Embed Size (px)

Citation preview

Review

Goal: Maximize Value of the Firm

Past Topics Investment Decision (spending money)

Financing Decision (raising money)

Future Topics

“Variations on a Theme”

Today’s Topics

Dividends • Define (CB / Investment variation)

• Div & Value of the Firm

Capital Structure• Define (financing variation)

• Cap Str & Value of the Firm

Dividends

A payment made by a company to the shareholders of the company.

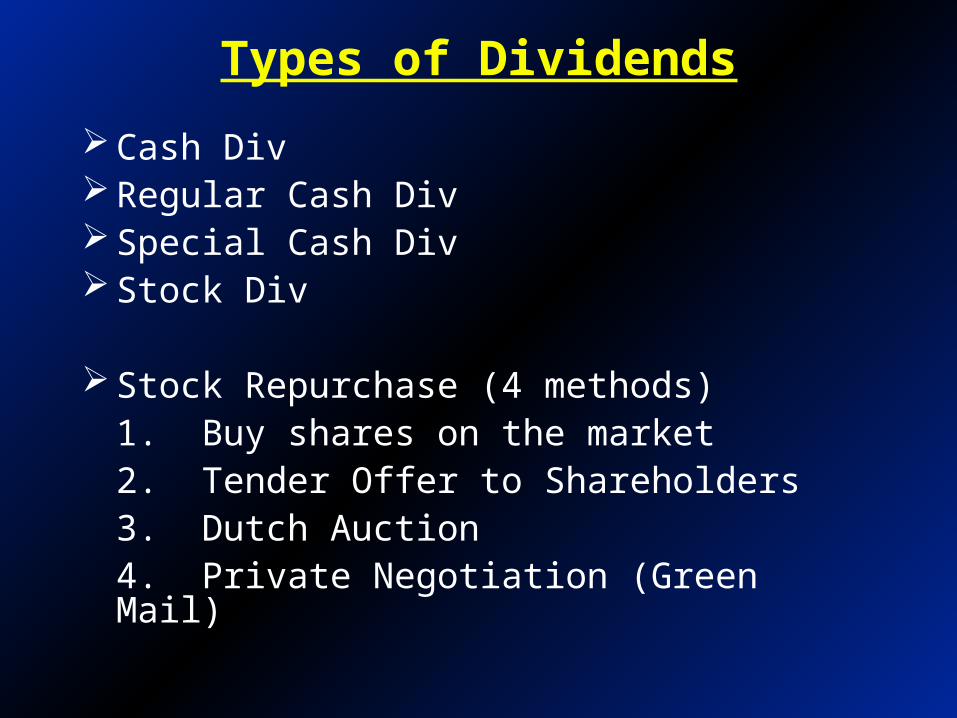

Types of Dividends

Cash Div Regular Cash Div Special Cash Div Stock Div

Stock Repurchase (4 methods)1. Buy shares on the market2. Tender Offer to Shareholders3. Dutch Auction4. Private Negotiation (Green Mail)

Dividend Terms

Record Date

Announcement Date

Payment Date

Ex-Dividend

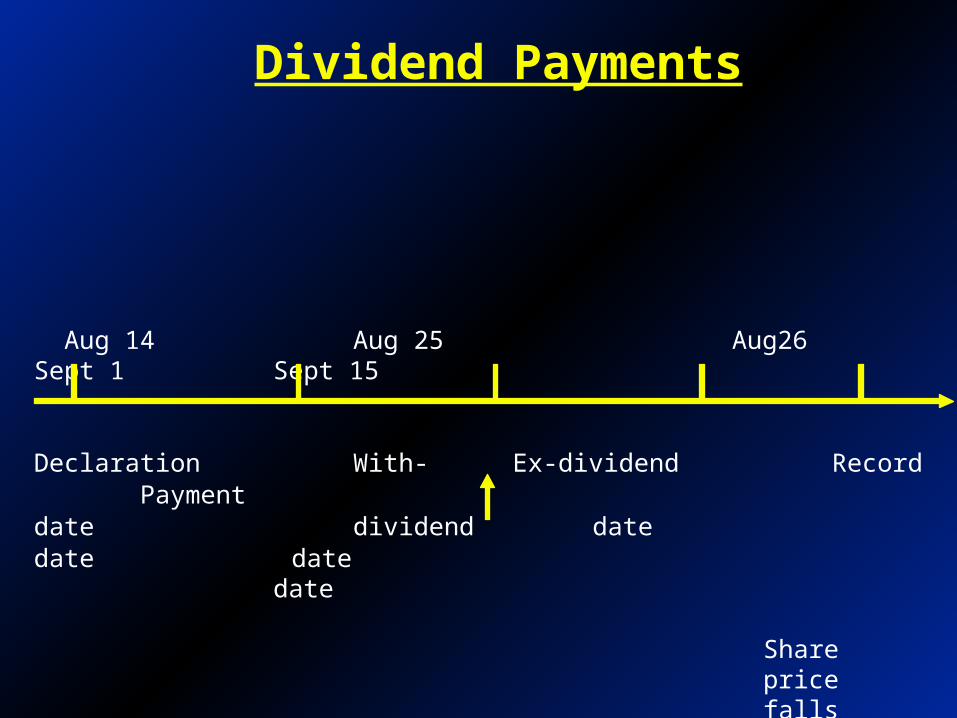

Dividend Payments

Aug 14 Aug 25 Aug26 Sept 1 Sept 15

Declaration With- Ex-dividend Record Paymentdate dividend date date date

date

Share price falls

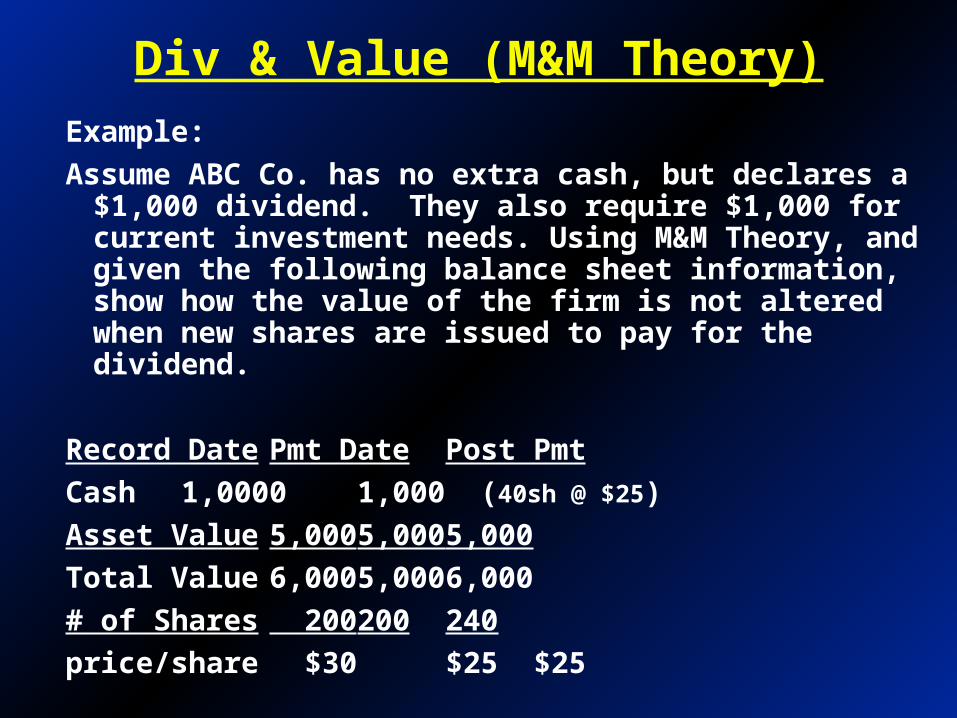

Div & Value (M&M Theory)

Example:

Assume ABC Co. has no extra cash, but declares a $1,000 dividend. They also require $1,000 for current investment needs. Using M&M Theory, and given the following balance sheet information, show how the value of the firm is not altered when new shares are issued to pay for the dividend.

Record Date

Cash 1,000

Asset Value 5,000

Total Value 6,000

# of Shares 200

price/share $30

Div & Value (M&M Theory)

Example:

Assume ABC Co. has no extra cash, but declares a $1,000 dividend. They also require $1,000 for current investment needs. Using M&M Theory, and given the following balance sheet information, show how the value of the firm is not altered when new shares are issued to pay for the dividend.

Record Date Pmt Date

Cash 1,000 0

Asset Value 5,000 5,000

Total Value 6,000 5,000

# of Shares 200 200

price/share $30 $25

Div & Value (M&M Theory)

Example:

Assume ABC Co. has no extra cash, but declares a $1,000 dividend. They also require $1,000 for current investment needs. Using M&M Theory, and given the following balance sheet information, show how the value of the firm is not altered when new shares are issued to pay for the dividend.

Record Date Pmt Date Post Pmt

Cash 1,000 0 1,000 (40sh @ $25)

Asset Value 5,000 5,000 5,000

Total Value 6,000 5,000 6,000

# of Shares 200 200 240

price/share $30 $25 $25

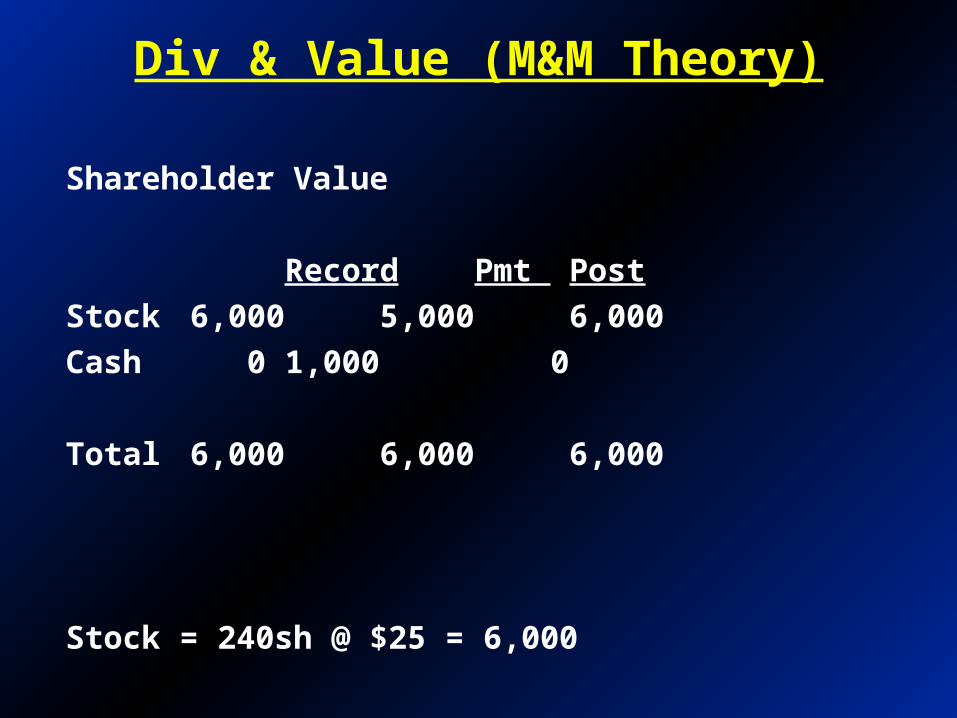

Div & Value (M&M Theory)

Shareholder Value

Record

Stock 6,000

Cash 0

Total 6,000

Stock = 200 sh @ $30 = 6,000

Div & Value (M&M Theory)

Shareholder Value

Record Pmt

Stock 6,000 5,000

Cash 0 1,000

Total 6,000 6,000

Stock = 200sh @ $25 = 5,000

Div & Value (M&M Theory)

Shareholder Value

Record Pmt Post

Stock 6,000 5,000 6,000

Cash 0 1,000 0

Total 6,000 6,000 6,000

Stock = 240sh @ $25 = 6,000

Dividend Theories

Leftists (M&M) - Div does not effect value

Rightists - Dividends increase value

Middle of the roaders - Leftist theory with some reality thrown in.

Dividends Increase Value

Market Imperfections and Clientele Effect

There are natural clients for high-payout stocks, but it does not follow that any particular firm can benefit by increasing its dividends. The high dividend clientele already have plenty of high dividend stock to choose from.

These clients increase the price of the stock through their demand for a dividend paying stock.

Dividends Increase Value

Dividends as Signals

Dividend increases send good news about cash flows and earnings. Dividend cuts send bad news.

Because a high dividend payout policy will be costly to firms that do not have the cash flow to support it, dividend increases signal a company’s good fortune and its manager’s confidence in future cash flows.

Dividends Decrease Value

Tax Consequences

Companies can convert dividends into capital gains by shifting their dividend policies. If dividends are taxed more heavily than capital gains, taxpaying investors should welcome such a move and value the firm more favorably.

In such a tax environment, the total cash flow retained by the firm and/or held by shareholders will be higher than if dividends are paid.

Taxes and Dividend Policy

Since capital gains are taxed at a lower rate than dividend income, companies should pay the lowest dividend possible.

Dividend policy should adjust to changes in the tax code.

Taxes and Dividend Policy

Rate of Income tax

0% 39.60%Operating Income 100 100Corporate tax (Tc=.35) 35 35After Tax income (paid as div) 65 65Income tax 0 25.7Cash to Shareholder 65 39.3

In U.S., shareholders are taxed twice (figures in dollars)

Taxes and Dividend Policy

Rate of Income tax

15% 33% 47%Operating Income 100 100 100Corporate tax (Tc=.33) 33 33 33After Tax income 67 67 67

Grossed up Dividend 100 100 100Income tax 15 33 47Tax credit for Corp Pmt -33 -33 -33Tax due from shareholder -18 0 14Cash to Shareholder 85 67 53

Under imputed tax systems, such as that in Australia, Shareholders receive a tax credit for the corporate tax the firm pays (figures in Australian dollars)

Capital Sturcture

Review Ch 17 on your own

Overview revisited now

201510% 5(%) shares on Return

2.001.501.00$.50shareper Earnings

2,0001,5001,000$500Income Operating

D C BA

Outcomes

10,000 $Shares of ValueMarket

$10shareper Price

1,000shares ofNumber

Data

Example - Macbeth Spot Removers - All Equity Financed

M&M (Debt Policy Doesn’t Matter)

Expected outcome

3025150%(%) shares on Return

321$0shareper Earnings

500,11,000500$0earningsEquity

500500500$500Interest

000,21,5001,000$500Income Operating

CBA

Outcomes

5,000 $debt of ueMarket val

5,000 $Shares of ValueMarket

$10shareper Price

500shares ofNumber

Data

D

Example

cont.

50% debt

M&M (Debt Policy Doesn’t Matter)

3020100%(%) investment$10 on Return

3.002.001.000 $investment on earningsNet

1.001.001.00$1.0010% @Interest :LESS

4.003.002.00$1.00shares twoon Earnings

DCBA

Outcomes

Example - Macbeth’s - All Equity Financed

- Debt replicated by investors

M&M (Debt Policy Doesn’t Matter)

MM'S PROPOSITION I

If capital markets are doing their job, firms cannot increase value by tinkering with capital structure.

V is independent of the debt ratio.

AN EVERYDAY ANALOGY

It should cost no more to assemble a chicken than to buy one whole.

No Magic in Financial Leverage

Proposition I and Macbeth

2015(%) shareper return Expected

1010($) shareper Price

2.001.50($) shareper earnings Expected Equityand Debt Equal

:Structure Proposed

EquityAll

:StructureCuttent

Macbeth continued

Leverage and Returns

securities all of uemarket val

income operating expectedr assets on return Expected a

EDA r

ED

Er

AD

Dr

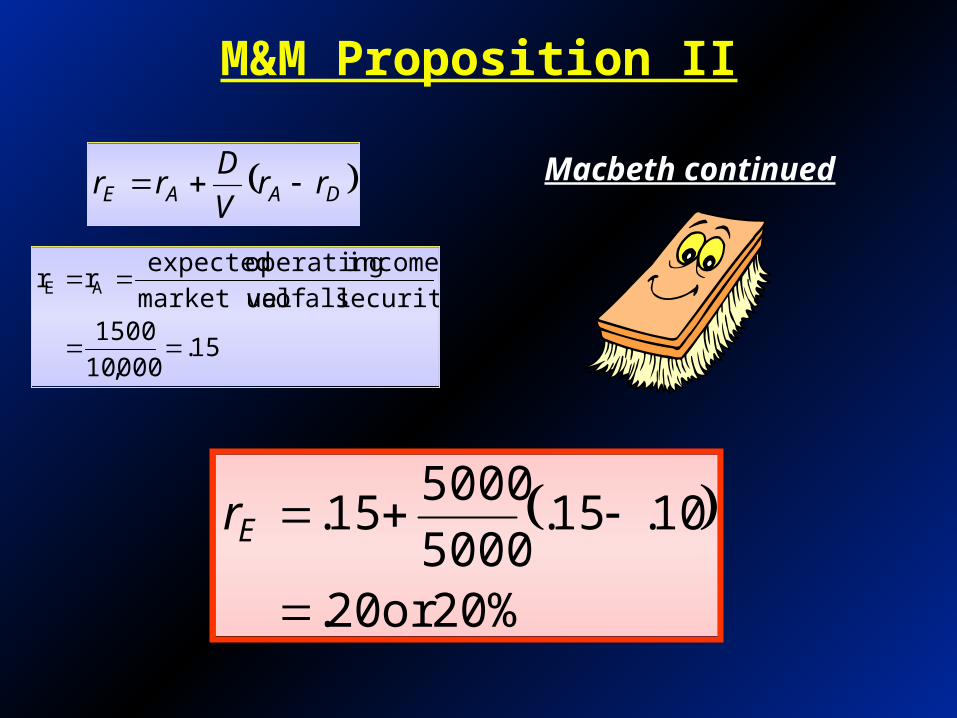

M&M Proposition II

15.000,10

1500securities all of uemarket val

income operating expectedr r AE

DAAE rrV

Drr

Macbeth continued

M&M Proposition II

15.000,10

1500securities all of uemarket val

income operating expectedr r AE

DAAE rrV

Drr

20%or 20.

10.15.5000

500015.

Er

Macbeth continued

r

DE

rD

rE

M&M Proposition II

rA

Risk free debt Risky debt

Leverage and Risk

200shares on Return

20($) shareper Earnings:debt % 50

155shares on Return

1.50.50($) shareper Earningsequity All$1,500

Income

$500

Operating

200shares on Return

20($) shareper Earnings:debt % 50

155shares on Return

1.50.50($) shareper Earningsequity All$1,500

Income

$500

Operating

Macbeth continued

Leverage increases the risk of Macbeth shares

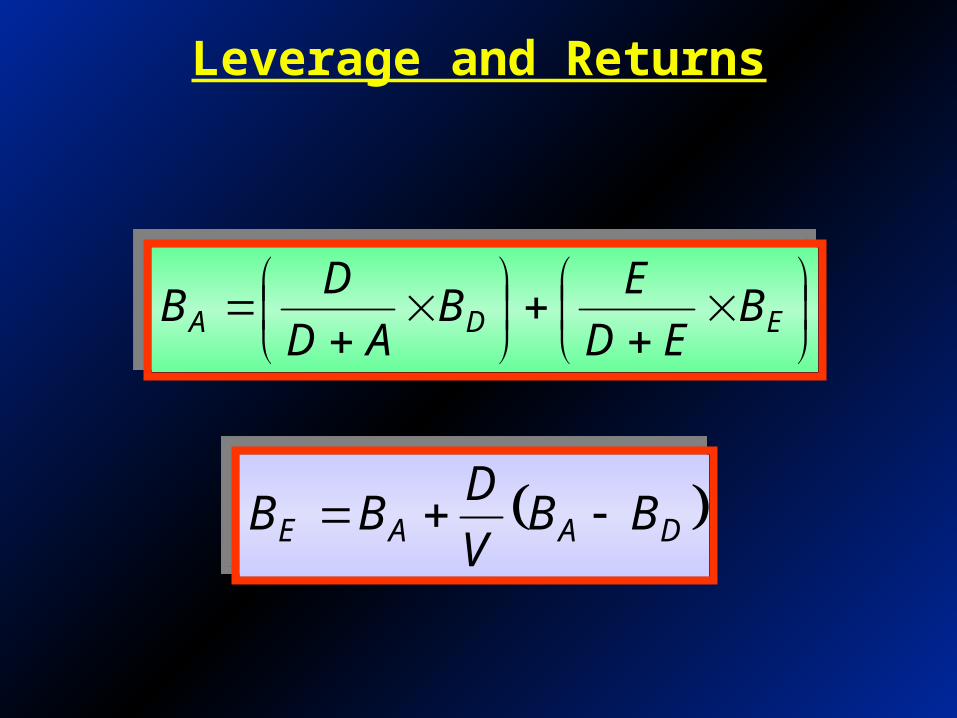

Leverage and Returns

EDA B

ED

EB

AD

DB

EDA B

ED

EB

AD

DB

DAAE BBV

DBB DAAE BB

V

DBB

WACC

EDA r

V

Er

V

DrWACC

EDA r

V

Er

V

DrWACC

WACC is the traditional view of capital structure, risk and return.

WACC

.10=rD

.20=rE

.15=rA

BEBABD

Risk

Expected Return

Equity

All assets

Debt

WACC

Example - A firm has $2 mil of debt and 100,000 of outstanding shares at $30 each. If they can borrow at 8% and the stockholders require 15% return what is the firm’s WACC?

D = $2 million

E = 100,000 shares X $30 per share = $3 million

V = D + E = 2 + 3 = $5 million

WACC

Example - A firm has $2 mil of debt and 100,000 of outstanding shares at $30 each. If they can borrow at 8% and the stockholders require 15% return what is the firm’s WACC?

D = $2 million

E = 100,000 shares X $30 per share = $3 million

V = D + E = 2 + 3 = $5 million

12.2%or 122.

15.5

308.

5

2

ED r

V

Er

V

DWACC

12.2%or 122.

15.5

308.

5

2

ED r

V

Er

V

DWACC

r

DV

rD

rE

rE =WACC

WACC

r

DV

rD

rE

WACC

WACC (traditional view)