Embed Size (px)

Citation preview

ISSUE 8: FEBRUARY 2012

REVIEW The quarterly review of SUSTAINABILITY in South African business

2011’s sustainability coverage top performers

Sustainability awards: Useful incentives or costly distractions?

Are you taking enough responsibility for your waste?

Joanne Yawitch: “Business must have the difficult conversations.”

Government has a sustainability vision – what’s yours?

siemens.com/answers

The South Africa of tomorrow needs answers that last.That’s why we’re building them today, with customers all over the country.

It ’s why we’re designing our technology to last longer and use fewer resources. It ’s why we’re helping our customers reduce their CO2 emissions. And it’s why we’re pioneering new answers with one of the world’s largest environmental portfolios.

As a result, we’ve been named the best in our business sector by the Dow Jones Sustainability Index. And recognized as the top company overall by the Carbon Disclosure Project, the world’s largest independent database of corporate climate change information.

Yet, we’d never claim to have all the answers. That’s why we’ve been working with customers in South Africa for more than 150 years. We’re helping develop South Africa’s infrastructure, promoting skills development and ensuring sustainable economic growth through projects across the country. In energy, industry, infrastructure and healthcare.

We’re working with South Africa today to create answers that last for the South Africa of tomorrow.

Windmills SA E Trailogue 210x273.indd 1 2012/01/30 12:03 PM

Extended producer responsibility: Out of sight, front of mind

Rewarding good behaviour or leading companies astray?

Joanne Yawitch

Current issues in numbers

Government’s visionary policies and how they impact your business

2011 in sustainability coverage: The relationships behind the numbers

CONTENTSEditorialEDITOR: Rob Worthington-SmithEDITORIAL MANAGEMENT: Michelle MatthewsCONTRIBUTORS: Cathy Duff, Susie Keane, Candice Landie, Michelle Matthews, Nick Rockey, Wadim Schreiner, Chris van CoppenhagenPROOFREADING: Shaun SwinglerPRODUCTION: Gillian MitriDESIGN AND TYPESETTING: GroundPepperPRINTING: CTP Web Printers

AdvertisingSALES: Karen PetersenADMINISTRATION: Vanessa Sampson

Contact DetailsCAPE TOWN JOHANNESBURGTel: 021 671 1640 Tel: 011 026 1308Fax: 021 671 0119

POSTAL ADDRESSPO Box 36104 Glosderry, 7702

www.trialogue.co.za

©Trialogue

All rights reserved. The material in this publication may not be reproduced, stored or transmitted in any form or by any means without the prior written permission of the copyright holder. If such permission is granted, any information used in other sources must accurately reference Trialogue and the title of this publication.

DisclaimerAlthough great care has been taken to ensure that all information contained in this publication is as accurate and complete as possible, Trialogue cannot accept any legal responsibility for the information given and the opinions expressed in it.

4LEAD FEATURE

8AWARDS

12ICON

2QUARTERLY REVIEW

14SUSTAINABILITY ISSUE

16IN THE MEDIA

siemens.com/answers

The South Africa of tomorrow needs answers that last.That’s why we’re building them today, with customers all over the country.

It ’s why we’re designing our technology to last longer and use fewer resources. It ’s why we’re helping our customers reduce their CO2 emissions. And it’s why we’re pioneering new answers with one of the world’s largest environmental portfolios.

As a result, we’ve been named the best in our business sector by the Dow Jones Sustainability Index. And recognized as the top company overall by the Carbon Disclosure Project, the world’s largest independent database of corporate climate change information.

Yet, we’d never claim to have all the answers. That’s why we’ve been working with customers in South Africa for more than 150 years. We’re helping develop South Africa’s infrastructure, promoting skills development and ensuring sustainable economic growth through projects across the country. In energy, industry, infrastructure and healthcare.

We’re working with South Africa today to create answers that last for the South Africa of tomorrow.

Windmills SA E Trailogue 210x273.indd 1 2012/01/30 12:03 PM

We are entering the season of results presentations. CEOs and their investor relations teams are polishing their PowerPoint slides and preparing for interviews with the analysts. Mostly it’s about financial performance and answering questions such as how the company intends employing its ‘lazy’ balance sheet to provide returns for the company’s shareholders.

However, interrogating the financial statements quantifies the story in the rear-view mirror, not the outlook for the company going forward. Yes, there is the company’s strategy, but how does it answer the leading, rather than the lagging, indicators of performance?

This is where non-financial issues, so-called sustainability issues (corporate governance, and social and environmental concerns), should become integral to the board’s agenda. Like cash flow and stock turn, issues such as customer satisfaction and employee motivation can also be defined, measured and monitored. These are, after all, the indicators that

will provide a clue as to how well the company is building up its relationships and using its resources to be successful over the long term. And it’s a good way to tell the story of how the company intends to add value.

How does a company sense the concerns of its customers, employees, shareholders and other stakeholders? Broader society raises long-term issues that are picked up by government; on the one hand through the development of new legislation, and on the other through changes in development policy. The article on page 14 of this issue takes a closer look at these emerging developments.

But if a company really wants to get ahead, it needs to pick up on issues long before the tide finally turns. This is where an understanding of the media is becoming increasingly important. The media may be irrational and irresponsible. But the rise of social networking is not to be underestimated. Individual rants coalesce quickly into formal advocacy

groups with clear agendas. These become sources for the traditional media journalist, looking for interesting stories. Ultimately, these perceptions become the facts in the eyes of the public. Our Sustainability Coverage Monitor (page 16), published in partnership with The Media Tenor Institute of Media Analysis, provides further insight into which companies and industries are engaging best with society on these issues.

This is the role of the Trialogue Sustainability Review – to bring you a synthesis of the issues concerning society, through opinion pieces, researched features, and analysis of perceptions as covered by the media.

We trust these insights will inform your strategies for doing responsible business – strategies that will garner those future income streams built into the share price. And by talking to these issues in your results presentations, you can add both colour and quality to your 2012 reporting season.

Rob Worthington-Smith

From the editor

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 2012 1

OUARTERLY REVIEW

On 7 December 2011 the Department of Energy announced 28 preferred renewable energy (RE) bidders, proposing 1 416MW of projects towards government’s target of 3 725MW of RE by 2016 (by way of comparison, Eskom’s new Medupi coal-fired power station will deliver 4 800MW – about 10% of total demand). The preferred bidders – selected from 53 projects – comprise eight wind, 18 photovoltaic and two concentrated solar power projects. The Industrial Development Corporation (IDC) approved funding worth R5.2 billion for 12 of the 28 preferred bidders.

Working > 60 hours for AppleApple released its list of suppliers for the first time in January 2012, after sustained pressure from stakeholders. The company’s audits found that most workers at its supplier factories exceeded the maximum prescribed work week of 60 hours. Currently, calls for consumers to boycott Apple over conditions at Chinese supplier Foxconn are receiving high-profile airtime in media.

$395bn by 2020Bloomberg New Energy Finance (BNEF) predicts in a November 2001 report, Global Renewable Energy Market Outlook, that global investment in renewable energy infrastructure will double over the next decade and throughout the 2020s, reaching $460 billion by 2030. Africa is among the markets where the desk envisions above-average growth.

50%+ HIV/Aids claimants return to workIn January 2012 life insurer Old Mutual reported that improved HIV/Aids workplace policies were having a positive impact on people at work. In 2003/4 income claims were paid for between six and ten years and 65% of claims ended on the death of the claimant. Today, policy holders claim for 18 months (on average) before returning to work, with only 20% of claims ending with death.

Unilever wants to reduce its emissions against its 1995 baseline by 40% by 2020. In line with this, the company’s new savoury food plant, launched in Durban in December 2011, has been built to ‘green’ standards. It is the second-biggest Unilever plant in the world – producing 65 000 tonnes of products a year – and cost R670 million to build. The design enables a variety of efficiencies; for example, 70% of water used can be recovered and the plant’s zero-waste goal is facilitated through innovations such as an on-site waste-to-energy plant.

OVERDRAWN

“By 2030, global freshwater withdrawals will have exceeded the current capacity to supply by over 40%,” said South African Breweries (SAB) at the launch of its industry-led initiative – the Water Resources Group – at Davos in January 2012. Together with the International Finance Corporation, Coca-Cola and Nestlé, SAB will work with a variety of stakeholders to manage the ‘nexus’ – “the point at which water security, energy security and food security overlap”.

40%

Shipping emissions are increasingly on the global policy agenda. Oxfam raised the possibility of a tax on emissions at COP17. In November 2011, UK advisory body, the Committee on Climate Change (CCC), recommended to government that shipping emissions be included in the UK’s official 2050 targets, while new rules to limit pollution from ships started moving through the European Parliament in late January 2012. Total emissions from international shipping are approximately 3% of global emissions, say WWF.

of global total

3%

Eskom has approved phase two of its demand market participation (DMP) programme, extending it from 20 large industrial users to 1000 small industrial and commercial users with flexible manufacturing processes. The state-owned power utility hopes to reduce load by 500MW by winter 2012 through demand-side management in these businesses – otherwise mandatory cuts are on the cards.

1 000ASKED TO REDUCE LOAD

In late 2011 government signed a Local Procurement Accord, based on suggestions emerging from the New Growth Path process, pledging to source three-quarters of goods from local suppliers. Standards and checks would be put in place to guard against profiteering, proponents said. The Accord ties in closely with the amended Preferential Procurement Policy Framework Act, which came into force in December 2011.

75%

buy-local

141628bidders

PRODUCING

MW

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 20122

OUARTERLY REVIEW

future

Nedbank launches the third instalment of the ‘My Future, My Career’ education project.In its commitment to help overcome the current and projected skills shortage in South Africa, as well as the high rate of unemployment among school-leavers, Nedbank, together with Primestars Marketing, presents ‘My Future, My Career’.

Providing underprivileged secondary school learners from grades 9 to 12 with expert career guidance, ‘My Future, My Career’ project content is presented in professionally shot and edited films, featuring 14 industries and over 100 careers. These films are screened

Strategic participants

Nedbank Ltd Reg N

o 1951/000009/06, VA

T Reg No 4320116074, 135 R

ivonia Road, Sandown, Sandton, 2196, South A

frica. We are an authorised fi

nancial services provider and a registered credit provider in term

s of the National C

redit Act (N

CR

Reg No N

CR

CP 16).

purple

berr

y 01

12/6

702

at strategically situated Ster-Kinekor cinemas nationwide, allowing for maximum participation.

Now in its third year, the ‘My Future, My Career’ initiative actively demonstrates Nedbank’s commitment to build intellectual sustainability and create a knowledge-based economy towards our country’s future growth.

‘My Future, My Career’ will be screened at selected cinemas nationwide during February, March and April 2012. For more information please contact Karen on 011 562 6353 or email [email protected].

view

nedbankmfmc_susad.indd 1 2/2/12 11:06:13

LEAD: ExTENDED PRODUCER RESPONSIBILITY

Out of sight,FRONT OF MIND

Increasing affluence and economic activity means waste production often outstrips population growth. With a population growth rate of 9%, Johannesburg, the economic hub of South Africa, will run out of landfill space in eight years’ time. The same is true for Cape Town and other major metropoles.

Compounding this is the effect of growing urbanisation. “We simply do not have the space to accommodate the continuously increasing levels of waste being generated as more people move into the City of Johannesburg,” declares Zandile Mpungose, environmental compliance executive at Johannesburg’s official waste management company Pikitup. Meanwhile, the National Planning Commission reports that unlicensed and poorly operated sites are having environmental and health impacts in smaller municipalities. The waste problem will not be swept under the carpet, and government is increasingly unwilling to take on the expense of handling it alone.

extended producer responsibility (ePr)While the ‘pollutor pays’ principle has been in our laws since the 1990s, the South African government has recently responded with revised legislation incorporating new approaches, a key aspect being that the scope of environmental liability for companies

Whether you are a producer or a merchant, or somewhere else in the supply chain, you will

increasingly be held responsible for what happens to the products you make and sell once your

customer no longer needs them for their primary purpose. Extended producer responsibility (EPR)

regulations are impacting businesses on several fronts, from the cost of designing and manufacturing

goods through to end-of-life waste fees. Will you wait to be legislated, or will you take responsibility?

as electronics, batteries, paint, car parts and pesticide containers.

There are a number of drivers building the business case for a more responsible approach to the product life-cycle:

• Increasingenvironmentalawarenessamong customers,

• Increasingmanufacturingandtransport costs of goods in poorly conceptualised packaging,

• Increasingpressureonresourcessuch as petroleum, metals and paper causing fluctuating prices,

• Thepotentialtocreateandmanagea new source of materials through recycling,

• Reputationaldamagefromscandalssuch as e-waste dumping in developing countries.

The big stickSection 18 of the Waste Act allows government to implement mandatory EPR initiatives. However, government intervention comes into play only if industry initiatives have failed or the waste substance has been declared a ‘priority waste’. “In the first instance, the role of regulation will be to strengthen and support voluntary EPR programmes which are initiated and run by industry,” according to the Department of Environmental Affairs’ (DEA) website, www.wastepolicy.co.za.

has been extended to the post-consumer stage of their products’ life-cycles. The Waste Act, which came into effect in 2009, establishes EPR as a regulatory mechanism.

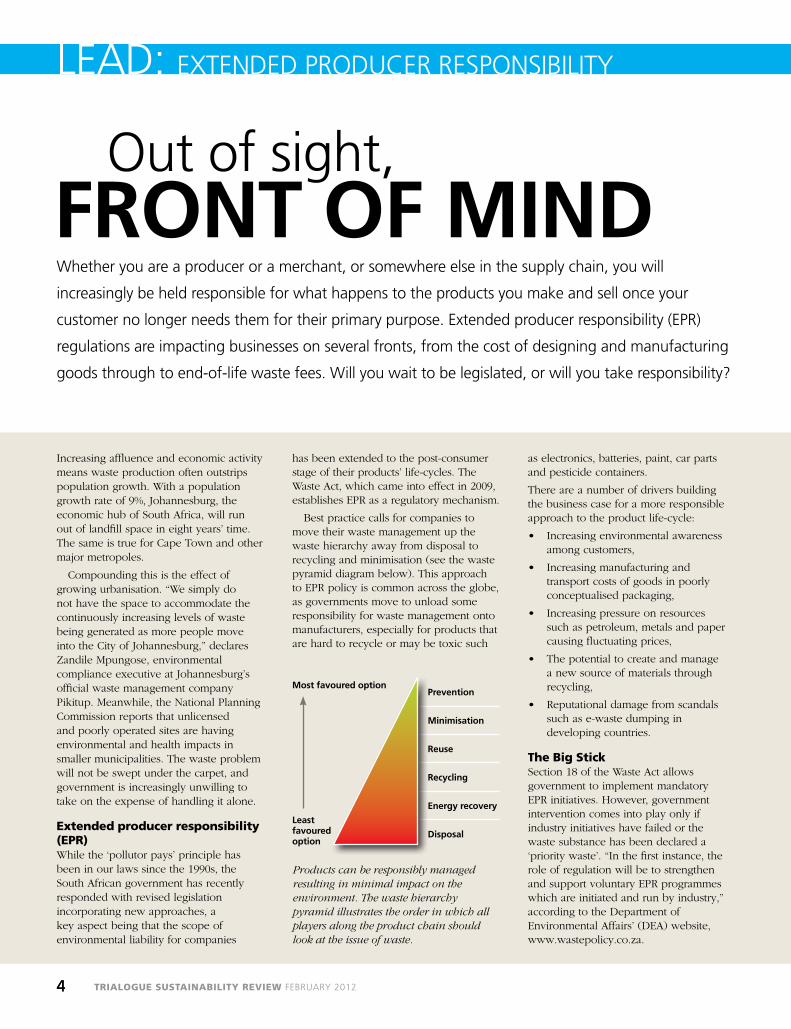

Best practice calls for companies to move their waste management up the waste hierarchy away from disposal to recycling and minimisation (see the waste pyramid diagram below). This approach to EPR policy is common across the globe, as governments move to unload some responsibility for waste management onto manufacturers, especially for products that are hard to recycle or may be toxic such

Products can be responsibly managed resulting in minimal impact on the environment. The waste hierarchy pyramid illustrates the order in which all players along the product chain should look at the issue of waste.

PreventionMost favoured option

Least favoured option

Minimisation

Reuse

Recycling

Energy recovery

Disposal

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 201244

Reporting by Trialogue, with additional reporting by Candice Landie, editor of RéSource magazine

Industries or companies with dangerous wastes or high volumes of waste are encouraged to develop their own industry waste management plans (IndWMP), or may be directed to do so by the Minister. The IndWMP sets out the industry’s strategy and commitments, and industries are then expected to report on their progress. Industries preparing IndWMPs in consultation with the DEA include tyres, paper and packaging, lighting (e.g. CFLs), and pesticides.

The Consumer Protection ActSection 59 of the Consumer Protection Act (CPA) states that suppliers of ‘particular goods’ have to accept the return of such goods and certain wastes – specifically components, remnants, containers or packaging that cannot be deposited into a common waste collection system – from consumers. The supplier is required to accept its goods or the waste generated by the use of such goods, without charging the consumer, irrespective of whether that particular supplier sold the product to the consumer in the first place.

South Africa’s new regulatory regime requires a far higher level of corporate awareness to ensure compliance. At the minimum, companies should undertake detailed assessments before concluding that the Waste Act or the waste-management requirements of the CPA are not relevant to their operations.

Mandatory ePr programme candidates

1. Products with toxic constituents that may become a problem at the end of life. Examples include batteries, electronics, used oil, pharmaceuticals, paint and paint products (latex and oil-based paints, and thinners), pesticides, radioactive materials, products containing mercury and cadmium including thermometers, thermostats, electrical switches (including automotive) and fluorescent lamps.

2. Large products that are not easily and conveniently thrown out as waste. Examples include carpets, building materials, TVs, computers, appliances, tyres, propane tanks and gas canisters.

3. Products with multiple material types that make them difficult to recover in traditional recycling systems. Examples include composite packaging, electronics and vehicles.

Source: Adapted from www.wastepolicy.co.za

One of the key challenges is establishing who along the value chain bears what portion of the costs. While government will facilitate the development of plans, it is not obliged to fund EPR initiatives. Whatever the mechanism, the message is clear: pre-empt legislation and manage the responsibility for your products’ extended life-cycles on your own terms. Done well and you garner the derived benefits. Wait for government and risk the consequences of generally inept delivery, or worse.

Creating a market Legislation, whether in the form of incentives, taxes or penalties, can be used to reinforce other drivers of behavior, such as natural market forces, or the developing consciousness of consumers.

Part of government’s mandatory IndWMP approach is to support the creation of markets. Scrap tyres, which are burned by informal collectors to recover the steel, are considered a significant environmental hazard in South Africa. In January this year, Environmental Affairs Minister Edna Molewa announced an Integrated Waste Plan for the tyre industry, proposing a levy of R2.30 per kilogramme which would support the creation of a recycling and energy-recovery industry and create about 15 000 jobs.

The plan was initially to be implemented and managed by the

Image courtesy of 35 Media

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 2012 5

LEAD: ExTENDED PRODUCER RESPONSIBILITY

Recycling and Economic Development Initiative of South Africa (REDISA), but in late January approval was withdrawn in order to give time for public engagement and to consider applications from other recycling companies who met the Department’s criteria. It is unclear what lessons government has learned from its plastic bag levy and the problems at recycling implementation entity Buyisa e-Bag, which has come under investigation for financial mismanagement and inability to deliver on its mandate.

Collect-a-Can, a joint initiative between ArcelorMittal and Nampak, creates a market by paying the otherwise unemployed to collect beverage cans for recycling. While Collect-a-Can is subsidised by ArcelorMittal and Nampak, some of the costs are offset once the cans are processed to recover both steel and tin, the latter being particularly valuable. Since 1993, when the initiative was launched, Collect-a-Can has increased the recovery of cans as a percentage of used can output from 18% to 70%.

In a 2009 paper on EPR in the packaging industry for the CSIR, Dr A Nahman argues that in South Africa, voluntary EPR is more effective in increasing waste recovery rates than government-led initiatives, comparing the successful Collect-a-Can, Glass Recycling Company and PETCO (PET plastics recycling) examples with the plastic bag recovery programme. It is clear that there are many benefits to business of taking the waste issue into its own hands, rather than waiting for the imposition of a government-run solution.

Ticking boxesPackaging is an issue for a wide variety of businesses, with even the most innocuous products producing packaging waste. Driven in part by consumer concerns, the packaging sector is entering a new era, one where market participants weigh very carefully the materials they choose for their packaging – taking into consideration the amount, the composition, and the end-of-life options.

Market leaders can gain the reputational benefits, but can also suffer the brunt of consumer ire. Internationally, companies such as Puma have made innovative packaging a core element of their brand.

On the other hand, UK environment minister Ben Bradshaw encouraged consumers in 2005 to dump ‘offending packaging’ at the checkout till. In 2009, Tesco, already rated the best retailer for responsible packaging, invited consumers to do just that, no doubt further boosting its reputation.

Last year, Coca-Cola introduced the PlantBottleTM – a recyclable polyethylene terephthalate (PET) bottle which is 30% sugarcane-based – to the South African market. The company plans for all its plastic bottles to be replaced by PlantBottlesTM by 2020, by which time they will be made of 100% plant material, decoupling Coca-Cola packaging from petroleum products. Even venerable industries such as the South African wine industry are making bold packaging changes. Boland Vineyards’ new PET wine bottles are light, recyclable and virtually unbreakable. The reduced packaging weight and smaller diameter have also resulted in improved transport efficiencies.

Companies see the business case in packaging waste recovery too. In September 2011, Nampak opened a R500 million waste paper mill expansion, and Propet (a PETCO affiliate) took over an ailing Cape Town polyester fibre factory, saving 100 direct jobs and maintaining a local source of fibre for 30 manufacturers. PETCO also uses the levies and grants it gathers from its industry members to keep PET prices stable during market fluctuations, thereby improving the viability of the PET recycling industry.

What, my waste?EPR is an issue that will affect all those producing and distributing products. Companies should consider the legislation and opportunities across their full product value chain and develop strategies that put them in control of the mechanisms and resulting benefits. As we have seen, efficiencies inevitably flow from smart initiatives, and these will further strengthen the business case for responsible behaviour as the costs of the carbon economy increase. Finally, leading exponents of responsible behaviour win the support of the public, adding precious stores of goodwill to brands hungry for recognition by the consumer.

industry-led voluntary ePr programmes

Used oil: A recycling initiative for used lubricating oil, co-ordinated by the Recycling Oil Saves the Environment (ROSE) Foundation, involves all 15 major lubricant marketers and blenders. These pay a voluntary contribution of 5c per litre of new lubricating oil to finance the collection of used oil and to fund R&D into oil waste processing. In 2010, the ROSE Foundation estimated that of the 120 million litres of used oil generated a year, up to three-quarters is being recovered. Government is assisting with developing norms and standards to ensure that the garage and motor vehicle maintenance industry participates in oil recycling activities that are aligned with the ROSE Foundation’s scheme.

Glass recycling: In 2005, glass manufacturers, packers and fillers came together to form The Glass Recycling Company, signing a memorandum of agreement with the DEA to increase the recovery rate of glass and stimulate job creation. Fillers pay a small levy when they buy glass from manufacturers and this funds recycling education and a network of glass drop-off points for consumers. In five years, the collection of waste glass has more than doubled to more than 300 000 tonnes per annum. The cullet thus obtained is absorbed back into mainstream glass manufacturing via Nampak’s purpose-built automatic sorting plant.

E-waste: Discarded electrical equipment is the fastest growing waste stream in South Africa, and only about 10% of it is recovered, despite much of it containing toxic or valuable materials. E-waste is highly regulated in Europe via Waste Electrical and Electronic Equipment (WEEE) directives, and South Africa will eventually be obliged to follow suit. The e-Waste Association of South Africa (eWASA) was established in 2008 to manage sustainability among manufacturers, vendors and distributors of electronic and electrical goods.

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 20126

CUT YOURELECTRICITYCOSTs WITHONE PHONECALL

0860037566

CUT YOURELECTRICITYCOSTs WITHONE PHONECALL

0860037566

08600 ESKOMEvery small to medium sized agricultural, industrial, and commercial business is searching forviable ways to reduce electricity consumption. Now it’s possible – just by picking up the phone.Across the country, Eskom is putting the advice of its electricity efficiency experts at your disposal, for free! No more worries about what to do, and costs. Our solutions can save youelectricity, and with funding assistance, even your accountant will smile. So the quicker you pick up that phone, the quicker you’ll benefit.

www.eskom.co.za/idm

It’s your call. We’ll pay you to save.

MO

HLA

LEN

G_

ESK

D_

374/

E /

ST

D O

FFER

AWARDS

Rewarding good behaviour or leading companies astray?

With high profile environmental disasters and corporate scandals dominating headlines, interest in corporate behaviour has never been greater, nor has it come from a more diverse array of stakeholders. Employees want to be proud of their company. Investors are increasingly building environmental and social considerations into their investment decisions. Corporate conduct is coming under deeper scrutiny, and with this spotlight comes the daunting task of sorting the visionaries from the bluffers. To this end, a number of ratings, indices and awards have sprung up, each with their own methodologies, requirements and rewards. Some of the most influential awards, and companies they have recognised, are listed in the tables on page 10.

Convincing stakeholders of your company’s commitment to sustainability comes with its rewards – such as improved reputation and access to investment and meeting regulatory requirements – but not without notable cost.

reporting is an investmentWith King III in effect, all listed South African companies will now be expected to address their social and environmental impact in their integrated annual report. For many, this presents new challenges and efforts. Add to this the pile of surveys and questionnaires required to be considered for most awards and indices, and you’ll see how quickly the effort will fill your employees’ time as well as your budget. But how meaningful are these ratings, and are they worth the investment?

Reporting is an essential component of communicating with stakeholders, who are increasing their scrutiny of companies’ sustainability claims. A variety of standards and awards claim to be able to recognise which companies are doing the best job. Should your business be chasing the accolades?

Comparability: the white whale of ratings Ultimately, ratings and awards should serve to benchmark sustainability performance and reporting quality, as well as highlight best practice. Often this is more easily said than done, however. While some issues – such as ethics, governance and transparency – are universally important, others vary widely in their materiality across sector lines. Two reports can be quite transparent, yet emphasise very different topics, leaving the reader hard-pressed to compare apples to apples.

In recent years, the Global Reporting Initiative (GRI) has introduced sector supplements, which help reporters to narrow in on the most material issues. While this generally improves intra-sector comparability on the number of topics discussed in a report, it also creates a potential pitfall for reporters who follow a ‘check-box’ disclosure approach, yet miss the heart of their story.

Goalposts can – and should – shiftAs the sustainability landscape evolves, companies must adapt, taking cues from sustainability leaders as well as the public sector, and responding to stakeholder input. The systems that rank performance, therefore, are beholden to the same evolution. Herein lies the challenge. Companies demand clear guidance and criteria, and like neat-and-tidy comparability from year to year. To stay relevant and robust, however, the ratings and awards must update their expectations according to shifting priorities and the leading edge of practice.

Though this co-evolution certainly presents challenges, it’s a necessary part of developing a well thought-out response, and, when done transparently and with sufficient lead-time, will help companies mature in their responses to material sustainability issues. It’s the very tension between aspirational goals and pragmatism that fuels innovation. As with any rapid evolution, from early flight to social networking, much progress happens when new ‘editions’ build on the best of the existing peer group.

Pursuing true transparency, not a costly data dump“Transparency!” has become a rallying cry among NGOs, the public sector and sustainability professionals, as well it should. It’s worth noting, however, that well-intentioned companies who go overboard to disclose each and every data point are missing the point of transparency and may be inadvertently running counter to the ideals of the awards they pursue – not to mention spending unnecessary resources.

True transparency is not dumping hundreds of pages of obscure data on an unsuspecting public. This buries the truth rather than illuminating it. Being transparent means openly discussing material challenges, risks and successes, and presenting meaningful data in context. That data should be available if relevant and requested, but never used to obscure the real story. Ratings or awards that encourage quantity of disclosure at the cost of quality only serve to incentivise lazy reporting. As they evolve, the best rankings will provide value in the quality of their analysis rather than the volume of data they collect.

What do awards say about performance?While there is some evidence that reporting can drive better sustainability performance, this link is by no means a hard and fast rule. Indeed, many companies are reporting openly on

Reporting by Susie Keane

IMA

GE

©iS

tock

phot

o.co

m /

DN

Y59

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 20128

AWARDS

Thomas P. Peschak, marine conservationist and photographer, on the importance of sardines and their role in the annual Sardine Run, a unique natural phenomenon of mass migration that takes place along South Africa’s East Coast between June and July.

The South African Maritime Safety Authority encourages all South Africans to play an active role in protecting our marine ecosystems for future generations.

The greatest shoal on earth...

But for how long?

For more information call 012 366 2600 or visit our website http://samsa.org.za

“ The survival of long beaked common dolphins, Brydes whales, bronze whaler sharks and Cape gannets is intrinsically linked to the health of sardine stocks. Without the vast silvery shoals pulsing along our shores, the many tens of thousands of predators that occupy the top of the marine food chain could soon disappear from

South Africa’s seas. ”

SR6_Advertorial.indd 4 21/07/2011 10:50

IMA

GE

©iS

tock

phot

o.co

m /

DN

Y59

increasing emissions or declining efficiencies. What is certain is that while the Johannesburg Stock Exchange Socially Responsible Investment (JSE SRI) and Dow Jones Sustainability Indexes (DJSI) indices are making efforts to track performance, there is still a long way to go before ratings are able to rank how well a company manages its sustainability risks and opportunities.

For one thing, using publicly available information and company-submitted survey responses can skew perception. Where ratings or indices aim to measure performance, not just reporting style, cutting through the fluff to determine the most sustainable companies is surprisingly difficult. Inevitably, with every round of rankings, erstwhile darlings of the sustainability world are cast into the sinners group, while analysts scratch their heads wondering how they didn’t see it coming.

While communicating performance is an important piece of the sustainability picture, reporting shouldn’t be seen as an end in itself. Awards that undervalue thoughtful self-analysis can end up lauding companies with glossy reports but without a good grasp of their own sustainability risks.

so, where’s the value? The sustainability ratings universe continues to evolve, and signs point to it eventually consolidating as the most robust and renowned endure. Until that happens, companies need to be conscious of duplicated efforts, or risk investing more of their budget chasing awards than lowering their business’s impact. Pay attention to ratings that give valuable benchmarking and guidance, not necessarily those whose surveys make you look the best. As the pack of raters thins out over time, the strongest will be those who offer value to their constituents beyond a plaque to hang on a wall.

At the end of the day, inclusion in an index, or being shortlisted for an award, should be seen as a pat on the back for a job well done. Under no circumstances should it be a sole driver of strategy. When pursuing ratings or awards, remain true to your motivations, as well as to the interests of your company’s key stakeholders. A focus on these ‘material issues’ will hold the best promise of sustainable business returns, and will be the best defence against being led astray by the fleeting glamour of awards.

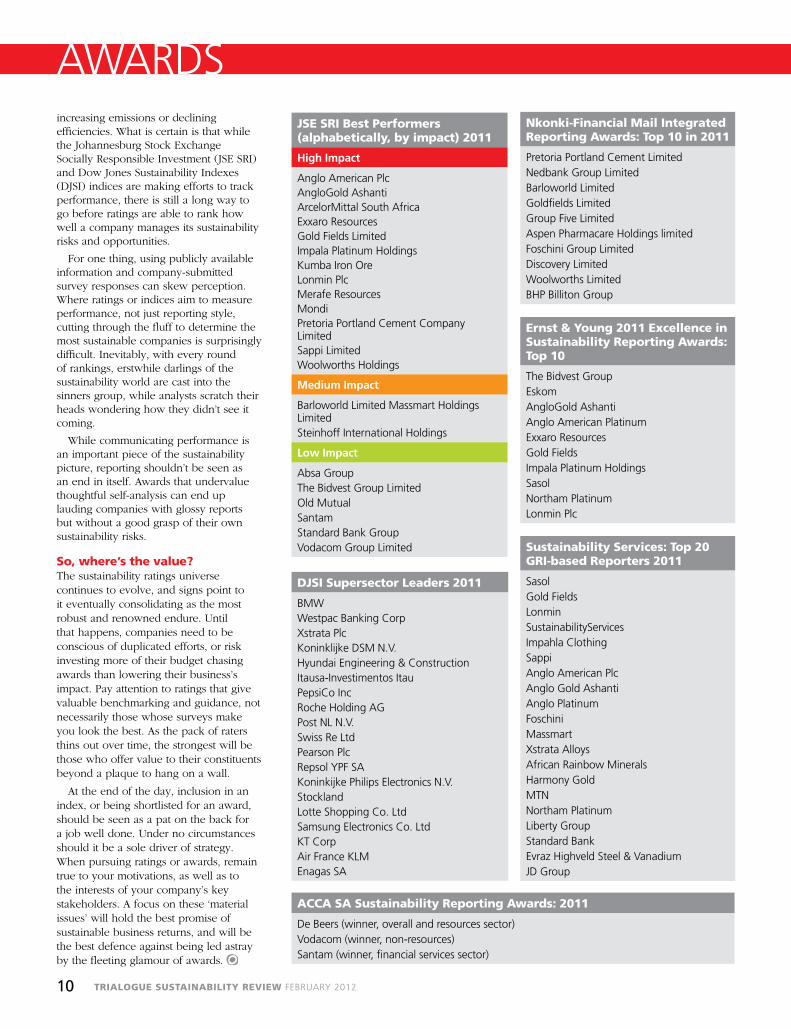

Jse sri best Performers (alphabetically, by impact) 2011

High Impact

Anglo American PlcAngloGold AshantiArcelorMittal South AfricaExxaro ResourcesGold Fields LimitedImpala Platinum HoldingsKumba Iron OreLonmin Plc Merafe Resources MondiPretoria Portland Cement Company LimitedSappi LimitedWoolworths Holdings

Medium Impact

Barloworld Limited Massmart Holdings LimitedSteinhoff International Holdings

Low Impact

Absa Group The Bidvest Group LimitedOld MutualSantamStandard Bank GroupVodacom Group Limited

dJsi supersector Leaders 2011

BMWWestpac Banking Corpxstrata PlcKoninklijke DSM N.V.Hyundai Engineering & ConstructionItausa-Investimentos ItauPepsiCo IncRoche Holding AGPost NL N.V.Swiss Re LtdPearson PlcRepsol YPF SAKoninkijke Philips Electronics N.V.StocklandLotte Shopping Co. LtdSamsung Electronics Co. LtdKT CorpAir France KLMEnagas SA

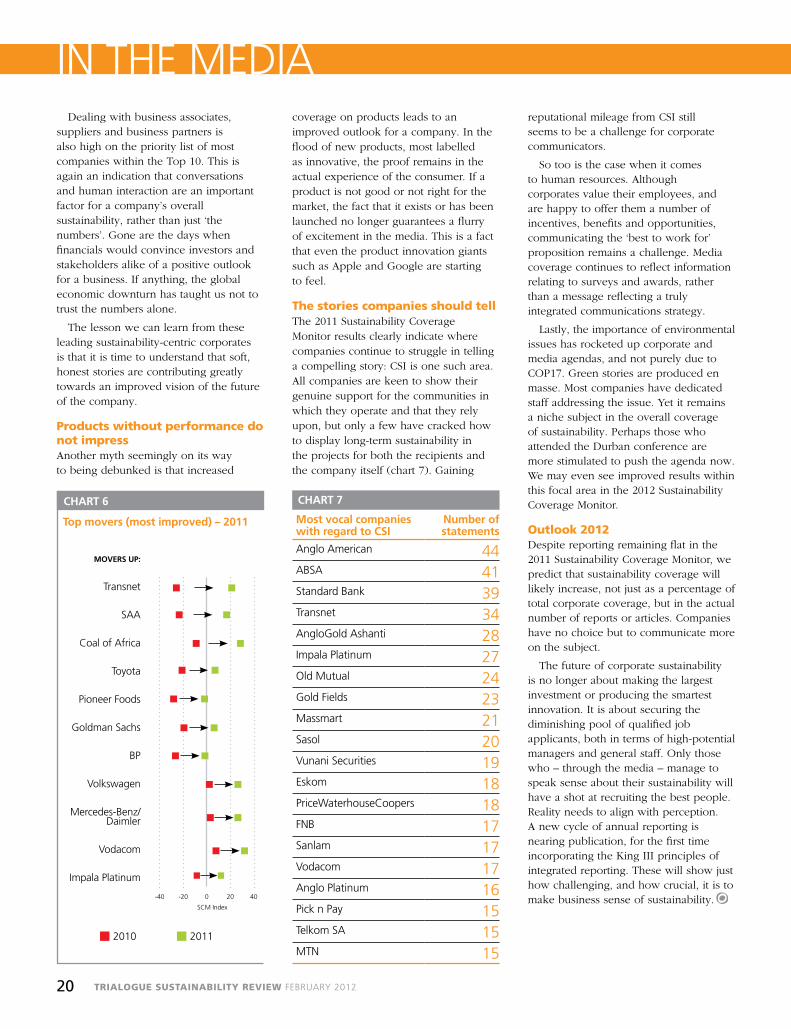

AWARDSNkonki-Financial Mail integrated reporting Awards: Top 10 in 2011

Pretoria Portland Cement LimitedNedbank Group LimitedBarloworld LimitedGoldfields LimitedGroup Five LimitedAspen Pharmacare Holdings limitedFoschini Group LimitedDiscovery LimitedWoolworths LimitedBHP Billiton Group

ernst & Young 2011 excellence in sustainability reporting Awards: Top 10

The Bidvest GroupEskomAngloGold AshantiAnglo American PlatinumExxaro ResourcesGold FieldsImpala Platinum HoldingsSasolNortham PlatinumLonmin Plc

sustainability services: Top 20 Gri-based reporters 2011

SasolGold FieldsLonminSustainabilityServicesImpahla ClothingSappiAnglo American PlcAnglo Gold AshantiAnglo PlatinumFoschiniMassmartxstrata AlloysAfrican Rainbow MineralsHarmony GoldMTNNortham PlatinumLiberty GroupStandard BankEvraz Highveld Steel & VanadiumJD Group

ACCA sA sustainability reporting Awards: 2011

De Beers (winner, overall and resources sector)Vodacom (winner, non-resources)Santam (winner, financial services sector)

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 201210

AWARDS

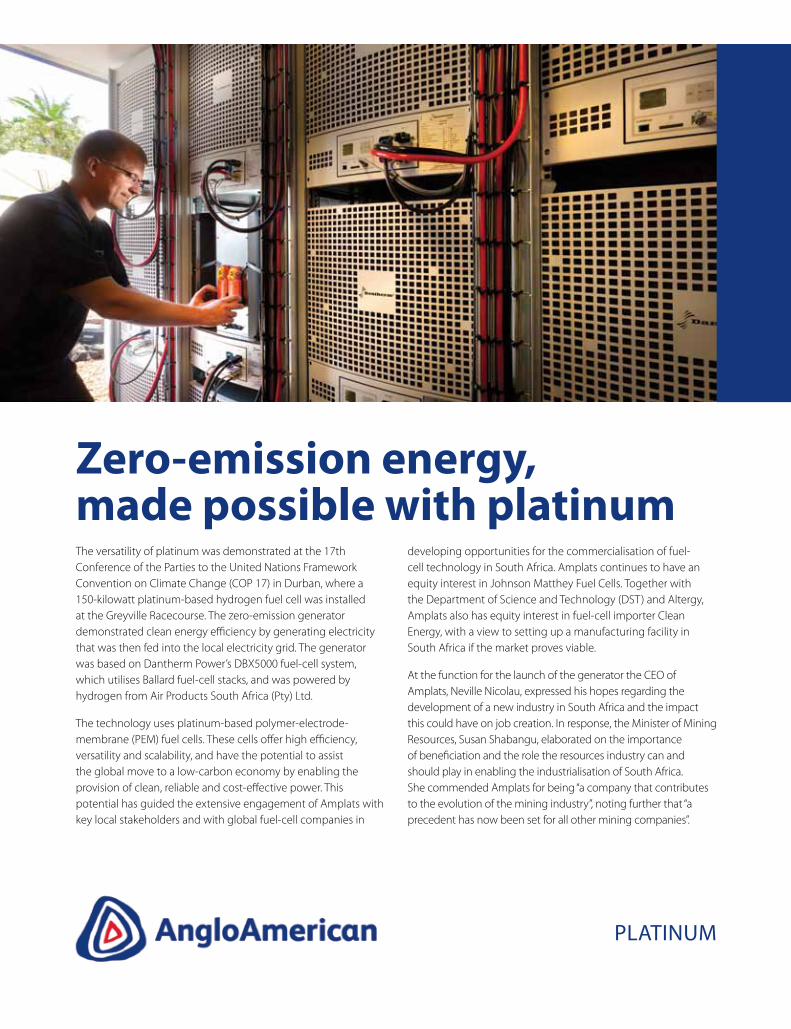

Zero-emission energy, made possible with platinumThe versatility of platinum was demonstrated at the 17th Conference of the Parties to the United Nations Framework Convention on Climate Change (COP 17) in Durban, where a 150-kilowatt platinum-based hydrogen fuel cell was installed at the Greyville Racecourse. The zero-emission generator demonstrated clean energy efficiency by generating electricity that was then fed into the local electricity grid. The generator was based on Dantherm Power’s DBX5000 fuel-cell system, which utilises Ballard fuel-cell stacks, and was powered by hydrogen from Air Products South Africa (Pty) Ltd.

The technology uses platinum-based polymer-electrode-membrane (PEM) fuel cells. These cells offer high efficiency, versatility and scalability, and have the potential to assist the global move to a low-carbon economy by enabling the provision of clean, reliable and cost-effective power. This potential has guided the extensive engagement of Amplats with key local stakeholders and with global fuel-cell companies in

developing opportunities for the commercialisation of fuel-cell technology in South Africa. Amplats continues to have an equity interest in Johnson Matthey Fuel Cells. Together with the Department of Science and Technology (DST) and Altergy, Amplats also has equity interest in fuel-cell importer Clean Energy, with a view to setting up a manufacturing facility in South Africa if the market proves viable.

At the function for the launch of the generator the CEO of Amplats, Neville Nicolau, expressed his hopes regarding the development of a new industry in South Africa and the impact this could have on job creation. In response, the Minister of Mining Resources, Susan Shabangu, elaborated on the importance of beneficiation and the role the resources industry can and should play in enabling the industrialisation of South Africa. She commended Amplats for being “a company that contributes to the evolution of the mining industry”, noting further that “a precedent has now been set for all other mining companies”.

PLATINUM

ICON

RECOGNISING BUSINESS AS

Joanne Yawitch was appointed CEO of

the National Business Initiative (NBI) in

March 2011 after many years working in

the Department of Environmental Affairs,

most recently as Deputy Director General of

Climate Change. Here she urges business

leaders to ‘walk the talk in a real way’.

There was no ‘aha’ moment for Joanne Yawitch who claims that the path to her current position was accidental rather than designed. Her career began in the land sector where she worked with non-profits tackling land issues. Following the 1994 elections she shifted from fighting forced removals to assisting the new government with rural development and land policies. After 17 years in government, a large portion of that focusing on the environment, she decided on a change and moved to head up the National Business Initiative (NBI).

And she has an acute sense of excitement about the move. “After almost one year in the position I have a good sense of the depth of the private sector’s commitment to embrace sustainability and to get things done. There are many companies that are showing leadership and implementing innovative and exciting sustainability projects.”

She cites numerous examples that have led her to this conclusion: Unilever’s ambitious sustainability plans, Vodacom’s new green innovation centre, Imperial Logistics’ work on reducing emissions, Exxaro’s plan to produce renewable energy, Woolworths’ sustainability journey, Siemens’ support of local government, Afrisam’s work on energy-efficient cement, and Anglo American’s new R100 million fund to support green economy enterprises.

ACTIVE AND INVOLVED

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 201212

ICON

Yawitch believes that the role of the NBI is to “get business to work together in a socially responsible way on critical societal issues and to create a joint platform to tackle sustainability issues broadly”. She says that its members have been asking for more support on sustainability issues and that this part of the organisation is set to grow.

Key sustainability issues for 2012In her view, two of the big issues that companies will face in 2012 are: climate change and sustainability, and skills development, which links to how we make the South African economy more productive and competitive. The first of these is a real challenge for South African companies as they operate in a centralised coal economy, which is also resource- and energy-intensive. The transition to a low-carbon economy is oft-touted and, indeed, laid out in the National Climate Change Response Policy White Paper. But Yawitch believes that “the debate is still in its infancy and there is as yet no clear road map to chart this low carbon transition”.

Aside from local policy and regulation in this area, the 17th United Nations Framework Convention on Climate Change (UNFCCC) conference of the parties (COP17) and its predecessors have resulted in directives that affect and involve the private sector. These include the establishment of a Green Climate Fund, a technology transfer mechanism including regional centres of excellence, the development of an adaptation committee, and work on mitigation. “Business needs to find ways to ensure

that its perspectives are integrated into the work done by the governmental negotiators at these UNFCCC negotiations,” states Yawitch.

To this end, she believes that the business programme at COP17 went well. The NBI co-ordinated the business pavilion comprising over 30 large corporations, hosted seminars running up to COP17 and convened a series of side events in Durban. The business pavilion and programme of events was well attended by local and international business and government.

But the key outcome of COP17 is that there will be further negotiations that result in a global legal pact on emission reductions. This pact must be completed by 2015 and will go into effect in 2020; it will almost certainly result in changes to the South African regulatory environment. Business needs to continue with the momentum created around COP17 by interacting with government on these issues and ensuring that its interests are clearly understood.

The NBI works to support companies in doing that. In its climate and energy focus area, it has encouraged good measurement and practice through the Energy Efficiency Accord (EEA), the Carbon Disclosure Project (CDP), the publication of case studies and an awards programme. For the past few years, the NBI has been involved in the development of a collective South African business approach to acting on climate change.

The second big issue is not a new one: the skills crisis. According to Yawitch, the impact of poor quality schooling and skills training on business is significant. Here too, the NBI has a number of programmes in which companies can get involved. In particular it is working with the Further Education and Training (FET) system to ensure that students get equipped with relevant skills and that they gain work experience during their studies

A call for regulatory clarity and business commitment“We have a very complex governance system in South Africa,” says Yawitch, before going on to explain that business gets mixed messages from government. “For example, how does the concept of a low carbon economy align with the call for a greater mineral beneficiation industry? And what will it really mean

for business to implement the policy proposals set out in the National Climate Change Response Policy White Paper? It is important that we find ways to have the difficult conversations; confronting and resolving policy contradictions. We must find means for the implementation of policy to be grounded in a shared understanding of what can be done.”

Yawitch believes that not only do we need clarity and alignment across policies and regulations, we also need to move policy into action more rapidly and more consistently; “there is a lot of stop-start work in South Africa”. Here again she feels that companies can play an important role in supporting the government. Citing the NBI’s own mentoring programme in the Eastern Cape, which has enlisted retired business people to coach provincial employees, with significant success, she explains that there is a lot more room for these types of programmes.

Overall, Yawitch views business as a positive and progressive force and thinks that the NBI needs to do more to create the sense that business is an important part of society with a valuable contribution to make to the key issues that confront our society. Business leaders too need to be more visible and vocal about this point. In parting, Yawitch offers the following advice: “In a society as polarised as ours, it is important that business leaders are clear about their commitment to change and have a vision of how they can play a positive role in a changed and transitioned environment.”

“IT IS IMPORTANT THAT BUSINESS

LEADERS ARE CLEAR ABOUT THEIR

COMMITMENT TO CHANGE AND HAVE

A VISION OF HOW THEY CAN PLAY A POSITIVE ROLE IN A CHANGED AND

TRANSITIONED ENVIRONMENT.”

“AFTER ALMOST ONE YEAR IN THE POSITION I HAVE A GOOD SENSE OF THE DEPTH OF THE PRIVATE SECTOR’S COMMITMENT TO EMBRACE SUSTAINABILITY AND TO GET THINGS DONE.”

Reporting by Cathy Duff

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 2012 13

SUSTAINABILITY ISSUE

Government’s vision for sustainable businessYOU CAN WATCH OR GET INVOLVEDRecently released government-led policy initiatives provide an optimistic view of the future – of a South Africa that is more equitable, productive and prosperous. Your response could be to ignore the commotion, to sit back and deal with the situation opportunistically as it unfolds. Alternatively, embrace it, understanding the complexities associated with its implementation, and accepting that, despite pitfalls along the way, getting involved could be good for business, and the future of the country.

Business strategy, if it is worth its salt, will incorporate sustainability strategy. Sustainability thinking provides a lens that offers a long-term perspective, which to a large extent is determined by the shifts in the external environment. Business must inevitably take a view on how these external shifts and events will unfold and in so doing, how the business should respond in a way that sustains operations. A robust analysis might draw on a PEST (political, economic, social and technological) type analysis, with variations including aspects such as legal or environmental trends.

Recently released plans and policy guidelines provide useful guidance for business strategists. These documents provide a high-level perspective on how government, business and civil society could collectively make a positive difference to our socio-economic landscape. The guidelines go a step further to introduce ideas for key programmes and actions, giving insight into which economic and developmental issues government is prioritising over the next decade.

The policiesThe New Growth Path (NGP): The framework of the New Growth Path was launched in 2010 by the Economic Development Department (EDD), with the main goal being to create five million jobs by 2020. Infrastructure development, which will drive job creation and the development of a local supplier industry,

commercialisation of intellectual property (IP). Metals fabrication, capital and transport equipment, green and energy-saving industries, and agro-processing were identified as new focus industries beyond those identified in IPAP1. The Plan includes 83 key action plans (KAPs) for implementation across government and its agencies. The new Revised Preferential Procurement Regulations are the result of the implementation of this Plan.

The National Development Plan (NDP): Following the National Planning Commission’s well-received Diagnosis document, the Plan, which took two years to develop, was dramatically launched at 11am on 11 November 2011 (11/11/11) by Commission head, ex-Finance Minister Trevor Manuel. Comprising 25 part-time commissioners nominated by the public and selected by the President, the NPC was given the mandate by Jacob Zuma to: “take a broad, cross-cutting, independent and critical view of South Africa, to help define the South Africa we seek to achieve in 20 years’ time and to map out a path to achieve those objectives.” Their ambitious vision document states that “it is possible to eliminate poverty and to sharply reduce inequality by 2030... All elements of the Plan must demonstrate their effect on these two goals.” The Plan prioritises nine areas for society (government, business and citizens) to focus on: Create jobs, expand infrastructure, change over to a low-carbon economy, transform urban and rural spaces, ensure quality education and training, provide quality healthcare, fight corruption, and unite the nation.

Government’s visionThese policies share many common themes including encouraging a green economy, expanding economic links into Africa, stimulating rural economic development, and improving skills and transfer of these to the workplace. Many of South Africa’s most successful industries were premised on a now-outdated notion of cheap energy, and this is putting the entire economy at risk of a slow-down.

is considered critical, but agriculture, manufacturing and the green economy also feature strongly. EDD has earmarked the spending of 75% of its 2011/12 budget – some R464.8 million – for government agencies and competition authorities in order to facilitate job creation and a more inclusive economy. Aside from industrial and infrastructure development, financing of high-potential new industries (such as renewable energy), and small business support are key focus areas for investment.

Development finance institutions such as the IDC, Khula and Samef have a crucial role to play. The IDC, already looking at R66 billion in development finance deals over the next five years, is being challenged to more than double its investments in New Growth Path priorities.

An NGP-linked Skills Accord, signed in mid-2011, commits business to taking on 17 000 internships over the next three years, as well as increasing training budgets by at least 3% over and above the current compulsory 1%.

Industrial Policy Action Plan 2 (IPAP2): This is the ‘manufacturing driver’ of the NGP and was launched in 2010 after consultation across all economic divisions in government, but sits with the Department of Trade and Industry (dti). Described as a “three year rolling industrial development road-map”, it highlights skills development, but also innovation and facilitating the

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 201214

SUSTAINABILITY ISSUE Reporting by Nick Rockey and Michelle Matthews

As well as plotting a shift to less energy-intensive industries (for example, from smelting to beneficiation in the mining sector), these policies look to reduce costs by cutting red tape, improving logistics, improving co-ordination within and between government departments, and fighting collusion and corruption.

In an excellent overview of the key plans since 1994 – including Gear, the RDP and AsgiSA – Business Day’s Tim Cohen asks “is [the ANC government] developing a gradual cogency through a lengthy contest of ideas?” In particular, he reflects on the relationship between the National Development Plan and the New Growth Path. The NDP, he says “is much longer, and much more exacting and in-depth. But it shares with the NGP the notion of a social compact — a ‘we are all in this together’ ethos. It overlaps and extends the NGP too, looking at everything from developing rural agriculture to foreign relations. In this sense, they are complementary.”

business and the social compactThe social compact is a strong and growing thread through government policy. The National Planning Commission defines it thus: “Social contracting or compacting occurs where different groups in society rise above their immediate short-term interests, and co-operate in pursuit of a society-wide and longer-term goal.” As Ebrahim Patel, Minister of

Economic Development, said in his 2011 budget presentation: “These goals [of the NGP] cannot remain solely government’s concern. The majority of new employment opportunities will come from outside the state… partnerships are critical for our success.” Business is expected to roll up its sleeves and pitch in.

The National Planning Commission, in its ‘Diagnostic’, is more high-minded: “Over the next 20 years, the ethics, actions and choices of our country’s leaders and its citizens, including the key social actors of labour, business and civil society, will determine whether we complete the transformation promised in 1994 or step back into a stagnant, divided, second-class country.”

What these policies mean for businessThe latest big-picture policies provide a framework from which business can identify opportunities and threats arising from government’s evolving thinking. Plans are easy and the ability to make real progress will depend on government-led initiatives, whether on the ground, in administration or in the policy space. It would be naive to expect a smooth journey, given the complex political landscape and vested interests of departments, agencies of government, unions and the like.

Companies that are able to predict and respond to trends – to work in synergy with shifts in the economy – are likely to find themselves better off. The NDP and NGP provide high-level direction as well as an outline of more specific interventions. It is up to businesses to distil from these policies the opportunities and threats that may arise and to factor these into their strategy and sustainability plans. As always, timing will be critical.

Businesses will need to watch closely and gauge the extent to which these plans are being adopted by the pertinent powers of government. Level of influence and capacity to act are key factors. Large businesses, acting individually or through business groupings, may chose to engage government at a policy level or hold government to account in meeting stated commitments, for instance through engagement on issues relating to corruption, local procurement and the like. At an operational level, opportunities will be presented to capitalise on

“I THINk [THE NATIONAL DEVELOPMENT PLAN] HAS TO BE VERY AMBITIOUS IN SCOPE, BECAUSE OTHERWISE IT WOULDN’T BE WORTH DOING… [HOWEVER] WITHOUT EFFECTIVE NATIONAL LEADERSHIP, THE PLAN IS NOT LIkELY TO ACHIEVE ITS CAREFULLY CONCEIVED OBJECTIVES... RECENT ExPERIENCE SUGGESTS THAT DEVELOPMENTAL RHETORIC, IF IT IS NOT BACkED BY POLITICAL LEADERSHIP, CAN SIMPLY SERVE AS A CLOAk FOR WASTE OR VULGAR ACCUMULATION.”

Anthony Butler, Witwatersrand politics professor and Business Day columnist.

NdP resolutions that could impact businessThe National Development Plan sketches a picture of what South Africa could look like in 2030 and, as such, provides the context for business’s long-term strategies. However, there are also some concrete recommendations and targets that could impact on business in the near future:

• Create 11 million new jobs by 2030 – unemployment rate to drop from 27% in 2011 to 14% by 2020 and to 6% by 2030.

• Increase the number of students eligible to study maths and science at university to 450 000 (three times the current levels) and produce 30 000 artisans a year by 2030.

• Establish a national skills planning system to conduct labour market research and produce different skills scenarios, which should inform training providers.

• Provide a tax subsidy to businesses to reduce cost of hiring young people.

• Simplify dismissal procedures for performance or misconduct.

• Broaden coverage of antiretroviral treatment to all HIV-positive people.

• Ensure buildings meet energy-efficient standards.

• Introduce a carbon tax.

• Improve and cut the cost of internet broadband by changing the regulatory framework.

• Centralise the awarding of large or long-running tenders.

• Governance of state-owned enterprise should be delinked from politicians; while the state should appoint the boards, the boards must appoint the chief executives.

incentives to upskill youth, or to respond to green economy targets such as one million solar water heaters installed by 2014.

The role of CEOs and business leadership in driving business that meets government imperatives should not be underestimated. Now would be a good time to pay attention to these policy guidelines and develop a ‘2030 vision’ for your business.

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 2012 15

IN THE MEDIA

Banks garnered the most sustainability coverage as the economic crisis wore on through 2011.

Companies that received the most media space communicated around relationships with customers

and business partners, as the effort to rebuild trust and confidence became a key strategic focus for

business.

The relationships behind the numbers

At first glance, the results of the 2011 Sustainability Coverage Monitor (SCM) appear encouraging. South African media’s overall focus on sustainability has remained stable at just under 18% of total coverage (chart 1) and the rating of sustainability issues has improved markedly from -15% to -5%, contrary to the generally depressed tone of overall company coverage.

It is hardly surprising that we have seen a significant increase in economic commentary, from a share of 2% in 2006 to close to 10% in 2011 (chart 2). Everyone, it seems, is becoming an ‘economic expert’. The banking industry in particular was responsible for the bulk of that commentary. From one perspective, it is good that the public is becoming more informed about what is happening to the major economic regions; the Eurozone, United States and Asia. More importantly, it is critical that we understand the impact of global economic conditions on South Africa.

banking gets the biggest sliceCynics would find irony in the new-found expertise being broadcast from the very industries – banking and financial services – that were largely responsible for the economic crisis in the first place. In such a volatile climate, these

economic assessments are debatable. Nonetheless, talking about the research makes business sense. Interacting with the media as a thought leader creates copy and strengthens the symbiotic relationship with the media.

Not surprisingly therefore, the banking industry further strengthened its lead in terms of sustainability coverage in the South African media ahead of the mining industry, retail and IT (the latter benefited

An independent, unpaid-for surveyThe Sustainability Coverage Monitor is an independent survey of corporate South Africa. No fees are solicited and no company or organisation has paid to be a part of this survey.

In order to analyse the media, Trialogue partners with The Media Tenor Institute of Media Analysis. Media Tenor scrutinises the news, opinion and business sections of leading South African print, broadcast and online media to provide a range of media intelligence to the corporate sector. Media Tenor uses its research data to compile the Sustainability Coverage Monitor (SCM), the results of which are published in this review every quarter. The data used is based on Media Tenor’s comprehensive day-by-day analysis of all relevant company-related articles appearing in 30 broad-based national daily and weekly newspapers and TV news broadcasts.

For more information on the methodology and categorisation of the SCM, please visit www.mediatenor.co.za or www.trialogue.co.za.

Sustainability issues in corporate coverage

CHART 1

Sustainability issues

% o

f to

tal c

orp

ora

te c

ove

rag

e

2006 2007 2008 2009 2010 2011

20%

15%

10%

2011 IN SUSTAINABILITY COVERAGE:

IMA

GE

©iS

tock

phot

o.co

m /

hide

sy

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 201216

IN THE MEDIA Reporting by Wadim Schreiner, Media Tenor SA

from the global discussion around smart phones, tablets, RIM and its BlackBerry woes, and the ‘war’ between Apple and Google around mobile operating systems and IP which drew companies such as HTC into the fray).

Industries outside of financial services also generate research and insightful information. The mining industry understands mineral reserves, political dynamics, human resource practices and environmental impacts. Retailers are experts on customer patterns, consumer behaviour and related interests. Yet it is curious that these industries seem to keep this information relatively private, possibly for competitive reasons. Notwithstanding these motivations, are they perhaps not missing an opportunity to promote their interests? Insightful analysis of topical issues, such as SAB’s press releases around responsible water management, provide interesting fodder for the reader, and exploit a relatively cost-effective and most influential communication channel.

The companies dominating coverage in 2011The results of the 2011 Sustainability Coverage Monitor clearly show the gulf between the coverage-intensive financial service industries and the rest. Of the top ten companies on our list, six are financial services institutions and five of these are banks.

Numbers and trends for sustainability coverage The share of sustainability coverage that particular themes commanded remained relatively stable in 2011. However, the softer issues are beginning to take a slightly larger share of sustainability coverage.

• Financialresultsasashareofsustainability coverage dropped from 18% in 2009 to 15% in 2011;

• Productcoverageincreasedslightlyfrom 7.5% to 8.5%;

• Businessstrategyremainedat10%(though down from 14% in 2006);

• Sustainabilityadvocacyclimbedto 1.8% (from 1.6% in 2010 and 0.4% in 2006); and

• HRmanagementremainedunmoved at 2%, as did stakeholder relations at 7%.

Absa has edged out 2010 leader, FNB by a small margin (chart 3). This was primarily driven through greater visibility in more media, although FNB received better quality coverage. Nedbank, positioned 5th in 2010, is now 3rd. One of the ‘small guys’, Capitec, has benefited from a buoyant year. They spoke often, on the right things (banking for the mass market) and to the right people. For that, they find themselves ranked 4th, followed by Standard Bank at number five.

In 6th place is Woolworths, a regular in the Sustainability Coverage Monitor Top 10. The retailer remained high on the media’s agenda through its communication regarding the opening of more stores in Africa and its better-sourcing policy. Doing things smarter, while expanding in a difficult market, is a good story to tell, both to the media and investors.

The effect of Woolworths’ run-in with the Advertising Standards Authority (ASA) over their alleged rip-off of Frankie’s retro sodas will be recorded in the SCM index for the first quarter of 2012. Suffice to say that Woolworths CEO Ian Moir’s comment is telling: “The biggest lesson for us is the power and impact of social media. We need to be in that space, responding to comments with facts,” he said.

SABMiller, tops in 2009, rejoins the Top 10 through its coverage on a

Economic commentary in corporate coverage

CHART 2

Economic commentary

% o

f to

tal c

orp

ora

te c

ove

rag

e

2006 2007 2008 2009 2010 2011

20%

10%

0%

CHART 3

Top 10 sustainability scores

2009 2010 2011

SABMiller FNB ABSA

Woolworths MTN FNB

Standard Bank Massmart Nedbank

MTN Investec Capitec

ABSA Nedbank Standard Bank

Deloitte Sanlam Woolworths

FNB Old Mutual SABMiller

Netcare Microsoft Vodacom

KPMG SABC Massmart

ACSA Rand Merchant Bank Liberty

potential merger with Foster and on its positive business outlook, much like Massmart (9th) through its merger with Walmart. Squeezed in between the beverage and retail giants is Vodacom, which despite a number of reputational setbacks in 2011, continues to tell its sustainability story well. Completing the Top 10 is Liberty, which features due to its improved business results and value.

IMA

GE

©iS

tock

phot

o.co

m /

hide

sy

TRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 2012 17

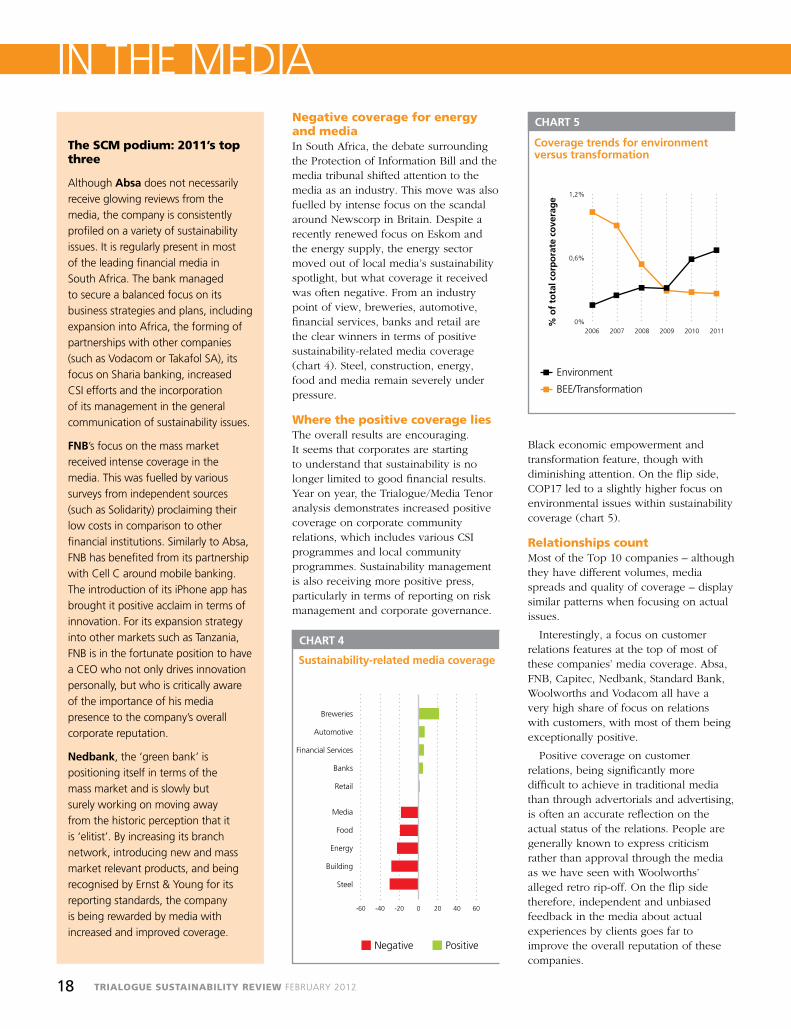

IN THE MEDIANegative coverage for energy and mediaIn South Africa, the debate surrounding the Protection of Information Bill and the media tribunal shifted attention to the media as an industry. This move was also fuelled by intense focus on the scandal around Newscorp in Britain. Despite a recently renewed focus on Eskom and the energy supply, the energy sector moved out of local media’s sustainability spotlight, but what coverage it received was often negative. From an industry point of view, breweries, automotive, financial services, banks and retail are the clear winners in terms of positive sustainability-related media coverage (chart 4). Steel, construction, energy, food and media remain severely under pressure.

Where the positive coverage liesThe overall results are encouraging. It seems that corporates are starting to understand that sustainability is no longer limited to good financial results. Year on year, the Trialogue/Media Tenor analysis demonstrates increased positive coverage on corporate community relations, which includes various CSI programmes and local community programmes. Sustainability management is also receiving more positive press, particularly in terms of reporting on risk management and corporate governance.

Black economic empowerment and transformation feature, though with diminishing attention. On the flip side, COP17 led to a slightly higher focus on environmental issues within sustainability coverage (chart 5).

relationships countMost of the Top 10 companies – although they have different volumes, media spreads and quality of coverage – display similar patterns when focusing on actual issues.

Interestingly, a focus on customer relations features at the top of most of these companies’ media coverage. Absa, FNB, Capitec, Nedbank, Standard Bank, Woolworths and Vodacom all have a very high share of focus on relations with customers, with most of them being exceptionally positive.

Positive coverage on customer relations, being significantly more difficult to achieve in traditional media than through advertorials and advertising, is often an accurate reflection on the actual status of the relations. People are generally known to express criticism rather than approval through the media as we have seen with Woolworths’ alleged retro rip-off. On the flip side therefore, independent and unbiased feedback in the media about actual experiences by clients goes far to improve the overall reputation of these companies.

Negative Positive

Sustainability-related media coverage

CHART 4

Breweries

Automotive

Financial Services

Banks

Retail

Media

Food

Energy

Building

Steel

0-20-40-60 20 40 60

Coverage trends for environment versus transformation

CHART 5

Environment

% o

f to

tal c

orp

ora

te c

ove

rag

e

2006 2007 2008 2009 2010 2011

1,2%

0,6%

0%

BEE/Transformation

The sCM podium: 2011’s top three

Although Absa does not necessarily

receive glowing reviews from the

media, the company is consistently

profiled on a variety of sustainability

issues. It is regularly present in most

of the leading financial media in

South Africa. The bank managed

to secure a balanced focus on its

business strategies and plans, including

expansion into Africa, the forming of

partnerships with other companies

(such as Vodacom or Takafol SA), its

focus on Sharia banking, increased

CSI efforts and the incorporation

of its management in the general

communication of sustainability issues.

FNB’s focus on the mass market

received intense coverage in the

media. This was fuelled by various

surveys from independent sources

(such as Solidarity) proclaiming their

low costs in comparison to other

financial institutions. Similarly to Absa,

FNB has benefited from its partnership

with Cell C around mobile banking.

The introduction of its iPhone app has

brought it positive acclaim in terms of

innovation. For its expansion strategy

into other markets such as Tanzania,

FNB is in the fortunate position to have

a CEO who not only drives innovation

personally, but who is critically aware

of the importance of his media

presence to the company’s overall

corporate reputation.

Nedbank, the ‘green bank’ is

positioning itself in terms of the

mass market and is slowly but

surely working on moving away

from the historic perception that it

is ‘elitist’. By increasing its branch

network, introducing new and mass

market relevant products, and being

recognised by Ernst & Young for its

reporting standards, the company

is being rewarded by media with

increased and improved coverage.

Water stewardshipAs a beverage company in the business of hydration, The Coca-Cola Company (TCCC) focuses on water stewardship. Our expertise in water allows us to make a significant and positive difference. Our three-part action water stewardship plan involves reducing and recycling water in our plants, and replenishing water in communities in which we operate.

Our bottler, ABI, Amalgamated Beverages Industries, has made a R10 million investment into its sustainable development objectives. Improvements to the bottling line at ABI’s Phoenix plant include the use of dry lube to speed the bottles along the track, reducing the amount of water needed to rinse bottles down before shipping. ABI has also put in place systems to recover water, which can be used in other parts of the plant. ABI is saving approximately 18 million litres of water annually through the careful management of this precious resource.

In South Africa, the replenish aspect of our three-part water stewardship approach has seen, among other investments, R30 million channelled to Coca-Cola’s Water for Schools project – part of the Replenishment Africa Initiative (RAIN) – which provides access to clean drinking water for learners.

Sustainable agricultureThe Coca-Cola Company is collaborating with local partners in the sugarcane industry to reduce the environmental and social impacts of sugarcane farming. Our partnership with World Wildlife Fund (WWF) promotes sustainable agriculture in the supply chain across the globe, focusing on the production of sugarcane and, more recently, on oranges and corn.

In South Africa, the focus is solely on sugarcane and, through WWF, partnerships have been created with the Noodsberg Canegrowers Association in the Midlands of KwaZulu-Natal. Our aim is to strengthen

and expand collaboration between commercial sugarcane growers and disadvantaged smallholder farmers. Training sugarcane farmers on sustainable management practices creates shared benefits for farmers and communities as a whole.

PlantBottleTM

In July 2011, Coca-Cola launched its innovative PlantBottleTM packaging – the first-ever recyclable PET plastic beverage bottle made from up to 30% plant matter that is 100% recyclable – in South Africa on its bottled spring water brand, Valpré. Within two years of its US launch in 2009, more than 2.5 billion PlantBottleTM packages had been produced, eliminating the equivalent of approximately 60 000 barrels of oil from Coca Cola’s plastic bottles. TCCC’s goal is to have a bottle made of 100% renewable resources by 2020.

PlantBottleTM was launched simultaneously with Coca-Cola’s Heidelberg Valpré Spring Water bottling facility, considered by many to be the “greenest plant in Africa”. The new Valpré plant is undergoing Leadership in Energy and Environmental Design (LEED) certification, accrediting the design of the facility, which maximises recycled materials and makes optimal use of water and solar energy. Valpré is the first Coca-Cola product to be distributed in the PlantBottleTM packaging in South Africa and in Africa.

Coca-Cola South Africa

Every day, the actions taken by our Company and our bottling partners touch billions of lives. Whether we are purchasing ingredients from our suppliers, creating our beverages, or supporting the communities where we operate, Coca-Cola strives to be a force for lasting, positive change. We are indebted to our bottling partners and the NGOs we work with, who are responsible for implementing so many of our shared plans.

Actions for positive change

www.coca-cola.co.zaTRIALOGUE SUSTAINABILITY REVIEW FEBRUARY 201218

IN THE MEDIA

Water stewardshipAs a beverage company in the business of hydration, The Coca-Cola Company (TCCC) focuses on water stewardship. Our expertise in water allows us to make a significant and positive difference. Our three-part action water stewardship plan involves reducing and recycling water in our plants, and replenishing water in communities in which we operate.

Our bottler, ABI, Amalgamated Beverages Industries, has made a R10 million investment into its sustainable development objectives. Improvements to the bottling line at ABI’s Phoenix plant include the use of dry lube to speed the bottles along the track, reducing the amount of water needed to rinse bottles down before shipping. ABI has also put in place systems to recover water, which can be used in other parts of the plant. ABI is saving approximately 18 million litres of water annually through the careful management of this precious resource.

In South Africa, the replenish aspect of our three-part water stewardship approach has seen, among other investments, R30 million channelled to Coca-Cola’s Water for Schools project – part of the Replenishment Africa Initiative (RAIN) – which provides access to clean drinking water for learners.

Sustainable agricultureThe Coca-Cola Company is collaborating with local partners in the sugarcane industry to reduce the environmental and social impacts of sugarcane farming. Our partnership with World Wildlife Fund (WWF) promotes sustainable agriculture in the supply chain across the globe, focusing on the production of sugarcane and, more recently, on oranges and corn.

In South Africa, the focus is solely on sugarcane and, through WWF, partnerships have been created with the Noodsberg Canegrowers Association in the Midlands of KwaZulu-Natal. Our aim is to strengthen

and expand collaboration between commercial sugarcane growers and disadvantaged smallholder farmers. Training sugarcane farmers on sustainable management practices creates shared benefits for farmers and communities as a whole.

PlantBottleTM

In July 2011, Coca-Cola launched its innovative PlantBottleTM packaging – the first-ever recyclable PET plastic beverage bottle made from up to 30% plant matter that is 100% recyclable – in South Africa on its bottled spring water brand, Valpré. Within two years of its US launch in 2009, more than 2.5 billion PlantBottleTM packages had been produced, eliminating the equivalent of approximately 60 000 barrels of oil from Coca Cola’s plastic bottles. TCCC’s goal is to have a bottle made of 100% renewable resources by 2020.

PlantBottleTM was launched simultaneously with Coca-Cola’s Heidelberg Valpré Spring Water bottling facility, considered by many to be the “greenest plant in Africa”. The new Valpré plant is undergoing Leadership in Energy and Environmental Design (LEED) certification, accrediting the design of the facility, which maximises recycled materials and makes optimal use of water and solar energy. Valpré is the first Coca-Cola product to be distributed in the PlantBottleTM packaging in South Africa and in Africa.

Coca-Cola South Africa