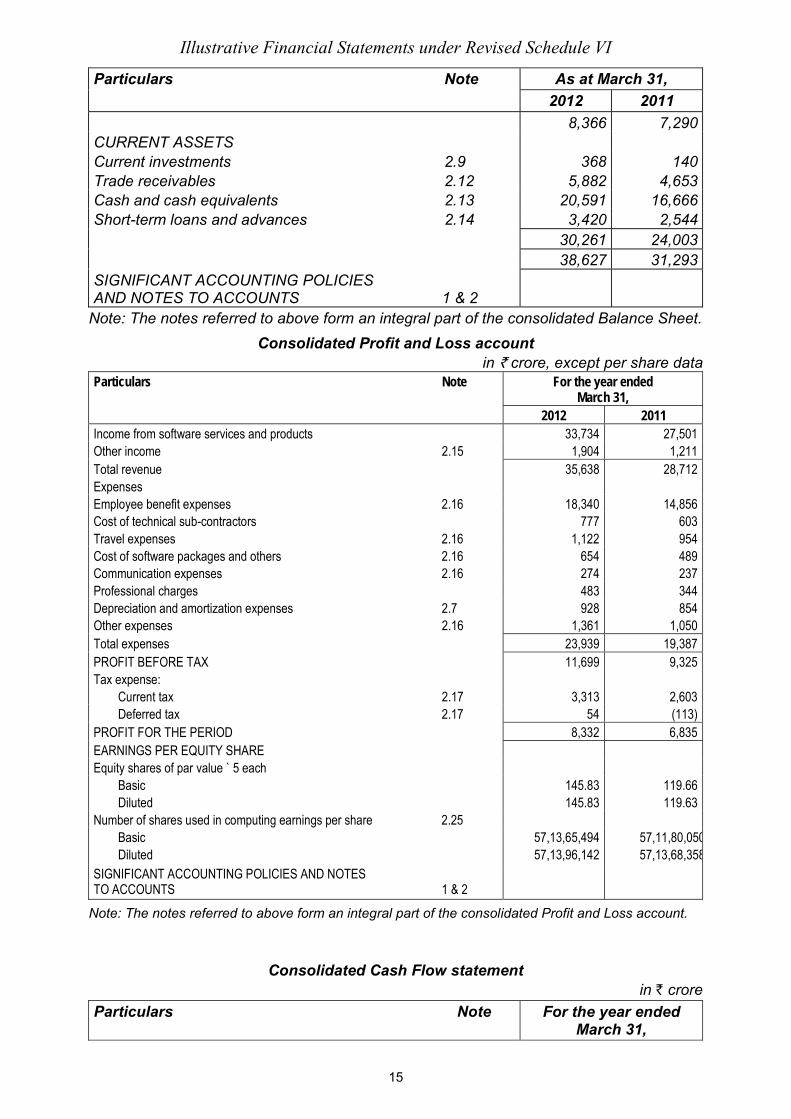

Illustrative Financial Statements under Revised Schedule VI

Particulars Note As at March 31, 2012 2011

8,366 7,290

CURRENT ASSETS

Current investments 2.9 368 140

Trade receivables 2.12 5,882 4,653

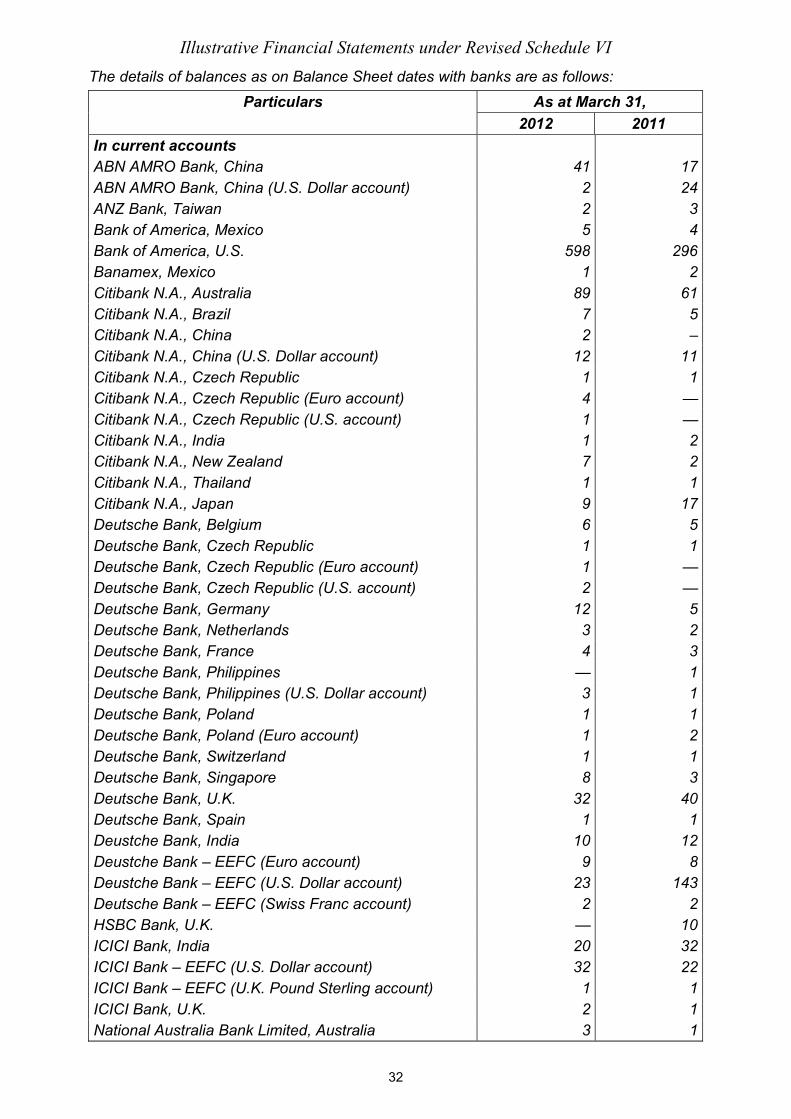

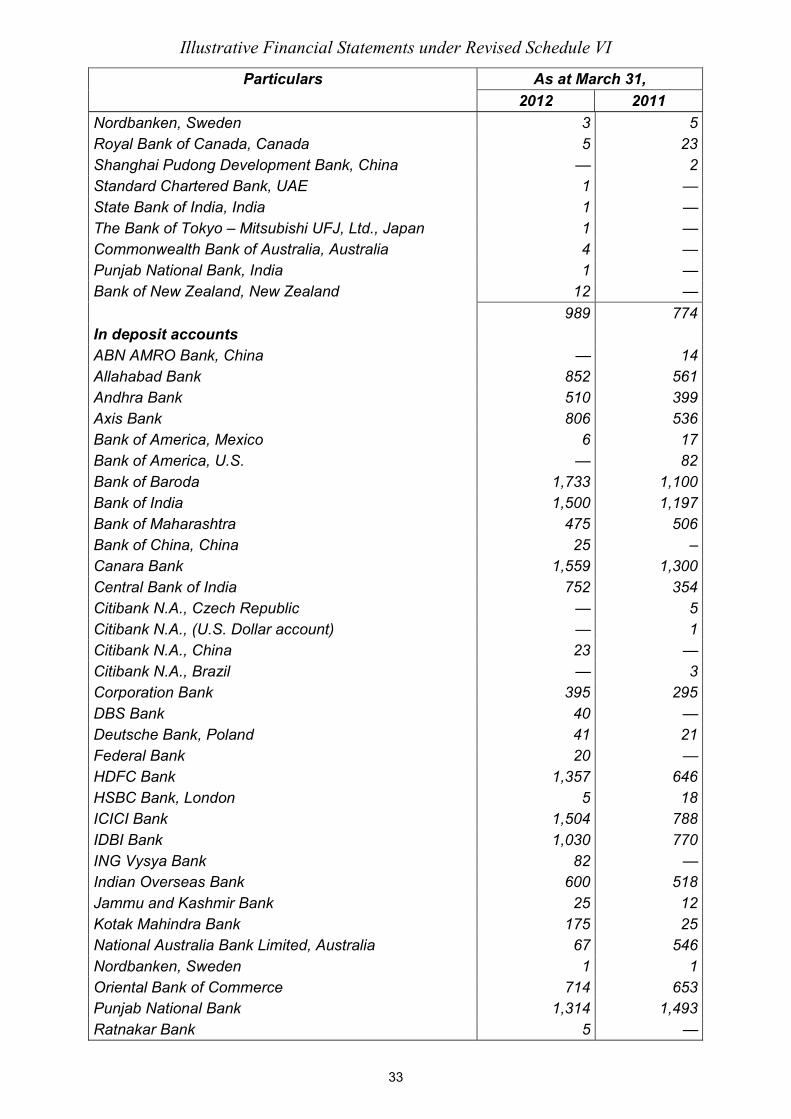

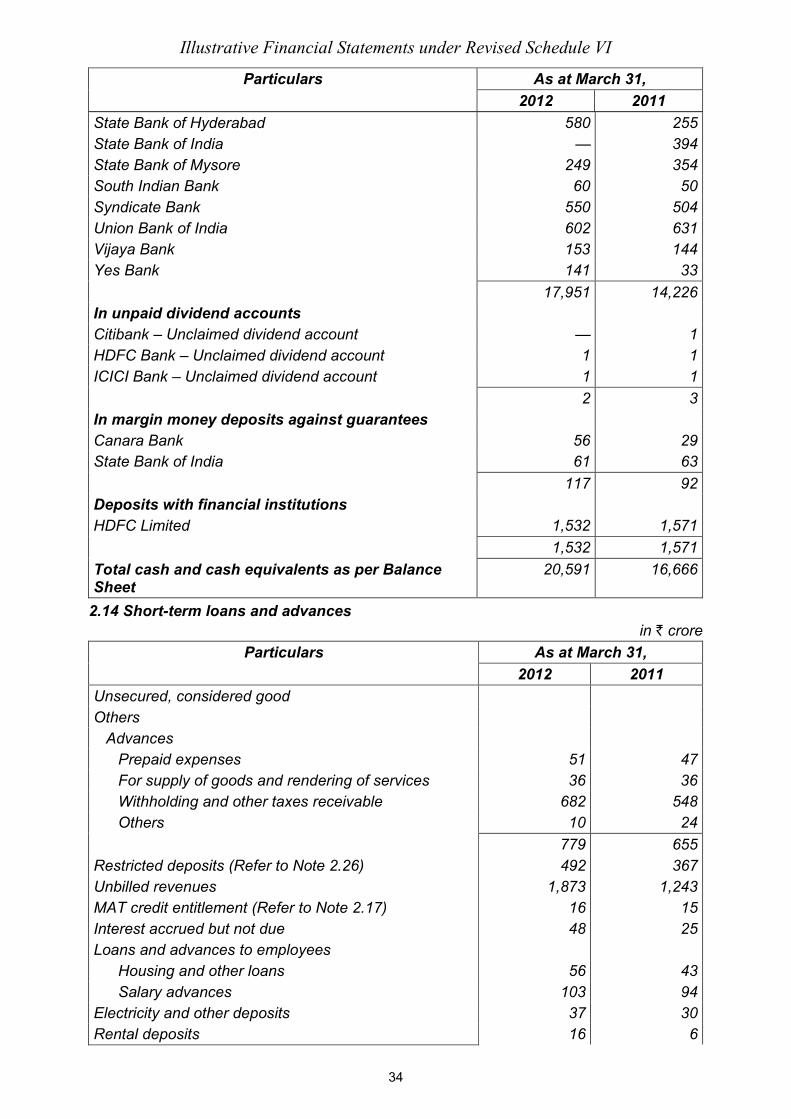

Cash and cash equivalents 2.13 20,591 16,666

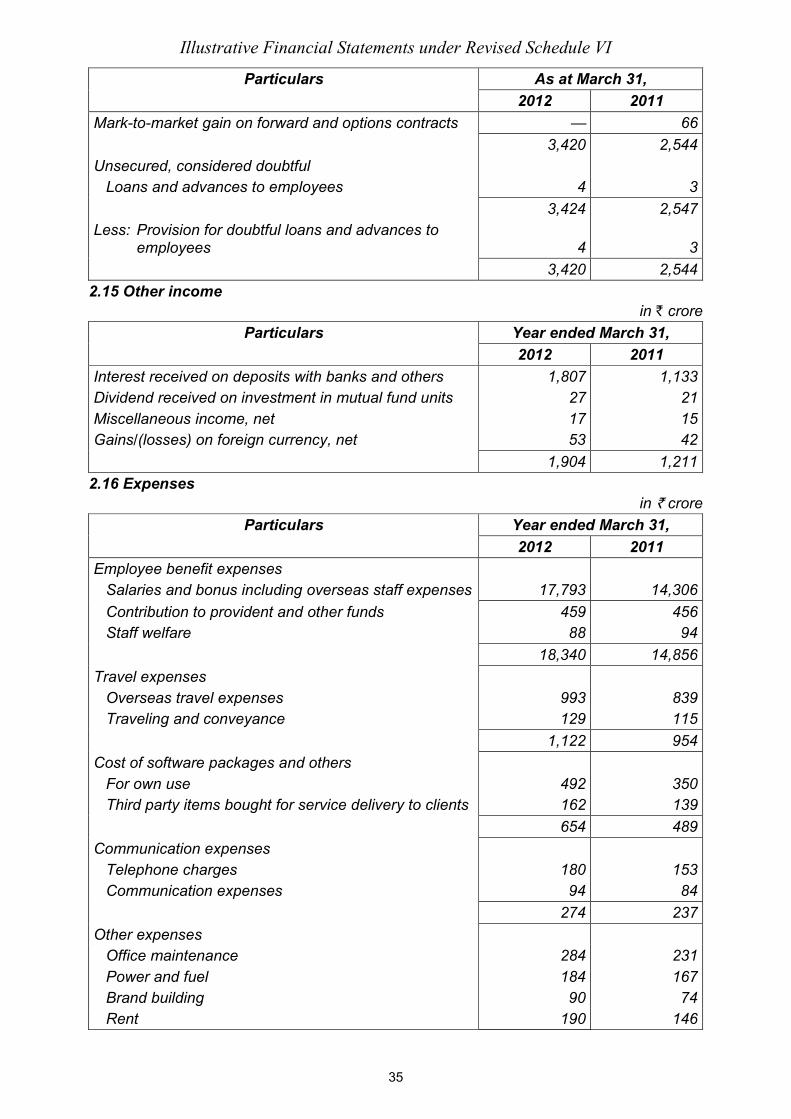

Short-term loans and advances 2.14 3,420 2,544

30,261 24,003

38,627 31,293

SIGNIFICANT ACCOUNTING POLICIES

AND NOTES TO ACCOUNTS 1 & 2

Note: The notes referred to above form an integral part of the consolidated Balance Sheet.

Consolidated Profit and Loss account in ` crore, except per share data

Particulars Note For the year ended March 31,

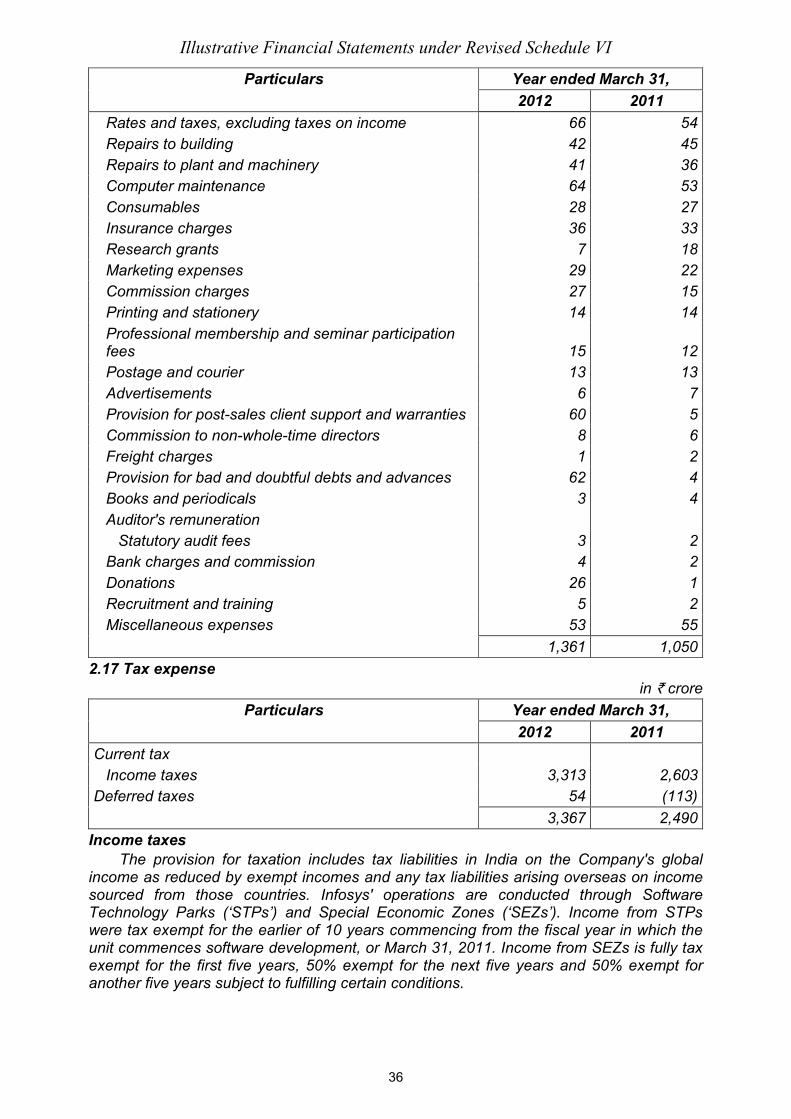

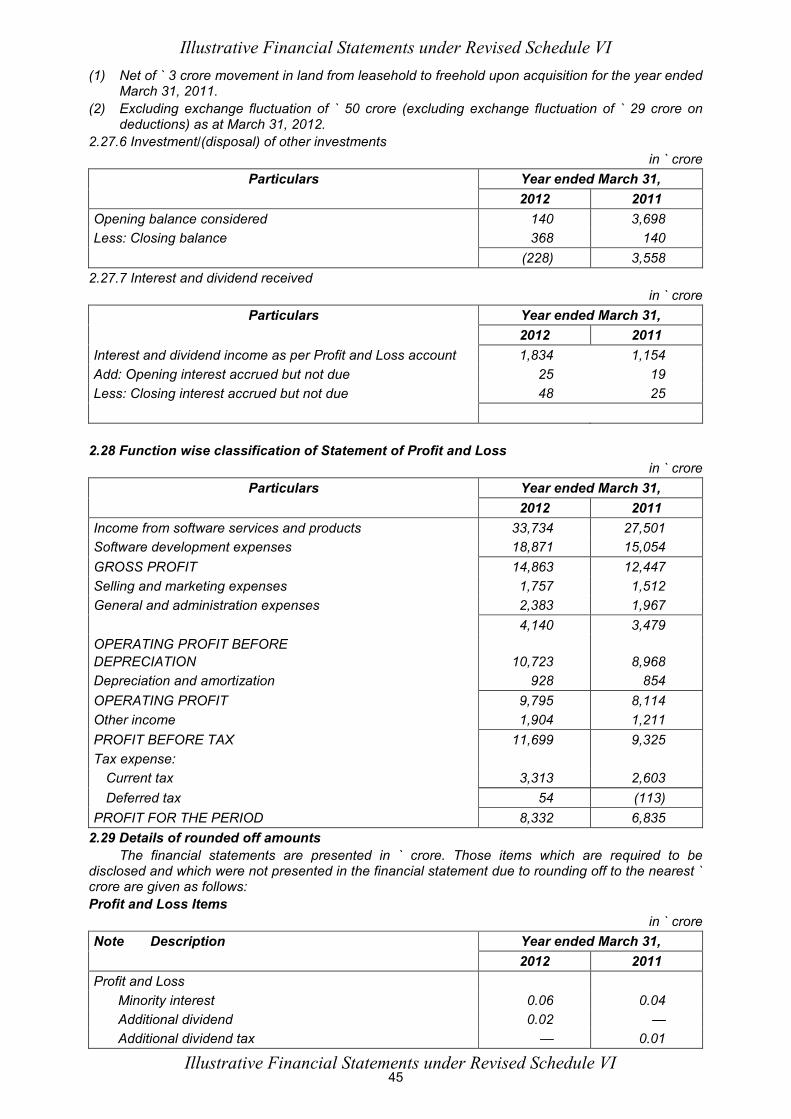

2012 2011 Income from software services and products 33,734 27,501Other income 2.15 1,904 1,211 Total revenue 35,638 28,712Expenses Employee benefit expenses 2.16 18,340 14,856Cost of technical sub-contractors 777 603Travel expenses 2.16 1,122 954Cost of software packages and others 2.16 654 489Communication expenses 2.16 274 237Professional charges 483 344Depreciation and amortization expenses 2.7 928 854Other expenses 2.16 1,361 1,050 Total expenses 23,939 19,387PROFIT BEFORE TAX 11,699 9,325 Tax expense:

Current tax 2.17 3,313 2,603 Deferred tax 2.17 54 (113)

PROFIT FOR THE PERIOD 8,332 6,835 EARNINGS PER EQUITY SHARE Equity shares of par value ` 5 each

Basic 145.83 119.66 Diluted 145.83 119.63

Number of shares used in computing earnings per share 2.25 Basic 57,13,65,494 57,11,80,050Diluted 57,13,96,142 57,13,68,358

SIGNIFICANT ACCOUNTING POLICIES AND NOTES TO ACCOUNTS 1 & 2

Note: The notes referred to above form an integral part of the consolidated Profit and Loss account.

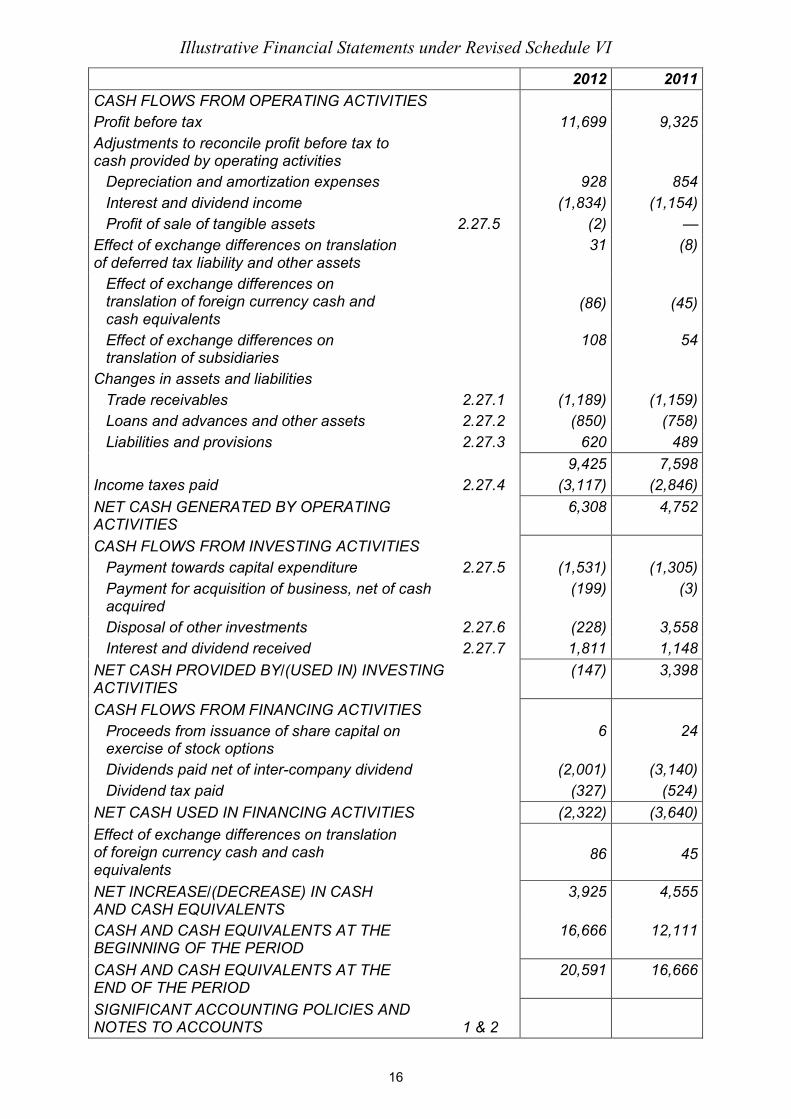

Consolidated Cash Flow statement in ` crore

Particulars Note For the year ended March 31,

15

Illustrative Financial Statements under Revised Schedule VI

2012 2011 CASH FLOWS FROM OPERATING ACTIVITIES

Profit before tax 11,699 9,325

Adjustments to reconcile profit before tax to

cash provided by operating activities

Depreciation and amortization expenses 928 854

Interest and dividend income (1,834) (1,154)

Profit of sale of tangible assets 2.27.5 (2) —

Effect of exchange differences on translation

of deferred tax liability and other assets

31 (8)

Effect of exchange differences on

translation of foreign currency cash and

cash equivalents (86) (45)

Effect of exchange differences on

translation of subsidiaries

108 54

Changes in assets and liabilities

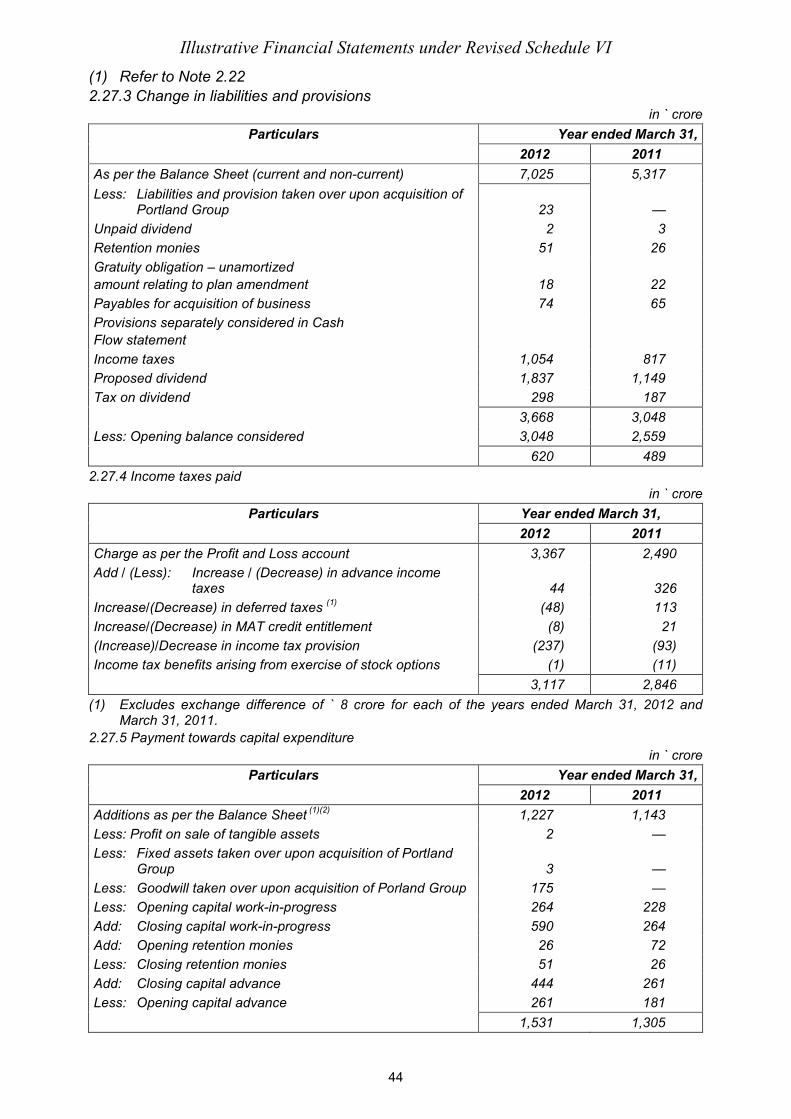

Trade receivables 2.27.1 (1,189) (1,159)

Loans and advances and other assets 2.27.2 (850) (758)

Liabilities and provisions 2.27.3 620 489

9,425 7,598

Income taxes paid 2.27.4 (3,117) (2,846)

NET CASH GENERATED BY OPERATING

ACTIVITIES

6,308 4,752

CASH FLOWS FROM INVESTING ACTIVITIES

Payment towards capital expenditure 2.27.5 (1,531) (1,305)

Payment for acquisition of business, net of cash

acquired

(199) (3)

Disposal of other investments 2.27.6 (228) 3,558

Interest and dividend received 2.27.7 1,811 1,148

NET CASH PROVIDED BY/(USED IN) INVESTING

ACTIVITIES

(147) 3,398

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from issuance of share capital on

exercise of stock options

6 24

Dividends paid net of inter-company dividend (2,001) (3,140)

Dividend tax paid (327) (524)

NET CASH USED IN FINANCING ACTIVITIES (2,322) (3,640)

Effect of exchange differences on translation

of foreign currency cash and cash

equivalents 86 45

NET INCREASE/(DECREASE) IN CASH

AND CASH EQUIVALENTS

3,925 4,555

CASH AND CASH EQUIVALENTS AT THE

BEGINNING OF THE PERIOD

16,666 12,111

CASH AND CASH EQUIVALENTS AT THE

END OF THE PERIOD

20,591 16,666

SIGNIFICANT ACCOUNTING POLICIES AND

NOTES TO ACCOUNTS 1 & 2

16

Illustrative Financial Statements under Revised Schedule VI

Note: The notes referred to above form an integral part of the consolidated Cash Flow

statement.

Significant accounting policies and notes to accounts Company overview

Infosys Limited (‘Infosys’ or ‘the Company’) along with its majority-owned and

controlled subsidiary, Infosys BPO Limited (‘Infosys BPO’) and wholly-owned and

controlled subsidiaries, Infosys Technologies (Australia) Pty. Limited (‘Infosys Australia’),

Infosys Technologies (China) Co. Limited (‘Infosys China’), Infosys Consulting India

Limited (‘Infosys Consulting India’), Infosys Technologies S. de R. L. de C. V. (‘Infosys

Mexico’), Infosys Technologies (Sweden) AB (‘Infosys Sweden’), Infosys Tecnologia do

Brasil Ltd. (‘Infosys Brasil’), Infosys Public Services Inc., U.S. (‘Infosys Public Services’)

and Infosys Technologies (Shanghai) Co. Limited (‘Infosys Shanghai’) is a leading global

technology services corporation. The group of companies (‘the Group’) provides business

consulting, technology, engineering and outsourcing services to help clients build

tomorrow's enterprise. In addition, the Group offers software products for the banking

industry.

1. Significant accounting policies 1.1 Basis of preparation of financial statements

These financial statements are prepared in accordance with Indian Generally

Accepted Accounting Principles (GAAP) under the historical cost convention on the

accrual basis except for certain financial instruments which are measured at fair values.

GAAP comprises mandatory accounting standards as prescribed by the Companies

(Accounting Standards) Rules, 2006, the provisions of the Companies Act, 1956 and

guidelines issued by the Securities and Exchange Board of India (SEBI). Accounting

policies have been consistently applied except where a newly issued accounting standard

is initially adopted or a revision to an existing accounting standard requires a change in

the accounting policy hitherto in use.

The financial statements are prepared in accordance with the principles and

procedures required for the preparation and presentation of consolidated financial

statements as laid down under the Accounting Standard (AS) 21, ‘Consolidated Financial

Statements’. The financial statements of Infosys – the parent company, Infosys BPO,

Infosys China, Infosys Australia, Infosys Mexico, Infosys Consulting India, Infosys

Sweden, Infosys Brasil, Infosys Public Services, Infosys Shanghai and controlled trusts

have been combined on a line-by-line basis by adding together book values of like items

of assets, liabilities, income and expenses after eliminating intra-group balances and

transactions and resulting unrealized gain/loss. The consolidated financial statements are

prepared by applying uniform accounting policies in use at the Group. Minority interests

have been excluded. Minority interests represent that part of the net profit or loss and net

assets of subsidiaries that are not, directly or indirectly, owned or controlled by the

Company.

1.2 Use of estimates The preparation of the financial statements in conformity with GAAP requires the

Management to make estimates and assumptions that affect the reported balances of

assets and liabilities and disclosures relating to contingent liabilities as at the date of the

financial statements and reported amounts of income and expenses during the period.

Examples of such estimates include computation of percentage-of-completion which

requires the Group to estimate the efforts expended to date as a proportion of the total

efforts to be expended, provisions for doubtful debts, future obligations under employee

retirement benefit plans, income taxes, post-sales customer support and the useful lives of

fixed assets and intangible assets.

Accounting estimates could change from period to period. Actual results could differ

from those estimates. Appropriate changes in estimates are made as the Management

17

Illustrative Financial Statements under Revised Schedule VI

becomes aware of changes in circumstances surrounding the estimates. Changes in

estimates are reflected in the consolidated financial statements in the period in which

changes are made and, if material, their effects are disclosed in the notes to the

consolidated financial statements.

The Management periodically assesses using, external and internal sources, whether

there is an indication that an asset may be impaired. An impairment loss is recognized

wherever the carrying value of an asset exceeds its recoverable amount. The recoverable

amount is higher of the asset's net selling price and value in use, which means the present

value of future cash flows expected to arise from the continuing use of the asset and its

eventual disposal. An impairment loss for an asset other than goodwill is reversed if, and

only if, the reversal can be related objectively to an event occurring after the impairment

loss was recognized. The carrying amount of an asset other than goodwill is increased to

its revised recoverable amount, provided that this amount does not exceed the carrying

amount that would have been determined (net of any accumulated amortization or

depreciation) had no impairment loss been recognized for the asset in prior years.

1.3 Revenue recognition Revenue is primarily derived from software development and related services and

from the licensing of software products. Arrangements with customers for software

development and related services are either on a fixed-price, fixed-timeframe or on a time-

and-material basis.

Revenue on time-and-material contracts are recognized as the related services are

performed and revenue from the end of the last billing to the Balance Sheet date is

recognized as unbilled revenues. Revenue from fixed-price and fixed-timeframe contracts,

where there is no uncertainty as to measurement or collectability of consideration, is

recognized based upon the percentage-of-completion method. When there is uncertainty

as to measurement or ultimate collectability revenue recognition is postponed until such

uncertainty is resolved. Cost and earnings in excess of billings are classified as unbilled

revenue while billings in excess of cost and earnings is classified as unearned revenue.

Provision for estimated losses, if any, on uncompleted contracts are recorded in the period

in which such losses become probable based on the current estimates.

Annual Technical Services revenue and revenue from fixed-price maintenance

contracts are recognized ratably over the period in which services are rendered. Revenue

from the sale of user licenses for software applications is recognized on transfer of the title

in the user license, except in case of multiple element contracts, which require significant

implementation services, where revenue for the entire arrangement is recognized over the

implementation period based upon the percentage-of-completion method. Revenue from

client training, support and other services arising due to the sale of software products is

recognized as the related services performed.

The Group accounts for volume discounts and pricing incentives to customers as a

reduction of revenue based on the ratable allocation of the discount/incentive amount to

each of the underlying revenue transactions that result in progress by the customer

towards earning the discount/incentive. Also, when the level of discount varies with

increases in levels of revenue transactions, the Group recognizes the liability based on its

estimate of the customer's future purchases. If it is probable that the criteria for the

discount will not be met, or if the amount thereof cannot be estimated reliably, then

discount is not recognized until the payment is probable and the amount can be estimated

reliably. The Group recognizes changes in the estimated amount of obligations for

discounts using a cumulative catch-up approach. The discounts are passed on to the

customer either as direct payments or as a reduction of payments due from the customer.

The Group presents revenues net of value-added taxes in its Consolidated Statement

of Profit and Loss.

Profit on sale of investments is recorded on transfer of title from the Group and is

determined as the difference between the sale price and carrying value of the investment.

18

Illustrative Financial Statements under Revised Schedule VI

Lease rentals are recognized ratably on a straight-line basis over the lease term. Interest

is recognized using the time-proportion method, based on rates implicit in the transaction.

Dividend income is recognized when the Group's right to receive dividend is established.

1.4 Provisions and contingent liabilities A provision is recognized if, as a result of a past event, the Group has a present legal

obligation that can be estimated reliably, and it is probable that an outflow of economic

benefits will be required to settle the obligation. Provisions are determined by the best

estimate of the outflow of economic benefits required to settle the obligation at the

reporting date. Where no reliable estimate can be made, a disclosure is made as

contingent liability. A disclosure for a contingent liability is also made when there is a

possible obligation or a present obligation that may, but probably will not, require an

outflow of resources. Where there is a possible obligation or a present obligation in

respect of which the likelihood of outflow of resources is remote, no provision or disclosure

is made.

1.5 Post-sales client support and warranties The Group provides its clients with a fixed-period warranty for corrections of errors

and telephone support on all its fixed-price, fixed-timeframe contracts. Costs associated

with such support services are accrued at the time when related revenues are recorded

and included in cost of sales. The Group estimates such costs based on historical

experience and the estimates are reviewed annually for any material changes in

assumptions.

1.6 Onerous contracts Provisions for onerous contracts are recognized when the expected benefits to be

derived by the Group from a contract are lower than the unavoidable costs of meeting the

future obligations under the contract. The provision is measured at lower of the expected

cost of terminating the contract and the expected net cost of fulfilling the contract.

1.7 Fixed assets, including goodwill, intangible assets and capital work-in-progress Fixed assets are stated at cost, less accumulated depreciation and impairment, if any.

Direct costs are capitalized until fixed assets are ready for use. Capital work-in-progress

comprises the cost of fixed assets that are not yet ready for their intended use at the

reporting date. Intangible assets are recorded at the consideration paid for acquisition of

such assets and are carried at cost less accumulated amortization and impairment.

Goodwill comprises the excess of purchase consideration over the fair value of the net

assets of the acquired enterprise. Goodwill arising on consolidation or acquisition is not

amortized but is tested for impairment.

1.8 Depreciation and amortization Depreciation on fixed assets is provided on the straight-line method over the useful

lives of assets estimated by the Management. Depreciation for assets purchased/sold

during a period is proportionately charged. Individual low cost assets (acquired for ` 5,000

or less) are depreciated over a period of one year from the date of acquisition. Intangible

assets are amortized over their respective individual estimated useful lives on a straight-

line basis, commencing from the date the asset is available to the Group for its use.

Leasehold improvements are written off over the lower of the remaining primary period of

lease or the life of the asset.

The Management estimates the useful lives for the other fixed assets as follows:

Buildings 15 years

Plant and machinery 5 years

Office equipment 5 years

Computer equipment 2 – 5 years

Furniture and fixtures 5 years

Vehicles 5 years

19

Illustrative Financial Statements under Revised Schedule VI

Depreciation methods, useful lives and residual values are reviewed at each reporting

date.

1.9 Retirement benefits to employees Gratuity

In accordance with the Payment of Gratuity Act, 1972, Infosys provides for gratuity, a

defined benefit retirement plan (‘the Gratuity Plan’) covering eligible employees of the

Company and Infosys BPO. The Gratuity Plan provides a lump-sum payment to vested

employees at retirement, death, incapacitation or termination of employment, of an

amount based on the respective employee's salary and the tenure of employment with the

Group.

Liabilities with regard to the Gratuity Plan are determined by actuarial valuation at

each Balance Sheet date using the projected unit credit method. The Company fully

contributes all ascertained liabilities to the Infosys Limited Employees' Gratuity Fund Trust

(‘the Trust’). In case of Infosys BPO, contributions are made to the Infosys BPO's

Employees' Gratuity Fund Trust. Trustees administer contributions made to the Trust and

contributions are invested in a scheme with Life Insurance Corporation as permitted by the

law. The Group recognizes the net obligation of the Gratuity Plan in the consolidated

Balance Sheet as an asset or liability, respectively in accordance with Accounting

Standard (AS) 15, ‘Employee Benefits’. The Group's overall expected long-term rate-of-

return on assets has been determined based on consideration of available market

information, current provisions of Indian law specifying the instruments in which

investments can be made, and historical returns. The discount rate is based on the

Government securities yield. Actuarial gains and losses arising from experience

adjustments and changes in actuarial assumptions are recognized in the Consolidated

Statement of Profit and Loss in the period in which they arise.

Superannuation

Certain employees of Infosys are also participants in a defined contribution plan. The

Company has no further obligations to the Plan beyond its monthly contributions. Certain

employees of Infosys BPO are also eligible for superannuation benefit. Infosys BPO has

no further obligations to the superannuation plan beyond its monthly contribution which

are periodically contributed to a trust fund, the corpus of which is invested with the Life

Insurance Corporation of India.

Certain employees of Infosys Australia are also eligible for the superannuation

benefit. Infosys Australia has no further obligations to the superannuation plan beyond its

monthly contribution.

Provident fund

Eligible employees receive benefits from a provident fund, which is a defined benefit

plan. Both the employee and the Company make monthly contributions to the provident

fund plan equal to a specified percentage of the covered employee's salary. The Company

contributes a part of the contributions to the Infosys Limited Employees' Provident Fund

Trust. The trust invests in specific designated instruments as permitted by Indian law. The

remaining portion is contributed to the government administered pension fund. The rate at

which the annual interest is payable to the beneficiaries by the trust is being administered

by the government. The Company has an obligation to make good the shortfall, if any,

between the return from the investments of the trust and the notified interest rate.

In respect of Infosys BPO, eligible employees receive benefits from a provident fund,

which is a defined contribution plan. Both the employee and Infosys BPO make monthly

contributions to this provident fund plan equal to a specified percentage of the covered

employee's salary. Amounts collected under the provident fund plan are deposited in a

government administered provident fund. Infosys BPO has no further obligations under

the provident fund plan beyond its monthly contributions.

Compensated absences

The employees of the Group are entitled to compensated absences which are both

20

Illustrative Financial Statements under Revised Schedule VI

accumulating and non-accumulating in nature. The expected cost of accumulating

compensated absences is determined by actuarial valuation based on the additional

amount expected to be paid as a result of the unused entitlement that has accumulated at

the Balance Sheet date. Expense on non-accumulating compensated absences is

recognized in the period in which the absences occur.

1.10 Research and development Research costs are expensed as incurred. Software product development costs are

expensed as incurred unless technical and commercial feasibility of the project is

demonstrated, future economic benefits are probable, the Company has an intention and

ability to complete and use or sell the software and the costs can be measured reliably.

1.11 Foreign currency transactions Foreign currency denominated monetary assets and liabilities are translated into the

relevant functional currency at exchange rates in effect at the Balance Sheet date. The

gains or losses resulting from such translations are included in the Statement of Profit and

Loss. Non-monetary assets and non-monetary liabilities denominated in a foreign

currency and measured at fair value are translated at the exchange rate prevalent at the

date when the fair value was determined. Non-monetary assets and non-monetary

liabilities denominated in a foreign currency and measured at historical cost are translated

at the exchange rate prevalent at the date of transaction.

Revenue, expense and cash-flow items denominated in foreign currencies are

translated into the relevant functional currencies using the exchange rate in effect on the

date of the transaction. Transaction gains or losses realized upon settlement of foreign

currency transactions are included in determining net profit for the period in which the

transaction is settled.

The functional currency of Infosys, Infosys BPO and Infosys Consulting India is the

Indian rupee. The functional currencies for Infosys Australia, Infosys China, Infosys

Mexico, Infosys Sweden, Infosys Brazil, Infosys Public Services and Infosys Shanghai are

their respective local currencies. The translation of financial statements of the foreign

subsidiaries from the local currency to the functional currency of the Company is

performed for Balance Sheet accounts using the exchange rate in effect at the Balance

Sheet date and for revenue, expense and cash-flow items using a monthly average

exchange rate for the respective periods and the resulting difference is presented as

foreign currency translation reserve included in ‘Reserves and Surplus’. When a

subsidiary is disposed off, in part or in full, the relevant amount is transferred to Profit or

Loss.

1.12 Forward and options contracts in foreign currencies The Group uses foreign exchange forward and options contracts to hedge its

exposure to movements in foreign exchange rates. The use of these foreign exchange

forward and options contracts reduce the risk or cost to the Group and the Group does not

use those for trading or speculation purposes.

Effective April 1, 2008, the Group adopted AS 30, ‘Financial Instruments: Recognition

and Measurement’, to the extent that the adoption did not conflict with existing accounting

standards and other authoritative pronouncements of the Company Law and other

regulatory requirements.

Forward and options contracts are fair valued at each reporting date. The resultant

gain or loss from these transactions are recognized in the Consolidated Statement of

Profit and Loss. The Group records the gain or loss on effective hedges, if any, in the

foreign currency fluctuation reserve until the transactions are complete. On completion,

the gain or loss is transferred to the Consolidated Statement of Profit and Loss of that

period. To designate a forward or options contract as an effective hedge, the Management

objectively evaluates and evidences with appropriate supporting documents at the

inception of each contract whether the contract is effective in achieving offsetting cash

21

Illustrative Financial Statements under Revised Schedule VI

flows attributable to the hedged risk. In the absence of a designation as effective hedge, a

gain or loss is recognized in the Consolidated Statement of Profit and Loss. Currently

hedges undertaken by the Group are all ineffective in nature and the resultant gain or loss

consequent to fair valuation is recognized in the Consolidated Statement of Profit and

Loss at each reporting date.

1.13 Income taxes Income taxes are accrued in the same period that the related revenue and expenses

arise. A provision is made for income tax annually, based on the tax liability computed,

after considering tax allowances and exemptions. Provisions are recorded when it is

estimated that a liability due to disallowances or other matters is probable. Minimum

Alternate Tax (MAT) paid in accordance with the tax laws, which gives rise to future

economic benefits in the form of tax credit against future income tax liability, is recognized

as an asset in the Consolidated Balance Sheet if there is convincing evidence that the

Group will pay normal tax after the tax holiday period and the resultant asset can be

measured reliably. The Group offsets, on a year on year basis, the current tax assets and

liabilities, where it has a legally enforceable right and where it intends to settle such assets

and liabilities on a net basis.

The differences that result between the profit considered for income taxes and the

profit as per the financial statements are identified, and thereafter a deferred tax asset or

deferred tax liability is recorded for timing differences, namely the differences that

originate in one accounting period and reverse in another, based on the tax effect of the

aggregate amount of timing difference. The tax effect is calculated on the accumulated

timing differences at the end of an accounting period based on enacted or substantively

enacted regulations. Deferred tax assets in a situation where unabsorbed depreciation

and carry forward business loss exists, are recognized only if there is virtual certainty

supported by convincing evidence that sufficient future taxable income will be available

against which such deferred tax asset can be realized. Deferred tax assets, other than in

situation of unabsorbed depreciation and carry forward business loss, are recognized only

if there is reasonable certainty that they will be realized. Deferred tax assets are reviewed

for the appropriateness of their respective carrying values at each reporting date. Deferred

tax assets and deferred tax liabilities have been offset wherever the Group has a legally

enforceable right to set off current tax assets against current tax liabilities and where the

deferred tax assets and deferred tax liabilities relate to income taxes levied by the same

taxation authority. Tax benefits of deductions earned on exercise of employee share

options in excess of compensation charged to the Consolidated Statement of Profit and

Loss are credited to the share premium account.

1.14 Earnings per share Basic earnings per share is computed by dividing the net profit after tax by the

weighted average number of equity shares outstanding during the period. Diluted earnings

per share is computed by dividing the net profit after tax by the weighted average number

of equity shares considered for deriving basic earnings per share and also the weighted

average number of equity shares that could have been issued upon conversion of all

dilutive potential equity shares. The diluted potential equity shares are adjusted for the

proceeds receivable had the shares been actually issued at fair value which is the

average market value of the outstanding shares. Dilutive potential equity shares are

deemed converted as of the beginning of the period, unless issued at a later date. Dilutive

potential equity shares are determined independently for each period presented.

The number of shares and potentially dilutive equity shares are adjusted

retrospectively for all periods presented for any share splits and bonus shares issues

including for changes effected prior to the approval of the consolidated financial

statements by the Board of Directors.

1.15 Investments Trade investments are the investments made to enhance the Group's business

interests. Investments are either classified as current or long-term based on the

22

Illustrative Financial Statements under Revised Schedule VI

Management's intention at the time of purchase. Current investments are carried at the

lower of cost and fair value of each investment individually. Cost for overseas investments

comprises the Indian rupee value of the consideration paid for the investment translated at

the exchange rate prevalent at the date of investment. Long-term investments are carried

at cost less provisions recorded to recognize any decline, other than temporary, in the

carrying value of each investment.

1.16 Cash and cash equivalents Cash and cash equivalents comprise cash and cash on deposit with banks and

corporations. The Group considers all highly liquid investments with a remaining maturity

at the date of purchase of three months or less and that are readily convertible to known

amounts of cash to be cash equivalents.

1.17 Cash flow statement Cash flows are reported using the indirect method, whereby profit before tax is

adjusted for the effects of transactions of a non-cash nature, any deferrals or accruals of

past or future operating cash receipts or payments and item of income or expenses

associated with investing or financing cash flows. The cash flows from operating, investing

and financing activities of the Group are segregated.

1.18 Leases Lease under which the Group assumes substantially all the risks and rewards of

ownership are classified as finance leases. Such assets acquired are capitalized at fair

value of the asset or present value of the minimum lease payments at the inception of the

lease, whichever is lower. Lease payments under operating leases are recognized as an

expense on a straight-line basis in the Consolidated Statement of Profit and Loss over the

lease term.

1.19 Government grants The Group recognizes government grants only when there is reasonable assurance

that the conditions attached to them shall be complied with, and the grants will be

received. Government grants related to depreciable assets are treated as deferred income

and are recognized in the Consolidated Statement of Profit and Loss on a systematic and

rational basis over the useful life of the asset. Government grants related to revenue are

recognized on a systematic basis in the Consolidated Statement of Profit and Loss over

the periods necessary to match them with the related costs which they are intended to

compensate.

2. Notes to accounts for the year ended March 31, 2012

Amounts in the financial statements are presented in ` crore, except for per share

data and as otherwise stated. Certain amounts that are required to be disclosed and do

not appear due to rounding off are detailed in note 2.29. All exact amounts are stated with

the suffix ‘/-’. One crore equals 10 million.

The previous years figures have been regrouped/re-classified, wherever necessary to

conform to the current presentation.

23

Illustrative Financial Statements under Revised Schedule VI

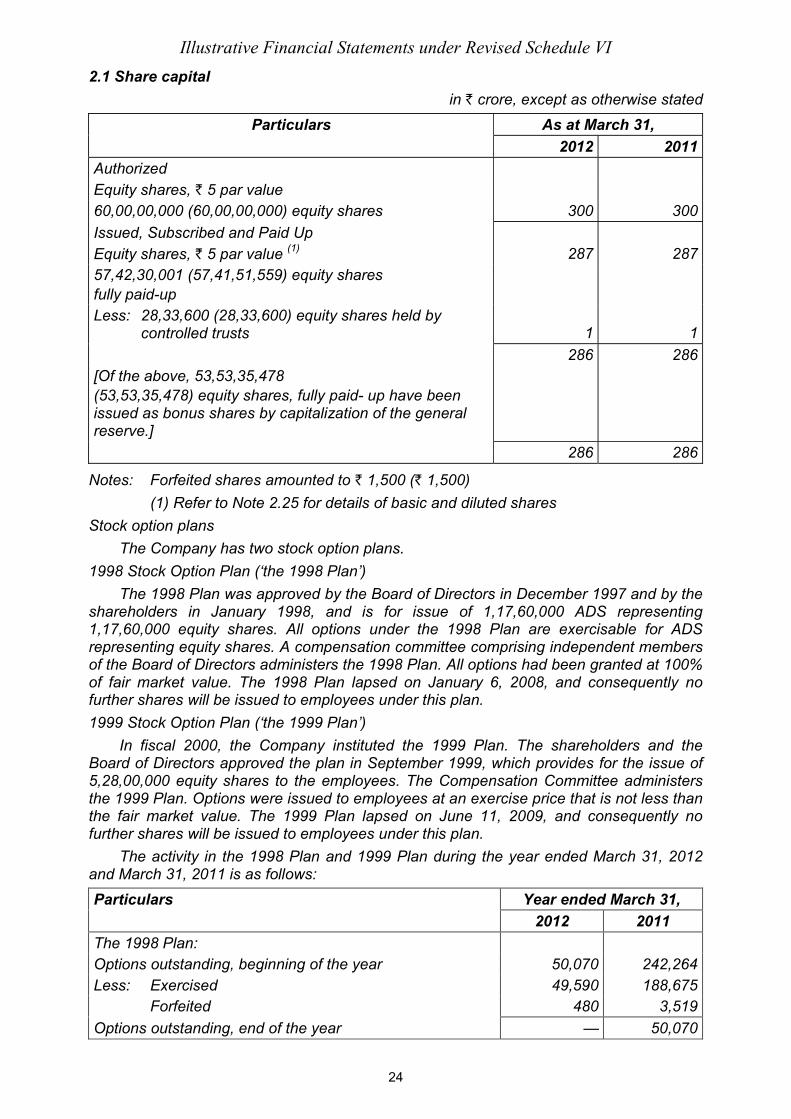

2.1 Share capital in ` crore, except as otherwise stated

Particulars As at March 31, 2012 2011

Authorized

Equity shares, ` 5 par value

60,00,00,000 (60,00,00,000) equity shares 300 300

Issued, Subscribed and Paid Up

Equity shares, ` 5 par value (1)

287 287

57,42,30,001 (57,41,51,559) equity shares

fully paid-up

Less: 28,33,600 (28,33,600) equity shares held by

controlled trusts 1 1

286 286

[Of the above, 53,53,35,478

(53,53,35,478) equity shares, fully paid- up have been

issued as bonus shares by capitalization of the general

reserve.]

286 286

Notes: Forfeited shares amounted to ` 1,500 (` 1,500)

(1) Refer to Note 2.25 for details of basic and diluted shares

Stock option plans

The Company has two stock option plans.

1998 Stock Option Plan (‘the 1998 Plan’)

The 1998 Plan was approved by the Board of Directors in December 1997 and by the

shareholders in January 1998, and is for issue of 1,17,60,000 ADS representing

1,17,60,000 equity shares. All options under the 1998 Plan are exercisable for ADS

representing equity shares. A compensation committee comprising independent members

of the Board of Directors administers the 1998 Plan. All options had been granted at 100%

of fair market value. The 1998 Plan lapsed on January 6, 2008, and consequently no

further shares will be issued to employees under this plan.

1999 Stock Option Plan (‘the 1999 Plan’)

In fiscal 2000, the Company instituted the 1999 Plan. The shareholders and the

Board of Directors approved the plan in September 1999, which provides for the issue of

5,28,00,000 equity shares to the employees. The Compensation Committee administers

the 1999 Plan. Options were issued to employees at an exercise price that is not less than

the fair market value. The 1999 Plan lapsed on June 11, 2009, and consequently no

further shares will be issued to employees under this plan.

The activity in the 1998 Plan and 1999 Plan during the year ended March 31, 2012

and March 31, 2011 is as follows:

Particulars Year ended March 31, 2012 2011

The 1998 Plan:

Options outstanding, beginning of the year 50,070 242,264

Less: Exercised 49,590 188,675

Forfeited 480 3,519

Options outstanding, end of the year — 50,070

24

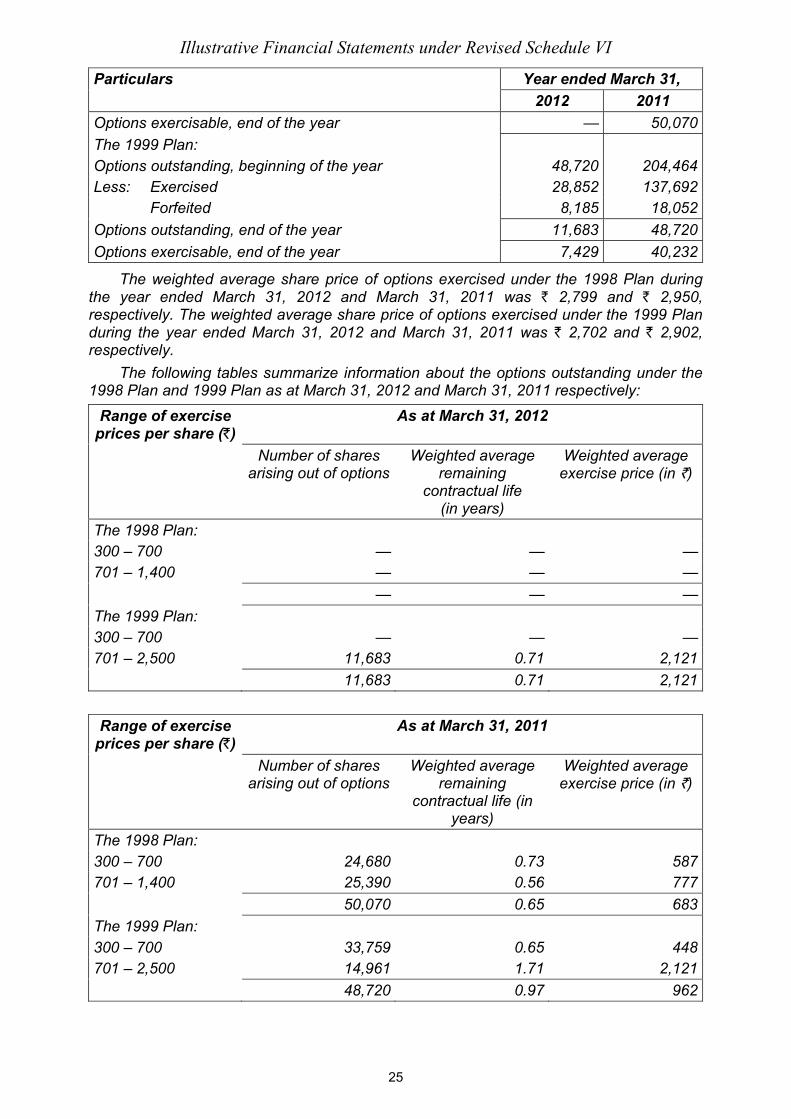

Illustrative Financial Statements under Revised Schedule VI

Particulars Year ended March 31, 2012 2011

Options exercisable, end of the year — 50,070

The 1999 Plan:

Options outstanding, beginning of the year 48,720 204,464

Less: Exercised 28,852 137,692

Forfeited 8,185 18,052

Options outstanding, end of the year 11,683 48,720

Options exercisable, end of the year 7,429 40,232

The weighted average share price of options exercised under the 1998 Plan during

the year ended March 31, 2012 and March 31, 2011 was ` 2,799 and ` 2,950,

respectively. The weighted average share price of options exercised under the 1999 Plan

during the year ended March 31, 2012 and March 31, 2011 was ` 2,702 and ` 2,902,

respectively.

The following tables summarize information about the options outstanding under the

1998 Plan and 1999 Plan as at March 31, 2012 and March 31, 2011 respectively:

Range of exercise prices per share (`)

As at March 31, 2012

Number of shares

arising out of options

Weighted average

remaining

contractual life

(in years)

Weighted average

exercise price (in `)

The 1998 Plan:

300 – 700 — — —

701 – 1,400 — — —

— — —

The 1999 Plan:

300 – 700 — — —

701 – 2,500 11,683 0.71 2,121

11,683 0.71 2,121

Range of exercise prices per share (`)

As at March 31, 2011

Number of shares

arising out of options

Weighted average

remaining

contractual life (in

years)

Weighted average

exercise price (in `)

The 1998 Plan:

300 – 700 24,680 0.73 587

701 – 1,400 25,390 0.56 777

50,070 0.65 683

The 1999 Plan:

300 – 700 33,759 0.65 448

701 – 2,500 14,961 1.71 2,121

48,720 0.97 962

25

Illustrative Financial Statements under Revised Schedule VI

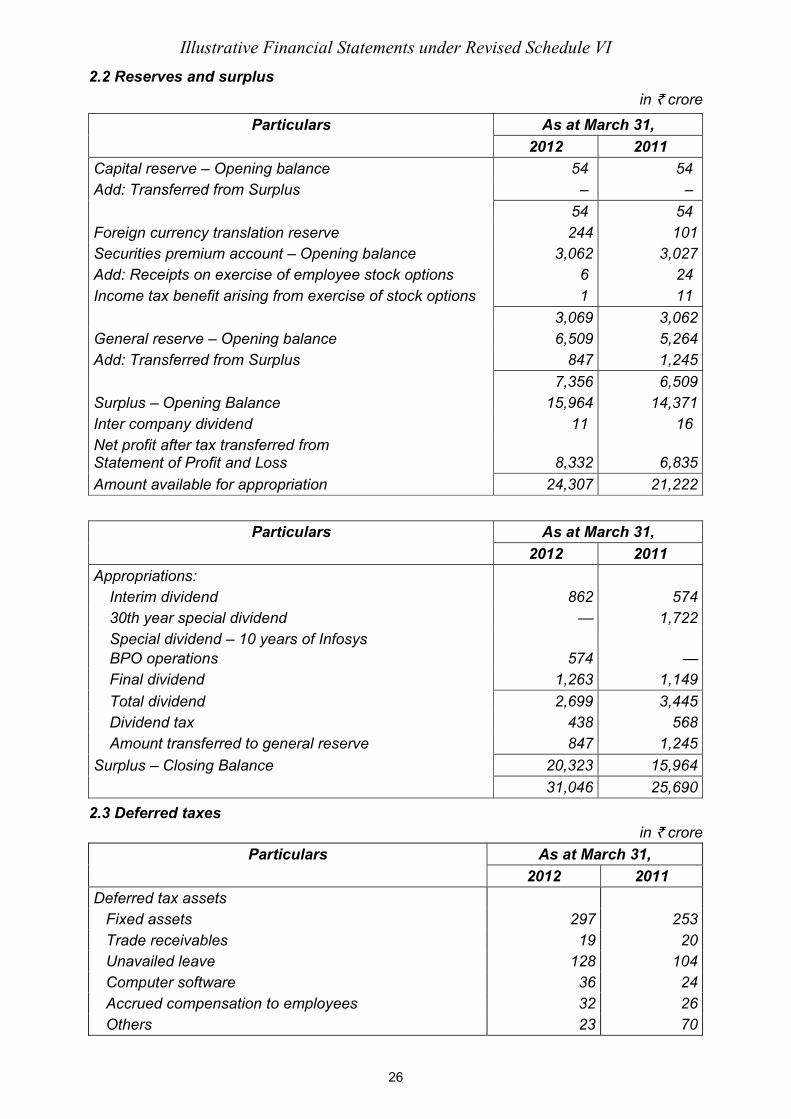

2.2 Reserves and surplus in ` crore

Particulars As at March 31, 2012 2011

Capital reserve – Opening balance 54 54

Add: Transferred from Surplus – –

54 54

Foreign currency translation reserve 244 101

Securities premium account – Opening balance 3,062 3,027

Add: Receipts on exercise of employee stock options 6 24

Income tax benefit arising from exercise of stock options 1 11

3,069 3,062

General reserve – Opening balance 6,509 5,264

Add: Transferred from Surplus 847 1,245

7,356 6,509

Surplus – Opening Balance 15,964 14,371

Inter company dividend 11 16

Net profit after tax transferred from

Statement of Profit and Loss 8,332 6,835

Amount available for appropriation 24,307 21,222

Particulars As at March 31, 2012 2011

Appropriations:

Interim dividend 862 574

30th year special dividend — 1,722

Special dividend – 10 years of Infosys

BPO operations 574 —

Final dividend 1,263 1,149

Total dividend 2,699 3,445

Dividend tax 438 568

Amount transferred to general reserve 847 1,245

Surplus – Closing Balance 20,323 15,964

31,046 25,690

2.3 Deferred taxes in ` crore

Particulars As at March 31, 2012 2011

Deferred tax assets

Fixed assets 297 253

Trade receivables 19 20

Unavailed leave 128 104

Computer software 36 24

Accrued compensation to employees 32 26

Others 23 70

26

Illustrative Financial Statements under Revised Schedule VI

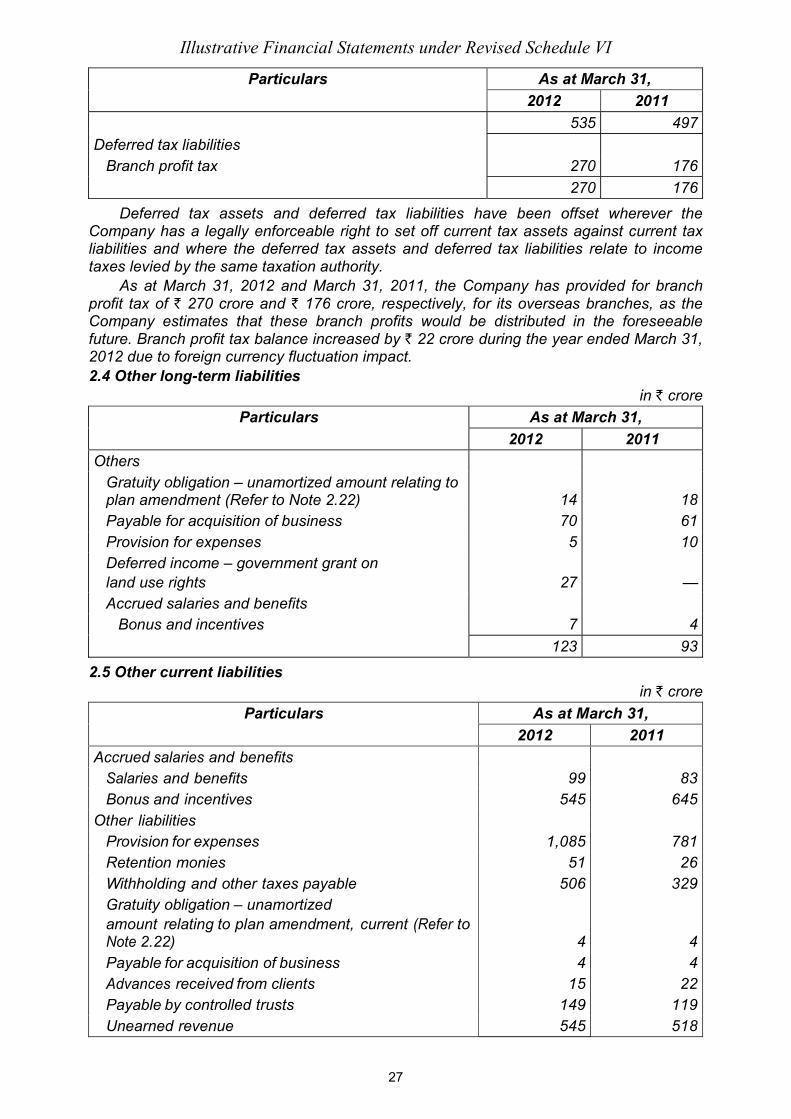

Particulars As at March 31, 2012 2011

535 497

Deferred tax liabilities

Branch profit tax 270 176

270 176

Deferred tax assets and deferred tax liabilities have been offset wherever the

Company has a legally enforceable right to set off current tax assets against current tax

liabilities and where the deferred tax assets and deferred tax liabilities relate to income

taxes levied by the same taxation authority.

As at March 31, 2012 and March 31, 2011, the Company has provided for branch

profit tax of ` 270 crore and ` 176 crore, respectively, for its overseas branches, as the

Company estimates that these branch profits would be distributed in the foreseeable

future. Branch profit tax balance increased by ` 22 crore during the year ended March 31,

2012 due to foreign currency fluctuation impact.